duxxi v19 final_english

TRANSCRIPT

1st SEMESTER 2014

A NEW BRAZILIANCOMPANY IN THE REAL ESTATE

BROKERAGE BUSINESSOWNED BY THE MANAGEMENT

LISTED IN THE SÃO PAULO

STOCK EXCHANGE BOVESPADXXI3

WHO IS DUXXI?

VISION, MISSION & VALUES

MISSION

Marketing of real estate with a deeper understanding of what

buyers seek and what assets mean to them, through the work

of most qualified professionals and innovative, efficient and

effective processes

BRAND

VALUESEthics, dedication, long-term commitment, human

development, innovation and owned by the management

VISIONTo transform the purchase of real estate into

a rewarding, secure and enjoyable experience for both

the buyer and the seller

TO THE BRAZILIAN REAL

ESTATE BROKERAGE MARKET

BUSINESS MODEL THAT

VALUES EFFICIENCY

TALENT AND TECHNOLOGY

OVER VOLUME

EXPERIENCED TEAMS

NO TIES TO PAST

MODELS AND NO

LIABILITIES OR

LEGACY COSTS

Headquartered in São Paulo, we offer services for

commercial and residential properties for all classes and

we bring true value to our clients, brokers and investors

NEW COMPANY

NEW BEGINNING

NEW APPROACH

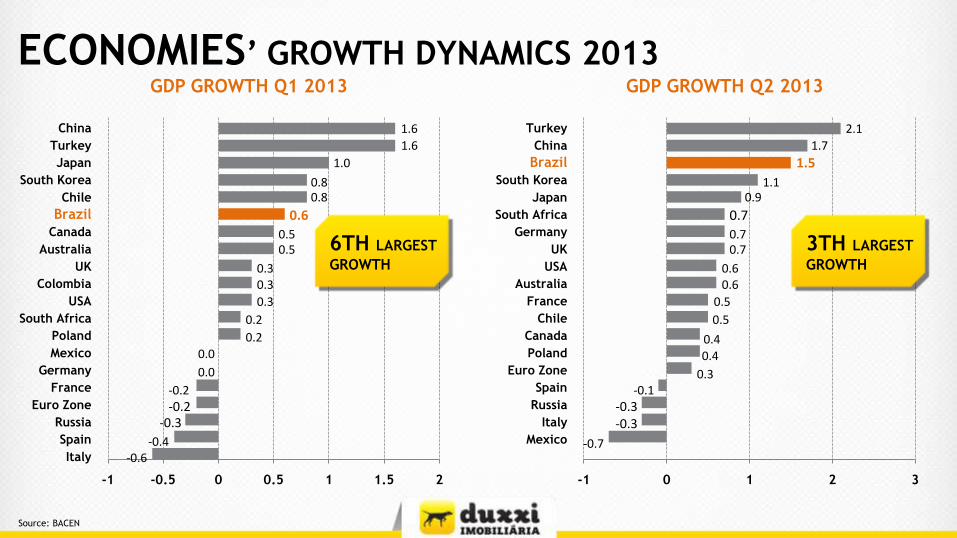

ECONOMIES’ GROWTH DYNAMICS 2013GDP GROWTH Q1 2013

China

Turkey

Japan

South Korea

Chile

Brazil

Canada

Australia

UK

Colombia

USA

South Africa

Poland

Mexico

Germany

France

Euro Zone

Russia

Spain

Italy

-1 -0.5 0 0.5 1 1.5 2

1.6

1.6

1.0

0.80.8

0.6

0.50.5

0.30.3

0.3

0.2

0.2

0.0

0.0

-0.2-0.2

-0.3

-0.4-0.6

GDP GROWTH Q2 2013

Turkey

China

Brazil

South Korea

Japan

South Africa

Germany

UK

USA

Australia

France

Chile

Canada

Poland

Euro Zone

Spain

Russia

Italy

Mexico

-1 0 1 2 3

2.1

1.7

1.5

1.10.9

0.7

0.70.7

0.60.6

0.5

0.5

0.4

0.4

0.3-0.1

-0.3-0.3

-0.7

6TH LARGEST

GROWTH

3TH LARGEST

GROWTH

Source: BACEN

BRAZIL’S SOCIAL & ECONOMIC SCENARIOBRAZIL IS NO LONGER AN ECONOMIC PROMISE. IT’S A REALITY

5%

REGIONAL POPULATION AND GDP

THE SOUTHEAST REGION

(SP, RJ, MG & ES)

CONCENTRATES

MORE THAN HALF OF BRAZIL’S GDPPOP.

GPD

14.3%

16.5%

2013 GPDUS$ 2,2

Trillion

POP.

GPD

8.4%

5.3%

POP.

GPD

27.8%

13.5%

POP.

GPD

7.4%

9.3%POP.

GPD 55.4%

42.1%

5%

AGRICULTURE

SERVICES

69%

26%

INDUSTRIES

SOURCE: IBGE

Brazil presented fast growth from

2000 to 2010, and although this pace

has slowed, the domestic economy

continues to growth despite the

unstable world scenario

Per capita GDP rose significantly

between 2000 and 2010, increasing

real household income

Interest rates and controlled inflation

facilitated access to credit market

growth of 7% - 8% p.a.

The value of real estate assets should

increase at an average annual rate of

4% until 2030 (in real terms)

GDP Growth

1.3%

2.7%1.2%

5.7%

3.2%4.0%

6.1%5.2%

- 0.3%

7.5%

2.7%0,9

4.3%

2000

2010

7,010

11,127

Interest Rates and Inflation Evolution

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

IPCA SELIC

Per Capita GDP: US$

TOTAL INHABITANTSAGE GROUP PYRAMID

Source: IBGE

BRAZIL’S SOCIAL &

ECONOMIC SCENARIO

SOCIAL CLASS POPULATION DISTRIBUTION

Sourc

es:

IPEA /

PN

AD

(IB

GE)

A CB D-E

6,4 10,5 6,4 10,5

65,9

100,396,2

69,6

Recently Brazil has become a nation with 50% of its population belonging to the middle class, with a great

potential for consumption. The richest classes (A and B) have also registered significant growth.

2003

2011

Total: 175 MM

Total: 195 MM

Classes:

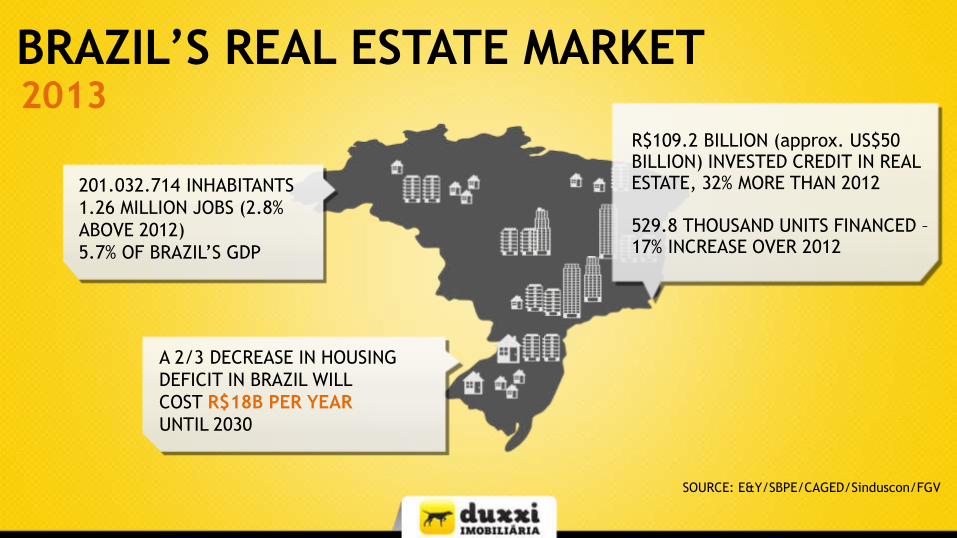

BRAZIL’S REAL ESTATE MARKET2013

A 2/3 DECREASE IN HOUSING

DEFICIT IN BRAZIL WILL

COST R$18B PER YEAR

UNTIL 2030

SOURCE: E&Y/SBPE/CAGED/Sinduscon/FGV

201.032.714 INHABITANTS

1.26 MILLION JOBS (2.8%

ABOVE 2012)

5.7% OF BRAZIL’S GDP

R$109.2 BILLION (approx. US$50 BILLION) INVESTED CREDIT IN REAL ESTATE, 32% MORE THAN 2012

529.8 THOUSAND UNITS FINANCED –17% INCREASE OVER 2012

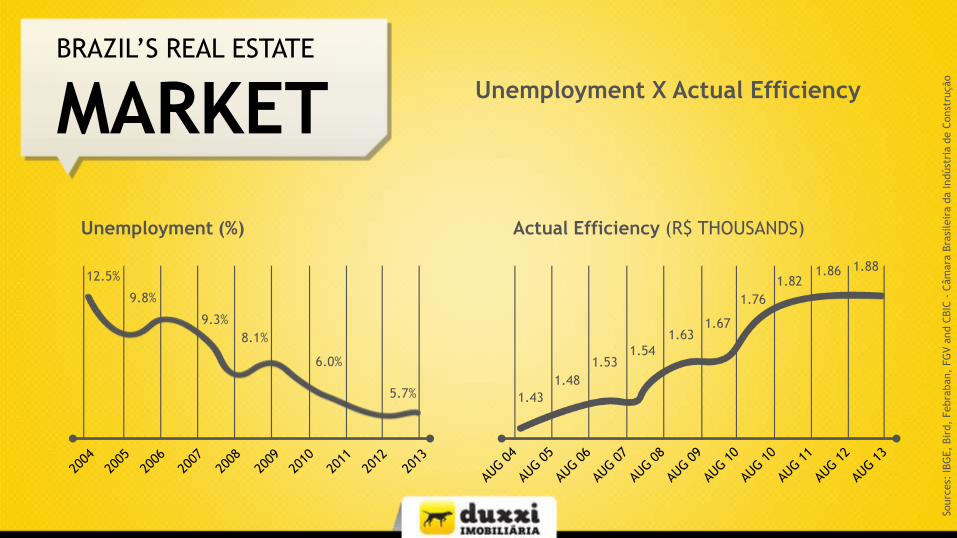

Unemployment (%)

Sourc

es:

IBG

E,

Bir

d,

Febra

ban,

FG

V a

nd C

BIC

-Câm

ara

Bra

sile

ira

da Indúst

ria

de C

onst

rução

BRAZIL’S REAL ESTATE

MARKET

12.5%

9.8%

9.3%

8.1%

6.0%

5.7% 1.43

1.48

1.531.54

1.631.67

1.76

1.821.86 1.88

Actual Efficiency (R$ THOUSANDS)

Unemployment X Actual Efficiency

Demand for New Homes During Period (millions) 36.9Demand for New Homes/Year (millions/year) 1.6Necessary Investments in Homes (R$ millions/year) 194,500

Estimated value of Housing Stock (R$ million) 1,967,000Annual Investments for Replacement (R$ million) 59,010

Total investments to reduce the deficit by 2/3

by 2030 (R$ million) 420,919Annual Investments (R$ million) 18,301

HOUSING DEFICIT

Replacement of Homes

DEMOGRAPHIC CHANGES

Main housing demand factors will generate an approximate

investment requirement of R$ 271 billion per year

What it is (2013)

R$ 222 bn

What it Should Be

R$ 271 bn/year

Real Estate

Sector’s GDP

BRAZIL’S REAL ESTATE

MARKET

258 261260

267267

277282 293

298308

317

338

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013P

What it is (2013)

R$ 222 bn

What it Should Be

R$ 271 bn/year

Real Estate

Sector’s GDP

133127

146 145 146

158169

184215

225 213222

1.7% 1.6% 1.8% 1.4% 1.6%1.7%

2.1%2.8%

4.8%

6.4%

3.7%

7.9%

BRAZIL’S REAL ESTATE

MARKET

BRAZIL’S REAL ESTATE

MARKETLaunches by Region

Brazil – 201279,9 million / 183 thousand units

28.5

11.1

3.93.3 3 2.7 2.4 2.2

2 2 1.9 1.50.711.11.3

10.8

Sourc

es:

IBG

E,

Bir

d,

Febra

ban,

FG

V a

nd C

BIC

-Câm

ara

Bra

sile

ira

da Indúst

ria

de C

onst

rução

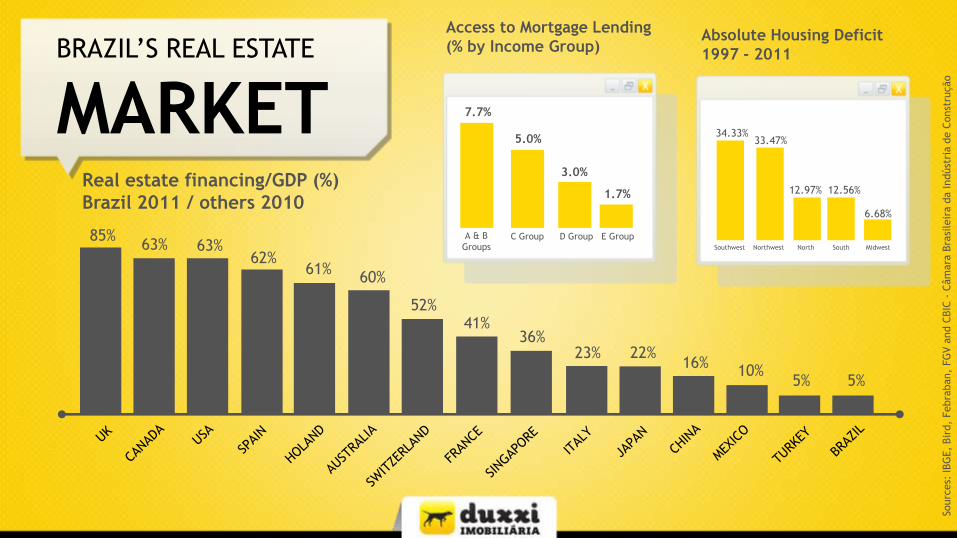

Real estate financing/GDP (%)

Brazil 2011 / others 2010

Access to Mortgage Lending

(% by Income Group)Absolute Housing Deficit

1997 - 2011

85%63% 63%

62%61%

60%

52%41%

36%23% 22%

16%10%

5% 5%

A & B

GroupsC Group D Group E Group

7.7%

5.0%

3.0%

1.7%

Southwest Northwest North South Midwest

34.33%33.47%

12.97% 12.56%

6.68%

Sourc

es:

IBG

E,

Bir

d,

Febra

ban,

FG

V a

nd C

BIC

-Câm

ara

Bra

sile

ira

da Indúst

ria

de C

onst

rução

BRAZIL’S REAL ESTATE

MARKET

BRAZIL’S REAL ESTATE

MARKET

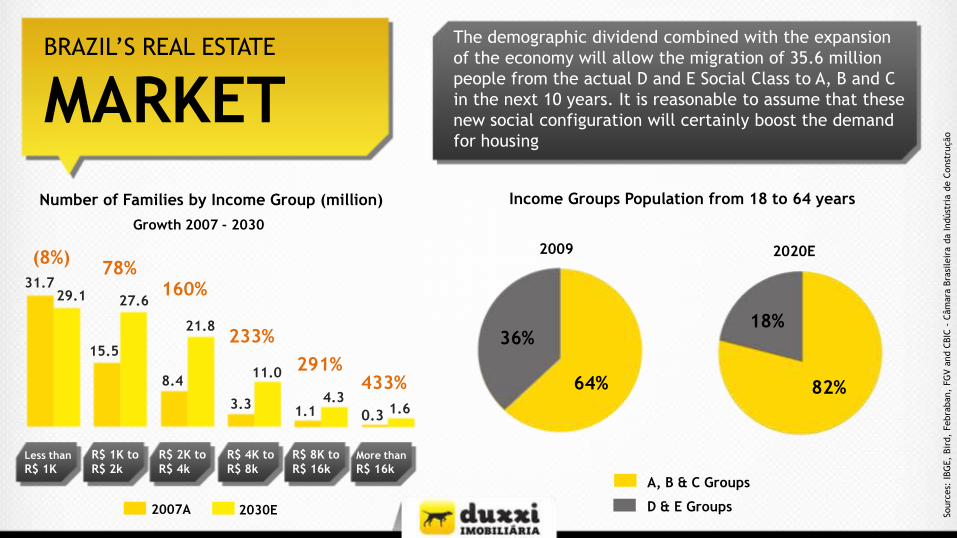

Income Groups Population from 18 to 64 yearsNumber of Families by Income Group (million)

Growth 2007 - 2030

Sourc

es:

IBG

E,

Bir

d,

Febra

ban,

FG

V a

nd C

BIC

-Câm

ara

Bra

sile

ira

da Indúst

ria

de C

onst

rução

2030E2007A

A, B & C Groups

D & E Groups

The demographic dividend combined with the expansion

of the economy will allow the migration of 35.6 million

people from the actual D and E Social Class to A, B and C

in the next 10 years. It is reasonable to assume that these

new social configuration will certainly boost the demand

for housing

15.5

8.4

3.31.1 0.3

29.1 27.6

21.8

11.0

4.31.6

31.7

(8%)78%

160%

233%

291%433%

Less than

R$ 1K

R$ 1K to

R$ 2k

R$ 2K to

R$ 4k

R$ 4K to

R$ 8k

R$ 8K to

R$ 16kMore than

R$ 16k

36%

64%

2009

18%

82%

2020E

THE REAL ESTATE

BROKERAGE MARKET

IS STILL PLAYED THE

OLD FASHIONED WAY

MUCH HAS CHANGED OVER THE

LAST 10 YEARS

Traditional Model Key Challenges

Companies need to explore new and smarter

ways to sell inventories and launches

THE TRADITIONAL MODEL CANNOT

KEEP UP WITH THE NEW DEMAND

M&A Based Models and/or Family

run businesses

Ordinary sales approach

Offline communications

Lack of investment in technology and processes

Low/no business intelligence

Unfocused operations/sectorized organization

Real Estate is still a favorable market:

only the best players will succeed

Real Estate IPO boom drove the industry

to higher inventory levels;

IT'S TIME TO

THE BRAZILIAN MARKETREINVENT

3

SALES FORCE

Market intelligence

department

Highly trained teams / client

management guidance

Well defined incentives;

commissioning + benefits

Enhanced capacity to attract

efficient salesforce

CAPACITY TO ATTRACT AND RETAIN THE

BEST SALESTEAM IN THE INDUSTRY

1PROCESS

Integrated front end; sales

front + ERP+ CRM

Streamlined process;

qualified team + contract

cycle management

Dynamic monitoring

salesteam activities

FOCUS ON CONTINUOUS IMPROVEMENT

2ONLINE TOOLS

Reversed approach versus

traditional sales

Clients will filter options on

the website BEFORE reaching

to sales team

Intelligent tool:

geolocation, local

convenience

(hospitals, malls, schools, con

venience stores,etc)ENABLES DEEP KNOWLEDGE ON

CUSTOMER BEHAVIOR

4 Capacity to offer tailor-made projects and to

address new industry demands

CONSISTENT AND PLANNED SALES STRATEGY

BUSINESS STRATEGY

READY FOR NEW

LOCAL CHALLENGES

OBJECTIVEOUR GOAL IS TO BECOME ONE OF TOP 3 COMPANIES

IN THE BRAZILIAN MARKET IN THE NEXT 10 YEARS

1TECHNOLOGYONLINE SALES TOOLS AND SMART

INTERFACES WITH CLIENTS AND

BROKERS

2PROCESSESINNOVATIVE TOOLS WILL ALLOW A LOW

COST OPERATION WITH EFFICIENCY, QUALITY

TO MAXIMIZE RESULTS

3TALENTSKEY MANAGERS ARE ALSO STOCKHOLDERS AND

BROKERS ARE RECRUITED FROM THE BEST IN THE

MARKET

STRATEGIC SHIFT IN

MARKET PARADIGMSUSER FRIENDLY INNOVATION

WORLD WIDE WEB IS THE

NEW MARKET PLACE FOR

ADVERTING AND MARKETING

REAL ESTATE PROPERTIES

DUXXI WILL LEVERAGE ON A

GROUND-BREAKING ONLINE STRATEGY

AND REINVENT THE BUSINESS MODEL FOR

DOING BUSINESS OVER THE INTERNET

WITH NEW SEARCHING, PRICING

AND COMPARING CAPABILITIES

STRATEGIC SHIFT IN

MARKET PARADIGMSOPERATION EXCELLENCE

DUXXI IS PLANNING, DEVELOPING AND

STRUCTURING THE MOST EFFICIENT

OPERATIONAL PROCESSES, BUILT UPON

THE BEST INDUSTRY PRACTICES

IN A NEW, FAST GROWING MARKET,

IT’S EASY TO BE OVERWHELMED BY THE

VOLUME OF BUSINESS COMING IN

WE AIM HAVING THE LOWEST

COST OPERATION, HIGHEST

EFFICIENCY AND QUALITY

PROCESS TO MAXIMIZE RESULTS

AND COMPETITIVENESS

DUXXI IS A NEW, FULL-SERVICE COMPANY FOUNDED,

OWNED AND MANAGED BY SOME OF THE MOST

SUCCESSFUL PROFESSIONALS IN THE BUSINESS

UNITED BY THE SAME PRINCIPLES AND VALUES

STRATEGIC SHIFT IN

MARKET PARADIGMSFOUNDED AND MANAGED BY OWNERS

A BUSINESS IS FORGED THROUGHINNOVATION, HARD WORK ANDFACE-TO-FACE RELATIONSHIPS

BY ATTRACTING TALENTS AS SHAREHOLDERS, WE

ENSURE LOYALTY AND LONG TERM COMMITMENT

TO OUR PROJECT

FINANCIAL

POSITION & CORPORATE GOVERNANCE

Board of directors (3 to 8 members, at least 1 independent)

Listed in BM&FBovespa

Audited by PWC

Quarterly financial reports

IFRS Accounting Standards

ERP system installed: Senior

Proprietary sales management

Legal Advisor: Levy & Salomão

OPERATIONAL SCHEDULE

Foundation and listing on BOVESPA & CVMBusiness Plan prepared

by E&Y Senior Management Hired

Headquarters and operational offices setup Supera IBG starts BPO

mapping

CRECI brokerage license obtainedBrokers team trained

and certified

Infrastructureand systems implemented

Offices in São Paulo, Campinas and Alphavilleinaugurated

Sales operations Started

Office in Santos Inaugurated

Expectations to inaugurate new offices

SEP 13 NOV 13 FEV 14

FUTUREDEZ 13OCT 13AUG 13PRIOR TOJUL 13