energy transition and the impact on oil

TRANSCRIPT

ENERGY TRANSITION AND THE IMPACT ON OIL

CLAUDIO GALIMBERTI

SENIOR VICE PRESIDENT, ANALYSIS

AUGUST 17, 2021

Meet the speaker

Claudio Galimberti

Senior Vice President, Analysis

Claudio Galimberti is a Senior Vice President of Analysis at Rystad Energy with an

expertise in oil demand forecasting, both short- and long-term, Energy Transition and oil

price modeling. An economist by training, he has worked in the oil industry for 20 years.

He started his career with Shell Trading and Supply in Europe and has held a variety of

senior Strategy, Commercial and Analytics roles out of the US over the past decade. He

was at Shell for more than 15 years and gave a decisive contribution to the development

of Shell Energy Transition Scenarios.

Prior to joining Rystad, he was with S&P Global Platts as Global Head of Demand,

Refining, Agriculture & Risk in the Analytics organization, and subsequently as Senior

Director of Platts Analytics Content Transformation. He was also at Trafigura as Global

Head of Product Analysis. Claudio holds a Laurea Degree in Economics from Bocconi

University in Milan, a Master of Finance from Tulane University and has been working on

his Finance PhD from EDHEC.

• Oil Demand in Rystad’s Three Energy Transition Scenarios

• Oil Supply, Call on Sanctioning and Oil Price projections under the Three Scenarios

• Global Energy System: Rystad’s latest 1.5 DG Scenario

• Signposts: which trajectories is the Energy Transition likelier to follow?

Topics

3

4

Long-term oil demand scenario

Rystad oil demand scenarios and IEA’s Net Zero Emissions: key characteristics and differences

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

Long-term oil demand scenario Million barrels per day

0

20

40

60

80

100

120

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

IEA NZE

Key obstacles to follow “net zero” scenario by IEA:

- Lack of regulatory framework

- Immature technologies in some low carbon sectors

- Need for new infrastructure

- Lack of economic diversification for some countries

- Need for structural change on demand side (towards low carbon products)

32

2029,

1062026,

104

2024,

102

IEA’s NZE

looks too

aggressive in

the short-term

1.5 DG

1.7 DG

1.9 DG

5

0

5

10

15

20

25

30

35

1.7 DG scenario 1.5 DG scenario 1.9 DG scenario

Base Case scenario by sector and scenario

Passenger road transport oil demand will undergo a profound shift in all three scenarios due to the fast-growing fleet of non-ICE powertrainsLong-term oil demand scenario revisionsMillion barrels per day

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

Vehicles Trucks Petchem Aviation Maritime Buildings Industry Ags Power

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

6

0

5

10

15

20

25

30

35

1.7 DG scenario 1.5 DG scenario 1.9 DG scenario

Base Case scenario by sector and scenario

Commercial road transport oil demand will be affected to a lesser degree, at least in the short-medium term, due to heavy duty vehicles’ reliance on dieselLong-term oil demand scenario revisionsMillion barrels per day

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

Vehicles Trucks Petchem Aviation Maritime Buildings Industry Ags Power

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

7

0

5

10

15

20

25

30

35

1.7 DG scenario 1.5 DG scenario 1.9 DG scenario

Base Case scenario by sector and scenario

Petrochemical could follow very different trajectories in the three scenarios based on regulatory/behavioral variables (plastic bans & recycling) & potential for fuel substitutionLong-term oil demand scenario revisionsMillion barrels per day

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

Vehicles Trucks Petchem Aviation Maritime Buildings Industry Ags Power

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

8

0

5

10

15

20

25

30

35

1.7 DG scenario 1.5 DG scenario 1.9 DG scenario

Base Case scenario by sector and scenario

Electrification is unlikely to affect aviation over the horizon considered but bio-jet could play an increasingly key role. In Maritime, LNG & H2/ammonia could displace fuel oilLong-term oil demand scenario revisionsMillion barrels per day

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

Vehicles Trucks Petchem Aviation Maritime Buildings Industry Ags Power

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

9

0

5

10

15

20

25

30

35

1.7 DG scenario 1.5 DG scenario 1.9 DG scenario

Base Case scenario by sector and scenario

Stationary sectors’ oil demand will continue to decline at varying speeds - with potential exception of Ags - following historical trends and the regulatory push to decarbonize.Long-term oil demand scenario revisionsMillion barrels per day

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

20

18

20

26

20

34

20

42

20

50

Vehicles Trucks Petchem Aviation Maritime Buildings Industry Ags Power

Source: Rystad Energy research and analysis, OilMarketCube, August 2021

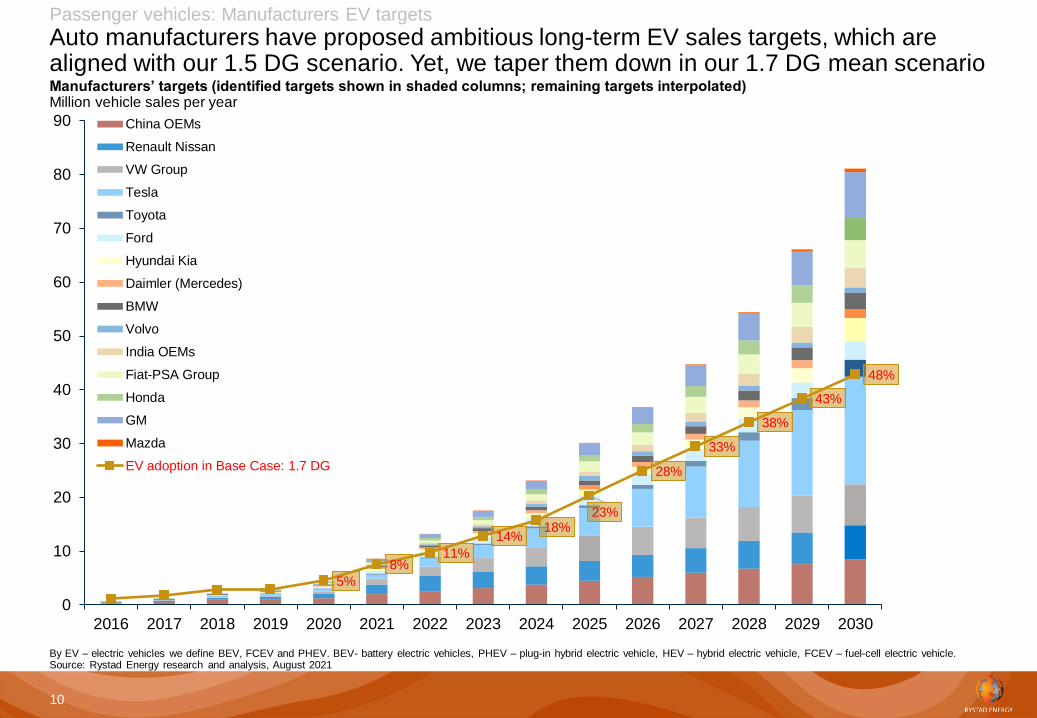

Passenger vehicles: Manufacturers EV targets

Auto manufacturers have proposed ambitious long-term EV sales targets, which are aligned with our 1.5 DG scenario. Yet, we taper them down in our 1.7 DG mean scenario

By EV – electric vehicles we define BEV, FCEV and PHEV. BEV- battery electric vehicles, PHEV – plug-in hybrid electric vehicle, HEV – hybrid electric vehicle, FCEV – fuel-cell electric vehicle. Source: Rystad Energy research and analysis, August 2021

5%

8%11%

14%18%

23%

28%

33%

38%

43%

48%

0

10

20

30

40

50

60

70

80

90

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

China OEMs

Renault Nissan

VW Group

Tesla

Toyota

Ford

Hyundai Kia

Daimler (Mercedes)

BMW

Volvo

India OEMs

Fiat-PSA Group

Honda

GM

Mazda

EV adoption in Base Case: 1.7 DG

10

Manufacturers’ targets (identified targets shown in shaded columns; remaining targets interpolated)Million vehicle sales per year

Passenger vehicles: EV adoption in Base Case (1.7 DG)

EVs sales pick up speed and market share after 2025 as technology is rapidly adopted worldwide, although we will still witness vast regional differences.

Source: Rystad Energy research and analysis, August 2021

EV adoption rates (EV sales / Total passenger vehicle sales) by region

0%

20%

40%

60%

80%

100%

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

United States

America S

China

India

Japan

Asia high

Asia low

Germany

Norway

Europe high

Europe low

Middle East high

Middle East low

Africa high

Africa low

Russia

Global

Passenger vehicles: EV adoption

Large variability in EV penetration in the three scenarios, depending on key regulatory and technology assumptions, with the 1.7 DG scenario as the most likely trajectory

BEV – battery electric vehicles, PHEV – plug-in hybrid electric vehicle, HEV – hybrid electric vehicle, FCEV – fuel-cell electric vehicle. By EV – electric vehicles we define BEV, FCEV and PHEV. Source: Rystad Energy research and analysis, August 2021

23%

48%

84%96%

29%

72%

98% 99%

15%

24%

49%

70%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%20

10

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

203

8

203

9

204

0

204

1

204

2

204

3

204

4

204

5

204

6

204

7

204

8

204

9

205

0

Base Case: Mean (1.7°)

Low Case:-Sigma (1.5°)

High case: +Sigma (1.9°)

12

EV share in total passenger vehicle sales by scenarioPercent

Passenger vehicles: EV adoption in Base Case (1.7 DG)

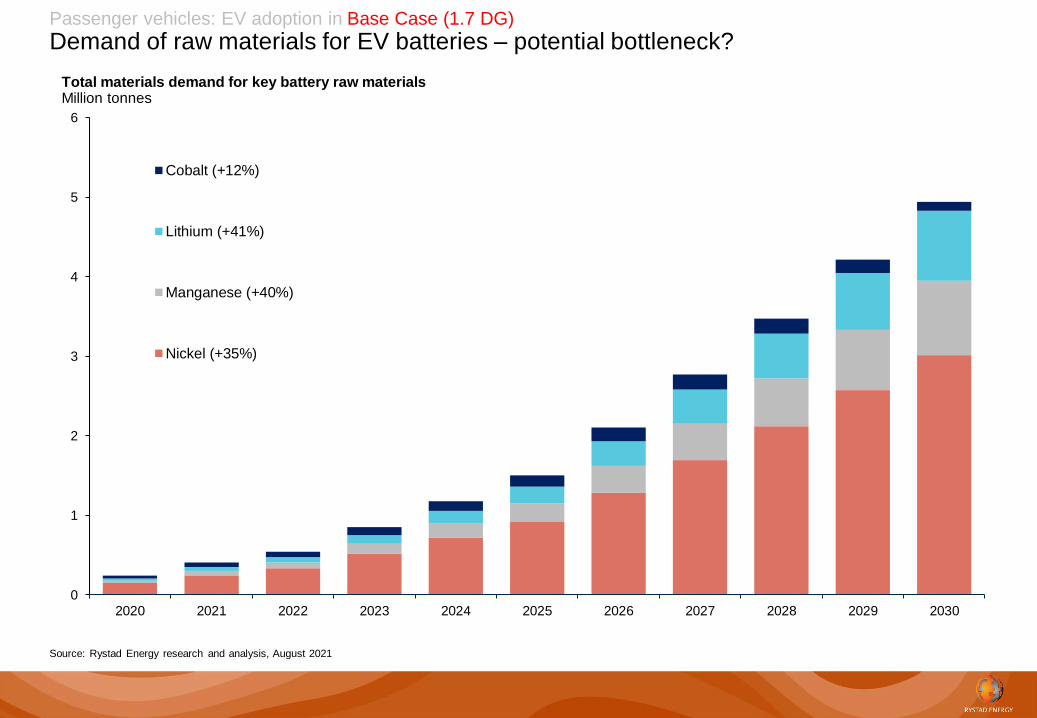

Demand of raw materials for EV batteries – potential bottleneck?

0

1

2

3

4

5

6

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Cobalt (+12%)

Lithium (+41%)

Manganese (+40%)

Nickel (+35%)

Total materials demand for key battery raw materials Million tonnes

Source: Rystad Energy research and analysis, August 2021

Passenger vehicles: Base Case (1.7 DG)

Global EV fleet reaches 18% of total LDVs by 2030, while passenger road transport oil demand remains high through the end of this decade

-

5

10

15

20

25

30

35

0

500

1,000

1,500

2,000

2,500

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

ICE* fleet PHEV fleet BEV fleet

ICE – internal combustion engine vehicles; BEV – battery electric vehicles; PHEV – plug-in hybrid electric vehicleSource: Rystad Energy research and analysis, OICA, IEA EV Outlook 2020, August 2021

Global passenger vehicle fleet Global passenger vehicle oil demand

Million vehicles Million barrels per day

EV share in total sales

EV share in total fleet

5%

2020

1%

23%

2025

6%

48%

2030

18%

73%

2035

37%

84%

2040

59%

90%

2045

76%

2050

88%

96%

Call on sanctioning

Mean demand scenario (1.7 DG) requires 61 million bpd of supply from new wells by 2030 and 65 million bpd by 2040.

* Under development does not include drilled but uncompleted (DUC) shale/LTO wells as a significant share of the investment decision lies aheadSource: Rystad Energy research and analysis, OilMarketCube, Ucube, August 2021

61

65

44

0

20

40

60

80

100

120

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

202

9

203

0

203

1

203

2

203

3

203

4

203

5

203

6

203

7

203

8

203

9

204

0

204

1

204

2

204

3

204

4

204

5

204

6

204

7

204

8

204

9

205

0

Seasonal (Other liquids) Producing (non-shale) Producing (shale)

Under development offshore Under development onshore Call on sanctioning (Mean = 1.7 DG)

Demand (Mean = 1.7 DG) Demand (1.5 DG) Demand (1.9 DG)

15

Liquids supply from producing wells and developments* vs total liquids demandMillion barrels per day

16

Call on sanctioning

Sanctioning is much needed in all three scenarios although existing stock of global discoveries is sufficient to meet demand, at least until mid-2030s.

* Volumes include drilled but uncompleted (DUC) shale / LTO wellsSource: Rystad Energy research and analysis, OilMarketCube, Ucube, August 2021

6165

44

55

49

31

65

80

69

0

10

20

30

40

50

60

70

80

90

100USD/bbl <40

USD/bbl 40-60

USD/bbl 60-80

USD/bbl > 80

Uncommercial

Call on sanctioning (Mean = 1.7 DG)

Call on sanctioning (1.5 DG)

Call on sanctioning (1.9 DG)

Liquids supply from pre-FID wells* and call on sanctioningMillion barrels per day

1.9 DG scenario calls for

additional exploration activity

17

*Includes crude oil, lease condensate and NGLs extracted at gas processing plants. Source: Rystad Energy research and analysis, OilMarketCube, Ucube, August 2021

US shale liquids: Long-term potential

Vast uncertainty for US Shale liquids production in 2025-2035 and convergence in 2040s.

US shale should be able to fill supply gaps via adequate price signals over next 15 years.

21.2

14.2

6.5

17.9

12.9

6.0

11.3

11.0

13.5

9.8

4.9

0

5

10

15

20

25

2010 2015 2020 2025 2030 2035 2040 2045 2050

Brent@70 Brent@60 Brent@50

US shale/LTO oil production* long-term outlook Million barrels per day

If there will be deficit of supply on the

market in 2025-2035 due to lack of

investment in upstream, US shale

would be one of the key source of

additional barrels

18

Call on sanctioning

Equilibrium price at $45/bbl should satisfy 2030 call on sanctioning, with onshore infill generating one third of the 61 million bpd needed.

* Shale/LTO volumes include drilled but uncompleted (DUC) wells. All supply segments include uncommercial discoveries and undiscovered projects.Source: Rystad Energy research and analysis, OilMarketCube, Ucube, August 2021

Cost of liquids supply curve for pre-FID wells* for 2030 by supply segment typeUSD per barrel (real), Brent-equivalent

5

10

15

20

25

30

35

40

45

50

55

60

65

70

- 5 10 15 20 25 30Million bpd

Shale/LTO*

Offshore (infill)

Offshore (new fields)

Onshore (infill)

Onshore (new fields)

Cut-off

High LTO volume

potential between

$30 and $45 /bbl.

Highly competitive

drilling in Mid East.

19

Global liquids supply cost curve

We maintain our base case of $50 Brent (real) in 1.7 DG Energy Transition scenario.

* Shale/LTO volumes include drilled but uncompleted (DUC) wells. All supply segments include uncommercial discoveries and undiscovered projects.Source: Rystad Energy research and analysis, OilMarketCube, Ucube, August 2021

Cost of liquids supply curve for 2030, 2040 and 2050 against range of demand scenariosUSD per barrel (real), Brent-equivalent

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

105

110

115

120

35 45 55 65 75 85 95 105 115

Million bpd

Cost of Supply 2050 Cost of Supply 2040 Cost of Supply 2030

1.7 DG

Demand in

2030

1.9 DG

Demand in

2030

1.5 DG

Demand in

2030

1.9 DG

Demand in

2040

1.7 DG

Demand in

2040

1.5 DG

Demand in

2040

1.9 DG

Demand in

2050

1.7 DG

Demand in

2050

1.5 DG

Demand in

2050

20

Long-term case price assumption

Rystad Dynamic Oil Price Model shows how equilibrium prices could play out in the three Energy Transition scenarios

* Nominal price using a 2.5% annualized inflation rate on the real (2021-dollar) price assumption.Source: Rystad Energy research and analysis, Ucube, August 2021

4650 48 42 40

37

4752 52 56

65

74

44 4340

3530

26

-5

15

35

55

75

95

115

135

2010 2020 2030 2040 2050

1.5 DG

Historical Forecast

Mean 1.7 DG

1.9 DG

Brent oil price (real 2021-terms) in the three demand scenarios

USD per barrel

21

The global energy system – real testing of case with disruptive technologies and recent policy statements

Source: Rystad Energy global energy system model; World Cube Pilot, August 2021

Heat Work Light/

Calc.

Use as

material

Industry• Chemicals/Plastics

• Mining/Metals

• Ceramics/Cement

• Textiles/Leather

• Pulp/Paper

• Machines/vessels

• Electronics/SW

• Food process

Transport and work• Road

• Sea

• Air

• Rail

• Construct.

• Other

Buildings• Heat/cool

• Cook/clean

• Work/play

Biofuel

Oil

Natural gas

Nuclear

End use

losses

Food and Land• Agriculture

• Forestry

Pumped hydro

Batteries

Gravity

Coal

H2 grey/blue

NH3

CH4 (na/syn)

NGLs

Gasoline

Diesel

Jetfuel

Coal, Coke

Upstream losses

Liquids

Storage

Shipping

Pipeline

Solar

Wind

Other renew.

Hydro

Geothermal

Gas

Solid

Heat

Transmission

Primary energy

Wood… Solid

H2 green

CCSU

Refine fuel Make electrons

En

d-u

se

of e

ne

rgy

Electricity

Molecules

Heat

Forest

Modern bioenergy

and waste

Plants and animals

Nuclear reactor

Gas turbine

Steam turbine

Steam turbine

Bio boiler

Fuel turbine

Heat

storage

H2 storage

Fuelcell

H2/NH3 Power

Distribution & Storage

Electricity

Grid

Refining losses Generation losses Distribution losses

Hydro turbine

CCSU

22

Global primary energy mix will see a rapid shift towards Renewables under Rystad 1.5 DG scenario

0

100

200

300

400

500

600

700Traditional Bio

Coal

Oil

Natural Gas

Nuclear

Modern biomass and waste

Geothermal

Hydro

Wind

Solar

Total primary energy

EJ

Forecast

Source: Rystad Energy Energy Scenario Cube – 1.5 DG scenario, August 2021

Historical

75%

23%

50%

11%

23

-

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Coal OilNatural Gas NuclearModern biomass and waste Traditional BioGeothermal HydroSolar Wind

Rystad Energy’s 1.5 DG Scenario vs. IEA’s NZE: more solar and more oil, less bioenergy and nuclear in Rystad’s.

Total primary energy – Rystad Energy, 1.5 DG August 2021

EJ

Source: Rystad Energy WorldCube – 1.5 DG scenario, August 2021

74%

48%

Total primary energy – IEA NZE May 2021

EJ

Oil 2030: 95 mpd

Oil 2030: 72 mpd

Solar: 50 PWh

0

100

200

300

400

500

600

700 WoodCoalLiquidsMethaneHeatHydrogen/AmmoniaElectricityElectricity via storageLosses from el gen

Total primary energy

EJHistorical Forecast

Source: Rystad Energy Energy Scenario Cube – 1.5 DG scenario, August 2021

67%

23%

Storage:

32%

Electrification – crucially accompanied by power storage - will play an increasingly dominant role in the 1.5 DG scenario

0

100

200

300

400

500

600

700Energy sector

Industry

Transport and work

Buildings

Losses

Source: Rystad Energy, Energy Scenario Cube – 1.5 DG scenario, August 2021

Total primary energy

EJForecastHistorical

From the end-user perspective and the economy, the 1.5 DG scenario will represent a massive efficiency gain!

51% of total

primary

energy is

currently lost

in

conversion

30%

48%

Signposts: Regulatory environment, economic signals and technology changes.

▪ Updated NDCs

▪ Compliance

Source: Rystad Energy research and analysis, August 2021

Passenger vehicles: Manufacturers’ EV targets

Investments in energy transition technology by producers, adoption rates by consumers and regulatory environment will ultimately determine the Energy Transition pace

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

20

16

20

19

20

21

20

23

20

25

20

16

20

19

20

21

2023

20

25

20

16

20

19

2021

20

23

20

25

20

16

20

19

20

21

20

23

20

25

20

16

20

19

20

21

2023

20

25

20

16

20

19

2021

20

23

20

25

20

16

20

19

20

21

20

23

20

25

20

16

20

19

20

21

20

23

20

25

20

16

20

19

2021

20

23

20

25

20

16

2019

20

21

20

23

20

25

BMW Regional OEMs* Ford Hyundai Kia Tesla Toyota VW Group Renault Nissan GM Others**

Targets as of 2Q21 Targets as of 1Q21BMW Regional OEMs*FordHyundai Kia TeslaToyotaVW GroupRenault NissanGMOthers**

Source: Rystad Energy research and analysis*Regional OEMs include vehicle Manufacturers in China and India ** Others include Fiat- PSA group, Daimler, Mazda and Honda, August 2021

27

Electric vehicle manufacturers’ targets: Recent reporting vs reporting as of Oct-20 (previous)Million vehicle sales

Disclaimer

This report has been prepared by Rystad Energy (the “Company”). All materials, content and forms contained in this report arethe intellectual property of the

Company and may not be copied, reproduced, distributed or displayed without the Company’s permission to do so. The information contained in this document

is based on the Company’s global energy databases and tools, public information, industry reports, and other general researchand knowledge held by the

Company. The Company does not warrant, either expressly or implied, the accuracy, completeness or timeliness of the information contained in this report. The

document is subject to revisions. The Company disclaims any responsibility for content error. The Company is not responsible for any actions taken by the

“Recipient” or any third-party based on information contained in this document.

This presentation may contain “forward-looking information”, including “future oriented financial information” and “financial outlook”, under applicable securities

laws (collectively referred to herein as forward-looking statements). Forward-looking statements include, but are not limited to, (i) projected financial

performance of the Recipient or other organizations; (ii) the expected development of the Recipient’s or other organizations’business, projects and joint

ventures; (iii) execution of the Recipient’s or other organizations’ vision and growth strategy, including future M&A activity and global growth; (iv) sources and

availability of third-party financing for the Recipient’s or other organizations’ projects; (v) completion of the Recipient’s or other organizations’ projects that are

currently underway, under development or otherwise under consideration; (vi) renewal of the Recipient’s or other organizations’ current customer, supplier and

other material agreements; and (vii) future liquidity, working capital, and capital requirements. Forward-looking statements are provided to allow stakeholders the

opportunity to understand the Company’s beliefs and opinions in respect of the future so that they may use such beliefs and opinions as a factor in their

assessment, e.g. when evaluating an investment.

These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily

involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periodsto differ materially from any

projections of future performance or result expressed or implied by such forward-looking statements. All forward-looking statements are subject to a number of

uncertainties, risks and other sources of influence, many of which are outside the control of the Company and cannot be predicted with any degree of accuracy.

In light of the significant uncertainties inherent in such forward-looking statements made in this presentation, the inclusion of such statements should not be

regarded as a representation by the Company or any other person that the forward-looking statements will be achieved.

The Company undertakes no obligation to update forward-looking statements if circumstances change, except as required by applicable securities laws. The

reader is cautioned not to place undue reliance on forward-looking statements.

Under no circumstances shall the Company, or its affiliates, be liable for any indirect, incidental, consequential, special or exemplary damages arising out of or

in connection with access to the information contained in this presentation, whether or not the damages were foreseeable and whether or not the Company was

advised of the possibility of such damages.

© Rystad Energy 2021. All Rights Reserved.

28

Rystad Energy is an independent energy consulting services

and business intelligence data firm offering global

databases, strategy advisory and research products for

energy companies and suppliers, investors, investment

banks, organizations, and governments. Rystad Energy’s

headquarters are located in Oslo, Norway.

Headquarters

Rystad Energy

Fjordalléen 16, 0250 Oslo, Norway

Americas +1 (281)-231-2600

EMEA +47 908 87 700

Asia Pacific +65 690 93 715

Email: [email protected]

© Copyright. All rights reserved.