copyright by harshit jayaswal 2017

TRANSCRIPT

i

Copyright

by

Harshit Jayaswal

2017

ii

The Thesis Committee for Harshit Jayaswal

Certifies that this is the approved version of the following thesis:

Macroscale Modeling Linking Energy and Debt: A Missing Linkage

APPROVED BY

SUPERVISING COMMITTEE:

Carey W. King

James K. Galbraith

Safa Motesharrei

Supervisor:

iii

Macroscale Modeling Linking Energy and Debt: A Missing Linkage

by

Harshit Jayaswal, B. Tech

Thesis

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment

of the Requirements

for the Degree of

Master of Science in Energy and Earth Resources

The University of Texas at Austin

May 2017

iv

Acknowledgements

I would like to acknowledge Carey W. King, James K. Galbraith, and Safa

Motesharrei for their continuous support and guidance. I would also like to acknowledge

Steve Keen from the Kingston University, London and Eric Kemp-Benedict from the

Stockholm Environment Institute for their highly informative thoughts throughout the

research. Last but not the least I would also like to acknowledge Richard Chuchla, Director

of the Energy and Earth Resources Program for his questions that enabled me to think out

of the box.

v

Abstract

Macroscale Modeling Linking Energy and Debt: A Missing Linkage

Harshit Jayaswal, M.S.E.E.R.

The University of Texas at Austin, 2017

Supervisor: Carey W. King

What if we realized that the fundamental economic framework of models that are meant to

guide a low-carbon energy transition prevents them from actually answering the question

they are supposed to answer? Instead of assuming a series of energy investments, and then

estimating the economic impacts of those choices, they actually do the exact opposite. They

assume economic growth and then make a series of investments to meet emissions targets

without actually factoring in how the energy systems themselves feedback to economic

growth. The research here would be to try to understand how energy and resource

extraction are linked with long-term economic outcomes, specifically addressing the idea

of accumulation of debt in the economy. Many economic models implicitly assume that

energy resources are not constraints on the economy. These energy-related constraints have

to be introduced if we are to effectively understand long-term debt and natural resource

interactions. Same is also true with various biophysical models which do not consider

economic parameters like debt, employment and wages etc. while modeling population

growth and resources in the system.

The research objective is to develop a consistently merged model combining both

a biophysical and an economic model to describe the industrial transition to the

contemporary macroeconomic state. The research approach would be to integrate macro-

vi

scale system dynamics models of money, debt, and employment (specifically the Goodwin

and Minsky models of (Keen, 1995 & Keen, 2013)) with system dynamics models of

biophysical quantities (specifically population and natural resources such as in (Meadows

et al., 1972, Meadows et al., 1974, Motesharrei et al., 2014)). The proposed research

concept is critical to link biophysical modeling concepts with those economic models that

specifically include the link of debt to employment and economic growth.

This type of modeling is anticipated to help answer important questions for a low-

carbon transition, for example, how does the rate of investment in “energy” feedback to

growth of population, economic output, and debt; and how does the capital structure (e.g.

fixed costs vs. variable costs) of fossil and renewable energy systems relate to, and affect,

economic outcomes.

vii

TABLE OF CONTENTS

TABLE OF CONTENTS ...................................................................................... vii

LIST OF TABLES ................................................................................................ xii

LIST OF FIGURES ............................................................................................. xiii

1. CHAPTER 1: INTRODUCTION 1

1.1. Research Question .................................................................................1

1.2. Problem Statement .................................................................................1

1.3. Research Objective ................................................................................1

2. CHAPTER 2: PREVIOUS RESEARCH 3

2.1. Literature Review...................................................................................3

2.1.1. Origin of Humans, .........................................................................3

2.1.2. Rise and Fall of Civilizations, .......................................................7

2.1.3. Is Earth Finite or Infinite? .............................................................9

2.1.3.1. The Limits to Growth..................................................................11

2.1.4. Economic Models and Different Types of Production Functions15

2.1.4.1. Solow-Swan Model of Economic Growth ..................................16

2.1.4.2. Cobb-Douglas Model of Production ...........................................20

2.1.4.3. Leontief Production Function .....................................................21

2.2. Gaps in Literature ................................................................................22

viii

3. CHAPTER 3: RESEARCH APPROACH 25

3.1. Research Approach ..............................................................................25

Research Approach .......................................................................................30

3.2. Background and Context......................................................................31

3.2.1. Lotka-Volterra-Predator-Prey Model ..........................................31

3.2.2. Multiplier-Accelerator Model .....................................................32

3.2.3. The Goodwin Model, ..................................................................36

3.2.3.1. Mathematics of Goodwin Model ................................................38

3.2.4. Human and Nature Dynamics (“HANDY”): Modeling inequality and

use of resources in the collapse or sustainability of societies ..............43

3.2.4.1. The Model ...................................................................................43

3.2.4.2. Different scenarios in the model .................................................46

3.2.4.3. Summary .....................................................................................49

3.2.5. A Monetary Minsky Model of The Great Moderation and The Great

Recession .............................................................................................50

4. CHAPTER 4: RESEARCH DESIGN 57

4.1. Scope of Research ................................................................................57

4.2. Overview of Methodology ...................................................................61

4.3. Research Goal ......................................................................................62

5. CHAPTER 5: RESULTS AND FINDINGS 63

5.1. Nature extraction as a function of Labor .............................................63

5.1.1. Nature extraction as a function of Labor not including debt and a

linear form for the Phillips curve .........................................................63

ix

5.1.2. Nature extraction as a function of Labor including debt, linear

Phillips curve, and a nonlinear investment curve ................................66

5.1.3. Nature extraction as a function of Labor without debt, nonlinear

Phillips curve, and a nonlinear investment curve ................................68

5.1.4. Nature extraction as a function of Labor including debt nonlinear

Phillips curve, and a nonlinear Investment curve ................................70

5.2. Nature extraction as a function of Capital ...........................................72

5.2.1. Nature extraction as a function of Capital without debt and a linear

form of the Phillips curve ....................................................................72

5.2.2. Nature extraction as a function of Capital including debt and a linear

form of the Phillips curve ....................................................................75

5.2.3. Nature extraction as a function of Capital without debt and a

nonlinear form of the Phillips curve ....................................................77

5.2.4. Nature extraction as a function of Capital including Debt, nonlinear

form of the Phillips curve, and a nonlinear form of the investment curve

.....................................................................................................79

5.3. Nature extraction as a function of Power Input ...................................82

5.3.1. Nature as a function of Power Input with a nonlinear form of the

Phillips curve without debt ..................................................................82

5.3.2. Nature as a function of Power Input in the model with a nonlinear

form of the Phillips curve including debt ............................................85

5.3.3. Varying power factor from 1% of wealth to 20% of wealth being

used as power input towards extracting nature ....................................87

5.4. Including Depreciation of Wealth ........................................................88

5.4.1. Comparing Results with and without depreciation of Wealth when

nature extraction is a function of Labor. ..............................................90

5.4.2. Comparing Results with and without Depreciation of Wealth when

Nature Extraction is a Function of Capital ..........................................91

5.4.3. Comparing Results with and without Depreciation of Wealth when

Nature Extraction is a Function of Power Input ..................................92

x

6. CHAPTER 6: DISCUSSIONS 93

6.1. Overview ..............................................................................................93

6.1.1. Effect of debt at high constant rate of interests when nature

extraction is a function of labor ...........................................................93

6.1.2. Effect of Debt at high constant rate of interests when nature

extraction is a function of Capital ........................................................95

6.1.3. Effect of Debt at high constant rate of interests when nature

extraction is a function of Power Input ................................................97

6.2. Conclusions ..........................................................................................99

6.3. Limitations .........................................................................................101

6.4. Future work ........................................................................................101

7. APPENDIX A-FIGURES & TABLES 103

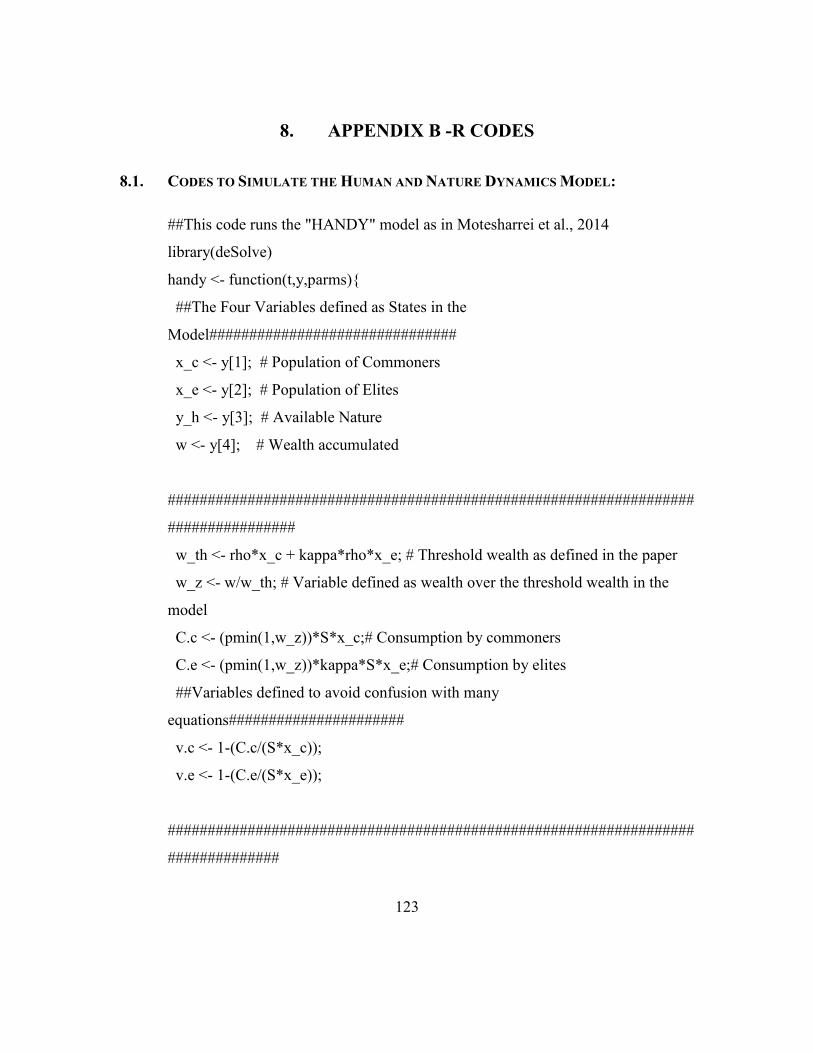

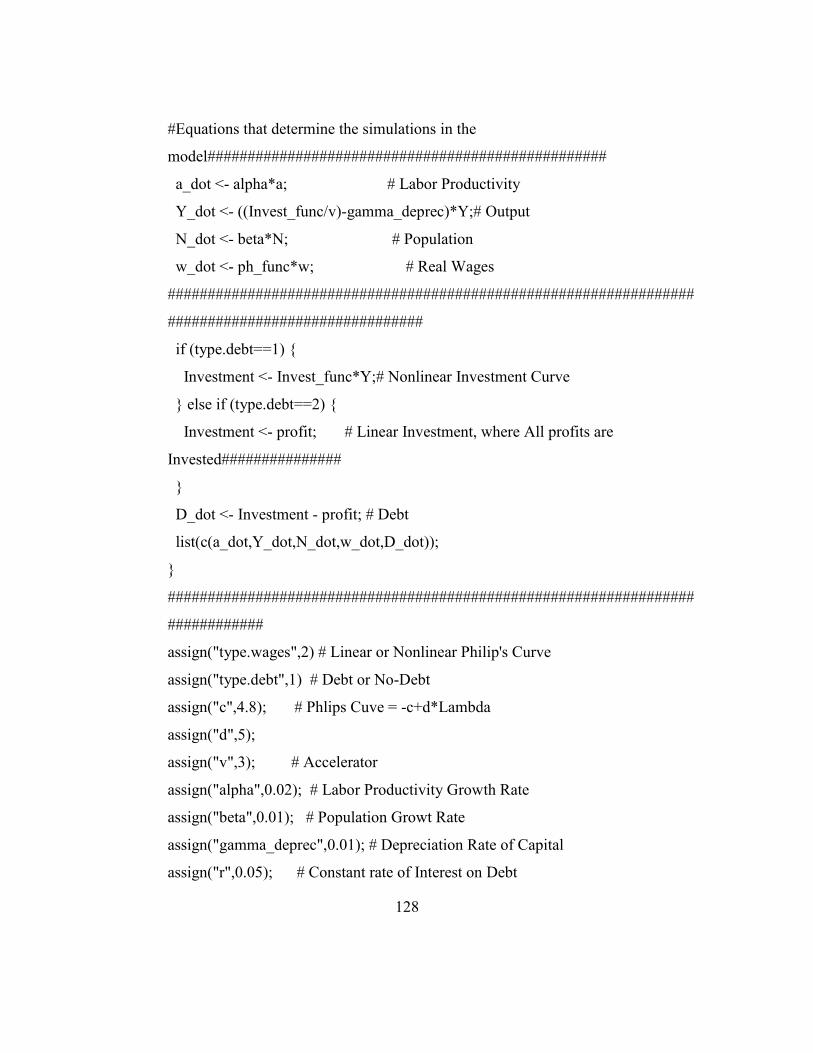

8. APPENDIX B -R CODES 123

8.1. Codes to Simulate the Human and Nature Dynamics Model: ...........123

8.2. Codes to Simulate the Goodwin Model with Debt and wages being

modeled either according to the linear or the nonlinear form of the Phillips

curve:..................................................................................................126

8.3. Codes to Simulate the Merged Model (“HANDY” + “The Goodwin

Model”) with and without Debt, wages being modeled either according to

the linear or the nonlinear form of the Phillips curve, and a nonlinear

investment curve: ...............................................................................131

8.3.1. Codes to read .CSV output files from the previous code in section

8.3 ...................................................................................................161

8.3.2. Plotting codes for the merged CSV’s from section 8.3.1 .........162

xi

9. REFERENCE 164

xii

LIST OF TABLES

Table 1. Equations for the merged model ......................................................................... 59

Table 2. Different parameters and variables with their values used to simulate the

Goodwin model with or without debt, including either a linear or a nonlinear form for the

Phillips and the investment curve as in Keen, 2013. ...................................................... 119

Table 3. Different parameters and variables with their values used to simulate the

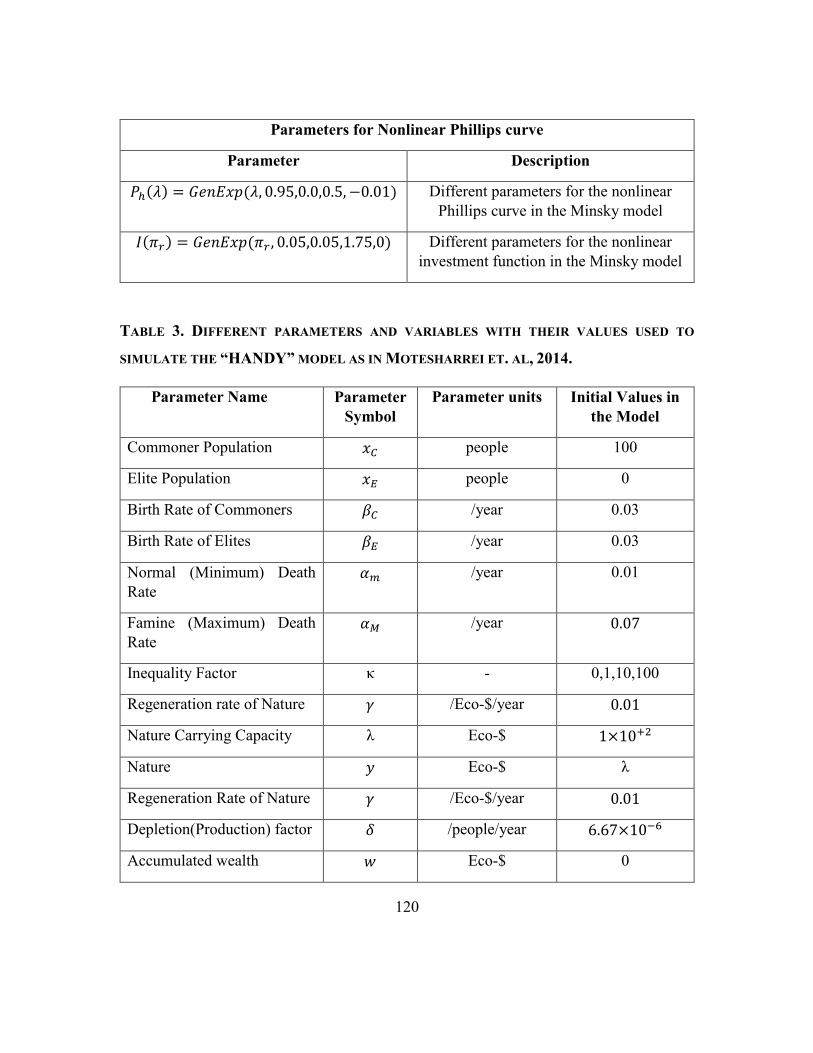

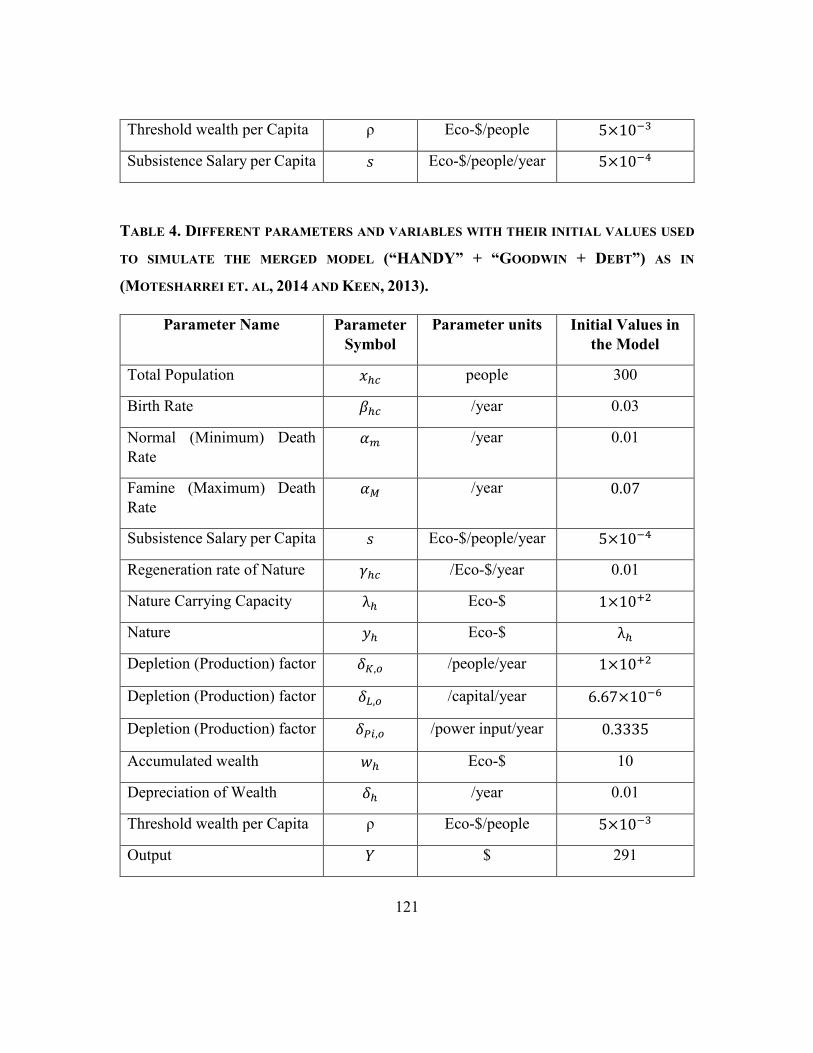

“HANDY” model as in Motesharrei et. al, 2014. ........................................................... 120

Table 4. Different parameters and variables with their initial values used to simulate the

merged model (“HANDY” + “Goodwin + Debt”) as in (Motesharrei et. al, 2014 and

Keen, 2013). .................................................................................................................... 121

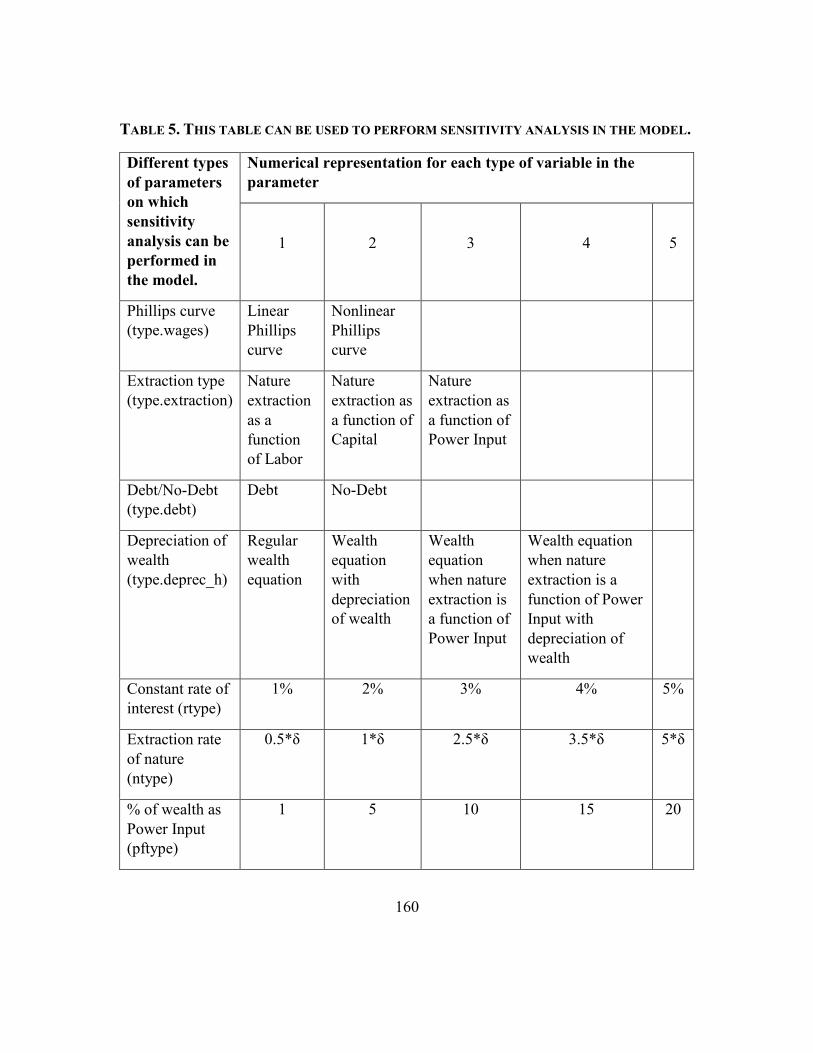

Table 5. This table can be used to perform sensitivity analysis in the model................. 160

xiii

LIST OF FIGURES

Figure 1. The northern route was taken by archaic Homo sapiens from East Africa via the

Sinai into Israel 120,000 years ago and it also shows the Southern Route taken by Homo

sapiens from East Africa via the Bab-al-Mandab strait into Yemen 70,000 years ago. ..... 4

Figure 2. The above figure shows the results from using the World3 model in the 1972

Limits to Growth book along with future predictions on the planet showing it matching a

trend. ................................................................................................................................. 13

Figure 3. World population 1750-2015 and projections until 2100.................................. 14

Figure 4. The research approach will focus to make a critical link between biophysical

modeling concepts and those of economic models that specifically include the link of

debt-based finance to employment and economic growth. ............................................... 30

Figure 5. A typical solution of the predator-prey system (Motesharrei, Rivas and Kalnay

2014, 3) obtained by running the system with a certain set of initial conditions for the

number of wolves and rabbits at the start of the simulation. ............................................ 32

Figure 6. Goodwin model with the Linear form for the Phillips curve (-c + d λ) where c =

4.8 and d =5 are constants and λ is the employment rate with an initial value of 0.97. The

initial value for the real wage rate 𝑤 is equal to 0.88 and that for the labor productivity 𝑎

is equal to 1. ...................................................................................................................... 42

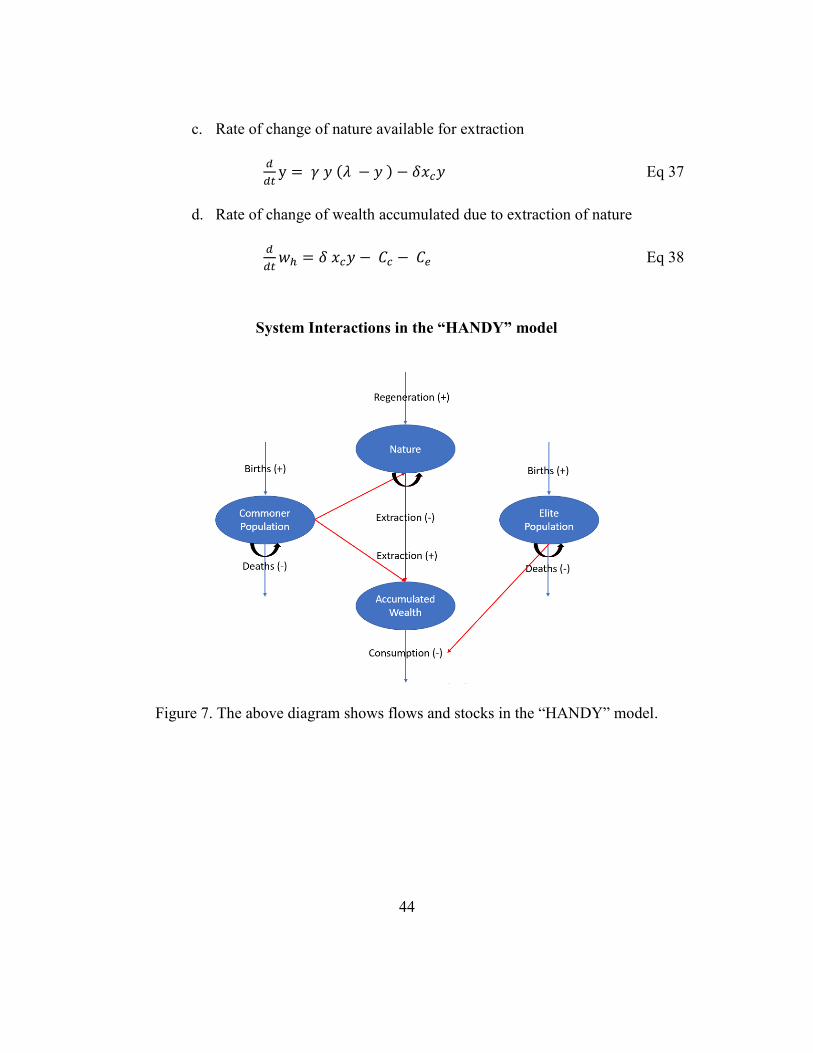

Figure 7. The above diagram shows flows and stocks in the “HANDY” model.............. 44

Figure 8. Consumption rates in HANDY. ........................................................................ 46

Figure 9. Death rates in HANDY. .................................................................................... 46

Figure 10. A soft landing to the optimal equilibrium is observed in the figure where the

elite population in red is equal to zero and the final population reaches the maximum

xiv

carrying capacity at a low value of the rate of depletion of nature δ = 6.67×10 − 6

Adapted from Motesharrei et al., 2014. ............................................................................ 48

Figure 11. An irreversible collapse is observed in the figure where again the elite

population in red is equal to zero in an egalitarian society. All the state variables collapse

to zero in this scenario due to over depletion of nature at a higher value of the rate of

depletion of nature δ = 36.685×10 − 6. Adapted from Motesharrei et al., 2014. .......... 48

Figure 12. An equilibrium between both Workers(Commoners) and Non-Workers(Elites)

can be attained with a low value of the rate of depletion of nature δ = 8.33×10 − 6.

Adapted from Motesharrei et al., 2014, 97. ...................................................................... 48

Figure 13. Whereas an Irreversible collapse in the society is observed at a higher value of

the rate of depletion of nature δ = 4.33×10 − 5.due to over depletion of nature. Adapted

from Motesharrei et al., 2014, 97. ..................................................................................... 48

Figure 14. With a moderate inequality c, the states in the model reach an optimal

equilibrium at a relatively lower depletion rate of nature δ = 6.35×10 − 6 and 𝑥𝑒 =3×10 + 3 Adapted from Motesharrei et al., 2014, 98. ..................................................... 49

Figure 15. Population Collapse following an apparent equilibrium due to a small initial

Elite population when κ =100 at a nature depletion value of δ = 6.67×10 − 6 and 𝑥𝑒 =1×10 − 3 Adapted from Motesharrei et al., 2014, 98. ..................................................... 49

Figure 16. The above diagram shows the different interactions of different parameters in

the model. .......................................................................................................................... 52

Figure 17. The level of Investment in GDP as a function of the rate of profit. ................ 54

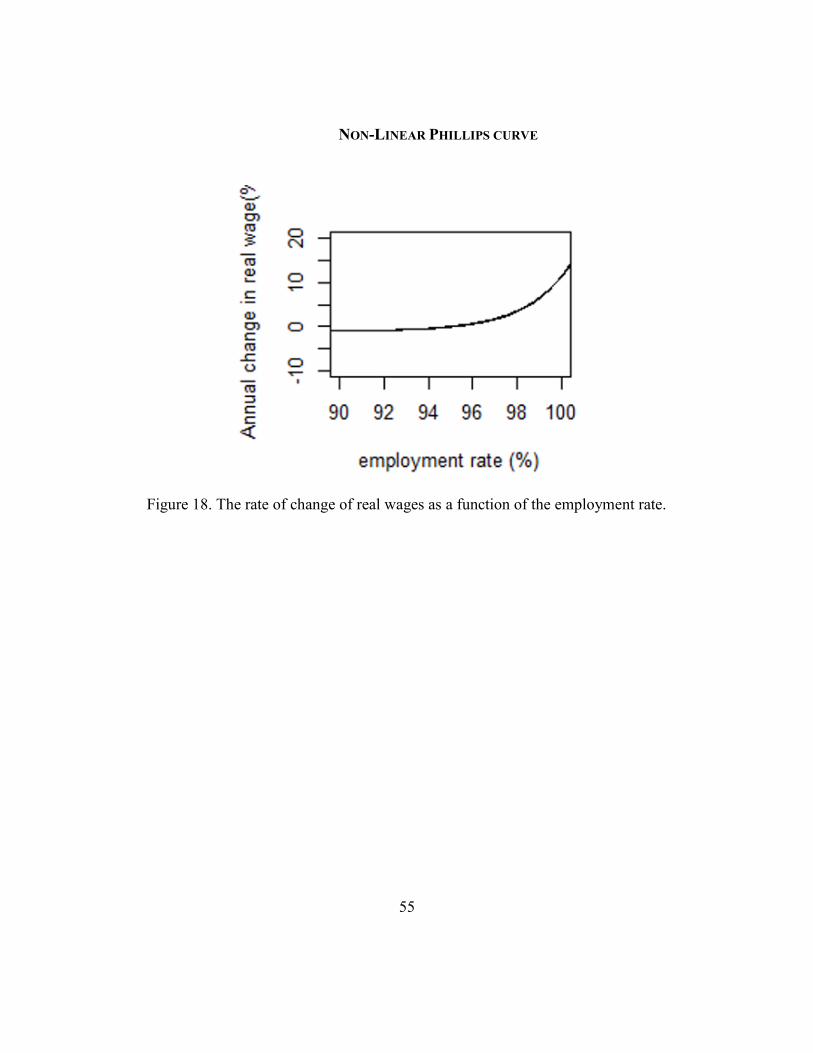

Figure 18. The rate of change of real wages as a function of the employment rate. ........ 55

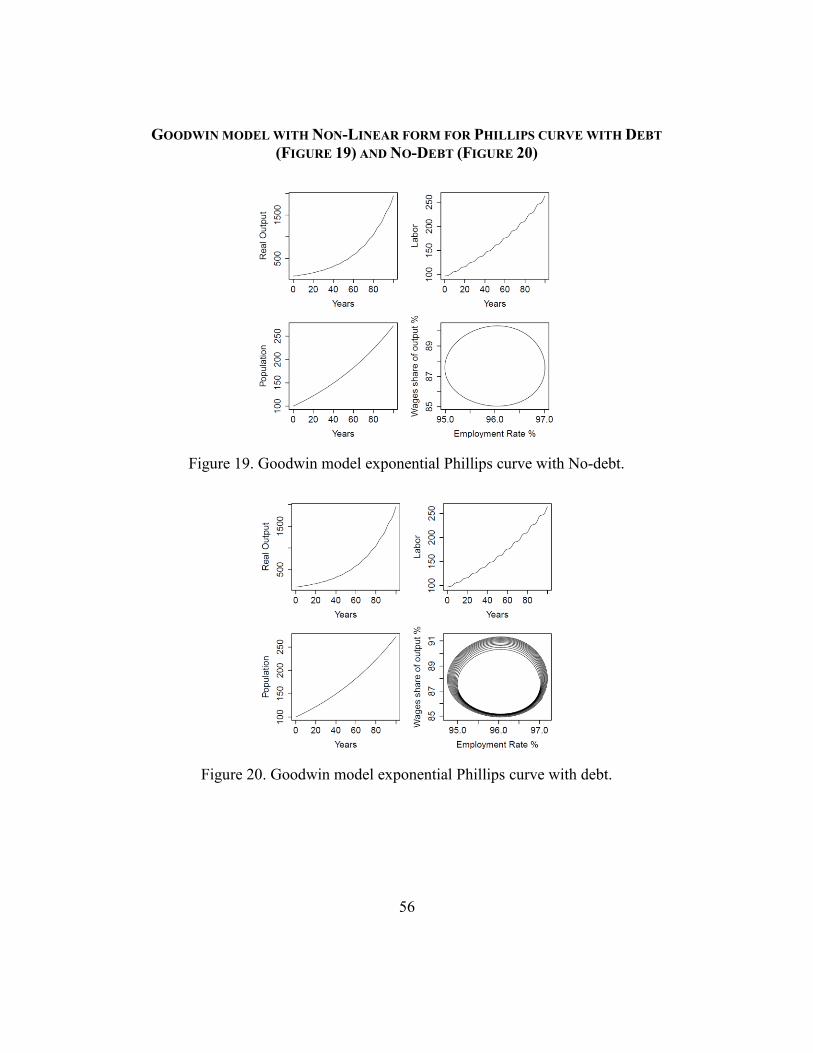

Figure 19. Goodwin model exponential Phillips curve with No-debt. ............................. 56

Figure 20. Goodwin model exponential Phillips curve with debt. ................................... 56

xv

Figure 21. The above diagram explains the how the 2 models have been integrated to

understand the dynamics of the merged model. ................................................................ 60

Figure 22. Different parameters from both the models which will be tweaked in the

merged model to understand how sensitive the model is to these parameters.................. 62

Figure 23. Simulation result when extraction rate of nature is only a function of Labor,

and a baseline rate of extraction 𝛿𝐿, 𝑜 = 6.67×10 − 6𝑝𝑒𝑟𝑠𝑜𝑛 − 1𝑡𝑖𝑚𝑒 − 1. Wages

being modeled according to a linear form of the Phillips curve without including debt. . 65

Figure 24. Simulation results for when extraction rate of nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 with debt being accumulated at a

constat rate of interest 𝑟 = 5% and a Linear form for the Phillips curve. ........................ 67

Figure 25. Simulation results for when extraction rate of nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 without debt and a nonlinear form

for the Phillips curve. ........................................................................................................ 69

Figure 26. Simulation results for when extraction rate of nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 .Where debt is being accumulated at

a constat rate of interest of 𝑟 5% and and wages modeled according to a noninear form of

the Phillips curve............................................................................................................... 71

Figure 27. Simulation results for when extraction rate of nature is a function of capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 including no debt and modeling

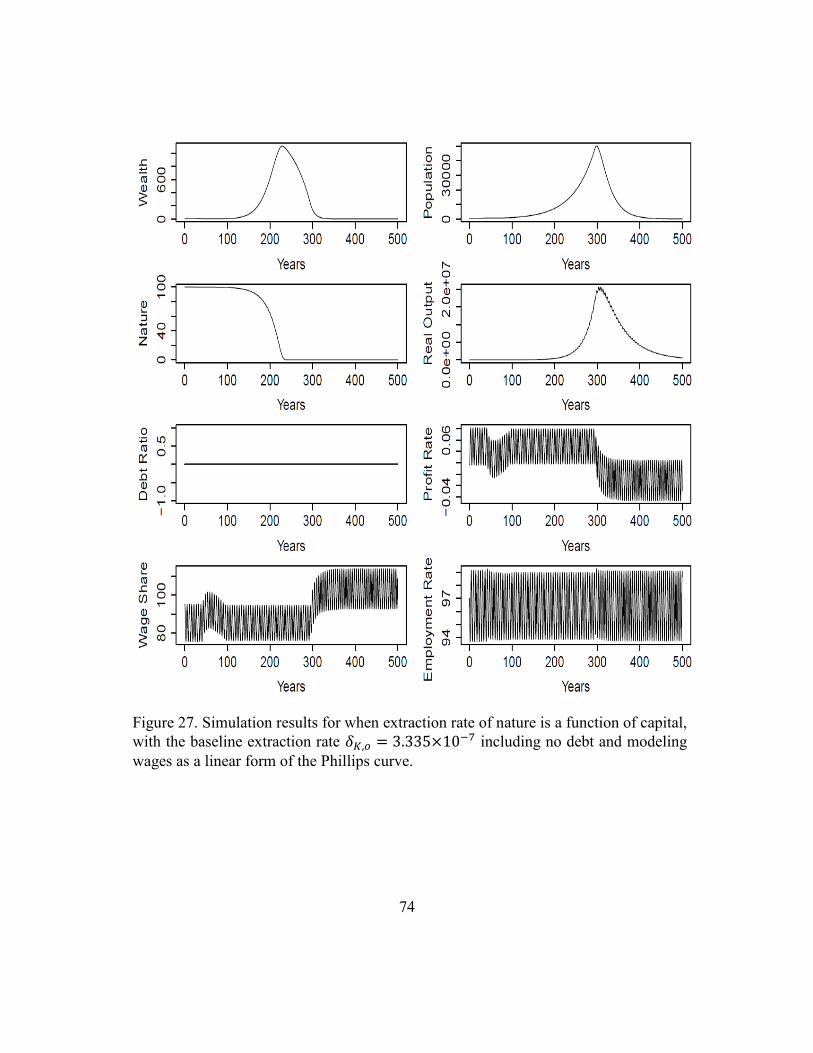

wages as a linear form of the Phillips curve. .................................................................... 74

Figure 28. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 with debt accumulating at a

constant rate of interest 𝑟 = 5% and wages being modeled according to the linear form of

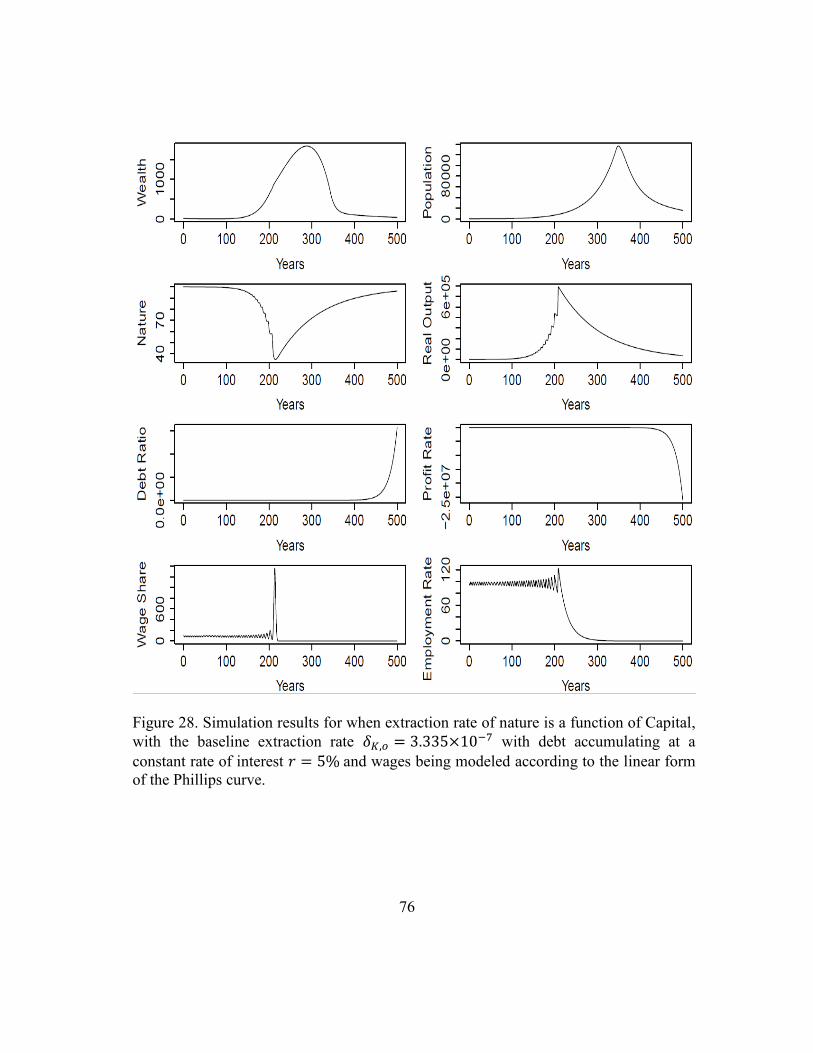

the Phillips curve............................................................................................................... 76

Figure 29. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 with no debt accumulating and

the nonlinear form of the Phillips curve. .......................................................................... 78

xvi

Figure 30. Simulation results for when extraction rate of nature is a function of Capital,

with a baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 with debt accumulating at a

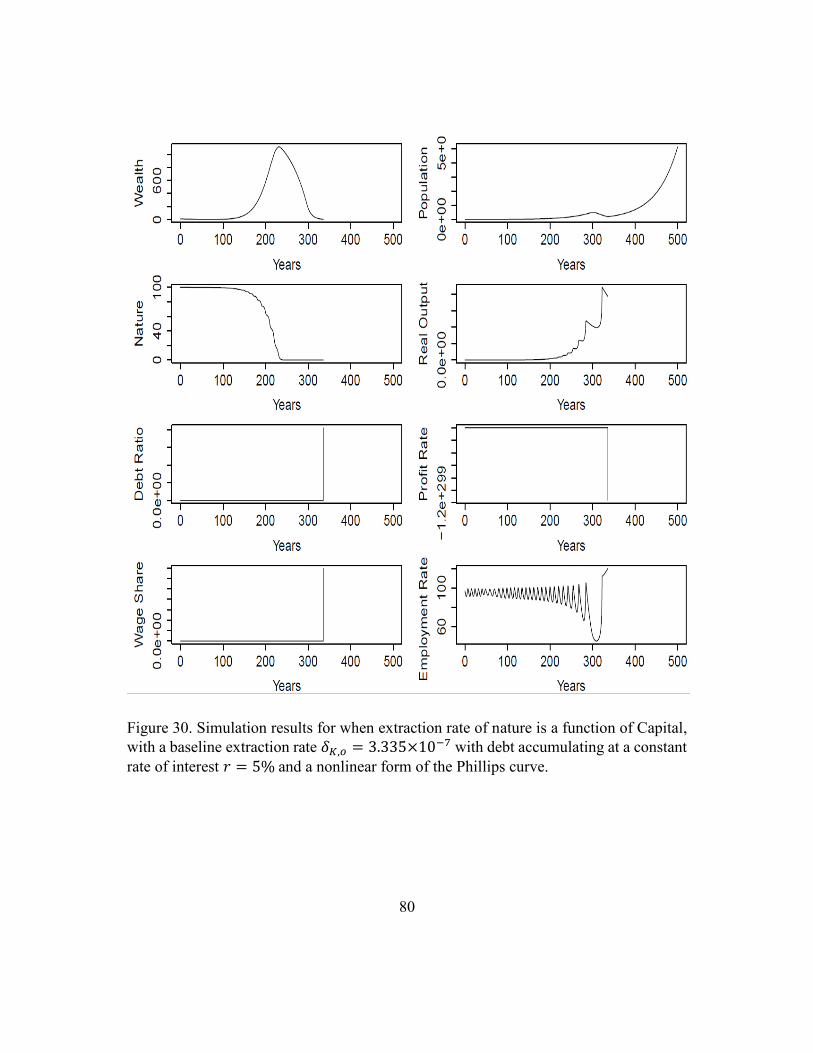

constant rate of interest 𝑟 = 5% and a nonlinear form of the Phillips curve. .................. 80

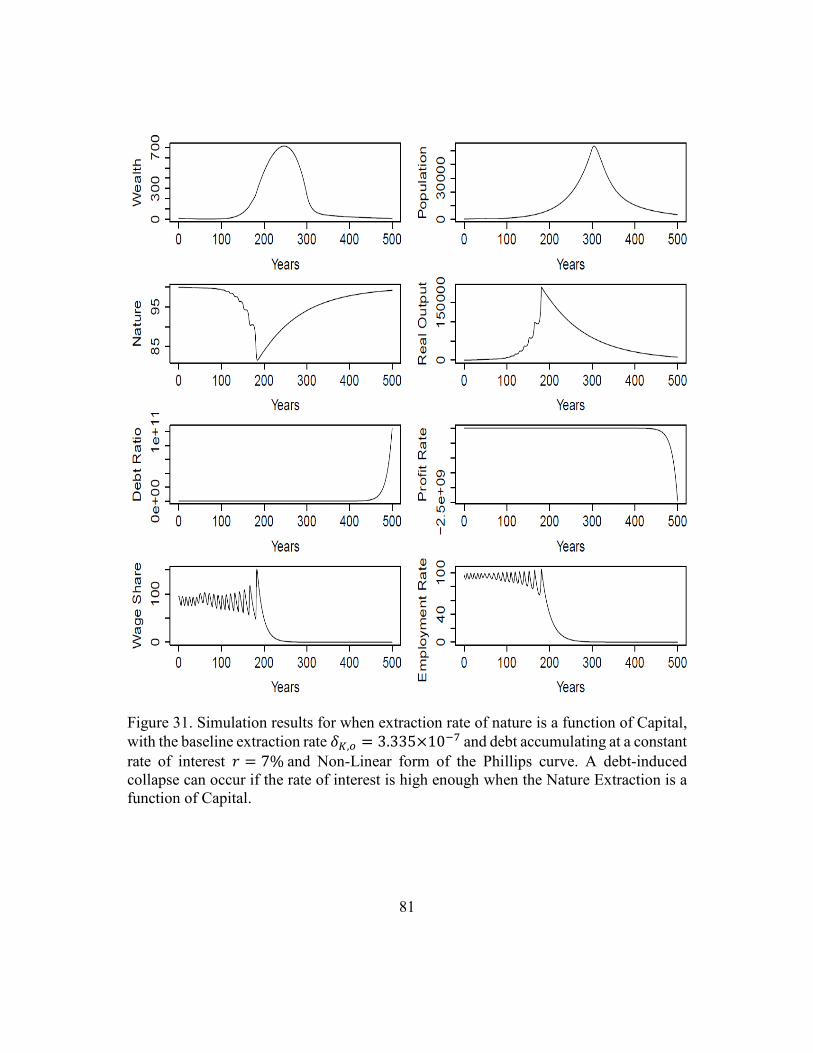

Figure 31. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 and debt accumulating at a

constant rate of interest 𝑟 = 7% and Non-Linear form of the Phillips curve. A debt-

induced collapse can occur if the rate of interest is high enough when the Nature

Extraction is a function of Capital. ................................................................................... 81

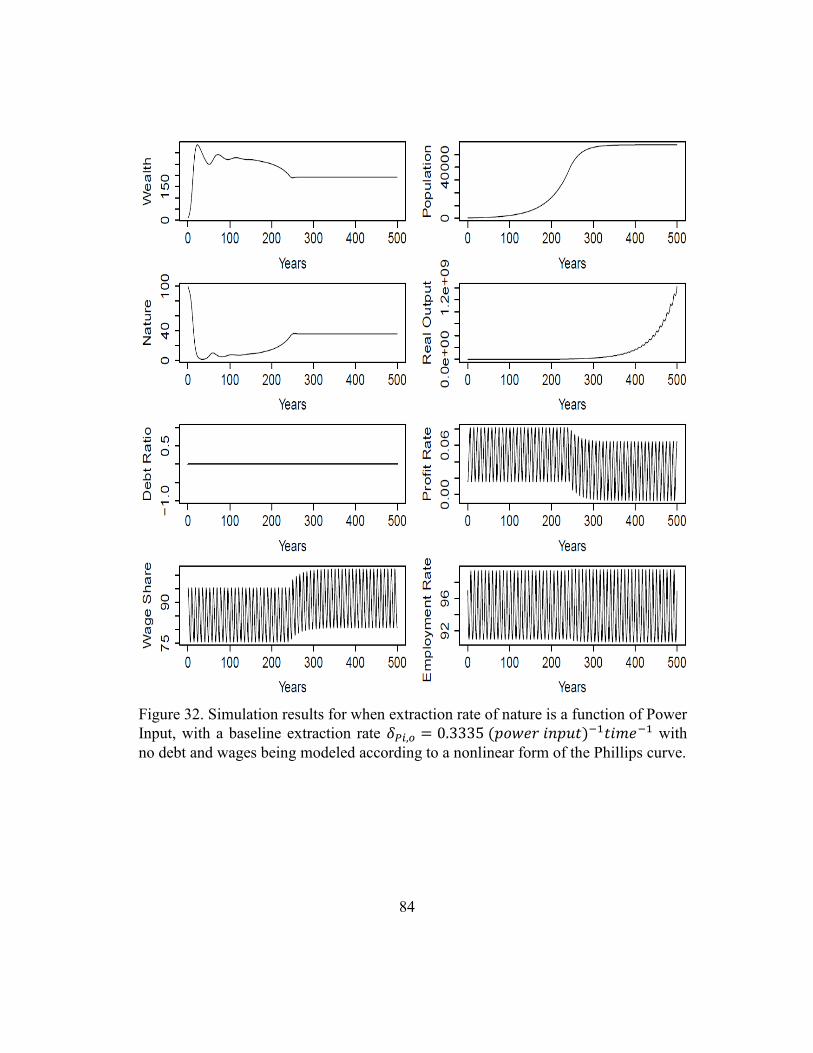

Figure 32. Simulation results for when extraction rate of nature is a function of Power

Input, with a baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1 with

no debt and wages being modeled according to a nonlinear form of the Phillips curve. . 84

Figure 33. Simulation results for when extraction rate of nature is a function of Power

Input, with the baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1

with debt accumulating at r=5% and wages modeled according to the nonlinear form of

the Phillips curve............................................................................................................... 86

Figure 34. Simulating results by altering the power factor pf from 1% to 20% of wealth

for when nature extraction is a function of Power Input, with the baseline extraction rate

𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1 including debt and wages modeled as a

nonlinear form of the Phillips curve. ................................................................................ 88

Figure 35. Simulating results for when nature is a function of labor with and without

depreciation of wealth in the model. Here a nonlinear form of the Phillips curve is

considered to model wages with a nonlinear form for investment including debt. The

baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6𝑝𝑒𝑟𝑠𝑜𝑛 − 1𝑡𝑖𝑚𝑒 − 1 is same as in section

5.1...................................................................................................................................... 90

Figure 36. Simulating results for when nature is a function of capital with and without

depreciation of wealth in the model. Here a nonlinear form of the Phillips curve is

considered to model wages with a nonlinear form for investment including debt. The

baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7𝑐𝑎𝑝𝑖𝑡𝑎𝑙 − 1𝑡𝑖𝑚𝑒 − 1 is same as in

section 5.2. ........................................................................................................................ 91

xvii

Figure 37. Simulating results for when nature is a function of power input with and

without depreciation of wealth in the model. Here a nonlinear form of the Phillips curve

is considered to model wages with a nonlinear form for investment including debt. The

baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1 is same as in

section 5.3. ........................................................................................................................ 92

Figure 38. Simulating nature as a function of labor including debt for interest rates 5% to

15% and no debt at a rate of extraction of nature 𝛿𝐿, 𝑜 = 6.67×10 − 6𝑝𝑒𝑟𝑠𝑜𝑛 −1𝑡𝑖𝑚𝑒 − 1. Higher interest rates lead to an earlier collapse of nature while reaching a

steady state without debt. ................................................................................................ 94

Figure 39.Simulating nature as a function of labor including debt for interest rates 5% to

15% and no debt at a rate of extraction of nature 𝛿𝐿, 𝑜 = 6.67×10 − 6𝑝𝑒𝑟𝑠𝑜𝑛 −1𝑡𝑖𝑚𝑒 − 1. Higher interest rates lead to an earlier collapse of population while reaching a

steady state without debt. .................................................................................................. 95

Figure 40. Simulating nature as a function of capital including debt for interest rates 5%

to 15% and no debt at a rate of extraction of nature 𝛿𝐾, 𝑜 = 3.335×10 − 7𝑐𝑎𝑝𝑖𝑡𝑎𝑙 −1𝑡𝑖𝑚𝑒 − 1. Higher interest rates lead to an earlier collapse of nature whereas the nature is

fully extracted at low interest rates and no debt. .............................................................. 96

Figure 41. Simulating nature as a function of capital including debt for interest rates 5%

to 15% and no debt at a rate of extraction of nature 𝛿𝐾, 𝑜 = 3.335×10 − 7𝑐𝑎𝑝𝑖𝑡𝑎𝑙 −1𝑡𝑖𝑚𝑒 − 1. Higher interest rates lead to an earlier collapse of population. ..................... 97

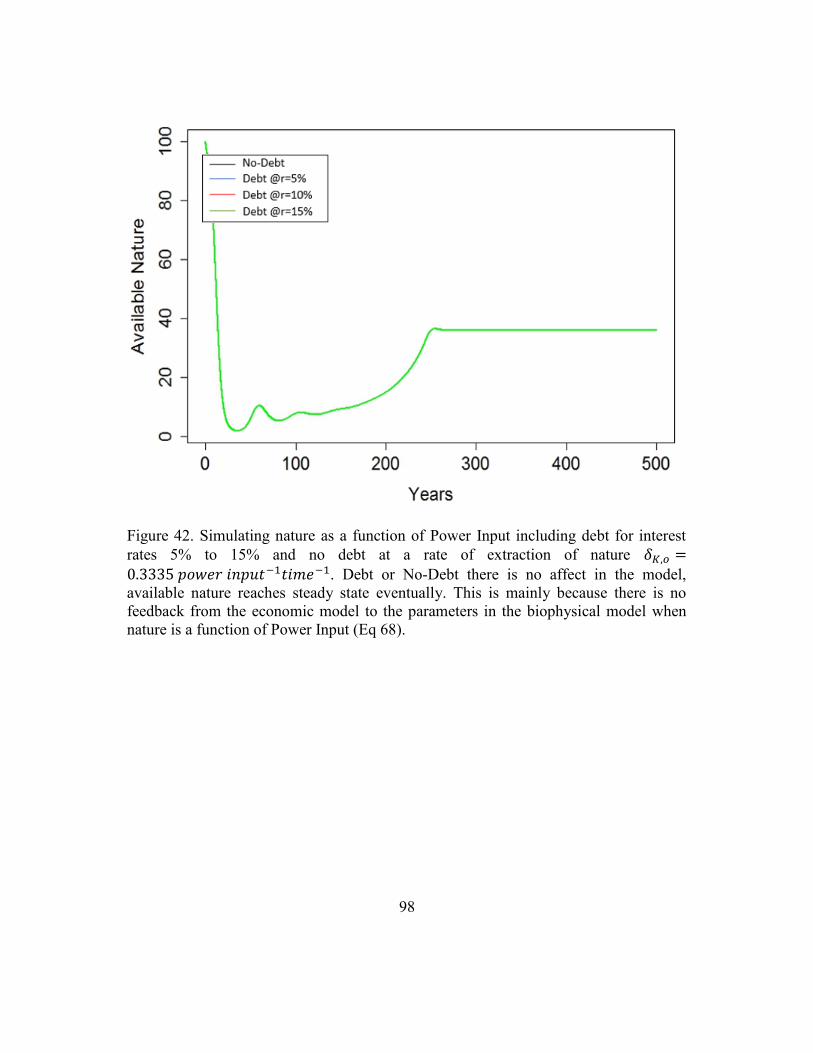

Figure 42. Simulating nature as a function of Power Input including debt for interest rates

5% to 15% and no debt at a rate of extraction of nature 𝛿𝐾, 𝑜 = 0.3335 𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡 −1𝑡𝑖𝑚𝑒 − 1. Debt or No-Debt there is no affect in the model, available nature reaches

steady state eventually. This is mainly because there is no feedback from the economic

model to the parameters in the biophysical model when nature is a function of Power

Input (Eq 68). .................................................................................................................... 98

Figure 43. Simulating nature as a function of Power Input including debt for interest rates

5% to 15% and no debt at a rate of extraction of nature 𝛿𝐾, 𝑜 = 0.3335 𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡 −1𝑡𝑖𝑚𝑒 − 1. Debt or No-Debt there is no affect in the model, the population reaches a

steady state eventually. This is mainly because there is no feedback from the economic

xviii

model to the parameters in the biophysical model when nature is a function of Power

Input (Eq 68). .................................................................................................................... 99

Figure 44. Simulation results for when extraction rate of Nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 being varied from 0.5𝛿𝐿, 𝑜 𝑡𝑜 5𝛿𝐿, 𝑜

without debt and wages being modeled according to a Linear form of the Phillips curve.

......................................................................................................................................... 103

Figure 45. Simulation results for 1000 years when extraction rate of nature is a function

of Labor, with the baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6𝑝𝑒𝑟𝑠𝑜𝑛 − 1𝑡𝑖𝑚𝑒 − 1 a

linear Phillips curve, and debt accumulating at a constant interest rate of 1%/yr. ......... 104

Figure 46. Simulation results for when extraction rate of Nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 being varied from 0.5𝛿𝐿, 𝑜 𝑡𝑜 5𝛿𝐿, 𝑜

with debt accumulating at a constat rate of interest of 𝑟 = 5% and wages being modeled

according to a linear form of the Phillips curve. ............................................................. 105

Figure 47. Simulation results for when extraction rate of nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6. While a constant rate of interest 𝑟

on Debt is being varied from 1% 𝑡𝑜 5% with wages modeled according to the Linear

form of Phillips curve. .................................................................................................... 106

Figure 48. Simulation results for when extraction rate of nature is a function of Labor,

with the baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 being varied from

0.5𝛿𝐿, 𝑜 𝑡𝑜 5𝛿𝐿, 𝑜 and wages being modeled according to a noninear form of the Phillips

curve. ............................................................................................................................... 107

Figure 49. Simulation results for when extraction rate of nature is a function of Labor,

with a baseline extraction rate 𝛿𝐿, 𝑜 = 6.67×10 − 6 being varied from 0.5𝛿𝐿, 𝑜 𝑡𝑜 5𝛿𝐿, 𝑜

with debt accumulating at a constat interest rate, 𝑟 = 5% and wages modeled according

to a nonlinear form of the Phillips curve. ....................................................................... 108

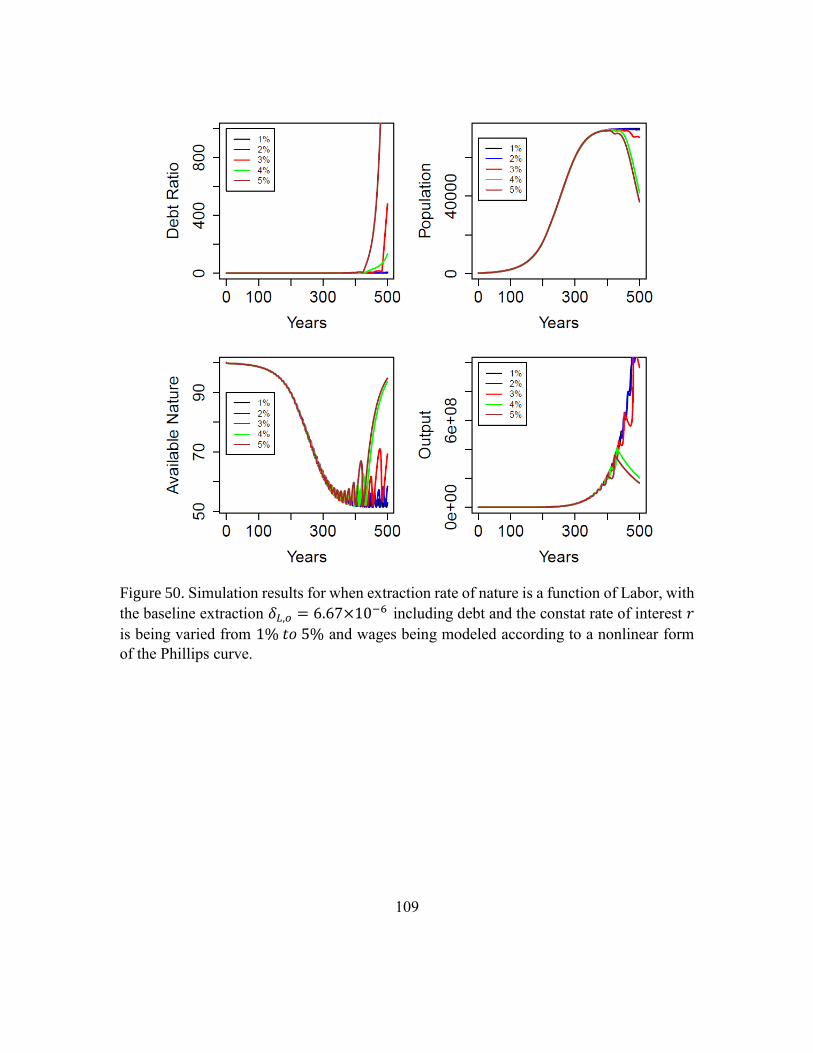

Figure 50. Simulation results for when extraction rate of nature is a function of Labor,

with the baseline extraction 𝛿𝐿, 𝑜 = 6.67×10 − 6 including debt and the constat rate of

interest 𝑟 is being varied from 1% 𝑡𝑜 5% and wages being modeled according to a

nonlinear form of the Phillips curve. .............................................................................. 109

xix

Figure 51. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 being varied from

0.5𝛿𝐾, 𝑜 𝑡𝑜 5𝛿𝐾, 𝑜 without debt and using a linear form of the Phillips curve to model

wages............................................................................................................................... 110

Figure 52. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 being varied from

0.5𝛿𝐾, 𝑜 𝑡𝑜 5𝛿𝐾, 𝑜 including debt and a linear form of the Phillips curve to model wages.

......................................................................................................................................... 111

Figure 53. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7including debt and the constant

rate of interest, 𝑟 is varied from 1% 𝑡𝑜 5% using a linear form of the Phillips curve to

model wages.................................................................................................................... 112

Figure 54. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 being varied from

0.5𝛿𝐾, 𝑜 𝑡𝑜 5𝛿𝐾, 𝑜 with no debt and a nonlinear form of the Phillips curve to model

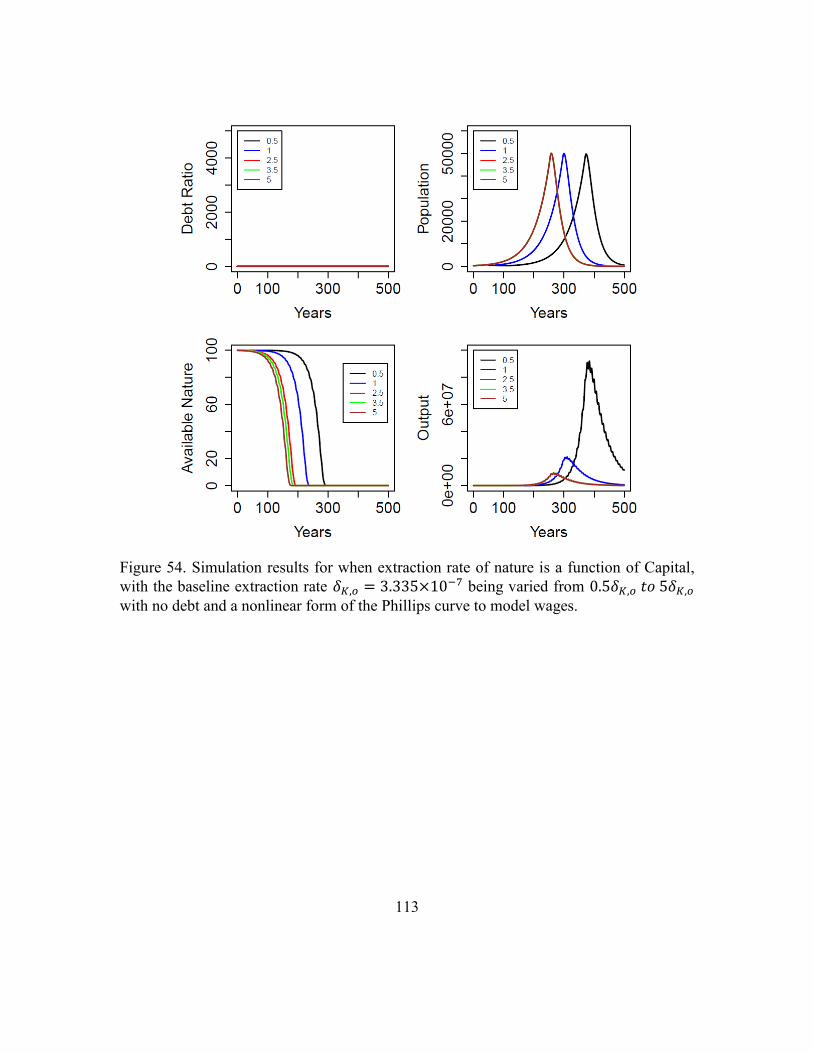

wages............................................................................................................................... 113

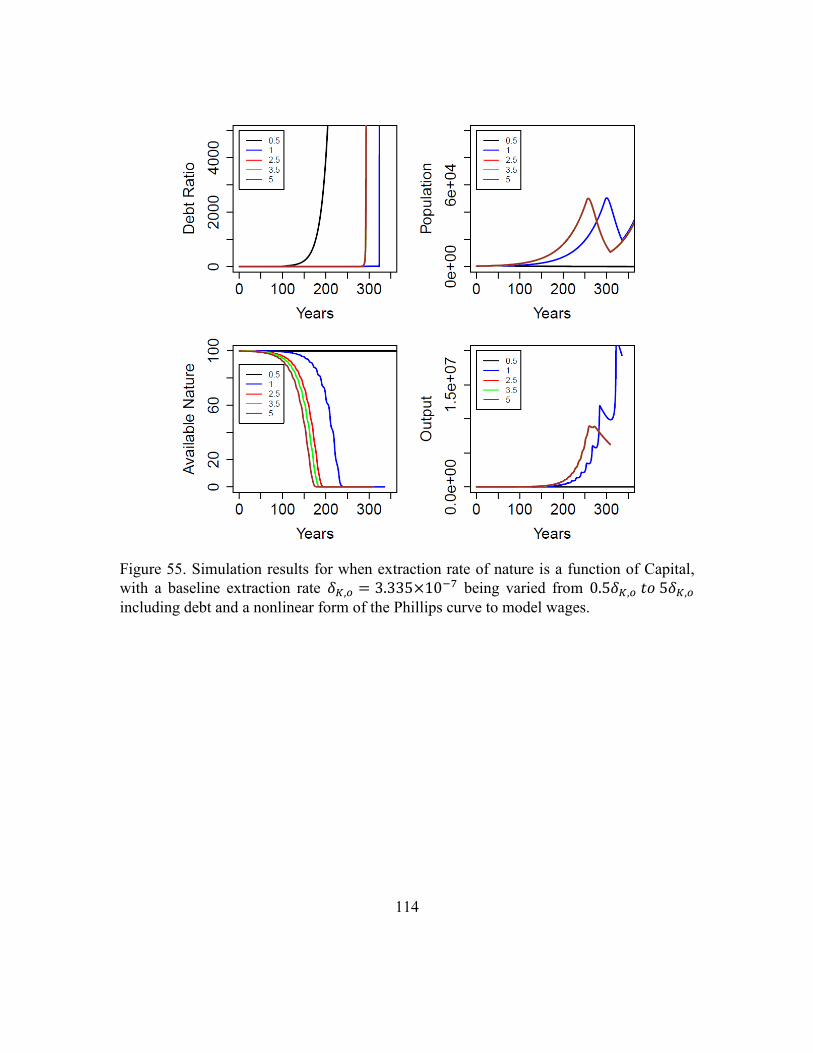

Figure 55. Simulation results for when extraction rate of nature is a function of Capital,

with a baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 being varied from

0.5𝛿𝐾, 𝑜 𝑡𝑜 5𝛿𝐾, 𝑜 including debt and a nonlinear form of the Phillips curve to model

wages............................................................................................................................... 114

Figure 56. Simulation results for when extraction rate of nature is a function of Capital,

with the baseline extraction rate 𝛿𝐾, 𝑜 = 3.335×10 − 7 including debt and the constant

rate of interest 𝑟 is being varied from 1% 𝑡𝑜 5% using a nonlinear form of the Phillips

curve to model wages...................................................................................................... 115

Figure 57. Simulation results for when extraction rate of nature is a function of Power

Input, with the baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1

being varied from 0.5𝛿𝑃𝑖, 𝑜 𝑡𝑜 5𝛿𝑃𝑖, 𝑜 without debt and a nonlinear form of the Phillips

curve to model wages...................................................................................................... 116

xx

Figure 58. Simulation results for when extraction rate of nature is a function of Power

Input, with the baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 being varied from

0.5𝛿𝑃𝑖, 𝑜 𝑡𝑜 5𝛿𝑃𝑖, 𝑜 with debt being accumulated at a constant rate of interest, 𝑟 = 5%

and a nonlinear form of the Phillips curve to model wages. ........................................... 117

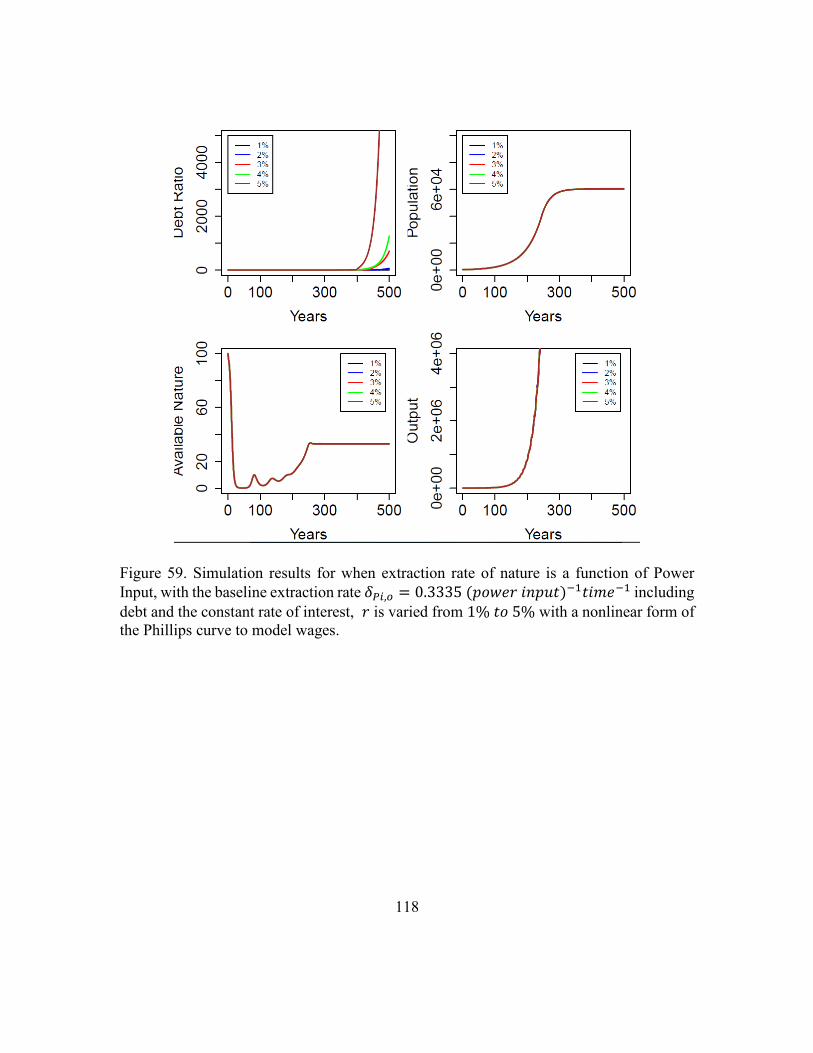

Figure 59. Simulation results for when extraction rate of nature is a function of Power

Input, with the baseline extraction rate 𝛿𝑃𝑖, 𝑜 = 0.3335 (𝑝𝑜𝑤𝑒𝑟 𝑖𝑛𝑝𝑢𝑡) − 1𝑡𝑖𝑚𝑒 − 1

including debt and the constant rate of interest, 𝑟 is varied from 1% 𝑡𝑜 5% with a

nonlinear form of the Phillips curve to model wages. .................................................... 118

1

1. Chapter 1: Introduction

1.1. RESEARCH QUESTION

To understand how energy and resource extraction are linked with long-term

economic outcomes, including the accumulation of debt in the economy.

1.2. PROBLEM STATEMENT

Many economic models implicitly assume that energy resources are not constraints

on the economy. These energy-related constraints have to be introduced if we are to

effectively understand long-term debt and natural resource interactions. This is also true

with various biophysical models that do not consider economic parameters like Debt,

Employment, and Wages. while modeling population growth and resource extractions.

1.3. RESEARCH OBJECTIVE

This objective seeks a consistent biophysical and economic framework to describe

the industrial transition to our contemporary macroeconomic state. Here the research seeks

to integrate macro-scale system dynamics models of money, debt, and employment

(specifically the Goodwin and Minsky models of (Keen, 1995 and Keen, 2013)) with

system dynamics models of biophysical quantities (specifically population and natural

resources such as in (Meadows et al., 1972, Meadows et al., 1974, Motesharrei et al.,

2014)). In other words, there are models of each separately, but they have not been

combined to fundamentally link the biophysical world to monetary frameworks. The

proposed research concept is critical to link biophysical modeling concepts with those

2

economic models that specifically include the link of debt-based finance to employment

and economic growth.

3

2. Chapter 2: Previous Research

2.1. LITERATURE REVIEW

2.1.1. ORIGIN OF HUMANS1,2

Homininans are assumed to be living on this planet for over 5 million years,

probably when some apelike creatures in Africa began to walk habitually on two legs. They

were flaking crude stone tools by 2.5 million years ago. Then some of them spread from

Africa into Asia and Europe after 2 million years ago. The modern human (Homo sapiens,

the only extent members of the Hominina Tribe, the Homininans) is supposedly had to

evolve from ancestors who had remained in Africa. They, too, moved out of Africa and

eventually replaced non-modern human species, notably the Neanderthals in Europe and

parts of Asia, and Homo erectus, typified by Java Man and Peking Man fossils in the far

East (Figure 1). An increase in population and competition and the ability to shape

sophisticated tools, hunt big game, and build permanent shelter may have spurred the first

wave of migration of Homo sapiens from Africa to the Middle East about 100,000 years

ago3. From there people slowly made their way into Central Asia and onward. A new push

into Southeast Asia occurred about 75,000 years ago, and as ice age cooled the earth and

water were concentrated in massive glaciers, the earth’s oceans receded and exposed land

bridges between continents. Taking a fragment of the islands of Indonesia and New Guinea.

By 60,000 BC some groups also crossed from New Guinea to Siberia and Alaska allowed

humans to cross into Americas around 16,000 BC. By 11,000 BC. The human had reached

the southernmost tip of South America.

1 http://www.nytimes.com/2002/02/26/science/when-humans-became-human.html

2 http://www.lanbob.com/lanbob/H-History/HH-02-Societies250KBC-500.html 3 http://www.lwrw.org/Part2.htm

4

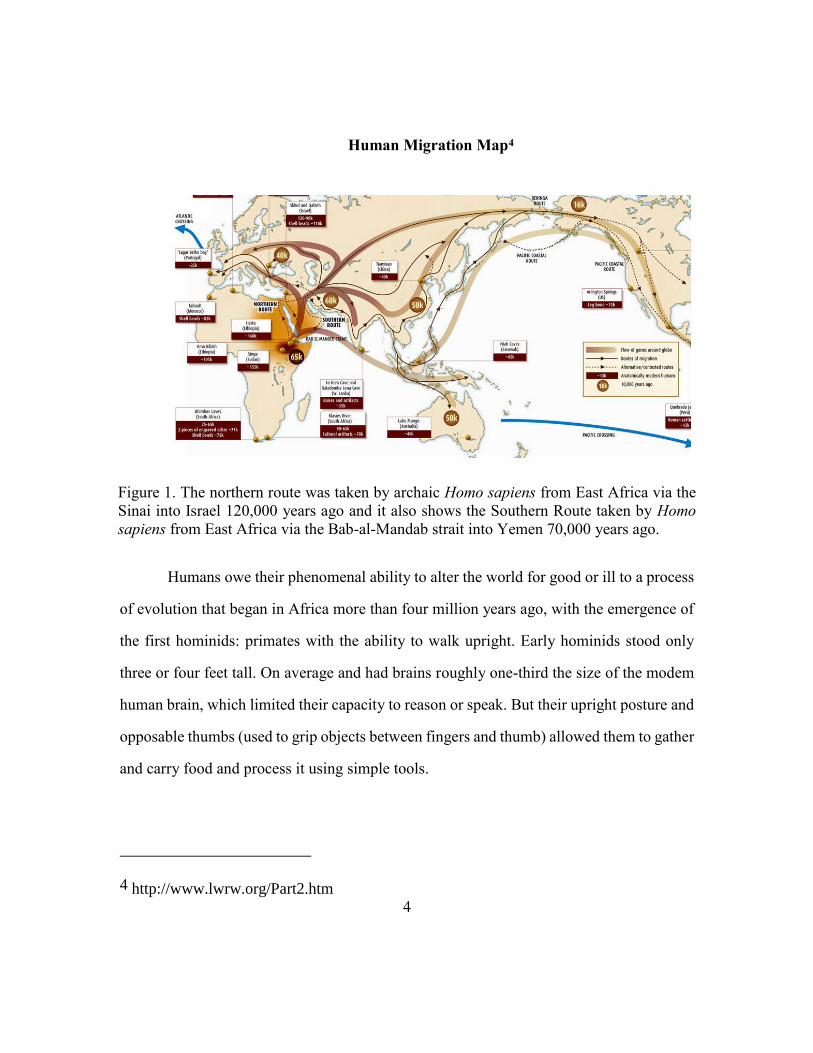

Human Migration Map4

Figure 1. The northern route was taken by archaic Homo sapiens from East Africa via the

Sinai into Israel 120,000 years ago and it also shows the Southern Route taken by Homo

sapiens from East Africa via the Bab-al-Mandab strait into Yemen 70,000 years ago.

Humans owe their phenomenal ability to alter the world for good or ill to a process

of evolution that began in Africa more than four million years ago, with the emergence of

the first hominids: primates with the ability to walk upright. Early hominids stood only

three or four feet tall. On average and had brains roughly one-third the size of the modem

human brain, which limited their capacity to reason or speak. But their upright posture and

opposable thumbs (used to grip objects between fingers and thumb) allowed them to gather

and carry food and process it using simple tools.

4 http://www.lwrw.org/Part2.htm

5

Over time, other species of hominids evolved that possessed larger brains and the

ability to fully articulate their thoughts, craft ingenious tools and weapons, and hunt

collectively. Homo sapiens, or modern humans, emerged in Africa perhaps 250,000 years

ago, and they had a talent for adapting to changing circumstances that allowed them to

occupy much of the planet (Trinkaus 2005) and (Antón and Swisher III 2005). By clothing

themselves in animal hide and living in caves warmed by fires, they survived winters in

northern latitudes during the most recent phase of the Ice Age, which came to an end around

12,000 years ago. That glaciation lowered sea levels and enabled people to walk from

Siberia to North America and reach Australia and other previously inaccessible land

masses.

During the Ice Age, humans gathered wild grains and other plants, but they owed

their survival and success largely to hunting. They became so, skilled were in hunting in

groups and killing larger animals that they probably contributed to the extinction of such

species as the mammoth and mastodon.5 Hunters paid tribute to the animals they stalked

in cave paintings that may have been intended to honor the spirit of those creatures so they

would offer up their bounty. From early times, the destructive power of humans as

predators was linked to their creative power as artists and inventors.

The warming of the planet that began around 10,000 BC forced humans to adapt,

and they did so with great ingenuity. Many of the larger animal’s people had feasted on

during the Ice Age died out as a result of global warming and over-hunting.6 At the same

time, edible plants flourished in places that had once been too cold or dry to support them.

5 http://www.nature.com/nature/journal/v532/n7598/full/nature17176.html

6 http://news.nationalgeographic.com/news/2001/11/1112_overkill_2.html

6

Based on the behavior of hunter-gatherers in recent times, women did much of the

gathering in ancient times and probably used their knowledge of plants to domesticate

wheat barley, rice, corn and other cereals. That allowed groups who had once roamed in

search of sustenance to settle in one place. The most productive societies those that

practiced agriculture by controlling animals and cultivating plants. Agriculture provided

food surpluses that allowed people to specialize in other pursuits and devise new tools and

technologies.

Some of the earliest advances in agriculture occurred in the Middle East, where

sizable towns such as Jericho developed. By 7000 BC Jericho had around 2,000 inhabitants

or more than ten times as many people as in a typical band of hunter‑gatherers. To protect

their community from raiders, the people of Jericho built a wall that became legendary.

Within Jericho and other such towns lived many people who specialized in non-agricultural

trades, including merchants, metalworkers, and potters. The demand for pots to hold grain

and other perishables led to the development of the potter's wheel, which may, in turn, have

inspired the first wheeled vehicles. Farmers here and elsewhere used wooden plows pulled

by cattle or other draft animals to cultivate their fields and exchanged surplus food for clay

pots, copper tools, and other crafted items.

By 5000 BC agriculture was being practiced in large parts of Europe, Asia, and

Africa. Few animals were domesticated in the Americas because they had few domestic -

able species. (Horses had died out and would not be reintroduced until Europeans reached

what they called the New World.) But the domestication of corn and other crops in the

Americas led to the growth of villages and complex societies, marked by a high degree of

specialization.

7

2.1.2. RISE AND FALL OF CIVILIZATIONS7,8

By 3500 BC the stage was set for the emergence of societies so complex and

accomplished they rank as civilizations, a word derived from the Latin civic or citizen. All

early civilizations had impressive cities or ceremonial centers adorned with fine works of

art and architecture. All had strong rulers capable of commanding the services of thousands

of people for public projects or military campaigns. Many but not all used writing to keep

records, codify laws, and preserve wisdom and lore in the form of literature.

Some of the early historical civilizations that existed were the Harrapan Civilization

which lasted from the 3,000 B.C. to 1500 B.C. (Wright 2009), the Egyptian Civilization

which nearly lasted for 3000 years (Dodson 2004), the Olmec Civilization which reigned

from 1,500 B.C. to 400 B.C. (Malmström 2014) to the recent once like the Roman Empire,

in which the western half of its empire lasted from 27 B.C. until 476 A.D. and the eastern

half from 330 A.D. until 1453 A.D. (Morris 2010), the Mongolian Empire which lasted

from 1206 A.D. to 1368 A.D. (D. Morgan 2007), and many others which saw their fall

either due to climate change or invasion from other rulers.9,10 People in these highly

complex societies possessed superior technology, but they were no better or wiser than

those in simpler societies.11 Civilizations embodied the contradictions in human nature.

They were enormously creative and hugely exploitative, enhancing the lives of some

7 http://www.historytoday.com/christopher-chippindale/collapse-complex-societies

8 http://www.historyandheadlines.com/top-ten-greatest-civilizations/

9 http://www.mnn.com/earth-matters/climate-weather/blogs/5-ancient-civilizations-were-

destroyed-climate-change

10 http://www.gold-eagle.com/article/rise-and-fall-civilizations-0

11 http://www.lanbob.com/lanbob/H-History/HH-02-Societies250KBC-500.htm

8

people and enslaving others. Their cities fostered learning, invention, and artistry, but many

were destroyed by other so‑called civilized people. The glory and brutality of civilization

were recognized by philosophers and poets, who knew that anything a ruler raised up could

be brought down. "When the laws are kept, how proudly his city stands!" wrote Sophocles.

"When the laws are broken, what of his city then?".

Joseph A. Tainter in his book “The Collapse of Complex Societies” defines

complex societies in economic and political terms – by the territorial organization,

specialized occupations, differentiation in terms of class rather than kinship, a state

monopoly of force, of legal jurisdiction, and of authority to direct resources and mobilize

people (J. A. Tainter, The Collapse of Complex Societies 1988) . Collapse he defines as a

rapid shift to a lower level of complexity. Then he looks at the varied theories of collapse,

those that look to external forces of hostile climate change, to internal contradictions of

class interest or to the hints of depleted finite resources, or the ones which appeal to

mystical or animist analysis, for if a civilization grows and flowers, must it not die in its

time also? This, at last, runs back to Vico, whose cyclical theory of history runs from First

Barbaric Times to Civil Societies and then to Returned Barbaric Times (Lifshitz 1948).

Tainter, whose viewpoint is from comparative anthropology, has not much patience

with tales of morality and redemption. He expects a rational reason to exist for collapse

and finds it in economics, generally as a law of declining marginal productivity which will

be discussed in the next paragraph. Farming takes the best land first; as farmed area

increases so it is forced on to more intractable and less productive land. Mines, which begin

with thick and shallow seams, are forced down to thinner and deeper seams. The same is

true of social complexity – of civilization – itself. The apparatus of elites, with their

9

ceremonial buildings, luxury goods, warfare and other consumptions are worth their

expense so long as there is, overall, a net benefit. So is the expense of conquering

neighboring lands, and administering their people. The time comes when extra investment

in more complexity and more empire generates no good at all, for the benefits are wholly

swallowed up in the costs of supporting the administration, bureaucracy and other parasites

that social complexity involves.

Tainter works through three examples to show his general pattern, one from

historical sources, two largely from archaeological. The western Roman empire failed

because maintaining a far-flung empire in a hostile environment imposed excessive costs

on its agricultural basis. The Maya failed because the burdens of competitive warfare and

propaganda displays in place of warfare, between the many city-states of the Maya realm

could no longer be borne by a weakened population. The Chaco complex, a highly-

developed pueblo society of the American southwest of about nine hundred years ago,

failed when communities found the costs of contributing to a regional network of

redistribution not worth the benefit and withdrew from it. The question becomes less, why

do civilizations collapse? and more, why do some civilizations push themselves so far into

the regions of greater cost for such small benefit?

2.1.3. IS EARTH FINITE OR INFINITE?

For a very long time researchers have argued the fact of whether we live in a planet

with either finite or infinite resource. You might think that the world is finite as the number

of atoms, however, big is finite they combine to form a finite number of molecules. The

mixture of these molecules might change with time but at the end, it still remains finite.

10

Then you come across economists like John Locke at the end of the 17th century to Adam

Smith in the middle of the 18th century who talked how the planet seemed to be capable

of supporting the expansion of the human estate for untold generations to come.12 They

saw the world where there was yet a vast reach of the globe that had to be mapped by

humans. Humans relatively were scarce by then and their powers not yet global in scale,

not yet amplified by energies of coal and oil. Many other economists still think that our

planet is infinite. One of the recent examples is one of the famous economists Milton

Mountebank who is said to have revolutionized economic thought, and now he has been

recognized for his singular efforts.13 He demonstrates his idea of infinite planet theory

through his book the “Infinity and Beyond: The Magical Triumph of Economics over Physics”.

Although his book has failed to reach the mainstream audiences, his work has been highly

influential among elite political and corporate leaders. Ronald Reagan being a prominent

example where once he famously said, “there are no limits to growth and human progress

when men and women are free to follow their dreams”.14 That’s a close paraphrasing to

Mountebank’s conclusion to his book.15

So, what is the true answer? Is our planet really finite or is it subjective to how we

see and interpret growth on this planet? Growth is central to our way of life. Businesses

are expected to grow. Every day new businesses are formed and new products are

developed. The world population is also growing, so all this adds up to a huge utilization

of resources. So, what if at some point, growth in resource utilization collides with the fact

12 http://www.iep.utm.edu/smith/

13 http://www.steadystate.org/mountebank-nobel/

14 http://www.presidency.ucsb.edu/ws/?pid=38697

15 "Of course, 'Milton Mountebank' is a spoof."

11

that the world is finite. We have grown up thinking that the world is so large that limits

will never be an issue. These are questions that need to be addressed and there exists a

reason to develop a method to do so.

2.1.3.1. THE LIMITS TO GROWTH16

“The Limits to Growth: a report for the Club of Rome's project on the predicament

of mankind” is a 1972 book models economic and population growth with finite resource

supplies (Meadows, et al. 1972). The authors were Donella H. Meadows, Dennis L.

Meadows, Jorgen Randers and Willian W. Behrens III. The book used a computer model

called the World3 model to simulate the consequence of interactions between the earth and

human systems. The World3 model was built specifically to invest 5 major trends of global

concern - accelerating industrialization, rapid population growth, widespread malnutrition,

depletion of nonrenewable resources, and a deteriorating environment. The conclusions

from the model were summarized in “A Report to The Club of Rome (1972)” by the authors

(Limits to Growth: A Report to the Club of Rome, pg. no.1) in 2 points as

(i) “If the present growth trends in world population, industrialization,

pollution, food production, and resource depletion continue unchanged, the limits to

growth on this planet will be reached sometime within the next one hundred years. The

most probable result will be a rather sudden and uncontrollable decline in both

population and industrial capacity”.

(ii) “It is possible to alter these growth trends and to establish a condition of

ecological and economic stability that is sustainable far into the future. The state of

16 https://www.bibliotecapleyades.net/sociopolitica/esp_sociopol_clubrome6.htm

12

global equilibrium could be designed so that the basic material needs of each people on

earth are satisfied and each people has an equal opportunity to realize his individual

human potential”.

The World3 model described in the book is a system dynamics model of present

trends in a way of looking into the future, especially the very near future, and especially if

the quantity being considered is not much influenced by other trends that are occurring

elsewhere in the system. Of course, none of the five factors they were examining are

independent. Each of the 5 trends constantly interacts with each other like

• Population cannot grow without food

• Food production is increased by growth of capital

• More capital requires more resources

• Discarded resources become pollution

• Pollution interferes with the growth of both population and food

Furthermore, over long periods of time, each of these factors also feedbacks to

influence each other. Some projections from the 1972 book using the World3 model can

be seen below in Figure 2 along with the observed trends up until 2000.

13

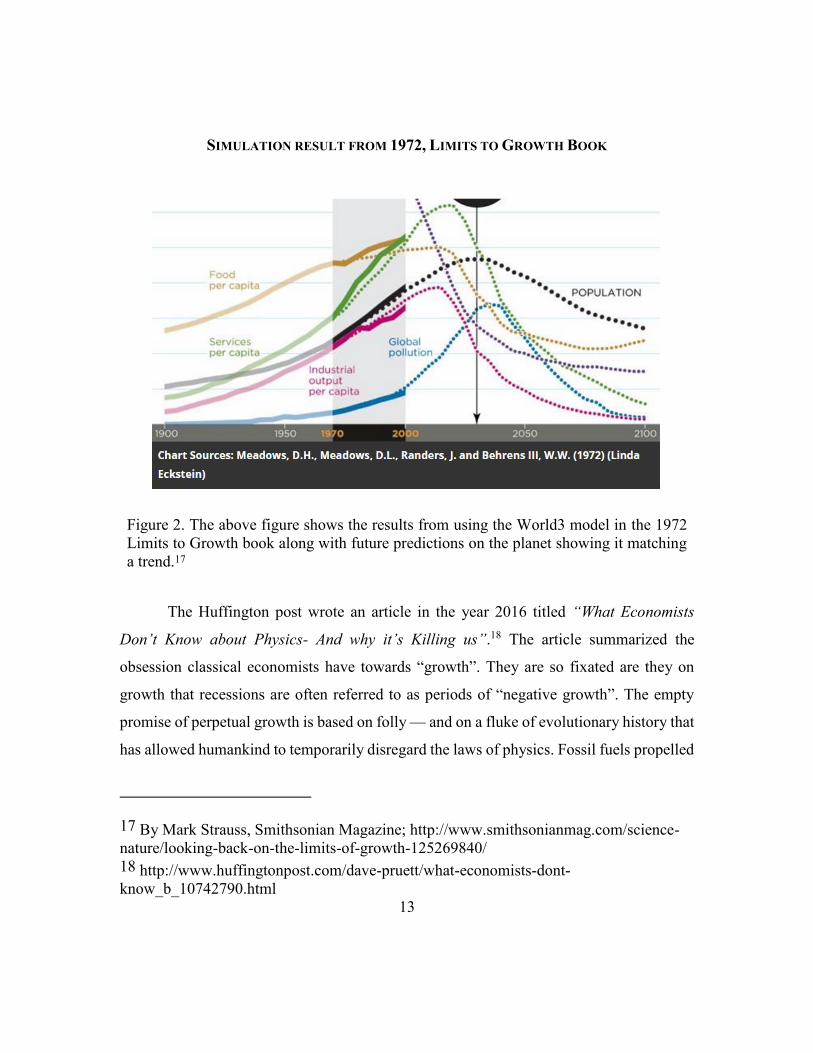

SIMULATION RESULT FROM 1972, LIMITS TO GROWTH BOOK

Figure 2. The above figure shows the results from using the World3 model in the 1972

Limits to Growth book along with future predictions on the planet showing it matching

a trend.17

The Huffington post wrote an article in the year 2016 titled “What Economists

Don’t Know about Physics- And why it’s Killing us”.18 The article summarized the

obsession classical economists have towards “growth”. They are so fixated are they on

growth that recessions are often referred to as periods of “negative growth”. The empty

promise of perpetual growth is based on folly — and on a fluke of evolutionary history that

has allowed humankind to temporarily disregard the laws of physics. Fossil fuels propelled

17 By Mark Strauss, Smithsonian Magazine; http://www.smithsonianmag.com/science-

nature/looking-back-on-the-limits-of-growth-125269840/

18 http://www.huffingtonpost.com/dave-pruett/what-economists-dont-

know_b_10742790.html

14

the Industrial Revolution, which in turn gave us mechanization, rapid transportation, the

subjugation of nature, and industrial agriculture, all the ingredients for modern, urbanized,

high-density societies. Powered first only by coal, then oil came into the picture, and now

gas has joined the race, the world’s human population more than tripled between 1950 and

2010 (Figure 3).

Figure 3. World population 1750-2015 and projections until 2100.19

Thermodynamics refer to isolated, closed, and open systems. An isolated system is

hermetically sealed: it can exchange neither matter nor energy with its surroundings. At

the other extreme, an open system can exchange both. With a semi-permeable boundary, a

closed system, can exchange energy but not matter. Mainstream economists tend to think

19 https://ourworldindata.org/world-population-growth/#note-4

15

of the economy as an abstract, mathematical computerization independent of the physical

world. But economic activity necessarily requires natural resources, which are in limited

supply as discussed in the opening paragraph. The notion of perpetual economic growth is

absurd on face value because it demands an unbounded supply of natural resources and

thus an infinitely large earth.20

2.1.4. ECONOMIC MODELS AND DIFFERENT TYPES OF PRODUCTION FUNCTIONS

An Economic model (M. S. Morgan 2008) is a theoretical construct representing

economic processes by a set of variables and a set of logical and/or quantitative

relationships between them. It’s a simplified framework designed to illustrate the complex

process, often but not always using mathematical techniques. An economic model may

have various exogenous variables, and those variables may change to create various

responses by economic variables. Methodological uses of models include investigation,

theorizing, and fitting theories to the world (M. S. Morgan 2008). These models are used

for many purposes like forecasting, economic policy, planning and allocation, logistics,

business management etc.

Economic models can be such powerful tools in understanding some economic

relationships that it is easy to ignore their limitations (Stanford 1993).

The fundamental issue is circularity: embedding one's assumptions as foundational

"input" axioms in a model, then proceeding to "prove" that, indeed, the model's "output"

supports the validity of those assumptions. Such a model is consistent with similar models

20 https://academic.oup.com/nsr/article/3/4/470/2669331/Modeling-sustainability-

population-inequality

16

that have adopted those same assumptions. But is it consistent with reality? As with any

scientific theory, empirical validation is needed, if we are to have any confidence in its

predictive ability. If those assumptions are, in fact, fundamental aspects of empirical

reality, then the model's output will correctly describe reality (if it is properly "tuned", and

if it is not missing any crucial assumptions). But if those assumptions are not valid for the

particular aspect of reality one attempts to simulate, then it becomes a case of "GIGO" –

Garbage In, Garbage Out".

2.1.4.1. SOLOW-SWAN MODEL OF ECONOMIC GROWTH

The Solow–Swan model (Solow 1956) is an exogenous growth model, an economic

model of long-run economic growth set within the framework of neoclassical economics.

It attempts to explain long-run economic growth by looking at capital accumulation, labor

or population growth, and increases in productivity commonly referred to as technological

progress. At its core, it is a neoclassical aggregate production function, usually of a Cobb–

Douglas type, which enables the model "to make contact with microeconomics”

(Acemoglu 2009). The model was developed independently by Robert Solow and Trevor

Swan in 1956 and superseded the post-Keynesian Harrod–Domar model (Harrod 1939)

and (Domar 1946) . In 1987 Solow was awarded the Nobel Prize in Economics for his

work. Today, economists use Solow’s sources-of-growth accounting to estimate the

separate effects on economic growth of technological change, capital, and labor.

17

Assumptions in the model:

The key assumption of the neoclassical growth model is that capital is subject to

diminishing returns in a closed economy.

1. Given a fixed stock of labor, the impact on output of the last unit of capital

accumulated will always be less than the one before.

2. Assuming for simplicity no technological progress or labor force growth,

diminishing returns implies that at some point the amount of new capital produced

is only just enough to make up for the amount of existing capital lost due to

depreciation (Acemoglu, 2009). At this point, because of the assumptions of no

technological progress or labor force growth, we can see the economy ceases to

grow.

3. Assuming non-zero rates of labor growth complicates matters somewhat, but the

basic logic still applies (Solow 1956) in the short-run, the rate of growth slows as

diminishing returns take effect and the economy converges to a constant "steady-

state" rate of growth (that is, no economic growth per-capita).

4. Including non-zero technological progress is very similar to the assumption of non-

zero workforce growth, in terms of "effective labor": a new steady state is reached

with constant output per worker-hour required for a unit of output. However, in this

case, per-capita output grows at the rate of technological progress in the “steady-

state” (Swan 1956) (that is, the rate of productivity growth).

18

The Solow-Swan model (Solow 1956) is set in a continuous-time world with no

government or international trade. There is only one commodity, output as a whole, whose

rate of production is designated 𝑌(𝑡). Thus we can speak unambiguously of the

community’s real income. Part of each instant’s output is consumed and the rest is saved

and invested. The fraction of output saved is a constant 𝑠, so that the rate of saving is

𝑠𝑌(𝑡). The community’s stock of capital 𝐾(𝑡) takes the form of an accumulation of the

composite commodity. Net investment is then just the rate of increase of this capital stock

𝑑𝐾

𝑑𝑡 𝑜𝑟 �̇� , so we have the basic identity at every instant of time:

�̇� = 𝑠𝑌 Eq 1

The output is produced with the help of two factors of production, capital, and labor,

whose rate of input is 𝐿(𝑡). Technological possibilities are represented by a production

function

𝑌 = 𝐹(𝐾, 𝐿) Eq 2

The output is to be understood as net output after making good the depreciation of

capital. About production, all we will say at the moment is that it shows constant returns

to scale. Hence the production function is homogeneous of the first degree. This amount to

assuming that there is no scarce non-augmentable resource like land. Constant returns to

scale seem the natural assumption to make in a theory of growth. The scarce-land case

would lead to decreasing returns to scale in capital and labor.

Inserting (Eq 2) in (Eq 1) we get

�̇� = 𝑠𝐹(𝐾, 𝐿) Eq 3

19

This is one equation in two unknowns. One way to close the system would be to

add a demand-for-labor equation: marginal physical productivity of labor equals real wage

rate; and a supply-of-labor equation. The latter could take the general form of making labor

supply a function of the real wage equal to a conventional subsistence level. In any case,

there would be three equations in the three unknowns 𝐾, 𝐿, 𝑟𝑒𝑎𝑙 𝑤𝑎𝑔𝑒.

Instead, if we proceed more in the spirit of the Harrod’s model (Harrod 1939). As

a result of exogenous population growth, the labor force increases at a constant relative

rate 𝑛. In the absence of technological change 𝑛 is Harrod’s natural rate of growth. Thus

𝐿(𝑡) = 𝐿𝑜𝑒𝑛𝑡 Eq 4

Alternatively, (Eq 4) can also be looked as a supply curve of labor. It says that the

exponentially growing labor force is offered for employment completely in-elastically. The

labor supply curve is a vertical line which shifts to the right in time as the labor force grows

according to (Eq 4). Then the real wage adjusts so that all available labor is employed, and

the marginal productivity equation according to (Eq 5) and (Eq 6) determines the wage rate

which will actually rule.

𝜕𝐹

𝜕𝐿=

𝑤

𝑝 Eq 5

𝜕𝐹

𝜕𝐾=

𝑞

𝑝 Eq 6

In (Eq 3) 𝐿 stands for total employment whereas in (Eq 4) 𝐿 stands for the available

supply of labor. By identifying the two we are assuming that full employment is perpetually

maintained. When we insert (Eq 4) in (Eq 3) to get

20

�̇� = 𝑠𝐹(𝐾, 𝐿𝑜𝑒𝑛𝑡) Eq 7

We have this basic equation that determines the time evolution of capital

accumulation that must be followed if all available labor is to be employed. In summary,

(Eq 5) is a differential equation in the single variable 𝐾(𝑡). Its solution gives the only time

profile of the community’s capital stock that can fully employ the available labor. Once we

know the time evolution of capital stock and that of the labor force, we can compute from

the production function the corresponding time path of real output.

2.1.4.2. COBB-DOUGLAS MODEL OF PRODUCTION

In economics, the Cobb–Douglas (Cobb and Douglas 1928) and (Douglas 1976)

production function is a particular functional form of the production function, widely used

to represent the technological relationship between the amounts of two or more inputs,

particularly physical capital and labor, and the amount of output that can be produced by

those inputs. Sometimes the term has a more restricted meaning, requiring that the function

display constant returns to scale (in which case 𝛽 = 1 − 𝛼 in the formula below). In its

most standard form for production of a single good with 2 factors, the function is

𝑌 = 𝐴𝐿𝛽𝐾𝛼 Eq 8

Where,

𝑌 = 𝑇𝑜𝑡𝑎𝑙 𝑝𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛 ( 𝑡ℎ𝑒 𝑟𝑒𝑎𝑙 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑎𝑙𝑙 𝑔𝑜𝑜𝑑𝑠 𝑝𝑟𝑜𝑑𝑢𝑐𝑒𝑑 𝑖𝑛 𝑎 𝑦𝑒𝑎𝑟)

𝐿 = 𝐿𝑎𝑏𝑜𝑟 𝐼𝑛𝑝𝑢𝑡 ( 𝑡ℎ𝑒 𝑡𝑜𝑡𝑎𝑙 𝑛𝑢𝑚𝑏𝑒𝑟 𝑜𝑓 𝑝𝑒𝑟𝑠𝑜𝑛𝑠 − ℎ𝑜𝑢𝑟𝑠 𝑤𝑜𝑟𝑘𝑒𝑑 𝑖𝑛 𝑎 𝑦𝑒𝑎𝑟)

𝐾 = 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝑖𝑛𝑝𝑢𝑡 ( 𝑡ℎ𝑒 𝑟𝑒𝑎𝑙 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑎𝑙𝑙 𝑚𝑎𝑐ℎ𝑖𝑛𝑒𝑟𝑦,

𝑒𝑞𝑢𝑖𝑝𝑚𝑒𝑛𝑡, 𝑎𝑛𝑑 𝑏𝑢𝑖𝑙𝑑𝑖𝑛𝑔𝑠)

21

𝐴 = 𝑡𝑜𝑡𝑎𝑙 𝑓𝑎𝑐𝑡𝑜𝑟 𝑝𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑣𝑖𝑡𝑦

𝛼 𝑎𝑛𝑑 𝛽 𝑎𝑟𝑒 𝑡ℎ𝑒 𝑜𝑢𝑡𝑝𝑢𝑡 𝑒𝑙𝑎𝑠𝑡𝑖𝑐𝑖𝑡𝑖𝑒𝑠 𝑜𝑓 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑎𝑛𝑑 𝑙𝑎𝑏𝑜𝑟, 𝑟𝑒𝑠𝑝𝑒𝑐𝑡𝑖𝑣𝑒𝑙𝑦.

If

𝛼 + 𝛽 = 1, Eq 9

The production function has constant returns to scale, meaning that doubling the usage of

capital K and Labor L will also double output Y. If

𝛼 + 𝛽 < 1, Eq 10

Returns to scale are decreasing, and if

𝛼 + 𝛽 > 1, Eq 11

Returns to scale are increasing. Assuming perfect competition21 and 𝛼 + 𝛽 = 1, 𝛼 𝑎𝑛𝑑 𝛽

can be shown to be capital’s and labor’s share of output.

2.1.4.3. LEONTIEF PRODUCTION FUNCTION

The Leontief production function or fixed proportions production function is a

production function that implies the factors of production will be used in fixed

(technologically pre-determined) proportions, as there is no substitutability between

factors. It was named after Wassily Leontief and represents a limiting case of the constant

21 http://economictimes.indiatimes.com/definition/perfect-competition

22

elasticity of substitution production function (Arrow, et al. 1961), (Jorgensen 2000) and

(Klump, William and McAdam 2007)

For the simple case of a good that is produced with two inputs, the function is of

the form

𝑞 = 𝑀𝑖𝑛(𝑧1

𝑎,

𝑧2

𝑏) Eq 12

where q is the quantity of output produced, z1 and z2 are the utilized quantities of

input 1 and input 2 respectively, and a and b are technologically determined constants.

2.2. GAPS IN LITERATURE

All economic models, no matter how complicated, are subjective approximations

of reality designed to explain observed phenomena. It follows that the model’s predictions

must be tempered by the randomness of the underlying data it seeks to explain and by the

validity of the theories used to derive its equations. A good example would be highlighting

the failure of existing models to predict or untangle the reasons for the global financial

crisis that began in 2008. Insufficient attention to the links between overall demand, wealth,

and in particular excessive financial risk taking has been blamed.22 No economic model

can be a perfect description of reality. Economic models can also be classified in terms of

the regularities they are designed to explain or the questions they seek to answer. For

example, some models explain the economy’s ups and down around an evolving long-run

path, focusing on the demand for goods and services without being too exact about the

sources of growth in the long run. Other models are designed to focus on structural issues,

22 http://www.imf.org/external/pubs/ft/fandd/basics/models.htm

23

such as the impact of trade reforms on long-term production levels, ignoring short term

oscillations.

Keynesian economics tells us that how in the short run, and especially during

recessions, economic output is strongly influenced by aggregate demand.23 In the

Keynesian view, aggregate demand does not necessarily equal the productive capacity of

the economy; instead, it is influenced by a host of factors and sometimes behaves

erratically, affecting production, employment, and inflation. The theories forming the basis

of Keynesian economics were first presented by the British economist John Maynard

Keynes during the Great Depression in his 1936 book, “The General Theory of

Employment, Interest, and Money” (Keynes 1936). Keynesian economists often argue

that private sector decisions sometimes lead to inefficient macroeconomic outcomes which

require active policy responses by the public sector, in particular, monetary policy actions

by the central bank and fiscal policy actions by the government, in order to stabilize output

over the business cycle. Keynesian economics advocates a mixed economy –

predominantly private sector, but with a role for government intervention during

recessions. Keynesian economics served as the standard economic model in the developed

nations during the latter part of the Great Depression, World War II, and the post-war

economic expansion (1945–1973), though it lost some influence following the oil shock

and resulting stagflation of the 1970’s. The advent of the financial crisis of 2007–08 caused

a resurgence in Keynesian thought, which continues as new Keynesian economics (Dixon

1999).

23 http://www.imf.org/external/pubs/ft/fandd/2014/09/basics.htm

24

Steve Keen is a professor of Economics at Kingston University London who writes

a blog called Steve Keen’s Debtwatch where he wrote an article titled “Neoclassical

Economics: mad, bad and dangerous to know”, which was published in 2009 (Keen,

Neoclassical Economics: mad, bad, and dangerous to know 2009). In this article, he

highlights how the most important thing that global financial crisis has done for economic

theory is to show that neoclassical economics is not merely wrong, but dangerous. He

justifies this by arguing how neoclassical economics contributed directly to the 2007-08

crisis by promoting a faith in the innate stability of a market economy, in a manner which

in fact increased the tendency to instability of the financial system, with its false belief that

all instability in the system can be traced to interventions in the market, rather than the

market itself, it championed the deregulation of finance and a dramatic increase in income

inequality. Its equilibrium vision of the functioning of finance markets led to the

development of the very financial products that are now threatening the continued

existence of capitalism itself.

Simultaneously it distracted economists from the obvious signs of an impending

crisis—the asset market bubbles, and above all the rising private debt that was financing

them. Paradoxically, as capitalism’s “perfect storm” approached, neoclassical

macroeconomists were absorbed in smug self-congratulation over their apparent success

in taming inflation and the trade cycle, in what they termed “The Great Moderation”.

25

3. Chapter 3: Research Approach

3.1. RESEARCH APPROACH

All models are wrong, and some are useful. The neoclassical economic framework

has proved useful for many purposes. But today’s challenges are those of new constraints

pushing the boundaries of economic thinking. Central banking interest rates are lower (now

negative in some cases) than any time in the history of central banking, and debt levels are

at all-time highs. Also, global food and energy are no longer getting cheaper (King 2015b)

after continuous decreases since the industrial revolution. Narratives and models exist for

describing past agrarian civilizations and their relation to resource access (J. A. Tainter,

The Collapse of Complex Societies 1988), (J. A. Tainter, Energy, Complexity, and

Sustainability: A Historical Perspective 2011) and (Tainter, et al. 2003) as well dynamics

of population and social structure (Turchin, Currie, et al. 2013) and (Turchin and Nefedov,

Secular Cycles 2009) These narratives often describe how the quality and quantity of

natural resources relate to the cyclical growth, structure, inequality, and/or complexity of

society and/or the economy overall.

However, it is unclear how these narratives translate both to today’s modern society

enabled by fossil fuels and to a low-carbon energy economy transition. Past agricultural

societies rose and fell powered essentially by renewable energy flows (e.g., sunlight).

These societies were also very unequal with a small number of elite collecting the vast

majority of the income while the vast majority of commoners worked in the energy and

food (e.g., agricultural) sectors. Fossil-fueled machinery, fertilizers, and irrigation enabled

energy and food costs to continually decrease since the start of industrialization. Thus,

today developed economies, primarily powered by fossil fuel stocks, have a very small

26

proportion of workers in energy and food sectors with an equal income and resource access

as compared to the preindustrial world (Mitchell 2013). If the food and energy costs have

reached their cheapest points then many current macroeconomic modeling approaches,

often calibrated only to relatively recent fossil-fueled history, might be insufficient for

understanding current and future economic growth with regard to constraints within food,

water, and energy sectors; climate change; and debt (Pindyck 2013), (Stern 2013) and

(Keen, A Monetary Minsky Model of the Great Recession 2013a). As we attempt to

transition to a low-carbon energy supply, largely based on renewable energy flows, it is

paramount to have internally consistent macro-scale models that track flows and

interdependencies among money, debt, employment and biophysical quantities (e.g.,

natural resources and population).

What if you realized that the fundamental economic framework of models that are

meant to guide a low-carbon energy transition prevents them from actually answering the

question they are supposed to answer? Instead of assuming a series of energy investments,

and then estimating the economic impacts of those choices, they actually do the exact

opposite. They assume economic growth and then make a series of investments to meet

emissions targets without actually factoring in how the energy systems themselves

feedback to economic growth or other social goals.

Monetary models of finance and debt assume that energy resources and technology

are not constraints on the economy. Energy transition scenario models assume that

economic growth, finance, and debt will not be constraints on the energy transition. These

assumptions must be eliminated, and the modeling concepts must be integrated if we are

27

to properly plan for and understand the dynamics of a low-carbon and/or renewable energy

transition.

Over the past 200 years, human civilization has transformed from one dependent

upon renewable energy flows (e.g., sunlight) to one dependent upon fossil energy stocks

(e.g., oil, gas, and coal). Climate change and resource depletion are driving society to

understand how to again live off of low-carbon renewable flows of primary energy. Except

for this time, we are much smarter, and we have increased technological know-how.

As we attempt to transition to a low-carbon energy supply, largely again based

again on renewable energy flows, it is paramount to have internally consistent macro-scale

models that track flows and interdependencies among money, debt, employment and

biophysical quantities (e.g., natural resources and population). This research objective is to

develop a framework to describe our contemporary and future macroeconomic situation

that is consistent with both biophysical and economic principles. Unfortunately, this

fundamental integration does not underpin our current thinking. This improved framework

can contribute to more robust policy-making ability under both current and future changing

circumstances.

The objective here is to develop a consistent biophysical and economic framework

to describe the industrial transition to our contemporary macroeconomic state. This

research seeks to integrate macro-scale system dynamics models of money, debt, and

employment (specifically the Goodwin and Minsky models of (Keen, Finance and

Economic Breakdown: Modeling Minsky's "Financial Instability Hypothesis" 1995) ) with

system dynamics models of biophysical quantities (specifically population and natural

resources such as in (Meadows, et al. 1972) and (Motesharrei, Rivas and Kalnay 2014). In

28

other words, there are models of each separately, but they have not been combined to

fundamentally link the biophysical world to monetary frameworks. Figure 4 outlines the

approach as a critical extension of existing literature.

This type of modeling can answer important questions for a low-carbon transition

(two examples):

1. How does the rate of transition feedback to the growth of population, economic

output, and debt?

The faster we transition, the more capital, labor, and natural resources will be

mobilized to become part of the “energy” sectors. The larger this mobilization, the higher

the cost of energy will become as there is an increasing number of “energy” sector workers

dependent upon selling energy to a decreasing set of “non-energy” sector consumers.

Increasing labor and capital shares for energy is the exact opposite trend of industrialization

as we know it, and there is a critical need to understand the associated feedbacks. For

example, the most recent oil and gas boom and bust cycle could possibly be explained by

too many resources being allocated to the energy sector over too short of a time for the rest

of the economy to adjust. It is important we understand this growth feedback between the

size (labor, capital, energy) of energy and food sectors and economic growth.

2. How do the capital structure (e.g., fixed costs versus variable costs) of fossil and

renewable energy systems relate to and affect economic outcomes?

Renewable and low-carbon energy systems (e.g., PV, the wind, nuclear,

electrochemical storage) are characterized by a much higher fraction of fixed (capital) costs

as compared to fossil energy systems (e.g., coal, natural gas, and oil). Higher fixed costs

29

systems are more favorable in certain (e.g., predictable) and lower growth (with low

discount rate) environments whereas lower fixed cost systems are more favorable in

uncertain and high growth situations (Chen 2016). The reason is that in high growth

situations you do not want to be “stuck” with old capital in which you are still waiting for