digital wallet

DESCRIPTION

ppt of digital walletTRANSCRIPT

DIGITAL WALLET

WHAT IS IN YOUR WALLET

WHAT IS A DIGITAL WALLETA digital wallet is a software component that allows a user to make an

electronic payment with a

financial instrument and hides the low-level details of executing the payment protocol that is

used to make the payment.

A digital wallet allows a user to make an electronic payment with a financial instrument (such as

a credit card or digital cash), and hides the low-level details of executing the payment protocol

that is used to make the payment.

It authenticates the consumer through the use of digital certificates or other encryption

methods, stores and transfers value, and secure the payment process from the consumer to the

merchant.

It can hold other than payments like Bank account details, Credit cards, Gift coupons and reward

certificates, Loyalty cards Offers.

COMPONENTS

A digital wallet has a software and information component.

The software provides security and encryption for the personal information and for the actual transaction.

Normally, digital wallets are stored on the client side and are easily self-maintained and fully compatible with most e-commerce Web sites.

A server-side digital wallet, also known as a thin wallet, is one that an organization creates for and about you and maintains on its servers. Server-side digital wallets are gaining popularity among major retailers due to the security, efficiency, and added utility it provides to the end-user, which increases their enjoyment of their overall purchase.

The information component is basically a database of user-inputted information. This information consists of your shipping address, billing address, payment methods (including credit card numbers, expiry dates, and security numbers), and other information.

HOW IT WORKS???

Sender Mobile sends request to Transfer Money. System checks available balance in Sender’s A/C from

that particular Bank. It transfers money from senders A/C to receivers A/C. After a successful money transfer it sends a

confirmation notification (SMS/Email) to receiver. Money can be send and/or receive from PayPoints.

PAYMENT MODELSFor point-of-sale transactions:-

A NFC-compatible “reader pad” can be deployed in retail stores.

When payment is required, consumers place their cell phone on/near the pad and all their valid payment options appear on a display.

They can then select the payment method they plan to use (cash, specific credit card, etc.) for the transaction.

The pad transmits the transaction request to the appropriate financial institutions using existing banking protocols provided by NETS, Visa, Amex, and MasterCard.

The consumer can provide any necessary signatures using a digital signature pad located next to the reader pad.

Once the transaction is verified and completed, the receipt is automatically sent to the cell phone and stored for future reference.

For peer-to-peer cash exchange, use the phone’s NFC capability together with an easy to use peer-to-peer cash application. Using the application, the payer can enter how much cash he needs to send to the other person. The payer then taps the cell phone of the payee and the cash is transferred instantaneously using NFC. The recipient is then informed of the exact amount transferred.

HOW TO SUPPORT CASH TRANSFER

Place cash in the digital wallet either by :a) Topping-up the cash on device at specific top-up machines

which are integrated with existing automated teller machinesb) Online by logging intobank’s online portal and transferring cash

into phone.

Transferring that cash to a retailer or another digital wallet by using NFC.

SECURE ELECTRONIC TRANSACTION (SET) PROTOCOL

Consumer’s Credit Card Issuing Bank1. Consumer makes purchase selects SET

payment option

Merchant

2. Merchant & consumer computers verify each other’s identity SET encrypts order & payment information

Merchant Bank

6 .Monthly statement issued with debit for purchase

3. Merchant software forwards encrypted message

4 . Clearinghouse verifies account & balance with issuing bank

5 . Issuing bank credits merchant account

Secure Line

Clearing House

FEATURES OF E–WALLET:Refillable

Infinite lifetime

Current balance can be stored and read

User authentication is provided

Universal access

Maximum possible cash

Cannot be duplicated

ADVANTAGESEase of use:

Withdraw or deposit value by telephone

Pay the exact amount, no fiddling for change

No signature required

Immediate payment

• Flexibility:

Transfer value by telephone

Pay person to person

For low or high values

Multi-currency capability

No age limit, so suitable for all the family

ADVANTAGES…Safety and control:

Spend only what you have

Read your balance

Load value at home

Lock your card or wallet

Keep track of what you have spent and where

Customer is traceable if a lost card is found

• Accessibility and convenience:

Cash machines and telephones give more access points to funds in bank account

Available 24 hours / 365 days

Cash machines and telephones cannot run out of electronic cash

DISADVANTAGES: System Outages: Information for digital wallets are stored on

the cloud of business servers; therefore, the risk of a system malfunction or shut down is always present. As a result, businesses will not be able to process payments or they will become increasingly slow due to high traffic in the servers.

Security: Companies must ensure that their customers' information is encrypted and well protected. One of the biggest concerns of adopting a digital wallet application is "will my information be safe"? This is the hurdle that companies must face and as a result, must develop security systems that are as safe and full proof as possible to avoid potential security issues.

Stake Holder Dynamics: Satisfying the business and strategic goals of multiple stake holders such as banks, retailers, regulatory bodies, is difficult.

Compelling user experience: A user-friendly wallet interface, easy to use and intuitive is difficult to produce.

PAYMENT METHOD

HOW IT IS BEING USED RIGHT NOW?

There are many different companies offering E-Wallets. Although each one is a little

different, they all perform the same basic tasks. Some of them are

• SQUARE Wallet

• GOOGLE e-wallet

• PayPal

GOOGLE E-WALLET

Google Wallet, currently available for purchases in the United States, lets you save all your loyalty cards in once place. You can also make payments online and at any merchant that has a card with credit attached to it. If you need to send money to someone, you can do so for free as long as they're using Google Wallet as well. Google Wallet offers tap to pay for NFC-enabled devices

SQUARE WALLET

Square Wallet lets you link a debit or credit card to your Square account and pay with it anywhere Square payments are accepted. If someone sends you a Square gift card you can also store that inside the Square Wallet app for use whenever you're at that merchant. For some places of business, you can even choose items from inventory and have your sale ready before even getting to the cash register.

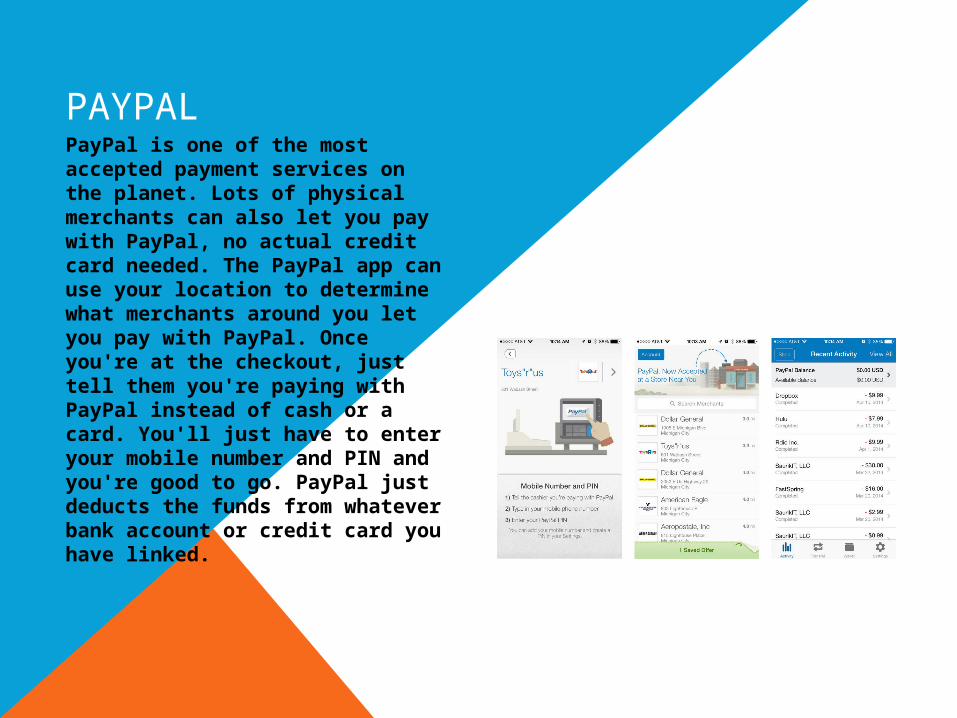

PAYPALPayPal is one of the most accepted payment services on the planet. Lots of physical merchants can also let you pay with PayPal, no actual credit card needed. The PayPal app can use your location to determine what merchants around you let you pay with PayPal. Once you're at the checkout, just tell them you're paying with PayPal instead of cash or a card. You'll just have to enter your mobile number and PIN and you're good to go. PayPal just deducts the funds from whatever bank account or credit card you have linked.

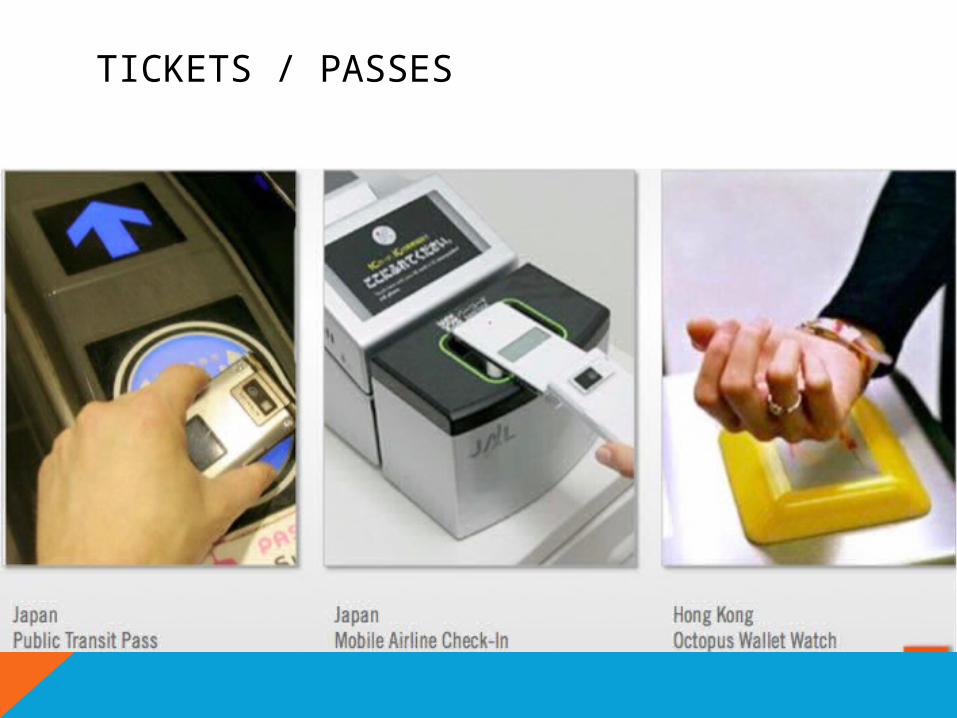

TICKETS / PASSES

Online shopping from mobile devices

Price comparison shopping

Bill Payments

Loyalty Redemption

Personal Information Access

Virtual Personal Organizer

Pre-emptive Purchasing

Device to Device Person to Person Payments

The electronic wallet will be able to facilitate purchasing from mobile phones and PDA’s.

FUTURE OF DIGITAL WALLET

The electronic wallet will allow comparison shopping at any Internet access point. This will provide true price transparency and consumer

control.The electronic wallet allow scheduling payment intervals for electronic bills and invoices and receiving bill reporting from any Internet access point.The electronic wallet will give consumers real time reporting of points

accrued under loyalty schemes and their conversion entitlements.The electronic wallet will become a single access personal financial portal including medical, insurance, motor vehicle, mortgage, superannuation and investment reporting.The electronic wallet will store the user’s calendar, contacts, tasks and lists on the network allowing this to be retrieved and updated from any device. The electronic wallet will be able to pre-empt purchasing based on habits and actually remind the consumer to make purchases on a regular basis.

THANK YOU!!