funding k-12 public education in...

TRANSCRIPT

Funding K-12 Public Education in NebraskaPresentation to the Revenue Committee and the Education

Committee of the Nebraska Legislature

Lincoln, Nebraska, August 28, 2015

Andrew Reschovsky, Ph.D.Fellow, Lincoln Institute of Land Policy

Professor Emeritus, University of [email protected]

Presentation Outline

Policy issues

Heavy reliance on the property tax for funding K-12 public education

Rapidly rising property taxes on agricultural property

Policy responses

Funding increases in state aid to education

Responding to the rise in property taxes on agricultural land

2

Policy Issue: Nebraska’s Heavy Reliance on the Property Tax for the Funding of K-12 Education

3

4

-10%

0%

10%

20%

30%

40%

50%

60%1

97

6-7

7

197

7-7

8

197

8-7

9

197

9-8

0

198

0-8

1

198

1-8

2

198

2-8

3

198

3-8

4

198

4-8

5

198

5-8

6

198

6-8

7

198

7-8

8

198

8-8

9

198

9-9

0

199

0-9

1

199

1-9

2

199

2-9

3

199

3-9

4

199

4-9

5

199

5-9

6

199

6-9

7

199

7-9

8

199

8-9

9

199

9-0

0

200

0-0

1

200

1-0

2

200

2-0

3

200

3-0

4

200

4-0

5

200

5-0

6

200

6-0

7

200

7-0

8

200

8-0

9

200

9-1

0

201

0-1

1

201

1-1

2

201

2-1

3

Sh

are o

f G

en

era

l R

ev

en

ue

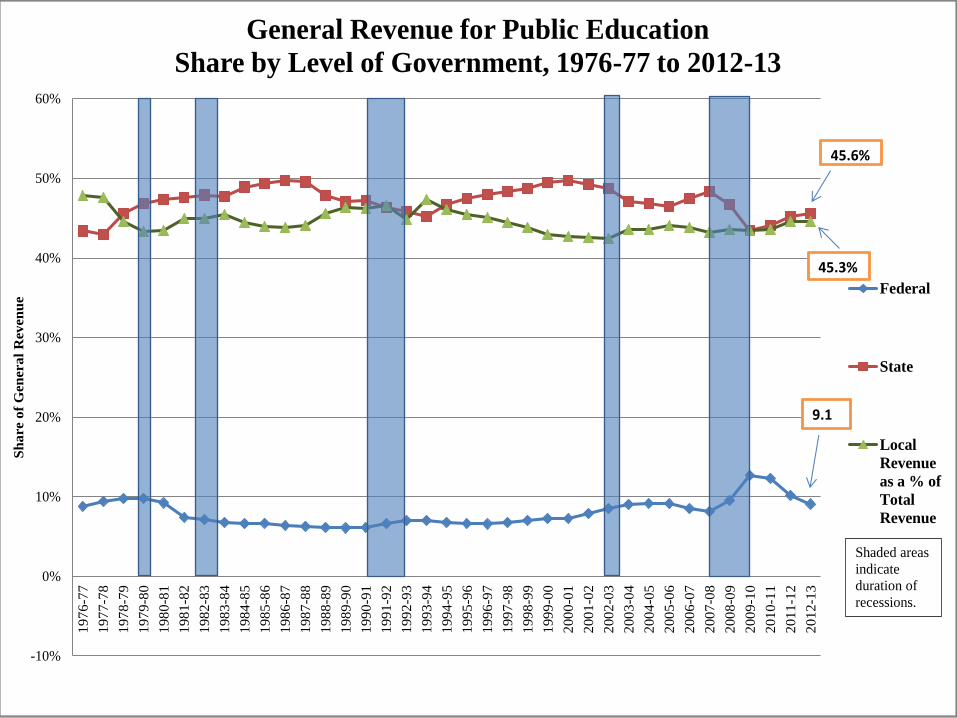

General Revenue for Public Education

Share by Level of Government, 1976-77 to 2012-13

Federal

State

Local

Revenue

as a % of

Total

Revenue

45.3%

9.1

45.6%

Shaded areas

indicate

duration of

recessions.

5Source: National Center for Education Statistics, Public Elementary-Secondary Education Finances, Fiscal Year 2013.

The Role of the Property Tax in Funding Public Education, 2011-12

6

Local Property Tax

as a % of Total

Total Revenue

New Hampshire 95.6% 57.4% 54.9%

Connecticut 97.3% 56.1% 54.6%

Illinois 88.3% 59.6% 52.6%

New Jersey 94.3% 55.1% 52.0%

Rhode Island 97.3% 53.3% 51.9%

Massachusetts 94.1% 54.1% 50.9%

Nebraska 85.2% (14) 59.6% (1) 50.8%

Average state 76.0% 41.7% 32.8%

Tennessee 47.9% 40.7% 19.5%

Idaho 83.3% 23.3% 19.4%

Minnesota 64.0% 28.6% 18.3%

Louisiana 41.9% 39.8% 16.7%

Alabama 46.8% 32.8% 15.3%

New Mexico 80.2% 17.0% 13.7%

Alaska 56.9% 21.0% 11.9%

Source: Calculations using data from the National Center for Education Statistics, National

Public Education Financial Survey Data, 2015. Available at nces.ed.gov/ccd/stfis.asp.

Property Tax

as a % of

Local Revenue

Local Revenue

as a % of

Total Revenue

Sources of Nebraska Education Revenue

7Source: National Center for Education Statistics, National Public Education Financial Survey

8

Nebraska = $1,592, U.S. average = $1,307

Source: U.S. Census Bureau, State and Local Government Finances

9

Nebraska = $1,592, U.S. average = $1,307

Source: U.S. Census Bureau, State and Local Government Finances

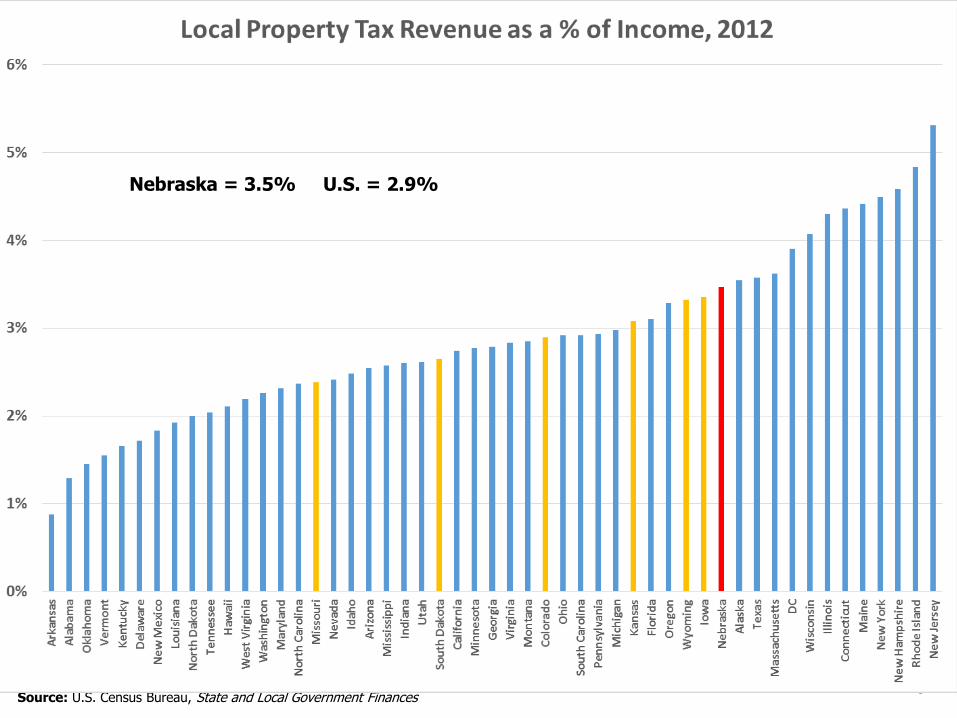

Nebraska = 3.5% U.S. = 2.9%

Property Tax Revenue as a % of Personal Income, 2012

10

11Source: U.S. Census Bureau, American Community Survey, 2008-2012

Average property tax burden: U.S. = 4.3% Nebraska = 4.3%

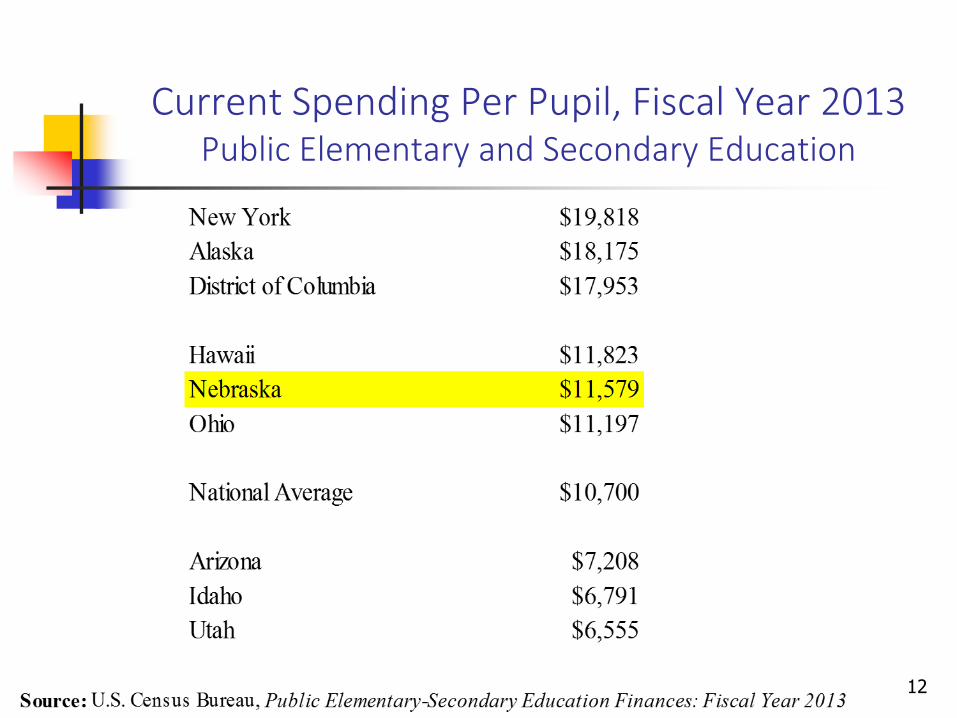

Current Spending Per Pupil, Fiscal Year 2013Public Elementary and Secondary Education

12

Nebraska’s High Quality Public Schools

Public schools are generally considered to be of high quality

Student performance on National Assessment of Education Progress (NAEP) above national averages

13

Nebraska U.S. Average

8th Grade Reading 285 284

8th Grade Mathematics 269 266

Policy Issue: Rapidly Rising Property Taxeson Agricultural Property

14

Growth in Agriculture’s Share of Total Property Values and Total Property Tax Levies, 2004-2014

15

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ag Share of Property Value Ag Share of Property Tax Levy

Property Tax Levy by Type of Property2004 and 2014

Agriculture, 32.0%

Residential, 45.3%

Commerical, Industrial & Mineral,

19.8%

Railroad, 1.9%Public Service &

Other, 1.1%

2014

16

Growth in Agriculture Property Tax Levies perFarmer & Rancher Income Tax Return, 2004-2014

17

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Nominal Dollars 2014 Dollars

Average rate of increase (nominal $) = 7.9%(2014 $) = 5.5%

Rate of increase, 2013-2014 (nominal $) = 13.9%(2014 $) = 12.0%

Average Agriculture Property Tax Levy Rate 2004-2014

181.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

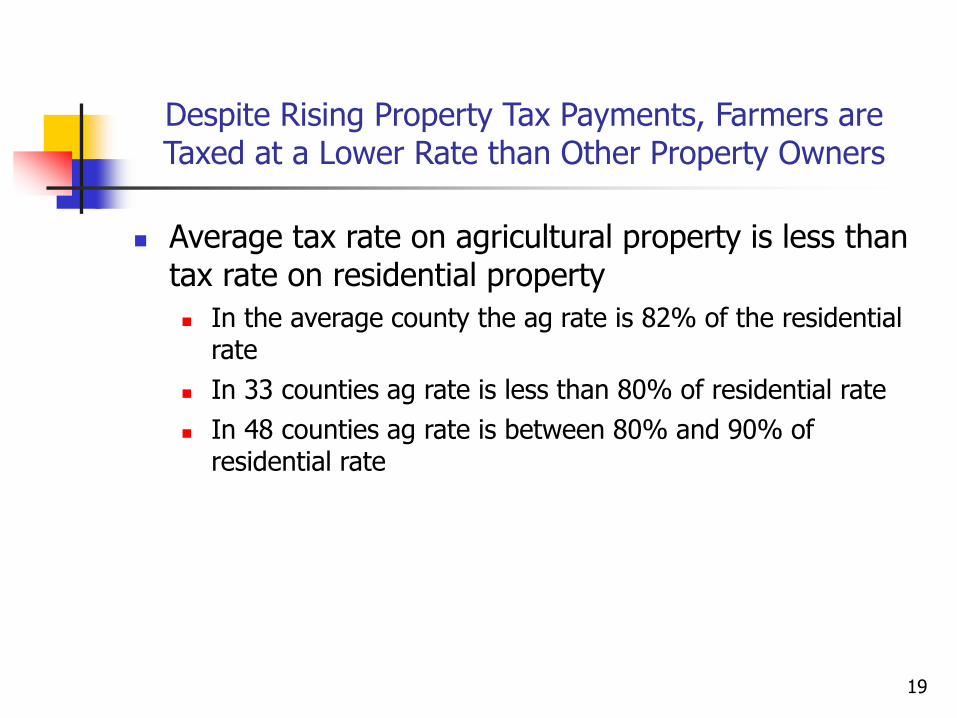

Despite Rising Property Tax Payments, Farmers are Taxed at a Lower Rate than Other Property Owners

Average tax rate on agricultural property is less than tax rate on residential property

In the average county the ag rate is 82% of the residential rate

In 33 counties ag rate is less than 80% of residential rate

In 48 counties ag rate is between 80% and 90% of residential rate

19

Why Are Agricultural Property Tax Levies Rising?

Local officials may find it easier to raise total levies because they can do so while lowering tax rates

Evidence (Anderson and Thompson) shows that over past decade school districts increased their levies by about 8% for every 10% increase in valuation

20

Why Are Agricultural Property Tax Levies Rising?

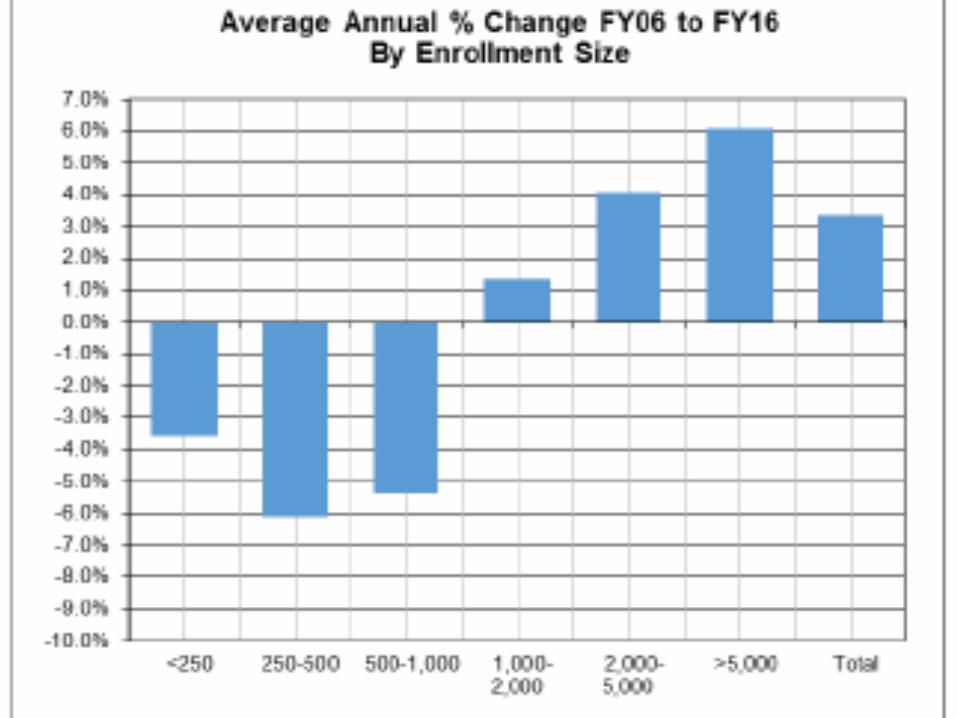

The rising costs of education, especially in small school districts

Spending per student is >50% higher than average in small (<250 students) districts

Average annual growth in per pupil spending 2004 to 2014 was 6.2% in small districts compared to 3.1% in large districts (>5,000 students)

School districts with <1,000 students have experienced declining enrollment in the past 10 years

About a 20% decline in enrollment in the smallest districts

Cutting spending in response to declining enrollment is very difficult

21

Why Are Agricultural Property Tax Levies Rising?

The combination of rising valuations and falling enrollment leads to reductions in equalization aid

Between 2007-08 & 2012-13, 60 districts lost all their equalization aid, and 30 districts lost more than ½ their aid

These districts were almost all rural

Over past decade, largest percentage declines in TEEOSA aid in small school districts (between 250 and 500 students)

In small districts (<1,000 students), state support is less than 25% of total school district revenue

About 55% of total state support comes from TEEOSA aid

22

23

Revenue Options for Funding IncreasedState Aid for K-12 Education

24

25

Tax Analysis Criteria

The efficiency of the tax

How does each tax effect the behavior/actions of individuals and businesses?

Does a tax reduce the competiveness of a state?

Revenue growth and volatility

Will tax revenues grow as the economy grows?

How volatile is revenue over the course of a business cycle?

Transparency and visibility

Tax fairness Two questions:

Who pays the tax? What is the incidence of the tax? (positive) Is the distribution of tax burdens fair? (normative)

Consider horizontal and vertical equity

Administrative feasibility Is the tax simple to administer and to comply with?

No Tax System or Tax PolicyWill Meet All the Criteria

All tax policy decisions require making trade-offs

Tax credits to enhance competitiveness will reduce simplicity

Highly progressive tax systems may hurt tax competiveness

Reduced revenue volatility often leads to a more regressive tax system

A well-balanced tax system can do a reasonably good job in achieving all the criteria

Reason that the Tax Modernization Committee chose “Balance” as the first criteria of a good tax system

26

Characteristics of Nebraska’s Tax System

27

Mix of State and Local Taxes, 2012Nebraska Compared to the United States

28

32.1%

22.1%

3.5%

22.7%

11.6%

1.8%

6.1%

36.4%

22.6%

2.9%

23.2%

7.3%

5.1%

2.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Property IndividualIncome

CorporateIncome

General Sales Selective Sales Motor VehicleLicense

Other Taxes

United States Nebraska

29Source: ITEP, Who Pays? A Distributional Analysis of the Tax Systems in all 50 States, 2015.

Annual Percentage Change in Nebraska State and LocalTax Revenue, by Type of Tax, 1992-2012

30

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Property Tax Sales Tax Select Sales Tax Individual Income Tax Corporate Income Tax

Increasing Individual Income Taxes to

Fund Additional State Aid to Education

31

Income Tax Policy

Nebraska has a quite good income tax system

Revenue could be increased by raising rates and/or adjusting brackets

Revenue could also be raised by reducing use of exemptions or credits

32

Income Tax Policy Considerations

Taxpayers can deduct state income tax payments on their federal income taxes (the federal offset)

Deductibility reduces the effective marginal tax rate difference between Nebraska and its neighbors

33

Income Tax Policy Considerations

Resist the temptation to use the income tax to achieve non-fiscal goals

Credits are a way to subsidize some activity

It is preferable to provide direct subsidies—they have the same impact on the budget, but they are much easier to curtail when budgets are tight or priorities change

34

Income Tax Policy Considerations

How to tax Social Security and pension income?

There are few economic justifications to treat these sources of income any different from other income

Favorable treatment of retirement income means that young families with children pay more

With the aging of the baby boom generation, the revenue costs of favorable treatment of retirement income will grow rapidly in the coming decades

A broader income tax base will generate more revenue and/or allow lower marginal tax rates

35

Increasing Sales Taxes to

Fund Additional State Aid to Education

36

Sales Tax Policy

An “ideal” sales tax system taxes the final consumption of all goods and services, but exempts all purchases of goods and services by businesses

Taxing business inputs leads to pyramiding

Exemptions of some necessities are justified as a way of protecting the poor by reducing the regressivity of the tax

Note that services now make up 64% of total consumption expenditures

37

Sales Tax Policy

To increase sales tax revenue Nebraska could:

Raise its rate

Abolish some of its existing exemptions

Expand the base to cover more consumer services

38

Sales Tax Policy

An ever increasing share of consumer spending is being done over the internet

In addition to internet sales, “cloud” purchases, such as music streaming, are growing very rapidly and most are escaping sales taxation

Allowing states to tax internet commerce in the absence of nexus will require Congressional action

The Marketplace Fairness Act passed by the Senate or an alternative

39

Increasing Corporate Income Taxes to

Fund Additional State Aid to Education

40

Corporate Income Tax Policy

Reduce or eliminate existing credits and exemptions States often enact credits and exemptions in order to help

specific industries or reward particular activities

The effectiveness of these subsidies/incentives is rarely evaluated

41

Policies to Address Rising Agriculture Property Taxes

42

Value Ag Property at 65% of Use Value

Down from 75%

Won’t reduce taxes in many communities, where ag property is a large % of total value

Elsewhere, will shift tax burden from farmers to non-farmers and other property owners in the same community

When ag values fall, lower ag taxes will place an increased burden on owners of non-ag property

On average, farmers have higher incomes than non-farmers

43

Average Income (Federal AGI) of Nebraska Farmers and Ranchers, 2003 to 2013

44$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

$110,000

$120,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

What About Farmers/Ranchers Who Face Rising Property Taxes, but Have Low Incomes?

Four approaches:

Change property tax policy

Reduce reliance on the property tax by increasing state education aid

Change the school aid formulas in a way that benefits school districts with lots of ag property

Education policies designed to reduce costs in small, rural school districts

45

Two Property Tax Policies that Could Help Farmers (and others) Facing Large Property

Tax Bills Relative to their Incomes

Real problem is one of liquidity

Farmers have an asset (land) that is growing rapidly in value, but their current income is inadequate to pay the property tax

Establish a tax deferral program

Establish a circuit breaker program

46

Tax Deferral Programs

Similar to a reverse equity mortgage

Local government lends taxpayer money to pay a portion of property tax, with loan paid back in future or when property sold

Can be triggered when tax is above a threshold % of income, or when tax increases at a very rapid rate

Could be an “opt out” program

Could be funded by state using bond funds

47

Circuit Breaker Programs

Circuit breakers target property tax relief to those taxpayers who face particularly high property tax burdens (property tax as a % of their income)

48

Property Taxes as a Percentage of IncomeWithout a Circuit Breaker

49

Property Taxes as a Percentage of IncomeWith a 5% Threshold Circuit Breaker

50

Circuit Breaker Programs

Renters are eligible for some programs by assuming that the property tax is equal to a fixed % of rent, e.g. 20% (lower if rent includes utilities)

Often paid as a refundable income tax credit

Many states limit circuit breakers to the elderly

Programs generally have income eligibility limits and maximum benefit levels

51

State-Funded Circuit Breaker Programs, 2009

52

Circuit Breaker Parameters for Selected States, 2012

53

State

All ages or

elderly only

Renters eligible

(yes/no) Income Ceiling

Maximum

Benefit Maximum Value

Iowa Elderly Yes $20,096 S1,000

Massachusetts Elderly Yes $80,000 $1,000 $705,000

New Jersey All

Yes, elderly

only

$75,000 (<65)

$150,000 (>65)

formula

determined $10,000 tax

Wisconsin All Yes $24,680 $1,168

Minnesota All Yes

$100,780 (owners)

$54,620 (renters)

$2,460 (owners)

$1,550 (renters)

Kansas Elderly Yes $32,400 $700 $350,000

Source: Lincoln Institue of Land Policy, Significant Features of the Property Tax

Nebraska’s Property Tax Relief Programs

54

Percentage Reduction in Property Tax from Nebraska Elderly Homestead Exemption

(For below average assessed values in a county withaverage assessed value equal to $100,000)

55

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Up to$31,000

$31,001 -$32,700

$32,701 -$34,400

$34,401 -$36,000

$36,001 -$37,700

$37,701 -$39,300

$39,301and above

Percentage Property Tax Savings of Median Homeownerfrom Property Tax Exemption and Credit Programs

(available to all property owners)

56

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

IN SC UT LA AR MS ID FL AZ WI AL DC OH MN OK TX ME IL NY NM NE IA GA KS CA

Source: Lincoln Institute of Land Policy, Significant Features of the Property Tax

Median Tax Savings for Homeowners fromNebraska’s Property Tax Credit, 2012

57

$54

$64

$75

$93

$132

$0

$20

$40

$60

$80

$100

$120

$140

Lowest Second Middle Fourth Highest

Me

dia

n T

ax S

avin

gs f

rom

Pro

pe

rty

Tax

Cre

dit

Income Quintiles of Nebraska Homeowners

Below $20,006 $20,007-$36,591 $36,592-$57,020 $57,021-$89,037 Above $89,037

Source: Lincoln Institute of Land Policy, Significant Features of the Property Tax

What About Farmers/Ranchers Who Face Rising Property Taxes, but Have Low Incomes?

Four approaches:

Change property tax policy

Reduce reliance on the property tax by increasing state education aid

Change the school aid formulas in a way that benefits school districts with lots of ag property

Education policies designed to reduce costs in small, rural school districts

58

What About Farmers/Ranchers Who Face Rising Property Taxes, but Have Low Incomes?

Four approaches:

Change property tax policy

Reduce reliance on the property tax by increasing state education aid

Change the school aid formulas in a way that benefits school districts with lots of ag property

Education policies designed to reduce costs in small, rural school districts

59

Increasing State Aid to Small, Rural Districts

Rising property taxes on farm land reflect increases in school costs in rural district and reductions in state aid

State aid formulas could be adjusted to account for higher costs in small school districts

Some states have categorical “sparsity” aid

60

What About Farmers/Ranchers Who Face Rising Property Taxes, but Have Low Incomes?

Four approaches:

Change property tax policy

Reduce reliance on the property tax by increasing state education aid

Change the school aid formulas in a way that benefits school districts with lots of ag property

Education policies designed to reduce costs in small, rural school districts

61

Education Policies to Reduce Costsof Rural Education

Further school consolidations are limited by large distances students would have to travel

New two-way video communication technology can allow for multi-location classrooms

Expanded distance education can reduce per pupil costs

State may want to consider grants for needed capital expenditures to implement new technology

62

In Defense of the Property Tax

63

The Strengths of the Property Tax

Over time, the most stable source of revenue for public schools has been the property tax

During the past 2 recessions, state aid was cut in most states

Between 2009 and 2012, school property tax revenue per pupil rose modestly

Heavily reliance on state funding effectively eliminates local control of public education

Lesson from California was substantial reduction in support for public education

Alternative local sources of education funding are all problematic 64

The Strengths of the Property Tax

The fact that the property tax is highly visible is a political liability, but also a virtue

School board accountability to residents is enhanced when they see clearly the link between what they pay each year and public services received

Other taxes tend to be “hidden”; the result is less transparency and accountability

A well-administered property tax system combined with a well-designed state aid system can deliver both educational excellence and tax relief

65

Thank You.

Questions and Comments?

66