for personal use only - asxh2/2016. drug in same class (fingolimod) previously failed in ppms. •...

TRANSCRIPT

Clinical Trials Update

For

per

sona

l use

onl

y

Safe Harbour Statements

This Presentation (and any financial information that may be provided by

Innate Immunotherapeutics Limited - the “Company”) may contain

forward looking statements that involve risks and uncertainties. Such

statements include statements regarding the Company’s belief or current

expectation and are necessarily based on the Company’s current

understanding of the markets and industries in which it operates. That

understanding could change or could prove to be inconsistent with

actual developments. The Company’s actual results could differ

materially from the results discussed in this Presentation, including those

anticipated in or implied by any forward looking statements.

2Effective Date: 30 July 2016

For

per

sona

l use

onl

y

Key Statistics as at 25 July 2016

ASX Code IIL (listed December 2013 at 20c)

Share price A$0.40 (low $0.12 – high $0.47)

Shares on issue 208.5 million

Market Cap ~A$85 million

Placements pending 13.5 million shares

Options 20.5 million (A$0.40 or higher)

Loyalty rights 33 million (expiry December 2016)

Cash in hand/pending A$8.5 million (inc R&D, placements)

Significant Shareholders

C. Collins (R-NY 27th District) 17.3%

Australian Ethical (fund) 9.8%

Caitlin & Cameron Collins 5.2%

Probe International Inc 2.6%

National MS Society (USA) 1.8%

3

For

per

sona

l use

onl

y

ASX:IIL - Investment thesis

• IIL’s lead drug candidate MIS416 will complete a double blindedplacebo controlled Phase 2B trial for secondary progressivemultiple sclerosis (SPMS) in April 2017

• There is already strong evidence of safety and likely efficacy fromprior trials and a unique 7 year ‘compassionate use’ programme

• There are no drugs currently approved for the safe ongoingtreatment of SPMS

• This unmet medical need could equate to a potential worldwideannual market of at least US$7.5B or more

• Many large drug companies are following IIL very closely

• IIL expects trial outcomes and a pharma transaction in H2/2017

4

For

per

sona

l use

onl

y

Bioshares: “What has been learned about the market need for your

product while it has been in clinical trials?”

• The unmet medical need in SPMS is just as great today as it was in 2009. Anest. 2.3 million people suffer from MS worldwide of which (30%) ~700,000have the progressive highly disabling SP form of MS.

• The commercial opportunity has increased significantly! Between 2008 and2012, US sales of disease modifying therapies (DMT) for RRMS doubled from$4 billion to nearly $9 billion annually. 2015 WW DMT sales = US$20.5 billion

5

• Before and since May 2009, no DMT’s have been approved forprogressive MS (either SPMS or PPMS):

• Dec 2014: RRMS anti S1-P1 drug Fingolimod failed Phase 3 in PPMS

• Oct 2015: RRMS drug Tysabri failed Phase 3 in SPMS

• Mar 2016: Phase 2 trial of repurposed Rituximab in SPMS abandoned

• Jun 2016: Biogen’s anti-lingo-1 misses primary endpoint in RRMS/SPMSFor

per

sona

l use

onl

y

Bioshares: “What has been learned about the market need for your

product while it has been in clinical trials?”

• What’s in the near-term SPMS Phase 3 pipeline?

• Novartis’ S1-P1 drug Siponimod Phase 3 trial in SPMS due to read out inH2/2016. Drug in same class (Fingolimod) previously failed in PPMS.

• Roche’s B-cell targeting Ocrelizumab should be approved for PRIMARYprogressive MS (NOT SPMS) later this year. Very modest efficacy signalin subset of PPMS patients. Likely some off-label use in SPMS.

6

• What’s our latest estimate of the SMPS market size?

• Based on 2015 RRMS drug sales of US$20.5 billon and RRMS patientsrepresenting ~60% of WW sufferers, we now estimate the potential WWmarket value for SPMS drugs to be US$7.5b to US$10b.

• Based on the RRMS experience, the SPMS market could support multipleUS$1b+ drugs once drugs like ours (MIS416) become available.

For

per

sona

l use

onl

y

Bioshares: “What have you learnt through the clinical trial process –

what would you have done differently?”

• Even if the CRO and the PIs tell you they can execute the study plan – it paysto have a plan ‘B’ or be able to develop one quick ...

• Resident patient population is not predictive of site recruitment performance!

• If you’re running an AU based study, it pays to also have as many NZ sites aspossible. Plan for it with a R&D incentive ‘Advance Finding’.

• Patients with SPMS who volunteer for clinical trials are tough and they stickwith the programme.

7

For

per

sona

l use

onl

y

Bioshares: “How much risk should investors be attributing

to your clinical programme?”

So here’s the bad news about clinical trials generally:

8

Transition success rates from phase to phase and likelihood of approval (LOA)from Phase I for all diseases, all modalities.

Sourc

e:C

linic

alD

eve

lopm

entS

ucc

ess

Rate

s2006-

2015.B

IOIn

dust

ryA

naly

sis

For

per

sona

l use

onl

y

Bioshares: “How much risk should investors be attributing

to your clinical programme?”

So here’s the good news about Innate’s clinical trial:

9

Two former clinical trial patients talk about their experiencewith MIS416: http://tinyurl.com/IILCUVideo

A new compassionate use patient (4-5 months):https://www.youtube.com/watch?v=KYIHFTbG-w8

A former clinical trial patient talks about her MIS416 experience:https://www.youtube.com/watch?v=Wtcnhe66fZU

“I would certainly recommend MIS416 as I have seen significant improvementin the motor skills and general wellbeing of my current MS patients.”

(Christchurch physician previously treating several SPMS patients as part of the NZ compassionate use programme)

For

per

sona

l use

onl

y

Bioshares: “Is Innate a binary investment play”

• Let’s be very clear - our SPMS clinical programme is ourmajor ‘asset’. Notwithstanding our other programmesin other indications, outright Phase 2B clinicalfailure would be very hard to survive!

• “Clinical failure” would equate to no real difference between MIS416 treatedpatients and placebo treated patients.

• We believe “clinical failure” to be an unlikely outcome – otherwise allprevious patient / caregiver / doctor reports of sustained and significantbenefits would need to be 100% attributable to nothing more than placeboeffect – sustained over several years. We do not believe that to be the case!

10

For

per

sona

l use

onl

y

Bioshares: “How would the quality of the result impact

a potential deal?”

So what does clinical success look like?

• Firstly, the absence of any currently approved treatment together with theseriousness of the disease means that the efficacy bar is set very low.

• Secondly, the goal to date has been to slow progression, i.e. to slow theworsening of disabilities. A drug that improves a range of disabilities wouldhave to be game changer.

11

• We think a modest result could be say 20% of the treated patients showinga 20% or better treatment effect compared to placebo.

• A good result could be 30% of the patients showing a 25% or better effect.

• A solid result could be 40% of the patients showing 30% or better effect.

• A really good day at the office would be 50% showing 30% or better.

• We believe any of the above would drive a significant “deal”. Obviously thebetter the result - the better the deal. .

For

per

sona

l use

onl

y

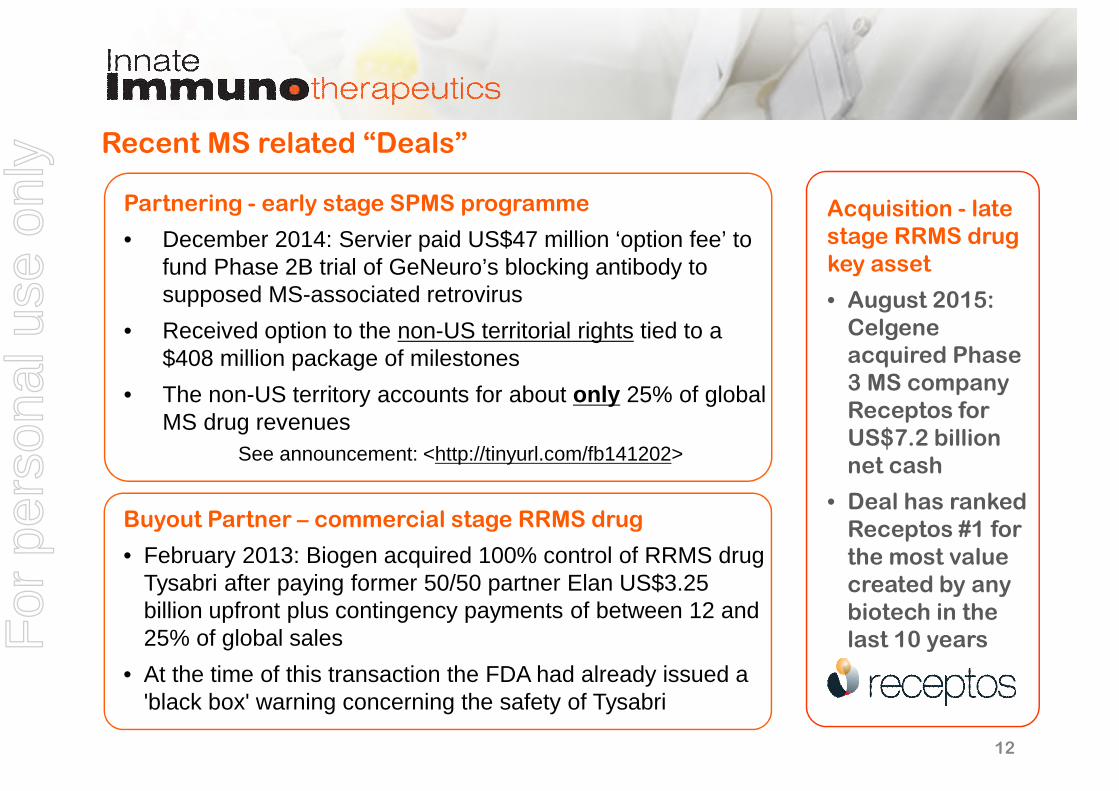

Recent MS related “Deals”

Partnering - early stage SPMS programme

• December 2014: Servier paid US$47 million ‘option fee’ tofund Phase 2B trial of GeNeuro’s blocking antibody tosupposed MS-associated retrovirus

• Received option to the non-US territorial rights tied to a$408 million package of milestones

• The non-US territory accounts for about only 25% of globalMS drug revenues

See announcement: <http://tinyurl.com/fb141202>

Acquisition - latestage RRMS drugkey asset

• August 2015:Celgeneacquired Phase3 MS companyReceptos forUS$7.2 billionnet cash

• Deal has rankedReceptos #1 forthe most valuecreated by anybiotech in thelast 10 years

12

Buyout Partner – commercial stage RRMS drug

• February 2013: Biogen acquired 100% control of RRMS drugTysabri after paying former 50/50 partner Elan US$3.25billion upfront plus contingency payments of between 12 and25% of global sales

• At the time of this transaction the FDA had already issued a'black box' warning concerning the safety of Tysabri

For

per

sona

l use

onl

y

Bioshares: “What is the upside for Innate if successful study

results are achieved?”

• The last patient in the current Phase 2B study will complete treatment in lateApril 2017. We expect to announce top line results about 4 months later.

• At that time, we expect there to be no more than 250 million shares on issue(assuming all current options convert). We carry no debt.

• We have been diligently and successfully building relationships with morethan 10 pharma companies who are keenly interested in the programme.

• We will most likely seek an outright sale of the Companythrough a competitive bidding process at the end of 2017.

13

Modest

RGDO

Solid

Good

• We believe that even a modest trial result will achievea very significant financial outcome for shareholders.

For

per

sona

l use

onl

y

www.innateimmuno.comAustralian Securities Exchange (ASX) ticker - IIL

Simon Wilkinson, CEO

[email protected] or tel +64 21 661 850

Thank you

For

per

sona

l use

onl

y