credit suisse (lux) multi-advisor equity alpha fund · 2017-01-27 · credit suisse (lux)...

TRANSCRIPT

Asset Management – Alternative Investments

Dirk Wieringa

January 2017

Alternative Funds Solutions

Credit Suisse (Lux) Multi-Advisor Equity Alpha

Fund

January 2017 Asset Management 2 The disclaimer at the end is also applicable to this page.

“Best Ideas Long/Short Equity”

January 2017 Asset Management 3 The disclaimer at the end is also applicable to this page.

Review of 2016

Environment where politics trump economic fundamentals

Important to distinguish between cyclical factors that affect strategy performance, and secular factors that alter the investment paradigm

Continued growth in passive/quantitative products including “smart beta” can provide a challenge for

active managers and stock pickers in particular However, dispersion in valuations across regions and sectors has reached a healthy level and

managers should now benefit from a return to fundamentals for both, their long, and short books

Q4 2016 was marked by significant post-election equity upside, dollar strengthening, and rising yields

Market participants stepped in early and heavily discounted the positive economic impact, but neglected

negatives

Markets may have already seen the best of the 140 characters stimulus program

January 2017 Asset Management 4 The disclaimer at the end is also applicable to this page.

2016: A Year of Rotations, Surprises and Sentiment Shifts

Significant Events Disrupted Fundamental Stock Picking

Source: Bloomberg, Credit Suisse; Index: MSCI World Total Return

Rotation

Brexit

Trump

January 2017 Asset Management 5 The disclaimer at the end is also applicable to this page.

Equity Factor Performance

Value Strikes Back in Q4

Source: Bloomberg, Morgan Stanley

Factor 2016

Momentum -16%

Quality -5%

Size 0%

Value +10%

Volatility -1%

January 2017 Asset Management 6 The disclaimer at the end is also applicable to this page.

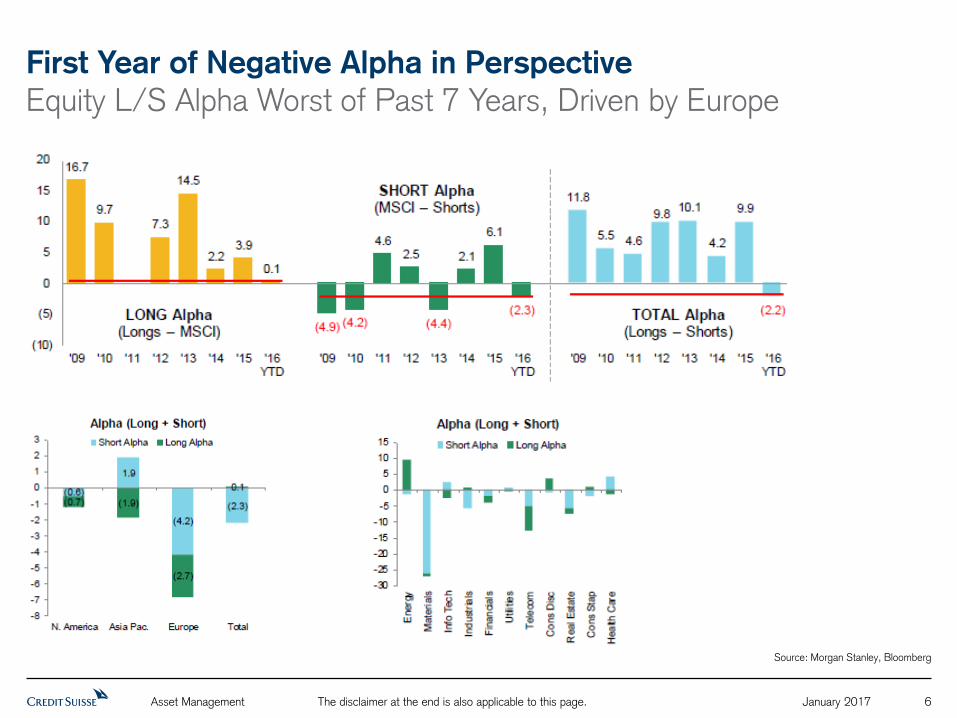

First Year of Negative Alpha in Perspective

Equity L/S Alpha Worst of Past 7 Years, Driven by Europe

Source: Morgan Stanley, Bloomberg

January 2017 Asset Management 7 The disclaimer at the end is also applicable to this page.

U.S. Equities Dispersion in Valuations by Sector Can Provide a Fertile Ground for Stock-picking

Source: JP Morgan

Many sectors still look undervalued relative to historical averages (HC, Tech, Consumer, Telecom)

January 2017 Asset Management 8 The disclaimer at the end is also applicable to this page.

Outlook into 2017

We anticipate additional volatility related to the European elections and US rates normalization

The triple punch of US yield increases, steepening of the yield curve, and dollar appreciation gives

a strong back drop for Discretionary Macro Traders

The ability to navigate through a choppy political agenda is crucial

Focus on managers with the ability to react to changing environments, either through broad

discretionary mandates, or quantitative approaches that allows for inbuilt “bottom-picking”

Key themes and positioning include:

– In equities, we maintain a preference for lower-net and opportunistic managers

– We turn positive on event driven due to continued high M&A volumes and cash rich company balance sheets

– We are optimistic towards fixed income arbitrage

– We continue to favor flexible Discretionary Macro managers

– We favor Multi-Strategy CTAs that should benefit from uncorrelated sources of alpha

January 2017 Asset Management 9 The disclaimer at the end is also applicable to this page.

Innovative Concept to Systematically Combine “Best Ideas”

into a Single Portfolio of High Conviction Long/Short Equities

January 2017 Asset Management 10 The disclaimer at the end is also applicable to this page.

Investment Rationale

Why Equity Long/Short? Why “Best Ideas”?

Long-only equity

mutual funds

Equity long/

short funds

“Best Ideas”

α

β

Excess return

Derived from stock

picks

No correlation to

market

Market return

Derived from expo-

sure to asset class

Perfect correlation

to market

β

α

β

α

β

Little alpha

Small excess return

High market

dependence

Alpha, but mostly from

high conviction trades

Generation of excess

returns

Some market dependence

Larger liquid alpha

generation

Opportunity for larger

excess returns

Low market dependence

Collect high

conviction

trades from

top equity

long/short

managers

Variable Variable

Investors’ returns derive

from either alpha (α) or

beta (β)

α

January 2017 Asset Management 11 The disclaimer at the end is also applicable to this page.

Investment Approach

Selecting Highest Conviction Trades from Top Managers

Long/short equity

manager universe

(>4,000) Credit Suisse AFS

approved

long/short

equity managers

(~30)

Selected

specialist

long/short

equity advisors

(~5–7)

“Best Ideas”

portfolio

Managers are subject to a rigorous due

diligence process covering:

Investment Operational Risk

Legal

Skill level assessment of each manager’s

stock selection ability

Advisors provide daily position level data of

top ten long and short holdings

Advisors’ top trades are combined in

a single portfolio

Portfolio construction process

IDEAS

IDEAS IDEAS IDEAS

Liquid, high-conviction ideas

Other ideas

January 2017 Asset Management 12 The disclaimer at the end is also applicable to this page.

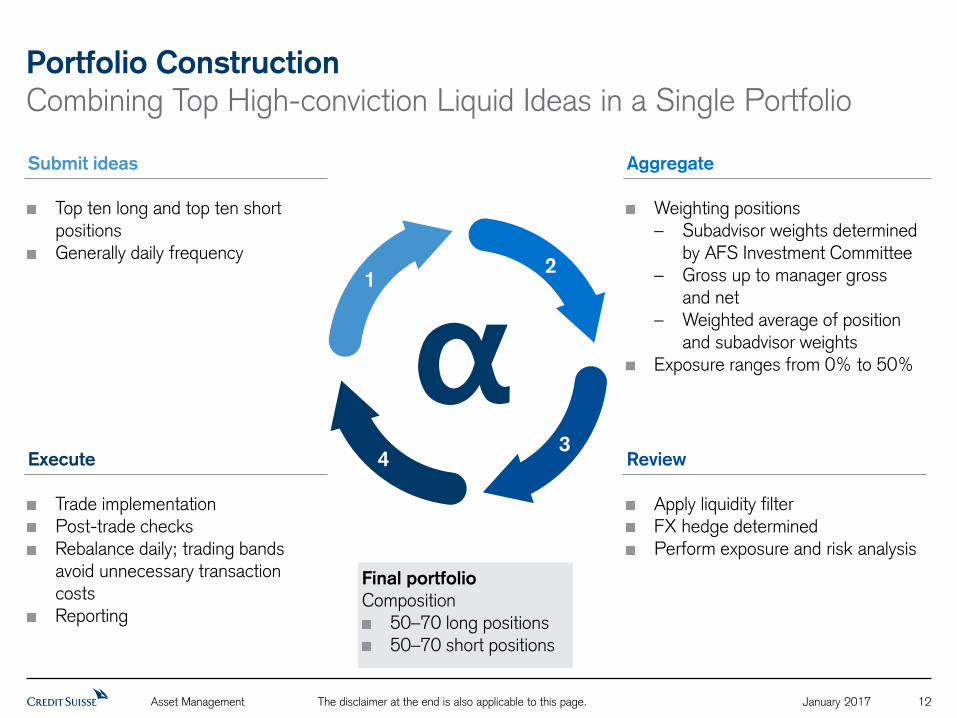

Portfolio Construction

Combining Top High-conviction Liquid Ideas in a Single Portfolio

Review

Apply liquidity filter FX hedge determined Perform exposure and risk analysis

α 1

2

3 4

Aggregate

Weighting positions – Subadvisor weights determined

by AFS Investment Committee – Gross up to manager gross

and net – Weighted average of position

and subadvisor weights Exposure ranges from 0% to 50%

Execute

Trade implementation Post-trade checks Rebalance daily; trading bands avoid unnecessary transaction costs Reporting

Submit ideas

Top ten long and top ten short positions Generally daily frequency

Final portfolio

Composition 50–70 long positions 50–70 short positions

January 2017 Asset Management 13 The disclaimer at the end is also applicable to this page.

Portfolio Exposures (as of December 31, 2016)

Sources: Credit Suisse, Bloomberg As of 31.12.2016

Portfolio positioning

Long exposure 80.9%

Short exposure -63.5%

Number of long positions 77

Number of short positions 67

Geographic exposure (% of NAV)

Region Long Short Gross Net

Asia ex Japan 8.4 -3.2 11.6 5.2

Europe 27.6 -17.6 45.1 10.0

Japan 2.9 -1.1 4.0 1.8

North America 0.0 0.0 0.0 0.0

South America 42.1 -41.6 83.7 0.6

Other 0.0 0.0 0.0 0.0

Total 80.9 -63.5 144.4 17.5

Sector exposure (% of NAV)

Industry Long Short Gross Net

Consumer discretionary 8.0 -11.9 19.9 -3.9

Consumer staples 1.7 -2.3 4.0 -0.6

Energy 1.1 0.0 1.1 1.1

Financials 4.5 -1.4 5.9 3.1

Health care 22.2 -18.7 40.9 3.5

Industrials 8.8 -8.2 17.0 0.7

Communications 8.7 -5.2 13.9 3.4

Materials 3.4 -1.1 4.5 2.3

Technology 18.2 -12.5 30.7 5.7

Utilities 2.3 -0.7 3.1 1.6

Market 2.0 -1.4 3.4 0.6

Total 80.9 -63.5 144.4 17.5

Market cap

Market Long Short Gross Net

Mega-cap 43.4 -33.3 76.7 10.2

Large-cap 12.1 -13.0 25.1 -0.9

Mid-cap 17.5 -14.3 31.8 3.1

Small-cap 5.9 -0.9 6.8 5.1

Index 2.0 -2.0 4.0 0.0

Total 80.9 -63.5 144.4 17.5

Top five long holdings

Sanofi 2.7

Eli Lilly & Company 2.3

GlaxoSmithKline PLC 2.2

Allergan plc 2.2

Alphabet Inc 2.2

Total 11.6

January 2017 Asset Management 14 The disclaimer at the end is also applicable to this page.

Return Potential of the “Best Ideas”

(Hypothetical Performance)

Hypothetical net performance backtest of subadvisors’ top high conviction, liquid stock ideas from January 2011 to December 2015. For January 2016 the figure represents paper trading of the approach. Net performance assumes a management fee of 1.00%, a 5% incentive fee and subadvisor fees of 1.0%. Based on monthly position data from subadvisors and constant weights to subadvisors. Simulated past performance indications and financial market scenarios are not reliable indicators of current or future performance.

Sources: Credit Suisse, Bloomberg As of 31.01.2016

Cumulative Returns of the “Best Ideas” compared to full portfolio returns of the basket of sub-advisors

(net of fees)

90

100

110

120

130

140

150

160

Dez 10 Jun 11 Dez 11 Jun 12 Dez 12 Jun 13 Dez 13 Jun 14 Dez 14 Jun 15 Dez 15

“Best Ideas” of the Sub-advisors Full Portfolio of the Sub-advisors

January 2017 Asset Management 15 The disclaimer at the end is also applicable to this page.

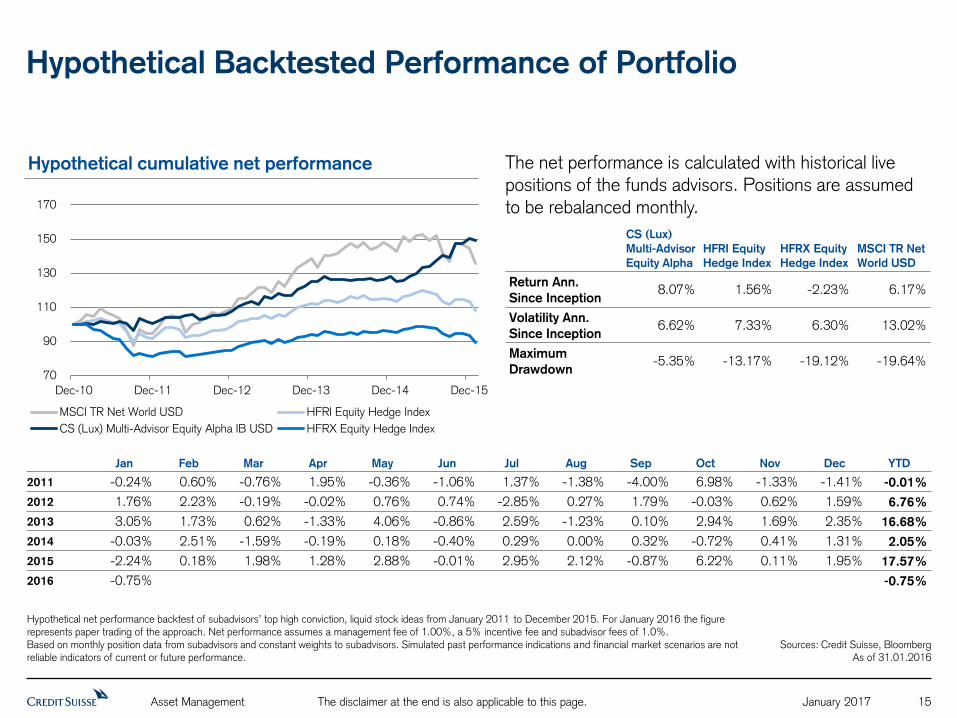

Hypothetical Backtested Performance of Portfolio

Hypothetical net performance backtest of subadvisors’ top high conviction, liquid stock ideas from January 2011 to December 2015. For January 2016 the figure represents paper trading of the approach. Net performance assumes a management fee of 1.00%, a 5% incentive fee and subadvisor fees of 1.0%. Based on monthly position data from subadvisors and constant weights to subadvisors. Simulated past performance indications and financial market scenarios are not reliable indicators of current or future performance.

Sources: Credit Suisse, Bloomberg As of 31.01.2016

Hypothetical cumulative net performance The net performance is calculated with historical live positions of the funds advisors. Positions are assumed to be rebalanced monthly.

CS (Lux)

Multi-Advisor

Equity Alpha

HFRI Equity

Hedge Index

HFRX Equity

Hedge Index

MSCI TR Net

World USD

Return Ann.

Since Inception 8.07% 1.56% -2.23% 6.17%

Volatility Ann.

Since Inception 6.62% 7.33% 6.30% 13.02%

Maximum

Drawdown -5.35% -13.17% -19.12% -19.64%

70

90

110

130

150

170

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

MSCI TR Net World USD HFRI Equity Hedge Index

CS (Lux) Multi-Advisor Equity Alpha IB USD HFRX Equity Hedge Index

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2011 -0.24% 0.60% -0.76% 1.95% -0.36% -1.06% 1.37% -1.38% -4.00% 6.98% -1.33% -1.41% -0.01%

2012 1.76% 2.23% -0.19% -0.02% 0.76% 0.74% -2.85% 0.27% 1.79% -0.03% 0.62% 1.59% 6.76%

2013 3.05% 1.73% 0.62% -1.33% 4.06% -0.86% 2.59% -1.23% 0.10% 2.94% 1.69% 2.35% 16.68%

2014 -0.03% 2.51% -1.59% -0.19% 0.18% -0.40% 0.29% 0.00% 0.32% -0.72% 0.41% 1.31% 2.05%

2015 -2.24% 0.18% 1.98% 1.28% 2.88% -0.01% 2.95% 2.12% -0.87% 6.22% 0.11% 1.95% 17.57%

2016 -0.75% -0.75%

January 2017 Asset Management 16 The disclaimer at the end is also applicable to this page.

Performance since Inception

Historical performance indications and financial market scenarios are no reliable indicators of future performance. The performance data do not take into account the commissions and costs incurred on the issue and redemption of fund units. February 2016 performance is calculated from February 2, 2016 through February 29, 2016. Paper trading results for February 1, 2016 were +0.68%.

Sources: Credit Suisse, Bloomberg As of 31.12.2016

Historical cumulative net performance (since inception February 2, 2016)

93

94

95

96

97

98

99

100

101

102

103

Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16 Nov 16 Dec 16

CS (Lux) Multi-Advisor Equity Alpha Fund IB USD

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2016 – -2.7% 1.4% -0.8% -0.1% 0.2% 2.6% -0.1% 1.1% -0.1% -3,3% -1,1 -3,2%

January 2017 Asset Management 17 The disclaimer at the end is also applicable to this page.

Performance

Return Independence

“Best Ideas” vs. MSCI World

(since inception February 2, 2016)

“Best Ideas” vs. MSCI World

(since inception February 2, 2016)

The Beta of daily returns vs. MSCI World is at around 0.11 for Best Ideas and far lower than that of the HFRX Equity Hedge Index to the MSCI World. Sources: Credit Suisse, Bloomberg

As of 31.12.2016

-2.50%

-1.50%

-0.50%

0.50%

1.50%

2.50%

-2.50% -1.50% -0.50% 0.50% 1.50% 2.50%

y = 0.4349x + 1E-05

R² = 0.7625

-2.50%

-1.50%

-0.50%

0.50%

1.50%

2.50%

-2.50% -1.50% -0.50% 0.50% 1.50% 2.50%

CS (Lux) Multi-Advisor Equity Alpha vs. MSCI World

Beta 0.11

R2 7.1%

HFRX Equity Hedge Index vs. MSCI World

Beta 0.43

R2 76.3%

January 2017 Asset Management 18 The disclaimer at the end is also applicable to this page.

Value Proposition

An innovative “best ideas” approach to long/short equity: the fund allocates directly to the highest

conviction, liquid long and short positions of a carefully selected group of long/short equity hedge fund managers.

1

2

3

Capturing the best long and short equity ideas in a single fund structure

Benchmark independent and alpha focused returns

Available in a regulated structure with daily liquidity

January 2017 Asset Management 19 The disclaimer at the end is also applicable to this page.

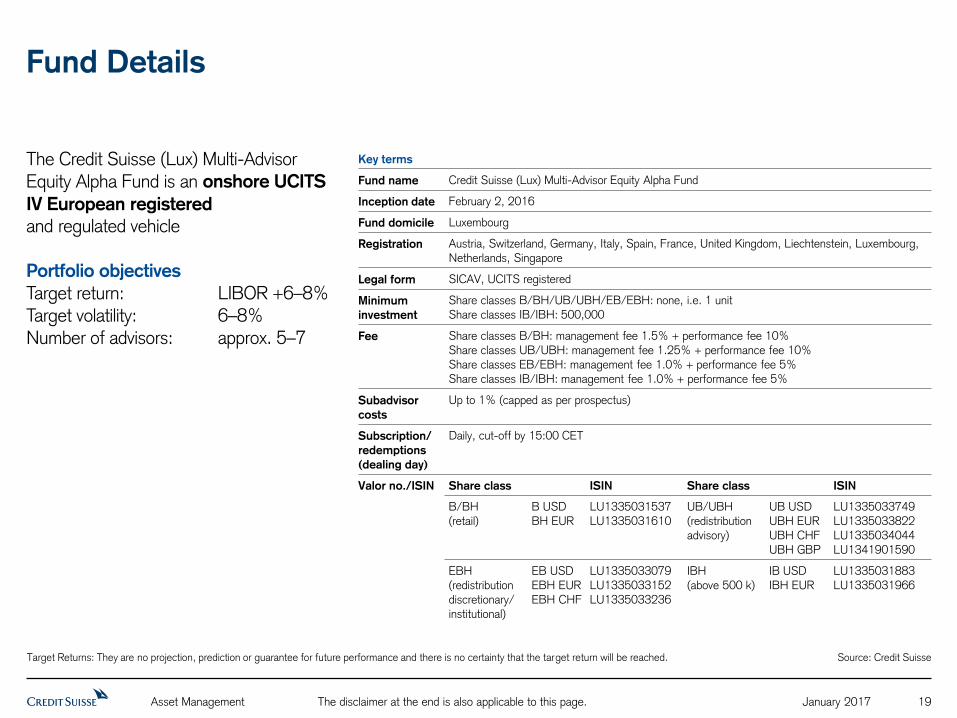

Fund Details

Target Returns: They are no projection, prediction or guarantee for future performance and there is no certainty that the target return will be reached. Source: Credit Suisse

The Credit Suisse (Lux) Multi-Advisor Equity Alpha Fund is an onshore UCITS

IV European registered

and regulated vehicle Portfolio objectives Target return: LIBOR +6–8% Target volatility: 6–8% Number of advisors: approx. 5–7

Key terms

Fund name Credit Suisse (Lux) Multi-Advisor Equity Alpha Fund

Inception date February 2, 2016

Fund domicile Luxembourg

Registration Austria, Switzerland, Germany, Italy, Spain, France, United Kingdom, Liechtenstein, Luxembourg,

Netherlands, Singapore

Legal form SICAV, UCITS registered

Minimum

investment

Share classes B/BH/UB/UBH/EB/EBH: none, i.e. 1 unit

Share classes IB/IBH: 500,000

Fee Share classes B/BH: management fee 1.5% + performance fee 10% Share classes UB/UBH: management fee 1.25% + performance fee 10% Share classes EB/EBH: management fee 1.0% + performance fee 5% Share classes IB/IBH: management fee 1.0% + performance fee 5%

Subadvisor

costs

Up to 1% (capped as per prospectus)

Subscription/

redemptions

(dealing day)

Daily, cut-off by 15:00 CET

Valor no./ISIN

Share class ISIN Share class ISIN

B/BH (retail)

B USD BH EUR

LU1335031537 LU1335031610

UB/UBH (redistribution

advisory)

UB USD UBH EUR

UBH CHF UBH GBP

LU1335033749 LU1335033822

LU1335034044 LU1341901590

EBH

(redistribution discretionary/

institutional)

EB USD

EBH EUR EBH CHF

LU1335033079

LU1335033152 LU1335033236

IBH

(above 500 k)

IB USD

IBH EUR

LU1335031883

LU1335031966

Appendix

January 2017 Asset Management 21 The disclaimer at the end is also applicable to this page.

Equity Long/Short Manager Alpha Generation

AFS-approved Managers do Create Alpha

1 Credit Suisse Alternative Funds Solutions. Historical performance indications and financial market scenarios are not reliable indicators of current or future performance.

Source: Credit Suisse As of 31.10.2016

Alpha of AFS-approved managers vs. MSCI World

Alpha for the AFS1 lineup of Equity Long/Short managers has averaged 3.33% per year since January 2011.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

January 2017 Asset Management 22 The disclaimer at the end is also applicable to this page.

Globally Diversified Portfolio of “Best Ideas”

There is no indication or guarantee that any actual client portfolio will make the same or similar investments as the sample portfolios described above.

Subadvisor F Subadvisor E

Global tech/media/telco

>5-year track record USD 100 mn+ in strategy AUM

Subadvisor A

Europe generalist

>10-year track record USD 1 bn+ in strategy AUM

“Best Ideas” Credit Suisse (Lux)

Multi-Advisor Equity Alpha Fund

Subadvisor B Subadvisor C

Subadvisor D

US generalist

>5-year track record USD 400 mn+ in strategy AUM

Global healthcare

>10-year track record USD 500 mn+ in strategy AUM

Asia generalist

>10-year track record USD 400 mn+ in strategy AUM

Highest conviction, liquid ideas Target net exposure range of 0% to 50% Global investment universe

Global generalist

>4-year track record USD 100 mn+ in strategy AUM

January 2017 Asset Management 23 The disclaimer at the end is also applicable to this page.

Investable Universe

Global and Unconstrained of Any Benchmark

The strategy is global and unconstrained of any benchmark to allow for maximum alpha potential

Geographies

Americas EMEA APAC (incl. Chinese A-shares) Emerging markets

Market cap

Mega cap Large cap Mid cap Small cap

Sectors

Consumer discretionary Consumer staples Energy Financials Health care Industrials IT Materials Telecommunication Services Utilities

January 2017 Asset Management 24 The disclaimer at the end is also applicable to this page.

Historical Exposure Levels

Figures represent backtested data until December 13, 2015, paper trading from December 15, 2015 to February 1, 2016 and live figures from February 2, 2016. Source: Credit Suisse

As of 31.10.2016

Historical market exposures

Gross exposures ranged from 140% to 190%; net exposures from 15% to 30% Gross exposure is largely a function of market volatility: when volatility increases, subadvisors will generally reduce their balance sheets as exhibited in the latter half of 2012 and the fall of 2015 Net exposure will fluctuate based on the expected risk/return from longs and shorts. For example, net has declined over the past few months as subadvisors are seeing more opportunities to generate alpha on the short side.

-100%

-50%

0%

50%

100%

150%

200%

250%

Long Exposure Short Exposure Net Exposure Long Exposure

Gross Exposure

Long Exposure Net Exposure

Short Exposure

Start of live

performance

January 2017 Asset Management 25 The disclaimer at the end is also applicable to this page.

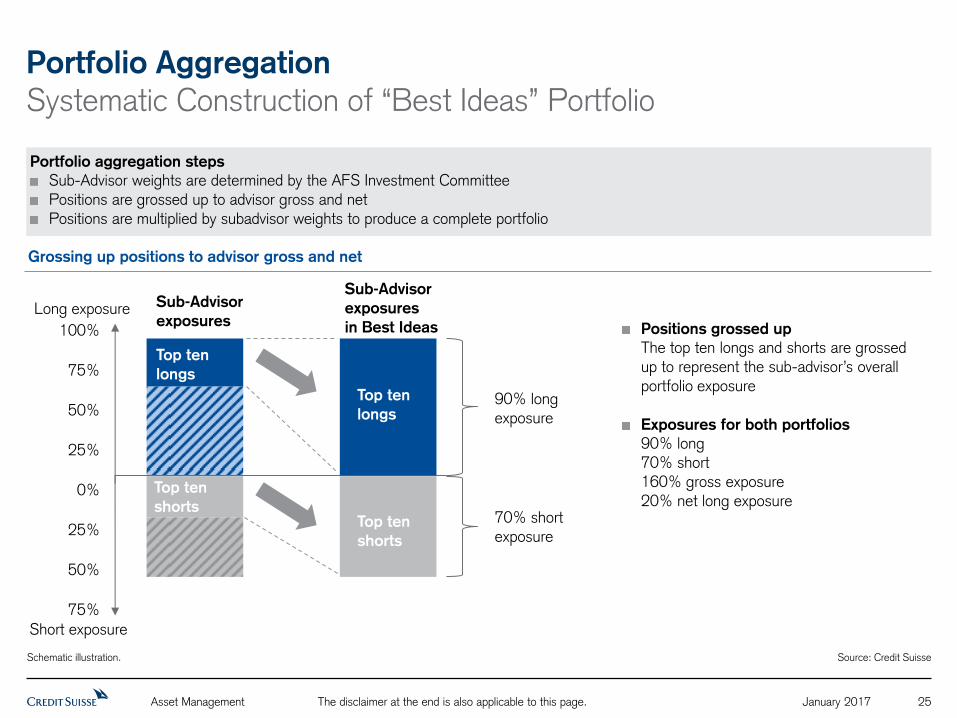

Portfolio Aggregation

Systematic Construction of “Best Ideas” Portfolio

Schematic illustration. Source: Credit Suisse

Portfolio aggregation steps

Sub-Advisor weights are determined by the AFS Investment Committee Positions are grossed up to advisor gross and net

Positions are multiplied by subadvisor weights to produce a complete portfolio

Positions grossed up

The top ten longs and shorts are grossed up to represent the sub-advisor’s overall portfolio exposure

Exposures for both portfolios

90% long 70% short

160% gross exposure 20% net long exposure

Short exposure

90% long

exposure

70% short exposure

Long exposure

Top ten

longs

Top ten

shorts Top ten

shorts

Top ten

longs

100%

75%

50%

25%

0%

25%

50%

75%

Sub-Advisor

exposures

Sub-Advisor

exposures

in Best Ideas

Grossing up positions to advisor gross and net

January 2017 Asset Management 26 The disclaimer at the end is also applicable to this page.

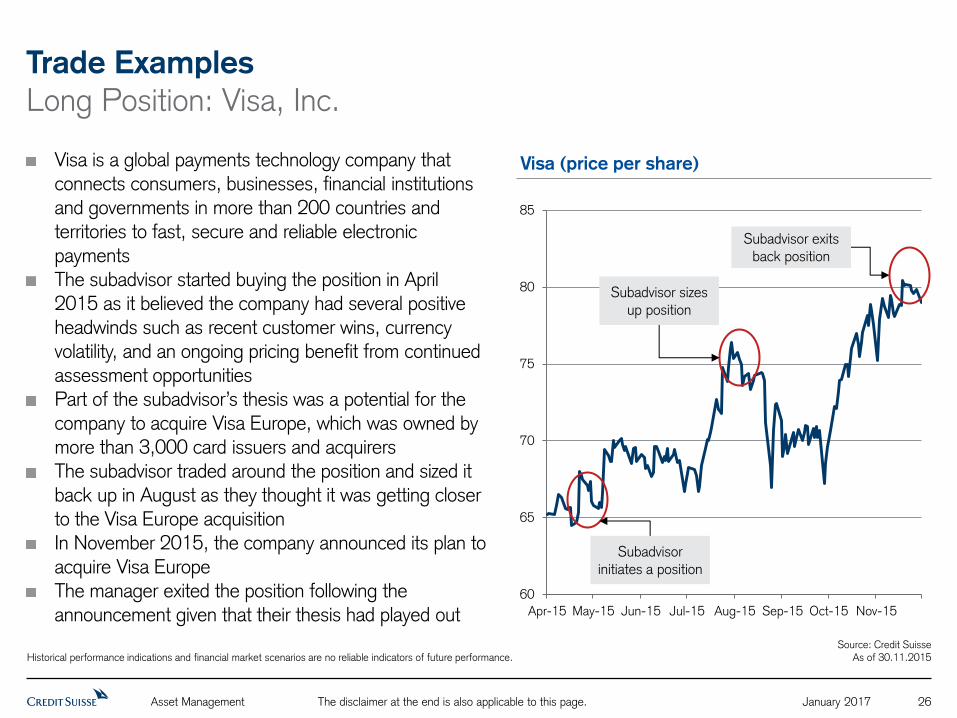

Trade Examples

Long Position: Visa, Inc.

Visa is a global payments technology company that connects consumers, businesses, financial institutions and governments in more than 200 countries and territories to fast, secure and reliable electronic

payments The subadvisor started buying the position in April 2015 as it believed the company had several positive headwinds such as recent customer wins, currency volatility, and an ongoing pricing benefit from continued

assessment opportunities Part of the subadvisor’s thesis was a potential for the

company to acquire Visa Europe, which was owned by more than 3,000 card issuers and acquirers The subadvisor traded around the position and sized it back up in August as they thought it was getting closer to the Visa Europe acquisition

In November 2015, the company announced its plan to

acquire Visa Europe The manager exited the position following the announcement given that their thesis had played out

Historical performance indications and financial market scenarios are no reliable indicators of future performance.

Source: Credit Suisse As of 30.11.2015

Visa (price per share)

60

65

70

75

80

85

Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

Subadvisor initiates a position

Subadvisor sizes up position

Subadvisor exits back position

January 2017 Asset Management 27 The disclaimer at the end is also applicable to this page.

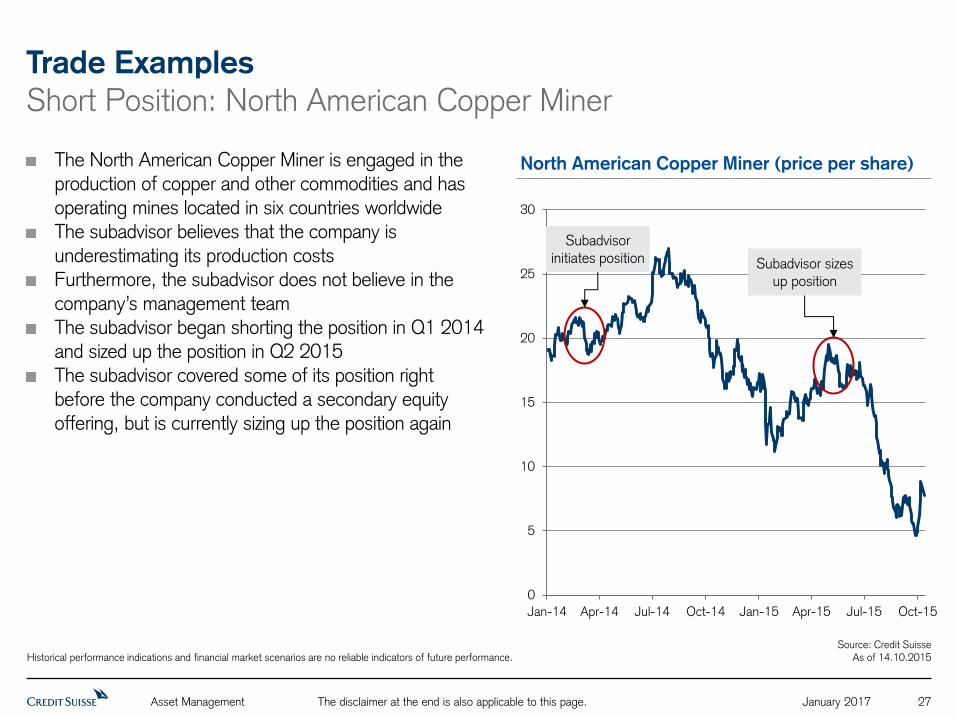

Trade Examples

Short Position: North American Copper Miner

The North American Copper Miner is engaged in the production of copper and other commodities and has operating mines located in six countries worldwide The subadvisor believes that the company is

underestimating its production costs Furthermore, the subadvisor does not believe in the company’s management team The subadvisor began shorting the position in Q1 2014 and sized up the position in Q2 2015

The subadvisor covered some of its position right before the company conducted a secondary equity

offering, but is currently sizing up the position again

Historical performance indications and financial market scenarios are no reliable indicators of future performance. Source: Credit Suisse

As of 14.10.2015

North American Copper Miner (price per share)

0

5

10

15

20

25

30

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Subadvisor initiates position Subadvisor sizes

up position

January 2017 Asset Management 28 The disclaimer at the end is also applicable to this page.

Robust Due Diligence Process

Coordinated Discussions between Independent Specific Expert Teams

The substantial professional resources of over 50 people are collectively committed to the business of AFS,

situated globally in five offices in New York, San Francisco, Tokyo, Singapore and Zurich.

Due Diligence Reports

Fund Review Committee

1. Investment Research

Experience and leadership

Cohesiveness

Market opportunity

and process

Industry knowledge

Value added

Competitive advantage

Internal resources

Economics

Investment Research

Operational Due Diligence

Legal Due Diligence

Market Risk Control

4. Risk Control

Processes and

infrastructure

Transparency

Exposures and limits

Decision-making

Performance

Risk/drawdown analysis

Realized/unrealized

returns

Portfolio composition

Adherence to strategy

2. Operational Due

Diligence

Manager overview

Legal and compliance

Governance and Conflicts

of Interests

Investment and trade

process

Pricing, Valuation

and NAV

Cash and counterparties

Service providers

3. Legal Due Diligence

Fund/investment

structure

Corporate and fund

governance

Liquidity terms

Fees and expenses

Regulatory events and

activity

Conflicts of interest

Steps

involved

Criteria

Schematic illustration. Source: Credit Suisse

January 2017 Asset Management 29 The disclaimer at the end is also applicable to this page.

Risks

There is no guarantee that losses can be avoided or that investment objectives will be achieved

The fund may have exposure to emerging markets which, by their nature, are riskier than developed

markets

Operational risks from deficient processes, technical failures or catastrophic events may cause losses

Political and legal risks: Investments are exposed to changes of rules and standards applied by specific

countries

January 2017 Asset Management 30 The disclaimer at the end is also applicable to this page.

Disclaimer

This document was produced by Credit Suisse AG and/or its affiliates (hereafter “CS”) with the greatest of care and to the best of its knowledge and belief. However, CS provides no guarantee with regard to its content and completeness and does not accept any liability for losses which might arise from making use of this information. The opinions expressed in this

document are those of CS at the time of writing and are subject to change at any time without notice. If nothing is indicated to the contrary, all figures are not audited. This document is provided for information purposes only and is for the exclusive use of the recipient. It does not constitute an offer or a recommendation to buy or sell financial instruments or banking services and does not release the recipient from exercising his/her own judgment. The recipient is in particular recommended to check that the information provided is in line with his/her

own circumstances with regard to any legal, regulatory, tax or other consequences, if necessary with the help of a professional advisor. This document may not be reproduced either in part

or in full without the written permission of CS. It is expressly not intended for persons who, due to their nationality or place of residence, are not permitted access to such information under local law. Neither this document nor any copy thereof may be sent, taken into or distributed in the United States or to any U.S. person (within the meaning of Regulation S under the US Securities Act of 1933, as amended). Every investment involves risk, especially with regard to fluctuations in value and return. Investments in foreign currencies involve the additional risk that the foreign currency might lose value against the investor's reference currency. Historical performance indications and financial market scenarios are not reliable indicators of current or

future performance. Performance indications do not consider commissions levied at subscription and/or redemption. Furthermore, no guarantee can be given that the performance of the benchmark will be reached or outperformed.

Emerging market investments usually result in higher risks such as political, economic, credit, exchange rate, market liquidity, legal, settlement, market, shareholder and creditor risks. Emerging markets are located in countries that possess one or more of the following characteristics: a certain degree of political instability, relatively unpredictable financial markets and economic growth patterns, a financial market that is still at the development stage or a weak economy.

Equities are subject to market forces and hence fluctuations in value, which are not entirely predictable. The investment funds mentioned in this publication have been established under Luxembourg law as undertakings for collective investment in transferable securities (UCITS) subject to EU

Directive 2009/65/EC, as amended. Subscriptions are only valid on the basis of the current sales prospectus, key investor information document (KIID) and the most recent annual report (or half-yearly report, if this is more recent). These and the funds management regulations and/or articles may be obtained free of charge, in English, from Credit Suisse Fund Management S.A., 5, rue Jean Monnet, L-2180 Luxembourg.

Copyright © 2017 Credit Suisse Group AG and/or its affiliates. All rights reserved.