effect of liquidity on size premium v7 - forensic economics · 3 the higher the size premium, the...

TRANSCRIPT

Effect of Liquidity on Size Premium and its Implications for Financial Valuations

[** Working Title]

Frank Torchio and Sunita Surana

Preliminary Draft August 2013

2

I. Size Premiums and Fair Value

Discounted Cash Flow (“DCF”) analysis is one of, if not, the key valuation method

taught by academics and used by practitioners. A critical parameter of a DCF analysis is the

weighted average cost of capital (used to discount expected cash flows) which comprises in part

the cost of equity. The cost of equity is generally computed using a version of the capital asset

pricing model (“CAPM”)1, for which the equation is:

Cost of Equity = Risk-free Rate + (Beta x Equity Risk Premium) (1)

Many valuation practitioners generally consider it appropriate to include in the

calculation of the cost of equity a premium based on the market capitalization of equity or size of

the firm being valued. Empirical studies, most notably published in the Ibbotson SBBI

Yearbooks (“Ibbotson SBBI”), have shown that the CAPM alone does not fully account for the

higher historical returns earned by smaller companies.2 These studies show that historical

returns for small firms are systematically greater than the returns implied by their betas (beta-

adjusted returns) from the standard CAPM in (1).

That is, the greater risk of smaller-sized firms is not fully accounted for in the standard

beta calculations for these firms. To account for this size-related effect, one of the variations of

the CAPM equation includes a size premium, defined as:

Cost of Equity = Risk-free Rate + (Beta x Equity Risk Premium) + Size Premium (2)

1 The CAPM is the cornerstone of asset pricing theory and is widely used for the

estimation of cost of capital. See, for example, Sharpe (1964) and Fama and French (2004). 2 See Ibbotson SBBI 2011Valuation Yearbook, pp. 87-90. Banz (1981) first presented

evidence that smaller firms earned higher risk-adjusted returns.

3

The higher the size premium, the higher is the cost of equity, and consequently the lower

is the DCF value, all else the same. Ibbotson SBBI has measured historic size premiums by

constructing portfolios of traded stocks by size. The size premiums are computed as the average

returns for each size portfolio less the average of the returns predicted by CAPM in (1) for the

stocks in each portfolio. Ibbotson has constructed both size-quartile portfolios and size-decile

portfolios. In 2001, Ibbotson refined its size analysis by dividing decile 10, the smallest stock

decile, into 10a and 10b.3 In 2010, Ibbotson further divided the 10th decile into four size

categories: 10w, 10x, 10y, and 10z.4 As can be seen in Table 1, the size premiums increase as

the company size decreases.

3 Ibbotson SBBI 2001Valuation Yearbook, pp. 122-3. 4 Ibbotson SBBI 2010 Valuation Yearbook, p. 91.

4

Table 1 Size Premiums for Size-Quartile and Size-Decile Portfolios

Notes: Source of data is Ibbotson SBBI 2011 Valuation Yearbook. Since the data in our analysis covers the time period 1926-2010, for comparability purposes, throughout this paper we report the statistics from the 2011 Yearbook that uses data also from 1926-2010. Market capitalization in each decile is as of September 30, 2010.

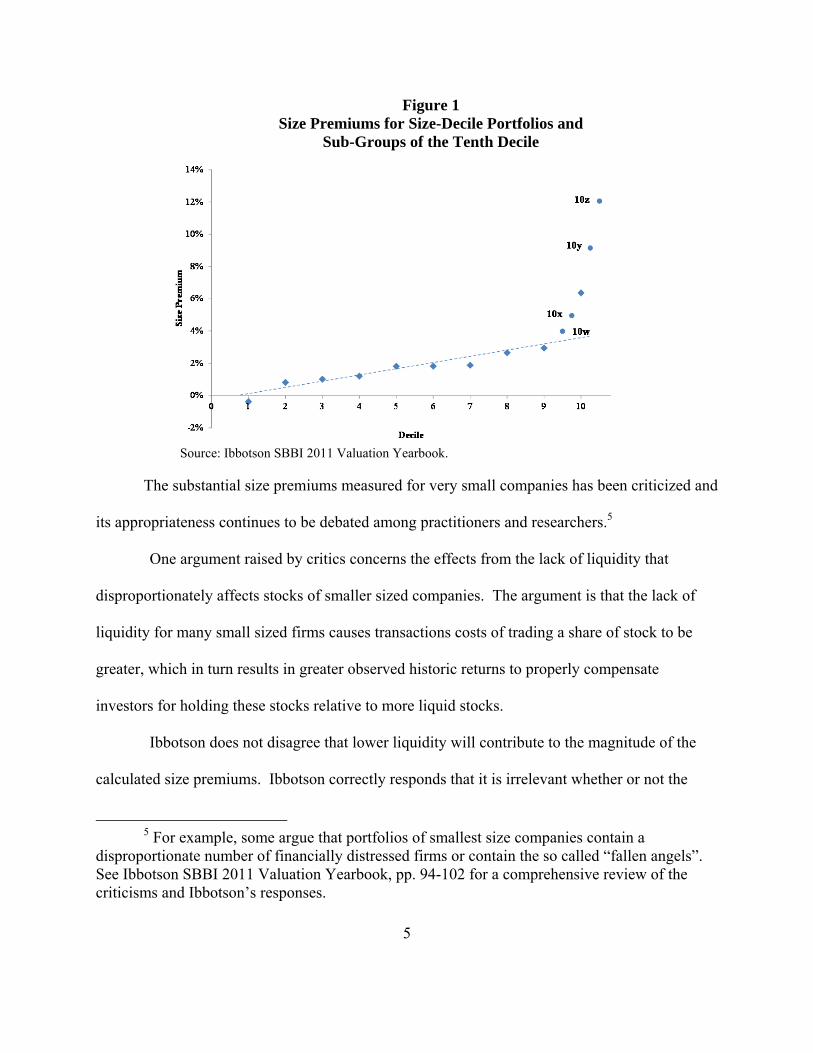

Figure 1 plots the size premiums for the ten deciles (diamonds shapes) and also shows the

size premiums for categories 10w, 10x, 10y, and 10z (circle shapes) contained in the Ibbotson

SBBI 2011 Yearbook. As can be seen in Figure 1, the increase in the size premium is

approximately linear for decile 1 (-0.38%) through decile 9 (2.94%). But for the smallest size

decile (decile 10), the premium increases substantially to 6.36%, which is above the linear trend

line based on the size premiums for deciles 1 through 9. Within decile 10, the increase in size

premiums is even more dramatic and ranges from 3.99% for size category 10w to 12.06% for the

smallest size category, 10z.

Quartile Groups

Size Premium

Decile Groups

Market Capitalization of Largest Company in Decile ($ millions)

Size Premium

1 314,623 -0.38%

2 15,080 0.81%

3 6,794 1.01%

4 3,711 1.20%

5 2,509 1.81%

6 1,776 1.82%

7 1,212 1.88%

8 772 2.65%

9 478 2.94%

10w 236 3.99%

10x 179 4.96%

10y 143 9.15%

10z 86 12.06%

Micro Cap (9-10)

4.07%

Large Cap (1-2)

n/a

Mid Cap (3-5)

1.20%

Low Cap (6-8)

1.98%

5

Figure 1 Size Premiums for Size-Decile Portfolios and

Sub-Groups of the Tenth Decile

Source: Ibbotson SBBI 2011 Valuation Yearbook.

The substantial size premiums measured for very small companies has been criticized and

its appropriateness continues to be debated among practitioners and researchers.5

One argument raised by critics concerns the effects from the lack of liquidity that

disproportionately affects stocks of smaller sized companies. The argument is that the lack of

liquidity for many small sized firms causes transactions costs of trading a share of stock to be

greater, which in turn results in greater observed historic returns to properly compensate

investors for holding these stocks relative to more liquid stocks.

Ibbotson does not disagree that lower liquidity will contribute to the magnitude of the

calculated size premiums. Ibbotson correctly responds that it is irrelevant whether or not the

5 For example, some argue that portfolios of smallest size companies contain a

disproportionate number of financially distressed firms or contain the so called “fallen angels”. See Ibbotson SBBI 2011 Valuation Yearbook, pp. 94-102 for a comprehensive review of the criticisms and Ibbotson’s responses.

6

computed size premium also reflects the lower liquidity in smaller-sized companies when

computing a stock’s fair market value; the return to equity used to compute fair market value

should include the additional return required to compensate investors for holding less liquid

stocks.6 This is because these transactions costs are real, can be substantial, and will affect the

prices paid for a share of stock.7 For example, if an investor were contemplating a purchase of

10 shares of a privately held company, the investor would certainly take into account in the

purchase price she pays the transaction costs she would have to incur in order to sell those shares

at a later time. So, to the extent that the computed size premium includes the effects of less

liquid stocks is largely irrelevant because it is generally appropriate that a fair market valuation

reflect any illiquidity effect on the expected return.

In certain circumstances, however, the purpose of valuation is not to assess the fair

market value, but rather to analyze and compute “fair value”. For example, the appropriate

measure of value in an appraisal for a merger is not fair market value but rather “fair value”. The

key differences between fair market value and fair value are that fair value requires that there be:

(1) no discount -- either direct or implied -- for the lack of liquidity; and (2) no discount for

minority interest.8

6 According to valuation literature, “fair market value” is generally defined as: “…the

amount at which property would change hands between a willing seller and a willing buyer when neither is acting under compulsion and when both have reasonable knowledge of the relevant facts.” See Pratt (2008), pp. 41-42.

7 Under the standard of fair market value, the focus must be on the specific property (ownership interest) being valued, basically “as is,” including control and marketability characteristics. Therefore, minority interests in closely held corporations or partnerships are valued to reflect lack of control and lack of marketability characteristics. See Pratt (2009), p. 10.

8 See Laro and Pratt (2011), pp. 12-13.

7

Therefore, there is general agreement that the fair value of even a completely illiquid,

privately held stock in an appraisal should not reflect any discount to the valuation that would

obtain for the same stock that traded in a completely liquid market. But, if a key valuation

parameter -- the cost of equity -- includes a premium for low liquidity, then the valuation

obtained will necessarily reflect a discount for illiquidity.

Is the value obtained from such an analysis the “fair value” of the stock if that value

reflects an implicit discount for illiquidity? Because fair value is a legal concept, the answer to

this question is left to the courts and legal scholars. This paper, however, provides an economic

context to assist in answering this question by quantifying the liquidity premium reflected in the

size-decile premiums that are currently used by many practitioners. Because the Ibbotson SBBI

Yearbooks are by far the most commonly cited and used source for size premiums, we use the

methods suggested by Ibbotson for computing size premiums and for measuring liquidity.

The rest of the paper is organized as follows. The next section discusses the relationship

between liquidity and asset pricing. The third section describes the data. Liquidity premiums,

without accounting for size, are calculated in the fourth section. The fifth section discusses the

replication of size premiums contained the Ibbotson SBBI 2011 Yearbook. The sixth section

shows the amount of liquidity premium subsumed in the calculation of size premiums for size-

decile portfolios and for the sub-groups of the tenth decile. Finally, the last section provides

concluding remarks.

II. Liquidity and Asset Pricing

The marketability or liquidity of an asset refers to the degree to which it can be converted

to cash quickly without incurring large transaction costs or price concessions. Financial theory

reasons that liquidity affects asset prices because investors price securities according to their

8

returns net of trading costs, such as transactions costs and expected price concessions, and

consequently investors require a greater return for higher expected costs of achieving liquidity,

all else the same. Thus, given two assets with the same expected cash flows but with different

liquidity, investors will pay less (demand a higher return) to hold the more illiquid asset.

Over the last 15 years, liquidity has been the subject of considerable research in the

financial literature. Many of these studies are discussed by Amihud, Mendelson, and Pedersen

(2005) who review the literature concerning the effects of liquidity on asset prices.

Thus, financial economists expect that asset and security prices will differ systematically

depending on the marketability characteristics of the securities, all else equal. For example,

restricted stock should be priced at a discount from the unrestricted stock’s traded “market” price

on a liquid exchange. Indeed, many empirical studies of restricted stock, of the relationship

between stock returns and bid-ask spreads, of a company’s block transactions, and of private

sales of a company’s stock prior to the company’s initial public offering have confirmed that

high transaction costs and other restrictions generally cause securities to be priced at significant

discounts from the market prices of comparable (often otherwise identical) liquid securities.

Table 2 summarizes the illiquidity discounts measured in several restricted stock studies.

These studies report median illiquidity discounts for restricted stock of 9% to 45% and means of

13% to 42% based on hundreds of transactions. Because the restricted stock studies provide a

direct measure of the costs of illiquidity, many experts and courts have chosen to rely on these

studies as an empirical guide in selecting illiquidity discounts to apply to the computed value

from a DCF analysis to arrive at a fair market value measure.

9

Table 2 Studies of Restricted Stock Marketability Discounts

Notes: [1] Discounts Involved in Purchases of Common Stock (1966-1969), Institutional Investor Study Report of the Securities and Exchange Commission, H.R. Doc. No. 64, Part 5, 92nd Congress, 1st Session, 1971, pp. 2444-56, cited in Pratt, Reilly and Schweihs (2000), pp. 396-398, 404. [2] Cited in Pratt, Reilly and Schweihs (2000), pp. 398-399, 404. [3] Cited in Pratt, Reilly and Schweihs (2000), pp. 399, 404. [4] Cited in Pratt, Reilly and Schweihs (2000), pp. 400, 404. [5] Cited in Pratt, Reilly and Schweihs (2000), pp. 400, 404. [6] Unpublished study, cited in Pratt, Reilly and Schweihs (2000), pp. 400, 404. [7] Discount for private placement of unregistered shares. Wruck also reports an average premium of 4.1% and median discount of 1.8% for 36 private placements of registered shares. [8] Discount for private placement of restricted shares. Hertzel and Smith also report an average discount of 15.6% for 88 private placements of non-restricted shares. [9] Oliver, R. & Meyers, R. Discounts Seen in Private Placements of Restricted Stock: The Management Planning, Inc., Long-Term Study (1980-1996). Chapter 5 in Reilly and Schweihs (2000), cited in Pratt, Reilly and Schweihs (2000), pp. 401-404. Median is approximate. [10] The 1980-1997 time period is assumed to match the previous study with additional transactions updated. [11] Unregisterd Shares. Bajaj et al. also report discounts for 37 private placements of registered shares of 14% (average) and 10% (median). [12] Study obtained from Columbia Financial Advisors, Inc. [13] Unpublished study, cited in Laro and Pratt (2005), p.289. [14] Unpublished study, cited in Laro and Pratt (2011), p. 287. [15] Unpublished study, cited in Laro and Pratt (2011), p. 287.

StudyTime

PeriodSample

SizePrice

DiscountGroup

AveragePrice

DiscountGroup

Average

SEC overall average (1971)1

Jan 1966 - June 1969 398 n/a 25.8%Gelman (1972) 1968 - 1970 89 33.0% 33.0%

Trout (1977)2

1968 - 1972 60 n/a 33.5%

Moroney (1973)3

na 146 33.0% 35.6%

Maher (1976)4

1969 - 1973 n/a n/a 35.4%

Pittock and Stryker (1983)5

Oct 1978 - June 1982 28 45.0% n/a

Willamette Management Associates6

Jan 1981 - May 1984 33 31.2% n/a

Wruck (1989)7

July 1979 - Dec 1985 37 12.2% 13.5%

Hertzel and Smith (1983)8

Jan 1980 - May 1987 18 n/a 42.0%Silber (1991) 1981 - 1988 69 n/a 33.8%Hall and Polacek (1994) 1979 - Apr 1992 100+ n/a 23.0%

Oliver and Meyers (2000)9

Jan 1980 - Dec 1996 53 25.0% 27.1%Robak and Hall (2001) 1980 - Apr 1997 230 20.1% 22.3%

Hall (2003)10 1980 - 1997 238 21.3% n/a

Hall and Polacek (1994) May 1991 - Apr 1992 17 n/a 21.0%

Bajaj, Denis, Ferris and Sarin (2001)11 Jan 1990 - Dec 1995 51 26.5% 28.1%

Johnson (1999) 1991 - 1995 72 n/a 20.2%

Finnerty (2003) Jan 1991 - Feb 1997 101 15.5% 20.1%

Aschwald (2000) Jan 1996 - Apr 1997 23 14.0% 21.0%Aschwald (2000) Jan 1997 - Dec 1998 15 9.0% 13.0%

Columbia Financial Advisors, Inc.12 June 1997 - June 2000 32 11.7% 13.5%

Columbia Financial Advisors, Inc.12 Jan 1999 - June 2000 24 11.7% 13.7%

Hall (2003) 1997 - 2000 182 25.9% n/a

FMV Opinions13 1997 - 2003 187 n/a 22.5%

FMV Opinions14 1997 - 2007 311 n/a 20.6%

Post 2007Studies

(six month holding period)

FMV Opinions15 2008 43 n/a n/a 12.6% 12.6%

1990-1997Studies

18.7% 22.1%

1997-2007Studies

(one year holding period)

14.6% 16.7%

Long-Horizon Studies

22.1% 24.1%

Median Average

Pre-1990Studies

30.9% 31.6%

10

The consensus in the liquidity literature is that theory and empirical evidence strongly

support three findings. First, investors require returns that compensate for the level of illiquidity

of an investment.9

Second, stocks in publicly traded equity markets can have substantially different degrees

of liquidity; liquidity is not a binary variable. That is, one cannot simply divide stocks into two

categories of liquidity based solely on whether or not the stock is publicly traded. While stocks

that are not publicly traded are generally characterized as illiquid, even among publicly traded

stocks, there can be important and substantial differences in the degree of liquidity.10

Third, illiquidity is correlated with size. That is, across all publicly traded stocks, more

small stocks tend to have lower liquidity than do large stocks.11 Practitioners and academics are

in general agreement that the negative relationship between returns and liquidity is stronger for

smaller stocks. In a recent study, Ibbotson et al. (2013) empirically studied the effect on returns

from differing levels of liquidity across all size quartile portfolios of publicly traded stocks

between 1972 and 2011. Their findings are presented in Table 3. Ibbotson et al. found that

within each size quartile portfolio, low liquidity portfolios generally earned higher returns than

the high liquidity portfolios. The authors, however, find that the size impact is quite inconsistent

across various levels of liquidity. Specifically, while among low liquidity stocks, small-sized

stock portfolios earned higher returns than the large stock portfolios, the opposite is true for high

9 The effect of liquidity on asset prices was first examined by Amihud and Mendelson

(1986). See also Datar, Naik, and Radcliffe (1998) and Amihud, Mendelson, and Pedersen (2005).

10 For example, Amihud and Mendelson (1986) divide publicly traded stocks into seven liquidity groups that show “significant variability”.

11 See, for example, Amihud (2002) and Ibbotson et al. (2013).

11

liquidity stocks. Thus, based on Ibbotson et al. (2013), at high levels of liquidity, the effect of

small size does not result in higher returns compared to the larger firms.

Table 3 Annualized Arithmetic Return for Size and Liquidity Quartile Portfolios

from Ibbotson et al. (2013)

Source: Ibbotson, R.G., Chen, Z., Kim, D. Y.-J., and Hu, W.Y., 2013. Liquidity as an Investment Style. Financial Analysts Journal, 69(3), Table 2 (partial).

Ibbotson et al. (2013) conclude:

Therefore, size does not capture liquidity (i.e., the liquidity premium holds regardless of size group). Conversely, the size effect does not hold across all liquidity quartiles, especially in the highest-turnover quartile. The liquidity effect, however, is strongest among microcap stocks and declines from micro- to small- to mid- to large-cap stocks.

The key finding implied by Ibbotson et al. (2013) is that for smaller-sized companies the

historic returns are substantially different between low liquidity and high liquidity stocks (first

row of Table 3). If the CAPM returns are not similarly different across the various liquidity

groups, then it implies that a substantial portion of the measure of what is generally referred to as

size premium subsumes the premium that compensates investors for holding low liquidity stocks.

II.a Liquidity Premium Creates an Illiquidity Discount to the Stock’s Valuation

If the size premium subsumes a substantial component that compensates investors for

holding less liquid stocks, then inclusion of such a size premium in the cost of equity will

necessarily result in an illiquidity discount to the stock’s fair value. There is no economic

Quartile Low LiquidityMid-Low Liquidity

Mid-High Liquidity

High Liquidity

Micro Cap 17.92% 20.00% 15.40% 6.78%

Small Cap 17.07% 16.82% 15.38% 9.89%

Mid Cap 15.01% 15.34% 14.51% 11.66%

Large Cap 12.83% 12.86% 12.81% 11.58%

12

distinction between a DCF in which the cost of capital is increased by a liquidity premium versus

a DCF that uses a cost of capital with no liquidity premium, but to which an illiquidity discount

is then applied.

As discussed in the recent Ibbotson SBBI Yearbooks, the economic equivalence can be

simply shown as follows.12 First, the valuation from a simple DCF model can be approximated

by the perpetuity model:

VL = C / R (3)

where,

VL = value of a liquid security;

C = annual cash flow; and

R = discount rate of the liquid security.

Assuming, C = $10 and R = 10%, gives VL = $10/10% or $100. Because less liquid

stocks are expected to earn higher returns to compensate investors for the lack of liquidity (all

else equal), the value of a less liquid stock can be expressed as:

VI = C / (R + P) (4)

where,

VI = value of a less liquid security; and

P = liquidity premium.

Alternatively, the value of the less liquid stock can be computed by applying an

illiquidity discount, D, to the value of the liquid stock, yielding the following equation:

VL (1 – D) = VI (5)

Solving for D gives: D = P / (R + P). Assuming a 5% liquidity premium yields a 33.3%

discount to the value of the liquid security. In other words, a liquidity premium added to the cost

of equity can always be mathematically translated to a discount for the lack of liquidity.

12 See, for example, Ibbotson SBBI 2011 Valuation Yearbook, p. 101.

13

There are two inferences from this simple economic equivalence. First, if one is

computing the fair value of a privately held stock, it is duplicative to apply a full illiquidity

discount factor to a DCF valuation when the DCF uses a cost of equity that includes a liquidity

premium. Second, if one is computing the fair value of a stock, the fair value computation will

reflect an implicit discount for lack of liquidity if the cost of equity includes a liquidity premium.

In the following sections we empirically investigate the magnitude of the liquidity

premium.

III. Data Description

We use monthly common stock data from 1926 through 2010 compiled by the Center for

Research in Security Prices (“CRSP”) at the University of Chicago Booth School of Business.

All common stock traded on the New York Stock Exchange (“NYSE”), American Stock

Exchange (“AMEX”)13, and NASDAQ stock markets are used. From 1926 through 2010, over 3

million monthly-level observations are available.

Monthly returns on the Standard & Poor’s (“S&P”) 500 index and 30-day U.S. Treasury

bill total return from 1926 through 2010 are also obtained from CRSP. Finally, long-term mean

income return component of 20-year government bonds and long-term equity risk premia are

obtained from Ibbotson SBBI 2011 Valuation Yearbook.

For the analysis of adjustment to NASDAQ volume to account for the potential over-

counting of traded volume, we use daily common stock data from 1990 through 2012 from

CRSP. For this time period, over 40 million daily-level observations are available.

13 In October 2008, AMEX was acquired by NYSE Euronext.

14

III.a Adjustment to NASDAQ Volume

Volumes in quote-driven dealer markets like NASDAQ were historically higher than

order-driven markets like NYSE because public buyers and sellers traded though the

intermediation of dealers on NASDAQ, leading to an over count of trades among public traders.

On NYSE, public buyers and sellers mostly traded among themselves. The differing market

structures caused higher volumes for NASDAQ stocks, all else equal. However, regulatory

interventions by the SEC (e.g., the 1997 SEC mandated order handling rules at NASDAQ14) as

well as the rapid growth of electronic trading mechanisms have caused the trading patterns on

different platforms to converge.

Ibbotson et al. (2013) divide volumes of NASDAQ stocks based on an adjustment factor

suggested by Anderson and Dyl (2005). Based on stocks switching from NASDAQ to NYSE

from 1997 through 2002, Anderson and Dyl find that the mean daily volume declined an average

of 24.7% and the median decrease was 37.9%. Further, based on the finding in Anderson and

Dyl (2007) that the relative over-reporting of NASDAQ stocks has not lessened during 2003-

2005 relative to the 1990-1996 time period, Ibbotson et al. (2013) apply the adjustment factor

throughout their study period of 1972-2011. While Anderson and Dyl (2007) found no evidence

that the over-reporting has lessened for NASDAQ stocks, using data from 1993-2010, Harris

(2011) reports that over time volumes between NYSE and NASDAQ stocks have become more

and more similar leading to the homogenization of US equity markets.

In light of the differences in the findings in Harris (2011) and Anderson and Dyl (2007)

and the vast changes in the stock trading landscape, we analyzed the volume of common stocks

14 See, for example, McInish, Van Ness, and Van Ness (1998).

15

switching from NASDAQ to NYSE starting in 1990 (since the regulatory changes likely to

impact the over counting of traded volume and the rapid growth of electronic trading

mechanisms occurred after 1990). We studied volume on sixty trading days before and after the

switch (with day one being the day of the switch). For each company switching from NASDAQ

to NYSE, average volume during 60 trading days before the switch is divided by average volume

during 60 trading days after the switch. The ratio of the two volumes is shown in figure 2. The

horizontal lines represent the median ratios for consecutive five year periods beginning in 1990.

As is evident from the figure and consistent with Harris (2011), the ratio has been decreasing

over time.

16

Figure 2 Average Volume on NASDAQ Before the Switch Divided by

Average Volume on NYSE After the Switch

Note: In order to focus on presenting the medians, the figure shows ratios between 0 and 4. A few outliers (greater than 4) are not shown in the figure but are used in the computation of the median ratios.

We use the median ratios over five year intervals to adjust NASDAQ volume.

Specifically, the ratio of 2.07 is used to divide NASDAQ volume prior to 1994; 1.75 is used to

divide NASDAQ volume between 1995 and 1999; 1.38 is used to divide NASDAQ volume

between 2000 and 2004; 1.32 is used to divide NASDAQ volume between 2005 and 2009; and

1.21 is used to divide NASDAQ volume after 2009.

0

1

2

3

4

1985 1990 1995 2000 2005 2010 2015

2.07

1.75

1.38 1.32

1.21

Median

17

IV. Liquidity Premium

We measure liquidity using average monthly share turnover in each quarter.15 Share

turnover is calculated as the volume of shares traded each month divided by the number of shares

outstanding at each month-end. This measure of liquidity is similar to the one used in Ibbotson

et al. (2013), except that whereas Ibbotson et al. (2013) create annual portfolios of stocks and

hence measure liquidity annually, we create portfolios of stocks that are rebalanced quarterly in

keeping with the size premium methodology in the Ibbotson SBBI Yearbooks, and hence, we

update the liquidity measure each quarter. The steps we take to create the liquidity-based

portfolios of stocks are described below.

We first rank companies with primary listings on the NYSE based on their liquidity at the

end of each quarter. As mentioned above, liquidity at the end of each quarter is measured as

average monthly share turnover in that quarter.

Second, based on these rankings, the companies are divided into two equally populated

groups based on the median liquidity at the end of each quarter. Group “H” contains companies

with liquidity greater than or equal to the median liquidity, or the high liquidity companies.

Group “L” contains companies with liquidity lower than the median liquidity, or the low

liquidity companies. The ranking of the stocks thus yields a liquidity cutoff demarcating the

“H” and “L” groups at the end of each quarter. These liquidity cutoffs obtained from NYSE

stocks are then used to assign common stocks listed on AMEX and Nasdaq to one of the two

liquidity groups based on the end of quarter liquidity measure for the AMEX and Nasdaq stocks.

15 Turnover rates and bid-ask spreads are typically used as measures of liquidity. See

Amihud et al. (2005). Another measure of liquidity is the price impact such as the ratio of absolute stock return to its dollar volume, averaged over some period (Amihud, 2002).

18

Third, the liquidity groupings are rebalanced quarterly. Each month, every company is

assigned a liquidity group based on its liquidity categorization in the previous quarter. For

example, the liquidity category that a company falls under as of the quarter ending in March is

used to assign its liquidity group for April, May, and June of that year. Thus, each stock remains

in the same liquidity group for each of the three months that follow its assignment to a liquidity

group using the liquidity measure from the end of the previous quarter. This methodology is

similar to the methodology used by CRSP and the Ibbotson SBBI Yearbooks for the creation of

the size-decile portfolios (discussed further below).

Fourth, we compute monthly portfolio returns as the average returns of the stocks in each

liquidity group from 1926 to 2010. Annual portfolio returns are computed by compounding the

monthly returns.16

Fifth, to compute the risk-adjusted portfolio returns, we compute the beta for each

liquidity portfolio using the single-factor CAPM model. Following the SBBI Yearbooks, we use

the following single-factor regression equation to estimate each portfolio’s systematic risk

(commonly referred to in the literature as the portfolio’s beta).

(rl – rf) = αl + βl (rm – rf) + εl (5)

where, rl represents monthly return on portfolio l; rf represents 30-day U.S. treasury bill total return; and rm represents monthly return on the market, measured by the S&P 500 index.

The slope of the regression, βl, in equation (5) measures the portfolio’s sensitivity to

variations in the market return, or its exposure to systematic risk.

16 Annual return is computed when monthly return data is available for each of the twelve

months.

19

Using the beta for each liquidity portfolio, βl, a CAPM portfolio return (in excess of the

riskless rate) is computed as the product of the estimated beta for that portfolio and the equity

risk premium (the difference between the mean total return of the S&P 500 index and the mean

income return component of 20-year government bonds for the time period 1926-2010).

Finally, for each liquidity portfolio of stocks, we calculate the difference between the

portfolio’s actual average annual return in excess of the risk-free rate (measured by the mean

income return component of 20-year government bonds for the time period 1926-2010) and the

CAPM return also in excess of the risk-free rate. We refer to this difference as the liquidity

premium. Table 4 presents the liquidity premiums for the “H” and “L” liquidity groups. We

find that while the high liquidity stocks have a liquidity premium of less than 1%, the liquidity

premium for the low liquidity stocks is over 7%.

Table 4 Long-Term Returns in Excess of Estimated CAPM Returns for

High and Low Liquidity Categories

Notes: Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

Using the same methodology described above, we also categorize the data into liquidity

quartiles. The results are presented in Table 5. Again, we find that liquidity premium increases

Liquidity Group Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate

Liquidity Premium (Return in Excess of CAPM Return)

[1] [2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

H 1.36 14.95% 9.78% 9.09% 0.69%

L 1.05 19.50% 14.33% 7.02% 7.31%

20

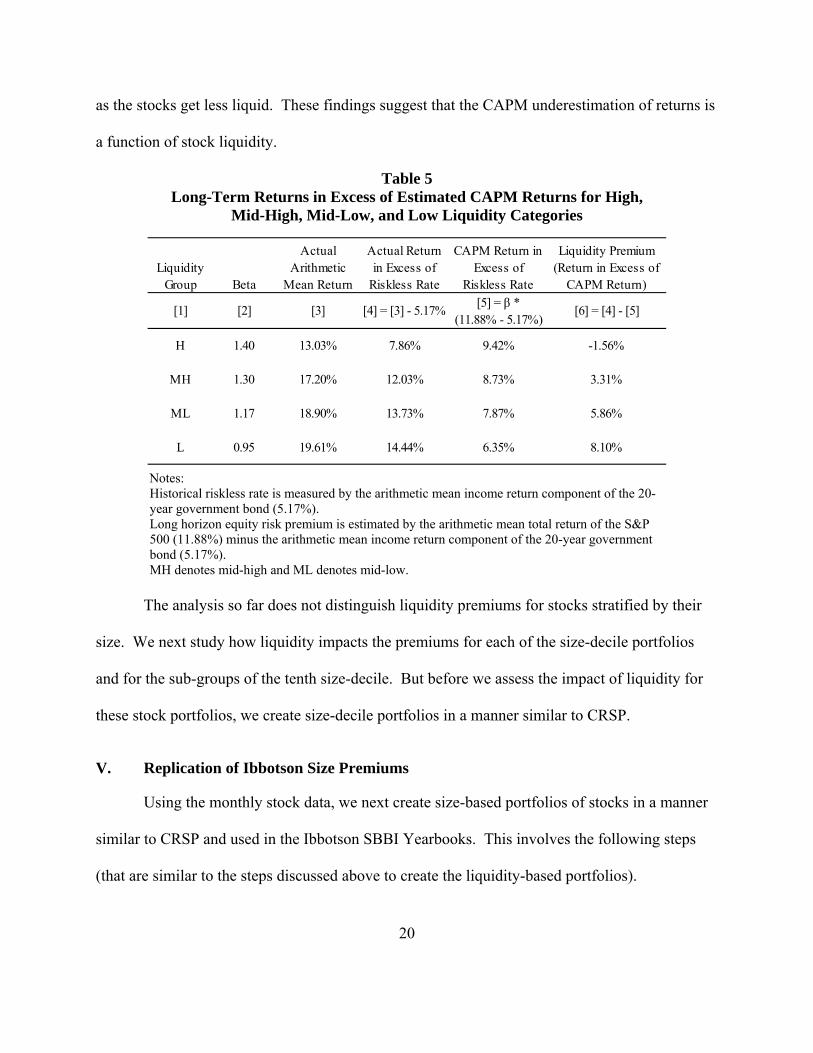

as the stocks get less liquid. These findings suggest that the CAPM underestimation of returns is

a function of stock liquidity.

Table 5 Long-Term Returns in Excess of Estimated CAPM Returns for High,

Mid-High, Mid-Low, and Low Liquidity Categories

Notes: Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%). MH denotes mid-high and ML denotes mid-low.

The analysis so far does not distinguish liquidity premiums for stocks stratified by their

size. We next study how liquidity impacts the premiums for each of the size-decile portfolios

and for the sub-groups of the tenth size-decile. But before we assess the impact of liquidity for

these stock portfolios, we create size-decile portfolios in a manner similar to CRSP.

V. Replication of Ibbotson Size Premiums

Using the monthly stock data, we next create size-based portfolios of stocks in a manner

similar to CRSP and used in the Ibbotson SBBI Yearbooks. This involves the following steps

(that are similar to the steps discussed above to create the liquidity-based portfolios).

Liquidity Group Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate

Liquidity Premium (Return in Excess of

CAPM Return)

[1] [2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

H 1.40 13.03% 7.86% 9.42% -1.56%

MH 1.30 17.20% 12.03% 8.73% 3.31%

ML 1.17 18.90% 13.73% 7.87% 5.86%

L 0.95 19.61% 14.44% 6.35% 8.10%

21

Using monthly data from 1926-2010, we first rank the companies with primary listings

on the NYSE based on their market capitalizations at the end of each quarter. Market

capitalization is calculated as the product of the closing price on the last trading date of the

quarter and the shares outstanding.17

Second, based on these rankings, the companies are divided into equally populated

deciles (decile 1 contains the largest companies, and decile 10 the smallest). Thus, the ranking

of the NYSE stocks yield size cutoffs for each decile, where the cutoffs are the highest and

lowest market capitalizations within each size-decile. These decile cutoffs obtained from NYSE

stocks are then used to assign common stocks listed on AMEX and Nasdaq to one of the size

deciles based on the end of fiscal quarter market capitalization for the AMEX and Nasdaq stocks.

Third, size-decile portfolios are constructed for the stocks based on the size-decile

rankings. Each month, every company is assigned a portfolio based on its decile ranking in the

previous quarter. For example, the decile ranking of a stock based on its market capitalization as

of the quarter ending in March is used to determine the stock’s size-decile for the months of

April, May, and June. Thus, each stock remains in the same size-decile for each of three months

that follow its assignment to a size-decile using the market capitalization from the end of the

previous quarter.

Fourth, monthly portfolio returns are computed as the weighted average returns of the

stocks in each size-decile, using market capitalizations based on the shares outstanding and

17 In the calculation of the liquidity portfolios discussed above we calculated the average

monthly share turnover over a quarter instead of just using the last month in the quarter in order to preserve observations in the analysis that otherwise would be lost due to missing volume data in the last months of the quarters.

22

closing price for the last trading day of the previous month as weights. Annual portfolio returns

are computed by compounding the monthly returns.

Fifth, to compute the risk-adjusted portfolio returns, we compute the beta for each size-

decile portfolio using the single-factor CAPM model. Again, following the SBBI Yearbooks, we

use the following single-factor regression equation to estimate each portfolio’s systematic risk.

(rs – rf) = αs + βs (rm – rf) + εs (6)

where, rs represents monthly return on portfolio s; rf represents 30-day U.S. treasury bill total return; and rm represents monthly return on the market, measured by the S&P 500 index.

The slope of the regression, βs, in equation (6) measures the portfolio’s sensitivity to

variations in the market return, or its exposure to systematic risk.

Using the beta for each size-decile portfolio, βs, a CAPM portfolio return (in excess of the

riskless rate) is computed as the product of the estimated beta for that portfolio and the equity

risk premium.

Finally, for each size-decile portfolio of stocks, we calculate the difference between the

portfolio’s actual average annual return in excess of the risk-free rate (measured by the mean

income return component of 20-year government bonds for the time period 1926-2010) and the

CAPM return also in excess of the risk-free rate. This difference is what is referred to as the size

premium in the Ibbotson SBBI publications.

Table 6 presents the size premiums by size-decile. As the table shows, our computed size

premiums are very similar to the size premiums reported in the Ibbotson SBBI 2011 Yearbook.

23

Table 6 Comparison of Ibbotson SBBI and Torchio-Surana Long-Term Returns in Excess of

Estimated CAPM Returns for Size-Decile Portfolios

Notes: Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

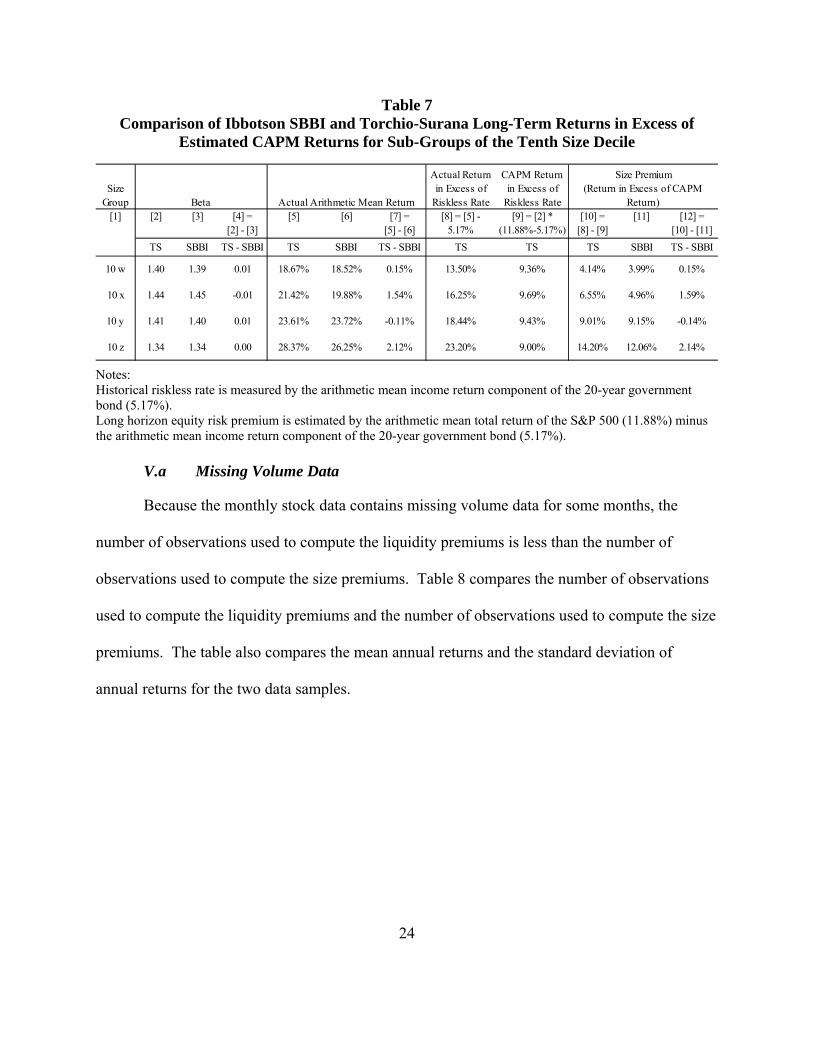

As discussed above, Ibbotson divides the smallest size-decile, decile 10, into 4 size sub-

groups (10w, 10x, 10y, and 10z) using the same methodology that is used to construct the 10

size-decile portfolios. In Table 7, we replicate that analysis and show the computed size

premiums for sub-size groups w, x, y, and z for decile 10 are quite close to the size premiums

reported in the Ibbotson SBBI 2011 Yearbook. One reason for the differences between our

estimates and those reported in the Ibbotson SBBI Yearbook is that Ibbotson SBBI uses its

internal database of companies for the sub-groups of the tenth decile (based on email

communication with Morningstar). Notwithstanding the differences, the results are wholly

consistent with that from Ibbotson.

Decile

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate[1] [2] [3] [4] =

[2] - [3][5] [6] [7] =

[5] - [6][8] = [5] - 5.17% [9] = [2] *

(11.88%-5.17%)[10] =

[8] - [9][11] [12] =

[10] - [11]TS SBBI TS - SBBI TS SBBI TS - SBBI TS TS TS SBBI TS - SBBI

1 0.92 0.91 0.01 10.87% 10.92% -0.05% 5.70% 6.15% -0.44% -0.38% -0.06%

2 1.03 1.03 0.00 13.02% 12.92% 0.10% 7.85% 6.89% 0.96% 0.81% 0.15%

3 1.10 1.10 0.00 13.44% 13.56% -0.12% 8.27% 7.40% 0.88% 1.01% -0.13%

4 1.13 1.12 0.01 14.04% 13.91% 0.13% 8.87% 7.57% 1.30% 1.20% 0.10%

5 1.17 1.16 0.01 14.66% 14.75% -0.09% 9.49% 7.82% 1.67% 1.81% -0.14%

6 1.19 1.19 0.00 14.93% 14.95% -0.02% 9.76% 7.97% 1.79% 1.82% -0.03%

7 1.23 1.24 -0.01 15.24% 15.38% -0.14% 10.07% 8.25% 1.82% 1.88% -0.06%

8 1.30 1.30 0.00 16.20% 16.54% -0.34% 11.03% 8.70% 2.33% 2.65% -0.32%

9 1.34 1.35 -0.01 17.01% 17.16% -0.15% 11.84% 8.99% 2.85% 2.94% -0.09%

10 1.40 1.41 -0.01 21.49% 20.97% 0.52% 16.32% 9.40% 6.93% 6.36% 0.57%

Size Premium (Return in Excess of CAPM Return)Beta Actual Arithmetic Mean Return

24

Table 7 Comparison of Ibbotson SBBI and Torchio-Surana Long-Term Returns in Excess of

Estimated CAPM Returns for Sub-Groups of the Tenth Size Decile

Notes: Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

V.a Missing Volume Data

Because the monthly stock data contains missing volume data for some months, the

number of observations used to compute the liquidity premiums is less than the number of

observations used to compute the size premiums. Table 8 compares the number of observations

used to compute the liquidity premiums and the number of observations used to compute the size

premiums. The table also compares the mean annual returns and the standard deviation of

annual returns for the two data samples.

Size Group

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate[1] [2] [3] [4] =

[2] - [3][5] [6] [7] =

[5] - [6][8] = [5] -

5.17%[9] = [2] *

(11.88%-5.17%)[10] =

[8] - [9][11] [12] =

[10] - [11]

TS SBBI TS - SBBI TS SBBI TS - SBBI TS TS TS SBBI TS - SBBI

10 w 1.40 1.39 0.01 18.67% 18.52% 0.15% 13.50% 9.36% 4.14% 3.99% 0.15%

10 x 1.44 1.45 -0.01 21.42% 19.88% 1.54% 16.25% 9.69% 6.55% 4.96% 1.59%

10 y 1.41 1.40 0.01 23.61% 23.72% -0.11% 18.44% 9.43% 9.01% 9.15% -0.14%

10 z 1.34 1.34 0.00 28.37% 26.25% 2.12% 23.20% 9.00% 14.20% 12.06% 2.14%

Size Premium (Return in Excess of CAPM

Return)Beta Actual Arithmetic Mean Return

25

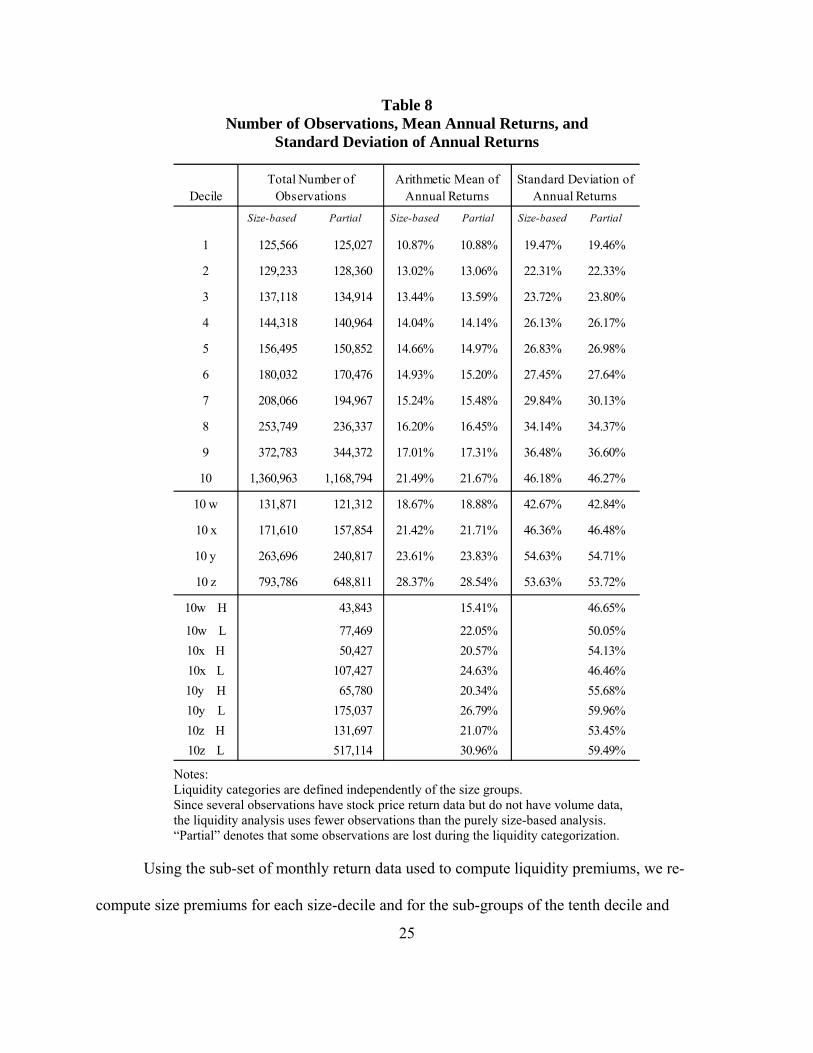

Table 8 Number of Observations, Mean Annual Returns, and

Standard Deviation of Annual Returns

Notes: Liquidity categories are defined independently of the size groups. Since several observations have stock price return data but do not have volume data, the liquidity analysis uses fewer observations than the purely size-based analysis. “Partial” denotes that some observations are lost during the liquidity categorization.

Using the sub-set of monthly return data used to compute liquidity premiums, we re-

compute size premiums for each size-decile and for the sub-groups of the tenth decile and

DecileTotal Number of

ObservationsArithmetic Mean of

Annual ReturnsStandard Deviation of

Annual Returns

Size-based Partial Size-based Partial Size-based Partial

1 125,566 125,027 10.87% 10.88% 19.47% 19.46%

2 129,233 128,360 13.02% 13.06% 22.31% 22.33%

3 137,118 134,914 13.44% 13.59% 23.72% 23.80%

4 144,318 140,964 14.04% 14.14% 26.13% 26.17%

5 156,495 150,852 14.66% 14.97% 26.83% 26.98%

6 180,032 170,476 14.93% 15.20% 27.45% 27.64%

7 208,066 194,967 15.24% 15.48% 29.84% 30.13%

8 253,749 236,337 16.20% 16.45% 34.14% 34.37%

9 372,783 344,372 17.01% 17.31% 36.48% 36.60%

10 1,360,963 1,168,794 21.49% 21.67% 46.18% 46.27%

10 w 131,871 121,312 18.67% 18.88% 42.67% 42.84%

10 x 171,610 157,854 21.42% 21.71% 46.36% 46.48%

10 y 263,696 240,817 23.61% 23.83% 54.63% 54.71%

10 z 793,786 648,811 28.37% 28.54% 53.63% 53.72%

10w H 43,843 15.41% 46.65%

10w L 77,469 22.05% 50.05%

10x H 50,427 20.57% 54.13%

10x L 107,427 24.63% 46.46%

10y H 65,780 20.34% 55.68%

10y L 175,037 26.79% 59.96%

10z H 131,697 21.07% 53.45%

10z L 517,114 30.96% 59.49%

26

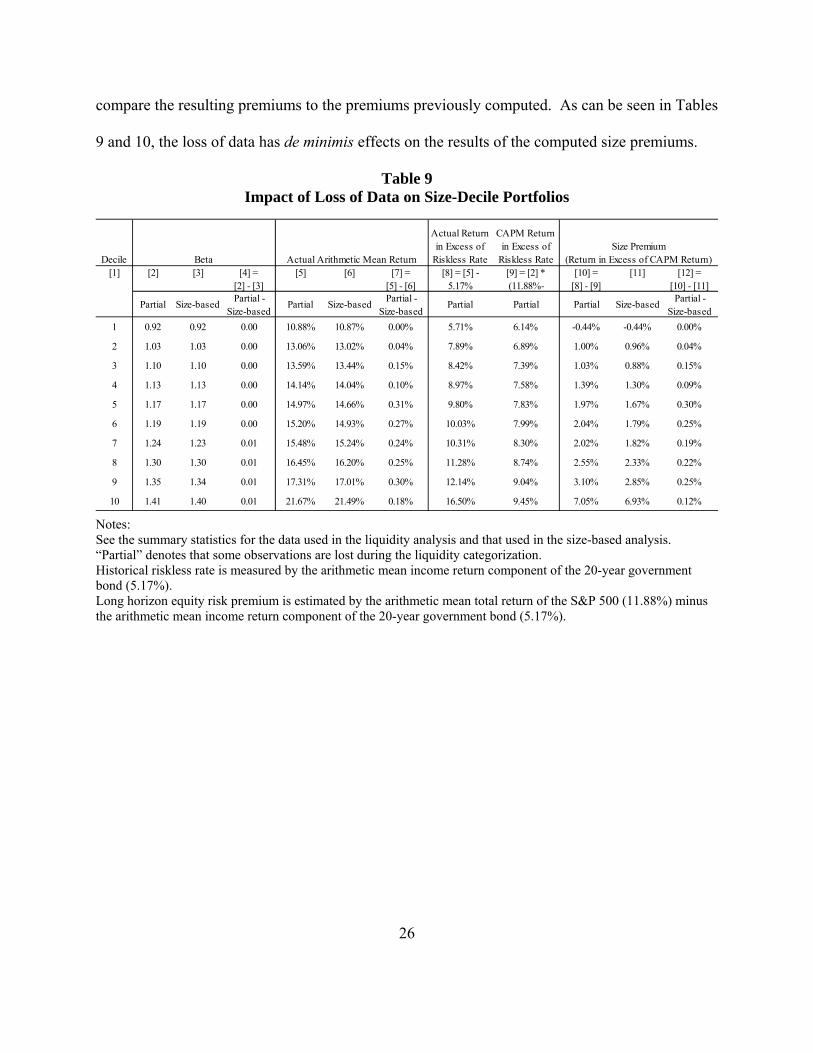

compare the resulting premiums to the premiums previously computed. As can be seen in Tables

9 and 10, the loss of data has de minimis effects on the results of the computed size premiums.

Table 9 Impact of Loss of Data on Size-Decile Portfolios

Notes: See the summary statistics for the data used in the liquidity analysis and that used in the size-based analysis. “Partial” denotes that some observations are lost during the liquidity categorization. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

Decile

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate[1] [2] [3] [4] =

[2] - [3][5] [6] [7] =

[5] - [6][8] = [5] -

5.17%[9] = [2] * (11.88%-

[10] = [8] - [9]

[11] [12] = [10] - [11]

Partial Size-basedPartial -

Size-basedPartial Size-based

Partial - Size-based

Partial Partial Partial Size-basedPartial -

Size-based

1 0.92 0.92 0.00 10.88% 10.87% 0.00% 5.71% 6.14% -0.44% -0.44% 0.00%

2 1.03 1.03 0.00 13.06% 13.02% 0.04% 7.89% 6.89% 1.00% 0.96% 0.04%

3 1.10 1.10 0.00 13.59% 13.44% 0.15% 8.42% 7.39% 1.03% 0.88% 0.15%

4 1.13 1.13 0.00 14.14% 14.04% 0.10% 8.97% 7.58% 1.39% 1.30% 0.09%

5 1.17 1.17 0.00 14.97% 14.66% 0.31% 9.80% 7.83% 1.97% 1.67% 0.30%

6 1.19 1.19 0.00 15.20% 14.93% 0.27% 10.03% 7.99% 2.04% 1.79% 0.25%

7 1.24 1.23 0.01 15.48% 15.24% 0.24% 10.31% 8.30% 2.02% 1.82% 0.19%

8 1.30 1.30 0.01 16.45% 16.20% 0.25% 11.28% 8.74% 2.55% 2.33% 0.22%

9 1.35 1.34 0.01 17.31% 17.01% 0.30% 12.14% 9.04% 3.10% 2.85% 0.25%

10 1.41 1.40 0.01 21.67% 21.49% 0.18% 16.50% 9.45% 7.05% 6.93% 0.12%

Size Premium (Return in Excess of CAPM Return)Beta Actual Arithmetic Mean Return

27

Table 10 Impact of Loss of Data on Sub-Groups of the Tenth Decile

Notes: See the summary statistics for the data used in the liquidity analysis and that used in the size-based analysis. “Partial” denotes that some observations are lost during the liquidity categorization. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

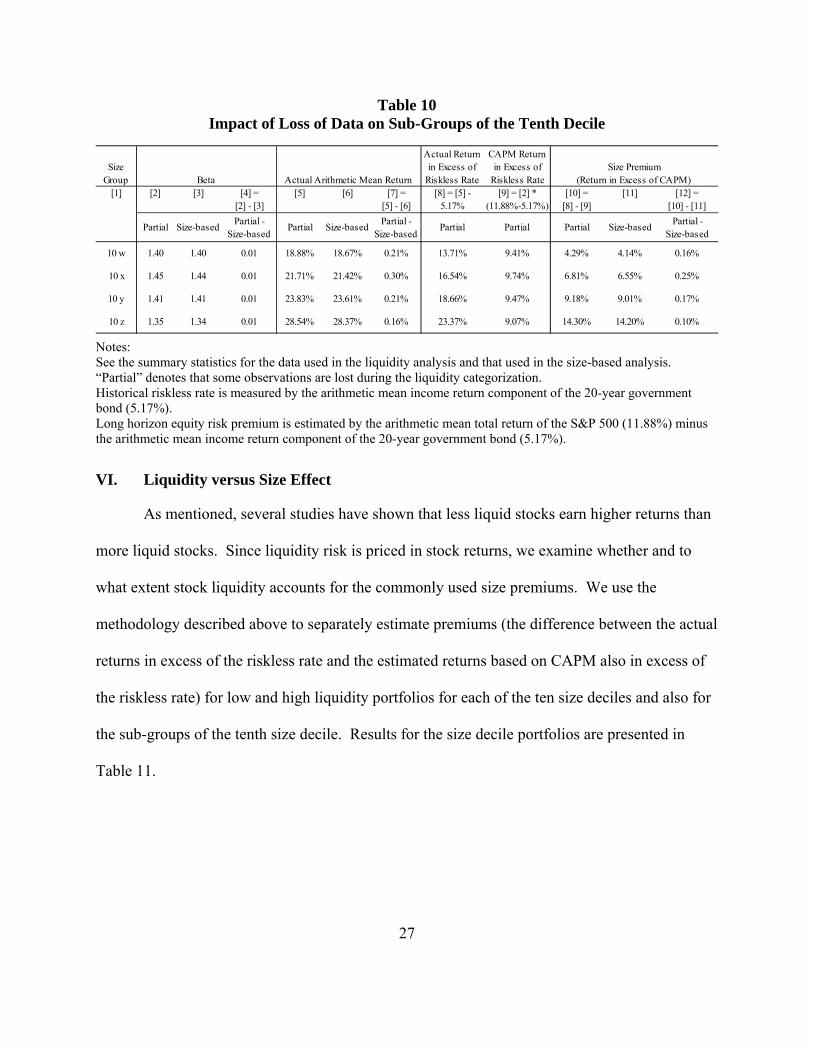

VI. Liquidity versus Size Effect

As mentioned, several studies have shown that less liquid stocks earn higher returns than

more liquid stocks. Since liquidity risk is priced in stock returns, we examine whether and to

what extent stock liquidity accounts for the commonly used size premiums. We use the

methodology described above to separately estimate premiums (the difference between the actual

returns in excess of the riskless rate and the estimated returns based on CAPM also in excess of

the riskless rate) for low and high liquidity portfolios for each of the ten size deciles and also for

the sub-groups of the tenth size decile. Results for the size decile portfolios are presented in

Table 11.

Size Group

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate[1] [2] [3] [4] =

[2] - [3][5] [6] [7] =

[5] - [6][8] = [5] -

5.17%[9] = [2] *

(11.88%-5.17%)[10] =

[8] - [9][11] [12] =

[10] - [11]

Partial Size-basedPartial -

Size-basedPartial Size-based

Partial - Size-based

Partial Partial Partial Size-basedPartial -

Size-based

10 w 1.40 1.40 0.01 18.88% 18.67% 0.21% 13.71% 9.41% 4.29% 4.14% 0.16%

10 x 1.45 1.44 0.01 21.71% 21.42% 0.30% 16.54% 9.74% 6.81% 6.55% 0.25%

10 y 1.41 1.41 0.01 23.83% 23.61% 0.21% 18.66% 9.47% 9.18% 9.01% 0.17%

10 z 1.35 1.34 0.01 28.54% 28.37% 0.16% 23.37% 9.07% 14.30% 14.20% 0.10%

Size Premium (Return in Excess of CAPM)Beta Actual Arithmetic Mean Return

28

Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate

Premium (Return in Excess of CAPM Return)

[2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

1 H 1.12 11.32% 6.15% 7.50% -1.35%

L 0.81 10.71% 5.54% 5.41% 0.13%

2 H 1.18 12.92% 7.75% 7.90% -0.16%

L 0.87 13.28% 8.11% 5.87% 2.25%

3 H 1.25 13.49% 8.32% 8.37% -0.05%

L 0.93 14.28% 9.11% 6.22% 2.88%

4 H 1.31 14.04% 8.87% 8.80% 0.07%

L 0.90 14.49% 9.32% 6.07% 3.25%

5 H 1.33 14.66% 9.49% 8.92% 0.57%

L 0.97 15.68% 10.51% 6.50% 4.01%

6 H 1.37 14.04% 8.87% 9.21% -0.33%

L 0.98 16.62% 11.45% 6.55% 4.90%

7 H 1.41 14.68% 9.51% 9.45% 0.06%

L 1.06 16.61% 11.44% 7.10% 4.34%

8 H 1.46 15.19% 10.02% 9.83% 0.19%

L 1.13 18.18% 13.01% 7.61% 5.40%

9 H 1.51 17.27% 12.10% 10.10% 1.99%

L 1.20 18.49% 13.32% 8.08% 5.25%

10 H 1.62 18.52% 13.35% 10.90% 2.46%

L 1.31 25.11% 19.94% 8.76% 11.18%

Group

[1]

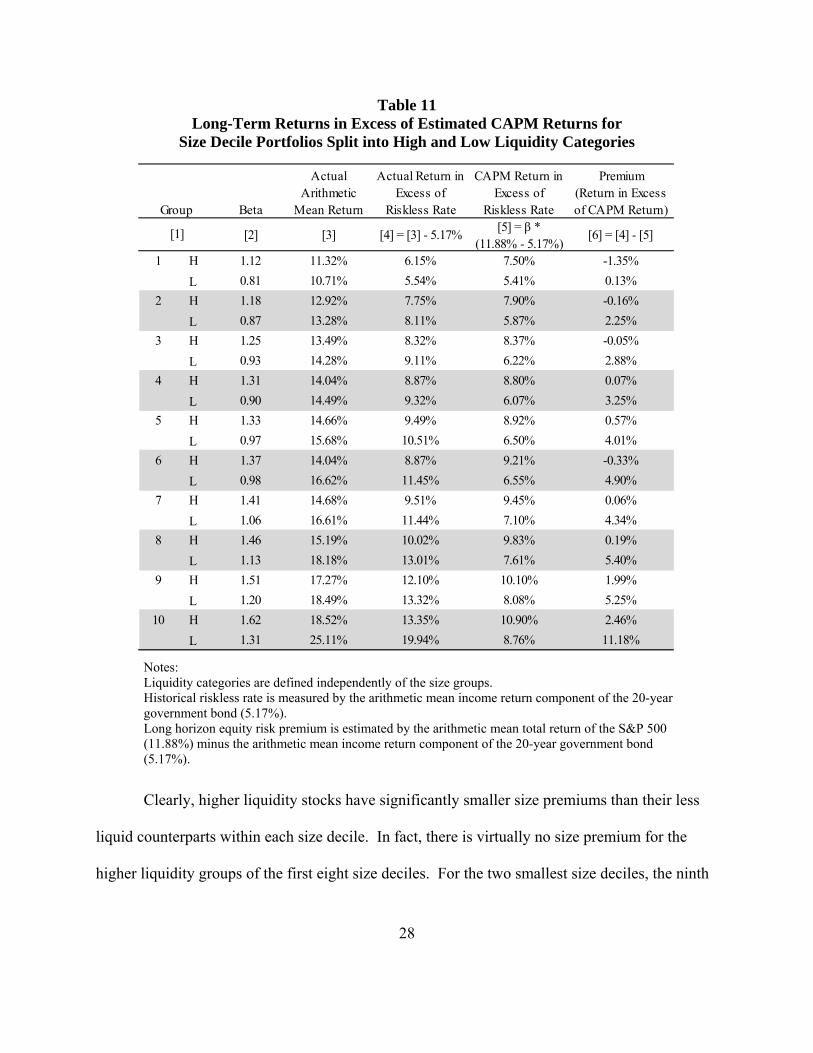

Table 11 Long-Term Returns in Excess of Estimated CAPM Returns for

Size Decile Portfolios Split into High and Low Liquidity Categories

Notes: Liquidity categories are defined independently of the size groups. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

Clearly, higher liquidity stocks have significantly smaller size premiums than their less

liquid counterparts within each size decile. In fact, there is virtually no size premium for the

higher liquidity groups of the first eight size deciles. For the two smallest size deciles, the ninth

29

Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

CAPM Return in Excess of

Riskless Rate

Premium (Return in Excess of CAPM Return)

[2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

10 w H 1.58 15.41% 10.24% 10.61% -0.37%

L 1.31 22.05% 16.88% 8.80% 8.08%

10 x H 1.61 20.57% 15.40% 10.84% 4.57%

L 1.35 24.63% 19.46% 9.06% 10.40%

10 y H 1.76 20.34% 15.17% 11.83% 3.34%

L 1.31 26.79% 21.62% 8.77% 12.85%

10 z H 1.84 21.07% 15.90% 12.33% 3.57%

L 1.23 30.96% 25.79% 8.24% 17.55%

Group

[1]

and the tenth deciles, the premiums for the high liquidity group are only 2% and 2.5%,

respectively.

Results for each of the sub-groups of the tenth decile (groups 10w, 10x, 10y, and 10z) are

shown in Table 12. As before, for each of the sub-groups of the tenth decile, premiums for the

portfolios of high liquidity stocks are considerably smaller than the premiums for their lower

liquidity counterparts. Indeed, the premium is not greater than 5% in any of the sub-groups’ high

liquidity portfolios of stocks.

Table 12 Long-Term Returns in Excess of Estimated CAPM Returns for

Sub-Groups of the Tenth Size Decile Split into High and Low Liquidity Categories

Notes: Liquidity categories are defined independently of the size groups. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%). One observation from Tables 11 and 12 is that within each size group the estimated beta

is greater for the high liquidity stocks than for the low liquidity stocks. Since higher liquidity

30

stocks by definition trade more frequently than less liquid stocks, their prices more quickly

reflect the movements of the broader market. Thus, the high liquidity stocks are less prone to the

under-estimation of beta that low liquidity stocks suffer because of a lagged response to the

market movements. Hence, the betas and therefore the estimated CAPM returns are higher for

more liquid stocks than less liquid stocks within the same size portfolio of stocks. Beta estimates

for low liquidity stocks can be improved by accounting for their lagged response to market

movements. We discuss one such methodology in the Appendix.

The second observation from Tables 11 and 12 is that within each size group, the average

actual returns for high liquidity stocks are greater than that for low liquidity stocks. This is

consistent with the findings in the general liquidity literature that investors require compensation

for holding low liquidity stocks, even within the same size group. The higher actual returns

combined with the lower CAPM returns explain the significantly higher premiums for the less

liquid stock relative to their more liquid counterparts within the same size group.

VI.a Comparison of Size Premiums of Higher Liquidity Stocks to Ibbotson SBBI Size Premiums

We next compare the size premiums of higher liquidity stocks to the frequently used size

premiums published in Ibbotson SBBI. Table 13 shows that for all size portfolios, the size

premiums for higher liquidity stocks are substantially smaller than the size premiums published

in Ibbotson SBBI.

31

Decile

Ibbotson SBBI High Liquidity

1 -0.38% -1.35%

2 0.81% -0.16%

3 1.01% -0.05%

4 1.20% 0.07%

5 1.81% 0.57%

6 1.82% -0.33%

7 1.88% 0.06%

8 2.65% 0.19%

9 2.94% 1.99%

10 6.36% 2.46%

10 w 3.99% -0.37%

10 x 4.96% 4.57%

10 y 9.15% 3.34%

10 z 12.06% 3.57%

Size Premium

Table 13 Comparison of Size Premiums of Higher Liquidity

Stocks to Ibbotson SBBI Size Premiums

Notes: [1] Ibbotson SBBI size premiums are from the 2011 Yearbook. [2] See Tables 11 and 12 for the computation of size premiums for the high liquidity stocks.

In summary, our research shows that, within each size portfolio, higher liquidity stocks

have substantially smaller size premiums than the size premiums computed for all (higher and

lower liquidity) stocks. This finding holds across all size portfolios. The lowest size portfolios

exhibit the largest difference in size premiums between higher liquidity stocks and all stocks.

The main inference from our findings is that the commonly used size premiums from

Ibbotson SBBI are overestimates of the true size premiums for higher liquidity stocks. This

arguably has significant implications in valuations for which the purpose is to compute fair

32

value, which requires no reduction to value for lack of liquidity. The implicit illiquidity discount

from using the commercial size premiums can be substantial. For example, for sub-group 10z

the difference between Ibbotson SBBI size premium of 12.06% and the 3.57% size premium for

higher liquidity stocks in sub-group 10z is 8.5%. This 8.5% difference results in an implicit

illiquidity discount of one-third for the average stock in sub-decile 10z (assuming a discount rate

of 17.5%). Hence, the effect is non-trivial.

VII. Conclusion

In many circumstances, it is necessary to compute a stock’s fair value, which by

definition eliminates any reduction to value because of a lack of marketability or liquidity. The

method of computing fair value most frequently used by practitioners is the DCF analysis. A

critical parameter of a DCF analysis is the computation of the cost of equity. Over the last

decade, many practitioners have included in the computation of the cost of equity, a premium

based on the finding that historic returns for firms with lower market capitalization are

systematically greater than the returns implied by the standard CAPM. This difference between

the observed returns for small-sized firms and the computed CAPM returns is called a size

premium. Ibbotson SBBI is the most common source of size premiums used by practitioners.

In theory, the size premium compensates investors for the systematic risk of holding

small capitalization companies. Researchers have recognized that the measurement of size

premiums can also include the effects from the lack of liquidity that disproportionately affects

stocks of smaller-sized companies. The lack of liquidity for small-sized firms causes

transactions costs of trading a share of stock to be greater, which in turn results in a premium to

properly compensate investors for holding these stocks relative to more liquid stocks.

33

Our research builds on the general research on liquidity premiums. We stratify the stocks

used by Ibbotson SBBI to compute size premiums by a measure of liquidity used by Ibbotson et

al. (2013). For each size grouping used by Ibbotson SBBI, we divide the size group into high

and low liquidity groups. Our findings show that the frequently used measure of size premiums

includes a substantial fraction that is explained by illiquid trading. For example, the size

premium in the smallest size grouping by Ibbotson SBBI (sub-group 10z) is 12.06%. When we

stratify the stocks by liquidity, the size premium for the high liquidity stocks in sub-group 10z is

reduced to 3.57%. Thus, the majority of the measure of commonly used size premiums is

attributable to the lack of liquidity.

This finding has implications for computing fair value which is meant to abstract from

reductions due to illiquidity. Specifically, valuations of small capitalization stocks that reflect

the Ibbotson SBBI size premium will cause the fair value to be reduced because of the effect of

illiquidity. The smaller the size, the greater is the reduction due to illiquidity from using the

Ibbotson SBBI size premiums.

Is the value obtained from such a DCF analysis that uses the standard size premium really

the “fair value” of the stock if that value reflects an implicit discount for illiquidity? Because

fair value is a legal concept, the answer to this question is left to the courts and legal scholars.

This paper, however, provides an economic context to assist in answering this question by

quantifying the liquidity premium reflected in the size-decile premiums that are currently used

by many practitioners.

34

APPENDIX Effect of the Sum Beta Methodology

One method suggested to provide a better estimate of beta, one that reduces the under-

estimation problem in less liquid stocks, is by accounting for the lagged response of small-sized

companies to market movements by including in the regression a lagged market return in

addition to the current market return. We use the method suggested by Ibbotson, Kaplan, and

Peterson (1997) and calculate a current and a lagged beta coefficient and then sum the two

coefficients to arrive at the beta estimate (called the sum beta). Tables 14 and 15 present the

premiums for the high and low liquidity groups for the ten size-decile portfolios and for the sub-

groups of the tenth decile, respectively, using the sum beta methodology. As expected, by better

capturing the response to market movements, the sum beta methodology lowers the estimated

premiums.

35

Table 14 Long-Term Returns in Excess of Estimated Returns using the Sum Beta

Methodology for Size Decile Portfolios Split into High and Low Liquidity Categories

Notes: Sum betas are estimated based on the methodology proposed by Ibbotson, Kaplan, and Peterson (1997). Liquidity categories are defined independently of the size groups. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

Sum Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

Estimated Return in Excess of

Riskless Rate

(Return in Excess of Estimated

Return)

[2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

1 H 1.12 11.32% 6.15% 7.54% -1.39%

L 0.78 10.71% 5.54% 5.25% 0.29%

2 H 1.19 12.92% 7.75% 8.00% -0.25%

L 0.91 13.28% 8.11% 6.08% 2.03%

3 H 1.26 13.49% 8.32% 8.44% -0.11%

L 0.99 14.28% 9.11% 6.64% 2.46%

4 H 1.35 14.04% 8.87% 9.06% -0.20%

L 1.01 14.49% 9.32% 6.75% 2.56%

5 H 1.37 14.66% 9.49% 9.17% 0.32%

L 1.09 15.68% 10.51% 7.33% 3.18%

6 H 1.45 14.04% 8.87% 9.73% -0.85%

L 1.13 16.62% 11.45% 7.60% 3.85%

7 H 1.48 14.68% 9.51% 9.96% -0.45%

L 1.25 16.61% 11.44% 8.39% 3.05%

8 H 1.63 15.19% 10.02% 10.94% -0.92%

L 1.39 18.18% 13.01% 9.33% 3.68%

9 H 1.67 17.27% 12.10% 11.22% 0.88%

L 1.46 18.49% 13.32% 9.82% 3.50%

10 H 1.82 18.52% 13.35% 12.20% 1.15%

L 1.67 25.11% 19.94% 11.23% 8.71%

Group

[1]

36

Sum Beta

Actual Arithmetic

Mean Return

Actual Return in Excess of

Riskless Rate

Estimated Return in Excess of

Riskless Rate

Premium (Return in Excess of Estimated Return)

[2] [3] [4] = [3] - 5.17%[5] = β *

(11.88% - 5.17%)[6] = [4] - [5]

10 w H 1.70 15.41% 10.24% 11.39% -1.15%

L 1.61 22.05% 16.88% 10.80% 6.08%

10 x H 1.91 20.57% 15.40% 12.79% 2.61%

L 1.75 24.63% 19.46% 11.72% 7.74%

10 y H 1.94 20.34% 15.17% 13.04% 2.13%

L 1.68 26.79% 21.62% 11.24% 10.38%

10 z H 2.34 21.07% 15.90% 15.73% 0.17%

L 1.61 30.96% 25.79% 10.83% 14.95%

Group

[1]

Table 15 Long-Term Returns in Excess of Estimated Returns using the Sum Beta

Methodology for Sub-Groups of the Tenth Size Decile Split into High and Low Liquidity Categories

Notes: Sum betas are estimated based on the methodology proposed by Ibbotson, Kaplan, and Peterson (1997). Liquidity categories are defined independently of the size groups. Historical riskless rate is measured by the arithmetic mean income return component of the 20-year government bond (5.17%). Long horizon equity risk premium is estimated by the arithmetic mean total return of the S&P 500 (11.88%) minus the arithmetic mean income return component of the 20-year government bond (5.17%).

The results show that by using sum betas, the beta estimates increase as compared to the

beta estimates from the single beta models used in Tables 11 and 12. Interestingly, the higher

betas that obtain from using the sum beta approach almost eliminate any size premium for size

deciles 1-10 for the higher liquidity stocks. Within decile 10, the results are somewhat mixed

with the size premium for higher liquidity stocks virtually zero for sub-groups 10w and 10z, but

positive 2.61% to 2.13% for sub-groups 10x and 10y, respectively.

37

REFERENCES

Amihud, Y., 2002. Illiquidity and stock returns: cross-section and time-series effects. Journal of Financial Markets, 5(1), pp.31–56.

Amihud, Y., Hendelson, H. & Pedersen, L., 2005. Liquidity and asset prices. Foundations and Trends in Finance, 1(4), pp.269–364.

Amihud, Y. & Mendelson, H., 1986. Asset pricing and the bid-ask spread. Journal of Financial Economics, 17, pp.223–249.

Anderson, A. & Dyl, E., 2005. Market structure and trading volume. Journal of Financial Research, XXVIII(1), pp.115–131.

Anderson, A.M. & Dyl, E.A., 2007. Trading Volume: NASDAQ and the NYSE. Financial Analysts Journal, 63(3), pp.79–86.

Aschwald, K., 2000. Restricted Stock Discounts Decline as a Result of 1-Year Holding Period. Shannon Pratt’s Business Valuation Update 6 (5), pp. 1-5.

Bajaj, M., Denis, D., Ferris, S., & Sarin, A., 2001. Firm Value and Marketability Discounts. The Journal of Corporation Law, Fall, pp.89-115.

Banz, R.W., 1981. The Relationship between Return and Market Value of Common Stocks. Journal of Financial Economics, 9(1), pp.3–18.

Datar, V.T., Naik, N.Y. & Radcliffe, R., 1998. Liquidity and stock returns: An alternative test. Journal of Financial Markets, 1(2), pp.203–219.

Van Dijk, M. a., 2011. Is size dead? A review of the size effect in equity returns. Journal of Banking & Finance, 35(12), pp.3263–3274.

Fama, E.F. & French, K.R., 2004. The Capital Asset Pricing Model: Theory and Evidence. Journal of Economic Perspectives, 18(3), pp.25–46.

Finnerty, J., 2003. The Impact of Transfer Restrictions on Stock Prices. Analysis Group Working Paper.

Gelman, M., 1972. An Economist-Financial Analyst’s Approach to Valuing Stock in a Closely Held Company. Journal of Taxation, June, pp. 353-354.

Hall, L., 2003. Why Are Restricted Stock Discounts Actually Larger for One-Year Holding Periods. Shannon Pratt’s Business Valuation Update 9 (9), September, pp.1,3-4.

38

Hall, L., & Polacek, T., 1994. Strategies for Obtaining the Largest Valuation Discounts. Estate Planning, January/February, pp. 38-44.

Harris, L., 2011. The Homogenization of US Equity Trading. Working Paper.

Hertzel, M., & Smith, R., 1983. Market Discounts and Shareholder Gains for Placing Equity Privately. The Journal of Finance, 48 (2), pp. 459-485.

Ibbotson, R.G. et al., 2013. Liquidity as an Investment Style. Financial Analysts Journal, 69(3), pp.30–44.

Ibbotson, R.G., Kaplan, P.D. & Peterson, J.D., 1997. Estimates of Small Stock Betas are Much Too Low. Journal of Portfolio Management, Summer.

Ibbotson SBBI Valuation Yearbook, Morningstar (formerly Ibbotson Associates), for years 2001, 2010, and 2011.

Johnson, B., 1999. Quantitative Support for Discounts for Lack of Marketability. Business Valuation Review 18 (4), pp. 152-155.

Laro, D. & Pratt, S., 2005. Business Valuation and Taxes: Procedure, Law, and Perspective. John Wiley & Sons.

Laro, D. & Pratt, S.P., 2011. Business Valuation and Federal Taxes: Procedure, Law and Perspective 2nd ed., John Wiley & Sons.

Maher, J., 1976. Discounts for Lack of Marketability for Closely Held Business Interests. Taxes, September , pp. 562-571.

McInish, T.H., Van Ness, B.F. & Van Ness, R.A., 1998. The Effect of the SEC’s Order-Handling Rules on Nasdaq. The Journal of Financial Research, XXI(3), pp.247–254.

Moroney, R., 1973. Most Courts Overvalue Closely Held Stocks. Taxes, March, pp. 144-155.

Pittock, W., & Stryker, C., 1983. Revenue Ruling 77-276 Revisited. SRC Quarterly Reports, Spring, pp. 1-3.

Pratt, S.P., 2009. Business Valuation: Discounts and Premiums 2nd ed., John Wiley & Sons, Inc.

Pratt, S.P., 2008. Valuing a Business, the Analysis and Appraisal of Closely Held Companies 5th ed., McGraw Hill.

Pratt, S., Reilly, R., & Schweihs, R., 2000. Valuing a Business: The Analysis and Appraisal of Closely Held Companies 4th ed., Mc-Graw Hill.

39

Robak, E. & Hall, L. 2001. Marketability Discounts: A New Data Source. Valuation Strategies, July/August .

Reilly, R., & Schweihs R. (eds), 2000. The Handbook of Advanced Business Valuation, McGraw Hill.

Sharpe, W.F., 1964. Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk. Journal of Finance, 19(3), pp.425–442.

Silber, W., 1991. Discounts on Restricted Stock: The Impact of Illiquidity on Stock Prices. Financial Analysts Journal, July-August, pp. 60-64.

Trout, R., 1977. Estimation of the Discount Associated with the Transfer of Restricted Securities. Taxes, June, pp. 381-385.

Wruck, K., 1989. Equity Ownership Concentration and Firm Value: Evidence from Private Equity Financings. Journal of Financial Economics, 23, pp. 3-28.