dartmouth college treasurers association

TRANSCRIPT

Dartmouth College Treasurers Association

2014 Annual Meeting Saturday, September 13, 2014

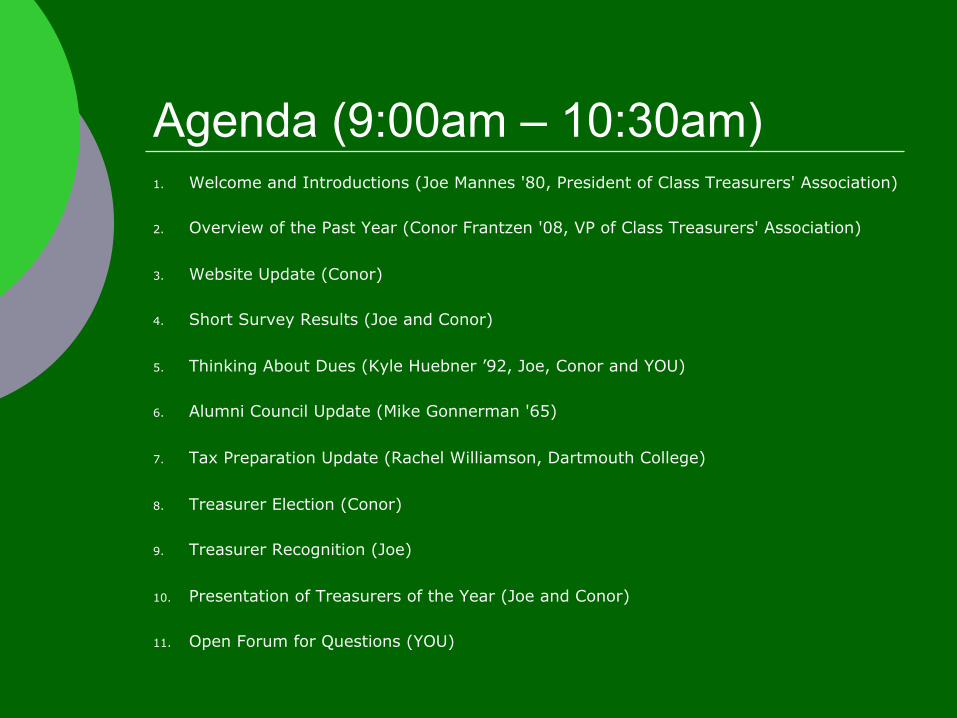

Agenda (9:00am – 10:30am) 1. Welcome and Introductions (Joe Mannes '80, President of Class Treasurers' Association)

2. Overview of the Past Year (Conor Frantzen '08, VP of Class Treasurers' Association)

3. Website Update (Conor)

4. Short Survey Results (Joe and Conor)

5. Thinking About Dues (Kyle Huebner ’92, Joe, Conor and YOU)

6. Alumni Council Update (Mike Gonnerman '65)

7. Tax Preparation Update (Rachel Williamson, Dartmouth College)

8. Treasurer Election (Conor)

9. Treasurer Recognition (Joe)

10. Presentation of Treasurers of the Year (Joe and Conor)

11. Open Forum for Questions (YOU)

1. Introductions

Jennifer Casey ’66a Director, Class Activities

Ann Harvey Class Dues Administrator

Joe Mannes ‘80 President, Treasurer’s Association

Conor Frantzen ‘08 Vice-President, Treasurer’s Association

Mike Gonnerman ‘65

Treasurer Representative to Alumni Council (2011-2014)

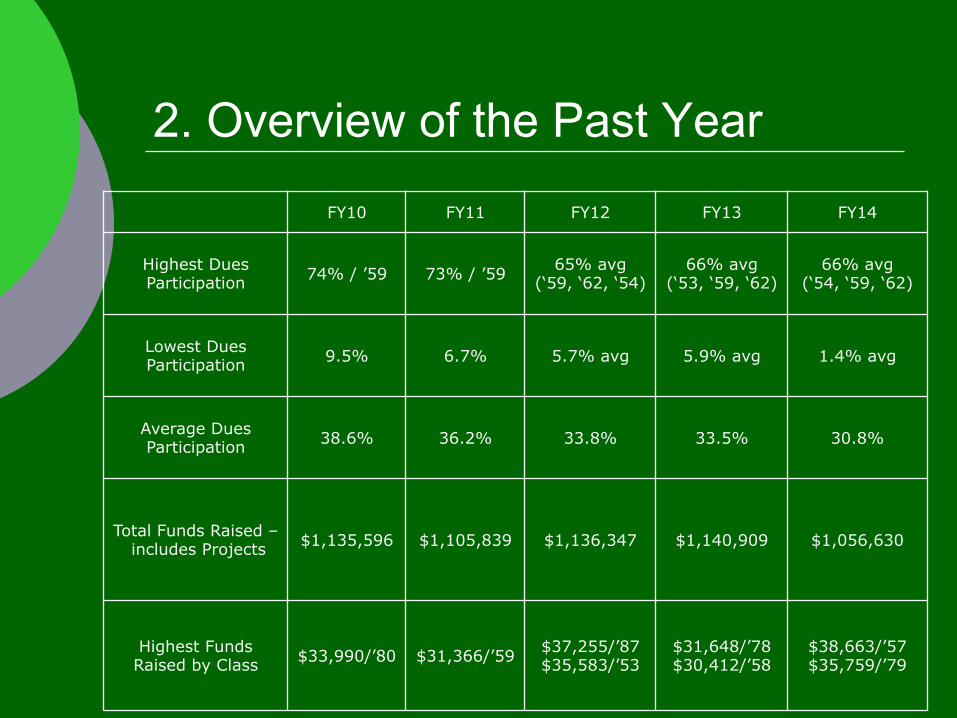

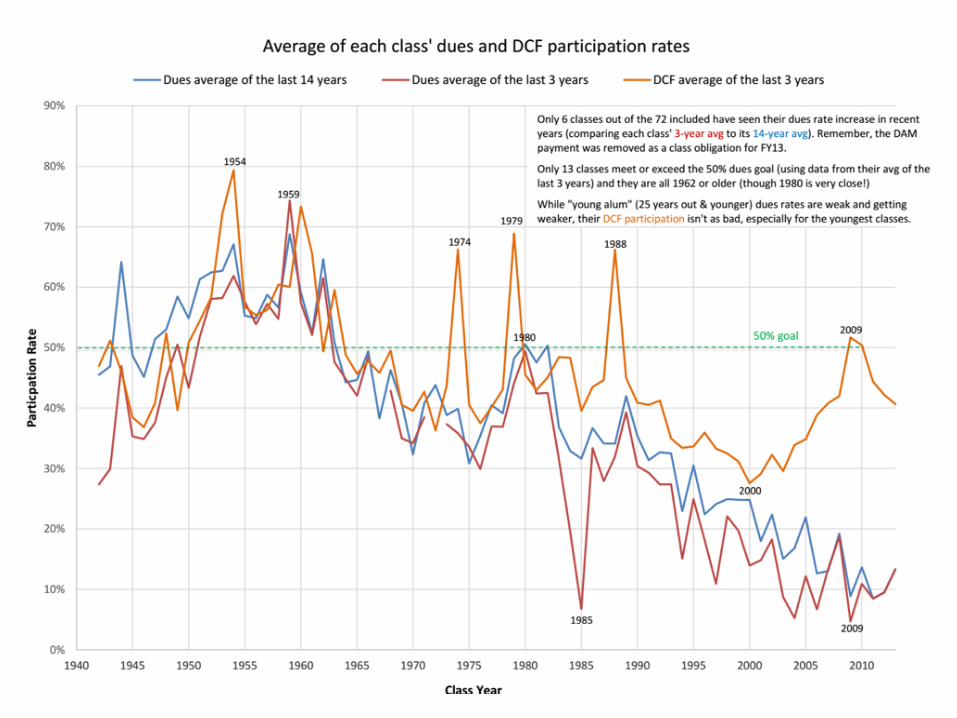

2. Overview of the Past Year

FY10 FY11 FY12 FY13 FY14

Highest Dues Participation 74% / ’59 73% / ’59 65% avg

(‘59, ‘62, ‘54) 66% avg

(‘53, ‘59, ‘62) 66% avg

(‘54, ‘59, ‘62)

Lowest Dues Participation 9.5% 6.7% 5.7% avg 5.9% avg 1.4% avg

Average Dues Participation 38.6% 36.2% 33.8% 33.5% 30.8%

Total Funds Raised – includes Projects $1,135,596 $1,105,839 $1,136,347 $1,140,909 $1,056,630

Highest Funds Raised by Class $33,990/’80 $31,366/’59 $37,255/’87

$35,583/’53 $31,648/’78 $30,412/’58

$38,663/’57 $35,759/’79

3. Website Update

¡ Class Treasurer’s website will be moving to a new URL with an iModules backend

¡ Same information, just slightly different look and location of some items

¡ Will continue to be the place to go to find answers to your questions!

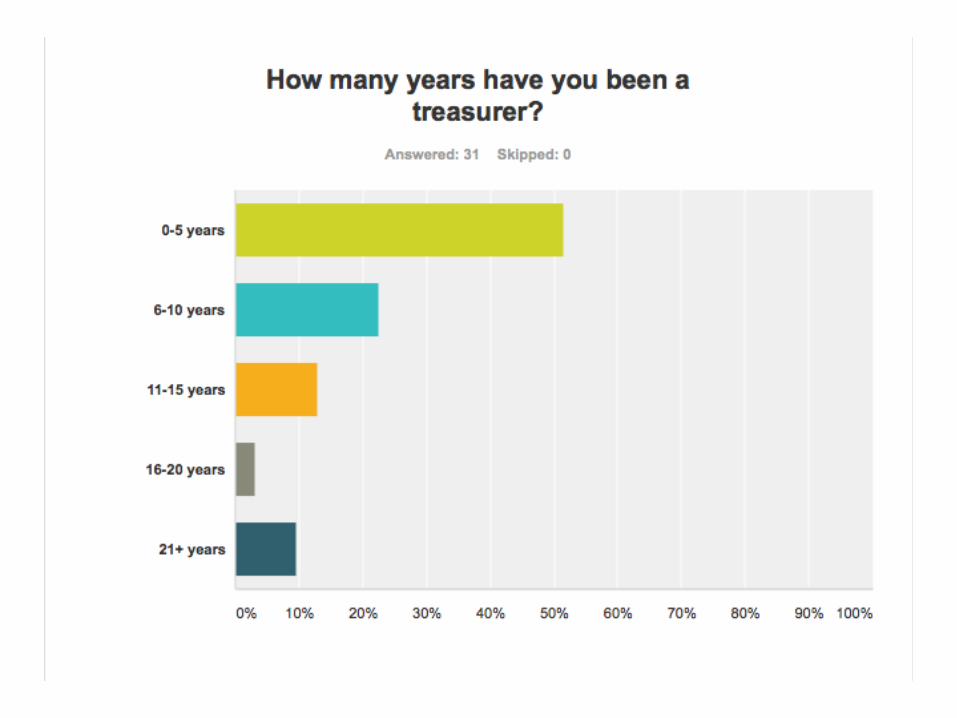

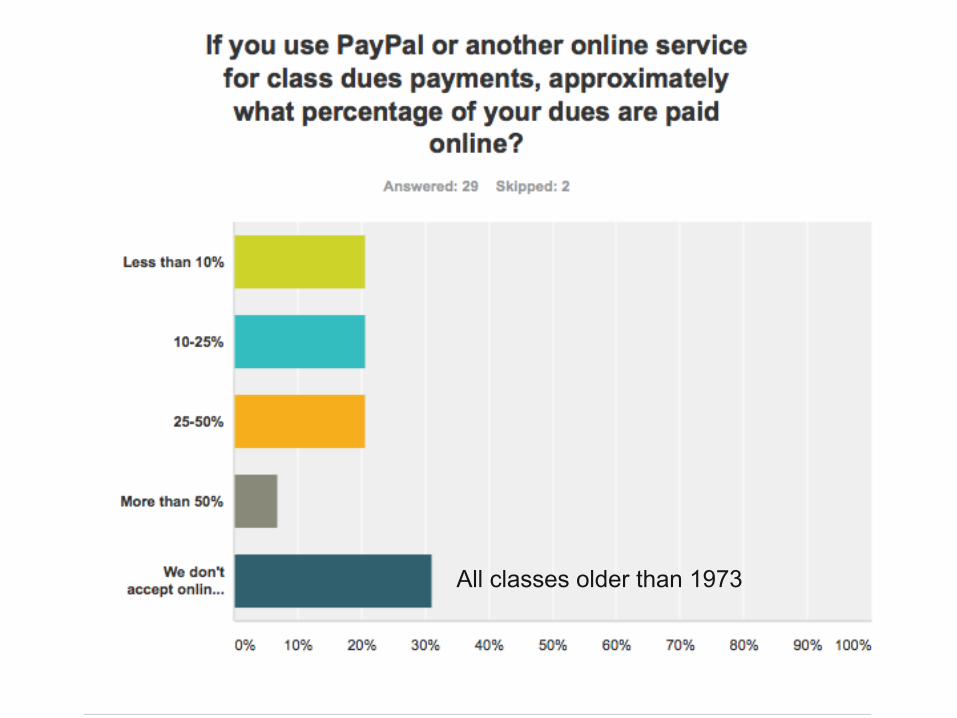

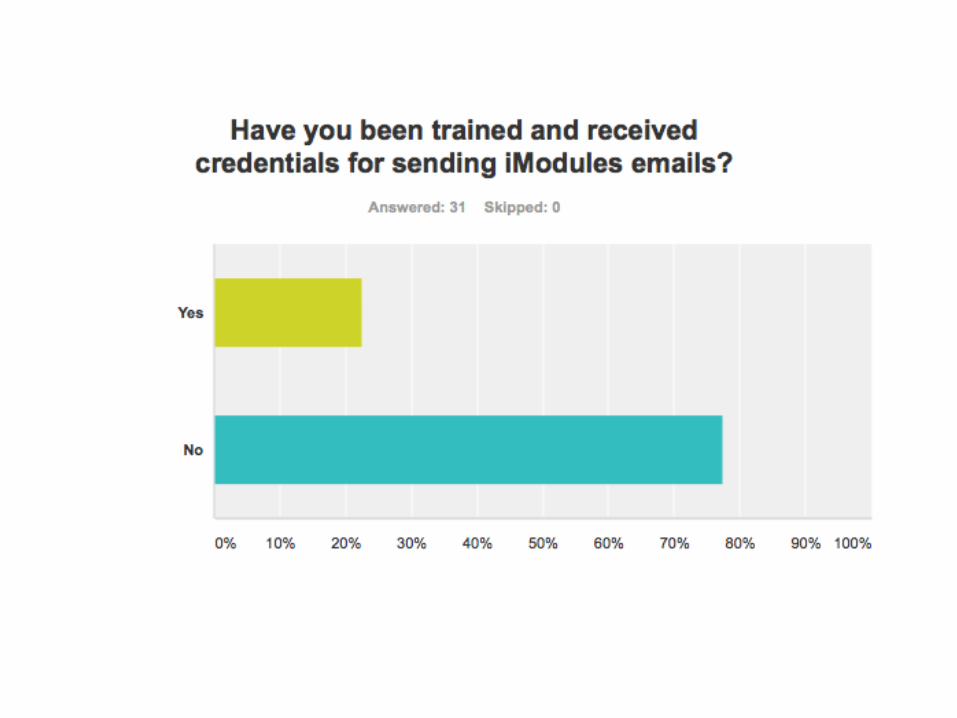

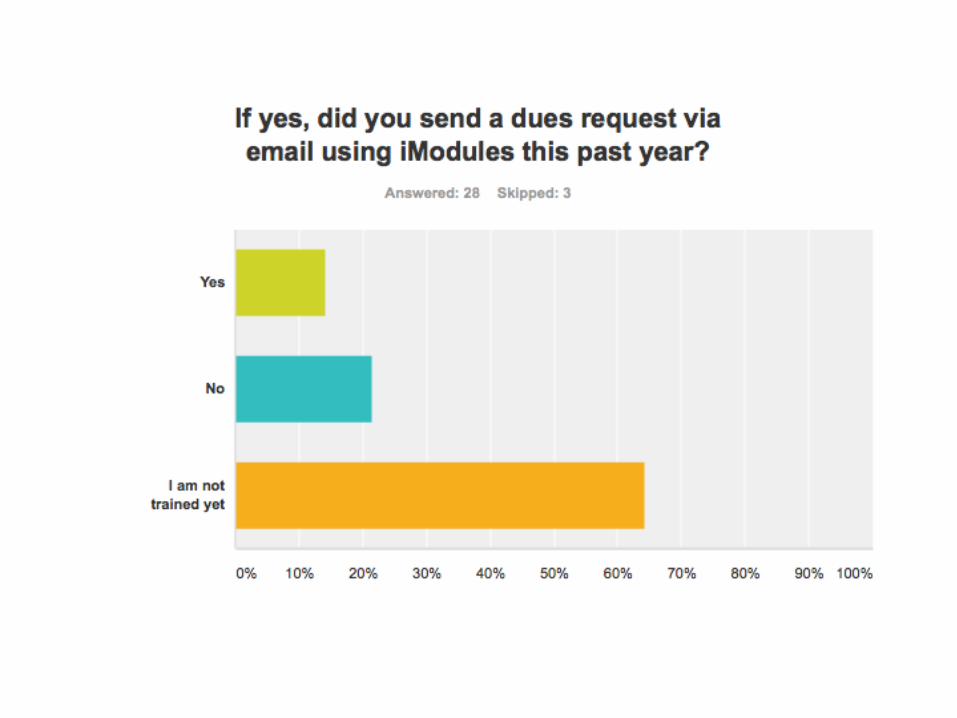

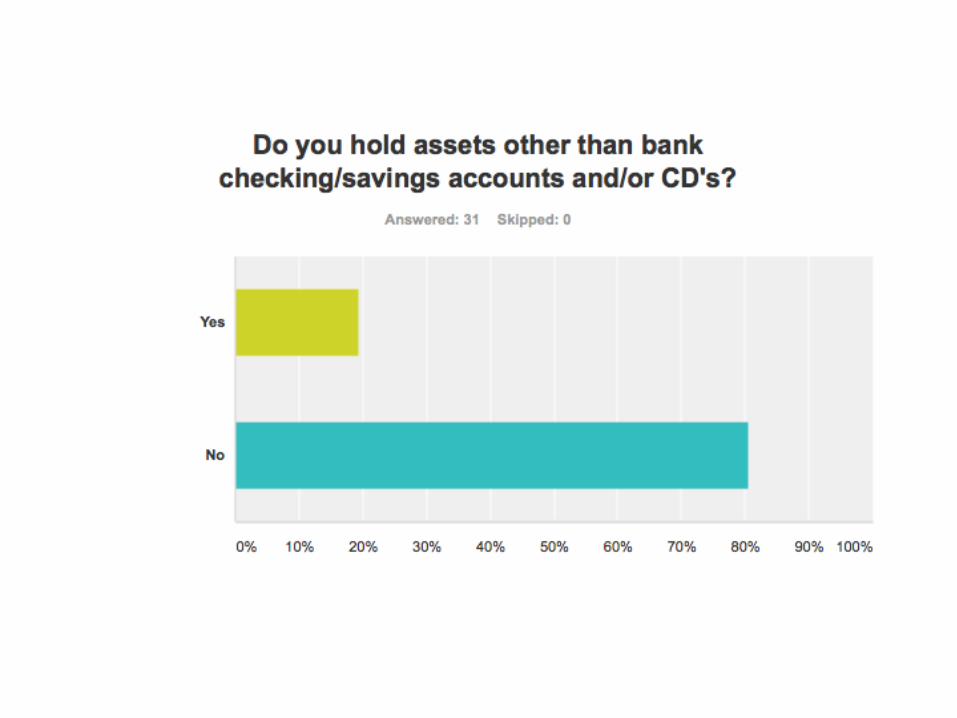

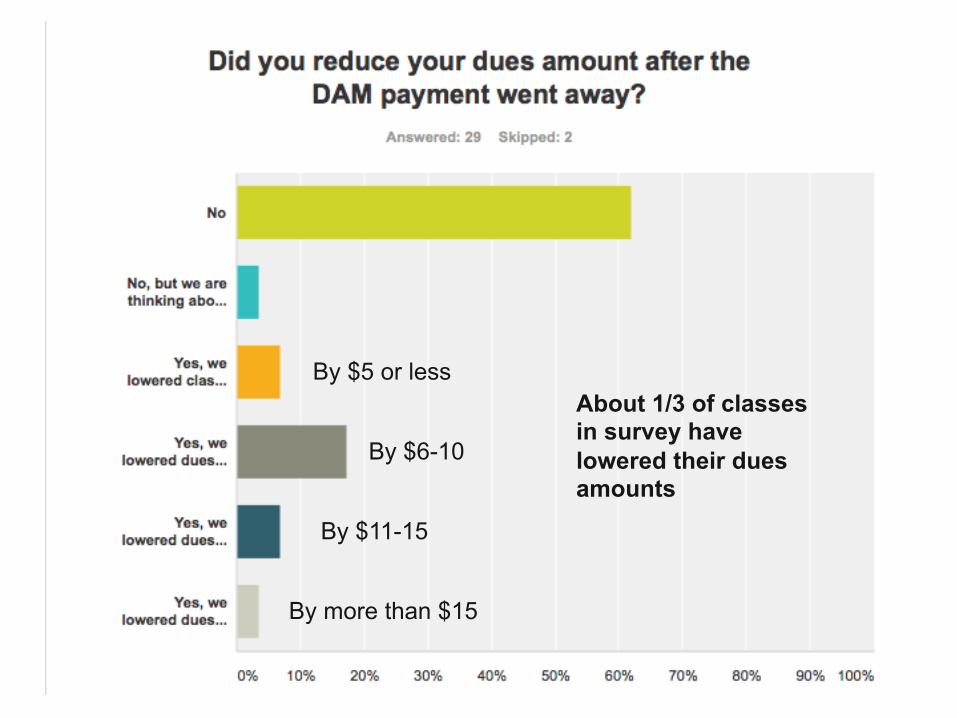

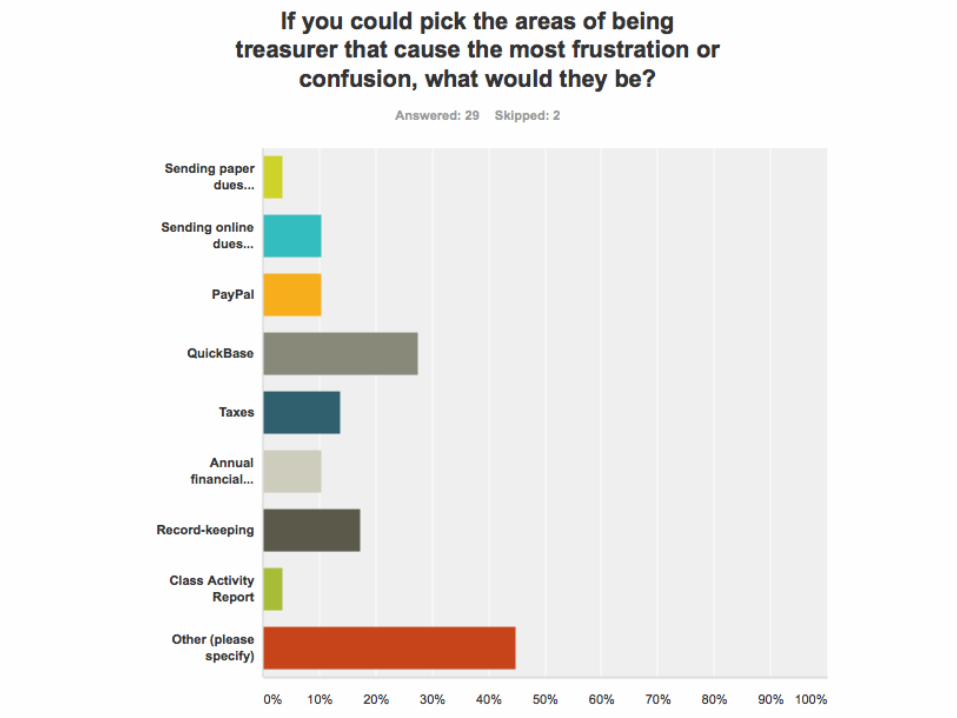

4. Survey Results

¡ 10 question survey ¡ 31 responses (over 45%) ¡ At least two replies from each decade

1950s-2000s

All classes older than 1973

1970s class

Two 1970s, one 1960s class

By $5 or less

By $6-10

By $11-15

By more than $15

About 1/3 of classes in survey have lowered their dues amounts

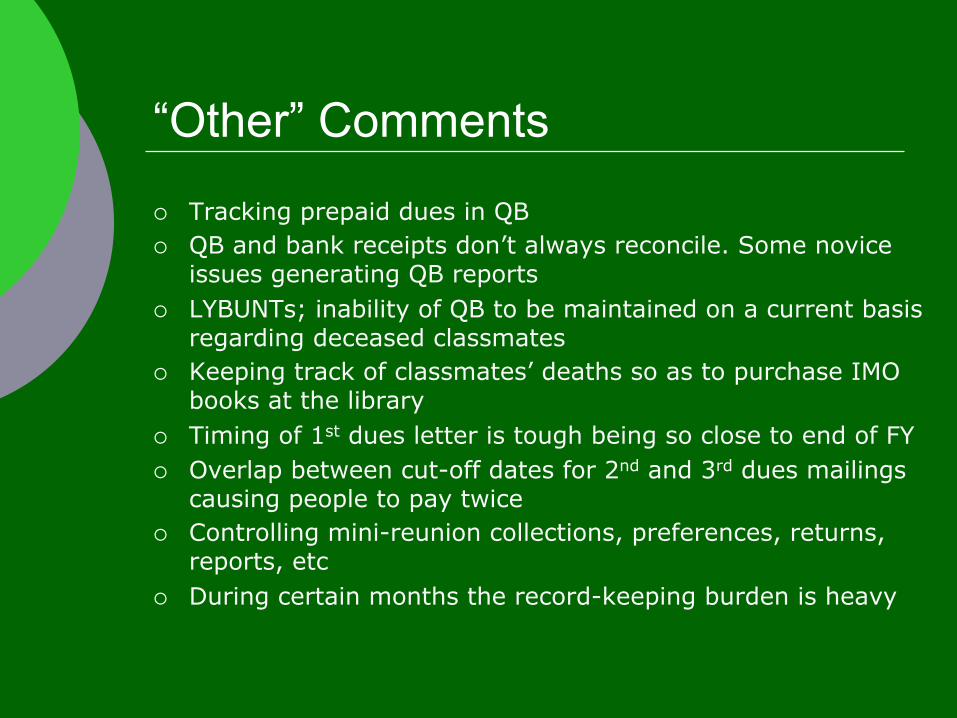

“Other” Comments

¡ Tracking prepaid dues in QB ¡ QB and bank receipts don’t always reconcile. Some novice

issues generating QB reports ¡ LYBUNTs; inability of QB to be maintained on a current basis

regarding deceased classmates ¡ Keeping track of classmates’ deaths so as to purchase IMO

books at the library ¡ Timing of 1st dues letter is tough being so close to end of FY ¡ Overlap between cut-off dates for 2nd and 3rd dues mailings

causing people to pay twice ¡ Controlling mini-reunion collections, preferences, returns,

reports, etc ¡ During certain months the record-keeping burden is heavy

5. Thinking about Class Dues

¡ In late July there was a conference call discussing the state of class dues

¡ Jennifer Casey ‘66a, Martha Beattie ‘76, Peter Pratt ‘71, Cathy Judd-Stein ‘82, Mike Gonnerman ‘65, Joe Mannes ‘80, Conor Frantzen ‘08, Kyle Huebner ‘92, David Plekenpol ‘82 and Dartmouth staff (Ann Harvey, Derrick Smith ‘07) were on the call

¡ Do we care that dues numbers are low? Do we change the marketing? What other paths might we suggest to classes?

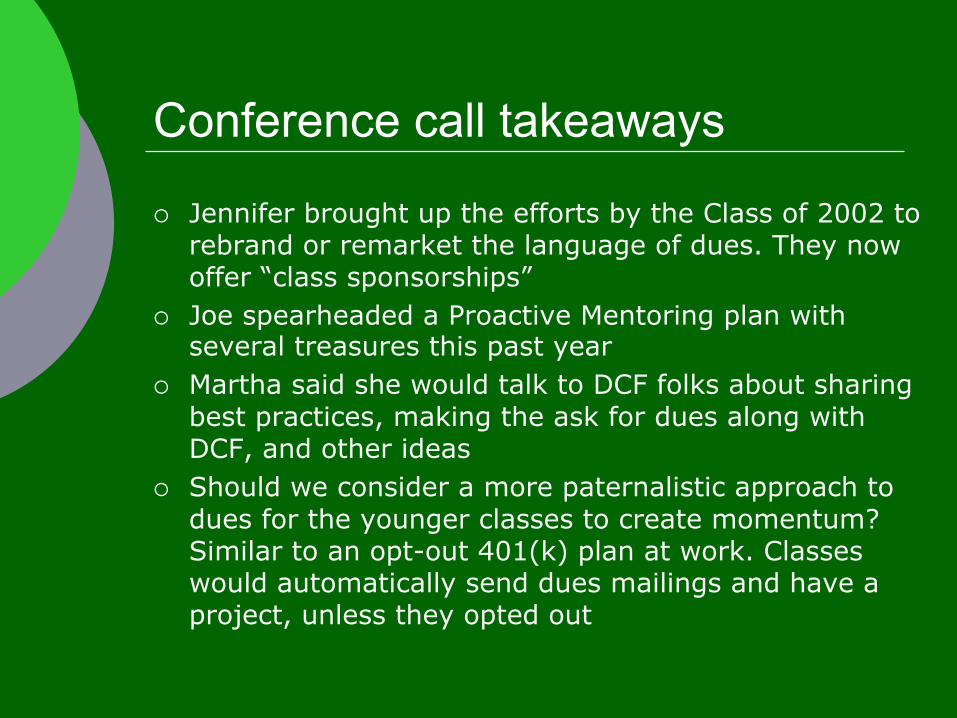

Conference call takeaways

¡ Jennifer brought up the efforts by the Class of 2002 to rebrand or remarket the language of dues. They now offer “class sponsorships”

¡ Joe spearheaded a Proactive Mentoring plan with several treasures this past year

¡ Martha said she would talk to DCF folks about sharing best practices, making the ask for dues along with DCF, and other ideas

¡ Should we consider a more paternalistic approach to dues for the younger classes to create momentum? Similar to an opt-out 401(k) plan at work. Classes would automatically send dues mailings and have a project, unless they opted out

6. Alumni Council Report

Mike Gonnerman ‘65

May 2014 Meeting

¡ Main theme -- extreme behavior on campus l Phil Hanlon comments l Councilors’ breakout sessions

¡ Significant presentations l Trustee Bill Burgess ‘81 l Dean of admissions Maria Laskaris ’81 l Abby d’Agostino l Nate Fick – alumni-nominated Trustee

October 2013 Meeting

¡ Student life focus ¡ Significant presentations

l Phil Hanlon kick-off l Rick Mills, CFO l Pam Peeden, Chief Investment Officer l AD Harry Sheehy l Dean Charlotte Johnson l Trustees Steve Mandel ’78 and Sherri

Oberg ‘82

Next Meeting -- October

¡ Joe Mannes to represent Treasurers

¡ THANK YOU

7. Tax Update for Alumni Classes

Rachel L. Williamson, CPA [email protected] [email protected] Joined Dartmouth College in June ‘13

Tax Update Agenda

¡ Maintaining Tax Exempt Status ¡ New in Fiscal 2014 ¡ Filing Requirements ¡ Filing Tips ¡ IRS Notices ¡ Financial Best Practices ¡ Questions

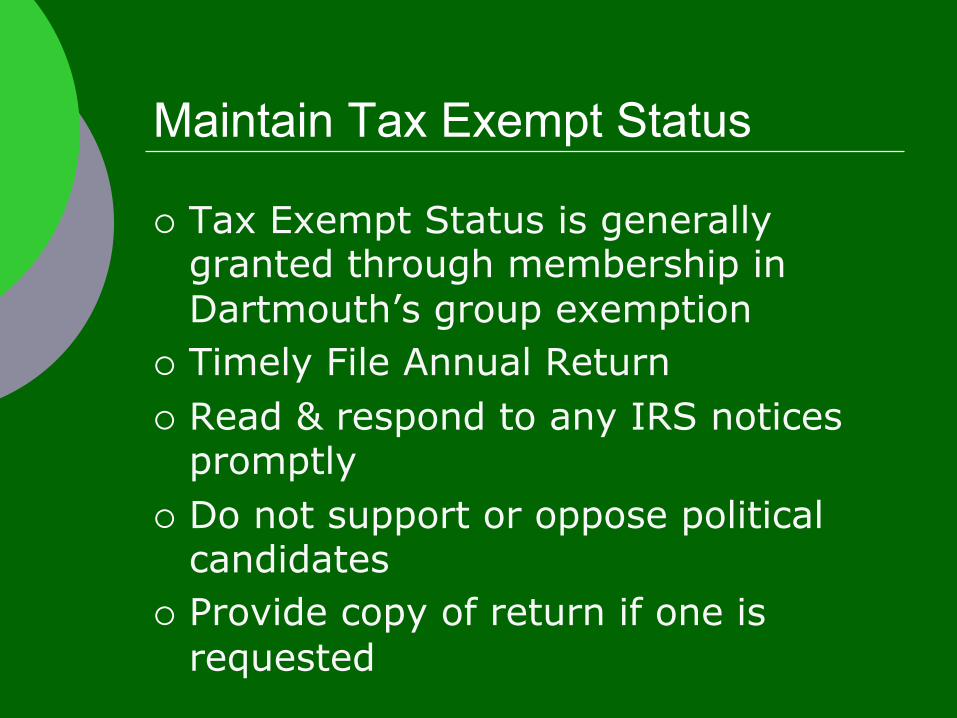

Maintain Tax Exempt Status

¡ Tax Exempt Status is generally granted through membership in Dartmouth’s group exemption

¡ Timely File Annual Return ¡ Read & respond to any IRS notices

promptly ¡ Do not support or oppose political

candidates ¡ Provide copy of return if one is

requested

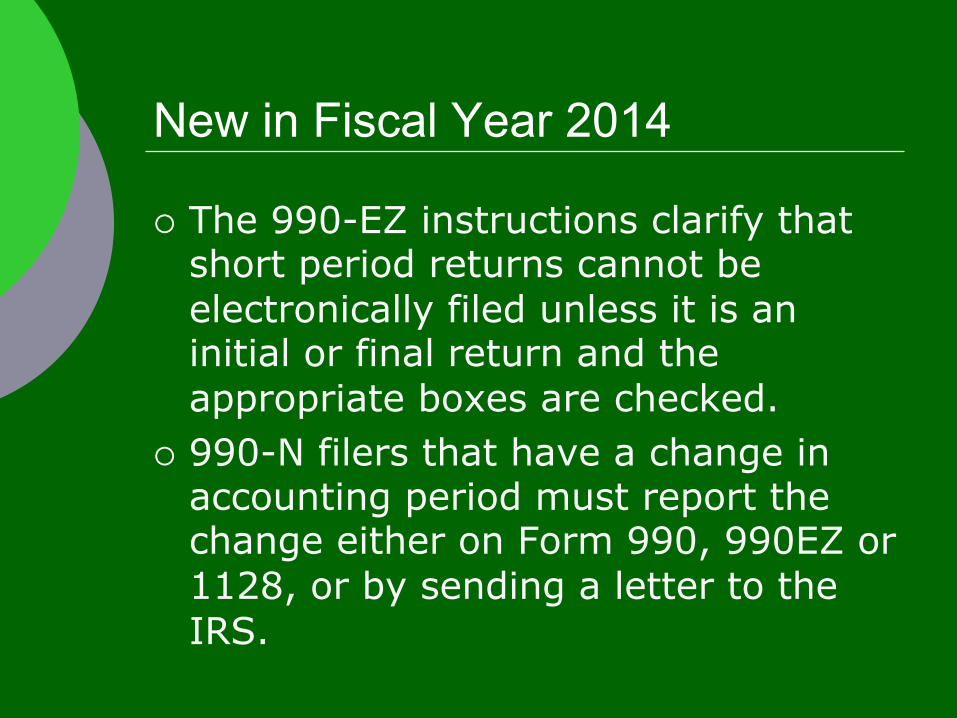

New in Fiscal Year 2014

¡ The 990-EZ instructions clarify that short period returns cannot be electronically filed unless it is an initial or final return and the appropriate boxes are checked.

¡ 990-N filers that have a change in accounting period must report the change either on Form 990, 990EZ or 1128, or by sending a letter to the IRS.

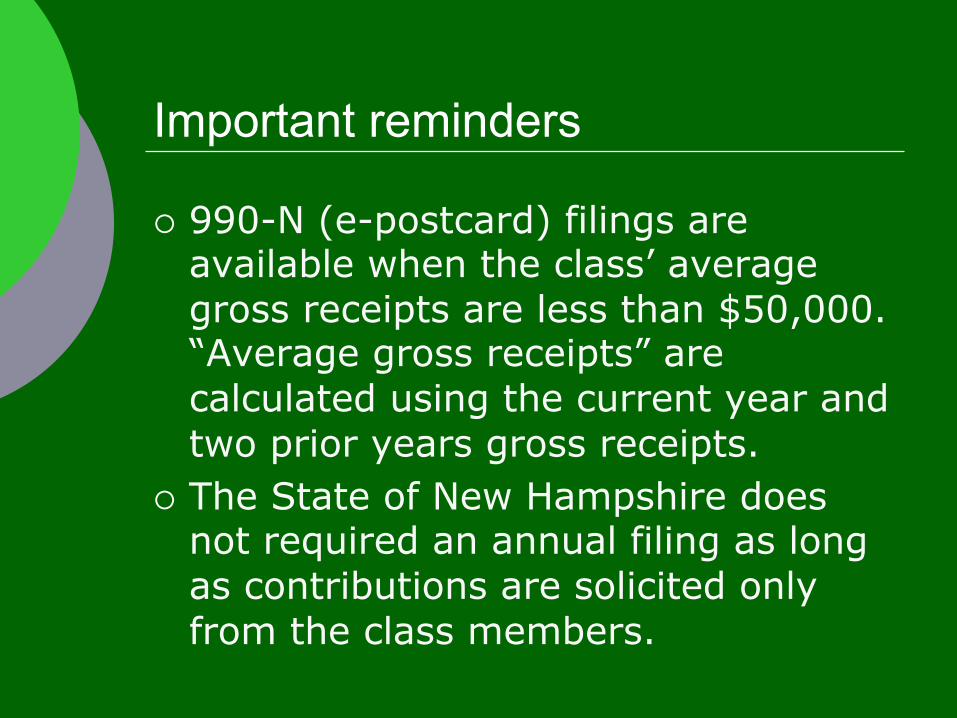

Important reminders

¡ 990-N (e-postcard) filings are available when the class’ average gross receipts are less than $50,000. “Average gross receipts” are calculated using the current year and two prior years gross receipts.

¡ The State of New Hampshire does not required an annual filing as long as contributions are solicited only from the class members.

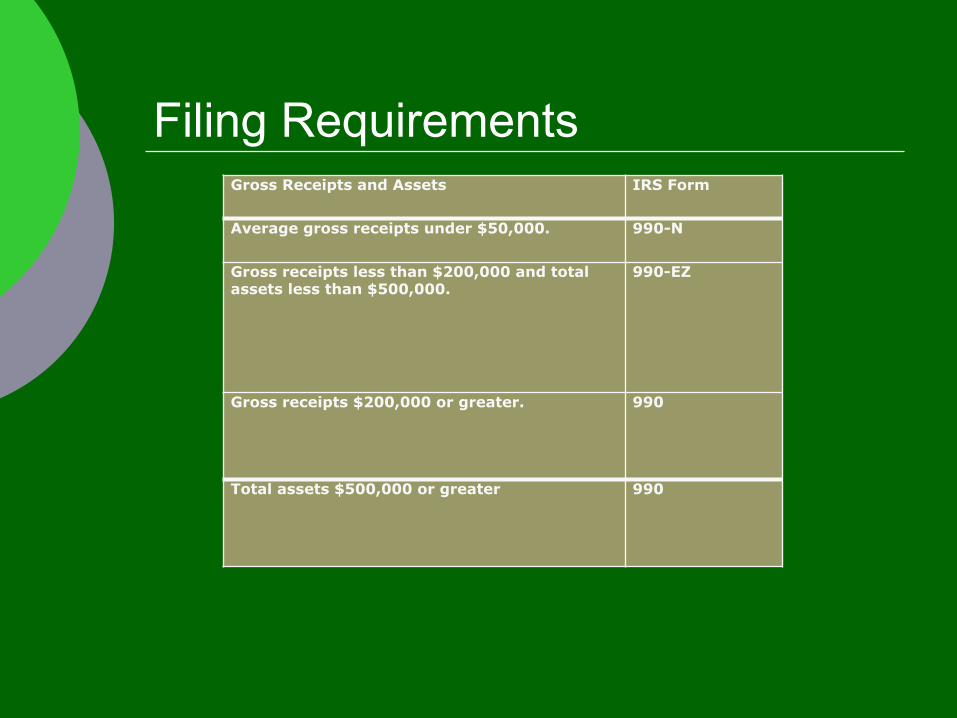

Filing Requirements

¡ Annual Federal Tax Filing is required to maintain tax exempt status

¡ Failure to file Form 990-EZ or Form 990 may result in fines of $20 per day past the due date to maximum of 5% of gross receipts.

¡ Failure to file for 3 consecutive years will result in loss of tax exempt status.

¡ Forms are due November 15, 2014. Extension can be filed on Form 8868 for 990 or 990-EZ filing.

¡ It is important to maintain accurate record of revenue and expenses to fulfill your fiduciary duty, document requirements for filing, and provide accurate reporting.

Filing Requirements Gross Receipts and Assets IRS Form

Average gross receipts under $50,000. 990-N

Gross receipts less than $200,000 and total assets less than $500,000.

990-EZ

Gross receipts $200,000 or greater. 990

Total assets $500,000 or greater 990

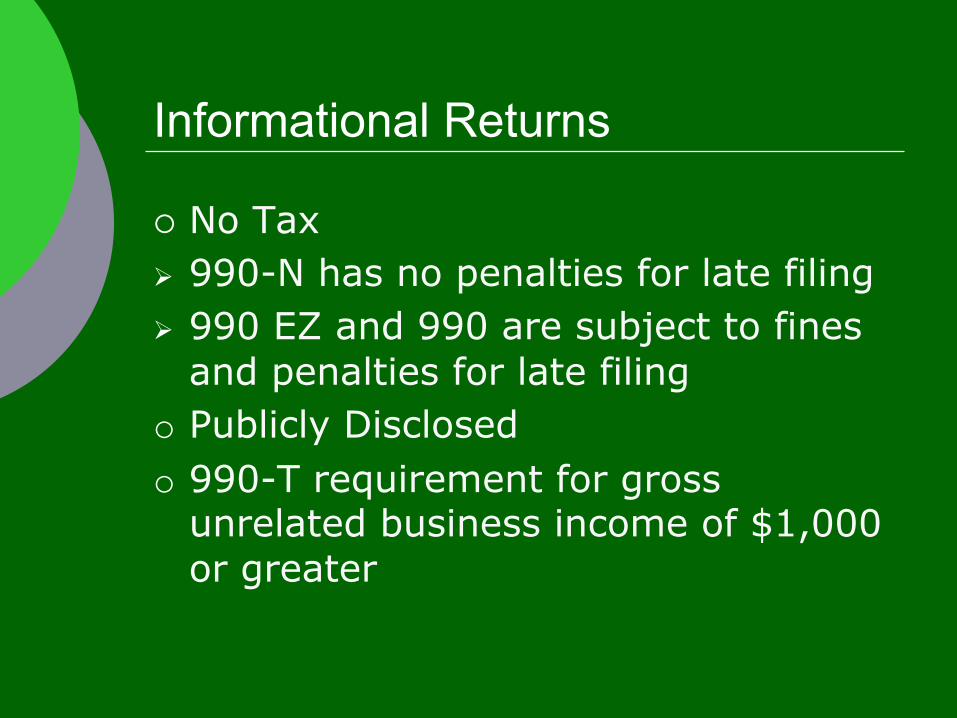

Informational Returns

¡ No Tax Ø 990-N has no penalties for late filing Ø 990 EZ and 990 are subject to fines

and penalties for late filing o Publicly Disclosed o 990-T requirement for gross

unrelated business income of $1,000 or greater

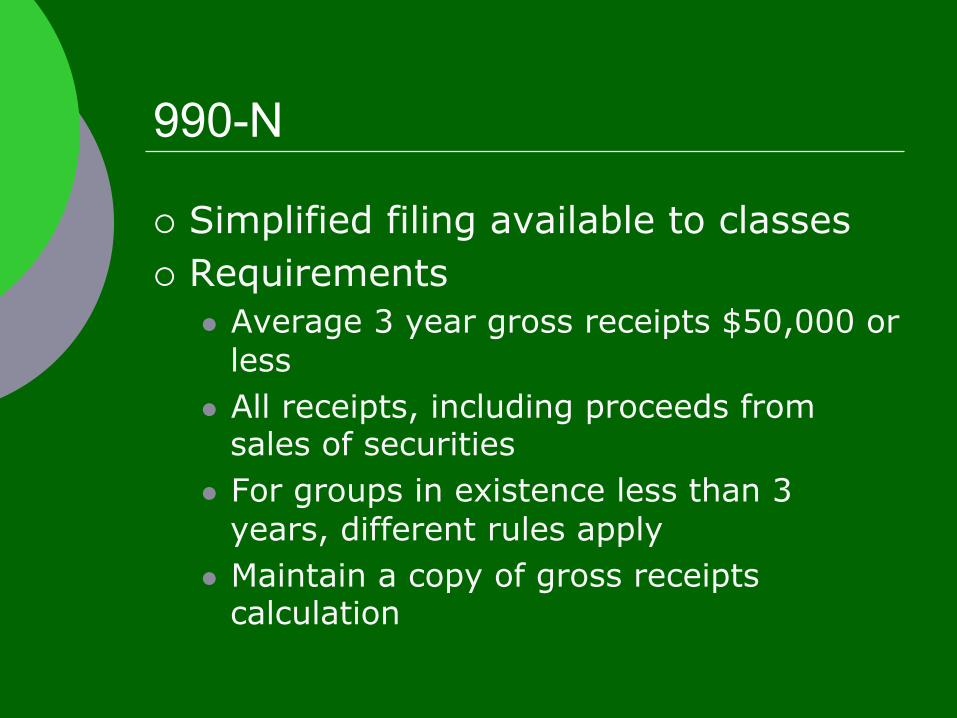

990-N

¡ Simplified filing available to classes ¡ Requirements

l Average 3 year gross receipts $50,000 or less

l All receipts, including proceeds from sales of securities

l For groups in existence less than 3 years, different rules apply

l Maintain a copy of gross receipts calculation

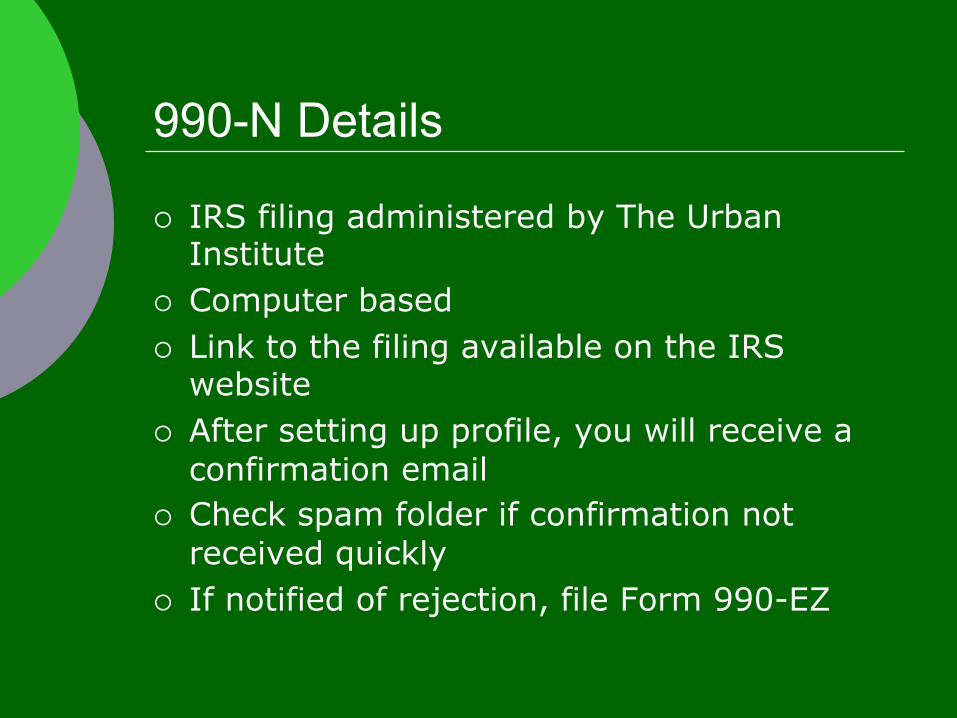

990-N Details

¡ IRS filing administered by The Urban Institute

¡ Computer based ¡ Link to the filing available on the IRS

website ¡ After setting up profile, you will receive a

confirmation email ¡ Check spam folder if confirmation not

received quickly ¡ If notified of rejection, file Form 990-EZ

990-N Details

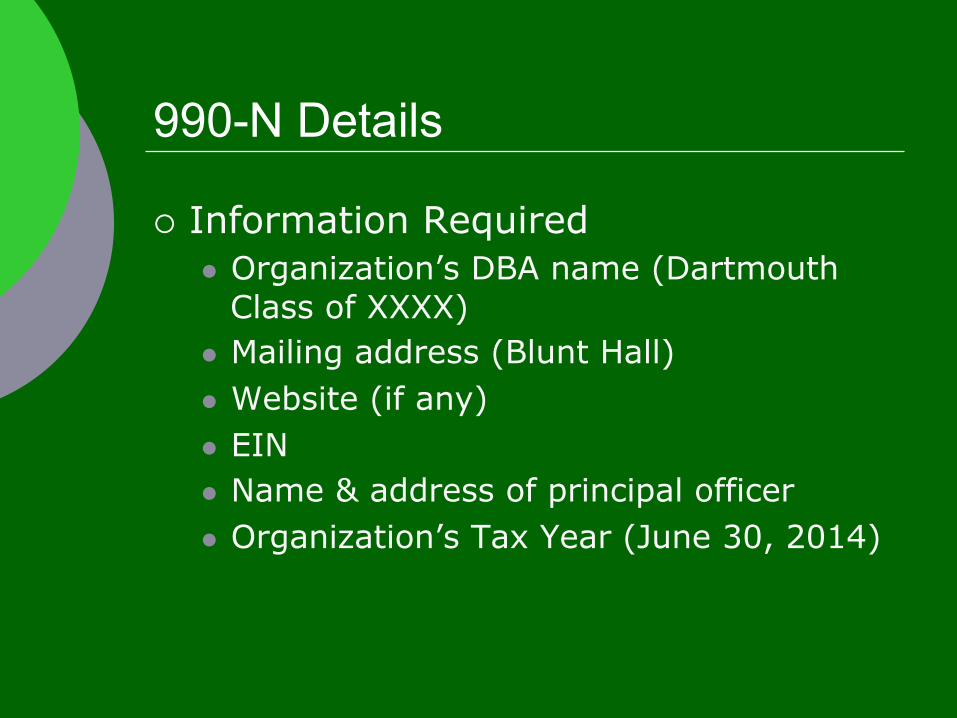

¡ Information Required l Organization’s DBA name (Dartmouth

Class of XXXX) l Mailing address (Blunt Hall) l Website (if any) l EIN l Name & address of principal officer l Organization’s Tax Year (June 30, 2014)

990-EZ

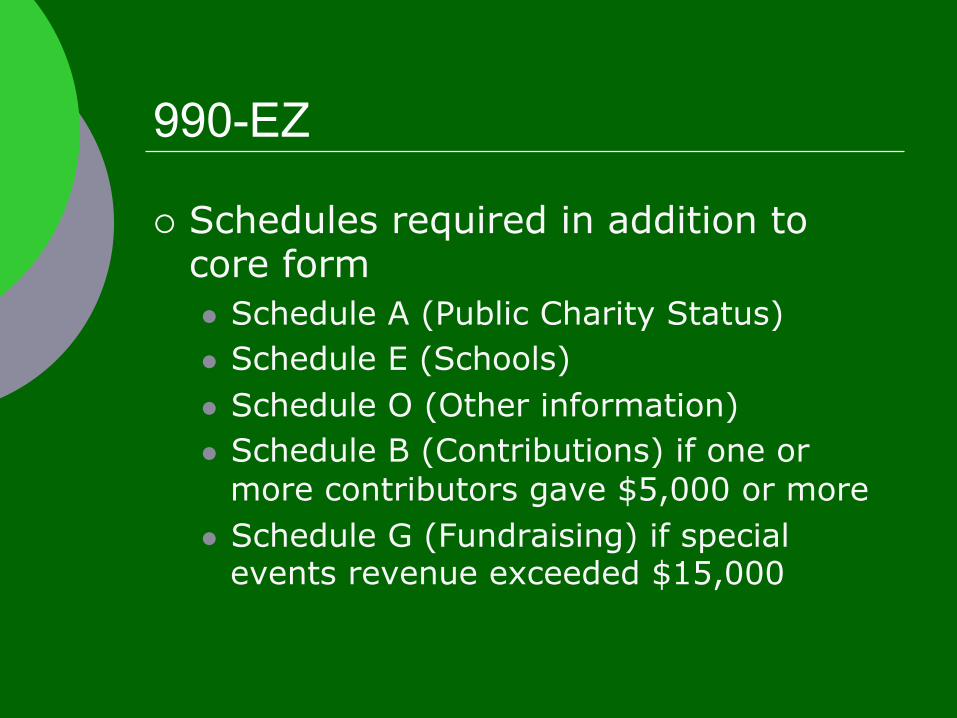

¡ Schedules required in addition to core form l Schedule A (Public Charity Status) l Schedule E (Schools) l Schedule O (Other information) l Schedule B (Contributions) if one or

more contributors gave $5,000 or more l Schedule G (Fundraising) if special

events revenue exceeded $15,000

990

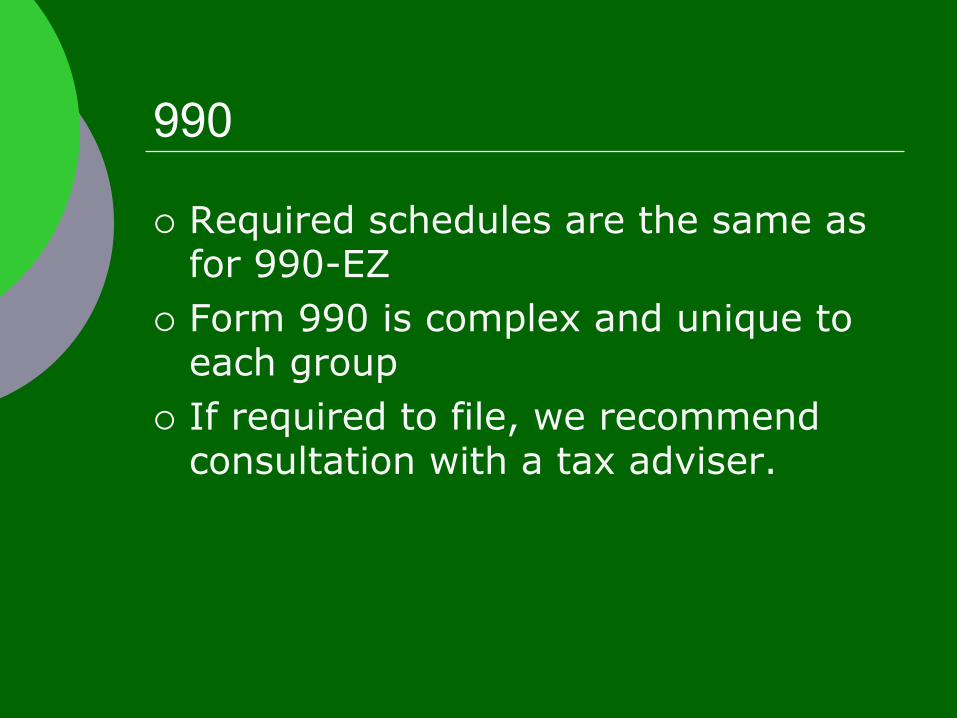

¡ Required schedules are the same as for 990-EZ

¡ Form 990 is complex and unique to each group

¡ If required to file, we recommend consultation with a tax adviser.

IRS Notices

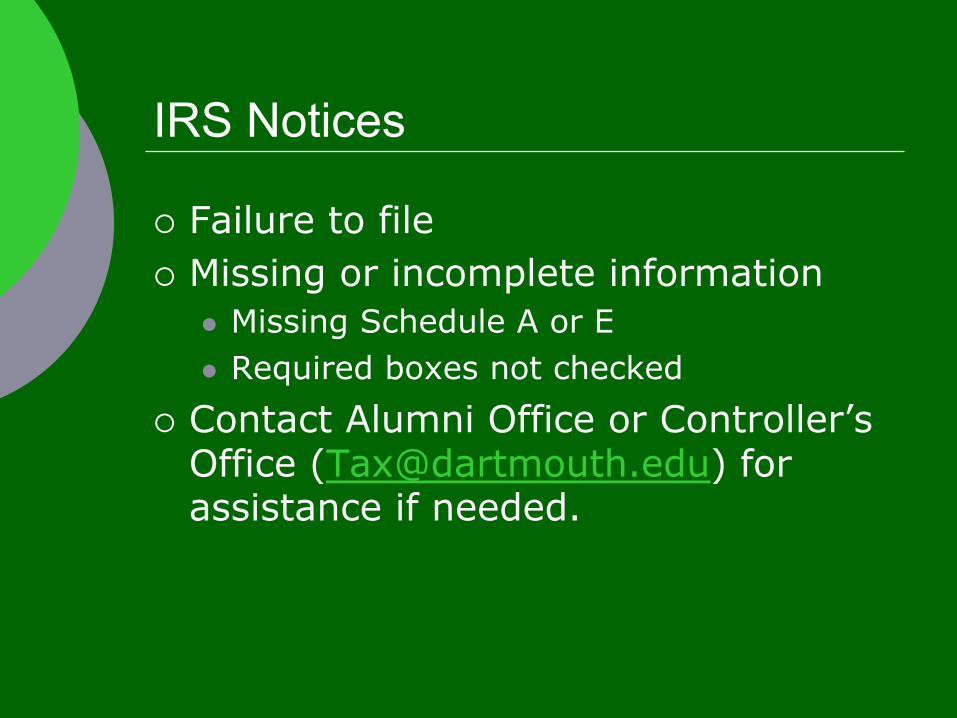

¡ Failure to file ¡ Missing or incomplete information

l Missing Schedule A or E l Required boxes not checked

¡ Contact Alumni Office or Controller’s Office ([email protected]) for assistance if needed.

Financial Best Practices

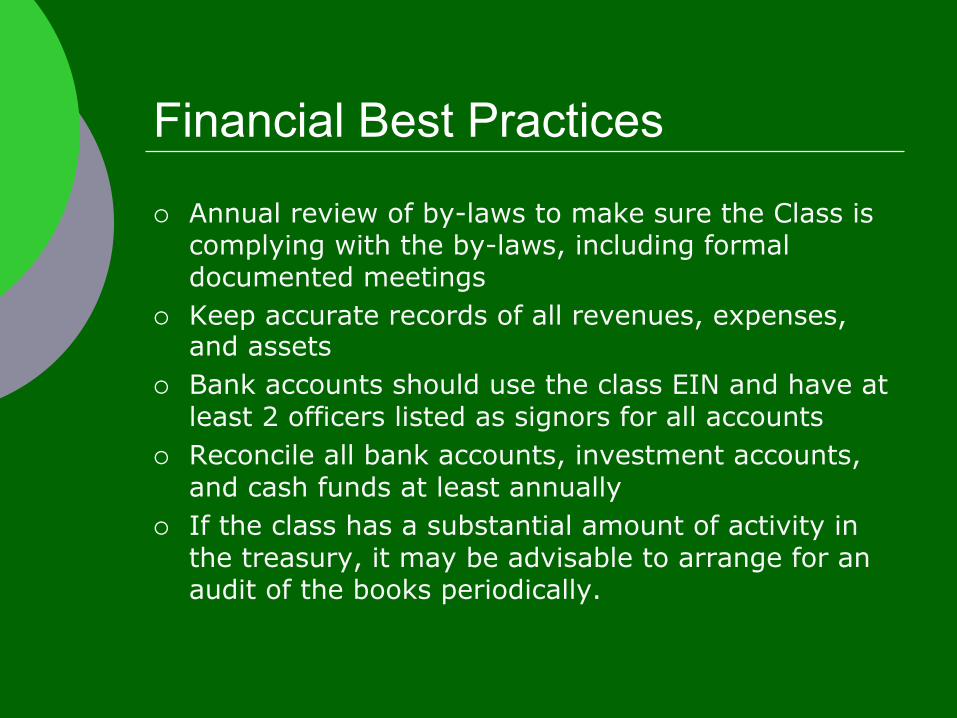

¡ Annual review of by-laws to make sure the Class is complying with the by-laws, including formal documented meetings

¡ Keep accurate records of all revenues, expenses, and assets

¡ Bank accounts should use the class EIN and have at least 2 officers listed as signors for all accounts

¡ Reconcile all bank accounts, investment accounts, and cash funds at least annually

¡ If the class has a substantial amount of activity in the treasury, it may be advisable to arrange for an audit of the books periodically.

Financial Best Practices

¡ Treasurer’s Report l The Treasurer should give a financial status

update at every board meeting and, ideally, provide quarterly reports.

l At the end of the fiscal year, a final report should be generated and presented to the Board.

l Copies of the final report should be sent to Alumni Relations to maintain historical records.

¡ Merchant Accounts l If you accept credit cards, make sure you have

procedures in place that are PCI compliant

Questions on Taxes

?

8. Treasurer Assoc. Election

Conor Frantzen

9. Treasurer Recognition

¡ 20 Years of Service & DAM Board l Tom Beecher III, 1989

¡ 15 Years of Service l Kirk Hinman, 1974

¡ Special Recognition for Distinguished Service l Art Quirk, 1959

10. Treasurers of the Year

Conor Frantzen Joe Mannes

11. Questions?