computerized banking system

TRANSCRIPT

L/O/G/O

Computerized Banking System

FHA. ShiblyLecturer in ITSouth Eastern University of Sri Lanka

Computerized Banking System

• Computerized banking system is a proven, secure, modular, on-line, real-time, flexible, scalable, multi-currency. It is user friendly, easy to manage, and easy to operate information system, based on fully integrated and co-operative components.

Advantages Computerized banking system

• Convenience: • Ubiquity: • Transaction speed: banking initiates speedy

transactions and they are very cost effective and is generally quicker than the transactions conducted at the ATM’s or at the bank

• Efficiency: Feel free to access, manage and control all bank accounts, including Individual Retirement Accounts, CDs, even securities, from one secure site.

• Effectiveness: Manage your money, investment, bank accounts without even going to the bank.

• Data Entry: - Processing presumes data entry. A bank customer operates an ATM facility to make a withdrawal. The actions taken by the customer constitute data which is processed after validation by the computerized personal banking system.

• Data Validation: - It ensures the accuracy and reliability of input data by comparing the same with some predefined standards or known data. This validation is made by the ‘Error Detection’ and ‘Error Correction’ procedures. The control mechanism, wherein actual input data is compared with predetermined norm is meant to detect errors while error correction procedures make suggestions for entering correct data input.

What inside????????

• Processing and Revalidation: - The processing of data occurs almost instantaneously in case of Online Transaction Processing (OLTP) provided a valid data has been fed to the system. This is called check input validity. Revalidation occurs to ensure that the transaction in terms of delivery of money by ATM has been duly completed. This is called check output validity.

• Storage: - Processed actions, as described above, result into financial transaction data i.e. withdrawal of money by a particular customer, are stored in transaction database of computerized personal banking system. This makes it absolutely clear that only valid transactions are stored in the database.

• Information: - The stored data is processed making use of the Query facility to produce desired information.

• Reporting: - Reports can be prepared on the basis of the required information content according to the decision usefulness of the report.

Limitations of computerized banking system

• Cost of Installation• Cost of Training• Self Decision Making• Maintenance• Dangers for Health

Need and requirements of computerized banking system

• Numerous Transactions• Instant Reporting• Reduction in paper work• Flexible reporting• Banking• On-line facility• Scalability• Accuracy• Security

Basic requirements of the computerized Banking system

• Banking framework: - It is the application environment of the computerized Banking system. A healthy Banking framework in terms of Banking principles, coding and grouping structure is a pre-condition for any computerized Banking system.

• Operating procedure: - A well-conceived and designed operating procedure blended with suitable operating environment of the enterprise is necessary to work with the computerized Banking system.

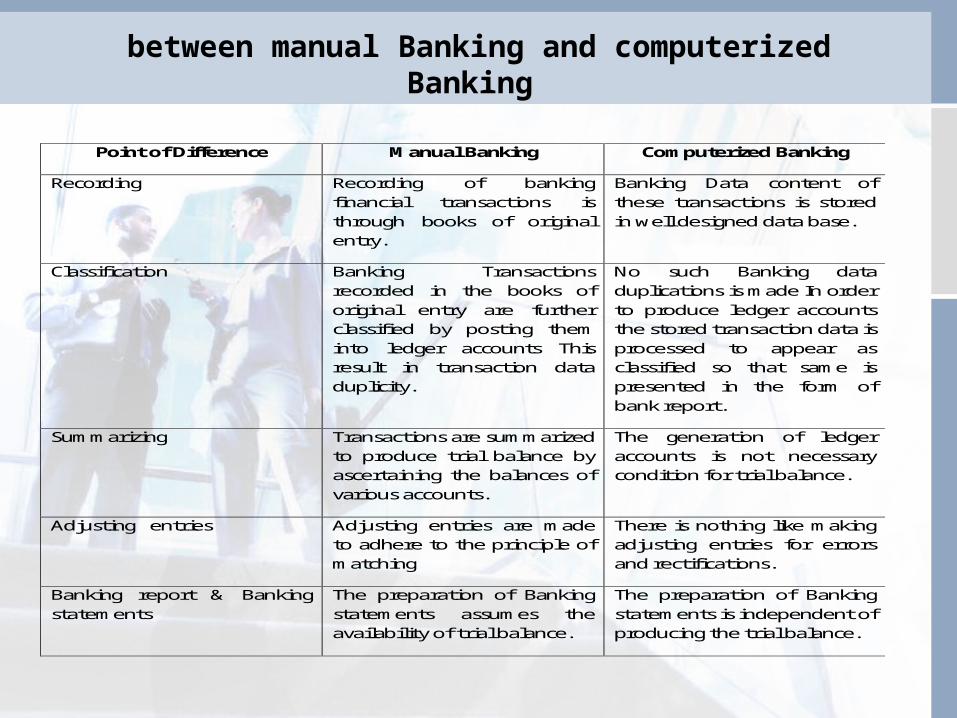

between manual Banking and computerized Banking

Point of Difference Manual Banking Computerized Banking

Recording Recording of banking financial transactions is through books of original entry.

Banking Data content of these transactions is stored in well designed data base.

Classification Banking Transactions recorded in the books of original entry are further classified by posting them into ledger accounts This result in transaction data duplicity.

No such Banking data duplications is made In order to produce ledger accounts the stored transaction data is processed to appear as classified so that same is presented in the form of bank report.

Summarizing Transactions are summarized to produce trial balance by ascertaining the balances of various accounts.

The generation of ledger accounts is not necessary condition for trial balance.

Adjusting entries Adjusting entries are made to adhere to the principle of matching

There is nothing like making adjusting entries for errors and rectifications.

Banking report & Banking statements

The preparation of Banking statements assumes the availability of trial balance.

The preparation of Banking statements is independent of producing the trial balance.

Unique IT Services in Islamic Finance and Key Players

• In the last 25 year, Islamic banking practice has progressed tremendously. The past two and a half decades, serious research done, has established that Islamic banking is a viable and efficient way of financial intermediation.

• Several Islamic banks have been established during this period under mixed, social and economic settings. Recently, many conventional banks, including some major multinational Western banks, have also started using Islamic banking techniques.

• All this is encouraging. Banks moving into Islamic banking require compliance with Sharia’a principles. This compliance has significant effect on bank products, processes and technology systems.

• As a result a healthy sub-sector of information technology (IT) services being catered to the Islamic Finance institutions is emerging.

• The technology implications vary considerably depending on delivery structure, such as through standalone Islamic operation or ‘Islamic windows’ and type of Islamic products offered.

• This impacts both banks and core system providers, with market likely to present diverse opportunities for different vendor types.

Unique Islamic Finance related attributes of IT services

• The complexity of Islamic banking as compared to conventional banking is that products must comply not only with the secular laws of a country but also to the interpretations of the holy Qur'an by Islamic scholars. A central tenet of Sharia'a is prohibition of Riba (interest).

Islamic banking systems today are still falling short of customer expectations because of the following reasons:

• Islamic banking technology systems are still far from the sophistication and quality of conventional systems.

• With existing products, there is limited flexibility to customize / alter the products according to the Sharia’a board of the bank.

• Systems lack some of the critical requirements like Zakat calculation and holiday treatment as per Lunar calendar which are mandatory as per Islamic principles

• Obtaining top level view of customer relationship is extremely difficult and even more difficult in case of Islamic banks with conventional sister concerns

• Client References of Islamic banking technology providers are few and assessing a vendor by reference is extremely difficult

• Islamic Bank implementation team members feel they end up in providing the vendors with more Islamic knowledge instead of vendors providing the banks with IF specific expertise

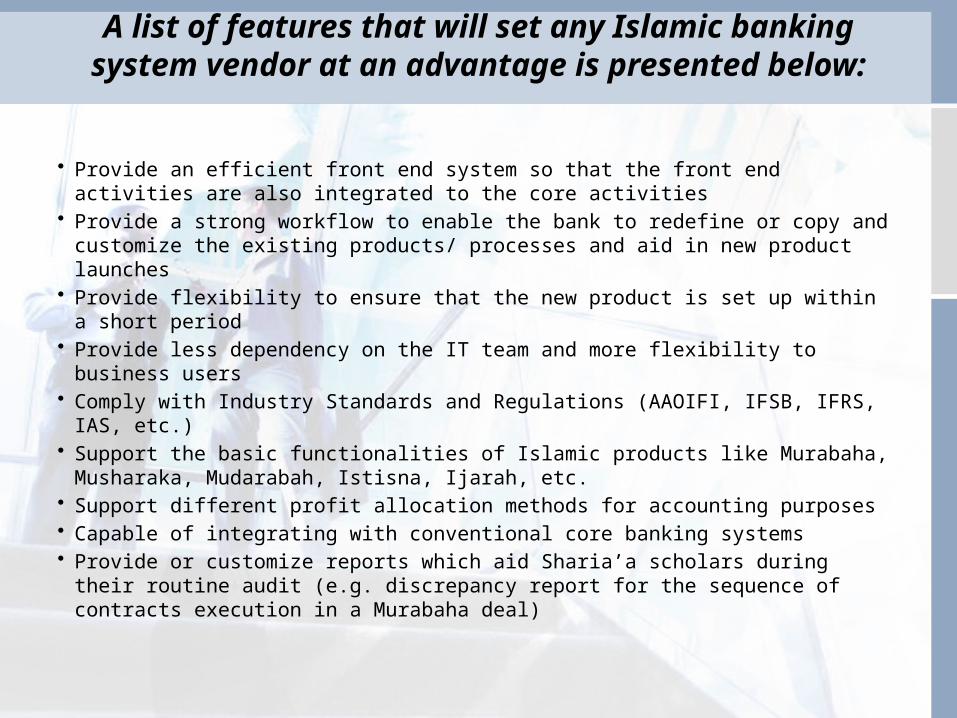

A list of features that will set any Islamic banking system vendor at an advantage is presented below:

• Provide an efficient front end system so that the front end activities are also integrated to the core activities

• Provide a strong workflow to enable the bank to redefine or copy and customize the existing products/ processes and aid in new product launches

• Provide flexibility to ensure that the new product is set up within a short period• Provide less dependency on the IT team and more flexibility to business users• Comply with Industry Standards and Regulations (AAOIFI, IFSB, IFRS, IAS, etc.)• Support the basic functionalities of Islamic products like Murabaha, Musharaka,

Mudarabah, Istisna, Ijarah, etc.• Support different profit allocation methods for accounting purposes• Capable of integrating with conventional core banking systems• Provide or customize reports which aid Sharia’a scholars during their routine

audit (e.g. discrepancy report for the sequence of contracts execution in a Murabaha deal)

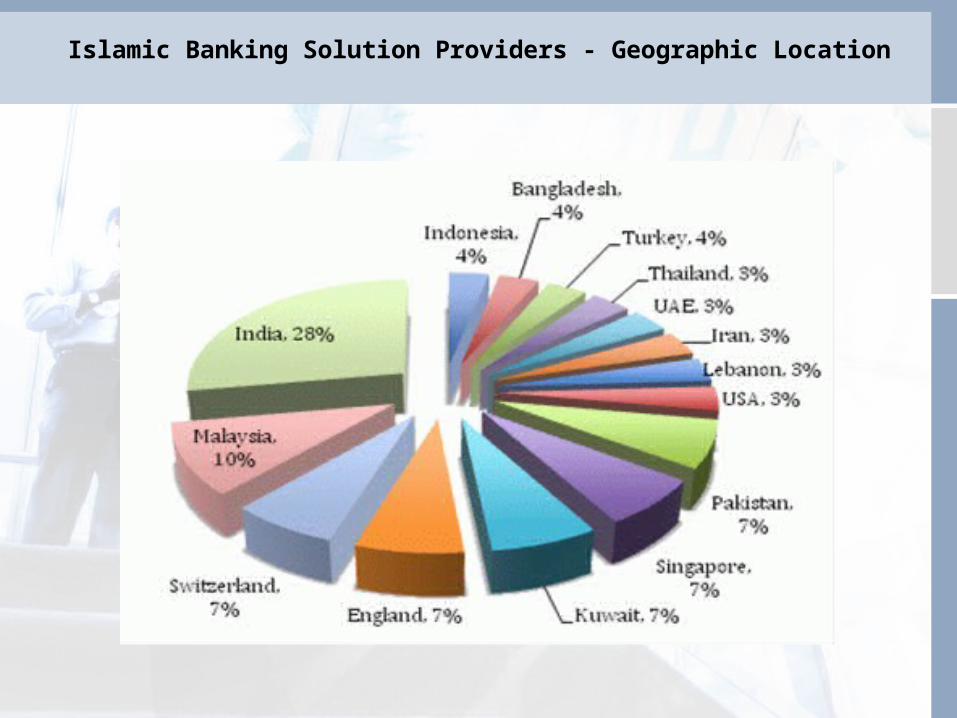

Islamic Banking Solution Providers - Geographic Location

• Large banking software vendors have successfully created Islamic banking software based on their conventional platform to fit the Islamic banking requirements. However their initial customers still feel that they ended up being midwifes because of the poor understanding of vendors requirements. Small IT companies that anticipated the growing Islamic banking market and managed to be the early entrants do face a situation whether to invest in further R&D or to wait for a potential client before committing any more funds.

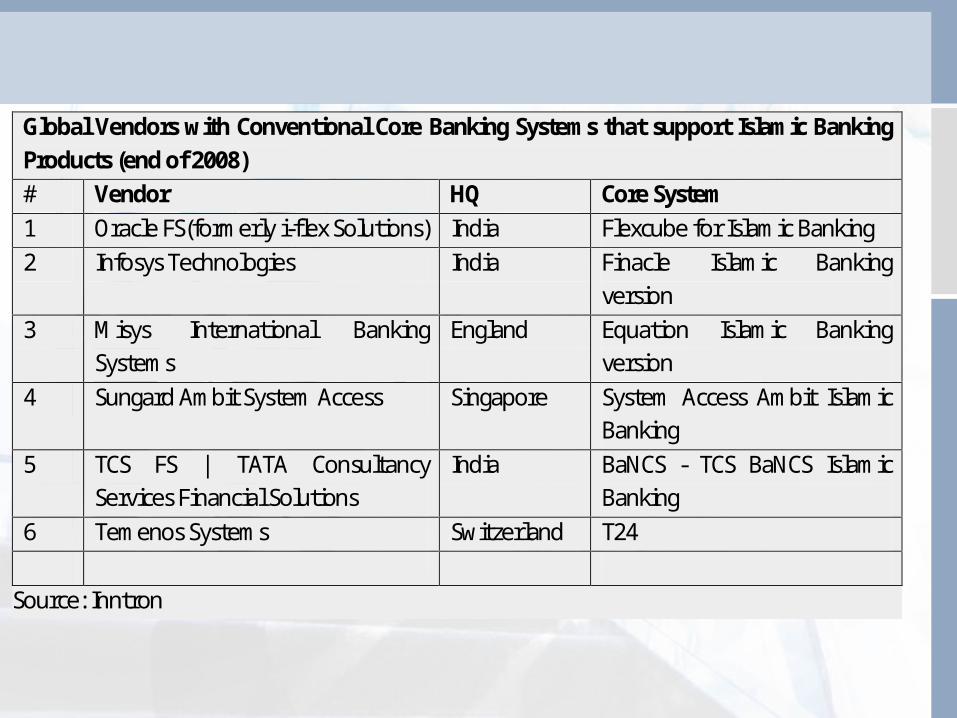

Global Vendors with Conventional Core Banking Systems that support Islamic Banking Products (end of 2008) # Vendor HQ Core System 1 Oracle FS(formerly i-flex Solutions) India Flexcube for Islamic Banking 2 Infosys Technologies India Finacle Islamic Banking

version 3 Misys International Banking

Systems England Equation Islamic Banking

version 4 Sungard Ambit System Access Singapore System Access Ambit Islamic

Banking 5 TCS FS | TATA Consultancy

Services Financial Solutions India BaNCS - TCS BaNCS Islamic

Banking 6 Temenos Systems Switzerland T24

Source: Inntron

Conclusion

• Demand for banking products compliant with Islamic law, or Sharia'a, continues to grow throughout the world. The Islamic assets growth is estimated at 15% annually.

• This growth in turn drives the creation of more Islamic banks and the addition of Sharia'a-compliant products at conventional banks. Banks, working with Islamic scholars, have been able to create a set of profitable banking products that meet the financial needs of their customer base while insuring adherence to the principles of Sharia'a.

L/O/G/O

DISCUSSIONS