federal healthcare reform – what’s next? willis human capital practice legislative and...

TRANSCRIPT

Federal Healthcare Reform – What’s Next?Willis Human Capital PracticeLegislative and Regulatory Update

Jay M. Kirschbaum, JD, LLM, FLMIPractice LeaderNational Legal & Research Group

This material and any accompanying remarks are provided for informational purposes only and nothing contained in either should be taken as a legal opinion or as legal advice Copyright 2010 All rights reserved

2

When you come to a fork in the road

take it.

- Yogi Berra

3

Healthcare Reform Impact on employers, employees, insurers Immediate issues for employers and employees

New Notices Grandfathered Status - What is it and how meaningful is it? Preventive Services Mandate New Appeals Process Annual and Lifetime Dollar Limit Prohibition and Waiver Process Adult Child Guidance “Insurance Reforms” OTC Guidance

Q&A Future issues for employers and employees if time permits

Highlights included on slides

4

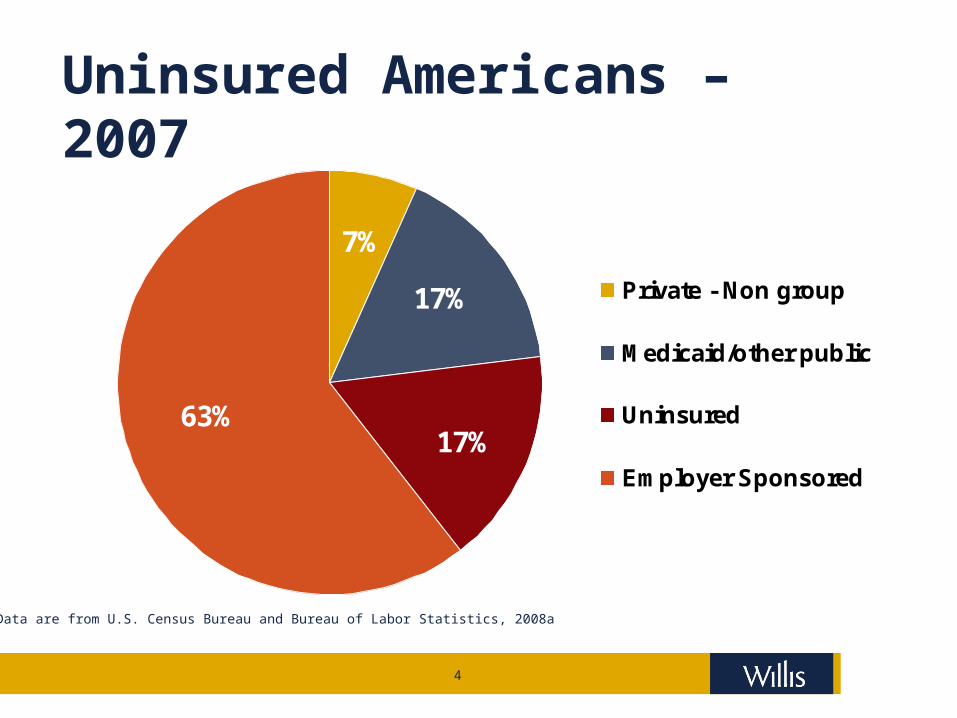

7%

17%

17%63%

Private - Non group

Medicaid/other public

Uninsured

Employer Sponsored

Uninsured Americans – 2007

Data are from U.S. Census Bureau and Bureau of Labor Statistics, 2008a

5

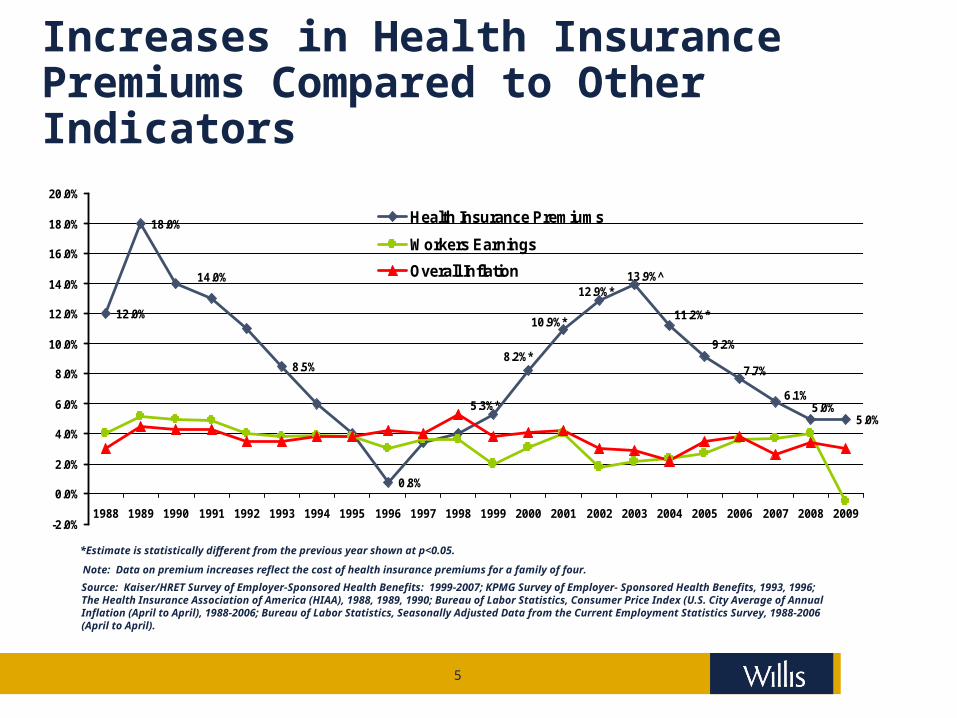

Increases in Health Insurance Premiums Compared to Other Indicators

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 1999-2007; KPMG Survey of Employer- Sponsored Health Benefits, 1993, 1996; The Health Insurance Association of America (HIAA), 1988, 1989, 1990; Bureau of Labor Statistics, Consumer Price Index (U.S. City Average of Annual Inflation (April to April), 1988-2006; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1988-2006 (April to April).

*Estimate is statistically different from the previous year shown at p<0.05.

Note: Data on premium increases reflect the cost of health insurance premiums for a family of four.

12.0%

18.0%

8.5%

0.8%

5.0%5.0%

6.1%

7.7%

9.2%

13.9%̂12.9%*

5.3%*

14.0%

8.2%*

10.9%*11.2%*

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Health Insurance Premiums

Workers Earnings

Overall Inflation

6

7

EXISTING MEASURES

Recent federal healthcare reform measures affecting employers

1996 HIPAA (portability,

nondiscrimination, standard electronic transactions, privacy, security, etc.)

MHPA NMHPA WHCRA

2003 MMA (HSAs and Medicare

Part D)

2008 GINA MHPA amendments Michelle’s Law MSP reporting

2009 CHIPRA ARRA (COBRA subsidy, breach

notification, comparative effectiveness research)

COBRA subsidy extension (does not seem to be in works again)

8

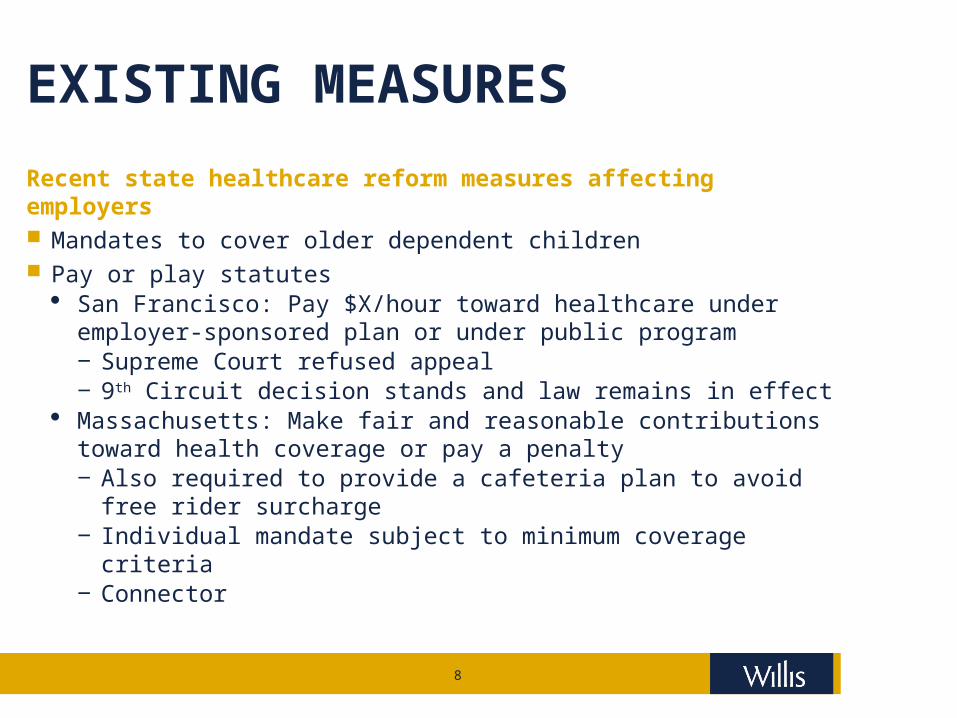

EXISTING MEASURES

Recent state healthcare reform measures affecting employers Mandates to cover older dependent children Pay or play statutes

San Francisco: Pay $X/hour toward healthcare under employer-sponsored plan or under public program‒ Supreme Court refused appeal‒ 9th Circuit decision stands and law remains in effect

Massachusetts: Make fair and reasonable contributions toward health coverage or pay a penalty‒ Also required to provide a cafeteria plan to avoid free rider

surcharge‒ Individual mandate subject to minimum coverage criteria‒ Connector

9

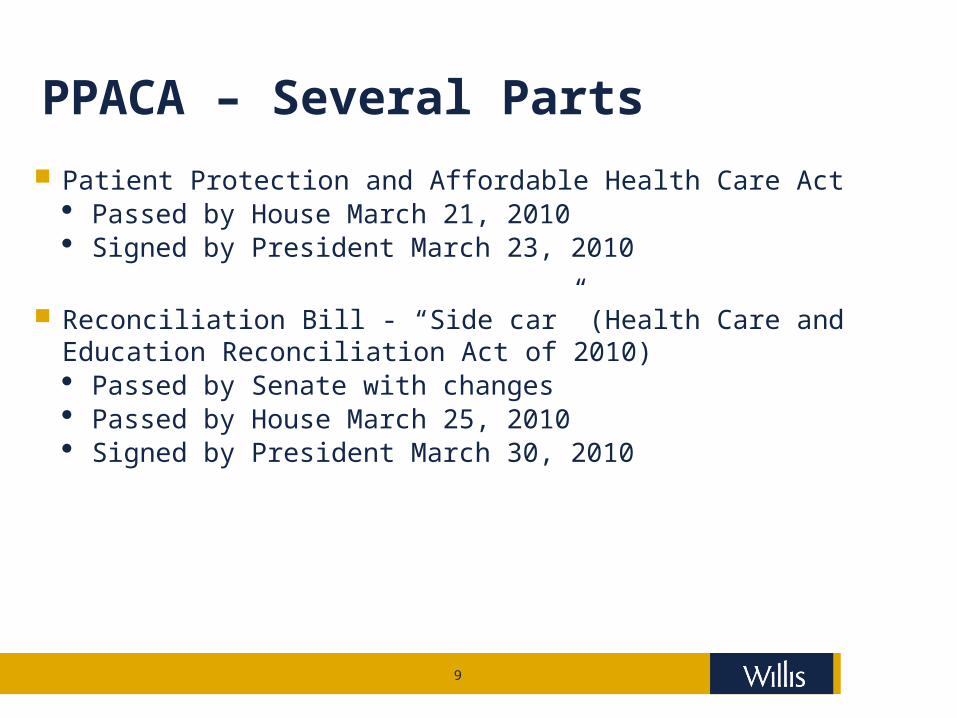

PPACA – Several Parts

Patient Protection and Affordable Health Care Act Passed by House March 21, 2010 Signed by President March 23, 2010

Reconciliation Bill - “Side car” (Health Care and Education Reconciliation Act of 2010) Passed by Senate with changes Passed by House March 25, 2010 Signed by President March 30, 2010

10

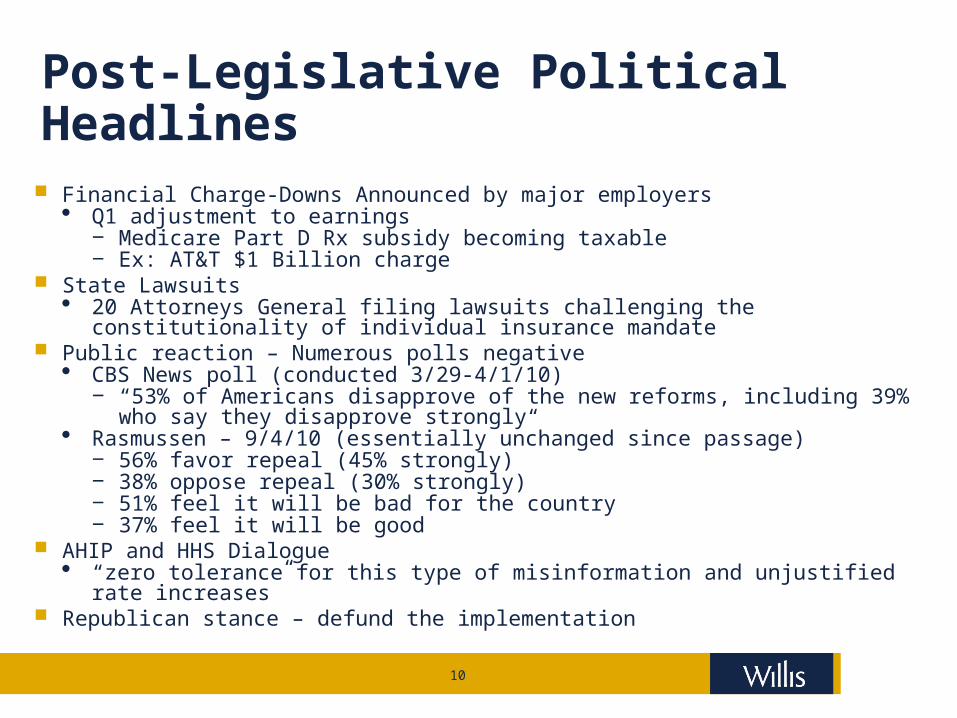

Post-Legislative Political Headlines

Financial Charge-Downs Announced by major employers Q1 adjustment to earnings

‒ Medicare Part D Rx subsidy becoming taxable‒ Ex: AT&T $1 Billion charge

State Lawsuits 20 Attorneys General filing lawsuits challenging the constitutionality of individual

insurance mandate Public reaction – Numerous polls negative

CBS News poll (conducted 3/29-4/1/10)‒ “53% of Americans disapprove of the new reforms, including 39% who say they

disapprove strongly“ Rasmussen – 9/4/10 (essentially unchanged since passage)

‒ 56% favor repeal (45% strongly)‒ 38% oppose repeal (30% strongly)‒ 51% feel it will be bad for the country‒ 37% feel it will be good

AHIP and HHS Dialogue “zero tolerance for this type of misinformation and unjustified rate increases”

Republican stance – defund the implementation

11

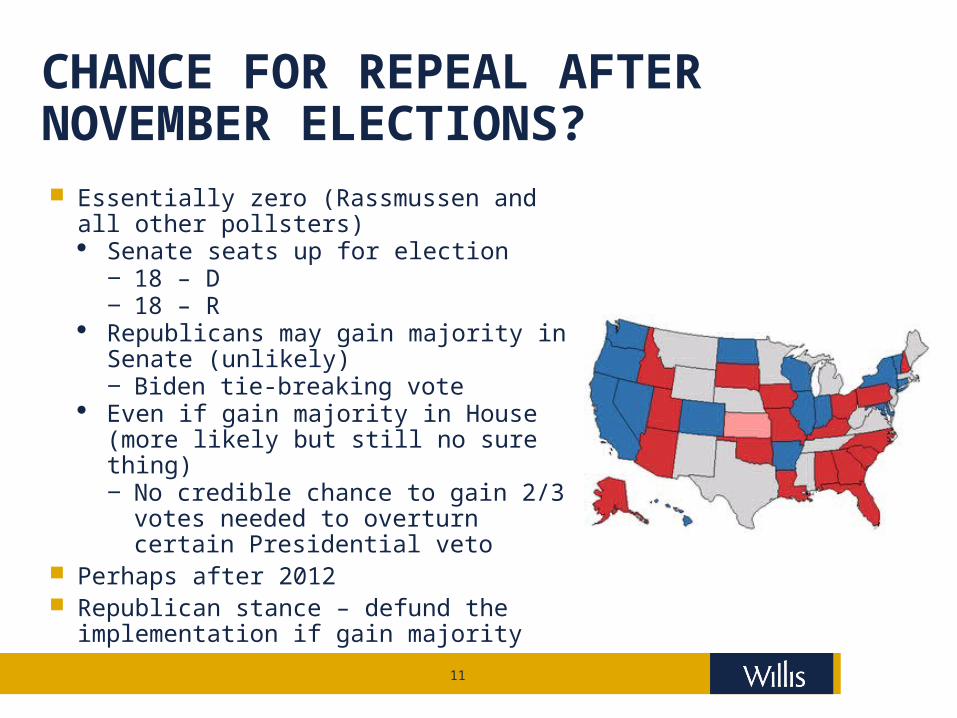

CHANCE FOR REPEAL AFTER NOVEMBER ELECTIONS? Essentially zero (Rassmussen and all other

pollsters) Senate seats up for election

‒ 18 – D‒ 18 – R

Republicans may gain majority in Senate (unlikely)‒ Biden tie-breaking vote

Even if gain majority in House (more likely but still no sure thing)‒ No credible chance to gain 2/3 votes

needed to overturn certain Presidential veto

Perhaps after 2012 Republican stance – defund the

implementation if gain majority

12

FEDERAL HEALTH CARE REFORM – OVERALL FINANCIAL IMPACT

13

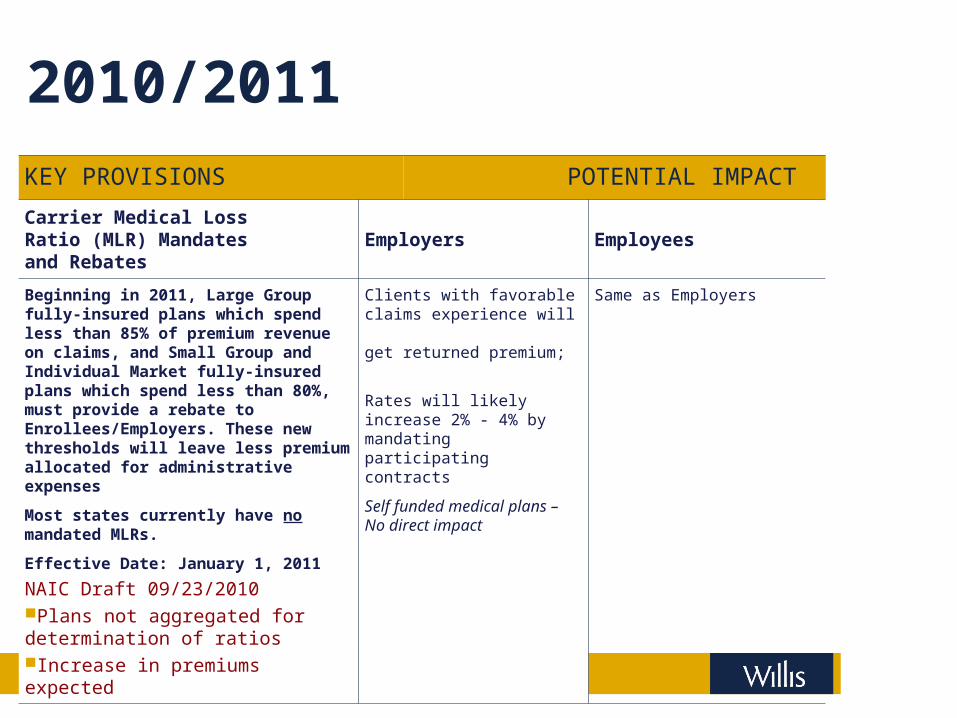

2010/2011KEY PROVISIONS POTENTIAL IMPACT

Carrier Medical Loss Ratio (MLR) Mandates and Rebates

Employers Employees

Beginning in 2011, Large Group fully-insured plans which spend less than 85% of premium revenue on claims, and Small Group and Individual Market fully-insured plans which spend less than 80%, must provide a rebate to Enrollees/Employers. These new thresholds will leave less premium allocated for administrative expenses

Most states currently have no mandated MLRs.

Effective Date: January 1, 2011

NAIC Draft 09/23/2010Plans not aggregated for determination of ratiosIncrease in premiums expected

Clients with favorable claims experience will get returned premium;

Rates will likely increase 2% - 4% by mandating participating contracts

Self funded medical plans – No direct impact

Same as Employers

14

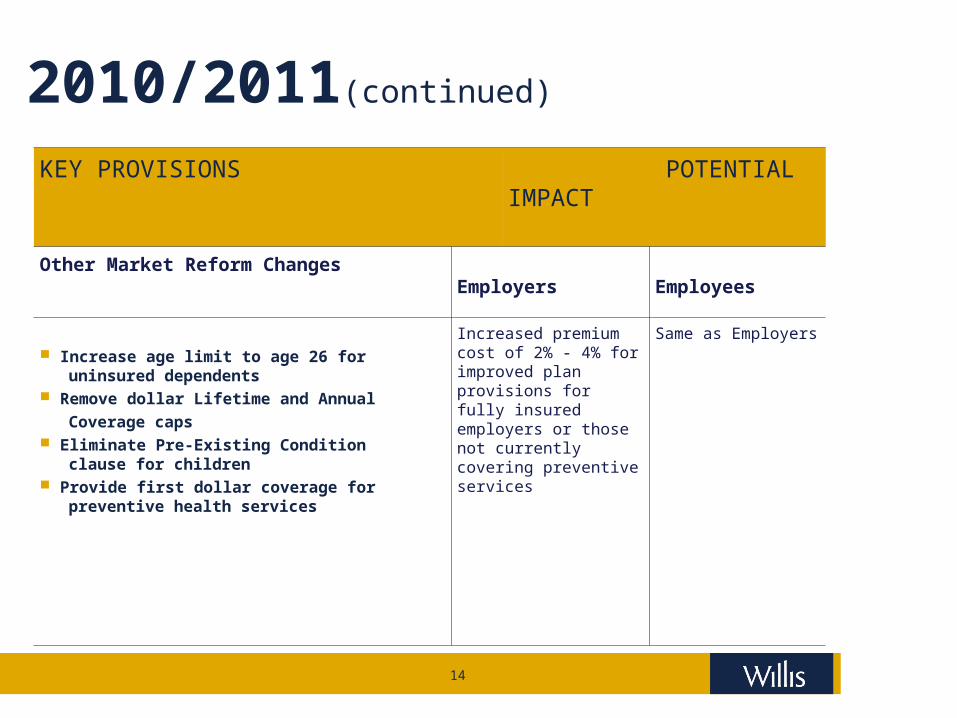

2010/2011(continued)

KEY PROVISIONS POTENTIAL IMPACT

Other Market Reform Changes Employers Employees

Increase age limit to age 26 for uninsured dependents Remove dollar Lifetime and Annual

Coverage caps Eliminate Pre-Existing Condition clause for children Provide first dollar coverage for preventive health services

Increased premium cost of 2% - 4% for improved plan provisions for fully insured employers or those not currently covering preventive services

Same as Employers

15

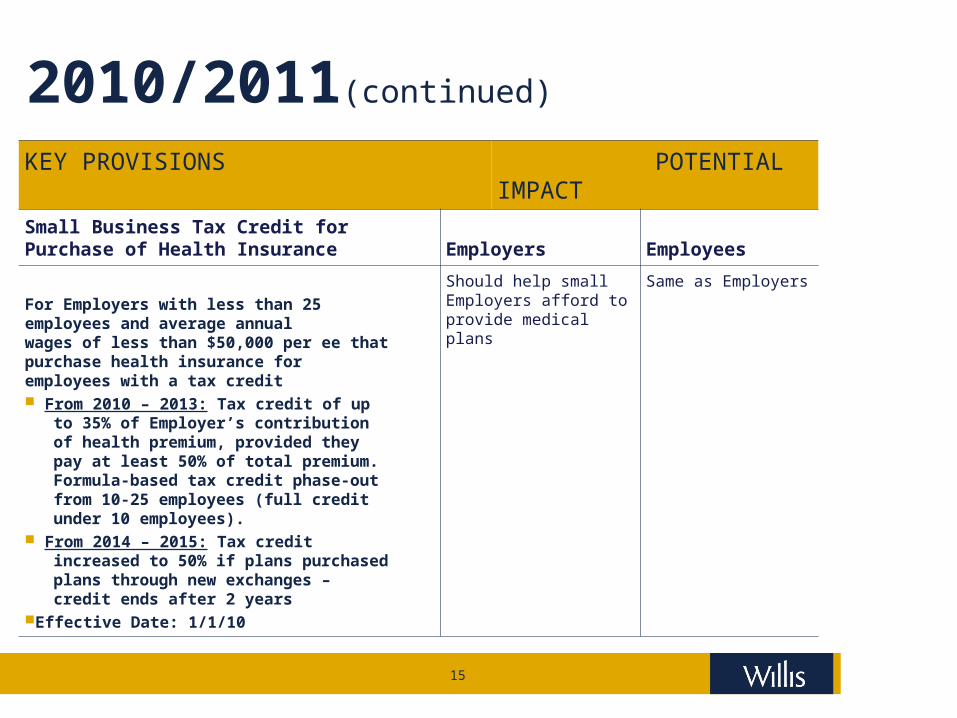

2010/2011(continued)

KEY PROVISIONS POTENTIAL IMPACT

Small Business Tax Credit for Purchase of Health Insurance

Employers Employees

For Employers with less than 25 employees and average annual wages of less than $50,000 per ee that purchase health insurance for employees with a tax credit From 2010 – 2013: Tax credit of up to 35% of Employer’s contribution of health premium, provided they pay at least 50% of total premium. Formula-based tax credit phase-out from 10-25 employees (full credit under 10 employees). From 2014 – 2015: Tax credit increased to 50% if plans purchased plans through new exchanges – credit ends after 2 yearsEffective Date: 1/1/10

Should help small Employers afford to provide medical plans

Same as Employers

16

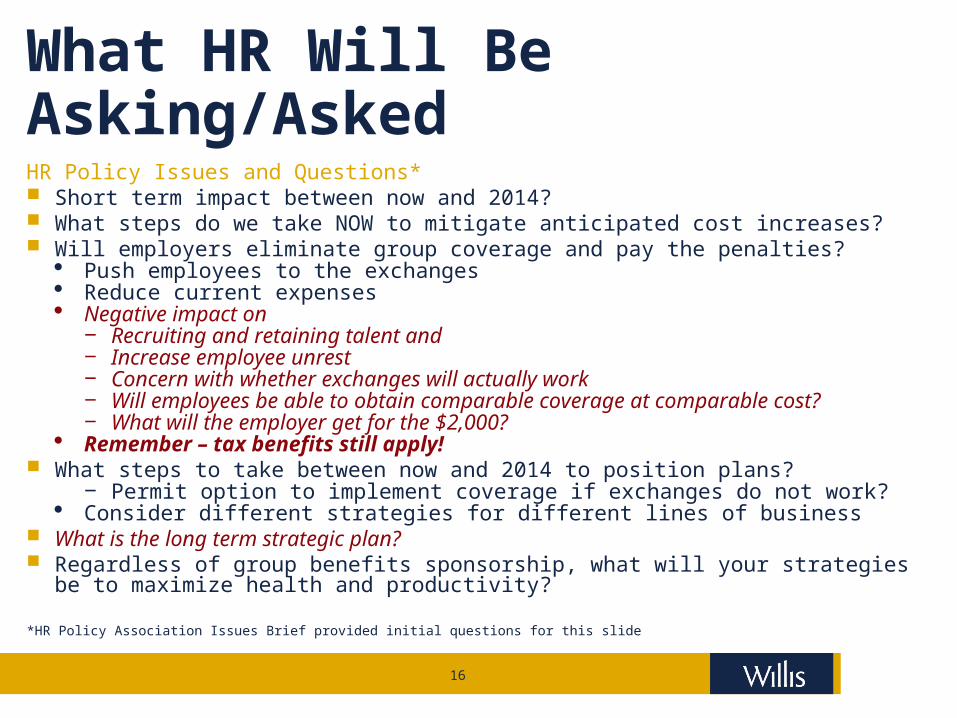

What HR Will Be Asking/AskedHR Policy Issues and Questions* Short term impact between now and 2014? What steps do we take NOW to mitigate anticipated cost increases? Will employers eliminate group coverage and pay the penalties?

Push employees to the exchanges Reduce current expenses Negative impact on

‒ Recruiting and retaining talent and‒ Increase employee unrest‒ Concern with whether exchanges will actually work‒ Will employees be able to obtain comparable coverage at comparable cost?‒ What will the employer get for the $2,000?

Remember – tax benefits still apply! What steps to take between now and 2014 to position plans?

‒ Permit option to implement coverage if exchanges do not work? Consider different strategies for different lines of business

What is the long term strategic plan? Regardless of group benefits sponsorship, what will your strategies be to maximize health

and productivity?

*HR Policy Association Issues Brief provided initial questions for this slide

17

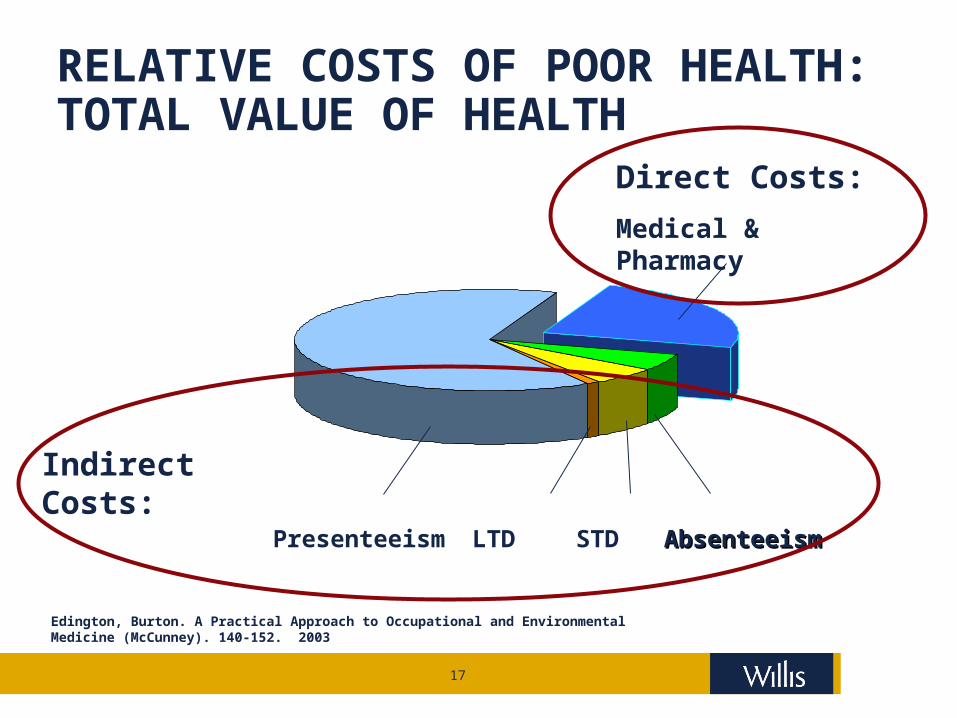

RELATIVE COSTS OF POOR HEALTH: TOTAL VALUE OF HEALTH

Presenteeism AbsenteeismAbsenteeismSTDLTD

Direct Costs:

Medical & Pharmacy

Indirect Costs:

Edington, Burton. A Practical Approach to Occupational and Environmental Medicine (McCunney). 140-152. 2003

18

FEDERAL HEALTH CARE REFORM – IMPACT ON PLAN COMPLIANCE

19

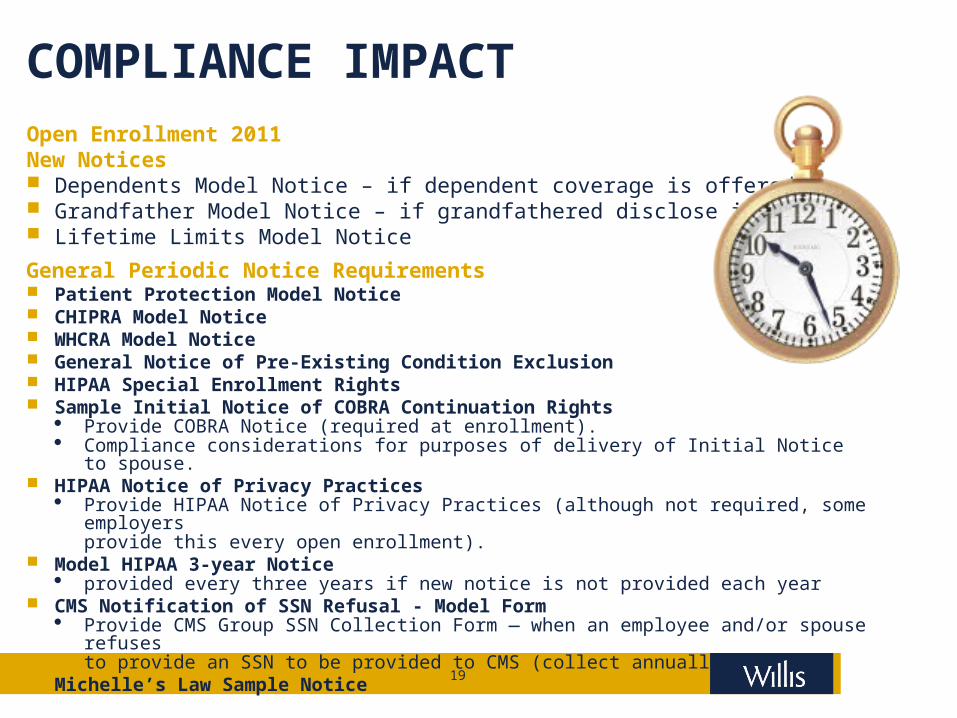

COMPLIANCE IMPACT Open Enrollment 2011New Notices Dependents Model Notice – if dependent coverage is offered Grandfather Model Notice – if grandfathered disclose impact Lifetime Limits Model Notice

General Periodic Notice Requirements Patient Protection Model Notice CHIPRA Model Notice WHCRA Model Notice General Notice of Pre-Existing Condition Exclusion HIPAA Special Enrollment Rights Sample Initial Notice of COBRA Continuation Rights

Provide COBRA Notice (required at enrollment). Compliance considerations for purposes of delivery of Initial Notice to spouse.

HIPAA Notice of Privacy Practices Provide HIPAA Notice of Privacy Practices (although not required, some employers

provide this every open enrollment). Model HIPAA 3-year Notice

provided every three years if new notice is not provided each year CMS Notification of SSN Refusal - Model Form

Provide CMS Group SSN Collection Form — when an employee and/or spouse refusesto provide an SSN to be provided to CMS (collect annually).

Michelle’s Law Sample Notice

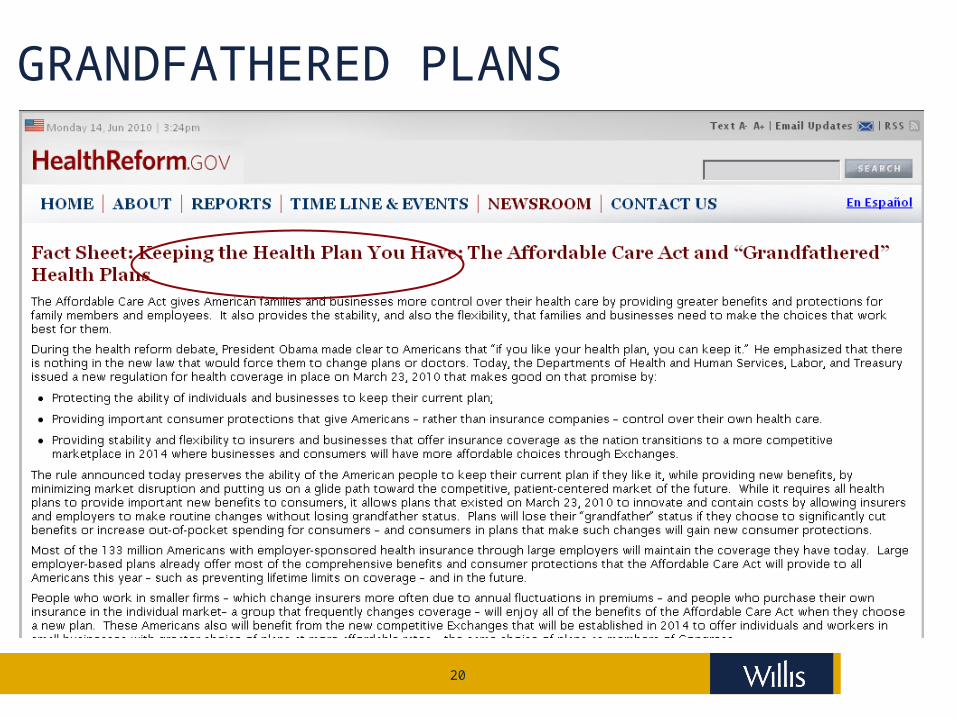

20

GRANDFATHERED PLANS

21

Who are you going to believe, me or your own eyes?

- Chico Marx

22

GRANDFATHERED PLANS

What is a Grandfathered Plan? What is the Impact? Any group health plan or individual plan in existence as

of March 23, 2010 Some compliance exemptions – but only for insurance

reforms All grandfathered plans must meet minimum coverage

requirements for purposes of meeting the individual mandate

Regulations issued permit some minor changes to retain status Most plans will lose status Determine value of status

23

GRANDFATHERED PLANS

What is a Grandfathered Plan?

IRS – 26 CFR Parts 54 and 602

DOL – 29 CFR Part 2590

HHS – 45 CFR Part 147 Any group health plan or individual plan in which an

individual was enrolled on March 23, 2010 (as long as it

maintains that status under the rules of the IFR) Applies to each benefit package (undefined) Does not lose status just because people (even all) who were enrolled on

3/23/2010 cease to be enrolled New policy, contract or certificate after 3/23/10 (FAQ – Will address

this in future guidance) Loses grandfathered status Special rule for collectively bargained plans

24

GRANDFATHERED PLANS

What is a Grandfathered Plan (cont)? Family members and new employees can join Anti-abuse rules

M&A‒ Principal purpose can’t be to use grandfather

Change in plan eligibility‒ Transfers must be for bona fide employment based reason

25

GRANDFATHERED PLANS

Maintenance of Grandfathered Status? Disclosure mandate Documentation requirement Changes that will cause plan to lose grandfathered status

Elimination of benefits‒ To diagnose or treat a particular condition

Increase in percentage cost-sharing (co-insurance) Increase in fixed-amount cost-sharing other

than a copayment (deductible or OOP) Increase in fixed-amount copayment

‒ More than $5 + medical inflation (since 3/23/10)‒ And more than medical inflation (currently .3%) plus

15% (since 3/23/2010) New policy, contract or certificate after 3/23/10 (may

change with new guidance)

26

GRANDFATHERED PLANS

Maintenance of Grandfathered Status (cont.) ? Changes that will cause plan to lose grandfathered status (cont.)

Decrease in contribution rate (by more than 5 percentage points)‒ Based on employer’s cost of coverage‒ Based on formula

Changes in annual limits‒ Adding limit or decreasing current

Decrease in lifetime limits Value of grandfathered status?

Uncertain Calculate value of status vs. need for design

changes

27

ISSUES AFFECTING EMPLOYERS AND PLANSRequirements and Prohibitions Effective first day of the first plan year that starts on or after

September, 23, 2010 Grandfathered and non-Grandfathered plans

No lifetime dollar limits on essential benefits No rescissions (retroactive revocation of coverage) except for

fraud/intentional misrepresentation of a material fact No annual limits on dollar value of “essential health benefits”

‒ Except as permitted by HHS until 2014 Must cover children of covered individual up to age 26

‒ No tax dependent requirement‒ Married/unmarried‒ Not child or spouse of dependent‒ Tax favored basis‒ Up to 1/1/2014 grandfathered plans can exclude if eligible for employment

based coverage (other than a parent’s plan) No pre-ex condition exclusions for enrollees under 19 (applies to all for 2014

plan year) Amend plan and SPD, prepare for 2011 open enrollment

28

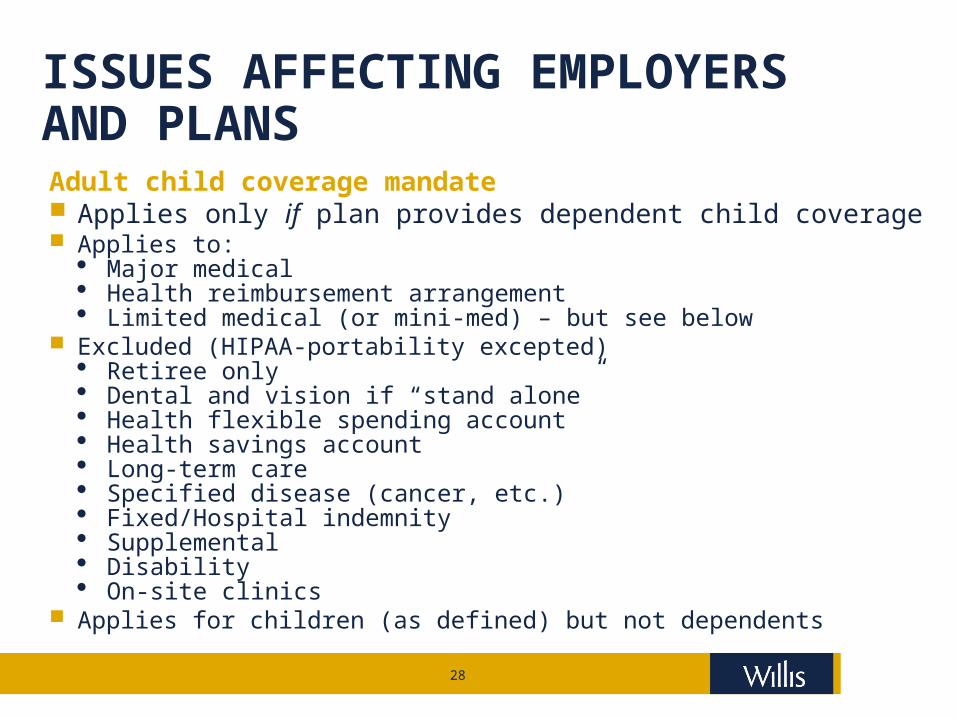

ISSUES AFFECTING EMPLOYERS AND PLANSAdult child coverage mandate Applies only if plan provides dependent child coverage Applies to:

Major medical Health reimbursement arrangement Limited medical (or mini-med) – but see below

Excluded (HIPAA-portability excepted) Retiree only Dental and vision if “stand alone” Health flexible spending account Health savings account Long-term care Specified disease (cancer, etc.) Fixed/Hospital indemnity Supplemental Disability On-site clinics

Applies for children (as defined) but not dependents

29

ISSUES AFFECTING EMPLOYERS AND PLANSAdult child coverage mandate Applies for children (as defined) but not dependents

Includes natural sons and daughters, step-children, foster and adopted children.

DOL Website Posting (9/21) - Grandchildren and others not so defined‒ Can be covered by plan (even as a dependent)‒ Adult child rules will not be mandatory‒ Plan permitted to cover them in the same way

30

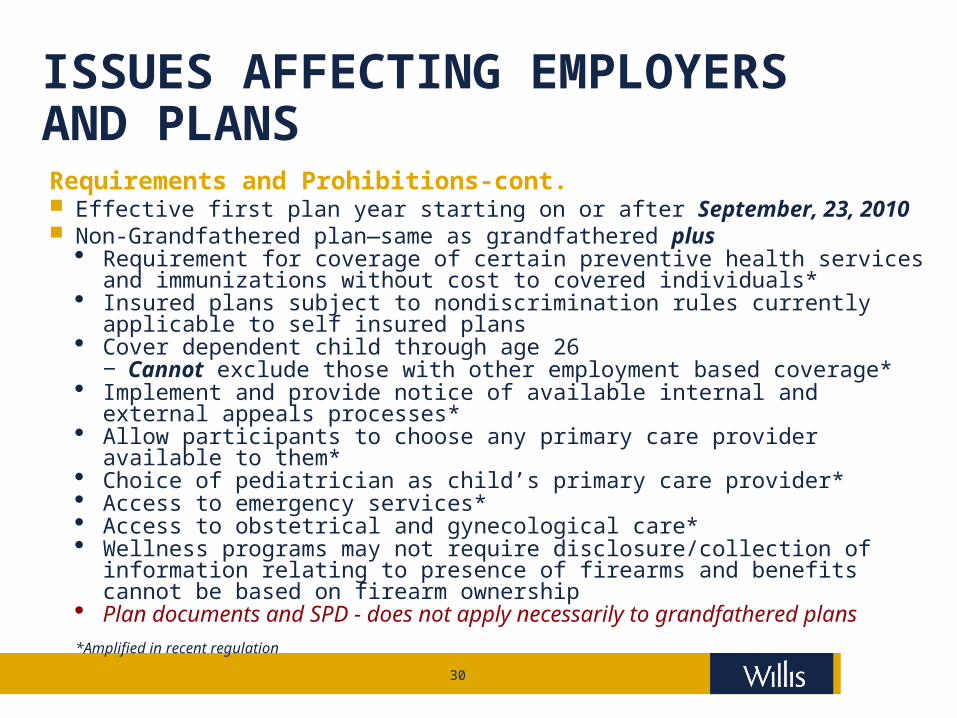

ISSUES AFFECTING EMPLOYERS AND PLANSRequirements and Prohibitions-cont. Effective first plan year starting on or after September, 23, 2010 Non-Grandfathered plan—same as grandfathered plus

Requirement for coverage of certain preventive health services and immunizations without cost to covered individuals*

Insured plans subject to nondiscrimination rules currently applicable to self insured plans

Cover dependent child through age 26‒ Cannot exclude those with other employment based coverage*

Implement and provide notice of available internal and external appeals processes*

Allow participants to choose any primary care provider available to them* Choice of pediatrician as child’s primary care provider* Access to emergency services* Access to obstetrical and gynecological care* Wellness programs may not require disclosure/collection of information

relating to presence of firearms and benefits cannot be based on firearm ownership

Plan documents and SPD - does not apply necessarily to grandfathered plans

*Amplified in recent regulation

31

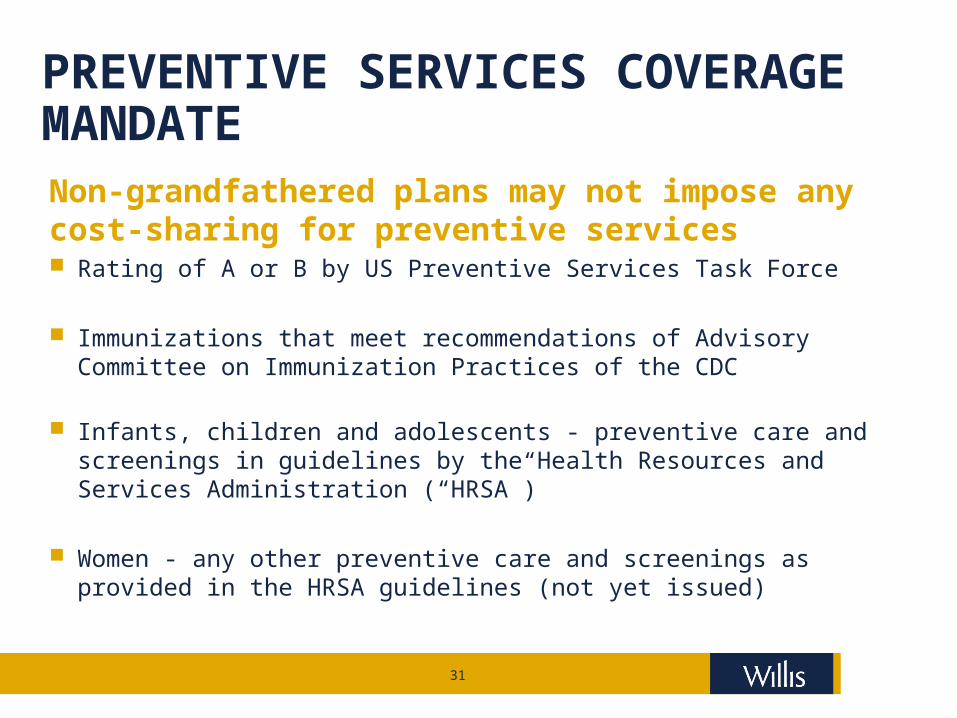

PREVENTIVE SERVICES COVERAGE MANDATENon-grandfathered plans may not impose any cost-sharing for preventive services Rating of A or B by US Preventive Services Task Force

Immunizations that meet recommendations of Advisory Committee on Immunization Practices of the CDC

Infants, children and adolescents - preventive care and screenings in guidelines by the Health Resources and Services Administration (“HRSA”)

Women - any other preventive care and screenings as provided in the HRSA guidelines (not yet issued)

32

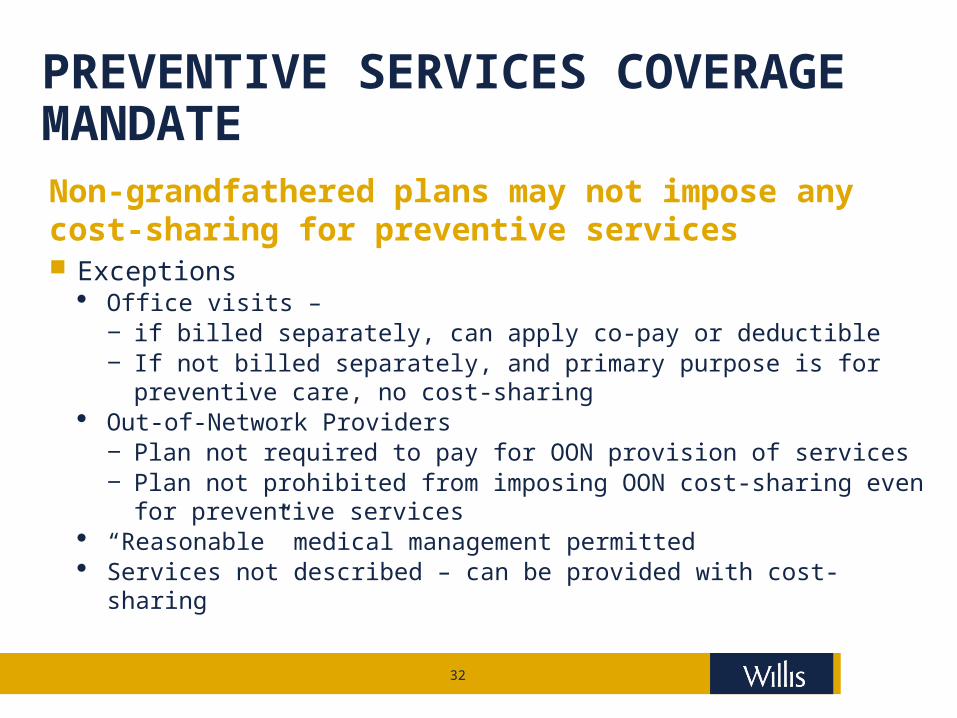

PREVENTIVE SERVICES COVERAGE MANDATENon-grandfathered plans may not impose any cost-sharing for preventive services Exceptions

Office visits – ‒ if billed separately, can apply co-pay or deductible‒ If not billed separately, and primary purpose is for preventive care, no cost-

sharing Out-of-Network Providers

‒ Plan not required to pay for OON provision of services‒ Plan not prohibited from imposing OON cost-sharing even for preventive

services “Reasonable” medical management permitted Services not described – can be provided with cost-sharing

33

PREVENTIVE SERVICES COVERAGE MANDATENon-grandfathered plans may not impose any cost-sharing for preventive services Miscellaneous

Effective plan years starting on or after 9/23/2010 or, if later, one year after recommendation or guideline is issued

Changes to guidelines or recommendations – ‒ Plan can stop providing the services if they are no longer recommended‒ May have to give advance notice

34

INTERNAL AND EXTERNAL APPEALS PROCESSNon-Grandfathered plans must implement internal and external appeals process

Effective for plan years starting after 9/23/2010

Internal Appeals – based on ERISA required procedures Must adhere to internal appeals rules or deemed exhausted Meaning – claimant can go directly to external appeals or court

External Appeals – DOL Tech Release - Issued 8/23/2010 Insured plans – not employer responsibility

State process for insurance issuers – not ERISA plan/employer responsibility If available, they can be used, otherwise new federal rules apply

Self-insured plans If subject to state requirements (church, government plans, MEWAS)

‒ If state rules available, they can be used, otherwise new federal rules apply Self- funded, non-grandfathered ERISA plans

‒ New federal rules apply

35

INTERNAL AND EXTERNAL APPEALS PROCESSNon-Grandfathered plans must implement internal and external appeals process Internal Claims appeal IFR issued 7/22/2010 Adverse benefit determination

Includes rescission (retroactive termination of coverage) Does not include eligibility

Urgent Care Claims – must be decided as soon as possible, but no longer than 24 hours

Procedural criteria Provide, in advance, new or additional evidence considered Disclose, in advance, any new rationale for denying claim Avoid conflict of interest – reviewers cannot be chosen on likelihood of

upholding initial adverse benefit determination or paid bonuses based on claims denied

36

INTERNAL AND EXTERNAL APPEALS PROCESSNon-Grandfathered plans must implement internal and external appeals process External Appeals (cont.) Procedural criteria (continued)

Notice requirements‒ Culturally and linguistically appropriate‒ Additional identifying information regarding claim (such as date of service,

amount of claim, etc.)‒ Additional information regarding claim denial (such as denial code and

meaning)‒ Contact information for health insurance commissioner or ombudsman‒ Strict adherence to internal process or internal process deemed exhausted

37

INTERNAL AND EXTERNAL APPEALS PROCESSDOL Technical Release – applies as safe harbor until further guidance Plan must consider request for external appeal if filed within 4 months of final adverse benefit decision

Preliminary review by plan Required within 5 days of receipt Must determine

Claimant covered by plan Denial based on ineligibility (not subject to external review) Claimant exhausted internal review process if required Claimant provided all necessary info to process review Within 1 day of determination must inform claimant, in writing, if request is not

eligible or incomplete

38

INTERNAL AND EXTERNAL APPEALS PROCESSDOL Technical Release – applies as safe harbor until further guidance Consideration of external appeal – ineligible or incomplete If not eligible, must include reasons and EBSA contact info In not complete, must describe info necessary to complete Claimant has remainder of 4 months or 48 hours (whichever is greater) to cureIf eligible for external review – assign to independent review organization (IRO) Must have at least three accredited IROs available and other rules to prevent

bias If IRO reverses, plan must immediately provide coverage or pay claimTech Release 2010-02 Enforcement grace period until 07/01/2011 for some changes

Urgent care determination timeframe Culturally and linguistically appropriate notices Broader content and specificity requirements Substantial compliance

39

LIFETIME AND ANNUAL LIMITSLifetime and annual dollar limits on “essential health benefits” prohibited Dollar limits on non essential benefits permitted Applies to dollar limits

Silent on other types of limits Presumption that number of visits, number of procedures, limits on cost per

procedure, etc., are permissible Annual limits phased in

$750,000 - Plan years starting on or after 09/23/2010 $1,250,000 - Plan years starting on or after 09/23/2011 $2,000,000 - Plan years starting on or after 09/23/2012 No limits - Plan years starting on or after 01/01/2014

Limited Medical (“mini-med”) – HHS may waive annual limits for plan years starting before 01/01/2014 if limits would result in Significant decrease in access to benefits or Significant increase in premiums for plan or coverage

40

LIFETIME AND ANNUAL LIMITSLifetime and annual dollar limits on “essential health benefits” prohibited Essential benefits in legislation – no further clarification, yet, in regulations

Ambulatory patient services Emergency services Hospitalization Maternity and newborn care Mental health and substance use disorder services, including behavioral

health treatment Prescription drugs Rehabilitative and habilitative services Laboratory services Preventive and wellness services and chronic disease management Pediatric services, including oral and vision care

IFR permits interpretation of essential health benefits based on “good faith efforts” to comply with a “reasonable interpretation” as long as that is consistently applied

41

LIFETIME AND ANNUAL LIMITSLifetime and annual limits on “essential benefits prohibited” (cont.) Excluded benefits

Health (NOT dependent care) FSA, MSA, HSA Integrated health reimbursement arrangement (HRA) Retiree-only plans (including HRA) Any HIPAA-excepted benefits (limited scope dental & vision, specified

disease, hospital fixed indemnity, supplemental) Stand-alone HRA – comments requested

Participant or beneficiary previously met lifetime limits Must provide notice and, if not currently enrolled, open enrollment period (of

at least 30 days) For first plan year starting after 09/23/2010

‒ Model notice from DOL‒ Can be included with annual enrollment materials if the notice is

“prominently” displayed If enrolled but some plan options not available, must permit to choose among

all coverage options generally available under the plan

42

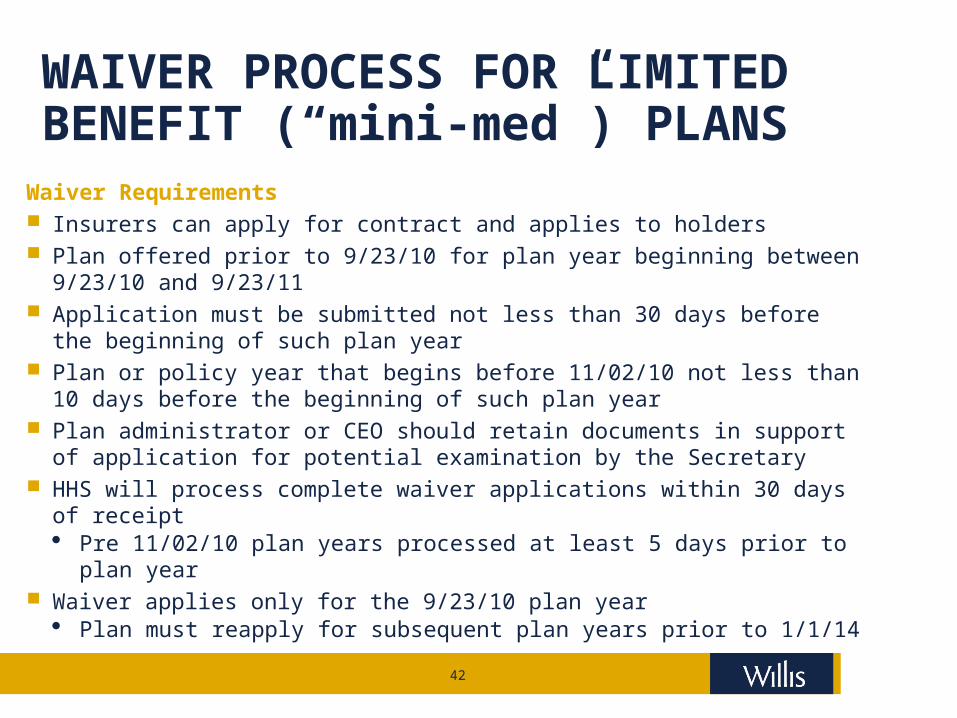

WAIVER PROCESS FOR LIMITED BENEFIT (“mini-med”) PLANS

Waiver Requirements Insurers can apply for contract and applies to holders Plan offered prior to 9/23/10 for plan year beginning between 9/23/10 and

9/23/11 Application must be submitted not less than 30 days before the beginning of

such plan year Plan or policy year that begins before 11/02/10 not less than 10 days before

the beginning of such plan year Plan administrator or CEO should retain documents in support of application

for potential examination by the Secretary HHS will process complete waiver applications within 30 days of receipt

Pre 11/02/10 plan years processed at least 5 days prior to plan year Waiver applies only for the 9/23/10 plan year

Plan must reapply for subsequent plan years prior to 1/1/14

43

WAIVER PROCESS FOR LIMITED BENEFIT (“mini-med”) PLANS

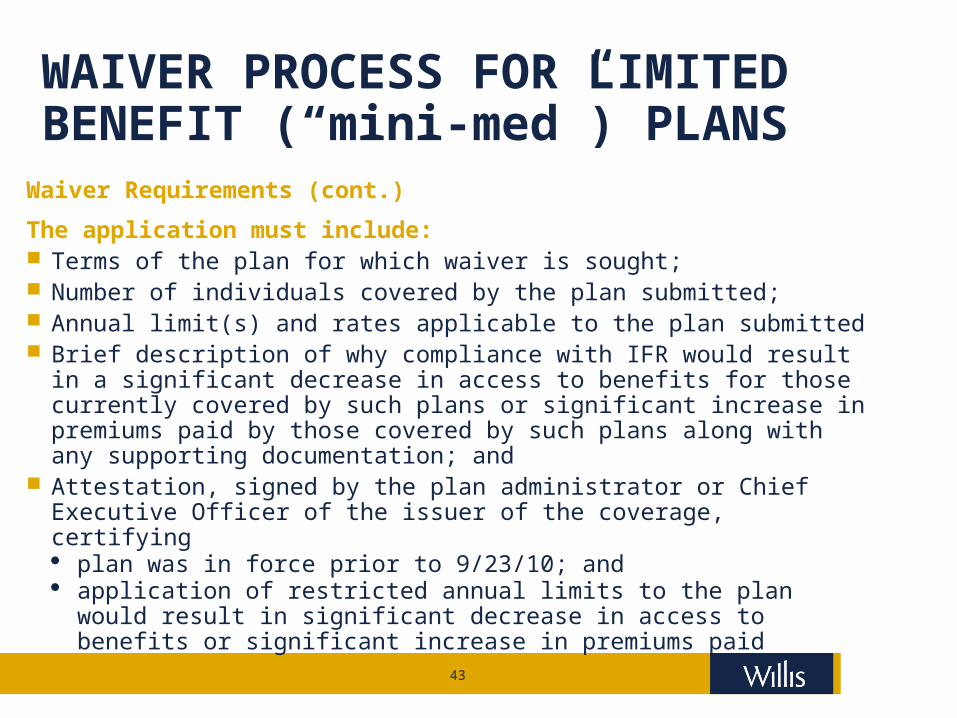

Waiver Requirements (cont.)

The application must include: Terms of the plan for which waiver is sought; Number of individuals covered by the plan submitted; Annual limit(s) and rates applicable to the plan submitted Brief description of why compliance with IFR would result in a

significant decrease in access to benefits for those currently covered by such plans or significant increase in premiums paid by those covered by such plans along with any supporting documentation; and

Attestation, signed by the plan administrator or Chief Executive Officer of the issuer of the coverage, certifying plan was in force prior to 9/23/10; and application of restricted annual limits to the plan would result in

significant decrease in access to benefits or significant increase in premiums paid

44

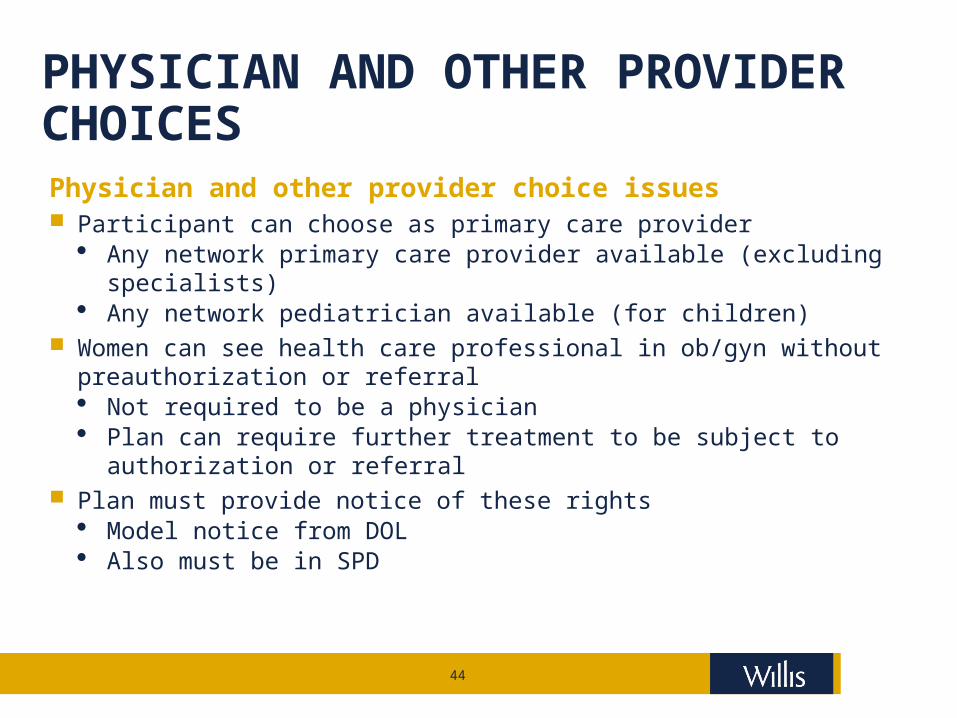

PHYSICIAN AND OTHER PROVIDER CHOICESPhysician and other provider choice issues Participant can choose as primary care provider

Any network primary care provider available (excluding specialists) Any network pediatrician available (for children)

Women can see health care professional in ob/gyn without preauthorization or referral Not required to be a physician Plan can require further treatment to be subject to authorization or referral

Plan must provide notice of these rights Model notice from DOL Also must be in SPD

45

EMERGENCY SERVICES

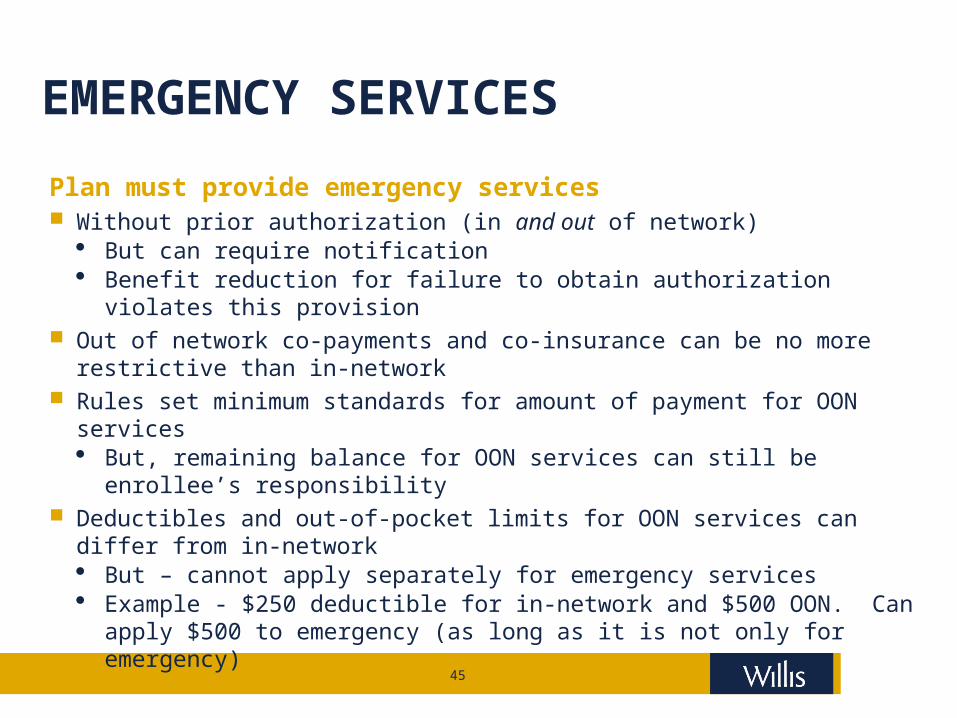

Plan must provide emergency services Without prior authorization (in and out of network)

But can require notification Benefit reduction for failure to obtain authorization violates this provision

Out of network co-payments and co-insurance can be no more restrictive than in-network

Rules set minimum standards for amount of payment for OON services But, remaining balance for OON services can still be enrollee’s responsibility

Deductibles and out-of-pocket limits for OON services can differ from in-network But – cannot apply separately for emergency services Example - $250 deductible for in-network and $500 OON. Can apply $500 to

emergency (as long as it is not only for emergency)

46

PREEXISTING CONDITIONS EXCLUSIONSPreexisting Condition Exclusions Prohibited Relatively small impact on employer plans (vs. individual coverage) given

HIPAA applications Limited time, only if 63 day break, etc. But there are additional restrictions

Preexisting condition exclusions entirely eliminated All participants

‒ Plan years starting on or after 01/01/2014 Enrollees under age 19

‒ Plan years starting first plan year that begins on or after 09/23/2010 (01/01/11 for calendar year plans)

Treatment requirement eliminated Cannot refuse treatment or coverage for any condition present prior to

effective date of coverage regardless of prior medical advice, diagnosis, care, or treatment

47

PREEXISTING CONDITIONS EXCLUSIONSPreexisting Condition Exclusions Prohibited (cont.) Applies to health status generally

Cannot deny coverage of conditions of individual based on information before effective date of coverage including pre-enrollment questionnaire, physical examination, or review of records

Does NOT require plan to provide coverage for conditions that would otherwise be excluded just because it arose prior to the effective date of the coverage

48

RESCISSIONS

New requirement regarding rescission of coverage (vs. revocation) Generally, plans cannot “rescind” coverage once an enrollee is covered Exceptions

Acts or practice by the covered individual consisting of fraud or intentional misrepresentation of a material fact ‒ No clarity on “material” or intent‒ Inadvertent omission or unintended misrepresentation will not permit a

recession Nonpayment of premiums

Cancellation permitted (not retroactive so not a rescission of coverage) Withdrawal from the market of the issuer or product (applies mainly to

insurance providers) Relocation outside service area Cessation of membership in sponsoring organization

49

RESCISSIONS

New requirement regarding rescission of coverage (vs. revocation) (cont.) Applies to “rescission”

Cancellation or discontinuance of coverage that has a “retroactive effect”‒ Void as of any date before the cancellation‒ Voids benefits paid prior to cancellation

Cancellation that applies prospectively is not a rescission (so not prohibited) Can also rescind retroactively if it is attributable to failure to pay premiums

for the period of coverage Advance notice required, when rescission is allowed

50

OTHER REQUIREMENTS

2011 Changes apply to Grandfathered and non-Grandfathered plans Health insurers report medical loss ratio to HHS and provide rebates to enrollees

if MLR is than 85% (80% for small groups) Auto enrollment for large employers (200 or more employees)

Immediate/retroactive effective date – unlikely OTC medications cannot be reimbursed pre-tax from FSA, HSA, HRA or MSA

Amend plans and SPDs Non-qualifying distributions from HSA and

MSA penalty increase to 20% Review material for HDHP and HSA contributions (vendor resp.?)

W-2 reporting of the value of employer providedcoverage (issued in January, 2012) Gather data for reporting on 2011 coverage

‒ Work with payroll vendors for details‒ COBRA premium calculation for 2011 will be

critical for many purposes

51

OTC GUIDANCE ISSUED

Prescription defined: Written or electronic order for a medicine or drug meeting legal

requirement state in which medical expense incurred Issued by individual legally authorized Effective date 1/1/11 regardless of employer's plan year and grace

period, if any Reimbursements after 1/1/11 prohibited even if funds set aside in 2010 Does NOT apply to non medicines or drugs such as (equipment,

supplies or diagnostic devices) Ex. - crutches, bandages and

blood sugar test kits.

52

OTC GUIDANCE ISSUEDDebit cards The IRS will not challenge the use of health FSA and HRA debit cards

for expenses incurred through January 15, 2011 because of inability to comply with substantiation requirement of debit card usage.

Medical expenses other than OTC medicines or drugs can continue to be reimbursed through debit card.

Debit cards may continue to be used at pharmacies that do not have a qualifying Inventory Information Approval System, as long as the store satisfies the requirement that 90% of its gross receipts were for medical care expenses and substantiation is properly submitted.

Retroactive amendments to conform torequirements if adopted no later thanJune 30, 2011, is permissible

53

EARLY RETIREE REINSURANCE PROGRAMCommenced as of June 1, 2010 ERRP Provisions

Employment based plans‒ State or local government, employee organization, VEBA, multiemployer

Early retiree = age 55 but not Medicare eligible 80% of medical claim at least $15k not exceeding $90k Claims incurred between June 1, 2010 and

January 1, 2014 Tax free

54

EARLY RETIREE REINSURANCE PROGRAM ERRP Provisions (cont.)

Application process open Not first come first served Errors will cause application to be returned Conditions

‒ Cost savings programs for chronic or high cost conditions and fraud and abuse

‒ Restrictions on use of proceeds‒ Subject to audits‒ Certified by Secretary of HHS‒ Sponsor must have PHI agreement with plan or insurer‒ Document actual medical claims costs‒ Medical costs = health benefits (e.g., not long-term care)‒ Payments must lower plan costs not be returned to general revenues

55

SMALL EMPLOYER INCENTIVES2011 Simple Cafeteria Plans

Safe harbor from nondiscrimination rules for cafeteria plans (and benefits offered through a cafeteria plan)

All “nonexcludable” employees eligible to participate Certain minimum contribution requirements met Employed an average of 100 or fewer employees on business days during

either of the two preceding years Small employer tax credit

25 or fewer employees with average annual wages of less than $50,000 Tax credit up to 35% (25% for tax exempt employers) of the employer’s

contribution‒ employer contributes at least 50% of a benchmark premium

10 or fewer employees with annual wages of less than $25,000 will be eligible for full credit

Credits phase out as size and wage increases Determine if credit applies or if plan can be amended to come within limits

56

CLASS ACT

2011 Optional for employers

Government run voluntary long term care program‒ Once program begins, participating employers required to automatically

enroll employees who do not opt out and facilitate payroll deductions‒ Eff. in 2011, but HHS must provide guidance

Employees must opt-out of program—if not wanting to participate Pays cash benefits of an average $50 per day Five year vesting period before

benefits provided‒ Prepare additional payroll deductions

and opt-out election‒ Prepare and distribute employee

communications

57

MISCELLANEOUS - GENERAL AND NEW STUFF

1099 reporting PPACA §9006 application to all vendors of more than $600 Possible political fix – failed in amendment to Small Business Jobs Act of

2010 Politically unpopular so opponents look for ways to pass repeal of that

provision Additional benefit to self-employed Small Business Jobs Act of 2010 (HR 5297) -

§2042 – Deduction for health insurance costs in computing self-employment taxes in 2010

58

Post-2011 Issues

59

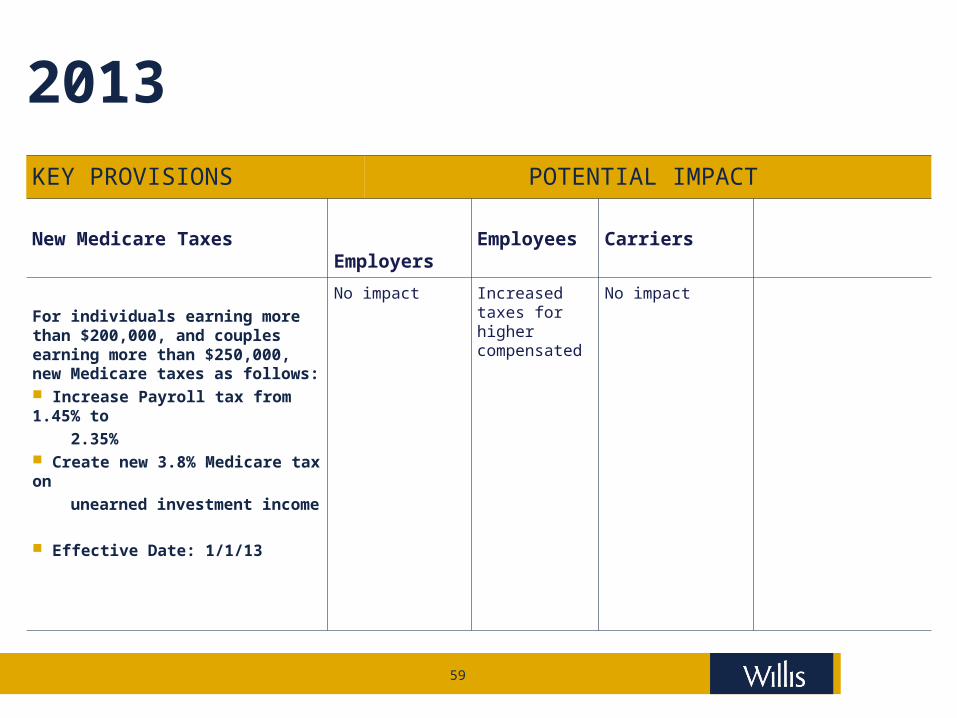

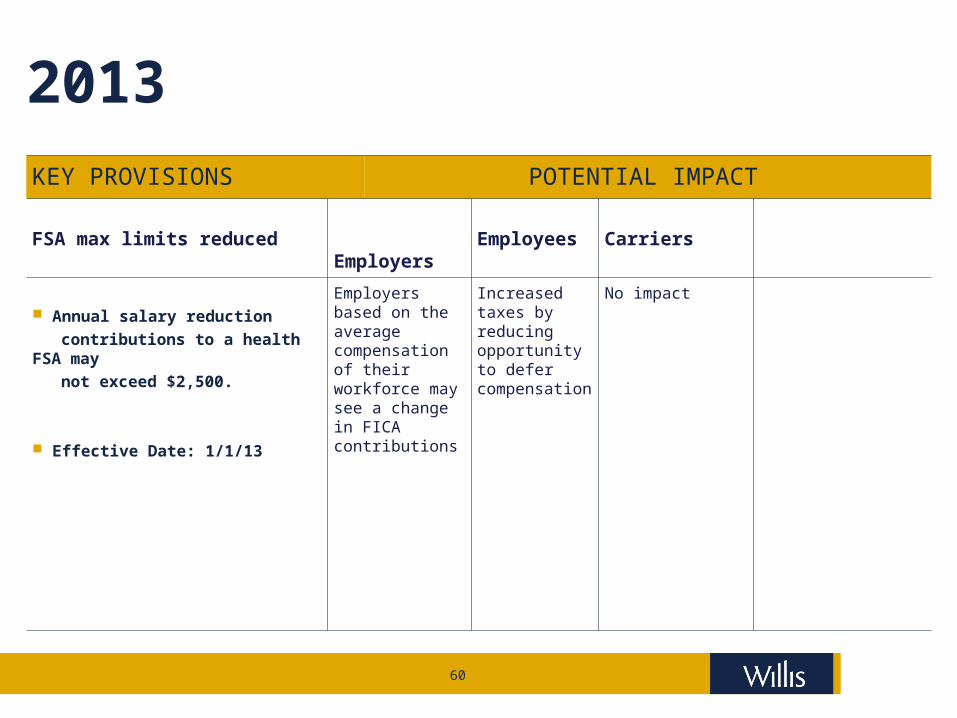

2013KEY PROVISIONS POTENTIAL IMPACT

New Medicare Taxes Employers Employees Carriers

For individuals earning more than $200,000, and couples earning more than $250,000, new Medicare taxes as follows: Increase Payroll tax from 1.45% to

2.35% Create new 3.8% Medicare tax on

unearned investment income

Effective Date: 1/1/13

No impact Increased taxes for higher compensated

No impact

60

2013KEY PROVISIONS POTENTIAL IMPACT

FSA max limits reduced Employers Employees Carriers

Annual salary reduction

contributions to a health FSA may

not exceed $2,500.

Effective Date: 1/1/13

Employers based on the average compensation of their workforce may see a change in FICA contributions

Increased taxes by reducing opportunity to defer compensation

No impact

61

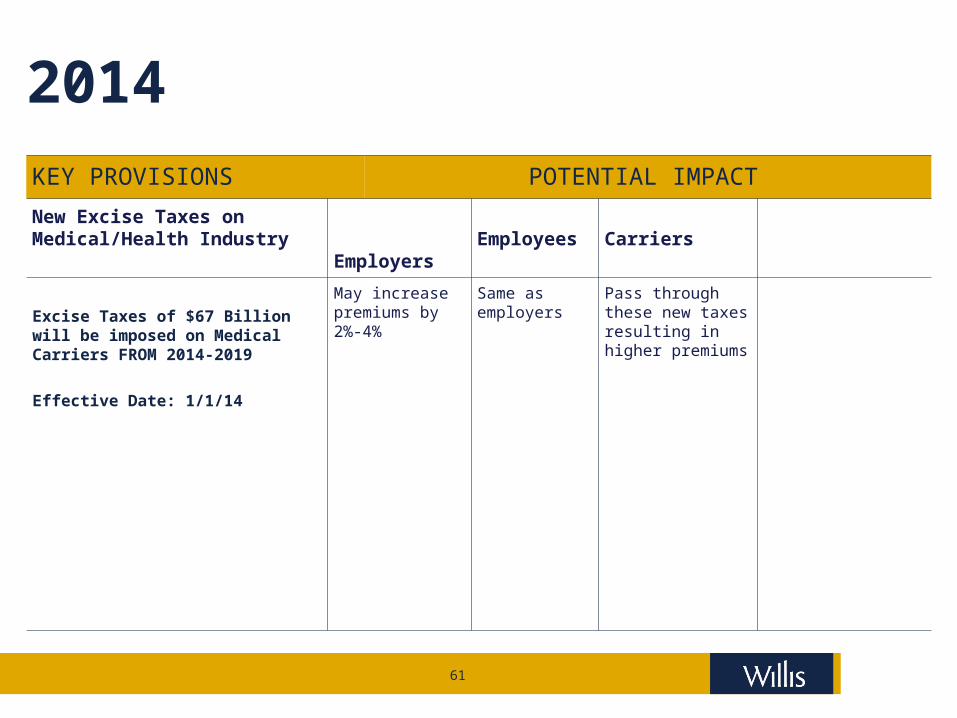

2014KEY PROVISIONS POTENTIAL IMPACT

New Excise Taxes on Medical/Health Industry

Employers Employees Carriers

Excise Taxes of $67 Billion will be imposed on Medical Carriers FROM 2014-2019

Effective Date: 1/1/14

May increase premiums by 2%-4%

Same as employers

Pass through these new taxes resulting in higher premiums

62

2014 (continued)

KEY PROVISIONS POTENTIAL IMPACT

Establishment of State-Based Insurance Exchanges

Employers Employees Carriers

State-based Insurance Exchanges will be established for individuals and small groups under 101 employees (In 2017, this access ceiling could be increased by each state). These exchanges will likely become the only market for these individuals and small Employers

Effective Date: 1/1/14

Could create lower cost options

Same as employers

May squeeze carrier pricing/ profitability further, but also provides access to newly covered enrollees

63

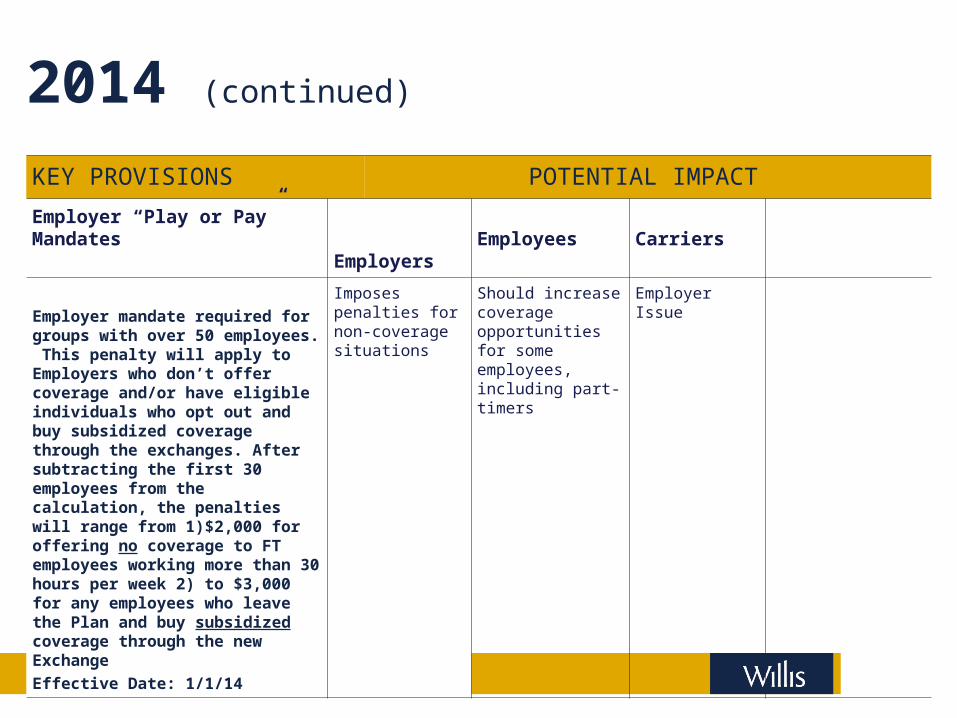

2014 (continued)

KEY PROVISIONS POTENTIAL IMPACT

Employer “Play or Pay” Mandates

Employers Employees Carriers

Employer mandate required for groups with over 50 employees. This penalty will apply to Employers who don’t offer coverage and/or have eligible individuals who opt out and buy subsidized coverage through the exchanges. After subtracting the first 30 employees from the calculation, the penalties will range from 1)$2,000 for offering no coverage to FT employees working more than 30 hours per week 2) to $3,000 for any employees who leave the Plan and buy subsidized coverage through the new Exchange

Effective Date: 1/1/14

Imposes penalties for non-coverage situations

Should increase coverage opportunities for some employees, including part-timers

Employer Issue

64

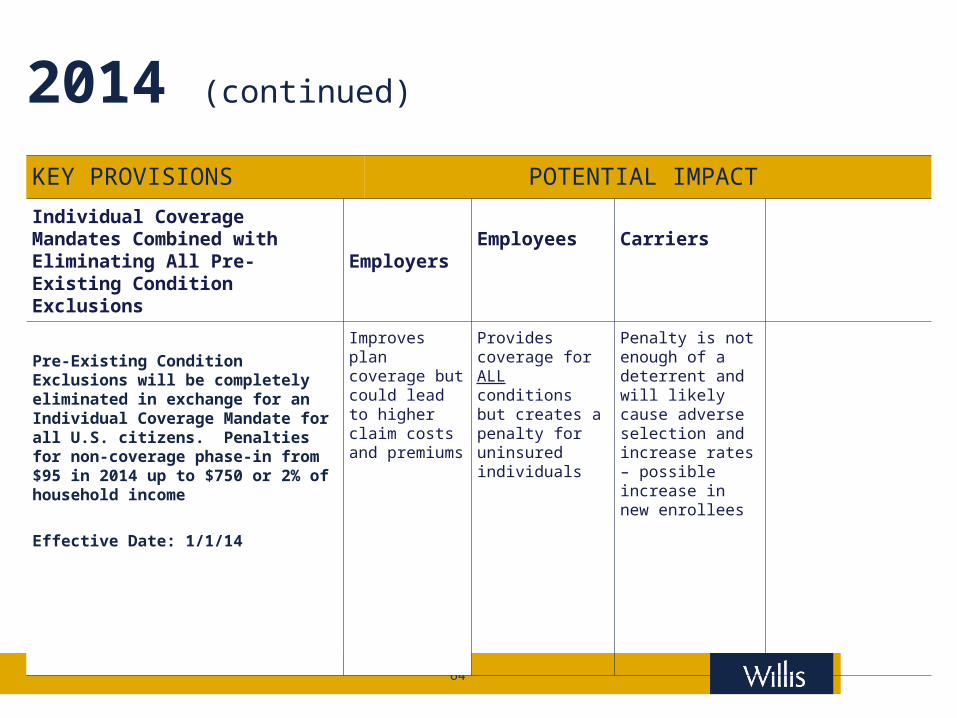

2014 (continued)

KEY PROVISIONS POTENTIAL IMPACT

Individual Coverage Mandates Combined with Eliminating All Pre-Existing Condition Exclusions

Employers Employees Carriers

Pre-Existing Condition Exclusions will be completely eliminated in exchange for an Individual Coverage Mandate for all U.S. citizens. Penalties for non-coverage phase-in from $95 in 2014 up to $750 or 2% of household income

Effective Date: 1/1/14

Improves plan coverage but could lead to higher claim costs and premiums

Provides coverage for ALL conditions but creates a penalty for uninsured individuals

Penalty is not enough of a deterrent and will likely cause adverse selection and increase rates – possible increase in new enrollees

65

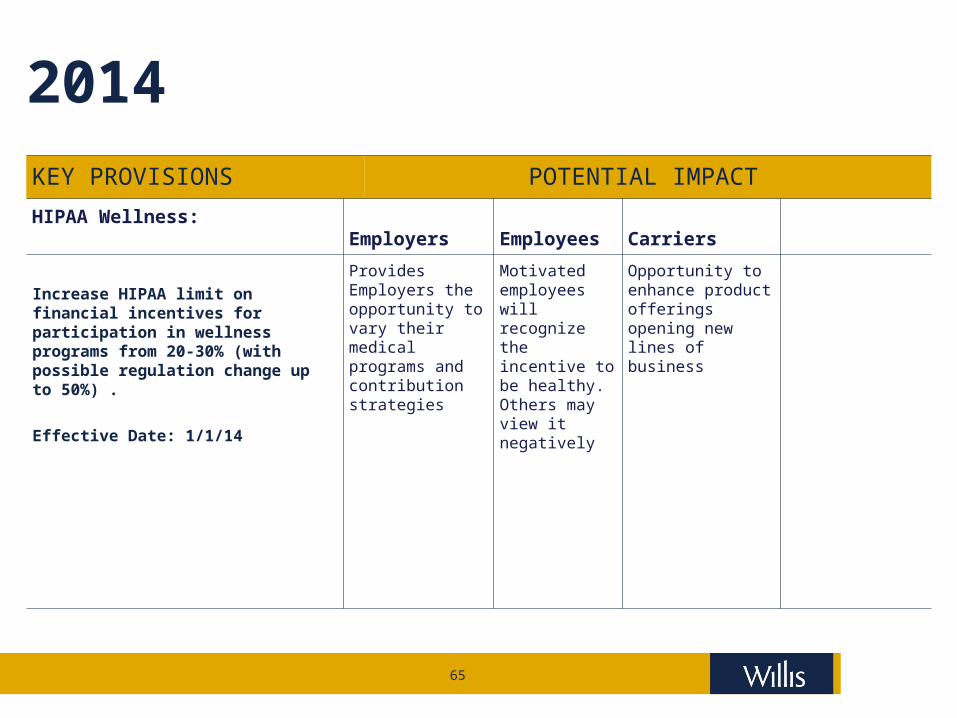

2014KEY PROVISIONS POTENTIAL IMPACT

HIPAA Wellness: Employers Employees Carriers

Increase HIPAA limit on financial incentives for participation in wellness programs from 20-30% (with possible regulation change up to 50%) .

Effective Date: 1/1/14

Provides Employers the opportunity to vary their medical programs and contribution strategies

Motivated employees will recognize the incentive to be healthy. Others may view it negatively

Opportunity to enhance product offerings opening new lines of business

66

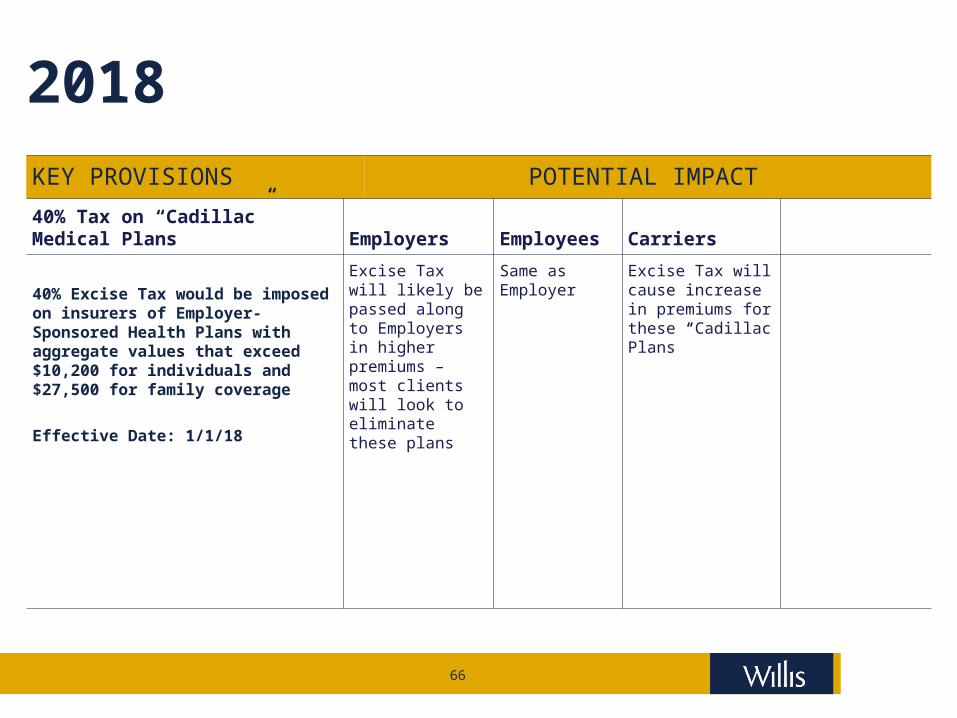

2018KEY PROVISIONS POTENTIAL IMPACT

40% Tax on “Cadillac” Medical Plans

Employers Employees Carriers

40% Excise Tax would be imposed on insurers of Employer-Sponsored Health Plans with aggregate values that exceed $10,200 for individuals and $27,500 for family coverage

Effective Date: 1/1/18

Excise Tax will likely be passed along to Employers in higher premiums – most clients will look to eliminate these plans

Same as Employer

Excise Tax will cause increase in premiums for these “Cadillac Plans”

67

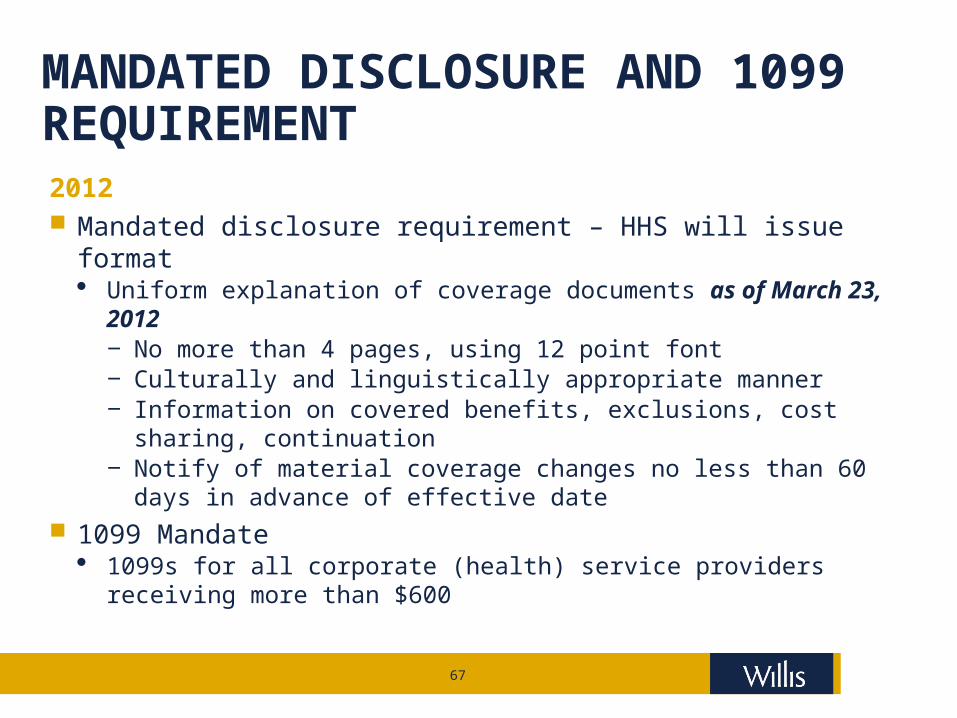

MANDATED DISCLOSURE AND 1099 REQUIREMENT2012 Mandated disclosure requirement – HHS will issue format

Uniform explanation of coverage documents as of March 23, 2012‒ No more than 4 pages, using 12 point font‒ Culturally and linguistically appropriate manner‒ Information on covered benefits, exclusions, cost sharing, continuation‒ Notify of material coverage changes no less than 60 days in advance of

effective date 1099 Mandate

1099s for all corporate (health) service providers receiving more than $600

68

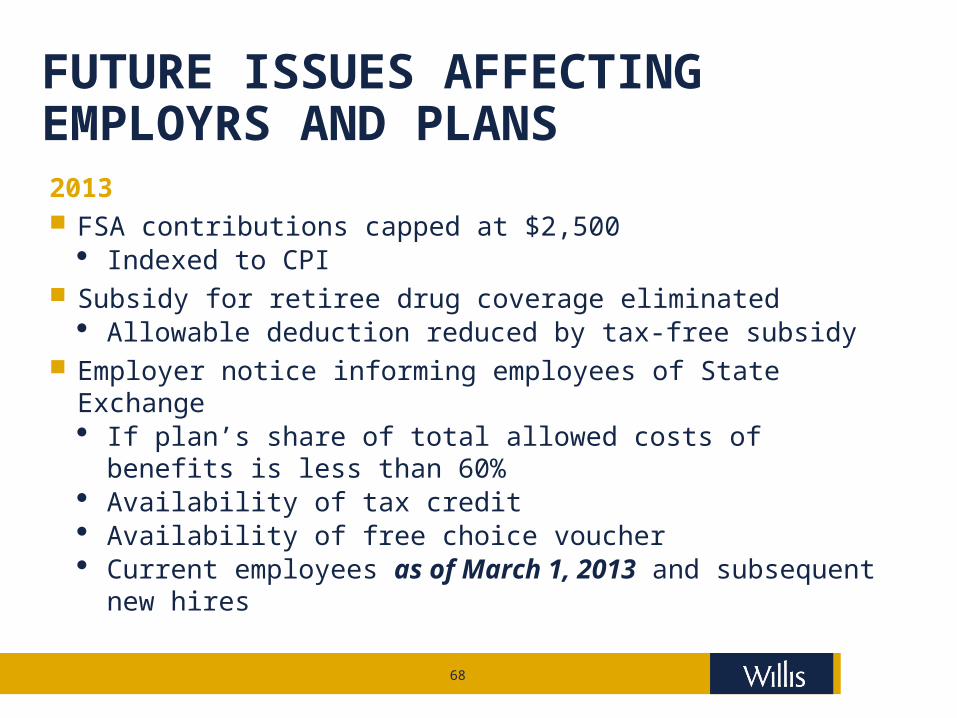

FUTURE ISSUES AFFECTING EMPLOYRS AND PLANS2013 FSA contributions capped at $2,500

Indexed to CPI Subsidy for retiree drug coverage eliminated

Allowable deduction reduced by tax-free subsidy Employer notice informing employees of State Exchange

If plan’s share of total allowed costs of benefits is less than 60% Availability of tax credit Availability of free choice voucher Current employees as of March 1, 2013 and subsequent new

hires

69

TAX CHANGES

2013 – Tax Changes Payroll tax increase

To .9% on earnings over $200,000 for individualsand joint filers over $250,000

Adds 3.8% tax on same individuals’ net investment income over $200,000/$250,000

‒ interest, dividends, royalties, rents, gross income from trade or business involving passive activities, and

net gain from disposition of property (other than property held in trade or business) - reduced by properly allocable deductions

Participant fee for comparative effectiveness research $1 per participant for first plan year ending after September 30, 2012 $2 per participant following year Not applicable to HIPAA exempt benefits Sunsets 1/1/2020

70

ADDITIONAL MANDATES

2014 Employer reports to IRS to enforce individual mandates

Coverage offered employees, length of waiting period, lowest cost option, actuarial value

Auto enrollment mandated for employer plans with 200 or more employees

Prohibits waiting periods greater than 90 days Wellness Programs will be able to increase incentives to 30% or up

to 50% if HHS approves

71

PAY OR PLAY MANDATE

Effective in 2014 Nondeductible penalty on some employer plans with 50 or more FT

(30 hours/week or more) employees Part time employee equivalents used to determine FT number First 30 FT employees excluded from tax Tax is $2,000 per FT employee if no coverage at all and at least

one employee receives tax credit for coverage on an exchange Tax is $3,000 per FT employee if employer DOES offer coverage

but employee receives tax credit for coverage on an exchange but no more than $2,000 X all employees

Seasonal employees are NOT excluded For the penalty, are to determine size of employer

72

VOUCHERS AND INDIVIDUAL MANDATEEffective in 2014 Vouchers

Employer must offer vouchers to permit certain employees‒ eligible under plan AND‒ required premium is between 8% and 9.8% of income AND‒ total household income does not exceed 400% of FPL

Voucher can be used to purchase coverage outside of employer plan and retain any excess tax free

Must equal the largest portion the employer provides toward type of coverage

No free rider penalty for employees receiving vouchers Individual mandate commences – fines for failure to purchase:

‒ $95 in 2014‒ $325 in 2015‒ $695 in 2016

Or‒ 1.0% of taxable income in 2014‒ 2.0% of taxable income in 2015‒ 2.5% of taxable income in 2016 and thereafter

73

INSURANCE REFORM MANDATESEffective in 2014 – Affects on all plans (grandfathered until

effective date) Mandated benefit package – determined by HHS Clinical trials for life threatening diseases (grandfathered plans

exempt) No discrimination of provider acting within scope of license No pre-existing condition exclusion No annual limits on essential benefits Cost sharing limitations-OOP does not exceed qualified HDHP coverage and deductibles do exceed $2,000/4,000 (grandfathered plans exempt) State insurance exchanges commence for individuals and small

businesses

74

INSURANCE EXCHANGES

Commence in 2017 State insurance exchanges commence for employers with more

than 100 employees

75

HIGH COST PLAN EXCISE TAX

Effective in 2018 Excise taxes on “Cadillac” plans

40% nondeductible tax Value of all employer – sponsored medical benefits in excess of:

‒ $10,200 for individual coverage‒ $27,500 for more than individual coverage

High risk occupations* and retirees‒ $11,850 individual‒ $30,950 more than individual

Indexed at CPI + 1% in 2019, CPI thereafter Active and retired employees

* Longshoremen, repair or install electrical or telecommunications lines, law enforcement, fire protection, EMT, construction, mining, agriculture (except not food processing), forestry and fishing

76

HIGH COST PLAN EXCISE TAX

2018 – Cadillac Plans – cont. Value includes

All medical coverage‒ Group medical‒ EAP‒ HSAs, FSAs, HRAs‒ Employer paid‒ Employee paid‒ Pre-tax‒ After-tax

Not disability or life

77

HIGH COST PLAN EXCISE TAX

Effective in 2018 – Cadillac Plans – cont. Excise tax on an individual basis

Threshold and tax calculated monthly Paid by the employer Based on COBRA determination amount Intent to keep employer plans under threshold so consider -

Reduce benefits? Reduce account based plans? Eliminate ancillary coverage?

78

QUESTIONS AND COMMENTS

Federal Healthcare Reform – What’s Next?Willis Human Capital PracticeLegislative and Regulatory Update

Jay M. Kirschbaum, JD, LLM, FLMIPractice LeaderNational Legal & Research Group

This material and any accompanying remarks are provided for informational purposes only and nothing contained in either should be taken as a legal opinion or as legal advice Copyright 2010 All rights reserved