dr andrew wilson domain group senior economist april...

TRANSCRIPT

marketview

Australian housing markets report

Melbourne shifts up a gear

Dr Andrew Wilson – Domain Group senior economist April 2015

Copyright 2015 Dr Andrew Wilson – all rights reserved

marketview

Housing market model – Wilson Curve

marketview

trough

peak

trough

peak

correction recovery

expansion

contraction

• Change points........

• Define phases

Housing market analysis – house price cycle model (Wilson 98)

Prices below last peak

Prices below last trough

Prices above last trough

Prices above last peak

marketview

Recent capital city performance

marketview

Capital city house price cycle - recent history

Correction 2011 Prices fall

Affordability falls from higher rates, higher prices PLUS economy down

Recovery 2012 Prices rise

Affordability improves as rates fall, lower prices AND economy revives

Expansion 2013 Price records emerge and consolidate as affordability peaks

Historically low rates, still solid economy, CONFIDENCE RESTORED

Expansion 2014 Price growth moderates as general economy and low rate impact wane

Sydney breaks clear of the pack - other capitals flat or flattening – CONFIDENCE TESTED

marketview

Current state of the national market

marketview

Current state of the national housing market

Expansion consolidated but now moderating All capital city house prices at or near record levels

Brisbane, Adelaide and Hobart still on the move with moderate growth

Perth prices growth remains modest, but better signs for Canberra - Darwin down

Solid finish to 2014 - all markets on the up – except Darwin

Peak price growth rates however moderated though 2014

Sydney still booming

CONTEXT Mixed-speed economies – AND housing markets

Markets and market segments patchy

Forward indicators and market drivers increasingly mixed and local

Lower rates to impact markets – affordability, confidence offset by local economy drag

marketview

Key price drivers

marketview

The future for house price growth?

....as usual depends on the economy

Key Drivers

Low unemployment and more jobs

Rising wages, incomes and profits

Lower interest rates

Rising stockmarket

Confidence

marketview

Recent prices growth

marketview

Correction phase 2011 - prices fall

-1.4%

-4.2%

-5.0%

-3.5%

-4.0%

-1.7%

-4.4%

-8.0%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Recovery phase 2012 - prices stabilise and rise

4.6%

0.8% 0.7%

-0.4%

5.5%

1.8%

-4.5%

12.6%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Expansion phase 2013 - all markets rising

15.4%

10.0%

5.1%

3.4%

9.6%

2.2%

5.0% 5.6%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Expansion phase 2014 - growth moderates

14.0%

4.1%

5.9% 4.6%

0.6% 0.9% 2.1%

-6.8%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Prices rise over December quarter – except Darwin

3.5%

0.6%

1.5% 0.9% 1.0%

1.9% 2.1%

-5.9%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Most markets now above or close to previous peaks

34.8%

8.4%

3.6% 3.0%

7.9%

3.2%

-2.1% -0.7%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Markets now well above previous price troughs

37.5%

16.6%

13.1%

9.5%

16.4%

4.9%

8.8%

10.9%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Current capital city price cycle

marketview

Capital city house price cycle (Wilson Curve)

correction recovery

expansion

contraction

Sydney

Perth Melbourne

Brisbane

Adelaide

Darwin

Hobart

Canberra

marketview

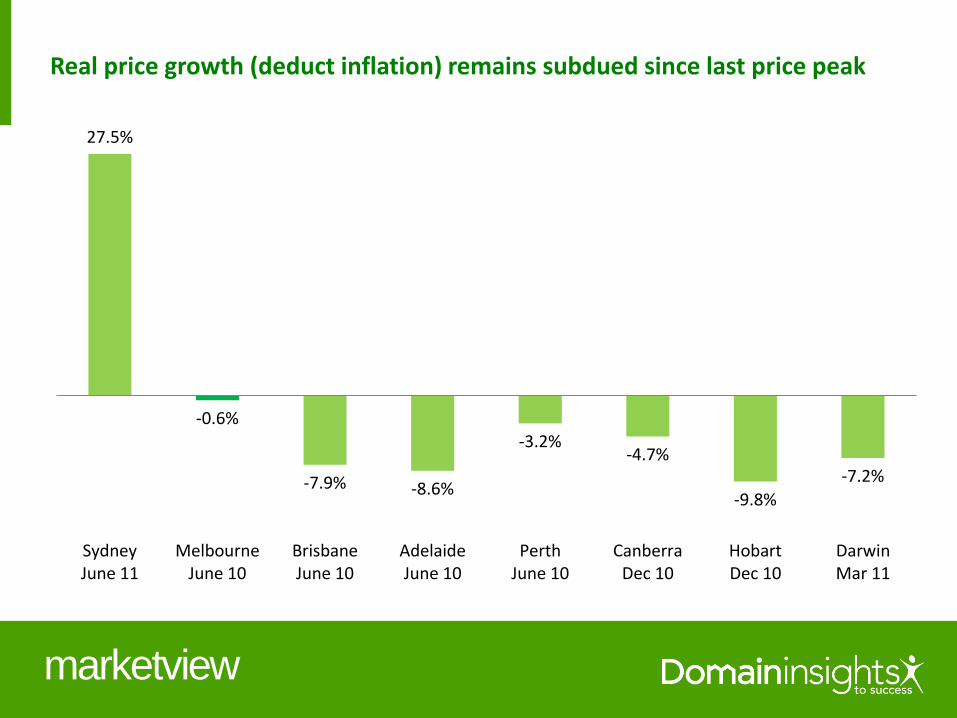

Real price growth (deduct inflation) remains subdued since last price peak

27.5%

-0.6%

-7.9% -8.6%

-3.2% -4.7%

-9.8%

-7.2%

SydneyJune 11

MelbourneJune 10

BrisbaneJune 10

AdelaideJune 10

PerthJune 10

CanberraDec 10

HobartDec 10

DarwinMar 11

marketview

Current capital city growth

marketview

Housing Market Barometer

4%

2%

0.5%

0%

Sydney 3.5%

Melbourne 0.6%

R

I

S

I

N

G

F

A

L

L

I

N

G

December quarter 2014

5%

4% 3%

2%

1%

0.5%

1%

2%

3%

4%

Boom

Strong

Solid

Moderate

Modest

Modest

Moderate

Solid

Strong

Bust

Flat

R

I

S

I

N

G

F

A

L

L

I

N

G

Perth 1.0%

Darwin -5.9%

Hobart 2.1% Canberra 1.9% Brisbane 1.5%

marketview

Sydney the most expensive – Melbourne affordable?

$872,811

$614,479

$489,128 $469,097

$615,280 $588,023

$332,998

$634,316

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

marketview

Melbourne price cycle

marketview

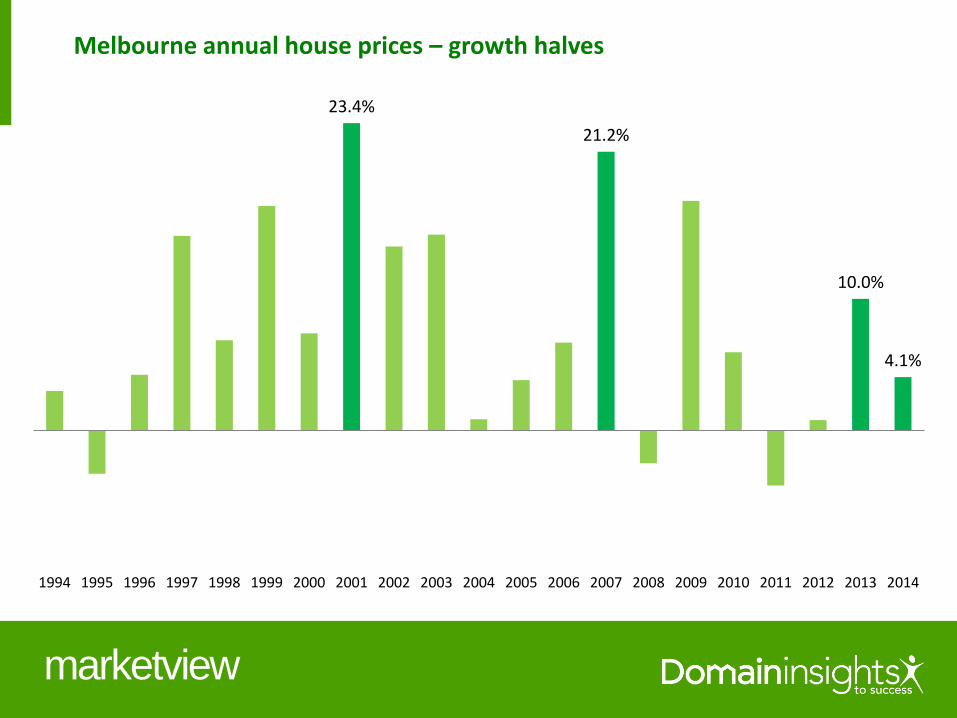

Melbourne annual house prices – growth halves

23.4%

21.2%

10.0%

4.1%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

marketview

Melbourne quarterly price growth – trend waning

6.8%

3.9%

0.6%

2007 2008 2009 2010 2011 2012 2013 2014

marketview

Melbourne house price cycle (Wilson Curve)

correction recovery

expansion

contraction

peak $566,661 June 2010

current $614,479 December 2014

trough $526,993 September 2012

marketview

Melbourne unit market

marketview

Melbourne houses versus units – in sync but units flatter

$614,479

$431,419

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Houses Units

marketview

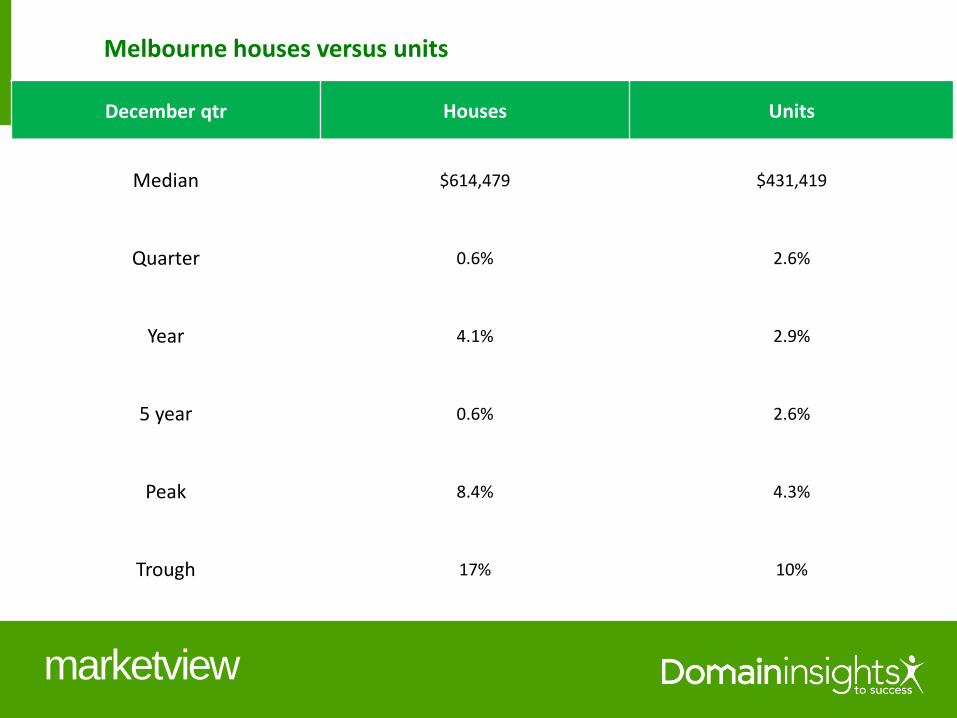

Melbourne houses versus units

December qtr Houses Units

Median $614,479 $431,419

Quarter 0.6% 2.6%

Year 4.1% 2.9%

5 year 0.6% 2.6%

Peak 8.4% 4.3%

Trough 17% 10%

marketview

Melbourne house price cycle (Wilson Curve)

correction recovery

expansion

contraction

Houses Units

marketview

Interest rates and housing markets

marketview

0%

1%

2%

3%

4%

5%

6%

7%

8%

$25 0,000

$35 0,000

$45 0,000

$55 0,000

$65 0,000

$75 0,000

$85 0,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Sydney Melbourne Brisbane Adelaide Perth Interest rate

Interest rates drive the cycle – for ALL capitals in sync

Rates rise 09-10 (FHOGB – mining boom 2)

Rates fall 11-12-13 (economy fades) Rates fall 08

(GFC) Rates rise 06-07 (mining boom 1)

marketview

Melbourne house prices and interest rates – underlying relationship

7.25%

3.00%

4.75%

2.50%

$614,479

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

0%

1%

2%

3%

4%

5%

6%

7%

8%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Interest rate Melbourne median

marketview

Melbourne buyer types

marketview

VIC buyer types market share – higher investors? (ABS Jan loans)

11.2%

47.5%

41.4%

First home buyers Investors Changeover buyers

marketview

VIC buyer type annual growth – investors best (ABS loans year to date Jan 2014 vs. Jan 2013 )

-13.7%

26.0%

0.0%

16.1%

First home buyers Investors Changeover buyers Total

marketview

45.0%

26.1%

13.9%

3.7%

8.4%

NSW VIC QLD SA WA

National investor market share – NSW nearly half (ABS January loans)

marketview

VIC investors and changeover buyers in sync but FHB’s flatter

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

Changeover Investors FHB

marketview

FHB local market share - VIC low but slowly recovering (ABS January loans)

6.5%

11.2% 10.5% 10.5%

18.3%

15.0%

13.3%

11.2% 10.1%

NSW VIC QLD SA WA TAS ACT NT AUS

marketview

Melbourne prices track VIC loans – reliable forward indicator

$0

$5

$10

$15

$20

$25

$300,000

$340,000

$380,000

$420,000

$460,000

$500,000

$540,000

$580,000

$620,000

$660,000

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

ABS loans Melbourne house price

marketview

Stable investor share through cycle reflects longer-term investment focus

32.2%

45.7%

37.1%

46.0%

38.2%

47.1%

41.5%

48.5%

41.4%

$190,000

$240,000

$290,000

$340,000

$390,000

$440,000

$490,000

$540,000

$590,000

$640,000

25%

30%

35%

40%

45%

50%

55%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Investor share Average investor share Melbourne house price

marketview

Melbourne price ranges

marketview

$250,000

$350,000

$450,000

$550,000

$650,000

$750,000

$850,000

$100,000

$300,000

$500,000

$700,000

$900,000

$1,100,000

$1,300,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Prestige Budget Middle

Melbourne price ranges in sync

Prestige top 10% of suburbs

Middle Middle 40% of suburbs

Budget Bottom 50% of suburbs

marketview

Price ranges – prestige still lagging

2.1%

3.3%

2.2%

5.3%

8.0%

5.1%

7.4%

13.5%

7.6%

Budget (up to $560k) Middle ($560k to $1.38m) Prestige ($1.38m+)

December Qtr Year Peak

marketview

Melbourne house price range cycle (Wilson Curve)

correction recovery

expansion

contraction

Prestige Middle

Budget

marketview

Melbourne regions

marketview

200000

300000

400000

500000

600000

700000

800000

900000

1000000

1100000

1200000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Inner East Inner Urban Inner South Outer East

North East North West South East

Melbourne prestige significant separation but outer east rising

Prestige

Middle

Budget

marketview

Melbourne’s east breaks clear

Houses Median Dec qtr 2014 5 year Last peak Listings per sale

Inner East $1,160,000 4.0% 16.9% 30.9% 21.5% 1.6

Inner Urban $1,080,500 9.3% 7.4% 22.8% 15.7% 1.5

Inner South $909,500 1.6% 9.3% 15.1% 10.6% 1.4

Outer East $641,600 5.9% 8.7% 28.3% 20.6% 1.6

North East $560,000 4.7% 6.4% 21.4% 11.4% 2.6

North $481,750 4.7% 3.6% 13.4% 4.7% 3.2

West $460,000 4.5% 3.4% 18.9% 7.0% 3.6

South East $434,000 2.1% 5.9% 19.4% 9.9% 3.8

marketview

Melbourne region house price cycle (Wilson Curve)

correction recovery

expansion

contraction

Outer east

North West

South east

Inner east

Inner urban

North east Inner south

marketview

Melbourne’s east breaks clear for units too

Units Median Dec qtr 2014 5 year Last peak Listings per sale

Inner East $585,000 4.5% 8.1% 13.0% 7.3% 2.8

Inner Urban $536,000 1.1% 1.1% 8.3% 3.1% 2.7

Inner South $522,500 13.6% 1.9% 13.3% 4.0% 2.2

Outer East $493,000 9.6% 8.4% 28.1% 16.4% 2.0

North East $412,000 1.0% 0.0% 6.7% 0.5% 2.4

North $398,000 2.8% -3.2% 4.7% -2.9% 2.7

West $385,000 2.7% 5.5% 14.1% -1.3% 3.2

South East $320,000 2.6% 3.2% 8.5% -0.6% 4.0

marketview

Melbourne region unit price range cycle (Wilson Curve)

correction recovery

expansion

contraction

Outer east

North

West

South east

Inner east

Inner urban

North east

Inner south

marketview

North suburbs

marketview

North top selling suburbs (6 months December 2014)

Houses Sold Median Listings per sale 6 month 1 year 5 year

Craigieburn 375 $386,000 4.6 5.4% 5.8% 14.9%

Glenroy 222 $485,000 1.3 7.8% 11.5% 13.2%

Coburg 217 $701,000 1.2 5.4% 12.2% 32.3%

Brunswick 174 $764,000 1.1 3.9% 4.7% 21.9%

Pascoe Vale 157 $558,000 1.1 5.8% 5.8% 7.2%

Roxburgh Park 132 $405,000 2.7 5.9% 11.0% 12.5%

Fawkner 113 $447,000 1.2 4.4% 9.0% 13.2%

Greenvale 98 $561,250 10.0 3.9% -2.0% 9.6%

Brunswick West 96 $705,500 1.1 -2.0% 9.5% 17.9%

Broadmeadows 95 $350,000 2.0 0.6% 2.9% 1.9%

marketview

North top selling suburbs (6 months December 2014)

Units Sold Median Listings per sale 6 month 1 year 5 year

Brunswick 105 $431,000 1.6 -10.0% -7.5% -2.7%

Brunswick East 61 $505,000 1.8 0.6% 5.2% 5.2%

Brunswick West 61 $398,000 1.7 0.1% 5.0% 12.1%

Coburg 46 $435,000 1.9 8.2% 8.5% 3.6%

Pascoe Vale 42 $426,250 1.3 -4.2% 0.3% 5.1%

Glenroy 39 $336,619 1.8 -10.6% -15.3% -7.5%

Craigieburn 20 $326,000 0.7 3.5% 3.2% 14.4%

Broadmeadows 14 $297,500 3.0 -1.0% 5.3% -0.2%

Oak Park 10 $368,500 1.6 -22.5% NA -4.3%

Tullamarine 10 $305,250 2.4 -6.9% -4.6% -4.6%

marketview

North east top selling suburbs (6 months December 2014)

Houses Sold Median Listings per sale 6 month 1 year 5 year

Reservoir 398 $520,000 1.3 4.4% 7.0% 23.2%

Preston 241 $685,000 1.1 7.0% 8.7% 29.2%

Epping 229 $390,000 5.3 0.0% 5.4% 8.6%

Bundoora 220 $550,000 1.3 3.8% 3.6% 25.7%

Mill Park 207 $430,500 1.3 0.1% 3.7% 13.0%

South Morang 200 $420,000 2.1 2.3% 0.0% 13.2%

Doreen 188 $450,000 6.8 7.1% 8.4% 13.9%

Greensborough 163 $580,000 1.2 7.4% 7.6% 27.2%

Eltham 160 $676,750 1.2 5.7% 9.2% 25.3%

Northcote 154 $940,000 1.1 4.4% 13.6% 34.2%

marketview

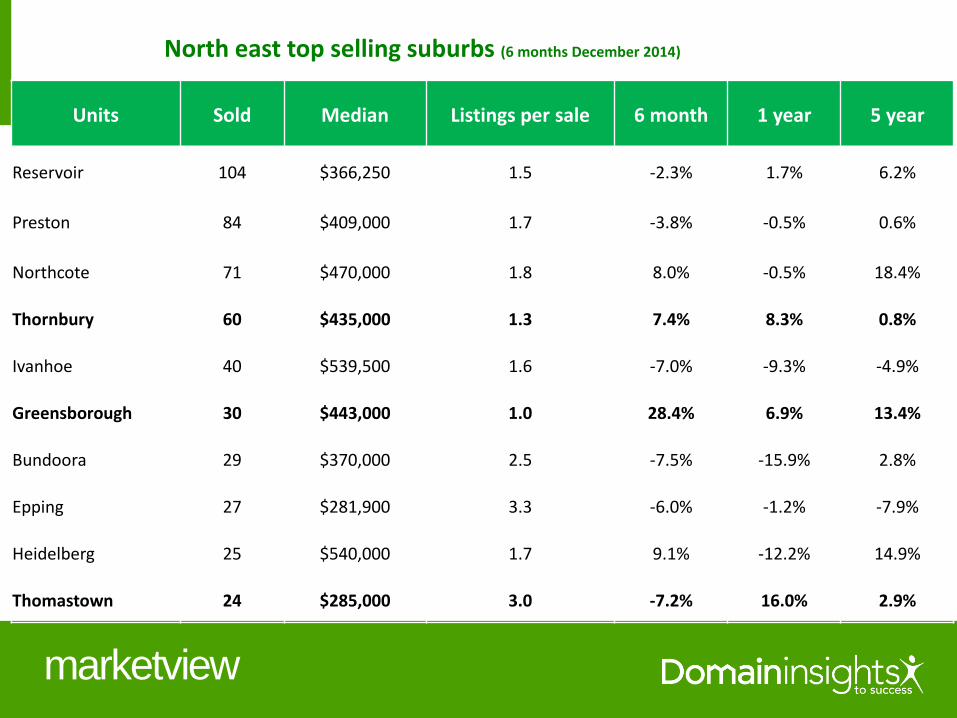

North east top selling suburbs (6 months December 2014)

Units Sold Median Listings per sale 6 month 1 year 5 year

Reservoir 104 $366,250 1.5 -2.3% 1.7% 6.2%

Preston 84 $409,000 1.7 -3.8% -0.5% 0.6%

Northcote 71 $470,000 1.8 8.0% -0.5% 18.4%

Thornbury 60 $435,000 1.3 7.4% 8.3% 0.8%

Ivanhoe 40 $539,500 1.6 -7.0% -9.3% -4.9%

Greensborough 30 $443,000 1.0 28.4% 6.9% 13.4%

Bundoora 29 $370,000 2.5 -7.5% -15.9% 2.8%

Epping 27 $281,900 3.3 -6.0% -1.2% -7.9%

Heidelberg 25 $540,000 1.7 9.1% -12.2% 14.9%

Thomastown 24 $285,000 3.0 -7.2% 16.0% 2.9%

marketview

West top selling suburbs (6 months December 2014)

Houses Sold Median Listings per sale 6 month 1 year 5 year

Point Cook 579 $471,000 3.6 4.7% 4.2% 16.3%

Sunbury 346 $358,975 2.2 -1.7% -0.3% 17.7%

Werribee 324 $320,000 3.1 4.9% 3.1% 19.9%

Hoppers Crossing 316 $340,000 1.9 -0.6% 2.4% 15.3%

Tarneit 291 $384,000 6.0 1.1% 2.4% 18.4%

Caroline Springs 251 $455,000 1.8 2.2% 2.9% 20.7%

St Albans 239 $370,000 2.0 1.4% 5.7% 10.4%

Wyndham Vale 193 $330,000 4.4 2.7% 6.0% 16.2%

Truganina 170 $369,900 11.6 4.5% 2.8% 17.5%

Yarraville 158 $739,250 1.1 6.9% 5.6% 32.2%

marketview

West top selling suburbs (6 months December 2014)

Units Sold Median Listings per sale 6 month 1 year 5 year

Footscray 93 $431,000 1.8 6.4% 9.1% 14.9%

Essendon 71 $400,000 1.9 -11.1% -10.8% -5.4%

Maribyrnong 62 $410,000 2.1 -6.8% -16.0% -6.6%

Kensington 58 $426,250 1.1 0.3% 1.5% 4.1%

Ascot Vale 48 $519,000 1.2 19.9% 17.4% 23.7%

West Footscray 41 $365,000 1.5 18.9% -2.7% 10.8%

St Albans 40 $280,000 3.0 -1.8% 3.7% 4.5%

Moonee Ponds 39 $405,000 2.3 -12.9% 0.4% 3.2%

Essendon North 34 $485,000 0.9 2.1% 15.5% 18.3%

Altona 32 $485,000 1.6 5.4% 9.0% 24.4%

marketview

Melbourne rental market

marketview

$200

$250

$300

$350

$400

$275,000

$325,000

$375,000

$425,000

$475,000

$525,000

$575,000

$625,000

$675,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

House price House rent

Melbourne house rents versus house prices

marketview

Melbourne unit rents versus unit prices

$100

$150

$200

$250

$300

$350

$220,000

$270,000

$320,000

$370,000

$420,000

$470,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Unit price Unit rent

marketview

Melbourne house rents versus unit rents

$200

$220

$240

$260

$280

$300

$320

$340

$360

$380

$400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Unit rent House rent

marketview

Melbourne house yields versus unit yields

4.08%

4.60%

3.0%

3.2%

3.4%

3.6%

3.8%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

House Unit

marketview

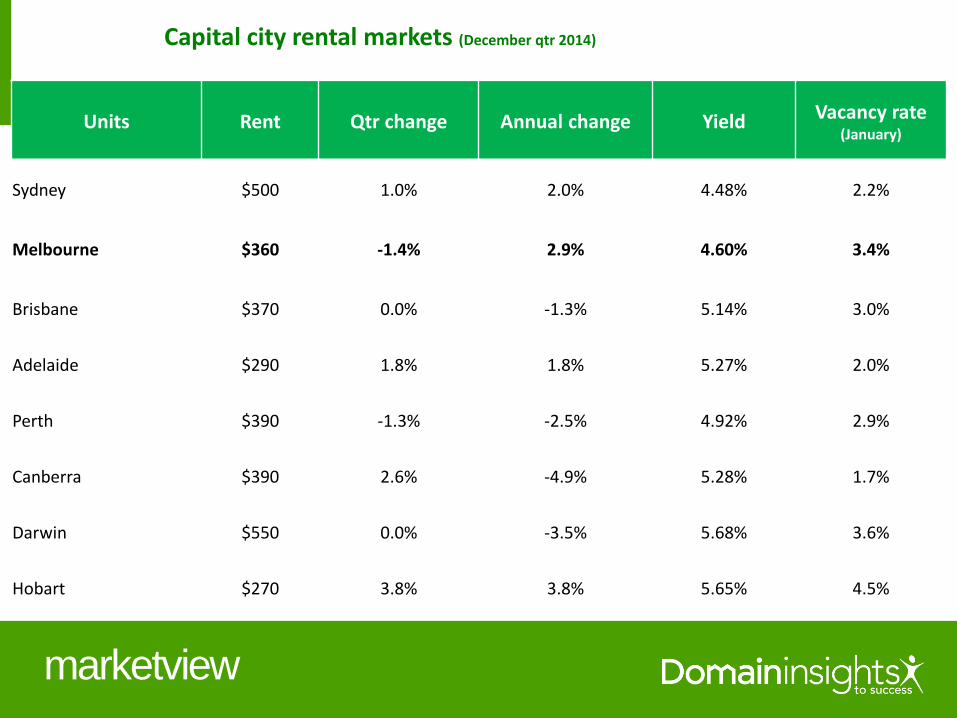

Capital city rental markets (December qtr 2014)

Houses Rent Qtr change Annual change Yield Vacancy rate (January)

Sydney $520 2.0% 4.0% 4.00% 1.8%

Melbourne $380 0.0% 0.0% 4.08% 2.0%

Brisbane $400 0.0% 0.0% 5.02% 2.1%

Adelaide $350 1.4% 0.0% 4.81% 1.3%

Perth $450 0.0% -6.3% 4.57% 2.4%

Canberra $450 0.0% -2.2% 4.55% 1.3%

Darwin $660 0.0% -5.7% 5.21% 1.3%

Hobart $320 3.2% 3.2% 5.44% 1.0%

marketview

Capital city rental markets (December qtr 2014)

Units Rent Qtr change Annual change Yield Vacancy rate (January)

Sydney $500 1.0% 2.0% 4.48% 2.2%

Melbourne $360 -1.4% 2.9% 4.60% 3.4%

Brisbane $370 0.0% -1.3% 5.14% 3.0%

Adelaide $290 1.8% 1.8% 5.27% 2.0%

Perth $390 -1.3% -2.5% 4.92% 2.9%

Canberra $390 2.6% -4.9% 5.28% 1.7%

Darwin $550 0.0% -3.5% 5.68% 3.6%

Hobart $270 3.8% 3.8% 5.65% 4.5%

marketview

Melbourne regions rental market

marketview

Region rental markets ( 3 months December 2014)

Houses Vacancies Rent 6 month change Annual change Yield

Inner Urban 2155 $600 3.4% 0.8% 2.9%

Inner East 1879 $515 3.0% -1.0% 2.3%

Inner South 2258 $500 1.0% 1.0% 2.9%

Outer East 2926 $400 0.0% 2.6% 3.2%

North East 3087 $360 0.0% 2.9% 3.3%

North 1990 $360 0.0% 2.3% 3.9%

South East 3956 $350 0.0% 2.9% 4.2%

West 6707 $350 0.0% 2.9% 4.0%

marketview

Region rental markets ( 3 months December 2014)

Units Vacancies Rent 6 month change Annual change Yield

Inner Urban 10127 $420 -2.3% 3.7% 4.1%

Inner East 2506 $360 -4.0% 1.4% 3.2%

Inner South 3157 $350 -2.8% 0.0% 3.5%

Outer East 1117 $350 1.4% 2.9% 3.7%

North 1203 $330 0.0% 0.0% 4.3%

North East 1829 $320 0.0% 3.2% 4.0%

West 2871 $310 0.0% 3.3% 4.2%

South East 1554 $290 0.0% 3.6% 4.7%

marketview

North rental market

marketview

North top rental suburbs ( 6 months December 2014)

Houses Vacancies Rent 6 month change Annual change Yield

Craigieburn 695 $340 0.0% 3.0% 4.6%

Brunswick 323 $520 4.0% 8.3% 3.5%

Glenroy 282 $350 1.4% 2.9% 3.8%

Coburg 264 $450 0.0% 2.3% 3.3%

Pascoe Vale 215 $370 -2.6% 2.8% 3.3%

Brunswick West 174 $490 2.6% 2.1% 3.6%

Wallan 161 $320 0.0% 3.2% 4.8%

Roxburgh Park 157 $360 2.9% 2.9% 4.7%

Brunswick East 154 $515 -1.0% 6.2% 3.9%

Broadmeadows 153 $320 3.2% 3.2% 4.8%

marketview

North top rental suburbs ( 6 months December 2014)

Units Vacancies Rent 6 month change Annual change Yield

Brunswick 507 $370 1.4% 0.0% 4.5%

Brunswick West 376 $310 0.0% 3.3% 4.1%

Brunswick East 257 $365 -2.0% 1.4% 3.8%

Coburg 214 $340 -0.7% 0.0% 4.0%

Glenroy 151 $300 -3.2% 0.0% 4.6%

Pascoe Vale 143 $330 -1.5% 0.0% 4.1%

Tullamarine 104 $300 1.7% 3.4% 5.1%

Oak Park 51 $330 3.1% 3.1% 4.3%

Broadmeadows 50 $310 3.3% 3.3% 5.4%

Fawkner 36 $313 4.2% 4.0%

marketview

North east top rental suburbs ( 6 months December 2014)

Houses Vacancies Rent 6 month change Annual change Yield

Reservoir 616 $340 3.0% 3.0% 3.4%

Epping 401 $340 3.0% 3.0% 4.5%

Preston 383 $400 0.0% 0.0% 3.0%

Bundoora 306 $355 1.4% 1.4% 3.4%

Northcote 303 $550 0.0% 10.0% 3.1%

Mill Park 291 $340 0.0% 0.0% 4.1%

Doreen 253 $350 0.0% 0.0% 4.0%

South Morang 252 $350 -1.4% 0.0% 4.3%

Mernda 241 $340 0.0% 3.0% 4.6%

Thornbury 232 $493 2.6% 7.0% 3.1%

marketview

North east top rental suburbs ( 6 months December 2014)

Units Vacancies Rent 6 month change Annual change Yield

Reservoir 462 $310 3.3% 3.3% 4.4%

Preston 346 $340 -2.9% -2.9% 4.3%

Thornbury 314 $300 -6.3% 0.0% 3.8%

Northcote 288 $360 2.9% 2.9% 4.0%

Bundoora 170 $340 3.0% 6.3% 4.8%

Ivanhoe 139 $340 -3.5% -2.9% 3.2%

Fairfield 135 $295 -4.8% -1.3% 3.3%

Heidelberg 129 $350 0.0% 2.9% 3.4%

MacLeod 124 $200 -4.8% -4.8% 2.0%

Epping 120 $290 -1.7% 0.0% 5.3%

marketview

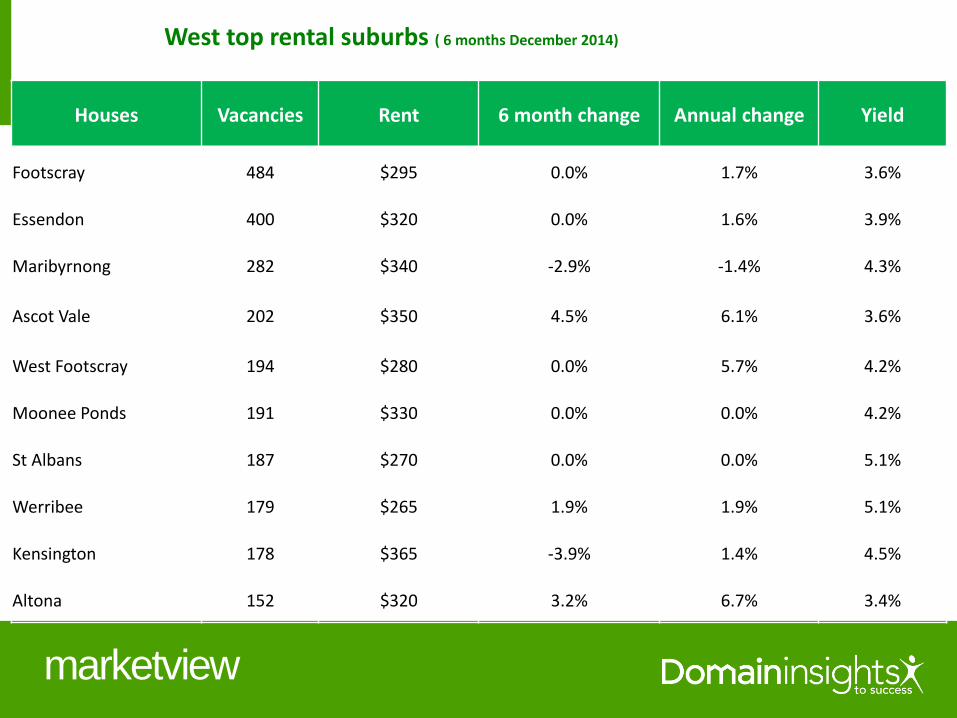

West top rental suburbs ( 6 months December 2014)

Houses Vacancies Rent 6 month change Annual change Yield

Footscray 484 $295 0.0% 1.7% 3.6%

Essendon 400 $320 0.0% 1.6% 3.9%

Maribyrnong 282 $340 -2.9% -1.4% 4.3%

Ascot Vale 202 $350 4.5% 6.1% 3.6%

West Footscray 194 $280 0.0% 5.7% 4.2%

Moonee Ponds 191 $330 0.0% 0.0% 4.2%

St Albans 187 $270 0.0% 0.0% 5.1%

Werribee 179 $265 1.9% 1.9% 5.1%

Kensington 178 $365 -3.9% 1.4% 4.5%

Altona 152 $320 3.2% 6.7% 3.4%

marketview

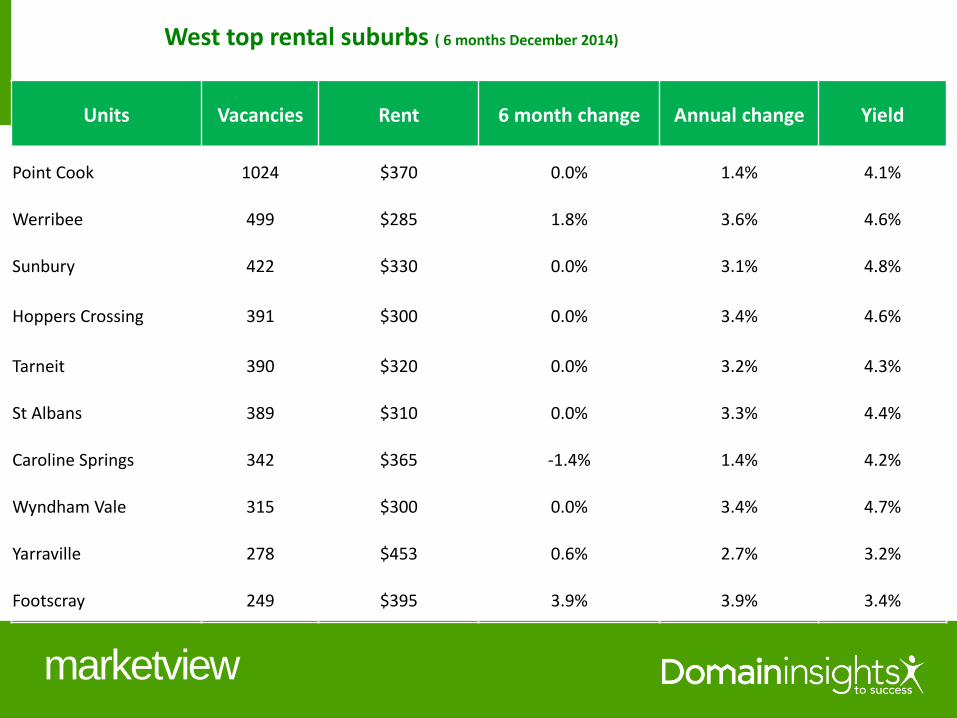

West top rental suburbs ( 6 months December 2014)

Units Vacancies Rent 6 month change Annual change Yield

Point Cook 1024 $370 0.0% 1.4% 4.1%

Werribee 499 $285 1.8% 3.6% 4.6%

Sunbury 422 $330 0.0% 3.1% 4.8%

Hoppers Crossing 391 $300 0.0% 3.4% 4.6%

Tarneit 390 $320 0.0% 3.2% 4.3%

St Albans 389 $310 0.0% 3.3% 4.4%

Caroline Springs 342 $365 -1.4% 1.4% 4.2%

Wyndham Vale 315 $300 0.0% 3.4% 4.7%

Yarraville 278 $453 0.6% 2.7% 3.2%

Footscray 249 $395 3.9% 3.9% 3.4%

marketview

Melbourne key market drivers

marketview

Melbourne ABS annual home approvals

18,633 18,562

22,284 22,838 21,654

26,451

41,471 40,216

48,735

2012 2013 2014

Houses Units Total

marketview

Melbourne ABS dwelling approvals year to date – many more units (February)

3388 3439

6827

3479

5173

8652

Houses Units Total

2014 2015

marketview

Melbourne ABS unit approvals - oversupplied again?

26,451

0

5,000

10,000

15,000

20,000

25,000

30,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

marketview

Victorian overseas migration drives local housing markets (ABS financial year)

48,165

55,854

62,532

68,141

2011 2012 2013 2014

marketview

Melbourne population growth drives prices (ABS financial year)

2.5%

2.2%

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Population growth House price

marketview

Melbourne economic performance

marketview

Melbourne job surge – 94,480 new jobs over year (ABS February)

2,098,809

2,156,136 2,150,997

2,212,810

2,190,006

2,284,486

1,950,000

2,000,000

2,050,000

2,100,000

2,150,000

2,200,000

2,250,000

2,300,000

2010 2011 2012 2013 2014 2015

marketview

Melbourne jobless falling (ABS February)

5.8%

5.4%

6.0% 6.2%

7.3%

6.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2010 2011 2012 2013 2014 2015

marketview

Melbourne in work rising - reflects strong migration effect waning (ABS February)

66.8%

67.2%

66.2%

66.9%

65.7%

66.6%

64%

64%

65%

65%

66%

66%

67%

67%

68%

2010 2011 2012 2013 2014 2015

marketview

National economic performance

marketview

National turnaround?

February ABS jobless rate 2014 2015 Trend

Sydney 5.8% 5.8%

Melbourne 7.3% 6.6%

Brisbane 6.7% 6.5%

Adelaide 7.5% 7.1%

Perth 6.3% 6.4%

Hobart 8.0% 6.8%

Canberra 3.6% 5.4%

Darwin 3.3% 3.1%

marketview

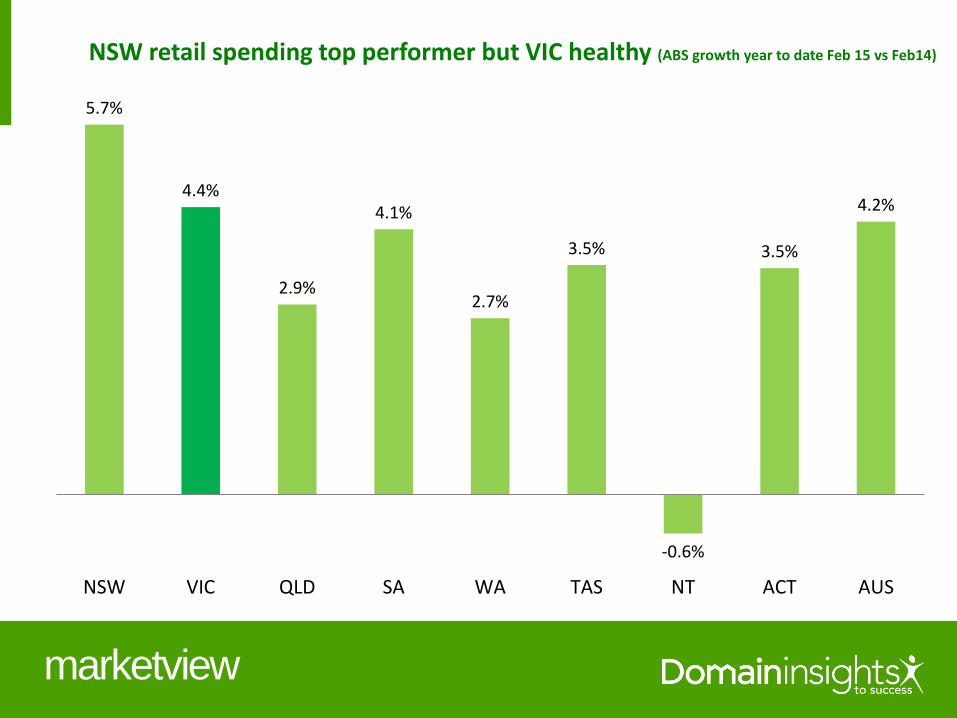

NSW retail spending top performer but VIC healthy (ABS growth year to date Feb 15 vs Feb14)

5.7%

4.4%

2.9%

4.1%

2.7%

3.5%

-0.6%

3.5%

4.2%

NSW VIC QLD SA WA TAS NT ACT AUS

marketview

VIC economy on the rise – state final demand (ABS rolling annual quarters Dec 2014)

2.8%

-1%

0%

1%

2%

3%

4%

5%

6%

2009 2010 2011 2012 2013 2014

marketview

VIC economy a top performer – state final demand (ABS Dec qtr 2014 vs Dec qtr 2013)

4.0%

2.7%

-3.5%

1.9%

-1.7%

1.6%

6.2%

1.5%

NSW VIC QLD SA WA TAS NT ACT

marketview

Economic outlook

marketview

Economic outlook 2015

Mixed national economic outlook Pessimism outweighing optimism - future cloudy - but a glimmer of hope? Reserve Bank still wary on near-term direction of economy but rates on hold

International economy wavering? Growth in China remains relatively strong but signs of fading international economy US economy continues to slowly revive but real growth (wages) still too low AUD to fall as USD rises with higher US rates

Mixed results for local economies VIC in transition as manufacturing base wanes but building and services holding up NSW solid growth trend – top performer as mixed economy spreads the load QLD up as dollar falls - strong exporter, tourism, population rising – confidence up slowly SA showing early signs of revival but will be a gradual and lengthy process WA still OK with population surge but mining building boom over and lower iron ore prices TAS showing early signs of revival but remains national underperformer NT boom resources economy creaking under population surge but set to resume growth

marketview

Economic drivers - rates, dollar, wages, profits all low and falling - but shares up

Interest rates remaining at 60 year low

Downward bias until jobless falls below 6% - less stimulus capacity from record low rates – deflation risk

Mortgage costs falling as banks compete for market share – but still at 2009 rates

Rate cuts likely to continue through 2015 - economy needs more stimulus – watch the currency

Stockmarket rising with lower dollar but hostage to global forces

Investors shift to shares and increased international investment with lower dollar

Solid growth upside as still 10% below 2007 peak, unlike other exchanges at or near highs

Lower dollar and looming deflation

Imports more expensive, living standards fall, spending and investment decline

Wages and profits subdued in low inflation economy – places lid on house price growth despite rate cuts

Government spending constrained by high deficit - horror budgets?

Retail sales, building, profits, sentiment and exports mixed - but not good enough yet

marketview

Melbourne housing market outlook

marketview

• Market to revive from lower rates, rising confidence and aspirational buyers in the east

• Changeover buyers in mid to higher price ranges resilient as value opportunities remain

• Lower rates and rising confidence to generate market momentum despite economic drag

• Investors to remain active - yields low but stable as fundamentals hold - better than deposit rates

• Prestige rising with shares and FHB’s to trickle back into market from low base

• CBD unit market oversupplied but inner suburban units to remain in demand

• Budget outer suburban markets however to continue to underperform due to concerns over job security

• Underperforming local economy showing some early signs of improvement

• Jobless falling, jobs growth resuming and participation rate higher despite surge in population

• Increased dwelling construction to continue – more unit approvals - creating jobs despite oversupply

• Rising population enhanced by improved economy

• Wealth effect from rising house prices to generate downstream economic activity

• Market still affordable with real prices growth flat over past 5 years

• Melbourne to record similar house price growth to last year up by a solid 5%

• Eastern suburbs remain strong from aspirational buyers with outer north and west modest

although improving with economy

Melbourne housing market outlook 2015 - a moderate revival from usual suspects

marketview

National housing market outlook

marketview

Housing Market Barometer

12%

2%

1%

0%

0%

Sydney 9%

Perth, Darwin, Canberra 2%

Brisbane 7%

R I S I NG

F A L L I N G

2015 forecasts

5%

4% 8%

6%

4%

2%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

Melbourne, Adelaide, Hobart 5%

marketview

Melbourne local housing market outlook

marketview

Housing Market Barometer

12%

2%

1%

0%

0%

Middle 7%

Prestige 5%

R I S I NG

F A L L I N G

2015 forecasts

5%

4% 8%

6%

4%

2%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

Budget 3%

marketview

Housing Market Barometer

12%

2%

1%

0%

0%

inner east, outer east 10%

north east, inner south, inner urban 5%

R I S I NG

F A L L I N G

2015 forecasts

5%

4% 8%

6%

4%

2%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

west, south east, north 3%

marketview

Melbourne auctions reliable and timely market indicator

marketview

Melbourne clearance rate reflects prices growth – reliable weekly indicator

$325,000

$375,000

$425,000

$475,000

$525,000

$575,000

$625,000

$675,000

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Median house price Auction clearance rate

marketview

Melbourne auction volumes also reflect prices growth – reliable weekly indicator

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

0

2000

4000

6000

8000

10000

12000

14000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Auctions Median house price 4 per. Mov. Avg. (Auctions)

marketview

North clearance rate reflects prices growth – reliable weekly indicator

$275,000

$325,000

$375,000

$425,000

$475,000

$525,000

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Median house price Clearance rate

marketview

North east clearance rate reflects prices growth – reliable weekly indicator

$275,000

$325,000

$375,000

$425,000

$475,000

$525,000

$575,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Median house price Clearance rate

marketview

West clearance rate reflects prices growth – reliable weekly indicator

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Median house price Clearance rate

marketview

March clearance rates rising

86.6% 82.5% 82.1%

73.7% 72.3% 71.5% 68.8%

61.7%

Outer East Inner East Inner South North East North Inner Urban West South East

marketview

Melbourne clearance rates rising

78.8%

68.9%

72.2%

Current 4 weekend average Previous 4 weekend average(Dec14)

Last year 4 weekend average

marketview

Melbourne auction volumes down - earlier Easter this year

7,400

8,778

2015 2014

marketview

North March clearance rates rising

61.7%

71.9%

2014 2015

marketview

North east March clearance rates – up sharply

66.6%

73.3%

2014 2015

marketview

West March clearance rates up

63.9%

68.5%

2014 2015

marketview

Auction clearance rates April 11 – strongest market since 2010

90.2% 86.0%

81.3% 81.2% 78.6% 78.3%

69.3%

60.9%

Outer East Inner East Inner Urban North East North Inner South West South East

marketview

The rising tide

marketview

House price history lesson

• Australian housing markets are historically trend-linked

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Sydney Melbourne Brisbane Adelaide Perth

marketview

Rising dwelling type tide

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Houses Units

marketview

Rising buyer type tide

2007 2008 2009 2010 2011 2012 2013 2014

Changeover Investors FHB

marketview

$25 0,000

$35 0,000

$45 0,000

$55 0,000

$65 0,000

$75 0,000

$85 0,000

$10 0,000

$30 0,000

$50 0,000

$70 0,000

$90 0,000

$1, 100,00 0

$1, 300,00 0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Prestige Budget Middle

Rising price ranges tide

marketview

Rising regional tide

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Inner East Inner Urban Inner South Outer East

North East North West South East

marketview

A rising tide lifts all boats - in time

Economies

Employment

Incomes

Population growth

Prosperity

Confidence

House prices

Monolithic Australian economy and housing market

marketview

Australian residential property’s best friend (the Wilson curve)

Secure reliable long-term tax-enhanced capital growth

marketview

Melbourne affordability debate

marketview

Falling repayments enable prices growth (Reserve Bank indicator rate, 30 year variable, ABS)

$535

$412

$662

$407

$486 $477

$614,479

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

$300.00

$350.00

$400.00

$450.00

$500.00

$550.00

$600.00

$650.00

$700.00

2007 2008 2009 2010 2011 2012 2013 2014

VIC average repayment Overall average repayment Melbourne median

marketview

Incomes rise, repayments fall, affordability improves and prices rise (ABS)

38.5%

29.3%

43.2%

25.0%

28.9%

32.5%

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

20%

25%

30%

35%

40%

45%

2007 2008 2009 2010 2011 2012 2013 2014

VIC loan % of Melbourne income Average VIC loan % of Melbourne income

Melbourne median

marketview

38.5%

29.3%

43.2%

25.0%

28.9%

32.5%

320

398

333

365

351

300

320

340

360

380

400

420

20%

25%

30%

35%

40%

45%

2007 2008 2009 2010 2011 2012 2013 2014

VIC loan % of Melbourne income

Average VIC loan % of Melbourne income

Weekly Melbourne income as a factor of Melbourne price

Average income as a factor of price

Incomes, prices, loans – which is the effective affordability benchmark? (ABS)

Income factor above average

Loan proportion still below average

marketview

Melbourne home owners higher interest rate vulnerability – just 2.7% (ABS)

28.2%

33.8%

35.4%

2.7%

Non-owners Outright owners

Repayments 30% or less than income Repayments 30% or more than income

marketview

Where do you go to find out what's really happening in your housing

market?

Buy? Sell? Hold? or Rent?

Expert real-time insights into the current state and future prospects of

your housing market

Coming soon Domain Marketview on the Domain website

Australian property market analysis - Domain Marketview

marketview

If you require any further information regarding Australian property

market analysis I may be contacted by email at

[email protected] or phone 0427 410 240

For all the real-time housing market insights follow me on twitter at

@DocAndrewWilson

Australian property market analysis

Thank you