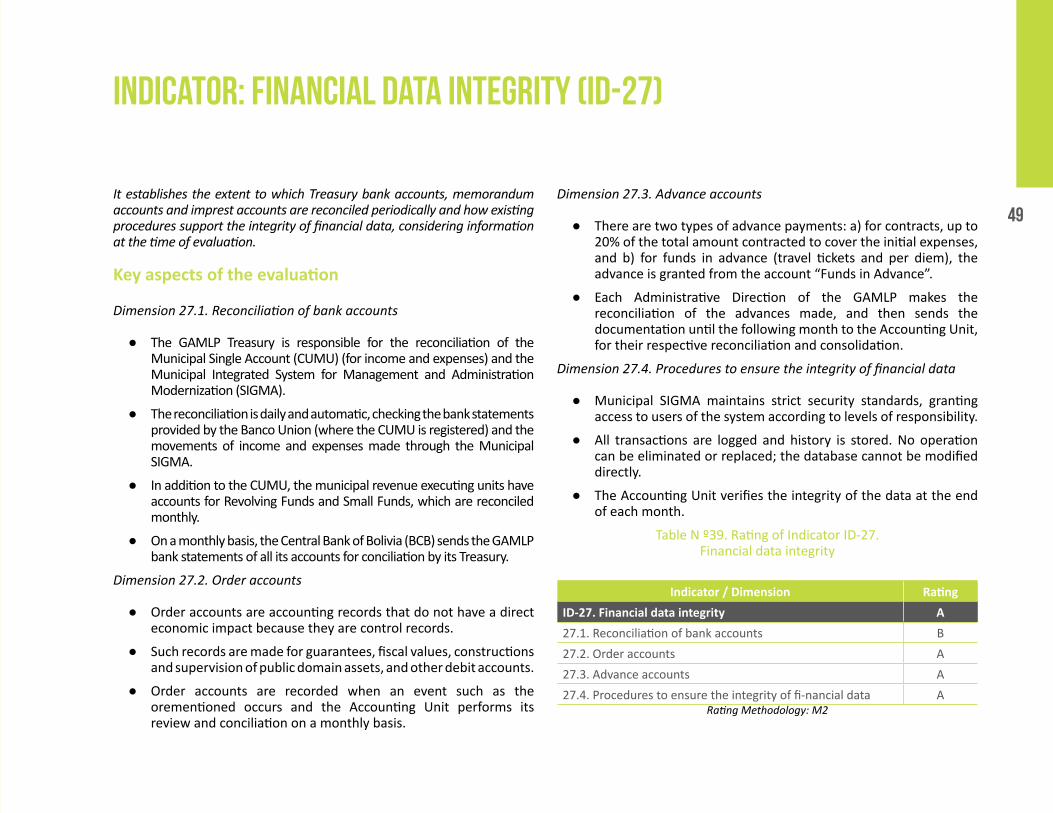

evaluation - pefa.org paz-apr17-pfmpr-sn... · maria eugenia soria sánchez, gladis andrade...

TRANSCRIPT

1

AUTONOMOUS MUNICIPAL GOVERNMENT OF LA PAZ

EVALUATIONOF PUBLIC EXPENDITURE AND FINANCIAL ACCOUNTABILITY UNDER THE PEFA METHODOLOGY

2

The Public Expenditure and Financial Accountability (PEFA) assessment of the GAMLP was carried out during the tenure of:

Dr. Luis Revilla HerreroMayor of the Autonomous Municipal Government of La Paz

GENERAL COORDINATION AND SUPERVISION:

Alvaro Blondel RossettiExecutive Municipal Secretary Roger Quiroga Becerra de La RocaStrategic AdvisorMabel Vargas RomanoMunicipal Secretary of Finance

TECHNICAL COORDINATION:

Claudia L. Apaza AngolaFinancial Management DirectorJavier Rivera ViaFinancing and Financial Analysis Director

SUPPORTING STAFF: Maria Daniela Calderon, Jose Abigail Rubin de Celis, Ruben Viscarra Siñani, Sergio A. Aguirre Velasco

TECHNICAL TEAM:

Budget Unit Alberto Peñaloza Carrasco, Juan Vega Arias, Gonzalo Castro Cuevas, Miguel Angel Cuaquira Herrera, Gorki Diaz Calderon, Yolanda Torrez Quispe, Ariana Peñaloza Flores, Manuel del Carpio SalcedoAccounting Unit Maria Eugenia Soria Sánchez, Gladis Andrade Velasquez, Nely Mamani Mamani, Jackeline Hinojosa Collao, Eunice Espiritu Quisbert, Emilio Tito Velasquez Antezana, Marianela Revollo Terrazas, Melany Revollo Salgado, Carlos Aliaga Condori, Oscar Olivera Palacios, Heidi Vargas Montero, Mariela Macuchapi Ortiz, Ronald Zapana Hoyos, Hugo Calderon Quispe, Alejandra Carvajal Rodriguez Treasury Unit Juan Carlos Sempertegui Miranda, Victor Hugo Villalpando Condori, Oscar Tapia Paredes, Leonard Mejillones Choque, Lilian Fernandez Flores, Nicodemo Mamani Tarquino, Marco Leaño, Javier Tenorio Ventura, Virginia Cabrera Rojas Public Credit UnitRodolfo Siñani Arias, Francisco Paz, Romy Vargas Koppensteiner, Ana Maria Aruquipa Rios. Economic and Financial Analysis Unit Freddy Barrios Chavez, Pamela Montesinos Lelarge, Miguel Angel Guevara Murillo, Melissa Martínez Duran

EDITING:Bernardo Fernandez Telleria

DESIGN AND LAYOUT:Dennis Vasquez Careaga

PRINT:SU EMPRESALa Paz – Bolivia, October 2017L.D.: 4 - 1 - 450 - 17 P.O.ISBN: 978 - 99905 - 47 - 77 - 1

The Municipal Secretariat of Finance of the Autonomous Municipal Government of La Paz authorizes the partial reproduction of the contents of this publication for research and academic purposes, so long as the source is always cited.

3

FOREWORD

An adequate management of public finances is essential for the correct allocation and use of public resources, in order to achieve the objectives of development policies; ensuring that revenues are collected efficiently and used in an appropriate and sustainable manner.

In recent years, the municipal financial management has undergone a substantial transformation due to the need to achieve fiscal sustainability and transparency. These modernization efforts have focused on the updating and improvement of the regulatory framework, the rationalization of the procedures and the implementation of more sophisticated models.

Fiscal discipline and the efficiency of public spending have been two pillars guiding the work of the Autonomous Municipal Government of La Paz. For this reason, its municipal financial management structure was submitted to a comparative assessment with respect to international good practices and standards, which has once again placed the Municipality of La Paz at the forefront of the evolution of public finances at national and international levels.

Consequently, in 2017, in coordination with the Municipal Secretariat of Finance, a group of external experts conducted the “Public Expenditure and Financial Accountability - PEFA” assessment under the so-called PEFA methodology, a tool that allows sustainable improvements to be achieved in financial management. Transparency and accountability mechanisms were also evaluated, in terms of access to information, reporting and auditing.

This document, the PEFA Report, describes the economic situation of the Municipality of La Paz, examines the nature of its policy-based strategies and planning procedures, and discusses how budget decisions are implemented.

The results of the Report show that the Municipality of La Paz has a responsible financial management structure which aims to achieve fiscal sustainability. The results place the Municipal Government’s performance at an important level when compared with international good practices and standards, and also put forward specific challenges that must be considered to allow for major improvements in our strategies and better definition of our priorities in terms of municipal finance reforms.

With this assessment, the Autonomous Municipal Government of La Paz not only becomes the first municipality to submit to this instrument in Bolivia, but also one of the first in Latin America, demonstrating our commitment to transparency, efficiency and leadership in financial management matters at a sub-national level.

4

The PEFA Program is a prestigious association of international partners that has developed a methodology to evaluate the performance of public financial management using a set of performance indicators

based on international standards and good practices, offering technical inputs that facilitate reform actions and capacity-building in the field of public finance. La Paz is the first municipality in the history

of Bolivia to undergo this evaluation, the main results of which are summarized in this document.

I. INTRODUCTION ● The Autonomous Municipal Government of La Paz (GAMLP, for its

Spanish acronym)1, has benefitted from over ten years of continuity in its administration, during which it’s been able to consolidate highly-qualified and committed technical teams able to carry forth the changes needed in the municipality of La Paz for the benefit of its citizens.

● The strategic vision of the municipality of La Paz, first set forth in the “Jayma 2007-2011” Plan and, since 2016, in the “Integral Plan La Paz 2040: The La Paz We Want”, is widely accepted by the population and has served to guide actions and the allocation of resources in recent years.

● The strategic pillar titled “Autonomous, Participative and Co-Responsible La Paz” of the aforementioned plan currently in force, establishes a general objective of consolidating an effective municipal institutional framework for the development of the municipality of La Paz and as one of its specific objectives related to public finances, guiding municipal management towards self-sufficiency.2

● Under this vision, the GAMLP recognizes the importance of technically evaluating the status of its financial management system, to ensure it provides basic information to guide the public financial management (PFM) and strengthen its monitoring, in order to create a common platform for dialogue and continuous improvement of public management.

1 Throughout the text, the acronyms of Bolivian institutions, such as GAMLP, will be used in Spanish. Acronyms for international organisations, such a UNDP, will be used in English.

2 The Autonomous Municipal Government of La Paz. “Integral Plan La Paz 2040: The La Paz We Want”, pg. 23.

5

● As noted, in November 2016 the GAMLP made the decision to implement the Public Expenditure and Financial Accountability (PEFA) methodology, widely recognized internationally for its objectivity, technical rigor and positive impact on public management capacity. Municipalities in Ecuador, Peru and Argentina and other countries in the region have implemented the PEFA methodology with highly positive results.

● Thus, the GAMLP carried out its first PEFA evaluation of public finance management thanks to funding from the Spanish Agency for Development Cooperation (AECID) and technical support from the World Bank (WB) and the Inter-American Bank of Development (IDB).

● The GAMLP PEFA evaluation aims to measure the performance of municipal public finance management systems, identifying the current situation of the areas in which these systems function adequately and those areas where improvements are needed.

● This diagnosis will serve as a baseline for the elaboration of an Action Plan focused on improving the management of municipal public finances, facilitating dialogue both internally and with GAMLP’s main strategic partners to achieve these objectives.

Methodology

● The methodology used is described in the following PEFA technical documents:3

�� Framework for the Evaluation of Public Finance Management (Feb-2016).

�� Supplementary Guide for Sub-national PEFA Evaluations (Oct-2016).

�� Practical Guide to PEFA Evaluations (Ago-2016).

● The evaluation period included the 2014, 2015 and 2016 terms, with a cut-off date of December 31, 2016.

3 Throughout the evaluation it was determined that the following indicators and/or dimensions of the methodology did not apply (NA): a) ID-6 “Municipal govern-ment operations not included in financial reports” in its third dimension (6.3), b) ID-7 “Transfers to sub-national governments” in its two dimensions (7.1 and 7.2) and c) ID-10 “Fiscal risk report” in its second dimension (10.2).

● The evaluation took into account the administration and management of all of the GAMLP’s organizational units, according to the following organizational levels:4

�� Legislative. Represented by the Municipal Council, composed of elected members with deliberative, oversight and legislative powers within the scope of their functions.

�� Executive. Headed by the Municipal Mayor and with the technical support from the Municipal Executive Secretariat (SEM), the Municipal Secretariat of Finance (SMF) and the Municipal Secretariat for Development Planning (SMPD).

�� Operational Level: Organizational units that facilitated the operational development of PEFA through the provision of timely and relevant information.5

�� Decentralized Level: Organizational units that have administrative, but not budgetary, independence, such as the Municipal Tax Administrator (ATM).

● The following activities were carried out during the evaluation:

�� A detailed revision of all the information and documents provided by the GAMLP.

�� A detailed revision of the legal framework at the national and municipal levels.

�� Interviews with officials from the SMF, SMPD and other GAMLP organizational units.

�� Interviews with representatives of the Organism for Participation and Social Control of the Municipality of La

4 Public municipal companies (EMAVIAS and EMAVERDE) were only taken into account for dimension 10.1 (follow-up of public companies and corporations) of indica-tor ID-10 “Fiscal risk report”5 The following participated directly: Directorate of Internal Auditing, Director-ate General for Legal Affairs, Directorate of Transparency and Fight against Corruption, Municipal Direction of Governance, Directorate of Human Resources Management, Di-rectorate of General Administration, Tenders and Contracts Directorate, Municipal Co-operation Agency, Directorate of Financial Management, Finance and Financial Analysis Directorate, Business Administration Directorate, Public Entities and Services, Manage-ment by Results Directorate, Strategic Planning, Governance and Supervision of Works.

6

Paz, in the context of the formal relationship between the Municipal Executive branch and civil society.

�� Interviews with technical staff from the Ministry of Economy and Public Finance, the Ministry of Development Planning and the State Comptroller General (CGE).

�� Interviews with representatives of the National Chamber of Industry and Commerce6.

Evaluation management ● The PEFA evaluation was carried out following an internal

technical recommendation from the Municipal Secretariat of Finance and the Comptroller Department of the GAMLP. It was financed by the Spanish Agency for International Cooperation for Development (AECID) and the municipal government itself.

● The evaluation was carried out by Strategy Advisors for Government Reform (SAXgr Bolivia). In order to ensure its success, the PEFA Secretariat continued to support the technical development of the project under the so-called “PEFA CHECK”.

PEFA CHECK is a process carried out by the PEFA Secretariat that verifies compliance with six criteria or milestones during the

Evaluation. These milestones can be found at the following link: https://pefa.org/sites/default/files/07_PEFA%20CHECK%20Guidance.pdf

● During the evaluation, a process of management, supervision and follow-up, required by the PEFA methodology, was implemented with the active participation of the GAMLP and several international institutions (AECID, WB, IDB and the PEFA Secretariat):

�� GAMLP executive and operational level officials formed the Monitoring Team (ES) and served as the evaluating team’s counterpart during the year, mainly providing timely and relevant information.

6 See Annex 3 for a full list of interviews.

7

A. PRELIMINARY PHASE

Organization of PEFA Evaluation Management

● Monitoring Team (ES): GAMLP. ● Responsible for the Evaluation: GAMLP Municipal Secretarial

of Finances. ● Evaluation team: SAXgr.

B. EVALUATION PHASE

Revision of the Concept Note and/or the Terms of Reference

● Date for revised draft Concept Note and/or Terms of Reference: January 18, 2017.

● Invited reviewers: Follow-up Committee (CS), which consisted of the GAMLP, The PEFA Secretariat, AECID, BID y BM.

● Reviewers who supplied comments: Follow-up Committee. ● Date for final version of the Concept Note and/or Terms of

Reference: February 3, 2017.

The Concept Note or the Terms of Reference define the objective, the reach, the coverage and the resources needed for the PEFA

evaluation

Revision and Presentation of the Evaluation Report

● Date of delivery of draft Preliminary Report: March 22, 2017. ● Date of presentation on the Preliminary Report: April 5 de

2017. ● Deadline for submission of comments on the Preliminary

Report: April 25, 2017. ● Invited Reviewers: Follow-up Committee.

The Evaluation Report presents the diagnosis and analysis of the seven pillars of the GAMLP’s public financial management system

(GFP), within the framework of the PEFA methodology

Presentation of Final Report: April 28, 2017

�� Representatives of external institutions, in addition to the GAMLP itself, formed the Follow-up Committee (CS), acting as “peer reviewers” of the evaluation’s technical documents and participating in regular meetings to coordinate and review the progress made.

● With the defined roles, the critical path for the evaluation process within PEFA CHECK is summarized below:

● El Estado Plurinacional de Bolivia se extiende en 1.098.581 Km2, divididos en 9 departamentos y 339 municipios. Su población total se estima en 11 millones de habitantes.

Box 1: Evaluation and quality controlmanagement under PEFA CHECK

8 ● The Plurinational State of Bolivia has an extension of 1,098,581

Km2, divided into 9 departments and 339 municipalities. Its total population is estimated at 11 million inhabitants.

● The high international prices of raw materials - including natural gas and minerals, which represent more than 60% of its exports - between 2005 and 2014 allowed the country to achieve an average growth of 5% in that decade.

● National tax revenues tripled between 2005 and 2014 as a result of the tax and royalty system in force for the extractive sectors. An important part of this income is distributed among regions and municipalities according to the law, and thus public finances of the sub-national governments also experienced a significant upsurge.

● By the end of 2014, the cycle of high international commodity prices had come to an end, and the country’s public finances were consequently impacted. In this regard, this PEFA evaluation is carried out in the context of more limited financial resources.

The financial situation of the Municipality of La Paz

● The Municipality of La Paz is the capital of the Murillo Province of the Department of La Paz. It has an extension of 3,022 km2, of which only 9% is urban. Since 1899, it is officially the seat of the Executive and Legislative organs of the State.

● The Municipality’s population reached 779,728 inhabitants according to the 2012 Census, and it is estimated that by 2020 it will reach 816,000. Close to 99% of its inhabitants settle in the urban area, which has turned the city of La Paz into the third largest urban center of the country.

● According to the Census, the percentage of population of the municipality of La Paz with Unsatisfied Basic Needs is 14.3%. The

II. BACKGROUND

9

coverage rates for basic services - water at 95.4%, sewerage at 91.0% and electricity at 98.9% of the population - are among the highest in the country, although in rural areas rates are much lower.

● According to the Human Development Report 20157, the Municipality of La Paz contributes 13% to the gross national product, the majority of which is generated in the services sector (public administration, real estate, and financial services) and manufacturing.

● Despite the significant increase in revenues and an improvement in the levels of average schooling of its population during the 2006-2014 boom, La Paz was unable to avoid concentrating its economic activities in the tertiary sector (trade and services), with over half of its population facing under-employment and/or working in the informal sector.

● Furthermore, the 2040 La Paz Plan identifies the following significant challenges for the Municipality:

�� To continue with the Municipality’s process of renovation and transformation, with high-impact infrastructure projects.

�� To employ adaptation and resilience mechanisms to predict the possible effects of climate change and accelerated and unbalanced urban population growth.

�� To strengthen and project the image of the Municipality at the departmental, national and international level.

�� To achieve the integral and sustainable development of the Municipality, for the wellbeing of its citizens.

7 United Nations Development Program (UNDP).

The GAMLP’s fiscal performance

● The ability to address the challenges mentioned above depends heavily on the current financial resources available to the GAMLP. These, in turn, are reliant on the municipal tax collections and the transfers it receives from the national government due to the current distribution scheme of national taxes on economic activity and the exploitation of natural resources, of which revenues from direct taxes to the Hydrocarbons (HDI) are the most significant.

● The fall in international commodity prices and the consequent reduction of national income as of 2015, led to lower transfers of resources to municipalities. For example, in 2016 the GAMLP received Bs. 287.2 million less in HDI transfers as compared to 2014.

● Despite this less favorable context, the GAMLP has gradually reduced its fiscal deficit as a result of prudent management of its public finances. This required readjusting its expenditure to the levels of income, especially in terms of investment in infrastructure, in order keep spending with a high social content virtually unchanged.

● Surpluses from previous terms and borrowing were used to finance the deficit. It should be noted, however, that debt indicators show high levels of sustainability8.

8 The sustainability (80.61%) and solvency (6.61%) indicators are far below the maximum thresholds set out by the Ministry of Finance, of 200% and 20%, respectively.

10

Table Nº1: GAMLP Aggregate Fiscal Data(Percentage of GDP)

Item 2014 2015 2016TOTAL INCOME 0,69% 0,74% 0,63%

Own income 0,27% 0,34% 0,32%Donations 0,00% 0,01% 0,00%Transfers 0,41% 0,39% 0,31%

TOTAL EXPENSES 0,78% 0,80% 0,67%Expenses without interest 0,77% 0,79% 0,66%Interest 0,01% 0,01% 0,00%

ACCUMULATED DEFICIT(Including donations) -0,09% -0,06% -0,04%

Primary deficit -0,08% -0,05% -0,04%Net financing -0,07% -0,05% -0,06%

External 0,03% 0,03% 0,01%Local -0,10% -0,08% -0,07%

PUBLIC DEBT(in financial leverage ratios)Sustainability Indicator(Present value/ Recurrent income t-1) 105,50% 102,07% 80,61%

Liquidity Indicator(Service/ Recurrent income t-1) 6,53% 7,59% 6,61%

GDP at current prices(millions of Bs) 228.003 228.031 233.602

Source: Municipal Secretariat of Finance. GAMLP and INE.

Allocation of resources to GAMLP public policy

● Considering the large areas of local public policy, it’s important to note the significant allocation of resources devoted to human development activities (infrastructure for education, health, social development and sports) and transport, with the implementation of the Municipal Transportation Service (SETRAM) starting in 2016. As a result of more restricted finances, in 2016 there were downward adjustments in administration expenditure and investment in general urban infrastructure.

Table Nº2: Budget Allocations by Policy Area(Percentage of total spending)

Sector 2014 2015 2016Comprehensive risk management 8,8% 8,8% 3,8%

Citizen security 1,5% 2,1% 1,3%Human development 13,8% 3,6% 20,3%

Culture 1,8% 2,4% 1,7%Economic promotion 3,4% 2,4% 2,5%

Infrastructure 14,4% 19,3% 10,8%Environmental management 0,0% 0,0% 2,3%

Transport 6,6% 0,1% 11,3%Administration 45,3% 54,6% 40,6%

Public debt 4,4% 6,7% 5,5%Total 100,0% 100,0% 100,0%Source: Municipal Secretariat of Finance, GAMLP.

● According to the classification by type of expenditure, the relative weight of current expenditure increased to 66.9% in 2016, as a result of the social spending powers entrusted to municipalities by national law and the increase in labor costs. On the other hand, the relative importance of capital expenditure was 33.1%, as a result of the reduction in municipal revenues, which led to a fall in gross fixed capital formation.

11

Table Nº3: Budget Allocations by Categories of Economic Classification(Percentage of total spending)

Item 2014 2015 2016CURRENT EXPENDITURE 61,5% 67,4% 66,9%

Wages and salaries 25,0% 28,3% 29,7%Goods and services 31,8% 34,0% 34,2%

Interests 1,2% 1,2% 1,1%Transfers 3,4% 2,5% 1,6%Others 0,2% 1,3% 0,3%

CAPITAL EXPENDITURE 38,5% 32,6% 33,1%Source: Municipal Secretariat of Finance, GAMLP.

Legal and regulatory framework for the Management of Public Finances in the GAMLP

● The relevant legal and regulatory framework is based on the Political Constitution of the State (CPE) of February 7, 2009, which establishes that Bolivia is a unitary state of “plurinational” law and, therefore, decentralized and autonomous. It also specifies that the country is organized territorially in departments, provinces, municipalities and peasant territories with autonomic capacity to, among other faculties, choose their authorities, define their organizational structure and manage their economic resources.

● Based on the provisions of the CPE, the legal framework is comprised of four main areas:

�� At the municipal level, Law No. 031 for Autonomies and Decentralization (19/07/2010), regulates the autonomy regime at all levels of the State, while Law No. 482 of Autonomous Municipal Governments (09/01/2014) regulates the organizational structure and functioning of local governments, in addition to the management of financial and debt securities.

�� In the area of government administration and control, Law No. 777 of the State’s Comprehensive Planning System (21/01/2016) guides the development planning process in all pertinent public entities. Law No. 1178 of

Government Administration and Control (20/07/1990) regulates systems that ensure proper management of state resources9. Finally, Law No. 2042 of Budgetary Administration establishes the general rules of this process in each fiscal year, for all public entities10.

�� In the area of taxation, Law No. 843 (30/04/2014) establishes the tax structure and the national tax administration. The Tax Code, for its part, establishes the principles, institutions, procedures and the fundamental norms that regulate the legal regime of the tax system. Finally, Law No. 154 of Classification and Definition of Taxes and Regulation for the Creation and / or Modification of Taxes of Domain of the Autonomous Governments (13/07/2011) classifies and defines taxes according to their national, departmental or municipal domain.

�� With regards to transparency and social control, Law No. 004 to Fight Against Corruption, Illegal Enrichment and Wealth Investigation “Marcelo Quiroga Santa Cruz” (31/04/2010) stipulates the mechanisms and procedures to prevent, prosecute and punish acts of corruption committed by public servants. In turn, Law No. 341 of Participation and Social Control (05/02/2013), establishes the general framework of accountability at different levels of the State.

9 There are eight systems governed by the following basic standards: Oper-ations Programming (Supreme Decree No. 225557), Administrative Organization (Su-preme Decree No. 217055), Budget (Supreme Decree No. 225558), Personnel Admin-istration (Supreme Decree No. 26115), Administration of Goods and Services (Supreme Decree No. 181), Treasury (Supreme Decree No. 218056), Integrated Accounting (Su-preme Decrees No. 222957 and No. 227121); and by the following regulations: Exercise of the Attributions of the State Comptroller General (Supreme Decree No. 23215) and Responsibility for Public Function (Supreme Decree No. 23318-A).10 The GAMLP currently has specific regulations for each of the systems, except for the Administration of Goods and Services, since this regulation is in the process of adapting to the new provisions of Law No. 482.

12

GAMLP institutional structure for PFM

● The Municipal Autonomous Government is made up of the Municipal Council, as a legislative, deliberative and supervisory body, and by the Executive Body.

MISION

We are an autonomous, municipal, progressive public entity, that generates public value, whose mission is to improve the quality of life of the inhabitants of the Municipality of La Paz, generating and implementing integral development policies in co-responsibility with our community, administering our territory and providing services with transparency, fairness, quality and warmth; with motivated, committed and highly qualified municipal public servants.

VISION

The Autonomous Municipal Government of La Paz is a cutting-edge, modern and competitive public entity, leaders at the national and international levels in the provision of public services, which improves the quality of life and promotes the integral development of its inhabitants and their environment; recognizing, respecting and managing their diversity and inter-culturalism; with solid, motivated, committed and competent human talent, which forms part of a strengthened institution, with democratic and participatory practice, and which fully exercises its autonomy.

● The Municipal Council, made up of eleven elected councilors, acts through four commissions: Financial Economic Development, Human Development and Cultures, Institutional Management and Planning and Territorial Management.

Box 2: Principal powers of the City CouncilLaw No. 482 of Autonomous Municipal Governments

● Approve the Annual Operating Program, Municipal Budget and their adjustments, presented by the highest executive authority (City Mayor).

● Approve the Municipal Development Plan (now called the Territorial Plan for Integral Development - PTDI) proposed by the Municipal Executive Branch.

● Oversee activities of the Mayor, Secretaries and other authorities of the Municipal Executive Body, its institutions and public companies.

● Approve, modify or suspend the Fees and Patents to the economic activity and special municipal contributions by means of Municipal Law.

● Approve, modify or suspend taxes that are of exclusive domain of the Municipal Autonomous Government by means Municipal Law.

● Approve, through Municipal Law, the issuance and / or purchase of securities, complying with current regulations.

● Approve the constitution of loans, which compromise revenues of the Municipal Autonomous Government, in accordance with current legislation.

● To supervise the implementation of the Municipal Plans, in accordance with the State Comprehensive Planning System (SPIE) and the application of its instruments.

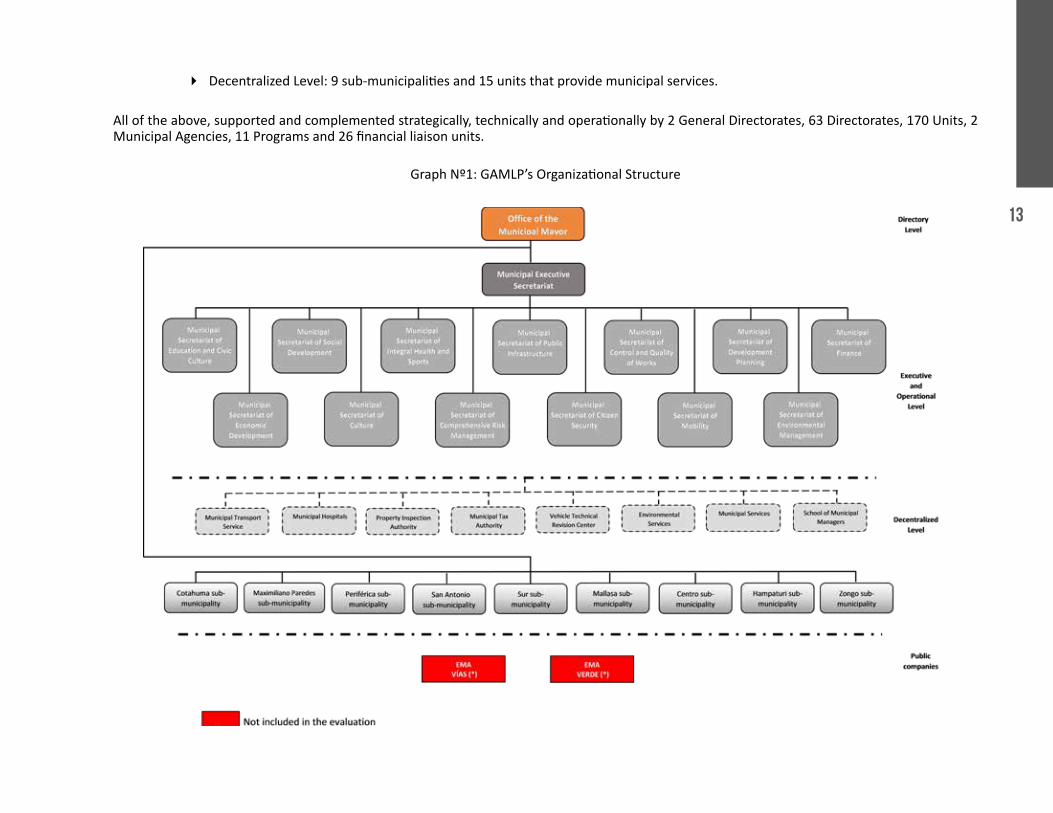

● Headed by the Municipal Mayor, the Municipal Executive Body is composed of 313 organizational units11, which include:

�� Directory Level: Office of the Mayor and Municipal Executive Secretariat.

�� Executive and Operational Level: 13 Municipal Secretariats.

11 These figures do not include public municipal companies

13

�� Decentralized Level: 9 sub-municipalities and 15 units that provide municipal services.

All of the above, supported and complemented strategically, technically and operationally by 2 General Directorates, 63 Directorates, 170 Units, 2 Municipal Agencies, 11 Programs and 26 financial liaison units.

Graph Nº1: GAMLP’s Organizational Structure

14

● The GAMLP serves 23 districts (21 urban and 2 rural) grouped in nine Macro-districts, through its nine sub-municipalities: Cotahuma (I), Maximiliano Paredes (II), Periferica (III), San Antonio (IV), South (V), Mallasa (VI), Center (VII), Hampaturi (VIII) and Zongo (IX).

● According to the Organization and Functions Manual (MOF) for the 2016 Municipal Executive Management Body, the organizational unit responsible for PFM is the Municipal Secretariat of Finance (SMF), which has been organized in two directorates:

�� The Financial Management Department (DGF) manages the Budgetary Financial Systems, Treasury and Accounting, through the issuance of specific regulations for the correct allocation of public resources and the generation of reliable and timely financial information. It has three units: Budget, Treasury and Accounting.

�� The Finance and Financial Analysis Division (DFAF) administers the Public Credit System through the planning and administration of public debt, and conducts economic, financial and fiscal research and analysis. It has two units: Public Credit and Economic and Financial Analysis.

● Finally, as additional strategic support to PFM, the following should be highlighted:

�� The Internal Audit Unit (UAI), which is attached to the Office of the Mayor, exercises internal governmental control over all areas of the GAMLP. It is also the institutional link with the State Comptroller General (CGE).

�� The Municipal Executive Secretariat (SEM) consists of four Directorates (E-Government and Modernization of Management, Human Resources Management, General Administration and Tenders and Contracts), and its functions and activities across the entire GAMLP structure contribute directly or indirectly to PFM.

�� Financial Administrative Units (FAU) serve as operational links between the SMF and the GAMLP areas, for the process and execution of the latter’s administrative and financial management.

15

III. PEFA PFM PERFORMANCE EVALUATION

The Town Hall (inaugurated in 1928) is the seat of the Municipal Council and the Office of the Mayor.

● This chapter presents the PFM assessment of the GAMLP for the period 2014-2016, based on seven pillars raised in the PEFA methodology, which include 31 indicators divided into 94 dimensions, assigning them qualifications based on international best practices.

● The performance of each indicator and dimension is measured on a scale from A to D. A score of A is achieved if there is clear evidence of an internationally recognized level of performance. A score equal to D indicates that the performance is below the basic level.

● Indicators with more than one dimension are scored either by taking the lowest score among their dimensions (M1) or the average score of their scores by dimension (M2).

● Indicator 7 (ID-7) is not considered in this assessment as it is closely associated with national governments. Additional indicator HLG-1, specifically aiming sub-national, entities is included instead.

16

PILLAR I: RELIABILITY OF THE BUDGET

17

INDICATOR: AGGREGATE EXPENDITURE OUTTURN (ID-1)

It assesses the extent to which the executed budget expenditure conforms to the amount initially programmed and approved, and how it is defined and reported in budget documentation and other fiscal reports.

Key aspects of the evaluation

Dimension 1.1 Aggregate Expenditure

● Aggregate expenditure includes budgeted expenditures and those incurred as a result of exceptional events, such as risk management and natural disasters.

● Expenses for such events can be met using contingency accounts or through the expense of each Secretariat or Sector Program.

● Expenditure made with external financing, through loans or grants, are also included in the budget.

Table Nº4: Results of the aggregate expenditure initially approved and executed (in Bs)

Term Initial Budget Budget Execution General Variation (%)

2014 1.920.726.117 2.033.536.435 105.9%2015 2.106.460.103 2.019.685.158 95.9%2016 1.833.010.762 1.855.554.592 101.2%

Source: SIGMA

● The information of the Integrated System for Management and Administration Modernization (SIGMA) is used, as it is the official tool for recording and generating budget and financial information for the entire Bolivian public sector.

● The indicator compares the deviation of the total budget originally approved with respect to the amount actually executed (accrued) during the terms analyzed.

● In 2015 and 2016 deviations were within the range of +/- 5% of the budgeted amount established by good practices. In the 2014 term the observed variation was above the parameter.

Table Nº5. Indicator Rating ID-1 Aggregate Expenditure Outturn

Indicator / Dimension Rating

ID-1 Aggregate Expenditure Outturn A1.1. Aggregate Expenditure A

Rating Methodology: One dimension

18

INDICATOR: EXPENDITURE COMPOSITION OUTTURN (ID-2)

It assesses the extent to which reassignments between major budget categories during budget execution have contributed to the variation of expenditure composition.

Key aspects of the evaluation

Dimension 1.2. Results of the composition of expenditure by functional classification

● Measures the variation between the original approved budget and the executed budget, with respect to its composition by administrative classification (e.g. programmed expenditure on health in relation to actual expenditure on health).

● The variation in the composition of expenditure by administrative classification was lower than the international reference of 10% in 2014 and 2016, but in 2015 it was 29%.

● Variations occur in all expenditure categories, but more so in those executing investment projects.

Dimension 2.2. Results of the composition of expenditure by economic classification

● Measures the variation between the original approved budget and the executed budget, with respect to its composition by economic classification (e.g. budgeted expenditure on wages and salaries in relation to actual expenditure on wages and salaries).

● The main economic classification categories are: wages and salaries, goods and services, fixed capital expenditures, interest, and social benefits.

● The variation was above the minimum recommended in international best practices (15%) in 2014 and 2015. In 2016 alone, the variation was 12.8%.

● Variations occur in all categories of expenditure, but with greater measure and impact in the accounts of interest payment and fixed capital expenses.

Table Nº6: Variation in budgetary expenditure and executed by

administrative and economic classification

YearComposition of variation

(Administrative Classification)

Composition of variation (Economic Classification)

2014 9,5% 16,4%2015 28,8% 20,7%2016 9,8% 12,8%

Source: SIGMA.

Dimension 2.3. Expenses charged to contingency reserves

● This dimension measures the average amount of the expense effectively charged to contingency reserves.

● The average proportion of the executed contingency expenses in relation to the total budget approved between 2014 and 2016 was 0.4%, a percentage lower than 3% established by international good practices.

Table Nº7. Rating of Indicator ID-2. Expenditure Composition Outturn

Indicator / Dimension Rating

ID-2. Expenditure Composition Outturn D+

2.1. Results in the composition of expenditure by functional classification B

2.2. Results in the composition of expenditure by economic classification D

2.3. Expenses charged to contingency reserves ARating Methodology: M1

19

INDICATOR: REVENUE OUTTURN (ID-3)

It evaluates the deviation in revenue between the original approved budget and the amount actually executed, as well as the composition of that deviation by type of income.

Key aspects of the evaluation

Dimension 3.1. Effective Revenue

● The methodology classifies income into three main groups: taxes, donations and other income. It does not consider transfers at the national level or borrowing.

● Deviations for two of the three years (2015 and 2016) were greater than the parameter established by international good practice (the change in at least two of the three years should be between 92% and 116% for a C grade).

Table Nº8: Variation between budget and executed income (in Bs)

Year Initial Budget Executed Budget Deviation

2014 567.489.743,0 617.240.248,1 108,8%

2015 623.549.506,0 775.754.595,4 124,4%

2016 979.207.701,0 778.320.959,7 79,5%Source: SIGMA Municipal.

Dimension 3.2. Income composition results

● According to the PEFA methodology, the main types of income are: taxes, donations, other income (sales of goods and services, royalties and fees) and interest and property rents.

● Variations for two of the three years evaluated (2014 and 2015) are higher than required by best international practice. (For a C grade, the change in the composition of income should not exceed 15% in two of the last three years evaluated).

Table Nº9: Variation of income composition

Year Composition variation

2014 17,3%

2015 16,2%

2016 10,1%Source: SIGMA.

● In 2014, the differences in taxes were due to the GAMLP tax regularization program and the receipt of larger donations from international organizations.

● In 2015, once again, higher tax revenues were achieved thanks to the same regularization program and higher than projected donations. In 2016 the large donations persisted, but tax revenues were reduced.

Table Nº10. Rating of Indicator ID-3. Revenue Outturn

Indicator / Dimension Rating

ID-3. Net Income Results D

3.1. Effective Revenue D

3.2. Income composition results DRating Methodology: M2

20

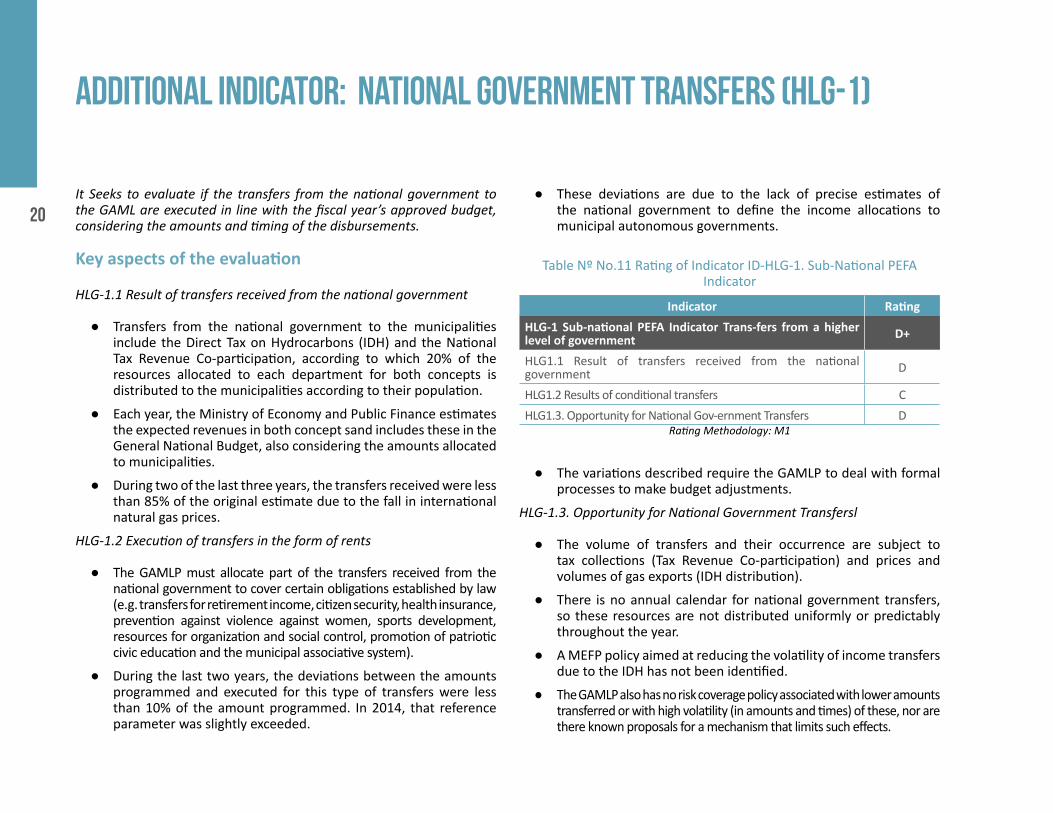

ADDITIONAL INDICATOR: NATIONAL GOVERNMENT TRANSFERS (HLG-1)

It Seeks to evaluate if the transfers from the national government to the GAML are executed in line with the fiscal year’s approved budget, considering the amounts and timing of the disbursements.

Key aspects of the evaluation

HLG-1.1 Result of transfers received from the national government

● Transfers from the national government to the municipalities include the Direct Tax on Hydrocarbons (IDH) and the National Tax Revenue Co-participation, according to which 20% of the resources allocated to each department for both concepts is distributed to the municipalities according to their population.

● Each year, the Ministry of Economy and Public Finance estimates the expected revenues in both concept sand includes these in the General National Budget, also considering the amounts allocated to municipalities.

● During two of the last three years, the transfers received were less than 85% of the original estimate due to the fall in international natural gas prices.

HLG-1.2 Execution of transfers in the form of rents

● The GAMLP must allocate part of the transfers received from the national government to cover certain obligations established by law (e.g. transfers for retirement income, citizen security, health insurance, prevention against violence against women, sports development, resources for organization and social control, promotion of patriotic civic education and the municipal associative system).

● During the last two years, the deviations between the amounts programmed and executed for this type of transfers were less than 10% of the amount programmed. In 2014, that reference parameter was slightly exceeded.

● These deviations are due to the lack of precise estimates of the national government to define the income allocations to municipal autonomous governments.

Table Nº No.11 Rating of Indicator ID-HLG-1. Sub-National PEFA Indicator

Indicator RatingHLG-1 Sub-national PEFA Indicator Trans-fers from a higher level of government D+

HLG1.1 Result of transfers received from the national government D

HLG1.2 Results of conditional transfers CHLG1.3. Opportunity for National Gov-ernment Transfers D

Rating Methodology: M1

● The variations described require the GAMLP to deal with formal processes to make budget adjustments.

HLG-1.3. Opportunity for National Government Transfersl

● The volume of transfers and their occurrence are subject to tax collections (Tax Revenue Co-participation) and prices and volumes of gas exports (IDH distribution).

● There is no annual calendar for national government transfers, so these resources are not distributed uniformly or predictably throughout the year.

● A MEFP policy aimed at reducing the volatility of income transfers due to the IDH has not been identified.

● The GAMLP also has no risk coverage policy associated with lower amounts transferred or with high volatility (in amounts and times) of these, nor are there known proposals for a mechanism that limits such effects.

21

PILLAR II: TRANSPARENCY OF PUBLIC FINANCES

22

INDICATOR: BUDGET CLASSIFICATION (ID-4)

It evaluates the different budget classifications used by the GAMLP in the processes of formulation, execution and accounting record of the budget, in relation to international standards, for the last fiscal year finalized (2016).

Key aspects of the evaluation

Dimension 4.1. Budget classification

● According to the Basic Norms of the Budget System, Regulations of Law No. 1178 of Government Administration and Control, budget classifiers are mandatory for all public-sector entities, including the GAMLP.

● These classifiers are approved and updated annually by the Ministry of Economy and Public Finance.

● The group of Budget Classifiers for the 2016 budget process are cited in Table 11.

Table Nº12: Budget Classifiers 2016

Type Classifier1. General 1.1 Institutional Classifier2. Income 2.1 Resources by Sector Classification

3. Expenditure

3.1 Object of Expenditure Classifier3.2 Purpose and Function by Expenses Classification3.3 Financing Sources Classifier3.4 Financing Organizations Classifier3.5 Economic Sector Classifier3.6 Geographic Classifier

Source: Budget Classifiers 2016. MEFP.

● By 2016, the Ministries of Economy and Public Finance and Development Planning determined that the formulation of the expenditures budget be carried out through the methodology of program budgeting.

● Furthermore, budgetary programs should be linked to the Comprehensive State Planning System (SPIE) through long, medium and short-term plans.

● Municipal governments must adopt a structure that distinguishes programs for the Municipal Executive, for the Municipal Council, and for the Central Administration, in addition to programs by Municipal Secretariats and non-assignable programs.

● In addition, budget programs should be linked to the pillars and goals of the National Government’s Economic and Social Development Plan (PDES).

● According to the Institutional Classifier in force for 2016, the GAMLP is identified with budget code 1201, so it is governed by national regulations, using the classifiers described.

● The budget execution and its accounting are carried out according to the approved GAMLP budget. Its processes maintain the budget classifiers and their linkage with the Single Plan of Accounting Accounts whose equivalents are incorporated in the municipal systems for its automatic application.

Table Nº13. Rating of Indicator ID-4. Budget Classification

Indicator / Dimension Rating

ID-4. Budget Classification A

4.1. Budget Classification ARating methodology: One dimension

23

INDICATOR: BUDGET DOCUMENTATION (ID-5)

It evaluates the integrity of the information provided in the documentation of the draft annual budget submitted to the Legislative Branch. The evaluation is made in relation to the last budget proposal submitted to the City Council (2017).

Key aspects of the evaluation

Dimension 5.1. Budget documentation

● The GAMLP annually submits to the Municipal Council the Annual Operational Program (POA) and Budget along with supporting documents.

● The diagnosis of the basic and additional documents identified by the methodology with reference to international good practices is presented in Table 13.

Table Nº14: Information included in the budget project 2017

Elements Includes

Basic elements:1. Forecasting the fiscal deficit or surplus YES2. Budget clearance for the previous year YES3. Current year’s budget NO4. Aggregate budgetary data on income and expenditure YESAdditional elements:5. Financing of the deficit YES6. Macroeconomic assumptions YES7. Balance of public debt YES8. Financial assets NO9. Summary information on existing fiscal risks NO10. Explanation of the budgetary implications of new initiatives NO11. Medium-term fiscal forecasts documentation NO12. Quantification of tax expenditures NO

Source: Municipal Secretariat of Finance

● The conclusion is that the GAMLP, through its Municipal Secretariat of Finance presents 3 out of 4 basic elements and 3 out of 8 additional elements, as defined by the PEFA methodology, to the Municipal Economic Development Committee of the Municipal Council.

Table Nº15. Rating of Indicator ID-5.Budget Documentation

Indicator / Dimension RatingID-5. Budget Documentation C

5.1 Budget Documentation CRating methodology: One dimension

24

INDICATOR: GOVERNMENT OPERATIONSNOT INCLUDED IN FINANCIAL REPORTS (ID-6)

It examines whether expenditures and revenues of extra budgetary entities and expenditures and revenues related to extra budgetary activities of budget entities are insignificant, or whether such revenues and expenditures should be included in the GAMLP ‘s ex - post financial reports. The evaluation is for year 2016.

Key aspects of the evaluation

Dimension 6.1 Expenses outside financial reports

● The GAMLP does not have extra budgetary entities; all units are within its budget. Neither does it have trusts.

● The budget presented by the Municipal Executive to the Municipal Council covers all levels of the GAMLP, including the legislative, executive, operational and decentralized levels.

● Existing national and sub-national regulations state that absolutely all GAMLP spending activities must be registered in the Municipal Integrated System for Management and Administration Modernization (SIGMA).

Dimension 6.2 Income not included in financial reports

● Existing national and sub-national regulations require all revenues to be recorded in the budget.

● Also, any resources collected by the GAMLP must be automatically transferred to the Municipal Single Account, in close coordination with the Ministry of Economy and Public Finance.

● The income from external donors or creditors for project financing should also be recorded, in coordination with the Vice Ministry of Public Investment and External Financing.

Dimension 6.3 Extra budgetary financial reports

● As described in previous dimensions, the GAMLP does not have extra budgetary entities or activities, so the evaluation of this dimension is not applicable.

Table Nº16 Rating of the Indicator ID-6. Operations not included in financial reports

Indicador / Dimensión RatingIndicator / Dimension A ID-6. Government operations not included in financial reports A6.1 Expenditure not included in financial re-ports A6.2 Income not included in financial reports NA6.3. Extra budgetary financial reports

Rating Methodology: M2

25

INDICATOR: INFORMATION ON SERVICE DELIVERY PERFORMANCE (ID-8)

It reviews the information about the performance in the delivery of services that is included in the draft budget and in the budget implementation reports at the end of the year. It also determines whether performance audits or assessments are carried out and the extent to which information is collected and recorded on the resources received for the provision of services.

Key aspects of the evaluation

● The GAMLP provides a variety of public services, with emphasis on health, education, mass transportation and cadastral registration.

Dimension 8.1 Planning of performance in service delivery (with information for 2017)

● The GAMLP has the Integral Plan La Paz 2040, the Institutional Strategic Plan 2014-2018 and the Annual Operational Program as long, medium and short-term planning instruments, respectively.

● These plans do not have indicators for measuring performance in the provision of public services. For this reason, the 2017 budget also does not consider these indicators.

Dimension 8.2 Results of performance in service delivery (with information to 2016)

● The GAMLP 2016 budget supporting documentation does not include indicators to measure the performance of public services.

● Approved and executed budget reports do not consider improvements in service delivery through the monitoring of performance indicators.

● Management reports and written publications, however, include information on the activities carried out and on the products of all service delivery units, including the amounts executed.

Dimension 8.3 Resources received by the units responsible for service delivery (with information of last three terms)

● Whether there is information on resources received by units responsible for the provision of services in at least two important secretariats, health and education, is evaluated.

● In this regard, the GAMLP publishes annual budget execution reports where information on education and health services is complete and disaggregated, and its sources of funding can be identified.

Dimension 8.4 Evaluation of the performance of service delivery (with information of last three terms)

● The GAMLP has not performed independent evaluations of the service delivery units during the 2014-2016 period.

● However, it has made specific evaluations of certain programs (e.g. Central Urban Park, and “Real Neighborhoods and Communities”) to measure its performance.

Table No17. Rating of Indicator ID-8. Information on performance of service delivery

Indicator / Dimension RatingID-8. Information on performance of service delivery C+8.1 Planning of performance in service deliv-ery C8.2 Results of performance in service delivery C8.3 Resources received by the units responsi-ble for service delivery A

8.4 Evaluation of the performance of service delivery DRating Methodology: M2

26

INDICATOR: PUBLIC ACCESS TO FISCAL INFORMATION (ID-9)

Table Nº18: Access to public fiscal information –2016

Information / Report Is there public access (Yes/No)

Basic elements:Draft annual budget docu-mentation YESApproved budget YESBudget execution reports for the current year NOAnnual report on Budget execution YESAudited annual financial report, as well as external audit report. NO

Pre-budget statement NOInformation of services de-livered to the community YESSummary of the budget project YESInformation on rates, tariffs and taxes NO

Source: GAMLP PEFA Evaluation

It assesses the integrity of publicly available fiscal information, taking as assessment parameters a set of pieces of information considered fundamental to be made available to the public. The evaluation is made in relation to the last finalized fiscal year (2016).

Key aspects of the evaluation

● The GAMLP produces a significant amount of information and technical documents. The department that consolidates this process is the Directorate of Research and Municipal Information of the Municipal Secretariat for Development Planning.

Dimension 9.1. Public access to fiscal information

● It is essential the public have access to nine elements (basic and additional).

● As can be seen in Table No. 18, the GAMLP makes three (3) of the basic elements and two (2) of the additional elements required for this indicator available to the public.

Table Nº 19. Rating of Indicator ID-9. Public access to fiscal information

Indicator / Dimension RatingID-9. Public Access to Fiscal Infor-mation D9.1. Public Access to fiscal infor-mation D

Rating Methodology: One dimension

27

PILLAR III: MANAGEMENT OF ASSETS AND LIABILITIES

28

INDICATOR: FISCAL RISK REPORTING (ID-10)

It analyzes the extent to which the fiscal risks faced by the GAMLP are reported. The analysis is made in relation to the last finalized fiscal year (2016).

Key aspects of the evaluation

● Fiscal risks may arise from adverse macroeconomic situations, the financial position of municipal enterprises, contingent program liabilities and GAMLP activities.

Dimension 10.1 Oversight of public companies and corporations

● The GAMLP has two municipal companies, EMAVIAS (since 2006) and EMAVERDE (since 2003). Since 2011 they operate with their own resources and are financed through contracts they make with other GAMLP organizational units and with private entities.

● The Business and Public Services Department of the GAMLP is in charge of monitoring the activities of municipal companies and the achievement of their performance goals.

● According to national regulations, companies must submit their Financial Statements until February 28 of the year following the closing fiscal year. In addition, they must submit monthly financial execution reports to the GAMLP, which are also sent to the Ministry of Economy and Public Finance.

● Despite all the above, and considering all available information, the GAMLP is not currently producing annual aggregate reports on these companies.

Dimension 10.2. Oversight of sub-national governments

● This dimension is not applicable for the purpose of this evaluation.

Dimension 10.3. Contingent liabilities and other tax risks

● The contingent liabilities to which the methodology refers to consist of general guarantees for different types of loans and various types of insurance.

● According to national regulations, the GAMLP cannot grant guarantees. Likewise, it does not currently participate in any type of insurance plan.

● The contingent liabilities recognized by the GAMLP refer mainly to pensions, labor litigation and / or criminal trials. They are duly monitored by the Accounting Unit in coordination with the General Directorate of Legal Affairs.

Table Nº 20. Rating of Indicator-10.Fiscal risk reporting

Indicator / Dimension RatingID-10. Fiscal Risk Reporting B 10.1 Oversight of public companies and corporations B10.2 Oversight of sub-national governments NA10.3 Contingent liabilities and other tax risks B

Rating Methodology: M2

29

INDICATOR: PUBLIC INVESTMENT MANAGEMENT (ID-11)

It analyzes whether the GAMLP performs economic analysis, technical selection and monitoring of public investment projects. In addition, it assesses whether medium-term projections of capital and recurrent costs are made. The evaluation is carried out with information on the major investment projects included in the 2016 Budget.

Key aspects of the evaluation

Dimension 11.1 Economic analysis of investment projects

● The economic analysis of GAMLP investment projects is institutionally based on the Law on Autonomies and Decentralization, the Specific Regulation for the National System of Public Investment and Supreme Decree No. 29894 passed on February, 2009.

● Investment projects for 2016 come from the La Paz 2040 Investment Plan and were included in the Annual Operational Program (POA) and the Budget. The Municipal Secretariat for Development Planning (SMPD) evaluates the economic analysis of the projects presented.

● Public investment projects have pre-investment studies and cost-benefit and / or cost-efficiency analyses.

● The results of the economic analysis are recorded in the Investment Information System and published in reports.

Dimension 11.2 Selection of investment projects

● The La Paz 2040 Investment Plan has rigorous criteria and procedures for prioritizing and selecting multi-management projects. This process is handled by the SMPD.

● In 2016, the Territorial Plan for Integral Development 2016-2020 of the Municipality of La Paz was also formulated, based on the projects from the La Paz 2040 Investment Plan, while linking them with the strategic plans of the Autonomous Departmental Government of La Paz and the central government’s Vice Ministry of Autonomies and Decentralization.

Dimension 11.3 Cost determination of investment projects

● Total costs of GAMLP projects are divided into investment and operating.

● All costs are recorded in the Municipal Information System (SIM) and the National Information System (SISIN).

● Although this information contributes to the development of the investment budget, the GAMLP does not include it in the supporting documents of the POA nor the Budget.

Dimension 11.4 Oversight of investment projects

● The GAMLP periodically monitors the administrative, physical and financial progress of all investment projects through SIM reports. The monthly aggregate information is also recorded in the SISIN.

● The Municipal Finance Department performs the monitoring of the process, detects deviations and recommends adjustment or correctional measures.

● Follow-up reports are done under standard procedures for all investment projects, according to Law No. 2042 of Budgetary Administration.

Table Nº 21. Rating of Indicator ID-11. Public investment management

Indicator / Dimension RatingID-11. Management of public investment B+11.1 Economic analysis of investment projects A11.2 Selection of investment projects A11.3 Cost determination of investment projects D11.4 Oversight of investment projects A

Rating Methodology: M2

30

INDICATOR: PUBLIC ASSET MANAGEMENT (ID-12)

It evaluates the management and monitoring of municipal public-sector assets and the transparency of their eventual disposal. The analysis is done for the last fiscal year (2016).

Key aspects of the evaluation

Dimension 12.1 Monitoring of financial assets

● All GAMLP financial assets are recorded in their Financial Statements. The main financial assets are shares in the Single Registry for Tax Administration (RUAT), EMAVIAS and EMAVERDE. Currently, these financial assets are not generating dividend income or capital gains.

● Although there is a record of all GAMLP’s financial assets, they are not being valued at their market value in accordance with international standards.

Dimension 12.2 Monitoring of non-financial assets

● The Directorate of General Administration (DAG) is in charge of monitoring non-financial assets, keeping updated records of them through existing information systems. This allows for the systematic management of non-financial assets, in addition to assisting in their maintenance and investment plans.

Table Nº22: Categories of GAMLP non-financial assets

AssetsFixed – Buildings and plants

Fixed – Machinery and equip-mentFixed – Other assets

StocksValuable Objects

Non- produced - LandNon- produced - Other non-produced intangibles

Source: GAMLP

● The DAG monitors non-financial assets through the Municipal Property Management System for movable assets, the Warehouse Management and Management System for consumer goods and the Municipal Property Registration System for municipal property, linked to the Territorial Information System. All these systems have adequate security procedures and mechanisms.

Dimension 12.3 Transparency in the disposal of assets

● The procedures for transfer and disposal of assets are in accordance with Executive Resolution 284/2014 based on the Basic Standards of the System of Administration of Goods and Services. Transfers to third parties are made through temporary provisions that preserve ownership for the GAMLP. In the case of municipal public companies, these transfers are consolidated in the Financial Statements of the GAMLP at the end of the fiscal year.

● GAMLP financial reports include reports on disposal and transfers with complete information about the original cost, value of the disposal and dates of purchase and disposal.

Table Nº 23. Rating of the Indicator ID-12. Public asset management

Indicator / Dimension RatingID-12. Management of public assets B12.1 Monitoring of financial assets C12.2 Monitoring of non-financial assets A12.3 Transparency in the disposal of assets B

Rating Methodology: M2.

31

INDICATOR: DEBTMANAGEMENT (ID-13)

Evaluates debt management (internal and external) and guarantees. It seeks to determine whether there are good registration and control practices to ensure that management mechanisms are effective and efficient.

Key aspects of the evaluation

Dimension 13.1. Registration and preparation of debt and guarantee reports

● The Finance and Financial Analysis Division (DFAF) of the GAMLP is in charge of the recording and reporting of internal and external debt (the latter intermediated by the National Government).

● The Municipal Debt Management and Administration System, which is operated under appropriate procedures, exists for registration and management of debt,

● The reconciliation of accounts and payments is carried out with the Central Bank of Bolivia on a semi-annual basis. Reconciliation and confirmation of internal debt payments is done monthly.

● The DFAF produces a monthly bulletin that includes balances and conditions of the debt in addition to the type of creditor, but does not include residual terms or risk indicators.

● The Municipal Finance Secretariat submits a quarterly budget execution report to the Municipal Council, which includes the municipal debt situation. However, the report is not publicly accessible.

Dimension 13.2. Approval of debt and guarantees

● The GAMLP operates within the context of a strict national legal framework that assigns powers to contract and issue debt and establish limits and conditions of indebtedness.

● The contracting of external debt is authorized by law of the Plurinational Legislative Assembly of Bolivia and the contracting of internal debt is authorized by the General Directorate of Public Credit (DGCP), part of the Vice Ministry of Treasury and Public Credit (VTCP) of the Ministry of Economy and Public Finance (MEFP).

● The Municipal Autonomous Government Act establishes that the Municipal Council must approve the issuance of securities and credits that compromise GAMLP’s revenues, ensuring compliance with MEFP rules

● The MEFP regulates sub-national indebtedness according to the Basic Norms of the Public Credit System (NBSCP), so that the borrowing strategies of regional and local entities are consistent with their development plans and financial capacity.

● The GAMLP complies strictly with the legislation and procedures in force regarding debt of sub-national entities. Its current debt ratios are well below the maximum limits established by the MEFP.

Dimension 13.3. Debt management strategy

● In the last three fiscal years, the GAMLP did not have an explicit medium-term debt management strategy based on its needs, which analyzes the market risks - interest rates, exchange rates and refinancing - that it faces.

● Since 2014, the DFAF has prepared a debt sustainability analysis every six month, the same one that was publicly presented for the first time in 2016.

Table Nº 24. Rating of Indicator ID-13. Debt management

Indicator / Dimension RatingID-13. Debt management C+ 13.1 Registration and preparation of debt and guarantees reports C13.2 Debt and guarantee approval A13.3. Debt management strategy D

Rating Methodology: M2.

32

PILLAR IV: POLICY-BASEDFISCAL STRATEGY AND BUDGETING

33

INDICADOR: MACROECONOMIC AND FISCAL FORECASTING (ID-14)

It measures the capacity of the municipal government to formulate sound macroeconomic and fiscal forecasts, so as to be able to design a sustainable fiscal strategy and give greater predictability to budgetary allocations. It assesses the capacity of the municipal government to estimate the fiscal impact of possible changes in economic conditions. The analysis is made considering the last three fiscal years finalized.

Key aspects of the evaluation

Dimension 14.1. Macroeconomic forecasting

● The GAMLP’s Municipal Finance Secretariat (SMF) has been preparing medium-term macroeconomic forecasts since the year 2014, using a macroeconomic model that allows projecting the evolution of the main macroeconomic variables under different scenarios. This analysis is currently incorporated into the entity’s debt sustainability analysis.

● The macroeconomic projections prepared by the GAMLP are not being used to guide the budget process, with the exception of the debt budget.

● On the other hand, these projections have not been examined by an entity other than the one that produces them, as required by good international practices.

Dimension 14.2. Fiscal forecasting

● The different revenue generating units prepare estimates of revenue to be received with the technical support and supervision of the SMF. It is important to highlight the Municipal Tax Administration, which has the capacity to estimate its own income in the short and medium term.

● The current and capital expenditure estimates for the budget year are carried out by all GAMLP units, although this practice is not applied for subsequent years, as this task falls under the SMF.

● Although estimates of revenues, expenses and fiscal balances are prepared in a timely manner, they are not included in the documents accompanying the budget.

● Nor are explanations given about the projections of income and expenses presented in previous years and how close they were to actual implementation.

Dimension 14.3. Macro fiscal sensitivity analysis

● The GAMLP has been analyzing alternative fiscal scenarios during the period of analysis to support the development of the debt sustainability analysis.

● These scenarios are sensitivity tests for the expected behavior of critical variables, such as the hydrocarbons price, which affects a set of variables in the economy, including transfers from the national government to GAMLP.

● This analysis was first made public in July 2016, as part of the document “Managing GAMLP Financing”.

Table Nº 25. Rating of the Indicator ID-14. Macroeconomic and fiscal forecasting

Indicator / Dimension RatingID-14. Macroeconomic and Fiscal Forecasting C14.1. Macroeconomic forecasting D14.2. Fiscal forecasting C14.3. Macro fiscal sensitivity analysis B

Rating Methodology: M2

34

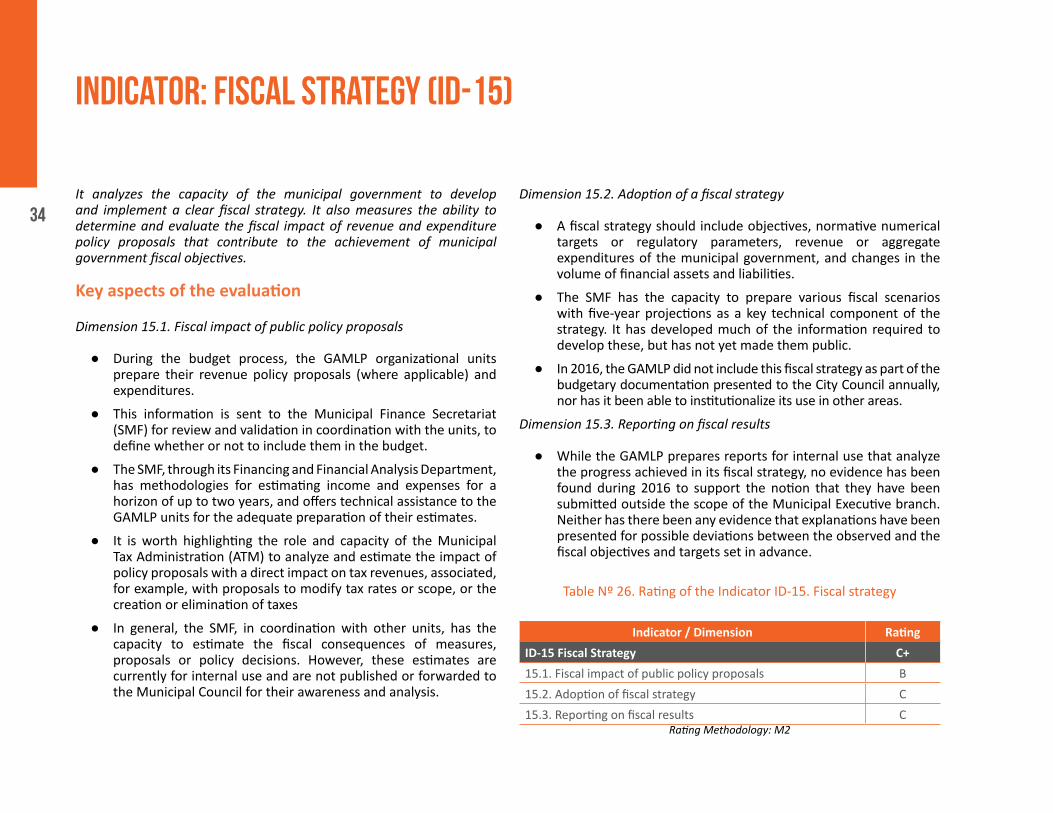

INDICATOR: FISCAL STRATEGY (ID-15)

It analyzes the capacity of the municipal government to develop and implement a clear fiscal strategy. It also measures the ability to determine and evaluate the fiscal impact of revenue and expenditure policy proposals that contribute to the achievement of municipal government fiscal objectives.

Key aspects of the evaluation

Dimension 15.1. Fiscal impact of public policy proposals

● During the budget process, the GAMLP organizational units prepare their revenue policy proposals (where applicable) and expenditures.

● This information is sent to the Municipal Finance Secretariat (SMF) for review and validation in coordination with the units, to define whether or not to include them in the budget.

● The SMF, through its Financing and Financial Analysis Department, has methodologies for estimating income and expenses for a horizon of up to two years, and offers technical assistance to the GAMLP units for the adequate preparation of their estimates.

● It is worth highlighting the role and capacity of the Municipal Tax Administration (ATM) to analyze and estimate the impact of policy proposals with a direct impact on tax revenues, associated, for example, with proposals to modify tax rates or scope, or the creation or elimination of taxes

● In general, the SMF, in coordination with other units, has the capacity to estimate the fiscal consequences of measures, proposals or policy decisions. However, these estimates are currently for internal use and are not published or forwarded to the Municipal Council for their awareness and analysis.

Dimension 15.2. Adoption of a fiscal strategy

● A fiscal strategy should include objectives, normative numerical targets or regulatory parameters, revenue or aggregate expenditures of the municipal government, and changes in the volume of financial assets and liabilities.

● The SMF has the capacity to prepare various fiscal scenarios with five-year projections as a key technical component of the strategy. It has developed much of the information required to develop these, but has not yet made them public.

● In 2016, the GAMLP did not include this fiscal strategy as part of the budgetary documentation presented to the City Council annually, nor has it been able to institutionalize its use in other areas.

Dimension 15.3. Reporting on fiscal results

● While the GAMLP prepares reports for internal use that analyze the progress achieved in its fiscal strategy, no evidence has been found during 2016 to support the notion that they have been submitted outside the scope of the Municipal Executive branch. Neither has there been any evidence that explanations have been presented for possible deviations between the observed and the fiscal objectives and targets set in advance.

Table Nº 26. Rating of the Indicator ID-15. Fiscal strategy

Indicator / Dimension RatingID-15 Fiscal Strategy C+15.1. Fiscal impact of public policy proposals B15.2. Adoption of fiscal strategy C15.3. Reporting on fiscal results C

Rating Methodology: M2

35It examines the extent to which the expenditure budget is formulated with a medium-term vision and within explicit expenditure limits established for the medium term. It also analyzes the extent to which annual budgets are derived from medium-term estimates and the degree of articulation between medium-term budget estimates and strategic plans. The evaluation is made based on the last short and medium-term budgets presented and approved by the Municipal Council.

Key aspects of the evaluation

Dimension 16.1 Medium-term expenditure estimations

● The medium-term instruments available to the GAMLP are the Integral Plan La Paz 2040, the Institutional Strategic Plan (PEI) 2014-2018 and the Territorial Plan for Integral Development (PTDI) 2016-2020, the latter required by the national government. The level of consistency between these documents is adequate.

● Although these three plans have a multi-year concept, they have not yet been able to influence the behavior of the annual budget, since the budget formulation guidelines are elaborated by the Ministry of Economy and Public Finance (MEFP), an entity that does not include the results and indicators offered by medium-term plans in its budgeting model.

Dimension 16.2. Medium-term spending limits

● The expenditure limits for the financial year are set at the beginning of the process by the MEFP, identified by the source of the funds to be used.

● These spending limits prevent expenditure from exceeding the availability in the budget year. However, this procedure is done with an annual perspective and not in the medium-term.

Dimension 16.3. Articulation of strategic plans and medium-term budgets

● The 2040 Plan is the GAMLP’s strategic plan, which supports the IEP (2014-2018) and the PTDI 2016-2020 as medium-term planning instruments.

● This foundation and its regular updating will be essential elements for building annual plans and budgets consistent with its medium-term peers, a task that should be addressed with priority by the GAMLP. Efforts should also be made to implement budgeting based on performance indicators.

Dimension 16.4. Consistency of budgets with estimates from the previous year

● About 50% of the GAMLP budget depends on transfers received from the national government. For this reason, budgeting and medium-term estimates do not have a fully predictable or fully controlled calculation basis.

Table Nº 27. Rating of Indicator ID-16. Medium-term perspective in expenditure budgeting

Indicator / Dimension RatingID-16 Medium-term perspective in expenditure budgeting D

16.1 Medium-term expenditure estimations D16.2 Medium-term spending limits D16.3 Articulation of strategic plans and medium-term budgets D

16.4 Consistency of budgets with estimates from the previous year D

Rating Methodology: M2

INDICATOR: MEDIUM-TERM PERSPECTIVE IN EXPENDITURE BUDGETING (ID-16)

36

INDICATOR: BUDGET PREPARATION PROCESS (ID-17)

It measures the effectiveness of the participation of relevant actors, including political authorities, in the process of preparing the budget, and establishes whether such participation is orderly and timely. The first dimension is evaluated with information from 2016, while the following two use information from the period 2014-2016.

Key aspects of the evaluation

Dimension 17.1. Budget schedule

● The GAMLP has as usual practice to start the budgeting process in the month of March or April of the previous year, with the realization of zone-specific workshops of prioritization of demand. However, this process has not yet been formalized through a specific instruction.

● The Ministry of Economy and Public Finance (MEFP) officially granted the GAMLP a four-week deadline to prepare, register and submit the preliminary draft budget to the MEFP itself and the Ministry of Development Planning.

● However, the PEFA evaluation measures the effective timeframe that would be granted to GAMLP units to carry out budget-building tasks. The timeframe was only seven days, and although all the units managed to present their contributions in time, it is considered a very short time period with respect to international practices.

Dimension 17.2. Guidelines for budget preparation

● The main instruments guiding the formulation of the Annual Operational Program and the Budget are the Budget Formulation Guidelines and the Specific Regulation of the Operations Programming System.

● In addition, the Municipal Mayor issues an annual instruction in which the deadlines and procedures for drawing up the budget are established.

● The Municipal Secretary of Development Planning and the Municipal Finance Secretariat (SMF) are responsible for defining and confirming budget ceilings for each organizational unit.

● All GAMLP units receive various budgeting instructions.

● Finally, SMF reviews and consolidates budgets, prepares the budget proposal for approval of the Municipal Mayor, who in the last instance refers the same to the Municipal Council.

Dimension 17.3. Presentation of the budget to the Legislative Power

● Between 2013 and 2016 the draft annual operating program and budget were presented in a timely manner to the Municipal Council (Municipal Legislative branch). In all cases the delivery was made at least four months before the beginning of the corresponding fiscal year and always within the time limits imposed by national regulations.

Table No28. Rating of Indicator ID-17. Budget preparation process

Indicator / Dimension Rating

ID-17. Budget preparation process B

17.1. Budget schedule C

17.2. Guidelines for Budget preparation C

17.3. Presentation of the Budget to the legisla-tive power ARating Methodology: M2

37

INDICATOR: LEGISLATIVE SCRUTINY OF BUDGETS (ID-18)

It assesses the nature and scope of legislative scrutiny of the annual budget. It evaluates the extent to which the Municipal Council examines, discusses, and approves it, and whether procedures are established and respected. It also reviews the existence of rules on amendments to the Budget in the course of the exercise, without prior approval of the Municipal Council.

Key aspects of the evaluation

Dimension 18.1. Scope of budget scrutiny

● Municipal Council scrutiny of the 2016 GAMLP budget began on August 27, 2015, when the Municipal Mayor forwarded the Annual Operational Plan (POA) and Budget to the Municipal Council, requesting its approval.

● Upon receipt of the information, the Municipal Council initiated an active scrutiny process, sending the POA and budget to all Councilors and especially to the Council’s Economic and Financial Development Committee.

● This Committee, the entity mainly responsible for the analysis and revision of the documentation, prepared a report to the plenary of the Municipal Council, which was analyzed and debated in public session, with the consequent approval of the POA and budget by majority vote.

● Finally, the Municipal Mayor proceeded to promulgate the corresponding Municipal Law. This process was developed in eight calendar days. However, the evaluation has identified an informal coordination process that began thirty days earlier.

Dimension 18.2. Legislative procedures for budget scrutiny