conv heding explained

TRANSCRIPT

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 1/16

Please refer to terms relating to the provision of this research at the end of the document.ABN AMRO Bank NV

250 Bishopsgate

London

EC2M 4AA

United Kingdom

Fixed IncomeRates Strategy - Global

Convexity hedging explainedThe latest dip in the housing numbers suggests residential activity

could be slowing. However, this will have little effect on the degree

of mortgage hedging which will continue to be a significant

influence until yields have risen at least a further 125bp.

Chart 1 : Mortgage amounts outstanding at various coupon levels

0

100

200

300

400

500

600

700

800

4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50 9.00

USD bn

Coupon %

Source: ABN AMRO

Despite the significance of recent mortgage related activity on bond

market volatility, there is some confusion surrounding exactly what it

means, the factors driving the behaviour of the mortgage market and the

mechanisms by which this behaviour impacts other asset classes.

In a changing interest rate environment, mortgage-backed

securities or bonds (MBS) exhibit characteristics that are the reverse of

those seen in standard bullet bonds. This arises as a direct result of the

ability of those taking out mortgages to re-mortgage at lower rates.

Effectively, the household taking out the mortgage has an imbedded put

option and it is this which causes mortgages and assets based upon them to

be negatively convex.

From the issuers' perspective, the prepayment risk they retain canbest be hedged using options as these can be used to replicate the duration

and convexity characteristics of the underlying mortgages.

27 August 2003

Adrian Davies

+44 207 678 3615

A N A LYSIS

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 2/16

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 2

R A T E S S T R A T E G Y

Convexity hedging explained

Introduction

The past quarter has seen bond market volatility reach record levels exacerbated

by mortgage related activity. However, despite the significance of this activity there

is some confusion surrounding exactly what it means, the factors driving the

behaviour of the mortgage market and the mechanisms by which this behaviour

impacts on other asset classes. This note is designed to answer these questions. It

is aimed at a broad range of investors with most definitions, details and

corroborating evidence contained in the appendix for brevity. To understand the

factors which underlie the behaviour of mortgage players it is best to start from

first principles in regard to mortgage bond price characteristics.1

Convexity

The relationship between a bond’s yield and price is not constant (linear) it changes

with the level of yields. The rate at which the relationship between changes in yield

and changes in price evolves is termed convexity. It is the second derivative

between yield and price. Thus, if a bond has positive convexity, if yields fall in

10bp steps its price will rise at an increasing rate for each 10bp fall in yields. Most

bonds exhibit positive convexity. The main exceptions are mortgage bonds which,

for each 10bp fall in yields the price of the bond rises at a decreasing rate.

Negative convexity1

In a changing interest rate environment mortgage-backed securities or bonds(MBS) exhibit characteristics that are the reverse of those seen in standard bullet

bonds and so the term negative convexity is applied to them. This arises as a

direct result of the ability of those taking out mortgages to close an existing

mortgage on their property and open a new one as and when its beneficial. In the

US over 85% of mortgages are fixed rate – most are 30-year mortgages with the

interest rate tied to the long bond.2

Thus, if the long bond yield declines sufficiently

the savings made from refinancing will exceed the costs of re-mortgaging leading

to a flood of refinancing. The mortgagee will repay the existing mortgage early and

take out a new one. If this mortgage forms part of a pool of mortgages against

which an MBS has been issued then the early repayment will mean the holder of

the associated MBS will receive the pre-prepayment. (The exact routing for the

pre-payments will be determined by the structure of individual bonds the mortgageissuer creates from the pool of underlying mortgages.)

Effectively, the household taking out the mortgage has an embedded put option

and it is this which causes mortgages and assets based upon them to be negatively

convex. Increased competition in the home loan market have caused re-mortgaging

costs to plunge over recent years and as a result the break-even change in yield

1 A more detailed explanation of duration and convexity is contained in the appendix.2 Note, that although the mortgage rate is tied to the long bond most hedging activity is done using either 5- or 10-year Treasuries or derivative based upon

them.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 3/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 3

required to make refinancing worthwhile has fallen towards 75bp or less.

Households have become a lot more aware of the potential savings to be made

from re-financing. The main issuers assume 50% of mortgages will be refinanced if

yields fall by 75bp for one month or more. This is illustrated by the annualised

liquidation rates published by FreddieMac for the period up to June 2003. (Note not

all outstanding mortgages are re-financed as yields fall below this level. Mortgage

backed securities can trade with prices in excess of 110 suggesting the remaining

households in the pool face transaction costs of 10% to refinance which is highlyunlikely. This implies a strong sense of inertia exists in the mortgage market.)

Table 1 : Liquidation rates

Annualised

Liquidation Rate

Mth avg

10yr yld

Annualised

Liquidation Rate

Mth avg

10yr yld

Mar 2002 27.2% 5.35 Jan 2003 51.1% 4.00

Apr 24.2% 5.15 Feb 51.0% 3.90

May 21.6% 5.15 Mar 57.2% 3.85

June 23.5% 4.85 Apr 70.4% 3.95

Jul 28.5% 4.60 May 62.6% 3.45

Aug 38.2% 4.25 Jun 67.3% 3.35

Sep 45.4% 3.85

Oct 62.0% 3.90

Nov 57.9% 4.05

Dec 57.2% 4.00

Source: ABN AMRO

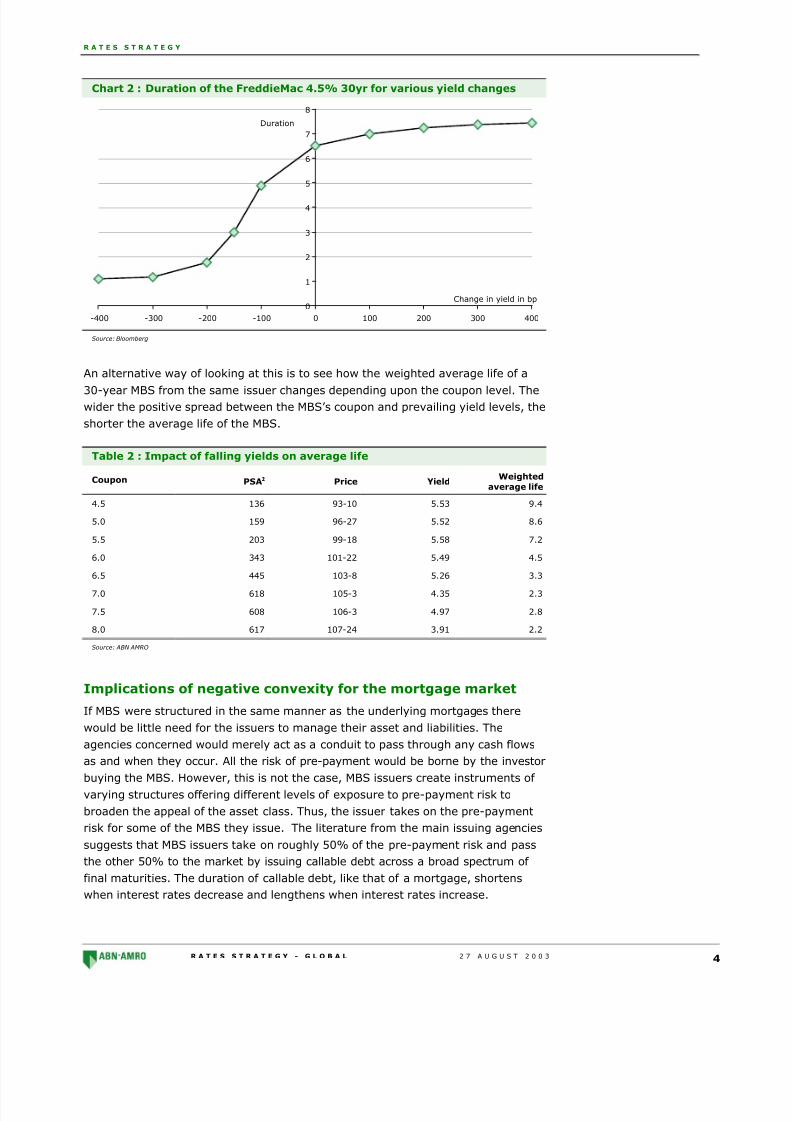

Pre-payments

There are many models designed to capture the pre-payment effect with the most

widely used prepayment assumption being The Bond Market Association Standard

Prepayment Model . Developed by the Bond Market Association to standardise the

measurement of prepayment risk, it assumes that, for new mortgage loans, theprobability of prepayment increases as rates decline or the mortgage “seasons,” or

ages. Both projected and historical prepayment rates are expressed or quoted as a

percentage of The Bond Market Association Standard Prepayment (PSA). Large

shifts in payment patterns has a big impact on the duration of the associated MBS

and the level of prepayments is primarily determined by the prevailing level of

interest rates relative to the pool of mortgages underlying the MBS. It is therefore

possible to calculate the relationship between yield changes and their effect on the

duration of a MBS. This is done in the chart below for the FreddieMac 4.5% 30

year. The effect is dramatic for yield declines of up to 200bp from the original

coupon level. At that point all those who will re-finance have normally done so

leaving those who through inertia or inability ignore the opportunity to re-finance at

cheaper levels. This leaves duration relatively unaffected for yield declines in excessof 200bp. The impact of a rise in yields from the MBS coupon level is less dramatic

as higher yields do not encourage pre-payments and so cash flows remain closely

tied to that envisaged by the MBS structure.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 4/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 4

Chart 2 : Duration of the FreddieMac 4.5% 30yr for various yield changes

0

1

2

3

4

5

6

7

8

-400 -300 -200 -100 0 100 200 300 400

Duration

Change in yield in bp

Source: Bloomberg

An alternative way of looking at this is to see how the weighted average life of a

30-year MBS from the same issuer changes depending upon the coupon level. Thewider the positive spread between the MBS’s coupon and prevailing yield levels, the

shorter the average life of the MBS.

Table 2 : Impact of falling yields on average life

Coupon PSA2222 Price YieldWeighted

average life

4.5 136 93-10 5.53 9.4

5.0 159 96-27 5.52 8.6

5.5 203 99-18 5.58 7.2

6.0 343 101-22 5.49 4.5

6.5 445 103-8 5.26 3.3

7.0 618 105-3 4.35 2.3

7.5 608 106-3 4.97 2.8

8.0 617 107-24 3.91 2.2

Source: ABN AMRO

Implications of negative convexity for the mortgage market

If MBS were structured in the same manner as the underlying mortgages there

would be little need for the issuers to manage their asset and liabilities. The

agencies concerned would merely act as a conduit to pass through any cash flows

as and when they occur. All the risk of pre-payment would be borne by the investor

buying the MBS. However, this is not the case, MBS issuers create instruments of

varying structures offering different levels of exposure to pre-payment risk to

broaden the appeal of the asset class. Thus, the issuer takes on the pre-payment

risk for some of the MBS they issue. The literature from the main issuing agencies

suggests that MBS issuers take on roughly 50% of the pre-payment risk and pass

the other 50% to the market by issuing callable debt across a broad spectrum of

final maturities. The duration of callable debt, like that of a mortgage, shortens

when interest rates decrease and lengthens when interest rates increase.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 5/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 5

It is important to remember that although the various structures allow the MBS

issuer to apportion some of the pre-payment risk between themselves and various

investor classes it does not diminish the overall pre-payment risk associated with

MBS securities. This risk has to be managed by either the issuer of MBS (if the MBS

has been stripped of the some of its pre-payment characteristics) or the investor (if

the MBS retains pre-payment risk).

End investors have a greater propensity to hedge their positions directly in cashmarkets such as the Treasury market but standard swaps are also used

extensively. For example, when yields are rising these investors tend to sell

Treasuries or pay fixed thus compounding the effect of the hedging being

implemented by the mortgage issuers. It is interesting to note that the bond rally

witnessed since the start of 2002 has shortened the duration of many outstanding

MBS to the degree that the duration characteristic of the 5-year Treasury is a closer

match than that of the 10-year Treasury the traditional hedging tool. As a result

more of the recent hedging activity has been conducted in the 5 year than

previously leading to heightened volatility in this area of the curve.

Mortgage market expansion

The ramifications of mortgage issuers hedging activities have been further

intensified by the growth in the size of the overall mortgage market. The MBS

market is one of the largest as the chart below illustrates and the effect of hedging

activity has grown with it.

Chart 3 : Relative bond market sizes

0

1000

2000

3000

4000

5000

6000

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

Treasury Mortgage Corporate

Bil

Source: ABN AMRO

The increases of MBS outstanding relative to the Treasury market has been

especially marked despite the recent rise in the federal government deficit. This

relative expansion of MBS is even more extreme once the effect of the increase in

central bank holdings of Treasuries are taken into account. Large scale intervention

in the foreign exchange markets means as of 1st July $1347bn of Treasury

securities are held by foreign investors, of this $713bn is held by foreign official

bodies with $502 held in Treasury bonds – some 16% of the total marketable

Treasuries outstanding. The majority of these holdings are concentrated in the

short and belly areas of the curve. As the rationale for the investment decision by

central banks is markedly divergent from that of the private sector, central banks

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 6/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 6

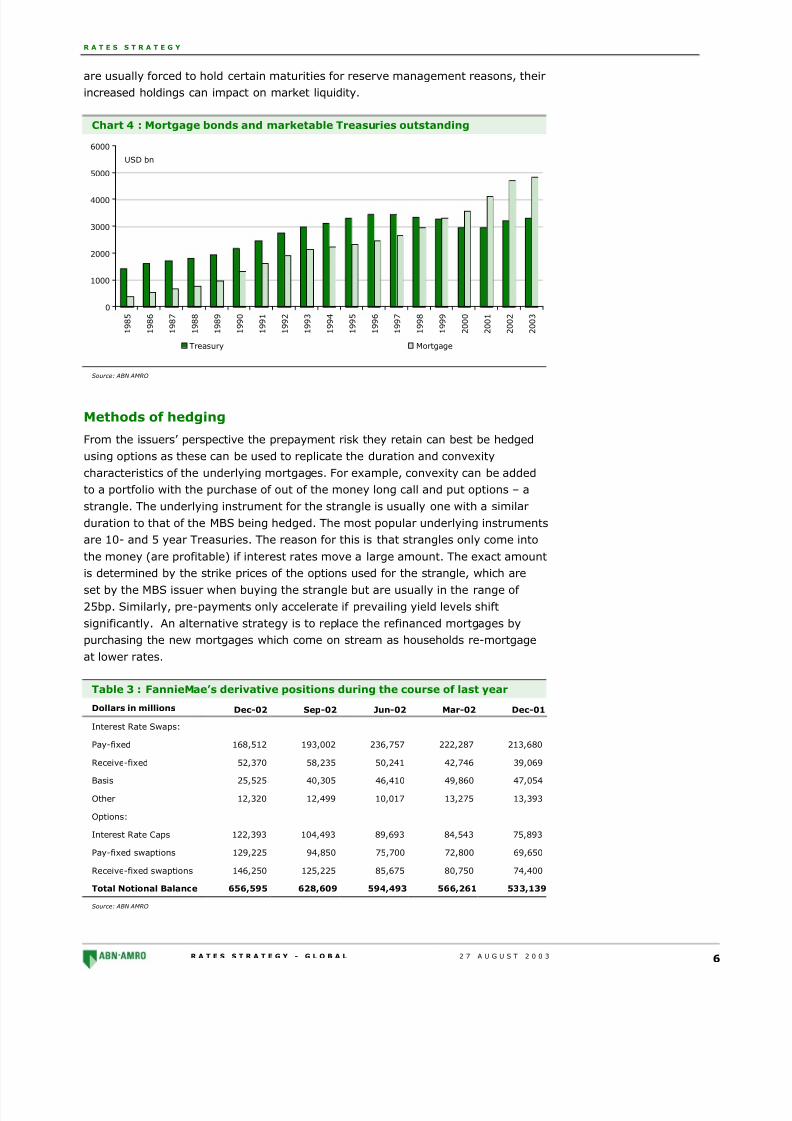

are usually forced to hold certain maturities for reserve management reasons, their

increased holdings can impact on market liquidity.

Chart 4 : Mortgage bonds and marketable Treasuries outstanding

0

1000

2000

3000

4000

5000

6000

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

Treasury Mortgage

USD bn

Source: ABN AMRO

Methods of hedging

From the issuers’ perspective the prepayment risk they retain can best be hedged

using options as these can be used to replicate the duration and convexity

characteristics of the underlying mortgages. For example, convexity can be added

to a portfolio with the purchase of out of the money long call and put options – a

strangle. The underlying instrument for the strangle is usually one with a similar

duration to that of the MBS being hedged. The most popular underlying instruments

are 10- and 5 year Treasuries. The reason for this is that strangles only come into

the money (are profitable) if interest rates move a large amount. The exact amount

is determined by the strike prices of the options used for the strangle, which are

set by the MBS issuer when buying the strangle but are usually in the range of 25bp. Similarly, pre-payments only accelerate if prevailing yield levels shift

significantly. An alternative strategy is to replace the refinanced mortgages by

purchasing the new mortgages which come on stream as households re-mortgage

at lower rates.

Table 3 : FannieMae’s derivative positions during the course of last year

Dollars in millions Dec-02 Sep-02 Jun-02 Mar-02 Dec-01

Interest Rate Swaps:

Pay-fixed 168,512 193,002 236,757 222,287 213,680

Receive-fixed 52,370 58,235 50,241 42,746 39,069

Basis 25,525 40,305 46,410 49,860 47,054

Other 12,320 12,499 10,017 13,275 13,393

Options:

Interest Rate Caps 122,393 104,493 89,693 84,543 75,893

Pay-fixed swaptions 129,225 94,850 75,700 72,800 69,650

Receive-fixed swaptions 146,250 125,225 85,675 80,750 74,400

Total Notional Balance 656,595 628,609 594,493 566,261 533,139

Source: ABN AMRO

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 7/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 7

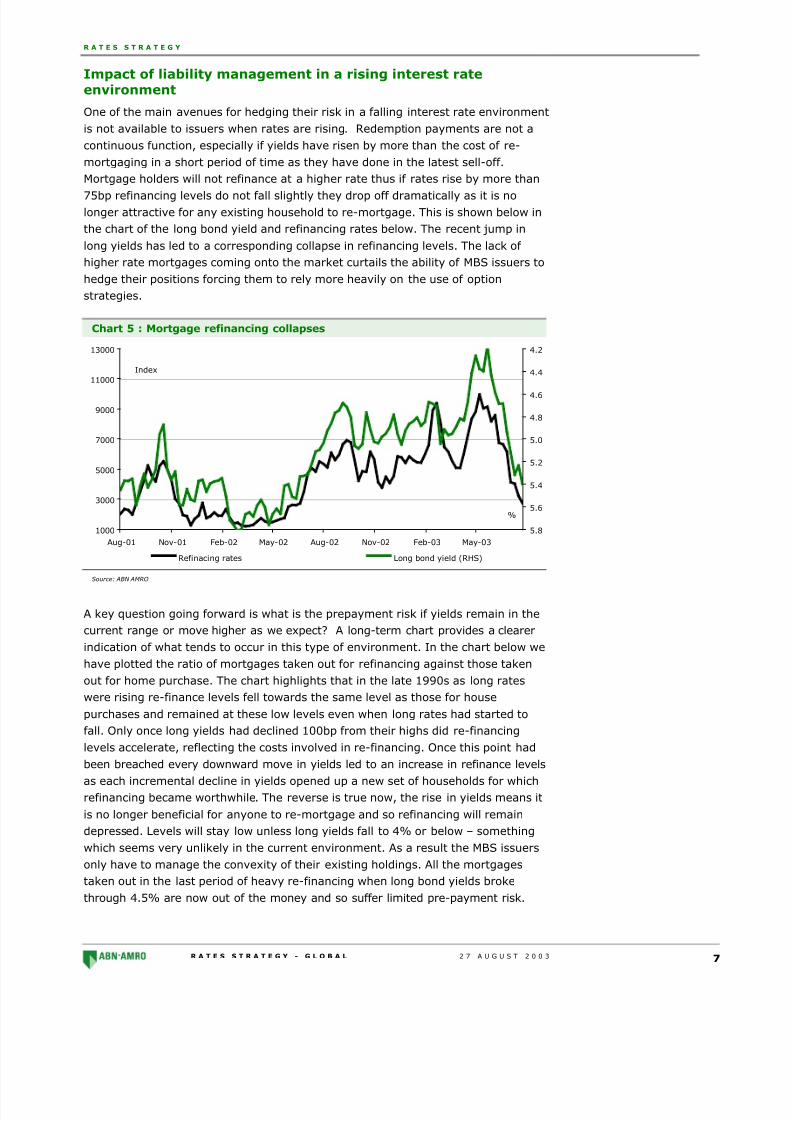

Impact of liability management in a rising interest rate

environment

One of the main avenues for hedging their risk in a falling interest rate environment

is not available to issuers when rates are rising. Redemption payments are not a

continuous function, especially if yields have risen by more than the cost of re-

mortgaging in a short period of time as they have done in the latest sell-off.

Mortgage holders will not refinance at a higher rate thus if rates rise by more than

75bp refinancing levels do not fall slightly they drop off dramatically as it is nolonger attractive for any existing household to re-mortgage. This is shown below in

the chart of the long bond yield and refinancing rates below. The recent jump in

long yields has led to a corresponding collapse in refinancing levels. The lack of

higher rate mortgages coming onto the market curtails the ability of MBS issuers to

hedge their positions forcing them to rely more heavily on the use of option

strategies.

Chart 5 : Mortgage refinancing collapses

1000

3000

5000

7000

9000

11000

13000

Aug-01 Nov-01 Feb-02 May-02 Aug-02 Nov-02 Feb-03 May-03

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

Refinacing rates Long bond yield (RHS)

Index

%

Source: ABN AMRO

A key question going forward is what is the prepayment risk if yields remain in the

current range or move higher as we expect? A long-term chart provides a clearer

indication of what tends to occur in this type of environment. In the chart below we

have plotted the ratio of mortgages taken out for refinancing against those taken

out for home purchase. The chart highlights that in the late 1990s as long rates

were rising re-finance levels fell towards the same level as those for house

purchases and remained at these low levels even when long rates had started to

fall. Only once long yields had declined 100bp from their highs did re-financing

levels accelerate, reflecting the costs involved in re-financing. Once this point had

been breached every downward move in yields led to an increase in refinance levels

as each incremental decline in yields opened up a new set of households for whichrefinancing became worthwhile. The reverse is true now, the rise in yields means it

is no longer beneficial for anyone to re-mortgage and so refinancing will remain

depressed. Levels will stay low unless long yields fall to 4% or below – something

which seems very unlikely in the current environment. As a result the MBS issuers

only have to manage the convexity of their existing holdings. All the mortgages

taken out in the last period of heavy re-financing when long bond yields broke

through 4.5% are now out of the money and so suffer limited pre-payment risk.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 8/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 8

Chart 6 : Mortgage refinancing over the longer term

0

5

10

15

20

25

Aug-98 Aug-99 Aug-00 Aug-01 Aug-02 Aug-03

4.0

4.5

5.0

5.5

6.0

6.5

Proportion LHS Long bond yield RHS

Remortgaging collapses

as yields rise and stay low

even as yields start to

decline. Remortgaging

only increase once yileds

have fallen 100bp from

their peak, the level

needed for refinancing to

become worthwhile.

100bp

refinancing remains elevated even during short

upward blips in yields

Inverse %

IndexMost of the mortgages taken out when

long bond yields were 5.5% are re-

mortgaged at 5% or below

Source: ABN AMRO

This being the case, convexity hedging of MBS based on these mortgages will also

slow at an increasing rate as yields rise. Chart 1 at the start of this piece and thetable below illustrate that the need to hedge for negative convexity as yields move

above the coupon level of the MBS is much lower as compared to when yields fall

below the coupon level. For example the duration of the FreddieMac 4.5% 30yr

increases 0.5 years from 6.5 years to 7.0 year if yields rise by 100bp. The

corresponding fall in duration for a 100bp yield decline is over three times as much

at 1.6 years from 6.5 to 4.9 years. Thus all outstanding mortgages that were

refinanced when long bond yields were in the 5.00 - 4.80 % range will require

much less hedging as yields rise above 5.50%.

Table 4 : Duration of the FreddieMac 4.5% 30yr for various yield changes

Duration 7.45 7.4 7.3 7.0 6.5 4.9 3 1.8 1.2 1.1

Yield change 400 300 200 100 0 -100 -150 -200 -300 -400

Source: ABN AMRO

However, this is only part of the story. The rise in yields will bring many more

mortgages which had coupon levels that were well above current market levels

closer to prevailing market yields as the table and chart below illustrate. Thus,

although mortgage hedging levels will decline for those mortgages which were

taken out during the recent spate of re-financing the effect of this will be swamped

by the volume of mortgages that are moving towards having coupons at current

market levels. The 5.5 to 6.0% coupon levels have particularly large amounts

outstanding suggesting that hedging activity will continue to weigh heavily on the

market for an extended time. Only once yields rise above 6.5% is hedging activitylikely to fall markedly from current levels.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 9/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 9

Table 5 : Amounts outstanding for each issuer per coupon level (USD bn)

Coupon FNMA FHLMC GNMA-1 GNMA-2 Total

4.50 71.9 67.1 2 0.1 141.1

5.00 228.5 156.8 19.5 8 412.8

5.50 412.4 226.9 58.3 26 723.6

6.00 330.4 215.5 64.9 34.8 645.6

6.50 256.2 181.4 75.5 35.4 548.5

7.00 108.6 65.2 52.9 21.4 248.1

7.50 41 25.2 22.5 6 94.7

8.00 17.8 12.1 15.2 2.7 47.8

8.50 5.6 4.1 4.5 0.5 14.7

9.00 2.7 2.2 4.2 0.2 9.3

Source: ABN AMRO

Chart 7 : Mortgage amounts outstanding

0

100

200

300

400

500

600

700

800

4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50 9.00

USD bn

Coupon %

Source: ABN AMRO

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 10/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 10

Appendix

MBS issuers

The main agencies for this are The Federal National Mortgage Association (Fannie

Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), though the

Federal Home Loan Bank System, the Federal Farm Credit Bank System are also

important players. They accomplishes their mission by operating in the secondary

rather than the primary mortgage market purchasing mortgage loans from

mortgage lenders such as mortgage companies, savings institutions, credit unions,

and commercial banks, thereby replenishing those institutions' supply of mortgage

funds. They then either package these loans into Mortgage-Backed Securities

(MBS), which they guarantees for full and timely payment of principal and interest,

or purchase the loans for cash and retain them in their portfolio. The agencies

obtain the funds to finance its mortgage purchases and other business activities by

selling debt securities in the international capital markets.

Duration (or Macaulay duration): The weighted average maturity of all a bond’s

remaining cash flows. It is calculated by multiplying the present value of each cash

flow by the length of time in years until those cash flows are received. These values

are then summed together and divided by the sum of the present value of all the

cash flows. Thus, if a cash flow comes in earlier or later than implied by the bonds

structure the change in the payment date will have a direct impact on the duration

of the bond. Duration is closely related to modified duration which gives an

approximation of the relationship between price and yield. (MD is the first

derivative of price with respect to yield). Thus, any change in payment dates will

also impact modified duration and so the relationship between the effect of a

change in yield on price.

Convexity: Even if a bond’s cash flows do not deviate from those scheduled in itsterms and conditions the relationship between changes in yield and the impact on

prices is not constant (linear) it changes with the level of yields. The rate at which

the relationship between a given change in yield and its effect on price evolves is

termed convexity. It is the second derivative between yield and price. Thus, if a

bond has positive convexity, if yields fall in 10bp steps its price will rise at an

increasing rate for each 10bp fall in yields. Most bonds exhibit positive convexity.

The main exception to this are mortgage bonds.

Structuring issues: Mortgage securities represent an ownership interest in

mortgage loans made by financial institutions (savings and loans, commercial

banks or mortgage companies) to finance the borrower’s purchase of a home or

other real estate. Mortgage securities are created when these loans are packaged,or “pooled,” by issuers or servicers for sale to investors.

As the underlying mortgage loans are paid off by the homeowners, the investors

receive payments of interest and principal. The most basic mortgage securities,

known as “pass throughs,” or participation certificates (PCs), represent a direct

ownership interest in a pool of mortgage loans. More complex type of mortgage

security known as a Collateralised Mortgage Obligation (CMO) allow cash flows to

be directed so that different classes of securities with different maturities and

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 11/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 11

coupons can be created. They may be collateralised by mortgage loans as well as

securitised pools of loans.

Pass-throughs or Participation Certificates (PCs): As the name suggests, the

issuer or servicer of pass-through securities collects the monthly payments from

the homeowners whose loans are in a given pool and “passes through” the cash

flow to investors in monthly payments which represent both interest and

repayment of principal. The payments of principal and interest on passthroughs areconsidered secure; however, the cash flow on these investments may vary from

month to month, depending on the actual prepayment rate of the underlying

mortgage loans. At issuance, the stated maturity of pass-through securities is

generally 30 years, although an increasing number may have 15-, seven- or five-

year stated maturities.

Most pass-throughs are backed by fixed-rate mortgage loans; however, adjustable-

rate mortgage loans (ARMs) are also pooled to create the securities. Most ARMs

have caps and floors limiting the extent of interest-rate changes, and these option-

like characteristics require that pass-throughs backed by ARMs have higher yields

than pure floating-rate debt securities. The market for ARMS is largely an

institutional market.

CMOs or REMICs (Real Estate Mortgage Investment Conduit): The CMO is a

multiclass bond backed by a pool of mortgage pass-throughs or mortgage loans. In

structuring a CMO, an issuer distributes cash flow from the underlying collateral

over a series of classes (called tranches) which constitute the bond issue. Each

CMO is a set of two or more tranches, each having average lives and cash-flow

patterns designed to meet specific investment objectives. The average life

expectancies of the different tranches in a four-part deal, for example, might be

two, five, seven and 20 years. Some CMOs issued have had more than 50 tranches.

As the payments on the underlying mortgage loans are collected, typically the CMO

issuer first pays the coupon rate of interest to the bondholders in each tranche. All

scheduled and unscheduled principal payments generated by the collateral, as

loans are repaid or prepaid, go first to investors in the first tranches. Investors in

later tranches do not start receiving principal payments until the prior tranches are

paid off. This basic type of CMO is known as a sequential pay or plain vanilla CMO.

Any collateral remaining after the final tranche has been paid is known as the

residual.

The final tranche of a CMO often takes the form of a Z-bond, also known as an

accrual bond or accretion bond. Holders of these securities receive no cash until the

earlier tranches are paid in full. During the period that the other tranches are

outstanding, the periodic interest accruals are added to the initial face amount of

the bond but are not paid to investors. When the prior tranches are retired, the Z-

bond receives coupon payments on its higher principal balance, plus any principal

prepayments from the underlying mortgage loans. The existence of a Z-bond

tranche helps stabilise the cashflow patterns in the other tranches. In a changing

interest rate environment, however, the value of the Z-bond itself tends to be more

volatile. As the CMO has evolved, some modifications in the classes of bonds have

become more prevalent. The planned amortisation class (PAC) and targeted

amortisation class (TAC), for example, were designed to reduce investors’

prepayment risk by establishing a sinking-fund structure. PAC and TAC bonds

assure to varying degrees that their investors will receive payments over a

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 12/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 12

predetermined time period under various prepayment scenarios. Although PAC and

TAC bonds are similar, PAC bonds tend to provide more stable cash flow under a

greater number of prepayment scenarios than TAC bonds.

The existence of a PAC or TAC tranche can create higher levels of risk for other

tranches in the CMO because the stability of the PAC or TAC tranche is achieved by

creating at least one other tranche—known as a companion bond or a support or

non-PAC bond—which absorbs the variability of collateral principal cash flows.Because companion bonds have a high degree of average life variability, they

generally pay a higher yield. Companion bonds are not always labelled as such,

however. Moreover, a TAC bond can have some of the prepayment variability of a

companion bond if there is also a PAC bond in the issue.

A Principal Only (PO) is created by stripping the coupon interest from the

underlying mortgages. Because it carries no coupon, a PO is extremely sensitive to

prepayments. Higher prepayments lead to a higher yield. In contrast, an Interest

Only (IO) is the coupon payments from the underlying mortgages. IOs are usually

sold at a deep discount relative to a notional principal amount. IOs increase in

value when prepayment rates decline. Finally, the floating-rate tranche has all the

attributes of multiclass securities except that coupon rates are periodically reset toa margin over the index. The key to analyzing a floating-rate CMO is understanding

the interaction between rate caps and prepayments. Another variation of the CMO

structure is the inverse floater, which has a coupon rate that moves inversely with

the index rate.

Callable Pass-throughs: One of the newest developments in the MBS market is

the Callable Pass-through. A Callable Pass-through is created by splitting a

passthrough into two classes: a “Callable Class” and a “Call Class.” The Callable

Class receives all of the principal and interest from the underlying collateral. The

Call Class receives no principal or interest. The holder of the Call Class has a right

to call the underlying pass-through at a stated price (usually par plus accrued

interest) from the Callable Class holders after a specified period of time has passed

from issuance of the two classes. The Callable Class holder is still long a bond and

short a call option, as is any MBS investor. But rather than just being short a series

of call options to a number of underlying borrowers who may or may not exercise

their option, the holder is also short one call option to one other investor. This

other investor, given his/her economic incentive, will call the underlying pass

through from the Callable Class holder in a much more efficient manner than the

mortgage borrower will. Thus, the Callable Class holder will have reduced

performance relative to pass-through holders if rates fall. For the more limited

upside performance potential, the investor is usually paid more in yield.

Callable Pass-throughs in CMOs. Callable Passthroughs can be used as collateral

to back CMOs or REMICs. Investors need to pay attention to this, as a call of the

underlying Callable Pass-throughs would result in a call of all the outstanding

tranches in a deal. This can be particularly important to holders of long-term

classes.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 13/16

R A T E S S T R A T E G Y

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 13

Table 6 : The various types of derivative hedging strategies used by issuers

are outlined in the table below

Derivative Instrument Impact of hedge

Interest-rate swap (Pay-fixed, receive-floating)

To protect against an increase in interest rates by converting the debt’svariable rate to a fixed rate.

Receive-fixed, pay variableinterest-rate swap

To protect against a decline in interest rate swap rates. Converts the debt’sfixed rate to a variable rate.

Basis swap or spread-lock To “lock in’’ or preserve the spread between variable-rate, interest-earningassets and variable-rate, interest bearing liabilities.

Pay-fixed swaptionTo protect against an increase in interest rates by having an option to payfixed rate.

CapsTo protect against an increase in interest rates by providing a limit on theinterest costs on our debt in a rising rate environment.

Receive-fixed swaptionTo protect against a decline in interest rates by having an option to receivefixed.

Source: ABN AMRO

Measuring the risk if things go wrong: The main measure of used by market

participants to asses the outstanding risk the MBS issuers face is the duration gap.

The duration gap uses prepayment and interest rate models to generate an option

adjusted measure of the difference, in months, between the average duration of

the mortgages held in portfolio and the liabilities that fund those mortgages. This isdone in most cases on monthly average basis.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 14/16

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 14

Companies mentioned:

_____________________________________________________________________________________________________

The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed andattributed to the research analyst or analysts in the research report accurately reflect their personal opinion(s) about thesubject securities and issuers and/or other subject matter as appropriate; and, (2) no part of his or her compensation was, isor will be directly or indirectly related to the specific recommendations or views contained in this research report. On a generalbasis, the efficacy of recommendations is a factor in the performance appraisals of analysts.

_____________________________________________________________________________________________________

Copyright 2003 ABN AMRO Bank N.V. and affiliated companies ("ABN AMRO"). All rights reserved.

This material was prepared by the ABN AMRO affiliate named on the cover or inside cover page. It is provided for informationalpurposes only and does not constitute an offer to sell or a solicitation to buy any security or other financial instrument. Whilebased on information believed to be reliable, no guarantee is given that it is accurate or complete. While we endeavour toupdate on a reasonable basis the information and opinions contained herein, there may be regulatory, compliance or otherreasons that prevent us from doing so. The opinions, forecasts, assumptions, estimates, derived valuations and target price(s)contained in this material are as of the date indicated and are subject to change at any time without prior notice. Theinvestments referred to may not be suitable for the specific investment objectives, financial situation or individual needs of recipients and should not be relied upon in substitution for the exercise of independent judgement. ABN AMRO may from timeto time act as market maker, where permissible under applicable laws, or, as an agent or principal, buy or sell securities,warrants, futures, options, derivatives or other financial instruments referred to herein. ABN AMRO or its officers, directors,employee benefit programmes or employees, including persons involved in the preparation or issuance of this material, mayfrom time to time have long or short positions in securities, warrants, futures, options, derivatives or other financialinstruments referred to in this material. ABN AMRO may at any time solicit or provide investment banking, commercial banking,credit, advisory or other services to the issuer of any security referred to herein. Accordingly, information may be available to

ABN AMRO, which is not reflected in this material, and ABN AMRO may have acted upon or used the information prior to orimmediately following its publication. Within the last three years, ABN AMRO may also have acted as manager or co-managerfor a public offering of securities of issuers referred to herein. The stated price of any securities mentioned herein is as of thedate indicated and is not a representation that any transaction can be effected at this price. Neither ABN AMRO nor otherpersons shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lostprofits arising in any way from the information contained in this material. This material is for the use of intended recipients onlyand the contents may not be reproduced, redistributed, or copied in whole or in part for any purpose without ABN AMRO's priorexpress consent. In any jurisdiction in which distribution to private/retail customers would require registration or licensing of the distributor which the distributor does not currently have, this document is intended solely for distribution to professionaland institutional investors.

Should you require additional information please contact your local ABN AMRO account representative, unless governing lawsdictate otherwise.

Australia: Any report referring to equity securities is distributed in Australia by ABN AMRO Equities Australia Ltd (ABN 84 002768 701), a participating organisation of the Australian Stock Exchange Ltd. Any report referring to fixed income securities isdistributed in Australia by ABN AMRO Bank NV (Australia Branch) (ARBN 079 478 612). Australian investors should note thatthis document was prepared for wholesale investors only.

Canada: The securities mentioned in this material are available only in accordance with applicable securities laws and may notbe eligible for sale in all jurisdictions. Persons in Canada requiring further information should contact ABN AMRO Incorporated.

Hong Kong: This document is being distributed in Hong Kong by, and is attributable to, ABN AMRO Asia Limited which isregulated by the Securities and Futures Commission of Hong Kong.

India: Shares traded on stock exchanges within the Republic of India may only be purchased by different categories of residentIndian investors, Foreign Institutional Investors registered with The Securities and Exchange Board of India ("SEBI") orindividuals of Indian national origin resident outside India called Non Resident Indians ("NRIs") and Overseas Corporate Bodies("OCBs"), predominantly owned by such persons or Persons of Indian Origin (PIO). Any recipient of this document wantingadditional information or to effect any transaction in Indian securities or financial instrument mentioned herein must do so bycontacting a representative of ABN AMRO Asia Equities (India) limited.

Italy: Persons in Italy requiring further information should contact ABN AMRO Bank N.V. Milan Branch.

Japan: This report is being distributed in Japan by ABN AMRO Securities Japan Ltd to institutional investors only.

New Zealand: This document is distributed in New Zealand by ABN AMRO Equities NZ Limited a New Zealand Stock ExchangeFirm.

Russia: The Russian securities market is associated with several substantial risks, legal, economic and political, and highvolatility. There is a relatively high measure of legal uncertainty concerning rights, duties and legal remedies in the RussianFederation. Russian laws and regulations governing investments in securities markets may not be sufficiently developed or maybe subject to inconsistent or arbitrary interpretation or application. Russian securities are often not i ssued in physical form andregistration of ownership may not be subject to a centralised system. Registration of ownership of certain types of securitiesmay not be subject to standardised procedures and may even be effected on an ad hoc basis. The value of investments inRussian securities may be affected by fluctuations in available currency rates and exchange control regulations.

Singapore: This document is distributed in Singapore by ABN AMRO Asia Securities (Singapore) Private Limited to clients who

fall within the description of persons in Regulation 49(5) of the Securities and Futures (Licensing and Conduct of Business)Regulations 2002. Investors should note that this material was prepared for professional investors only.

United Kingdom: Equity research is distributed in the United Kingdom by ABN AMRO Equities (UK) Limited, which is registeredin England (No 2475694), and is authorised and regulated by the Financial Services Authority. All other research is distributedin the United Kingdom by ABN AMRO Bank NV, London Branch, which is authorised by the Dutch Central Bank and by theFinancial Services Authority; and regulated by the Financial Services Authority for the conduct of UK business. The investmentsand services contained herein are not available to private customers in the United Kingdom.

United States: Distribution of this document in the United States or to US persons is intended to be solely to major institutionalinvestors as defined in Rule 15a-6(a)(2) under the US Securities Act of 1934. All US persons that receive this document bytheir acceptance thereof represent and agree that they are a major institutional investor and understand the risks involved inexecuting transactions in securities. Any US recipient of this document wanting additional information or to effect anytransaction in any security or financial instrument mentioned herein, must do so by contacting a registered representative of ABN AMRO Incorporated, Park Avenue Plaza, 55 East 52nd Street, New York, N.Y. 10055, US, tel + 1 212 409 1000, fax +1212 409 5222.

1 Material means all research information contained in any form including but not limited to hard copy, electronic form,presentations, e-mail, SMS or WAP.

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 15/16

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 15

8/6/2019 Conv Heding Explained

http://slidepdf.com/reader/full/conv-heding-explained 16/16

R A T E S S T R A T E G Y - G L O B A L 2 7 A U G U S T 2 0 0 3 16