eli lilly ranbaxy joint venture case study

TRANSCRIPT

ELI LILLY IN INDIA RETHINKING THE JOINT VENTURE

STRATEGY Abhay Kishore – 01Abhishek Kunal – 05Anil Kumar Jadli – 11 J.Harish – 25 Khushal Malik – 28Sharad Singh – 49

PHARMACEUTICAL INDUSTRY – Global Trend

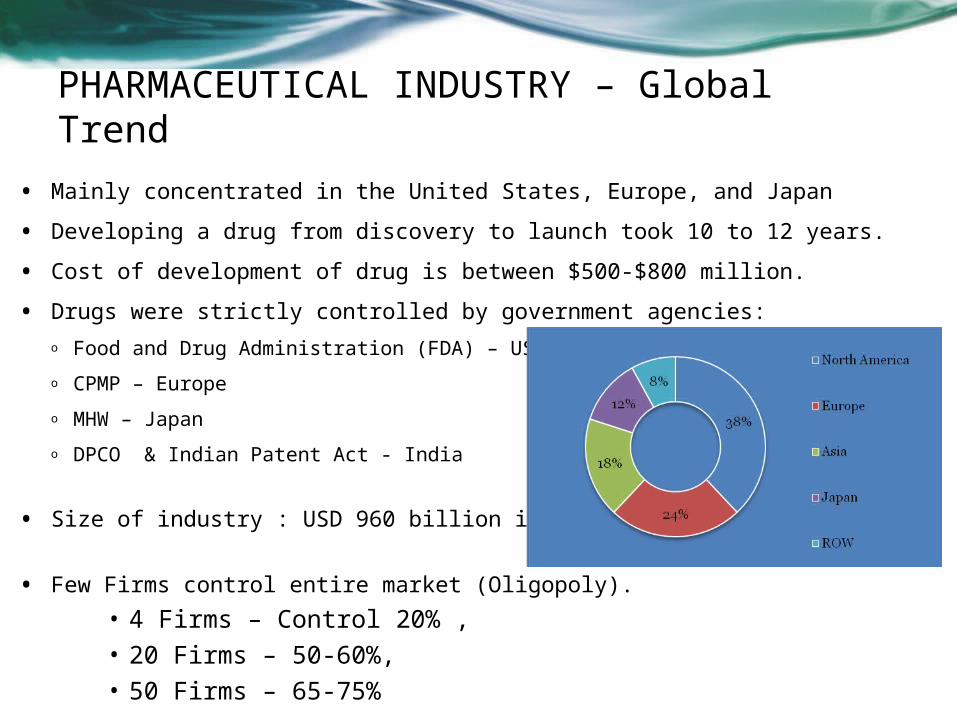

• Mainly concentrated in the United States, Europe, and Japan

• Developing a drug from discovery to launch took 10 to 12 years.

• Cost of development of drug is between $500-$800 million.

• Drugs were strictly controlled by government agencies:o Food and Drug Administration (FDA) – USA,

o CPMP – Europe

o MHW – Japan

o DPCO & Indian Patent Act - India

• Size of industry : USD 960 billion in 2012.

• Few Firms control entire market (Oligopoly).

• 4 Firms – Control 20% ,• 20 Firms – 50-60%,• 50 Firms – 65-75%

PHARMACEUTICAL INDUSTRY – Global Trend

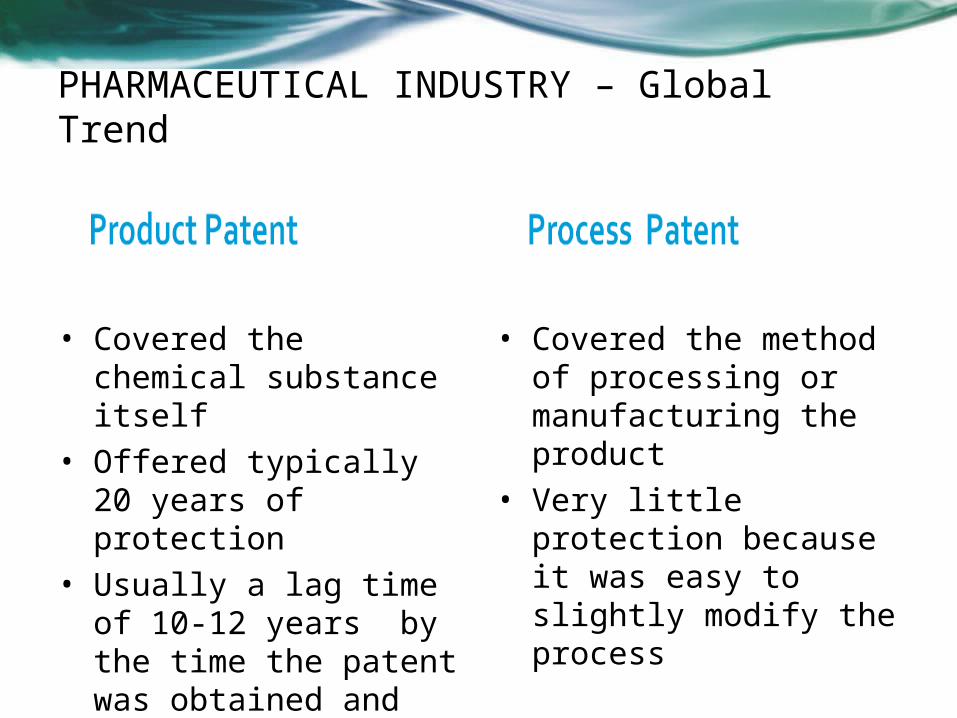

• Covered the chemical substance itself

• Offered typically 20 years of protection

• Usually a lag time of 10-12 years by the time the patent was obtained and the launch date

• Covered the method of processing or manufacturing the product

• Very little protection because it was easy to slightly modify the process

• Prices in of the drugs varied in developed countries• US & Canada by factor 1.2 to 2.5. • Europe by factor 1.1 to 2.5.

• Parallel Trade: an outside company sells a patented product in a

market not designated to sell the drug. o Independent firm exploited parallel trade by using the differentials in

price across various countries.

• Generic Drugs: unbranded drugs of comparable efficacy available

at fractional cost of branded product.o Posed as major challenge for pricing power of large pharma companies. o No additional expense for drug R&D of new compounds.o Generic companies made money by copying the products discovered &

developed by other major pharmaceuticals companies.

Global Issues in Pharma Sector

Issues in Indian Pharma Sector

• Initially country had no indigenous production capability & was

totally dependent on imports.

• Post independence HAL (promoted by WHO ) & IDPL (Russian

assistance) were established in 1954 & 1961 respectively.

• Indian Patent Act was passed in 1970, it abolished Product patent &

permitted process patent for 5-7 years.

• Drug Price Control Order (DPCO) instituted price control by which

govt. stipulated prices for all the drugs.

• Indian drug prices hovered around 5%-20% of U.S. prices due to

these.

• Prime minister Gandhi had said at World Health assembly in 1982:

“The idea of a better-ordered world is one in which medical

discoveries will be free of patents and there will be no profiteering

from life and death.”

• In 1990s , post globalisation, FDI upto 51% (up from 40%) was

allowed in Drugs & Pharmaceuticals industries.

• A suitable Environment for entry of Eli Lilly entry into India.

Eli Lilly & Company

• Founded in 1876 with $1400 and 4 employees

• Chairman Dick Wood decided to take the company

global in the mid-1980s

• By 1992, Lilly manufactured in 25 countries and sold in

more than 130 countries.

• Gerhard Mayr, head Lily International wanted to

expand operation in Asia including India due to :

• Opening of market for foreign investment

• Opportunity for clinical testing

Ranbaxy Laboratories Ltd

• Began as a family business in the 1960s

• By the 1990s, it grew to become India’s largest

manufacturer of bulk drugs and generic drugs.

• Had a domestic market share of 15% (1996).

• Capital cost was 50-75% lower than comparable US plants.

• The higher price in foreign countries provided the impetus

for Ranbaxy to pursue international market.

• It had presence in 47 markets outside India, mainly

through exports.

• R&D expenditure of company was 2-5% of annual sales.

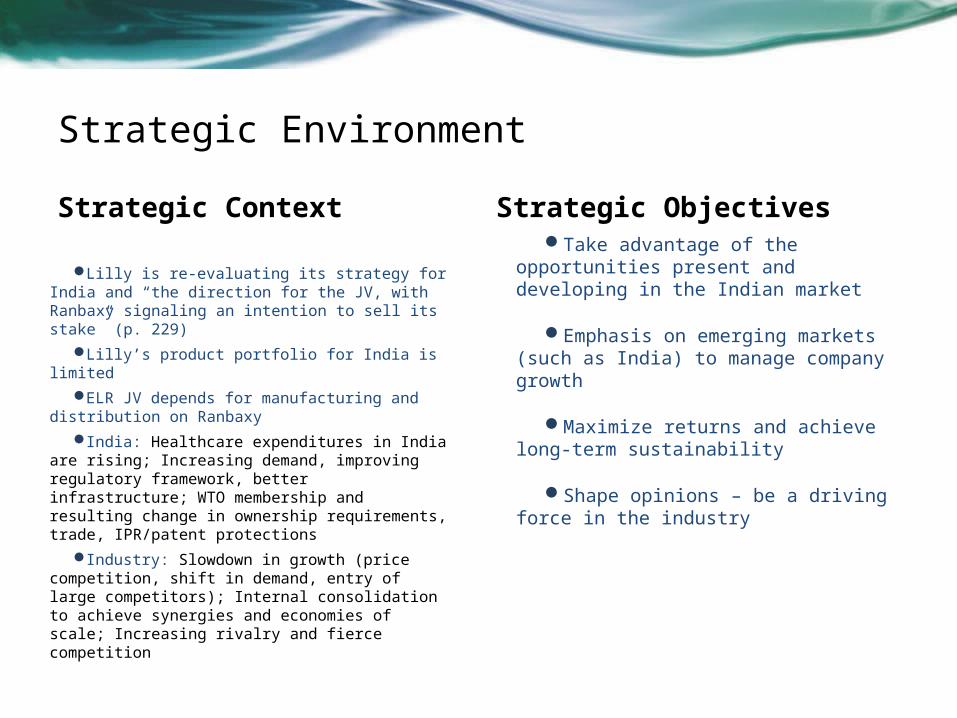

Strategic Environment

Strategic Context

Lilly is re-evaluating its strategy for India and “the direction for the JV, with Ranbaxy signaling an intention to sell its stake” (p. 229)

Lilly’s product portfolio for India is limited

ELR JV depends for manufacturing and distribution on Ranbaxy

India: Healthcare expenditures in India are rising; Increasing demand, improving regulatory framework, better infrastructure; WTO membership and resulting change in ownership requirements, trade, IPR/patent protections

Industry: Slowdown in growth (price competition, shift in demand, entry of large competitors); Internal consolidation to achieve synergies and economies of scale; Increasing rivalry and fierce competition

Strategic ObjectivesTake advantage of the

opportunities present and developing in the Indian market

Emphasis on emerging markets (such as India) to manage company growth

Maximize returns and achieve long-term sustainability

Shape opinions – be a driving force in the industry

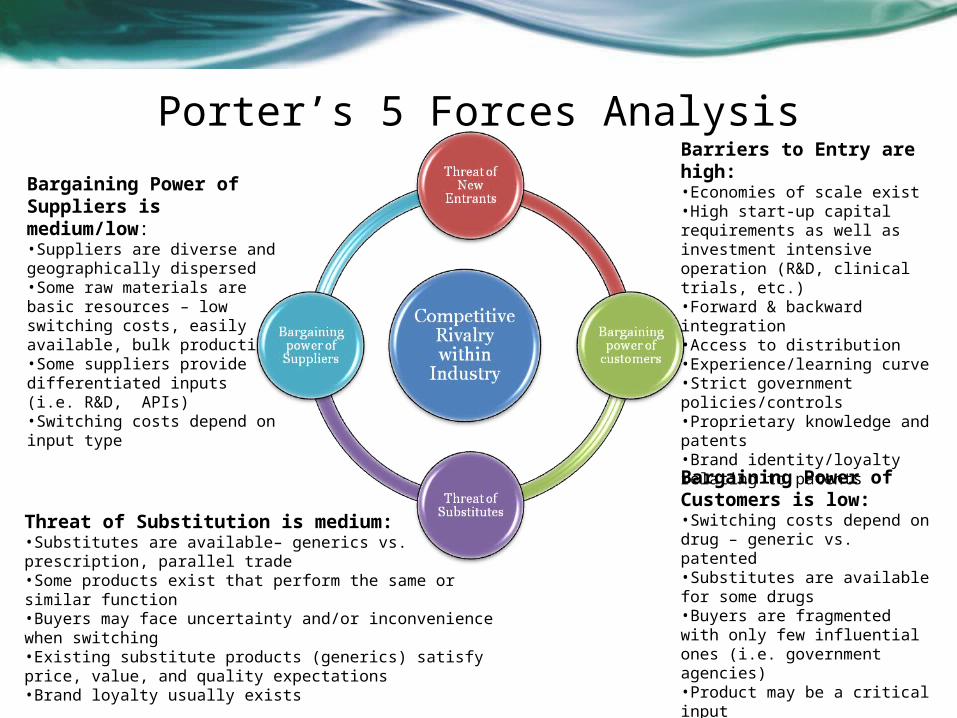

Porter’s 5 Forces AnalysisBarriers to Entry are high:•Economies of scale exist•High start-up capital requirements as well as investment intensive operation (R&D, clinical trials, etc.)•Forward & backward integration•Access to distribution•Experience/learning curve•Strict government policies/controls•Proprietary knowledge and patents•Brand identity/loyalty relating to patents

Threat of Substitution is medium:•Substitutes are available– generics vs. prescription, parallel trade•Some products exist that perform the same or similar function•Buyers may face uncertainty and/or inconvenience when switching•Existing substitute products (generics) satisfy price, value, and quality expectations •Brand loyalty usually exists

Bargaining Power of Suppliers is medium/low:•Suppliers are diverse and geographically dispersed•Some raw materials are basic resources – low switching costs, easily available, bulk production•Some suppliers provide differentiated inputs (i.e. R&D, APIs)•Switching costs depend on input type

Bargaining Power of Customers is low:•Switching costs depend on drug – generic vs. patented•Substitutes are available for some drugs•Buyers are fragmented with only few influential ones (i.e. government agencies)•Product may be a critical input

SWOT Analysis

Eli Lilly & Ranbaxy - The start of the JV

• JV signed in November 1992, named as Eli Lilly - Ranbaxy.

• Each had a 50% stake with an initial investment of roughly $10

million

• Board of Director of JV: comprising of 6 directors, 3 from each

Company.

• Management committee comprised of 2 directors, 1 from each.

• Lilly retained right to appoint the CEO of the JV.

• Alignment of broad values.

• Ranbaxy would supply certain products they already made under

the JV then formulate and finish some of Lilly’s products locally in

India.

• Ranbaxy would also package and distribute Lilly’s products.

• Exit option: Agreement provided for transfer of share incase any

partner desired to dispose a part or its entire share in the

company.

• Ranbaxy was driven by the generics business, Lilly was driven by

innovation and discovery

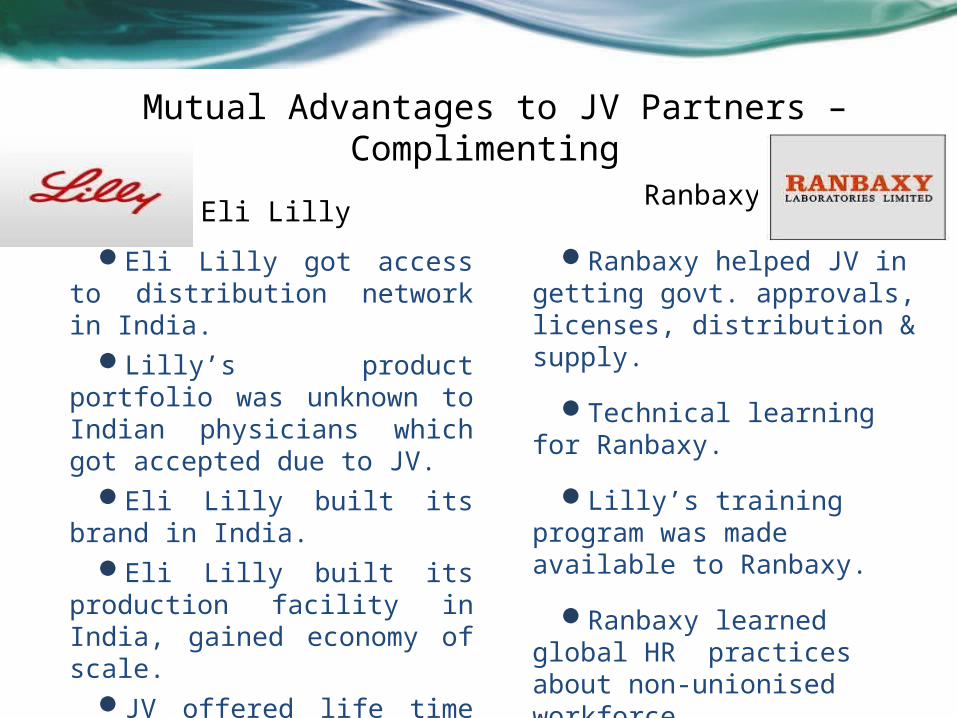

Mutual Advantages to JV Partners – Complimenting

Eli Lilly

Eli Lilly got access to distribution network in India.

Lilly’s product portfolio was unknown to Indian physicians which got accepted due to JV.

Eli Lilly built its brand in India.

Eli Lilly built its production facility in India, gained economy of scale.

JV offered life time association to new employees to counter employee turn over.

Ranbaxy

Ranbaxy helped JV in getting govt. approvals, licenses, distribution & supply.

Technical learning for Ranbaxy.

Lilly’s training program was made available to Ranbaxy.

Ranbaxy learned global HR practices about non-unionised workforce.

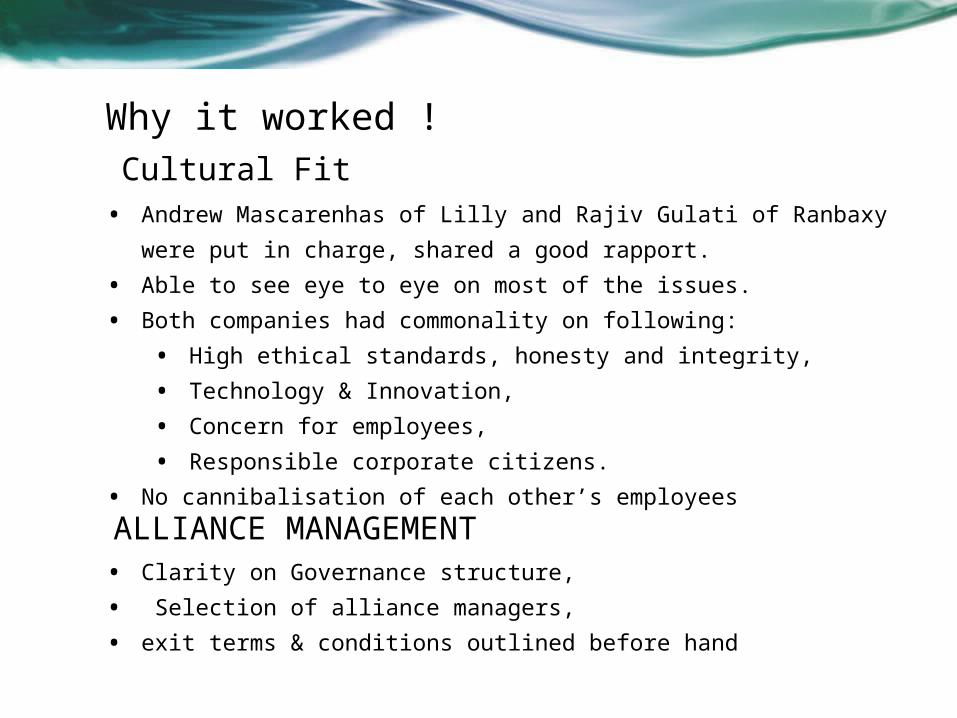

Why it worked !

• Andrew Mascarenhas of Lilly and Rajiv Gulati of Ranbaxy were

put in charge, shared a good rapport.

• Able to see eye to eye on most of the issues.

• Both companies had commonality on following:

• High ethical standards, honesty and integrity,

• Technology & Innovation,

• Concern for employees,

• Responsible corporate citizens.

• No cannibalisation of each other’s employees

• Clarity on Governance structure,

• Selection of alliance managers,

• exit terms & conditions outlined before hand

Cultural Fit

ALLIANCE MANAGEMENT

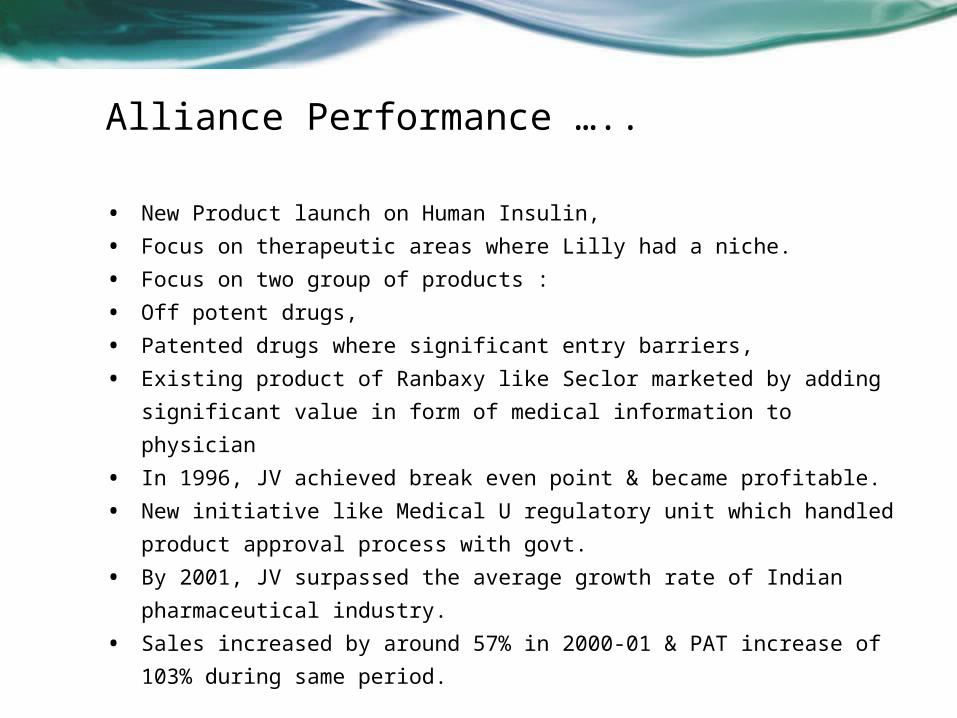

Alliance Performance …..

• New Product launch on Human Insulin,

• Focus on therapeutic areas where Lilly had a niche.

• Focus on two group of products :

• Off potent drugs,

• Patented drugs where significant entry barriers,

• Existing product of Ranbaxy like Seclor marketed by adding

significant value in form of medical information to physician

• In 1996, JV achieved break even point & became profitable.

• New initiative like Medical U regulatory unit which handled product

approval process with govt.

• By 2001, JV surpassed the average growth rate of Indian

pharmaceutical industry.

• Sales increased by around 57% in 2000-01 & PAT increase of 103%

during same period.

Changing World Order …..

• Consolidation trend in industry through Merger &

Acquisition. In 1990 top 10 Cos accounting for 28%

Market, In 2000 same were accounting for 45% of

market.

• Partnership on pharmaceutical & biotechnology

companies was growing rapidly.

• Increased challenges of

• increased R&D cost and development,

• Approval time &

• Competition from generics.

Changing World Order …..

• Consolidation trend in industry through Merger & Acquisition. In

1990 top 10 Cos accounting for 28% Market, In 2000 same were

accounting for 45% of market.

• Partnership on pharmaceutical & biotechnology companies was

growing rapidly.

• Increased challenges of

• increased R&D cost and development,

• Approval time &

• Competition from generics.

• India signed GATT & became member of WTO, according to

which India would grant product patent recognition form 2005

onwards.

• Indian govt. decision to allow 100% FDI in Drug and

Pharmaceutical industries in 2001.

• Eli Lilly had established foothold in Indian market &

expanded their network.

• Ranbaxy formulated a new mission to be a Research based

International Pharmaceuticals Company.

• Ranbaxy started forming JVs for developed market for US,

Canada & Ireland.

• Due to increased competition in India JV might be less

profitable than other markets.

Change in Order …..

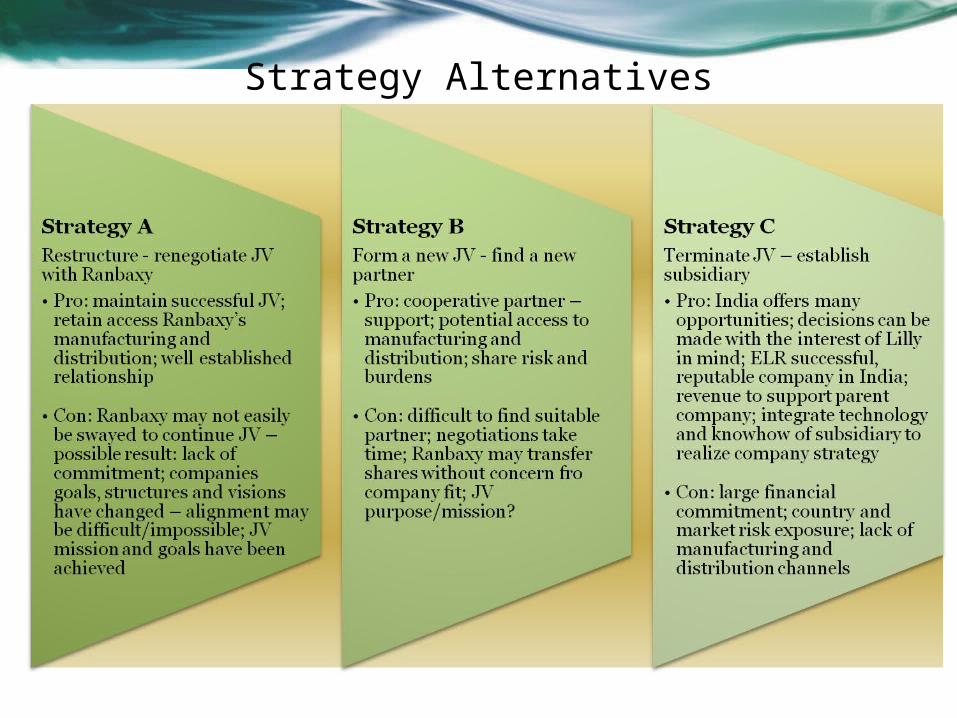

Strategy Alternatives

• Eli Lilly had established foothold in Indian market &

expanded their network.

• Ranbaxy formulated a new mission to be a Research based

International Pharmaceuticals Company.

• Ranbaxy started forming JVs for developed market for US,

Canada & Ireland.

• Due to increased competition in India JV might be less

profitable than other markets.

Evaluating Strategic Options …..

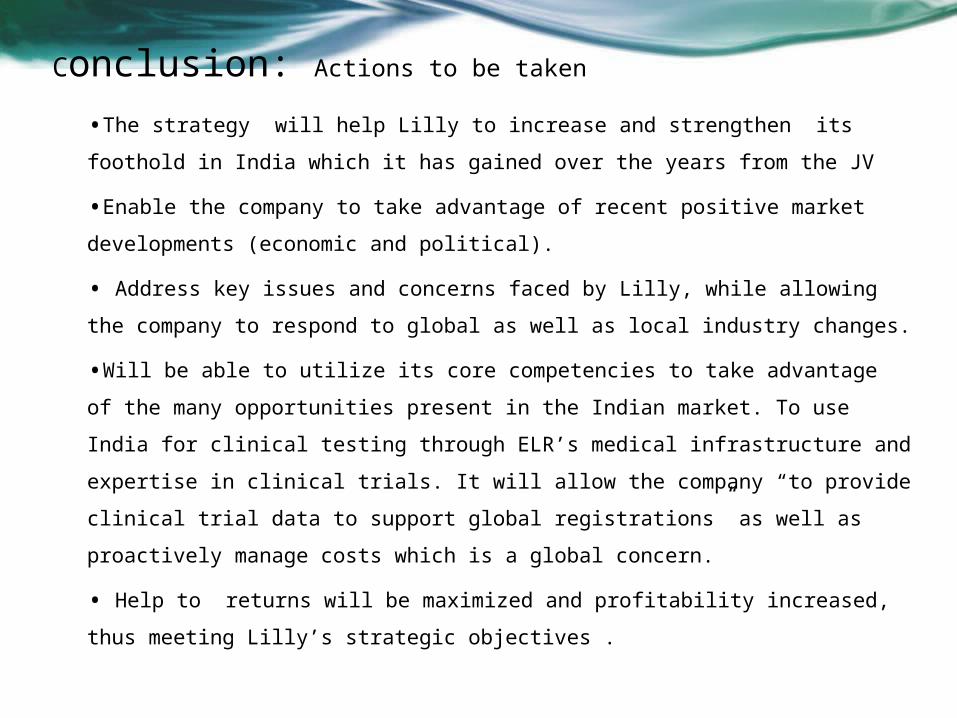

Conclusion: Actions to be taken

•The strategy will help Lilly to increase and strengthen its foothold in

India which it has gained over the years from the JV

•Enable the company to take advantage of recent positive market

developments (economic and political).

• Address key issues and concerns faced by Lilly, while allowing the

company to respond to global as well as local industry changes.

•Will be able to utilize its core competencies to take advantage of the many

opportunities present in the Indian market. To use India for clinical testing

through ELR’s medical infrastructure and expertise in clinical trials. It will

allow the company “to provide clinical trial data to support global

registrations” as well as proactively manage costs which is a global

concern.

• Help to returns will be maximized and profitability increased, thus

meeting Lilly’s strategic objectives .

Thank you