credit appraisal

TRANSCRIPT

A

SUMMER TRAINING REPORT

ON

“CREDIT APPRAISAL”

UNDERTAKEN AT

SUBMITTED BY

TAILOR MAYANKKUMAR DINESHBHAI

MBA (Semester - II) 2010-2011

Enrollment No: 107160592050

UNDER THE GUIDANCE OF:

INTERNAL GUIDE: MRS. NUPUR ANGIRISH

EXTERNAL GUIDE: P.K.VESUNA

SUBMITTED TO

GIDC RAJJU SHROFF ROFEL INSTITUTE OF

MANAGEMENT STUDIES, VAPI

Gujarat Technological University

DECLARATION

I, Mr. MAYANK TAILOR Student of M.B.A – Semester-II, GIDC RAJJU SHROFF

INSTITUTE OF MANAGEMENT STUDIES VAPI. hereby declare that the Report on

Summer Training & project work entitled CREDIT APPRAISAL SURAT, GUJARAT is

been result of my own work and has been carried out under supervision of PROF. NUPUR

ANGIRISH.

I declare that this submitted work is done solely by me and to the best of my knowledge; no

such work has been submitted by any other person for the award of post graduation degree or

diploma.

I also declare that all the information collected from various secondary sources has been duly

acknowledged in this project report.

PLACE: Mayank Tailor

DATE:

CERTIFICATE

This is to certify that Mr. MAYANK TAILOR has satisfactory completed the project work

entitled, CREDIT APPRAISAL IN SURAT, GUJARAT. Based on the declaration made by

the candidate and me association as a guide for carrying out this project work, I

recommended this project for evaluation as a part of the MBA programme of Gujarat

Technological University.

Place: VAPI

Date: PROF: NUPUR ANGIRISH

Place: VAPI

Date: Dr D.S.Sarupria

Director

ACKNOWLEDGEMENT

My debts are many and I acknowledge them with much pride and delight. This summer

project was undertaken as a part of MBA Programme pursuing at GIDC RAJJU SHROFF

Rofel Institute of Management Studies, Vapi. (GRIMS). I would like to thank my institute

and Central Bank of India which has provided me with the infrastructure and opportunity for

doing this project work.

I am very great full to Mr. P.K.VESUNA (Loan/Advances), who has given me the permission

to carry out this project work at their esteemed organization.

I am extremely great full to Dr. Dalpat Sarupria, Director of GIDC RAJJU SHROFF Rofel

Institute of Management Studies, Vapi. (GRIMS), for his invaluable help and guidance

throughout my work. He kindly evinced keen interest in my work and furnished some useful

comments, which could enrich the work substantially.

I am very much thankful to my internal guide Prof. NUPUR ANGIRISH for her keen

guidance and support.

In fact it is very difficult to acknowledge all the names and nature of help and encouragement

provided by them. I would never forget the help and support extended directly or indirectly

to me by all.

TABLE OF CONTENTS

PARTICULARS PAGE NO.

1 RESEARCH METHODOLOGY 1

2 INTRODUCTION TO BANKING SECTOR 4

3 GLOBAL AND LOCAL SCENARIO OF BANKING

SECTOR 9

4 INDUSTRY ANALYSIS 22

5 INTRODUCTION TO CENTRAL BANK OF INDIA 28

6 INTRODUCTION TO SME 30

7 OVERVIEW OF CREDIT APPRAISAL 34

8 CREDIT APPRAISAL MODEL 58

9 CASE STUDY 70

10 OTHER DEPARTMENT OF BANKS 80

11 FINDING 83

12 CONCLUSION 85

13 BIBLIOGRAPHY 86

EXECUTIVE SUMMARY

I had a valuable experience doing my summer internship at Central Bank of India in Surat.

The duration for my internship was 23 days, starting from 7th july 2011 to 29th july 2011 in

Surat Main branch and, I was working on the “CREDIT APPRISAL”

My Project Guide was Mr.P.K.VESUNA for SURAT branch, respectively of his department.

This was my First exposure to the corporate world and had an experience of working in a

banking. I was directly working under loan/advances : I was working on the credit appraisal,

which I feel is the basic requirement of any bank. While working I observed the significance

of the loan/advances in a bank, its working. I also got to observe various functions of the

bank department.

The project, which was given to me in this period of my summer internship, project was to

know the credit appraisal. For that, I have to talk to manager and try to understand concept of

credit in the bank.

Thus during this internship-period working on project and simultaneously observing has

proved to be a great experience in all as I have got to see and understand various situations of

the employees. I would like to conclude by saying that it is been a great learning for me

through this internship. I understand some realities of the bank , as, I was part of the everyday

activities of the organization. I also learned the fact that no department can work on its own

each department have to depend on other in one-way or the other.

RESEARCH METHODOLOGY

INTRODUCTION:

Credit appraisal means investigation/assessment done by the bank before providing any loans and

advances/project finance and also checks the commercial, financial &industrial viability of the

project proposed its funding pattern and further checks the primary & collateral security cover

available for recovery of such funds.

PROBLEM STATEMENT :

To study the credit appraisal system in SME sector, at Central bank of India.

OBJECTIVES:

To study the credit appraisal methods.

To understand the commercial, financial & technical viability of the proposal

proposed and it’s finding pattern.

DATA COLLECTION :

Primary data:

Informal interview with manager and other staff members at Central bank of India

Secondary data:

Books

websites

database at Central bank of India

library research

BENEFICIARIES:

Researchers:

This report will help researchers improving knowledge about the credit appraisal system and to have

practical exposure of the credit appraisal system at Central bank of India.

Management Students:

The project will help the management student to know the patterns of credit appraisal in Central

bank of India.

LIMITATION OF THE STUDY

As the credit appraisal is one of the crucial areas for any bank, some of the

technicalities are not revealed.

Credit appraisal system includes various types of detail studies for different areas of

analysis, but due to time constraint, our analysis was of limited areas only.

INTRODUCTION TO BANKING SECTOR

A SNAPSHOT OF THE BANKING INDUSTRY

The Reserve Bank of India (RBI), as the central bank of the country, closely monitors developments in

the whole financial sector.

DEFINITION/MEANING OF A BANK

The word bank has originated from English word Banco, Bancus or Banque. Its meaning is bench or

table. In Europe in the middle age, the money transactions were undertaken sitting on a bench.

As per Indian Banking Act, “ A service to accept deposits from people with the intention to invest or

lend with the condition of returning it immediately whenever demanded at any predetermined time.

An institute this service is Bank”

Banking is a service helpful to the business, its function is to borrow money from people and further

lend the same.

While analyzing definition of bank as per Indian Banking Act, below mentioned matters are clarified:

(1) Bank accepts monetary deposits from people.

(2) The intention behind accepting these deposits is to invest or lend the respective fund.

(3) The function of accepting deposit or lending money is made under the condition that

on demand or as predetermined otherwise the same amount has to be refunded

immediately.

(4) The institution doing this type of business is called bank.

The banking sector is dominated by Scheduled Commercial Banks (SBCs). As at end March 2002,

there were 296 Commercial banks operating in India. This included 27 Public Sector Banks (PSBs), 31

Private, 42 Foreign and 196 Regional Rural Banks. Also, there were 67 scheduled co-operative banks

consisting of 51 scheduled urban cooperative banks and 16 scheduled state co-operative banks.

Scheduled commercial banks touched, on the deposit front, a growth of 14% as against 18%

registered in the previous year. And on advances, the growth was 14.5% against 17.3% of the earlier

year.

State Bank of India is still the largest bank in India with the market share of 20% ICICI and its two

subsidiaries merged with ICICI Bank, leading creating the second largest bank in India with a balance

sheet size of Rs. 1040bn.

Higher provisioning norms, tighter asset classification norms, dispensing with the concept of ‘past

due’ for recognition of NPAs, lowering of ceiling on exposure to a single borrower and group

exposure etc., are among the measures in order to improve the banking sector.

A minimum stipulated Capital Adequacy Ratio (CAR) was introduced to strengthen the ability of

banks to absorb losses and the ratio has subsequently been raised from 8% to 9%. It is proposed to

hike the CAR to 12% by 2004 based on the Basle Committee recommendations.

Retail Banking is the new mantra in the banking sector. The home Loans alone account for nearly

two-third of the total retail portfolio of the bank. According to one estimate, the retail segment is

expected to grow at 30-40% in the coming years.

Net banking, phone banking, mobile banking, ATMs and bill payments are the new buzz words that

banks are using to lure customers.

With a view to provide an institutional mechanism for sharing of information on borrowers /

potential borrowers by banks and Financial Institutions, the Credit Information Bureau (India) Ltd.

(CIBIL) was set up in August 2000. The Bureau provides a framework for collecting, processing and

sharing credit information on borrowers of credit institutions. SBI and HDFC are the promoters of the

CIBIL.

The RBI is now planning to transfer of its stakes in the SBI, NHB and National bank for Agricultural

and Rural Development to the private players. Also, the Government has sought to lower its holding

in PSBs to a minimum of 33% of total capital by allowing them to raise capital from the market.

Banks are free to acquire shares, convertible debentures of corporate and units of equity oriented

mutual funds, subject to a ceiling of 5% of the total outstanding advances (including commercial

paper) as on March 31 of the previous year.

REFORMS IN THE BANKING SECTOR

The first phase of financial reforms resulted in the nationalization of 14 major banks in 1969 and

resulted in a shift from Class banking to Mass banking. This in turn resulted in a significant growth in

the geographical coverage of banks. Every bank has to earmark a minimum percentage of their Loan

portfolio to sectors identified as “priority sectors”. The manufacturing sector also grew during the

1970s in protected environs and the banking sector was a critical source. The next wave of reforms

saw the nationalization of 6 more commercial banks in 1980. Since then the number scheduled

commercial banks increased four-fold and the number of banks branches increased eight-fold.

After the second phase of financial sector reforms and liberalization of the sector in the early

nineties, the Public Sector Banks (PSB) s found it extremely difficult to complete with the new private

sector banks and the foreign banks. The new private sector banks first made their appearance after

the guidelines permitting them were issued in January 1993. Eight new private sector banks are

presently in operation. These banks due to their late start have access to state-of-the-art technology,

which in turn helps them to save on manpower costs and provide better services.

During the year 2000, the State Bank of India (SBI) and its 7 associates accounted for a 25% share in

deposits and 28.1% share in credit. The 20 nationalized banks accounted for 53.5% of the deposits

and 47.5% of credit during the same period. The share of foreign banks ( numbering 42 ), regional

rural banks and other scheduled commercial banks accounted for 5.7%, 3.9% and 12.2% respectively

in deposits and 8.41%, 3.14% and 12.85% respectively in credit during the year 2000

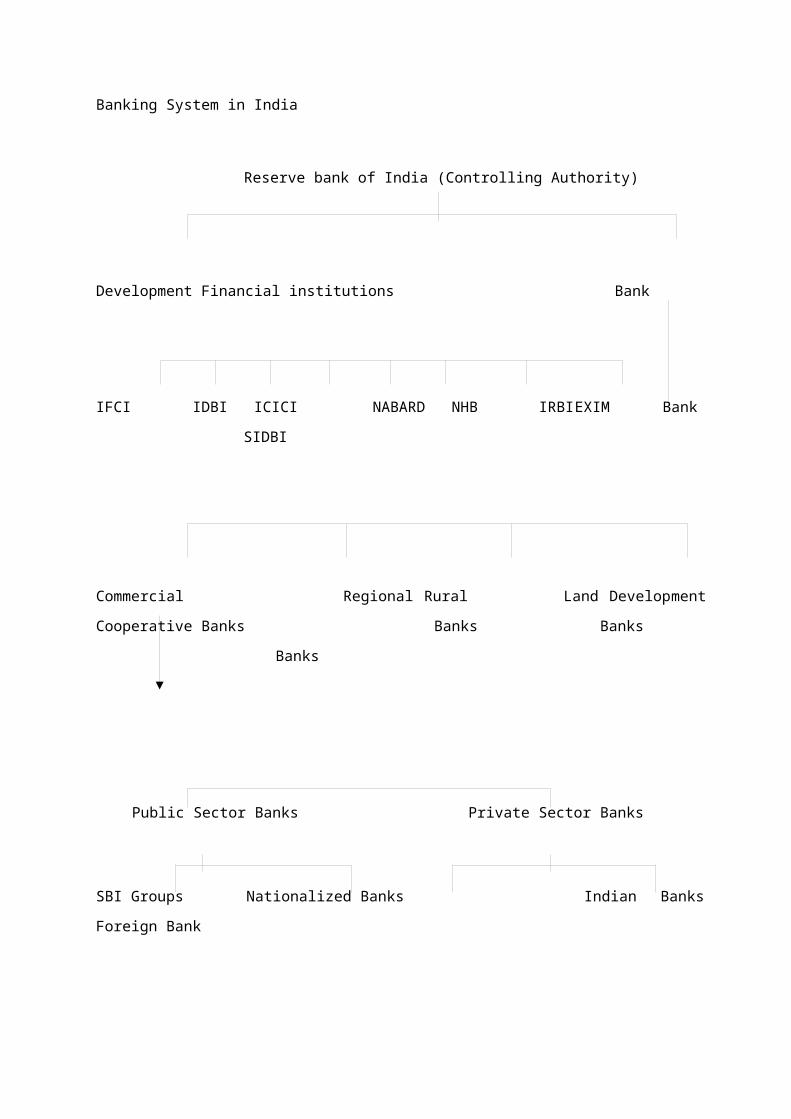

CLASSIFICATION OF BANKS:

The Indian banking industry, which is governed by the Banking Regulation Act of India 1949 can

be broadly classified into two major categories, non-scheduled banks and scheduled banks.

Scheduled banks comprise commercial banks and the co-operative banks. In Terms of ownership,

commercial banks can be further grouped into nationalized banks, the State Bank of India and its

group banks, regional rural banks and private sector banks (the old / new domestic and foreign).

These banks have over 67,000 branches spread across the country. The Indian banking industry

is a mix of the public sector, private sector and foreign banks. The private sector banks are

again spilt into old banks and new banks.

Banking System in India

Reserve bank of India (Controlling Authority)

Development Financial institutions Bank

IFCI IDBI ICICI NABARD NHB IRBI EXIM Bank SIDBI

Commercial Regional Rural Land Development Cooperative Banks

Banks Banks Banks

Public Sector Banks Private Sector Banks

SBI Groups Nationalized Banks Indian Banks Foreign Bank

GLOBAL AND LOCAL SCENARIO OF BANKING SECTOR

INDIAN BANKING SYSTEM: THE CURRENT STATE & ROAD AHEAD

INTRODUCTION:

Recent time has witnessed the world economy develop serious difficulties in terms of lapse of

banking & financial institutions and plunging demand. Prospects became very uncertain causing

recession in major economies. However, amidst all this chaos India’s banking sector has been

amongst the few to maintain resilience.

A progressively growing balance sheet, higher pace of credit expansion, expanding profitability and

productivity akin to banks in developed markets, lower incidence of nonperforming assets and focus

on financial inclusion have contributed to making Indian banking vibrant and strong. Indian banks

have begun to revise their growth approach and re-evaluate the prospects on hand to keep the

economy rolling. The way forward for the Indian banks is to innovate to take advantage of the new

business opportunities and at the same time ensure continuous assessment of risks.

A rigorous evaluation of the health of commercial banks, recently undertaken by the Committee on

Financial Sector Assessment (CFSA) also shows that the commercial banks are robust and versatile.

The single-factor stress tests undertaken by the CFSA divulge that the banking system can endure

considerable shocks arising from large possible changes in credit quality, interest rate and liquidity

conditions. These stress tests for credit, market and liquidity risk show that Indian banks are by and

large resilient.

Thus, it has become far more imperative to contemplate the role of the Banking Industry in fostering

the long term growth of the economy. With the purview of economic stability and growth, greater

attention is required on both political and regulatory commitment to long term development

programmed. FICCI conducted a survey on the Indian Banking Industry to assess the competitive

advantage offered by the banking sector, as well as the policies and structures that are required to

further the pace of growth. The results of our survey are given in the following sections.

GENERAL BANKING SCENARIO:

The pace of development for the Indian banking industry has been tremendous over the past

decade. As the world reels from the global financial meltdown, India’s banking sector has been one

of the very few to actually maintain resilience while continuing to provide growth opportunities, a

feat unlikely to be matched by other developed markets around the world. FICCI conducted a survey

on the Indian Banking Industry to assess the competitive advantage offered by the banking sector, as

well as the policies and structures required to further stimulate the pace of growth.

The predicament of the banks in the developed countries owing to excessive leverage and lax

regulatory system has time and again been compared with somewhat unscathed Indian Banking

Sector. An attempt has been made to understand the general sentiment with regards to the

performance, the challenges and the opportunities ahead for the Indian Banking Sector.

A majority of the respondents, almost 69% of them, felt that the Indian banking Industry was in a

very good to excellent shape, with a further 25% feeling it was in good shape and only 6% of the

respondents feeling that the performance of the industry was just average. In fact, an overwhelming

majority (93.33%) of the respondents felt that the banking industry compared with the best of the

sectors of the economy, including pharmaceuticals, infrastructure, etc.

Most of the respondents were positive with regard to the growth rate attainable by the Indian

banking industry for the year 2009-10 and 2014-15, with 53.33% of the view that growth would be

between 15-20% for the year 2009-10 and greater than 20% for 2014-15.

On being asked what is the major strength of the Indian banking industry, which makes it resilient in

the current economic climate; 93.75% respondents feel the regulatory system to be the major

strength, 75% economic growth, 68.75% relative insulation from external market, 56.25% credit

quality, 25% technological advancement and 43.75% our risk assessment systems.

Change is the only constant feature in this dynamic world and banking is not an exception. The

changes staring in the face of bankers relates to the fundamental way of banking-which is going

through rapid transformation in the world of today. Adjust, adapt and change should be the key

mantra. The major challenge faced by banks today is the ever rising customer expectation as well as

risk management and maintaining growth rate. Following are the results of the biggest challenge

faced by the banking industry as declared by our respondents (on a mode scale of 1 to 7 with 1 being

the biggest challenge):

They also asked their respondents to rate India on certain essential banking parameters (Regulatory

Systems, Risk Assessment Systems, Technological System and Credit Quality) in comparison with

other countries i.e. China, Japan, Brazil, Russia, Hong Kong, Singapore, UK and USA.

The recent financial crisis has drawn attention to under-regulation of banks (mainly investment

banks) in the US. Though, the Indian story is quite different. Regulatory systems of Indian banks were

rated better than China, Brazil, Russia, and UK; at par with Japan, Singapore and Hong Kong where as

all our respondents feel that we are above par or at par with USA. On comparing the results with

their previous survey where the respondents had rated Indian Regulatory system below par the US

and UK system, they see that post the financial crisis Indian Banks are more confident on the Indian

Regulatory Framework.

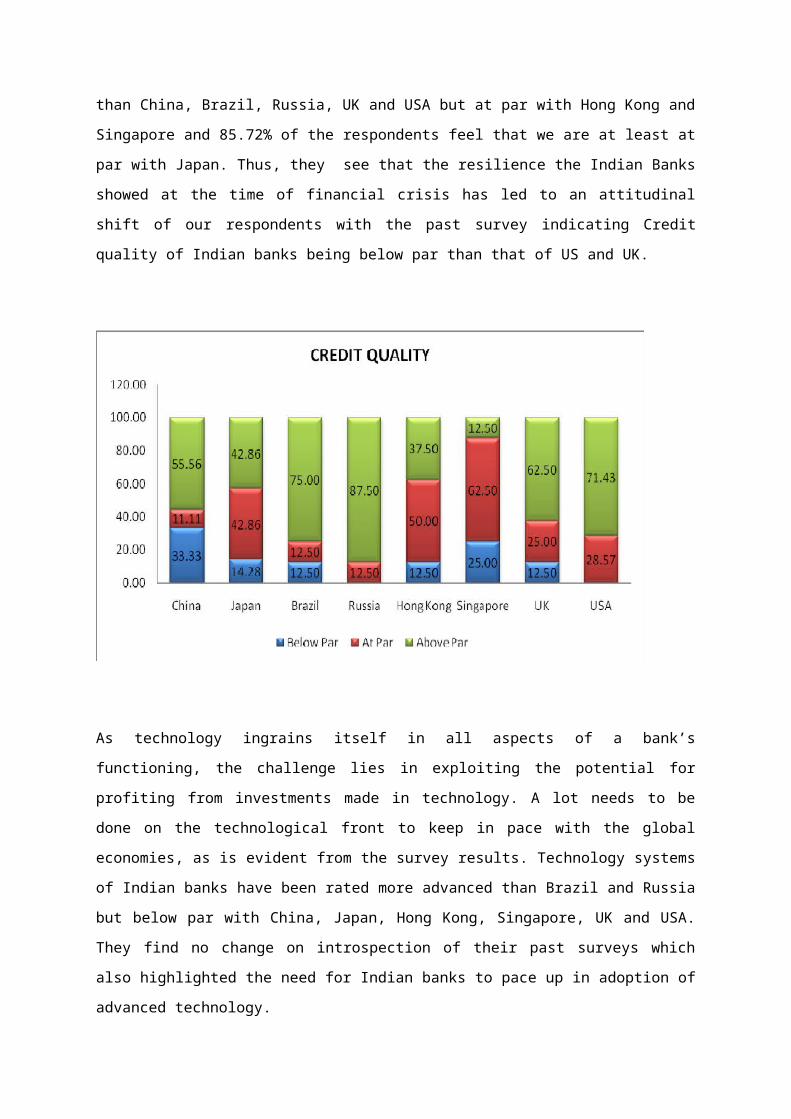

The global meltdown started as a banking crisis triggered by the credit quality. Indian banks seem to

have paced up in terms of Credit Quality. Credit quality of banks has been rated above par than

China, Brazil, Russia, UK and USA but at par with Hong Kong and Singapore and 85.72% of the

respondents feel that we are at least at par with Japan. Thus, they see that the resilience the Indian

Banks showed at the time of financial crisis has led to an attitudinal shift of our respondents with the

past survey indicating Credit quality of Indian banks being below par than that of US and UK.

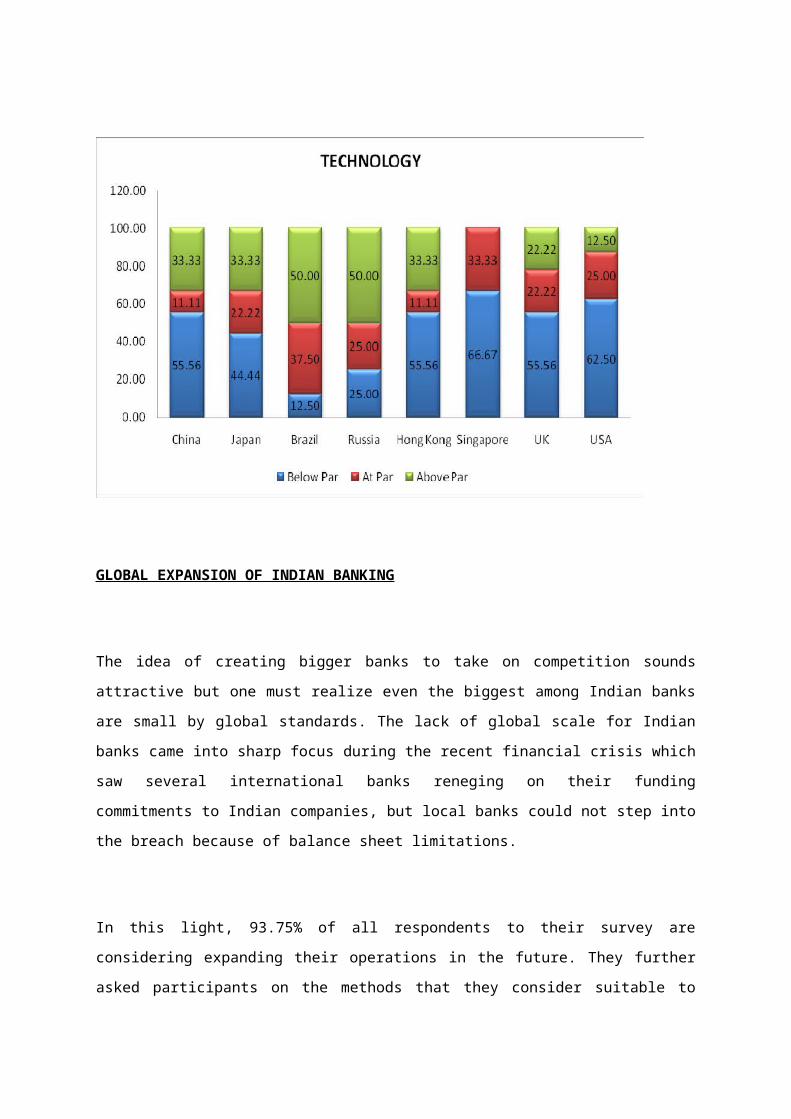

As technology ingrains itself in all aspects of a bank’s functioning, the challenge lies in exploiting the

potential for profiting from investments made in technology. A lot needs to be done on the

technological front to keep in pace with the global economies, as is evident from the survey results.

Technology systems of Indian banks have been rated more advanced than Brazil and Russia but

below par with China, Japan, Hong Kong, Singapore, UK and USA. They find no change on

introspection of their past surveys which also highlighted the need for Indian banks to pace up in

adoption of advanced technology.

GLOBAL EXPANSION OF INDIAN BANKING

The idea of creating bigger banks to take on competition sounds attractive but one must realize even

the biggest among Indian banks are small by global standards. The lack of global scale for Indian

banks came into sharp focus during the recent financial crisis which saw several international banks

reneging on their funding commitments to Indian companies, but local banks could not step into the

breach because of balance sheet limitations.

In this light, 93.75% of all respondents to their survey are considering expanding their operations in

the future. They further asked participants on the methods that they consider suitable to meet their

expansion needs. They divide them into organic means of growth that comes out of an increase in

the bank’s own business activity, and inorganic means that includes mergers or takeovers.

We see from the above graph that amongst organic means of expansion, branch expansion finds

favor with banks while strategic alliances is the most popular inorganic method for banks

considering scaling up their operations. On the other hand, new ventures and buyout portfolios are

the least popular methods for bank expansion.

SCOPE FOR NEW ENTRANTS:

81.25% also felt that there was further scope for new entrants in the market, in spite of capital

management and human resource constraints, as there continue to remain opportunities in

unbanked areas. With only 30-35% of the population financially included, and the Indian banking

industry unsaturated with CAGR of well above 20%, participants in their survey felt that the market

definitely has scope to accommodate new players.

While there has been prior debate, they questioned banks on NBFCs and Industrial houses being

established as banking institutions and find opinion to be marginally against the notion, with 35.71%

in favour while 42.86% were against them being established as banks.

However, on further questioning, 57.14% of respondents feel that the above may be allowed but

only if it is along with specific regulatory limitations. Banks felt that limitations regarding track

record, ensuring adequate capitalization levels, a tiered license that enables new entrants to enter

into specific areas of the business only after satisfactorily achieving set milestones for the prior

stages, cap on promoter's holdings and wider public holding in addition to a common banking

regulator on a level playing field are essential before they may set themselves up as banks.

BANKING ACTIVITIES:

Over the last three decades, there has been a remarkable increase in the size, spread and scope of

activities of banks in India. The business profile of banks has transformed dramatically to include

non-traditional activities like merchant banking, mutual funds, new financial services and products

and the human resource development.

Their survey finds that within retail operations, banks rate product development and differentiation;

innovation and customization; cost reduction; cross selling and technological up gradation as equally

important to the growth of their retail operations. Additionally a few respondents also find pro-

active financial inclusion, credit discipline and income growth of individuals and customer

orientation to be significant factors for their retail growth.

There is, at the same time, an urgent need for Indian banks to move beyond retail banking, and

further grow and expand their fee- based operations, which has globally remained one of the key

drivers of growth and profitability. In fact, over 80% of banks in their survey have only up to 15% of

their total incomes constituted by fee- based income; and barely 13% have 20-30% of their total

income constituted by fee-based income.

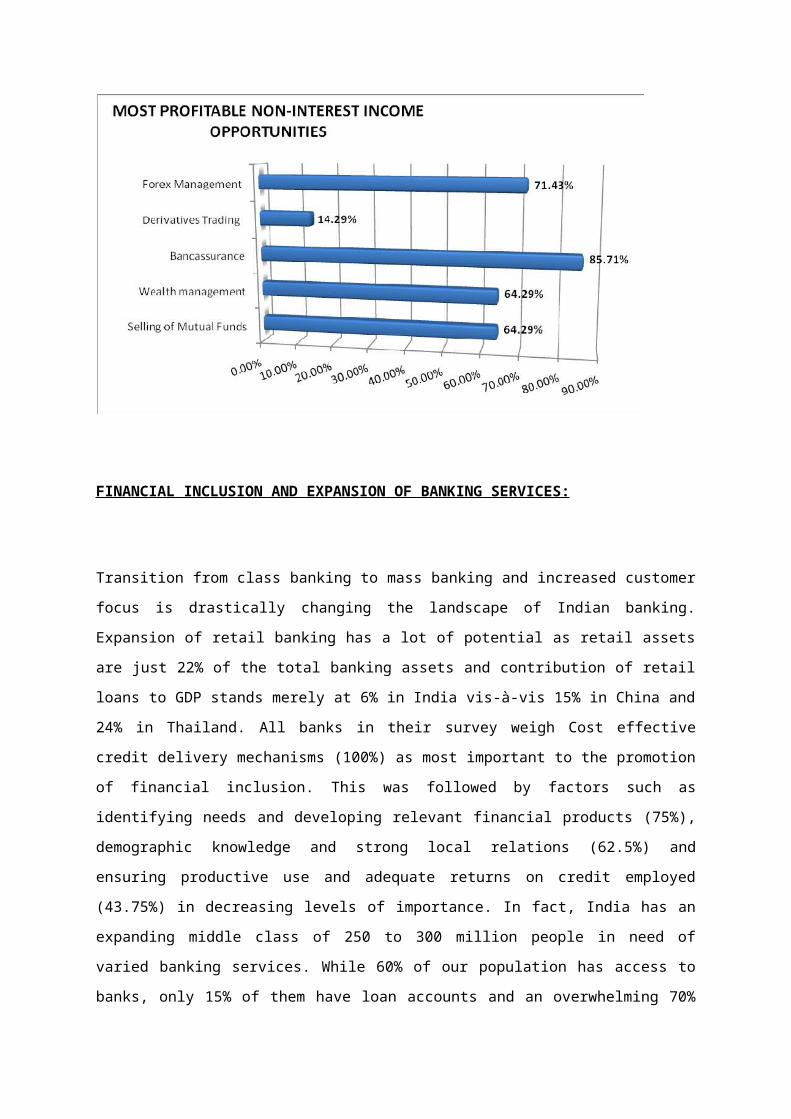

Out of avenues for non-interest income, we see that Banc assurance (85.71%) and FOREX

Management (71.43%) remain most profitable for banks. Derivatives, understandably, remains the

least profitable business opportunity for banks as the market for derivatives is still in its nascent

stage in India.

There is nevertheless a visibly increased focus on fee based sources of income. 71% of banks in their

survey saw an increase in their fee based income as a percentage of their total income for the FY

2008-09 as compared to FY 2007-08. Indian banks are fast realizing that fee-based sources of income

have to be actively looked at as a basis for future growth, if the industry is to become a global force

to reckon with.

FINANCIAL INCLUSION AND EXPANSION OF BANKING SERVICES:

Transition from class banking to mass banking and increased customer focus is drastically changing

the landscape of Indian banking. Expansion of retail banking has a lot of potential as retail assets are

just 22% of the total banking assets and contribution of retail loans to GDP stands merely at 6% in

India vis-à-vis 15% in China and 24% in Thailand. All banks in their survey weigh Cost effective credit

delivery mechanisms (100%) as most important to the promotion of financial inclusion. This was

followed by factors such as identifying needs and developing relevant financial products (75%),

demographic knowledge and strong local relations (62.5%) and ensuring productive use and

adequate returns on credit employed (43.75%) in decreasing levels of importance. In fact, India has

an expanding middle class of 250 to 300 million people in need of varied banking services. While

60% of our population has access to banks, only 15% of them have loan accounts and an

overwhelming 70% of farmers have no access to formal sources of credit, reflective of immense

potential for the banking system This is mirrored in the fact that while our survey finds no

discernible shift in the lending pattern of banks across Tier 1, Tier 2 and Tier 3 cities over the last two

years, 93% Indian Banking System: The Current State & Road Ahead Page | 20 participants still find

rural markets to be to be a profitable avenue, with 53% of respondents finding it lucrative in spite of

it being a difficult market. Cost of accessing markets has been the only sour note in the overall

experience of our respondents in rural markets At the same time, more than 81.25% of our

respondents have a strategy in place to tap rural markets, with the remainder as yet undecided on

their plan of action. Tie ups with micro finance institutions (MFIs)/SHG and introduction of

innovative and customized products are considered most important to approaching rural markets

according to respondents, more so as compared to internet kiosks, post offices and supply chain

management techniques

Additionally, 81.25% of respondents found branchless banking to be an effective and secure way of

reaching out to rural markets, with mobile, biometric and handheld devices, equally popular

amongst banks. Some respondents also found the Business Correspondents model to be an

untapped model for financial inclusion.

As Indian financial markets mature over time, there is also a need for innovative instruments to

deepen the market further. Suggestions ranged from micro saving and micro insurance initiatives,

Cash deposit machines, warehouse receipts, to prepaid cash cards, derivatives, interest rate futures

and credit default swaps as a means to further the financial inclusion and expansionary process.

CREDIT FLOW AND INDUSTRY:

India Inc is completely dependent on the Banking System for meeting its funding requirement. One

of the major complaints from the industry has in fact been high lending rates in spite of massive cuts

in policy rates by the RBI. We asked the banks what they felt were major factors responsible for rigid

prime lending rates.

None of the banks in their survey considered the cap on bank deposit rates to be one of the causes

of inflexible lending rates. Due to long-term maturity, the trend seems to be changing. However,

there are other factors which have led to the stickiness of lending rates such as wariness of

corporate credit risk (33.33%), competition from government small savings schemes (26.67%).

Benchmarking of SME and export loans against PLR (20.00%) on the other hand, do not seem to

have as significant an influence over lending rates according to banks

The great Indian industrial engine has nevertheless continued to hum its way through most of the

year long crisis. We asked banks about the sectors that they consider to be most profitable in the

coming years (Fig. 12). All respondents were confident in the infrastructure sector leading the

profitability for the industry, followed by retail loans (73.33%) and others

(Source: Annual survey, February 2010)

(FEDERATION OF INDIAN CHAMBERS OF COMMERCE & INDUSTRY)

INDUSTRY ANALYSIS

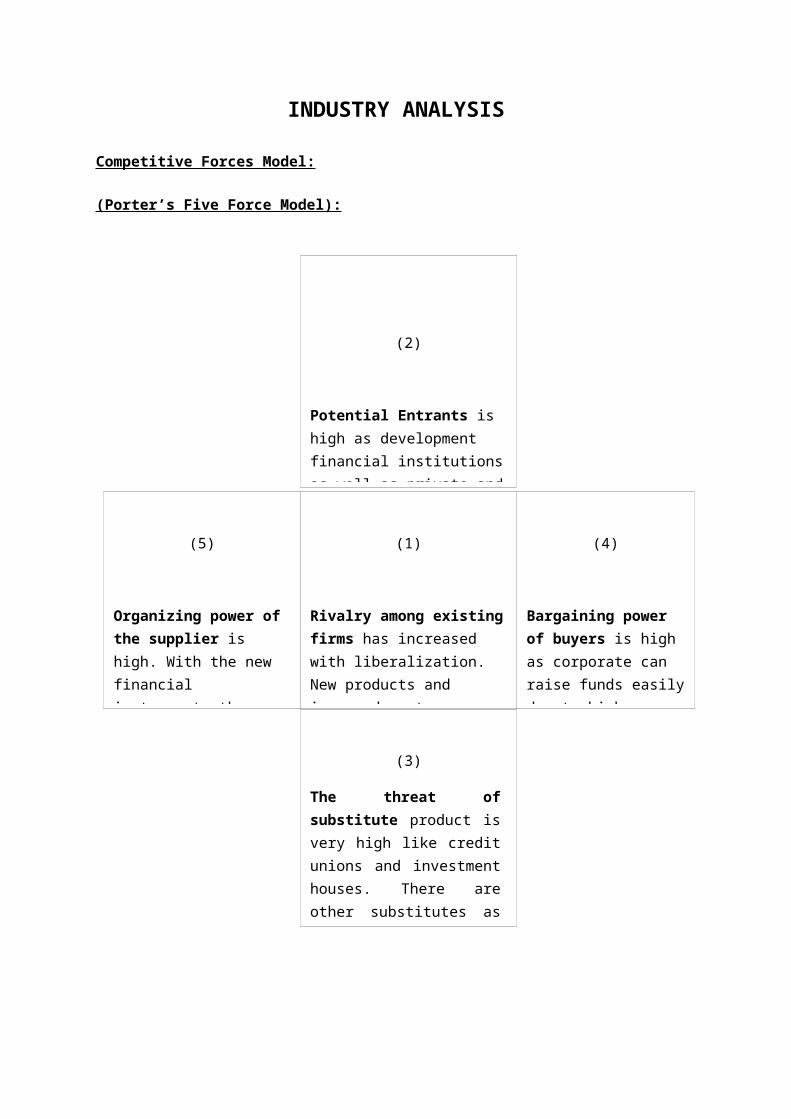

Competitive Forces Model:

(Porter’s Five Force Model):

(2)

Potential Entrants is high as development financial institutions as well as private and Foreign Banks have entered in a big way

(1)

Rivalry among existing firms has increased with liberalization. New products and improved customer services is the focus.

(4)

Bargaining power of buyers is high as corporate can raise funds easily due to high Competition.

(3)

The threat of substitute product is very high like credit unions and investment houses. There are other substitutes as well banks like mutual funds, stocks, government securities, debentures, gold, real estate

(5)

Organizing power of the supplier is high. With the new financial instruments they are asking higher return on the investments

1. Rivalry among existing firms

With the process of liberalization, competition among the existing banks has increased. Each

bank is coming up with new products to attract the customers and tailor made Loans are provided.

The quality of services provided by banks has improved drastically.

2. Potential Entrants

Previously the development financial Institutions mainly provided project finance and

development activities. But they now entered into retail banking which has resulted into stiff

competition among the exiting players.

3. Threats from Substitutes

Competition from the non-banking financial sector is increasing rapidly. The threat of substitute

product is very high like credit unions and in investment houses. There are other substitutes as well

banks like mutual funds, stocks, government securities, debentures, gold, real estate etc.

4. Bargaining Power of Buyers

Corporate can raise their funds through primary market or by issue of GDRs, FCCBs. As a result

they have a higher bargaining power. Even in the case of personal finance, the buyers have a

high bargaining power. This is mainly because of competition.

5. Bargaining Power of Suppliers

With the advent of new financial instruments providing a higher rate of returns to the

investors, the investments in deposits is not growing in a phased manner. The suppliers demand

a higher return for the investments.

6. Overall Analysis

The key issue is how banks can leverage their strengths to have a better future. Since the

availability of funds is more and deployment of funds is less, banks should evolve new products

and services to the customers. There should be a rational thinking in sanctioning Loans, which will

bring down the NPAs. As there is a expected revival in the Indian economy Banks have a major

role to play.

SWOT ANALYSIS:

The banking sector is also taken as a proxy for the economy as a whole. The performance of bank

should therefore, reflect “Trends in the Indian Economy”. Due to the reforms in the financial sector,

banking industry has changed drastically with the opportunities to the work with, new accounting

standards new entrants and information technology. The deregulation of the interest rate,

participation of banks in project financing has changed in the environment of banks.

The performance of banking industry is done through SWOT Analysis. It mainly helps to know the

strengths and Weakness of the industry and to improve will be known through converting the

opportunities into strengths. It also helps for the competitive environment among the banks.

a) STRENGTHS

1. Greater securities of Funds

Compared to other investment options banks since its inception has been a better avenue in terms

of securities. Due to satisfactory implementation of RBI’s prudential norms banks have won public

confidence over several years.

2. Banking network

After nationalization, banks have expanded their branches in the country, which has helped banks

build large networks in the rural and urban areas. Private banks allowed to operate but they mainly

concentrate in metropolis.

3. Large Customer Base

This is mainly attributed to the large network of the banking sector. Depositors in rural areas prefer

banks because of the failure of the NBFCs.

4. Low Cost of Capital

Corporate prefers borrowing money from banks because of low cost of capital. Middle income

people who want money for personal financing can look to banks as they offer at very low rates of

interests. Consumer credit forms the major source of financing by banks.

b) WEAKNESS

1. Basel Committee

The banks need to comply with the norms of Basel committee but before that it is challenge for

banks to implement the Basel committee standard, which are of international standard.

2. Powerful Unions

Nationalization of banks had a positive outcome in helping the Indian Economy as a whole. But this

had also proved detrimental in the form of strong unions, which have a major influence in decision-

making. They are against automation.

3. Priority Sector Lending

To uplift the society, priority sector lending was brought in during nationalization. This is good for

the economy but banks have failed to manage the asset quality and their intensions were more

towards fulfilling government norms. As a result lending was done for non-productive purposes.

4. High Non-Performing Assets

Non-Performing Assets (NPAs) have become a matter of concern in the banking industry. This is

because reduced to meet the international standards of change in the total outstanding advances,

which has to be reduced to meet the international standards.

c) OPPORTUNITIES

1. Universal Banking

Banks have moved along the value chain to provide their customers more products and services. like

home finance, Capital Markets, Bonds etc. Every Indian bank has an opportunity to become

universal bank, which provides every financial service under one roof.

2. Differential Interest Rates

As RBI control over bank reduces, they will have greater flexibility to fix their own interest rates

which depends on the profitability of the banks.

3. High Household Savings

Household savings has been increasing drastically. Investment in financial assets has also increased.

Banks should use this opportunity for raising funds.

4. Untapped Foreign Markets

Many Indian banks have not sufficiently penetrated in foreign markets to generate satisfactory

business therefore, it can be concluded clear opportunity exists in such markets.

5. Interest Banking

The advance in information technology has made banking easier. Business can Effectively carried out

through internet banking.

d) THREATS

1. NBFCs, Capital Markets and Mutual funds

There is a huge investment of household savings. The investments in NBFCs deposits, Capital Market

Instruments and Mutual Funds are increasing. Normally these instruments offer better return to

investors.

2. Changes in the Government Policy

The change in the government policy has proved to be a threat to the banking sector. Due to some

major changes in policies related to deposits mobilization credit deployment, interest rates- the

whole scenario of banking industry may change.

3. Inflation

The interest rates go down with a fall in inflation. Thus, the investors will shift his investments to the

other profitable sectors.

4. Recession

Due to the recession in the business cycle the economy functions poorly and this has proved to be a

threat to the banking sector. The market oriented economy and globalization has resulted into

competition for market share. The spread in the banking sector is very narrow. To meet the

competition the banks has to grow at a faster rates and reduce the overheads. They can introduce

the new products and develop the existing services.

INTRODUCTION TO CENTRAL BANK OF INDIA

.

Build a better life around us.

Establish in 1911, Central Bank of India was the first Indian commercial bank which was wholly

owned and managed by Indians. The establishment of the Bank was the ultimate realization of

the dream of Sir Sorabji Pochkhanawala, founder of the Bank. Sir Pherozesha Mehta was the first

Chairman of a truly 'Swadeshi Bank'. In fact, such was the extent of pride felt by Sir Sorabji

Pochkhanawala that he proclaimed Central Bank of India as the 'property of the nation and the

country's asset'. He also added that 'Central Bank of India lives on people's faith and regards itself

as the people's own bank'.

During the past 99 years of history the Bank has weathered many storms and faced many

challenges. The Bank could successfully transform every threat into business opportunity and

excelled over its peers in the Banking industry.

A number of innovative and unique banking activities have been launched by Central Bank of

India and a brief mention of some of its pioneering services are as under:

1921 Introduction to the Home Savings Safe Deposit Scheme to build saving/thrift habits in all

sections of the society.

1924 An Exclusive Ladies Department to cater to the Bank's women clientele.

1926 Safe Deposit Locker facility and Rupee Travellers' Cheques.

1929 Setting up of the Executor and Trustee Department.

1932 Deposit Insurance Benefit Scheme.

1962 Recurring Deposit Scheme.

Subsequently, even after the nationalisation of the Bank in the year 1969, Central Bank continued

to introduce a number of innovative banking services as under:

1976 The Merchant Banking Cell was established.

1980 Centralcard, the credit card of the Bank was introduced.

1986 'Platinum Jubilee Money Back Deposit Scheme' was launched.

1989 The housing subsidiary Cent Bank Home Finance Ltd. was started with its headquarters at

Bhopal in Madhya Pradesh.

1994 Quick Cheque Collection Service (QCC) & Express Service was set up to enable speedy

collection of outstation cheques.

Further in line with the guidelines from Reserve Bank of India as also the Government of India,

Central Bank has been playing an increasingly active role in promoting the key thrust areas of

agriculture, small scale industries as also medium and large industries. The Bank also introduced a

number of Self Employment Schemes to promote employment among the educated youth.

Among the Public Sector Banks, Central Bank of India can be truly described as an All India Bank,

due to distribution of its large network in 27 out of 29 States as also in 3 out of 7 Union Territories

in India. Central Bank of India holds a very prominent place among the Public Sector Banks on

account of its network of 3656 branches and 178 extension counters at various centres

throughout the length and breadth of the country.

Customers' confidence in Central Bank of India's wide ranging services can very well be judged

from the list of major corporate clients such as ICICI, IDBI, UTI, LIC, HDFC as also almost all major

corporate houses in the country.In surat central bank have total 11 branches are works.

INTRODUCTION TO SME

In the Indian context, the small and medium enterprises (SME) sector is broadly a Term used for

small scale industrial (SSI) units and medium-scale industrial units. Any industrial unit with a total

investment in its fixed assets or leased assets or hire-purchase asset of up to Rs 10 million, can be

considered as an SSI unit and any investment of up to Rs 100 million can be Termed as a medium

unit. An SSI unit should neither be a subsidiary of any other industrial unit nor be owned or

controlled by any other industrial unit.

An SME is known by different ways across the world. In India, a standard definition surfaced only in

October 2, 2006, when the Ministry of Micro, Small and Medium Enterprises, Government of India,

imposed the Micro, Small and Medium enterprises Development (MSMED) Act,2006.

This definition, however was changed according to the changing economic scenario and thus has

separate definitions to it. For instance, an SME definition for manufacturing enterprises is different

from what an SME definition for service enterprises has to say.

HISTORY:

Small and Medium Enterprises or SMEs are vital for the growth and well being of the country. This

sector was recognized and given importance right from independence and is being encouraged ever

since then.

Though, it commenced on a small scale, it gradually gained significance, because it employed a

considerable number of people.

When it started gaining momentum, this sector was defined as an enterprise with investment in

plant and machinery of up to Rs 1 lakh and situated in towns and villages with strength of less than

50,000 people. The policy statement put in place special legislation to recognize and protect self

employed people in cottage and home industries. District industries canters (DICs) were set up and

made the focal point of SSI development, bypassing large cities and state capitals. Also, the

government started providing special services akin to product standardization, quality control and

marketing surveys in order to assist the SSIs in enabling them to market their products in an

underdeveloped market.

The scenario for the small-scale sector changed with the Industrial Policy of July 1991, which, for the

first time in India’s development history spoke of liberalization. What this meant was that medium

and large enterprises would no longer need licenses to run. Export-oriented enterprises could be

wholly foreign owned and foreign equity participation was selectively allowed. Industries could

import capital goods with much fewer restrictions.

1996 saw the government involved in the setting up of a higher level committee, known as the Abid

Hussain Committee, to review policies for small industries and recommend measures to help

formulate a strong and innovative policy package for the rapid development of SMEs. With

liberalization, rapid changes were seen in the Indian economy. Indian companies were no longer

insulated from the global economy. In fact, there was an urgent need to make them, especially

SMEs, more competitive and resilient.

In 1991, the growth rate of SSIs was almost three times that of the total industrial sector at 3.1

percent. From 1991 to 1995, the growth rate of SSIs exceeded that of the total industrial sector. Yet,

in 1995-96, the growth rate of SSIs was slightly lower than the total industrial sector, however it

increased again in 1996 and continued to be higher than the total industrial growth rate till 1999. till

2006, the SME segment saw a lot more development and support from the government.

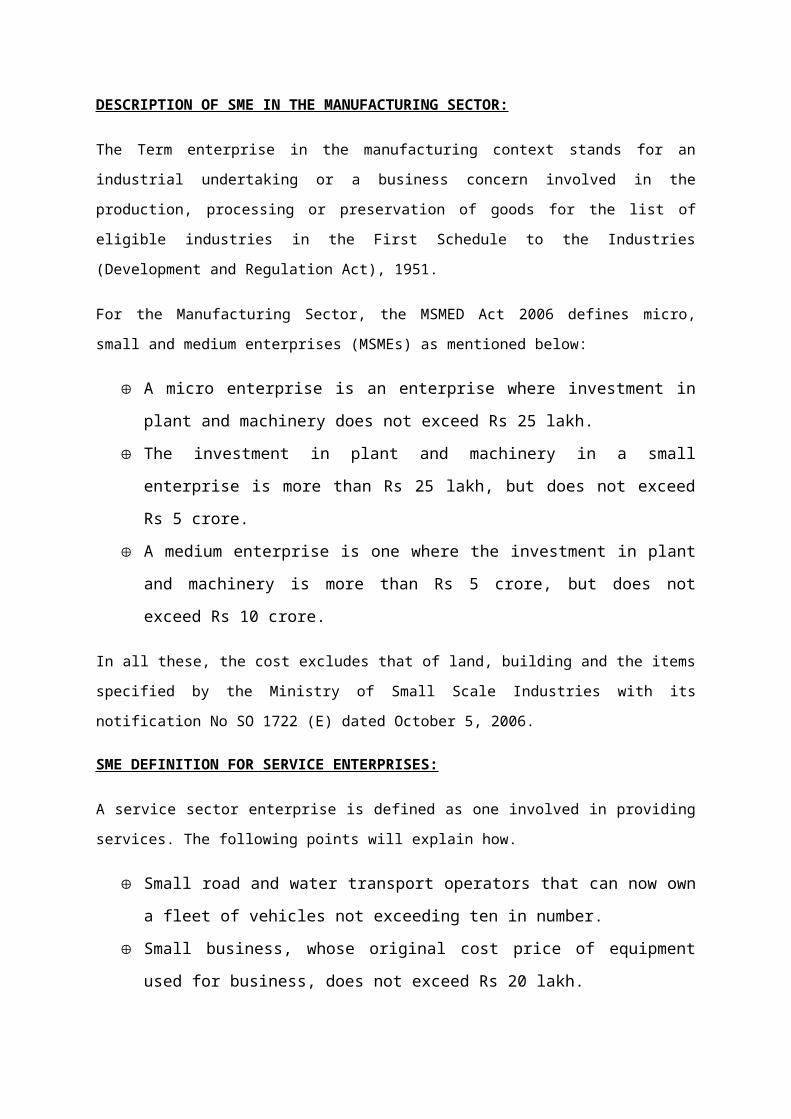

DESCRIPTION OF SME IN THE MANUFACTURING SECTOR:

The Term enterprise in the manufacturing context stands for an industrial undertaking or a business

concern involved in the production, processing or preservation of goods for the list of eligible

industries in the First Schedule to the Industries (Development and Regulation Act), 1951.

For the Manufacturing Sector, the MSMED Act 2006 defines micro, small and medium enterprises

(MSMEs) as mentioned below:

A micro enterprise is an enterprise where investment in plant and machinery does not

exceed Rs 25 lakh.

The investment in plant and machinery in a small enterprise is more than Rs 25 lakh,

but does not exceed Rs 5 crore.

A medium enterprise is one where the investment in plant and machinery is more than

Rs 5 crore, but does not exceed Rs 10 crore.

In all these, the cost excludes that of land, building and the items specified by the Ministry of Small

Scale Industries with its notification No SO 1722 (E) dated October 5, 2006.

SME DEFINITION FOR SERVICE ENTERPRISES:

A service sector enterprise is defined as one involved in providing services. The following points will

explain how.

Small road and water transport operators that can now own a fleet of vehicles not

exceeding ten in number.

Small business, whose original cost price of equipment used for business, does not

exceed Rs 20 lakh.

Professional and self-employed persons, whose borrowing limits do not exceed Rs 10

lakh of which not more than Rs 2 lakh should be for working capital requirements

Professionally qualified medical practitioners setting up a practice in semi urban and

rural areas, whose borrowing limits should not be less than Rs 15 lakh with a sub-

ceiling of Rs 3 lakh for working capital requirements.

CHALLENGES FACED BY SME:

The challenges being faced by the small and medium sector may be briefly set out as

Follows-

Small and Medium Enterprises (SME), particularly the tiny segment of the small

enterprises have inadequate access to finance due to lack of financial information and

non-formal business practices. SMEs also lack access to private equity and venture

capital and have a very limited access to secondary market instruments.

SMEs face fragmented markets in respect of their inputs as well as products and are

vulnerable to market fluctuations.

SMEs lack easy access to inter-state and international markets.

The access of SMEs to technology and product innovations is also limited. There is

lack of awareness of global best practices.

SMEs face considerable delays in the settlement of dues/payment of bills by the large

scale buyers. With the deregulation of the financial sector, the ability of the banks to

service the credit requirements of the SME sector depends on the underlying

transaction costs, efficient recovery processes and available security. There is an

immediate need for the banking sector to focus on credit and SMEs

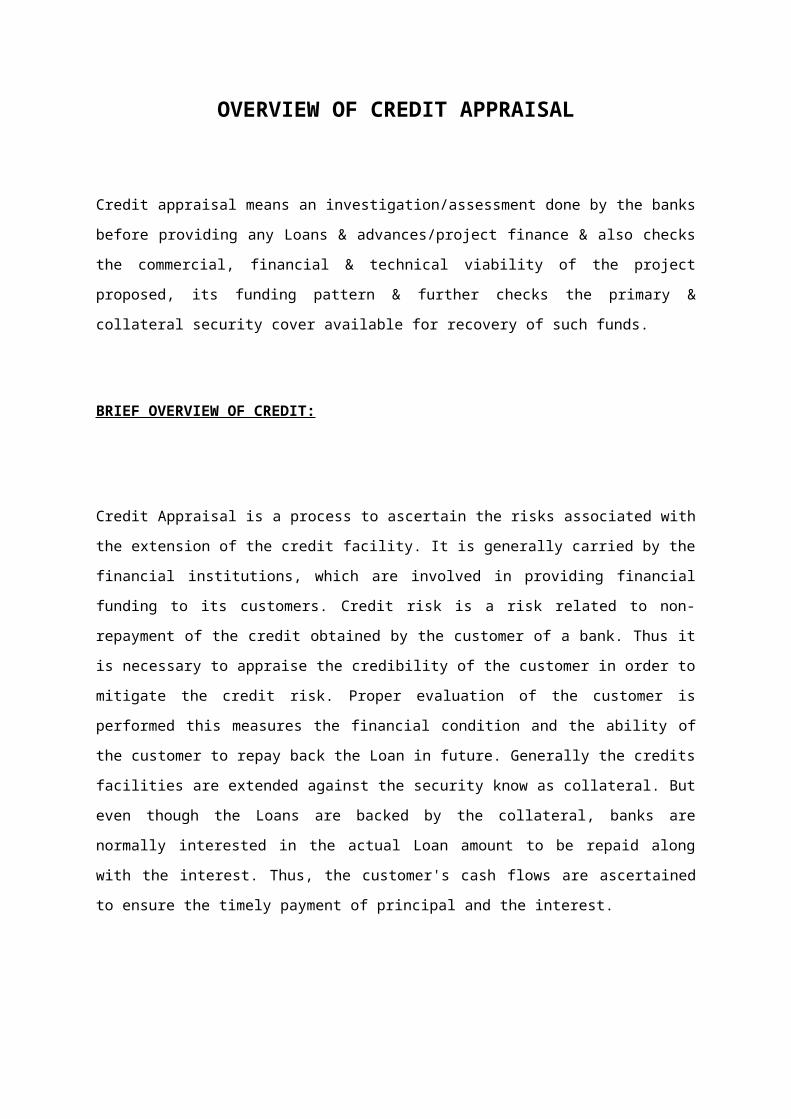

OVERVIEW OF CREDIT APPRAISAL

Credit appraisal means an investigation/assessment done by the banks before providing any Loans &

advances/project finance & also checks the commercial, financial & technical viability of the project

proposed, its funding pattern & further checks the primary & collateral security cover available for

recovery of such funds.

BRIEF OVERVIEW OF CREDIT:

Credit Appraisal is a process to ascertain the risks associated with the extension of the credit facility.

It is generally carried by the financial institutions, which are involved in providing financial funding to

its customers. Credit risk is a risk related to non-repayment of the credit obtained by the customer

of a bank. Thus it is necessary to appraise the credibility of the customer in order to mitigate the

credit risk. Proper evaluation of the customer is performed this measures the financial condition and

the ability of the customer to repay back the Loan in future. Generally the credits facilities are

extended against the security know as collateral. But even though the Loans are backed by the

collateral, banks are normally interested in the actual Loan amount to be repaid along with the

interest. Thus, the customer's cash flows are ascertained to ensure the timely payment of principal

and the interest.

It is the process of appraising the credit worthiness of a Loan applicant. Factors like age, income,

number of dependents, nature of employment, continuity of employment, repayment capacity,

previous Loans, credit cards, etc. are taken into account while appraising the credit worthiness of a

person. Every bank or lending institution has its own panel of officials for this purpose.

However the 3 ‘C’ of credit are crucial & relevant to all borrowers/ lending, which must be kept in

mind, at all times.

Character

Capacity

Collateral

If any one of these is missing in the equation then the lending officer must question the viability of

credit. There is no guarantee to ensure a Loan does not run into problems; however if proper credit

evaluation techniques and monitoring are implemented then naturally the Loan loss probability /

problems will be minimized, which should be the objective of every lending Officer.

Credit is the provision of resources (such as granting a Loan) by one party to another party where

that second party does not reimburse the first party immediately, thereby generating a debt, and

instead arranges either to repay or return those resources (or material(s) of equal value) at a later

date. The first party is called a creditor, also known as a lender, while the second party is called a

debtor, also known as a borrower.

Credit allows you to buy goods or commodities now, and pay for them later. We use credit to buy

things with an agreement to repay the Loans over a period of time. The most common way to avail

credit is by the use of credit cards. Other credit plans include personal Loans, home Loans, vehicle

Loans, student Loans, small business Loans, trade. A credit is a legal contract where one party

receives resource or wealth from another party and promises to repay him on a future date along

with interest. In simple Terms, a credit is an agreement of postponed payments of goods bought or

Loan. With the issuance of a credit, a debt is formed.

BASIC TYPES OF CREDIT:

There are four basic types of credit. By understanding how each works, you will be able to get the

most for your money and avoid paying unnecessary charges.

Service credit is monthly payments for utilities such as telephone, gas, electricity, and water. You

often have to pay a deposit, and you may pay a late charge if your payment is not on time.

Loans let you borrow cash. Loans can be for small or large amounts and for a few days or several

years. Money can be repaid in one lump sum or in several regular payments until the amount you

borrowed and the finance charges are paid in full. Loans can be secured or unsecured.

Installment credit may be described as buying on time, financing through the store or the easy

payment plan. The borrower takes the goods home in exchange for a promise to pay later. Cars,

major appliances, and furniture are often purchased this way. You usually sign a contract, make a

down payment, and agree to pay the balance with a specified number of equal payments called

installments. The finance charges are included in the payments. The item you purchase may be used

as security for the Loan.

Credit cards are issued by individual retail stores, banks, or businesses. Using a credit card can be

the equivalent of an interest-free Loan- end of each month.-if you pay for the use.

BRIEF OVERVIEW OF LOANS:

Loans can be of two types fund base & non-fund base:

Fund Base includes:

Working Capital

Term Loan

Non-fund Base includes:

Letter of Credit

Bank Guarantee

Fund Base:

Working capital

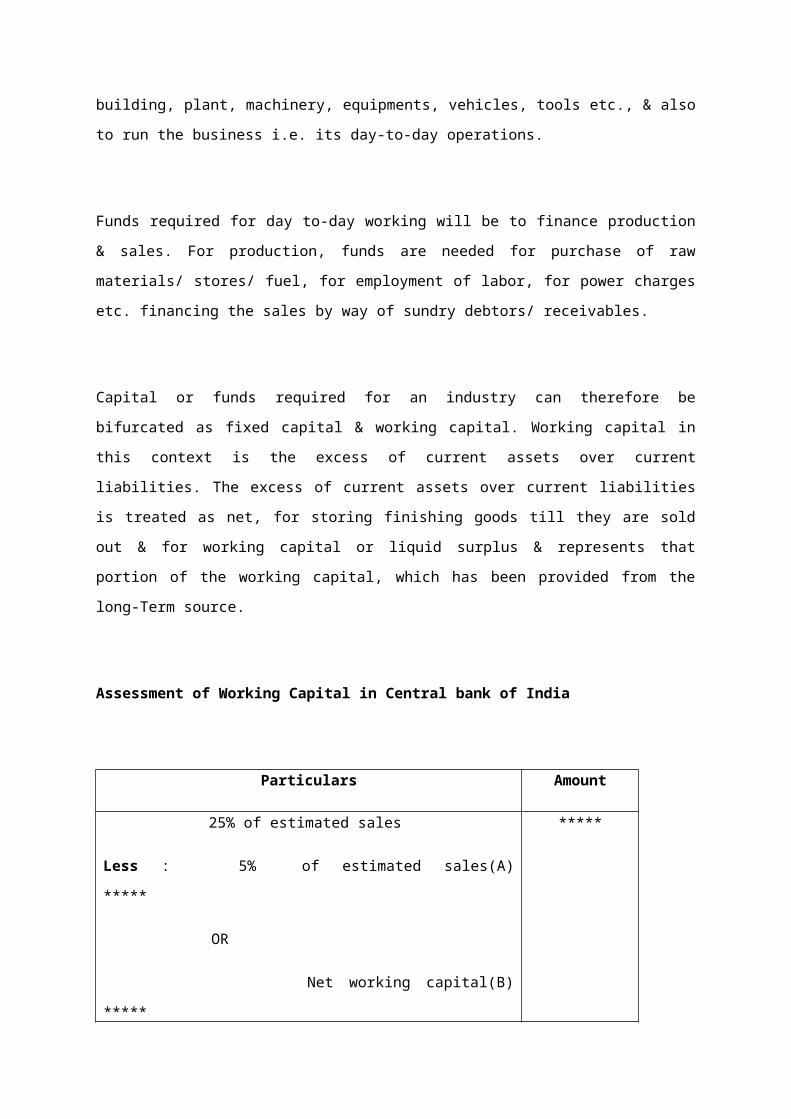

The objective of running any industry is earning profits. An industry will require funds to acquire

“fixed assets” like land, building, plant, machinery, equipments, vehicles, tools etc., & also to run the

business i.e. its day-to-day operations.

Funds required for day to-day working will be to finance production & sales. For production, funds

are needed for purchase of raw materials/ stores/ fuel, for employment of labor, for power charges

etc. financing the sales by way of sundry debtors/ receivables.

Capital or funds required for an industry can therefore be bifurcated as fixed capital & working

capital. Working capital in this context is the excess of current assets over current liabilities. The

excess of current assets over current liabilities is treated as net, for storing finishing goods till they

are sold out & for working capital or liquid surplus & represents that portion of the working capital,

which has been provided from the long-Term source.

Assessment of Working Capital in Central bank of India

Particulars Amount

25% of estimated sales

Less : 5% of estimated sales(A) *****

OR

Net working capital(B) *****

Which is higher ( A or B)

*****

*****

MPBF

(Maximum Permissible Bank Finance)

*****

Term Loan

A Term Loan is granted for a fixed Term of 3 years to 7 years intended normally for financing fixed

assets acquired with a repayment schedule normally not exceeding 8 years.

A Term Loan is a Loan granted for the purpose of capital assets, such as purchase of land,

construction of, buildings, purchase of machinery, modernization, renovation or rationalization of

plant, & repayable from out of the future earning of the enterprise, in installments, as per a

prearranged schedule.

From the above definition, the following differences between a Term Loan & the working capital

credit afforded by the Bank are apparent:

The purpose of the Term Loan is for acquisition of capital assets.

The Term Loan is an advance not repayable on demand but only in installments ranging

over a period of years.

The repayment of Term Loan is not out of sale proceeds of the goods & commodities per

se, whether given as security or not. The repayment should come out of the future cash

accruals from the activity of the unit.

The security is not the readily saleable goods & commodities but the fixed assets of the

units.

It may thus be observed that the scope & operation of the Term Loans are entirely different from

those of the conventional working capital advances. The Bank’s commitment is for a long period &

the risk involved is greater. An element of risk is inherent in any type of Loan because of the

uncertainty of the repayment. Longer the duration of the credit, greater is the attendant uncertainty

of repayment & consequently the risk involved also becomes greater.

However, it may be observed that Term Loans are not so lacking in liquidity as they appear to be.

These Loans are subject to a definite repayment programmed unlike short Term Loans for working

capital (especially the cash credits) which are being renewed year after year. Term Loans would be

repaid in a regular way from the anticipated income of the industry/ trade.

These distinctive characteristics of Term Loans distinguish them from the short Term credit granted

by the banks & it becomes necessary therefore, to adopt a different approach in examining the

applications of borrowers for such credit & for appraising such proposals.

The repayment of a Term Loan depends on the future income of the borrowing unit. Hence, the

primary task of the bank before granting Term Loans is to assure itself that the anticipated income

from the unit would provide the necessary amount for the repayment of the Loan. This will involve a

detailed scrutiny of the scheme, its capital assets. Financial aspects, economic aspects, technical

aspects, a projection of future trends of outputs & sales & estimates of cost, returns, flow of funds &

profits.

Eligibility of term loan

Particulars Amount

Cost of machineries *****

Cost of accessories/equipment *****

Total cost of machines *****

Less : 25% of margin *****

Eligible amount of term loan *****

Non-fund Base:

Letter of credit

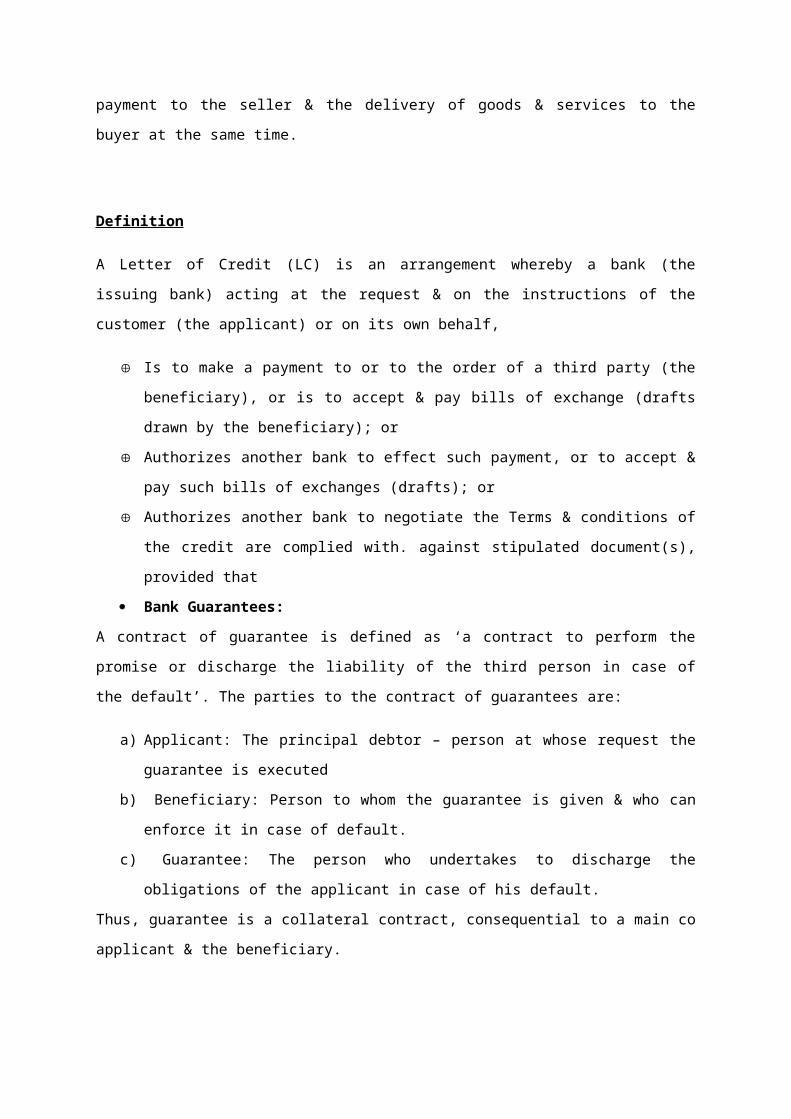

The expectation of the seller of any goods or services is that he should get the payment immediately

on delivery of the same. This may not materialize if the seller & the buyer are at different places

(either within the same country or in different countries). The seller desires to have an assurance for

payment by the purchaser. At the same time the purchaser desires that the amount should be paid

only when the goods are actually received. Here arises the need of Letter of Credit (LCs). The

objective of LC is to provide a means of payment to the seller & the delivery of goods & services to

the buyer at the same time.

Definition

A Letter of Credit (LC) is an arrangement whereby a bank (the issuing bank) acting at the request &

on the instructions of the customer (the applicant) or on its own behalf,

Is to make a payment to or to the order of a third party (the beneficiary), or is to accept &

pay bills of exchange (drafts drawn by the beneficiary); or

Authorizes another bank to effect such payment, or to accept & pay such bills of exchanges

(drafts); or

Authorizes another bank to negotiate the Terms & conditions of the credit are complied

with. against stipulated document(s), provided that

Bank Guarantees:

A contract of guarantee is defined as ‘a contract to perform the promise or discharge the liability of

the third person in case of the default’. The parties to the contract of guarantees are:

a) Applicant: The principal debtor – person at whose request the guarantee is executed

b) Beneficiary: Person to whom the guarantee is given & who can enforce it in case of default.

c) Guarantee: The person who undertakes to discharge the obligations of the applicant in case

of his default.

Thus, guarantee is a collateral contract, consequential to a main co applicant & the beneficiary.

Purpose of Bank Guarantees

Bank Guarantees are used to for both preventive & remedial purposes. The guarantees executed by

banks comprise both performance guarantees & financial guarantees. The guarantees are structured

according to the Terms of agreement, viz., security, maturity & purpose.

Branches may issue guarantees generally for the following purposes:

a) In lieu of security deposit/earnest money deposit for participating in tenders;

b) Mobilization advance or advance money before commencement of the project by the

contractor & for money to be received in various stages like plant layout, design/drawings in

project finance;

c) In respect of raw materials supplies or for advances by the buyers;

d) In respect of due performance of specific contracts by the borrowers & for obtaining full

payment of the bills;

e) Performance guarantee for warranty period on completion of contract which would enable

the suppliers to period to be over; realize the proceeds without waiting for warranty) To

allow units to draw funds from time to time from the concerned indenters against part

execution of contracts, etc.

f) Bid bonds on behalf of exporters

g) Export performance guarantees on behalf of exporters favoring the Customs Department

under EPCG scheme.

CREDIT APPRAISAL PROCESS:

Receipt of application from applicant

Receipt of documents

(Balance sheet, KYC papers, Different govt. registration no., MOA, AOA, and properties documents

Pre-sanction visit by bank officers

Check for RBI defaulters list, willful defaulters list, CIBIL data, ECGC, Caution list etc

Title clearance reports of the properties to be obtained from empanelled

Advocates

Valuation reports of the properties to be obtained from empanelled valuer/engineers

Preparation of financial data

LOAN ADMINISTRATION PRE- SANCTION PROCESS:

Appraisal, Assessment and Sanction functions

1. Appraisal

A. Preliminary appraisal

Sound credit appraisal involves analysis of the viability of operations of a business and the

capacity of the promoters to run it profitably and repay the bank the dues as and when they fall

Towards this end the preliminary appraisal will examine the following aspects of a proposal.

Bank’s lending policy and other relevant guidelines/RBI guidelines,

Prudential Exposure norms,

Industry Exposure restrictions,

Group Exposure restrictions,

Industry related risk factors,

Credit risk rating,

Profile of the promoters/senior management personnel of the project,

List of defaulters,

Caution lists,

Acceptability of the promoters,

Compliance regarding transfer of borrower accounts from one bank to another, if applicable;

Government regulations/legislation impacting on the industry; e.g., ban on financing of

industries producing/ consuming Ozone depleting substances;

Applicant’s status vis-à-vis other units in the industry,

Financial status in broad Terms and whether it is acceptable The Company’s Memorandum

and Articles of Association should be scrutinized carefully to ensure (i) that there are no

clauses prejudicial to the Bank’s interests, (ii) no limitations have been placed on the

Company’s borrowing powers and operations and (iii) the scope of activity of the company.

Required Documents for Process of Loan

Application for requirement of loan

Proposal preparation

Assessment of proposal

Documentations, agreements, mortgages

Sanction/approval of proposal by appropriate sanctioning authority

Disbursement of Loan

Post sanction activities

Copy of Memorandum & Article of Association

Copy of incorporation of business

Copy of commencement of business

Copy of resolution regarding the requirement of credit facilities

Brief history of company, its customers & supplies, previous track records, orders In hand.

Also provide some information about the directors of the company

Financial statements of last 3 years including the provisional financial statement for the year

2010-11

Copy of PAN/TAN number of company

Copy of last Electricity bill of company

Copy of GST/CST number

Copy of Excise number

Photo I.D. of all the directors

Address proof of all the directors

Copies related to the property such as 7/12 & 8A utara, lease/ sales deed, 2R Permission,

Allotment letter, Possession

Bio-data form of all the directors duly filled & notarized

Financial statements of associate concern for the last 3 years

After undertaking the above preliminary examination of the proposal, the branch will arrive at a

decision whether to support the request or not. If the branch (a reference to the branch includes

a reference to SECC/CPC etc. as the case may be) finds the proposal acceptable, it will call for

from the applicant(s), a comprehensive application in the prescribed proforma, along with a

copy of the proposal/project report, covering specific credit requirement of the company and

other essential data/ information. The information, among other things, should include:

Organizational set up with a list of Board of Directors and indicating the qualifications,

experience and competence of the key personnel in charge of the main functional areas

e.g., purchase, production, marketing and finance; in other words a brief on the managerial

resources and whether these are compatible with the size and scope of the proposed

activity.

Demand and supply projections based on the overall market prospects together with a copy

of the market survey report. The report may comment on the geographic spread of the

market where the unit proposes to operate, demand and supply gap, the competitors’ share,

competitive advantage of the applicant, proposed marketing arrangement, etc.

Current practices for the particular product/service especially relating to Terms of credit

sales, probability of bad debts, etc.

Estimates of sales cost of production and profitability.

Projected profit and loss account and balance sheet for the operating years during the

Currency of the Bank assistance.

If request includes financing of project(s), branch should obtain additionally

Appraisal report from any other bank/financial institution in case appraisal has been

done by them.

‘No Objection Certificate’ from Term lenders if already financed by them and

Report from Merchant bankers in case the company plans to access capital market,

wherever necessary.

In respect of existing concerns, in addition to the above, particulars regarding the history of the

concern, its past performance, present financial position, etc. should also be called for. This

data/information should be supplemented by the supporting statements

Such as:

Audited profit loss account and balance sheet for the past three years (if the latest audited

balance sheet is more than 6 months old, a pro-forma balance sheet as on a recent date

should be obtained and analyzed). For non-corporate borrowers, irrespective of market

segment, enjoying credit limits of Rs.10 lacs and above from the banking system, audited

balance sheet in the IBA approved formats should be submitted by the borrowers.

Details of existing borrowing arrangements, if any,

Credit information reports from the existing bankers on the applicant Company, and

Financial statements and borrowing relationship of Associate firms/Group Companies.

B. Detailed Appraisal

The viability of a project is examined to ascertain that the company would have the ability to

service its Loan and interest obligations out of cash accruals from the business. While appraising

a project or a Loan proposal, all the data/information furnished by the borrower should be

counter checked and, wherever possible, inter-firm and inter-industry comparisons should be

made to establish their veracity.

The financial analysis carried out on the basis of the company’s audited balance sheets and

profit and loss accounts for the last three years should help to establish the current viability.

In addition to the financials, the following aspects should also be examined:

The method of depreciation followed by the company-whether the company is following

straight line method or written down value method and whether the company has changed

the method of depreciation in the past and, if so, the reason therefore;

Whether the company has revalued any of its fixed assets any time in the past and the

present status of the revaluation reserve, if any created for the purpose;

Record of major defaults, if any, in repayment in the past and history of past sickness,

The position regarding the company’s tax assessment - whether the provisions made in the

balance sheets are adequate to take care of the company’s tax liabilities;

The nature and purpose of the contingent liabilities, together with comments thereon;

Pending suits by or against the company and their financial implications (e.g. cases relating

to customs and excise, sales tax, etc.);

Qualifications/adverse remarks, if any, made by the statutory auditors on the company’s

accounts;

Dividend policy;

Apart from financial ratios, other ratios relevant to the project;

Trends in sales and profitability, past deviations in sales and profit projections, and

estimates/projections of sales values;

Production capacity & use: past and projected;

o Estimated requirement of working capital finance with reference to acceptable build

up of inventory/ receivables/ other current assets;

Projected levels: whether acceptable; and

Compliance with lending norms and other mandatory guidelines as applicable

Project financing:

If the proposal involves financing a new project, the commercial, economic and

Financial viability and other aspects are to be examined as indicated below:

Statutory clearances from various Government Depts. / Agencies

Licenses/permits/approvals/clearances/NOCs/Collaboration agreements, as applicable

Details of sourcing of energy requirements, power, fuel etc.

Pollution control clearance

Cost of project and source of finance

Build-up of fixed assets (requirement of funds for investments in fixed assets to be critically

examined with regard to production factors, improvement in quality of products, economies

of scale etc.)

Arrangements proposed for raising debt and equity

Capital structure (position of Authorized, Issued/ Paid-up Capital, Redeemable

o Preference Shares, etc.)

Debt component i.e., debentures, Term Loans, deferred payment facilities, unsecured

Loans/ deposits. All unsecured Loans/ deposits raised by the company for financing a project

should be subordinate to the Term Loans of the banks/ financial institutions and should be

permitted to be repaid only with the prior approval of all the banks and the financial

institutions concerned. Where central or state sales tax Loan or developmental Loan is taken

as source of financing the project, furnish details of the Terms and conditions governing the

Loan like the rate of interest (if applicable), the manner of repayment, etc.

Feasibility of arrangements to access capital market

Feasibility of the projections/ estimates of sales, cost of production and profits covering the

period of repayment

Break Even Point in Terms of sales value and percentage of installed capacity under a

o Normal production year

Cash flows and fund flows

Proposed amortization schedule

Whether profitability is adequate to meet stipulated repayments with reference to Debt

Service Coverage Ratio, Return on Investment

Industry profile & prospects

Critical factors of the industry and whether the assessment of these and management plans

in this regard are acceptable

Technical feasibility with reference to report of technical consultants, if available

Management quality, competence, track record

Company’s structure & systems

Applicant’s strength on inter-firm comparisons

For the purpose of inter-firm comparison and other information, where necessary, source data from

Stock Exchange Directory, financial journals/ publications, professional entities like CRIS-INFAC,

CMIE, etc. with emphasis on following aspects:

Market share of the units under comparison

Unique features

Profitability factors

Financing pattern of the business

Inventory/Receivable levels

Capacity utilization

Production efficiency and costs

Bank borrowings patterns

Financial ratios & other relevant ratios

Capital Market Perceptions

Current price

52week high and low of the share price

P/E ratio or P/E Multiple

Yield (%)- half yearly and yearly

Also examine and comment on the status of approvals from other Term lenders, market view (if

anything adverse), and project implementation schedule. A pre-sanction inspection of the project

site or the factory should be carried out in the case of existing units. To ensure a higher degree of

commitment from the promoters, the portion of the equity / Loans which is proposed to be brought

in by the promoters, their family members, friends and relatives will have to be brought upfront.

However, relaxation in this regard may be considered on a case to case basis for genuine and

acceptable reasons. Under such circumstances, the promoter should furnish a definite plan

indicating clearly the sources for meeting his contribution. The balance amount proposed to be

raised from other sources, viz., debentures, public equity etc., should also be fully tied up.

C. Present relationship with Bank:

Compile for existing customers, profile of present exposures:

Credit facilities now granted

Conduct of the existing account

Utilization of limits - FB & NFB

Occurrence of irregularities, if any

Frequency of irregularity i.e., number of times and total number of days the account was

irregular during the last twelve months

Repayment of Term commitments

Compliance with requirements regarding submission of stock statements, Financial

Follow-up Reports, renewal data, etc.

Stock turnover, realization of book debts

Value of account with break-up of income earned

Pro-rata share of non-fund and foreign exchange business

Concessions extended and value thereof

Compliance with other Terms and conditions

Action taken on Comments/observations contained in RBI Inspection Reports: CO

Inspection & Audit Reports

D. Credit risk rating : Draw up rating for (i) Working Capital and (ii) Term Finance.

E. Opinion Reports : Compile opinion reports on the company, partners/ promoters

and the proposed guarantors.

F. Existing charges on assets of the unit : If a company, report on search of charges

with ROC.

G. Structure of facilities and Terms of Sanction:

Fix Terms and conditions for exposures proposed - facility wise and overall:

Limit for each facility – sub-limits

Security - Primary & Collateral, Guarantee

Margins - For each facility as applicable

Rate of interest

Rate of commission/exchange/other fees

Concessional facilities and value thereof

Repayment Terms, where applicable

ECGC cover where applicable

Other standard covenants

H. Review of the proposal:

Review of the proposal should be done covering (i) strengths and weaknesses of the exposure

proposed (ii) risk factors and steps proposed to mitigate them

(ii) Deviations, if any, proposed from usual norms of the Bank and the reasons therefore

I. Proposal for sanction:

Prepare a draft proposal in prescribed format with required backup details and with

recommendations for sanction.

J. Assistance to Assessment:

Interact with the assessor, provide additional inputs arising from the assessment, incorporate these

and required modifications in the draft proposal and generate an integrated final proposal for

sanction.

2. Assessment :

Indicative List of Activities Involved in Assessment Function is given below:

Review the draft proposal together with the back-up details/notes, and the borrower’s

application, financial statements and other reports/documents examined by the appraiser.

Interact with the borrower and the appraiser.

Carry out pre-sanction visit to the applicant company and their project/factory site.

Peruse the financial analysis (Balance Sheet/ Operating Statement/ Ratio Analysis/

Fund Flow Statement/ Working Capital assessment/Project cost & sources/ Break Even

analysis/Debt Service/Security Cover, etc.) to see if this is prima facie in order. If any

deficiencies are seen, arrange with the appraiser for the analysis on the correct lines.

Examine critically the following aspects of the proposed exposure.

Bank’s lending policy and other guidelines issued by the Bank from time to time

RBI guidelines

Background of promoters/ senior management

Inter-firm comparison

Technology in use in the company

Market conditions

Projected performance of the borrower vis-à-vis past estimates and performance

Viability of the project

Strengths and Weaknesses of the borrower entity.

Proposed structure of facilities.

Adequacy/ correctness of limits/ sub limits, margins, moratorium and repayment schedule

Adequacy of proposed security cover o Credit risk rating

Pricing and other charges and concessions, if any, proposed for the facilities

Risk factors of the proposal and steps proposed to mitigate the risk

Deviations proposed from the norms of the Bank and justifications there for

To the extent the inputs/comments are inadequate or require modification, arrange for

additional inputs/ modifications to be incorporated in the proposal, with any required

modification to the initial recommendation by the Appraiser

Arrange with the Appraiser to draw up the proposal in the final form.

Recommendation for sanction: Recapitulate briefly the conclusions of the appraisal and

state whether the proposal is economically viable. Recount briefly the value of the