credit appraisal of tjsb bank

DESCRIPTION

Credit Appraisal of TJSB BankTRANSCRIPT

GENESIS OF THE PROJECT

The project is on Credit Appraisal Process of TJSB Bank. Credit Appraisal is an

important activity carried out by the Special Credit Cell department of the bank which

determines whether to accept or reject the proposal for finance. It means an

investigation or assessment done by the bank before providing any Loans and Advances

or Project finance and also checks the commercial, financial and technical viability of

the project proposed, its funding patterns and further check the primary and collateral

security cover available of recovery of such funds.

It is the process of appraising the credit worthiness of a Loan applicant. Factors like

age, income, number of dependents, nature of employment, continuity of employment,

repayment capacity, previous Loans, credit cards, etc. are taken into account while

appraising the credit worthiness of a person.

Proper assessment of credit risk is important as it helps in establishing credit limits. In

assessing credit risks the 5 C’s of credit are crucial & relevant to all borrowers/ lending,

which must be kept in mind, at all times.

Character: The willingness of the customer to honor his obligations. It reflects

integrity, a moral attribute that is considered very important by credit managers.

Capacity: The ability of the customers to meet credit obligations from the operating

cash flows.

Capital: The financial reserves of the customers. If the customer has problems in

meeting credit obligations from operating cash flow, the focus shifts to its capital.

Collateral: The security offered by the customer in the form of pledged assets.

Conditions: The general economic conditions that affect the customers.

To get information on the five C’s a Firm may rely on the Financial Statements, Bank

References, Experience of the firm and Prices and yields on Securities.

1

Numerical Credit Scoring: In traditional credit analysis, customers are assigned to

various risky classes on the basis of the five C’s of credit. Credit Analysts may,

however, want to use a more systematic numerical credit scoring system. Such a system

may involve the following steps:

1. Identify factors relevant for credit evaluation.

2. Assign weights to these factors that reflect their relative importance.

3. Rate the customer on various factors, using suitable rating scale.

4. For each factor, multiply the factor rating with the factor weight to get the factor score.

5. Add all the factor scores to get the overall customer rating index.

6. Based on the rating index, classify the customer.

OVERVIEW OF LOANS

Loans can be of two types fund base & non-fund base:

Fund Base includes:

Working Capital

Term Loan

Non-fund Base includes:

Letter of Credit

Bank Guarantee

2

BACKGROUND OF THE BANKING SECTOR

DEFINITION OF A BANK

The word bank has originated from English word Banco, Bancus or Banque. Its

meaning is bench or table. In Europe in the middle age, the money transactions were

undertaken sitting on a bench.

As per Indian Banking Act, “A service to accept deposits from people with the

intention to invest or lend with the condition of returning it immediately whenever

demanded at any predetermined time. An institute this service is Bank”

Banking is a service helpful to the business, its function is to borrow money from

people and further lend the same. While analyzing definition of bank as per Indian

Banking Act, below mentioned matters are clarified:

(1) Bank accepts monetary deposits from people.

(2) The intention behind accepting these deposits is to invest or lend the respective fund.

(3) The function of accepting deposit or lending money is made under the condition that on

demand or as predetermined otherwise the same amount has to be refunded immedi-

ately.

(4) The institution doing this type of business is called bank.

The banking sector is dominated by Scheduled Commercial Banks (SBCs). As at end

March 2002, there were 296 Commercial banks operating in India. This included 27

Public Sector Banks (PSBs), 31 Private, 42 Foreign and 196 Regional Rural Banks.

Also, there were 67 scheduled co-operative banks consisting of 51 scheduled urban

cooperative banks and 16 scheduled state co-operative banks.

State Bank of India is still the largest bank in India with the market share of 20% ICICI

and its two subsidiaries merged with ICICI Bank, leading creating the second largest

bank in India. Higher provisioning norms, tighter asset classification norms, dispensing

with the concept of ‘past due’ for recognition of NPAs, lowering of ceiling on exposure

to a single borrower and group exposure etc., are among the measures in order to

improve the banking sector.

3

A minimum stipulated Capital Adequacy Ratio (CAR) was introduced to strengthen the

ability of banks to absorb losses and the ratio has subsequently been raised from 8% to

9%.

Retail Banking is the new mantra in the banking sector. The home Loans alone account

for nearly two-third of the total retail portfolio of the bank. According to one estimate,

the retail segment is expected to grow at 30-40% in the coming years.

Net banking, phone banking, mobile banking, ATMs and bill payments are the new

buzz words that banks are using to lure customers.

With a view to provide an institutional mechanism for sharing of information on

borrowers / potential borrowers by banks and Financial Institutions, the Credit

Information Bureau (India) Ltd. (CIBIL) was set up in August 2000. The Bureau

provides a framework for collecting, processing and sharing credit information on

borrowers of credit institutions. SBI and HDFC are the promoters of the CIBIL.

The RBI is now planning to transfer of its stakes in the SBI, NHB and National bank

for Agricultural and Rural Development to the private players. Also, the Government

has sought to lower its holding in PSBs to a minimum of 33% of total capital by

allowing them to raise capital from the market. Banks are free to acquire shares,

convertible debentures of corporate and units of equity oriented mutual funds, subject

to a ceiling of 5% of the total outstanding advances (including commercial paper) as on

March 31 of the previous year.

4

CLASSIFICATION OF BANKS:

The Indian banking industry, which is governed by the Banking Regulation Act of

India 1949 can be broadly classified into two major categories, non-scheduled banks

and scheduled banks. Scheduled banks comprise commercial banks and the co-

operative banks. In Terms of ownership, commercial banks can be further grouped into

nationalized banks, the State Bank of India and its group banks, regional rural banks

and private sector banks (the old / new domestic and foreign). These banks have over

67,000 branches spread across the country. The Indian banking industry is a mix of the

public sector, private sector and foreign banks. The private sector banks are again spilt

into old banks and new banks.

Banking System in India

Reserve bank of India (Controlling Authority)

Development Financial institutions Bank

IFCI IDBI ICICI NABARD NHB IRBI EXIM Bank SIDBI

Commercial Regional Rural Land Development Cooperative Banks

Banks Banks Banks

Public Sector Banks Private Sector Banks

SBI Groups Nationalized Banks Indian Banks Foreign Bank

5

About Co-operative Bank

A Co-operative bank is financial entities which belongs to its members, who are at the

same time the owners and customers of their bank. Co-operative banks are often

created by persons belonging to the same local or professional community or sharing a

common interest. Co-operative banks generally provide their members with wide range

of financial and banking services. (loans, deposits, banking accounts etc).

Co-operative bank differ from stockholder banks by their organization, their goals, their

values and their governance. In most countries, they are supervised and controlled by

banking authorities and have to respect prudential banking regulations, which put them

at a level playing field with stockholder banks. Depending on countries, this control and

supervision can be implemented directly by state entities or delegated to a co-operative

federation or central body. Co-operative banking is retail and commercial banking

organized on a co-operative basis.

Co-operative banking institutions take deposits and lend money in most part of the

world. Co-operative banking institutions take deposits and lend money in most parts of

the world. It includes retail banking, as carried out by credit unions, mutual savings and

loan associations, building societies and co-operatives, as well as commercial banking

services provided by mutual organizations to co-operative businesses.

The structure of commercial banking is of branch –banking type , while the co-

operative banking structure is a 3 tier federal one .

- A state Co-operative bank works at the apex level ( i.e. .works at state level )

- The central Co-operative bank works at the intermediate level. (i.e.District Co-

operative banks ltd. works at district level )

6

INTRODUCTION OF TJSB BANK

Since 1972 TJSB is in co-operative field, the dynamism infused by the Board of

Directors, unflinching loyalties of clientele and devotion of staff has propelled the

sound foundation of The TJSB Sahakari Bank Ltd (TJSB) and has emerged as one of

the leading multi state scheduled co-operative Bank in the country

.

Presently TJSB is catering the needs of the society through close network of 63

branches and 1 Extension counters spread all over the city of Thane, Nashik, Navi-

Mumbai, Pune, Aurangabad, Satara, Nagpur, Kolhapur, Goa, Latur& Karnataka. All

these branches has shown remarkable progress. TJSB focusing on business strategy

solely, has created a Visionary Growth Plan for Stakeholders.

Technology Initiatives :

TJSB was successful in implementing the Core Banking Solution which has helped

Bank to migrate the branches from being the processing centers to marketing customer

centric outfits. It also improved Banks multiple deliver channels such as ATM, Internet,

Mobile etc.

TJSB is the first co-operative sector to install Cheque Depositary System in all their 63

branches, which are operational 24 x 7.

TJSB has also placed Real Time Gross Settlement System (RTGS) to customers.

Automated Cheque Issuance Machine was first introduced by TJSB which enable

customers to take Personalized Cheque Book 24 x 7.

7

Business Process Re-engineering:

With the help of Core Banking Solution TJSB has initiated Business Process Re-

engineering by establishing:

• Specialized Credit Cell

• Specialized Retail Banking Cell

• Centralized Monitoring Cell

• Centralized Back office Processing Cell

• E-lobby

Bancassurance:

TJSB act as an agent for Max New York Life Insurance Company Ltd for life insurance

product and with The Oriental Insurance Company Ltd for general Insurance.

Business Expansion Plan:

Recognizing opportunity, TJSB has done its expansion through Merger and Takeover of

the other Banks. It has recently acquired two Pune based Co-operative Banks namely

The Navjeevan Nagrik Sahakari Bank Ltd and The Sadguru Jungli Maharaj Sahakari

Bank Ltd.

Rewards and Recognition :

TJSB was awarded as TECHNOLOGY BANK OF THE YEAR in the Co-operative

Bank Category for Financial Year 2009.

TJSB has got 1st prize for The Best Co-operative Bank in Maharashtra by “Maharashtra

State Urban Bank’s Federation Ltd” for the Financial year 2004-2005.

TJSB has been awarded 1st prize as “Padmabhushan Vasandada Patil Utkarsha Nagri

Sahakari Bank” for the financial year 2003-2004 from Kokan Region for the second

time consecutively,

TJSB was recognized amongst top 5 co-operative banks in the country, during cente-

nary celebration of Co-operative movement by Kalupur Commercial Co-operative

Bank

8

Organisation Structure -TJSB

BOARD

CEO

CGM

GM

GM GM (Credit, Audit, HR) (IT)

DGM

Forex Accounts PCRO

AGM

Recovery Credit SCC Audit & Admin IT Vigilance

Managers

Officers

9

OBJECTIVES AND SCOPE OF THE PROJECT

Objectives and scope:

To study the credit appraisal system in banks.

To understand the commercial, financial & technical viability of the proposal proposed

and it’s finding pattern.

To study the various funded and non-funded credit facilities offered by the bank

Scope of my project is to know the Credit Appraisal in Co-operative Bank. What are

the parameters and risk factors are taken into consideration in Credit process. How

Specialize Credit Cell (SCC) works.

10

RESEARCH METHODOLOGY

1. Descriptive Research:

TJSB Bank sanctions the limits after proper appraisal of the genuine working capital

requirements of the borrowers keeping in mind their business cycle and short term

credit requirement. Relationship between Credit score and Ratios helps us to know

whether bank has taken viable decision before granting loans.

2. Sampling:

As no Primary data was collected, the whole conclusion was made on the basis of

Secondary data. No Sampling is done.

3. Data Analysis:

Data Analysis is done by using Correlation analysis. In Correlation it explains the

relationship between the Rating and Ratios. Rating is the total score obtained by each

customer based on the various financial parameters. It covers financial risk, Business

Risk, Management Risk and Industry risk. Different Ratios are taken in consideration

such as, Current Ratio, Collateral Coverage, Cash Accruals and TOL-QE/TNW+QE.

11

Literature review

Literature review provides available research with respect to the selected topic of the

projector research findings by an author which has been done with respect to the

research to research topic. This chapter provides the overall view of the available

literature with respect to the topic of the project. The review of the related research

works are described as under:-

1. A researcher Machiko Nissanke, Ernest Aryeetey in their book: Financial Integra-

tion and Development explained about the loan administration and risk reduction by

formal lenders(i.e. banks), Credit Analysis Standards, Increase Project equity require-

ments, Loan screening of banks and assessing creditworthiness during screening. Banks

consider return on project as an important indicator for appraising the projects

2. A research was conducted by Mr. V.M.V. Subha Rao, on “Monitoring of Advances -

A New look”. The research gave two views on the commencement of monitoring

process-(i)Narrow view- the monitoring starts only after the advance is disbursed,

(ii)Broad view- at the time of conducting credit investigation of the borrower continue

in all other stages of credit cycle.

3. Mritunjay Kumar Pandey conducted a study on Financial Performance Appraisal of

TISCO. The Objectives of the study was to check the profitability and efficiency of the

firm in the near future, to give brief summery about the ratios which affect the organi-

zation‟s financial structure and to point out the relationship between ratios and reasons

behind it.

4. Eleanor Charles in his paper “Appraising the Role of the Appraiser”, talked about the

centralized function of the appraiser to grant the loan and virtually every loan applicant

will have to rely on an appraisal to set a value on the property against which the loan is

to be made.

12

TJSB BANK – CREDIT RATING OF SME’s

About SMEs

In India, small and medium enterprise (SME) is a generic term used to describe small

scale industrial (SSI) units and medium-scale industrial units. Any industrial unit with a

total investment in its fixed assets or leased assets or hire-purchase asset up to Rs10

million is considered as a SSI unit and investment up to Rs. 100 million is considered

as a medium unit. In addition, an SSI unit should neither be a subsidiary of any other

industrial unit nor can it be owned or controlled by any other industrial unit.

The SME sector produces a wide range of industrial products such as food products,

beverage, tobacco and tobacco products, cotton textiles, wool, silk, synthetic products,

jute, hemp & jute products, wood & wood products, furniture and fixtures, paper &

paper products, printing publishing and allied industries, machinery, machines,

apparatus, appliances and electrical machinery. SME sector also has a large number of

service industries.

TJSB Bank Services to SMEs

TJSB Bank has special focus for extending credit facilities to Small and Medium Size

Enterprises. Bank has customized solutions for Small Business Enterprises, Small Scale

Industries and Medium Scale Industries. Credit Facilities are offered in the nature of

Term Loans for establishment of new industries, acquisition of machineries, technology

up-gradation, or execution of ad-hoc orders or for expansion, modernization or

diversification programs. Finance offered will be in the form of Fund base as well as

non fund base facilities as per the requirements of the Business. Working Capital Term

Loan requests are considered for viable small and medium size enterprises requiring

infusion of fresh funds by way of one time core working capital assistance.

Products:

13

Establishment \ modernization \up-gradation of Fixed Assets: Bank provide property

loans to SME for purchase of factory premises &modernization of existing factory

building. They also offer hypothecation loans to SME’s for purchase / import of ma-

chinery

Setting up Office, Renovation of the premises: Bank offer property loans to SME to

set-up the business office & branch office for the expansion of business plans. They

also offer term loans to renovate existing office premises.

Purchase of commercial vehicles: Bank offer hypothecation loan to the transport opera-

tors to purchase new commercial vehicles such as Buses, Trucks, Tempo, etc.

Working Capital Limits: Bank offer credit facility in the form of Cash Credit limit,

Working capital term loan to the SME’s against the hypothecation of stock & Book

Debts. It helps to meet working capital requirement and Short term financial need.

Project Finance: Bank offer project finance loans to technically qualified, trained and

experienced Entrepreneurs to execute the prestigious orders in hand.

Export Finance:

Pre-shipment Credit

Pre-shipment Credit facility is offered to an exporter by way of packing credit to enable

him to purchase/import of raw materials, processing and packing of the goods meant

for export order.

Post –shipment credit

Post-shipment Credit facility is offered to an exporter to finance export bills receivables

after the date of shipment of goods till the date of realisation of export proceeds on sub-

mission of documents.

Fund Base:

14

Working capital

Funds required for day to-day working will be to finance production & sales. For

production, funds are needed for purchase of raw materials/ stores/ fuel, for

employment of labour, for power charges etc. financing the sales by way of sundry

debtors/ receivables.

Capital or funds required for an industry can therefore be bifurcated as fixed capital &

working capital. Working capital in this context is the excess of current assets over

current liabilities. The excess of current assets over current liabilities is treated as net,

for storing finishing goods till they are sold out & for working capital or liquid surplus

& represents that portion of the working capital, which has been provided from the

long-Term source.

Term Loan

A Term Loan is granted for a fixed Term of 3 years to 7 years intended normally for

financing fixed assets acquired with a repayment schedule normally not exceeding 8

years.

A Term Loan is a Loan granted for the purpose of capital assets, such as purchase of

land, construction of, buildings, purchase of machinery, modernization, renovation or

rationalization of plant, & repayable from out of the future earning of the enterprise, in

installments, as per a prearranged schedule.

Non-fund Base:

Bank Guarantee Limits & Letter of Credit limit:

Bank offer to issue various types of guarantees such as performance, financial, bid

bond, tenders, customs etc & we have tie-up with Nationalised Banks also to issue BG.

They also issue inland letter of credit facility to our customers to purchase raw material,

machinery etc. They also have tie-up with Nationalised Banks to issue foreign letter of

credit to import machinery, raw material etc.

Eligibility:

• Individuals/Partnership Firms/Companies.

15

• Experience /qualification in the proposal line of activity..

Loan Amount:

• Cash credit limit, Property loan & Hypothecation loan will be assessed according to the project requirement.

Rate of interest:

• Bank’s PLR is 13.50 % p.a. & Bank offer attractive rate of interest to SME’s

based on their credit ratings.

Security:

• Hypothecation of Asset financed

• Mortgage of immovable property

• Personal Guarantee of Director / Partner.

Period:

• Period for cash credit account will be of 12 months and limits being renewed

yearly.

• Period for Terms loans will be 36 months to 84 months.

• Moratorium period will be 6 months.

• Period for project finance variable from project to project and reviewed on yearly

basis.

TJSB Bank Commercial Loan Processing:

16

The commercial loans provide an attractive source of income in terms of interest,

lenders exercise a lot of care and study in evaluating borrowers to ensure that funds lent

out are along with the earnings.

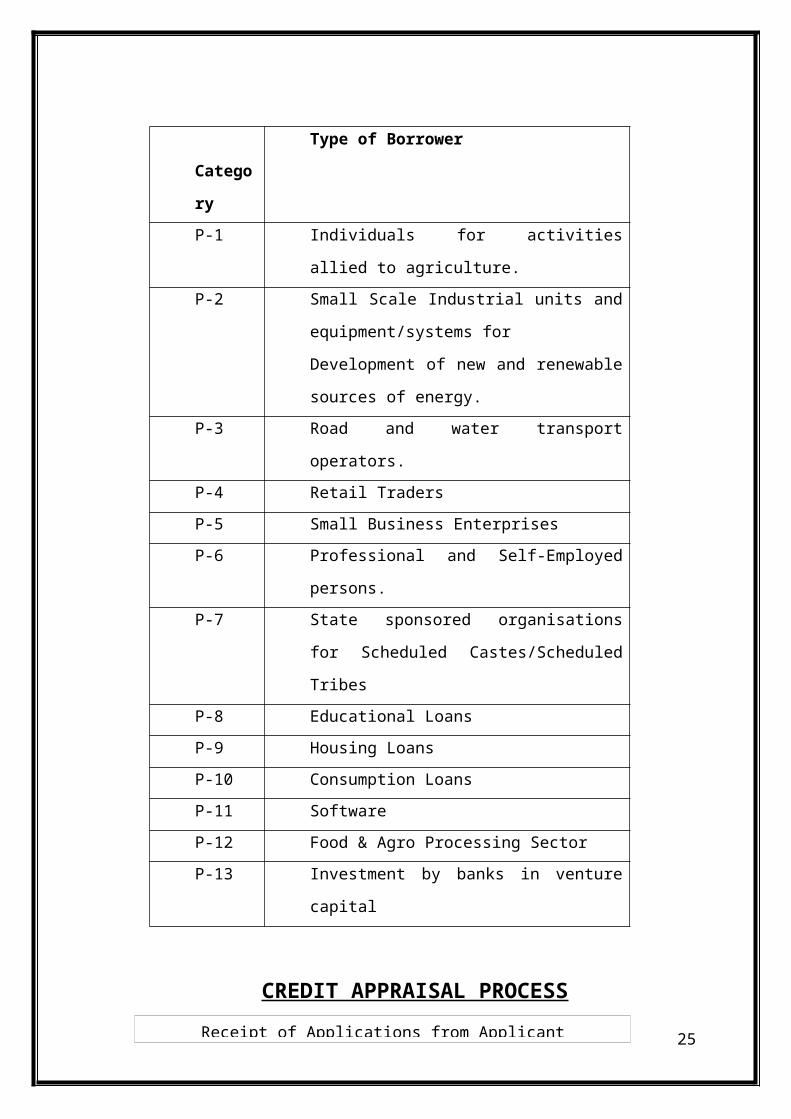

TJSB Bank provides separate loan for different categories of borrowers. The loan

application form contains information relating to Background of borrower, personal and

professional details, purpose of loan, nature of facility, period of repayment, nature of

security offered, and financial status of borrower.

Types of Borrowers

Category

Type of Borrower

P-1 Individuals for activities allied to agriculture.

P-2 Small Scale Industrial units and

equipment/systems for

Development of new and renewable sources of

energy.

P-3 Road and water transport operators.

P-4 Retail Traders

P-5 Small Business Enterprises

P-6 Professional and Self-Employed persons.

P-7 State sponsored organisations for Scheduled

Castes/Scheduled Tribes

P-8 Educational Loans

P-9 Housing Loans

P-10 Consumption Loans

P-11 Software

P-12 Food & Agro Processing Sector

P-13 Investment by banks in venture capital

CREDIT APPRAISAL PROCESS

17Receipt of Applications from Applicant

Required Documents for Process of Loans

18

Communicate with client documents required for the said proposal

Follow-up Sheet

Pre-sanction visit by bank officers

Check for RBI defaulters list, CIBIL data, ECGC, Caution list etc

Assessment of proposal

Title clearance reports of the properties to be obtained from Empanelled

Valuation reports of the properties to be obtained from Empanelled

Preparation of financial data

Proposal preparation

Sanction/approval of proposal by appropriate sanctioning authority

Documentation, agreement, mortgages, pre-disbursement requirements

Disbursement of loans

Post sanction activities

1. Audited / Provisional P& L A/c, Balance Sheet for Current Year i.e. upto31.03.2012.

2. IT Return Copy of the Firm for A.Y 2012-2013 or latest filed.

3. Reason for increase or decrease (as applicable) in sales / net worth / profits in compari-

son with earlier year’s figures.

4. Month wise Sales & Purchase for Current year April 2012.

5. Latest Debtors / Creditors / Stock statements. (Debtors statement should be age-wise)

6. Projected sales turnover of the Firm for, 2012-2013.

7. I.T Returns copy along with individual Balance sheet of all partners / Directors / Propri-

etors for A.Y 2012-2013 (F.Y 2011-2013) or else latest filed.

8. Approximate amount of Bad Debts as on last month.

9. Undertaking for No change in constitution.

10. Current status of payments of statutory dues (E.g. PF/Excise/Sales Tax etc) Salary/LIC

deductions etc.

11. Copy of Sales Tax annual returns for F.Y 2011-2012 and copy of latest return filed in

2012-2013, if applicable.

12. Statement of payment of statutory dues as on 31.03.2012 duly certified by CA.

13. Dully filled CC Renewal form signed by Borrowers / Guarantors.

14. Board Resolution for Renewal Credit limits. (Incase of PVT Ltd and Ltd Company).

15. Guarantors ITd Return Copies along with Balance sheet, Profit & loss A/c for F.Y.

2011-2012.

16. Xerox copy of registration certificate under shop and establishment Act, 1948.

Credit Rating of TJSB Bank

19

Credit Rating is done before sanctioning any finance to customer. Under this method

marks are assigned to each of the parameters.

The following are the parameters have been considered for determining the rating of

borrowers in the SME category:

Financial Risk

Business Risk

Industry Risk

Management Risk

Within each of these broad areas, various parameters have been used for obtaining an

overall rating of the borrower. The total marks a borrower can be awarded on being

analyzed using these parameters shall be 100.

Marks Obtained By Borrower

Weighted Marks in % =

Total Marks assigned to various Parameters

As per Banks guideline, concession in Rate of Interest is provided which is subject to

credit rating of the borrower.

The Credit Rating Scale to be used to rate the applicant is as follows:

1) PRIMARY REQUIRE-

MENTS :

20

Marks of the

Applicant

Rating of the

Applicant

75 & Above A+

Between 60 to75 A

Between 50 to

60

B

Between 35 to

50

C

Between 0 to 35 D

A business loan requires detailed documents stating entire business profile that states

the general background of the business and its operations. Borrower is required to

primarily submit personal financial statements listing all the assets and liabilities,

income tax details along with audited profit & loss account and balance sheet of

previous 2 to 3 years along with current year. Bank may also demand borrower to

submit estimated future projections and statements, expansion plans and details of

guarantors.

Security

Another fundamental requirement for loan application is details of Prime and collateral

security offered by the borrower. Collateral Security for loan may include assets such as

real estate, stocks or bonds, hard goods such as machinery & equipment and various

other personal assets.

To ensure the safety of funds lent, the first and most important factor considered by a

bank is the capacity of borrowers to repay the amount of loan but bank can hardly

afford to take any risk in this regard. The bank therefore relies primarily on the nature

of security offered by the borrower. In case borrower fails to repay the amount banks

recover money by attaching the assets. Bank can sell the assets offered as security and

realise the amount.

For security purpose banks create charge on assets offered by borrower in

following ways:

a. Hypothecation:

It is the most common and popular mode of charge whose important features are as

under

It is not defined under any law.

Extended idea of pledge.

It relates to goods/commodities, movable machinery, vehicles, book-debts.

Ownership remains with the borrower.

21

Possession is also with the borrower.

Symbolic/constructive possession with creditor (Bank).

It creates an equitable charge.

Hypothecation Agreement gives Banker a right to take possession of hypothecated

goods, machines.

b. Pledge:

Under section 172 of Indian Contract Act pledge means “Bailment of Goods as a

security for repayment of a debt or performance of a promise”.

A common example of pledge is gold ornaments, which are pledged with the bank

as a security against which Gold Loan is given.

Important features of Pledge are –

Actual delivery of security is given to the Bank.

Ownership remains with bailers (Borrower).

Liable to return after fulfillment of promise or repayment of loan amount.

Disposal possible only after default and giving due notice to the Borrower.

c. Mortgage:

Transfer of Property Act 1882 defines Mortgage as: -“Transfer of an interest in specific

immovable property for the purpose of securing the payment of money advanced by

way of loan, on existing or future debt or the performance of an engagement which may

give rise to pecuniary liability”.

Mortgagor must be the owner or a person having interest in immovable property.

Mortgagor must have a contractual capacity.

Property must be a specific immovable property.

Purpose is to secure the loan repayment.

2) PROCESSING APPLICATION :

22

After receiving all the required documents from the borrower a loan officer will then

review the application and documentary attachments. Loan officer will then analyse and

review various credit reports, documentation as well as income details provided by the

borrower.

There are three principals of bank lending:

Safety: As Bank lends funds entrusted to it by the depositors, the first and foremost

principal of lending is to ensure safety of the funds lent. Safety mean by capacity and

willingness of borrower to repay.

Liquidity: Liquidity mean by granting loan against security of assets which are easily

marketable without much loss.

Profitability: The sound principle of lending is not to sacrifice safety or liquidity for

the sake of higher profitability. Bank should not grant advances to unsound parties even

if they are ready to pay high interest.

Bank therefore has to consider creditworthiness of borrower, borrower’s background,

soundness of his project or business activity. Banker has to ensure that the business of

the borrower is permissible for lending as per the guidelines & policy of the bank. For

assessing credit worthiness of borrower, banker has to collect information through

number of sources.

This is important stage in loan process as it involves preparation of Process Note, and

analysis of loan application. Important steps carried out by loan officer are as follows.

Analysis of financial statements:

23

Banks approach towards analysis of financial statement is to find and study the

solvency or repaying capacity of the borrower. Bank is concerned with the estimation

of the risks if any, involved in lending to the borrower.

Processing officer carefully analyses all the financial statements and records of the

borrower. Financial Statement analysis assists the loan officer in assessing the financial

and administrative efficiency of the borrower. Various financial ratios are calculated

and trend analysis is carried out to check the consistency and growth of business.

Various recommendations and observations are drawn based on the ratios.

Ratios computed are as follows:

Tangible Net Worth

Debt-Equity Ratio

Unsecured Loans

Asset Turnover Ratio

Liquidity Ratio

Sales

Profitability & DSCR

Visit Report

Loan processing officer conduct visit to the commercial or factory site of the borrower

and also to its registered office for inspection. Objective behind visit is to verify the

operational setup and soundness of the borrower in respect of loan. After the visit

detailed visit report is prepared containing observations of visit and recommendations.

Working Capital Assessment :

24

Working capital facilities are required by industries .trading concerns and also units

engaged in extending services. Need of working capital in majority of cases remain

more or less constant throughout the year.

Methods of Assessment of working capital

a. Maximum Permissible Bank Finance (MPBF) Method:

Audited financial statements of last two years have to be studied. The data in Profit &

Loss Statement & in the Balance Sheet in whatever format is first reconstructed in the

prescribed format.

The total build-up of current assets & current liabilities is to be studied. The inventory,

Debtors & Creditors which have been expressed in the monetary terms in balance sheet

should be converted into holding into months or days.

Current assets & current liabilities are assessed based on projected sales.

Finding the Working Capital Gap & deciding the contribution of Borrower & Banks

contribution for bridging the Gap

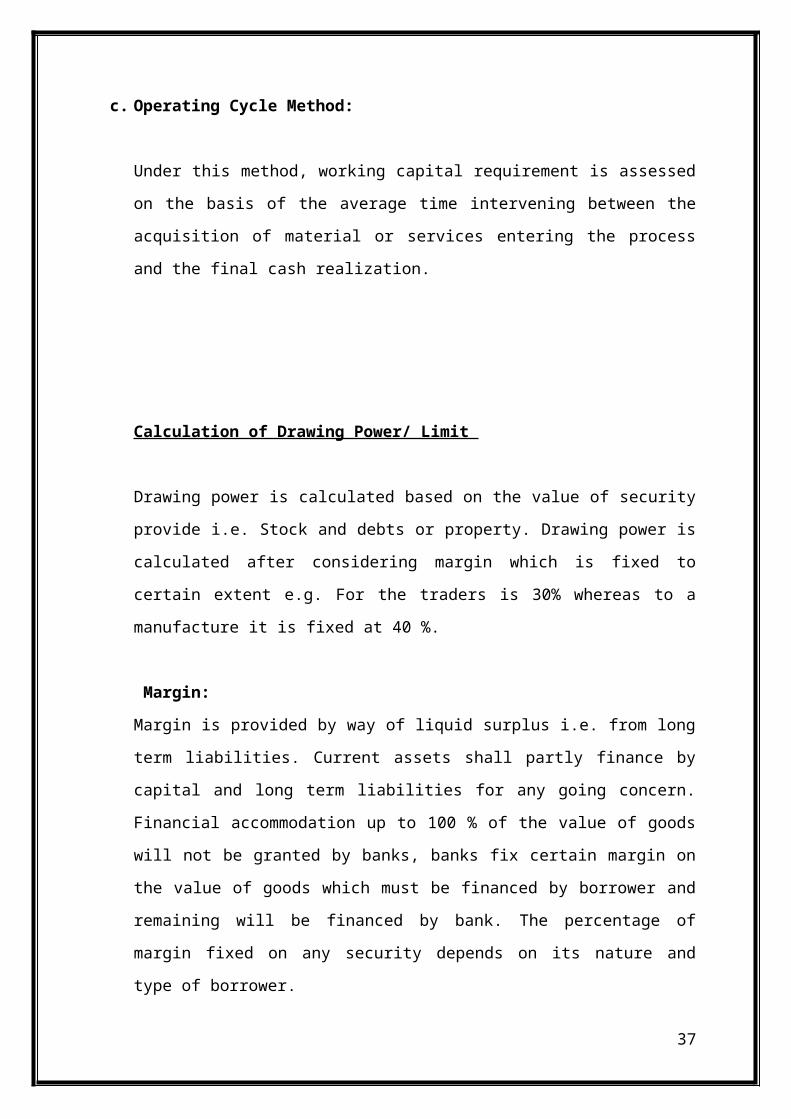

b. Turnover Method:

Under this method, working capital is assessed on the basis of 20% of the projected /

actual sales of the borrower.

c. Operating Cycle Method:

Under this method, working capital requirement is assessed on the basis of the average

time intervening between the acquisition of material or services entering the process

and the final cash realization.

Calculation of Drawing Power/ Limit

25

Drawing power is calculated based on the value of security provide i.e. Stock and debts

or property. Drawing power is calculated after considering margin which is fixed to

certain extent e.g. For the traders is 30% whereas to a manufacture it is fixed at 40 %.

Margin:

Margin is provided by way of liquid surplus i.e. from long term liabilities. Current

assets shall partly finance by capital and long term liabilities for any going concern.

Financial accommodation up to 100 % of the value of goods will not be granted by

banks, banks fix certain margin on the value of goods which must be financed by

borrower and remaining will be financed by bank. The percentage of margin fixed on

any security depends on its nature and type of borrower.

Thus Process note comprise of entire analysis of the loan application and borrower

including drawing power of the borrower, his working capital requirements, security

details, valuation reports, details of guarantors, financial statement analysis, visit report

and other terms and conditions of sanctioning of loan. Once process note is completed

it is forwarded to sanctioning authority for final review and assessment

3) APPLICATION REVIEW AND SANCTIONING OF LOAN

After the loan application is processed and all the findings are satisfactory, the loan

application is then submitted to sanctioning authority. Sanctioning authority then

assesses and eventually decides whether the loan will be approved.

Sanctioning authority & Delegation of Authority

To regulate the deployment of the credit as well as for speedy sanction and disposal of

the credit, the Board of Directors of the bank determines the lending and discretionary

powers of various authorities at different level.

As per the level of the official from Manager to CEO powers are assigned for sanctions.

Authority includes per party Exposure, Group exposure, Funded and Non -funded

26

limits, Waiver in processing fee, concessions in Interest rate etc. Board is the apex level

of authority and all the proposals beyond the powers of CEO will be looked into by the

Directors. Board of Directors also formulates overall policy of the bank with regard to

credit.

Insurance Details of the assets and securities offered by the borrower against the loan

are also mandatory to ensure credit recovery. Hence the details of amount of insurance

along with the insuring company and their due dates are mentioned in process notes.

After the approval from the sanctioning authority the processing officer then forwards

the sanction letter to the borrower. Sanction letter includes amount of financing, terms

& conditions of payment, details of Prime and collateral security, and other conditions

regarding loan sanction.

4) Loan Disbursement

Once borrower is agreed on all the conditions mentioned in sanction letter, Borrower is

required to sign final set of loan documents. With all the requirements met and all

closing documents in order, loan officer generates Disbursement Order (DO) and loan

is finally disbursed.

Documentation

Banks generally lend for productive purpose. Documentation is done to create legally

valid and effective charge over assets which bind the borrower and guarantors

personally. Documents contains specifically and precisely the terms and conditions to

the contract between the borrower and bank. Which is examined by the court of law

incase of legal recourse. It is therefore necessary that right type of documents properly

filled up, adequately stamped and executed are obtained on record.

Purpose and importance of documentation

27

Documents are prepared and executed to record the fact that borrower has taken a loan

from the Bank and thereby evidence is created. The second purpose of documents is to

incorporate the terms and conditions on which the loan has been given. This is very

necessary to avoid confusion and ambiguities in future. The third important purpose is

to create a charge in favour of the Bank on the assets offered as a security.

By and large the loans are repaid by the Borrowers as per agreed terms and conditions.

But when the Borrower fails to repay or does not adhere to the agreed terms and

conditions, the Bank has to take action. It may be by way of realizing the asset given as

security or enforce the agreed terms and conditions or to take legal action to recover the

bank dues. At that time the loan documents prepared and executed are required to

produce. Documents, which are not properly executed, cannot be enforced against the

borrower and their purpose itself is defeated.

REGISTRATION OF CHARGES OF COMPANIES WITH ROC

The charge on the assets of the company created in favour of the Bank as security for

loan is required to be registered with Registrar of Companies. Failure to do so renders

such charge void as against liquidator or other registered creditors. Thus in order to

protect the interest of the Bank every charge created in favour of the bank needs to be

registered.

The registration of charge is a notice to the general public of Banks charge on the assets

of the company. Charges such as hypothecation, mortgage requires registration. The

charge is required to be registered within a period of 30 days from the date of creation.

The delay, however, can be condoned by the Registrar of Companies.

For creation of charge Form No 8 together with the original instrument creating a

charge or certified copy is to be filed with the Registrar. Requisite fee prescribed is also

to be paid. Registrar after due verification of the charge form and registering the charge

on company’s records with him issues a certificate of Registration of Charge.

28

Where a modification of charge is to be done e.g. when limit is enhanced, additional

security is charged etc Form No 13 is also to be filed along with Form No 8. Procedure

for filing modification of charge is similar to filing original charge.

Post Sanction Monitoring Of Advances

The most important stage in the loan begins after the full disbursal of the loan. All the

care taken in appraising the project will be nullified due to faulty monitoring. Thus a

good asset/loan account can turn bad for the bank if danger signals or negative

indicators are not looked into or analysed properly.

When input cost goes up small industries can come under strain. Depending on their

ability they may either pass on the cost to the customer or absorb the cost or they may

have to sacrifice the profits. In such case accounts will turn bad.

The bank should have a strong monitoring mechanism in place at various levels, which

will help capture the account before it moves into an NPA. Bank should carefully

monitor the end use of funds and see that the funds are used for the purpose intended

for. An advance given for working capital used for trading in stock market increases the

risk of default.

A monitoring mechanism should look out for early warning signs in the following

areas.

Unusual increase in debtor level.

Substantial decline in sales levels.

Status of borrowers with other banks.

Information of group companies.

High projection of sales/ Profits should be analysed.

Correlation Analysis

29

Keeping in mind, the above process of credit appraisal of TJSB, it would be interesting

to understand how the financial ratios form a very important part of determining credit

scores of the borrowers. In order to establish the above relationship, simple correlation

analysis is done between the ratios and the scores. It also helps in knowing whether

bank has taken viable decision before granting loans.

ParticularsScores

RatiosCurrent Ratio

TOL-QE / TNW+QE

Cash Accruals/ Net Sales

Collateral Coverage

Refex Air Ltd 89

0.96 3.21 - 50%

Kulkarni Cranes Ltd 77

0.84 4.87 9% 29%

Moksh Raymond 148 2.11 1.06 3% 427%Oman Laboratories Ltd 128 0.8 1.14 3% 51%Suraj Lifters Pvt Ltd 133

2.45 3.03 -3% 49%

Current Ratio

Current ratio shows the relation between Current Assets and Current Liabilities. In

30

CORREL

ATION

Particulars

(Ratings/Ratios)

Score Obtained

Current Ratio 0.70346368

TOL-QE/

TNW+QE

-0.8451471

Cash Accruals/Net

Sales

-0.7758631

Collateral

Coverage

0.63527706

Correlation the results shows that every enterprise whose rating shows better short term

working capital, which can be easily turned into finished goods within a less debtors

turnover days. If the ratings are been negative then it can be said that debtors may be

responding late.

TOL-QE/TNW+QE

Quasi equity is a debt taken on by a company that has some traits of equity, such as

having flexible repayment options or being unsecured. In total outside liability includes

both liability of bank as well as outside. Negative correlation shows that there is not

much investment made as Quasi Equity.

Cash Accruals

Cash Accrual is the profit earned by company including depreciation. As per the

ratings, accrual income is showing negative sign which says repayable capacity is not

much stronger.

Collateral Coverage

Collateral is "an additional form of security which can be used to assure a lender that

you have a second source of loan repayment. In this, higher the security higher the

ratings. Security is given on behalf of the Term loan and not applicable in Overdraft

and Cash Credit. As Correlation shows positive sign, i.e Bank can able to sustain even

the loan goes unpaid.

OUTCOME OF THE STUDY

31

Credit appraisal is done to check the commercial, financial & technical viability of the

project proposed, its funding pattern & further checks the primary or collateral security

cover available for the recovery of such funds

Credit is core activity of the banks and important source of their earnings which goes to

pay interest to depositors, salaries to employees and dividend to shareholders

Credit and risk go hand in hand

In the business world, risk arises out of:-

o Deficiencies /lapses on the part of the management

o Uncertainties in the business environment

o Uncertainties in the industrial environment

o Weakness in the financial position

A banker’s task is to identify/ assess the risk factors/ parameters and manage/ mitigate

them on continuous basis

These risks have been categorized broadly into financial, business, industrial and man-

agement risks which are rated separately

The assessment of financial risk involves appraisal of the financial strength of the bor-

rower based on performance & financial indicators

To determine the Credit worthiness of a particular customer the above factor mentioned

come into play. All the factors were studied in detail while carrying out the project.

LIMITATION OF THE PROJECT

32

As the credit appraisal is one of the crucial areas for any bank, some of the technicali-

ties are not revealed

As some of the information is not revealed, whatever suggestions generated, are based

on certain assumptions.

Credit appraisal system includes various types of detail studies for different areas of

analysis, but due to time constraint, my analysis is restricted to few sectors.

LEARNING FROM THE PROJECT

33

I had a valuable experience doing my summer internship at TJSB Bank in Thane. The

duration for my internship was 2 months, starting from 2nd May 2012 to 2nd 2012 in

Thane Main branch and, I was working on the “CREDIT APPRISAL”

My Project Guide was Mr. Pravin Pandurang Pandit, Chief Executive officer for Thane

SCC branch, respectively of his department.

This was my First exposure to the corporate world and had an experience of working in

banking. I was working on the credit appraisal, which I feel is the basic requirement of

any bank. While working I observed the significance of the Credit in a bank, its

working.

The project, which was given to me in this period of my summer internship, project was

to know the credit appraisal. For that, I have to talk to manager and try to understand

concept of credit in the bank.

Thus during this internship-period working on project and simultaneously observing

has proved to be a great experience in all as I have got to see and understand various

situations of the employees. I would like to conclude by saying that it is been a great

learning for me through this internship. I understand some realities of the bank, as I was

part of the everyday activities of the organization. I also learned the fact that no

department can work on its own each department have to depend on other in one-way

or the other.

BIBLIOGRAPHY/REFERENCE

34

BIBLIOGRAPHY

Financial Management, Theory and Practice (Seventh Edition)

-Prasanna Chandra

Link

www.rbi.org.in

www.thanejanata.co.in

www.dsir.gov.in

www.sidbi.com

www.ijmra.us

Reference

Business Standards

35

Co-operative Banks (Seasonal Article), May 2012

ANNEXURE PROCESS NOTE SPECIMEN

36

.

Branch: SCC/ Date: 12.06.2012

NOTE TO BE PLACED BEFORE

NAME OF APPLICANT :

(Membership No:)

A. PRESENT PROPOSAL :

B. BRIEF BACKGROUND :

1. CONSTITUTION :

2. ASSET CLASSIFICATION :

3. ADDRESS :

FACTORY: (Owned/Rented/Leased) :

OFFICE: (Owned/Rented/Leased) :

4. DATE OF ESTABLISHMENT :

5. BANKING SINCE :

6. CATEGORY :

7. ACTIVITY:

(a) Main Activity :

(b) Industry :

(c) List of major clients :

37

8. NAME(S) OF DIRECTORS/PARTNERS/PROPRIETOR & THEIR NET WORTH

(Amount in RsLacs)

NAME AG

E

ANNUA

L

INCOM

E

NETWOR

TH

9. NAME OF THE GUARANTORS OTHER THAN DIRECTORS / PARTNERS /

PROPREITOR & THEIR NET WORTH (Amount in Rs. Lacs)

NAME AGE ANNUAL

INCOME

NETWORTH

(Specific mention if Directors/ Partners / proprietor are not guarantors in their individual

capacity)

BRIEF ABOUT THE PARTNERS :

ABOUT THE PRODUCTS:

ABOUT THE PRODUCTION PROCESS:

10. POSITION OF ACCOUNT:

10.1 POSITION OF THE ACCOUNT OF FIRM / COMPANY

38

(As on 02.08.201) (Amount in Rs. Lacs)

FACILIT

Y

SAN

C.

LIM

IT

O

/S

B

A

L.

OV

ER

DU

E

INTERE

ST RATE

SECU

RITY

Cash

Credit

ADVHYP

PRLN

TOTAL

DETAILS OF COLLATERAL SECURITY VALUE

Prime

TOTAL SECURITY VALUE

10.2 POSITION OF THE ACCOUNT OF ASSOCIATE FIRM /COMPANY (Not

Applicable)

(As on )

Facility L

i

m

i

t

O/

S

Ba

l

O

v

e

r

D

u

e

s

R

.

O

.

I

.

Primary

Security

Type

Value

Funded [A]

Non Funded

39

[B]

Total [A+B]

Security

details & its

value

Detail Description of security: Value:

TOTAL OF PRIMARY +

COLLATERAL:

Value:

Security Coverage of the Group

NAME OF

A/CEXPOSURE

TOTAL

SECURITIES

%

TOTAL

VALUATION DETAILS:

Name of Valuer

Date of Valuation

Valuation of land Rs.

Valuation of Building / Residential Property Rs.

Valuation of Machinery Rs.

Valuation of Vehicles / Cranes Rs.

Valuation of Dies / Tools and other misc.

equipments

Rs.

DEPOSIT RELATIONSHIP (Amount in

Lacs)

40

12. CONDUCT OF THE ACCOUNT:

a) General Conduct :

A] TURNOVER

PARTICULARS Credit Debit

Current Year

TOTAL

1) General Conduct :

2) Comments on Turnover: Comments on turnover: (Diff. in turnover / Multiple Banking arrange-

ments / Submission of Bank a/c statements of the Banks etc)

B] DRAWING POWER

Drawing Power (As on 30.06.2011)

Particulars Debtors up to

90 days

Upto180

days

Entire

Debtors

Stock

Add: Debtors

Sub total (a)

Less Creditors

Sub total (b)

Margin © = @ 30 %

41

S

r

n

o

PARTICUALA

RS

TOTAL

AMOUN

T OF

DEPOSI

T

COLLATER

AL

SECURITY

FREE

DEPOSI

TS

a.

TOTAL

of (b)

Drawing Power (b-c)

Average Drawing Power Rs.

Whether operations within DP :

iv) Date of Last Renewal

13. TOTAL EARNINGS FROM ACCOUNT:

Previous Year Current Year

i. Interest

ii. Commission

iii

.

Other

TOTAL

VISIT DETAILS:

14.1 Visit Details

Date of

visit

18.08.201

0

14.2 Observations during Visit in Brief:

15. INSURANCE DETAILS

Security Description Amount (in Due Date

42

lacs)

Whether existing securities are adequately insured:

16. Compliance of all Terms and Conditions of earlier sanction (YES/NO)

(If NO – Terms which are pending and reasons, No reason for if YES)

17. A] Noting of Charge with ROC (in case of Ltd./ Pvt. Ltd. Co.)

B] Noting of Charge with R.T.O [For Vehicles / Cranes]

Report only pending compliances with reasons and plans to comply the same.

18. Reserve Bank of India/ Statutory Auditors/Concurrent Auditors/Internal Auditors

observations, if any Steps taken by Branch for compliance of the same.

19. BRIEF FINANCIAL INDICATORS:-

(Rs. In Lacs)

PARTICULARS 2009-10

(AUDITED)

2010-11

(AUDITED)

2011-12

(PROV.)

Tangible Net Worth

Debt /Equity Ratio

Current Ratio

Net Working Capital

Receivables Ratio

Creditors Turnover

Stock Turnover

Net Sales

% of

increase/(decrease)

Net Profit

% to sales

43

Sales from April 10 to

June 10

COMMENTS BASED ON PROVISIONAL FINANCIALS OF 2011-2012 :

1) Tangible Net Worth:

2) Debt-Equity Ratio:

3) Current Ratio & Net Working Capital:-

4) Turnover Ratios:-

5) Net Sales and Profitability:-

6) Future projections / D.S.C.R.:-

DELEGATION POWERS:

Parameters Benchmark Actual

Committee II Committee I

Current Ratio 1.17:1 1:1

TOL/TNW 6:1 8:1

Debt Equity

Ratio

3:1 4:1

DSCR 1.75 1.50

Margin 25% 20%

Repayment Pe-

riods

7 Years 10 Years

Collateral Se-

curity

50% 25%

ROI Not below 13% Not below

12.50%

44

Processing

waiver

25% 75%

Considering deviation in delegation of power in case of collateral security, the note is put

up before Committee I

7) Recommendation

8) TERMS AND CONDITIONS:

Pre-disbursement:

Post-disbursement:

OFFICER CHIEF MANAGER ASST.GEN. MANAGER (SCC) (SCC) (SCC)

Decision of Credit Committee-II

Additional Terms & Conditions :

CHAIRMANCREDIT COMMITTEE-IIDATE:

45