fashion marketing and branding brand … singaporeans will demand less of sugary drinks and fast...

TRANSCRIPT

FASHION MARKETING AND BRANDING

Brand environment

Module: FASH10102

Batch: BFMD1 1202A

By: Chinmay Mahesh Daswani

FIN NO: G1181475T

Executive Summary

SmartWater is bottled water that is being introduced into the Singapore market. This is a premium nutrient enhanced brand from

the United States.

The Singapore bottled water market is analysed in order to identify competitors in the market and identify how SmartWater can be

positioned and communicated in the market effectively, to set it apart from its competitors. Smartwaters’ consumer profile is

identified and a market strategy is developed towards the target market. The marketing mix for SmartWater is developed

supported by a questionnaire survey carried out and secondary research.

Forecasted sales have been projected to identify the rate of the payback period.

1

CONTENTS PAGE

Introduction Page No 1.0 Purpose, Scope, Limitations ------------------------------------------------------------------------------------------------------ 5

1.1 Company background ------------------------------------------------------------------------------------------------------------------ 6

1.2 Rationale for choosing SmartWater nutrient enhanced water -------------------------------------------------------------- 6

Situation Analysis 2.0 Singapore drinks industry ------------------------------------------------------------------------------------------------------------8

2.1 Singapore soft drinks Segments --------------------------------------------------------------------------------------------------- 9

2.2 Singapore bottled water market ---------------------------------------------------------------------------------------------------10

2.3 Growth of the Singapore bottled water market ------------------------------------------------------------------------------- 11

2.4 SmartWater market in Singapore--------------------------------------------------------------------------------------------------12

2.5 Consumer trends ----------------------------------------------------------------------------------------------------------------------14

2.6 SmartWater SWOT analysis---------------------------------------------------------------------------------------------------------15

2.7 Singapore Pestle analysis------------------------------------------------------------------------------------------------------------16

2.8 Porters 5 forces model---------------------------------------------------------------------------------------------------------------19

2.9 Functional/Flavoured bottled water competitor analysis-------------------------------------------------------------------22

Market objectives

4.0 SmartWater Marketing objectives--------------------------------------------------------------------------------------------------25

4.1 Market Segmentation------------------------------------------------------------------------------------------------------------------26

4.2 Target segment --------------------------------------------------------------------------------------------------------------------------28

4.3 Target market-----------------------------------------------------------------------------------------------------------------------------30

4.4 Consumer profile-------------------------------------------------------------------------------------------------------------------------30

4.5 Market positioning-----------------------------------------------------------------------------------------------------------------------34

4.5 Perceptual mapping----------------------------------------------------------------------------------------------------------------------34

2

4.6 Competitor brand share--------------------------------------------------------------------------------------------------------------35

Marketing mix for Singapore market 5.0 Product----------------------------------------------------------------------------------------------------------------------------------37

5.1 Price--------------------------------------------------------------------------------------------------------------------------------------43

5.2 Place-------------------------------------------------------------------------------------------------------------------------------------47

5.3 Promotion------------------------------------------------------------------------------------------------------------------------------49

Budgeting & Forecasts 6.0 Sales forecast--------------------------------------------------------------------------------------------------------------------------- 59

Marketing mix summary 7.0 SmartWater marketing mix summary----------------------------------------------------------------------------------------------64

References---------------------------------------------------------------------------------------------------------------------------------------69

List of exhibits-----------------------------------------------------------------------------------------------------------------------------------68

Appendix------------------------------------------------------------------------------------------------------------------------------------------69

3

4

Introduction

1.0 Purpose, Scope, Limitations

A) Purpose

Introducing a new bottled water in Singapore.

B) Scope

This report encompasses this chosen bottle water and rational for the introduction of the brand. An analysis of the bottle water market

in Singapore and the chosen brands’ potential market. Competitors and gaps in the market are identified. Marketing objectives and

targets for the brand are set. Further, the marketing mix for the brand will be discussed as well as a sales forecast.

C) Limitations

Research for this report was obtained through a questionnaire survey, online databases, news articles and reports

5

1.1 Company Background:

Smart water is premium bottled water (non-carbonated) owned by Glaceau, which also produces VitaminWater and FruitWater. SmartWater is vapour distilled electrolyte-

enhanced water, which offers a flavourless, calorie free option to water drinkers.

Glaceau was founded by J. Darius Bikoff under the name Energy Brands Inc in 1996 in Whitestone, New York. Energy brands sourced from the glacial aquifers in Litchfield

County, Connecticut and established an extremely advanced vapour distillation process. It offers superior purity using a heating process which extracts extra molecules and

particles. After this process, the water is then enhanced with electrolytes; magnesium, potassium and calcium to increase hydration in the body. In 2007, Glaceau was

acquired by coca-cola Inc., but it remains a virtually independent brand under the name.

1.2 Rationale for introducing SmartWater – nutrient enhanced water

SmartWater fills the gap in the market for beverages which provide health benefits and hydration.

SmartWater can be consumed as drinking water or a sports beverage.

Singaporeans are becoming increasingly health conscious consumers; 57% (Neilson, 2010) of Singaporeans consider themselves on the heavier side. Also majority

of the 57% would change their diet (75%) or exercise (66%) to achieve their goal.

Slowdown in sales of carbonated sodas. Consumers are turning to drinks to provide additional health benefits, extra energy to help them improve physical

performance during sport and recovery after exercise. Sports drink consumption (litres) is forecasted to grow by 25.6% from 2012 - 2016.

SmartWater will be the only enhanced water in the market which is healthy( sugar-free, Calorie-free) which will appeal to health conscious consumers

VitaminWater assists in promotion; VitaminWater also produced by Glaceau has been well established in the market since 2010. This will assist in promotion.

Consumers are likely to purchase SmartWater, because of consumer’s familiarity with VitaminWater/Zero.

6

7

Situation Analysis

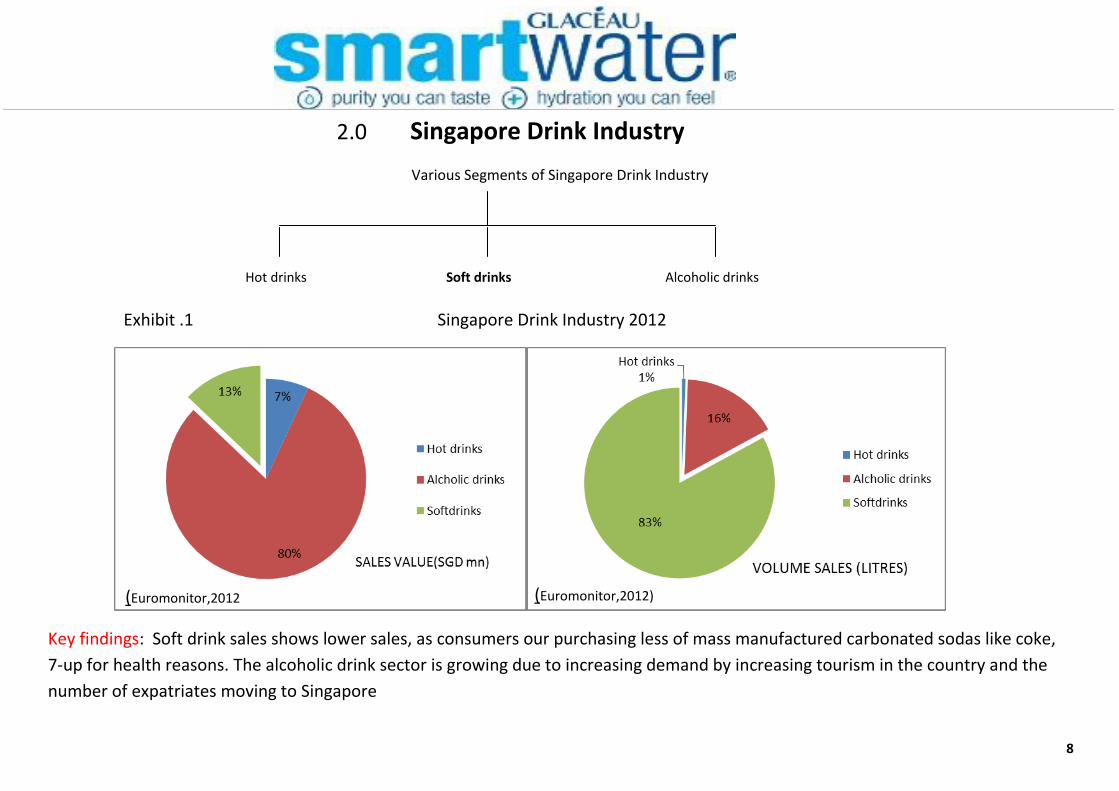

2.0 Singapore Drink Industry

Various Segments of Singapore Drink Industry

Exhibit .1 Singapore Drink Industry 2012

Key findings: Soft drink sales shows lower sales, as consumers our purchasing less of mass manufactured carbonated sodas like coke,

7-up for health reasons. The alcoholic drink sector is growing due to increasing demand by increasing tourism in the country and the

number of expatriates moving to Singapore

Hot drinks Soft drinks Alcoholic drinks

8

(Euromonitor,2012

)

(Euromonitor,2012)

2.1 Singapore soft drink segments

Soft drinks

Carbonates Concentrates Fruit/vegetable

juices

Bottled

water Sports/energy

drinks

Asian speciality

drinks

RTD coffee RTD Tea

Carbonated

water

Brands:

-Perrier

-San Pellegrino

-Spritzer

(sparkling)

-No Frills

Flavoured/Functional

water Still bottled water

Brands:

-H-two-o

-100Plus

-VitaminWater

-pocari sweat

-Gatorade

-Pink dolphin

Brands:

--F&N ice mountain

-Aqua

-Evian

-Volvic

-Fair Price

-Dasani

-First Choice

-Aquarin

-Carrefour

-Spritzer (still)

9

2.2 Singapore Bottled Water Market (2011)

Exhibit. 2

(Source: Euromonitor, 2012)

Key findings:

- Still bottled water holds the highest value in sales and volume due to its low prices in the market and because it is considered a

basic product in Singapore.

- Carbonated Water is experiencing the lowest value in sales and volume because brands like Perrier, san Pellegrino and spritzer

are popular as mixers and not for basic consumption in the Singapore market.

10

2.3 Growth of the Singapore bottled water market

Exhibit. 3

(Source: Euromonitor, 2012)

Key findings:

-Flavoured and functional bottled water shows strong growth in the market. This is due to rising health consciousness among Singaporeans who are now

demanding healthier drinks with additional health benefits.

- Many Singaporeans also see sports drinks as an alternative to bottled water because it also rehydrates. It is also perceived to be equally healthy to bottled

water.

- Sports drinks are also being consumed throughout the day, which also accounts for the functional/flavoured bottled water growth

4% growth

11

2.4 The SmartWater market in Singapore

Functional Bottled Water

‘The Booming Market’

- SmartWater operates in the functional bottled water market because of the electrolyte enhancement of SmartWater (calcium,

potassium, magnesium)

- Functional water can be defined as water-based beverages where various fruit/ herbal concentrates and minerals are added to

water for nutrient value. These consist of sports drinks and flavoured water.

Exhibit.4

12

Source (Euromonitor, 2012)

Key findings: - The functional bottled water market is showing strong growth rates during the forecast period.

- The growth is accounted for by the on-going rising demand for sports drinks like 100Plus and H-Two-O due to rising health conscious consumers (57%

health conscious Singaporeans, neilson,2010) and because it’s considered healthy in Singapore and an alternative to bottled water.

- The market for such products in Singapore is considered the biggest threat to the growth of the bottled water market.

13

2.5 Consumer trends

A high percentage of the population are taking an interest in their health.

Exhibit.5

Source: Ac Nielsen CATI Omnibus

-

Key findings

- There is a higher percentage of people

that watch their health then people

that don’t in Singapore.

- The youth have started taking their

health seriously at an early age.

- This implies that Singapore will have a

healthy population and increased life

span.

- Singaporeans will demand less of

sugary drinks and fast food which are

the key reasons for obesity in the

country.

- Singaporeans will increase their

demand for bottled water for a healthy

option for hydration.

14

• Family brand, VitaminWater by Glaceau helps to

promote SmartWater

• Vapour distilled with electrolytes (calcium, potassium

and magnesium)

• Its sugar-free , no calories, carbohydrates or sodium

• Hydrates the body faster than regular water

• Famous within the United States, consumed by many

celebrities

• Potential competition with family brand vitamin water.

• Possible cannibalism effect

• Flavourless

• Lack knowledge on the benefits of SmartWater(vapour distilled

,electrolytes)

• People may not want their water enhanced.

• Company is more focused on VitaminWater

Current trend in health conscious consumers

Health benefits of SmartWater

Expanding into different geographical markets

Mature market(competition)

• High-end bottled water

• Tap water

• Increasing number of substitute products

trengths eakness

pportunties

2.6 SmartWater SWOT analysis

hreats

15

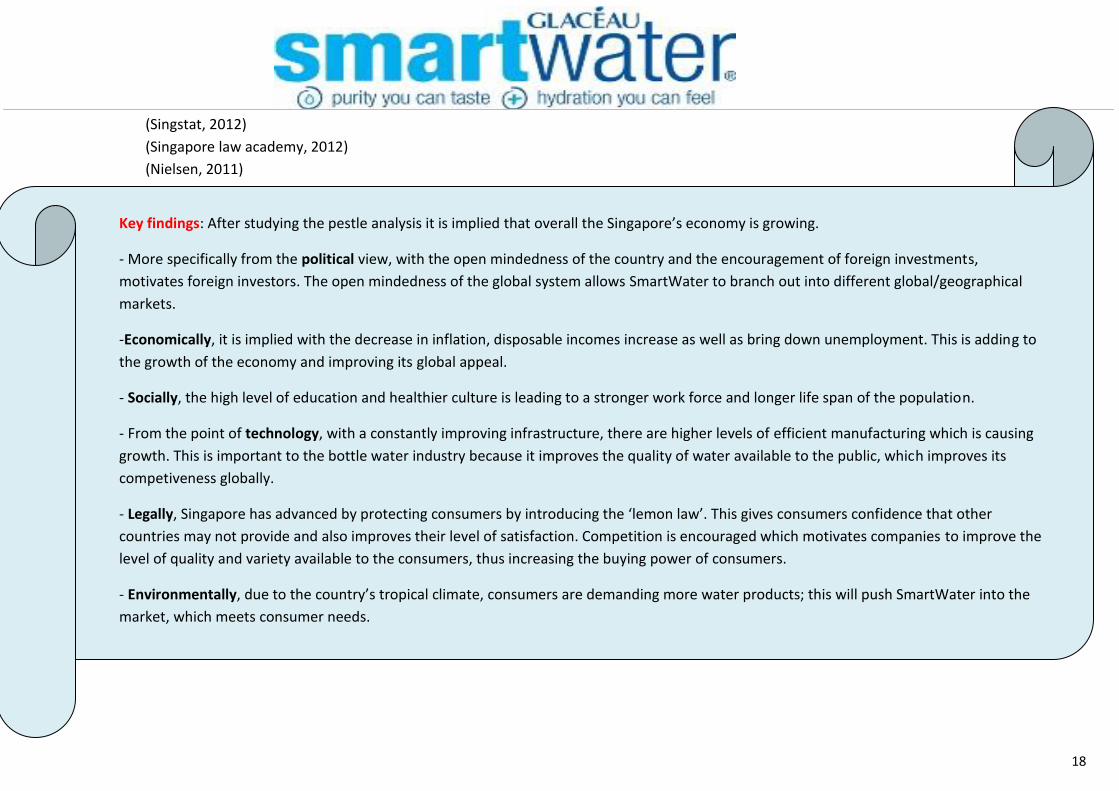

2.7 Singapore pestle analysis for SmartWater

Political sound water policies

Government encouraging foreign investments.

The termination of the franchise agreement between Coca-Cola an F&N ltd has created intense competition between the two

companies

Economic Inflation 3.6 %( 2012) has decreased in comparison to 5.7% in 2011. This decrease in inflation rate leads to the average household

having more income thus having a higher disposable income leading them to spend more on products such as SmartWater

Economy grew by 1.5% in 2012 and is forecasted to expand by 1% to 3% in 2013. Since the economy is forecasted to grow, this would

mean that there would be an increase in jobs bringing down unemployment rate. Thus, increasing the incomes for the average

household and in turn increasing the disposable income that each individual owns. With a higher disposable income, individuals would

be able to spend more on non-essential goods such as SmartWater.

Singapore food & drink business environment rating- Singapore was ranked 4th in the BMI’s reward/risk ratings for Asia-Pacific. Its

growth outlook is fairly uninspiring, reflected by a overall low reward score of 38.7

Singapore enjoys high existing food and drink consumption level; but the developed and mature market suggests limited scope for

growth in the future.

Presence of strong incumbents such as Fraser and Neave and YEN, competitors to Cocoa-Cola.co owners of Glaceau.

Singapore has the benefit of a conducive business environment, which will continue to bolster its overall investment appeal to foreign

consumer goods investors

Social

Social

Spending power by Singaporeans is not expected to slow down in the upcoming year supported by a falling unemployment rate and a

generally high GDP per capital in Singapore of 33529.83 US dollars.

Singaporeans are highly educated with a literacy rate of 96% - Consumers are aware of health hazards caused by various consumer

products.

16

Singaporeans becoming health conscious (57%) - watching their diet and becoming increasingly physically active. Demand for sport

drinks and bottled water rising, while consumers are cutting down on their consumption of sodas.

Singaporeans are increasingly spending their leisure time exercising.

Technological Advanced technological infrastructure

Technology as a key driver, there’s strong growth in Singapore’s water industry. Quality of tap water provided to homes improve,

increasing its competitiveness in the drink industry

- -Gov’t bodies (PUB) research & innovation in water technology to improve water industry.

- -S$470 million by the National Research Foundation to fund water research by public and private sectors.

Highest level of internet penetration in Southeast Asia

-85% of digital consumers in Singapore own an internet-capable mobile phone.

-Internet advertising will be an effective way to create awareness of SmartWater in Singapore.

• As technology increases, the machinery and tools used in manufacturing and production of goods are advanced as well. Therefore,

the production of SmartWater would become more efficient and move at a quicker pace.

Legal A new law passed in September 2012 ‘Lemon Law’ which protects consumers from defective products or products of unsatisfactory or

performance standards. This allows consumers to get refunds on products and allows businesses to alter their product.

- SmartWater should not mislead consumers. Otherwise this could affect brand image and increase their cost.

The presence of competition in Singapore is encouraged by laws which prevent mergers, selling prices etc. that could dampen

competition. SmartWater has many competitors in Singapore and consequences of infringement of competition laws leads to financial

penalty (10%) of the turnover of the business for 3 years. Affected parties also have the right of action.

Environmental Tropical climate in Singapore creates demand by consumers for beverages that improve hydration

Waste management is an issue in Singapore (7,600 tonnes of waste collected a day) Use of recyclable material is encouraged.

Main Sources: (Trading economics, 2012 cited in ministry of manpower, trade& industry, environment and waste collection, 2012)

17

(Singstat, 2012)

(Singapore law academy, 2012)

(Nielsen, 2011)

Key findings: After studying the pestle analysis it is implied that overall the Singapore’s economy is growing.

- More specifically from the political view, with the open mindedness of the country and the encouragement of foreign investments,

motivates foreign investors. The open mindedness of the global system allows SmartWater to branch out into different global/geographical

markets.

-Economically, it is implied with the decrease in inflation, disposable incomes increase as well as bring down unemployment. This is adding to

the growth of the economy and improving its global appeal.

- Socially, the high level of education and healthier culture is leading to a stronger work force and longer life span of the population.

- From the point of technology, with a constantly improving infrastructure, there are higher levels of efficient manufacturing which is causing

growth. This is important to the bottle water industry because it improves the quality of water available to the public, which improves its

competiveness globally.

- Legally, Singapore has advanced by protecting consumers by introducing the ‘lemon law’. This gives consumers confidence that other

countries may not provide and also improves their level of satisfaction. Competition is encouraged which motivates companies to improve the

level of quality and variety available to the consumers, thus increasing the buying power of consumers.

- Environmentally, due to the country’s tropical climate, consumers are demanding more water products; this will push SmartWater into the

market, which meets consumer needs.

18

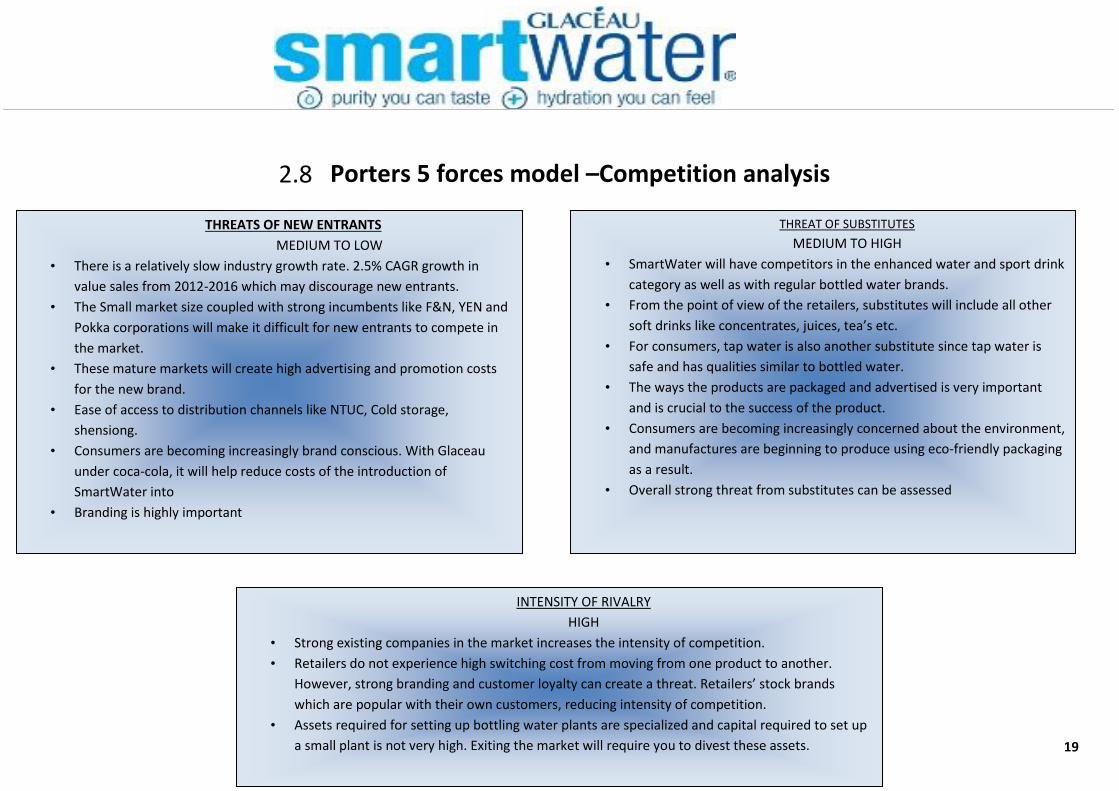

2.8

THREATS OF NEW ENTRANTS

MEDIUM TO LOW

• There is a relatively slow industry growth rate. 2.5% CAGR growth in

value sales from 2012-2016 which may discourage new entrants.

• The Small market size coupled with strong incumbents like F&N, YEN and

Pokka corporations will make it difficult for new entrants to compete in

the market.

• These mature markets will create high advertising and promotion costs

for the new brand.

• Ease of access to distribution channels like NTUC, Cold storage,

shensiong.

• Consumers are becoming increasingly brand conscious. With Glaceau

under coca-cola, it will help reduce costs of the introduction of

SmartWater into

• Branding is highly important

THREAT OF SUBSTITUTES

MEDIUM TO HIGH

• SmartWater will have competitors in the enhanced water and sport drink

category as well as with regular bottled water brands.

• From the point of view of the retailers, substitutes will include all other

soft drinks like concentrates, juices, tea’s etc.

• For consumers, tap water is also another substitute since tap water is

safe and has qualities similar to bottled water.

• The ways the products are packaged and advertised is very important

and is crucial to the success of the product.

• Consumers are becoming increasingly concerned about the environment,

and manufactures are beginning to produce using eco-friendly packaging

as a result.

• Overall strong threat from substitutes can be assessed

INTENSITY OF RIVALRY

HIGH

• Strong existing companies in the market increases the intensity of competition.

• Retailers do not experience high switching cost from moving from one product to another.

However, strong branding and customer loyalty can create a threat. Retailers’ stock brands

which are popular with their own customers, reducing intensity of competition.

• Assets required for setting up bottling water plants are specialized and capital required to set up

a small plant is not very high. Exiting the market will require you to divest these assets.

Porters 5 forces model –Competition analysis

19

BARGAINING POWER OF SUPPLIERS

MEDIUM - HIGH PRESSURE

• Spring water and mineral water must come from a specific underground

source and be bottled at the source. For companies, it’s important to

access land that has an aquifer suitable for exploitation

• Switching costs in both cases are high. It’s difficult for the customers to opt

for an alternative water utility and for companies relying on underground

sources

• Substitute input. Supplier power is increased due to limited substitutes.

The quality of inputs is also important, because they must meet specific

criteria’s. Sources of water are limited and are costly.

• As natural resources become more and more scarce, the power of water

suppliers are ever increasing. Strong relationships are needed with water

suppliers to ensure a continuous supply of water to the bottling companies.

• Suppliers of plastic and other chemical inputs rely on these companies for

their livelihood.

• Overall Supplier power can be assessed as moderate. This makes the

industry fairly attractive for new entrants.

BARGAINING POWER OF BUYERS

MEDUIM/HIGH

• Some of the main buyers in the market are retail chains. With 57% of

consumers changing towards healthier lifestyles, the competitors are

looking for ways to differentiate their products in line with current

consumer trends (healthy).

• With branding being an important factor for the end-users, retailers

stock brands that are popular with their customers. This weakens

their buyer power.

• Bottled water manufactures and these retailers are different

businesses together so it’s unlikely for vertical integration to occur.

• The bottled water sales are just a sub-segment of the soft drink

market. This reduces the importance to retailers who also sell a wide

variety of drinks. This strengthens the buyer power slightly.

• In the end, it is the consumer and final buyer of the product that

determines its success. Therefore, it is essential to understand the

changing preferences and wants of the buyers in order to keep them

satisfied.

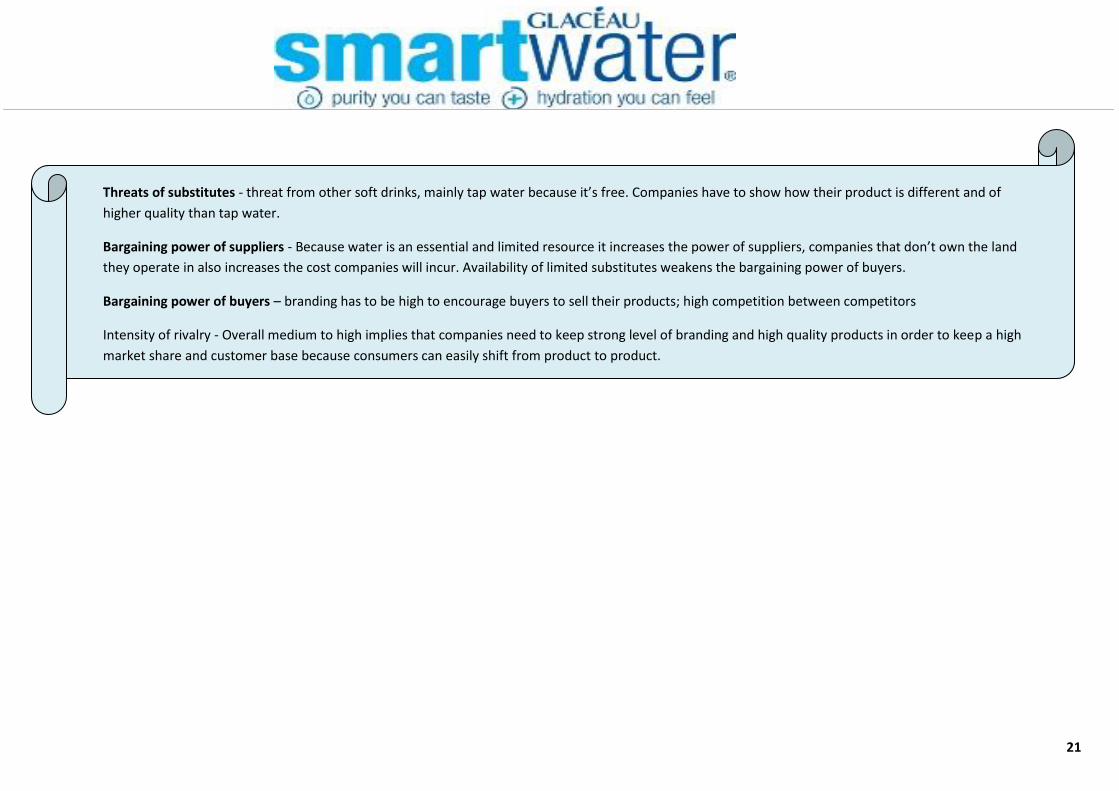

Key findings: Overall this model implies that SmartWater in the industry will have medium pressure from all sides, due to competition encouraged, thus there will

always be risk taking.

Threat of entrants – This biggest barrier to entry is the current existence of strong brands in the marketplace. So when entering the marketplace, Coco-cola should

establish SmartWater as a product with a strong brand name and try to grab as much market share as possible. Retailers also have to be convinced of the strength

of the new brand before allocating space to it. It’s the strength of the brand that creates high barriers to entry for future companies.

20

Threats of substitutes - threat from other soft drinks, mainly tap water because it’s free. Companies have to show how their product is different and of

higher quality than tap water.

Bargaining power of suppliers - Because water is an essential and limited resource it increases the power of suppliers, companies that don’t own the land

they operate in also increases the cost companies will incur. Availability of limited substitutes weakens the bargaining power of buyers.

Bargaining power of buyers – branding has to be high to encourage buyers to sell their products; high competition between competitors

Intensity of rivalry - Overall medium to high implies that companies need to keep strong level of branding and high quality products in order to keep a high

market share and customer base because consumers can easily shift from product to product.

21

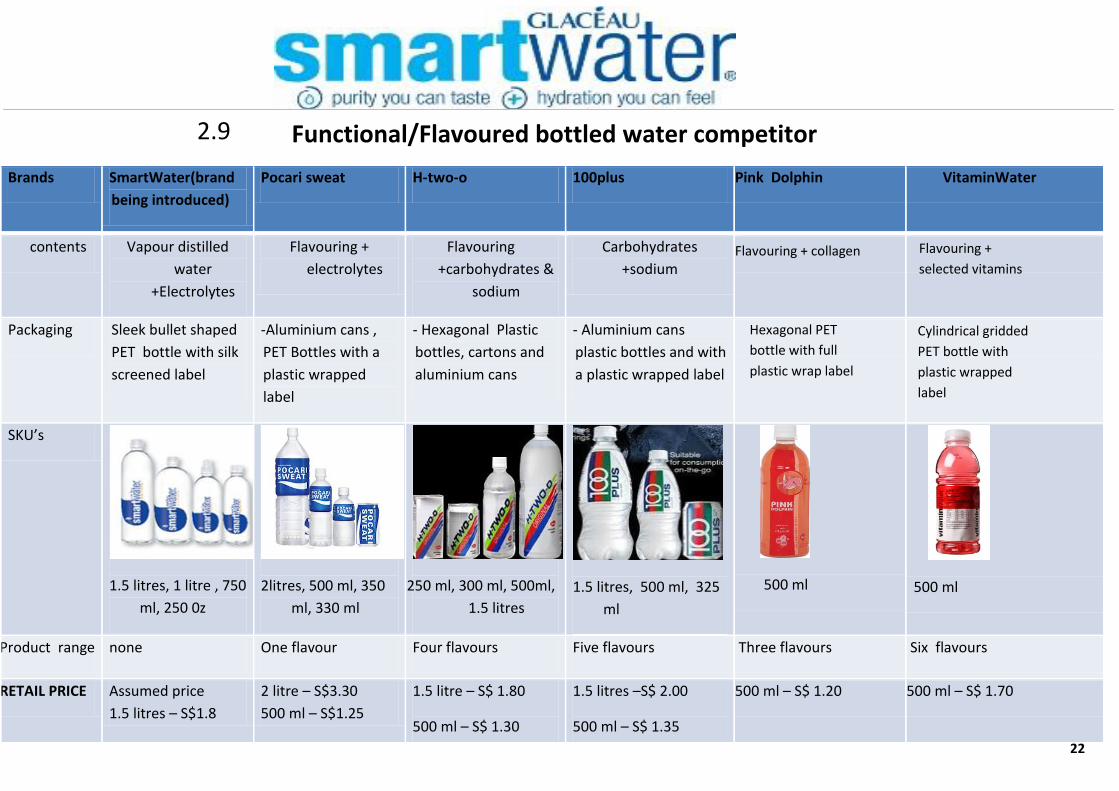

2.9

Brands SmartWater(brand

being introduced)

Pocari sweat H-two-o 100plus Pink Dolphin VitaminWater

contents Vapour distilled

water

+Electrolytes

Flavouring +

electrolytes

Flavouring

+carbohydrates &

sodium

Carbohydrates

+sodium

Packaging Sleek bullet shaped

PET bottle with silk

screened label

-Aluminium cans ,

PET Bottles with a

plastic wrapped

label

- Hexagonal Plastic

bottles, cartons and

aluminium cans

- Aluminium cans

plastic bottles and with

a plastic wrapped label

SKU’s

1.5 litres, 1 litre , 750

ml, 250 0z

2litres, 500 ml, 350

ml, 330 ml

250 ml, 300 ml, 500ml,

1.5 litres

1.5 litres, 500 ml, 325

ml

500 ml

500 ml

Product range none One flavour Four flavours Five flavours Three flavours Six flavours

RETAIL PRICE Assumed price

1.5 litres – S$1.8

2 litre – S$3.30

500 ml – S$1.25

1.5 litre – S$ 1.80

500 ml – S$ 1.30

1.5 litres –S$ 2.00

500 ml – S$ 1.35

500 ml – S$ 1.20 500 ml – S$ 1.70

Flavouring + collagen Flavouring +

selected vitamins

Hexagonal PET

bottle with full

plastic wrap label

Cylindrical gridded

PET bottle with

plastic wrapped

label

Functional/Flavoured bottled water competitor

analysis

22

1 litres - S$1.6

750 ml – S$1.4

25 oz – S$ 1.2

350 ml – S$0.95

330 ml(can) – S$1.05

250 ml - 325 ml – S$ 1.50

TARGET

MARKET

Health conscious con-

sumers /Active

lifestyle

Physically

active/athletes.

Physically

active/Athletes

Physically

active/Athletes

Health conscious

consumers

Consumers looking for

more than just regular

water

BRAND’S

KEY

MESSAGE

A beverage for your

workout to your

night out( brains

perform best when

hydrated)

- A health drink that

aptly replaces

minerals and fluids

lost through physical

activities at work,

sport or at

home(http://www.po

carisweat.com.ph/)

- Your perfect

buddy to complement

your active lifestyle to

combat dehydration

and power up your

performance for

optimal results!

(http://www.yeos.com.

sg/h-two-

o/original/Refuel_With_

H-TWO-O_Original.php)

)

Isotonic, thirst

quenching drink

formulated to restore

what the body loses

during physical

exertion and to help

achieve optimum

hydration and

electrolyte balance

(http://www.100plus.co.z

a/site/home)

An invigorating light

fruity peach- flavoured

drink jazzed up with

vitamins, perfect for the

chic& confident who

takes pride in their health

and body

(http://www.yeos.com.sg/p

inkdolphin/products.php)

Hydration for every

occasion

(http://www.coca-

cola.com.sg/bevera

ge_benefits/vitami

nwater.asp)

Key findings: Competition is intense due to similar pricing and similar target consumers. This generally shows low profits due to competitor price cuts in

order to capture sales from competitors. Similarity within the existing competitors gives way for new entrants to enter and tap into potential areas which

have not been targeted.

Strongest players identified are H-TWO-O and 100Plus

23

Market Objectives

24

4.0 SmartWater marketing objectives

Marketing Tactics: Gain strong alliance

with retailers (buyers) to boost brand

awareness.

25

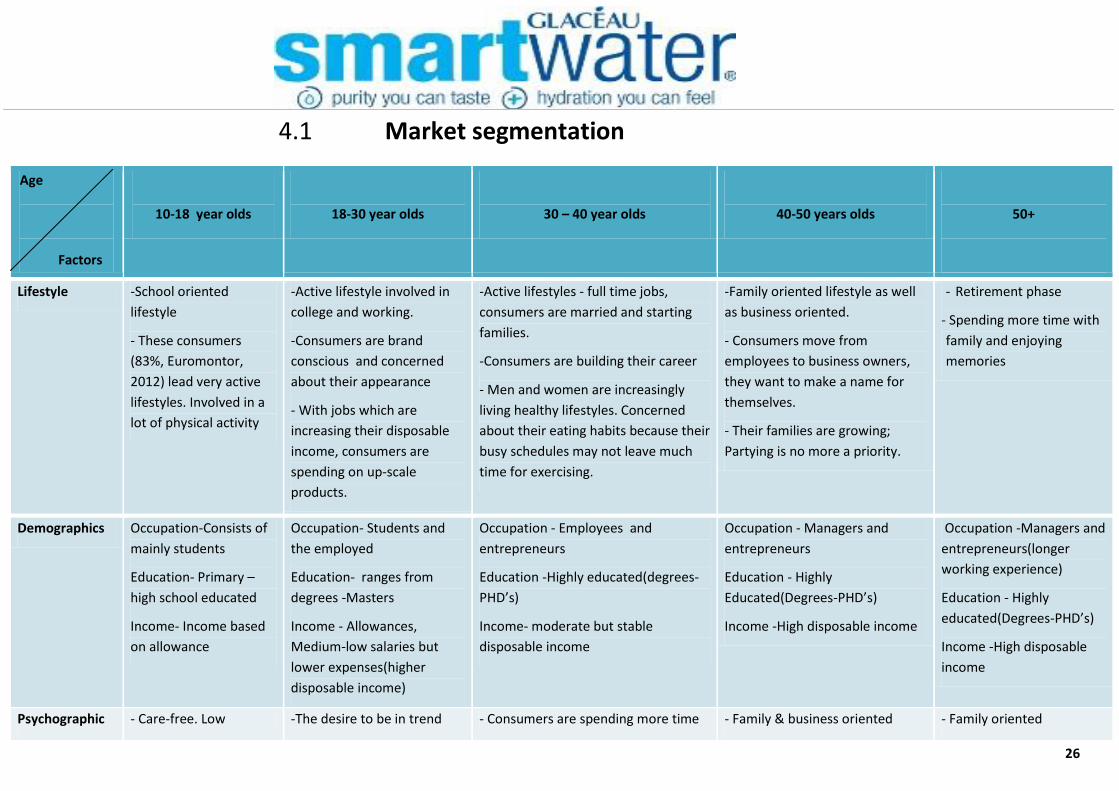

4.1 Market segmentation

Age

10-18 year olds

18-30 year olds

30 – 40 year olds

40-50 years olds

50+

Lifestyle -School oriented

lifestyle

- These consumers

(83%, Euromontor,

2012) lead very active

lifestyles. Involved in a

lot of physical activity

-Active lifestyle involved in

college and working.

-Consumers are brand

conscious and concerned

about their appearance

- With jobs which are

increasing their disposable

income, consumers are

spending on up-scale

products.

-Active lifestyles - full time jobs,

consumers are married and starting

families.

-Consumers are building their career

- Men and women are increasingly

living healthy lifestyles. Concerned

about their eating habits because their

busy schedules may not leave much

time for exercising.

-Family oriented lifestyle as well

as business oriented.

- Consumers move from

employees to business owners,

they want to make a name for

themselves.

- Their families are growing;

Partying is no more a priority.

- Retirement phase

- - Spending more time with

family and enjoying

memories

Demographics Occupation-Consists of

mainly students

Education- Primary –

high school educated

Income- Income based

on allowance

Occupation- Students and

the employed

Education- ranges from

degrees -Masters

Income - Allowances,

Medium-low salaries but

lower expenses(higher

disposable income)

Occupation - Employees and

entrepreneurs

Education -Highly educated(degrees-

PHD’s)

Income- moderate but stable

disposable income

Occupation - Managers and

entrepreneurs

Education - Highly

Educated(Degrees-PHD’s)

Income -High disposable income

Occupation -Managers and

entrepreneurs(longer

working experience)

Education - Highly

educated(Degrees-PHD’s)

Income -High disposable

income

Psychographic - Care-free. Low -The desire to be in trend - Consumers are spending more time - Family & business oriented - Family oriented

Factors

26

concern about health

issues

and brand conscious

-Fewer obligations

-Consumers are concerned

about keeping their bodies

fit(watch their diet)

with their family

-higher obligations

-Consumers are exercising more and

eating healthy

-Consumers are concerned about

saving for their family

-Consumers are exercising to

control their weight and cutting

down on salty and fatty foods

-Increasing savings for

retirement

- Consumers are aware of

health hazards they are

prone to at this age.

Consumers are cutting

alcohol intake and

watching their diet.

Behavioural -Consumers at this age

prefer sweet

products(sodas)

- consumers like to try

different products

-Low brand loyalty

- Consumers are highly

influenced by brand image

- Consumers are looking for

healthy beverages to keep

them alert & hydrated

throughout the day

-Brand loyalty towards

brands in trend

-Consumers are influenced by

branding

- Consumers are willing to spend more

on healthier and organic products.

- Consumers look at products for

hydration during and after exercising

- Consumers pick products which are

low-fat and low in sugar content

- High brand loyalty

- Consumers are spending less on

non-essentials

- Consumers look for healthy

foods which have health benefits

- Consumers most likely will seek

tap water for hydration

-Brand loyalty is moderate

- Consumers spend mostly

on essentials

- Consumers stick to

products that have less

sugar and low calories.

- Consumers prefer

products they are familiar

with

-High brand loyalty.

(Kotler, 2010, pg.217)

Sources: Euromonitor. 2012. Consumer Lifestyle. [ONLINE] Available at: http://www.euromonitor.com/consumer-lifestyles-in-singapore/report. [Accessed 14 January 13].

27

4.2 Targeted Segment

2 sub-groups of the market will be targeted, because of similar characteristics present in each of these segments. Consumers are health conscious and are

constantly on-the-go. Consumers are able to spend extra on a beverage which will suit their healthy lifestyle and at the same time keep they hydrated for

their days’ activity.

Age

Factors

18-30 year olds 30 – 40 year olds

Lifestyle -Active lifestyle involved in college and working.

-Consumers are brand conscious and concerned about their

appearance

- With jobs which are increasing their disposable income,

consumers are spending on up-scale products.

-Active lifestyles - full time jobs, consumers are married and starting families.

-Consumers are building their career

- Men and women are increasingly living healthy lifestyles. Concerned about their

eating habits because their busy schedules may not leave much time for exercising.

Demographics Occupation- Students and the employed

Education- ranges from degrees -Masters

Income - Allowances, Medium-low salaries but lower

expenses(higher disposable income)

Occupation - Employees and entrepreneurs

Education -Highly educated(degrees-PHD’s)

Income- moderate but stable disposable income

Psychographic -The desire to be in trend and brand conscious

-Fewer obligations

-Consumers are concerned about keeping their bodies fit(watch

their diet)

- Consumers are spending more time with their family

-higher obligations

-Consumers are exercising more and eating healthy

Behavioural - Consumers are highly influenced by brand image

- Consumers are looking for healthy beverages to keep them alert &

-Consumers are influenced by branding

- Consumers are willing to spend more on healthier and organic products.

28

hydrated throughout the day

-Brand loyalty towards brands in trend

- Consumers look at products for hydration during and after exercising

- Consumers pick products which are low-fat and low in sugar content - High brand

loyalty

29

4.3 Target Market

The defined target market is the young active men and women with disposable incomes. With many competitors in the industry,

making it harder to market new products, the audience here is looking for more than plain water which matches SmartWater’s

selling proposition. Our target audience would fall in the 18-40 year-old range. Young people have more disposable income and

are more susceptible to branding and peer influence. The older target groups will not be targeted because they are more

concerned with saving money. The aim is to target consumers concerned about a healthy lifestyle.

4.5 Consumer profile

Age -18-40 year olds- This age group consists of the active population from students to working men and women as well

as young active housewives. The youthful population are prone to spending and are more influential.

Income 90% (sing stats) of the Singaporean population engages in full time employment. Majority of this portion consists of

the youthful population. Consumers in this category have disposable income and are willing to spend(less

concerned about saving); Consumers are influenced by trends and brands in this category which will increase their

willingness to spend on non-essentials.

lifestyle Consumers are health conscious, make an effort to watch their diet and exercise. Consumers are constantly on the

move and are interested in beverages that can keep them hydrated and refreshed throughout the day.

Occupation Consumers are active students and full time employees who need a perfect solution to keep them going throughout

the day.

Education Consumers are at least high school graduates. Consumers are aware and educated about our environment,

common health hazards and are knowledgeable on the benefits of electrolytes.

30

31

Consumer Profile Mood board

32

Exhibit .6 Target consumers - Brand awareness

18- 30 year olds 30 -40 year olds

Total target consumer Population(persons) 820,000 (singstat,2012) 620,000 (Singstat, 2012)

1st year Targeted brand awareness 20% of population 20% of population

2nd year Targeted brand awareness 30% of population 30% of population

3rd year Targeted brand awareness 45% of population 45% of population

Target unit purchases

Forecasted period

Population

18- 30 year olds

820,000(Singstat, 2012)

30 – 40 year olds

620,000 (Singstat, 2012)

1st year Total targeted brand awareness(of

population)

164000 persons 124000 persons

1st year estimated consumer purchase 10% of target population 10% of target population

1st year total estimated purchase

units

40,000 units 40,000 units

2nd year Total targeted brand awareness( of

population)

246,000 (persons) 186,000 (persons)

2nd year estimated consumer

purchase

25% of target population 25% of target population

Exhibit.7

33

2nd year total estimated purchase units 56,000 units 56,000 units

3rd year total targeted brand awareness(of

population)

369,000 (persons) 279,000 ( persons)

3rd year total estimated consumer

purchase

40% of target population 40% of target population

3rd year estimated purchase units 84,000 units 84,000 units

33

4.5 Market Positioning

The product will be seen as vapour distilled water with an edge. The product will be marketed as calorie-free enhanced water which provides quick

hydration throughout the day. The product will operate in the functional/flavoured bottled water market and compete with strong local brands such

as 100plus, h-two-o, pink dolphin and family brand VitaminWater.

Positioning statement: To the young and active, who need to stay hydrated throughout the day. SmartWater provides you vapour-distilled water

with an edge. Magnesium, potassium and calcium to hydrate you from your workout to your night out, without worrying about sugars or calories

4.5 Competitor Perceptual Mapping

Exhibit.8

34

Key findings: The market for enhanced water without flavouring/ sweeteners hasn’t been exploited yet in Singapore. SmartWater will have to be clearly

differentiated from other enhanced beverages in the market to set it apart. Strongest Competitors in the market are 100 plus and H-Two-o through their

strong branding positioning. A Luxury thirst quencher which is unflavoured /un-sweetened will suit consumers who are looking for more than just plain

water. They are constantly on the move and need an efficient hydrator. Such consumers are health conscious and are particular about what they consume.

4.6 Competitors brand share

Exhibit.9

Bottled water market(2011) Market Value S$ ‘000

37,898 (100%)

Functional/Flavoured bottled

water(2011)

S$ 6990 (18%)

Strongest Players % market value

100PLUS brand share 49%

H-TWO-O brand share 11%

SmartWater aims to capture 1.5% of the flavoured/ functional bottle water market value in its first year of operation. With strong

brand positioning of the brand, setting it apart from its competitors, it sets to capture 4% of brand share from its two strongest

competitors in the next 3 years.

35

SmartWater Marketing Mix for the Singapore market

36

5.0 SmartWater Marketing Mix: Product

- Glaceau SmartWater electrolyte enhanced water will be introduced into the functional/flavoured bottled water market in

Singapore.

- SmartWater will be targeted at consumers who need a beverage to keep them hydrated during exercise and active throughout

the day.

- SmartWater will be introduced in four different sizes.

1. 1.5 litres

2. 1 litre

3. 750- ml sport bottle

4. 25- oz

- Consumers today are highly influenced by appearance and the physical look.

- SmartWater’s bottle packaging and name is one of the products strengths. Its sleek and unique design gives it an exclusive look

and it’s what makes it stand out from bottled waters on shelves.

SmartWater Sports (750- mL)

- SmartWater bottled water with a sports cap will be introduced into the market. This is will satisfy the needs of consumers

involved in physical activity, making it easier for them to hydrate themselves without spilling.

SmartWater Packaging

Brand Name: The brand name SmartWater will be maintained. Results from a questionnaire carried out

implied that ‘SmartWater’ is a unique name which will catch people’s attention in the market and fits

appropriately to the function of the product. Other brand names are stereotypical which reflect where

37

the water has been sourced from like Fiji or Evian. The name ‘SmartWater’ has a mysterious feel which catches the attention of

the consumers, thus urge them to purchase the product.

Label: The label will tell a cohesive story on both sides of the bottle, which will communicate the brand benefits and establish

the brands personality and style.

The front logo of the bottle will be maintained, however the backside of the bottle label will be adjusted.

The label graphics include a fluid raindrop shape in navy blue which also flows across the shelf when the bottles are placed

together. This creates energy and movement relating to the products electrolyte enhancement.

While other bottled water graphics normally capture consumer’s attention on the front-label, Glaceaus’s SmartWater will

engage consumers on both sides of the bottle.

The label is printed using silk screening and UV flex, in nine colours and a varnish coating.

Initially - On the reverse side, an image of a gold-fish visually communicates that ‘spring water is for swimming and SmartWater

is for drinking’. This image of the gold fish can be misunderstanding and give consumers a different impression.

38

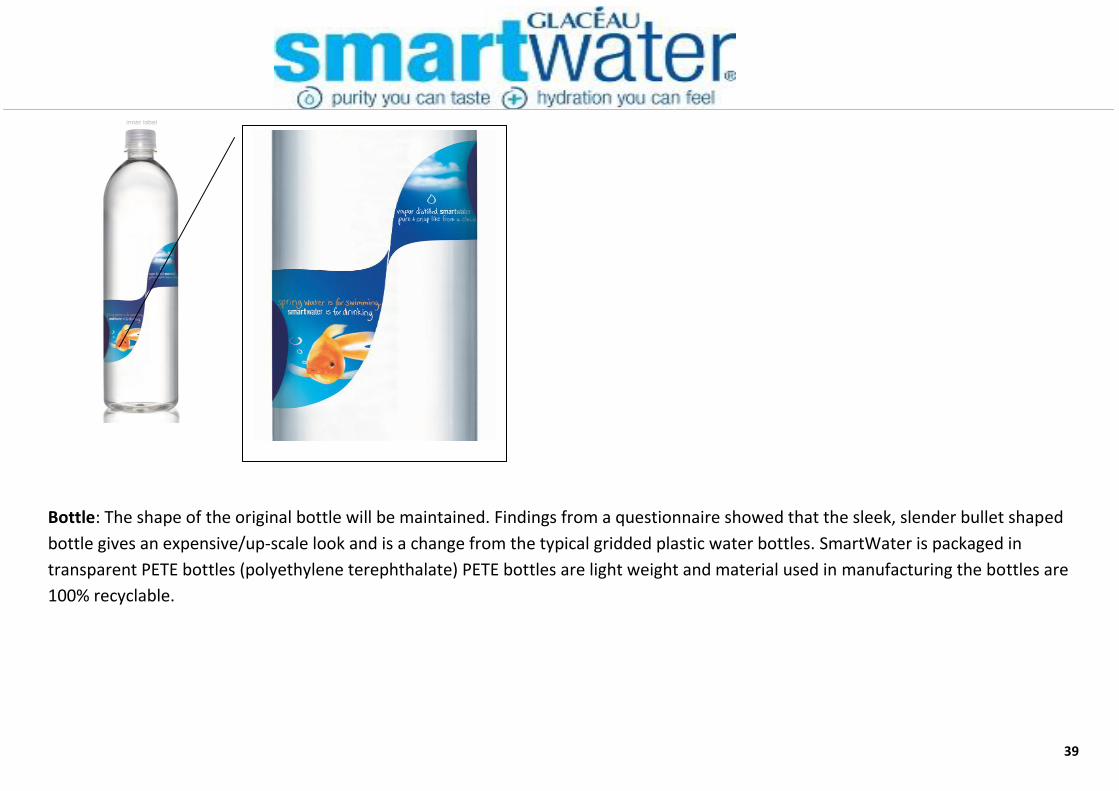

Bottle: The shape of the original bottle will be maintained. Findings from a questionnaire showed that the sleek, slender bullet shaped

bottle gives an expensive/up-scale look and is a change from the typical gridded plastic water bottles. SmartWater is packaged in

transparent PETE bottles (polyethylene terephthalate) PETE bottles are light weight and material used in manufacturing the bottles are

100% recyclable.

39

Packaging Mood board

40

Dual branding which will engage consumers on both sides of the bottle.

41

Three levels of SmartWater

Exhibit.10

(Kotler, 2010,pg.250)

42

5.1 SmartWater Marketing Mix: Price - With SmartWater being a premium brand in its current operating market(U.S.A), prices will be kept low in the Singapore market in order to compete

effectively with such tight competition.

- High levels of expenditure in the beginning will not enable penetration pricing strategy to be used.

Market-Based pricing will be used during the introduction of SmartWater in order to stay competitive in the market. Prices will be set in line with

competitors. This will still attract buyers and capture market share of its competitors.

Competitor price comparison

Competitor price set per 500 ml (SGD DOLLAR)

Exhibit.11

BRANDS SmartWater(750ml

-1.40)

100PLUS H-TWO-O POCARI

SWEAT

VitaminWater PINK Dolphin

Retail price

per 500ml

$ 1.25 $ 1.35 $ 1.30 $ 1.25 $ 1.70 $ 1.20

43

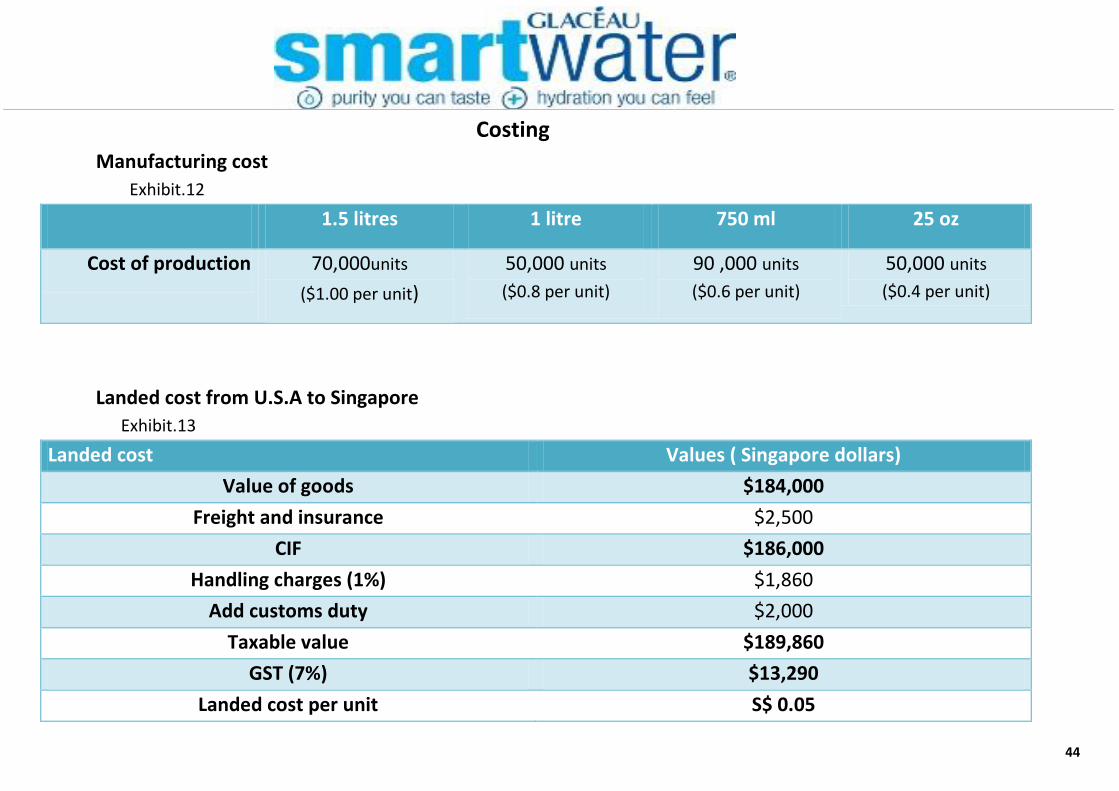

Costing

Manufacturing cost

Exhibit.12

1.5 litres 1 litre 750 ml 25 oz

Cost of production 70,000units

($1.00 per unit)

50,000 units

($0.8 per unit)

90 ,000 units

($0.6 per unit)

50,000 units

($0.4 per unit)

Landed cost from U.S.A to Singapore

Exhibit.13

Landed cost Values ( Singapore dollars)

Value of goods $184,000

Freight and insurance $2,500

CIF $186,000

Handling charges (1%) $1,860

Add customs duty $2,000

Taxable value $189,860

GST (7%) $13,290

Landed cost per unit S$ 0.05

44

Summary of SmartWater’s cost and pricing Exhibit.14

SKU’S 1.5 litre 1 litres 750 ml(sports

bottle)

25 0z

Landed cost(manufacturing

cost + importation cost)

S$ 1.05 S$0.85 S$0.65 S$0.45

Selling price(cost +profit

margin)

S$1.8 S$1.60 S$1.40 S$1.20

retailing price(20%) S$ 2.0 S$ 1.9 S$ 1.60 S$ 1.40

45

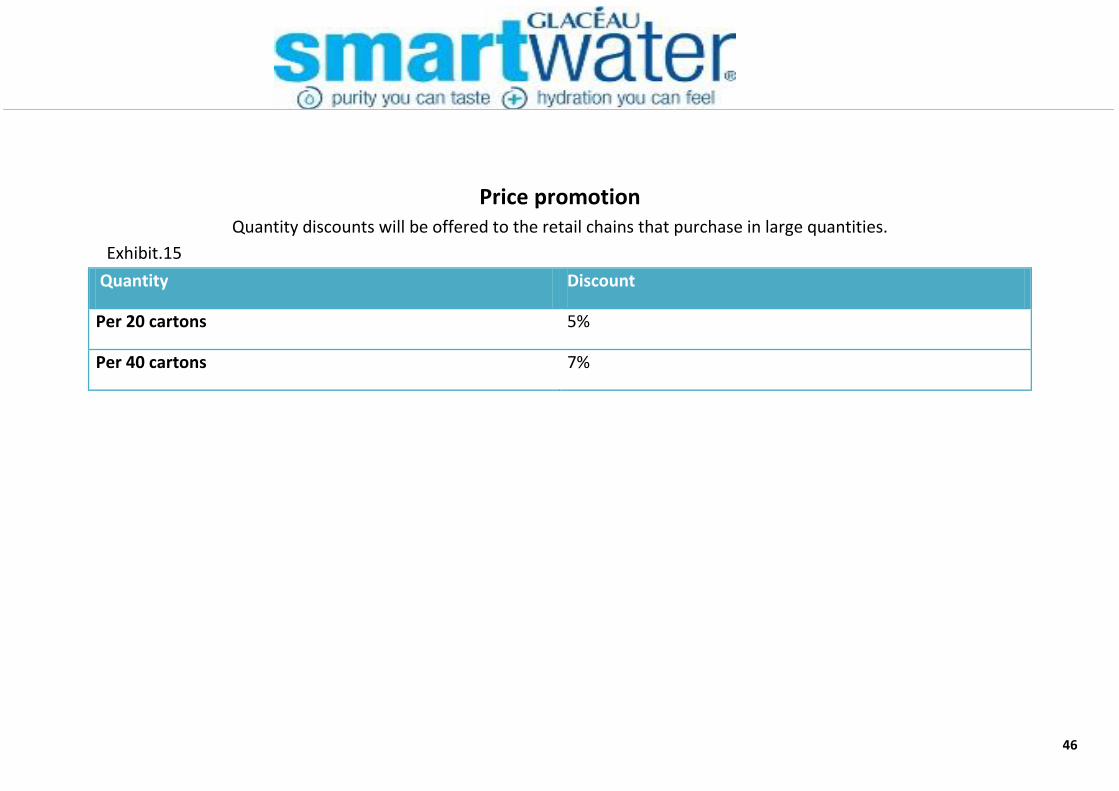

Price promotion Quantity discounts will be offered to the retail chains that purchase in large quantities.

Exhibit.15

Quantity Discount

Per 20 cartons 5%

Per 40 cartons 7%

46

5.2 SmartWater Marketing Mix: Place

Direct marketing approach will be used. SmartWater will be distributed directly to the retail chains; this will provide an

opportunity to gain strong alliances with the retailers who sell to the end consumers.

Distribution will mainly be to the popular retail outlets and convenience store. Results from a questionnaire supports this

decision, as consumers said they mostly purchased their enhanced water bottles from such purchase points.

DISTRIBUTION CHANEL

47

Target number of retail outlets SmartWater is targeting 15% of each of the retailer’s outlet during its first year in the market. This 15% will be the top busiest retail

outlets in Singapore. This approach will also apply for the following years.

48

5.3 SmartWater Marketing Mix: Promotion

Target Audience- active lifestyle

SmartWater target audience will be the 18-40 year olds. We want to target the young ‘hip’ and upcoming age. The younger half

of the target audience will be college students who need a beverage to keep them hydrated. The other portion of our audience

will be young businessmen and women who are beginning to establish stable careers and take an interest in maintaining and

looking after their health.

Geographic scope

In order to make a push in areas that have been recognised as having potential for the brand SmartWater, advertisement

campaigns will be mainly placed around the universities in Singapore and the prime business areas to catch the attention of

students and the active businessmen and women. Advertisements will be placed in lifestyle magazines, on buses, in train

stations and via social media platforms. The placement will create awareness both publicly and also in the key market areas.

Objective

- SmartWater considered the smartest choice for a healthy beverage for efficient hydration.

Advertising campaign/slogan ‘Brains perform best when they are hydrated’

49

50

Advertising Mood Board

51

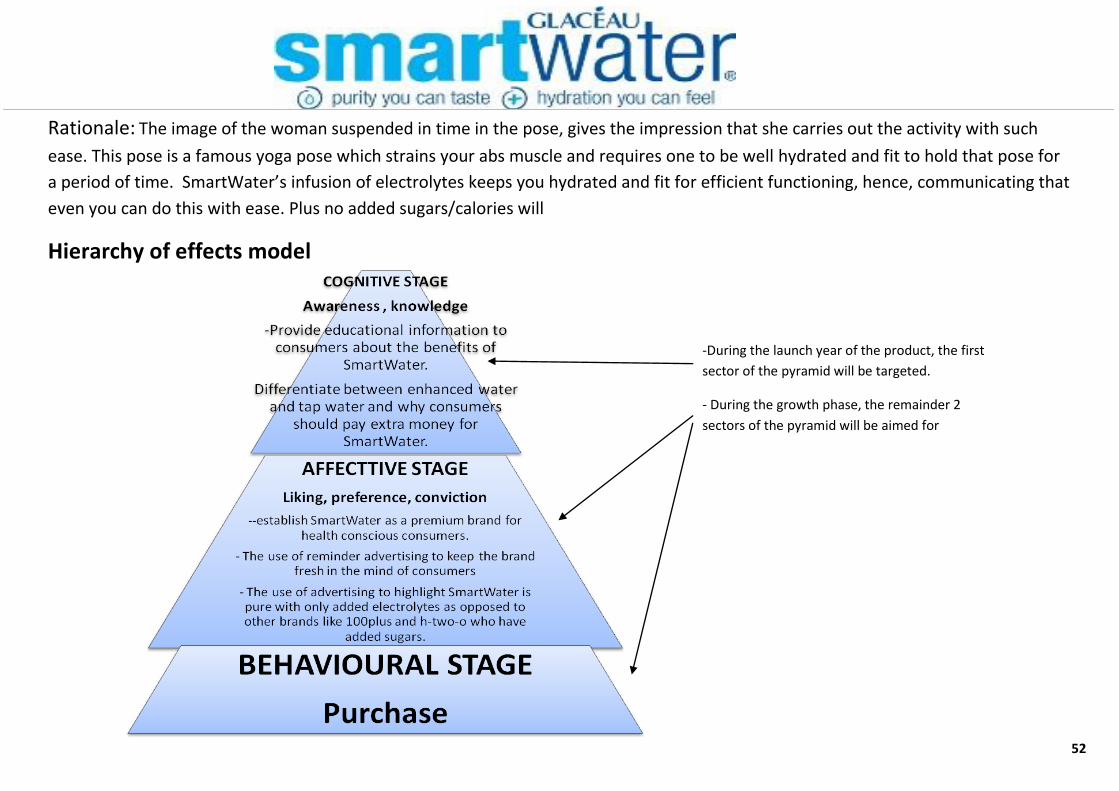

Rationale: The image of the woman suspended in time in the pose, gives the impression that she carries out the activity with such

ease. This pose is a famous yoga pose which strains your abs muscle and requires one to be well hydrated and fit to hold that pose for

a period of time. SmartWater’s infusion of electrolytes keeps you hydrated and fit for efficient functioning, hence, communicating that

even you can do this with ease. Plus no added sugars/calories will

Hierarchy of effects model

-During the launch year of the product, the first

sector of the pyramid will be targeted.

- During the growth phase, the remainder 2

sectors of the pyramid will be aimed for

52

Outcomes

- Created brand awareness of SmartWater

- SmartWater established as a brand for healthy consumers who are now knowledgeable on the health benefits.

- Gain 20% brand awareness within its target market within its first year.

Medium

Choices of Media mix:

Billboards:

-Four billboards will be placed around the

top 3 universities in the country (NUS, NTU,

and SMU)

Transits:

-Ads on top 4 SMRT bus routes and at

the top 5 business district SMRT

stations

Magazines

-Her world -Men’s health -Harpers bazaar -shape

Internet:

Social media:

-facebook page

53

Media plan

Magazines About/Costs

Her world

- Singapore’s best-read women’s magazine on fashion, beauty and lifestyle trends

Monthly publication

Readership: 203,000

Readership profile: predominately women; go getters, sophisticated, stylish and self-assured.

Inside back cover – S$ 6.026

Men’s health - it’s an authority on male fitness, health, sex , fashion and grooming

Monthly publication

Readership: 105,000

Readership profile: predominately men; well-educated, health-conscious, intelligent, affluent

and lead active lifestyles.

Inside back cover: 4,500

Harpers bazaar - a source that converges fashion and beauty with design, technology and culture.

Monthly publication

Readership:

Readership profile: predominately women; they personify self-assurance, modern

sophistication, high aspirations and is unwilling to compromise when it comes to quality,

style and good taste.

Colour full page: 4,300

Shape

- Singapore’s only mind and body guide for women. Provides the latest practical information

on wellness, beauty, health and nutrition.

Monthly publication

Readership: 46,000

Readership profile: young, well educated, health conscious, smart, affluent and lives an

55

active lifestyle.

Colour full page: 3,500

SMRT STATIONS Dhoby Ghaut , Orchard, Bayfront, Raffles, harbour front

Platform screen doors (full length 96 doors)

Minimum 4 weeks per ad

Production cost: S$10,000 per station

Total cost: S$30,000 per station

Buses - Top 4 SMRT bus routes

- Single-deck rear

- Production cost s$380

1 week media: S$200 per bus

Total cost : S$580 per bus

Billboard - Around the top 3 universities in Singapore

240 by 120 inches

Production cost s$ 2500

Total cost: S$ 3500 per billboard

55

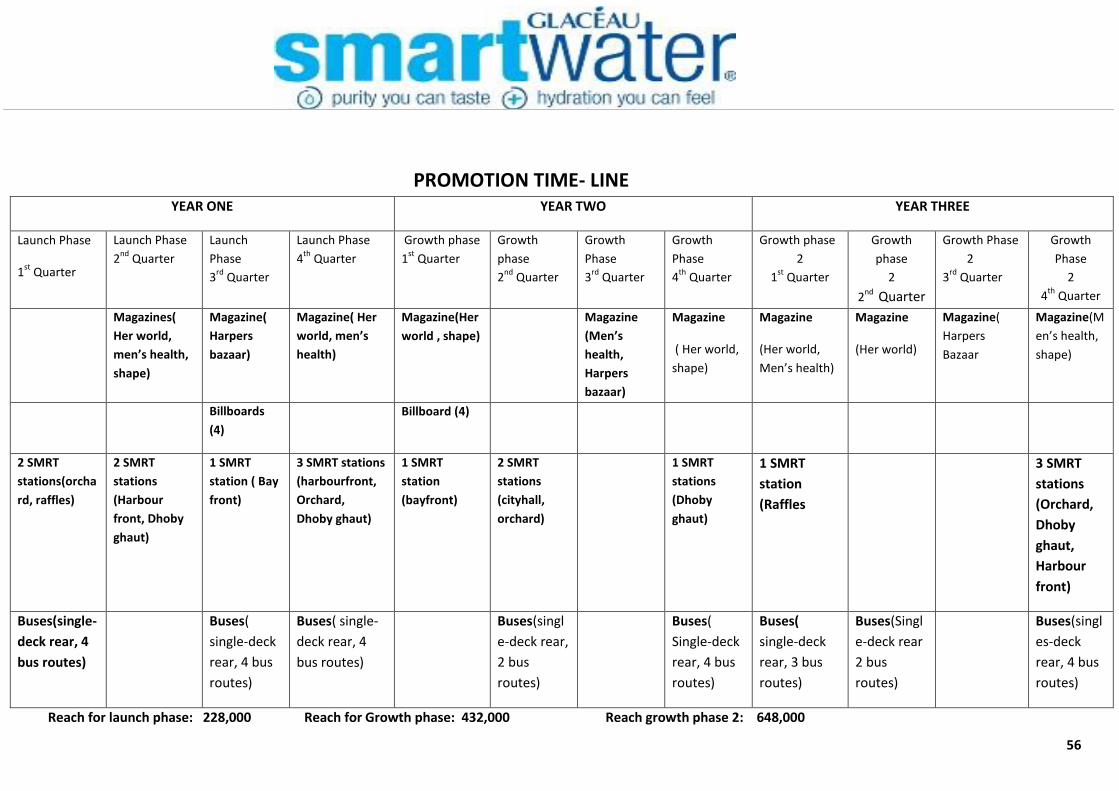

PROMOTION TIME- LINE YEAR ONE YEAR TWO YEAR THREE

Launch Phase

1st

Quarter

Launch Phase

2nd

Quarter

Launch

Phase

3rd

Quarter

Launch Phase

4th

Quarter

Growth phase

1st

Quarter

Growth

phase

2nd

Quarter

Growth

Phase

3rd

Quarter

Growth

Phase

4th

Quarter

Growth phase

2

1st

Quarter

Growth

phase

2

2nd

Quarter

Growth Phase

2

3rd

Quarter

Growth

Phase

2

4th

Quarter

Magazines(

Her world,

men’s health,

shape)

Magazine(

Harpers

bazaar)

Magazine( Her

world, men’s

health)

Magazine(Her

world , shape)

Magazine

(Men’s

health,

Harpers

bazaar)

Magazine

( Her world,

shape)

Magazine

(Her world,

Men’s health)

Magazine

(Her world)

Magazine(

Harpers

Bazaar

Magazine(M

en’s health,

shape)

Billboards

(4)

Billboard (4)

2 SMRT

stations(orcha

rd, raffles)

2 SMRT

stations

(Harbour

front, Dhoby

ghaut)

1 SMRT

station ( Bay

front)

3 SMRT stations

(harbourfront,

Orchard,

Dhoby ghaut)

1 SMRT

station

(bayfront)

2 SMRT

stations

(cityhall,

orchard)

1 SMRT

stations

(Dhoby

ghaut)

1 SMRT

station

(Raffles

3 SMRT

stations

(Orchard,

Dhoby

ghaut,

Harbour

front)

Buses(single-

deck rear, 4

bus routes)

Buses(

single-deck

rear, 4 bus

routes)

Buses( single-

deck rear, 4

bus routes)

Buses(singl

e-deck rear,

2 bus

routes)

Buses(

Single-deck

rear, 4 bus

routes)

Buses(

single-deck

rear, 3 bus

routes)

Buses(Singl

e-deck rear

2 bus

routes)

Buses(singl

es-deck

rear, 4 bus

routes)

Reach for launch phase: 228,000 Reach for Growth phase: 432,000 Reach growth phase 2: 648,000

56

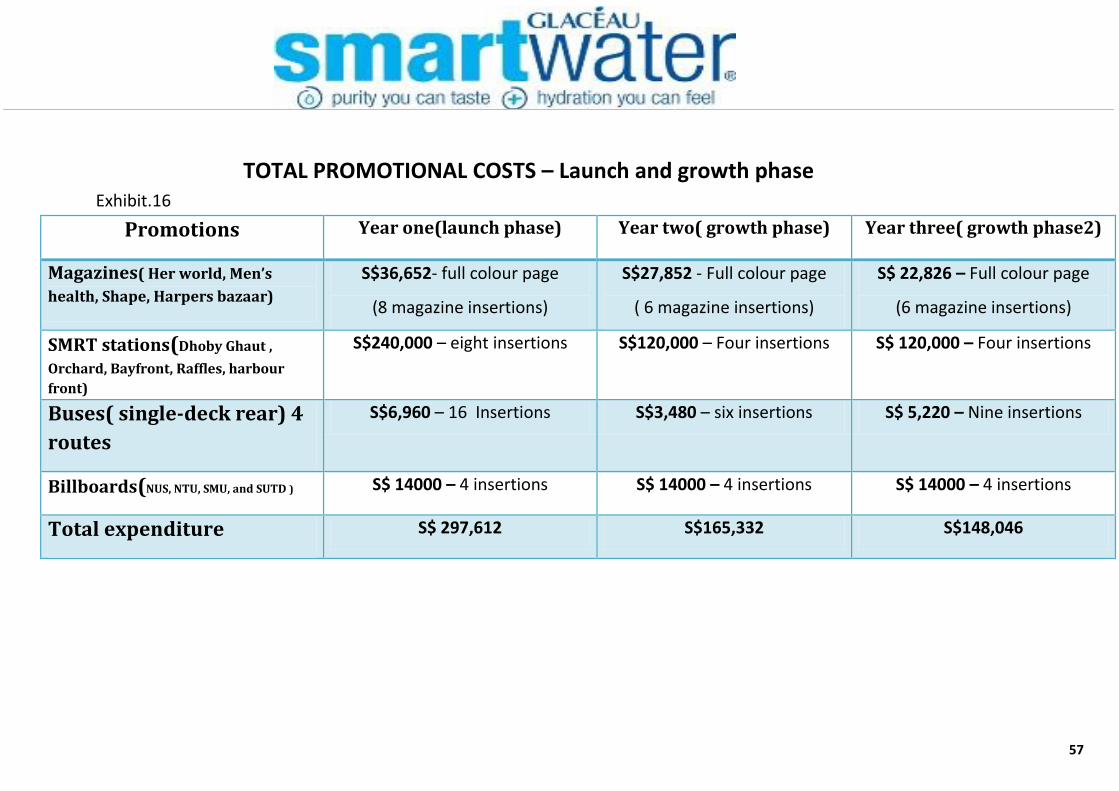

TOTAL PROMOTIONAL COSTS – Launch and growth phase Exhibit.16

Promotions Year one(launch phase) Year two( growth phase) Year three( growth phase2)

Magazines( Her world, Men’s

health, Shape, Harpers bazaar)

S$36,652- full colour page

(8 magazine insertions)

S$27,852 - Full colour page

( 6 magazine insertions)

S$ 22,826 – Full colour page

(6 magazine insertions)

SMRT stations(Dhoby Ghaut ,

Orchard, Bayfront, Raffles, harbour

front)

S$240,000 – eight insertions S$120,000 – Four insertions S$ 120,000 – Four insertions

Buses( single-deck rear) 4

routes

S$6,960 – 16 Insertions S$3,480 – six insertions S$ 5,220 – Nine insertions

Billboards(NUS, NTU, SMU, and SUTD ) S$ 14000 – 4 insertions S$ 14000 – 4 insertions S$ 14000 – 4 insertions

Total expenditure S$ 297,612 S$165,332 S$148,046

57

58

Budgeting& Forecasts

6.0 Sales Forecast

Forecasted unit sales per SKU

a) 1.5 litre sales forecast Exhibit.17 Year 1

Launch phase

Year2

Growth phase

Year 3

Consolidation Phase

Forecast unit sale S$ 10,000 S$ 20000 S$35000

Revenue( selling price to retailers @

S$ 1.8)

S$ 18,000 S$ 36,000 S$ 63,000

Cost of sales(landed cost, S$ 1.05 per

unit)

S$ 10,500 S$21,000 S$36,750

Gross margin S$ 7,500 S$ 15,000 S$ 26250

b) 1 Litre sales forecast Exhibit.18 Year 1

Growth phase

Year 2

Growth phase

Year 3

Consolidation Phase

Forecast unit sale 30,000 36,000 49,000

Revenue( selling price to retailers

@ S$ 1.6)

48,000 58,000 79,000

59

Cost of sales (landed cost, S$ 0.85

per unit)

25,500 30,600 41,650

Gross margin 25,500 27,400 37,350

C) 750 ml sales forecast Exhibit.19 Year 1

Launch phase

Year 2

Growth Phase

Year 3

Consolidation Phase

Forecast unit sale 20,000 28,000 42,000

Revenue( selling price to retailers

@S$ 1.4)

S$ 28,000 S$ 40,000 S$ 59,000

Cost of sales ( landed cost, S$ 0.65

per unit)

S$ 13,000 S$18,200 S$ 27,300

Gross margin S$ 15,000 S$ 21,800 S$ 31,700

60

d) 25 oz sales forecast Exhibit.20 Year 1

Launch phase

Year 2

Growth Phase

Year 3

Consolidation Phase

Forecast unit sale 20,000 28,000 42,000

Revenue(selling price to retailers

@S$ 1.20)

S$ 24,000 S$ 34,000 5S$ 1,000

Cost of goods (landed cost, 0.45 per

unit)

S$ 9,000 S$ 12,600 S$ 18,900

Gross margin S$ 15,000 S$ 21,400 S$ 32,100

61

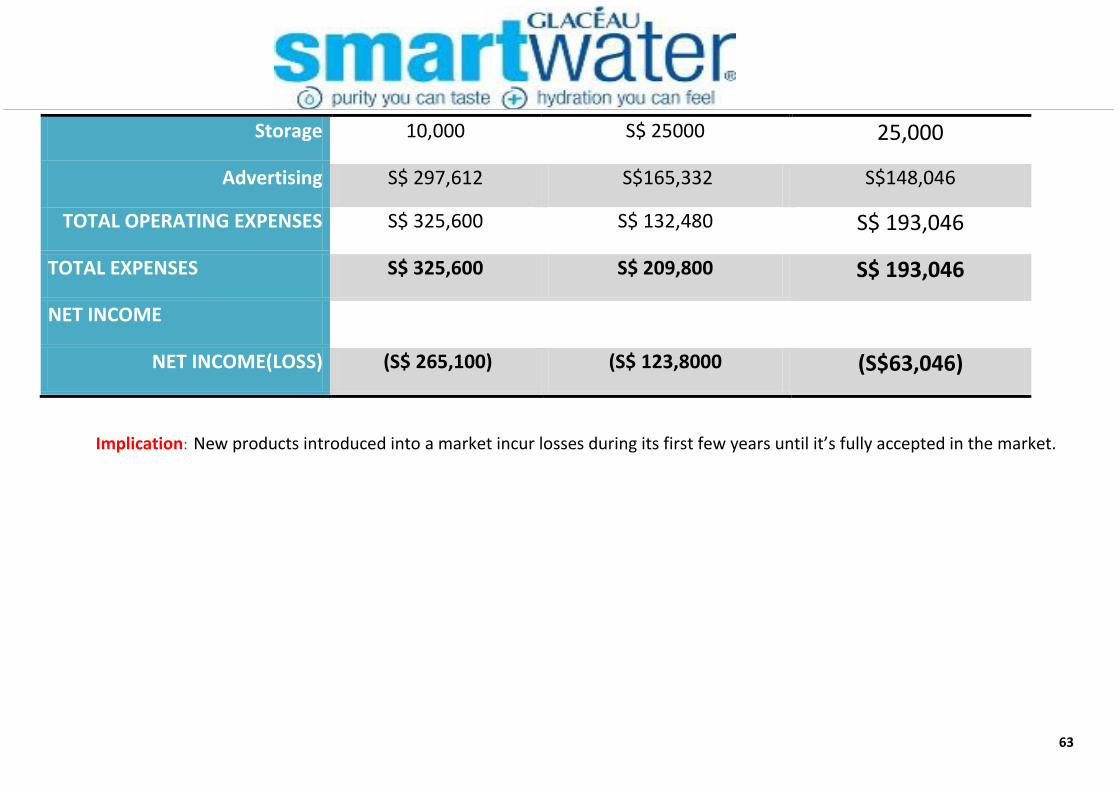

Total sales forecast – Profit & loss statement Exhibit.21

Forecasted period Year 1

Launch Phase

Year 2

Growth Phase

Year 3

Consolidation phase

INCOME

REVENUE S$ 118,000 S$ 168,000 S$ 254,000

Cost of goods sold - S$ 57,500 - S$ 82,000 - S$ 124,00

Gross profit S$ 60,500 S$ 86,000 S$ 130,000

TOTAL GROSS PROFIT S$ 60,500 S$ 86,000 S$ 130,000

EXPENSES

Operating expenses

Wages S$ 10,000 S$ 10,500 11,000

Transportation S$ 8,000 S$ 9,000 9,000

62

Storage 10,000 S$ 25000 25,000

Advertising S$ 297,612 S$165,332 S$148,046

TOTAL OPERATING EXPENSES S$ 325,600 S$ 132,480 S$ 193,046

TOTAL EXPENSES S$ 325,600 S$ 209,800 S$ 193,046

NET INCOME

NET INCOME(LOSS) (S$ 265,100) (S$ 123,8000 (S$63,046)

Implication: New products introduced into a market incur losses during its first few years until it’s fully accepted in the market.

63

7.0 SmartWater marketing Mix summary

Product

Positioned as a healthy beverage for the young and active consumers

Introducing four different SKU’s into the market

Sleek bullet shaped bottle using dual branding on both sides of the bottle

label

Label printing via silk screening

Price

Market-based pricing approach

selling price to retailers derived by adding a 60% profit margin

Retailing price derived by Singapore standard retail top up of

20%

5 to 7% Quantity discounts offered to retailers

Place Promotion

Distributed to retail and convenience stores via direct marketing Advertisements placed in magazines, train stations, on buses and billboards

around

Campaign slogan – ‘brains perform best when hydrated’

15% of each retail chain outlet targeted for the 1st year

25% of each retail chain outlet targeted for the 2nd year

40% of each retail chain outlet targeted for the 3rd year

64

References Online sources

The Edge. 2012. Nov 16: GDP forecast, OUE, F&N, SIA. [ONLINE] Available at: http://www.theedgesingapore.com/the-daily-edge/business/41166-nov-16-

gdp-forecast-oue-fan-sia.html. [Accessed 27 December 12].

Ministry of manpower. 2012. Singapore unemployment rate. [ONLINE] Available at: http://www.tradingeconomics.com/singapore/unemployment-rate.

[Accessed 27 January 13].

Ministry of trade and industry. 2012. Singapore GDP growth rate. [ONLINE] Available at: http://www.tradingeconomics.com/singapore/gdp-growth. [Accessed

27 January 13].

Ministry of trade and industry. 2012. Singapore inflation rate. [ONLINE] Available at: http://www.tradingeconomics.com/singapore/inflation-cpi. [Accessed 27

January 13].

Department of statistics Singapore. 2012. Singapore in Figures. [ONLINE] Available at: http://www.singstat.gov.sg/pubn/reference/sif2012.pdf. [Accessed 27

January 13].

Nielsen. 2011. Singaporeans can’t get enough of digital media. [ONLINE] Available at: http://www.sg.nielsen.com/site/NewsReleaseJuly112011.shtml.

[Accessed 27 January 13].

RIKVIN (Singapore company registration specialists). 2012. Lemon law will boost will boost retail Singapore's industry. [ONLINE] Available at:

http://www.prweb.com/releases/singapore/lemon-law-news/prweb9273922.htm. [Accessed 27 January 13].

Singapore Law academy. 2013. Competition law. [ONLINE] Available at: http://www.singaporelaw.sg/content/CompetitionLaw.html. [Accessed 27 December

12].

Ministry of environment and waste collection. 2012. Waste production. [ONLINE] Available at:

http://app.mewr.gov.sg/web/Contents/contents.aspx?contid=1539. [Accessed 27 December 12].

Ministry of finance. 2012. Corporate income tax. [ONLINE] Available at:

http://app.mof.gov.sg/(X(1)S(1l2jv4553bx2ga55s4tsqf55))/TemSub.aspx?pagesid=20090918965913283168&pagemode=live&&AspxAutoDetectCookieSuppor

t=1. [Accessed 27 December 12].

65

Movemedia. 2012. Media rate books. [ONLINE] Available at: http://www.moovemedia.com.sg/media.html. [Accessed 05 February 13].

Singapore press holding. 2012. Magazines. [ONLINE] Available at: http://www.sph.com.sg/pdf/Mediapedia/2nd/SPHMediapedia_Magazines.pdf. [Accessed

05 February 13].

Baure media group. 2012. Harper’s bazaar Singapore. [ONLINE] Available at: http://www.acpmagazines.com.sg/harpers-bazaar-singapore.htm. [Accessed 05

February 13].

Diseno advertising. 2012. Shape rate card 2012. [ONLINE] Available at: http://www.diseno.com.sg/services/advertising/rate-cards/. [Accessed 05 February

13].

Diseno advertising. 2012. Men's health rate card 2012. [ONLINE] Available at: http://www.diseno.com.sg/services/advertising/rate-cards/. [Accessed 05

February 13].

Diseno advertising. 2012. Her world rate card 2012. [ONLINE] Available at: http://www.diseno.com.sg/services/advertising/rate-cards/. [Accessed 05 February

13].

Yeo Hiap Seng. 2012. Refuel with H-TWO-O. [ONLINE] Available at: http://www.yeos.com.sg/h-two-o/original/Refuel_With_H-TWO-O_Original.php.

[Accessed 05 February 13].

Fraser and Neave. 2012. Rehydrate with 100 plus. [ONLINE] Available at: http://www.100plus.co.za/site/home. [Accessed 05 February 13].

Otsuka pharmaceutical. 2012. Pocari sweat. [ONLINE] Available at: http://www.pocarisweat.com.ph/default.aspx. [Accessed 05 February 13].

Nielsen. 2011. Health consciousness increases in Singapore. [ONLINE] Available at: http://healthmad.com/weight-loss/health-consciousness-increase-in-

singapore/. [Accessed 25 December 12].

66

Reports/Databases Euromonitor. 2012. Singapore soft drink industry. [ONLINE] Available at: http://www.euromonitor.com/soft-drinks-in-

singapore/report. [Accessed 14 January 13].

Euromonitor. 2012. Consumer Lifestyle. [ONLINE] Available at: http://www.euromonitor.com/consumer-lifestyles-in-

singapore/report. [Accessed 14 January 13].

Euromonitor. 2012. Bottled water in Singapore. [ONLINE] Available at: http://www.euromonitor.com/bottled-water-in-

singapore/report. [Accessed 14 January 13].

Euromonitor. 2012. Energy and sports drinks in Singapore. [ONLINE] Available at: http://www.euromonitor.com/sports-

and-energy-drinks-in-singapore/report. [Accessed 14 January 13].

BOOKS Kotler Philip, R, 2010. Principles of marketing. 13th ed. Singapore: Pearson.

67

List of Exhibits Page no Exhibit.1---------------------------------------------------------------------------------------------------------------------------------------------------8

Exhibit.2---------------------------------------------------------------------------------------------------------------------------------------------------10

Exhibit.3---------------------------------------------------------------------------------------------------------------------------------------------------11

Exhibit.4---------------------------------------------------------------------------------------------------------------------------------------------------12

Exhibit.5---------------------------------------------------------------------------------------------------------------------------------------------------14

Exhibit.6---------------------------------------------------------------------------------------------------------------------------------------------------33

Exhibit.7---------------------------------------------------------------------------------------------------------------------------------------------------33 - 34

Exhibit.8---------------------------------------------------------------------------------------------------------------------------------------------------34

Exhibit.9---------------------------------------------------------------------------------------------------------------------------------------------------35

Exhibit.10--------------------------------------------------------------------------------------------------------------------------------------------------42

Exhibit.11--------------------------------------------------------------------------------------------------------------------------------------------------43

Exhibit.12---------------------------------------------------------------------------------------------------------------------------------------------------44

Exhibit.13---------------------------------------------------------------------------------------------------------------------------------------------------44

Exhibit.14---------------------------------------------------------------------------------------------------------------------------------------------------45

Exhibit.15---------------------------------------------------------------------------------------------------------------------------------------------------46

Exhibit.16---------------------------------------------------------------------------------------------------------------------------------------------------57

Exhibit.17---------------------------------------------------------------------------------------------------------------------------------------------------59

Exhibit.18---------------------------------------------------------------------------------------------------------------------------------------------------59 - 60

Exhibit.19---------------------------------------------------------------------------------------------------------------------------------------------------60

Exhibit.20---------------------------------------------------------------------------------------------------------------------------------------------------61

Exhibit.21 --------------------------------------------------------------------------------------------------------------------------------------------------62

68

Appendix Questionnaire survey Objective: target market preferences for enhanced bottled water.

1. Were you born after 1962?

Yes no (terminate)

2. Which of the following products do you drink?

100PLUS

H-TWO-O

POCARI SWEAT

Gatorade

69

3. What comes to mind when you think of 100Plus?

4. What comes to mind when you think H-two-o?

5. What comes to mind when you think of Gatorade?

VitaminWater

None of the above (terminate)

Pink Dolphin

70

6. What comes to mind when you think of Pocari sweat?

7. What comes to mind when you think of VitaminWater?

8. What comes to mind when you of Pink Dolphin?

9. Please rate your three most preferred drinks 1 (most preferred) to 3 (least preferred).

Pocari sweat ------------

VitaminWater ------------

H-two-o ------------

Gatorade -------------

100plus -------------

Pink Dolphin ------------

71

10. On what occasions do you usually drink brands such as 100plus/H-two-o/VitaminWater /Gatorade?

11. Where do you normally buy drinks such as 100plus/H-two-o/VitaminWater /Gatorade?

Vending Machine

Eating outlet

Supermarkets

Convenience store (e.g. 7 /11, cheers)

12. How often do you drink brands such as100plus/H-two-o/VitaminWater /Gatorade?

Everyday Weekly Every other week monthly less frequently

13. When you are thirsty, what type of drink do you usually have?

Objective: Consumer thoughts and feeling towards SmartWater

14. (A) Would you try a drink that tastes like water, with no sweetener/flavours but has other ingredients similar to 100plus/Gatorade/VitaminWater

Yes

No

72

(B) If yes. Why?

(C). If no, why?

15. (A) Imagine a drink that tastes like water, with no sweetener/flavours but with ingredients similar to 100Plus/Gatorade/VitaminWater. What do you think of

the following names?

‘SmartWater’

‘Fitness’

‘Boost’

‘Healthy Life'

73

(B) Which name do you prefer?

Healthy Life

Boost

Fitness

SmartWater

(C) Why do you prefer this name?

16. A) For a drink that tastes like water, with no sweetener/flavours but with ingredients similar to 100plus/Gatorade, which bottle shape do you prefer? (choose

one)

Bottle A Bottle B Bottle C

74

b) Reason for your choice?

Consumer profile

17. What is your occupation?

18. What do you like to do after work/School?

19. What do you like to do on weekends?

20. Which bottled/can/carton drinks do you consider healthy?

Thank you for your time

75