establishing a baseline for running cost – potential methodology

Upload: pusat-informasi-virtual-air-minum-dan-penyehatan-lingkungan-piv-ampl

Post on 13-Jul-2015

170 views

TRANSCRIPT

1

Establishing a Baseline for Running Cost – Potential

Methodology

Presented by Michael Hunter

Budget Advisor,

Australian Department of Finance and Deregulation

2

Example of a Baseline

Baseline is the cost of implementing the current Government policy over the Budget year and forward years.

It is the starting point for an MTEF.For Example, the baseline for an aid program is ($m):

2008 2009 2010 2011National Literacy program 43.2 62.6 186.3 248.2

3

(i) Running Cost

Definition:

Are those costs that could be under the control of managers to allow flexibility in the use of inputs in order to get more efficient program delivery (e.g personnel and materials expenditure)

4

Running Cost – Steps for Establishing the Baseline

1. Identify running cost versus non-running cost2. Identify length of program3. Enter Input Costs Items & Volumes for the Budget Year

and Forward Years4. Map account codes of inputs into Expense Groups that

have similar cost drivers (used for projecting prices, external control under PBB)

5. Ministry of Finance to apply parameters to the prices over the forward years.

1. Identify running cost versus non-running cost

Identify whether the program and all its elements are running cost or non-running cost.

If there are multiple elements, than each element needs to have the baseline established separately.

2. Identify length of program

Identify Government policy to determine if the program is either terminating in a particular year or ongoing policy.

MTEF is based on budgeting for the Budget Year and over the four forward years.

7

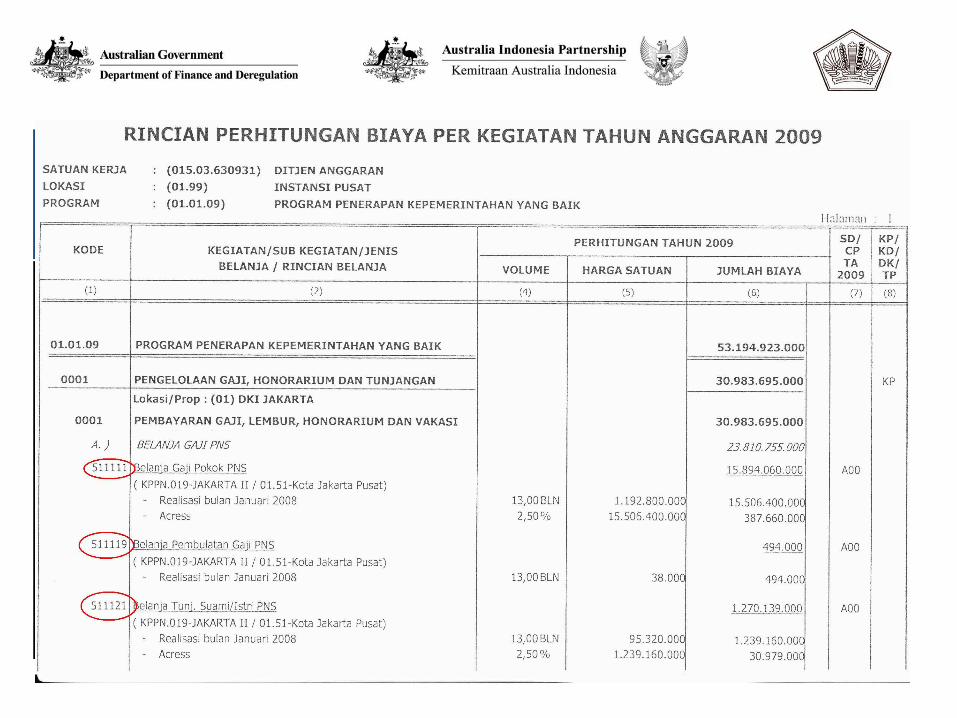

3. Enter Input Costs & Volumes for the Budget Year and Forward Years

8

Volume over the Forward Years will usually be constant.

If the Government wants to undertake additional work during the Forward Years, than that will be “New Policy”.

MTEF is based on “Existing Policy” only.

9

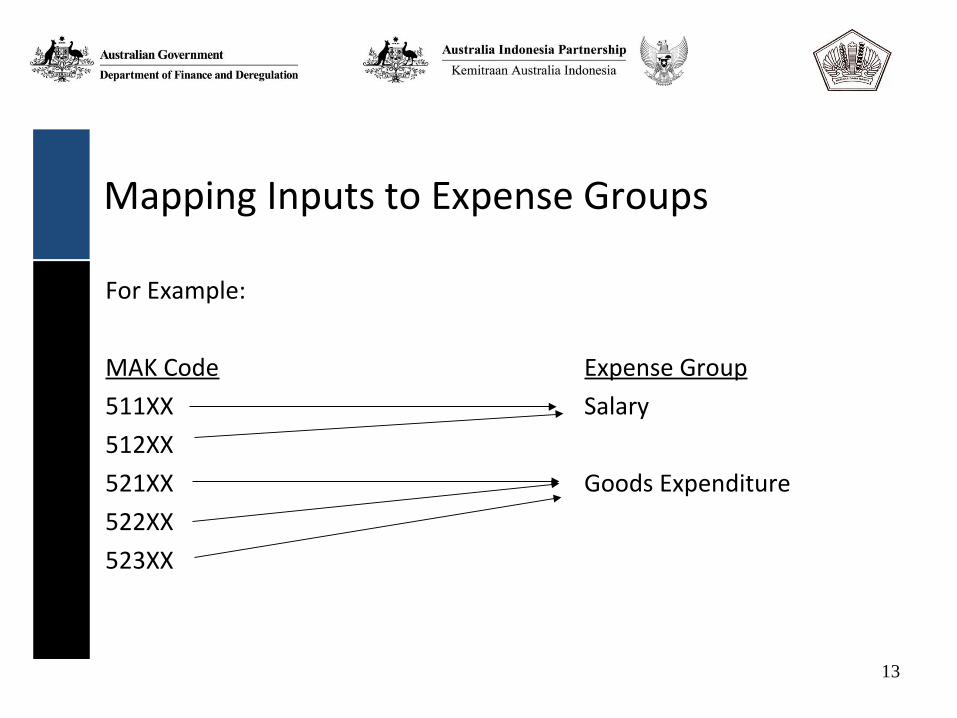

4. Map account codes of inputs into Expense Groups that have similar cost drivers (used for projecting prices and external control under PBB)

• As an example, Expense Groups can include (but not limited to):– Salary & Allowance– Honorarium– Goods– Services– Maintenance– Travel

10

For example: Under ‘Goods’ you could group the following inputs:

BELANJA KEPERLUAN PERKANTORAN/ Expenditure for office supplies

BELANJA PENGIRIMAN SURAT DINAS POS PUSAT / Expenditure for letter shipping by mail

BELANJA BARANG OPERASIONAL LAINNYA / Expenditure for Other operational goods

BELANJA BARANG NON OPERASIONAL LAINNYA / Expenditure for other non-operational goods

11

For example: Under ‘Services’ you could group the following inputs:

BELANJA SEWA/ Expenditure for Rentals

BELANJA JASA PROFESI / Expenditure for Professional Services

BELANJA JASA LAINNYA / Expenditure for Other Services

12

13

Mapping Inputs to Expense Groups

For Example:

MAK Code Expense Group

511XX Salary

512XX

521XX Goods Expenditure

522XX

523XX

14

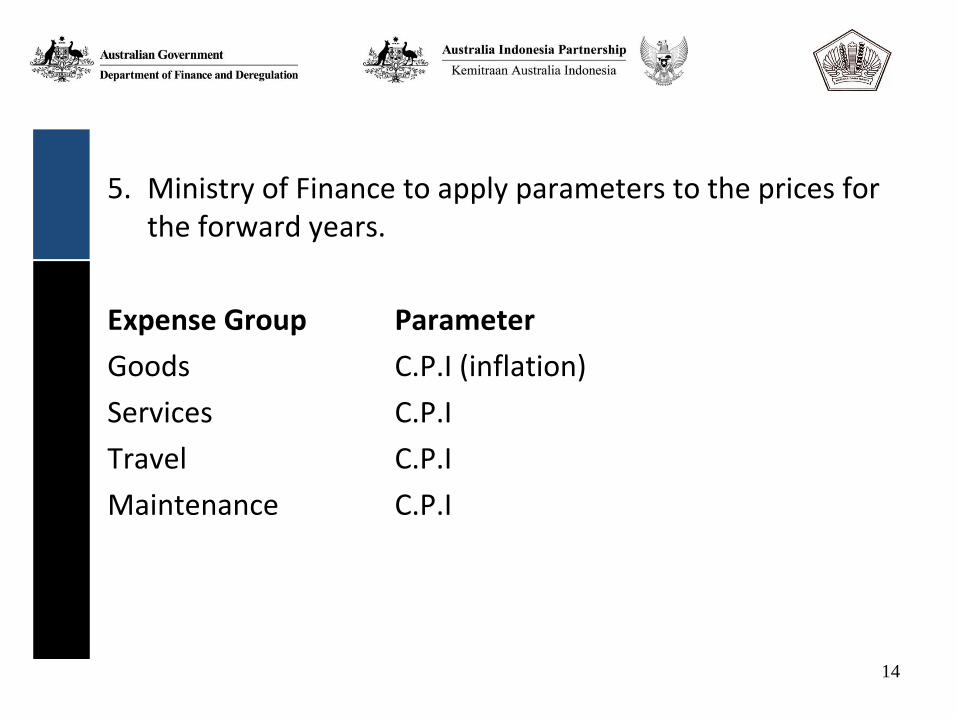

5. Ministry of Finance to apply parameters to the prices for the forward years.

Expense Group Parameter

Goods C.P.I (inflation)

Services C.P.I

Travel C.P.I

Maintenance C.P.I

15

Application of Parameters 2009 2010 2011 2012 2013

C.P.I 8.50% 8.50% 9.00% 9.00% 8.50%

16

Total Expenses 2009 2010 2011 2012 2013

Salary & Allowance 29,368,010

Honorarium 1,223,980

Goods 8,091,555

Services 8,307,455

Maintenance 3,192,239

Travel 27,862,854

Application of Parameters 2009 2010 2011 2012 2013

Salary & Allowance 29,368,010 29,368,010 29,368,010 29,368,010 29,368,010

Honorarium 1,223,980 1,223,980 1,223,980 1,223,980 1,223,980

Goods 8,091,555 8,779,337 9,569,478 10,430,730 11,317,343

Services 8,307,455 9,013,589 9,824,812 10,709,045 11,619,314

Maintenance 3,192,239 3,463,579 3,775,301 4,115,079 4,464,860

Travel 27,862,854 30,231,197 32,952,004 35,917,685 38,970,688

TOTAL 78,046,093 82,079,692 86,713,585 91,764,529 96,964,195

2009 2010 2011 2012 2013

MTEF Baseline 78,046,093 82,079,692 86,713,585 91,764,529 96,964,195

Important Features of this Methodology

The key features required for Indonesia to implement this methodology is:

* Classify running cost or non-running cost

* Agree on Expense Groups (also for PBB)

* Develop and assign parameters for the Expense Groups

* Calculate parameters for the Budget Year and Forward Years