Download - Africa Energy Outlook

© OECD/IEA 2014

London, 13 October 2014

© OECD/IEA 2014

The sub-Saharan context

GDP is rising, but almost half of a fast-growing population lives in extreme poverty: energy is vital to the prospects for development

Region accounts for 13% of global population, but only 4% of its energy demand: half of this is biomass

Poor electricity infrastructure is a key impediment to growth

Large resource base, exploited only in part in the case of oil, gas & coal, largely untouched in renewables

Domestic energy reforms gaining speed, but two-thirds of energy investment since 2000 went to develop resources for export

© OECD/IEA 2014

Rich in resources

In the last 5 years, almost 30% of global oil & discoveries were in sub-Saharan Africa;

Hydro

WindOil

Oil

Oil

OilGas

Gas

Oil

Coal

Gas

Fossil fuels

Solar

the region has vast untapped renewables potential, notably hydro & solar

© OECD/IEA 2014

In sub-Saharan Africa, 620 million people – two-thirds of the population – live without electricity. Only a handful of countries have electrification rates above 50%.

Less than 50%

More than 50%

Share of population withaccess to electricity:

Rich in resources, but poor in supply

© OECD/IEA 2014

Biomass remains at the centreof the sub-Saharan energy mix

Total primary energy demand in sub-Saharan Africa

Reliance on fuelwood and charcoal remains high, even as incomes grow; 650 million people still cook with biomass in an inefficient & hazardous way in 2040

300 400 500Mtoe

100 200

Nuclear

Gas

Modern renewables

Coal

Oil

Biomass

2012

Additional demand in 2040

Mtoe

© OECD/IEA 2014

Power to shape the future

Installed power generation capacity by fuel in sub-Saharan Africa

Renewables account for almost half the growth in overall power supply & for two-thirds of the mini-grid and off-grid systems installed in rural areas

Coal45%

Gas, 14%

Oil, 17%

Nuclear, 2%

Hydro22%

Other renewables0%

2012 capacity: 90 GW

2040 capacity: 380 GW

Coal22%

Gas25%

Oil7%

Hydro24%

Solar12%

Nuclear2%

Bioenergy, windgeothermal

8%

© OECD/IEA 2014

Different paths to power across the continent

The power mix by subregion reflects local resource endowments; well-functioning regional power pools help to unlock new projects, lower costs & improve reliability

100

200

300

400

500

600

2000 2020 2040

West

TWh

30

60

90

120

150

2000 2020 2040

Central

TWh

50

100

150

200

250

300

2000 2020 2040

East

TWh

CoalOilGasNuclear

HydroSolar PV

Otherrenewables

200

400

600

800

1 000

2000 2020 2040

Southern

TWh

© OECD/IEA 2014

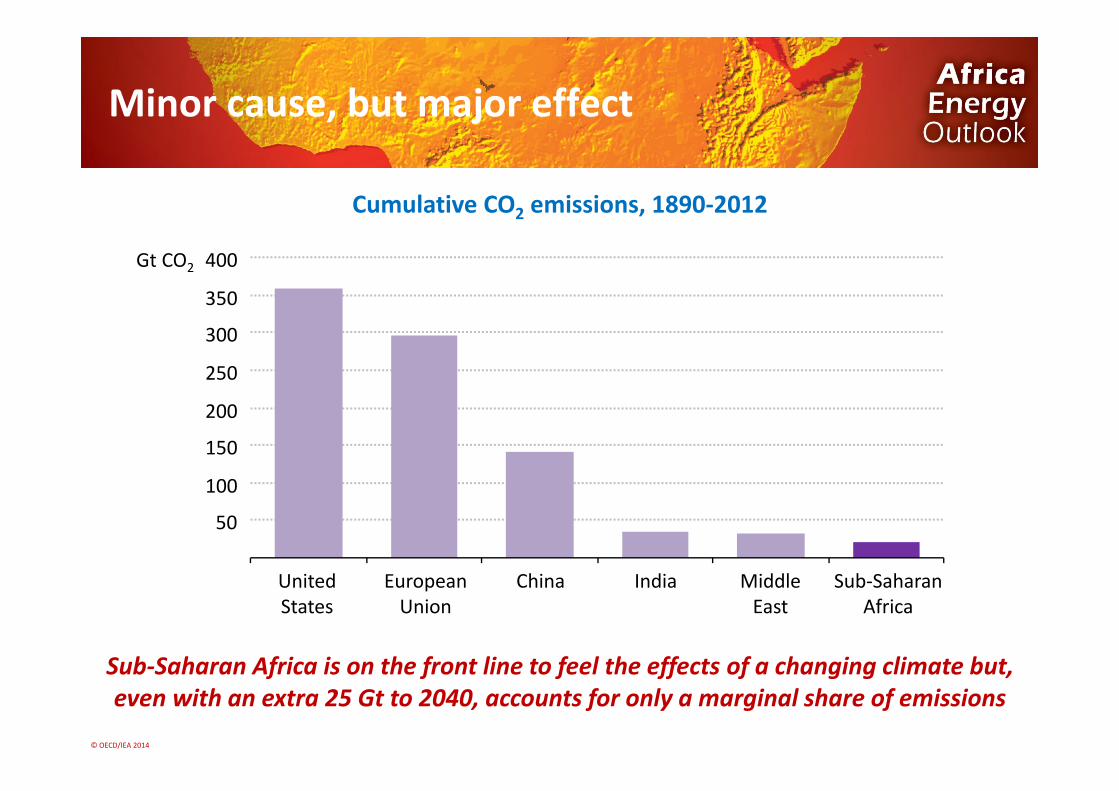

Minor cause, but major effect

Cumulative CO2 emissions, 1890-2012

Sub-Saharan Africa is on the front line to feel the effects of a changing climate but, even with an extra 25 Gt to 2040, accounts for only a marginal share of emissions

50

100

150

200

250

300

350

400

UnitedStates

EuropeanUnion

China India MiddleEast

Sub-SaharanAfrica

Gt CO2

© OECD/IEA 2014

A changing balance to oil production

Oil production in sub-Saharan Africa

The region remains a major global supplier, although regulatory uncertainty, unrest & oil theft in Nigeria make Angola the main producer of crude oil until the 2020s

Other

Angola

Nigeria

Production:

1

2

3

4

5

6

7

2000 2013 2020 2030 2040

mb/d

© OECD/IEA 2014

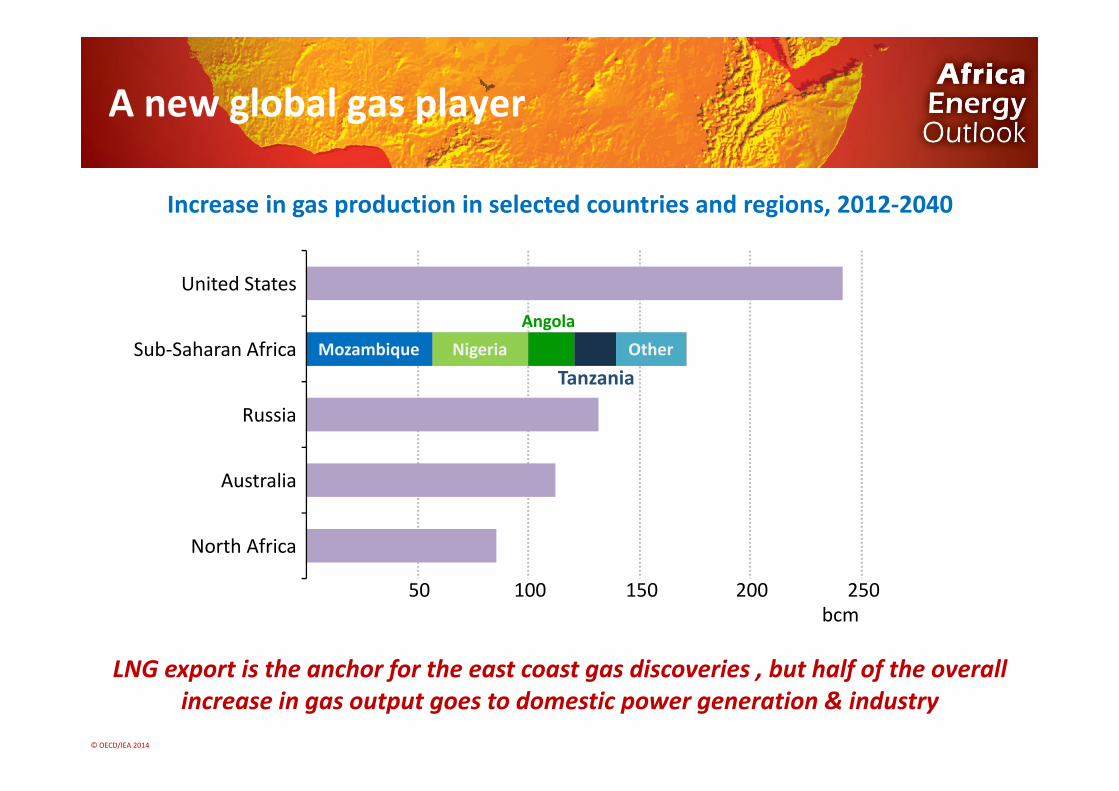

A new global gas player

Increase in gas production in selected countries and regions, 2012-2040

LNG export is the anchor for the east coast gas discoveries , but half of the overall increase in gas output goes to domestic power generation & industry

50 100 150 200 250

North Africa

Australia

Russia

Sub-Saharan Africa

United States

bcm

Mozambique Nigeria Other

Angola

Tanzania

© OECD/IEA 2014

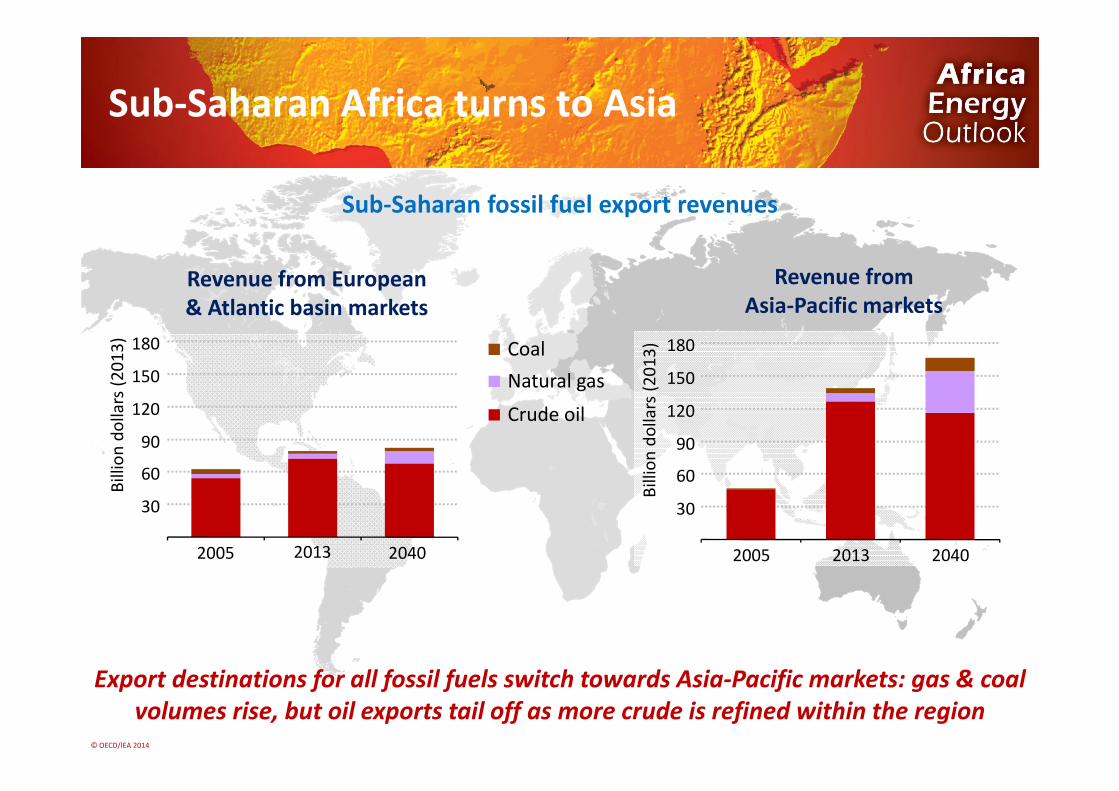

Sub-Saharan fossil fuel export revenues

Sub-Saharan Africa turns to Asia

Export destinations for all fossil fuels switch towards Asia-Pacific markets: gas & coal volumes rise, but oil exports tail off as more crude is refined within the region

Revenue from European & Atlantic basin markets

Revenue from Asia-Pacific markets

30

60

90

120

150

180

2005 2013 2040

30

60

90

120

150

180

2005 2013 2040

Coal

Natural gas

Crude oil

Billi

ondo

llars

(201

3)

Billi

on d

olla

rs(2

013)

© OECD/IEA 2014

Investment has to come home

Fuels

Electricity

For export

For consumption withinsub-Saharan Africa:

In a reversal of current trends, 2 out of 3 future investment dollars produce energy for sub-Saharan consumers, but this is still not enough to meet their needs in full

Average annual investment in sub-Saharan energy supply

20

40

60

80

100

120

2000-2013 2014-2035

Billi

on d

olla

rs (2

013)

⅓

⅔ ⅓

⅔

© OECD/IEA 2014

A large step towards universal access, but still a long way to go

Access to electricity in sub-Saharan Africa

2012 2020 2025 2030 2035 2040

300

600

900

1 200

1 500

1 800Million

Population withelectricity access

Population withoutelectricity access

Nearly 1 billion people gain access to electricity, but this still leaves 530 million, primarily in rural communities, without power in 2040

© OECD/IEA 2014

How could energy make the 21st an African Century?

Energy could do more to act as an engine of inclusive economic and social growth

An African Century Case assesses the impact of faster movement in three key areas:

An upgraded power sector; reducing power outages by half & achieving universal access in urban areas

Deeper regional co-operation; expanding markets & unlocking a greater share of the continent’s hydropower potential

Better management of resources & revenues; more efficiency & transparency in financing essential infrastructure

© OECD/IEA 2014

100

200

300

400

500

600

700

Mill

ion

peop

le

Without accessto electricity

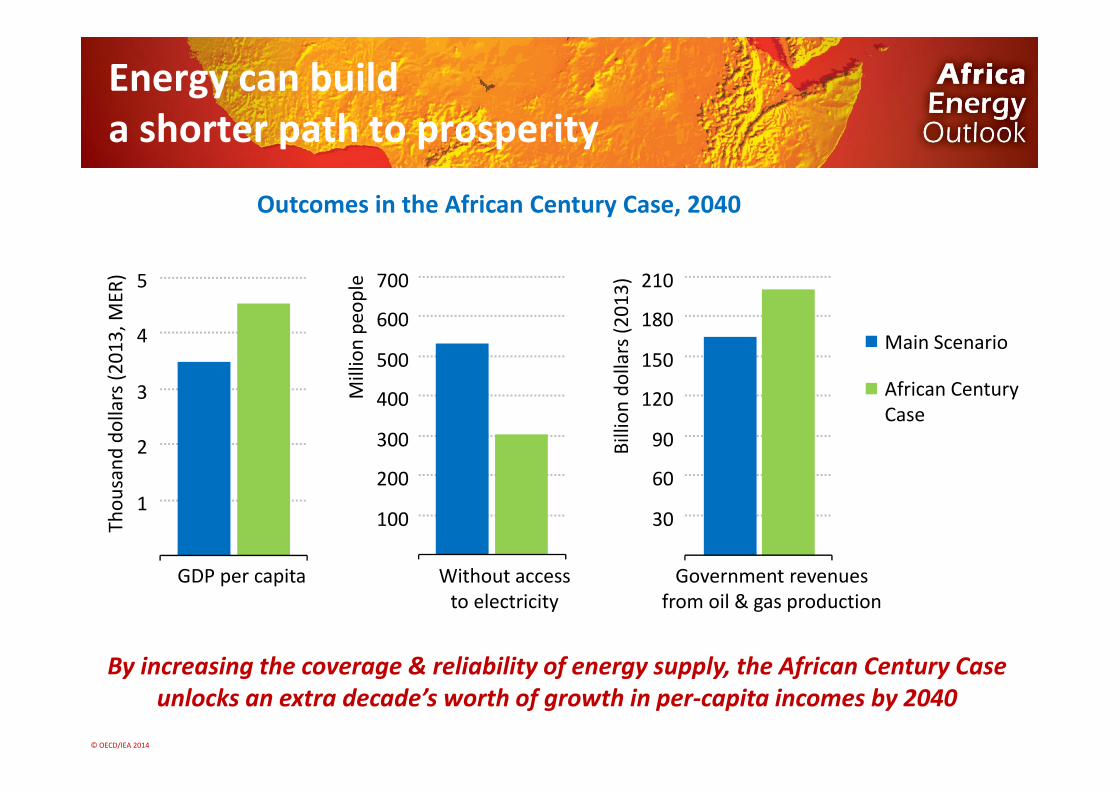

Energy can build a shorter path to prosperity

Outcomes in the African Century Case, 2040

By increasing the coverage & reliability of energy supply, the African Century Case unlocks an extra decade’s worth of growth in per-capita incomes by 2040

Main Scenario

African CenturyCase

1

2

3

4

5

Thou

sand

dol

lars

(201

3, M

ER)

GDP per capita

Billi

on d

olla

rs (2

013)

Government revenuesfrom oil & gas production

30

60

90

120

150

180

210

© OECD/IEA 2014

Conclusions

Energy is a cornerstone of sub-Saharan strategies for poverty reduction & economic growth

Improvements in sector governance are needed to bring in new energy investors & kick-start development

More efficient & sustainable use of biomass will create a more healthy domestic energy balance

Sub-Saharan Africa remains a mainstay of global oil production & emerges as a major player in natural gas

Concerted action to improve the functioning of the energy sector is essential if the 21st is to become an African century.