copyright: dcg - this material should not be shared or copied without the consent of dcg overview of...

TRANSCRIPT

Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Overview of Asset Management

A Level 1 CertificationDCG – Domain Enablement Initiative

2Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Course Overview

•Introduction to Asset Management 3 – 5

•Mutual Funds 6 – 44

•Hedge Funds 45 - 53

•Wealth Management 54 - 65

3Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Introduction to Asset Management

4Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

What is Asset Management?

Management of tangible assets such as

– Securities

– Currency

– Real estate

– Commodities …

In the Securities industry, the term means investment and management of financial assets (money and securities) by asset managers.

Classifications:

–Proprietary funds: Own funds of any corporation, institution, bank treasury management

–Public Investment Funds : Mutual Funds, Pension plans, 401(K) plans

–Special : Hedge funds, Private wealth Management

–Nature of Investment : Stock funds, Emerging market funds

5Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

What does it involve ?

• Meeting Objectives

– Maximize returns within the asset class or portfolio for a defined amount of risk

– Manage fund according to prospectus, corporate guidelines

– Meet specified regulatory, tax and liquidity requirements

• Responsibilities:

– to the investor(s), shareholders

– to the Trustees/ Corporate Board

– to the regulator, central authorities

• Operational:

– Managed by Investment / Fund managers supported by research analysts

– Performance measured against benchmarks

– Remuneration as performance fees

6Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Players in the Asset Management Industry

• Mutual Funds

• Hedge Funds

• Wealth Managers

• Money Managers

• Financial Advisors

What all is included in asset management?

7Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Mutual Funds

8Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Mutual Funds

• A collection of assets managed by an investment company on behalf of many investors with similar investment objectives

• An investment company is a Financial Intermediary that raises funds entirely by issuing equity claims or shares or units.

• For example, Vanguard 500 Index's VFINX four largest holdings are Microsoft MSFT (3.25% of its portfolio as of June 2002), General Electric GE (3.16%), ExxonMobil XOM (3.04%), and Wal-Mart Stores WMT (2.68%). Your $1,000 investment in the fund means you own $32.50 worth of Microsoft, $31.60 of General Electric, and so on. In an indirect way, you own the 500 stocks in the fund's portfolio.

• Why Mutual Funds

– Diversification

– Professional Management

– Liquidity

– Different Products for Various Needs

9Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Banking Banking

Board of

Trustee

Board of

Trustee

Mutual Fund - Concept

Investors - Institutional, RetailInvestors - Institutional, Retail

M F Asset management CompanyM F Asset management Company

Broker - AgentsBroker - Agents

Security Issuers / ExchangeSecurity Issuers / Exchange

Regulator Regulator

BrokingBroking

Other

services

Other

services

Custody Custody

10Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Why Mutual Fund?• Investment Barrier

• How many can you buy?

• Continuous call on market

• Information search

• Transaction costs

• Risk concentration

• More stocks exposure for a given sum

• Sharing of risk

• Professional support

• Research and information efficiency

• Ability to take part in private placement deals

• Transaction cost efficiency

• More stocks exposure for a given sum

• Sharing of risk

• Professional support

• Research and information efficiency

• Ability to take part in private placement deals

• Transaction cost efficiency

– Convenient

– Well diversified

– Professional fund management services at low cost

– Tax efficient

– Well regulated

– BUT, no control over what securities are bought / sold

– Expenses are passed on to investors (for marketing, sales loads, management etc)

– Convenient

– Well diversified

– Professional fund management services at low cost

– Tax efficient

– Well regulated

– BUT, no control over what securities are bought / sold

– Expenses are passed on to investors (for marketing, sales loads, management etc)

11Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Types of Mutual Funds• Closed Vs Open Ended Funds

• Growth Vs Income Funds (Stock Vs Bonds)• Balanced Funds (Mix of Growth & Income)• Index Funds (Active Vs Passive Management)• Sector Funds - Utilities (AT&T, Pacific Gas, Consumer’s Waters etc) / Energy ( Chevron,

Pennzoil, Noble Drilling etc) / Financial (Amex, JPM, Citi etc) / Retail, Technology, Consumer durables, Health etc. – T Rowe Price Media and Telecommunications (PRMTX)

Open Ended Closed Ended

No defined Life Life is Fixed

Issues & Redeems shares on demand – No limit to number of shares

Set No. of shares that trade in an exchange

Transaction at NAV Transactions at Market Price

12Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Types of Mutual Funds - Contd….• Large Cap / Mid Cap / Small Cap / Micro Cap

• Load vs No-Load fund• Pension Funds

– Sold to corporate– Matching contribution - Employer, Government– Tax breaks - PF, 401 K

Large Cap Mid Cap Small Cap Micro Cap

Features & Risk – Return Equations

>5 Billion USD

Less Volatile. Established. Moderate returns.

Janus Advisor Cap Appreciation

1 to 5 Billion

Moderate Volatility. Good option to diversify

Fidelity Advisor Midcap T

< 1 Billion

Growing Firms. High Risk

Berger Small Cap Value

< 250 Million

Start Ups or Take over targets

Franklin Microcap Value

13Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Mutual Fund – by Investment Objective

• Growth Vs Value Funds – Blend Funds• Money Market Funds – Liquid Funds – Best for parking money

short term – Vanguard Prime Money Market Fund• Municipal Bonds – Munis – Bonds issued for building state or

national facilities. These are tax exempt. – Drefus General NY Muni Bond

• Multi Funds – Fund on Fund• Real Estate Investment Trusts (REITs) – Fidelity Real Estate

Investments• Global Funds, International Funds, Country Specific and

Emerging Markets – Morgan Stanley Emerging Market Debt, GMO World Equity, T Row Price Latin America etc.

Growth?..Aggressive growth?……Income?…Value?…Liquidity?….Tax planning?……

14Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

MF Service Models

Main Services Offered :Fund Performance Savings PlanningLiquidity Risk managementFinancial Information Tax efficiencyFinancial flexibility Easy Operability

Service Models for an MF• To primarily have own set up for marketing, distribution and front

end processing • To concentrate on asset management and corporate marketing but

outsource distribution and processing to channels• To become a financial supermarket offering a variety of services

related to asset management

15Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

MF Broker Service Model

Services to The Investor• Distribution MF Products -

Collection of money, applications• Provide Liquidity - by handling

repurchase orders• Account details of investors• Operational support - funding,

switching• Fund administration• Information about MF company• Financial Advisory Services• Market Information

Services to the Fund

Marketing services• Share operational load

– Pricing of trades

– Pre and post trade processing

– Maintain shareholders register& accounting

• Wholesale Collection & payment services

• Credible distribution mechanism & Reach

• Complimentary investor services (like banking, share trading)

16Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

FUNDS – SALES AND DISTRIBUTION

Client servicing

Investment back-office

PortfolioManagement

Investment Sales & Marketing

• Providing market information

• Marketing of Products

• Financial Advice• Distribution

through,•Institutional Sales Force •Brokerage Firms •Banks •Insurance Companies •Financial Planners •Registered Investment Advisors

17Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund Distributor

• Exclusive right of selling shares as ‘principal underwriter’

• Registered as a broker dealer

• Responsible for ‘suitability’ of sale to investors

• Affiliated to fund company

• Distributes funds through

– Own agents

– As wholesaler – through other broker dealers

• Selling through brokers can be proprietary (eg: AEFA, Merrill funds) or non proprietary (e.g Putnam, Franklin)

– The latter sells mainly loaded funds

18Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Distribution

• The Asset management company typically uses distribution channels to sell funds

– Open end funds redeem / sell any number of shares on any business day

• Assets in billion dollars

38%

31%

16%

11%4%

Distribution (direct) #

Third party brokers

Captive

Bank

Institutional

# includes direct sales, sales thru fund supermarkets, financial advisors, DC plans etc

@ Source :Financial Research Corporation

19Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Distribution channels

• DIRECT - Typically no load funds– Pure Direct : Fund company directly sells to

investor• Eg: Fidelity, Vanguard

– Supermarkets : • Discount brokerage – help smaller funds

sales, does detailed record keeping also• No txn fees for customers- Commissions

based on AUM and funded via 12 b fees• eg Schwab

• INTERMEDIATED – Broker dealers– Banks– Retirement plans– Financial advisers, wrap programs

• Fee based package of advice and securities (funds) broking;

no trading commissions• Offered by financial advisors/brokerages

CLIENT PROFILINGAdviser conducts a thorough assessment of client’s financial status, investment objectives, time horizon, and risk tolerance.ASSET ALLOCATIONInvestment consultants evaluate profile and, with client’s approval, allocate the dollars to the appropriate products (securities, funds) / investment managers.MONITORINGConsultants track portfolio performance, reporting to adviser and client on a regular basisASSET-BASED FEESCost is an all-in-one fee that covers all the services. The fee is between 1- 3% but drops with the size of the account and through discounting.

20Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Mutual Fund - Financials

• Load – Sales Commission – Front End or Deferred sales Fee (Back End)

• Redemption Fee – Operate for short life periods to discourage redemptions.

• Administration Fee – Basic Fund Operations, Office Space, Custody Fee, R&T Fee , Brokerage etc.

• Management Fee – Advisors Fee

• Taxes

• Expense Ratio is Expenses / Total Assets – The lower it is, the better.

21Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Front-end load or sales charge is added to the sale price of an open mutual fund share; the loads vary usually from 1% upwards (maximum permissible is 8.5% of NAV) and are usually used to pay commissions to brokers / agents who sell the funds.

A redemption fee, deferred sales charge, or back end load refers to the amount deducted when the mutual fund shares are redeemed or repurchased. In many cases, they are reduced gradually to zero after a long enough holding period (period when the investor holds the shares).

A mutual fund that has neither front end nor back ended charges is called a no-load fund. No-load funds are generally not sold through brokers or financial advisors, but are sold directly to investors.

Mutual funds – Fee & Structure

All Mutual funds charge annual operating expenses for management, research, trading and administrative expenses.

The asset management fees, which is paid to the AMC, is usually the largest ranging from 0.75 % - 1.5% typically (of funds managed)

Marketing fees are charged annually for eg. In US a Rule 12b-1 fee is used to pay either commissions or advertising expenses and is charged annually (maximum permissible is 0.75% of average assets).

A fund can also offer different classes of shares (A, B or C). these represent ownership in the same mutual fund, but are differentiated based on certain parameters such as specific time of entry. These are also used to provide different shareholder cost structures to investors

22Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Regulation• SEC regulates Investment companies• NASD regulates B/ D• Four principal acts govern Mutual Funds

– Investment Company Act, 1940– Securities Act, 1933– Securities Exchange Act, 1934– Investment Advisers Act, 1940

• 1940 Investment Company Act imposes specific requirements for fund companies– Registration, capital requirements– Investment objective, prospectus– NAV reporting

• Rule 12b – Distribution expenses• Rule 134 / 135 A/ 482– advertising• Rule 18f-3 – multi-class shares• Fund Prospectus and disclosure

23Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

FUNDS – MANAGEMENT

Client servicing

Investment mid & back-office

PortfolioManagement

Investment Sales & Marketing

• Track investment opportunities

• Identify securities in each asset class

• Build thorough understanding of the risks in each asset class

• Identify the lowest cost opportunity of trading and execution

• Solicit quotes from floor brokers

• Place orders and execute trades

• Ensure compliance• Manage risks and

liquidity

24Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Portfolio Management• Asset Allocation

– Fund manager decides on initial asset allocation in adherence with investment guidelines

– Fund manager sees cash position everyday– Deploys cash– Adopts either

• Stock Picking (Bottom-Up) strategy• Top Down approach

• Portfolio Realignment– Keeps realigning the portfolio to investment objectives

• Enters trading strategies / orders into PMS– May not have a PMS / may just inform Traders to enter into

OMS• Portfolio Manager - Traits Needed

– Constant monitoring of companies, stock & bond prices, news, etc.

– Quick thinking of impact of news on stock and bond prices; Analysis of companies

– Relationships with company management to understand business strategies adopted by companies

Asset Allocation

Portfolio Realignment

25Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Portfolio Analysis

• Slicing & dicing the portfolio

– Asset Classes – Equities, Bonds, G-Secs, Derivatives, Convertibles,

Real Estate, etc.

– Sectoral Allocation

– Geographical Spread

• Risk-Return (Expected) Tradeoff

– Optimal combination of risk-return

– Mean-variance analysis

– Own analysis models – qualitative, quantitative, etc.

26Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Investment Research & Analysis

• Fundamental research

– Equity Research

– Fixed Income, others

– Economic data

– Internal versus Third-party (mainly broker) research

• Approach

– Top-down

– Bottom-up

• Technical Analysis

• Research evaluation

27Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Order Management• Order generation

– PM’s order is taken by Trader who “works the order”– Order will be fed into Order Management System (OMS)

• Block trades– Large orders (could be clubbing of small orders) executed

within a certain price– Negotiated trades

• Compliance– All AMCs have to meet strict compliance rules

• External: market regulator norms (% holding, sale rules, etc.); stock-exchange (blacklists)

• Internal: broad investment objectives; % holdings; blacklisted sectors / companies; etc.

– Order is checked for compliance– Vendor-developed compliance systems

• Execution / Dealing– Trader may get Indication of Interest (IOIs) from brokers– Has to keep Portfolio Manager updated on Order Execution

• Notice Of Execution (NOE)– Broker gives NOE to Trader; entered into OMS; feeds to PMS– Portfolio manager constantly monitors PMS for executed trades

Price Feeds to OMS

Working the Order

Compliance

28Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

INVESTMENT MANAGEMENT

Client servicing

Investment mid &

back-office

PortfolioManagement

Investment Sales & Marketing

• Portfolio modeling

• Risk management

• Allocation• Confirm trade

• Reconciliation of positions & trades

• Performance measurement

• Fund accounting

• Custody services

29Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Risk Management• Systematic and Unsystematic Risks• Risk Management

– Limit monitoring– Value at Risk (VAR) for Market Risk– Trend towards computationally intensive risk

management• Collecting & using information

– Reliable news and price sources – Reuters, Bloomberg, Thomson, Dow Jones

– Stock Exchanges, Derivatives Exchanges• Common risk models & risk analytics vendors

– Barra– Riskmetrics – started by JP Morgan– Standard & Poors (mainly for debt)– Moodys – acquired KMV

Sources of Risk

Market Risk – price moves

adversely

Credit Risk – counterparty

does pay (more relevant for

debt)

Liquidity Risk – cannot enter

or exit huge positions

Settlement Risk – cannot

settle transactions (more for

cross-border transactions)

Regulatory Risk

30Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Performance Measurement

• Performance is the KEY (and probably only) measure– Helps in marketing & getting more Assets for management– Need to perform better than peers

• Performance Measurement– Absolute Performance – Net Asset Value (mandatory for

mutual funds)– Relative Performance – benchmarked against broad market

indices• Performance Attribution

– Securities contributing to performance– Act: Portfolio Realign

• Performance Measurement Vendors– Lipper Analytics– Russel Analytics

Remember: Fund is different from

the Asset Management

Company (AMC)

AMC’s revenue depends on

Assets Under Management

Performance

31Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Investment Back-office• Investment Operations

– Trade confirmation, allocation, reconciliation

– Custodial interactions

– Bank interactions

• Fund Accounting (Detailed Slide)

– Account for net assets

– Fees for the AMC

– Expenses borne by the Fund – apportioned Sales expenses; advisory expenses; etc.

• Securities data management

– Static Data – Securities Master

– Price Hub – feeds from exchanges or pricing vendors – Price Master

• Compliance

– Pre / post trade – external and internal compliance

– Risk management – monitor risk

32Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Back Office Processes

• Allocation

– Allocate securities to various funds

• Confirmation of Net Proceeds

– Brokerage

– Average price of execution

• Reconciliation

– Trades / Positions with Brokers

– Cash with Brokers / Banks

– Securities Holdings with Custodials

33Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Custodial Operations (Question)– Settle cash / securities, Regulatory / other reporting– Safe keeping of assets, depository accounts– Corporate actions– Securities lending, credit lines

Corporate 1Fund F1 Fund F2Corporate security 2 Corporate security 4

Corporate 2Custodian SecurityA 2A 4 Corporate 3B 1

Fund F3 Fund F4 B 2Corporate security 1 Corporate security 3 B 3 Corporate 4Corporate security 2

DEPOSITORY

Custodian A

Custodian B

34Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund Accounting - Key Functions (Questions)

• Effect trades and settlements

• Effect capital changes

• Record corporate actions on underlying

• Record expenses & fees

• Calculate NAV

• Effect distribution announcements

• Reports

• Reconciliation

35Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

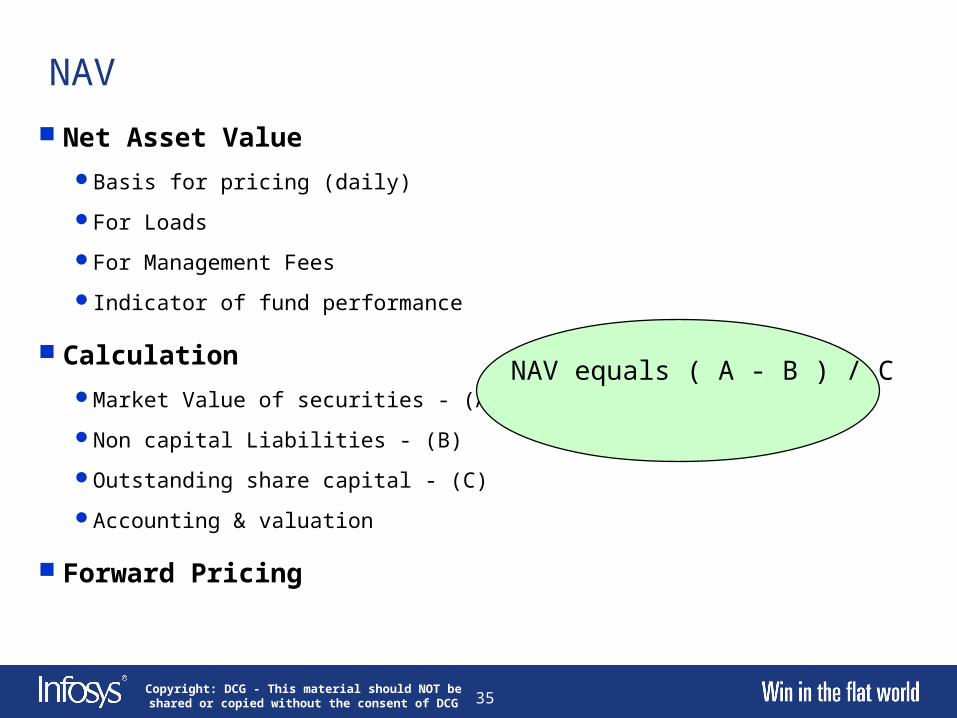

NAV

Net Asset Value

Basis for pricing (daily)

For Loads

For Management Fees

Indicator of fund performance

Calculation

Market Value of securities - (A)

Non capital Liabilities - (B)

Outstanding share capital - (C)

Accounting & valuation

Forward Pricing

NAV equals ( A - B ) / C

36Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

An Illustration of NAVPUMA FUNDS - BALANCE SHEET

On Dec 31, 2000 ( in $ '000)

Liabilities Assets Mkt Value

Issued shares 1000 Value of Investments 900 1500 ( # 0.1 mn shares)Reserves 400 Cash 300 300Others 100 Others 300 300

Total 1500 Total 1500

NAV (31-12-00) 2 million $NAV per share 20 $

On Dec 31, 2001 ( in $ '000)

Liabilities Assets Mkt Value

Issued shares 600 Value of Investments 500 600 (# 0.05 mn shares)Reserves 100 Cash 50 50Others 100 Others 250 250

Total 800 Total 800

NAV (31-12-01) ?? million $ 0.8NAV per share ? $ 16

Questions:

1. What has been the growth in NAV of the fund?

2. Has it done well ?

NASD100 :

2500 (31/12/00)

1500 (31/12/01)

37Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

CLIENT SERVICING PROCESSES

Client servicingInvestment

mid & back-office

PortfolioManagement

Investment Sales & Marketing

• Shareholder accounting & maintenance

• Commissions

• Tax

38Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Key Entities

AMC

Brokers & distribution

Intermediaries

Third partyService

providers (transfer agent,

auditor..)Industry infrastructure (Mkt data, DTCC, MU)

Securities Market

Participants (broker,

custodian)

Investor

Money Flow

Brokerage / fees

Fees

Commissions

share

purchases

Redemptions, distribution

Market purchases/ sales

Fees, charges Fees

Fund

39Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

• Nearly every function can be contracted out by fund!

– Investment advisory – Research services– typically in-house by AMC

– Transfer agents– Fund accounting– Custodial services– Auditing– Consulting & Legal

• Analytical and Rating services ( Lipper, Morningstar, Strategic Insight..)

Third Party Services

Typical MF Fee expenses

% of AUMAMC (advisory & administration) 0.467Shareholder servicing 0.115Custody 0.023Audit 0.004Legal 0.004Others (printing, postage, taxes..) 0.03

Total 0.643 (Source: Strategic Insight, 1998)

40Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Brokers – 2 Roles

• BROKER (Sell side)– Intermediary for investing in capital markets– Earn brokerage fees from funds

• BROKER (Selling intermediary)– Sells fund shares– Other services (account keeping, distribution etc.)– Earns commission : front end, trailing or back end, 12-b fees

41Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund Distributions

• Capital Gains

• Distributions from a fund– Dividends– Capital Gains

• Cash or Reinvestment proceeds– Reinvestment at NAV

• Winding up of a fund

How does an investor obtain returns from a MF investment?

42Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund Distributions - Tax

• Tax impact on the Mutual Fund– Usually favorable tax rates for MF

• Tax impact on Investors– Flow through based on source of distributed income (L.T.

capital gain / tax free interest/ dividend)– Resident status; Foreign taxes– Valuation basis – LIFO / FIFO, holding period– Special treatment

• Wash sale : 30 days period• Six month conversion rule

• Sales load basis deferral

43Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Tax – An example

• Mr Smart has a certain net short term gain of $50 over which he would like to reduce his income tax incidence; Remember that short term gain (or income) tax rates are typically higher than long term capital gains tax rate. Let us assume they are 40% and 20% respectively for this illustration. Thus potentially he has to pay tax of $20 on short term gain.

• His net pay-off is $50-20 = $30; (A)• Now assume a mutual fund quoting at $ 10 announces distribution of $1 dividend terming it

as long term capital gain – this will attract long term gain tax rate; normally after the distribution the value of the share will immediately drop by $1.

• Mr Smart buys and thereafter sells the fund before and after the distribution to incur a short term loss; he thus transacts 10 shares and he loses $10 (short term loss) and gains cash of $10 long term dividend.

• His net pay off would now be-– Short term net gain of $50 (as before) less $10 loss incurred on mutual fund txn = $40 on which he will pay $16 tax; net gain is $24

• Long term gain of $10 less tax @20% = $8 net gain• Thus his net pay off is $32 (B) !!

To prevent this the six month conversion rule exists; Under this

rule, the loss of $10 on mutual fund share sales to the extent of long term capital gain dividend (here $10 and therefore fully) will be considered to

be long term loss.

44Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund/SERV

NSCCFUND/SERV

•Fund houses, transfer agents

•e.g. Fidelity, DST

•Brokerage firms

•Clearing NSCC participant (e.g. Pershing)

Confirmation, acknowledgements, master information on activity, position, dividend etc.

•Fund orders

•Account opening

•Account maintenance

Net settlement Notifications for orders, disbursements

Confirmation, acknowledgements, master information on activity, position, dividend etc.

•Fund orders

•Account opening

•Account maintenance

Net settlement Notifications for orders, disbursements

Centralizes settlement – supports multiple settlement cycles and payment thru Fed Funds

Customized to fund requirements

45Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Fund Administration - Key modules

1. Account creation

3. Customer request /order management

9. Distribution of benefits,Corporate Actions

10.Regulatory, taxreporting

12. Reference data mtce(price, nav, forex rates,

fund info...)

5. Sales and customerservice support

6.Agents commission 2. Account maintenance

8.Payment Settlement Fund ClientAdiminstration

- Key Business Modules

4. Client transaction andposition

processing

11.Agents datamaintenance

7.Funds Order generationand Settlement

15. Tax Logic

17. Funds Parameters

13.System logic (date oftxn, special cases, batch

logic,interfaces..)

14. Fees Logic

16. Billing

18. New Products

Business Logic

46Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Note on Retirement Assets (Difference between IRA & 401K)

• Account for about 38% of mutual fund investments

• Main types:– Individual Retirement Account (IRA) :

• Individuals make tax deferred limited contributions to IRA accounts investing in securities including funds.

• IRA accounts are offered by fund houses/brokers and other savings institutions

– 401 (K) plan : It is a defined contribution plan (DC). • Similar to IRA but plan sponsored by the employer who also decides

the investment choice universe (in funds, shares etc). Investment providers are typically fund houses

• Employee makes contribution, directs the actual investment choice of his account and can switch /`transfer.

• Employer can make matching contribution

• DC plan requires specialized record keeping. Some times the record keeping is sold along with investment providing service.

47Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Hedge Funds

48Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Hedge Funds – An Overview (Very important)

• What?

– Private limited investment partnerships available to wealthy individuals and institutions (“sophisticated accredited investors”)

– Composed of General Partners (discretionary powers) & Limited Partners (invest capital - $200,000 to $500,000)

– Estimated to be a $400-$500 billion industry and growing at 20% per year, with 7,000 active hedge funds (approx).

• Why?

– Primarily reduce volatility and risk

– Seek above-average returns using aggressive, high-risk strategies unavailable to mutual funds and other traditional money managers

49Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

• Who invests?– Pension funds– Private Banks– High Net-Worth Individuals ($1mn or more)– Insurance Companies– Fund of Funds– Retail Brokerage Firms– Independent Financial Advisors– Insurance Policies– Endowments & Foundations

• Compensation structure– Management Fee - 1% of assets charged in 0.25% increments quarterly – Performance Fee - 20% of profits charged annually – High-Water Mark or Hurdle rates (say at 10%)– Lock up period of I year

Hedge Funds – An Overview - Contd…

50Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Hedge Funds

• Private investment vehicles • May use leverage extensively • May engage in short selling • May use derivatives • Large minimum investments • Restricted from advertising • Offered by private placement memo • Liquidity varies from monthly to

annually • Manager compensated on performance • Manager invests own capital

• Flexibility in investment strategies • Usually aim for absolute return

objective

Mutual Funds

• SEC Registered investment vehicles • Limited use of leverage • Maximum 30% of profits from short-sales • May not use derivatives • Small minimum investments • May freely advertise and promote • Offered by prospectus • Daily liquidity and redemption

• Manager paid a salary and bonus • Manager typically does not invest own capital

• Relatively inflexible • Aim to outperform known market benchmark

Hedge Funds Vs. Mutual Funds

51Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Strategy Description Sub-Strategies Holding Period

Expected Volatility

Directional Trading

• Based upon speculation of market direction in multiple asset classes.

• Both model-based systems and subjective judgment are used to make Trading decisions.

• Discretionary Trading

• Macro Trading• Systems Trading

Medium Very High

Relative Value • Focus on spread relationship between pricing components of financial assets.

• Market risk is kept to a minimum. Many managers use leverage to enhance returns.

• Convergence Arbitrage

• Merger Arbitrage• Risk Arbitrage• Statistical

Medium Moderate

Specialist Credit • Based on lending to credit sensitive issuers. • Funds in this strategy conduct a high level of due

diligence in order to identify relatively inexpensive securities.

• Distressed Securities• Positive Carry• Private Placements

Medium/Long Low - Moderate

Stock Selection • Combine long and short positions, primarily in equities, in order to exploit under or overvalued securities.

• Market exposure can vary substantially.

•Long Bias•No Bias•Short Bias•Variable Bias

Short/Medium Very High

Hedge Fund Investment Strategies

52Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Hedge Fund – Investment Process

Client Investment ObjectivesClient Investment Objectives

Top – Down Approach Bottom – Up Fund Selection

Economic & Market IndicatorsEconomic & Market Indicators

Tactical Asset Allocation

Tactical Asset Allocation

Strategic Asset Allocation

Strategic Asset Allocation

Style WeightingsStyle Weightings

Quantitative Due-DiligenceQuantitative

Due-DiligenceQualitative

Due-DiligenceQualitative

Due-Diligence

“Approved” Funds“Approved” Funds

Fund 1Fund 1 Fund 2Fund 2 Fund 3Fund 3 Etc.,Etc.,

Portfolio Construction

Risk ManagementRisk Management

53Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Typical Structure of a Hedge Fund Offering (Very important)

Fund Administrator

Fund Administrator

Hedge FundHedge Fund CustodianCustodian

Prime Broker / Dealer

Prime Broker / Dealer

Hedge Fund Manager

Hedge Fund Manager

Record & bookkeeping.Independently verify asset value of fund.

Holds the assets of the fund monitors &

controls flow of capital To meet margin calls

Executes the transactions ordered by the Hedge Fund

Manager

Sets and undertakes the investment strategies

of the fund

Registrar & Transfer AgentRegistrar &

Transfer AgentProcesses subscriptions

& Redemptions. Maintain register of shareholders.

Ownership/Shareholding

Contractual Relationship

General PartnerGeneral PartnerInvestor

(Limited Partners)Investor

(Limited Partners)

54Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Technology and Service providers to Hedge funds

55Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Major Accounting issues unique to Hedge Funds

56Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Role of the Prime Broker(Roles of Prime broker)

• Prime brokers provide many services, including technology, to the hedge fund industry.

57Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Role of Prime Brokerages

Value Addition• Facilitates the transacting process in situations where trading

partners would otherwise not transact with one another because of their different levels of creditworthiness and appetite for credit risk.

• Facilitates access to financial markets for less creditworthy market participants.

• Allows market participants to execute transactions in their own name or in the name of the prime broker, whilst the settlement of these transactions occurs in the name and under the responsibility of the prime broker.

• Enables Credit intermediation and anonymous trading

58Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Role of the Prime Broker in Hedge Fund trading

59Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Sources of Income for Prime Brokerages…

• Generally, Prime brokers do not charge a fee for the bundled package of services which they provide.

• Revenues are typically derived from three sources

– Spreads on financing (including stock loan)

– Trading commissions and fees for the settlement of transactions done away from the prime broker.

– Financing and lending spreads charged in basis points on the value of client loans (debit balances), client deposits (credit balances), client short sales (short balances), and synthetic financial products such as swaps and CFDs (Contracts for Difference), make up the vast majority of prime brokerage revenue.

60Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Client Reporting

Sample Client Reporting services offered by Prime Brokers

Positions & Values

•Real time Value, Book Value

•Real time Bid / Ask

•Average Price

•Exposure Weights

•MTM & P&L

•% change

•Yield & Risk measures

Information

•Industrial Indexes

•Deal Dates / Settlement Dates

•Deal Counterparties

•Corporate Actions

•Coupons and Dividends

•Fee break up

Holdings & Balances

•Daily / Historical

•Asset Breakdown

•Projections

•Account activity

•Borrow Lend Details

•Balance Forecast

•Collateral details

•Open Positions

•Unsettled Positions

Portfolio Analytics

•Daily / Historical

•Asset Breakdown

•Projections

•Account activity

•Borrow Lend Details

•Balance Forecast

•Collateral details

•Open Positions

•Unsettled Positions

Reports

•Position Reports

•P&L Reports

•Valuation Reports

•Risk Reports

•Transaction Reports

•Free Reports

•Rule Break Reports

•Commission & Tax Reports

Prime BrokerageCalculations, Reporting, Rule Engine, Processing & Valuation Engines, Notification tools

61Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Risk Challenge

Credit Risk Managing exposure to highly leveraged clients (hedge funds) Establishing appropriate credit terms (VaR vs Initial Margin) Real time monitoring of liquidity within the terms of the Give-Up Agreement Lack of standardized Give-Up Agreements

Liquidity Risk Prime Brokers share credit lines with the Firm’s Franchise Business

Operational Risk

Monitoring of post execution events (exercises, barriers..) Clients outsourcing operations Notification of the “give-up” trade is primarily manual (Reuters & e-mail) Identifying incoming trades as Franchise or Prime Brokerage related

Market Risk Managing basis risk introduced by a client putting on option and NDF positions and taking off these positions with different executing brokers (pass through / non pass through)

Resolving disputes between the client and executing broker

Reputational Risk

Creating a “Chinese wall” to segregate a Firm’s Franchise and Prime Brokerage business (client confidentiality)

Identifying off market trades

Risks & Challenges for the Prime Broker

62Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

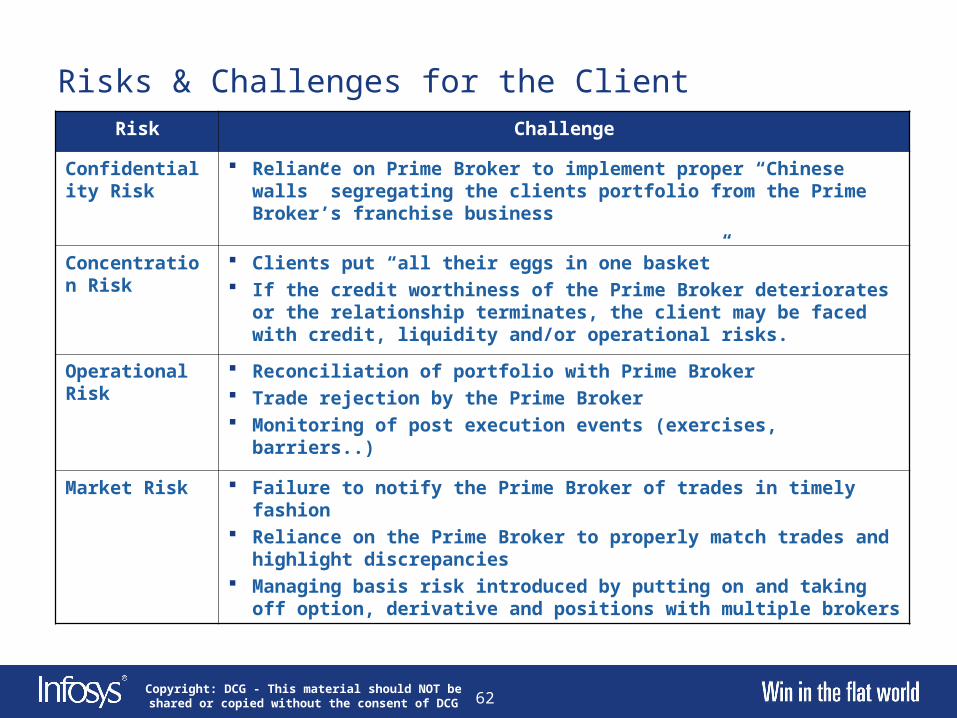

Risk Challenge

Confidentiality Risk

Reliance on Prime Broker to implement proper “Chinese walls” segregating the clients portfolio from the Prime Broker’s franchise business

Concentration Risk

Clients put “all their eggs in one basket” If the credit worthiness of the Prime Broker deteriorates or the

relationship terminates, the client may be faced with credit, liquidity and/or operational risks.

Operational Risk

Reconciliation of portfolio with Prime Broker Trade rejection by the Prime Broker Monitoring of post execution events (exercises, barriers..)

Market Risk Failure to notify the Prime Broker of trades in timely fashion Reliance on the Prime Broker to properly match trades and highlight

discrepancies Managing basis risk introduced by putting on and taking off option,

derivative and positions with multiple brokers

Risks & Challenges for the Client

63Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Primary Concerns About Investing in Hedge Funds

64Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Wealth Management

65Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Accumulate Seek financial security Save for major expense Obtain access to

liquidity solutions Save for retirement Send children/

grandchildren to college Maximize employee/

executive compensation Create a legacy for

children or other beneficiaries

Preserve Manage income taxes Revise portfolio to

reflect lifestyle changes Plan single stock risk

strategies Oversee retirement

plan distributions Preserve income and

assets in the event of death or disability

Manage cash flow Sell or preserve

business interests

Transfer Transfer wealth

during lifetime Manage estate taxes Distribute estate

to designated beneficiaries at appropriate time in appropriate manner

Give to charity

Three Components of Wealth Management (Important)

• There are three key components of wealth management — accumulation, preservation and transfer. Below are common needs and goals that may apply to clients over the course of a lifetime.

66Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

WM Customer segmentation (Important)

67Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

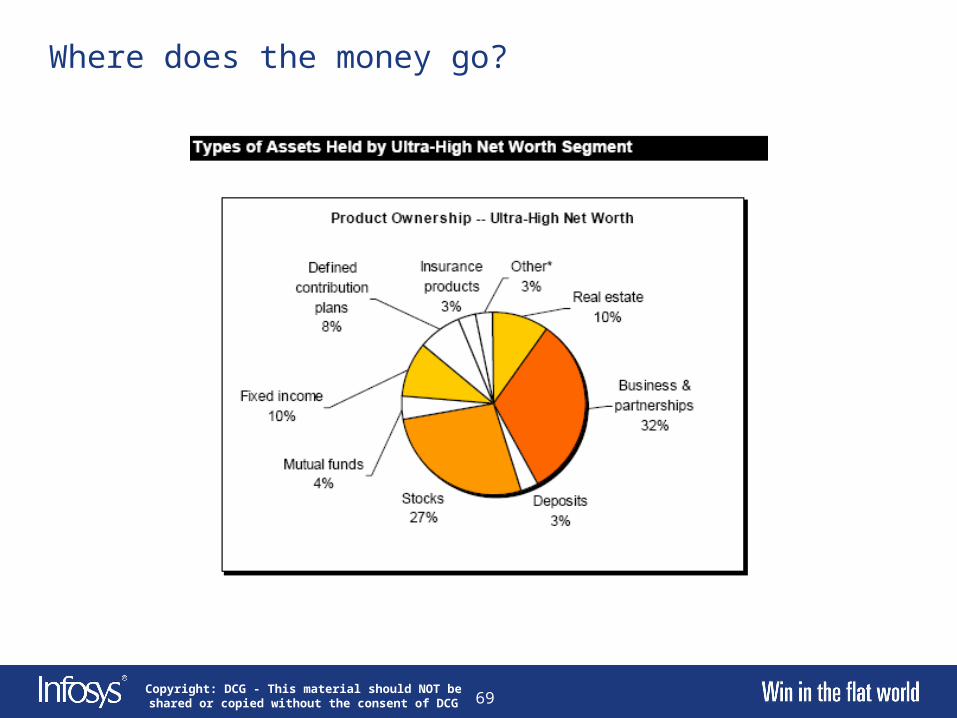

Where does the money go?

68Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Where does the money go?

69Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Where does the money go?

70Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

New products being considered by wealthy clients(Very Important)

71Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Financial Institution Segmentation

72Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

Priorities of Wealth Management Firms

• Acquire & retain high value clients• Increase assets and fee based revenues• Automate non productive tasks• Improve client communication including reporting• Monitor risk and provide exceptional returns• Differentiate from competitors

Copyright: DCG - This material should NOT be shared or copied without the consent of DCG

THANK YOU