cutting taxes to increase prosperity: turning iceland into the nordic tiger reykjavik, iceland –...

TRANSCRIPT

Cutting Taxes to Increase Prosperity: Turning Iceland into the Nordic Tiger

Reykjavik, Iceland – July 26, 2007

Three Key Questions

Should Iceland embrace – or escape – the Nordic Model?What is the goal of good tax policy?Have Iceland’s reforms moved policy in the right direction?

The Nordic Model

What is the Nordic Model?Open markets and laissez-faire policies, but a big welfare state and concomitantly high tax rates.Does the Nordic Model Generate better results?There certainly is a perception that the Nordic Model is successful.

Praise for the Nordic ModelA study published by a government-subsidized think tank in Brussels asserts: “…the ‘Nordic’ and the ‘Anglo-Saxon’ models are both efficient, but only the former manages to combine both equity and efficiency.”An article by foreign-aid advocate Jeffrey Sachs states: “…the Nordic countries outperform the Anglo-Saxon ones on most measures of economic performance.”The head of the Tax Policy Centre for the Organization for Economic Cooperation and Development (OECD) bragged that taxes are twice as high in Sweden as they are in the United States, but that growth is twice as fast.

Real-World DataFaster Growth in America

United States

United States

United States

Nordic Nations

Nordic NationsNordic Nations

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

OECD (1981-1991) OECD (1992-2006) IMF ((1981-2006)

An

nu

al

Ec

on

om

ic G

row

th

Americans Enjoy More Economic Output

United States United States

United States

Nordic Average Nordic Average

Nordic Average

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

World Bank 2005 OECD 2005 IMF 2006

Per

Cap

ita G

DP

Per Capita Disposable Income

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Iceland Norway Denmark Sweden Finland USA

Source: OECD

Private Consumption per Capita

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Norway Denmark Iceland Sweden Finland United States

Dan

ish

Kro

ne

Source: Danish Finance Ministry

Why the Gap Between US and Nordics?Burden of Government Spending

20%

25%

30%

35%

40%

45%

50%

55%

60%

Denmark Finland Iceland Norway Sweden United States1

Sh

are

of

GD

P

OECD Fiscal Indicators, 2006

Government Revenue

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

Denmark Finland Iceland Norway Sweden United States

Sh

are

of

GD

P

Total Receipts (2006)

Tax Revenues (2003)

Source: OECD

Top Tax Rate on Personal Income

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

Denmark Finland Iceland Norway Sweden United States

With Employee Share of Payroll Tax

Personal Income Tax

Source:OECD

Good News About Nordic Nations

They grow faster than most other European nations.They rank highly in both Economic Freedom of the World and the Index of Economic Freedom.Low tax rates on capital.Economic reforms such as personal retirement accounts.

What is Good Tax Policy?Tax Income at one low rate, ideally no more than 20 percent.Define the tax base correctly, taxing Income only one time.Tax all income alike, since neutrality ensures economic criteria rather than tax provisions determine resource allocation.Tax only income earned inside national borders, the common-sense notion of territorial taxation.

Why Have a Low Tax Rate?The marginal tax rate – the burden on the next increment of income – must be kept low.A low marginal tax rate rewards productive behavior. People will work more, save more, and invest more.Incentives to hide, shelter, under-report income are lower when the marginal tax rate is reasonable.Research indicates that the marginal tax rate should be no higher than 20 percent.

Why Tax Income Only One Time?Many nations impose multiple layers of tax on income that is saved and invested.This is the wrong definition of the tax base.Taxes on interest, dividends, capital gains, and inheritances are examples of the discriminatory treatment of capital.This is a self-destructive policy since it harms the activity – capital formation – that all economic theories agree is necessary for economic growth and rising living standards.

Why Neutrality?Government should not pick winners and losers.Special preferences and penalties distort the allocation of capital and undermine efficiency, leading to lower incomes.Special preferences and penalties also encourage taxpayers to squander time and energy in search of political advantage instead of concentrating on productive behavior.

Benefits of Tax ReformThere are many reasons to adopt a flat tax, including:LibertySimplicityProsperityOpportunityEqualityPrivacyEnforcementRevenue

Tax CompetitionThe ability of jobs and investment to cross national borders is a powerful constraint on politicians.

Tax competition is a powerful force for economic liberalization, one that should be celebrated rather than persecuted.The rewards for good tax policy have never been greater.If the “goose that lays the golden eggs” can fly across the border, governments must behave more responsibly.

Tax CompetitionToday’s global economy makes good tax policy much more important.Lower tax burdens is one reason why the U.S. is doing much better than the E.U., with faster growth and more employment. Good tax policy is especially important for smaller jurisdictions, which necessarily are more open to the global economy.

Iceland’s Supply-Side Tax Reforms

Low-rate corporate income taxLow-rate flat tax on capital incomeMinimal death taxNo wealth taxMedium-rate flat tax on labor incomeOther pro-growth reforms include personal retirement accounts and property rights for fisheries

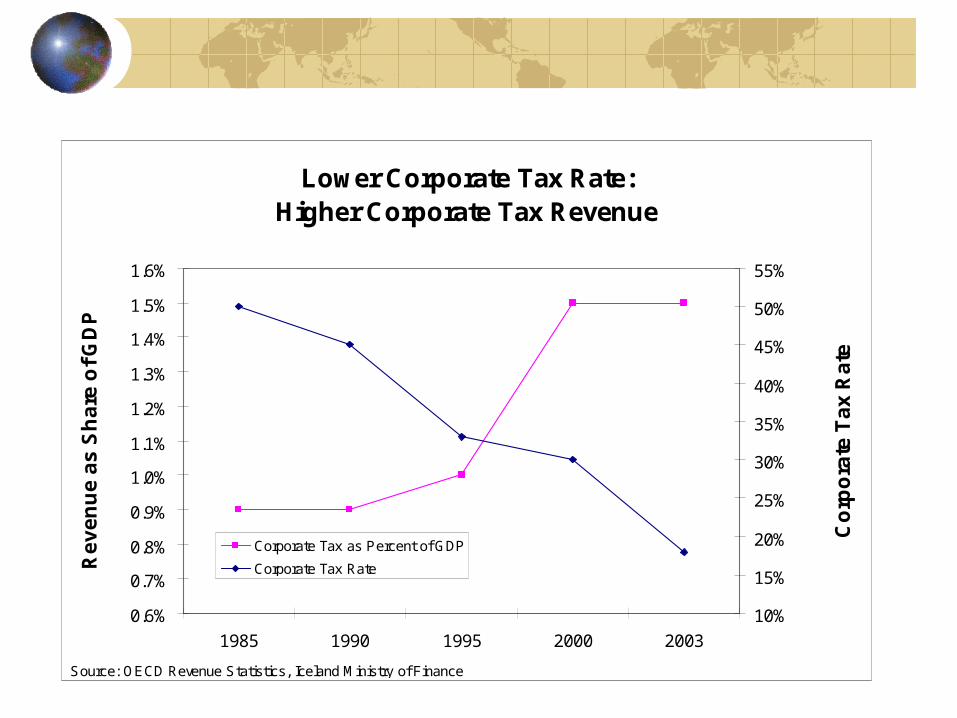

Positive ResultsIceland is now the world’s fifth-richest nation according to both the International Monetary Fund and the Organisation for Economic Cooperation and Development. Iceland now ranks as the world’s 9th freest economy according to Economic Freedom of the World and the 15th freest economy according to the Index of Economic Freedom. Lower tax rates have generated a supply-side feedback effect. The government is collecting substantially more corporate tax revenue with a rate of 18 percent instead of 50 percent. Revenues from the 10 percent tax on capital income also have been robust.

Per Capita GDP

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Lower Corporate Tax Rate: Higher Corporate Tax Revenue

0.6%

0.7%

0.8%

0.9%

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

1985 1990 1995 2000 2003

Re

ve

nu

e a

s S

ha

re o

f G

DP

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

Co

rpo

rate

Ta

x R

ate

Corporate Tax as Percent of GDP

Corporate Tax Rate

Source: OECD Revenue Statistics, Iceland Ministry of Finance

Remaining Challenges

Lower the rate of the flat tax, which is higher than the highest rate in the US system.Lower the corporate tax rate, building on earlier successes.Control the size of government, learning from nations such as Ireland and New Zealand.

Conclusion

Iceland’s reforms are impressive and have generated large benefits.Other nations are competing and implementing their own reforms, so Iceland must continue to reduce the burden of government.With any luck, Iceland will serve as a role model for the United States!