form 6-k - shell · royal dutch petroleum company the “shell” transport and trading company,...

TRANSCRIPT

FORM 6-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington D.C.

20549

REPORT OF FOREIGN PRIVATE ISSUER

Pursuant to Rule 13a-16 or 15d-16 of

The Securities Exchange Act of 1934

For the month of May 2005

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b):82-

Commission File Number: 1-3788 Commission File Number: 1-4039

N.V. Koninklijke Nederlandsche

Petroleum Maatschappij (Exact name of registrant as

specified in its charter)

The “Shell” Transport and Trading Company, Public Limited Company

(Exact name of registrant as specified in its charter)

Royal Dutch Petroleum Company

(Translation of registrar’s name into English)

The Netherlands

(Jurisdiction of incorporation or organisation) England

(Jurisdiction of incorporation or organisation)

30, Carel van Bylandtlaan, 2596 HR The Hague The Netherlands

Tel No: (011 31 70) 377 9111 (Address of principal executive officers)

Shell Centre, London SE1 7NA, England

Tel No: (011 44 20) 7934 1234 (Address of principal executive officers)

Form 20-F [X] Form 40-F [ ]

Yes [ ] No [X]

Royal Dutch Petroleum Company

The “Shell” Transport and Trading Company, p.l.c.

Royal Dutch Petroleum Company and The “Shell” Transport and Trading Company (the Registrants) are furnishing the following exhibits on this Report on Form 6-K, each of which is hereby incorporated by reference:

END

Exhibit No. Description

99.1 Regulatory release. 99.2

Royal Dutch/Shell Group of Companies First Quarter 2005 Unaudited Condensed Interim Financial Report.

99.3

N.V. Koninklijke de Nederlandsche Petroleum Maatschappi (Royal Dutch Petroleum Company) First Quarter 2005 Unaudited Condensed Interim Financial Report.

99.4

The “Shell” Transport and Trading Company, p.l.c. First Quarter 2005 Unaudited Condensed Interim Financial Report.

Contact — Investor Relations UK: David Lawrence +44 20 7934 3855UK: Gerard Paulides +44 20 7934 6287Continental Europe: Bart van der Steenstraten +31 70 377 3996USA: Harold Hatchett +1 212 218 3112 Contact — Media International & UK: Andy Corrigan +44 20 7934 5963

Simon Buerk +44 20 7934 3453Lisa Givert +44 20 7934 2914

Bianca Ruakere +44 20 7934 4323Susan Shannon +44 20 7934 3277

The Netherlands: Shell Media contact +31 70 377 8750

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, each registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorised.

ROYAL DUTCH PETROLEUM COMPANY THE “SHELL” TRANSPORT AND TRADING COMPANY,

PUBLIC LIMITED COMPANY(Registrant) (Registrant) By:/s/ Jeroen van der Veer

By:/s/ Mark Edwards

Name: Jeroen van der Veer Title: President/Managing Director

Name: Mark Edwards Title: Assistant Company Secretary

By:/s/ Michiel Brandjes

Name: Michiel Brandjes Title: Company Secretary

Date: 9 May 2005

99.1 Regulatory release

First Quarter 2005 Unaudited Condensed Interim Financial Reports

Today, the Royal Dutch/Shell Group of Companies (the Group), Royal Dutch Petroleum Company (Royal Dutch) and The “Shell” Transport and Trading Company, p.l.c. (Shell Transport) released their First Quarter 2005 Unaudited Condensed Interim Financial Reports (the Reports). This release presents the unaudited interim financial information, including condensed notes, for the Group, Royal Dutch and Shell Transport on a basis that is consistent with the first quarter results for the Group that were published on 28 April 2005.

The Reports published today have been prepared for incorporation into the Listing Particulars and incorporation by reference into the Form F-4 filing with the SEC as part of the required documentation for the proposed unification of Royal Dutch and Shell Transport under one company, Royal Dutch Shell plc. This document can be downloaded from www.shell.com/results or www.sec.gov.

Contact — Investor Relations UK: Gerard Paulides +44 20 7934 6287 Europe: Bart van der Steenstraten +31 70 377 3996 USA: Harold Hatchett +1 212 218 3112

Contact — Media UK: Andy Corrigan +44 7934 5963 Simon Buerk +44 20 7934 3453 Lisa Givert +44 20 7934 2914 Bianca Ruakere +44 20 7934 4323 Susan Shannon +44 20 7934 3277

The Netherlands: Shell Media Contact +31 70 377 8750

Disclaimer statement: This announcement contains forward-looking statements, that are subject to risk factors associated with the oil, gas, power, chemicals and renewables business. It is believed that the expectations reflected in these statements are reasonable, but may be affected by a variety of variables which could cause actual results, trends or reserves replacement to differ materially, including, but not limited to: price fluctuations, actual demand, currency fluctuations, drilling and production results, reserve estimates, loss of market, industry competition, environmental risks, physical risk, risks associated with the identification of suitable potential acquisition properties and targets and the successful negotiation and consummation of transactions, the risk of doing business in developing countries, legislative, fiscal and regulatory developments including potential litigation and regulatory effects arising from recategorisation of reserves, economic and financial market conditions in various countries and regions, political risks, project delay or advancement, approvals and cost estimates.

Please refer to the Annual Report on Form 20-F/A (Amendment No. 1) for the year ended December 31, 2004 for a description of certain important factors, risks and uncertainties that may affect the Registrants’ businesses. Neither of the Registrants undertake any obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or otherwise.

Royal Dutch/Shell Group of Companies

First Quarter 2005

Unaudited Condensed Interim Financial Report

CONTENTS

Page

OPERATIONAL AND FINANCIAL REVIEW FOR FIRST QUARTER 2005 1 STATEMENT OF INCOME 4 BALANCE SHEET 5 STATEMENT OF CHANGES IN EQUITY 6 STATEMENT OF CASH FLOWS 7 NOTES TO THE CONDENSED INTERIM FINANCIAL REPORT 8

Unaudited Condensed Interim Financial Report

Operational and Financial Review for First Quarter 2005

The Group’s income for first quarter 2005 was $6,673 million, an increase of 42% from the comparative period in 2004, reflecting higher hydrocarbon realisations, strong LNG earnings and higher earnings in Oil Products and Chemicals. Income in the first quarter 2005 included net gains of $220 million, mainly from divestments partly offset by certain charges, compared with a net gain of $490 million in 2004.

Exploration & Production segment earnings of $2,955 million were 9% higher than a year ago ($2,707 million) mainly reflecting higher realised prices partly offset by lower volumes and higher costs including exploration and depreciation. Segment earnings in the first quarter 2005 included charges of $41 million (mainly from divestment gains of $82 million which were more than offset by a $172 million charge for marking-to-market certain gas supply contracts in the UK), compared with net gains of $245 million in the first quarter of 2004. Excluding these charges and net gains, segment earnings were 22% higher than a year ago.

Liquids realisations were 44% higher than a year ago, compared to an increase in Brent of 49% and WTI of around 41%. Outside the USA, gas realisations increased by 29%. In the USA gas realisations increased by 18%, compared to an increase in Henry Hub of 14%.

Hydrocarbon production for the first quarter 2005 was 3,847 thousand boe per day. Excluding the impact of divestments of 18 thousand boe per day and the end of a Middle East gas contract of 100 thousand boe per day, total production was 2% lower than the same quarter last year, reflecting a 7% decrease in oil production and a 4% increase in gas production.

Production benefited from new fields mainly in the UK and the USA and the ramp-up of production in the USA totalling some 183 thousand boe per day versus a year ago. New production volumes exceeded field declines of approximately 147 thousand boe per day, mainly in the USA, Norway and Oman. This net increase was more than offset by operational issues totalling some 100 thousand boe per day, mainly in the UK North Sea, compared to a year ago.

Gas & Power segment earnings were $476 million, including gains of $48 million mainly from divestments, compared to $522 million a year ago, which included divestment gains of $166 million. Earnings were helped by record LNG volumes (up 15%) and higher LNG prices and increased by 17% excluding the effect of divestments.

Oil Products segment earnings were $3,051 million compared to $1,573 million for the first quarter of 2004. Results included net gains of $427 million mainly from divestments versus a net gain of some $100 million a year ago. Higher earnings due to increased refining margins (benefiting from wide light heavy crude differentials particularly in the USA, and in Europe from middle distillates strength) were partially offset mainly by the impact of lower retail marketing margins in the USA (due to the impact of rising product cost which could not be fully recovered in the marketplace), lower trading results and higher costs mainly due to the weaker US dollar.

Chemicals segment earnings were $449 million, compared to segment earnings of $221 million in the same quarter last year. Earnings reflected higher operating rates, increased capacity and improved margins.

Chemicals segment earnings in the first quarter 2005 included an impairment of the Group’s investment in Basell of $214 million. In 2004, Shell and BASF announced the review of strategic options for the Basell joint venture (Group interest 50%) and on May 5, 2005 announced that the companies are to sell Basell (see page 3). The activities of Basell, including impairments, are reported as discontinued operations.

Corporate and Other net costs were $127 million in the first quarter 2005 compared to $176 million a year ago, due to lower net interest expense from lower net gearing partly offset by lower insurance results.

Royal Dutch/Shell Group of Companies 1

$ millionFirst Quarter First Quarter

2005 2004

Income from continuing operations 7,018 4,827Income from discontinued operations (214) 20

Income for the period 6,804 4,847

Attributable to minority interests 131 145

Income attributable to Parent Companies 6,673 4,702

Unaudited Condensed Interim Financial Report

Cash flow from operating activities totalled $8.1 billion in the first quarter 2005. There were $1.1 billion gross proceeds from divestments, including $0.8 billion in Oil Products with sales of businesses in Romania, the Canary Islands and the Eastern part of the Caribbean, the LPG business in Portugal and the Bakersfield refinery in the USA.

Capital investment1 in the first quarter 2005 was $3.2 billion, compared with $3.1 billion in the comparative period, of which $2.4 billion was in Exploration & Production.

First quarter 2005 and subsequent events: investments and portfolio developments Upstream portfolio developments during the quarter were:

The production licences for Upper and Western Salym (Shell share 50%) in Russia were extended until 2032 and 2034 respectively.

In Kazakhstan, Shell increased its equity interest in the North Caspian Sea Production Sharing Agreement (NCPSA), which includes the Kashagan Project, by 1.85% to 18.52% following the sale by BG Group.

In Australia, Shell’s divestment of the mature Laminaria (22% share interest) and Corallina (25% share interest) oil fields, is expected to be completed in the second quarter of 2005.

Successful exploration wells were drilled in Nigeria, Norway, USA, Malaysia, the Netherlands, the UK and Oman. Results to date are encouraging but awaiting completion of evaluation and clearance from governments and partners to provide more definitive information. Successful appraisal wells were drilled in Malaysia, Egypt, the Netherlands and the UK.

In Alaska, Shell is expected to be awarded 86 blocks in Lease Sale 195 for the Beaufort Sea. In the Gulf of Mexico, Shell is expected to be awarded nine blocks in Lease Sale 194. In Canada, Shell Canada acquired a 20% interest in eight existing exploration licences in the Orphan Basin under a farm-in agreement. In Algeria, an exploration contract was awarded to Shell in the Reggane and Timimoun basins covering some 30,000 square kilometres (sq km). In Egypt, Shell acquired 30% of four Western Desert concessions covering some 60,000 sq km of exploration acreage.

Shell and Qatar Petroleum signed a Heads of Agreement for the development of a large-scale integrated LNG project including Upstream gas and liquids production and a 7.8 million tonnes per annum (mtpa) LNG train (Qatargas 4, Shell share 30%). Intended LNG markets are North America and Europe with first deliveries expected to commence around 2010-2012.

The Sakhalin II LNG joint venture (Shell share 55%) and Malaysia Tiga LNG (Shell share 15%) concluded 20-years sales commitments with Kogas, the Korean gas company to supply 1.5 to 2.0 mtpa each beginning in 2008.

Shell and its partners in the Australian Gorgon LNG and domestic gas project agreed to integrate their interests in the Greater Gorgon area. Shell will hold a 25% interest in the joint venture to construct two 5 mtpa LNG trains. Shell expects to sell all or part of its share of gas from the Gorgon LNG project to the North American and Mexican markets.

Shell received approval from the US Maritime Administration for a 7.7 mtpa (initial capacity) offshore LNG import terminal (Gulf Landing) in the Gulf of Mexico. In Europe, Shell announced plans for the development of a 5.8 mtpa LNG import terminal in Sicily, Italy (Shell share 50%).

In April 2005, Shell signed a Memorandum of Understanding with the Nigerian National Petroleum Corporation (NNPC) and partners for the joint development of a greenfield LNG project (Olokola LNG) in Nigeria. The project is expected to include a joint venture infrastructure and operating company, and initially up to four 5 mtpa LNG trains. Two of the four trains will be owned by NNPC and Shell. The intended markets are North America and Europe.

In April 2005, Shell and Bechtel Enterprises Energy B.V. signed an agreement to sell InterGen N.V. (Shell share 68%) including 10 of its power plants for $1.75 billion. Excluded from the sale are InterGen’s assets in the United States, Colombia and Turkey pending further review. The transaction is expected to close mid-2005 and is subject to certain conditions and regulatory approvals.

On May 3, 2005, The National Oil Corporation of the Great Socialist People’s Libyan Arab Jamahiriya (NOC) and Shell Exploration and Production Libya GmbH (“Shell”) announced that they have reached a long-term agreement for a major gas exploration and development deal. The agreement covers the rejuvenation and upgrade of the existing Liquified Natural Gas (LNG) Plant at Marsa Al-Brega on the Libyan coast, together with exploration and development of five areas located in the heart of Libya’s major oil and gas producing Sirte Basin. The contract follows the Heads of Agreement signed in March 2004 between NOC and Shell, in which both parties agreed to establish a long-term strategic partnership in the Libyan gas sector.

Downstream continued implementation of the Group’s strategy for reshaping the portfolio during the quarter.

On 1 January 2005, Shell implemented one integrated Downstream organisation for the Oil Products and Chemicals businesses with a global line of business structure to optimise manufacturing facilities, standardise processes and improve services to customers.

Oil Products completed the earlier announced sales of its businesses in Romania, the Canary Islands and the Eastern part of the Caribbean. In addition, Shell completed the sale of the LPG business in Portugal and the Bakersfield Refinery in the USA. Total gross proceeds amounted to

$762 million.

In China, the joint venture (Shell share 40%) with Sinopec started operating its first retail stations. At the end of the quarter over 200 retail stations were in operation. The joint venture is expected to build and operate 500 retail outlets in the Jiangsu Province.

2 Royal Dutch/Shell Group of Companies

1 Capital investment is defined as capital expenditure plus exploration expense plus new equity investments or loans to equity accounted investments.

Unaudited Condensed Interim Financial Report

Shell signed a Letter of Intent with Qatar Petroleum for the development of a world-scale ethane-based cracker and derivatives complex in Ras Laffan, Qatar.

In 2004, Shell and BASF announced the review of strategic options for the Basell joint venture (Shell share 50%). On May 5, 2005 BASF and Shell Chemicals announced that they are to sell Basell for a consideration of €€ 4.4 billion, including debt. The transaction is subject to approval by the relevant antitrust authorities and closing is expected in the second half of 2005.

Royal Dutch/Shell Group of Companies 3

Unaudited Condensed Interim Financial Report

Statement of Income

Presented under IFRS

The Notes on pages 8 to 30 are an integral part of this report. 4 Royal Dutch/Shell Group of Companies

$ millionFirst Quarter First Quarter

2005 2004

Sales proceeds 90,068 74,748Less: Sales taxes, excise duties and similar levies 17,912 17,480

Revenuea 72,156 57,268Cost of salesb 58,565 47,437

Gross profit 13,591 9,831Selling and distribution expenses 3,164 2,913Administrative expenses 370 463 Exploration 261 111Share of profit of equity accounted investments 1,573 1,131Net finance costs 83 262Other income 5 436

Income before taxation 11,291 7,649Taxation 4,273 2,822

Income from continuing operations 7,018 4,827Income from discontinued operations (see Note 6) (214) 20

Income for the period 6,804 4,847

Attributable to minority interests 131 145

Income attributable to Parent Companies 6,673 4,702

a Includes net proceeds related to buy/sell contracts: 7,155 5,625 b Includes costs related to buy/sell contracts: 7,114 5,619

Unaudited Condensed Interim Financial Report

Balance Sheet

Presented under IFRS

The Notes on pages 8 to 30 are an integral part of this report.

Royal Dutch/Shell Group of Companies 5

$ millionMar 31 Dec 31

2005 2004

ASSETS Non-current assets Property, plant and equipment 85,779 87,918 Intangible assets 4,428 4,528 Investments: equity accounted investments 18,763 20,493 financial assets 3,704 2,700 Deferred tax 2,775 2,789 Employee benefit assets 2,250 2,479 Other 6,206 4,490

123,905 125,397

Current assets Inventories 17,517 15,375 Accounts receivable 45,189 37,439 Cash and cash equivalents 8,888 8,453

71,594 61,267

Total assets 195,499 186,664

LIABILITIES Non-current liabilities Debt 7,977 8,858 Deferred tax 12,625 12,930 Employee benefit obligations 6,358 6,795 Other provisions 6,821 6,828 Other 5,788 5,800

39,569 41,211

Current liabilities Debt 5,755 5,795 Accounts payable and accrued liabilities 45,691 38,289 Taxes payable 11,225 9,056 Employee benefit obligations 308 339 Other provisions 1,527 1,812 Dividends payable to Parent Companies 2,085 4,750

66,591 60,041

Total liabilities 106,160 101,252

EQUITY Equity attributable to Parent Companies 83,662 80,099 Minority interests 5,677 5,313

Total equity 89,339 85,412

Total liabilities and equity 195,499 186,664

Unaudited Condensed Interim Financial Report

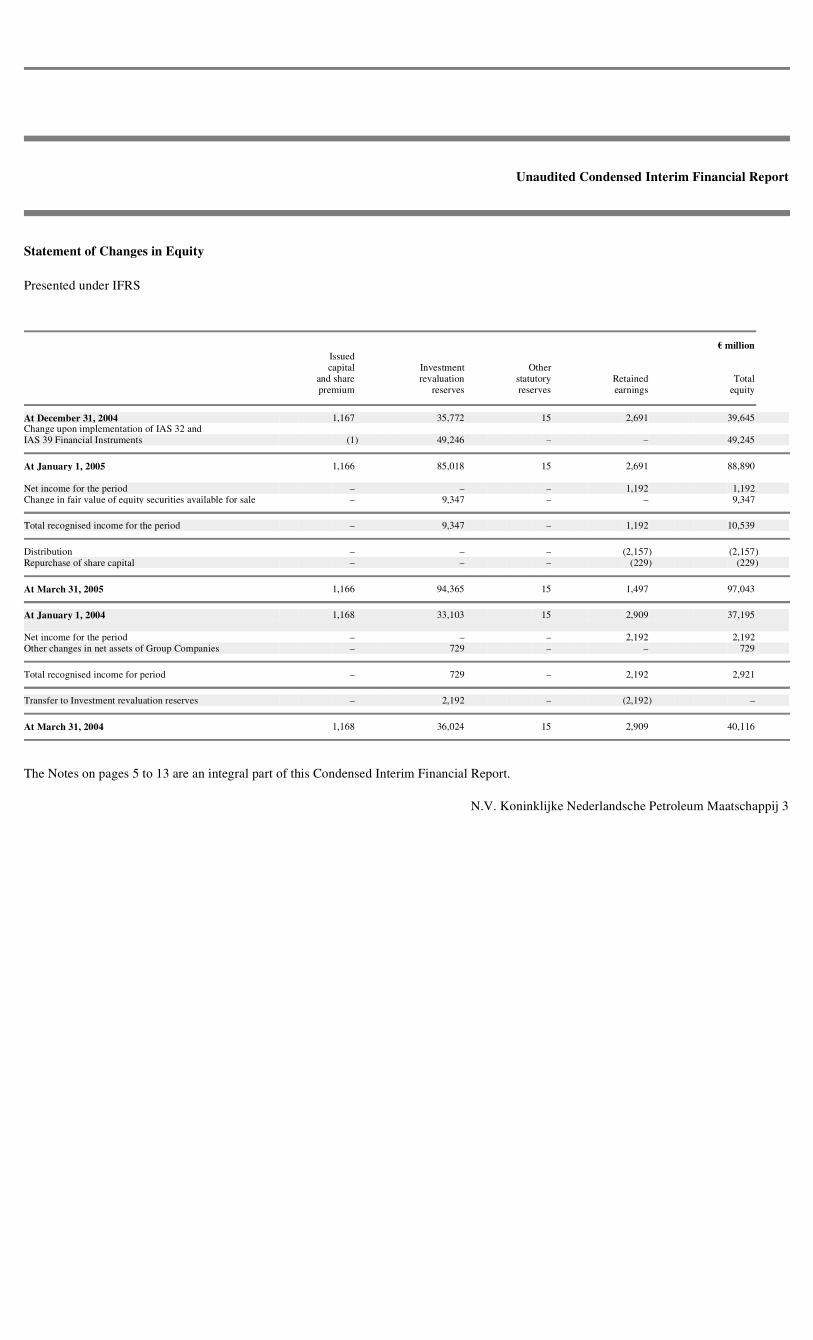

Statement of Changes in Equity

Presented under IFRS

The Notes on pages 8 to 30 are an integral part of this report. 6 Royal Dutch/Shell Group of Companies

$ millionEquity attributable to Parent Companies

ParentInvested Other Companies’

by Parent Retained equity shares Minority TotalCompanies earnings accounts1 held Total interests equity

At December 31, 2004 741 80,450 3,095 (4,187) 80,099 5,313 85,412 Change upon implementation of IAS 32 and 39

Financial instruments (see Note 7) –

(7)

823

–

816

–

816

At January 1, 2005 741 80,443 3,918 (4,187) 80,915 5,313 86,228 Income for First Quarter 2005 – 6,673 – – 6,673 131 6,804 Income/(expense) recognised directly in equity – – (1,464) – (1,464) 74 (1,390)

Total recognised income/(expense) for First Quarter 2005

–

6,673

(1,464)

–

5,209

205

5,414

Distributions – (2,605) – – (2,605) (47) (2,652)Decrease in Parent Companies’ shares held, net of

dividends received – – – 143 143 – 143

Change in minority interests – – – – – 206 206

Equity owner changes in First Quarter 2005 – (2,605) – 143 (2,462) 159 (2,303)

At March 31, 2005 741 84,511 2,454 (4,044) 83,662 5,677 89,339

At January 1, 2004 741 69,898 570 (3,428) 67,781 3,408 71,189 Income for First Quarter 2004 – 4,702 – – 4,702 145 4,847 Income/(expense) recognised directly in equity – – (757) – (757) (28) (785)

Total recognised income/(expense) for First Quarter 2004 – 4,702 (757) – 3,945 117 4,062

Distributions – – – – – (46) (46)Increase in Parent Companies’ shares held, net of

dividends received – – – (8) (8) – (8)Change in minority interests – – – – – 287 287

Equity owner changes in First Quarter 2004 – – – (8) (8) 241 233

At March 31, 2004 741 74,600 (187) (3,436) 71,718 3,766 75,484

1 See Note 4

Unaudited Condensed Interim Financial Report

Statement of Cash Flows

Presented under IFRS

The Notes on pages 8 to 30 are an integral part of this report.

Royal Dutch/Shell Group of Companies 7

$ millionFirst First

Quarter Quarter2005 2004

Cash flow from operating activities: Income for the period 6,804 4,847Adjustment for: Taxation accrued 4,311 2,916Interest incurred 160 300Depreciation, depletion and amortisation 3,155 2,703(Profit)/loss on sale of assets (558) (663)Decrease/(increase) in net working capital (2,137) 17Share of profit of equity accounted investments (1,359) (1,151)Dividends received from equity accounted investments 992 753 Deferred taxation and other provisions (392) (66)Other 303 (143)

Cash flow from operating activities (pre-tax) 11,279 9,513Taxation paid (3,186) (1,395)

Cash flow from operating activities 8,093 8,118

Cash flow from investing activities: Capital expenditure (2,934) (2,636)Proceeds from sale of assets 1,008 728Proceeds from sales and (additions): equity accounted investments (138) (427) investments: financial assets (24) 938Interest received 190 108

Cash flow from investing activities (1,898) (1,289)

Cash flow from financing activities: Net increase/(decrease) in debt with maturity period within three

months (990) (810)Other debt: new borrowings 815 2,134 repayments (548) (4,370)Interest paid (254) (210)Change in minority interests 351 277Dividends paid to: Parent Companies (5,137) – Minority interests (47) (46)Parent Companies’ shares: net sales/(purchases) and dividends received 143 (8)

Cash flow from financing activities (5,667) (3,033)

Currency translation differences relating to cash and cash equivalents (93) (15)

Increase/(decrease) in cash and cash equivalents 435 3,781Cash and cash equivalents at beginning of period 8,453 1,942

Cash and cash equivalents at end of period 8,888 5,723

Unaudited Condensed Interim Financial Report

Notes to the Condensed Interim Financial Report

1. The Royal Dutch/Shell Group of Companies

The Parent Companies, Royal Dutch Petroleum Company (Royal Dutch) and The “Shell” Transport and Trading Company, p.l.c. (Shell Transport) together own, directly or indirectly, investments in numerous companies known collectively as the Royal Dutch/ Shell Group. The interim financial information of the Parent Companies is not included in this Condensed Interim Financial Report, the objective of which is to reflect the financial position, results of operations and cash flows of the Group Holding Companies (Shell Petroleum N.V. and The Shell Petroleum Company Limited) on a combined basis.

Group companies are engaged in all principal aspects of the oil and natural gas industry. They also have interests in chemicals and additional interests in power generation and renewable energy (chiefly in wind and solar energy). The Group conducts its business through five principal segments, Exploration & Production, Gas & Power, Oil Products, Chemicals and Other businesses. These activities are conducted in more than 140 countries and territories and are subject to changing economic, regulatory and political conditions.

2. Basis of preparation

The First Quarter Condensed Interim Financial Report of the Royal Dutch/ Shell Group has been prepared in accordance with International Accounting Standard (IAS) 34 Interim Financial Reporting and with the policies set out in Note 3. These are the policies which the Group expects to apply in its first annual financial statements under International Financial Reporting Standards (IFRS) for the year ending December 31, 2005. The policies are in accordance with the recognition and measurement requirements of those IFRS and International Financial Reporting Interpretations Committee (IFRIC) interpretations issued by the International Accounting Standards Board that are effective or will be early adopted by the Group at December 31, 2005.

This represents the Group’s first application of IFRS and the accounting policies are set out in Note 3 below. Group Financial Statements for 2004 had been prepared in accordance with US Generally Accepted Accounting Principles (GAAP); accounting policies were set out in Note 3 in those Financial Statements. US GAAP differs in certain respects from IFRS and comparative figures for 2004 have been restated as necessary in accordance with IFRS. Reconciliations and descriptions of the effect of the transition from US GAAP to IFRS on equity, income and cash flows are given below in Note 9, including a description of the nature of the changes in accounting policies. As part of the Group’s adoption of IFRS, the following elections were made under IFRS 1 First-time Adoption of International Financial Reporting Standards as at January 1, 2004:

The policies have been consistently applied to all periods presented except for those relating to the classification and measurement of financial instruments to the extent that IFRS differs from US GAAP. The Group has also taken the exemption available under IFRS 1 to only apply IAS 32 and IAS 39 from January 1, 2005 and the impact on transition is described in Notes 3 and 7.

The Condensed Interim Financial Report has been prepared under the historical cost convention as modified by the revaluation of certain financial assets and liabilities. 8 Royal Dutch/Shell Group of Companies

• cumulative currency translation differences were eliminated by transfer to retained earnings. • cumulative previously unrecognised actuarial gains and losses on post-employment benefits were recognised. • prior business combinations have not been restated. • IFRS 2 Share-based Payment has only been applied to options issued after November 7, 2002 and not vested by January 1, 2005.

Unaudited Condensed Interim Financial Report

The preparation of interim financial information in conformity with IFRS requires the use of certain accounting estimates. It also requires management to exercise its judgment in the process of applying the Group’s accounting policies. Actual results could differ from those estimates.

This report should be read in conjunction with the Group Financial Statements and notes thereto in the 2004 Annual Report on Form 20-F/A (Amendment No.1).

3. Accounting policies

Nature of the Condensed Interim Financial Report The Condensed Interim Financial Report, which is presented in US dollars, includes the accounts of companies in which Royal Dutch and Shell Transport together, either directly or indirectly, have control either through a majority of the voting rights (including potential voting rights) or the right to exercise control or to obtain the majority of the benefits and be exposed to the majority of the risks.

Revenue recognition Sales of oil, natural gas, chemicals and all other products are recorded when title passes to the customer. Revenue from the production of oil and natural gas properties in which the Group has an interest with other producers are recognised on the basis of the Group’s working interest (entitlement method). Gains and losses on derivatives contracts and contracts involved in energy trading and risk management are shown net in the Statement of Income if these contracts are held for trading purposes. Purchase and sale of hydrocarbons under exchange contracts that are necessary to obtain or reposition feedstock utilised in the Group’s refinery operations are shown net in the Statement of Income. Sales between Group companies, as disclosed in the segment information, are based on prices generally equivalent to commercially available prices.

In Exploration & Production and Gas & Power title typically passes (and revenues are recognised) when product is physically transferred into a vessel, pipe or other delivery mechanism. For sales by refining companies, title typically passes (and revenues are recognised) either when product is placed onboard a vessel or offloaded from the vessel, depending on the contractually agreed terms. Revenues on wholesale sales of oil products and chemicals are recognised when transfer of ownership occurs and title is passed, either at the point of delivery or the point of receipt, depending on contractual conditions.

Property, plant and equipment and intangible assets (a) Recognition on the Balance Sheet

Property, plant and equipment, including expenditure on major inspections, and intangible assets are initially recorded on the Balance Sheet at cost where it is probable that they will generate future economic benefits. This includes capitalisation of decommissioning and restoration costs associated with provisions for asset retirement (see “Provisions”) and certain development costs (see “Research and development”). Accounting for exploration costs is described separately below (“Exploration costs”). Intangible assets include goodwill. Interest is capitalised, as an increase in property, plant and equipment, on significant capital projects during construction.

Property, plant and equipment and intangible assets are subsequently recognised at cost less accumulated depreciation and impairment.

(b) Depreciation, depletion and amortisation

Property, plant and equipment related to oil and natural gas production activities are depreciated on a unit-of-production basis over the proved developed reserves of the field concerned, except in the case of assets whose useful life is shorter than the lifetime

Royal Dutch/Shell Group of Companies 9

Unaudited Condensed Interim Financial Report

of the field, in which case the straight-line method is applied. Rights and concessions are depleted on the unit-of-production basis over the total proved reserves of the relevant area. Unproved properties are amortised as required by particular circumstances. Other property, plant and equipment are generally depreciated on a straight-line basis over their estimated useful lives which is generally 20 years for refineries and chemicals plants, 15 years for retail service station facilities, and until the next planned major inspection (generally 3 to 5 years) for inspection costs. Property, plant and equipment held under finance leases are depreciated over the shorter of the assets’ estimated useful lives and the lease term.

Goodwill is not amortised but instead tested for impairment annually. Other intangible assets are amortised on a straight-line basis over their estimated useful lives (with a maximum of forty years).

(c) Recoverability of assets

Other than properties with no proved reserves (where the basis for carrying costs on the Balance Sheet is explained under “Exploration costs”), the carrying amounts of major Exploration & Production property, plant and equipment are reviewed for possible impairment annually, while all assets are reviewed whenever events or changes in circumstances indicate that the carrying amounts for those assets may not be recoverable. If assets are determined to be impaired, the carrying amounts of those assets are written down to recoverable amount which is the higher of fair value less costs to sell and value in use. For this purpose, assets are grouped based on separately identifiable and largely independent cash flows. Assets held for sale are recognised at the lower of carrying amount and fair value less costs to sell.

Estimates of future cash flows used in the evaluation for impairment of assets related to hydrocarbon production are made using risk assessments on field and reservoir performance and include outlooks on proved reserves and unproved volumes, which are then discounted or risk-weighted utilising the results from projections of geological, production, recovery and economic factors.

Impairments, except those related to goodwill, are reversed as applicable to the extent that the events or circumstances that triggered the original impairment have changed.

Exploration costs Group companies follow the successful efforts method of accounting for oil and natural gas exploration costs. Exploration costs are charged to income when incurred, except that exploratory drilling costs are included in property, plant and equipment, pending determination of proved reserves. Exploration wells that are more than 12 months old are expensed unless (a) (i) they are in an area requiring major capital expenditure before production can begin and (ii) they have found commercially producible quantities of reserves and (iii) they are subject to further exploration or appraisal activity in that either drilling of additional exploratory wells is under way or firmly planned for the near future, or (b) proved reserves are booked within 12 months following the completion of exploratory drilling.

Associated companies and joint ventures Investments in companies over which Group companies have significant influence but not control are classified as associated companies and are accounted for on the equity basis. Interests in jointly controlled entities are also recognised on the equity basis. Interests in jointly controlled assets are recognised by including the Group share of assets, liabilities, income and expenses on a line-by-line basis.

Inventories Inventories are stated at cost to the Group or net realisable value, whichever is lower. Such cost is determined by the first-in first-out (FIFO) method and comprises direct purchase costs, cost of production, transportation and manufacturing expenses and taxes.

Deferred taxation Deferred taxation is provided using the liability method of accounting for income taxes based on provisions of enacted or substantively enacted laws. Recognition is given to deferred tax assets and liabilities for the expected future tax consequences of events that have been recognised in the Interim Financial Report or in the tax returns (temporary differences); deferred tax is not generally provided on initial recognition of an asset or liability in a transaction that, at the time of the transaction, affects neither accounting nor taxable profit. In estimating these tax consequences, consideration is given to expected future events.

Deferred tax assets are recognised where future recovery is probable. Deferred tax assets and liabilities are presented separately in the Balance Sheet except where there is a right of set-off within fiscal jurisdictions.

Deferred tax is not provided for taxes on possible future distributions of retained earnings of Group companies and equity accounted investments where the timing of the distribution can 10 Royal Dutch/Shell Group of Companies

Unaudited Condensed Interim Financial Report

be controlled and it is probable that the retained earnings will be substantially reinvested by the companies concerned.

Employee benefits (a) Employee retirement plans

Retirement plans to which employees contribute and many non-contributory plans are generally funded by payments to independent trusts. Where, due to local conditions, a plan is not funded, a provision is made. Valuations of both funded and unfunded plans are carried out by independent actuaries.

For plans which define the amount of pension benefit to be provided, pension cost primarily represents the increase in actuarial present value of the obligation for pension benefits based on employee service during the year and the interest on this obligation in respect of employee service in previous years, net of the expected return on plan assets.

Unrecognised gains and losses at the date of transition to IFRS have been recognised in the 2004 opening balance sheet. The Group recognises actuarial gains and losses that arise subsequent to January 1, 2004 using the corridor method. Under this method, to the extent that any cumulative unrecognised actuarial gain or loss exceeds 10% of the greater of the present value of the defined benefit obligation and the fair value of plan assets, that portion is recognised in income over the expected average remaining working lives of the employees participating in the plan. Otherwise, the actuarial gain or loss is not recognised.

For plans where benefits depend solely on the amount contributed to the employee’s account and the returns earned on investments of these contributions, pension cost is the amount contributed by Group companies for the period.

(b) Postretirement benefits other than pensions

Some Group companies provide certain postretirement healthcare and life insurance benefits to retirees, the entitlement to which is usually based on the employee remaining in service up to retirement age and the completion of a minimum service period. These plans are not funded and a provision is made. Valuations of benefits are carried out by independent actuaries.

The expected costs of postretirement benefits other than pensions are accrued over the periods employees render service to the Group. Unrecognised gains and losses at the date of transition to IFRS have been recognised in the 2004 opening balance sheet.

(c) Share-based compensation plans

The fair value of share options granted to employees after November 7, 2002, and which had not vested by January 1, 2005, is recognised as an expense from the date of grant over the vesting period with a corresponding increase directly in equity. The fair value of the Group’s share options was estimated using a Black-Scholes option pricing model.

Leases Agreements under which Group companies make payments to owners in return for the right to use an asset for a period are accounted for as leases. Leases that transfer substantially all the risks and benefits of ownership are recorded at inception as finance leases within property, plant and equipment and debt. All other leases are recorded as operating leases and the costs are charged to income as incurred.

Financial instruments and other derivative contracts The Group adopted IAS 32 and IAS 39 with effect from January 1, 2005 and therefore accounted for financial instruments and other derivative contracts until the end of 2004 under US GAAP. Information for 2004 has not been restated and the impact on transition, which is restricted to certain commodity contracts and embedded derivatives and unquoted investments with estimable fair values, is described below.

(a) Financial assets

Investments: financial assets comprise debt and equity securities.

Securities of a trading nature Securities of a trading nature are carried at fair value with unrealised holding gains and losses being included in income.

Securities held to maturity Securities held to maturity are carried at amortised cost, unless impaired.

Available for sale securities All other securities are classified as available for sale and are carried at fair value, other than unquoted equity securities with no estimable fair value which are reported at cost, less any impairment. Unrealised holding gains and losses other than impairments are taken directly to equity, except for translation differences arising on foreign currency debt securities which are taken to income. Upon sale or maturity, the net gains and losses are included in income.

Fair value is based on market prices where available, otherwise it is calculated as the net present value of expected future cash flows.

Royal Dutch/Shell Group of Companies 11

Unaudited Condensed Interim Financial Report

From January 1, 2005 this has resulted in certain unquoted equity securities being recognised at fair value compared with recognition at cost under US GAAP and the impact on transition is disclosed in Note 7. This change in accounting has no impact on the timing of recognition of income arising from these investments.

Securities forming part of a portfolio which is required to be held long-term are classified under investments.

Interest on debt securities is accounted for in income by applying the effective interest method. Dividends on equity securities are accounted for in income when receivable.

Receivables are recognised initially at fair value based on amounts exchanged and subsequently at amortised cost less any impairment.

Cash and cash equivalents include cash in hand, short-term deposits and other investments which have a maturity from acquisition of three months or less and are readily convertible into known amounts of cash.

(b) Financial liabilities

Debt and accounts payable are recognised initially at fair value based on amounts exchanged and subsequently at amortised cost, except for fixed rate debt subject to fair value hedging.

Interest expense, other than interest capitalised, is accounted for in income using the effective interest method.

(c) Derivative contracts

Group companies use derivatives in the management of interest rate risk, foreign currency risk and commodity price risk. These derivative contracts are recognised at fair value, using market prices.

Those derivatives qualifying and designated as hedges are either: (1) a “fair value” hedge of the change in fair value of a recognised asset or liability or an unrecognised firm commitment, or (2) a “cash flow” hedge of the change in cash flows to be received or paid relating to a recognised asset or liability or a highly probable forecasted transaction.

A change in the fair value of a hedging instrument designated as a fair value hedge is taken to income, together with the consequential adjustment to the carrying amount of the hedged item. The effective portion of a change in fair value of a derivative designated as a cash flow hedge is recognised directly in equity, until income reflects the variability of underlying cash flows; any ineffective portion is taken to income.

Group companies formally document all relationships between hedging instruments and hedged items, as well as risk management objectives and strategies for undertaking hedge transactions. The effectiveness of a hedge is also continually assessed and when it ceases, hedge accounting is discontinued.

Certain contracts to purchase and sell commodities are required to be recognised at fair value, generally based on market prices, (with gains and losses taken to income). These are contracts which can be net settled or sales contracts containing volume optionality.

Certain embedded derivatives within contracts are required to be separated from their host contract and recognised at fair value, generally based on market prices, (with gains and losses taken to income) if the economic characteristics and risks of the embedded derivative are not closely related to that of the host contract.

These policies are very similar to those applied until the end of 2004 under US GAAP and the impact of the application on January 1, 2005 is shown in Note 7.

Provisions Provisions are liabilities where the timing or amount of future expenditure is uncertain. Provisions are recorded at the best estimate of the present value of the expenditure required to settle the present obligation at the balance sheet date. Non-current amounts are discounted using the risk-free rate. Specific details for decommissioning and restoration costs and environmental remediation are described below.

Estimated decommissioning and restoration costs are based on current requirements, technology and price levels and are stated at fair value, and the associated asset retirement costs are capitalised as part of the carrying amount of the related property, plant and equipment. The liability, once an obligation, whether legal or constructive, crystallises, is recognised with a corresponding amount of property, plant and equipment in the period when a reasonable estimate of the fair value can be made. The fair value is calculated using amounts discounted over the useful economic life of the assets. The effects of changes resulting from revisions to the timing or the amount of the original estimate of the provision are incorporated on a prospective basis.

Provisions for environmental remediation resulting from ongoing or past operations or events are recognised in the period in which an obligation, legal or constructive, to a third party arises and the

12 Royal Dutch/Shell Group of Companies

Unaudited Condensed Interim Financial Report

amount can be reasonably estimated. Measurement of liabilities is based on current legal requirements and existing technology. Recognition of any joint and several liability is based upon Group companies’ best estimate of their final pro rata share of the liability. Liabilities are determined independently of expected insurance recoveries. Recoveries are recognised and reported as separate events and brought into account when reasonably certain of realisation. The carrying amount of provisions is regularly reviewed and adjusted for new facts or changes in law or technology.

Parent Companies’ shares held by Group companies Parent Companies’ shares held by Group companies are not included in assets but, after deducting dividends received, are reflected at cost as a deduction from equity.

Administrative expenses Administrative expenses are those which do not relate directly to the activities of a single business segment and include expenses incurred in the management and co-ordination of multi-segment enterprises.

Research and development Development costs which are expected to generate probable future economic benefits are capitalised. All other research and development expenditure is charged to income as incurred, with the exception of that on buildings and major items of equipment which have alternative use.

Discontinued operations Discontinued operations comprise those activities which have been disposed of during the period, or remain held for sale at period end, and represent a separate major line of business or geographical area of operation which can be clearly distinguished, operationally and for financial reporting purposes, from other activities of the Group.

Business combinations Assets acquired and liabilities assumed on a business combination are recognised at their fair value at the date of the acquisition; the amount of the purchase consideration above this value is reflected as goodwill.

Currency translation Assets and liabilities of non-US dollar Group companies are translated to US dollars at year-end rates of exchange, whilst their statements of income and cash flows are translated at quarterly average rates. Translation differences arising on aggregation are taken directly to a currency translation differences account within equity. As part of the transition to IFRS, the balance of this account was eliminated at January 1, 2004 and transferred to retained earnings with no impact on total equity. Upon divestment or liquidation of an entity, cumulative currency translation differences related to that entity are taken to income.

The US dollar equivalents of exchange gains and losses arising as a result of foreign currency transactions (including those in respect of inter-company balances unless related to transactions of a long-term investment nature) are included in income.

New accounting standards and interpretations Certain new IFRS and IFRIC interpretations have been published which are not mandatory for 2005. The Group has elected to early adopt in 2005 IFRS 6 Exploration for and Evaluation of Mineral Resources and IFRIC 4 Determining whether an Arrangement Contains a Lease, and these are reflected in the accounting policies described above. The Group is assessing the impact of IFRIC 3 Emission Rights which also remains subject to potential change prior to its mandatory use in 2006. All other published pronouncements, which are not mandatory in 2005, are not expected to have an impact on the Group.

IFRS is currently being applied in Europe and in other parts of the world simultaneously for the first time. Furthermore, due to a number of new and revised standards included within the body of standards that comprise IFRS, there is not yet a significant body of established practice on which to draw in forming judgements regarding interpretation and application. Accordingly, practice is continuing to evolve and the full financial effect of reporting under IFRS as it will be applied and reported on in the Group’s first IFRS Financial Statements cannot be determined with certainty at this stage.

Royal Dutch/Shell Group of Companies 13

Unaudited Condensed Interim Financial Report

4. Income/(expense) recognised directly in equity attributable to Parent Companies

Presented under IFRS

14 Royal Dutch/Shell Group of Companies

$ millionIncome/(expense)

At December 31, IAS At January 1, First At March 31,2004 32/39 2005 Quarter 2005

after IAS 32/39transition

Cumulative currency translation differences 2,729 – 2,729 (1,450) 1,279

Unrealised gains/(losses) on securities 350 823 1,173 (23) 1,150

Unrealised gains/(losses) on cash flow hedges (157) – (157) (34) (191)

Share-based compensation 173 – 173 43 216

Total 3,095 823 3,918 (1,464) 2,454

$ million2004

Income/(expense)

January 1 First March 31Quarter

Cumulative currency translation differences – (347) (347)

Unrealised gains/(losses) on securities 700 (418) 282

Unrealised gains/(losses) on cash flow hedges (188) (11) (199)

Share-based compensation 58 19 77

Total 570 (757) (187)

Unaudited Condensed Interim Financial Report

5. Information by business segment

Presented under IFRS

Royal Dutch/Shell Group of Companies 15

Segment information — First Quarter 2005 $ millionExploration & Gas & Power Oil Products Chemicals Corporate and Eliminations Total

Production Other Group

2005

Revenue Third party 4,565 3,277 55,996 8,026 292 72,156 Inter-segment 7,240 370 1,535 748 – (9,893)

Total 11,805 3,647 57,531 8,774 292 (9,893) 72,156

Segment result 5,528 196 3,477 804 (209) 9,796 Share of profit of equity accounted

investments 714

257

518

84

–

1,573

Net finance costs 83Other income 5 Taxation 4,273

Income from continuing operations 7,018 Income from discontinued operations (214) (214)

Income for the period 6,804

Segment information — First Quarter 2004 $ millionExploration & Gas & Power Oil Products Chemicals Corporate and Eliminations Total

Production Other Group

2004

Revenue Third party 3,776 2,161 45,394 5,581 356 57,268 Inter-segment 5,666 331 1,036 699 3 (7,735)

Total 9,442 2,492 46,430 6,280 359 (7,735) 57,268

Segment result 4,353 108 1,832 151 (100) 6,344 Share of profit of equity accounted

investments 609 229 230 63 – 1,131

Net finance costs 262 Other income 436Taxation 2,822

Income from continuing operations 4,827 Income from discontinued operations 20 20

Income for the period 4,847

Unaudited Condensed Interim Financial Report

The information above is provided in accordance with IAS 14 Segment Reporting. Operating segment results are appraised by management on the basis of income including equity accounted investments and certain net finance costs and other (income)/ expense and after tax, and this forms the basis of the discussion of segment results in the Operational and Financial Review (OFR). The table below reconciles the foregoing segment information to the information used for management reporting and is consistent with how the information will be presented in the Group’s annual financial statements to comply with SFAS 131.

6. Discontinued operations

Discontinued operations comprise the activities of Basell, a jointly controlled Chemicals entity (Group interest 50%), which has been held for sale at fair value less costs to sell since the announcement in 2004 of a review of strategic alternatives regarding this venture. The loss for the First Quarter 2005 comprises an impairment in order to reflect the carrying amount at March 31, 2005 at fair value less costs to sell.

7. Implementation of IAS 32 and IAS 39 Financial Instruments

As described in Note 3, the impact on transition at January 1, 2005 resulting from recognising at fair value certain additional derivative contracts and unquoted securities was an increase in total equity of $0.8 billion. This was reflected by increases in assets and liabilities at January 1, 2005 as follows:

16 Royal Dutch/Shell Group of Companies

Income for the period by segment — First Quarter 2005 $ millionExploration & Gas & Power Oil Products Chemicals Corporate and Total

Production Other Group

Segment result - IAS 14 5,528 196 3,477 804 (209) 9,796 Share of profit of equity accounted investments 714 257 518 84 – 1,573 Net finance costs and other (income)/expense 113 (37) 44 (1) (41) 78 Taxation 3,174 14 900 226 (41) 4,273 Discontinued operations – – – (214) – (214)

Segment result - OFR 2,955 476 3,051 449 (127) 6,804

Income for the period by segment — First Quarter 2004 $ millionExploration & Gas & Power Oil Products Chemicals Corporate and Total

Production Other Group

Segment result - IAS 14 4,353 108 1,832 151 (100) 6,344 Share of profit of equity accounted investments 609 229 230 63 – 1,131 Net finance costs and other (income)/expense 62 (200) (41) 8 (3) (174)Taxation 2,193 15 530 5 79 2,822 Discontinued operations – – – 20 – 20

Segment result - OFR 2,707 522 1,573 221 (176) 4,847

$ million

Investments: financial assets 1,018Non-current assets: deferred tax 5Current assets 42Non-current liabilities: deferred tax (195)Current liabilities (54)

816

Unaudited Condensed Interim Financial Report

8. Contingencies and litigation

Shell Oil Company (including subsidiaries and affiliates, referred to collectively as SOC), along with numerous other defendants, has been sued by public and quasi-public water purveyors, as well as governmental entities, alleging responsibility for groundwater contamination caused by releases of gasoline containing oxygenate additives. Most of these suits assert various theories of liability, including product liability, and seek to recover actual damages, including clean-up costs. Some assert claims for punitive damages. As of May 9, 2005, there were approximately 66 pending suits by such plaintiffs that asserted claims against SOC and many other defendants (including major energy and refining companies). Although a majority of these cases do not specify the amount of monetary damages sought, some include specific damage claims collectively against all defendants. While the aggregate amounts claimed against all defendants for actual and punitive damages in such suits could be material to the Financial Statements if they were ultimately recovered against SOC alone rather than apportioned among the defendants, management of the Group considers the amounts claimed in these pleadings to be highly speculative and not an appropriate basis on which to determine a reasonable estimate of the amount of the loss that may be ultimately incurred, for the reasons described below.

The reasons for this determination can be summarised as follows:

For these reasons, management of the Group is not currently able to estimate a range of reasonably possible losses or minimum loss for this litigation; however, management of the Group does not currently believe that the outcome of the oxygenate-related litigation pending as of May 9, 2005 will have a material impact on the Group’s financial condition, although such resolutions could have a significant effect on results for the period in which they are recognised.

A $490 million judgment in favour of 466 plaintiffs in a consolidated matter that had once been nine individual cases was rendered in 2002 by a Nicaraguan court jointly against SOC and three other named defendants (not affiliated with SOC), based upon Nicaraguan Special Law 364 for claimed personal injuries resulting from alleged exposure to dibromochloropropane (DBCP) — a pesticide manufactured by SOC prior to 1978. This special law imposes strict liability (in a predetermined amount) on international manufacturers of DBCP. The statute also provides

Royal Dutch/Shell Group of Companies 17

• While the majority of the cases have been consolidated for pre-trial proceedings in the U.S. District Court for the Southern District of New York, there are many cases pending in other jurisdictions throughout the U.S. Most of the cases are at a preliminary stage. In many matters, little discovery has been taken and many critical substantial legal issues remain unresolved. Consequently, management of the Group does not have sufficient information to assess the facts underlying the plaintiffs’ claims; the nature and extent of damages claimed, if any; the reasonableness of any specific claim for money damages; the allocation of potential responsibility among defendants; or the law that may be applicable. Additionally, given the pendency of cases in varying jurisdictions, there may be inconsistencies in the determinations made in these matters.

• There are significant unresolved legal questions relating to claims asserted in this litigation. For example, it has not been established

whether the use of oxygenates mandated by the 1990 amendments to the Clean Air Act can give rise to a products liability based claim. While some trial courts have held that it cannot, other courts have left the question open or declined to dismiss claims brought on a products liability theory. Other examples of unresolved legal questions relate to the applicability of federal preemption, whether a plaintiff may recover damages for alleged levels of contamination significantly below state environmental standards, and whether a plaintiff may recover for an alleged threat to groundwater before detection of contamination.

• There are also significant unresolved legal questions relating to whether punitive damages are available for products liability claims or, if

available, the manner in which they might be determined. For example, some courts have held that for certain types of product liability claims, punitive damages are not available. It is not known whether that rule of law would be applied in some or all of the pending oxygenate additive cases. Where specific claims for damages have been made, punitive damages represent in most cases a majority of the total amounts claimed.

• There are significant issues relating to the allocation of any liability among the defendants. Virtually all of the oxygenate additives cases

involve multiple defendants including most of the major participants in the retail gasoline marketing business in the regions involved in the pending cases. The basis on which any potential liability may be apportioned among the defendants in any particular pending case cannot yet be determined.

Unaudited Condensed Interim Financial Report

that unless a deposit (calculated as described below) of an amount denominated in Nicaraguan cordobas is made into the Nicaraguan courts, the claims would be submitted to the US courts. In SOC’s case the deposit would have been between $19 million and $20 million (based on an exchange rate between 15 and 16 cordobas per US dollar). SOC chose not to make this deposit. The Nicaraguan courts did not, however, give effect to the provision of Special Law 364 that requires submission of the matter to the US courts. Instead, the Nicaraguan court entered judgment against SOC and the other defendants. Further, SOC was not afforded the opportunity to present any defences in the Nicaraguan court, including that it was not subject to Nicaraguan jurisdiction because it had neither shipped nor sold DBCP to parties in Nicaragua. At this time, SOC has not completed the steps necessary to perfect an appeal in Nicaragua and, as described below, the Nicaraguan claimants have sought to enforce the Nicaraguan judgment against SOC in the U.S. and in Venezuela. SOC does not have any assets in Nicaragua. In 2003, an attempt by the plaintiffs to enforce the Nicaraguan judgment described above in the United States against Shell Chemical Company and purported affiliates of the other named defendants was rejected by the U.S. District Court for the Central District of California, which decision is on appeal before the Ninth Circuit Court of Appeals. Enforcement of the Nicaraguan judgment was rejected because of improper service and attempted enforcement against non-existent entities or entities that were not named in the Nicaraguan judgment. Thereafter, SOC filed a declaratory judgment action seeking ultimate adjudication of the non-enforceability of this Nicaraguan judgment in the U.S. District Court for the Central District of California. This district court denied motions filed by the Nicaraguan claimants to dismiss SOC claims that Nicaragua does not have impartial tribunals, the proceedings violated due process, the relationship between SOC and Nicaragua made the exercise of personal jurisdiction unreasonable, and Special Law 364 is repugnant to U.S. public policy because it violates due process. A finding in favour of SOC on any of these grounds will result in a refusal to recognize and enforce the judgment in the United States. Several requests for Exequatur were filed in 2004 with the Tribunal Suprema de Justicia (the Venezuelan Supreme Court) to enforce Nicaraguan judgments. The petitions imply that judgments can be satisfied with assets of Shell Venezuela, S.A., which was neither a party to the Nicaraguan judgment nor a subsidiary of SOC, against whom the Exequatur was filed. The petitions are pending before the Tribunal Suprema de Justicia. As of May 9, 2005, five additional Nicaraguan judgments had been entered in the collective amount of approximately $226.5 million in favor of 240 plaintiffs jointly against Shell Chemical Company and three other named defendants (not affiliated with Shell Chemical Company) under facts and circumstances almost identical to those relating to the judgment described above. Additional judgments are anticipated (including a suit seeking more than $3 billion). It is the opinion of management of the Group that the above judgments are unenforceable in a U.S. court, as a matter of law, for the reasons set out in SOC’s declaratory judgment action described above. No financial provisions have been established for these judgments or related claims.

Since 1984, SOC has been named with others as a defendant in numerous product liability cases, including class actions, involving the failure of residential plumbing systems and municipal water distribution systems constructed with polybutylene plastic pipe. SOC fabricated the resin for this pipe while the co-defendants fabricated the raw materials for the pipe fittings. As a result of two class action settlements in 1995, SOC and the co-defendants agreed on a mechanism to fund until 2009 the settlement of most of the residential plumbing claims in the United States. Financial provisions have been taken by SOC for its settlement funding needs anticipated at this time. Additionally, claims that are not part of these class action settlements or that challenge these settlements continue to be filed primarily involving alleged problems with polybutylene pipe used in municipal water distribution systems. It is the opinion of management of the Group that exposure from this other polybutylene litigation pending as of May 9, 2005, is not material. Management of the Group cannot currently predict when or how all polybutylene matters will be finally resolved.

In connection with the recategorisation of certain hydrocarbon reserves that occurred in 2004, a number of putative shareholder class actions were filed against Royal Dutch, Shell Transport, Managing Directors of Royal Dutch during the class period, Managing Directors of Shell Transport during the class period and the external auditors for Royal Dutch, Shell Transport and the Group. These actions were consolidated in the United States District Court in New Jersey and a consolidated complaint was filed in September 2004. The parties are awaiting a decision with respect to defendants’ motions to dismiss asserting lack of jurisdiction with respect to the claims of non-United States shareholders who purchased on non-United States securities exchanges and failure to state a claim. Merits discovery has not begun. The case is at an early stage and subject to substantial uncertainties concerning the outcome of the material factual and legal issues relating to the litigation, including the pending motions to dismiss on lack of jurisdiction and failure to state a claim. In addition, potential damages, if any, in a fully litigated securities class action would depend on the losses caused by the alleged wrongful conduct that would be demonstrated by individual class members in their purchases and sales of Royal Dutch and Shell Transport shares during the relevant class period. Accordingly, based on the current status of the litigation, management of the Group is unable to estimate a range of possible losses or any minimum loss. Management of the Group will review this determination as the litigation progresses.

Also in connection with the hydrocarbon reserves recategorisation, putative shareholder class actions were filed on behalf of participants in various Shell Oil Company qualified plans alleging that Royal Dutch, Shell Transport and various current and former officers and directors breached various fiduciary duties to employee participants imposed by the Employee Retirement Income Security Act of 1974 (ERISA). These suits were consolidated in the United States District Court in New Jersey and a consolidated class action complaint was filed in July 2004. Defendants’ motions to dismiss have been fully briefed. Some document discovery has taken place. The case is at an early stage and subject 18 Royal Dutch/Shell Group of Companies

Unaudited Condensed Interim Financial Report

to substantial uncertainties concerning the outcome of the material factual and legal issues relating to the litigation, including the pending motion to dismiss and the legal uncertainties with respect to the methodology for calculating damage, if any, should defendants become subject to an adverse judgment. The Group is in settlement discussions with counsel for plaintiffs, which it hopes will lead to a successful resolution of the case without the need for further litigation. No financial provisions have been taken with respect to the ERISA litigation.

The reserves recategorisation also led to the filing of shareholder derivative actions in June 2004. The four suits pending in New York state court, New York federal court and New Jersey federal court demand Group management and structural changes and seek unspecified damages from current and former members of the Boards of Directors of Royal Dutch and Shell Transport. The suits are in preliminary stages and no responses are yet due from defendants. The Group is in settlement discussions with counsel for plaintiffs, which it hopes will lead to a successful resolution of the case without the need for further litigation. Because any money “damages” in the derivative actions would be paid to Royal Dutch and Shell Transport, management of the Group does not believe that the resolution of these suits will have a material adverse effect on the Group’s financial condition or operating results.

The United States Securities and Exchange Commission (SEC) and UK Financial Services Authority (FSA) issued formal orders of private investigation in relation to the reserves recategorisation which Royal Dutch and Shell Transport resolved by reaching agreements with the SEC and the FSA. In connection with the agreement with the SEC, Royal Dutch and Shell Transport consented, without admitting or denying the SEC’s findings or conclusions, to an administrative order finding that Royal Dutch and Shell Transport violated, and requiring Royal Dutch and Shell Transport to cease and desist from future violations of, the antifraud, reporting, recordkeeping and internal control provisions of the US Federal securities laws and related SEC rules, agreed to pay a $120 million civil penalty and undertook to spend an additional $5 million developing a comprehensive internal compliance program. In connection with the agreement with the FSA, Royal Dutch and Shell Transport agreed, without admitting or denying the FSA’s findings or conclusions, to the entry of a Final Notice by the FSA finding that Royal Dutch and Shell Transport breached market abuse provisions of the UK’s Financial Services and Markets Act 2000 and the Listing Rules made under it and agreed to pay a penalty of £17 million. The penalties from the SEC and FSA have been paid by Group companies and fully included in the Income Statement of the Group for the year 2004. The United States Department of Justice has commenced a criminal investigation, and Euronext Amsterdam, the Dutch Authority Financial Markets and the California Department of Corporations are investigating the issues related to the reserves recategorisation. Management of the Group cannot currently predict the manner and timing of the resolution of these pending matters and is currently unable to estimate the range of reasonably possible losses from such matters.

Group companies are subject to a number of other loss contingencies arising out of litigation and claims brought by governmental and private parties, which are handled in the ordinary course of business.

The operations and earnings of Group companies continue, from time to time, to be affected to varying degrees by political, legislative, fiscal and regulatory developments, including those relating to the protection of the environment and indigenous people, in the countries in which they operate. The industries in which Group companies are engaged are also subject to physical risks of various types. The nature and frequency of these developments and events, not all of which are covered by insurance, as well as their effect on future operations and earnings, are unpredictable.

Royal Dutch/Shell Group of Companies 19

Unaudited Condensed Interim Financial Report

9. Reconciliations from US GAAP to IFRS

(a) Reconciliation of Statement of Income

First Quarter 2004 $ millionEffect of transition

US GAAP to IFRS1 IFRS

Sales proceeds 74,908 (160) 74,748Less: Sales taxes, excise duties and similar

levies 17,694

(214)

17,480

Revenue 57,214 54 57,268Cost of sales 47,261 176 47,437

Gross profit 9,953 (122) 9,831 Selling and distribution expenses 2,835 78 2,913Administrative expenses 471 (8) 463Exploration 124 (13) 111Research and development 136 (136) –Share of profit of equity accounted

investments 1,290

(159)

1,131

Net finance costs 152 110 262 Other income 436 – 436

Income before taxation 7,961 (312) 7,649Taxation 3,490 (668) 2,822

Income from continuing operations 4,471 356 4,827Income from discontinued operations 262 (242) 20

Income for the period 4,733 114 4,847

Attributable to minority interests 125 20 145

Income attributable to Parent Companies 4,608 94 4,702

2004 $ millionEffect of transition

US GAAP to IFRS2 IFRS

Sales proceeds 337,522 1,234 338,756Less: Sales taxes, excise duties and similar

levies 72,332

38

72,370

Revenue 265,190 1,196 266,386Cost of sales 221,678 1,581 223,259

Gross profit 43,512 (385) 43,127Selling and distribution expenses 12,340 210 12,550 Administrative expenses 2,516 6 2,522Exploration 1,823 (14) 1,809Research and development 553 (553) –Share of profit of equity accounted

investments 5,653

(638)

5,015

Net finance costs 561 54 615Other income 1,013 – 1,013

Income before taxation 32,385 (726) 31,659 Taxation 15,136 (2,969) 12,167

Income from continuing operations 17,249 2,243 19,492Income from discontinued operations 1,560 (1,794) (234)

Income for the period 18,809 449 19,258

Attributable to minority interests 626 91 717

20 Royal Dutch/Shell Group of Companies

Income attributable to Parent Companies 18,183 358 18,541

1 See Note 9(d). 2 See Note 9(e).

Unaudited Condensed Interim Financial Report

(b) Reconciliation of Equity At January 1, 2004 (date of transition to IFRS)

Royal Dutch/Shell Group of Companies 21

$ millionEffect of transition

US GAAP to IFRS1 IFRS

ASSETS Non-current assets Property, plant and equipment 87,088 (807) 86,281 Intangible assets 4,735 (342) 4,393 Investments: equity accounted investments 19,371 (192) 19,179 financial assets 3,403 (54) 3,349 Deferred tax 2,092 971 3,063 Employee benefit assets 6,516 (5,055) 1,461 Other 2,741 138 2,879

125,946 (5,341) 120,605

Current assets Inventories 12,690 (13) 12,677 Accounts receivable 28,969 (326) 28,643 Cash and cash equivalents 1,952 (10) 1,942

43,611 (349) 43,262

Total assets 169,557 (5,690) 163,867

LIABILITIES Non-current liabilities Debt 9,100 174 9,274 Deferred tax 15,185 (1,384) 13,801 Employee benefit obligations 4,927 2,018 6,945 Other provisions 3,955 986 4,941 Other 6,054 (2,032) 4,022

39,221 (238) 38,983

Current liabilities Debt 11,027 6 11,033

Accounts payable and accrued

liabilities 32,347

(1,568)

30,779

Taxes payable 5,927 (561) 5,366 Employee benefit obligations – 319 319 Other provisions – 1,075 1,075 Dividends payable to Parent Companies 5,123 – 5,123

54,424 (729) 53,695

Total liabilities 93,645 (967) 92,678

EQUITY Equity attributable to Parent

Companies 72,497

(4,716)

67,781

Minority interests 3,415 (7) 3,408

Total equity (see Note 9(c)) 75,912 (4,723) 71,189

Total liabilities and equity 169,557 (5,690) 163,867

1 See Note 9(f)

Unaudited Condensed Interim Financial Report

At March 31, 2004

$ millionEffect of transition

US GAAP to IFRS1 IFRS

ASSETS Non-current assets Property, plant and equipment 86,141 (603) 85,538 Intangible assets 4,708 (335) 4,373 Investments: equity accounted investments 19,976 (88) 19,888 financial assets 2,648 (51) 2,597 Deferred tax2 2,092 958 3,050 Employee benefit assets 6,881 (5,223) 1,658 Other 3,034 142 3,176

125,480 (5,200) 120,280

Current assets Inventories 13,615 (13) 13,602 Accounts receivable 30,664 (435) 30,229 Cash and cash equivalents 5,732 (9) 5,723

50,011 (457) 49,554

Total assets 175,491 (5,657) 169,834

LIABILITIES Non-current liabilities Debt 9,728 174 9,902 Deferred tax2 15,174 (1,414) 13,760 Employee benefit obligations 4,940 1,949 6,889 Other provisions 4,360 883 5,243 Other 6,189 (1,897) 4,292

40,391 (305) 40,086

Current liabilities Debt 7,548 4 7,552

Accounts payable and accrued

liabilities 32,377

(869)

31,508

Taxes payable 9,950 (1,200) 8,750 Employee benefit obligations – 315 315 Other provisions – 1,048 1,048 Dividends payable to Parent Companies 5,091 – 5,091

54,966 (702) 54,264

Total liabilities 95,357 (1,007) 94,350

EQUITY Equity attributable to Parent

Companies 76,359

(4,641)

71,718

Minority interests 3,775 (9) 3,766

Total equity (see Note 9(c)) 80,134 (4,650) 75,484

Total liabilities and equity 175,491 (5,657) 169,834

1 See Note 9(g). 2 The amount of deferred tax assets at March 31, 2004 under US GAAP has not been recalculated from the amount at December 31, 2003.

22 Royal Dutch/Shell Group of Companies

Unaudited Condensed Interim Financial Report

At December 31, 2004

Royal Dutch/Shell Group of Companies 23

$ millionEffect of transition

US GAAP to IFRS1 IFRS

ASSETS Non-current assets Property, plant and equipment 88,940 (1,022) 87,918 Intangible assets 4,890 (362) 4,528 Investments: equity accounted investments 19,743 750 20,493 financial assets 2,748 (48) 2,700 Deferred tax 1,995 794 2,789 Employee benefit assets 8,278 (5,799) 2,479 Other 4,369 121 4,490

130,963 (5,566) 125,397

Current assets Inventories 15,391 (16) 15,375 Accounts receivable 37,998 (559) 37,439 Cash and cash equivalents 8,459 (6) 8,453

61,848 (581) 61,267

Total assets 192,811 (6,147) 186,664