destination brazil · obligation to present the siscoserv has already started for certain...

TRANSCRIPT

Destination Brazil

Brazilian Taxes Recent changes April 25th, 2013

www.pwc.com

PwC

Content

1. Overview of Brazilian tax environment, legislation, and courts

2. Recent change inside Brazil

3. Recent change on flows between Brazil and French investors

2

PwC

Overview of Brazilian tax environment, legislation, and administrative process

3

1

PwC

In 2011, Brazil placed 30th among countries with the highest tax burdens in the world.

Source: Brazilian Institute of Tax Planning (IBPT)

45,00% 44,20% 44,05% 44,00% 43,40%

36,02%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Denmark (1st) France (2nd) Sweden (3rd) Belgium (4th) Finland (5th) Brazil (30th)

4

Highest Tax Burdens in the World

% of GDP

1.1. Brazilian Tax Environment

PwC

1.1. Brazilian Tax Environment Tax Burden in Brazil, as a Percentage of GDP, Including Informal Sector

5

30,03% 30,81% 32,64% 32,53%

33,49% 34,13% 34,52% 34,69% 34,85% 34,41% 35,04% 36,02% 36,27%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: Brazilian Institute of Tax Planning (IBPT)

PwC

1.1. Brazilian Tax Environment

Brazil has a complex tax system organized across 3 levels:

1.Federal taxes and social contributions (including social charges);

2. State taxes (26 states +1): each State has its own specific legislation, following general guidelines established at the federal level; and

3. Municipal taxes (5.500+ municipalities): similar to State taxes, municipal legislation varies from municipality to municipality, but follows federal rules which impose limits to such taxes’ applicability (e.g., tax rate ranges).

6

PwC

Principal Taxes in Brazil

7

Income Taxes Federal State Municipal Rates

Corporate Income Tax (IRPJ) X 25%

Social Contribution on Net Profits (CSLL) X 9%

Transaction Taxes Federal State Municipal Rates

Tax on Imports (II) X 5% to 20% (average)

Excise Tax (IPI) X 0% to 15% (average)

Social Contributions on Imports (PIS/COFINS – imports) X 9.25%

Social Contributions (PIS/COFINS) X 3.65% or 9.25%

Tax on Financial Transactions (IOF) – 0% if < 360 X 0% up to 25%

Contribution for the Intervention of Economic Domain (CIDE)

X 10%

State Value Added Tax (ICMS) X 17% to 18% (average)

Municipal Service Tax (ISS) X 2% up to 5%

1.1. Brazilian Tax Environment

PwC 8

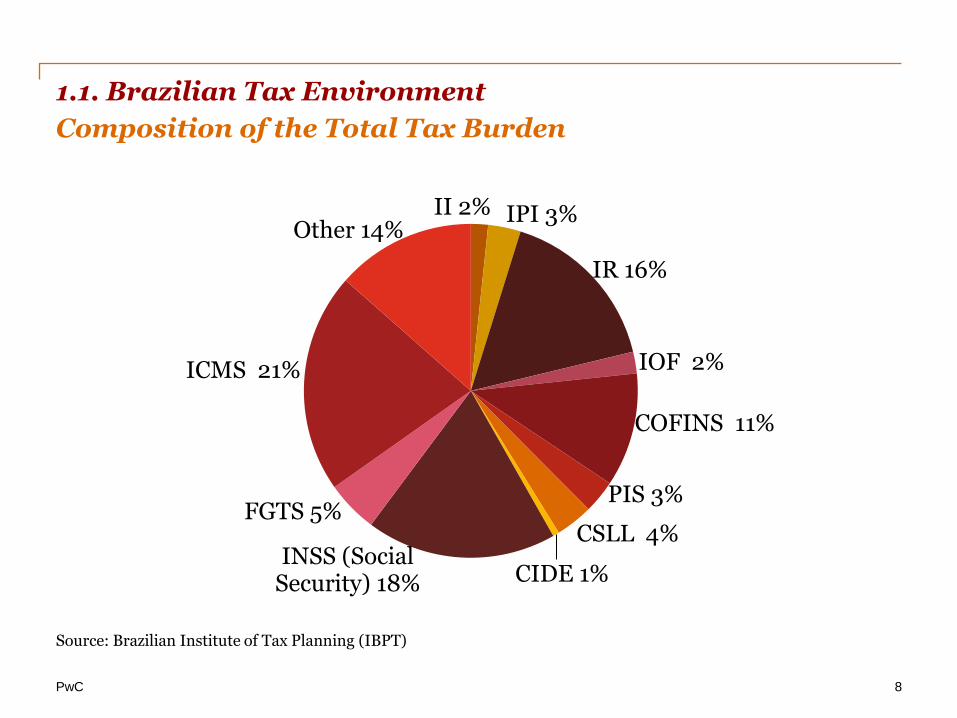

Composition of the Total Tax Burden

Source: Brazilian Institute of Tax Planning (IBPT)

II 2% IPI 3%

IR 16%

IOF 2%

COFINS 11%

PIS 3%

CSLL 4%

CIDE 1% INSS (Social

Security) 18%

FGTS 5%

ICMS 21%

Other 14%

1.1. Brazilian Tax Environment

PwC

1.2. Reminder of the legislative process – Tax matters

• Taxes are usually ruled by ordinary or complimentary laws:

• Legislative Procedure is bicameral;

• a Project of Law (PLP) must be:

approved by the Plenary of the Original Legislative House, and then

submitted to the Reviser House - if amendments are required, the PLP is sent back to the Original Legislative House for evaluation.

• if the project is approved by the majority of the Reviser House members, it is sent to the President of the Republic for ratification

• Notwithstanding, a significant quantity of tax rules are inserted in our system through

Provisional Measures (MP)

• Issued by the President/Executive Power, with power of law

• May be issued in urgent and relevant cases only

• Approval by Congress required within 60 days (renewable once)

9

PwC

1.3. Reminder of the administrative process

CARF – Superior Chamber

CARF – Chambers at Lower Level

Federal Revenue Officer

• Brazilian legislation establishes a five-year statute of limitations during which Tax Authorities (at Federal Revenue Offices) may assess taxpayers.

i. Federal Revenue Officers;

ii. CARF – Lower Level Court;

iii. CARF – Superior Chamber (“Câmara Superior de Recursos Fiscais”) – this is activated when:

Decisions contrary to the law, evidence collected, or not unanimous decisions - only Tax Authorities may appeal;

Decisions that interpret the Law differently from other chambers or from the CARF’s Superior Chamber – the taxpayer may also appeal.

• CARF does not decide on Constitutional issues.

• CARF must follow decisions of the Superior and Supreme Courts of Justice.

• Similar administrative entities exist at State and local levels.

• After going through the administrative path, taxpayer may still appeal to the judicial courts.

• Not necessary to wait until conclusion of the process at administrative level

10

PwC

Most common topics for French investors

• Bureaucracy – requires planning and local assistance (is SPED a remedy?)

• Brazilian Transfer Pricing rules – not aligned with the OECD rules ; based on minimum

and maximum profit margins, fixed by law.

• Service /management fees – high taxation (approx. 41%) and risk of non-deductibility

• Securing deduction of goodwill – appropriate acquisition structure needed

• Excess VAT credits – the need to properly consider the distribution chain in order to

appropriately define location of manufacturing plants, distribution centers, etc.

• VAT withholding – taxation under the substitution regime

• Royalties : deductions limited to between 1% and 5% of net revenue

• Application of DTTs (e.g., Brazilian WHT on management fees)

• Tax incentives – may be available for several specific industries

1.4. Brazilian Tax Environment

11

PwC

Recent changes in Brazil

12

2

PwC

2.1. Changes to Transfer Pricing Rules

Transfer Pricing Rules

• Brazil’s transfer pricing (TP) rules do not adopt the arm’s length principle.

• Maximum ceilings for deductible expenses on inter-company import transactions and minimum gross income floors for inter-company export transactions defined by law.

• The TP calculation methods have to be applied on an individual basis (not by individual transaction, but product by product).

• Brazilian TP legislation establishes, for exports, relief from proof under certain circumstances.

• TP adjustments are not isolated items for tax purposes, but rather part of the CIT calculation.

• Rules allow for the election of the method which provides the lowest tax cost and the Brazilian tax authorities are bound by this method.

13

PwC

2.1. Changes to Transfer Pricing Rules

• Imports and exports of commodities, quoted in commodities exchange market, must be

tested through the new PCI and PECEX methods

• based on daily average quote for each product

• Few adjustments allowed

• Products not quoted in the exchange market: taxpayers may use information obtained from independent sources, provided by internationally recognized institutes involved in researches of specific sectors

• For exports, prices can also be tested based on prices informed by regulatory agencies.

14

New methods applicable to commodities

Enforceable as from January 1, 2013

PwC

• Important changes also affected the PRL Method, the Brazilian equivalent to the Resale Price Method:

• The former PRL 20 calculation method has been extinguished

• The statutory margin of the PRL 60 was modified: 30% or 40% margins applicable to the following industries – a 20% margin for other industries/sectors:

• 40% mark-up:

• pharma chemicals and pharmaceuticals; • smoke products; • optical, photographic and cinematographic

equipment; • trading of machines, apparatus and

equipment for dental, medical, and hospital use;

• extraction of oil and natural gas; and • production of oil derivative products.

• 30% mark-up:

• production of chemical products; • production of glass and glass products; • production of pulp, paper, and paper

products; and • metallurgy.

2.1. Changes to Transfer Pricing Rules

15

Changes in the PRL Method

Enforceable as from January 1, 2013

PwC

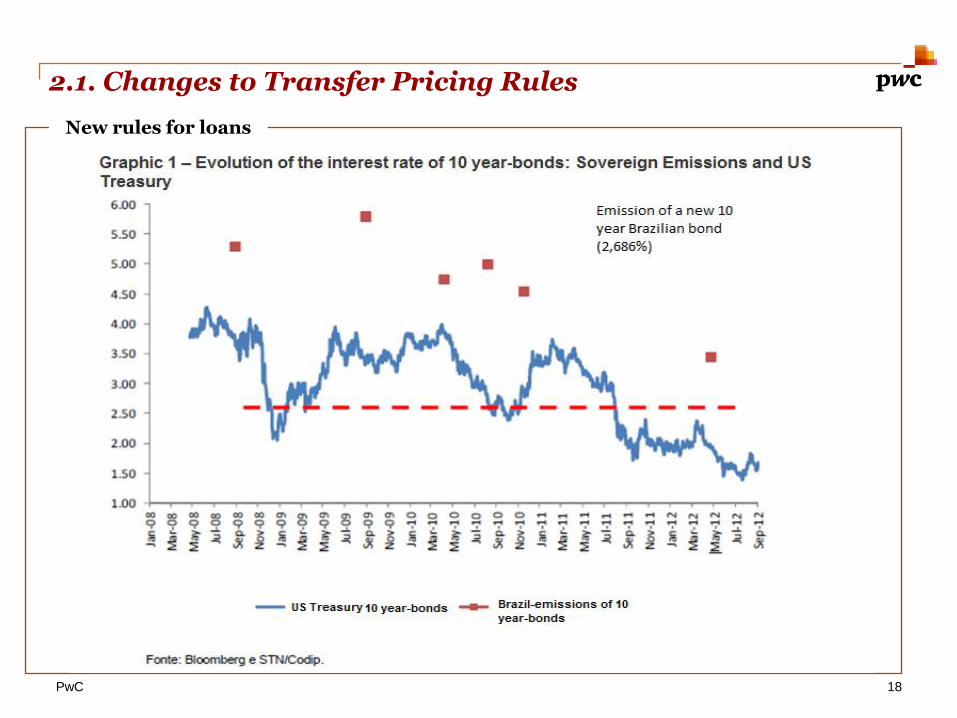

• Interest - deductible up to an amount not exceeding the rates below, plus a spread to be determined by the Ministry of Finance based on an average market spread:

• For US dollar-based transactions with fixed interest rate: use the rate of Brazilian

sovereign bonds issued in US dollars in foreign markets;

• For transactions in Brazilian reais, with fixed interest rate: rate of Brazilian sovereign bonds issued in Brazilian reais in foreign markets;

• in all other cases: London Interbank Offered Rate - LIBOR for the period of six months.

• In the case of transactions in Brazilian reais, subject to floating interest rate, the

Ministry of Finance can determine a different base rate.

2.1. Changes to Transfer Pricing Rules

16

New rules for loans

Enforceable as from January 1, 2013

PwC

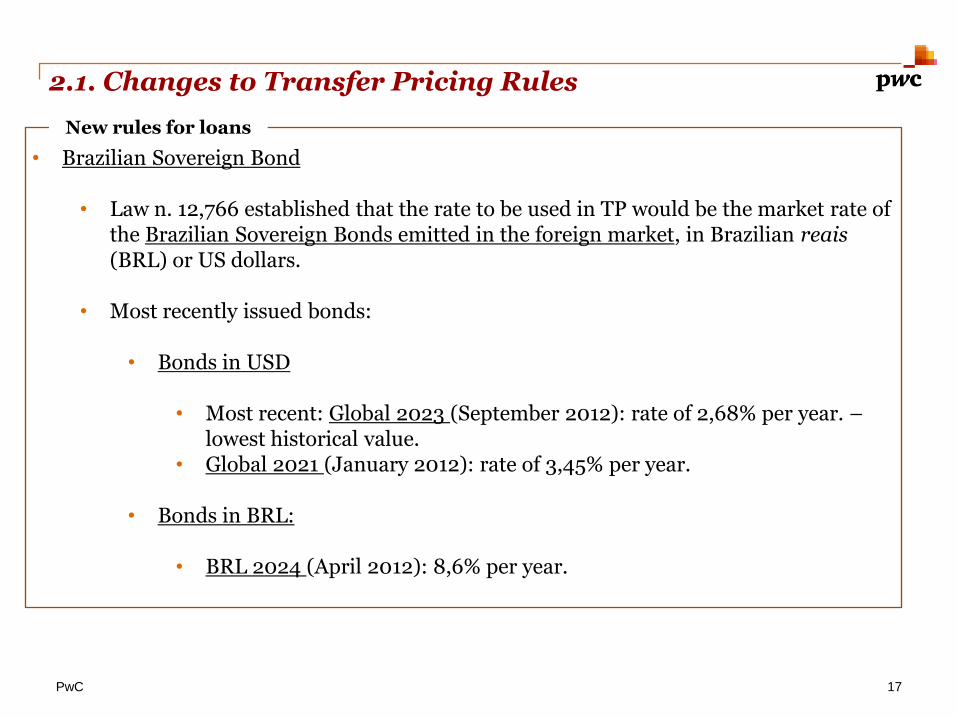

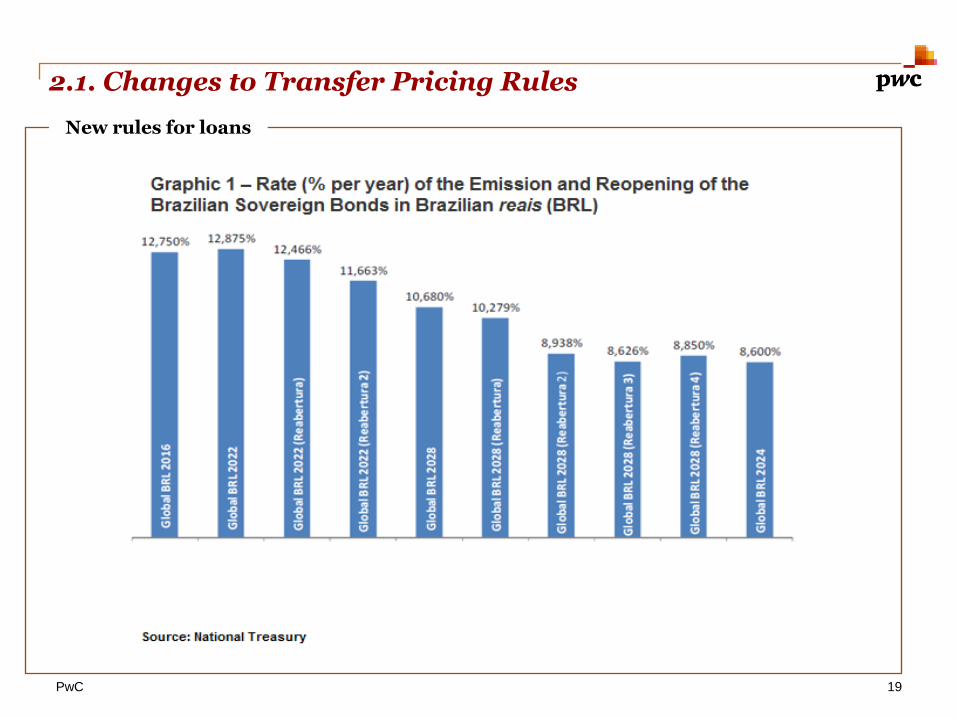

• Brazilian Sovereign Bond

• Law n. 12,766 established that the rate to be used in TP would be the market rate of

the Brazilian Sovereign Bonds emitted in the foreign market, in Brazilian reais (BRL) or US dollars.

• Most recently issued bonds:

• Bonds in USD

• Most recent: Global 2023 (September 2012): rate of 2,68% per year. –

lowest historical value. • Global 2021 (January 2012): rate of 3,45% per year.

• Bonds in BRL:

• BRL 2024 (April 2012): 8,6% per year.

2.1. Changes to Transfer Pricing Rules

17

New rules for loans

PwC

2.1. Changes to Transfer Pricing Rules

18

New rules for loans

PwC

2.1. Changes to Transfer Pricing Rules

19

New rules for loans

PwC

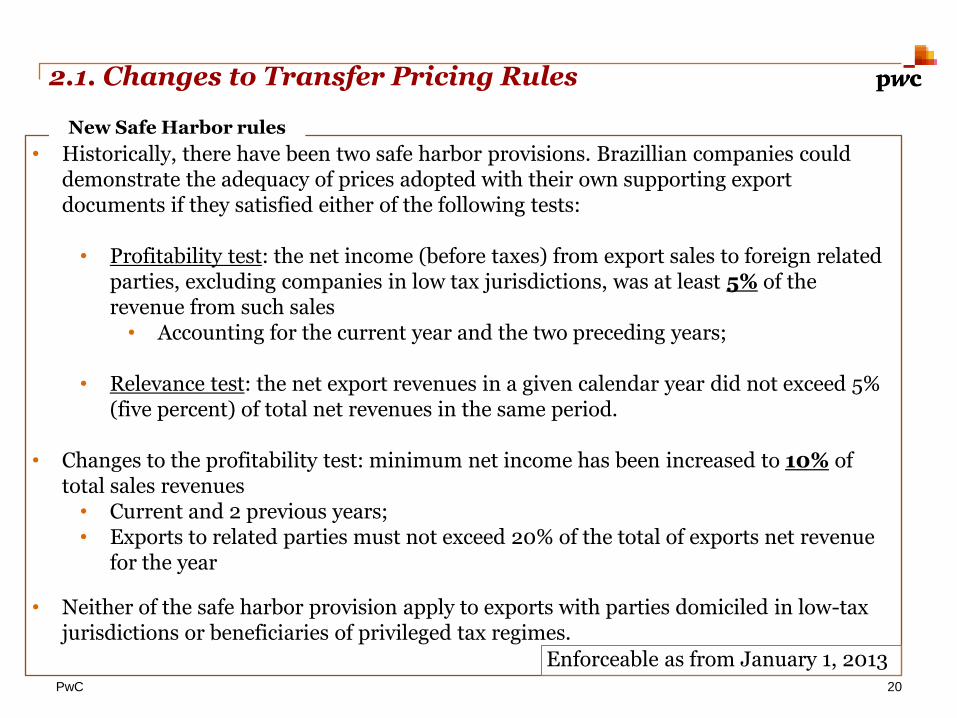

• Historically, there have been two safe harbor provisions. Brazillian companies could demonstrate the adequacy of prices adopted with their own supporting export documents if they satisfied either of the following tests:

• Profitability test: the net income (before taxes) from export sales to foreign related

parties, excluding companies in low tax jurisdictions, was at least 5% of the revenue from such sales • Accounting for the current year and the two preceding years;

• Relevance test: the net export revenues in a given calendar year did not exceed 5%

(five percent) of total net revenues in the same period. • Changes to the profitability test: minimum net income has been increased to 10% of

total sales revenues • Current and 2 previous years; • Exports to related parties must not exceed 20% of the total of exports net revenue

for the year

• Neither of the safe harbor provision apply to exports with parties domiciled in low-tax jurisdictions or beneficiaries of privileged tax regimes.

2.1. Changes to Transfer Pricing Rules

20

New Safe Harbor rules

Enforceable as from January 1, 2013

PwC

• Plano Brasil Maior

• Amendment to the Social Security Contribution (INSS) legislation:

• Replacing of the 20% contribution on payroll

• By • Contribution of 1% to 2% of gross revenue, excluding:

• export revenues, • unconditional discounts, • cancelled sales and • IPI (excise tax) on sales.

• New rule applies for companies in different industries:

• IT • Textile • Hotteling • Transportation • etc

2.2. INSS (Social Security Contribution) on Gross Revenue

21

Temporary – enforceable from 2011 up to end of 2014 – depending on industry

PwC

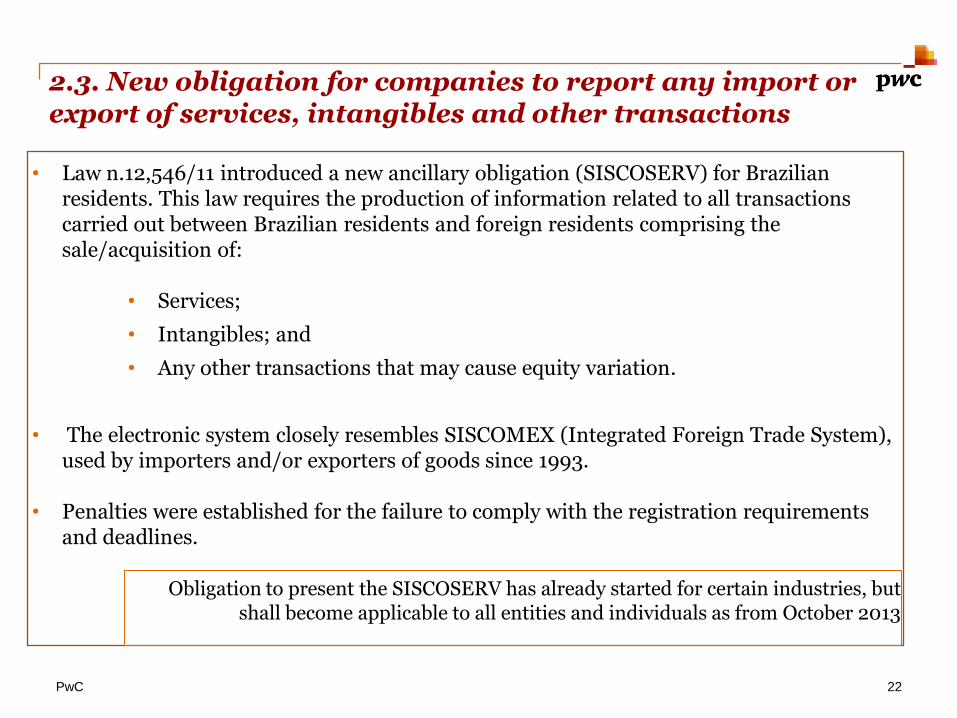

• Law n.12,546/11 introduced a new ancillary obligation (SISCOSERV) for Brazilian residents. This law requires the production of information related to all transactions carried out between Brazilian residents and foreign residents comprising the sale/acquisition of:

• Services;

• Intangibles; and

• Any other transactions that may cause equity variation.

• The electronic system closely resembles SISCOMEX (Integrated Foreign Trade System), used by importers and/or exporters of goods since 1993.

• Penalties were established for the failure to comply with the registration requirements and deadlines.

Obligation to present the SISCOSERV has already started for certain industries, but

shall become applicable to all entities and individuals as from October 2013

2.3. New obligation for companies to report any import or export of services, intangibles and other transactions

22

PwC

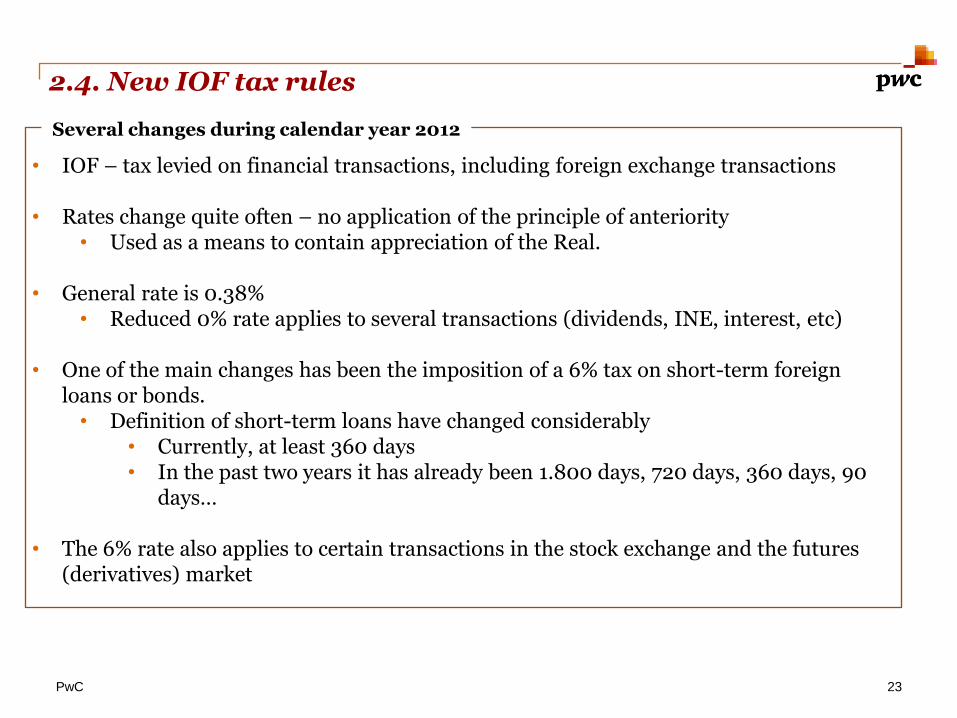

• IOF – tax levied on financial transactions, including foreign exchange transactions

• Rates change quite often – no application of the principle of anteriority

• Used as a means to contain appreciation of the Real.

• General rate is 0.38% • Reduced 0% rate applies to several transactions (dividends, INE, interest, etc)

• One of the main changes has been the imposition of a 6% tax on short-term foreign

loans or bonds. • Definition of short-term loans have changed considerably

• Currently, at least 360 days • In the past two years it has already been 1.800 days, 720 days, 360 days, 90

days…

• The 6% rate also applies to certain transactions in the stock exchange and the futures (derivatives) market

2.4. New IOF tax rules

23

Several changes during calendar year 2012

PwC

• Brazilian corporate taxpayers may chose to calculate CIT pursuant to either of two

different methods:

• Actual profit method (standard method) – taxable income calculated based on

adjusted accounting profits

• Presumed profit method – taxable income calculated based on the application of

specific margins determined by law on to gross revenue per type of activity

• As a general rule, the presumed profit method historically could not be adopted by

companies with a gross revenue in the previous year in excess of BRL 48 million. • As of January 1, 2014, such threshold will be increased to:

• BRL 72 million during the previous calendar-year; or • BRL 6 million multiplied by the number of activity months of the previous

calendar-year.

2.5. New limit established for the Presumed Profit Regime

24

Currently regulated by Provisional Measure

PwC

• State VAT (ICMS) rates normally vary from State to State

• In the case of Inter-State transactions, however, such rates are fixed by Federal legislation: • 7% on sales from the Southeastern Region (except Espírito Santo) to the North,

Central West, Northeastern Regions and the State of Espírito Santo; • 12% on the other way around

• Resulted in tax war between States - a “Port War” - focused on the import of

goods

• As of January 1, 2013, however, the applicable ICMS rate for the inter-state transfer of imported goods (less than 60% national content) is now 4% • Certain exceptions apply

• Further changes (reductions) to inter State rates expected (under negotiations)

2.6. ICMS – new rules regarding Inter State transactions

25

PwC

Changes in flows between Brazil and French Investors

26

3

PwC

3.1. Goodwill amortization – general comments

27

Tax Consideration

• Business purpose analysis

• Proper transaction needs to be implemented so that the goodwill becomes deductible (merger, liquidation)

Advantages:

• Deductibility of the goodwill amortization reduces taxable income of the OpCo Brazil

Disadvantages:

• Implementation of IFRS in Brazil creates difficulties regarding the support to the amount of amortizable goodwill

• Increasing pressure from the tax authorities, but

Recent positive decision at administrative level

Acquisition through Brazil

Merger

Foreign Parent

OpCo Brazil

Target

PwC

3.1. Goodwill amortization – “in house” goodwill

Historically, the Taxpayer’s Council (CARF) had continuously denied “in house” goodwill

amortization´s deductibility due CARF had continuously denied “in house” goodwill amortization´s deductibility due to alleged lack of business substance.

• Recently, CARF issued a landmark decision in a case involving the amortization of goodwill generated in a company´s sale within the same economic group. The fundamentals of the decision are the following:

• Where there is no abuse, well-grounded internal goodwill may be accepted.

• Tax planning is not forbidden

• Tax authorities plan to change the applicable legislation to expressly avoid deductibility of goodwill in such cases.

28

PwC

3.2. Brazilian WHT on service fees

• According to the Brazilian tax authoritiy’s opinion on service fee remittances abroad, where a DTT is in place, article 7 should not apply, but the “other income” article instead: • Compared to the wording of article 22 of the OECD Model, this article is usually

drafted in the "Brazilian Model" as follows:

"Other income - Items of income of a resident of a Contracting State which are not expressly mentioned in the foregoing articles of this Convention may be taxed in both Contracting States"

• According to the existing Declaratory Act, such should be the case even where a

DTT does not have a “other income” clause.

• The Brazilian Superior Court has recently issued a decision against such understanding: • article 7 - generally include service fees; taxation in Brazil of a foreign entity only if

there is a permanent establishment in Brazil • DTTs prevail over internal infra-legal normative acts.

• Important precedent

29

PwC

3.3. Brazilian CFC Rules

• On April 10, 2013, STF announced the result of a case regarding unconstitutionality of

article 74 of the Provisional Measure (MP) 2,158-35/2001 and of article 43, paragraph 2° of the Brazilian National Tax Code.

• These articles determine that Brazilian entities should include in IRPJ and CSLL´s taxable basis, at year end, the profits earned by foreign controlled or associated companies.

• By a majority of votes, the Court decided, with binding and erga omnes effects, that:

• Concerning associated companies not located in tax havens Article 74 is unconstitutional;

• Regarding controlled companies located in tax havens Article 74 is constitutional

• Retroactivity of the rule to periods prior to 2002 is unconstitutional (sole paragraph of Article 74)

30

PwC

3.4. Brazilian CFC and tax treaties

• Another favorable decision is the still unpublished decision of the Taxpayer’s Council, which ruled on the applicability of Brazilian CFC rules. According to that decision:

• The concept of controlled entities should not comprise indirectly controlled

entities;

• Income of indirectly controlled entities should not be taxed in Brazil without

addressing the situation of the intermediary holding company abroad;

• Holding companies have business substance where the holding company performs

acquisitions and sets strategic directives for the group;

• DTT signed between Brazil and Spain shall prevail over internal CFC rules.

• Notably, this decision does not necessarily set a trend.

31

PwC

3.5. PIS and COFINS on import of goods – unconstitutionality

• Taxes due on import transactions tend to be levied on top of each other. • Ex: PIS and COFINS are normally levied on CIF + ICMS + PIS + COFINS

• However, the Brazilian Supreme Court, by unanimous decision, decided that:

• There is no constitutional basis for the levy of PIS/COFINS on the ICMS amount,

and

• There is no constitutional basis for the gross-up calculation (inclusion of PIS/COFINS in their own calculation basis)

• Effects need to be verified on a case-by-case basis – creditable contributions in most

cases

• The decision does not have erga omnes effect

• possible to challenge in Court.

32

PwC

3.6. Opinion 202/2013 – Dividends and profits exemption

• As a general rule, dividends paid out of profits generated as of January 1, 1996 are exempt of income taxation (WHT) in Brazil.

• However, according to the Attorney-General of the National Treasury (PGFN), this exemption is allowable only to the extent such profits are the same as the ones used for calculation of taxable income. Therefore, there is a difference between:

• Accounting profits (according to “Brazilian IFRS”); vs. • Adjusted accounting profits (Transitional Tax Regime).

• As a result, amounts paid based on the profits of a company calculated as per the new

Brazilian GAAP, but in excess of the profits computed in accordance with the Transitional Tax Regime rules (RTT) could be subject to taxation in Brazil (subject to further discussion).

• This issue should be avoided with the eminent publication of the new rule on RTT and tax profits.

33

PwC

Gustavo Carmona Sanches PwC Brazil - ITS Senior Manager [email protected] PricewaterhouseCoopers Av. Francisco Matarazzo, 1.400 - Torre Torino, São Paulo - Brasil - 05001-903 Alice de Massiac Avocat – Tax Partner +33 (0) 1 56 57 41 15 | P : +33 (0) 6 89 33 10 71 [email protected] Landwell & Associés, société d’avocats | Membre du réseau international PwC Crystal Park – 61, rue de Villiers – 92208 Neuilly-sur-Seine Cedex – France

34

Thank you!