financial times series - math.chalmers.se

TRANSCRIPT

Financial Times Series

Lecture 7

Regime Switching

• We sometimes talk about bull and bear markets

• By bull market we mean a market where prices are increasing and where volatility is relatively low

• By bear market we mean a market where prices are decreasing and where volatility is relatively high

Regime Switching

• So if we would like to model log-returns under the assumption that the market switches between the bull and bear states we let

𝑟𝑡 = 𝜇𝑏𝑢𝑙𝑙 + 𝜎𝑏𝑢𝑙𝑙𝜀𝑡, 𝑠𝑡= 𝑏𝑢𝑙𝑙𝜇𝑏𝑒𝑎𝑟 + 𝜎𝑏𝑒𝑎𝑟𝜀𝑡, 𝑠𝑡= 𝑏𝑒𝑎𝑟

• Here 𝑠𝑡 denotes the state of the market at time 𝑡 and 𝜀𝑡 is i.i.d 𝑁 0,1

Regime Switching

• Typically we cannot tell what state the market is in but using some filtering techniques and assumptions on the switching mechanism we can estimate switching probabilities, drifts and volatilities

• We may assume that the switching between the states is Markovian, i.e. the probability of switching from one state to another depends only on which state the market is in a the time point of switching and not on in which states the market has been in or returns at previous time points

𝑃 𝑠𝑡|𝑠𝑡−1 = 𝑃 𝑠𝑡|𝑠𝑡−1, 𝑠𝑡−2, … , 𝑟𝑡−1, 𝑟𝑡−2, …

Regime Switching

• If we denote the market states 0 and 1 we let

𝑝00 = 𝑃 𝑠𝑡 = 0|𝑠𝑡−1 = 0 𝑝01 = 𝑃 𝑠𝑡 = 1|𝑠𝑡−1 = 0 𝑝10 = 𝑃 𝑠𝑡 = 0|𝑠𝑡−1 = 1 𝑝11 = 𝑃 𝑠𝑡 = 1|𝑠𝑡−1 = 1

• Clearly 𝑝00 = 1 − 𝑝01 and 𝑝11 = 1 − 𝑝10

Estimation

• So given a series of observations 𝑟1, … , 𝑟𝑇 we want to estimate the parameters 𝜃 = 𝑝00, 𝑝11, 𝜇0, 𝜇1, 𝜎0, 𝜎1

• Since we cannot tell which state we are in at a given time point it is not obvious how the estimations can be done but we may formally write the likelihood function

𝐿 𝜃 = 𝑓 𝑟1|𝜃 𝑓 𝑟2|𝜃, 𝑟1 ⋯𝑓 𝑟𝑇|𝜃, 𝑟1, … , 𝑟𝑇−1

where 𝑓 is the density of a 𝑁 𝜇𝑠, 𝜎𝑠2 random variable

Estimation

• So the contribution of 𝑟𝑡 to the log-likelihood is

log𝑓 𝑟𝑡|𝜃, 𝑟1, … , 𝑟𝑡−1

• Using conditional probabilities and the Markov property, we can write (exercise)

𝑓 𝑠𝑡 , 𝑠𝑡−1, 𝑟𝑡|𝜃, 𝑟1, … , 𝑟𝑡−1= 𝑓 𝑠𝑡−1|𝜃, 𝑟1, … , 𝑟𝑡−1 𝑓 𝑠𝑡|𝑠𝑡−1, 𝜃 𝑓 𝑟𝑡|𝑠𝑡 , 𝜃

Estimation

• Above 𝑓 𝑠𝑡|𝑠𝑡−1, 𝜃 is the switching probability and

𝑓 𝑟𝑡|𝑠𝑡, 𝜃 =1

2𝜋𝜎𝑠𝑡𝑒𝑥𝑝 −

1

2

𝑟𝑡−𝜇𝑠𝑡𝜎𝑠𝑡

2

• The function 𝑓 𝑠𝑡−1|𝜃, 𝑟1, … , 𝑟𝑡−1 is given by

𝑓 𝑠𝑡−1,𝑠𝑡−2=0,𝑟𝑡−1|𝜃,𝑟1,…,𝑟𝑡−2 +𝑓 𝑠𝑡−1,𝑠𝑡−2=1,𝑟𝑡−1|𝜃,𝑟1,…,𝑟𝑡−2

𝑓 𝑟𝑡−1|𝜃,𝑟1,…,𝑟𝑡−2

Estimation

• So we get

𝑓 𝑟𝑡|𝜃, 𝑟1, … , 𝑟𝑡−1 = 𝑓 𝑠𝑡 = 𝑖, 𝑠𝑡−1 = 𝑗, 𝑟𝑡|𝜃, 𝑟1, … , 𝑟𝑡−1

2

𝑗=1

2

𝑖=1

• To start the recursion we may let

𝑓 𝑠1 = 0, 𝑟1|𝜃 =1

2

1

2𝜋𝜎0𝑒𝑥𝑝 −

1

2

𝑟1 − 𝜇0𝜎0

2

𝑓 𝑠1 = 1, 𝑟1|𝜃 =1

2

1

2𝜋𝜎1𝑒𝑥𝑝 −

1

2

𝑟1 − 𝜇1𝜎1

2

Estimation

• This gives

𝑓 𝑟1|𝜃 = 𝑓 𝑠1 = 0, 𝑟1|𝜃 + 𝑓 𝑠1 = 1, 𝑟1|𝜃

• and

𝑓 𝑠1 = 0|𝜃, 𝑟1 =𝑓 𝑠1 = 0, 𝑟1|𝜃

𝑓 𝑟1|𝜃

𝑓 𝑠1 = 1|𝜃, 𝑟1 =𝑓 𝑠1 = 1, 𝑟1|𝜃

𝑓 𝑟1|𝜃

Estimation

• Next we get

𝑓 𝑟2|𝜃, 𝑟1 = 𝑓 𝑠1 = 𝑖, 𝑠2 = 𝑗, 𝑟2|𝜃, 𝑟1

2

𝑗=1

2

𝑖=1

• where

𝑓 𝑠1 = 𝑖, 𝑠2 = 𝑗, 𝑟2|𝜃, 𝑟1

= 𝑓 𝑠1 = 𝑖|𝜃, 𝑟1 𝑝𝑗𝑖1

2𝜋𝜎𝑗𝑒𝑥𝑝 −

1

2

𝑟2 − 𝜇𝑗

𝜎𝑗

2

• And so forth…

Estimation

• So, the maximization of the likelihood-function cannot be done manually but using standard routines like fminsearch or fmincon in matlab we can find our parameter estimates

• There is a matlab package by Marcelo Perlin called MS_Regress available online (for free) that does the parameter estimation and then some…

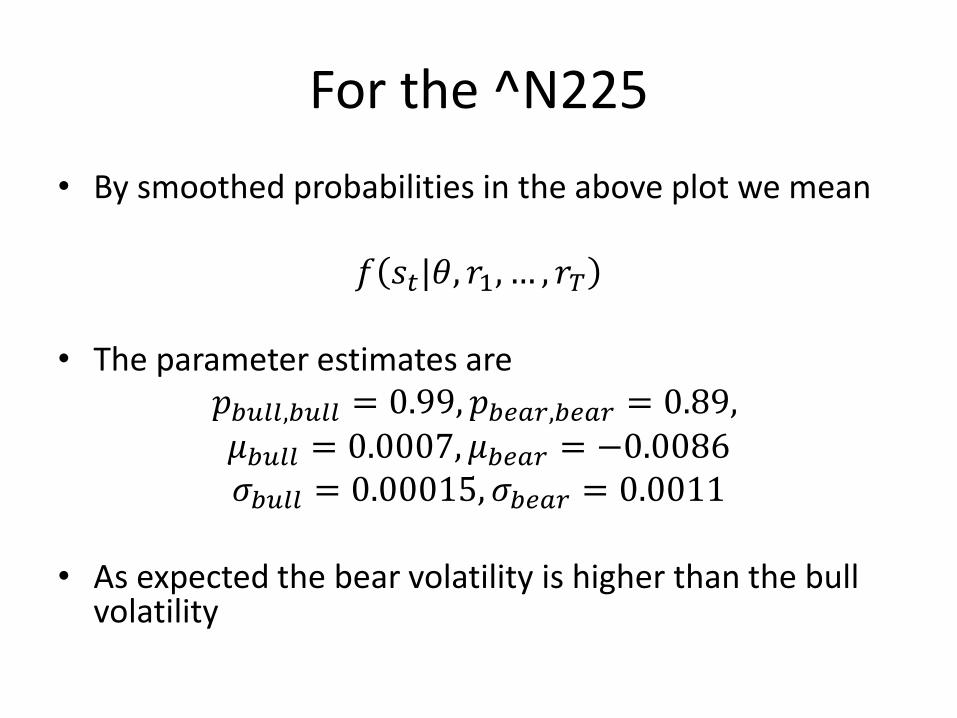

For the ^N225

For the ^N225

• By smoothed probabilities in the above plot we mean

𝑓 𝑠𝑡|𝜃, 𝑟1, … , 𝑟𝑇

• The parameter estimates are 𝑝𝑏𝑢𝑙𝑙,𝑏𝑢𝑙𝑙 = 0.99, 𝑝𝑏𝑒𝑎𝑟,𝑏𝑒𝑎𝑟 = 0.89, 𝜇𝑏𝑢𝑙𝑙 = 0.0007, 𝜇𝑏𝑒𝑎𝑟 = −0.0086 𝜎𝑏𝑢𝑙𝑙 = 0.00015, 𝜎𝑏𝑒𝑎𝑟 = 0.0011

• As expected the bear volatility is higher than the bull

volatility

Non-parametric models

• What if we do not make any distribution assumptions?

• Assume that 𝑟𝑡 and 𝑥𝑡 are two time series for which we want to explore their relationship

• Maybe it is possible to fit a model

𝑟𝑡 = 𝑚 𝑥𝑡 + 𝑎𝑡 where 𝑚 is some smooth function to be estimated from the data

Non-parametric models

• If we had independent observerations 𝑟1, … , 𝑟𝑇 for a fixed 𝑥𝑡 = 𝑥 the we could write

𝑟𝑡𝑇𝑡=1

𝑇= 𝑚 𝑥 +

𝑎𝑡𝑇𝑡=1

𝑇

• For a sufficiently large 𝑇 the mean of the noise (LLN)

will be close to zero so in this case

𝑚 𝑥 = 𝑟𝑡𝑇𝑡=1

𝑇

Non-parametric models

• In financial applications we will typically not have data as above. Rather we will have pairs of observations

𝑟1, 𝑥1 , … , 𝑟𝑇 , 𝑥𝑇

• But if the function 𝑚 is sufficiently smooth then a

value of 𝑟𝑡 for which 𝑥𝑡 ≈ 𝑥 will still give a good approximation of 𝑚 𝑥

• For a value of 𝑟𝑡 for which 𝑥𝑡 is not close to 𝑥 will give a less accurate approximation of 𝑚 𝑥

Non-parametric models

• So instead of a simple average, we use a weighted average

𝑚 𝑥 =1

𝑇 𝑤𝑡(𝑥)𝑟𝑡

𝑇

𝑡=1

where the weights 𝑤𝑡(𝑥) are large for those 𝑟𝑡 with 𝑥𝑡 close to 𝑥 and weights are small for 𝑟𝑡 with 𝑥𝑡 not close to 𝑥

Non-parametric models • Above we assume that 𝑤𝑡 𝑥 = 𝑇𝑇

𝑡=1

• One may also treat 1

𝑇 as part of the weights and work

under the assumption 𝑤𝑡 𝑥 = 1𝑇𝑡=1

• A construction like the one at hand where we will let the weights depend on a choice of measure for the distance between 𝑥𝑡 and 𝑥 and the size of the weights depends on the distance may be referred to as a local weighted average

Kernel regression

• One way of finding appropriate weights is to use kernels 𝐾 𝑥 which are typically probability density functions

𝐾(𝑥) ≥ 0 and 𝐾 𝑥 𝑑𝑥 = 1∞

−∞

• For flexibility we will allow scaling of the kernel using a ”bandwidth” ℎ

𝐾ℎ 𝑥 =1

ℎ𝐾 𝑥 ℎ , 𝐾ℎ 𝑥 𝑑𝑥 = 1

∞

−∞

• The weights may be defined as

𝑤𝑡 𝑥 =𝐾ℎ 𝑥 − 𝑥𝑡

𝐾ℎ 𝑥 − 𝑥𝑡𝑇𝑡=1

Nadaraya-Watson

• The N-W kernel estimator (N-W 1964) is given by

𝑚 𝑥 = 𝑤𝑡(𝑥)𝑟𝑡

𝑇

𝑡=1

= 𝐾ℎ 𝑥 − 𝑥𝑡 𝑟𝑡𝑇𝑡=1

𝐾ℎ 𝑥 − 𝑥𝑡𝑇𝑡=1

• The choice of kernel is often (Gaussian)

𝐾ℎ 𝑥 =1

ℎ 2𝜋𝑒𝑥𝑝 −

𝑥2

2ℎ2

or (Epanechnikov)

𝐾ℎ 𝑥 =3

4ℎ1 −

𝑥2

ℎ2𝟏 𝑥 ≤ ℎ

What does the bandwidth do?

• If we use the Epanechnikov kernel we get

𝑚 𝑥 = 𝐾ℎ 𝑥 − 𝑥𝑡 𝑟𝑡𝑇𝑡=1

𝐾ℎ 𝑥 − 𝑥𝑡𝑇𝑡=1

= 1 −

𝑥 − 𝑥𝑡2

ℎ2𝟏 𝑥 − 𝑥𝑡 ≤ ℎ 𝑟𝑡

𝑇𝑡=1

1 −𝑥 − 𝑥𝑡

2

ℎ2𝟏 𝑥 − 𝑥𝑡 ≤ ℎ𝑇

𝑡=1

• If ℎ → ∞

𝑚 𝑥 →1

𝑇 𝑟𝑡

𝑇

𝑡=1

and if ℎ → 0

𝑚 𝑥 → 𝑟𝑡 where 𝑟𝑡 is the observation for which 𝑥 − 𝑥𝑡 is smallest within the sample

Bandwidth Selection

• Fan and Yao (2003) suggest

ℎ = 1.06𝑠𝑇−1/5

for the Gaussian Kernel and

ℎ = 2.34𝑠𝑇−1/5

for the Epanechnikov kernel where 𝑠 is the sample standard deviation of 𝑥𝑡 which is assumed stationary

Cross Validation

• Let

𝑚 ℎ,𝑗 𝑥𝑗 =1

𝑇 − 1 𝑤𝑡 𝑥𝑗 𝑦𝑡𝑡≠𝑗

which is an estimate of 𝑦𝑗 where the weights sum to 𝑇 − 1. • Also let

𝐶𝑉 ℎ =1

𝑇 𝑦𝑗 −𝑚 ℎ,𝑗 𝑥𝑗

2𝑊 𝑥𝑗

𝑇

𝑗=1

where 𝑊 ∙ is anonnegative weight function satisfying 𝑊 𝑥𝑗 = 𝑇𝑇𝑗=1

Cross Validation

• The function 𝐶𝑉 ℎ is called the cross-validation function since it validates the ability of the smoother 𝑚 to predict 𝑦𝑡

• The weight function 𝑊 may be chosen to downweight certain observations if necessary

but 𝑊 𝑥𝑗 = 1 is often sufficient

Cross Validation

• It is an exercise to show that

𝐶𝑉 ℎ =1

𝑇 𝑦𝑗 −𝑚 ℎ,𝑗 𝑥𝑗

2𝑇

𝑗=1

=1

𝑇 𝑦𝑗 −𝑚 𝑥𝑗

2/ 1 −

𝐾ℎ 0

𝐾ℎ 𝑥𝑗 − 𝑥𝑖𝑇𝑖=1

2𝑇

𝑗=1

N-W Volatility Estimation

• Assume that 𝑟𝑡 is our log-return series that has been centered at zero so that

𝐸 𝑟2𝑡 = 𝜎2𝑡

• We also assume that 𝑟2𝑡 = 𝜎2𝑡 + 𝜀𝑡 where 𝜀𝑡 is WN

N-W Volatility Estimation

• We may then use the N–W kernel estimator

𝜎 2𝑡 = 𝐾ℎ 𝑡 − 𝑖 𝑟2𝑖𝑡−1𝑖=1

𝐾ℎ 𝑡 − 𝑖𝑡−1𝑖=1

• Below we use Gaussian kernels for OMXS30 data

OMXS30 returns (100104-130412)

OMXS30 N-W volatility estimates

• CV gives ℎ = 23.26 and volatility estimates:

OMXS30 N-W volatility devolatized returns

The Ljung-Box null hypothesis of no autocorrelations cannot be rejected at 5% level p=0.4433

Autocorrelation for devolatized returns

Another application

• Remember the ARIMA example for the Swedish GDP

• What if we try to use N-W to model log GDP 𝑝𝑡 as

𝑝𝑡 = 𝑚 𝑝𝑡−1 + 𝑎𝑡

where 𝑎𝑡 is WN

Log BNP

• Using CV we find ℎ = 0.0367 to be the optimal threshold for the Gaussian kernel and

Residuals

• The seasonality seen using the ARIMA is still left, but we know how to deal with that