fmai chapter 2-lecture 1

TRANSCRIPT

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 1/37

Time Value of MoneySupply of Loanable Funds

Demand for Loanable Funds

Equilibrium Interest Rate

Term Structure of Interest RatesForecasting Interest Rates

Chapter 2 Determinants of

Interest rates

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 2/37

Skövde University, Autumn 2008 2

Interest Rate Fundamentals

Nominal interest rates - the

interest rate that are actuallyobserved in financial markets

±directly affect the value (price) of most securities traded in the market

±affect the relationship between spotand forward FX rates

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 3/37

Skövde University, Autumn 2008 3

Time Value of Money and InterestRates

Time value refers to that a dollar received today is worth more than adollar received at some future date

Compound interest

± interest earned on an investment isreinvested

Simple interest

± interest earned on an investment is notreinvested

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 4/37

Skövde University, Autumn 2008 4

Calculation of Simple Interest

Value = Principal + Interest (year 1) + Interest (year 2)

Example:

$1,000 to invest for a period of two years at 12 percent

Value = $1,000 + $1,000(.12) + $1,000(.12)

= $1,000 + $1,000(.12)(2)

= $1,240

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 5/37

Skövde University, Autumn 2008 5

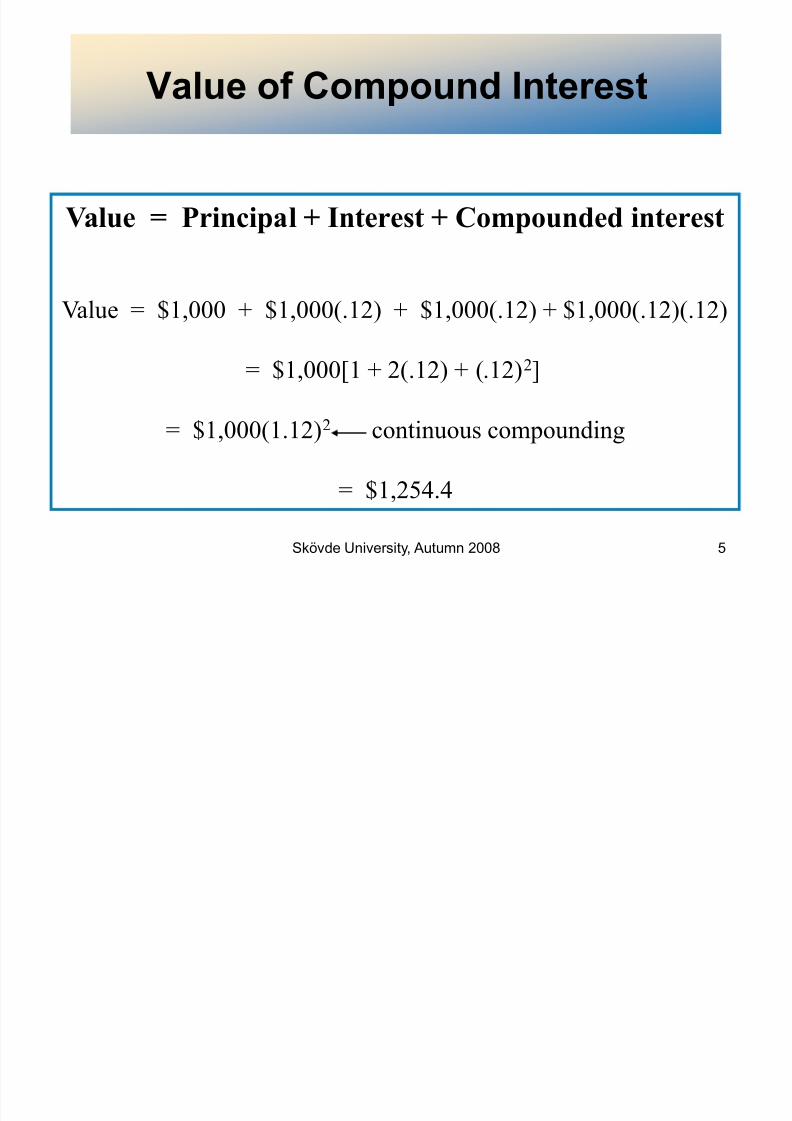

Value of Compound Interest

Value = Principal + Interest + Compounded interest

Value = $1,000 + $1,000(.12) + $1,000(.12) + $1,000(.12)(.12)

= $1,000[1 + 2(.12) + (.12)2]

= $1,000(1.12)2 continuous compounding

= $1,254.4

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 6/37

Skövde University, Autumn 2008 6

Present Value of a Lump Sum Payment

PV function converts future cash flowsinto an equivalent present value bydiscounting future cash flows back tothe present using current marketinterest rate

± lump sum payment

±annuity

PV decreases as interest rates increase:the discount rate is higher for theforeseeable future.

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 7/37

Skövde University, Autumn 2008 7

Calculating Present Value (PV) of aLump Sum payment

PV = FVt (1/(1 + i ))t = FVt (PVIFit )where:

PV = present value

FV = future value (lump sum) received in t years

i = simple annual interest rate earned

t = number of years in the investment horizon

PVIF = present value interest factor of a lump sum

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 8/37

Skövde University, Autumn 2008 8

Calculating Present Value (PV) of a Lump Sumwith multiple interest payment per year

PV = FVn(1/(1 + i/m))nm = FV

n(PVIFi/m,nm)

where:

PV = present value

FV = future value (lump sum) received in n years

i = simple annual interest rate earned

n = number of years in investment horizon

m = number of compounding periods in a year

i/m = periodic rate earned on investments

nm = total number of compounding periods

PVIF = present value interest factor of a lump sum

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 9/37

Skövde University, Autumn 2008 9

Calculating Present Value of aLump Sum

You are offered a security investment thatpays $10,000 at the end of 6 years in exchangefor a fixed payment today.

PV = FVn /(1 + i/m)nm =FV(PVIFi/m,nm)

8% interest PV= $10,000 /(1+0,08)6 = $6,301.70

12% interest PV= $10,000 /(1+0,12)6 = $5,066.31

16% interest PV= $10,000 /(1+0,16)6 = $4,104.42

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 10/37

Skövde University, Autumn 2008 10

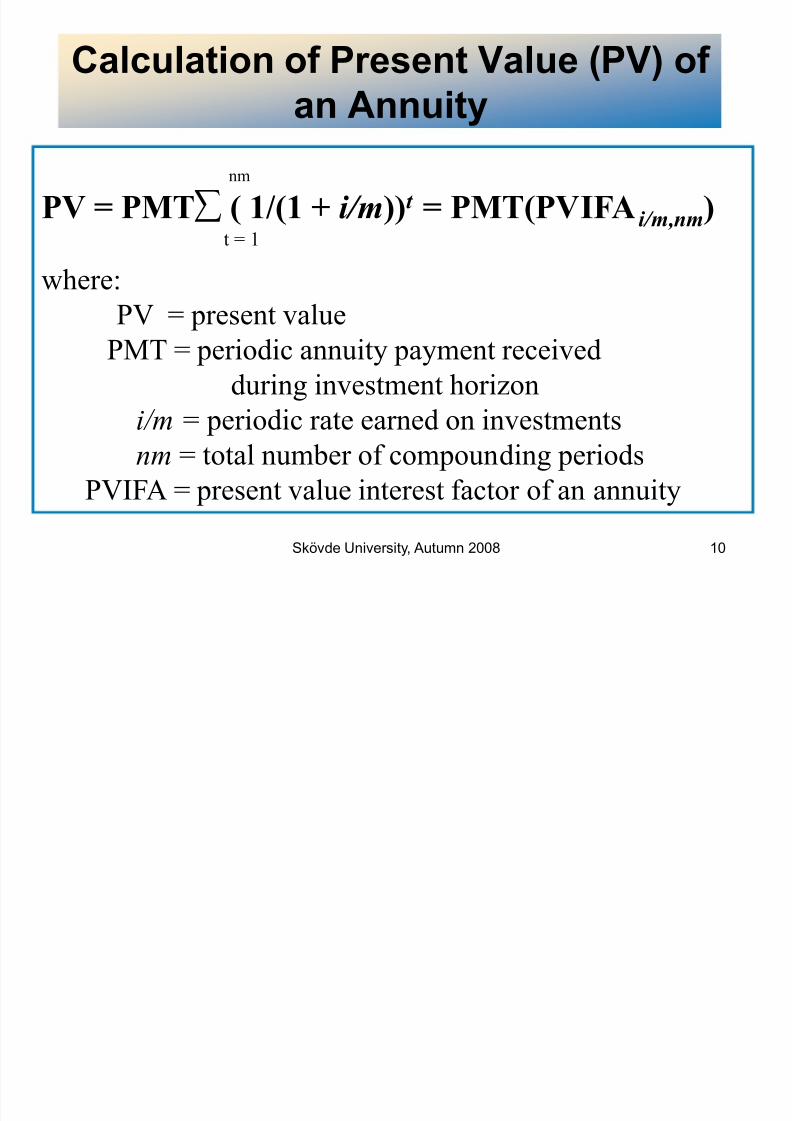

Calculation of Present Value (PV) of an Annuity

nm

PV = PMT§ ( 1/(1 + i/m))t = PMT(PVIFA i/m,nm)t = 1

where:PV = present value

PMT = periodic annuity payment received

during investment horizon

i/m = periodic rate earned on investmentsnm = total number of compounding periods

PVIFA = present value interest factor of an annuity

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 11/37

Skövde University, Autumn 2008 11

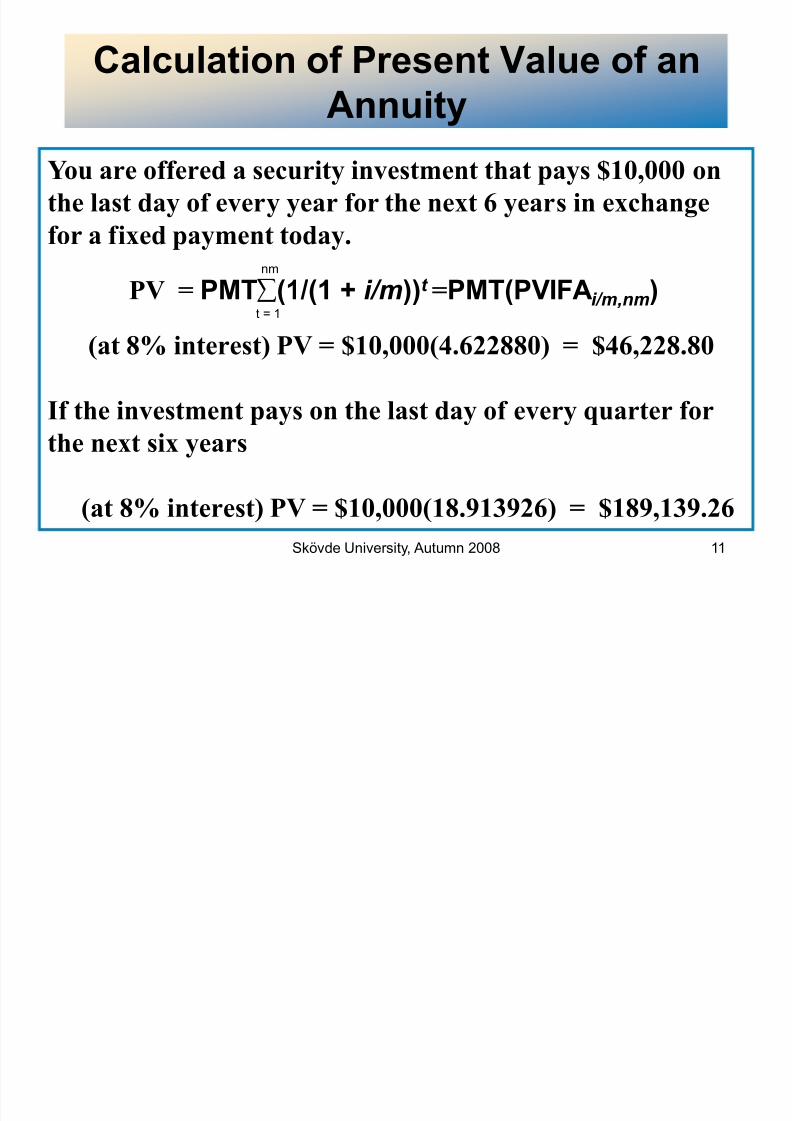

Calculation of Present Value of anAnnuity

You are offered a security investment that pays $10,000 on

the last day of every year for the next 6 years in exchange

for a fixed payment today.nm

PV = PMT§(1 /(1 + i/m))t =PMT(PVIFAi/m,nm)t = 1

(at 8% interest) PV = $10,000(4.622880) = $46,228.80

If the investment pays on the last day of every quarter forthe next six years

(at 8% interest) PV = $10,000(18.913926) = $189,139.26

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 12/37

Skövde University, Autumn 2008 12

Future Values Equations

FV of lump sum equation

FVn = PV(1 + i/m)nm = PV(FVIF i/m, nm)

FV of annuity payment equation

nm-1

FVn = PMT § (1 + i/m)t = PMT(FVIFAi/m, mn)t = 0

Note: the last value paid on Annuity pays no interest.

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 13/37

Skövde University, Autumn 2008 13

Relation between Interest Ratesand Present and Future Values

PresentValue

(PV)

Interest Rate

Future

Value(FV)

Interest Rate

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 14/37

Skövde University, Autumn 2008 14

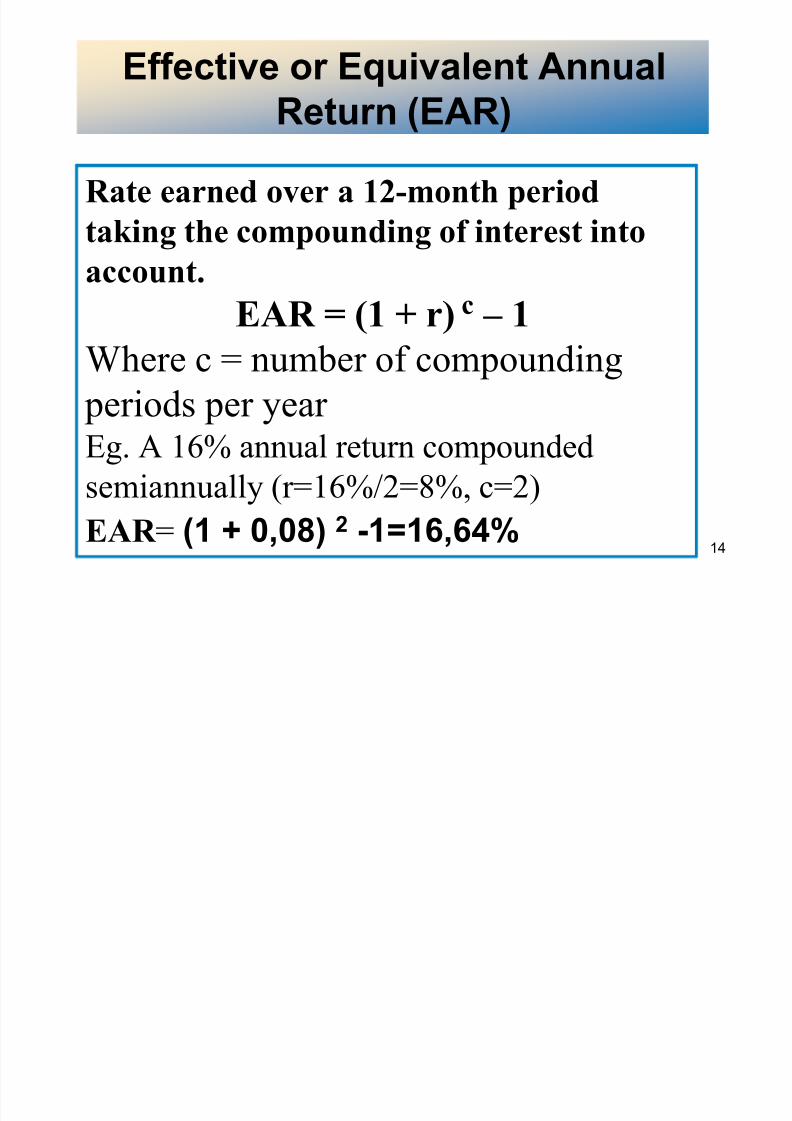

Effective or Equivalent AnnualReturn (EAR)

Rate earned over a 12-month period

taking the compounding of interest into

account.EAR = (1 + r) c ± 1

Where c = number of compounding

periods per year Eg. A 16% annual return compounded

semiannually (r=16%/2=8%, c=2)

EAR = (1 + 0,08) 2 -1=16,64%

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 15/37

Skövde University, Autumn 2008 15

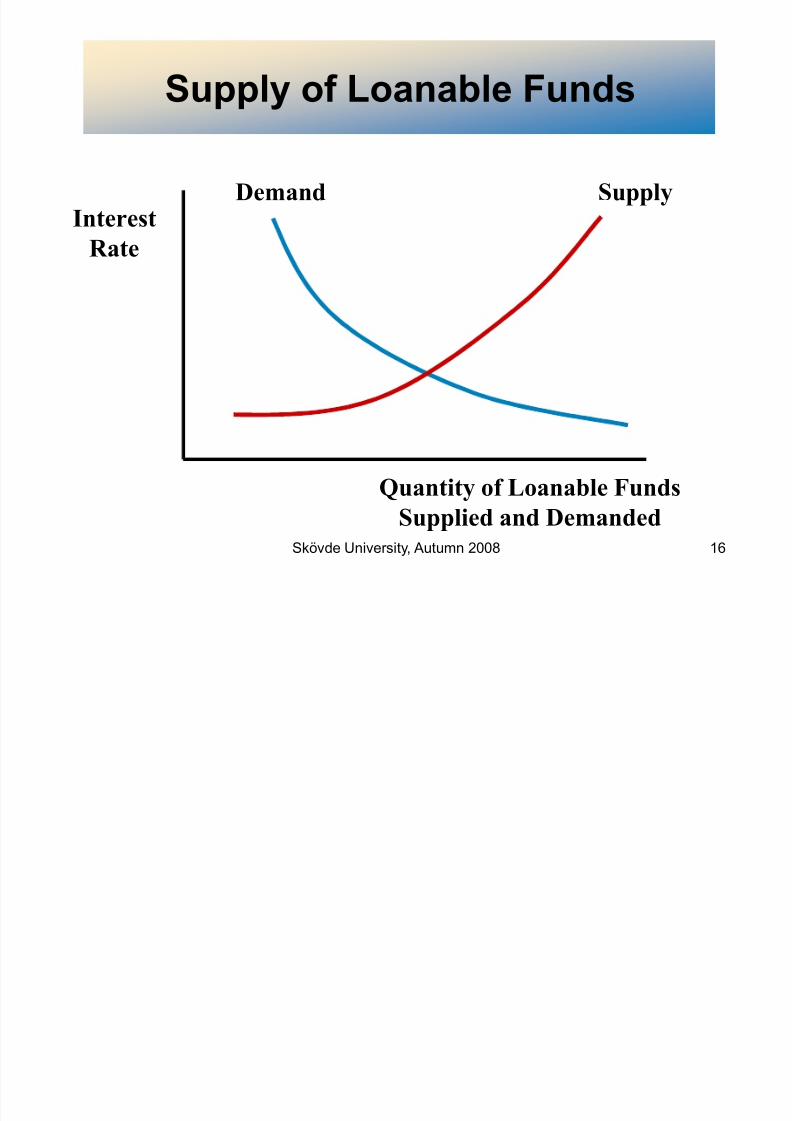

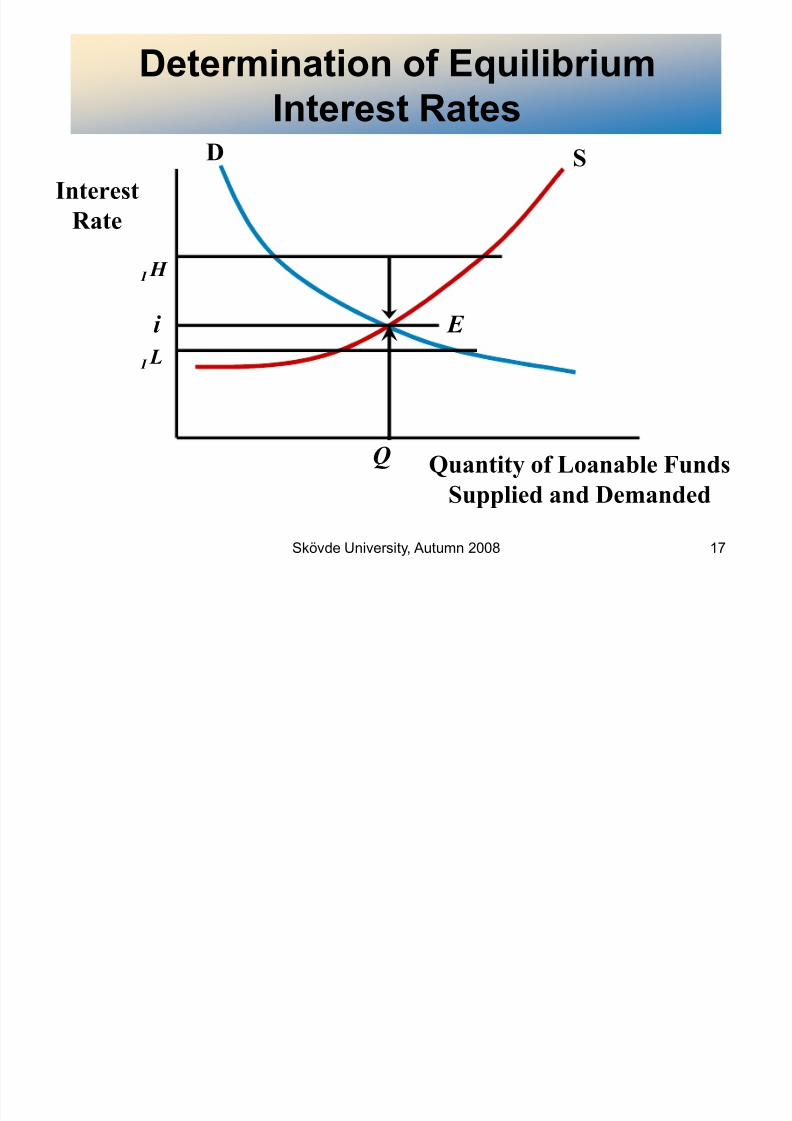

Loanable Funds Theory

A theory of interest rate determinationthat views equilibrium interest rates in

financial markets as a result of thesupply and demand for loanable funds

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 16/37

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 17/37

Skövde University, Autumn 2008 17

Determination of EquilibriumInterest Rates

Interest

Rate

Quantity of Loanable Funds

Supplied and Demanded

D S

I H

i

I L

E

Q

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 18/37

Skövde University, Autumn 2008 18

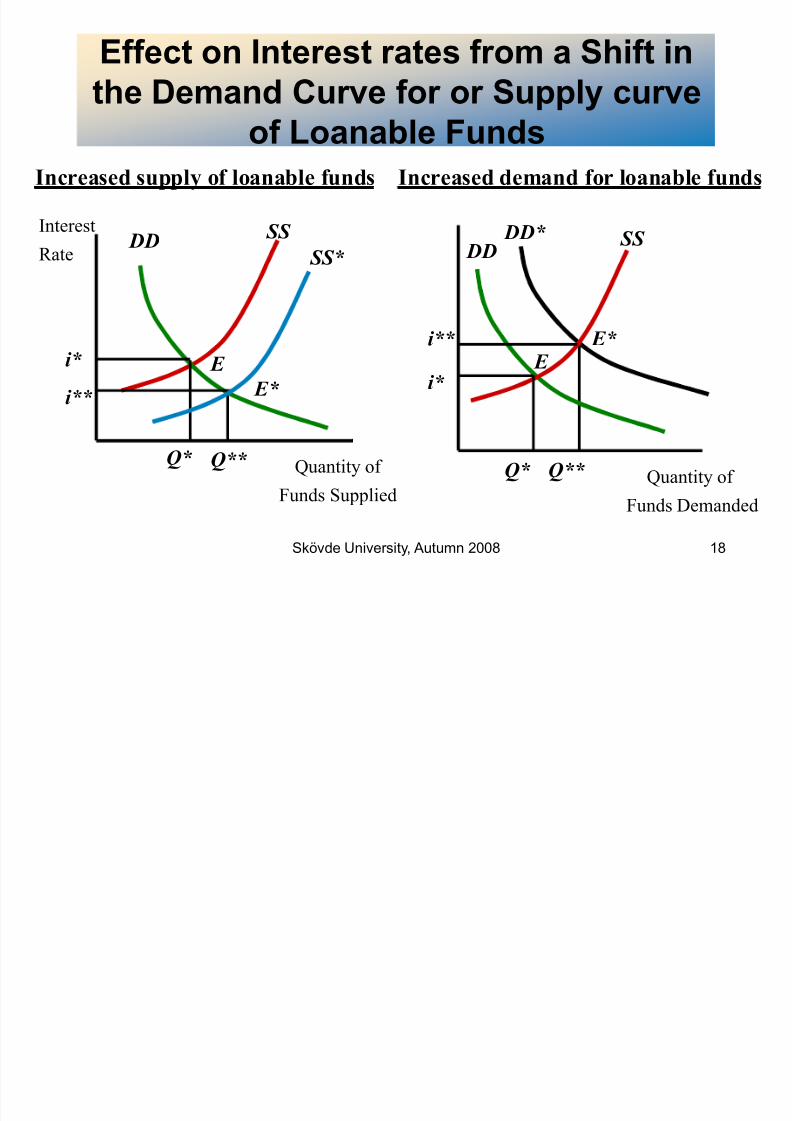

Effect on Interest rates from a Shift inthe Demand Curve for or Supply curve

of Loanable FundsIncreased supply of loanable funds Increased demand for loanable funds

Quantity of

Funds Supplied

Interest

RateDD

SS

SS*

E

E *

Q*

i *

Q**

i **

Quantity of

Funds Demanded

DD

DD* SS

E E *

i *

i **

Q* Q**

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 19/37

Skövde University, Autumn 2008 19

Factors Affecting Nominal InterestRates

Inflation

Real Interest Rate Default Risk

Liquidity Risk

Special Provisions Term to Maturity

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 20/37

Skövde University, Autumn 2008 20

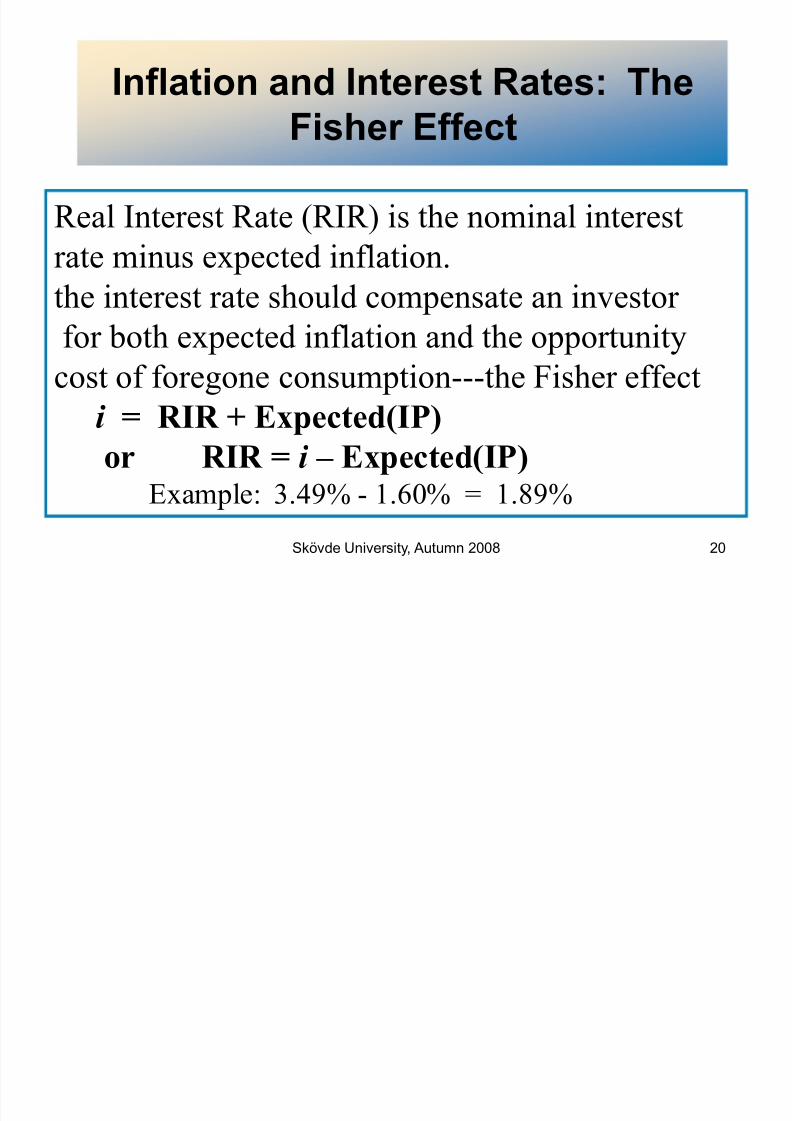

Inflation and Interest Rates: The

Fisher Effect

Real Interest Rate (RIR) is the nominal interest

rate minus expected inflation.

the interest rate should compensate an investor

for both expected inflation and the opportunity

cost of foregone consumption---the Fisher effect

i = RIR + Expected(IP)or RIR = i ± Expected(IP)

Example: 3.49% - 1.60% = 1.89%

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 21/37

Skövde University, Autumn 2008 21

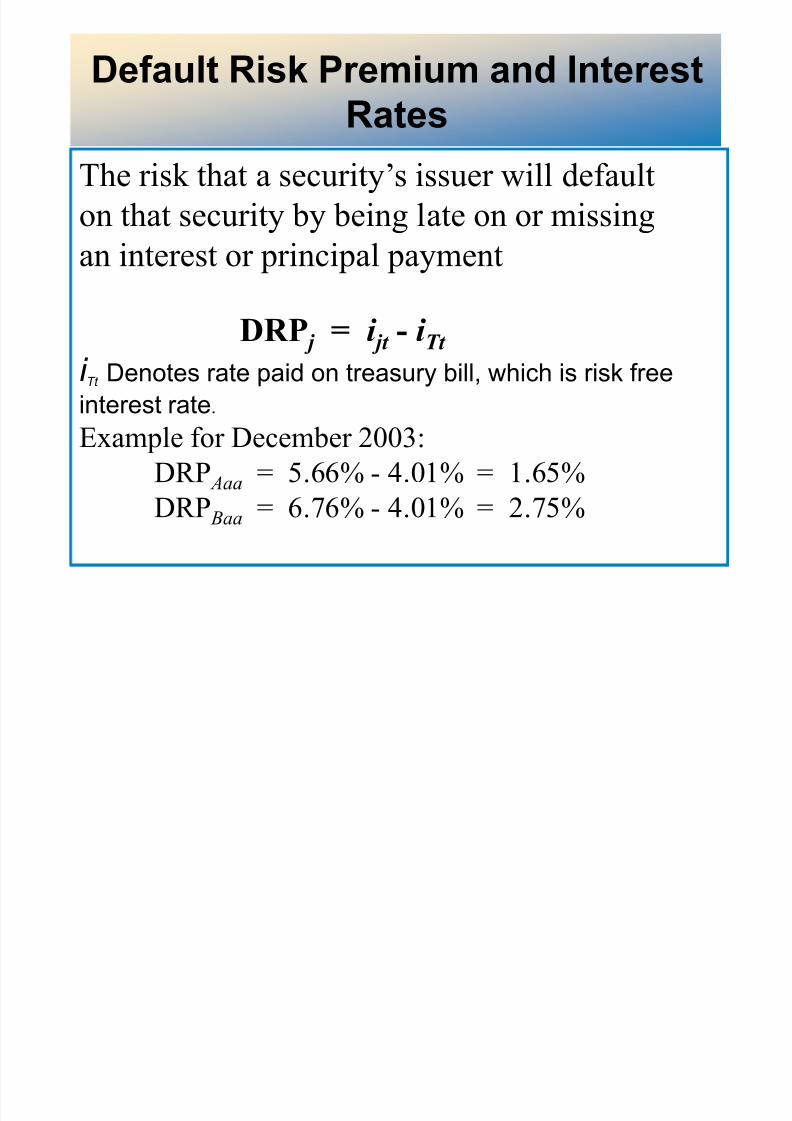

Default Risk Premium and InterestRates

The risk that a security¶s issuer will default

on that security by being late on or missing

an interest or principal payment

DRP j = i j t - i Tt i Tt Denotes rate paid on treasury bill, which is risk free

interest rate.

Example for December 2003:

DRP Aaa = 5.66% - 4.01% = 1.65%

DRP Baa = 6.76% - 4.01% = 2.75%

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 22/37

Skövde University, Autumn 2008 22

Term to Maturity and InterestRates: Yield Curve

Yield to

Maturity

Time to Maturity

(a)

(b)

(c)

(a) Upward sloping

(b) Inverted or downward

sloping

(c) Flat

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 23/37

Skövde University, Autumn 2008 23

Term Structure of Interest Rates

Unbiased Expectations Theory

Liquidity Premium Theory Market Segmentation Theory

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 24/37

Skövde University, Autumn 2008 24

Expectations Theory

Key Assumption: Bonds of different maturities areperfect substitutes

Implication: R e on bonds of different maturities

are equal

Investment strategies for two-period horizon

1. Buy $1 of one-year bond and when matures buy another one-year bond

2. Buy $1 of two-year bond and hold it

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 25/37

Skövde University, Autumn 2008 25

Expectations Theory

Investment strategies for two-period

horizon

1. Buy $1 of one-year bond and whenmatures buy another one-year bond

2. Buy $1 of two-year bond and hold it

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 26/37

Skövde University, Autumn 2008 26

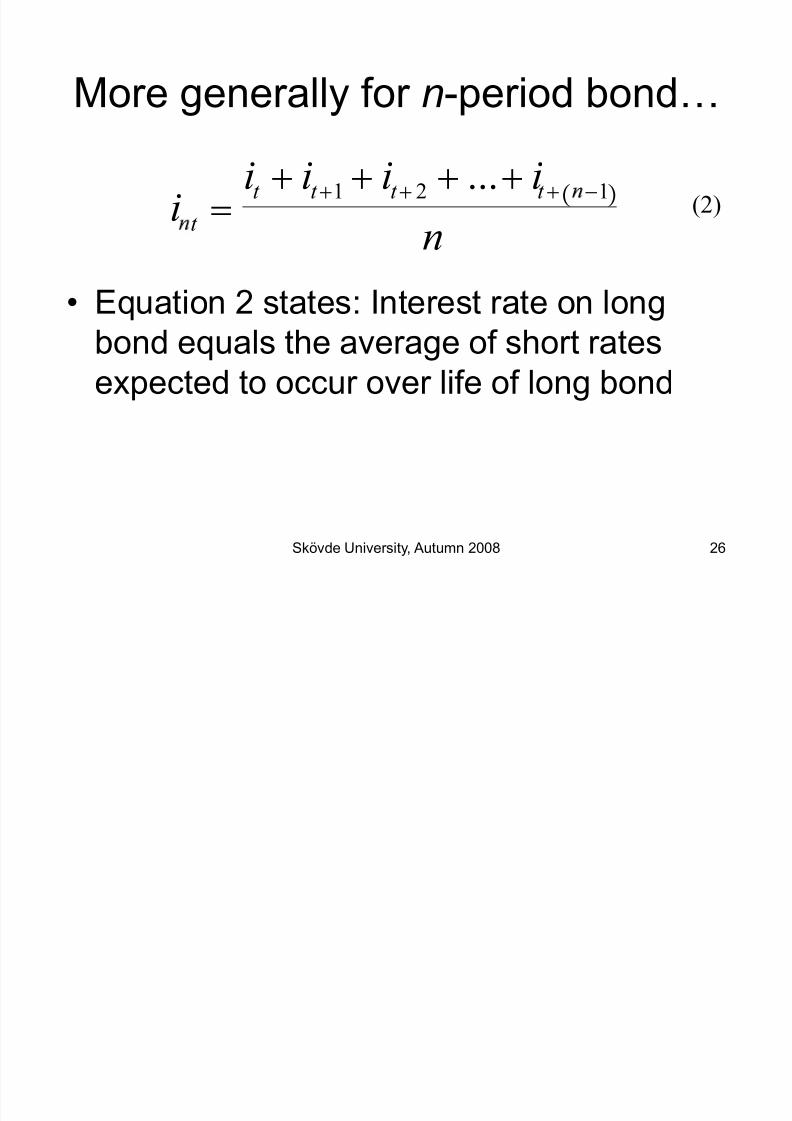

it

!it

it 1 i

t 2 ... it 1

n

More generally for n-period bond«

Equation 2 states: Interest rate on longbond equals the average of short ratesexpected to occur over life of long bond

(2)

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 27/37

Skövde University, Autumn 2008 27

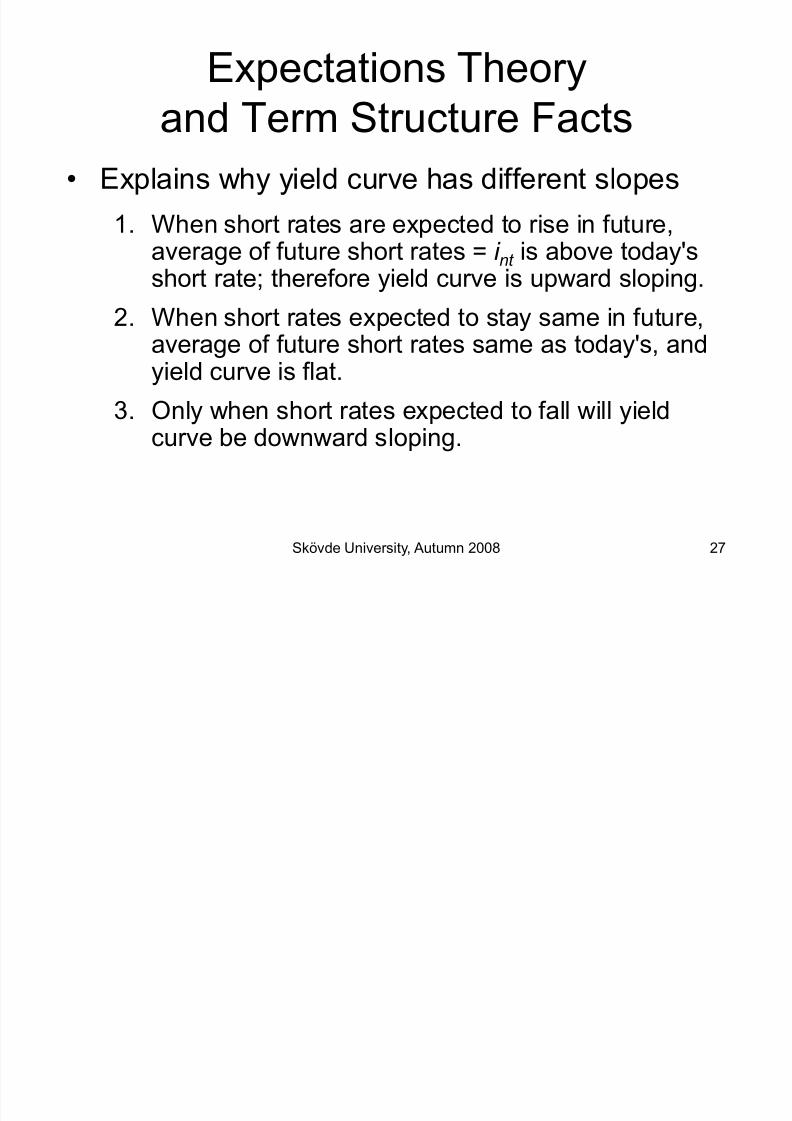

Expectations Theoryand Term Structure Facts

Explains why yield curve has different slopes

1. When short rates are expected to rise in future,average of future short rates = i

nt is above today's

short rate; therefore yield curve is upward sloping.2. When short rates expected to stay same in future,

average of future short rates same as today's, andyield curve is flat.

3. Only when short rates expected to fall will yieldcurve be downward sloping.

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 28/37

Skövde University, Autumn 2008 28

Market Segmentation Theory

Key Assumption: Bonds of different maturities arenot substitutes at all

Implication: Markets are completely

segmented; interest rate at each maturity determinedseparately

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 29/37

Skövde University, Autumn 2008 29

Market Segmentation Theory

Explains fact 3²that yield curve is usuallyupward sloping ± People typically prefer short holding periods and thus have

higher demand for short-term bonds, which have higher prices and lower interest rates than long bonds

Does not explain fact 1 or fact 2 because itsassumes long-term and short-term rates aredetermined independently

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 30/37

Skövde University, Autumn 2008 30

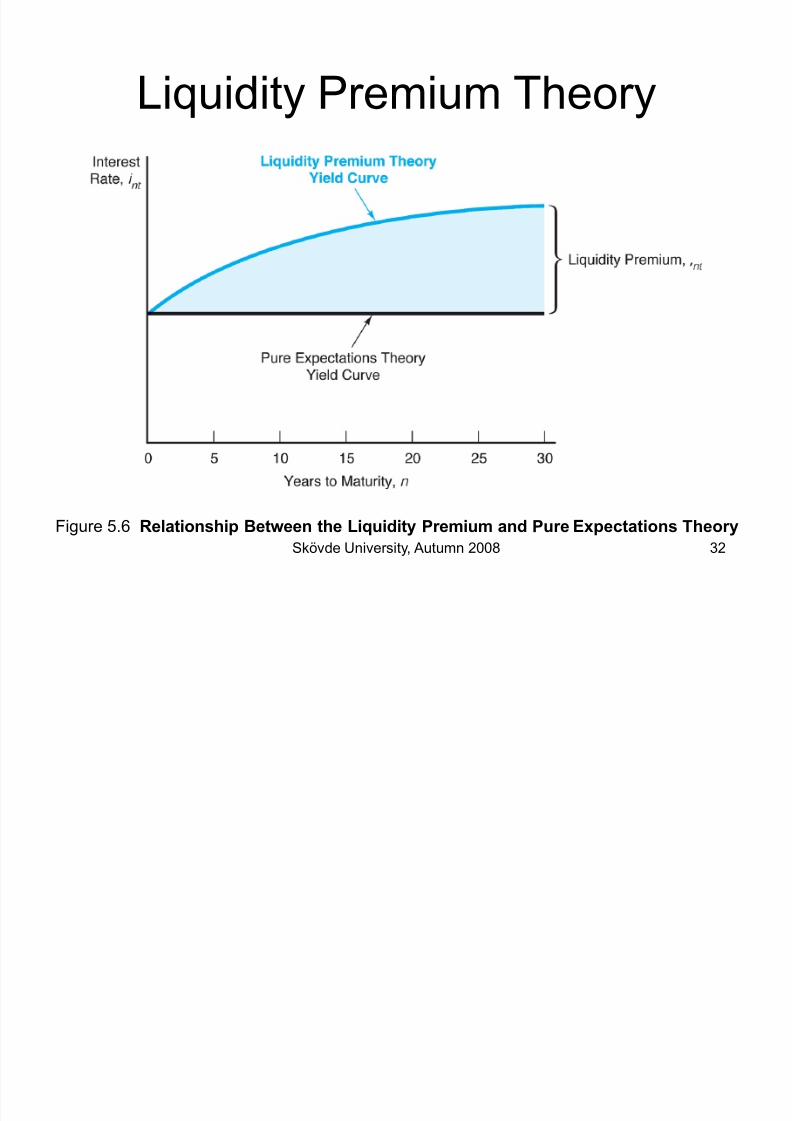

Liquidity Premium Theory

Key Assumption: Bonds of different maturitiesare substitutes, but are notperfect substitutes

Implication: Modifies ExpectationsTheory with features of MarketSegmentation Theory

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 31/37

Skövde University, Autumn 2008 31

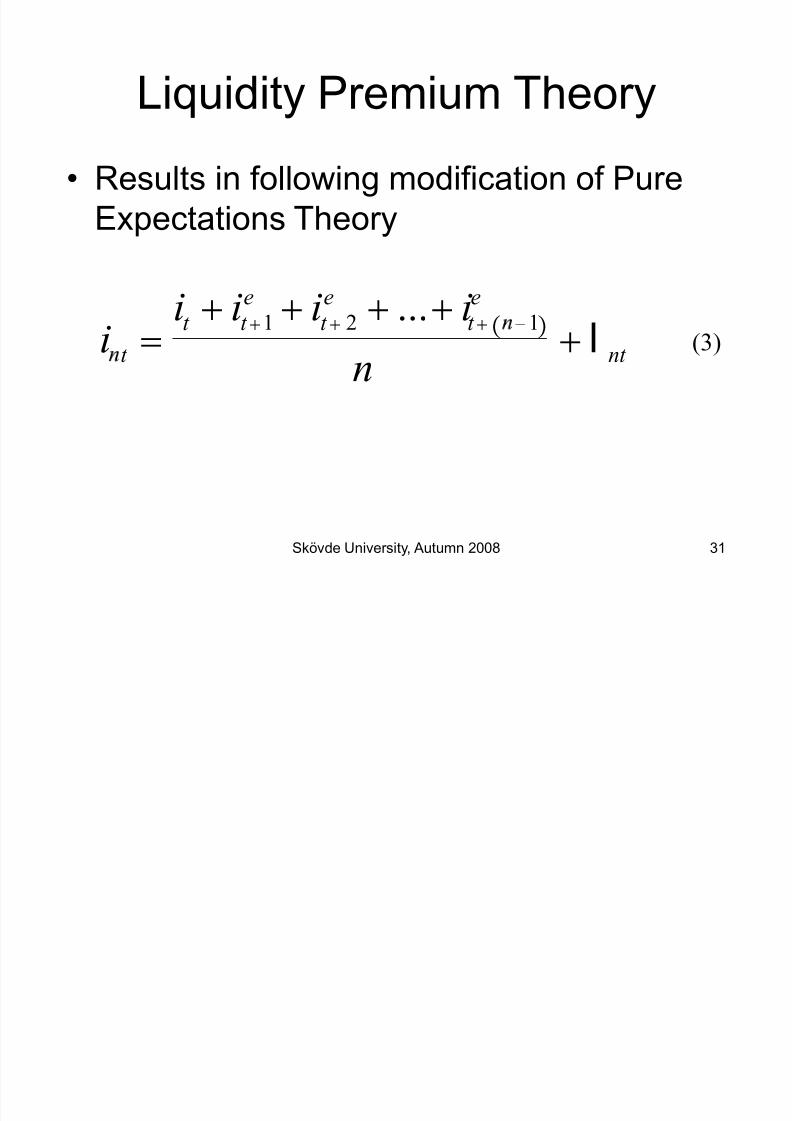

i

t !

it

it 1

e

it 2

e

... it 1

e

n

lnt

Liquidity Premium Theory

Results in following modification of PureExpectations Theory

(3)

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 32/37

Skövde University, Autumn 2008 32

Figure 5.6 Relationship Between the Liquidity Premium and Pure Expectations Theory

Liquidity Premium Theory

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 33/37

Skövde University, Autumn 2008 33

Forecasting Interest Rates

Forward rate is an expected or ³implied´ rate

on a security that is to be originated at some

point in the future using the unbiased

expectations theory _ _

1R 2 = [(1 + 1R 1)(1 + (2f 1))]1/2 - 1

where 2f 1 = expected one-year rate for year 2, or the implied

_ _ forward one-year rate for next year 2f 1=[(1+ 1R2 )2 /(1+1R1)]-1

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 34/37

Skövde University, Autumn 2008 34

Present Value of Cash Flows:Example

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 35/37

Skövde University, Autumn 2008 35

U.S. Real and Nominal InterestRates

Figure 3-1 Real and Nominal Interest Rates (Three-Month Treasury Bill), 1953±2004Sample of current rates and indexeshttp://www.martincapital.com/charts.htm

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 36/37

Skövde University, Autumn 2008 36

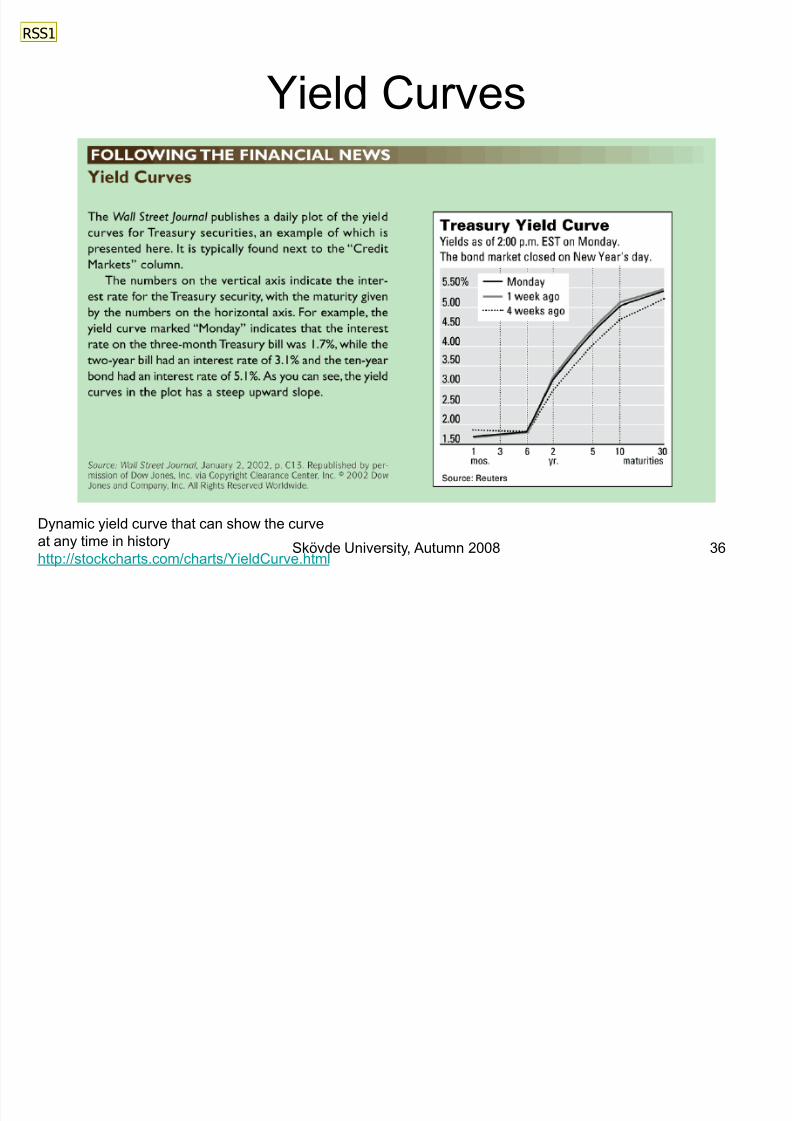

Yield Curves

Dynamic yield curve that can show the curveat any time in history

http://stockcharts.com/charts/YieldCurve.html

RSS1

8/8/2019 FMAI Chapter 2-Lecture 1

http://slidepdf.com/reader/full/fmai-chapter-2-lecture-1 37/37

Slide 36

RSS1 Change title to: Reading the Wall St. JournalRick Swasey, 12/12/2004