dealing with disruption - oracle blogscdn.app.compendium.com/uploads/user/a33eed35-8a44-4da7... ·...

TRANSCRIPT

IHS QUARTERLY Q4-2014

DEALING WITH DISRUPTIONGeopolitics, technology, demographics, the environment, competitors.

Disruption is everywhere. Are you prepared?

WHY TESLA MATTERS Challenging the old order

P62

RETHINKING PRODUCTION 3D printing gains traction

P30

SHIFTING BORDERS Redrawing the world map

P36

NEW ENERGY SCENARIO Rivalry defines the future

P46

NANOTECH ACCELERATES From the lab to the market

P54

Your source for comprehensive insight, information, and expertise on key topics shaping today’s global business landscape.

We invite you to continue the conversation...

IHS QUARTERLY Q4-2014

main red

PMS 1795CC0 M96 Y90 K2

YOUTUBE LOGO SPECS

PRINTgradient bottom

PMS 1815CC13 M96 Y81 K54

on dark backgroundson light backgrounds

standard

no gradients

watermark

stacked logo (for sharing only)

standard

no gradients

watermark

stacked logo (for sharing only)

white

WHITEC0 M0 Y0 K0

black

BLACKC100 M100 Y100 K100

Visit and subscribe: ihs.com/IHSQ14

Contact: [email protected]

Join the conversation: @IHS

Engage: #IHSQuarterly

IHS Quarterly | Q4-2014 | 3

IHS QUARTERLY Q4-2014

FEATURES

WHEN MACROECONOMICS AND GLOBAL SUPPLY CHAINS COLLIDE Economics, geopolitics, and demographics influence global trade and impact the supply chains that are its lifeblood. Understanding the interaction of these macro-phenomena and their implications provides an edge that global companies need to stay competitive.By Chris G. Christopher, Jr. and David Deull

P 18

REELING IN ILLEGAL FISHING It is estimated that one-third of all fish caught on the high seas is done illegally. Global action to combat the crisis is now focusing on the establishment of an identification scheme for all fishing vessels.By Alex Gray

P 24

A NEW MANUFACTURING BLUEPRINT? 3D printing has already made inroads in a number of industries, enabling the creation of highly complex shapes and unprecedented customization. As printer costs fall and new competitors emerge, “traditional” industrial production models and their supply chains will be threatened.By Alex Chausovsky

P 30

NEW DIMENSIONS, NEW MAPS: SHIFTING BORDERS, BOUNDARIES, AND SOVEREIGNTY From Western Europe to the Western Pacific, state and non-state actors alike are challenging existing land and maritime borders. What are the implications for the defense, security, and business communities?By Tate Nurkin

P 36

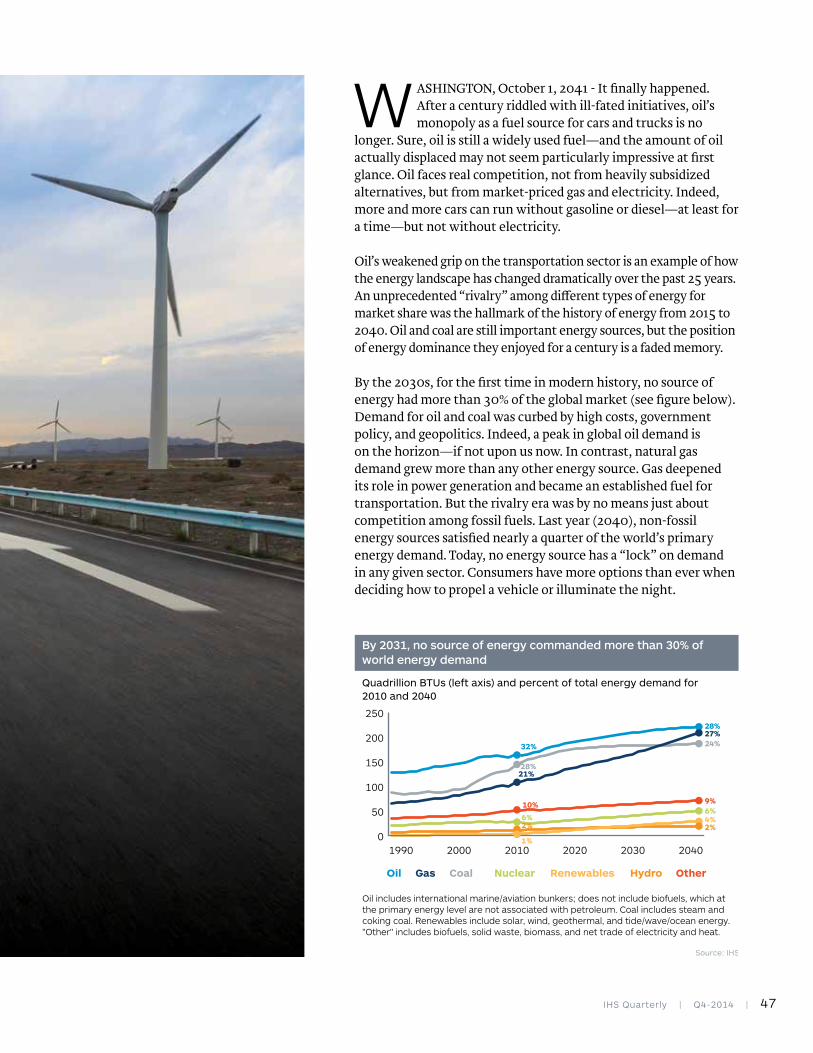

THE RIVALRY ERA: A BRIEF HISTORY OF THE ENERGY INDUSTRY FROM 2015 TO 2040 Dateline 2041: The energy rivalry of the past 25 years has profoundly impacted the energy industry. Oil no longer holds a monopoly as a transport fuel. Use of renewable energy has grown rapidly—and demand for gas has soared.By Jim Burkhard

P 46

VERY SMALL PARTICLES WITH VERY BIG IMPLICATIONS Nanotechnology has been in commercial products for some time, but the pace of development of new nanomaterials is accelerating. The field could prove transformative for many industries, including the one responsible for producing the nanomaterials: chemicals.By Michelle Lynch, Mark Morgan, and Jagdish Rebello

P 54

TESLA MOTORS: A CASE STUDY IN DISRUPTIVE INNOVATION The IHS Technology Teardown Team took apart a 2013 Tesla Model S and found systems and components unique in the auto industry. But Tesla’s disruptive influence goes beyond semiconductors. It’s about a vision for the car that is helping shape the future of the century-old auto industry.By Mark Boyadjis

P 62

DEALING WITH DISRUPTIONIHS provides global corporations with information, insight, and expertise to help them manage disruption and their businesses. Whether it is a tactical operational challenge or a strategic bet-the-company shift, we help businesses deal with disruption by paying attention to the smallest details and by showing them the big picture. IHS Quarterly reflects this mission by providing insight and expertise from our thought leaders to help readers deal with disruption no matter what their industry, be it aerospace, defense & security, automotive, chemicals, energy, maritime, or technology. Our depth and breadth can elevate your understanding of complex issues and give you an edge.

IHS QUARTERLY

COPYRIGHT NOTICE AND LEGAL DISCLAIMER© 2014 IHS No portion of this publication may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS. Content reproduced or redistributed with IHS’s permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America). TRADEMARKSIHS Quarterly and the IHS globe design are trademarks of IHS. Other trademarks appearing in this publication are the property of IHS or their respective owners.

4 | IHS Quarterly | Q4-2014

#IHSQuarterly

VISIONTHE YIN AND YANG OF DISRUPTION By Scott Key P 5

INSIGHTSShale gas could drive economics of hydrogen fuel-cell vehicles P 6

Cyber threats against industry: Are asset owners prepared? P 7

Naphtha outlook in limbo amid shifting crude, chemical markets P 8

Home health technologies look to reshape patient care P 9

Emerging countries drive a hard bargain in defense market P 10

Escalating costs drive diminishing returns for oil companies P 11

Scrubbers gain favor as shipowners gird for SOx regulations P 12

US utilities test business case for behind-the-meter storage P 13

A new home for homeless hydrocarbons? P 14

China’s ‘green fence’ pressures recyclers to upgrade operations P 15

ANALYTICSCHEMICALS ON THE MOVE Source: IHS P 16

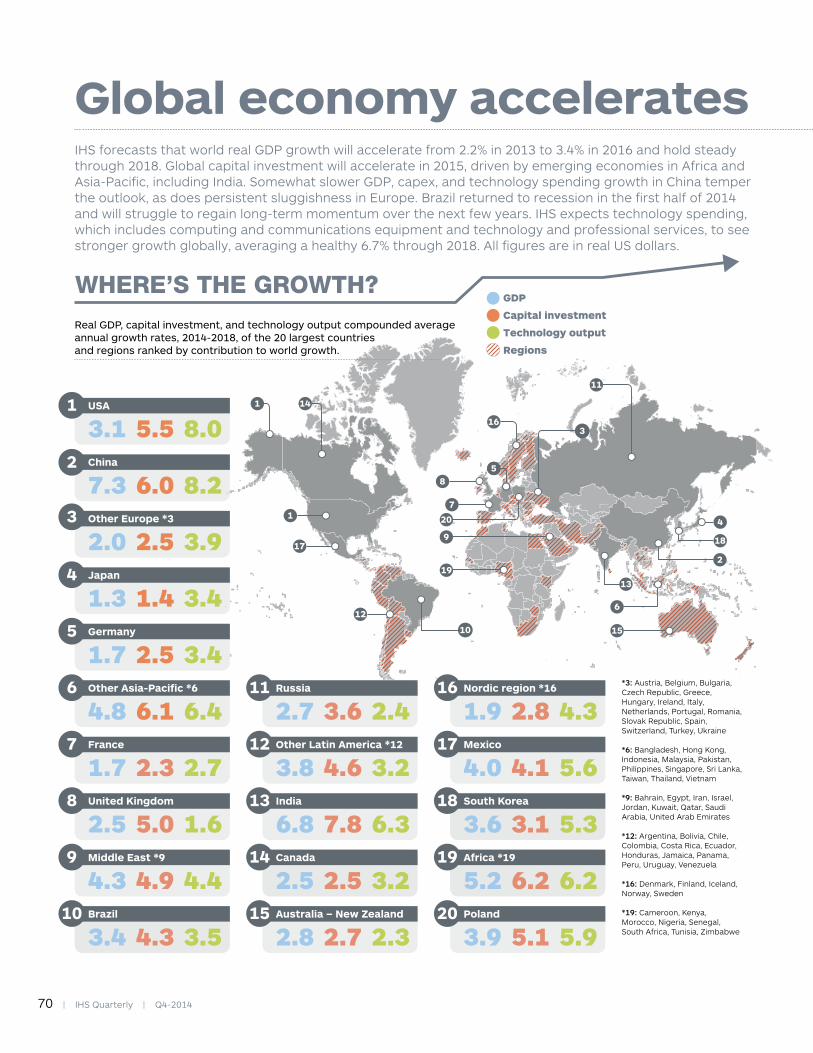

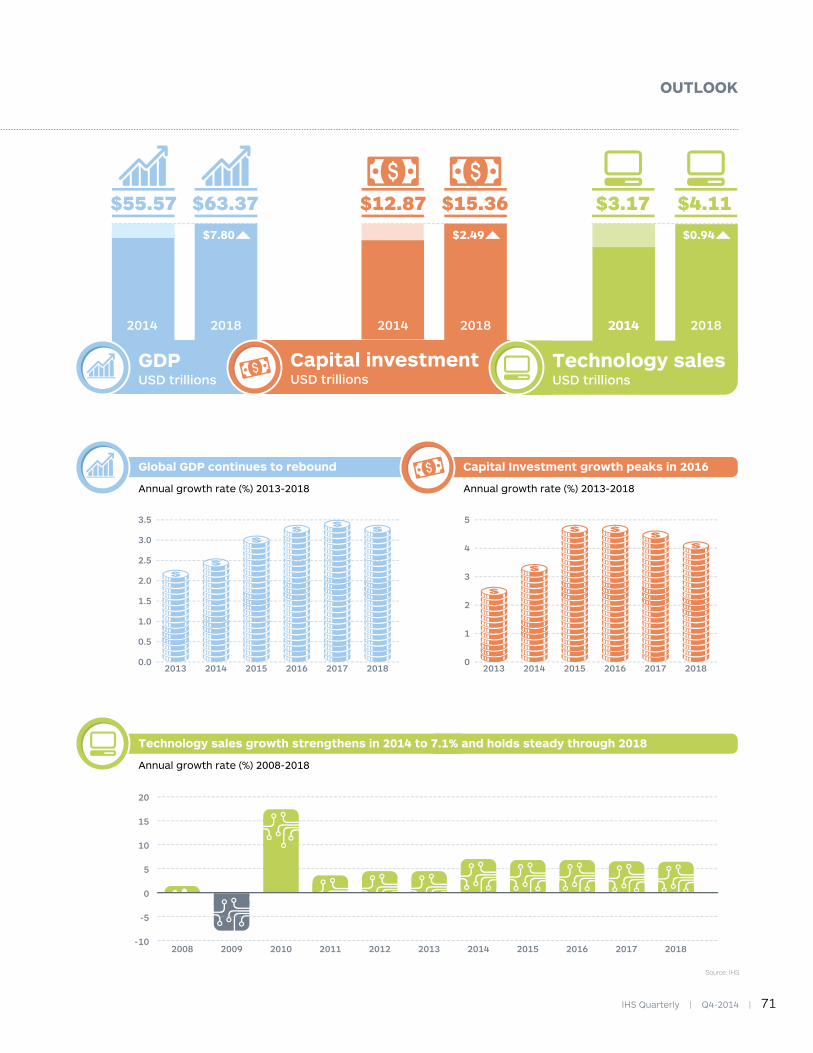

OUTLOOKGLOBAL GDP, CAPITAL INVESTMENT, AND TECHNOLOGY SPENDING Source: IHS P 70

NUMBERS11 METRICS THAT MATTER Source: IHS P 72

SPOTLIGHTLIFE IN THE VERY FAST LANE By Dale Ford P 74

IHS QUARTERLY Q4-2014

IHS Inc.

Scott KeyPresident & Chief Executive Officer

Jonathan GearSenior Vice President – Industrials

Anurag GuptaExecutive Vice President – Strategy, Products & Operations

IHS Quarterly

Sheri RhodineVice President, Integrated Marketing

John WardSenior Director, Thought Leadership

Bruce RaynerEditorial Director, IHS Quarterly

Thomas GoodfellowSenior Strategist, Thought Leadership

John SimpsonSenior Editor, IHS Quarterly

Peter BeddowCreative Director, IHS Quarterly

IHS Global Editing, Design, and Production Team

IHS Quarterly Editorial Council

Tim ArmstrongVice President, IHS Automotive

Atul AryaSenior Vice President, IHS Energy

Nariman BehraveshChief Economist, IHS

Richard ClaytonChief Maritime Analyst IHS Maritime & Trade

Mark EramoVice President, IHS Chemical

Dale FordVice President, IHS Technology

Chad HawkinsonVice President, IHS Product Design

Scott LockhartSenior Vice President, IHS OperationalExcellence & Risk Management

Tate NurkinManaging Director, IHS Aerospace, Defense & Security

Zbyszko TabernackiVice President, IHS Economics & Country Risk

IHS Quarterly | Q4-2014 | 5

VISION

The yin and yang of disruption

Disruption is a part of life, whether small interruptions to our daily schedules or life-changing events that put us on a new path. In business, disruption is often defined as an unplanned—and often unanticipated—externality that increases risk and cost. But just as in life, business disruptions can create new opportunities that, if managed well, lead to new products, services, and business models. At the core of the yin and yang of disruption is the opportunity to learn.

This issue of IHS Quarterly tackles disruption head on. In Shifting borders, boundaries, and sovereignty, Tate Nurkin explores the causes for and implications of some of the challenges to borders we are seeing unfolding around the world. Beyond the human cost, these shifts can have profound and long-lasting impacts on global businesses. To survive and thrive in this unsettled environment, companies need sophisticated tools and techniques to help them prepare for and respond to shifting borders.

Two articles explore the disruptive impact of emerging technologies: one on 3D printing and another on nanotechnology. In both articles, the authors discuss the implications of these technologies for companies across the value chain and provide roadmaps for how these technologies will move from novelty to ubiquity. How companies choose to adapt to these disruptions will likely shape their futures for the next decade and beyond.

Written from the perspective of 2041, Jim Burkhard’s article, The Rivalry Era, looks back over the past 25 years to document the changes within the energy industry wrought by the emergence of new energy resources. As the acceptance of natural gas and renewables grew, crude oil’s share of the energy market declined. This new energy “rivalry” is one possible version of the future that lies ahead and is IHS Energy’s new planning scenario to help energy companies understand and prepare for the disruptions to come in the next 25 years.

Our feature on Tesla Motors provides a case study in disruption occurring within the automotive industry. The article draws from the wealth of information gathered by the IHS Technology Teardown Team from its dissection of a 2013 Model S to uncover the design, manufacturing, and service innovations Tesla has built into the car. While Tesla may be in the spotlight, the rest of the auto industry is busy learning from the disruption.

Analyzing and interpreting the impact disruption has on business operations are what IHS does every day. Applying insight and expertise to help companies learn from disruption is our business.

Scott Key President and Chief Executive Officer IHS

6 | IHS Quarterly | Q4-2014

INSIGHTS

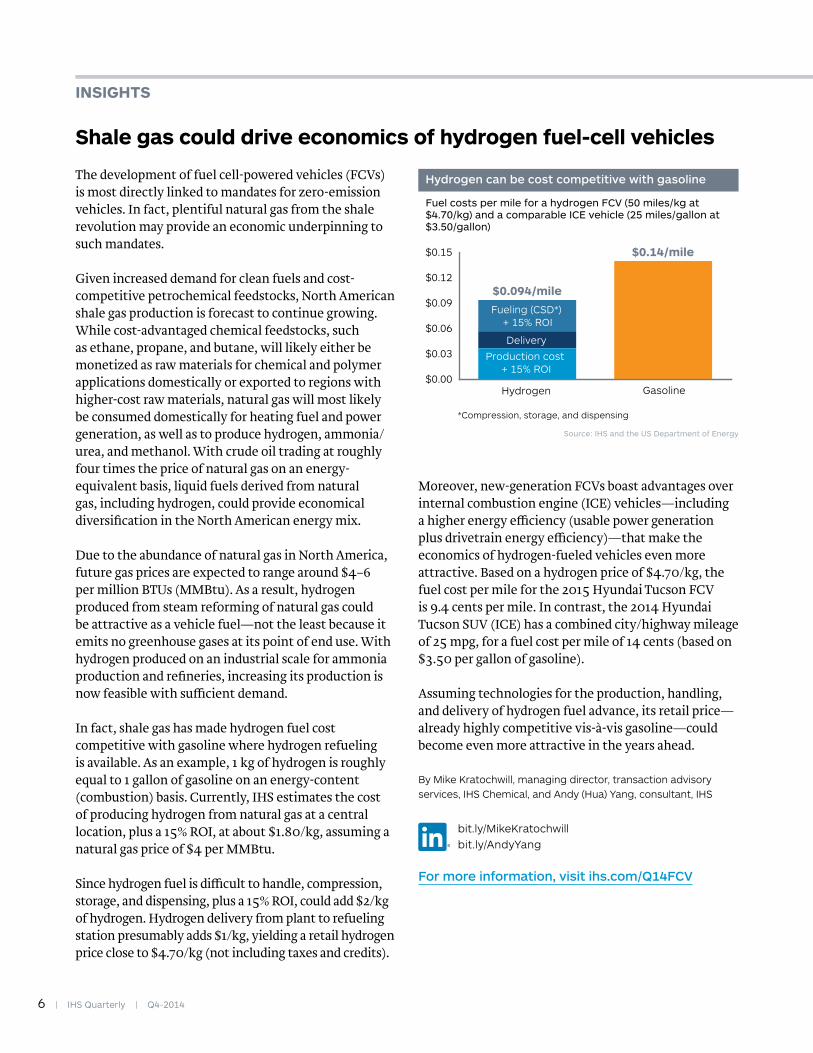

The development of fuel cell-powered vehicles (FCVs) is most directly linked to mandates for zero-emission vehicles. In fact, plentiful natural gas from the shale revolution may provide an economic underpinning to such mandates.

Given increased demand for clean fuels and cost-competitive petrochemical feedstocks, North American shale gas production is forecast to continue growing. While cost-advantaged chemical feedstocks, such as ethane, propane, and butane, will likely either be monetized as raw materials for chemical and polymer applications domestically or exported to regions with higher-cost raw materials, natural gas will most likely be consumed domestically for heating fuel and power generation, as well as to produce hydrogen, ammonia/urea, and methanol. With crude oil trading at roughly four times the price of natural gas on an energy-equivalent basis, liquid fuels derived from natural gas, including hydrogen, could provide economical diversification in the North American energy mix.

Due to the abundance of natural gas in North America, future gas prices are expected to range around $4–6 per million BTUs (MMBtu). As a result, hydrogen produced from steam reforming of natural gas could be attractive as a vehicle fuel—not the least because it emits no greenhouse gases at its point of end use. With hydrogen produced on an industrial scale for ammonia production and refineries, increasing its production is now feasible with su¡cient demand.

In fact, shale gas has made hydrogen fuel cost competitive with gasoline where hydrogen refueling is available. As an example, 1 kg of hydrogen is roughly equal to 1 gallon of gasoline on an energy-content (combustion) basis. Currently, IHS estimates the cost of producing hydrogen from natural gas at a central location, plus a 15% ROI, at about $1.80/kg, assuming a natural gas price of $4 per MMBtu.

Since hydrogen fuel is di¡cult to handle, compression, storage, and dispensing, plus a 15% ROI, could add $2/kg of hydrogen. Hydrogen delivery from plant to refueling station presumably adds $1/kg, yielding a retail hydrogen price close to $4.70/kg (not including taxes and credits).

Moreover, new-generation FCVs boast advantages over internal combustion engine (ICE) vehicles—including a higher energy e¡ciency (usable power generation plus drivetrain energy e¡ciency)—that make the economics of hydrogen-fueled vehicles even more attractive. Based on a hydrogen price of $4.70/kg, the fuel cost per mile for the 2015 Hyundai Tucson FCV is 9.4 cents per mile. In contrast, the 2014 Hyundai Tucson SUV (ICE) has a combined city/highway mileage of 25 mpg, for a fuel cost per mile of 14 cents (based on $3.50 per gallon of gasoline).

Assuming technologies for the production, handling, and delivery of hydrogen fuel advance, its retail price—already highly competitive vis-à-vis gasoline—could become even more attractive in the years ahead.

By Mike Kratochwill, managing director, transaction advisory services, IHS Chemical, and Andy (Hua) Yang, consultant, IHS

bit.ly/MikeKratochwill bit.ly/AndyYang

For more information, visit ihs.com/Q14FCV

Fuel costs per mile for a hydrogen FCV (50 miles/kg at $4.70/kg) and a comparable ICE vehicle (25 miles/gallon at $3.50/gallon)

Hydrogen can be cost competitive with gasoline

Source: IHS and the US Department of Energy

$0.00

$0.03

$0.06

$0.09

$0.12

$0.15 $0.14/mile

Hydrogen Gasoline

$0.094/mile

Delivery

Production cost + 15% ROI

Fueling (CSD*) + 15% ROI

*Compression, storage, and dispensing

Shale gas could drive economics of hydrogen fuel-cell vehicles

IHS Quarterly | Q4-2014 | 7

Cyber attacks targeting retailers may garner more media attention, but threats to industrial control systems are a growing concern. The US Department of Homeland Security responded to 257 such incidents in 2013—up from 198 in 2012 and 130 in 2011—over half of them attacks on energy infrastructure.

While the vulnerability of business-critical operations is widely known, the investment needed to secure them has not been made. An IHS survey of 12 major asset-owning industries, including energy, automotive, and chemical, shows high awareness of the threats faced at the operations level but a resistance to investing in cybersecurity measures because of their cost (see figure).

Global revenues of hardware, software, and services to secure automation/production networks across the surveyed industries are estimated at $600 million for 2013. While that market is projected to grow 12% annually, to $1.2 billion by 2019, cybersecurity products will still account for only 1% of all automation spending.

Holding back investment is the perceived lack of return associated with it. As it is virtually impossible to know whether a cybersecurity investment helped prevent an attack, security is viewed as a sunk cost less attractive to management than competing projects that provide measurable returns—although after-the-fact remediation is staggeringly expensive.

Several initiatives may encourage a change in thinking. Among those is the development of IEC 62243, an international standard aiming to establish best practices for securing operational technologies covering all aspects of industrial cybersecurity during an asset’s lifecycle.

Such a standard could apply across geographically dispersed facilities. And, unlike existing regulations such as NERC-CIP—which uses a prescriptive approach to secure assets critical to the operation of the US electric grid—IEC 62243 is risk based, allowing asset owners to prioritize investment and solutions rather than work through a list of mandatory requirements.

In the long run, the standard may bear more directly on automation suppliers—limiting their certification

work and driving them to develop products that are secure by design.

Another factor that may drive asset owners’ adoption of cybersecurity products is the changing attitude to cyber risk by insurers, who in assessing the risks of unsecured control systems are o©ering reduced premiums to companies that implement cybersecurity measures. As yet, asset owners surveyed by IHS ranked “lower insurance premiums” among the least important factors driving their cybersecurity spending. However, that attitude could change dramatically in the event of a damaging, high-profile cyber attack against a critical infrastructure asset.

By Toby Colquhoun, senior analyst, discrete and process automation, IHS Technology

bit.ly/TobyColquhoun

For more information, visit ihs.com/Q14CyberSecurity

Cyber threats against industry: Are asset owners prepared?

May 2014 survey results of companies in major asset-owning industries asked to rank factors hindering investment in cybersecurity: 5 = strongly agree; 1 = strongly disagree

Biggest hurdle to securing cyberspace: cost

Source: IHS

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Cost of software is too high

Cost of services is too high

Cost of hardware is too high

Senior management has low awareness of cybersecurity threats

Decision making hampered by limited tech knowledge of cybersecurity

Tension between IT and Engineering on overall project responsibility

Operations/IT/Engineering have low awareness of cybersecurity threats

5 4 3 2 1

8 | IHS Quarterly | Q4-2014

INSIGHTS

Naphtha—a refined petroleum product marketed in “heavy” and “light” varieties—plays a key role in the production of petrochemicals and gasoline. Heavy naphtha is a feedstock for high-octane gasoline and to produce the aromatic chemicals used to make PET bottles and polyester fiber. Lighter “para¡nic” naphtha is a gasoline blend-stock and a feedstock used to produce the olefins ethylene and propylene.

Light and heavy naphtha yield 40% of the global gasoline pool. Supply, demand, and prices of para¡nic and heavy naphtha are linked, as both are made from crude oil and are major gasoline constituents.

In 2012-13 aromatics manufacturers expressed concern over potential shortages of heavy naphtha for the new aromatics capacity expected in 2014-16. Their rationale was that oversupply of light naphtha from US unconventional oil/gas would spur demand for heavy naphtha required to blend sub-octane para¡nic naphtha. IHS analysis in “The Impact of Tight Oil and Shale Gas on Refining and Petrochemicals” concluded that North American light and heavy naphtha supplies were in fact balanced, and the impact of lower-quality heavy naphtha would be mostly diluted in about 7 million barrels of US Gulf Coast refining capacity. By 2014 tight oil production had accelerated, which when combined with weaker downstream demand in the short term has created some surplus, particularly in para¡nic naphtha.

While strong petrochemical demand and gasoline seasonality may push heavy naphtha prices above those of gasoline, in the long run they are likely to trend below gasoline prices. Similarly, light naphtha prices can fall below crude prices, but subsequent poor or negative refining margins as well as decreased crude processing tend to rebalance prices.

Self-balancing mechanisms are also in play on the global market. While naphtha demand as a feedstock in US petrochemical plants is being displaced by lower-cost ethane, demand for US ethane, propane, and butane (EPB) by European and Asian steam crackers will tend to boost prices of EPB feeds and steam cracking co-products, improving naphtha cracking economics over time.

IHS believes several factors will undergird naphtha demand, including:• In the United States, light naphtha and natural

gasoline prices will be supported by their gasoline-blend values and strong demand from Alberta bitumen crude blending.

• Depending on the extent of EPB penetration, global naphtha demand from steam cracking could decrease from as high as 2% annual growth to -1% annual decline (see chart). Aromatic demand for heavy naphtha will grow at close to 4% annually.

• Gasoline demand will increase 1-1.5% annually over the medium term.

Subject to shifting market dynamics and the extent of EPB cracking, naphtha’s outlook is for weaker short- to medium-term and improving longer-term demand, driven particularly by Asian and Middle Eastern petrochemical manufacturers.

By Nick Rados, director of feedstocks and energy, IHS Chemical

bit.ly/NickRados

For more information, visit ihs.com/Q14Naphtha

Naphtha demand as feedstock, 2014 - 2021, under baseline and high-EPB feed scenarios. Left scale: kilotons/annum; right scale: 5-year average annual growth rate (AAGR)

Chemical plants' higher use of ethane, propane, and butane (EPB) could lower short-term naphtha demand

Source: IHS

-8,000

-4,000

0

4,000

8,000

12,000

20212020201920182017201620152014

Baseline EPB - 5Y AAGRHigh EPB - 5Y AAGR

Baseline EPB - volumeHigh EPB - volume

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Naphtha outlook in limbo amid shifting crude, chemical markets

IHS Quarterly | Q4-2014 | 9

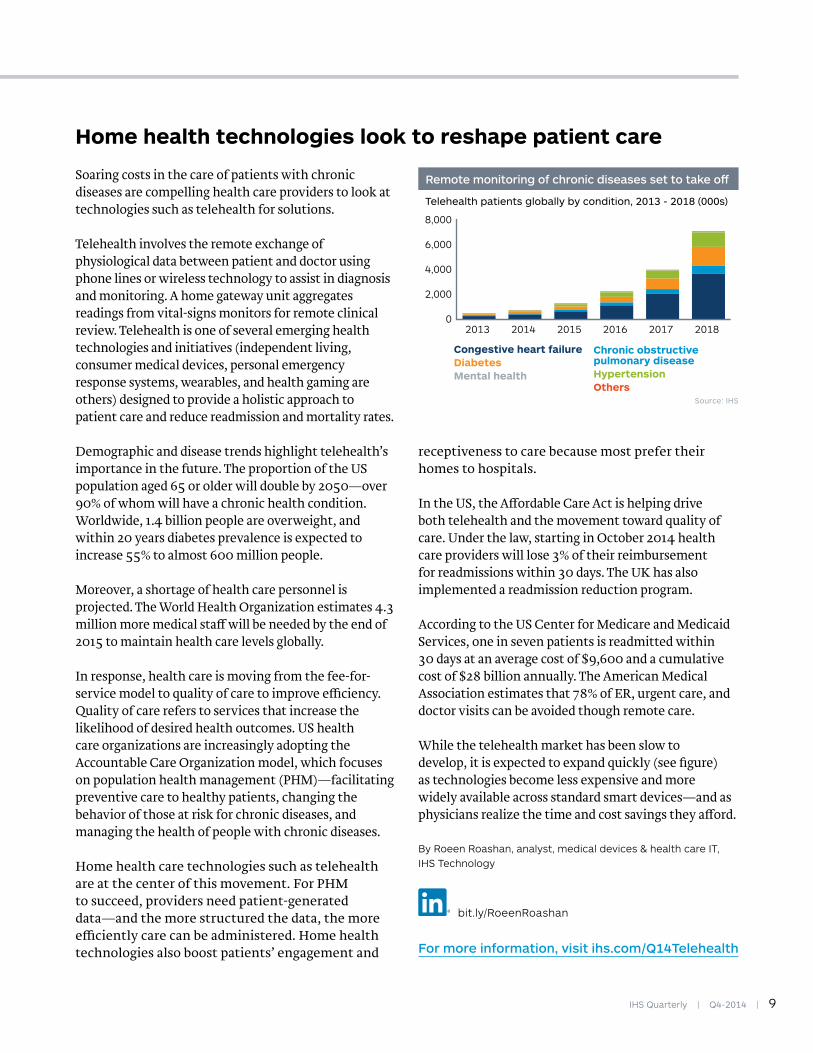

Soaring costs in the care of patients with chronic diseases are compelling health care providers to look at technologies such as telehealth for solutions.

Telehealth involves the remote exchange of physiological data between patient and doctor using phone lines or wireless technology to assist in diagnosis and monitoring. A home gateway unit aggregates readings from vital-signs monitors for remote clinical review. Telehealth is one of several emerging health technologies and initiatives (independent living, consumer medical devices, personal emergency response systems, wearables, and health gaming are others) designed to provide a holistic approach to patient care and reduce readmission and mortality rates.

Demographic and disease trends highlight telehealth’s importance in the future. The proportion of the US population aged 65 or older will double by 2050—over 90% of whom will have a chronic health condition. Worldwide, 1.4 billion people are overweight, and within 20 years diabetes prevalence is expected to increase 55% to almost 600 million people.

Moreover, a shortage of health care personnel is projected. The World Health Organization estimates 4.3 million more medical sta© will be needed by the end of 2015 to maintain health care levels globally.

In response, health care is moving from the fee-for-service model to quality of care to improve e¡ciency. Quality of care refers to services that increase the likelihood of desired health outcomes. US health care organizations are increasingly adopting the Accountable Care Organization model, which focuses on population health management (PHM)—facilitating preventive care to healthy patients, changing the behavior of those at risk for chronic diseases, and managing the health of people with chronic diseases.

Home health care technologies such as telehealth are at the center of this movement. For PHM to succeed, providers need patient-generated data—and the more structured the data, the more e¡ciently care can be administered. Home health technologies also boost patients’ engagement and

receptiveness to care because most prefer their homes to hospitals.

In the US, the A©ordable Care Act is helping drive both telehealth and the movement toward quality of care. Under the law, starting in October 2014 health care providers will lose 3% of their reimbursement for readmissions within 30 days. The UK has also implemented a readmission reduction program.

According to the US Center for Medicare and Medicaid Services, one in seven patients is readmitted within 30 days at an average cost of $9,600 and a cumulative cost of $28 billion annually. The American Medical Association estimates that 78% of ER, urgent care, and doctor visits can be avoided though remote care.

While the telehealth market has been slow to develop, it is expected to expand quickly (see figure) as technologies become less expensive and more widely available across standard smart devices—and as physicians realize the time and cost savings they a©ord.

By Roeen Roashan, analyst, medical devices & health care IT, IHS Technology

bit.ly/RoeenRoashan

For more information, visit ihs.com/Q14Telehealth

Telehealth patients globally by condition, 2013 - 2018 (000s)

Remote monitoring of chronic diseases set to take o�

0

2,000

4,000

6,000

8,000

201820172016201520142013

Source: IHS

Chronic obstructive pulmonary diseaseHypertensionOthers

Congestive heart failureDiabetesMental health

Home health technologies look to reshape patient care

10 | IHS Quarterly | Q4-2014

INSIGHTS

Among the consequences of emerging countries’ growing share of the global defense procurement market has been an accompanying rise in their use of o©sets in the award of defense contracts. Twenty-six countries have introduced formal o©set programs since 2000, bringing to 80 the number of governments imposing some form of obligation in kind on defense contractors from whom they purchase equipment.

O©sets are direct or indirect compensation intended to counter the financial burden of a defense purchase incurred by the acquiring government. And as emerging markets’ procurement budgets grow, they increasingly are leveraging their position to demand o©sets—often tied to economic growth objectives.

As o©set programs proliferate and their conditions grow more demanding, so grows the burden on defense contractors. And as purchasers’ thresholds—the minimum contract size that commands an o©set—remain static, the inflation-adjusted size of such contracts shrinks, squeezing defense suppliers’ profits.

O©sets may be direct (relating directly to the main procurement program through sub-contracting), semi-direct (relating to analogous military domains but not the actual procurement program), or indirect (typically completely unrelated programs, often in civilian areas). Inevitably, they incorporate one or more of the following features: program joint development, direct investment/facilitation of investment, technology transfer, placement of contracts with the buyer’s national industrial base, export/sales facilitation, or sub-contracting/work share.

The benefits of o©set for the procuring government are many and can include gaining access to technologies, improving foreign direct investment, easing trade imbalances, and countering foreign currency outflows.

O©sets can appear expensive—with the procuring government at times requesting o©sets equal to or greater than the value of the purchased equipment. In such cases, multipliers are typically used (e.g., $1 invested in, say, alternative energy earns an o©set credit of $10) to steer investment to priority areas.

While emerging markets have become more assertive in attaching o©sets to their defense contract awards, developed nations are moving in the opposite direction. The WTO’s Government Procurement Agreement prohibits o©set demands by members but allows them to be employed when deemed necessary to protect security interests. A 2011 EU directive contains a similar loophole.

The net e©ect is that, despite developed nations tightening rules on imposing o©sets in procurement deals, they are a booming business for emerging markets. IHS estimates o©set obligations of $94 billion will be negotiated between 2012 and 2022—with no slowing in sight.

Ultimately, the goal of some emerging nations is to build defense systems domestically—if not to become outright exporters in the future. Such a development would mean the loss of a portion of a very high-margin and profitable industry that has long been the province of the West.

By Guy Anderson, senior principal analyst, IHS Aerospace, Defense, and Security

bit.ly/GuyAnderson

For more information, visit ihs.com/Q14O�sets

O�set returns forecast to be accrued, 2012 - 2022

Defense o�sets: Big business for emerging markets

0 2 4 6 8 10 12 14

Colombia

Israel

South Korea

Taiwan

Canada

Turkey

India

United Arab Emirates

Saudi Arabia

Source: IHS

Obligation value (US$ billions)

Emerging countries drive a hard bargain in defense market

IHS Quarterly | Q4-2014 | 11

Escalating costs drive diminishing returns for oil companies

Despite higher crude prices, oil companies’ returns on average capital employed (ROACE) are lower now than in 2001, when prices were less than one-third their current level. That could spell trouble for companies that fail to enact cost containment measures or exercise greater discipline around the return on their capital investments—particularly if oil prices decline.

ROACE is a useful metric for analyzing the performance of businesses in capital-intensive industries, such as oil. Companies that produce higher profits from a given investment will have a higher ROACE than those that are not as e¡cient in converting capital into profit.

Analysis of performance and capital returns on 80 oil and gas companies by IHS Energy shows that, collectively, oil companies averaged an 11% ROACE in 2012 and 8.6% in 2013, both of which are weaker than the ROACE achieved in 2001 when the West Texas Intermediate (WTI) crude oil price hovered at just under $27 per barrel. The WTI crude oil price averaged $94 per barrel in 2012 and $98 per barrel in 2013.

While returns—net income (after-tax profits) adjusted for financing costs—increased by 400% from 2000 to 2012, capital employed rose 535% over the same period, squeezing margins. Returns actually outstripped the rate of increase in capital employed between 2004 and 2008 as oil prices surged. But earnings were slammed in 2009 by the collapse of commodity prices while the capital base continued to rise.

The culprit is cost escalation. In the upstream sector, which comprises the majority of business of the companies analyzed, lifting costs, or the cost of producing oil and gas after drilling is complete, have more than quadrupled since 2000 to more than $21 per barrel. Finding and developing costs have followed a similar trajectory, reaching nearly $22 per barrel of oil equivalent in 2013. Moreover, government fiscal take (based on financial disclosure) increased from 49% of pretax profits in 2000 to 60% in 2013.

Integrated oil companies have fared better than pure exploration and production (E&P) companies—earning a 15% ROACE since 2000 compared with 11%—which

is largely a function of their geographically and functionally diversified portfolios, more disciplined capital spending programs, and the lower cost basis of the legacy assets that comprise a large portion of their operations. Integrated oil companies have also grown their profits faster, up 350% since 2000 compared with a doubling by the E&Ps—attributable to their upstream portfolios generally being more oil weighted and less exposed to North American natural gas markets and their diversified asset base, which includes refining, midstream, and chemicals businesses that, on balance, have enjoyed good market fundamentals and profit margins in recent years.

Capital investment among oil companies is typically highest in times of rising crude prices. While WTI prices have climbed most of the way back from their 10-year lows of February 2009, ROACE has not followed. Companies that are not now paring back their capital investments prudently are likely to see ROACE diminished further if oil prices retreat.

By Nicholas Cacchione, director of energy equity research, IHS

bit.ly/NCacchione

For more information, visit ihs.com/Q14ROACE

Left scale: return on average capital employed (%) Right scale: price per barrel of West Texas Intermediate (US$)

Oil companies' ROACE sag while crude prices surge

0

5

10

15

20

25

2013e2011200920072005200320010

20

40

60

80

100

Source: IHS

Return on average capital employed (%)WTI price (US$/bbl)

12 | IHS Quarterly | Q4-2014

INSIGHTS

As enforcement of new emission regulations draws closer for the maritime industry, vessel operators are weighing their compliance options.

Beginning January 2015, the sulfur oxide (SOx) content of emissions from all vessels operating within emission control areas (ECAs), of which there are currently four—North America (including Hawaii), US Caribbean, North Sea, and Baltic Sea—will be required not to exceed 0.1%. The current 1% limit was set in 2010 under MARPOL Annex VI.

One option is to burn fuel with lower sulfur content, which is estimated to cost 70% more than the higher-sulfur fuel now used. For vessels already in service, however, the installation of “scrubbers,” SOx abatement systems, appears to be an attractive second option. With scrubbers in place, vessels will be able to operate on higher-sulfur fuel and remain compliant under the emission regulations.

While scrubbing technology has been employed in power generation and other industries for a number of years, it is relatively new to the maritime sector. On ships, scrubbers work on the principle of spraying seawater as mist into the exhaust gases to neutralize the acids. In an open-loop scrubber, the wastewater is discharged overboard, where the natural alkalinity of the seawater neutralizes the acidic discharge. In a closed-loop scrubber, the washwater is mixed with a strong alkaline (caustic), which reacts with the acidic (sulfur) particles. The waste is then stored on board in sludge tanks for later disposal onshore.

Hybrid scrubbers provide flexibility for ships to switch between open and closed loop, permitting zero discharge where local regulations prevent such actions. In Europe, ferry operator DFDS Seaways has led the way in installing this technology. The Tor Ficaria (later renamed Ficaria Seaways) was installed with a hybrid system developed by Aalborg Industries (now part of Alfa-Laval) in May 2009, which laid the foundation for a large-scale fleet investment. Thus far, 11 of the company’s vessels that service routes in the Baltic Sea and North Sea have been retrofitted with the system.

While DFDS’ decision is driven largely by the fact that its operations are almost entirely within ECA zones, other owners have been mulling the decision to install scrubbers to provide operational flexibility. Carnival Corporation has committed to retrofit over 70 of its vessels with scrubbers. The cruise ship giant will install a proprietary “compact” scrubber unit on vessels in its Princess Cruises, Cunard, Aida Cruises, Costa Crociere, and Holland America brands. This will enable its fleet to transit in and out of ECA areas without having to switch fuels.

Retrofitting a vessel with a scrubber can be done reasonably quickly—as little as 10 days in some cases—as the units can be preassembled before installation on board. While scrubbers add weight to a vessel, their ability to allow ships to run on cheaper fuel, for now, appears to be making them the compliance option of choice for cost-conscious maritime operators.

By Krispen Atkinson, principal analyst, IHS Maritime & Trade

bit.ly/KrispenAtkinson

For more information, visit ihs.com/Q14Scrubbers

Number of vessels, by category, that have scrubbers installed to meet new emissions requirements

Cruise ships account for almost half of all vessels now outfitted with SO scrubbers

Source: IHS

Cruise ship 69

Ro-ro cargo ship 31

Tanker 12

Bulk carrier 11

LPG tanker 6

Dry cargo ship 5

Ferry 5

Vehicles carrier 4

Container ship 2

x

Scrubbers gain favor as shipowners gird for SOx regulations

IHS Quarterly | Q4-2014 | 13

Will customer-sited, grid-connected batteries eliminate the need for construction of new power plants to meet peak electricity demand? Utilities in some of the most densely populated US corridors are experimenting to see if batteries could play such a role, encouraging customers to install behind-the-meter storage to serve as capacity to help shave peak demand loads.

In February 2014, New York utility Consolidated Edison introduced a demand management program that includes incentives of $2,100/kW for battery storage systems sited on customer premises that charge during o© hours and discharge during peak periods. The initiative followed the largest request for proposal for storage resources to date: Southern California Edison’s 2013 call for at least 50 MW of storage capacity, primarily for the Los Angeles area. Both moves were prompted by regulators’ reliability concerns amid the looming closure of nuclear power plants.

Faced with growing regulatory and cost restrictions a©ecting their siting of peaking units—particularly in urban areas—utilities are increasingly considering storage for incremental capacity needs. With steadily improving cost and e¡ciency, batteries are becoming a promising option in these high-density service areas. In ConEd’s case, IHS estimates its storage incentive is roughly equal to the New York Independent System Operator’s estimated “cost of new entry” for a gas peaking unit.

ConEd’s program is attracting project developers whose core business models are predicated on developing, owning, and operating behind-the-meter storage. These companies are following the path of early movers in the distributed solar PV industry: leveraging state incentives, targeting commercial and industrial (C&I) customers, o©ering financing, and streamlining installation processes.

To make project economics work, developers are banking on a combination of utility incentives and customer savings on peak demand charges, which can account for over one-third of C&I customers’ electricity costs. By identifying customers with especially “peaky” load and carefully sizing their battery o©erings,

developers are signing contracts with a variety of customers to provide peak load management.

Will such programs reduce peak demand as intended? Their e¡cacy is limited by the number of customers with a su¡ciently peaky load profile and, more significantly, the limited value non-coincident peak-shaving—i.e., load reductions not coordinated by the utility—provides the system. Nonetheless, as battery costs continue to fall, storage will become more attractive to shave peak load. IHS estimates that the market opportunity for battery storage in New York City could grow to 1 GW—10% of peak demand—if total unsubsidized battery project costs fall 75% from current levels to below $150/kWh.

Perhaps more important, ConEd now joins similar programs in California, Germany, and Japan in establishing a growing global storage market opportunity that will provide greater certainty for battery manufacturers, component suppliers, and system integrators to continue investing in the research and development of kW-scale storage products.

By Andy Lubershane, senior analyst, IHS Emerging Energy Research

bit.ly/ALubershane

For more information, visit ihs.com/Q14Utilities

Potential peak load savings (MW) in New York City in 2020 under various battery-price scenarios (US$ per kWh)

Peak demand shaving crests as battery costs approach $150/kWh

0

200

400

600

800

1,000

$500-1,000

$200-300

$150-200

$100-150

<$100>$1,000

Source: IHS

US utilities test business case for behind-the-meter storage

14 | IHS Quarterly | Q4-2014

INSIGHTS

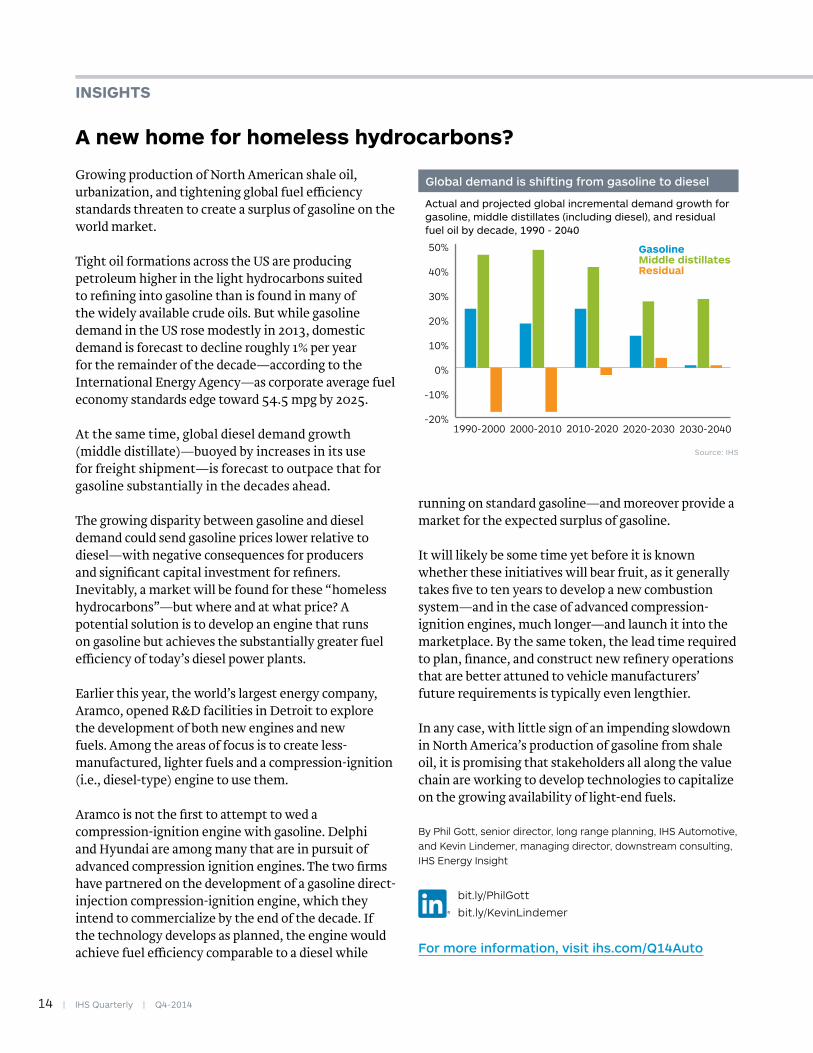

Growing production of North American shale oil, urbanization, and tightening global fuel e¡ciency standards threaten to create a surplus of gasoline on the world market.

Tight oil formations across the US are producing petroleum higher in the light hydrocarbons suited to refining into gasoline than is found in many of the widely available crude oils. But while gasoline demand in the US rose modestly in 2013, domestic demand is forecast to decline roughly 1% per year for the remainder of the decade—according to the International Energy Agency—as corporate average fuel economy standards edge toward 54.5 mpg by 2025.

At the same time, global diesel demand growth (middle distillate)—buoyed by increases in its use for freight shipment—is forecast to outpace that for gasoline substantially in the decades ahead.

The growing disparity between gasoline and diesel demand could send gasoline prices lower relative to diesel—with negative consequences for producers and significant capital investment for refiners. Inevitably, a market will be found for these “homeless hydrocarbons”—but where and at what price? A potential solution is to develop an engine that runs on gasoline but achieves the substantially greater fuel e¡ciency of today’s diesel power plants.

Earlier this year, the world’s largest energy company, Aramco, opened R&D facilities in Detroit to explore the development of both new engines and new fuels. Among the areas of focus is to create less-manufactured, lighter fuels and a compression-ignition (i.e., diesel-type) engine to use them.

Aramco is not the first to attempt to wed a compression-ignition engine with gasoline. Delphi and Hyundai are among many that are in pursuit of advanced compression ignition engines. The two firms have partnered on the development of a gasoline direct-injection compression-ignition engine, which they intend to commercialize by the end of the decade. If the technology develops as planned, the engine would achieve fuel e¡ciency comparable to a diesel while

running on standard gasoline—and moreover provide a market for the expected surplus of gasoline.

It will likely be some time yet before it is known whether these initiatives will bear fruit, as it generally takes five to ten years to develop a new combustion system—and in the case of advanced compression-ignition engines, much longer—and launch it into the marketplace. By the same token, the lead time required to plan, finance, and construct new refinery operations that are better attuned to vehicle manufacturers’ future requirements is typically even lengthier.

In any case, with little sign of an impending slowdown in North America’s production of gasoline from shale oil, it is promising that stakeholders all along the value chain are working to develop technologies to capitalize on the growing availability of light-end fuels.

By Phil Gott, senior director, long range planning, IHS Automotive, and Kevin Lindemer, managing director, downstream consulting, IHS Energy Insight

bit.ly/PhilGott

bit.ly/KevinLindemer

For more information, visit ihs.com/Q14Auto

Actual and projected global incremental demand growth for gasoline, middle distillates (including diesel), and residual fuel oil by decade, 1990 - 2040

Global demand is shifting from gasoline to diesel

-20%

-10%

0%

10%

20%

30%

40%

50%

1990-2000 2000-2010 2030-20402020-20302010-2020

Source: IHS

GasolineMiddle distillatesResidual

A new home for homeless hydrocarbons?

IHS Quarterly | Q4-2014 | 15

China’s recent crackdown on the importation of contaminated scrap has served warning to US and European recyclers that they will have to improve their processing facilities or turn elsewhere for their waste disposal.

For years, China has been the global leader in scrap recycling—importing up to 70% of the world’s post-consumer plastic waste alone. For China, the plastics provide a ready, low-cost resin supply for the country’s thriving manufacturing sector. Exporting countries, for their part, can divert a portion of their waste that might otherwise be landfilled or incinerated. Shipowners have benefitted as well, as the very container ships used to haul manufactured goods from China can be refilled with scrap for the return passage.

In 2013, however, China enacted the “Green Fence Initiative,” carrying out intensive inspections of scrap shipments at its ports for contamination—including insects, food, and medical and animal waste—as well as improperly mixed scrap. In some instances, shippers have been charged fees for the added inspection time, while in others their scrap bales have been denied entry entirely.

The driving factors behind China’s enforcement of regulations that actually date to 1996 are to reduce environmental degradation and customs corruption. Mixed plastic and film bales are under particular scrutiny, as Chinese recyclers buy #3 to #7 plastics in mixed bales seeking polypropylene content (#4 and #5) and discard PVC (#3), polystyrene (#6), dirty film, and other resins (#7) in the country’s bloated and increasingly toxic landfills.

The situation leaves many municipalities—particularly in the United States—in a bind. China’s ready acceptance of municipal waste has meant that many communities have neglected to develop their own recycling infrastructure to reprocess the ever-increasing volumes of plastic scrap. The proportion of US plastics waste that is landfilled today stands at 75-80%.

Western Europe has a more advanced plastic-recycling infrastructure, with more than 35% of

plastic scrap used for energy recovery and an overall plastics reclamation rate (i.e., including recycling) above 60%. Additionally, as European manufacturers face comparatively high polyethylene production expenses, there is a relatively healthy market for the use of recycled plastic as a feedstock in place of virgin chemicals.

With requirements to ship cleaner and more segregated plastic waste, scrap recyclers face new pressures to improve their collection and sorting processes—a challenge made more costly and di¡cult by the unrelenting introduction of new plastic packaging materials with unique compositions tailored to provide superior performance for specific applications.

By Jim Glauser, specialty chemicals analyst, IHS Chemical

bit.ly/JimGlauser

For more information, visit ihs.com/Q14Recycling

China’s ‘green fence’ pressures recyclers to upgrade operations

0

2

4

6

8

10

12

14

2014*201320122011

Chinese imports of plastic scrap, 2011 - 2014 (millions of metric tons)

Fencing out unwanted waste

Source: IHS*Estimated

ChinaHong Kong

16 | IHS Quarterly | Q4-2014

0

13

26

39

52

65

78

91

104

117

130

Ethylene

Propylene

Methanol

United StatesSaudi ArabiaChina

Source: IHS

0

12

24

36

48

60

72

84

96

108

120

0

12

24

36

48

60

72

84

96

108

120

United StatesSaudi ArabiaChina

0

35

70

105

140

175

210

245

280

315

350

Saudi ArabiaUSChinaWorld

0

35

70

105

140

175

210

245

280

315

350

Saudi ArabiaUSChinaWorld

0

35

-35

70

105

140

175

210

245

280

315

350

0

13

26

39

52

65

78

91

104

117

130

United StatesSaudi ArabiaChina

GLOBAL PRODUCTION TREND

GLOBAL PRODUCTION TREND

0

13

26

39

52

65

78

91

104

117

130

ET

HY

LEN

EP

RO

PY

LEN

EM

ET

HA

NO

L

ETHYLENE

PROPYLENE

METHANOL Chlorine

Benzene

WorldChina

US Saudi Arabia

CAPACITY UTILIZATION RATES IN 2020

Global production of ethylene, propylene, and methanol in 2020 is projected to be 385 million metric tons, while global capacity will reach 478 million metric tons, resulting in a utilization rate of 81%.

CHINA IS DRIVING GLOBAL CHEMICAL DEMAND

From relative obscurity in 2000, China’s demand for the three basic chemicals has grown rapidly and is forecast to account for 39% of global demand by 2020, making it the largest consumer of chemicals in the world by a significant margin. The Middle East & Africa, and South America, have seen strong growth as well. (Percent growth of equivalent demand for the three basic chemicals by region, 2000 to 2020. Equivalent demand includes net trade of chemical derivatives)

WHERE CAPACITY IS BEING ADDED

China, the US, and Saudi Arabia account for 63% of the projected 283 million metric tons in global chemical capacity investment for the three basic chemicals between 2000 and 2020. China dominates at 45% of the total as it strives to reduce dependence on imports. The US is a distant second at 10%, trailed by Saudi Arabia at 8.5%. (Millions of metric tons added, 2000 to 2020)

0 100 200 300 400 500 600 700 800

0 40 80 120 160 2000.0 40.4 80.8 121.2 161.6 202.0

503350

2000 2010 2020ethylene propylene methanol

50

117

76

32

95

49

0

10

20

30

40

50

60

70

80

90

100

GLOBAL PRODUCTION TREND

WHAT CHEMICALS ARE MADE FROM

Feedstocks are changing around the world. China is investing in coal and methanol-to-olefins technology; the US is tapping cheap domestic ethane from natural gas; and high-cost crude oil is causing a decline in the use of naphtha. (Feedstocks as a percent of total production for 2000 (inside ring), 2010 (middle ring), and 2020 (outside ring))

BIG INVESTMENTS IN CAPACITY

Global capacity of the three basic chemicals is expected to more thandouble between 2000 and 2020. (Global production trend line in millions of metric tons for 2000, 2010, and 2020. Bar chart is global capacity in millions of metric tons for 2000 and 2020)

Chemicals on the moveThe next five years will see accelerated growth in the global supply of three key chemical building blocks—ethylene, propylene, and methanol—as advantaged feedstock availability drives significant investment in China, the United States, and Saudi Arabia. What these chemicals will be made from, where they will be produced, and where they will be consumed are all in motion. China dominates all categories of growth, playing a significant role in determining future market conditions for the industry.

ANALYTICS

ETHYLENE

89%PROPYLENE

82%METHANOL

67%

250%

Europe

29

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

NaphthaEthanePropaneButaneCoal to olefinsGas oilMethanol to olefinsOthers

Steam crackersFCC splittersDehydroCoal to olefinsMetathesisHS FCCMethanol to olefinsCoal to propyleneOlefin crackingOthers on-purpose

Natural gasHeavy liquidsCoal to methanolOther

2000

2020

98194

2000

2020

60142

2000

2020

37142

0

50

100

150

200

250

300

350

400

China

579Middle

East & Africa

246South

America

113

World

125

Asia (excluding China)

102North

America

7

91

173

122

utilization rate

81%

IHS Quarterly | Q4-2014 | 17

0

13

26

39

52

65

78

91

104

117

130

Ethylene

Propylene

Methanol

United StatesSaudi ArabiaChina

Source: IHS

0

12

24

36

48

60

72

84

96

108

120

0

12

24

36

48

60

72

84

96

108

120

United StatesSaudi ArabiaChina

0

35

70

105

140

175

210

245

280

315

350

Saudi ArabiaUSChinaWorld

0

35

70

105

140

175

210

245

280

315

350

Saudi ArabiaUSChinaWorld

0

35

-35

70

105

140

175

210

245

280

315

350

0

13

26

39

52

65

78

91

104

117

130

United StatesSaudi ArabiaChina

GLOBAL PRODUCTION TREND

GLOBAL PRODUCTION TREND

0

13

26

39

52

65

78

91

104

117

130

ET

HY

LEN

EP

RO

PY

LEN

EM

ET

HA

NO

L

ETHYLENE

PROPYLENE

METHANOL Chlorine

Benzene

WorldChina

US Saudi Arabia

CAPACITY UTILIZATION RATES IN 2020

Global production of ethylene, propylene, and methanol in 2020 is projected to be 385 million metric tons, while global capacity will reach 478 million metric tons, resulting in a utilization rate of 81%.

CHINA IS DRIVING GLOBAL CHEMICAL DEMAND

From relative obscurity in 2000, China’s demand for the three basic chemicals has grown rapidly and is forecast to account for 39% of global demand by 2020, making it the largest consumer of chemicals in the world by a significant margin. The Middle East & Africa, and South America, have seen strong growth as well. (Percent growth of equivalent demand for the three basic chemicals by region, 2000 to 2020. Equivalent demand includes net trade of chemical derivatives)

WHERE CAPACITY IS BEING ADDED

China, the US, and Saudi Arabia account for 63% of the projected 283 million metric tons in global chemical capacity investment for the three basic chemicals between 2000 and 2020. China dominates at 45% of the total as it strives to reduce dependence on imports. The US is a distant second at 10%, trailed by Saudi Arabia at 8.5%. (Millions of metric tons added, 2000 to 2020)

0 100 200 300 400 500 600 700 800

0 40 80 120 160 2000.0 40.4 80.8 121.2 161.6 202.0

503350

2000 2010 2020ethylene propylene methanol

50

117

76

32

95

49

0

10

20

30

40

50

60

70

80

90

100

GLOBAL PRODUCTION TREND

WHAT CHEMICALS ARE MADE FROM

Feedstocks are changing around the world. China is investing in coal and methanol-to-olefins technology; the US is tapping cheap domestic ethane from natural gas; and high-cost crude oil is causing a decline in the use of naphtha. (Feedstocks as a percent of total production for 2000 (inside ring), 2010 (middle ring), and 2020 (outside ring))

BIG INVESTMENTS IN CAPACITY

Global capacity of the three basic chemicals is expected to more thandouble between 2000 and 2020. (Global production trend line in millions of metric tons for 2000, 2010, and 2020. Bar chart is global capacity in millions of metric tons for 2000 and 2020)

Chemicals on the moveThe next five years will see accelerated growth in the global supply of three key chemical building blocks—ethylene, propylene, and methanol—as advantaged feedstock availability drives significant investment in China, the United States, and Saudi Arabia. What these chemicals will be made from, where they will be produced, and where they will be consumed are all in motion. China dominates all categories of growth, playing a significant role in determining future market conditions for the industry.

ANALYTICS

ETHYLENE

89%PROPYLENE

82%METHANOL

67%

250%

Europe

29

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

NaphthaEthanePropaneButaneCoal to olefinsGas oilMethanol to olefinsOthers

Steam crackersFCC splittersDehydroCoal to olefinsMetathesisHS FCCMethanol to olefinsCoal to propyleneOlefin crackingOthers on-purpose

Natural gasHeavy liquidsCoal to methanolOther

2000

2020

98194

2000

2020

60142

2000

2020

37142

0

50

100

150

200

250

300

350

400

China

579Middle

East & Africa

246South

America

113

World

125

Asia (excluding China)

102North

America

7

91

173

122

utilization rate

81%

18 | IHS Quarterly | Q4-2014

When macroeconomicsand global supply chains collidePopulation dynamics, geopolitics, income flows, and shifts in production and

consumption around the world influence global trade and directly a�ect the supply

chains that are its lifeblood. A nuanced understanding of the interaction of these

macro-phenomena and their long-term implications provides an edge that global

corporations need to stay competitive.

By Chris G. Christopher, Jr. and David Deull

Sh

utt

erst

ock

IHS Quarterly | Q4-2014 | 19

G lobal trade and its many supply chains are continually subject to shifts in economic conditions, geopolitical regimes, and

demographics. Anticipating these changes is essential for companies that depend on their supply chains to adapt and thrive. Several global macroeconomic and demographic trends have emerged recently that are a©ecting trade flows and have the potential to disrupt those supply chains.

Chief among them is the slowdown of emerging market growth. A number of emerging markets have experienced a rapid deterioration in their economic performance over the last few years. There are four reasons for this slowdown. First, the hyper-globalization of the last 20 years is over, replaced by a more modest and perhaps sustainable growth path. Second, the related surge in commodity prices, known as the commodity super cycle, has come to an end for now. Third, emerging markets no longer have access to credit at historically low rates. And fourth, global trade liberalization has not made much progress recently.

As a consequence, life for supply chain executives is becoming more complicated. Easy opportunities for cost savings in sourcing materials and labor, and rapid growth in new emerging markets, are harder to come by. Growth will be more incremental in the future and depend on closely monitoring economic and political trends to identify new sourcing and demand opportunities.

20 | IHS Quarterly | Q4-2014

The emerging market slowdownMuch has been made of the extraordinary growth of emerging markets—in particular, the BRIC countries (Brazil, Russia, India, and China) during the 2000s—as US and European companies en masse moved manufacturing operations overseas. But during these boom years, many emerging markets failed to institute the necessary structural reforms that would enable them to transition to a slower but more sustainable and stable pace of economic growth.

China is still maintaining relatively strong growth—last year real GDP growth was 7.7% and this year it is projected to be approximately 7.5%—but Brazil, Russia, and India have all entered economic slowdowns. Russia is closely tied to the ups and downs of oil markets and now is being impacted by Western sanctions. India faces a much slower GDP growth rate due to declining fixed investment and factor productivity. Brazil’s real GDP growth for 2013 was just 2.5%. The country slipped into recession in the first half of 2014 due to declining investment, the end of the commodity super cycle, and a slowdown in private sector consumption.

As the pace of growth slows for these economies, the biggest impact is felt by the new middle class and the still high number of households living in poverty, which devote a significant proportion of their income to food, housing, and other daily necessities.

India’s annual GDP per capita is about $1,500, compared to $6,800 in China and $54,000 in the US. As a result, a national economic slowdown would have a greater impact on the average Indian family’s quality of life than the average American or even Chinese family. As growth slows in countries with low personal income per household or low GDP per capita, it feels like a recession.

The result is slowing demand growth for non-essential consumer goods, which will likely continue and perhaps worsen if structural changes are not addressed. If global companies fail to understand the causes of the slowdown in emerging markets and do not correctly forecast the implications, it will adversely impact their businesses. For frontline companies serving these markets, that means a hit to sales and an increase in finished goods inventory.

Further up the supply chain—distributors, wholesalers, manufacturers, and component and materials

suppliers—the consequences can be amplified, a phenomenon commonly referred to as the “bull-whip e©ect.” That is, as the shock wave of the slowdown ripples back through the supply chain, the impact on sales, inventory, and manufacturing operations grows.

Western markets strugglingDeveloped markets are struggling in their own ways. Real GDP growth in the US averaged 3.2% annually between 1980 and 2007. Since the end of the Great Recession in June 2009, the recovery has been anemic, with real GDP growth averaging 2.2% annually. As a consequence, real median household income has been flat for two years and is now 8% below the 2007 level.

In the European Union, the recovery has been hampered by the two-tiered growth performance of the northern and southern countries. The north is relatively stable economically, while the south is slowly digging out of a deep economic hole. Income inequality between the two tiers is rising.

Declining real median household income, elevated poverty rates, and the rise of income inequality in both the US and Europe have caused a bifurcation of consumer spending patterns. Luxury and discount stores are doing well, while the middle-tier retailers are having a hard time regaining traction.

The combination of the slowdown in emerging markets and stagnation of US and Western European economic performance has slowed world trade growth. While IHS expects global real GDP growth to accelerate in 2014 and 2015, globalization—defined as the share of world imports as a percentage of global GDP—is not expected to follow suit. Instead, globalization will hover around 30%, where it has been since 2010 (see figure above).

World imports as a percent of GDP

Long-term growth in world trade is expected to flatten out

20

25

30

35

40

1997 2002 2007 2012 2017 2022Source: IHS

Supply and demand balancingIn 2014, China’s GDP is expected to represent 13% of global GDP, while the US will account for almost a quarter. However, by 2024 China and the US are likely to be even at about 20% each, which is expected to balance global production more uniformly between East and West.

It is likely that US consumers will still claim the highest percentage share of global consumption for the next few years, but emerging market consumers are closing the gap. The rise of China’s consumer class is likely to propel its economy to a much greater share of global consumption over the next six to eight years, fueled by accumulating wealth and an increasing number of middle-income households. In fact, IHS expects consumption in the BRICs to surpass Western Europe by 2019 and the US by 2020.

On a per capita basis, China and other emerging markets have a long way to go to catch up with the advanced economies, but the signs of their increasing influence are clear. In 2004, Chinese consumers were responsible for only 4% of global consumer spending. By 2014, they are likely to account for 8% and, by 2024, 15%. This means that the Chinese consumer’s share of global private consumption will have increased by nearly a factor of four in two decades.

By contrast, American consumer spending is expected to decline from 33% of global GDP in 2004 to 28% in 2014 and to less than 20% a decade later. Consumer spending in Western Europe peaked in 2004 at nearly 18% and continues to decline. IHS predicts that by 2020, US and Western European consumer spending combined will account for only 24% of world GDP, down considerably from 38% in 2002. As the disparity

in production and consumption between emerging markets and the West diminishes, these levels will come into relative balance (see figure at left).

These changing international trade, production, and consumption patterns have several implications for global supply chain managers. First, the relative decrease in the US consumer’s importance to global trade will serve to reduce production volatility. As global producers become less reliant on one market, they will be able to spread market risk around the world in a more balanced way.

Second, the major trading blocs are becoming increasingly connected and their performance correlated. As retailers struggle for market share in the West, the growth of the middle classes in China and India has also slowed. A strategy that considers relative growth opportunities across multiple markets will enable global corporations to maximize their market opportunities.

Evidence of the relative importance of emerging markets abounds. Some computer manufacturers launch their products in emerging markets before the US. Some American automobile manufacturers have been introducing new models in Asia before they hit the US market. Even Hollywood has responded to the production and consumption balancing by releasing some films in emerging markets prior to their US launch.

Demography has spoken In the late 1970s and early 1980s, many demographers and economists were asking whether it would be possible to prevent the world’s population from reaching 25 billion by the end of the 21st century. Current estimates now project a world population of around 10 billion by 2050 with little increase thereafter. This slowing of the world’s population growth will lead to an uneven slowing in the global economy.

The reason for the population growth slowdown is falling fertility rates. Globally, women and families are choosing to have fewer children than in the past. This is because as a country urbanizes and industrializes, the need for large families to work the farm decreases. Approximately 70% of all nations have child-bearing rates below or approaching the replacement level in developed countries of 2.1 children per woman. Coupled with longer life expectancies, this e©ect is turning the traditional population pyramid on its head.

IHS Quarterly | Q4-2014 | 21

Domestic consumption as a share of world GDP (%)

As emerging markets mature, consumer spending rises to match Western countries

0

5

10

15

20

25

2000 2005 2010 2015 2020

Western EuropeUS

BRIC

Source: IHS

22 | IHS Quarterly | Q4-2014

Some regions are seeing a particularly strong aging e©ect (see figure above). In China, for example, the one-child policy, coupled with increasing urbanization, has taken a toll on population growth. In Japan, the working-age population has started to shrink because of the aging of the overall population. Since 2006, the number of deaths in Japan has outpaced the number of births. And in Central and Eastern Europe, population growth rates are close to 0% and expected to remain there for the foreseeable future.

Declining population growth and increased urbanization have implications for trade and supply chains as well. Increasing levels of urbanization and the emergence of megacities will require increased productivity of the food supply chain. They will also necessitate improvements in both intra- and inter-city logistics. This e©ect is pronounced in China, where increased urbanization and an aging population combine with a large and growing middle class.

In most developed countries, urbanization stabilized last century, but emerging markets are catching up. The global urbanization rate

surpassed 50% sometime between 2000 and 2004 (see figures at right).

Who’s next?Nations that show promise in terms of their end-use or sourcing potential are emerging. Chief among the contenders are Mexico and Vietnam.

Mexico’s increased competitiveness is helping the country regain its share of US imports at China’s expense. In 2001, China’s entry into the WTO caused a major shift in trade as China quickly outpaced Mexico in exports to the US. Between 2001 and 2005, Mexico’s share of US imports of manufactured goods fell from 12.1% to 10.4%, while China’s share rose from 11% to 19.2%. But Mexico staged a comeback in 2005. By 2009, China’s share of US manufactured goods imports leveled o© at around 26%, while Mexico’s share grew to 13% by 2013.

There are several reasons for Mexico’s rebound. First and foremost is its proximity to the US. The relatively stronger US recovery after the Great Recession benefited Mexico disproportionately. The relatively high cost of ocean shipping compared to that of an

China no longer has the cost advantage that made it the world’s manufacturer. There is growing concern about broader risks, such as civil instability, shadow banking, a real estate bubble, and military adventurism.

Compound annual average growth rate (%)

Regional population growth rates around the world are declining

Source: IHS

Sub-Saharan

Africa

Mideast&

N. Africa

OtherAsia-

Pacific

JapanEmergingEurope

WesternEurope

-1

0

1

2

31990–19992000–2009

2010–20192020–2029

NAFTA OtherAmericas

IHS Quarterly | Q4-2014 | 23

improved north-south transportation infrastructure between the US and Mexico was a contributing factor as well.

Mexico’s diligent observance of the principles of the 1992 North American Free Trade Agreement (NAFTA) and its adherence to international standards of intellectual property rights have also been factors. And as China’s middle class grows, wage inflation in its manufacturing sector is outpacing that of many competing emerging markets, including Mexico.

China can no longer boast the same cost advantages that allowed it to become a dominant player in global manufacturing. Not only are labor costs rising, but there is growing concern about broader macroeconomic and political risks, such as civil instability, shadow banking, a real estate bubble, and military adventurism. These factors have ignited a reassessment by Western companies of their reliance on China.

This concern is helping to drive growth in Vietnam, China’s southern neighbor. The country has been a member of the WTO since 2007 and its manufacturing wages are roughly half those paid in China. These advantages have triggered a recent surge in manufacturing foreign direct investment and led to a tenfold increase in the value of Vietnam’s merchandise exports since 2000, with shipments in 2014 expected to hit $150 billion.

The African continent, and especially the sub-Saharan region, has been another surprise winner as demographics shift. Improving social and economic fundamentals in many African nations have placed the continent on many multinationals’ radar screens. IHS forecasts that between 2013 and 2017, sub-Saharan

African economies are likely to outpace every major regional economic bloc except China in real GDP growth and projects that the region will lead the world in population growth.

All the social metrics are pointing in the right direction for Africa. Improving health outcomes and strengthening civil society are responsible for an improving development picture. HIV infections and infant mortality rates are falling, while life expectancies and enrollment rates for primary school all the way through college are on the rise. From the late 1980s to the early 1990s, few African nations were considered a democracy; today, the vast majority of the 55 African states enjoy some form of multi-party democracy.

The long arc of changing global production and consumption patterns should have generally positive implications for global supply chains. On the consumption side of the equation, a more regionally balanced demand for goods around the world reduces dependence on any one market and lowers overall supply chain risk. Likewise, on the production side, the emergence of viable regional manufacturing centers—in Asia, the Americas, Africa, and elsewhere—will distribute and perhaps minimize the risks for downstream manufacturers, distributors, suppliers, and other members of the global supply chain.

Chris G. Christopher, Jr. is director of US Macroeconomics and Global Consumer Markets, IHS Economics, and David Deull is a US economist, IHS Economics

bit.ly/ChrisChristopher

bit.ly/DavidDeull

For more information, visit ihs.com/Q14SupplyChain

Millions of urban dwellers

China leads the world in urban population…

0

200

400

600

800

2000 20202005 2010 2015

China

India

US

EU4*

Source: IHS*France, Germany, Italy, and UK

Percent of population that are urban dwellers

But the US and Europe lead in urban density

0%

20%

40%

60%

80%

100%

2000 20202005 2010 2015

China

India

US

EU4*

Source: IHS*France, Germany, Italy, and UK

24 | IHS Quarterly | Q4-2014

M ore people are giving thought to where their food comes from, and

there is perhaps no better example than seafood. With the power of global logistics, it is possible to enjoy fresh lobster, fish, shrimp, and other delicacies of the deep in a restaurant thousands of miles from the nearest coast. However, eco-conscious consumers increasingly want to know where their food originated and whether it was harvested in an environmentally sustainable fashion.

While seafood is a luxury for some, more than one billion people around the world rely on the oceans for their daily nutritional intake. Worldwide, an average of 17 kilograms (kg) of seafood is consumed per person annually, according to the United Nations

Food and Agriculture Organization (FAO), making marine wild-capture fisheries one of the most important human food and protein sources. FAO’s charter includes improving global maritime and environmental conditions.

However, these resources are being depleted rapidly due to poor management and overfishing. Globally, more than 30% of fishery catches are illegal, unreported, and unregulated (IUU). Black-market IUU activities undermine the economic and environmental sustainability of global fisheries and fish stocks and impact all countries.

Shining the light of transparencyA global e©ort is now under way to increase the transparency of the global fishing fleet to

reduce the environmental and economic impacts of IUU fishing activities. The primary focus is on establishing a global record of fishing, which would require a permanent unique vessel identifier (UVI) scheme like the 27-year-old United Nations International Maritime Organization (IMO) ship identification system that tracks the world’s large merchant vessels.

Under the IMO system, all seagoing merchant vessels of 100 gross tons or more, including container ships, tankers, bulk carriers, and cruise liners, are assigned and must display a seven-digit number throughout their service life, from the construction berth to the breaker’s yard. The number remains assigned to that vessel through changes in ownership, name, and flag state. Vessels identified in this

Reeling in

illegal fishing It is estimated that one-third of all fish caught on the high seas is done illegally.

Unregulated vessels that do not report their catches are a major contributor to

the depletion of fish stocks the world over—to the point that some species may

never recover. Global action to combat the crisis is now focusing on the

establishment of an identification scheme for fishing vessels.

By Alex Gray

IHS Quarterly | Q4-2014 | 25

Sh

uttersto

ck

manner can be tracked and monitored at sea and in port for regulatory and security oversight.

Originally established and maintained by Lloyd’s Register, the number issuance scheme is now administered for the IMO by IHS Maritime & Trade. It has been accepted as the best available global identification system because each number is connected with data about the vessel and managed by an independent third party that is held responsible for continually updating and verifying data against multiple sources.

Prior to 2014, fishing vessels were exempt from the requirement to be issued an IMO number. In 2013, the IMO General Assembly removed the exemption for fishing vessels of 100 gross tons or greater, e©ective in 2014. This means that IMO member states, regional fisheries management organizations (RFMOs), coastal states, and flag states could require an IMO number on fishing vessels in this class. This is the first step in establishing the IMO number as the fundamental building block for transparency of the international fishing fleet.

Top 20 fishing fleets of vessels 100 gross tons and larger by flag as of January 2014

Half the world's large fishing vessels are registered in four countries: US, Russia, South Korea, and Japan

0 700 1,400 2,100 2,800 3,500

AustraliaChile

MexicoIndonesia

FranceCanada

ArgentinaUnited Kingdom

PeruHondurasMoroccoNorway

PhilippinesChina

Chinese TaipeiSpainJapan

South KoreaRussia

United States

Source: IHS

Gross tonnage (total)No. of vessels

421,8991,390,187

698,266

248,426286,685

282,132286,127

147,941364,901142,420102,840133,560139,332162,525104,589111,75975,960

168,75149,792

82,036

Top 20 fishing fleets of vessels 1,000 gross tons and larger by ownership nation as of January 2014

Russia accounts for one-fifth of the world's super-sized fishing vessels

0 100 200 300 400

PhilippinesUkraine

PortugalGhana

CanadaDenmark

South AfricaChina

New ZealandFrance

NetherlandsUnited Kingdom

MexicoChile

United StatesSouth Korea

IcelandNorway

SpainRussia

Source: IHS

Gross tonnage (total)No. of vessels

158,290210,362