comprehensive annual financial report - lane county · we are pleased to submit the comprehensive...

TRANSCRIPT

Comprehensive Annual Financial Report

Lane County, Oregon

Responsibly managing limited resources to deliver vital, customer-focused services with passion, innovation, and integrity.

For the Fiscal Year Ended June 30, 2016

COMPREHENSIVE ANNUAL FINANCIAL REPORT LANE COUNTY, OREGON

FOR THE FISCAL YEAR ENDED JUNE 30, 2016

REPORT PREPARED BY LANE COUNTY OPERATIONS DIVISION - FINANCIAL SERVICES

INTRODUCTORY SECTION

INTRODUCTORY SECTION Page(s)

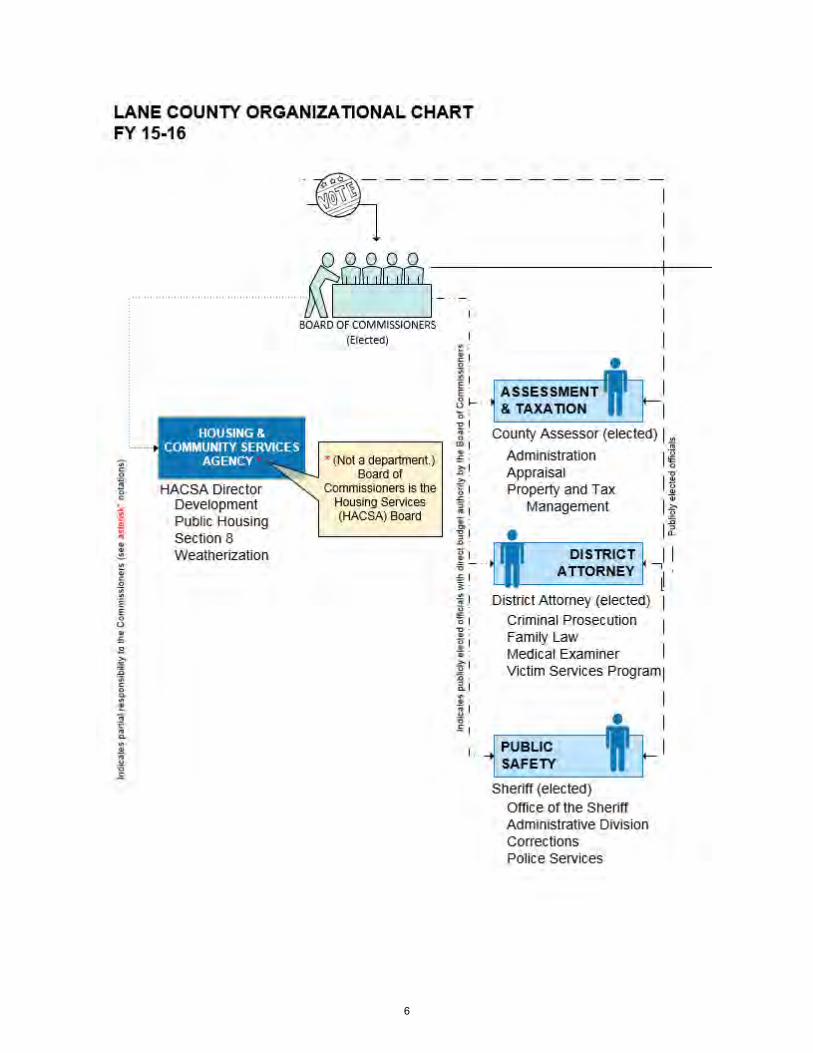

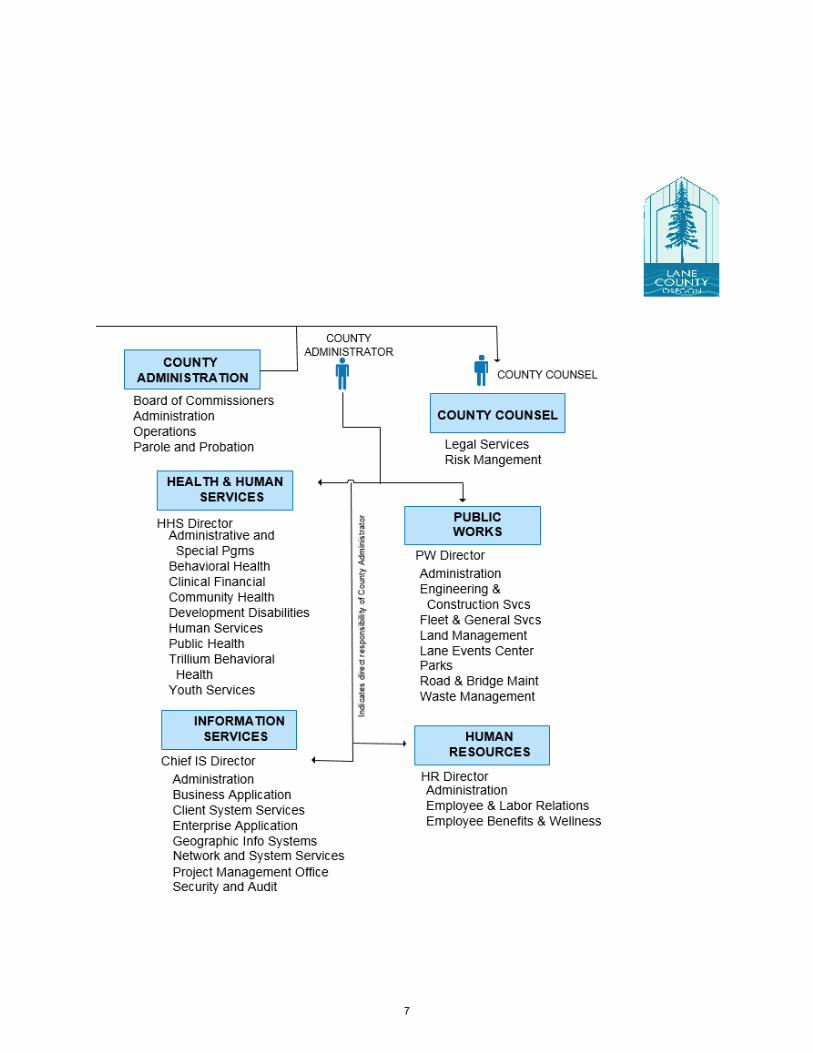

Letter of Transmittal 1 - 5Organizational Chart 6 - 7GFOA Certificate of Achievement 8Listing of Principal Officials 9

FINANCIAL SECTION

Report of Independent Auditor 11 - 13Management’s Discussion and Analysis 14 - 26

Basic Financial Statements:

Government-wide Financial Statements:Statement of Net Position 27Statement of Activities 28 - 29

Fund Financial Statements:Balance Sheet – Governmental Funds 30 - 31

Reconciliation of the Balance Sheet of Governmental Fundsto the Statement of Net Position 33

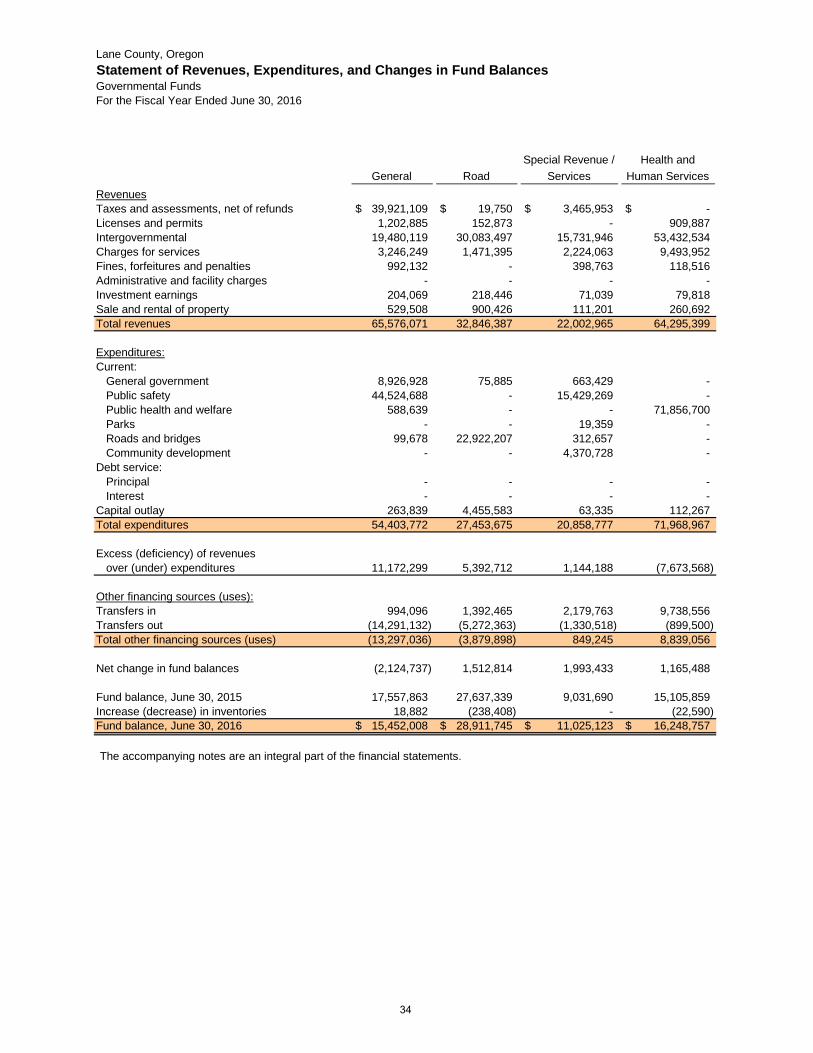

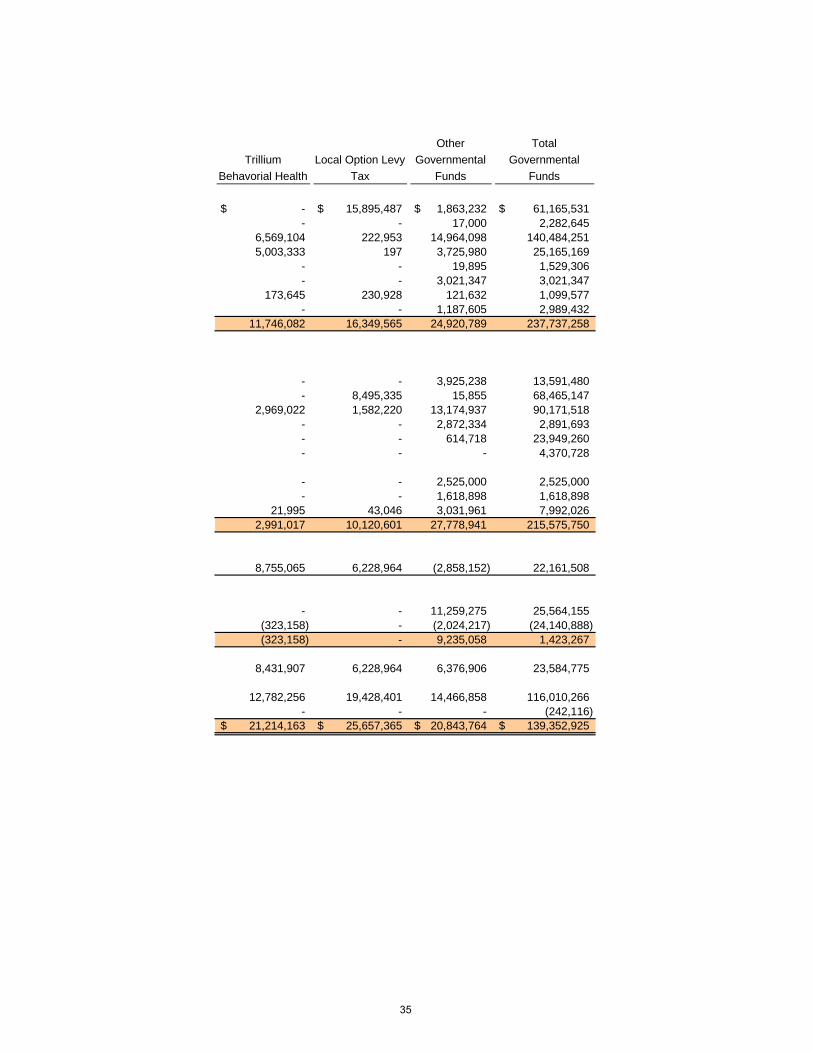

Statement of Revenues, Expenditures, and Changes in Fund Balances – Governmental Funds 34 - 35

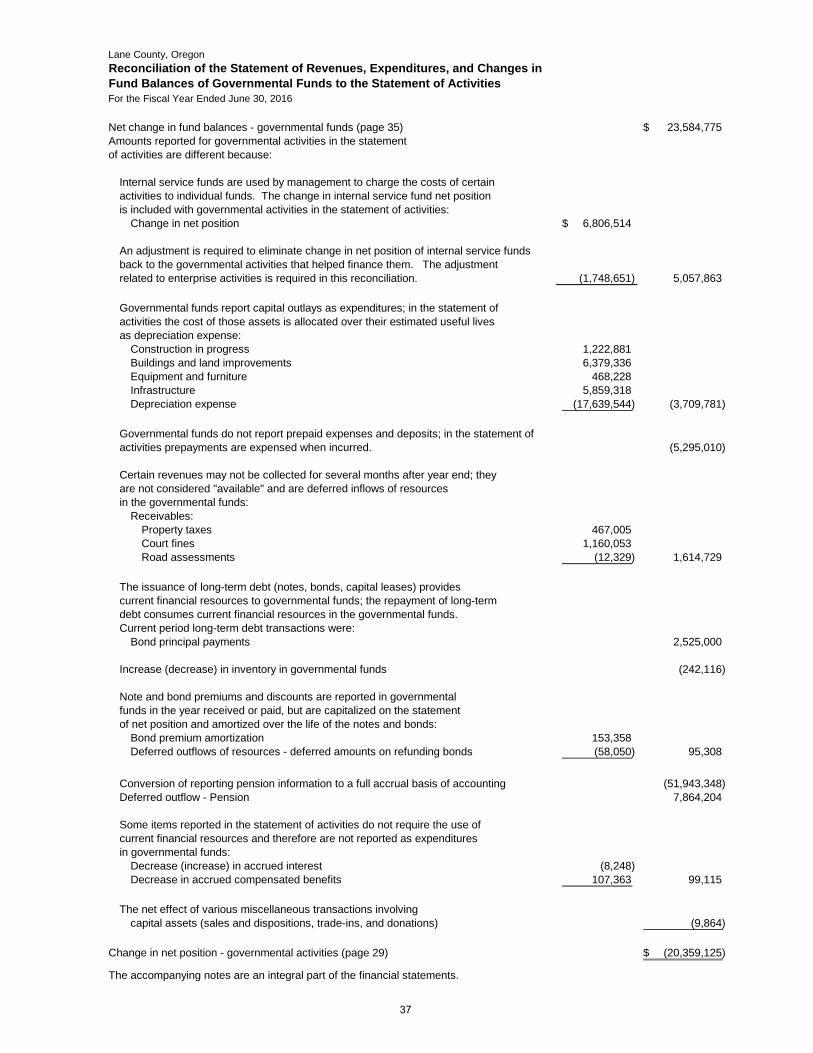

Reconciliation of the Statement of Revenues, Expenditures,and Changes in Fund Balances of Governmental Fundsto the Statement of Activities 37

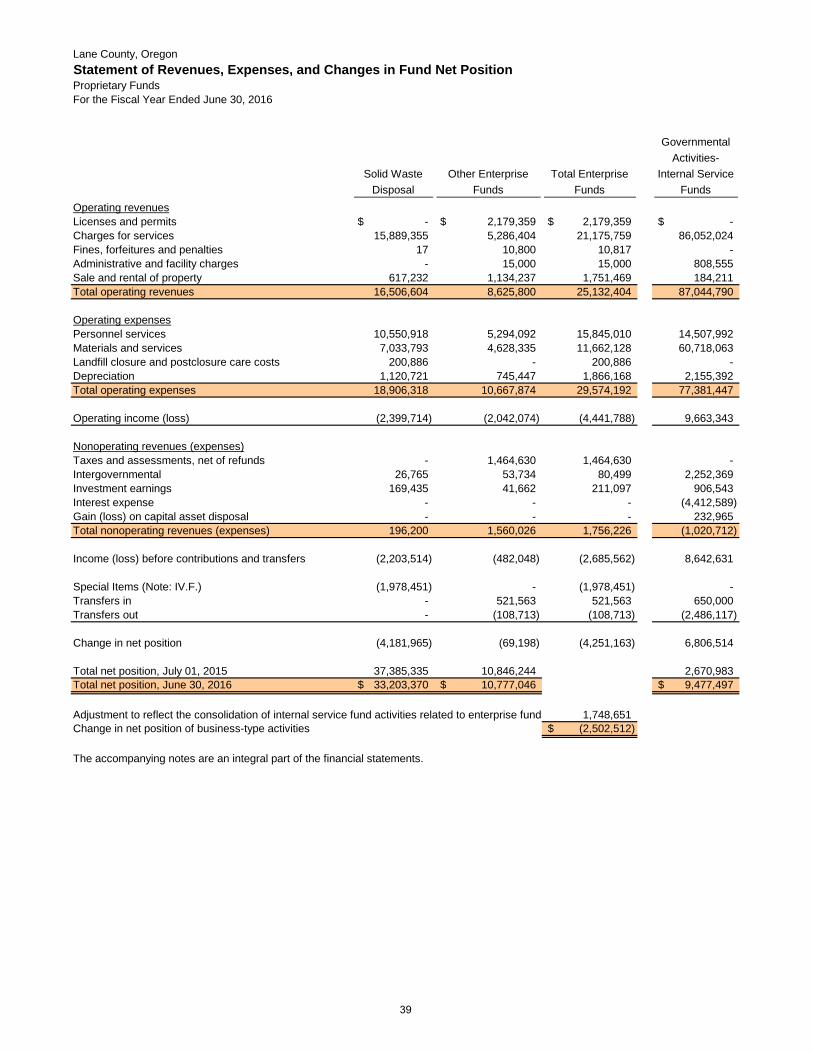

Statement of Fund Net Position – Proprietary Funds 38

Statement of Revenues, Expenses, and Changes in FundNet Position – Proprietary Funds 39

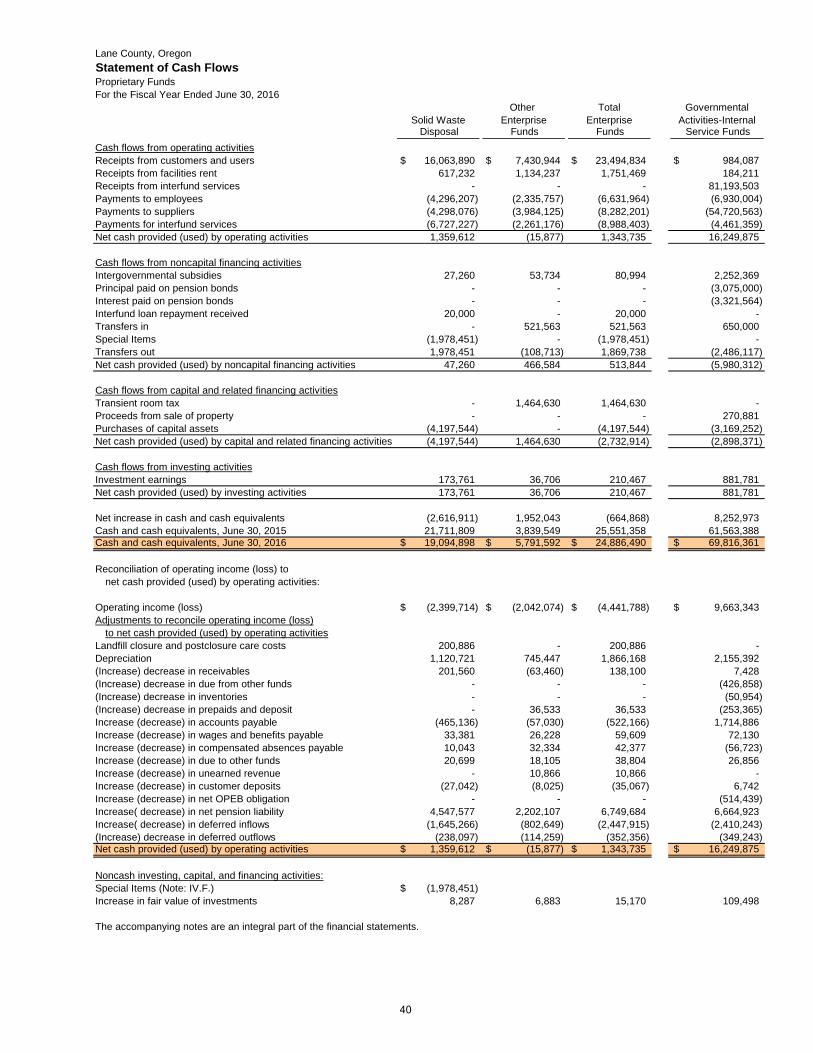

Statement of Cash Flows – Proprietary Funds 40

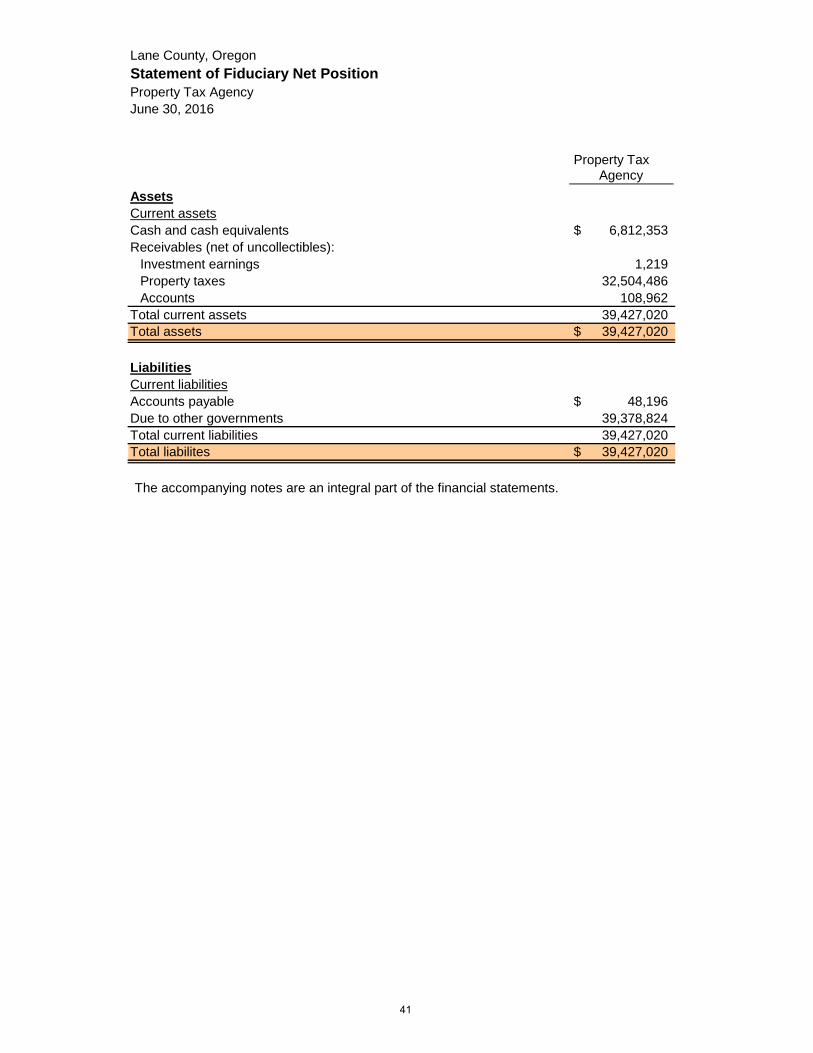

Statement of Fiduciary Net Position 41

Notes to Basic Financial Statements 43 - 89

Required Supplementary Information:Schedule of Revenues, Expenditures, and Changes in Fund

Balance – Budget and Actual:

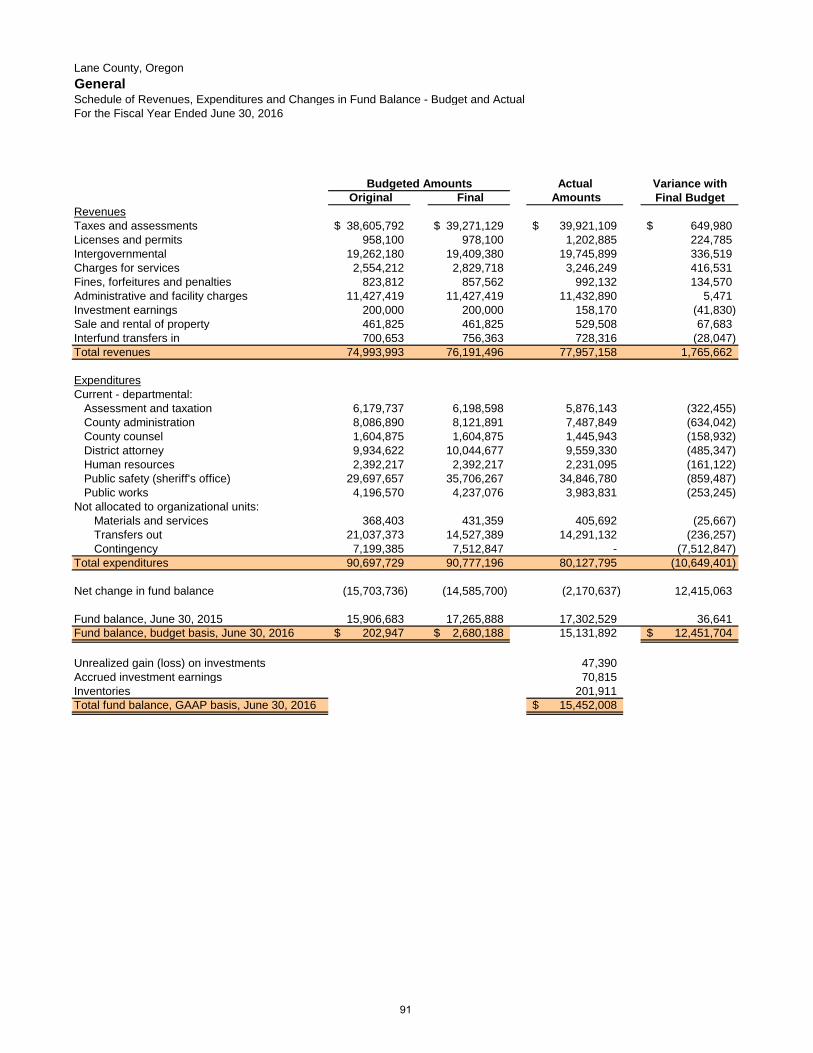

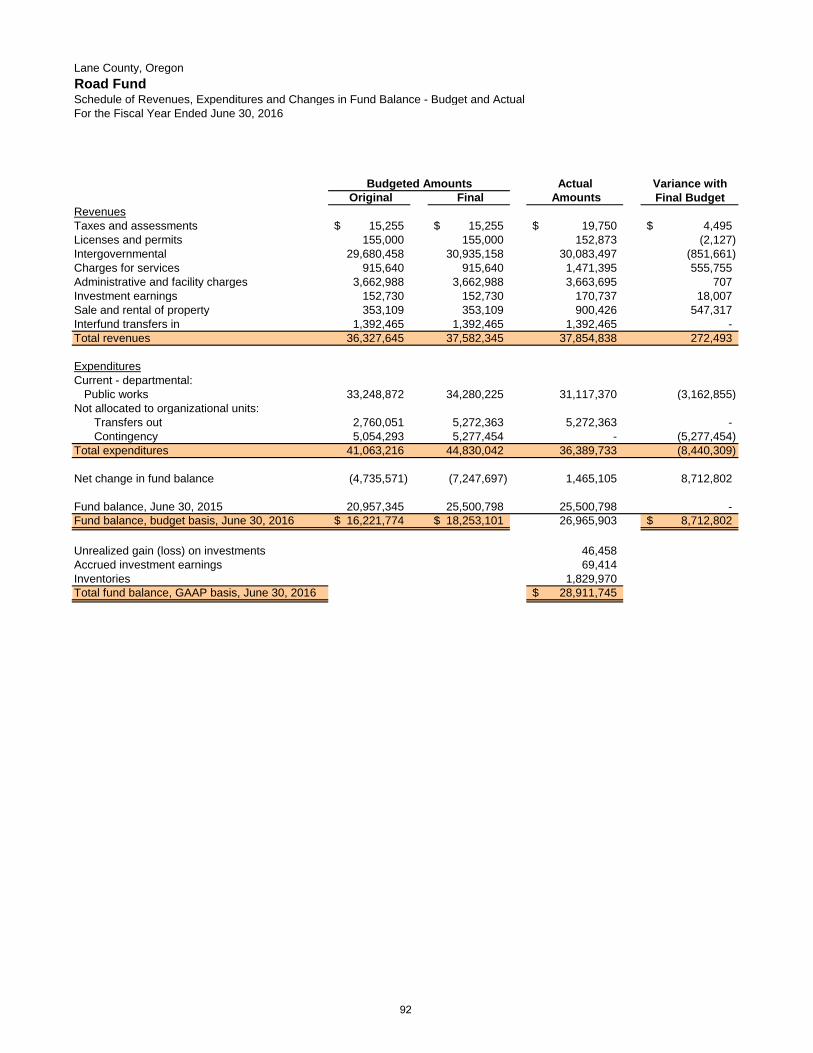

General Fund 91Road Fund 92Special Revenue / Services Fund 93Health and Human Services Fund 94Trillium Behavioral Health 95Local Option Tax Levy Fund 96

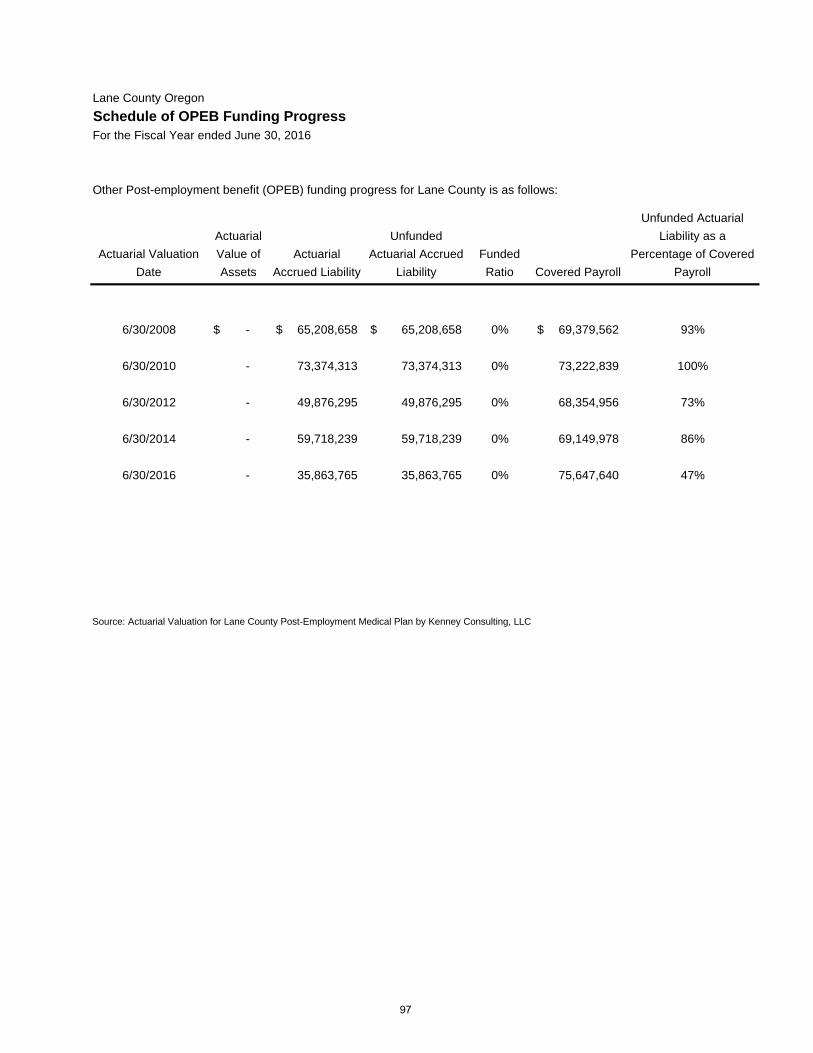

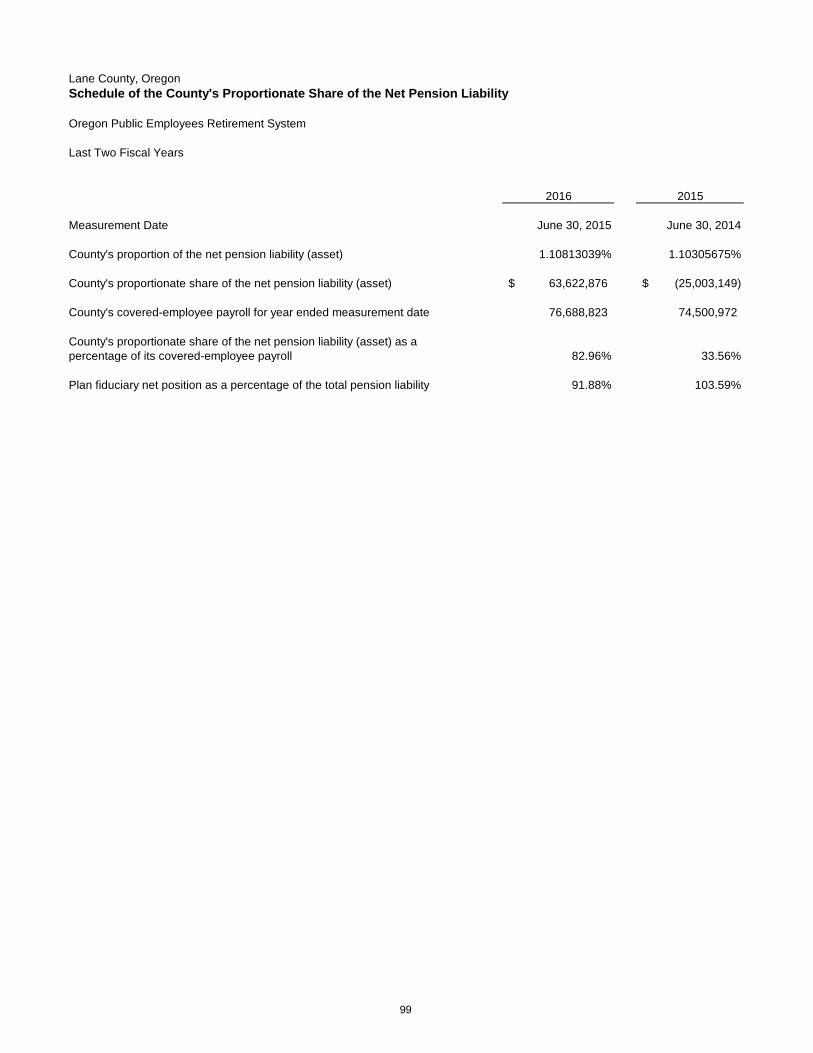

Schedule of OPEB Funding Progress 97Schedule of County Contributions 98Schedule of the County's Proportionate Share of the Net Pension Liability 99

Notes to Required Supplementary Information 100

Lane County, OregonLane County, OregonComprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2016

TABLE OF CONTENTS

i

FINANCIAL SECTION, continued: Page(s)

Other Supplementary Information:Nonmajor Governmental Funds Combining Statements:

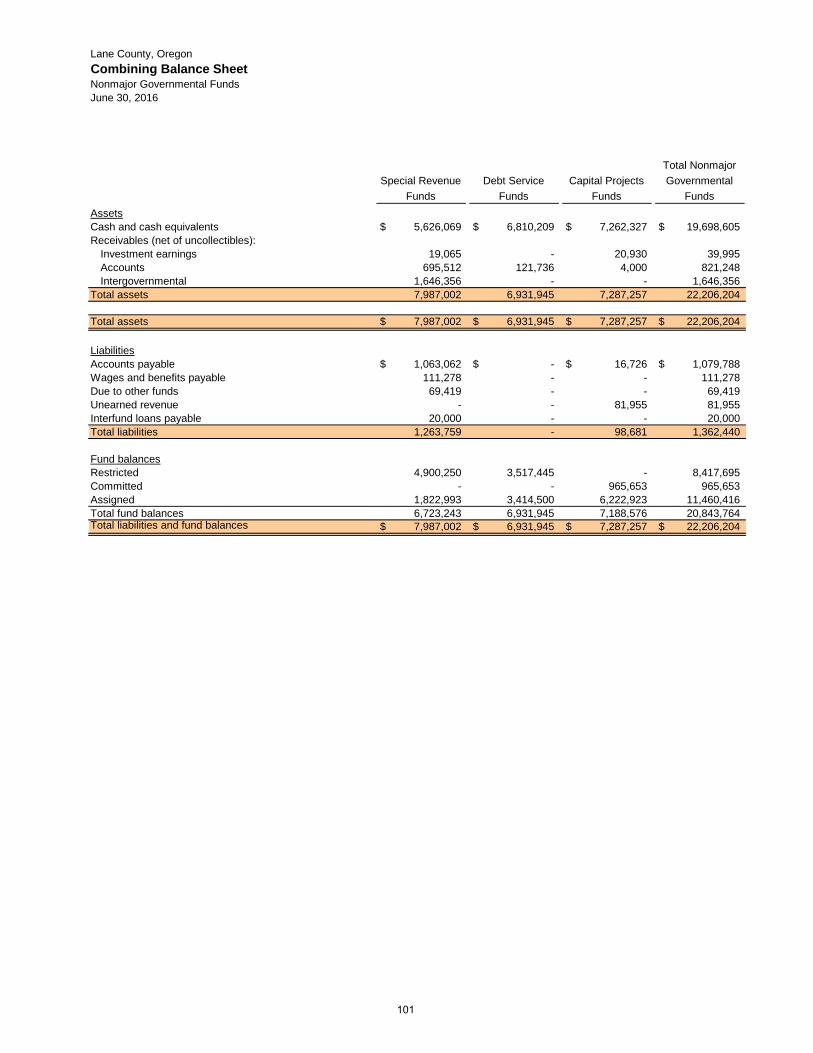

Combining Balance Sheet – Nonmajor Governmental Funds 101

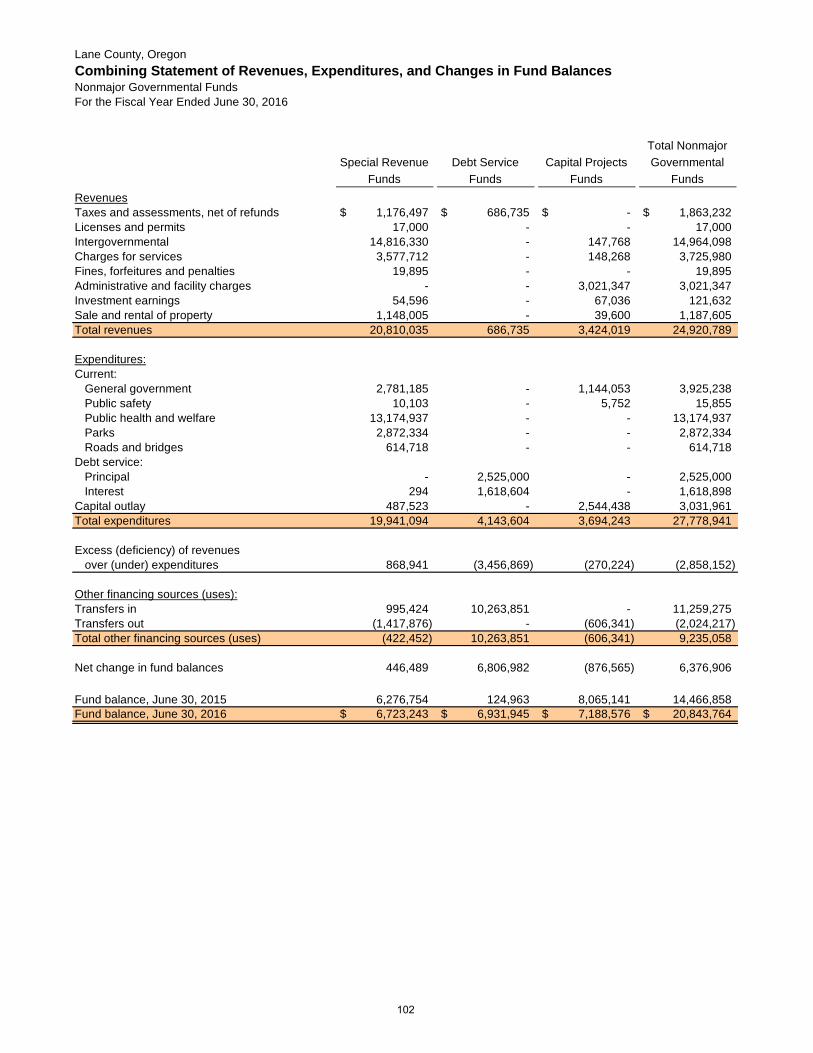

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances – Nonmajor Governmental Funds 102

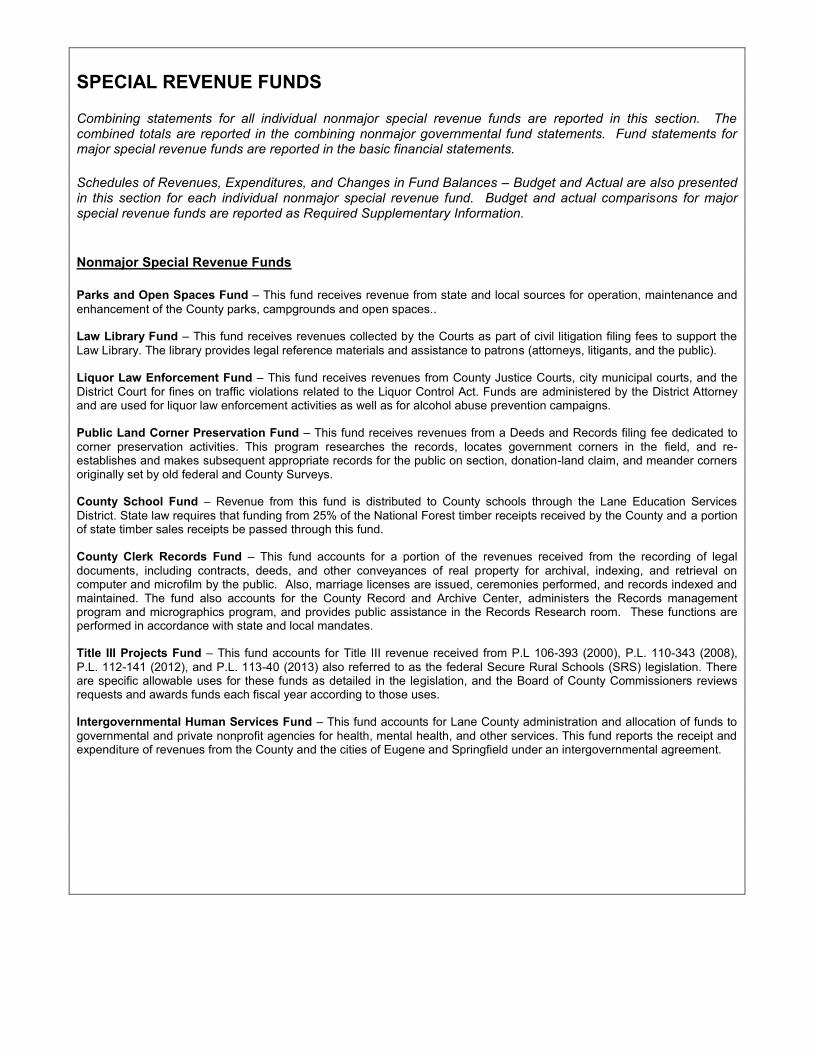

Special Revenue Funds:

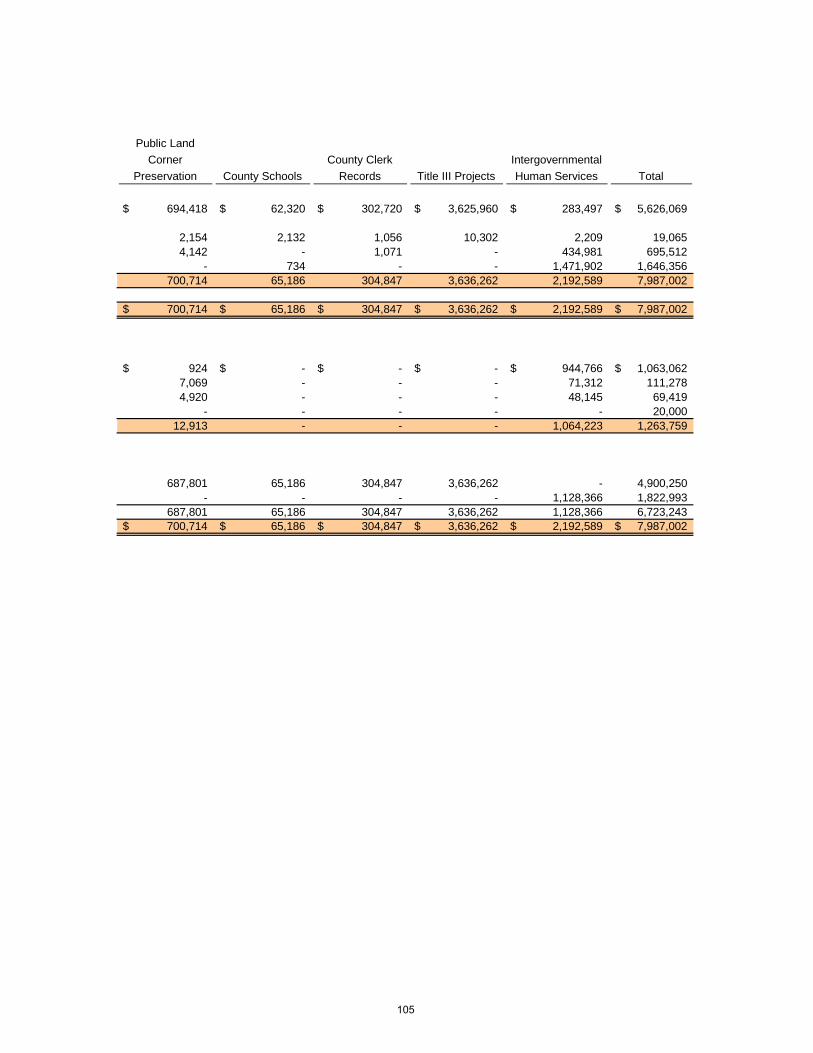

Combining Balance Sheet – Nonmajor Special Revenue Funds 104 - 105

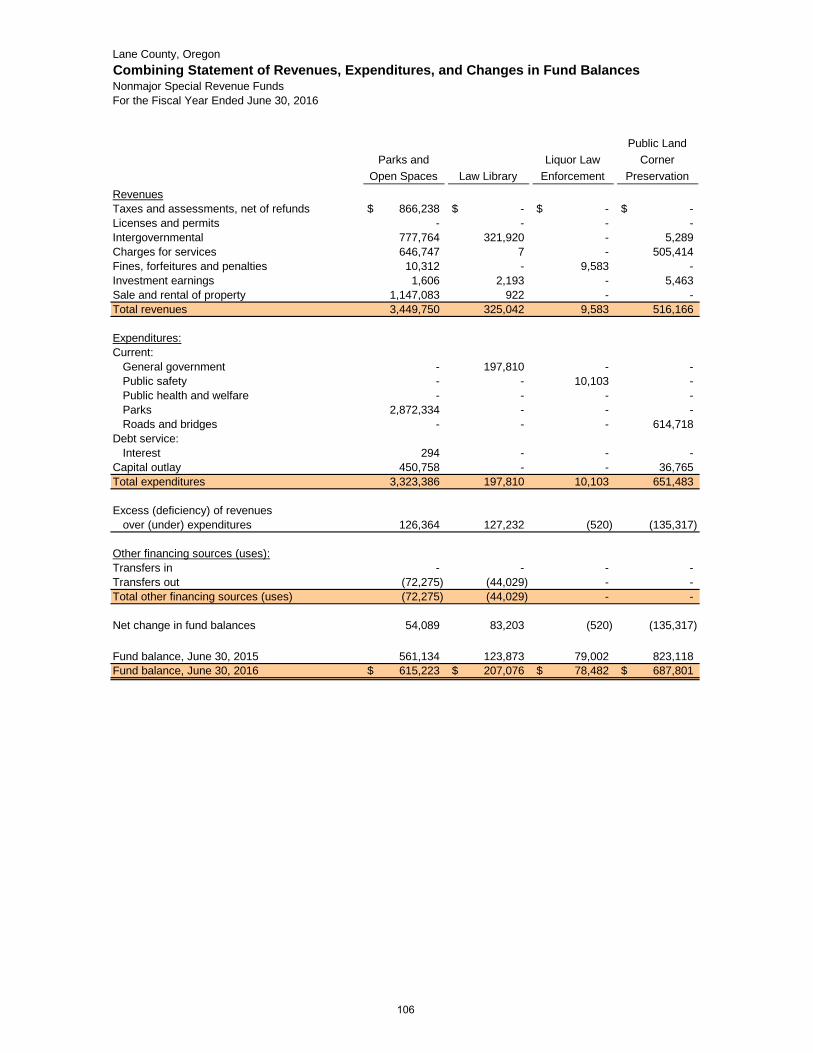

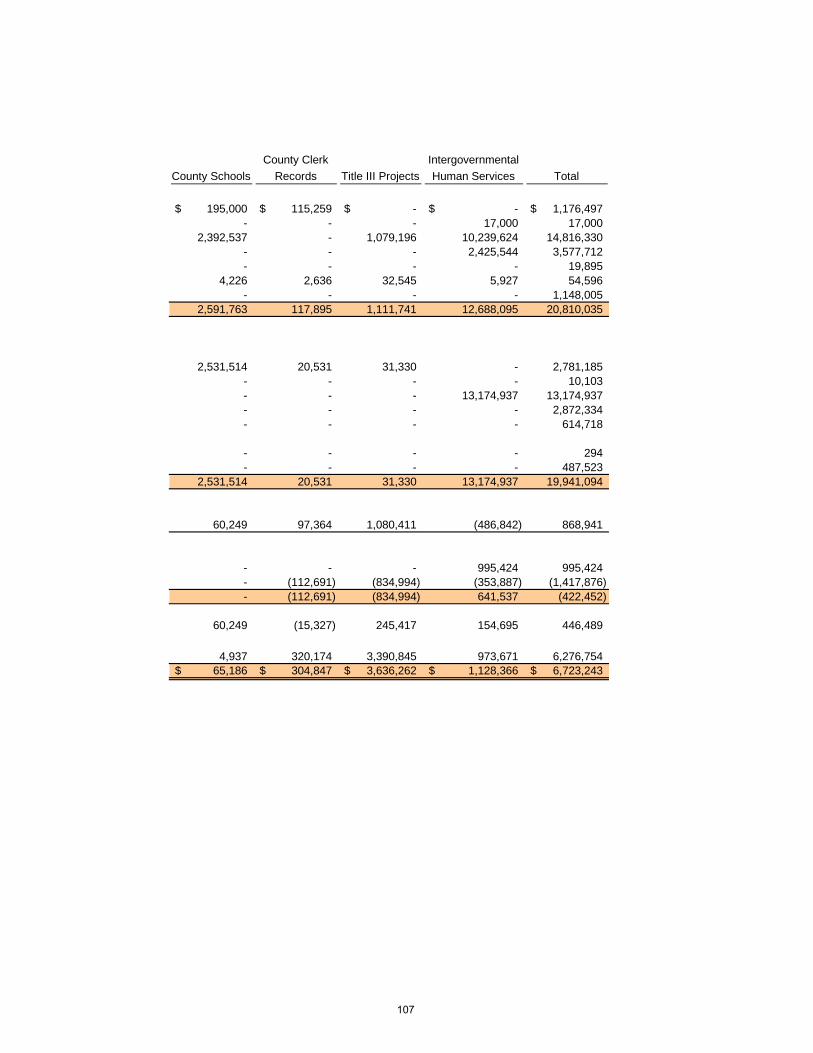

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances – Nonmajor Special Revenue Funds 106 - 107

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual:

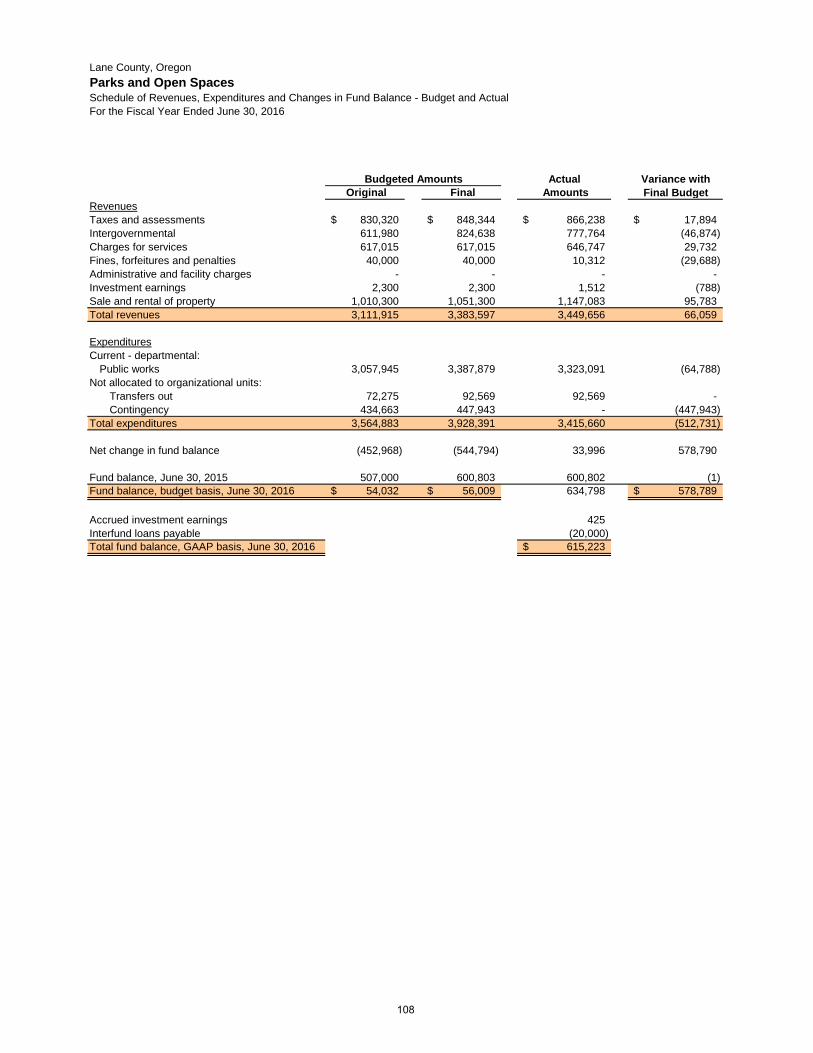

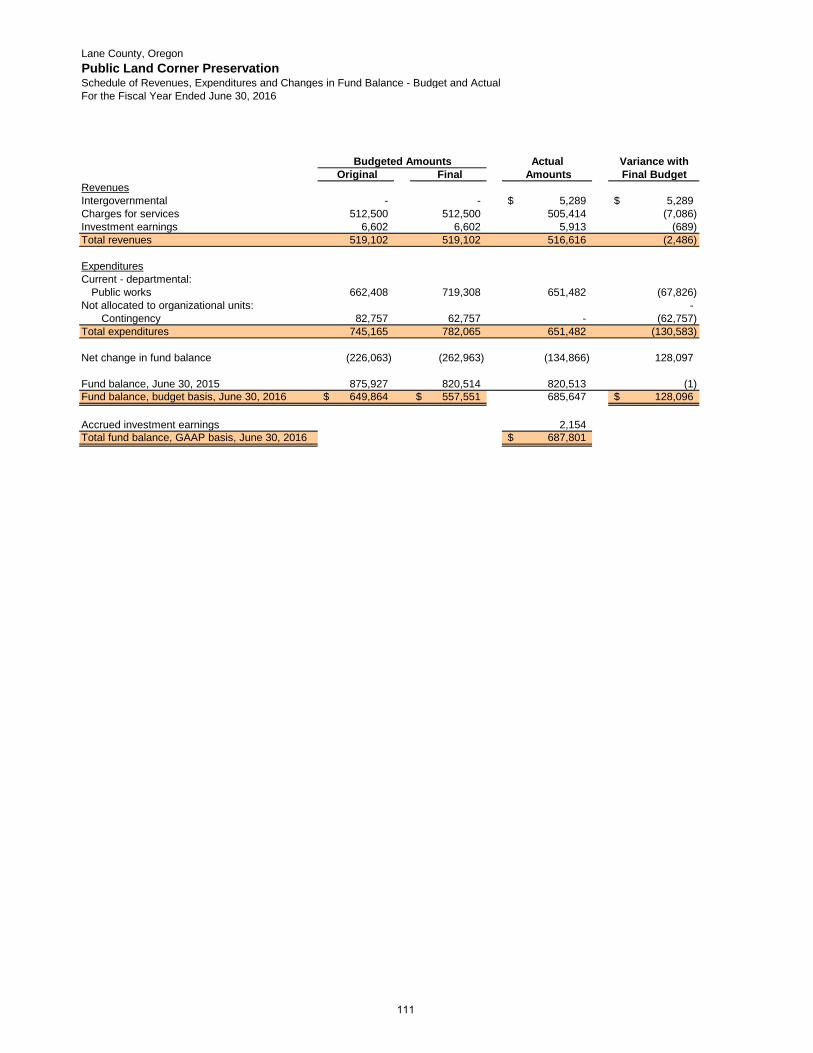

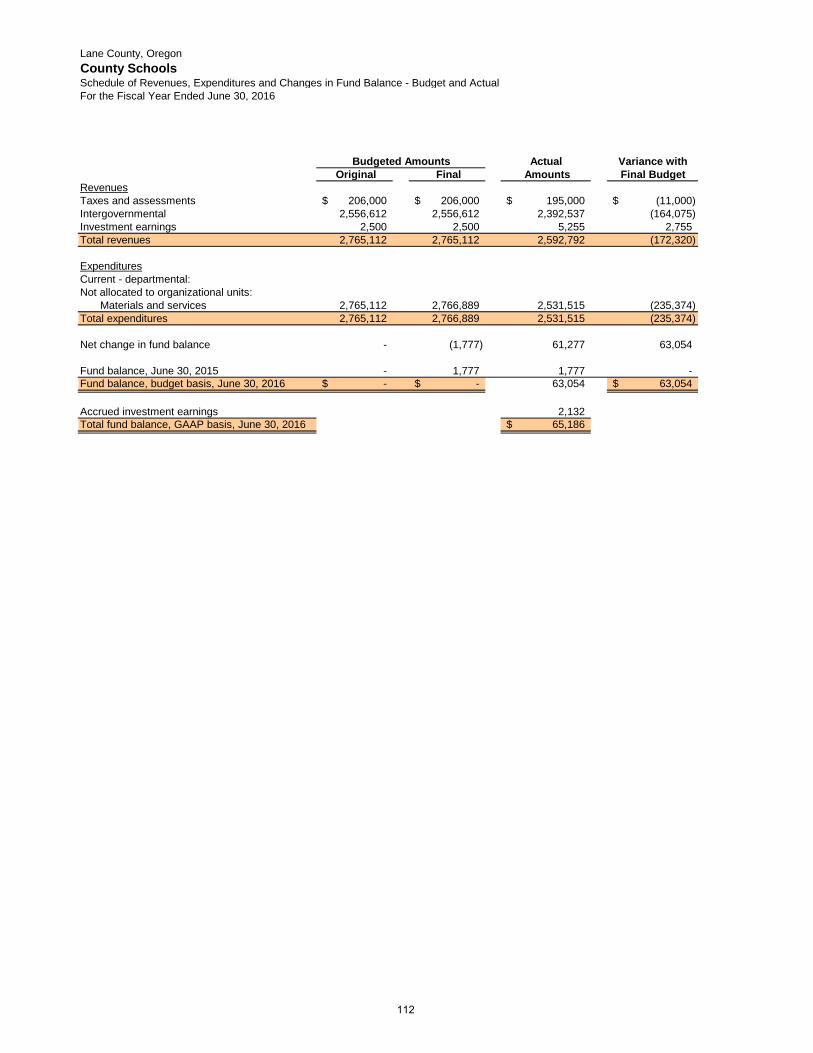

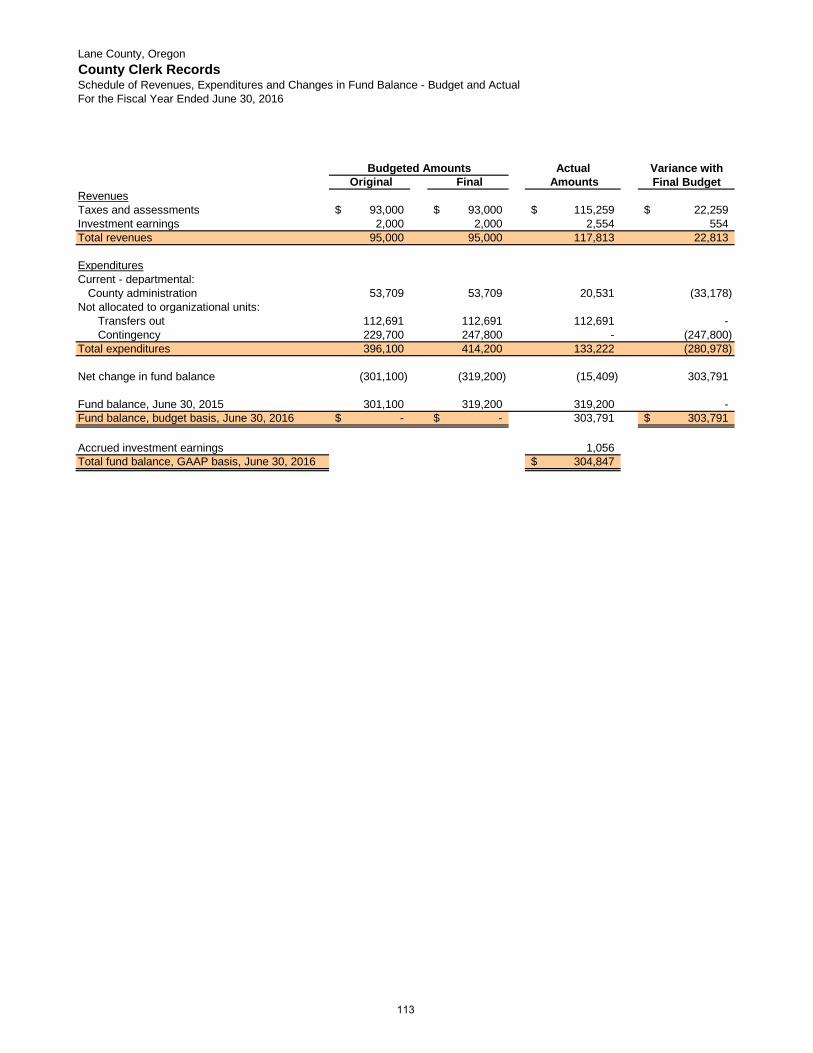

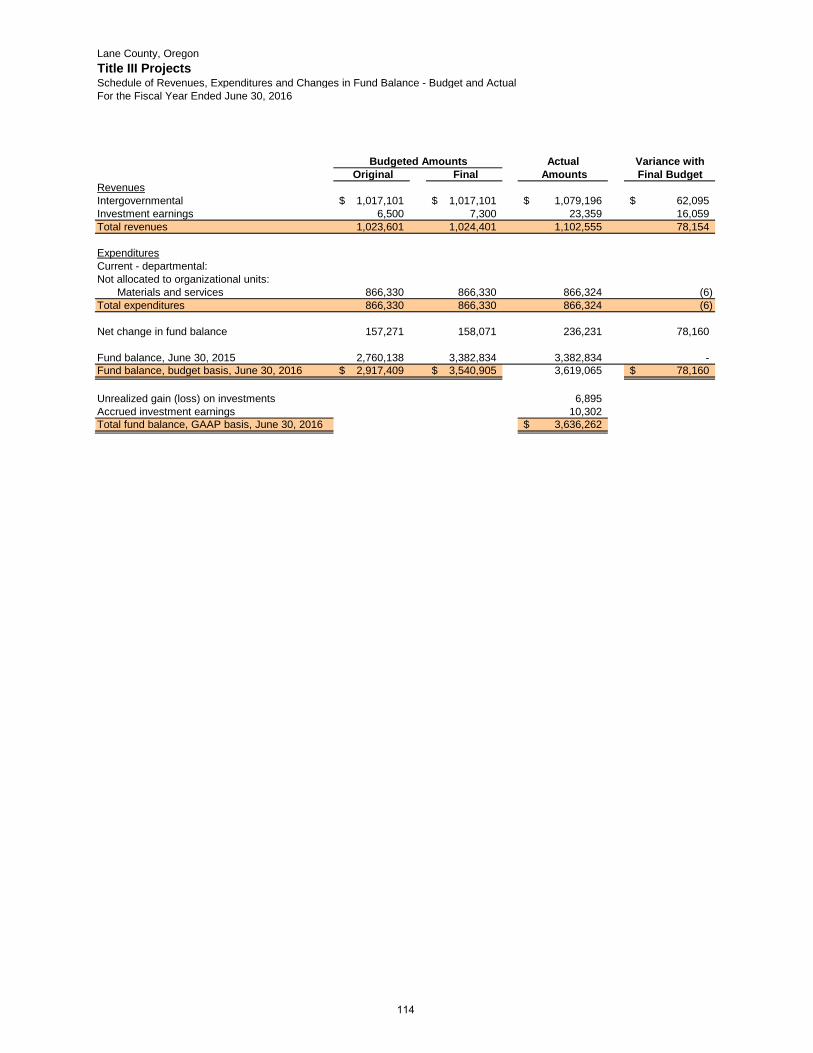

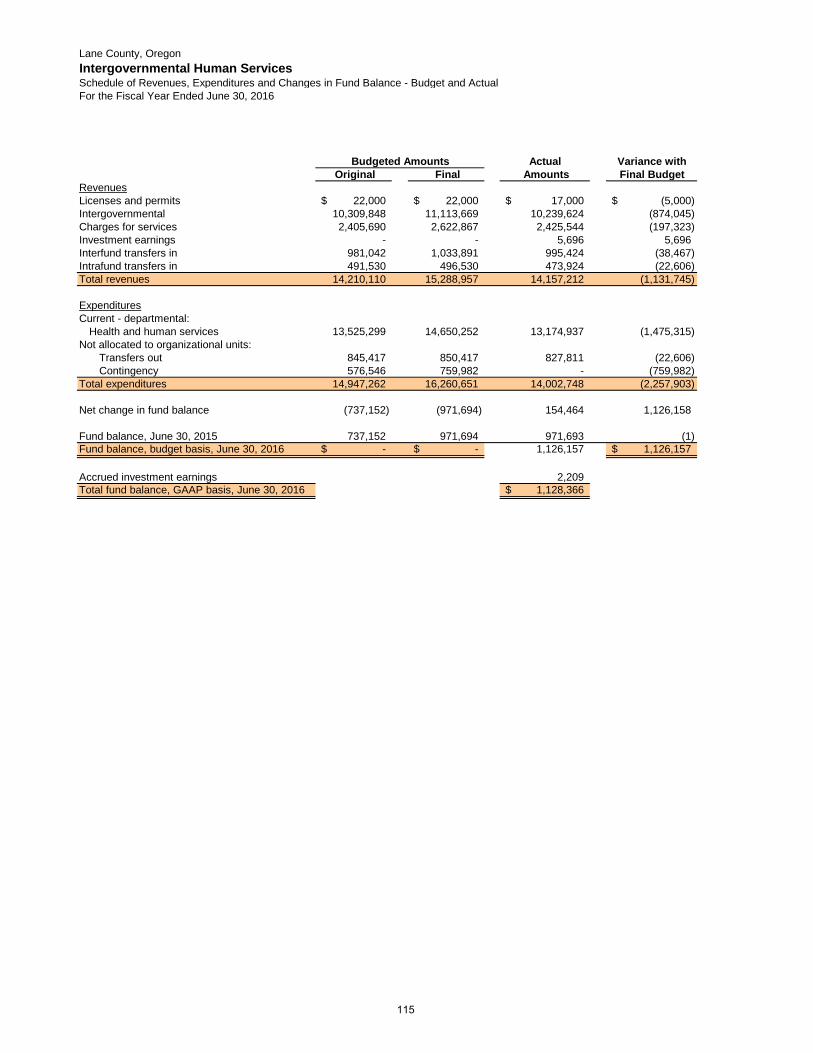

Parks and Open Spaces Fund 108Law Library Fund 109Liquor Law Enforcement Fund 110Public Land Corner Preservation Fund 111County Schools Fund 112County Clerk Records Fund 113Title III Projects Fund 114Intergovernmental Human Services Fund 115

Debt Service Funds:

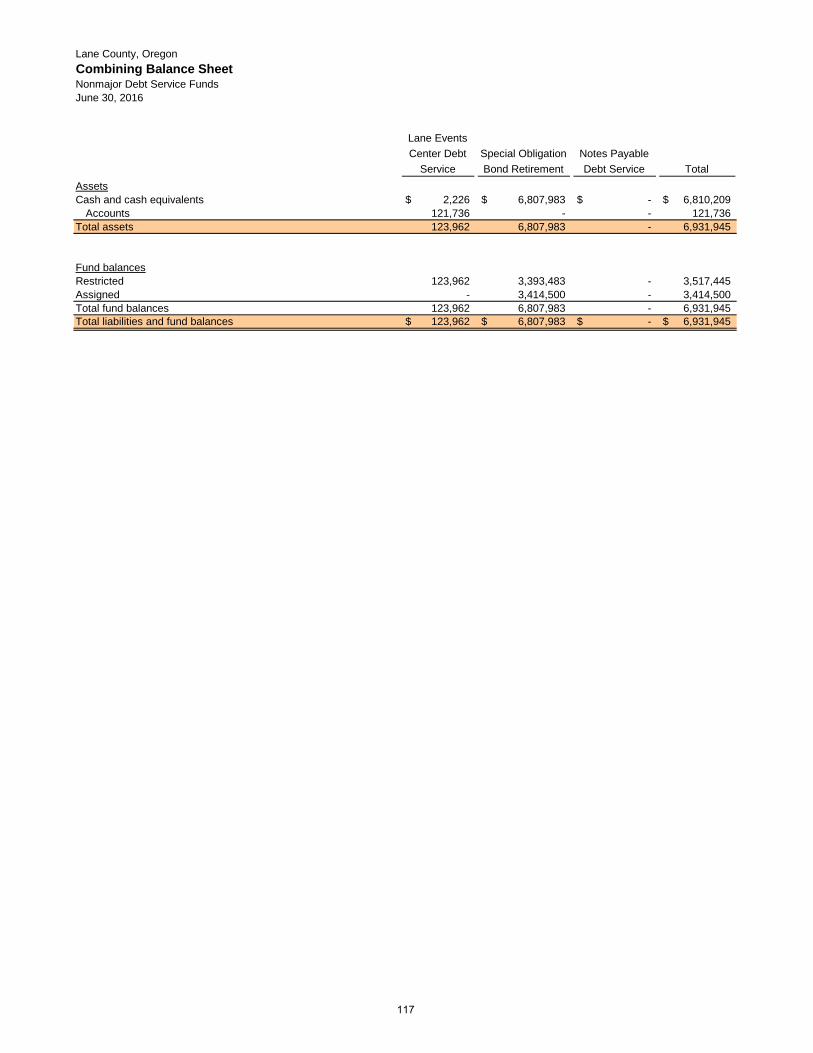

Combining Balance Sheet – Nonmajor Debt Service Funds 117

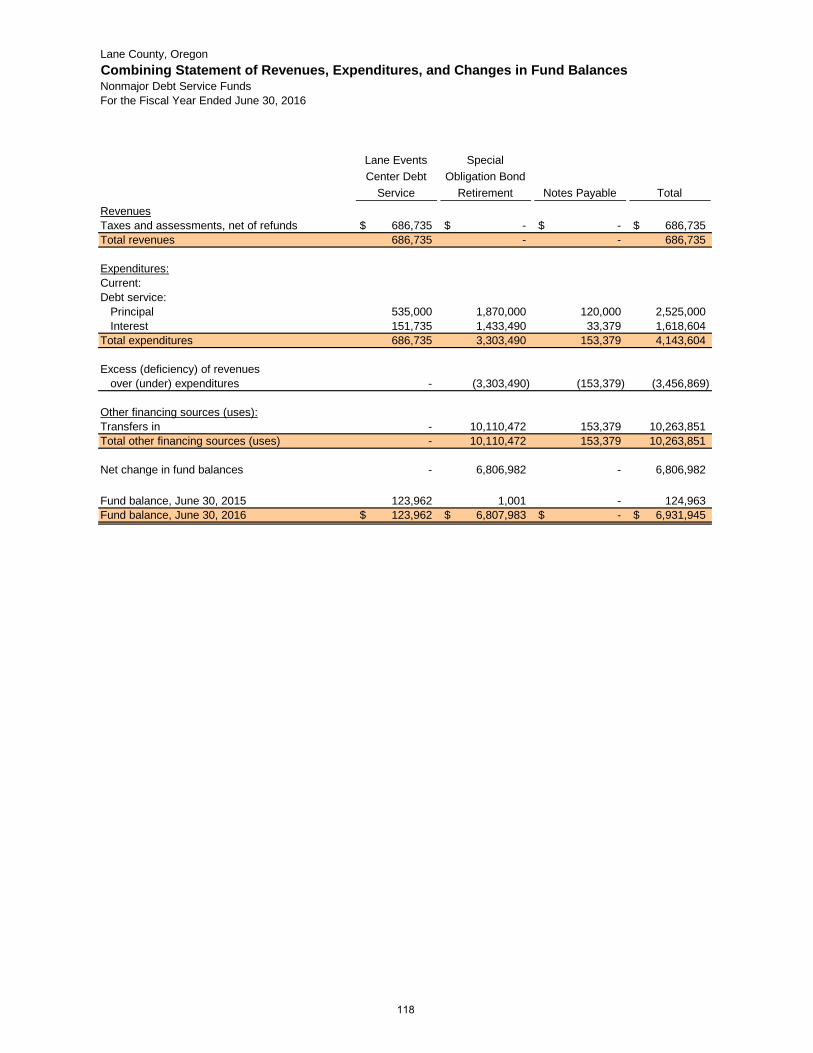

Combining Statement of Revenues, Expenditures, and Changes inFund Balances – Nonmajor Debt Service Funds 118

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual:

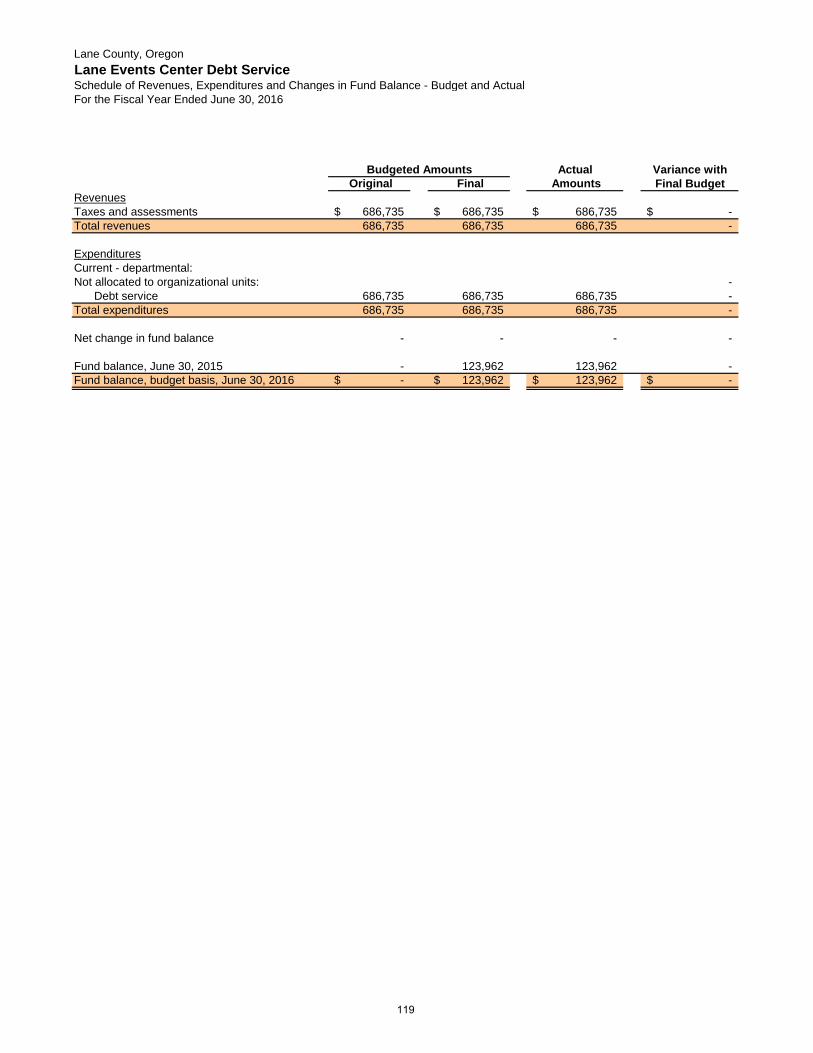

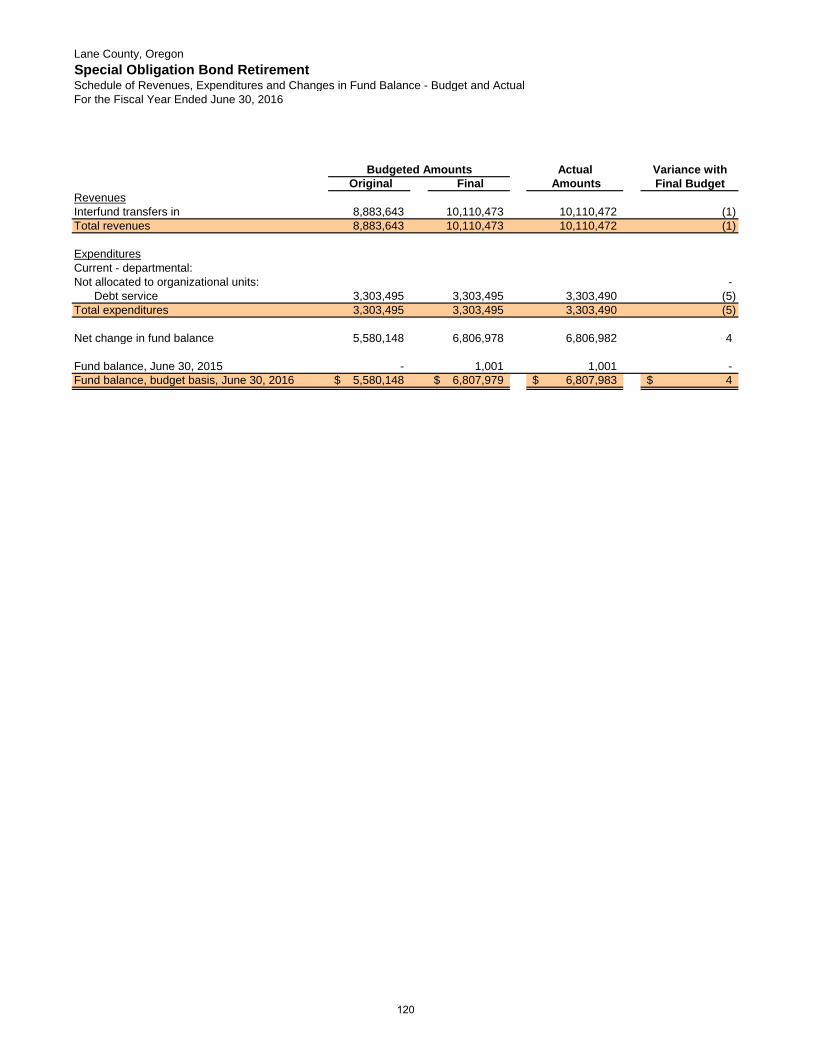

Lane Events Center Debt Service Fund 119Special Obligation Bond Retirement Fund 120Notes Payable Debt Service Fund 121

Capital Projects Funds:

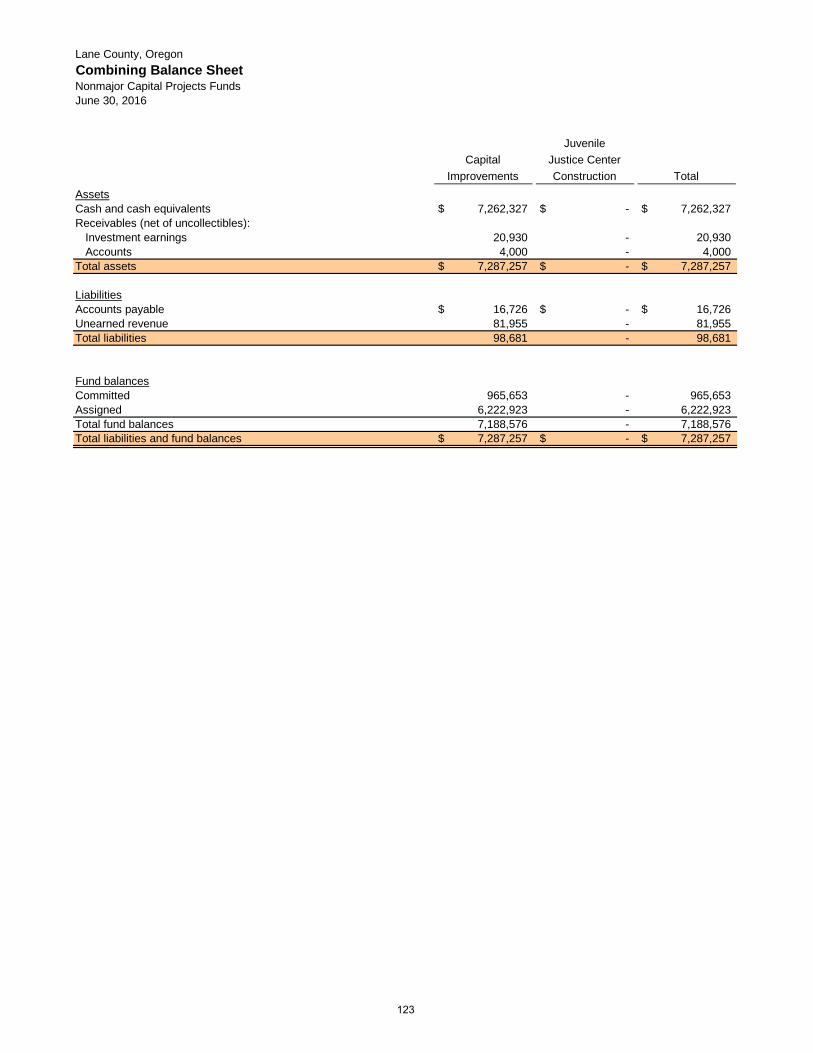

Combining Balance Sheet – Nonmajor Capital Projects Funds 123

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances – Nonmajor Capital Projects Funds 124

Lane County, OregonComprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2016

Table of Contents, Continued

ii

Lane County, OregonComprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2016

Table of Contents, Continued

FINANCIAL SECTION, continued: Page(s)

Other Supplementary Information, continued:Capital Projects Funds, continued:

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual:

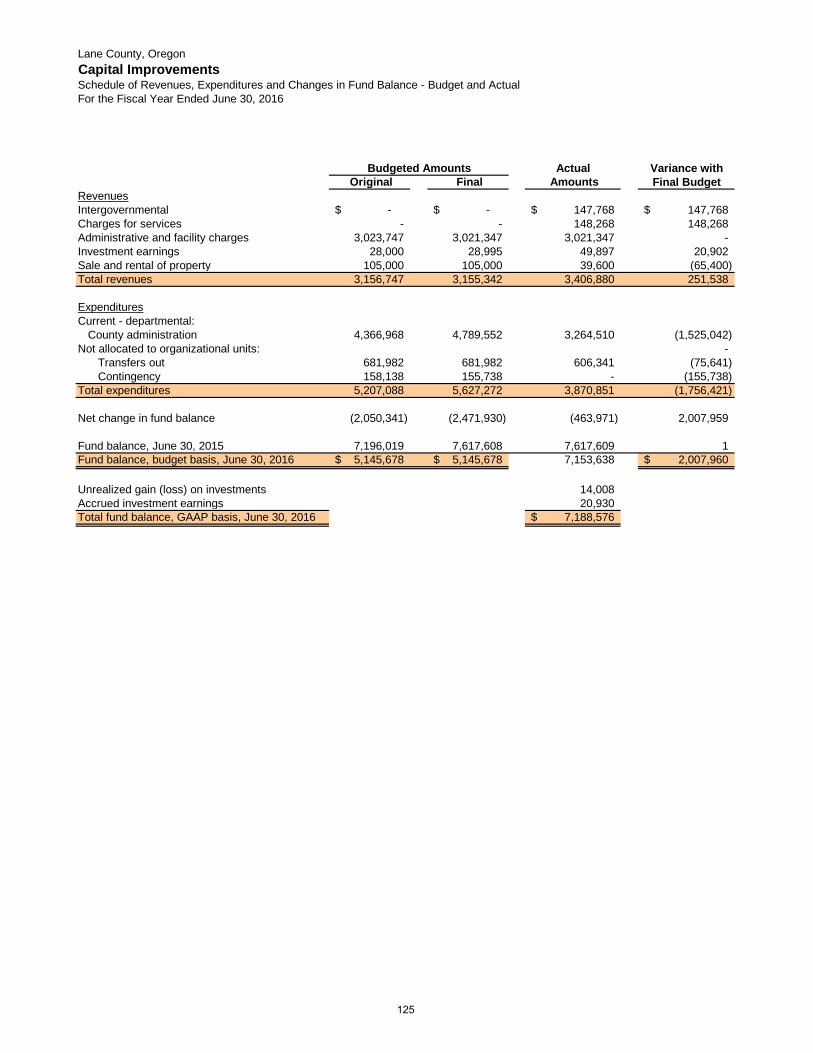

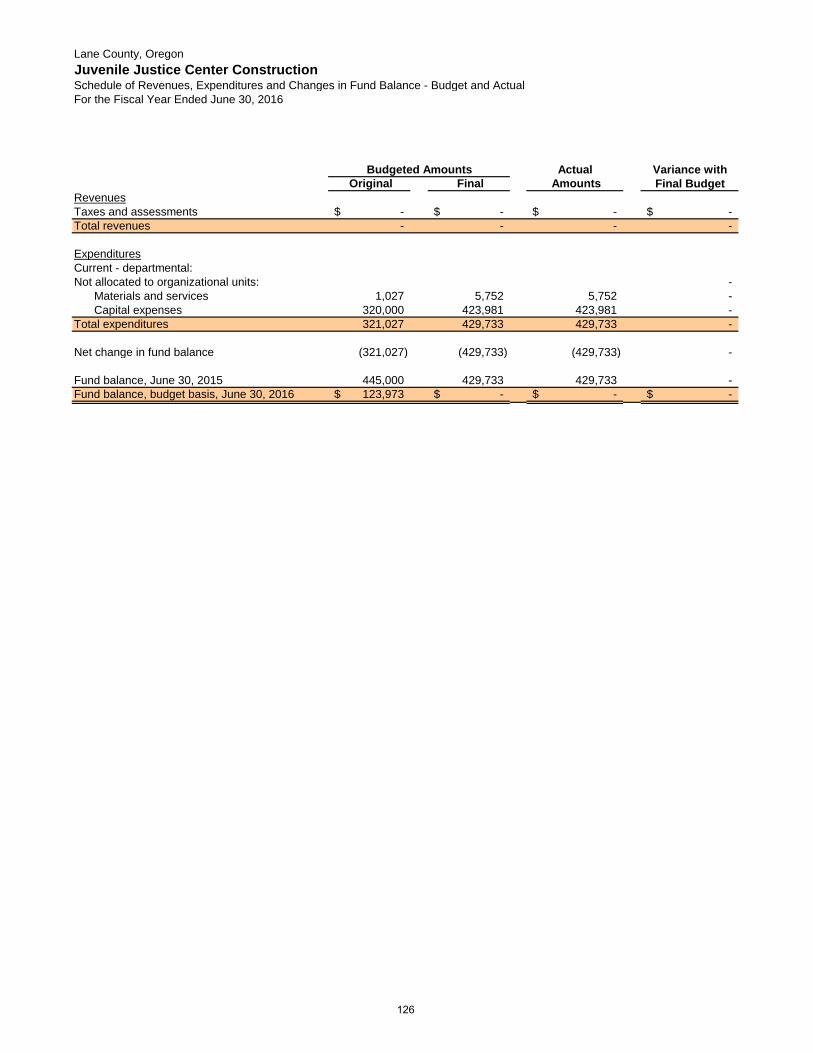

Capital Improvements Fund 125Juvenile Justice Center Construction Fund 126

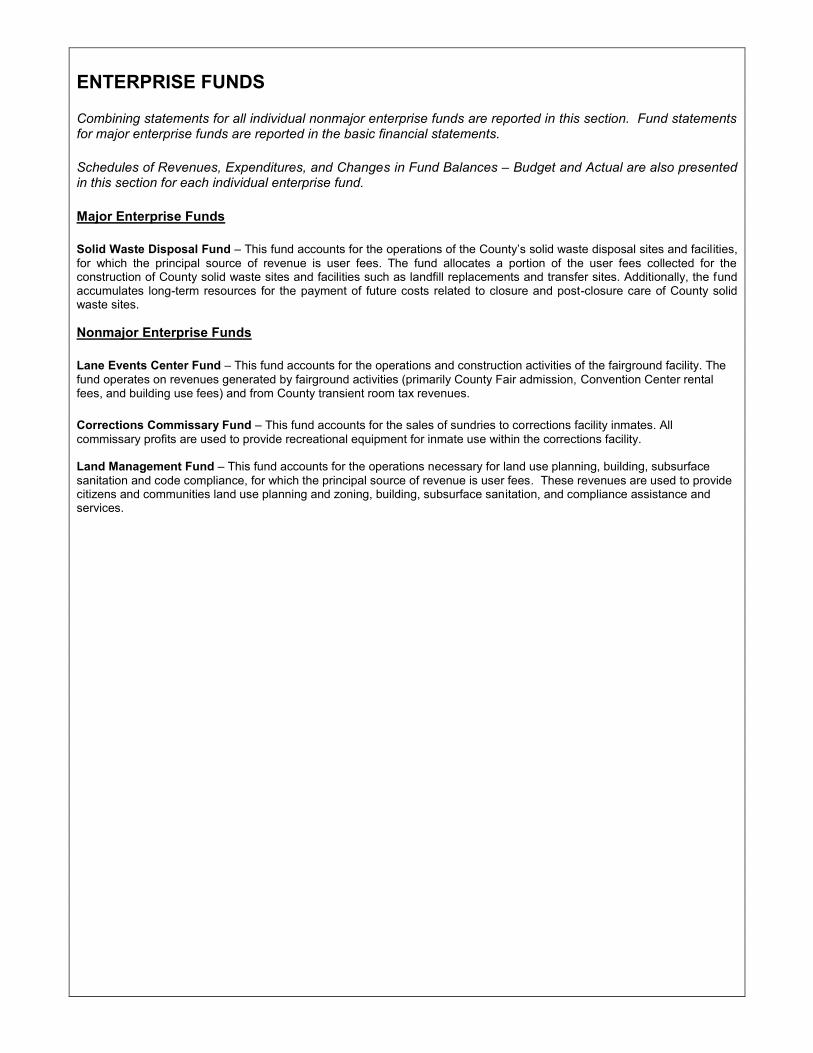

Enterprise Funds:

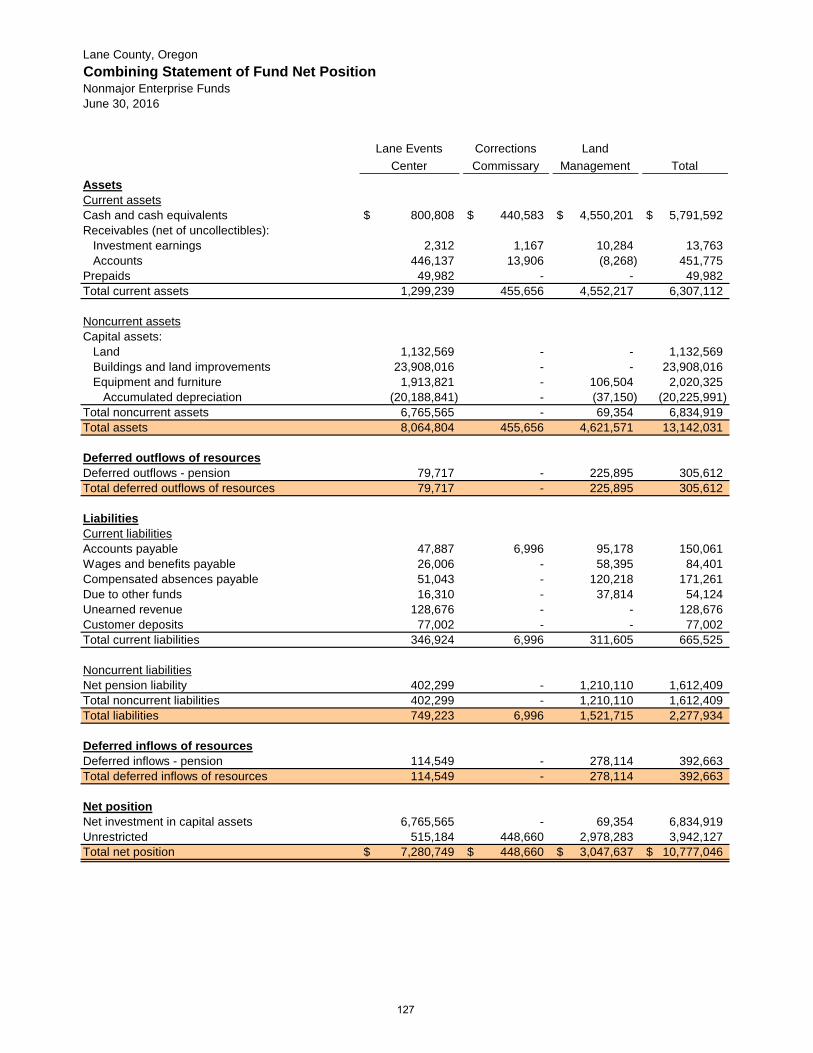

Combining Statement of Fund Net Position – Nonmajor Enterprise Funds 127

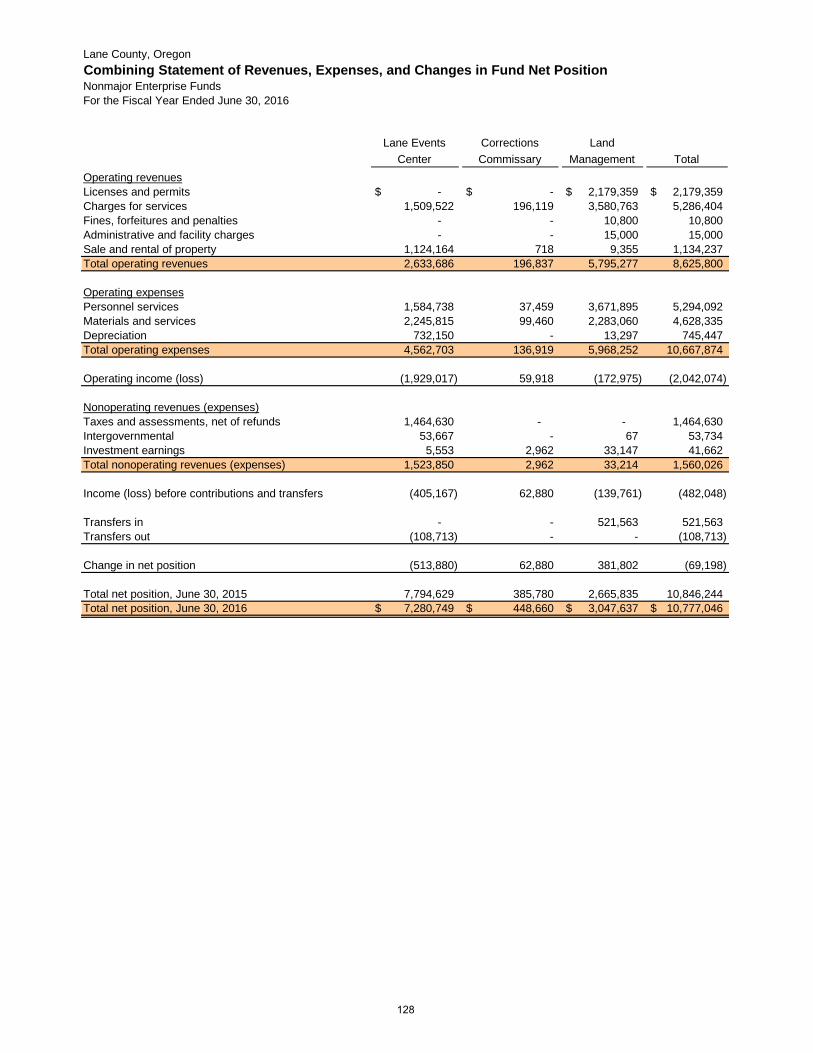

Combining Statement of Revenues, Expenses, and Changes in Fund Net Position – Nonmajor Enterprise Funds 128

Combining Statement of Cash Flows – Nonmajor Enterprise Funds 129

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual:

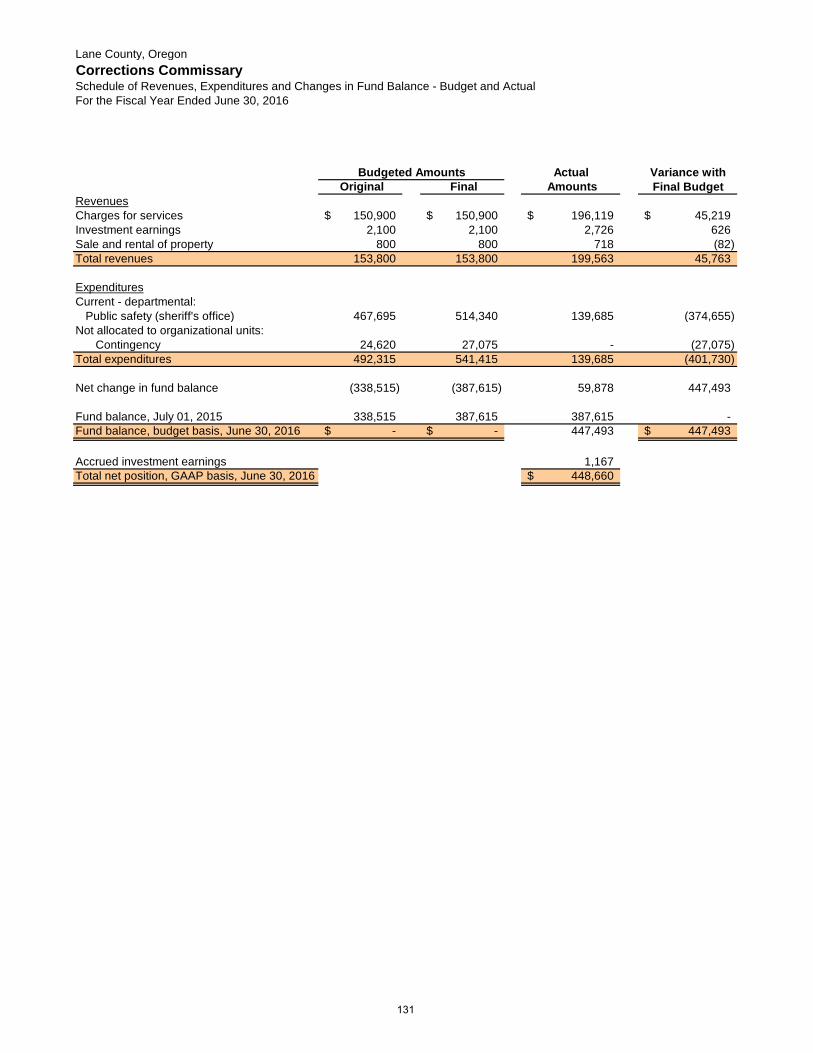

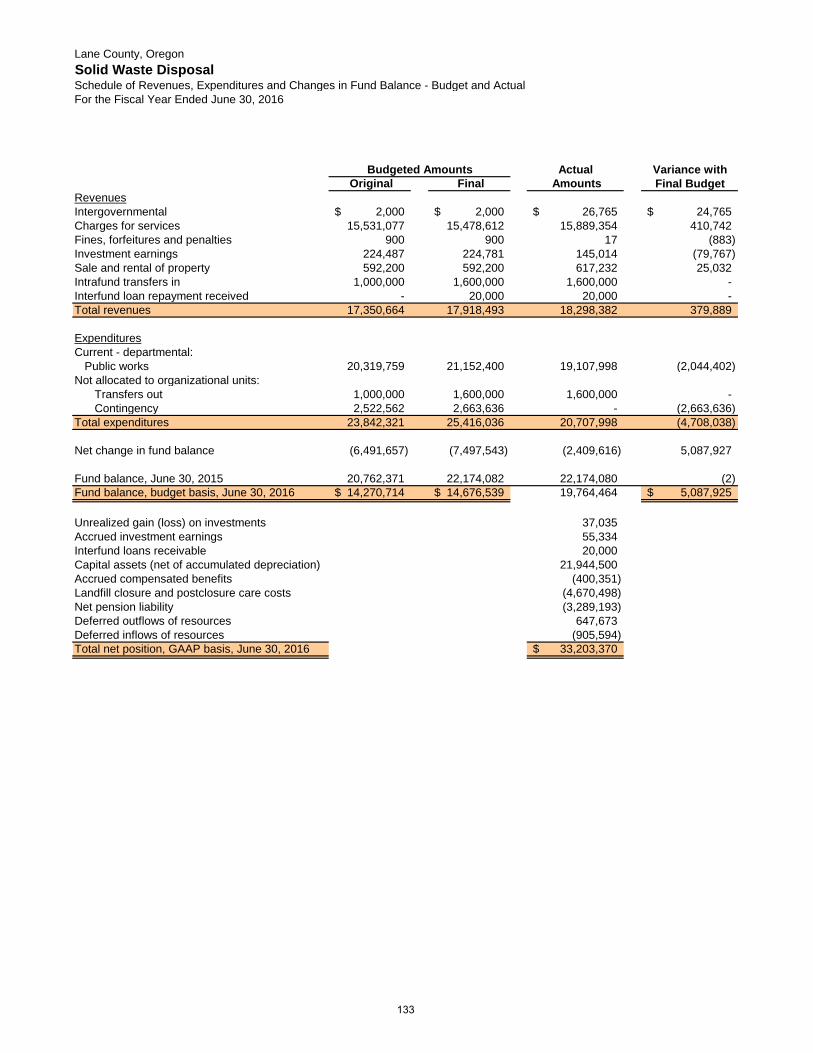

Lane Events Center Fund 130Corrections Commissary Fund 131Land Management Fund 132Solid Waste Disposal Fund 133

Internal Service Funds:

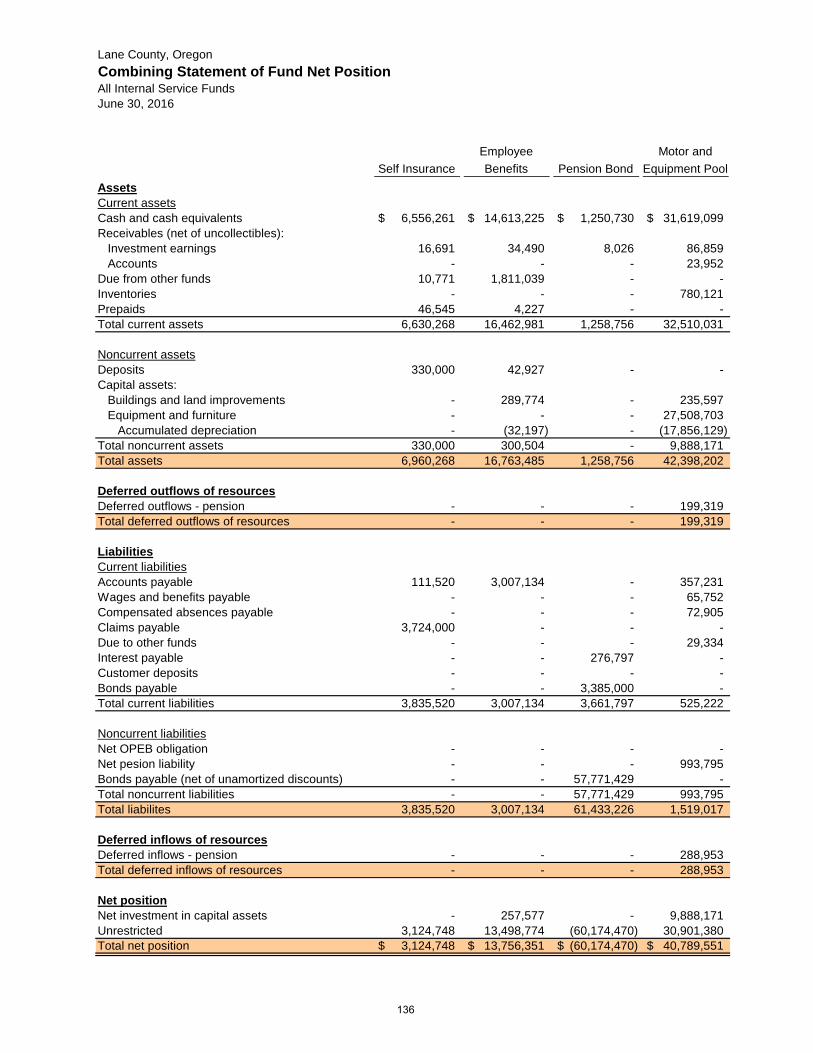

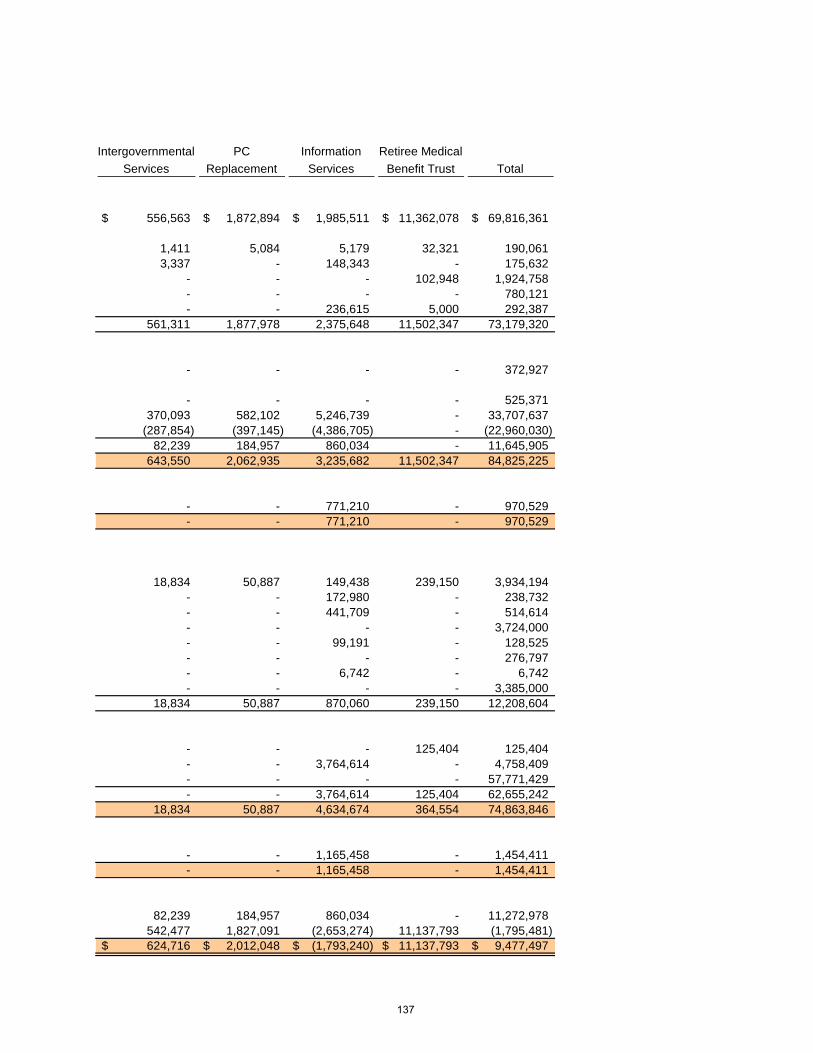

Combining Statement of Fund Net Position – All Internal Service Funds 136 - 137

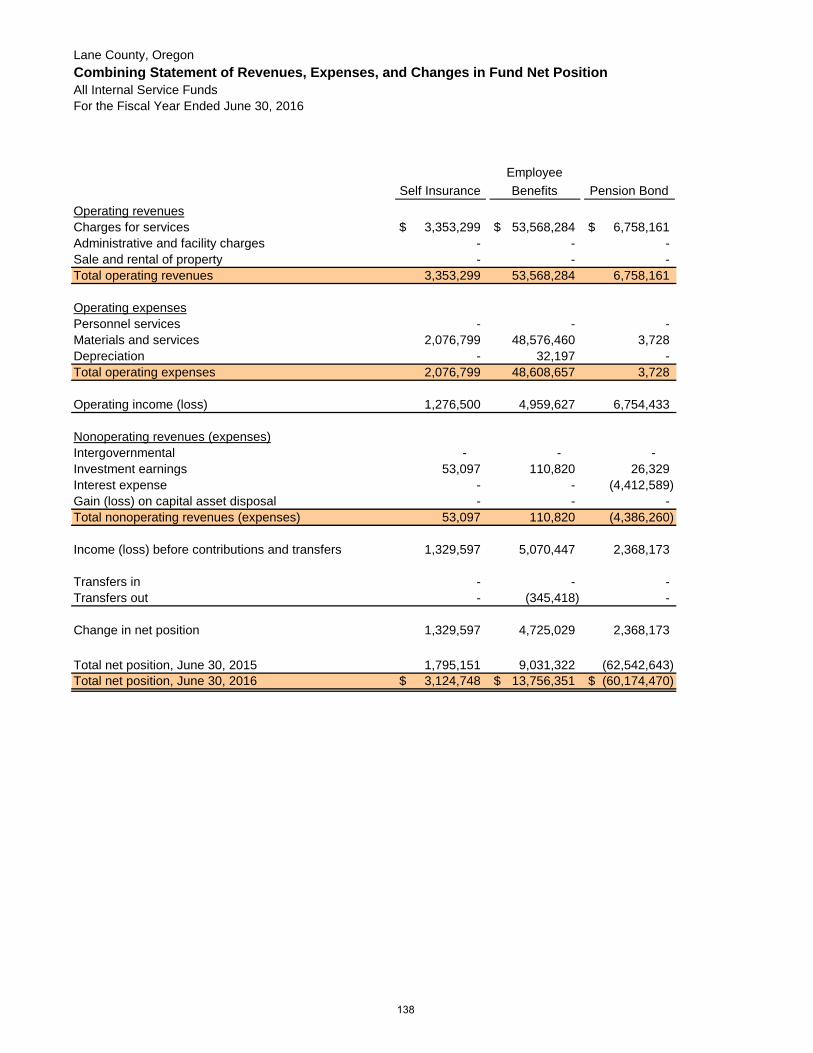

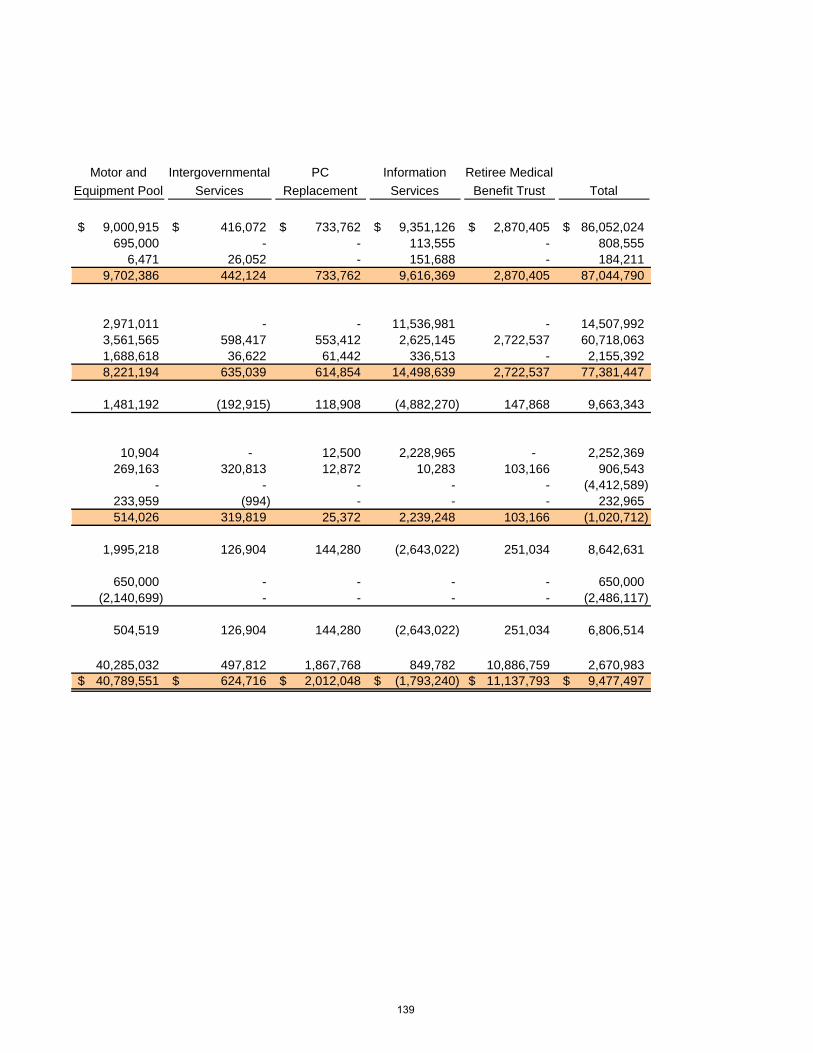

Combining Statement of Revenues, Expenses, and Changes in Fund Net Position – All Internal Service Funds 138 - 139

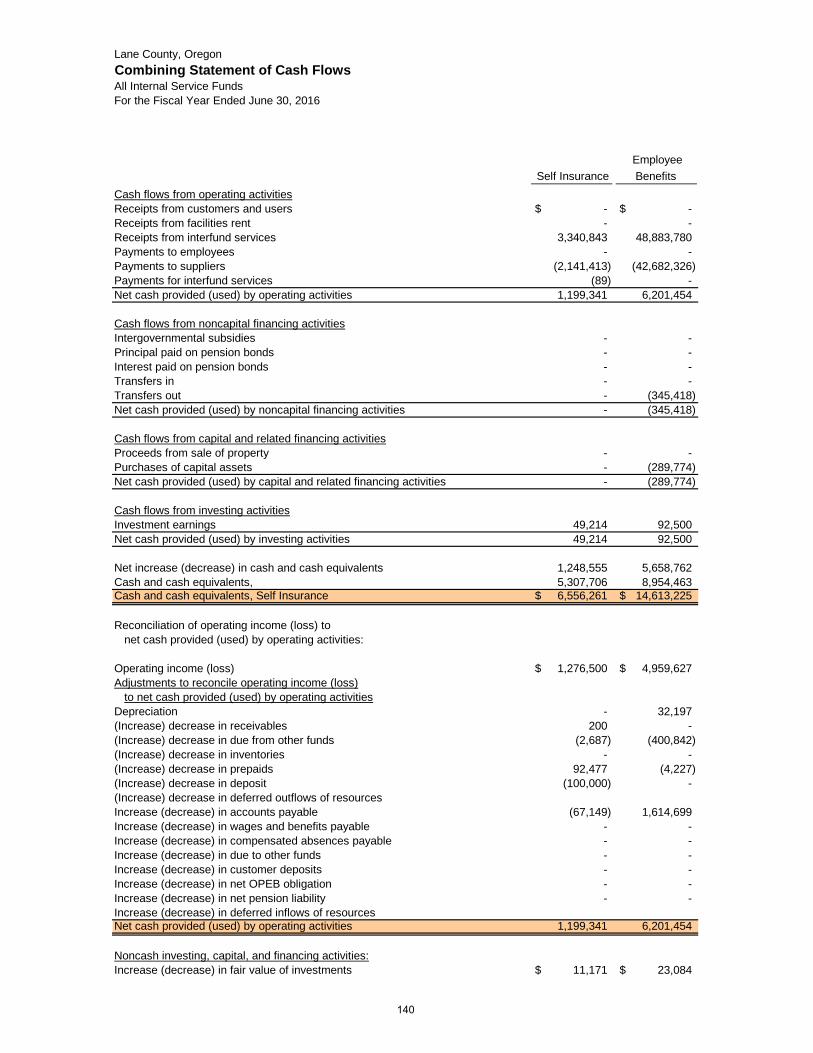

Combining Statement of Cash Flows – All Internal Service Funds 140 - 141

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual:

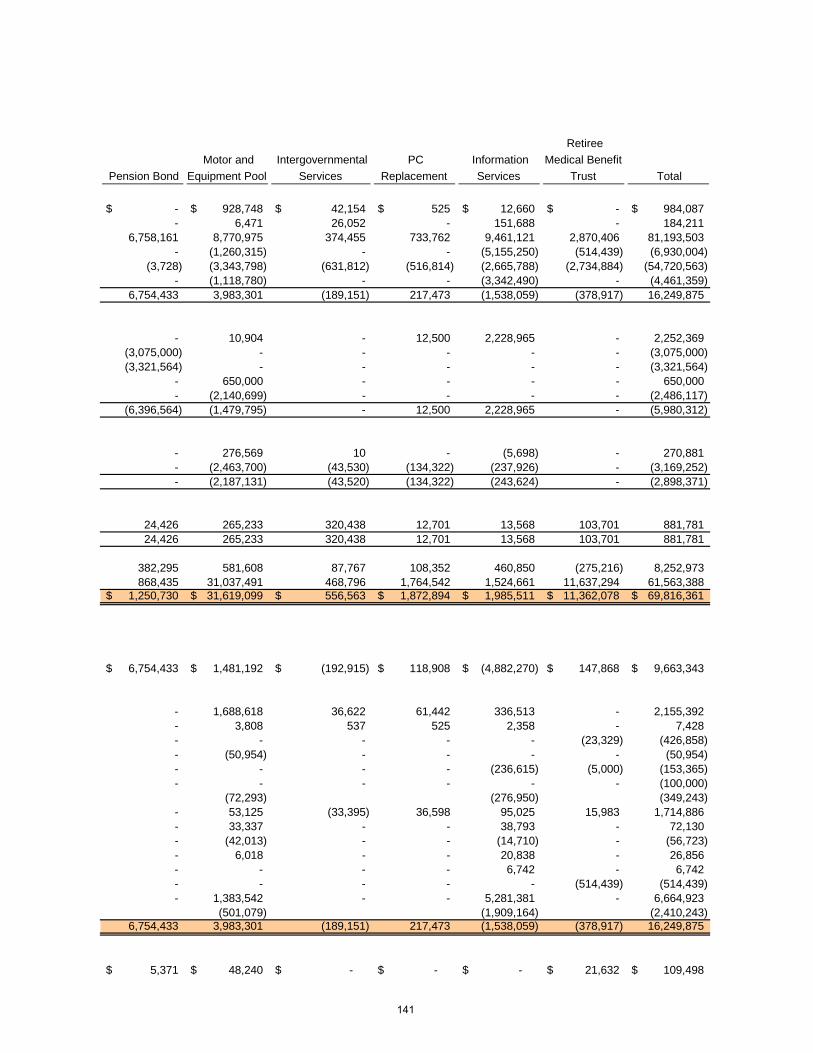

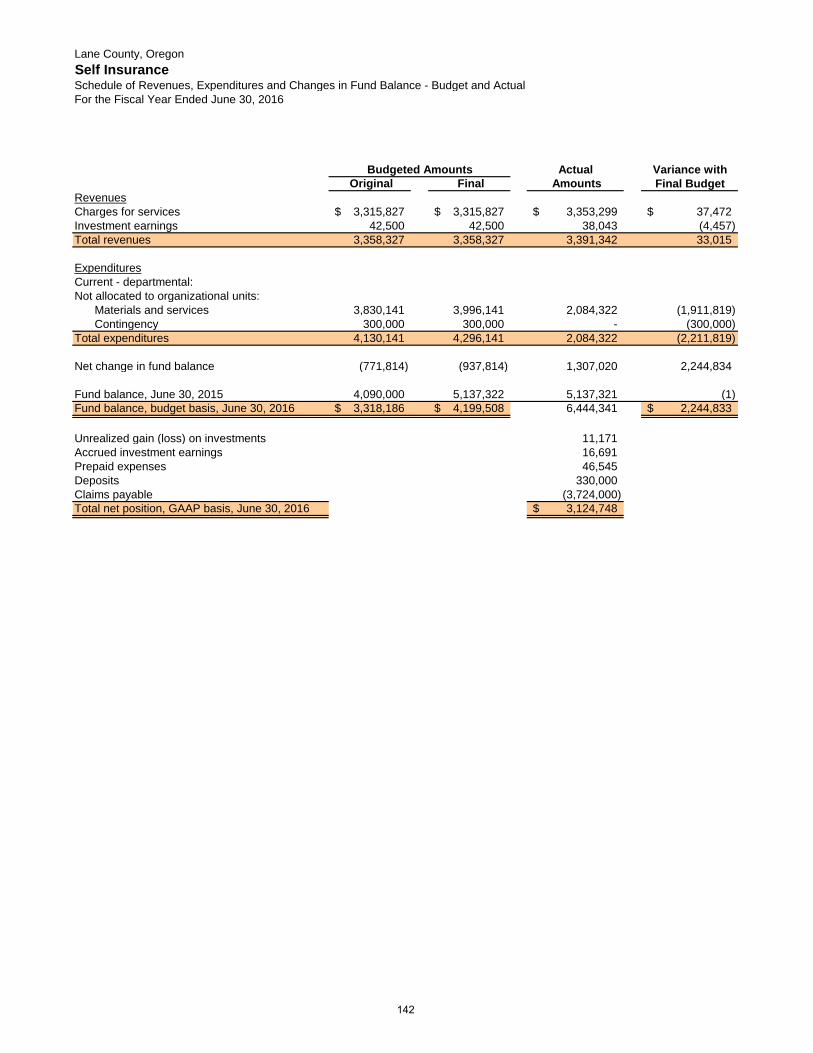

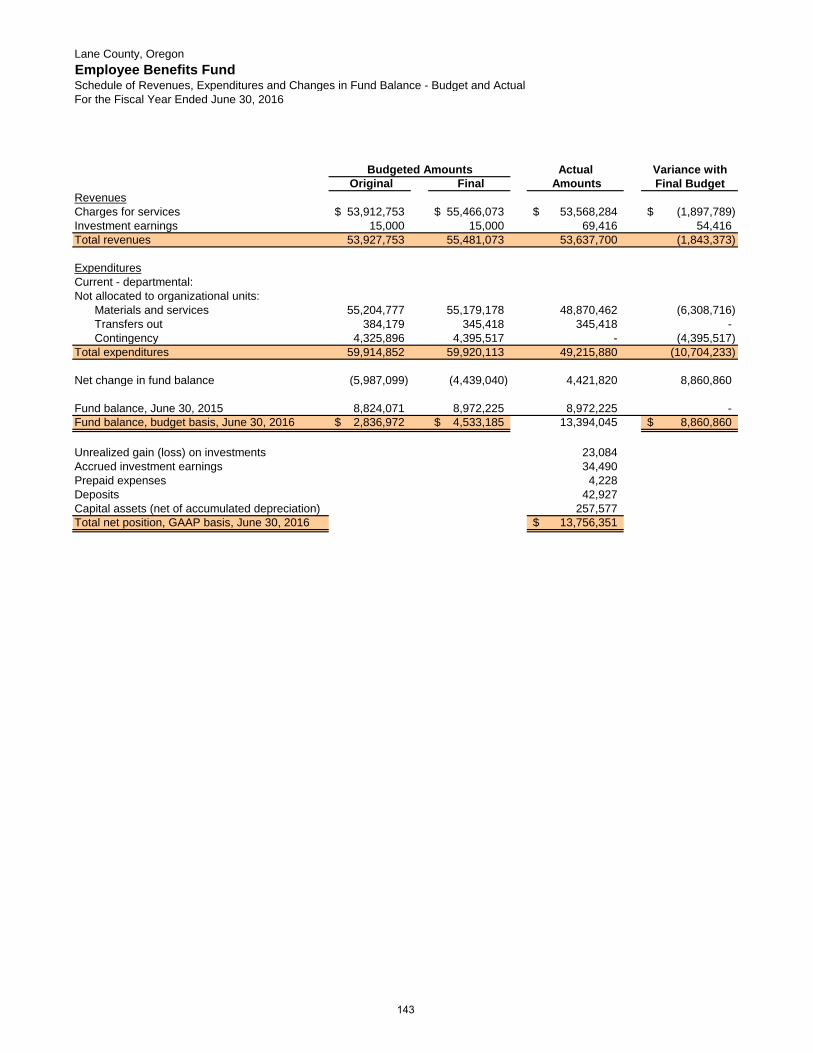

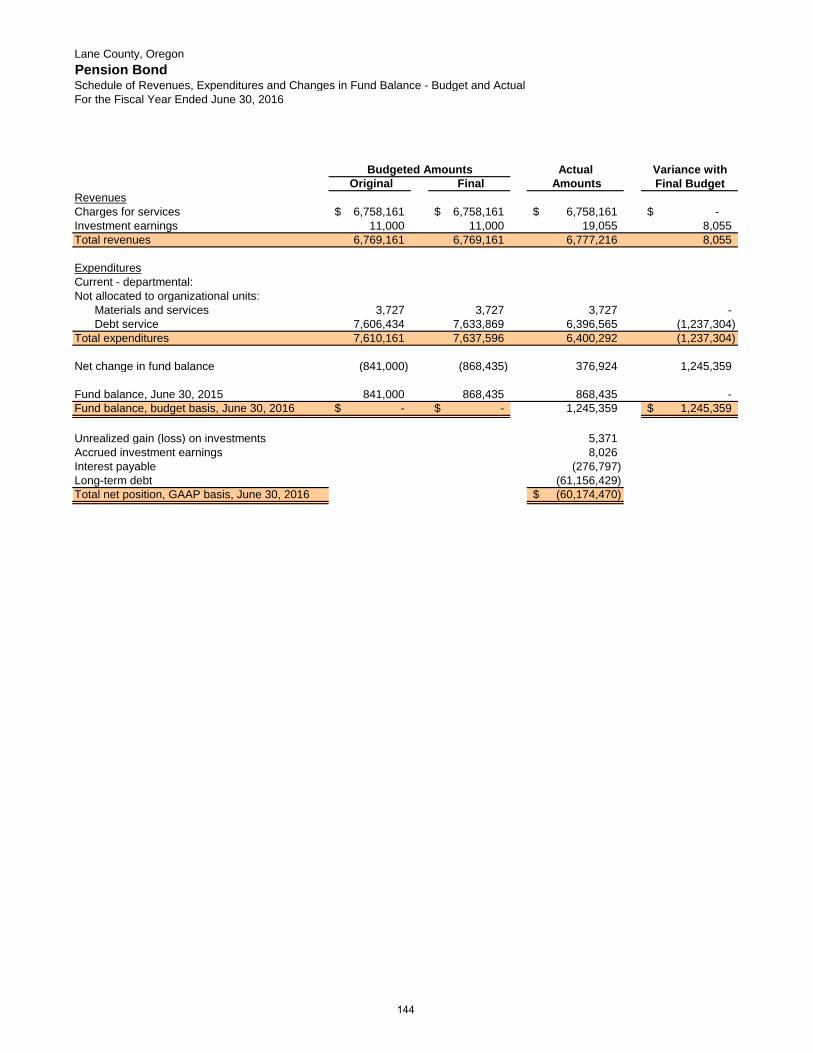

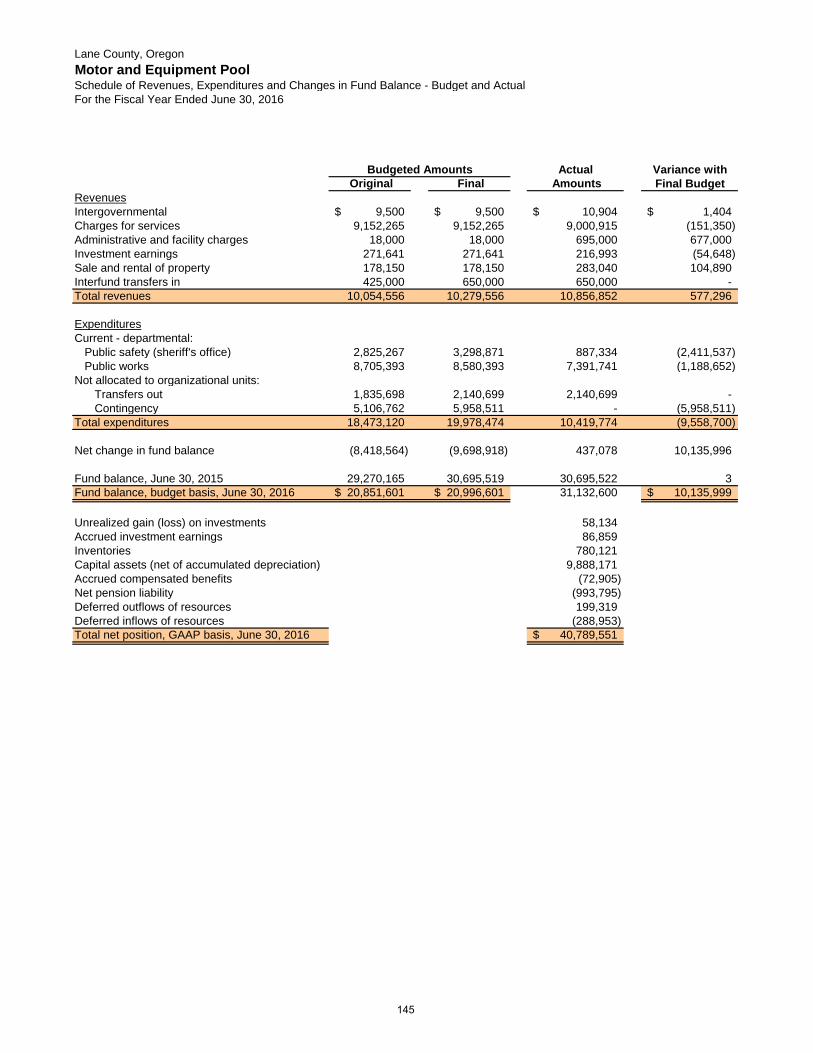

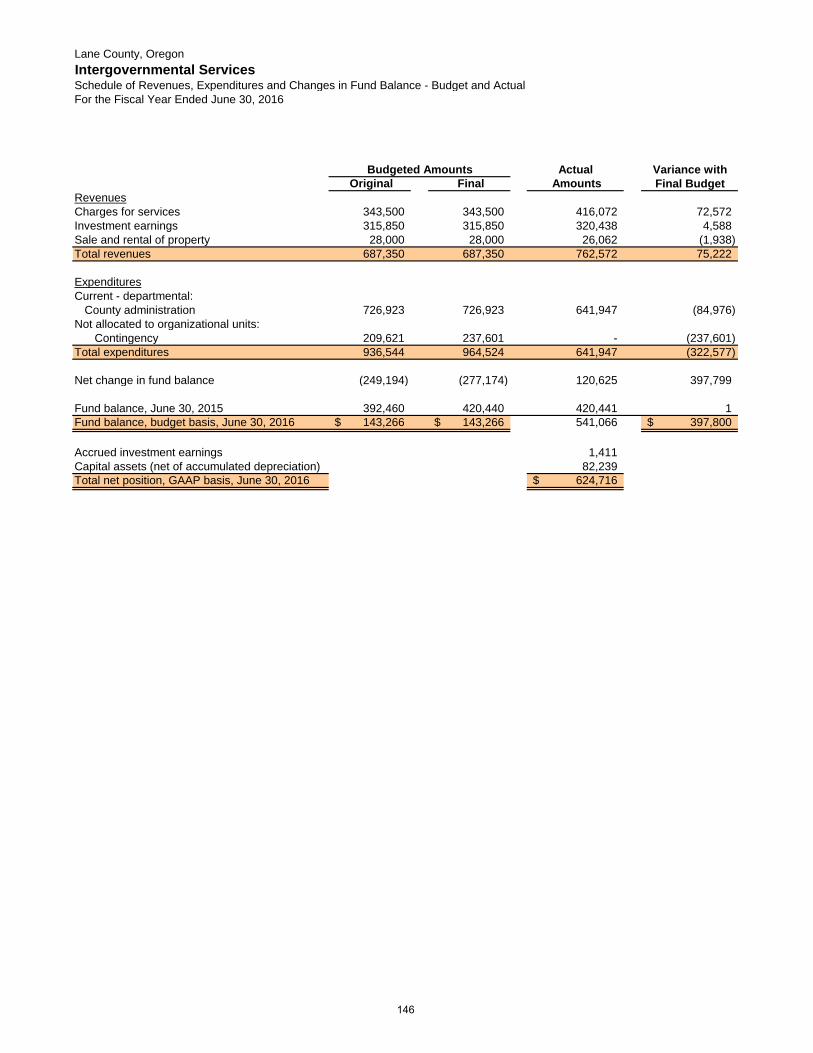

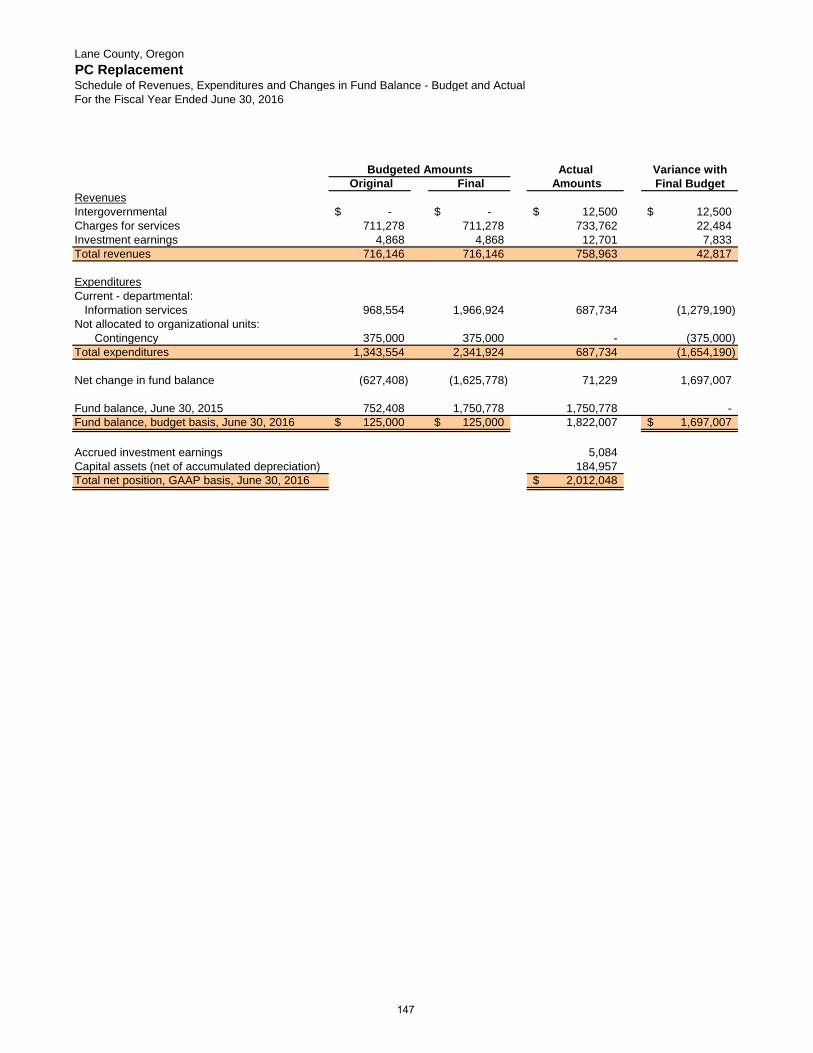

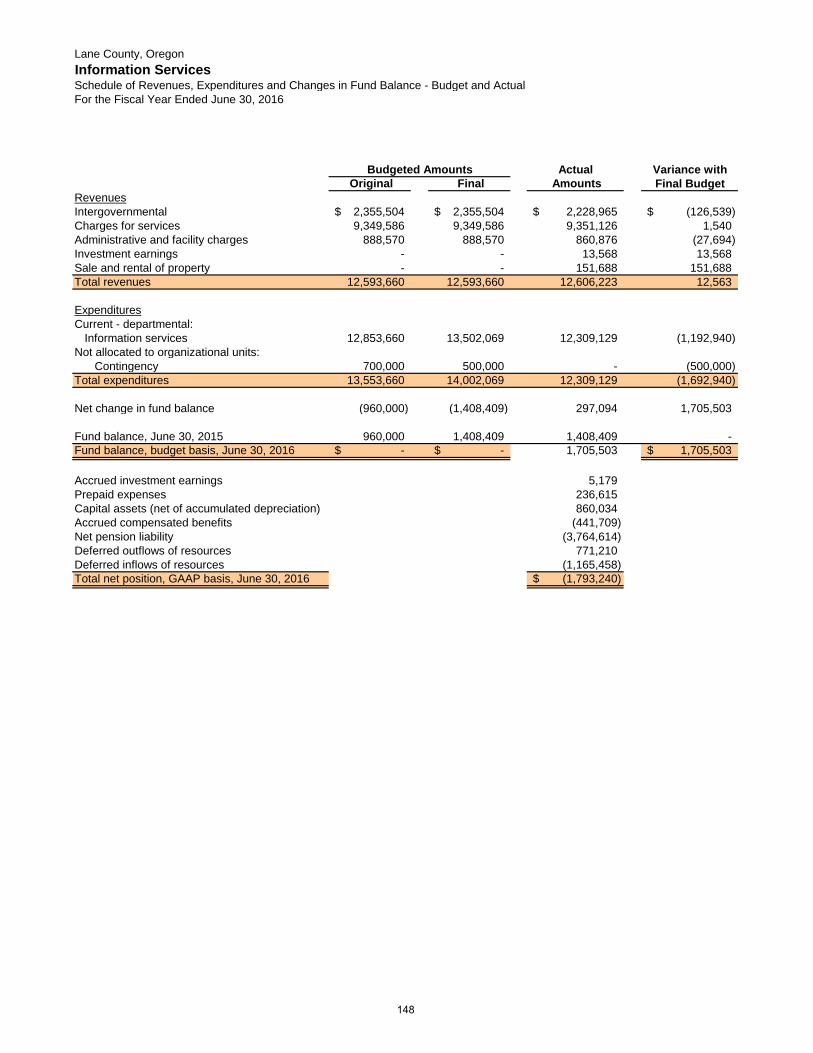

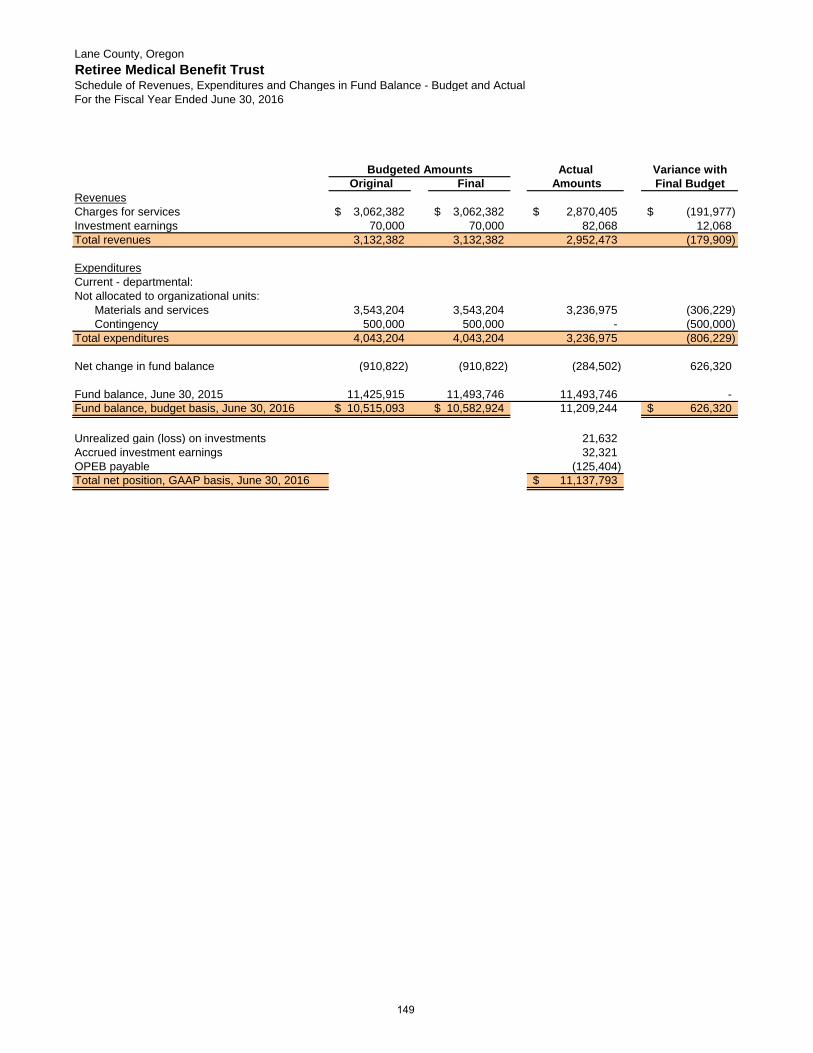

Self Insurance Fund 142Employee Benefits Fund 143Pension Bond Fund 144Motor and Equipment Pool Fund 145Intergovernmental Services Fund 146PC Replacement Fund 147Information Services Fund 148Retiree Medical Benefit Trust Fund 149

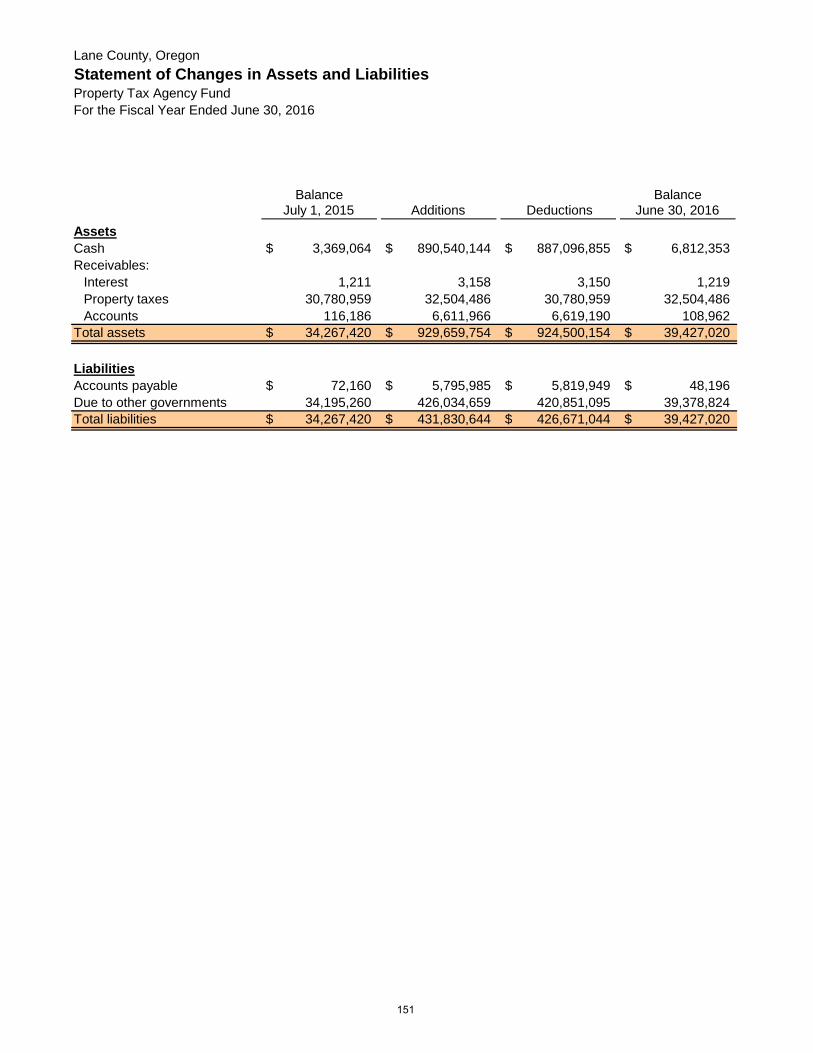

Fiduciary Funds:Statement of Changes in Assets and Liabilities - Property Tax Agency Fund 151

iii

FINANCIAL SECTION, continued: Page(s)

Other Supplementary Schedules:

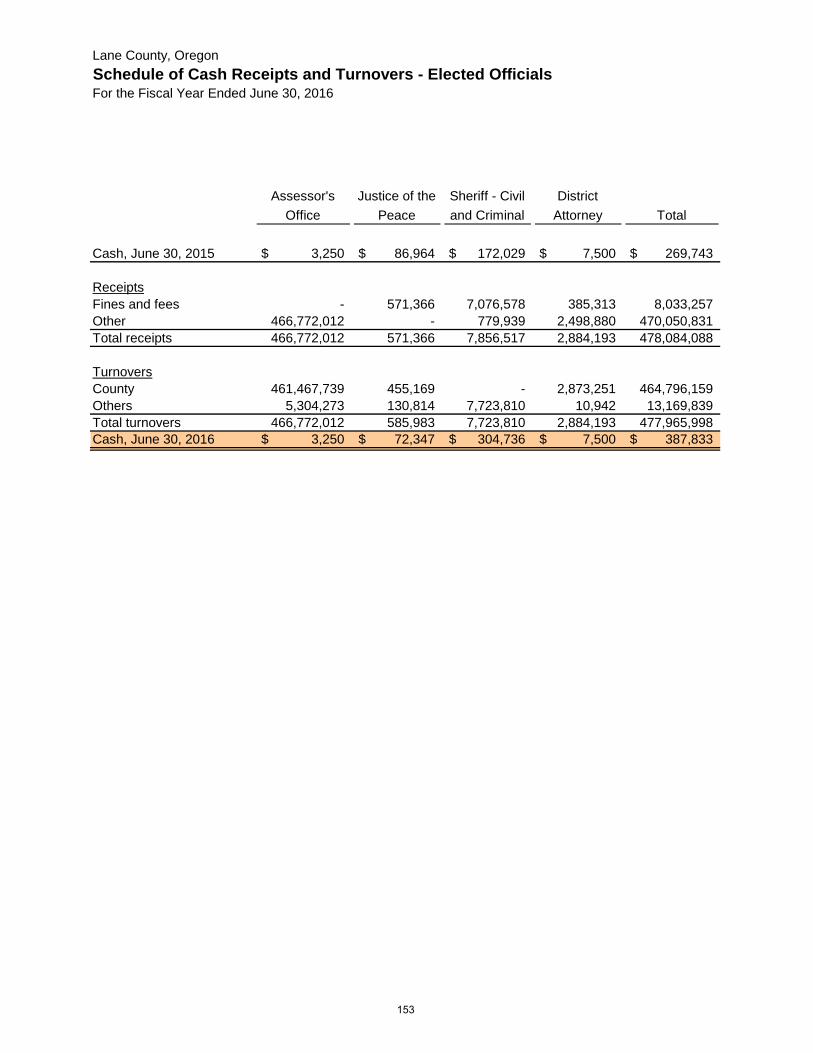

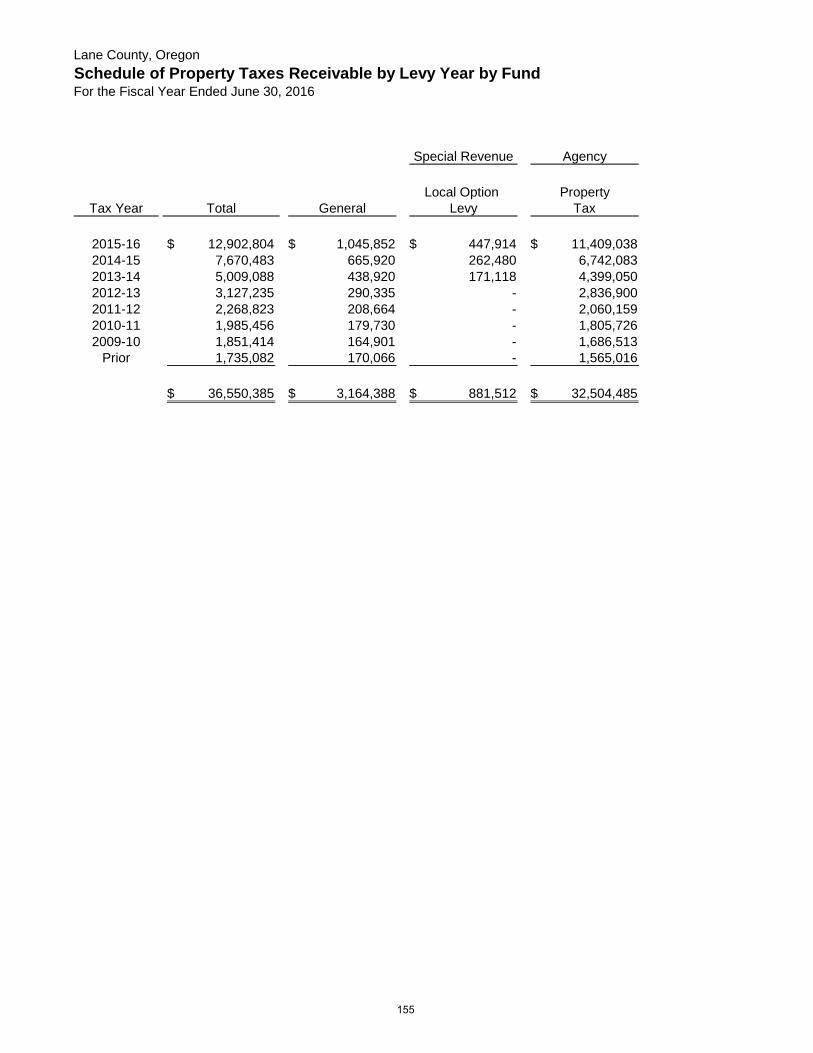

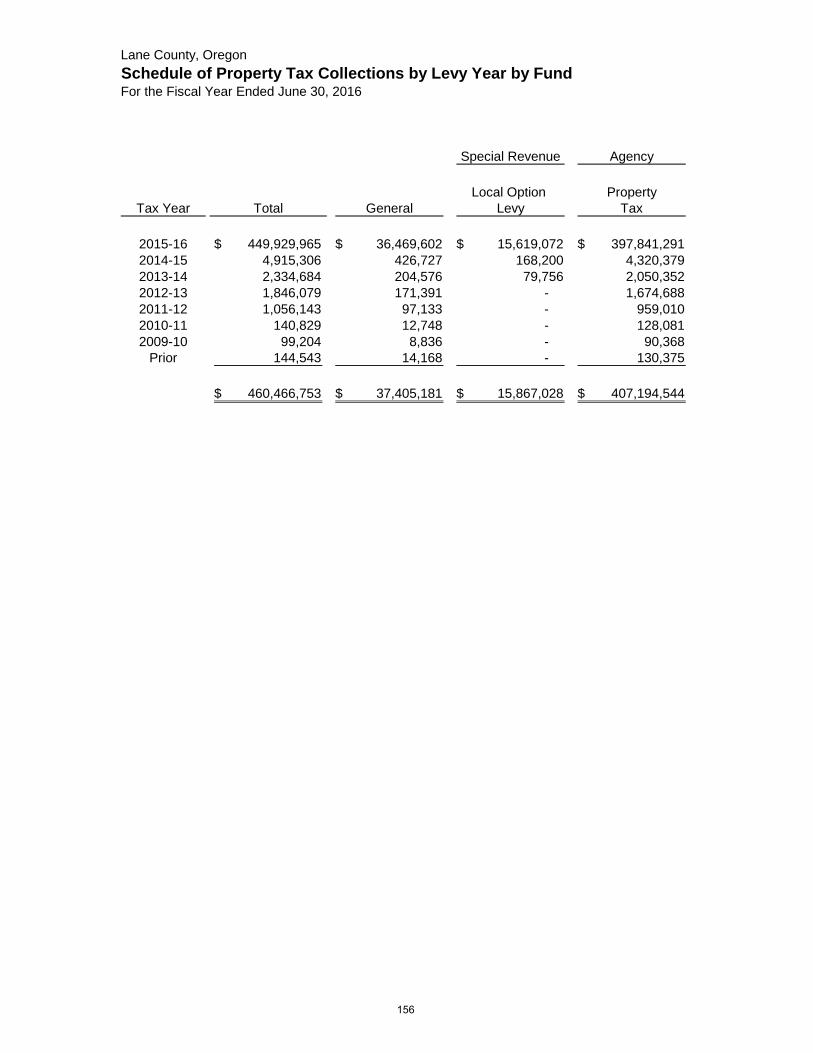

Schedule of Cash Receipts and Turnovers – Elected Officials 153Schedule of Property Tax Transactions 154Schedule of Property Taxes Receivable by Levy Year by Fund 155Schedule of Property Tax Collections by Levy Year by Fund 156

STATISTICAL SECTION

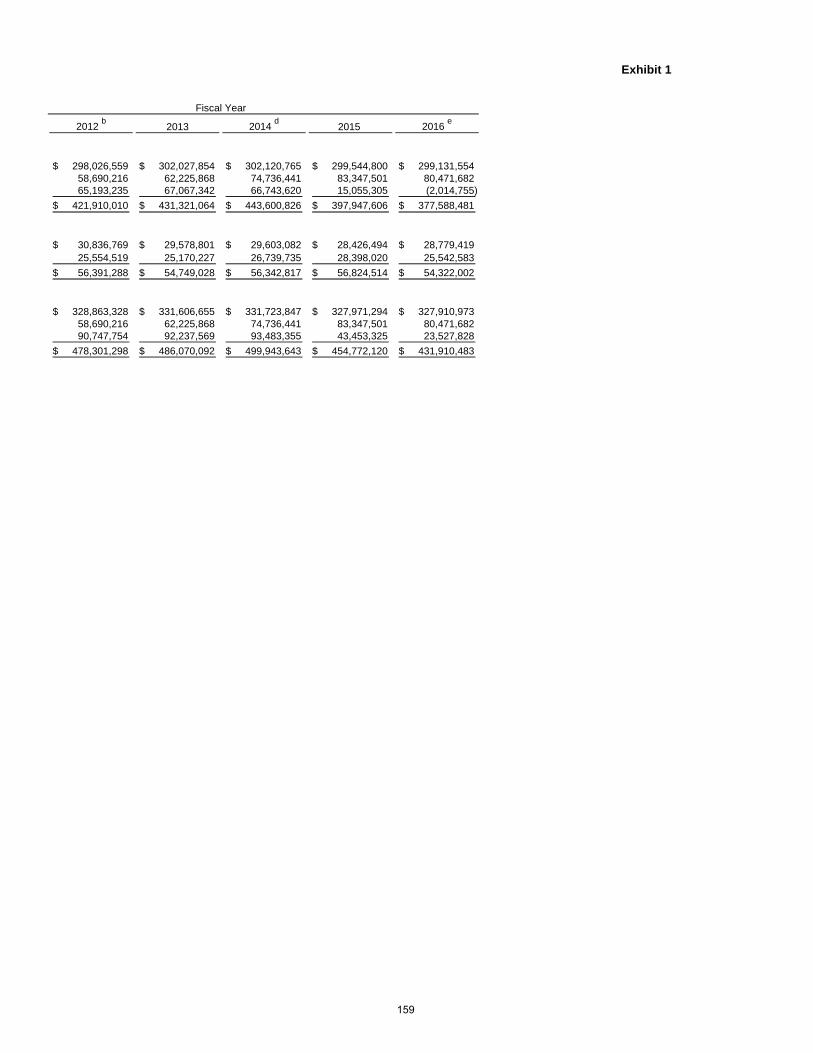

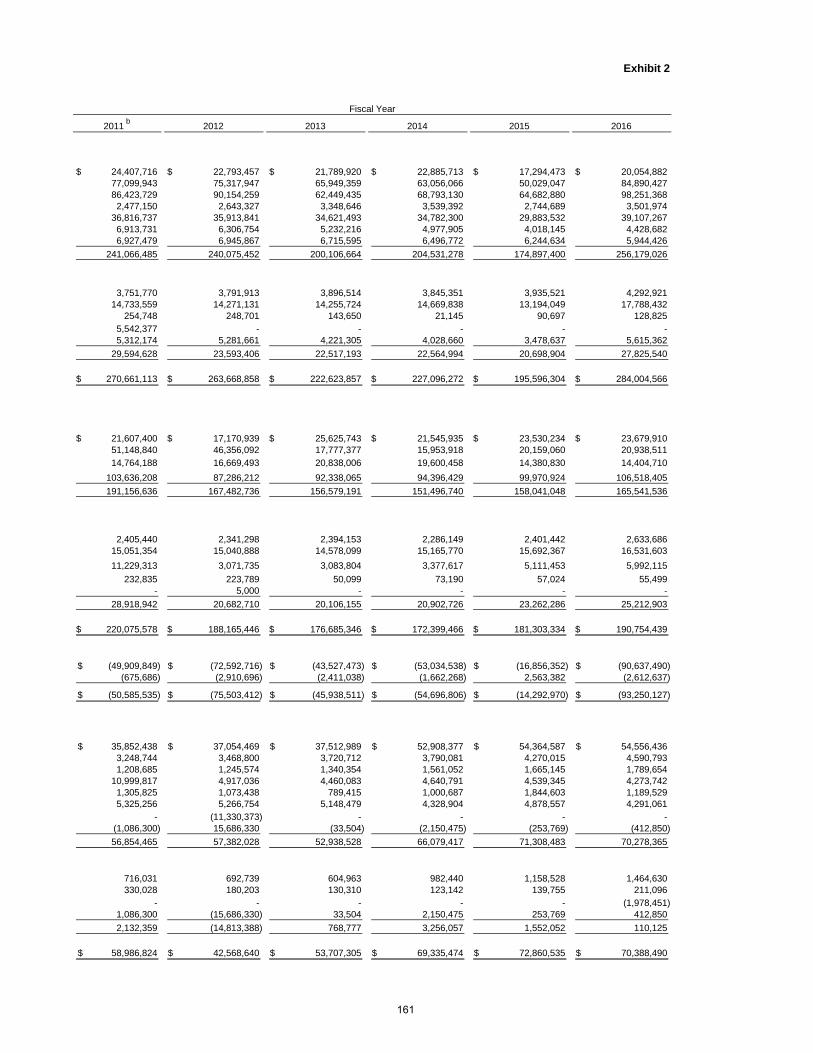

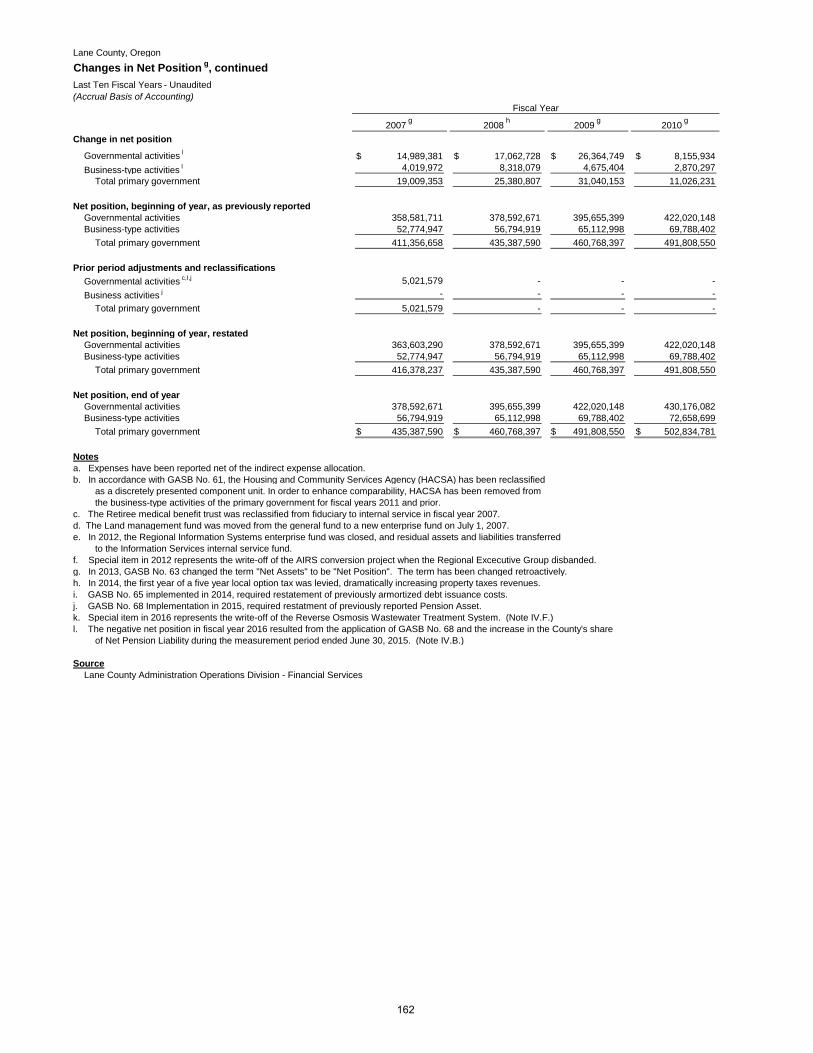

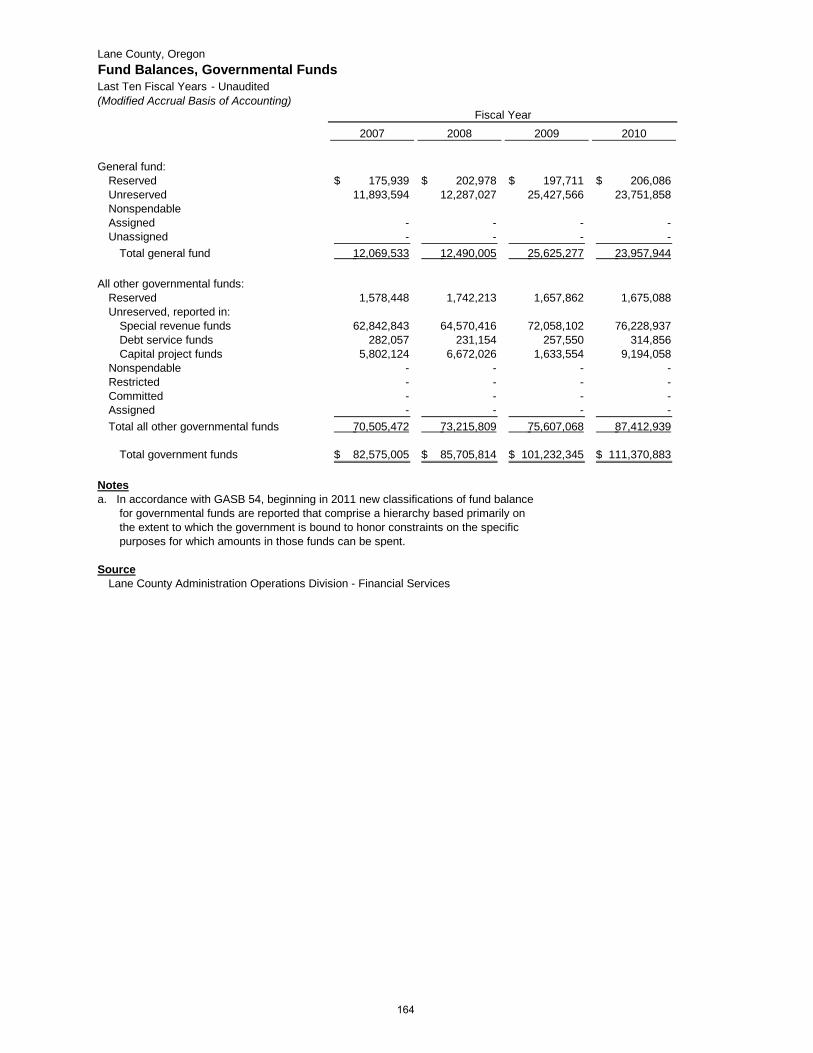

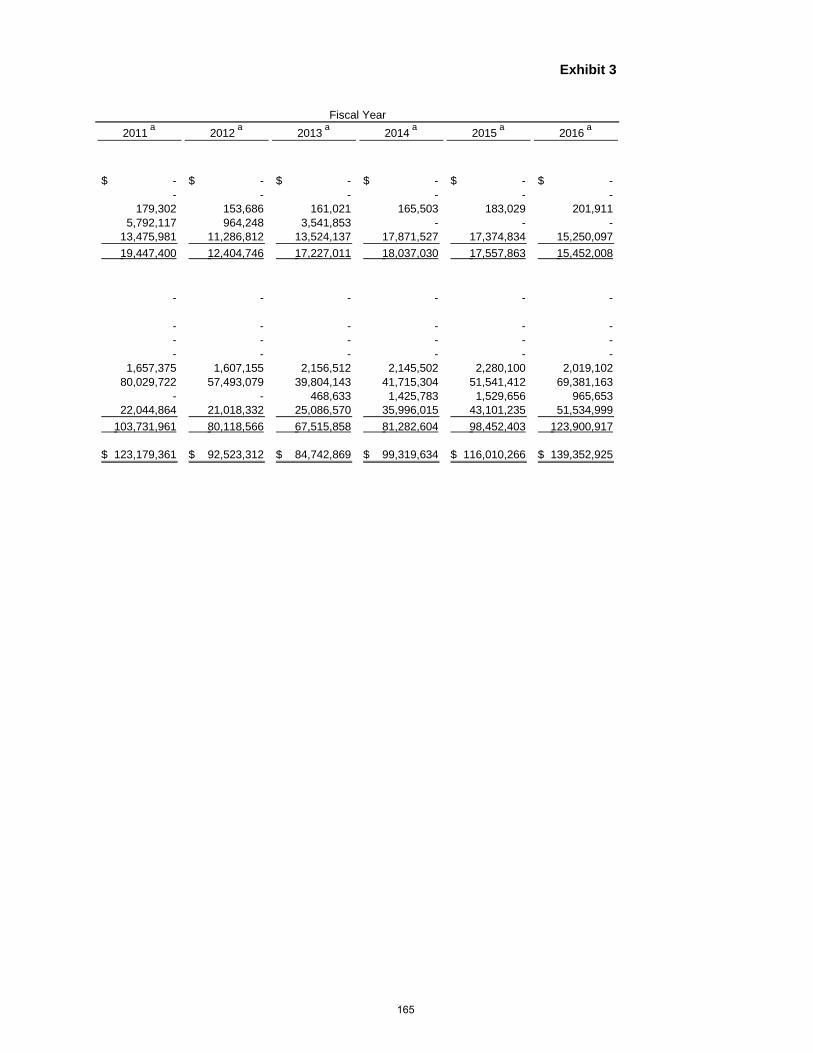

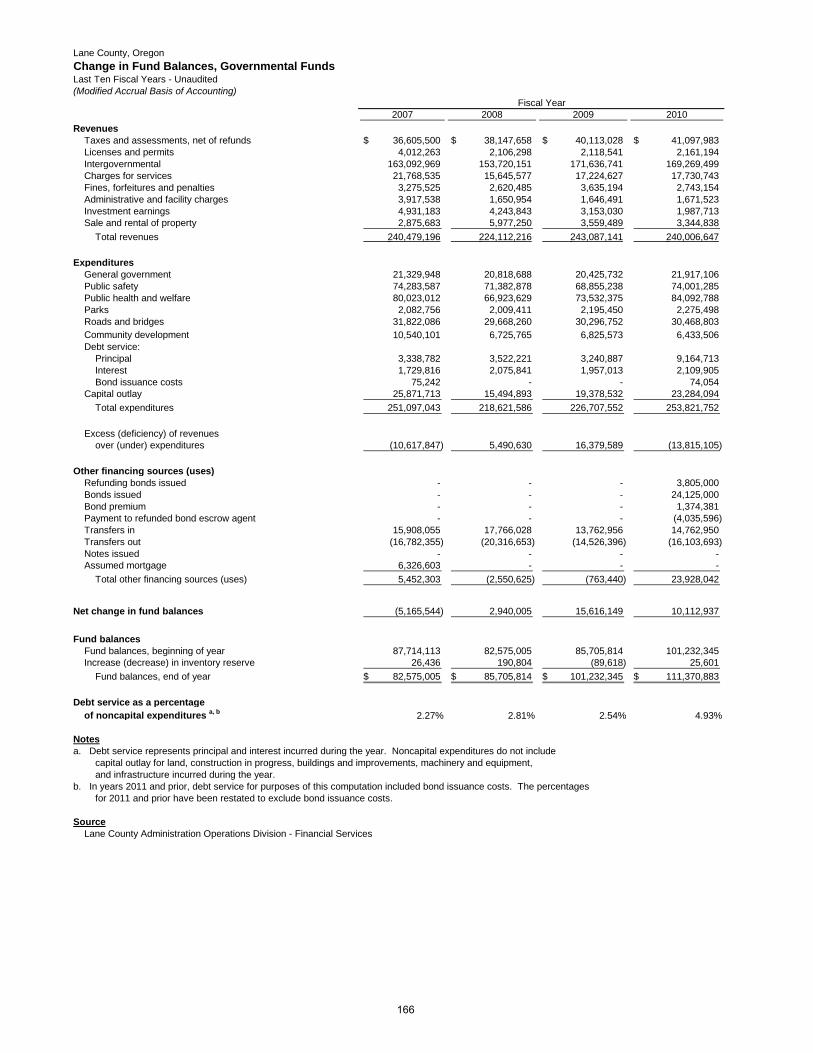

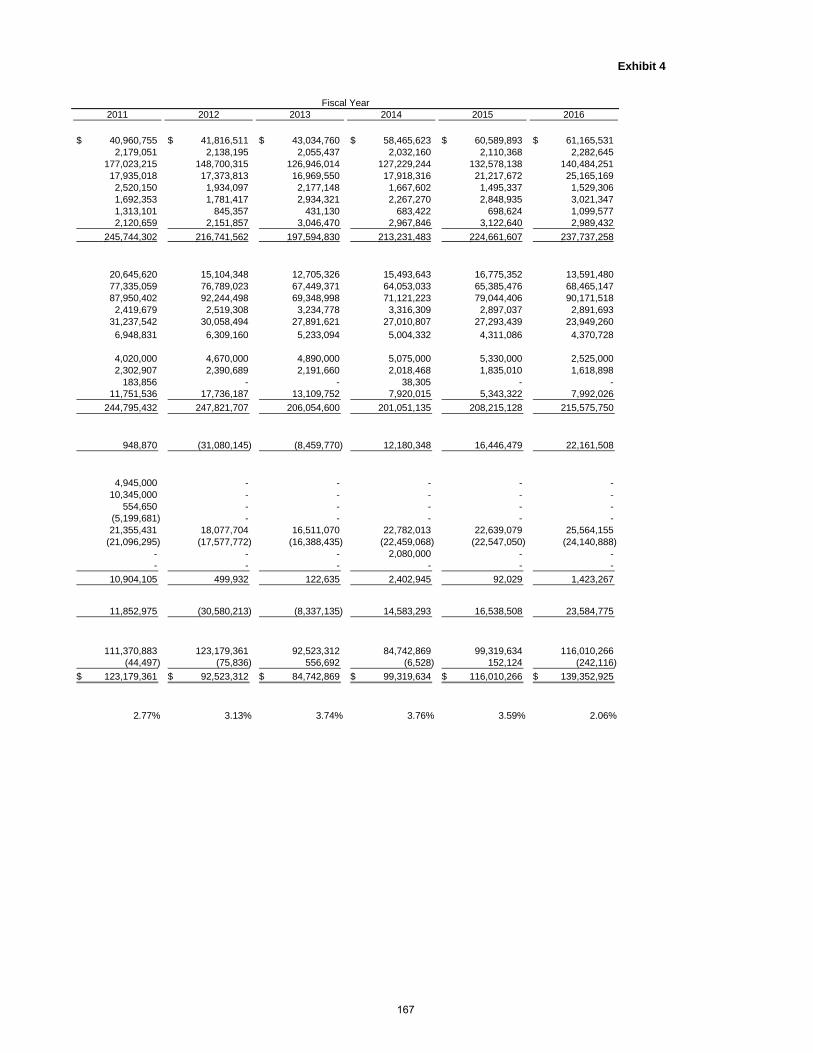

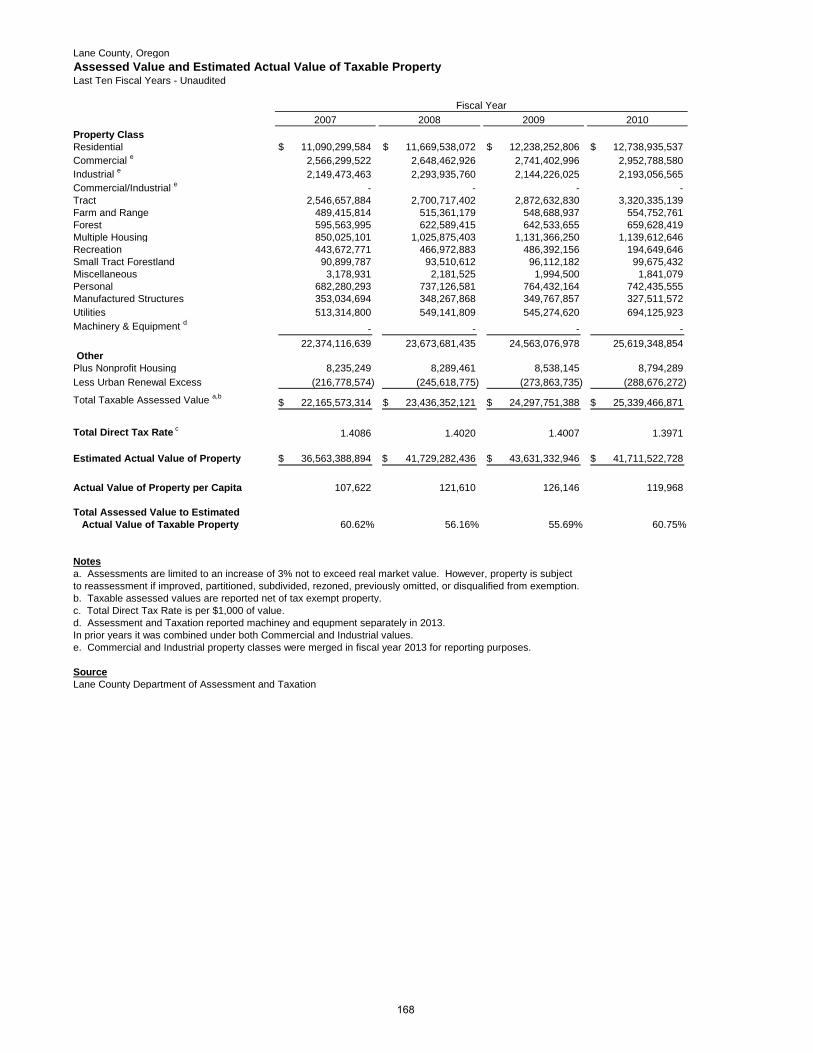

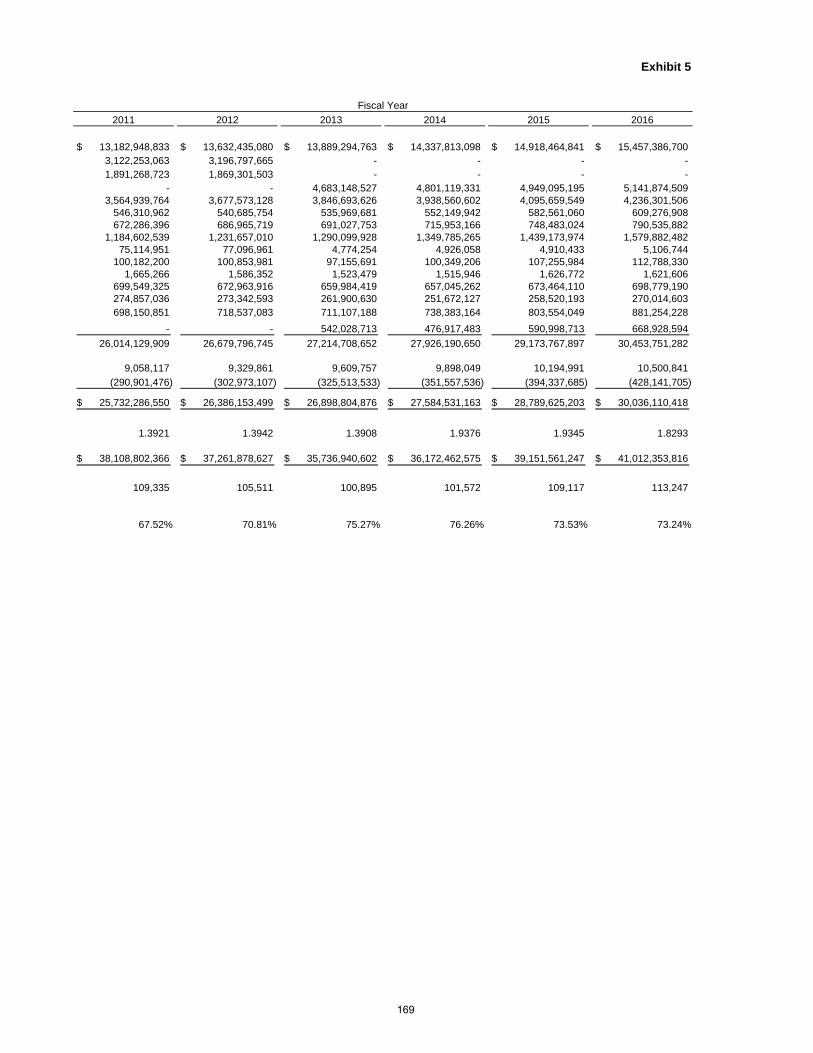

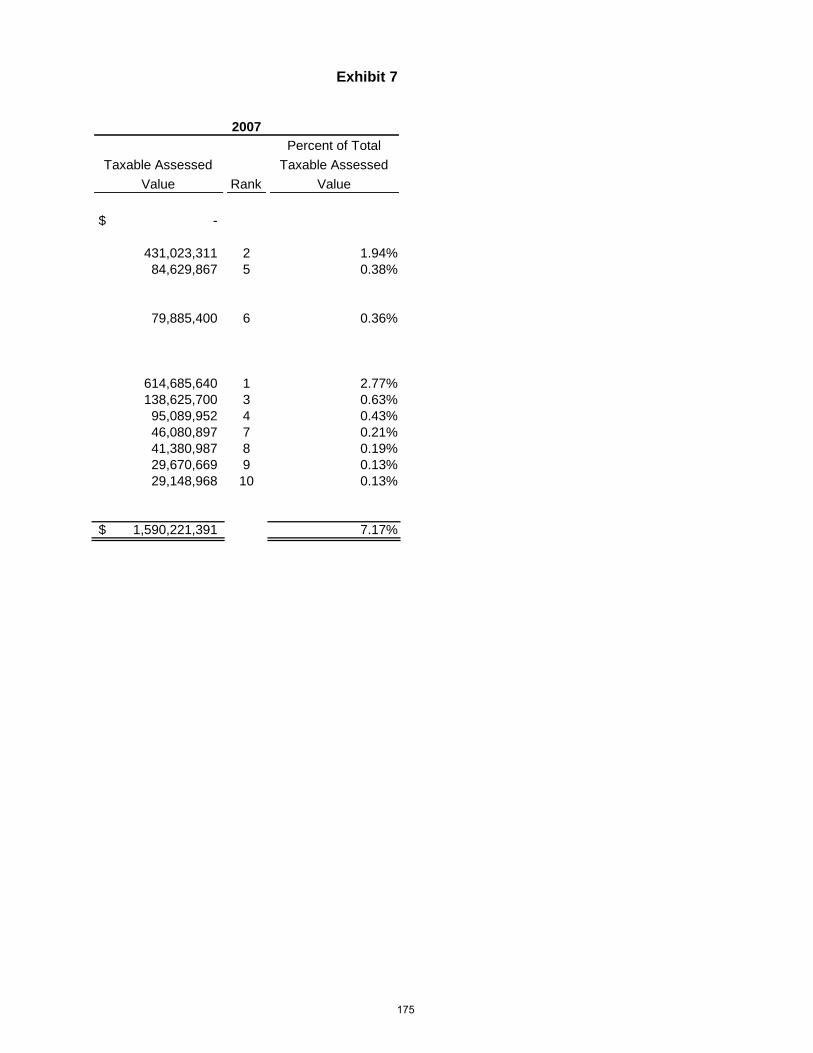

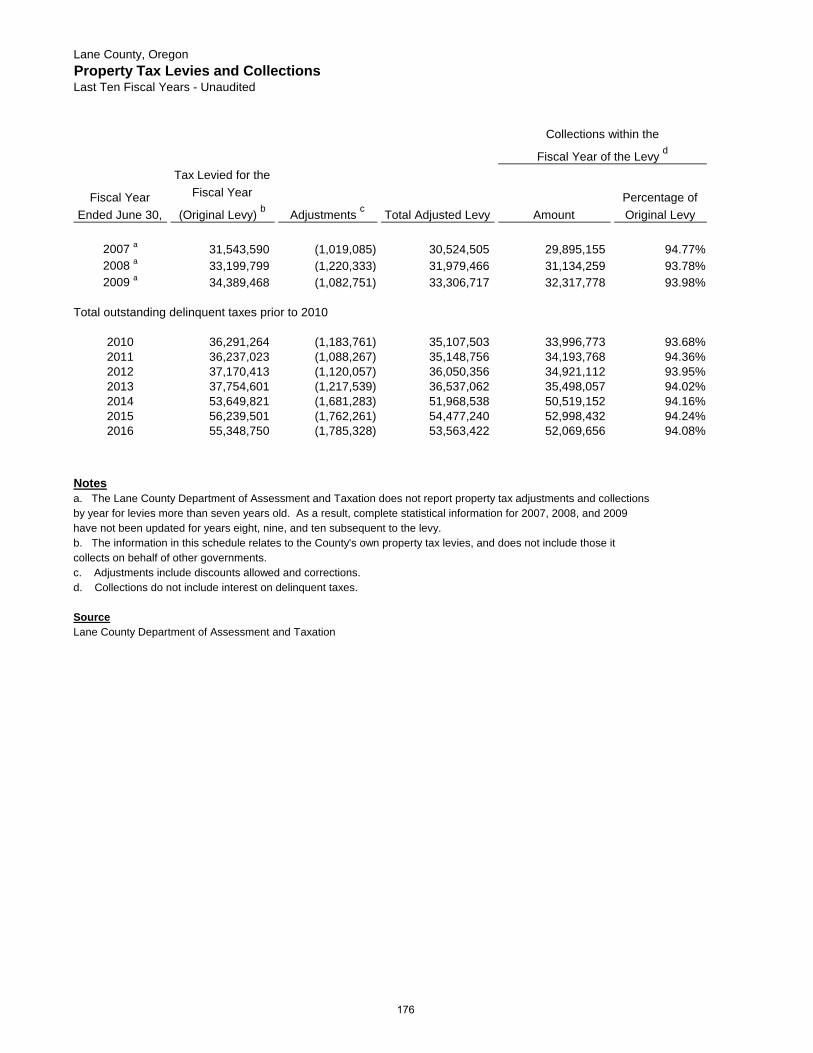

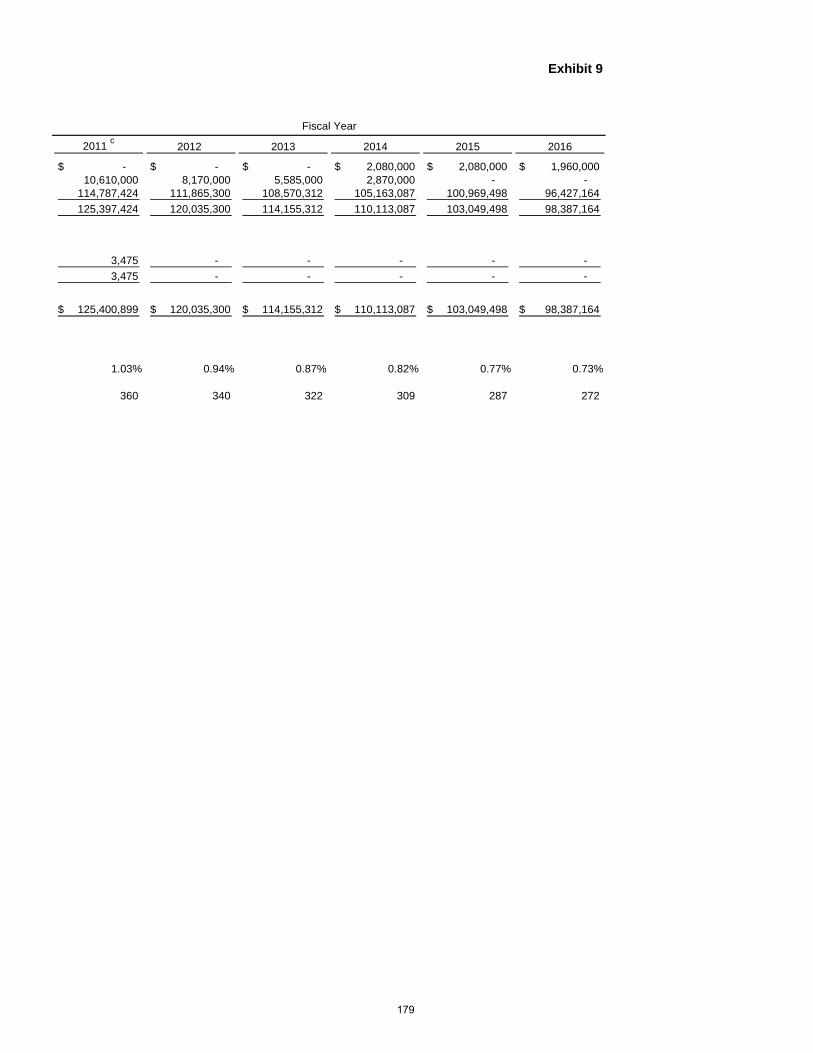

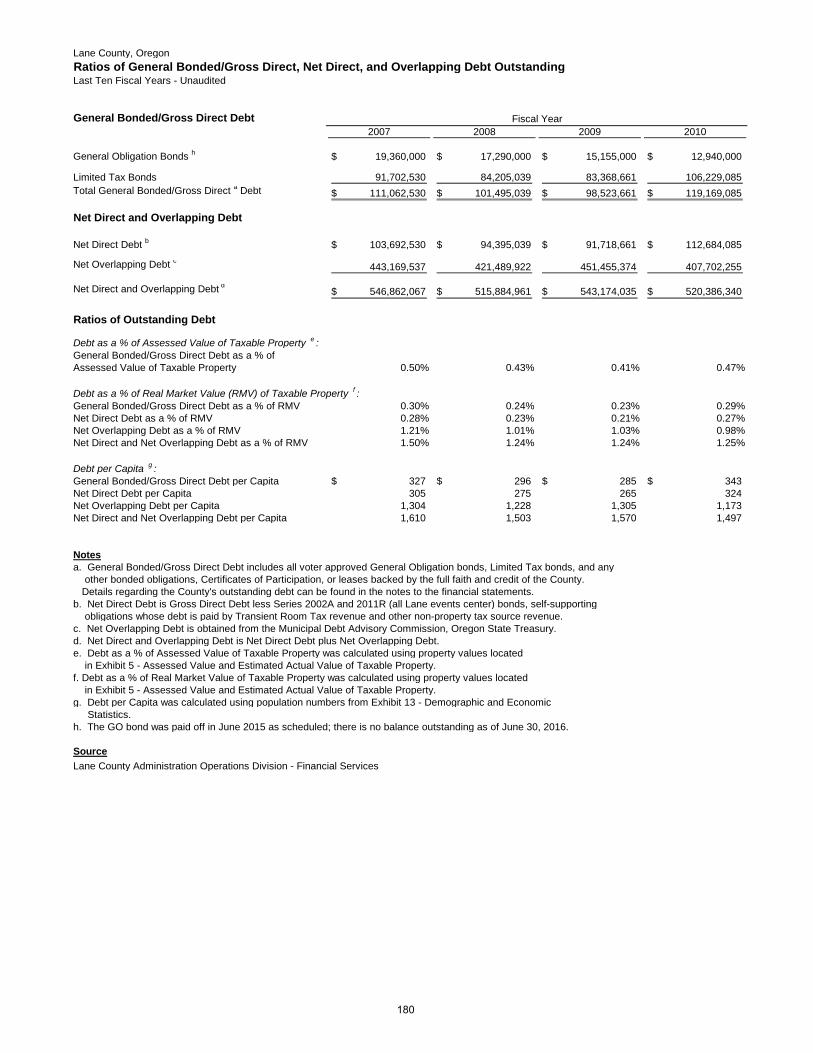

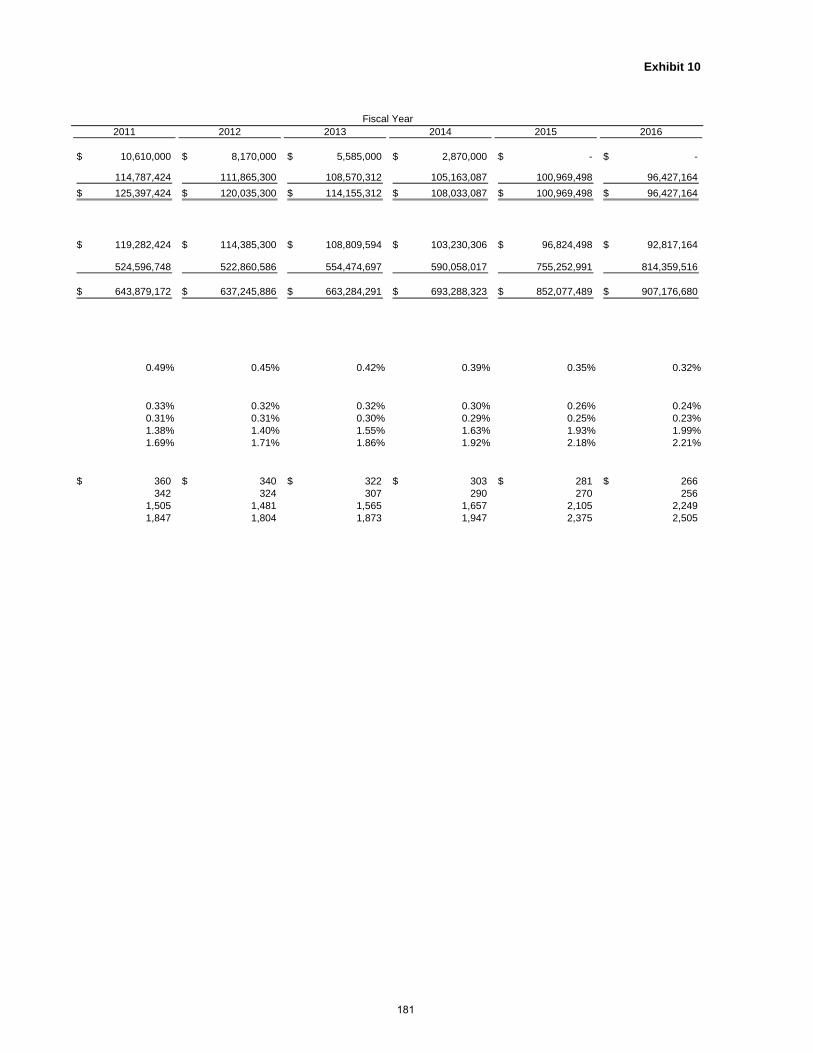

Exhibit 1 – Net Position by Component 158 - 159Exhibit 2 – Changes in Net Position 160 - 163Exhibit 3 – Fund Balances, Governmental Funds 164 - 165Exhibit 4 – Change in Fund Balances, Governmental Funds 166 - 167Exhibit 5 – Assessed Value and Estimated Actual Value of Taxable Property 168 - 169Exhibit 6 – Direct and Overlapping Property Tax Rates 170 - 173Exhibit 7 – Principal Property Tax Payers 174 - 175Exhibit 8 – Property Tax Levies and Collections 176 - 177Exhibit 9 – Ratios of Outstanding Debt by Type 178 - 179Exhibit 10 – Ratios of General Bonded/Gross Direct,

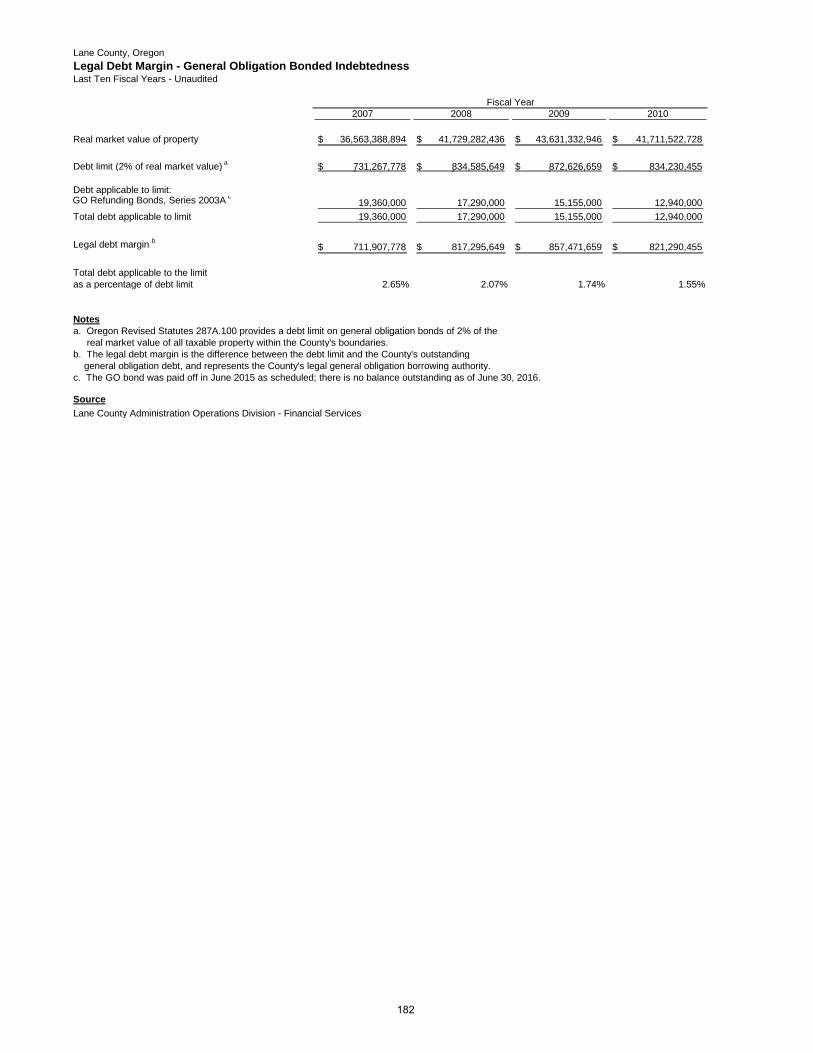

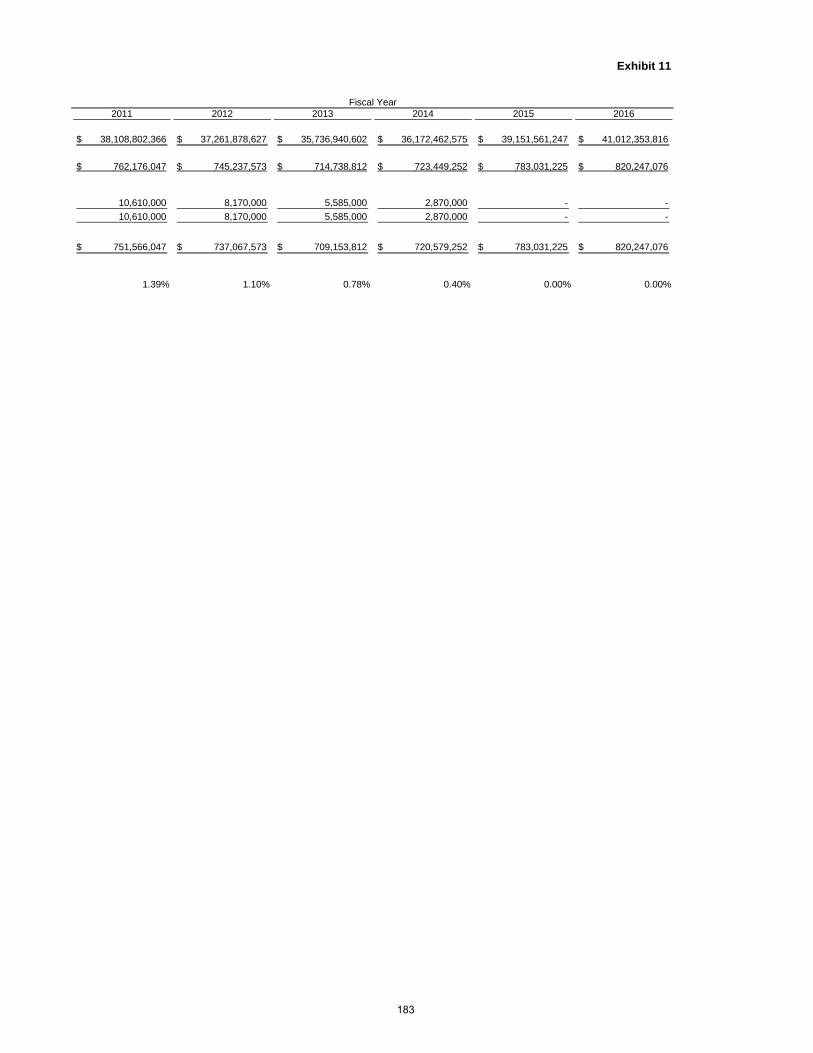

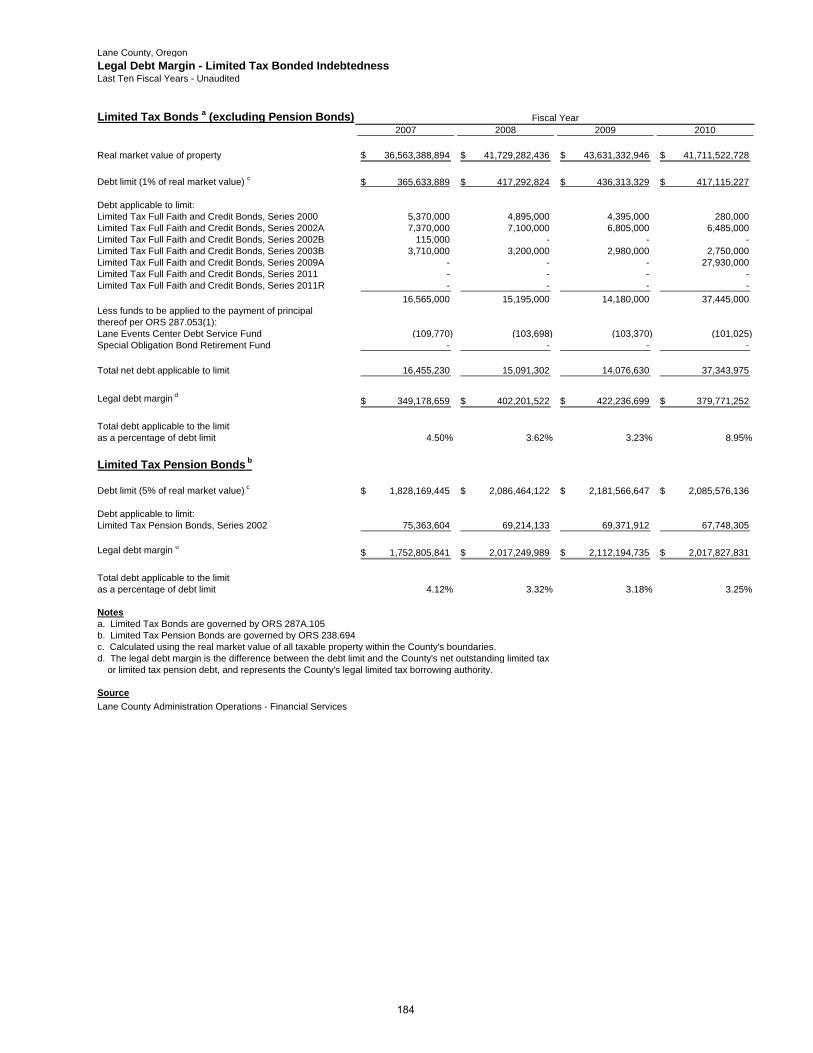

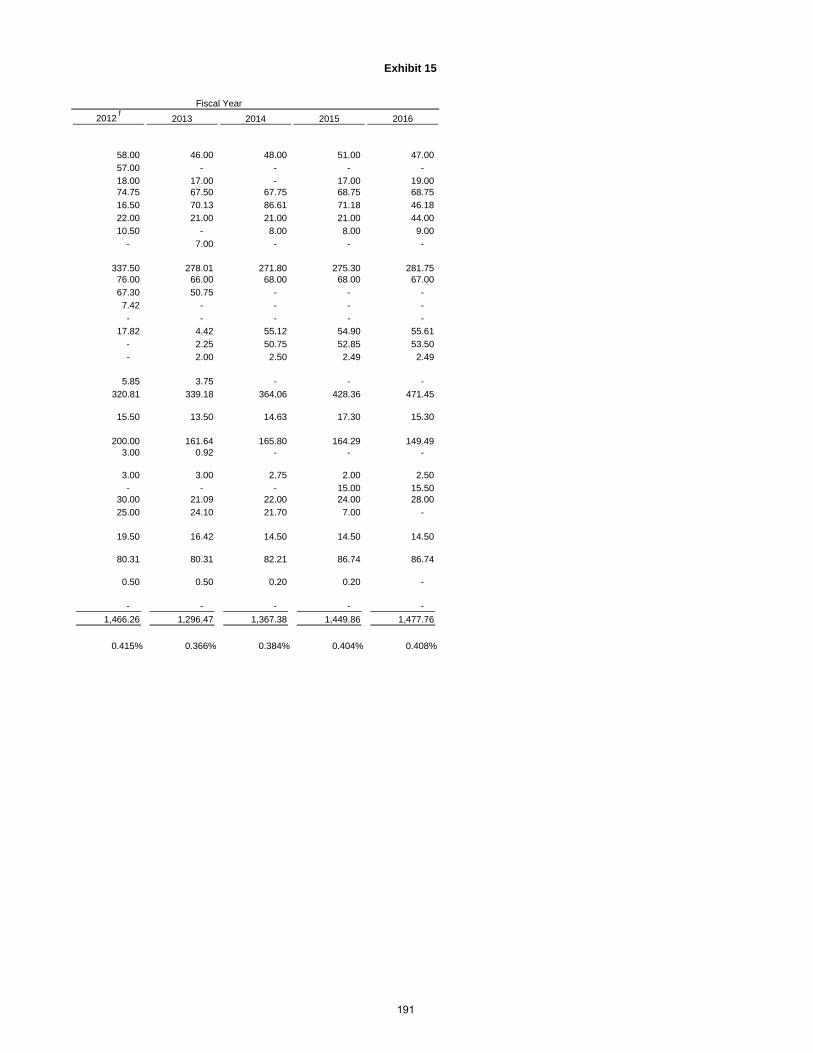

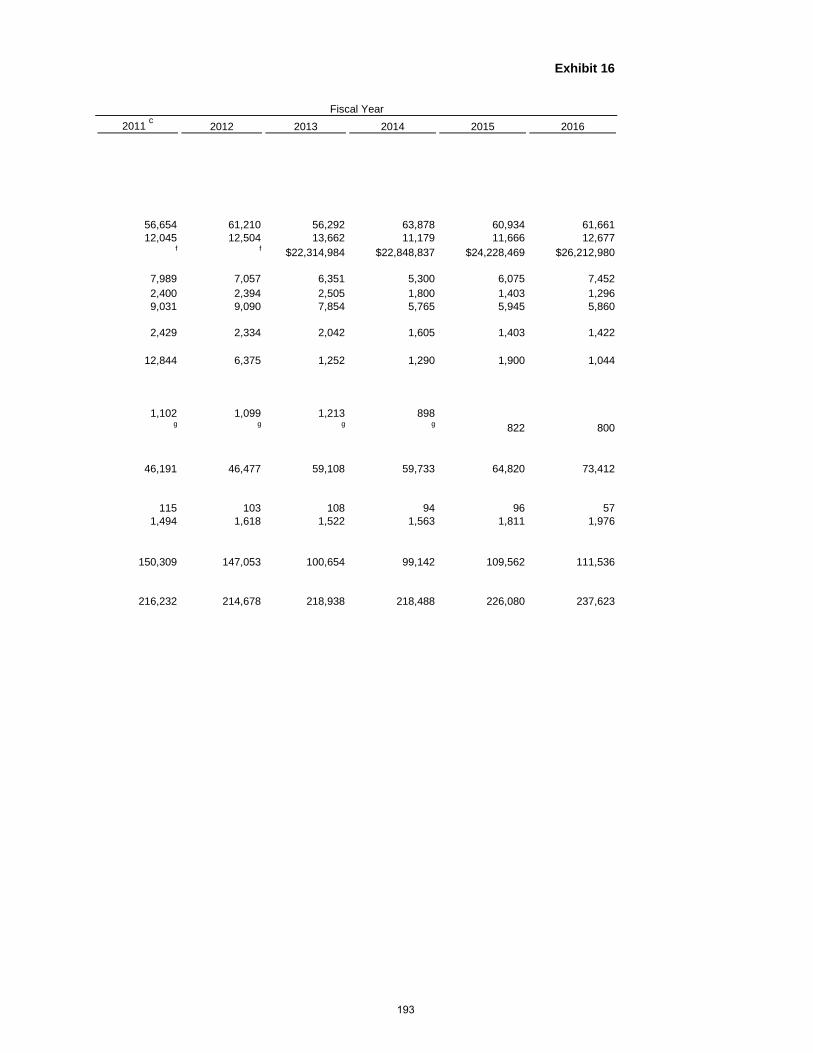

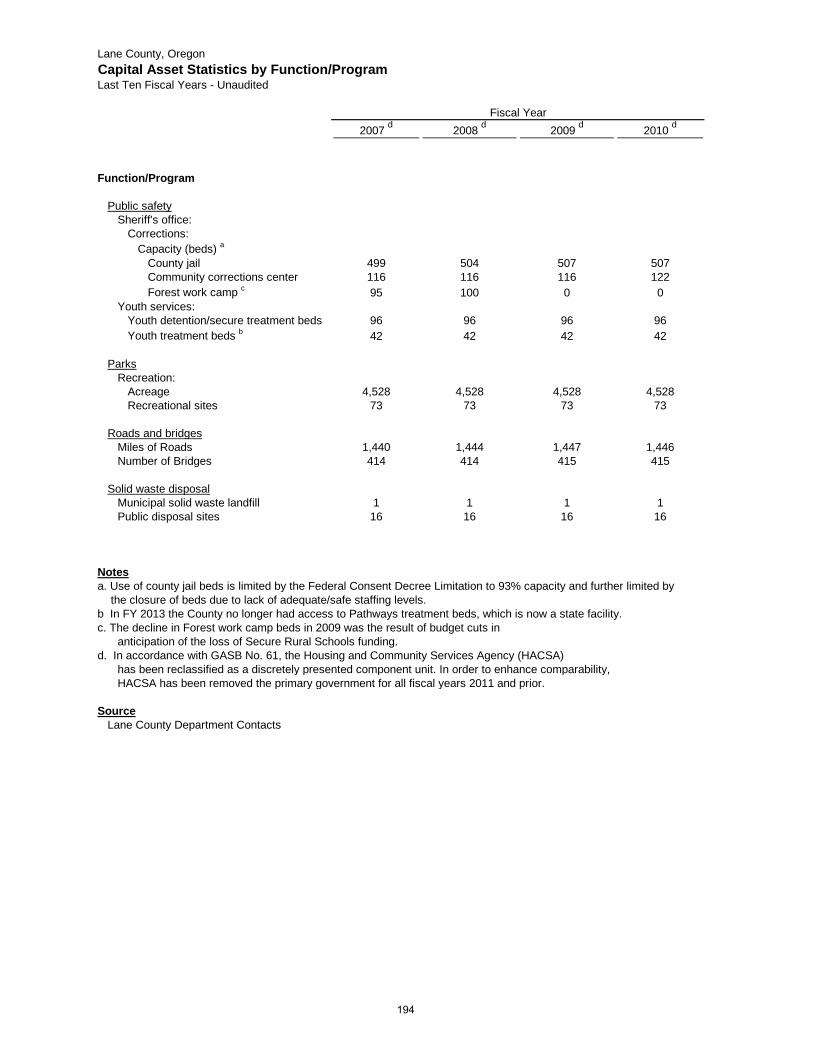

Net Direct, and Overlapping Debt Outstanding 180 - 181Exhibit 11 – Legal Debt Margin - General Obligation Bonded Indebtedness 182 - 183Exhibit 12 – Legal Debt Margin - Limited Tax Bonded Indebtedness 184 - 185Exhibit 13 – Demographic and Economic Statistics 187Exhibit 14 – Principal Employers 188 - 189Exhibit 15 – Authorized Number of Employees by Function/Program 190 - 191Exhibit 16 – Operating Indicators by Function/Program 192 - 193Exhibit 17 – Capital Asset Statistics by Function/Program 194 - 195

AUDIT COMMENTS AND GOVERNMENT AUDITING STANDARDS SECTIONS

Audit Comments:

Report of Independent Auditors on Compliance and on Internal Control Over FinancialReporting Based on an Audit of Financial Statements Performed in Accordance with Oregon Minimum Audit Standards 199 - 200

Government Auditing Standards:

Report of Independent Auditors on Internal Control Over Financial Reporting and onCompliance and Other Matters Based on an Audit of Financial StatementsPerformed in Accordance with Government Auditing Standards 203 - 204

Report of Independent Auditors on Compliance for Each Major Federal Program and Report on Internal Control over Compliance Required by the Uniform Guidance 206 - 207

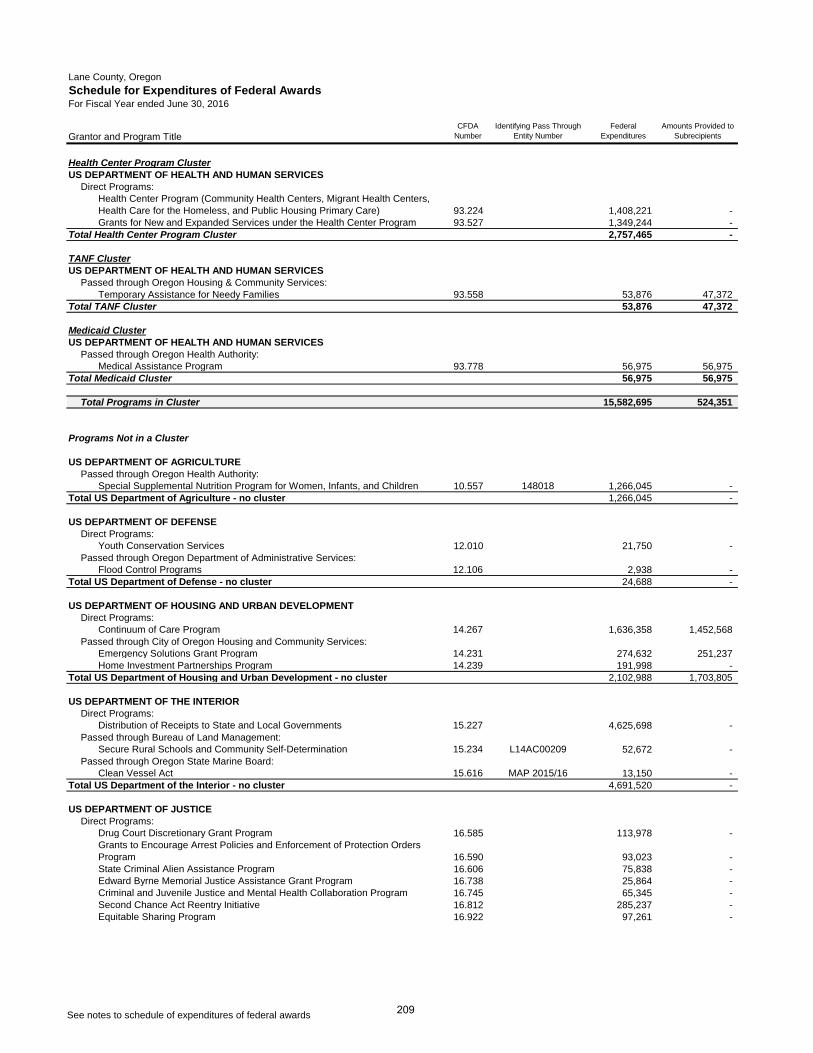

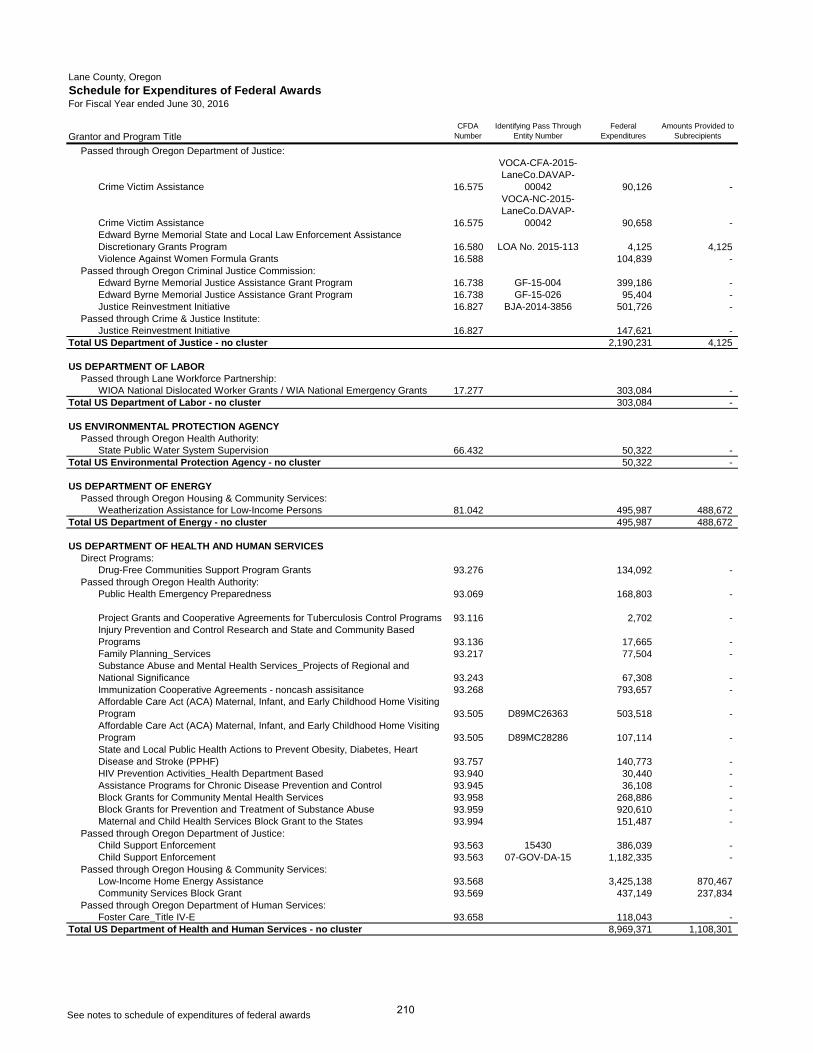

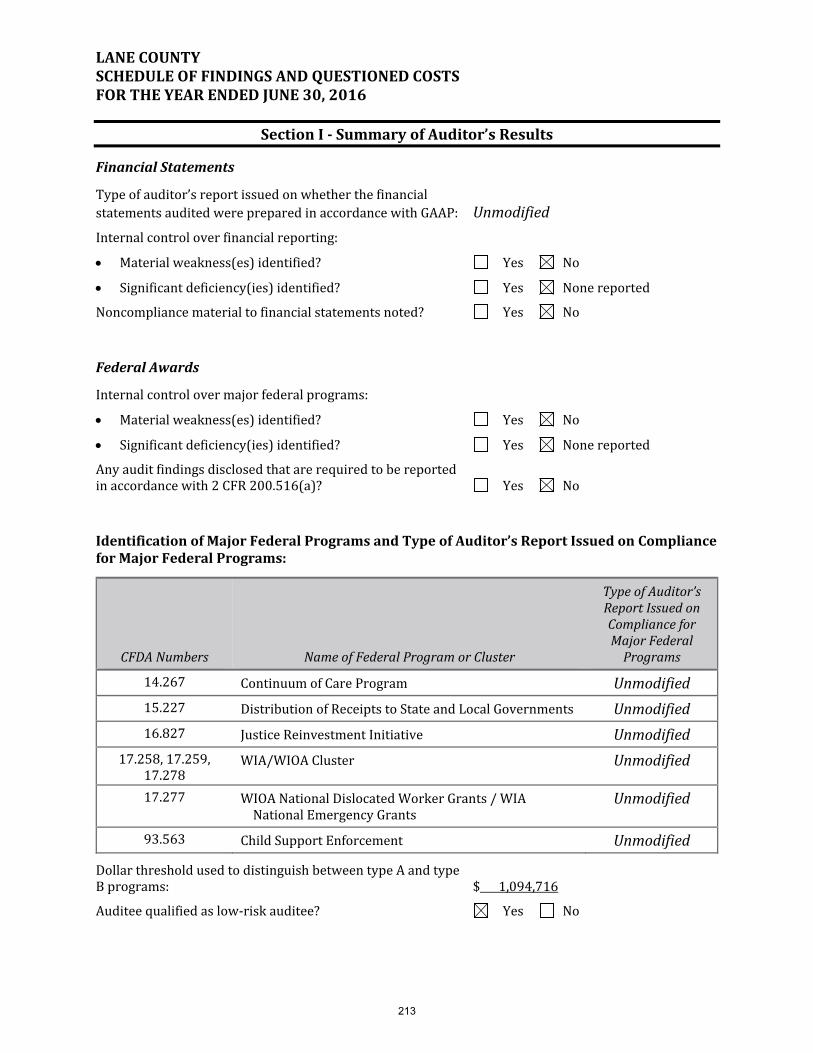

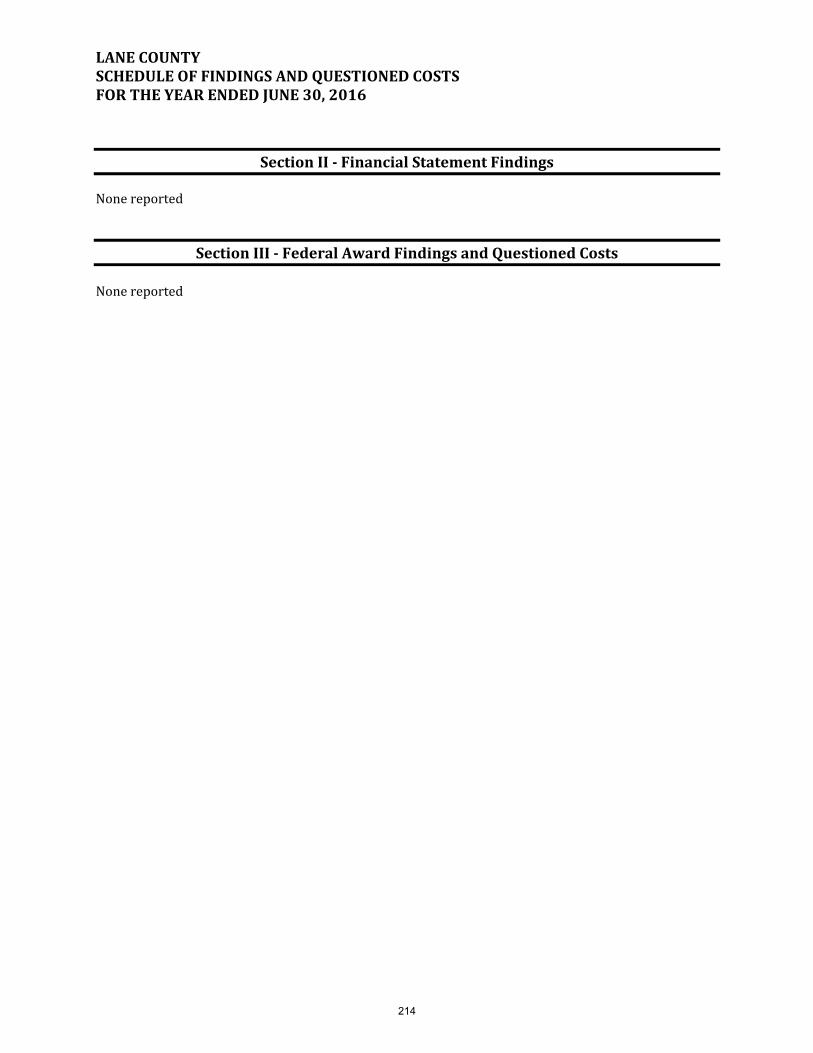

Schedule of Expenditures of Federal Awards 208 - 211Notes to Schedule of Expenditures of Federal Awards 212Schedule of Findings and Questioned Costs 213 - 214

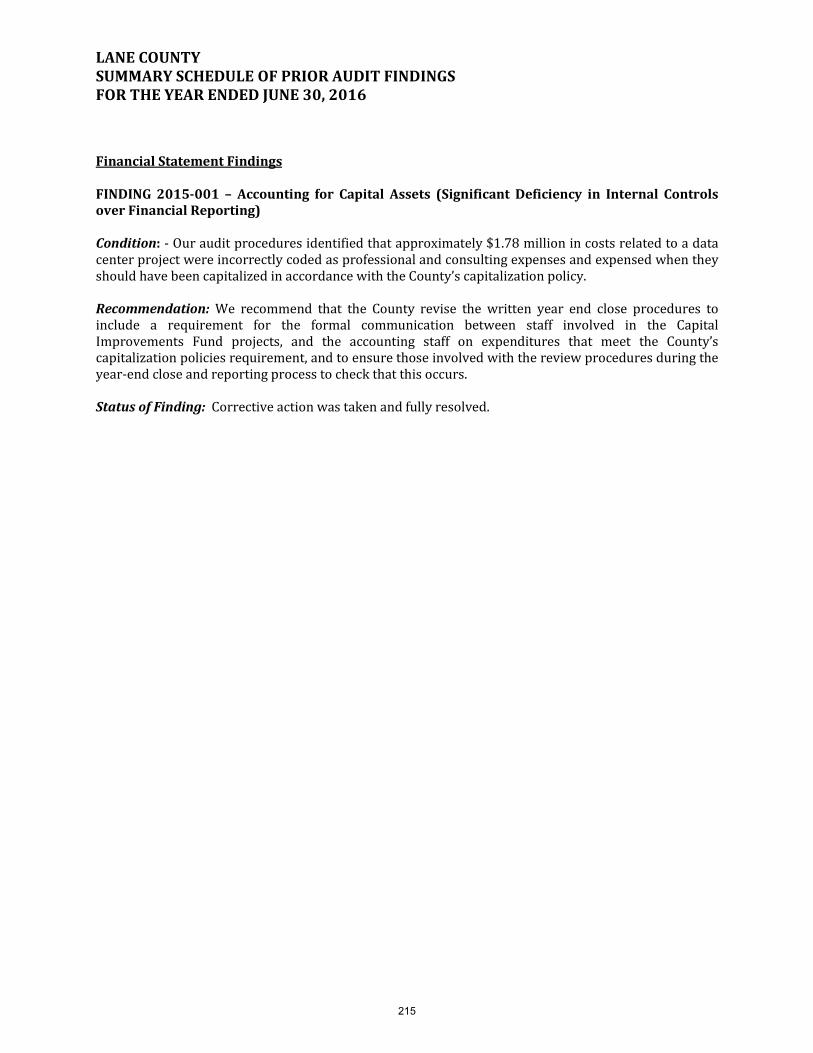

Summary Schedule of Prior Audit Findings 215

iv

Table of Contents, Continued

Comprehensive Annual Financial ReportFor the Fiscal Year Ended June 30, 2016

Lane County, Oregon

December 12, 2016 To the Board of County Commissioners and the Citizens of Lane County, Oregon We are pleased to submit the Comprehensive Annual Financial Report (CAFR) of Lane County, Oregon for the fiscal year ended June 30, 2016, together with the report of our independent certified public accountants, Moss Adams LLP. Financial Services, as part of the Operations Division of County Administration, prepares this report. This report is published to provide the Board of County Commissioners, citizens, County staff, and other readers with detailed information about the financial position and results of operations of the County, and to demonstrate fiscal and operational accountability in the use of County resources. The report consists of management’s representations concerning the finances of Lane County. Consequently, management assumes full responsibility for the completeness and reliability of all information presented in this report. To provide a reasonable basis for making these representations, County management has established a comprehensive internal control framework designed to protect Lane County’s assets from loss, theft, or misuse, and to compile sufficient reliable information for the preparation of the County’s financial statements. Because the cost of internal controls should not outweigh their benefits, the County’s comprehensive framework of internal controls is designed to provide reasonable assurance that the financial statements will be free from material misstatement. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects.

THE REPORT In accordance with Oregon law and Lane County Code, Moss Adams, LLP has audited the County’s basic financial statements. The objective of the audit is to provide reasonable assurance that the financial statements of the County for the fiscal year ended June 30, 2016, are free of material misstatement. The audit was conducted in accordance with auditing standards generally accepted in the United States of America, standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, and Minimum Standards for Audits of Oregon Municipal Corporations as prescribed by the Secretary of State, State of Oregon. The unmodified opinion rendered in this report indicates that the financial statements were prepared in accordance with generally accepted accounting principles (GAAP) accepted in the United States of America and meet the standards prescribed by the Secretary of State. The auditor’s report on these financial statements is located in the Financial Section of this report. The independent audit of the financial statements is part of a broader, federally mandated “Single Audit”. The Single Audit standards require that the independent auditor report not only on the fair presentation of the basic financial statements, but also on the County’s internal controls and legal requirements involving the administration of federal grant awards. Those reports are included in the Government Auditing Standards Section of this report. GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. Lane County’s MD&A can be found immediately following the independent auditors’ report.

PROFILE OF THE COUNTY Lane County was established in 1851 and is geographically situated on the west side of Oregon, about midway down the state’s coastline. The County encompasses 4,722 square miles and, in many ways, typifies Oregon. The county’s lands are geographically a microcosm of the state, ranging from rugged glaciated mountains in the east, through a broad valley spreading across the Willamette River mid-county, to a beautiful and rugged coastline along the western edge. Portland State University’s Population Research Center’s estimate of the 2015 population for Lane County is 362,150. Lane County’s population is increasing, with an estimated growth rate of 3 percent since 2010. Lane County is the fourth most populous county in Oregon and the third most populous metropolitan statistical area (MSA) in the state.

1

Lane County government operates under a home rule charter approved by voters in 1962. The Charter grants authority to a full-time compensated, five-person Board of County Commissioners to legislate and administer County government within the limits of that non-partisan authority. Lane County voters individually elect commissioners from specific geographic regions for four-year terms. The County operates under the provisions of the County Charter and the Lane County Code, as well as the Oregon Constitution and State law (Oregon Revised Statutes). Board action is effected by a simple majority vote of three of the five Board members. As a general purpose government, the mission of Lane County is to responsibly manage limited resources to deliver vital, customer-focused services with passion, innovation, and integrity. Lane County consists of services grouped into three categories: Public Services (Assessment and Taxation, Health & Human Services, Public Works); Public Safety (District Attorney, Department of Public Safety, Health & Human Services – Youth Services, County Administration – Parole and Probation); and Support Services (Board of Commissioners, County Administration, County Counsel, Information Services, Human Resources). As the foundation of the County’s annual financial planning and control, the budget is prepared and adopted for all County funds as required by Oregon Local Budget Law (Chapter 294 of the Oregon Revised Statutes). The board order adopting the budget establishes appropriations for expenditures within each fund which cannot legally be exceeded. The expenditure appropriations lapse at the end of the fiscal year. Additional resources and corresponding expense appropriations may be added to the budget during the fiscal year through a supplemental budget process. Original and supplemental budgets may be modified during the fiscal year by the use of appropriation transfers between categories. Budget and actual comparisons are presented in this report for each individual fund for which an appropriated annual budget has been adopted. For the General Fund, Road Fund, Special Revenue / Services Fund, Health and Human Services Fund, Trillium Behavioral Health Fund, and Local Option Tax Levy Fund, the budget and actual comparisons are presented in this report in the Required Supplementary Information section. For all other funds the budget and actual comparisons are presented in the Other Supplementary Information section of the report. Additional information on the County’s budgetary process is contained in Note II.A. of the Notes to Basic Financial Statements in this report. For financial reporting purposes, the County is a primary government under the provisions of Governmental Accounting Standards Board Statement No. 14, as amended by GASB 61. This report also includes all organizations and activities for which the elected officials exercise financial control. The County reports one discretely presented component unit; the Housing and Community Services Agency of Lane County (HACSA). The financial information of this entity is included in this report as appropriate to its relationship to the County. More information on the reporting entity and its component unit can be found in Note I.A. of the Notes to Basic Financial Statements in this report.

FINANCIAL CONDITIONS AND OUTLOOK Local Economy – While lumber and wood products remain the largest single component of the manufacturing industry in Lane County, it saw a 35 percent decline in employment between 2001 and 2010 mainly due to changes in Federal logging practices. Other top industries in the county include agriculture (with main crops being nursery crops and Christmas trees), tourism, and retail trade. As the home of several educational institutions, including the University of Oregon, multiple utility companies, and a federal courthouse, government employment helps add stability to Lane County's economy.

2

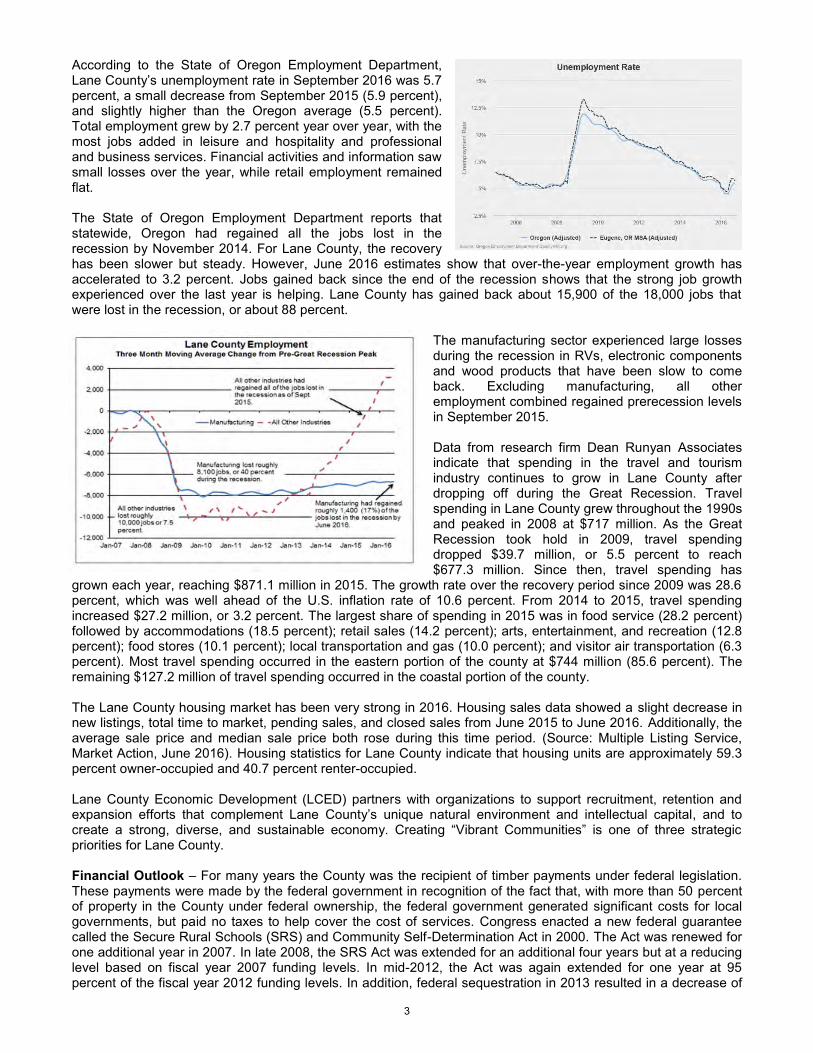

According to the State of Oregon Employment Department, Lane County’s unemployment rate in September 2016 was 5.7 percent, a small decrease from September 2015 (5.9 percent), and slightly higher than the Oregon average (5.5 percent). Total employment grew by 2.7 percent year over year, with the most jobs added in leisure and hospitality and professional and business services. Financial activities and information saw small losses over the year, while retail employment remained flat. The State of Oregon Employment Department reports that statewide, Oregon had regained all the jobs lost in the recession by November 2014. For Lane County, the recovery has been slower but steady. However, June 2016 estimates show that over-the-year employment growth has accelerated to 3.2 percent. Jobs gained back since the end of the recession shows that the strong job growth experienced over the last year is helping. Lane County has gained back about 15,900 of the 18,000 jobs that were lost in the recession, or about 88 percent.

The manufacturing sector experienced large losses during the recession in RVs, electronic components and wood products that have been slow to come back. Excluding manufacturing, all other employment combined regained prerecession levels in September 2015. Data from research firm Dean Runyan Associates indicate that spending in the travel and tourism industry continues to grow in Lane County after dropping off during the Great Recession. Travel spending in Lane County grew throughout the 1990s and peaked in 2008 at $717 million. As the Great Recession took hold in 2009, travel spending dropped $39.7 million, or 5.5 percent to reach $677.3 million. Since then, travel spending has

grown each year, reaching $871.1 million in 2015. The growth rate over the recovery period since 2009 was 28.6 percent, which was well ahead of the U.S. inflation rate of 10.6 percent. From 2014 to 2015, travel spending increased $27.2 million, or 3.2 percent. The largest share of spending in 2015 was in food service (28.2 percent) followed by accommodations (18.5 percent); retail sales (14.2 percent); arts, entertainment, and recreation (12.8 percent); food stores (10.1 percent); local transportation and gas (10.0 percent); and visitor air transportation (6.3 percent). Most travel spending occurred in the eastern portion of the county at $744 million (85.6 percent). The remaining $127.2 million of travel spending occurred in the coastal portion of the county. The Lane County housing market has been very strong in 2016. Housing sales data showed a slight decrease in new listings, total time to market, pending sales, and closed sales from June 2015 to June 2016. Additionally, the average sale price and median sale price both rose during this time period. (Source: Multiple Listing Service, Market Action, June 2016). Housing statistics for Lane County indicate that housing units are approximately 59.3 percent owner-occupied and 40.7 percent renter-occupied. Lane County Economic Development (LCED) partners with organizations to support recruitment, retention and expansion efforts that complement Lane County’s unique natural environment and intellectual capital, and to create a strong, diverse, and sustainable economy. Creating “Vibrant Communities” is one of three strategic priorities for Lane County. Financial Outlook – For many years the County was the recipient of timber payments under federal legislation. These payments were made by the federal government in recognition of the fact that, with more than 50 percent of property in the County under federal ownership, the federal government generated significant costs for local governments, but paid no taxes to help cover the cost of services. Congress enacted a new federal guarantee called the Secure Rural Schools (SRS) and Community Self-Determination Act in 2000. The Act was renewed for one additional year in 2007. In late 2008, the SRS Act was extended for an additional four years but at a reducing level based on fiscal year 2007 funding levels. In mid-2012, the Act was again extended for one year at 95 percent of the fiscal year 2012 funding levels. In addition, federal sequestration in 2013 resulted in a decrease of

3

an additional 5.1 percent of the fiscal year 2013 amount, bringing the actual revenue received down to $4.46 million. In mid-April, 2015, Congress passed an additional two-year extension of the SRS payments, at a continued 5 percent step down each year. SRS payments are not included in the fiscal year 2017 budget. The County continues to work on reducing its dependence on these federal funds. The County remains hopeful that a long-term, ongoing solution will be found, and there continues to be work at the federal, state and local levels to determine what that solution may be. Long-term Financial Planning - Long-term strategic and financial planning is an important part of ensuring excellent service and stewardship of taxpayer resources. The County makes use of two primary financial planning models. The first model is a multi-year forecast for the County’s General Fund and the second is a similar model prepared for the Road Fund. Both models are designed to predict over a multi-year horizon the outcome of certain policy choices, ranging from policy-driven expenditure reductions and revenue enhancements to externally-driven factors such as rising health care costs and fluctuating levels of timber receipts. While these financial models can be very helpful, they are not without limitations. The models are thoughtfully built on a series of assumptions that represent, at one point in time, the best judgments of information available to preparers of the model. A tolerance of a mere one or two percent can alter the model significantly when resources are scarce. Due to decreasing federal revenues and the current property tax structure, Lane County, like many local governments, has struggled with a structural deficit since the early nineties. Historically the General Fund revenues have grown around 3 percent annually, while expenses continue to increase closer to 5 percent. Lane County’s ability to increase revenues is severely constrained with statewide constitutional limitations on tax rate increases and tax ceilings. As long as the County continues to have an operating deficit – whereby continuing expenses for existing services are higher than revenue received or generated by those services – future budgets will remain unstable and there will likely be service impacts. In fiscal year 2016, the County Administrator developed a three-year plan to reduce the deficit by looking for new and innovative ways to cut expenditures and preserve critical services. While this may not completely eliminate the structural deficit due to the slow growth of revenue, it will help stabilize services and provide a good base line for policy makers to refer to when making long-term financial decisions. Major Initiatives – The Board of Commissioners adopted its Lane County Strategic Plan in November of 2014. The 2014-2017 Strategic Plan laid out a vision for the future focusing on “Priorities” because they are seen as the supporting elements for the vision of Lane County. These three focal points are the foundation of the efforts going forward: A Safe, Healthy County; Vibrant Communities; and Infrastructure. The County readily acknowledges the scarcity of resources created by the steady decline in federal timber receipts and the recent end of Secure Rural Schools funding, as well as one of the lowest county property tax rates in the state. Facing this ongoing challenge, the County is focused on two goals: 1) Enhance critical services to make our community safer, healthier and more vibrant; and 2) Create long-term financial stability through a structurally balanced budget. The County is committed to the 10-Year Public Safety Plan approved by the Board of Commissioners to begin to stabilize and repair the local public safety system by maintaining funding for priority services such as 24-hour Sheriff’s patrols, criminal prosecution, parole and probation, youth services and human services. The fiscal year 2017 budget funds several targeted investments in achieving phase two of the 10-Year Public Safety Plan. The budget includes funding for two new positions in the District Attorney’s Office to reduce the number of no-file cases by approximately 400 per year. There is also increased General Fund support for the jail to enhance services that specifically engage individuals in the corrections system in ongoing treatment services, as well as connect individuals to community-based services upon release. The goal of enhancing these services is to reduce the number of individuals continuously cycling through the corrections system and connect them with proven treatment services that break the cycle of crime. The County continues efforts to improve the overall public safety system, particularly related to the intersection of behavioral health services with the criminal justice system. This work is in collaboration with many partners, including law enforcement, defense and prosecuting attorneys and court personnel, and is aimed at addressing

4

the needs of individuals who are frequent utilizers of crisis, jail and emergency services. Advances in this work include:

A new community crisis center will address the needs of individuals experiencing a mental health crisis that would otherwise be utilizing the emergency rooms or jail

Expansion of other crisis services including CAHOOTS and crisis respite housing options Expansion of the Jail Intercept program for individuals in the jail system that can be better served at Lane

County Behavioral Health; the goal of this program is to reduce the number of individuals cycling through the criminal justice system by engaging them in ongoing mental health services

In May 2013, voters passed a limited local option levy property tax in the amount of $0.55 per $1,000 maximum assessed value to restore jail beds and critical youth service for a period of five years. The purpose of the levy is to rebuild the public safety system and a means of finding funding sources other than the decreasing timber funds to provide critical services to residents. Due to reduced expenses during the first two years, in 2016, the tax rate was lowered to $0.38 per $1,000 maximum assessed value, thus reducing the costs to the taxpayers. The County continues to focus on reducing internal costs, such as health insurance, debt, vehicles and other expenses. Health insurance costs in the marketplace are projected to increase nearly ten percent next year. Lane County’s health insurance costs, however, are estimated to be nearly flat at approximately 1.5 percent growth from the prior year. This is due to the shift to a self-funded health insurance model in 2015 and the continued investment in various wellness initiatives that seek to improve health and control costs. The County also targeted and successfully achieved cost reductions for County vehicles, as well as reduced costs for computers. The County goal is to reduce the vehicle fleet by 10 percent over the next two years to continue to shrink costs. Also, the County will use one-time reserves to reduce debt obligations to reduce ongoing costs. Relevant Financial Policies – The County has adopted financial and budget policies to support the County’s strategic goals, ensure stability in service delivery and promote the efficient use of public funds. It is Lane County’s policy to establish reserve funds which can be used to reduce the impact of substantial revenue fluctuations, thus providing for a more stable delivery of services to Lane County citizens. Reserves can be observed as part of cash and cash equivalents, as well as fund balance.

AWARDS AND ACKNOWLEDGEMENTS Certificate of Achievement – The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to Lane County, Oregon for its comprehensive annual financial report for the fiscal year ended June 30, 2015. This was the thirteenth consecutive year that Lane County has achieved this award. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program’s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate. Acknowledgements - The preparation of this CAFR would not have been possible without the dedicated services of the Financial Services staff. We extend our sincere appreciation for their assistance in the preparation of this report. We also acknowledge the cooperation and assistance of other County staff contributing to this effort. Finally, we extend appreciation to the County Administrator, the members of the Finance & Audit Committee and the Board of County Commissioners for their interest and support in managing the financial operations of Lane County. Respectfully submitted,

Greg Rikhoff Robert Tintle Director of Operations Financial Services Manager

5

6

7

8

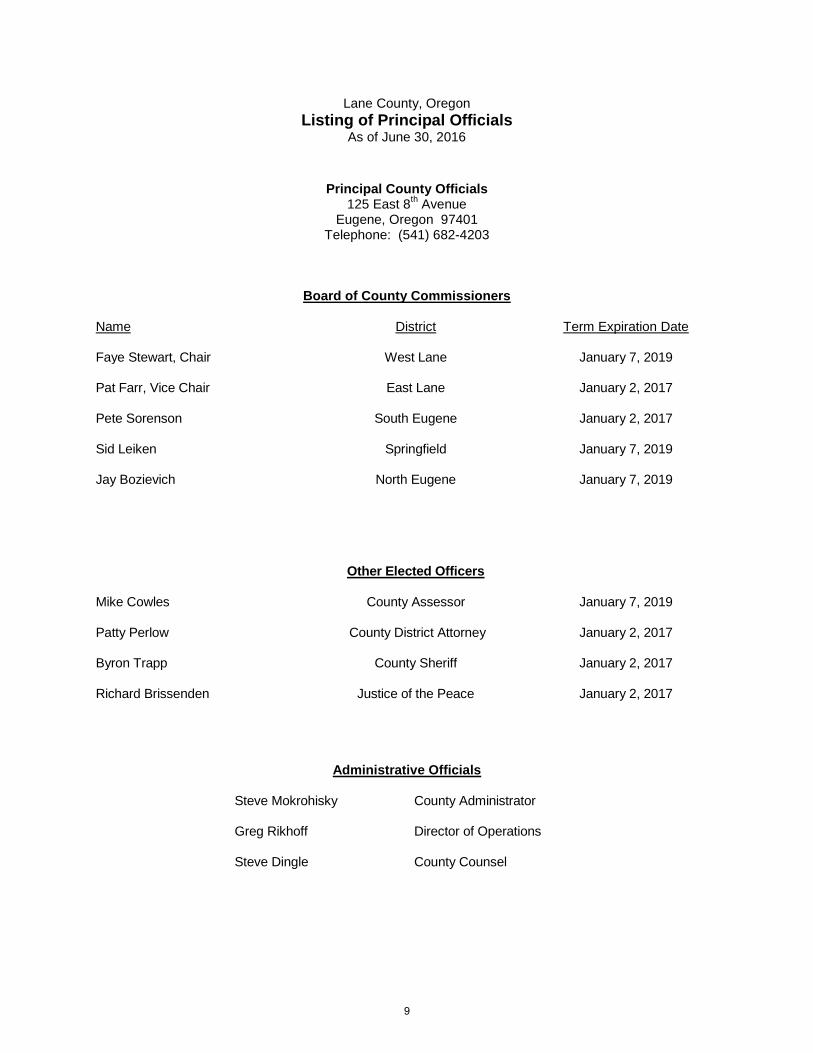

Lane County, Oregon Listing of Principal Officials

As of June 30, 2016

Principal County Officials 125 East 8th Avenue

Eugene, Oregon 97401 Telephone: (541) 682-4203

Board of County Commissioners Name District Term Expiration Date Faye Stewart, Chair West Lane January 7, 2019 Pat Farr, Vice Chair East Lane January 2, 2017 Pete Sorenson South Eugene January 2, 2017 Sid Leiken Springfield January 7, 2019 Jay Bozievich North Eugene January 7, 2019 Other Elected Officers Mike Cowles County Assessor January 7, 2019 Patty Perlow County District Attorney January 2, 2017 Byron Trapp County Sheriff January 2, 2017 Richard Brissenden Justice of the Peace January 2, 2017

Administrative Officials Steve Mokrohisky

Greg Rikhoff

County Administrator Director of Operations

Steve Dingle County Counsel

9

10

FINANCIAL SECTION

INDEPENDENT AUDITOR’S REPORT

REPORTOFINDEPENDENTAUDITORSBoardofCountyCommissionersLaneCounty,OregonReportontheFinancialStatementsWe have audited the accompanying financial statements of the governmental activities, the business‐typeactivities, the discretely presented component unit, each major fund, and the aggregate remaining fundinformationofLaneCounty,Oregon(the“County”)asofandfortheyearendedJune30,2016,andtherelatednotestothefinancialstatements,whichcollectivelycomprisetheCounty’sbasicfinancialstatementsaslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyaccepted intheUnitedStatesofAmerica;this includesthedesign,implementation,andmaintenanceofinternalcontrolrelevanttothepreparationandfairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditor’sResponsibilityOurresponsibilityistoexpressopinionsonthesefinancialstatementsbasedonouraudit.Wedidnotauditthe financial statementsof theHousingandCommunityServicesAgencyofLaneCounty (“HACSA”),whichrepresent100%oftheassets,netposition,andrevenuesofthediscretelypresentedcomponentunitoftheCounty. Thosestatementswereauditedbyotherauditors,whosereporthasbeenfurnishedtous,andouropinion, insofaras it relates to theamounts included forHACSA, isbasedsolelyon thereportof theotherauditors.We conducted our audit in accordancewith auditing standards generally accepted in theUnitedStates of America and the standards applicable to financial audits contained in Government AuditingStandards,issuedbytheComptrollerGeneraloftheUnitedStates.Thosestandardsrequirethatweplanandperform the audit to obtain reasonable assurance about whether the financial statements are free frommaterialmisstatement.Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthefinancialstatements.Theproceduresselecteddependontheauditor’sjudgment,includingtheassessmentoftherisksofmaterialmisstatementofthefinancialstatements,whetherduetofraudorerror.Inmakingthoserisk assessments, the auditor considers internal control relevant to the entity’s preparation and fairpresentation of the financial statements in order to design audit procedures that are appropriate in thecircumstances,butnotforthepurposeofexpressinganopinionontheeffectivenessoftheentity’sinternalcontrol.Accordingly,weexpressnosuchopinion.Anauditalso includesevaluating theappropriatenessofaccountingpoliciesusedandthereasonablenessofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinions.

11

OpinionsInouropinion,basedonourauditandthereportofotherauditors,thefinancialstatementsreferredtoabovepresent fairly, in allmaterial respects, the respective financial position of the governmental activities, thebusiness‐type activities, the discretely presented component unit, each major fund, and the aggregateremainingfundinformationoftheCountyasofJune30,2016,andtherespectivechangesinfinancialpositionand,whereapplicable,cashflowsthereoffortheyearthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.OtherMattersRequiredSupplementaryInformationAccounting principles generally accepted in the United States of America require that the management’sdiscussionandanalysisonpages14through26;theschedulesofrevenues,expendituresandchangesinfundbalance – budget and actual and related notes (“the budgetary schedules”); the schedule of the County’sproportionate share of the net pension liability and schedule County contributions for the Oregon PublicEmployees’ Retirement System; and the schedule of OPEB funding progress on pages 91 through 100, bepresented to supplement thebasic financial statements. Such information, althoughnot apartof thebasicfinancialstatements,isrequiredbytheGovernmentalAccountingStandardsBoardwhoconsidersittobeanessentialpartoffinancialreportingforplacingthebasicfinancialstatementsinanappropriateoperational,economic,orhistoricalcontext.Wehaveappliedcertainlimitedprocedurestothemanagement’sdiscussionandanalysis,thescheduleoftheCounty’sproportionateshareof thenetpension liabilityandscheduleCountycontributionsfortheOregonPublic Employees’ Retirement System; and the schedule of OPEB funding progress in accordance withauditing standards generally accepted in the United States of America, which consisted of inquiries ofmanagementaboutthemethodsofpreparingtheinformationandcomparingtheinformationforconsistencywith management's responses to our inquiries, the basic financial statements, and other knowledge weobtained during our audit of the basic financial statements.Wedo not express an opinion or provide anyassuranceonthe informationbecausethe limitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.Our auditwas conducted for thepurpose of formingopinionson the financial statements that collectivelycomprise the County's basic financial statements. The budgetary schedules described above are theresponsibilityofmanagementandwerederived fromand relatedirectly to theunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements.Thebudgetaryscheduleshavebeensubjectedtothe auditing procedures applied in the audit of the basic financial statements and certain additionalprocedures,includingcomparingandreconcilingsuchinformationdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatementsortothebasicfinancialstatementsthemselves,and other additional procedures in accordance with auditing standards generally accepted in the UnitedStatesofAmerica.Inouropinion,thebudgetaryschedulesarefairlystated,inallmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.SupplementaryInformationOur auditwas conducted for thepurpose of formingopinionson the financial statements that collectivelycomprise the County's basic financial statements. The other supplementary information on pages 101through156,andthescheduleofexpendituresoffederalawardsonpages208through212,asrequiredbyTitle2U.S.CodeofFederalRegulations(CFR)Part200,UniformAdministrativeRequirements,CostPrinciples,and Audit Requirements for Federal Awards; each as listed in the table of contents (collectively, thesupplementaryinformation),arepresentedforpurposesofadditionalanalysisandisnotarequiredpartofthebasicfinancialstatements.

12

The supplementary information is the responsibility of management and was derived from and relatesdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements.Suchinformation has been subjected to the auditing procedures applied in the audit of the basic financialstatementsandcertainadditionalprocedures,includingcomparingandreconcilingsuchinformationdirectlytotheunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatementsortothebasicfinancial statements themselves, and other additional procedures in accordance with auditing standardsgenerally accepted in the United States of America. In our opinion, the other supplementary information,other financial schedules, and schedule of expenditures of federal awards are fairly stated, in allmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.OtherInformation

Our auditwas conducted for thepurpose of formingopinionson the financial statements that collectivelycomprise the County’s basic financial statements. The introductory section and statistical section arepresentedforpurposesofadditionalanalysisandarenotarequiredpartofthebasicfinancialstatements.Theintroductorysectionandstatisticalsectionhavenotbeensubjectedtotheauditingproceduresappliedinthe audit of the basic financial statements, and accordingly,we do not express on opinion or provide anyassuranceonit.

ReportsofOtherLegalandRegulatoryRequirementsOtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedDecember12,2016on our consideration of the County's internal control over financial reporting and on our tests of itscompliancewithcertainprovisionsoflaws,regulations,contracts,andgrantagreementsandothermatters.Thepurposeofthatreportistodescribethescopeofourtestingofinternalcontroloverfinancialreportingandcomplianceandtheresultsofthattesting,andnottoprovideanopiniononinternalcontroloverfinancialreporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards in considering the County's internal control over financial reporting andcompliance.OtherReportingRequiredbyMinimumStandardsforAuditsofOregonMunicipalCorporationsInaccordancewiththeMinimumStandardsforAuditsofOregonMunicipalCorporations,wehaveissuedourreportdatedDecember12,2016,onourconsiderationoftheCounty’scompliancewithcertainprovisionsoflaws and regulations, including the provisions of Oregon Revised Statutes as specified in OregonAdministrativeRules.Thepurposeofthatreportistodescribethescopeofourtestingofcomplianceandtheresultsofthattestingandnottoprovideanopiniononcompliance.

ForMossAdamsLLPEugene,OregonDecember12,2016

13

Management’s Discussion and Analysis The management of Lane County, Oregon (County) presents this narrative overview to facilitate both a short-term and long-term analysis of the financial activities of the County for the fiscal year ended June 30, 2016. This Management’s Discussions and Analysis (MD&A) is based on currently known facts, decisions, and conditions that existed as of the date of the independent auditor’s report. Additional information outside the scope of this analysis can be found in the Letter of Transmittal.

Financial Highlights

The assets and deferred outflows of resources of Lane County exceeded its liabilities and deferred inflows of resources at June 30, 2016, by $431.9 million (total net position). The County’s unrestricted portion of net position is $23.5 million, while restricted net position is $80.5 million, both of which may be used to meet the County’s ongoing obligations to citizens and creditors.

Net Position decreased from $454.8 million to $431.9, a decrease of $22.9 million. The decrease is mainly

due to the recognition of the County’s portion of the OPERS net pension liability. The Oregon Supreme Court decision in Moro v. State of Oregon, issued on April 30, 2015, reversed a significant portion of the reductions in the 2013 Oregon Legislature made to future system Cost of Living Adjustments (COLA) through Senate Bills 822 and 861. This reversal increased the benefits projected to be paid by employers compared to those developed in the prior actuarial valuation, and consequently increased plan liabilities and resulted in a significant increase in the County’s pension expense and net pension liability. Adjusting for the impact of the Moro Decision, the County recognized net pension expense of $61.2 million. This amount was allocated to the functions on the Statement of Activities based on their share of the pension obligation, resulting in a significant increase in the overall direct expenses and decrease in net position. Additionally, at June 30, 2015, the County reported a net pension asset of $25 million. Conversely, at June 30, 2016, the County reported a net pension liability of $63.6 million.

At June 30, 2016, the County’s governmental funds reported combined ending fund balances of $139.4 million, an increase of $23.3 million. The majority of the increase is a direct result of the public safety local option tax levy that generated $6.2 million in additional spendable fund balances by year end and $8.4 million from the administration of the behavioral health benefits to Oregon Health Plan members, funded through a contract with Trillium Community Health. Approximately $67.8 million is available for spending by the board.

Spendable, non-restricted fund balance for the General Fund is $15.3 million at the end of the current fiscal

year, or 23.3 percent of General Fund total revenues.

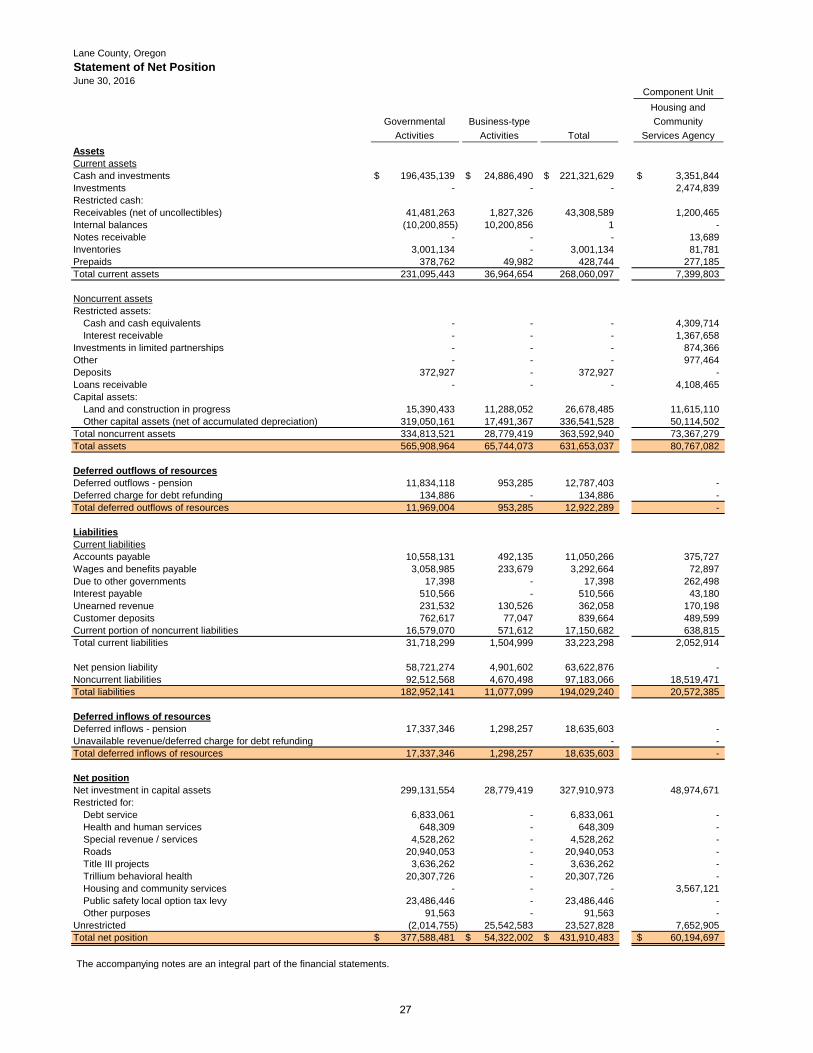

Overview of the Financial Statements The following discussion and analysis is intended to serve as an introduction to Lane County’s basic financial statements. The County’s basic financial statements comprise three components: 1) government-wide financial statements, 2) fund financial statements and 3) notes to basic financial statements. This report also contains other supplementary information in addition to the basic financial statements. Government-wide financial statements. The government-wide financial statements are designed to provide readers with a broad overview of the Lane County’s finances, in a manner similar to a private-sector business. The Statement of Net Position presents information on all of the Lane County’s assets, deferred outflows of resources, liabilities and deferred inflows of resources. Assets and deferred outflows of resources less liabilities and deferred inflows of resources are reported as total net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the County is improving or deteriorating.

14

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

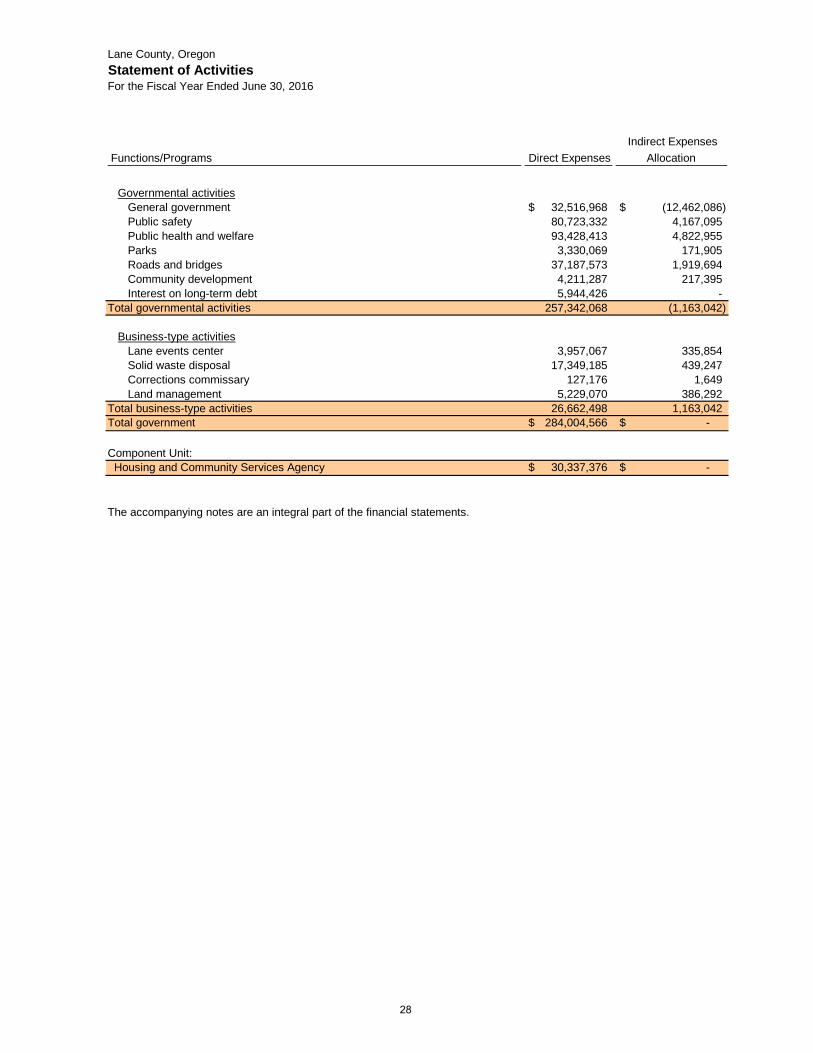

The Statement of Activities presents information showing how the County’s net position changed during fiscal year ended June 30, 2016. Changes in net position are reported when the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will result in cash flows in a future fiscal period. Examples include property taxes and accrued compensated absences. Each of these government-wide financial statements, Statement of Net Position and Statement of Activities, distinguish functions of the County that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all, or a significant portion of, their costs through charges for services (business-type activities). The governmental activities of the County include the following:

General government Public health and welfare Roads and bridges

Public safety Parks Community development

The business-type activities of the County include the following:

Lane events center Corrections commissary

Solid waste disposal Land management

The government-wide financial statements include not only Lane County, the primary government, but also the legally separate Housing and Community Services Agency of Lane County (HACSA), for which Lane County is financially accountable. Although HACSA is legally separate and provides no financial benefit or burden to Lane County, HACSA’s governing body is substantially identical to Lane County’s. As a result HACSA’s financial statements are discretely presented in the County’s financial statements. There was no change to the governing body of HACSA during fiscal year 2016. See pages 43-44 and 71-73 of this report for more information. The government-wide financial statements also include the Lane Events Center, a division of Public Works. The operation of the Lane Events Center is managed by a director who reports to the county administrator, while the County Fair is governed by a separate Fair Board appointed by the Board of County Commissioners. The government-wide financial statements can be found on pages 27-29 of this report. Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. Lane County, like other state and local governmental entities, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the County can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental funds. Governmental funds are used to account for many of the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on the acquisition and use of current spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating the County’s near-term requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the County’s near-term financial decisions. Both the governmental fund balance sheet and statements of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. These reconciliations can be found on pages 33 and 37 of this report. The County maintains 19 individual governmental funds made up of 1 general fund, 13 special revenue funds, 3 debt service funds, and 2 capital projects funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statements of revenues, expenditures, and changes in fund balances for the General Fund, Road, Special Revenue/Services, Health and Human Services, Trillium Behavioral Health, and Local Option Tax Levy special revenue funds, all of which are considered to be major funds. Data from the other 16 governmental funds are combined into a single, aggregated presentation. Summary data by fund-type for these nonmajor governmental funds is provided in the form of combining statements on pages 101-102 of this

15

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

report. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements on pages 104-107, 117-118 and 123-124. The basic governmental fund financial statements can be found on pages 30-31 and 34-35. Proprietary funds. The County maintains two different types of proprietary funds – enterprise funds and internal service funds. Enterprise funds are used to report the same functions presented as business-type activities in the governmental-wide financial statements. The County uses enterprise funds to account for the events center, solid waste disposal operations, corrections commissary operations, and land management functions. Internal service funds are an accounting device used to accumulate and allocate costs internally among the County’s various functions. The County uses internal service funds to account for its self-insurance and employee benefits activities, pension bond servicing, motor pool operations, intergovernmental services activities, technology (PC) replacement and information services activities, and retiree medical benefits. Because internal service funds predominantly benefit governmental rather than business-type functions, these fund assets, deferred outflows, liabilities, and deferred inflows have been included with governmental activities in the government-wide financial statements. Proprietary funds provide the same type of information as reported for the business-type activities in the government-wide financial statements, but in more detail. The proprietary fund financial statements provide separate information for the solid waste disposal operations, which is considered to be a major fund of the County. Conversely, the three remaining enterprise funds are combined into a single, aggregated presentation in the proprietary fund financial statements, as are all internal service funds. Individual fund data for the three nonmajor enterprise funds and each of the internal service funds is provided in the form of combining statements on pages 127-129 and 136-141 of this report. The basic proprietary fund financial statements can be found on pages 38-40 of this report. Fiduciary funds. Fiduciary funds are used to account for resources held for the benefit of parties outside the County. Fiduciary funds are not reflected in the government-wide financial statements because the resources are not available to support the County’s own programs. The accounting used for fiduciary funds is similar to that used for proprietary funds. The basic fiduciary fund financial statements can be found on page 41 of this report. The statement of changes in assets and liabilities in agency funds can be found on page 151. Budgetary comparisons. The County adopts an annual appropriated budget for all its funds except for agency funds. To demonstrate compliance, budgetary comparison statements have been provided for major funds as part of the basic financial statements on pages 91-96 of this report. Budgetary comparisons for all other funds are provided on pages 108-115, 119-121, 125-126,130-133 and 142-149 of this report. Notes to basic financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages 43-89 of this report. Other information. In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information. Budget-to-actual comparisons for the General Fund and the Road, Special Revenue/Services, Health and Human Services, Trillium Behavioral Health, and Local Option Tax Levy special revenue funds are presented in this section, along with reconciliations between the budgetary basis of accounting and Generally Accepted Accounting Principles (GAAP). The schedule of OPEB funding progress is presented in this section concerning the County’s progress in funding its obligation to provide other post-employment benefits (OPEB) to its employees. The information related to the pension plan is also presented as the schedule of County contributions, and the schedule of the County’s proportionate share of the net pension liability. This required supplementary information is found on pages 98-99 of this report. The combining statements for the nonmajor governmental funds, enterprise funds, and internal service funds are presented immediately following the required supplementary information as Other Supplementary Information.

16

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

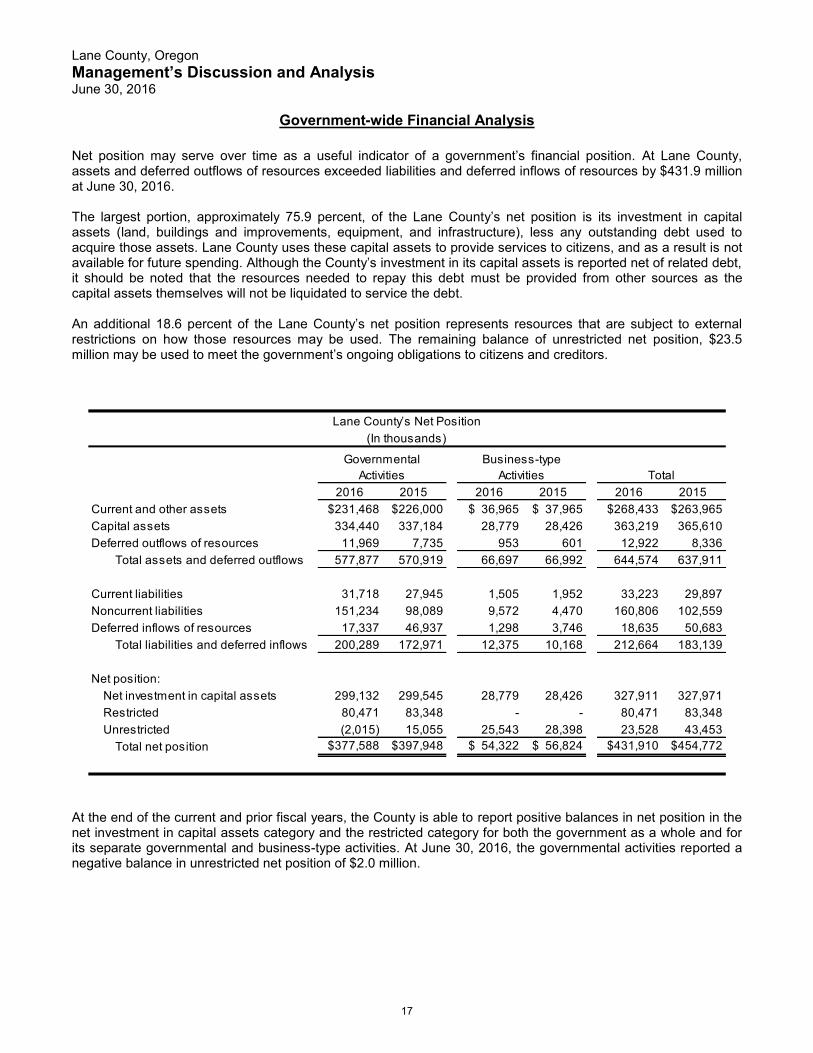

Government-wide Financial Analysis

Net position may serve over time as a useful indicator of a government’s financial position. At Lane County, assets and deferred outflows of resources exceeded liabilities and deferred inflows of resources by $431.9 million at June 30, 2016. The largest portion, approximately 75.9 percent, of the Lane County’s net position is its investment in capital assets (land, buildings and improvements, equipment, and infrastructure), less any outstanding debt used to acquire those assets. Lane County uses these capital assets to provide services to citizens, and as a result is not available for future spending. Although the County’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources as the capital assets themselves will not be liquidated to service the debt. An additional 18.6 percent of the Lane County’s net position represents resources that are subject to external restrictions on how those resources may be used. The remaining balance of unrestricted net position, $23.5 million may be used to meet the government’s ongoing obligations to citizens and creditors.

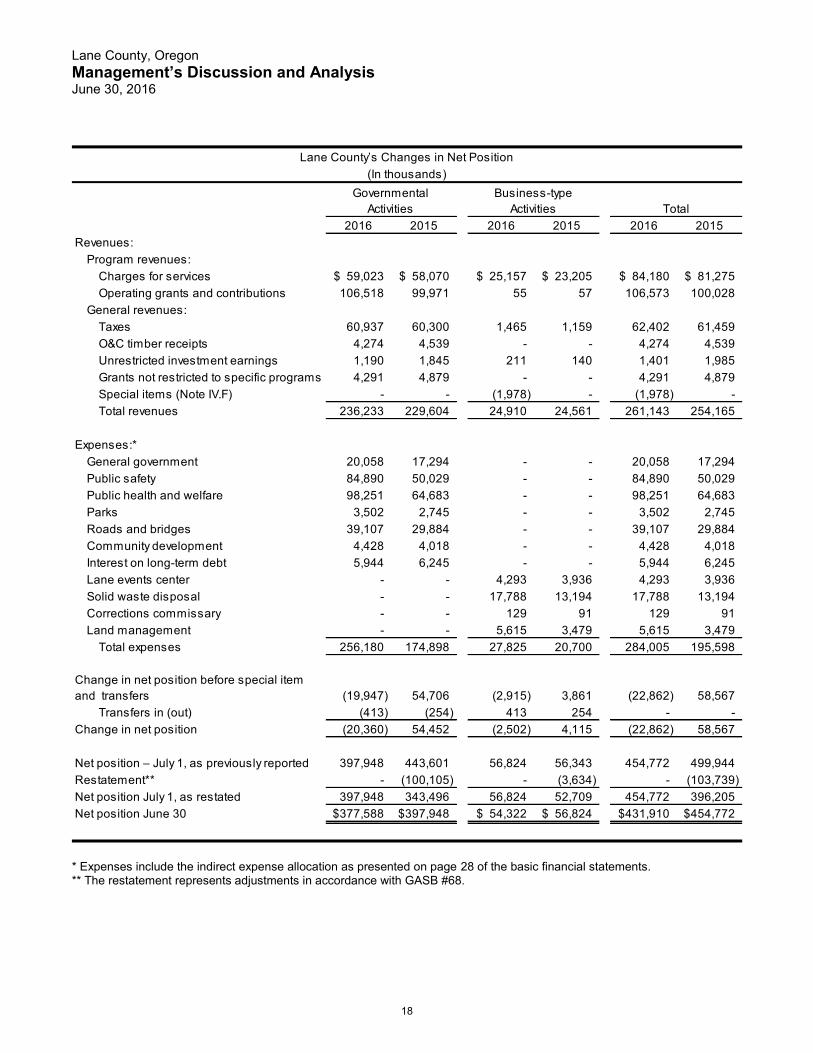

2016 2015 2016 2015 2016 2015Current and other assets $231,468 $226,000 $ 36,965 $ 37,965 $268,433 $263,965 Capital assets 334,440 337,184 28,779 28,426 363,219 365,610 Deferred outflows of resources 11,969 7,735 953 601 12,922 8,336

Total assets and deferred outflows 577,877 570,919 66,697 66,992 644,574 637,911

Current liabilities 31,718 27,945 1,505 1,952 33,223 29,897 Noncurrent liabilities 151,234 98,089 9,572 4,470 160,806 102,559 Deferred inflows of resources 17,337 46,937 1,298 3,746 18,635 50,683

Total liabilities and deferred inflows 200,289 172,971 12,375 10,168 212,664 183,139

Net position:Net investment in capital assets 299,132 299,545 28,779 28,426 327,911 327,971 Restricted 80,471 83,348 - - 80,471 83,348 Unrestricted (2,015) 15,055 25,543 28,398 23,528 43,453

Total net position $377,588 $397,948 $ 54,322 $ 56,824 $431,910 $454,772

Governmental Activities Total

Lane County’s Net Position (In thousands)

Business-type Activities

At the end of the current and prior fiscal years, the County is able to report positive balances in net position in the net investment in capital assets category and the restricted category for both the government as a whole and for its separate governmental and business-type activities. At June 30, 2016, the governmental activities reported a negative balance in unrestricted net position of $2.0 million.

17

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

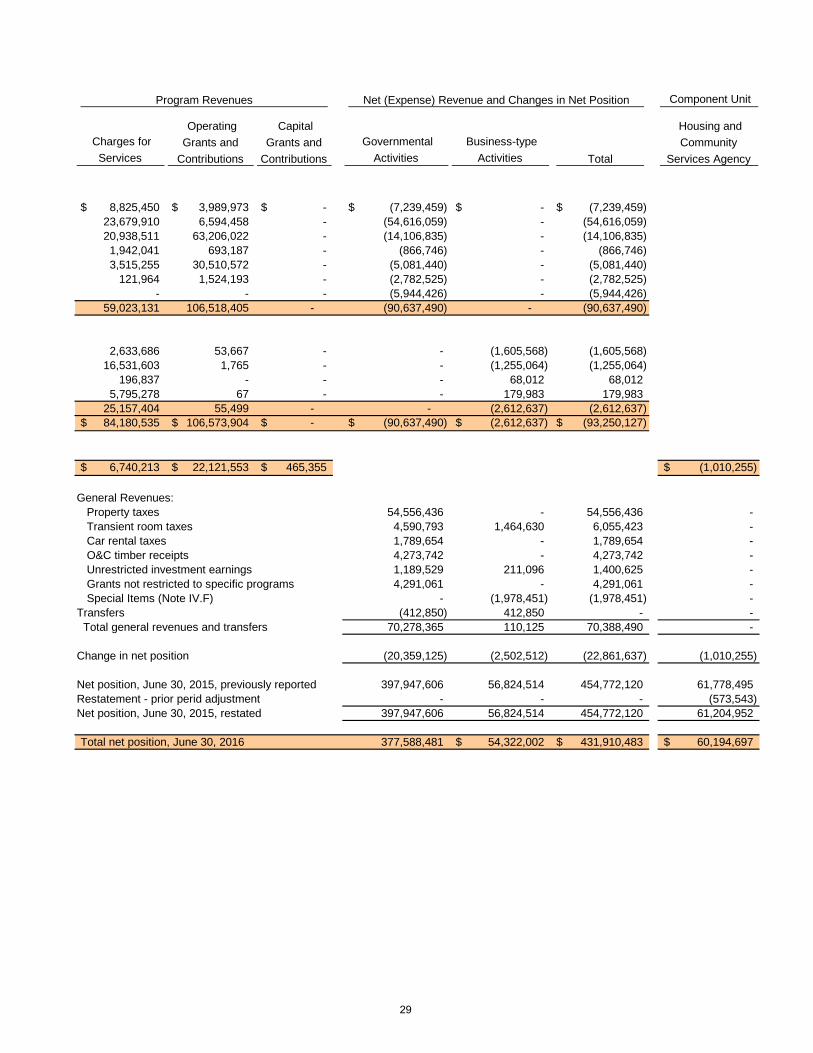

2016 2015 2016 2015 2016 2015Revenues:

Program revenues:Charges for services 59,023$ 58,070$ 25,157$ 23,205$ 84,180$ 81,275$ Operating grants and contributions 106,518 99,971 55 57 106,573 100,028

General revenues:Taxes 60,937 60,300 1,465 1,159 62,402 61,459 O&C timber receipts 4,274 4,539 - - 4,274 4,539 Unrestricted investment earnings 1,190 1,845 211 140 1,401 1,985 Grants not restricted to specific programs 4,291 4,879 - - 4,291 4,879 Special items (Note IV.F) - - (1,978) - (1,978) - Total revenues 236,233 229,604 24,910 24,561 261,143 254,165

Expenses:*General government 20,058 17,294 - - 20,058 17,294 Public safety 84,890 50,029 - - 84,890 50,029 Public health and welfare 98,251 64,683 - - 98,251 64,683 Parks 3,502 2,745 - - 3,502 2,745 Roads and bridges 39,107 29,884 - - 39,107 29,884 Community development 4,428 4,018 - - 4,428 4,018 Interest on long-term debt 5,944 6,245 - - 5,944 6,245 Lane events center - - 4,293 3,936 4,293 3,936 Solid waste disposal - - 17,788 13,194 17,788 13,194 Corrections commissary - - 129 91 129 91 Land management - - 5,615 3,479 5,615 3,479

Total expenses 256,180 174,898 27,825 20,700 284,005 195,598

Change in net position before special item and transfers (19,947) 54,706 (2,915) 3,861 (22,862) 58,567

Transfers in (out) (413) (254) 413 254 - - Change in net position (20,360) 54,452 (2,502) 4,115 (22,862) 58,567

Net position – July 1, as previously reported 397,948 443,601 56,824 56,343 454,772 499,944 Restatement** - (100,105) - (3,634) - (103,739) Net position July 1, as restated 397,948 343,496 56,824 52,709 454,772 396,205 Net position June 30 377,588$ 397,948$ 54,322$ 56,824$ 431,910$ 454,772$

Governmental Activities

Business-type Activities Total

Lane County’s Changes in Net Position(In thousands)

* Expenses include the indirect expense allocation as presented on page 28 of the basic financial statements. ** The restatement represents adjustments in accordance with GASB #68.

18

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

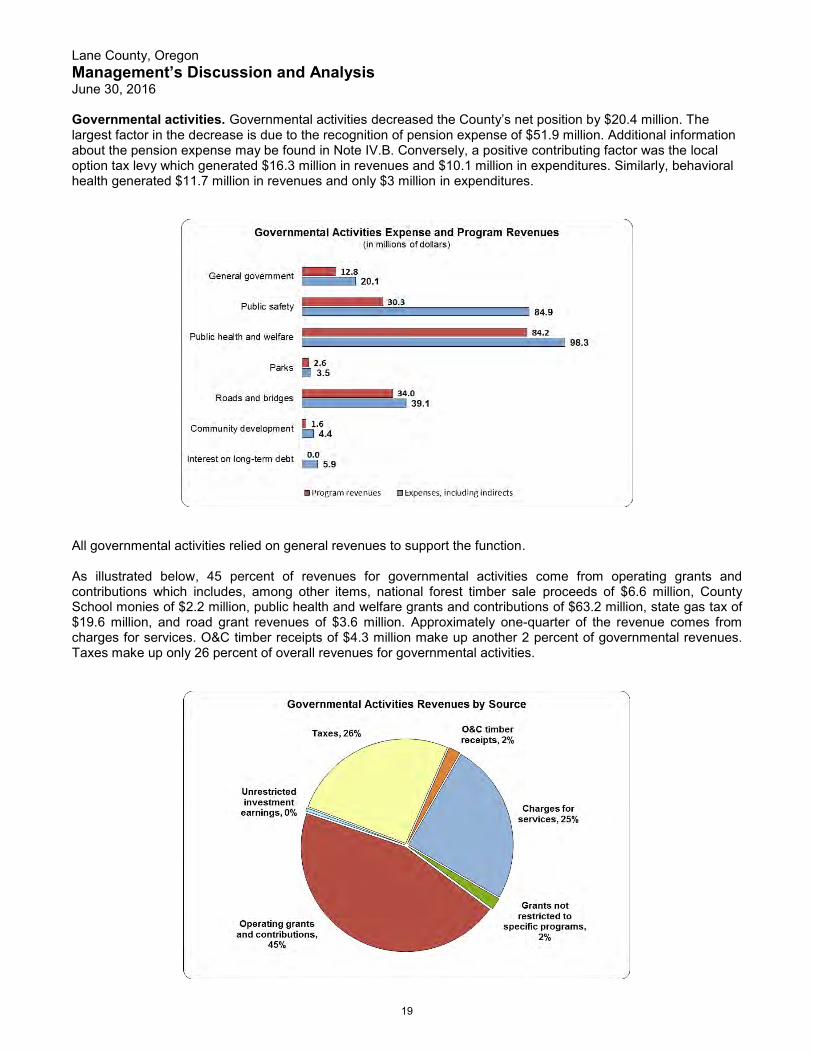

Governmental activities. Governmental activities decreased the County’s net position by $20.4 million. The largest factor in the decrease is due to the recognition of pension expense of $51.9 million. Additional information about the pension expense may be found in Note IV.B. Conversely, a positive contributing factor was the local option tax levy which generated $16.3 million in revenues and $10.1 million in expenditures. Similarly, behavioral health generated $11.7 million in revenues and only $3 million in expenditures.

All governmental activities relied on general revenues to support the function. As illustrated below, 45 percent of revenues for governmental activities come from operating grants and contributions which includes, among other items, national forest timber sale proceeds of $6.6 million, County School monies of $2.2 million, public health and welfare grants and contributions of $63.2 million, state gas tax of $19.6 million, and road grant revenues of $3.6 million. Approximately one-quarter of the revenue comes from charges for services. O&C timber receipts of $4.3 million make up another 2 percent of governmental revenues. Taxes make up only 26 percent of overall revenues for governmental activities.

19

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

Business-type activities. Business–type activities decreased the County’s net position by $2.5 million. The major component of the decrease came from the Solid Waste Disposal fund due to an equipment write-off of $2 million for a reverse osmosis wastewater treatment system intended to treat all of the landfill’s leachate on-site. The system was discontinued due to the failed performance and an uncompleted residuals management system. Also contributing to an overall net position decrease in business-type activities is due to the recognition of pension expense of $4.7 million for the fiscal year.

Within the business-type activities, only corrections commissary and land management activities generated sufficient operating revenues during fiscal year 2016 to cover operating expenses. Approximately 94 percent of the revenues for business-type activities come from charges for services, as illustrated below, with only about 5 percent generated by transient room taxes.

20

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

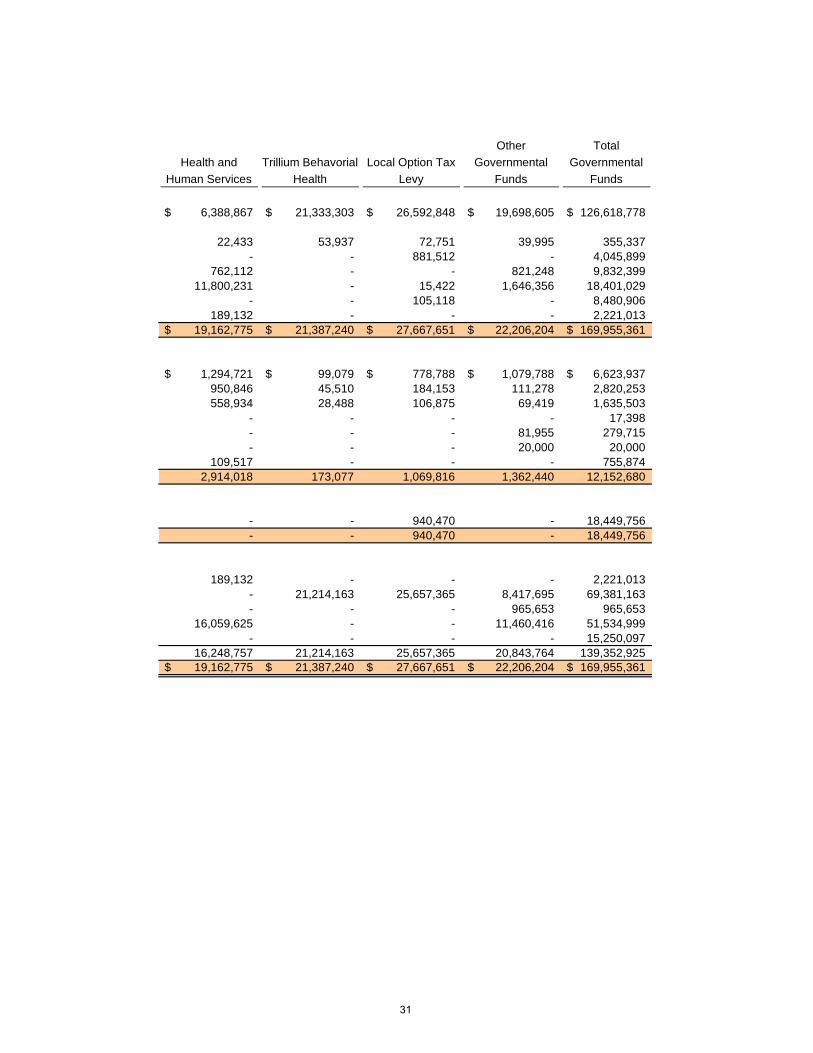

Fund-based Financial Analysis

The County uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental funds. The focus of the County’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the County’s financing requirements. In particular, spendable, non-restricted fund balance may serve as a useful measure of the County’s net resources available for spending at the end of the fiscal year. As of June 30, 2016 Lane County’s governmental funds reported combined ending fund balances of $139.4 million, an increase of $23.3 million over fiscal year 2015. Approximately $67.8 million, 48.6 percent, constitutes spendable, non-restricted fund balance which is available for appropriation in the subsequent year by the Board of County Commissioners. The remaining fund balance is either externally restricted by creditors, grantors, contributors, or laws/regulations, or internally restricted by law through constitutional provisions or enabling legislation ($69.4 million), or is not available for new spending because it represents amounts that have already been spent ($2.2 million in inventories). The General Fund is the chief operating fund of the County. At June 30, 2016 total fund balance for the General Fund was $15.5 million. Of this amount, $15.3 million is reported as unassigned. As a measure of the General Fund’s ability to liquidate fund liabilities, it may be useful to compare both spendable, non-restricted fund balance to total fund revenues. At the end of the current fiscal year, spendable, non-restricted fund balance represented 23.3 percent of total General Fund revenues and total fund balance represents 23.6 percent of those same revenues. The fund balance of the General Fund decreased $2.1 million from the prior year. Fiscal year 2016 reported an increase in taxes and assessments revenue of $2.4 million over the prior year. However, expenditures in public safety increased $4.4 during the same period. This increase is due to Patrol Services transferring into the General Fund following the elimination of Road Fund support. During fiscal year 2016, the ending fund balance of the Road Fund increased by $1.3 million to $28.9 million. The increase is due to a combination of an increase in State Highway Trust Funds (gas tax revenue) of $0.5 million over the prior year, and a decrease in expenditures of $0.6 million (due to the Volunteer Separation Incentive Program (VSIP), a mild winter, and savings in road work supplies).

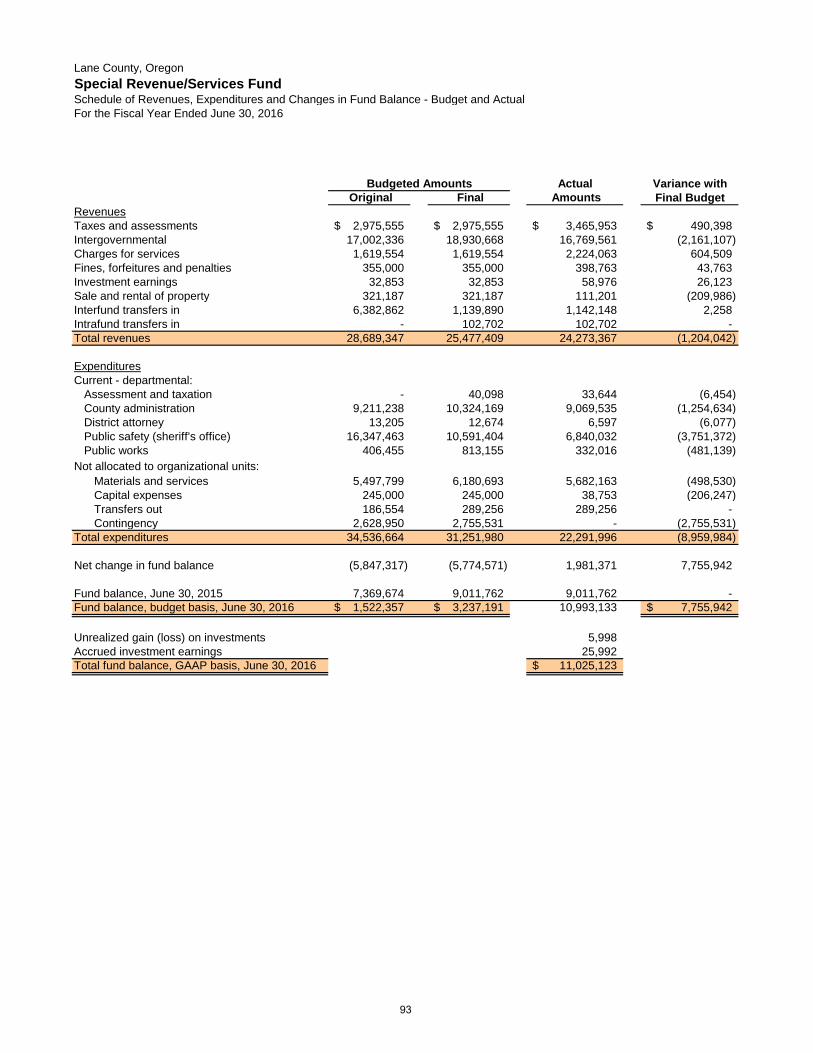

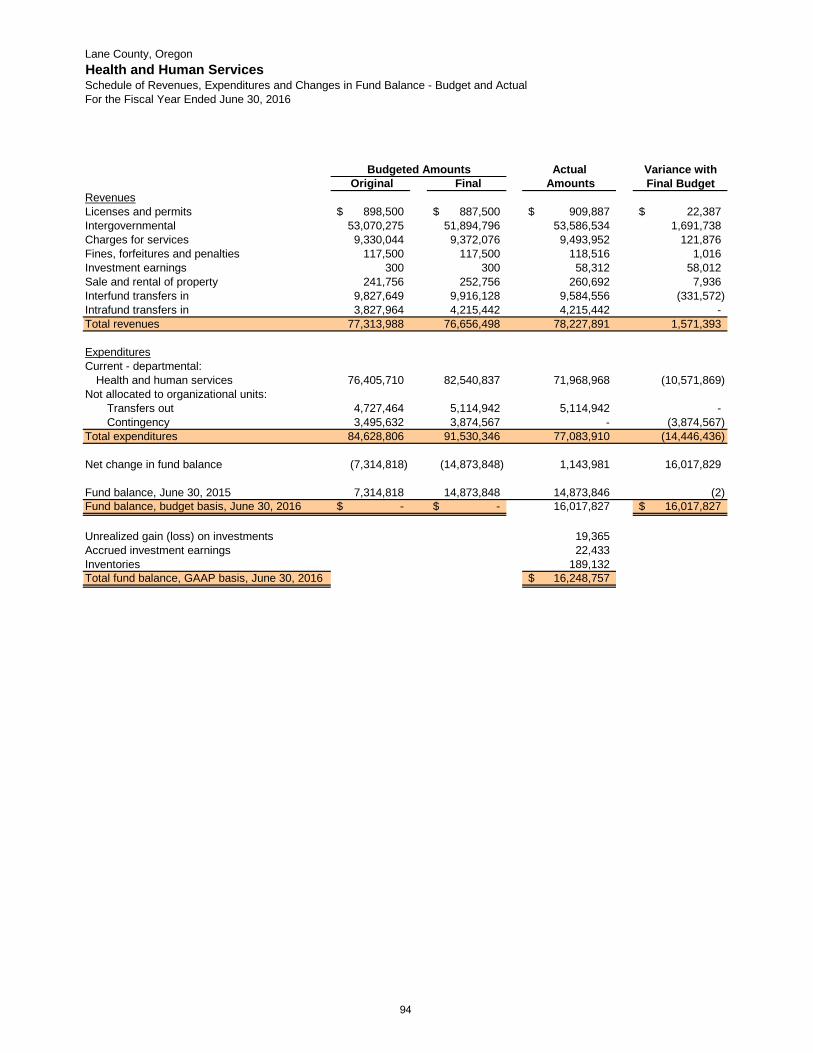

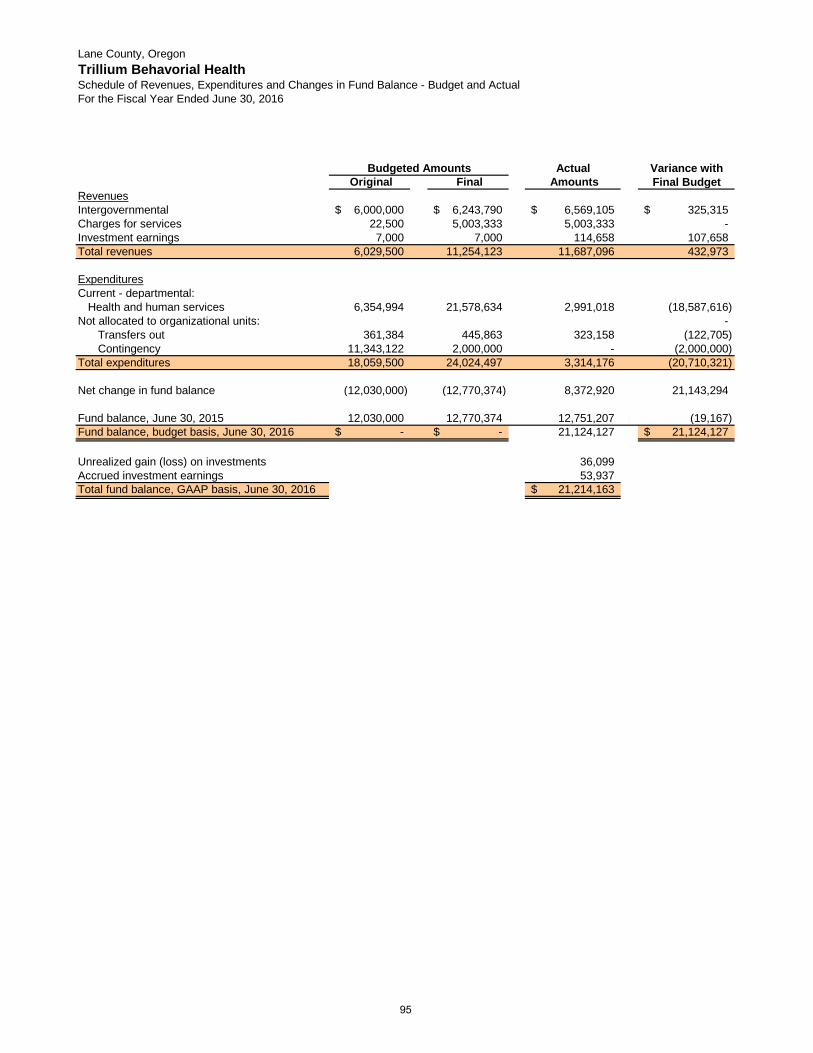

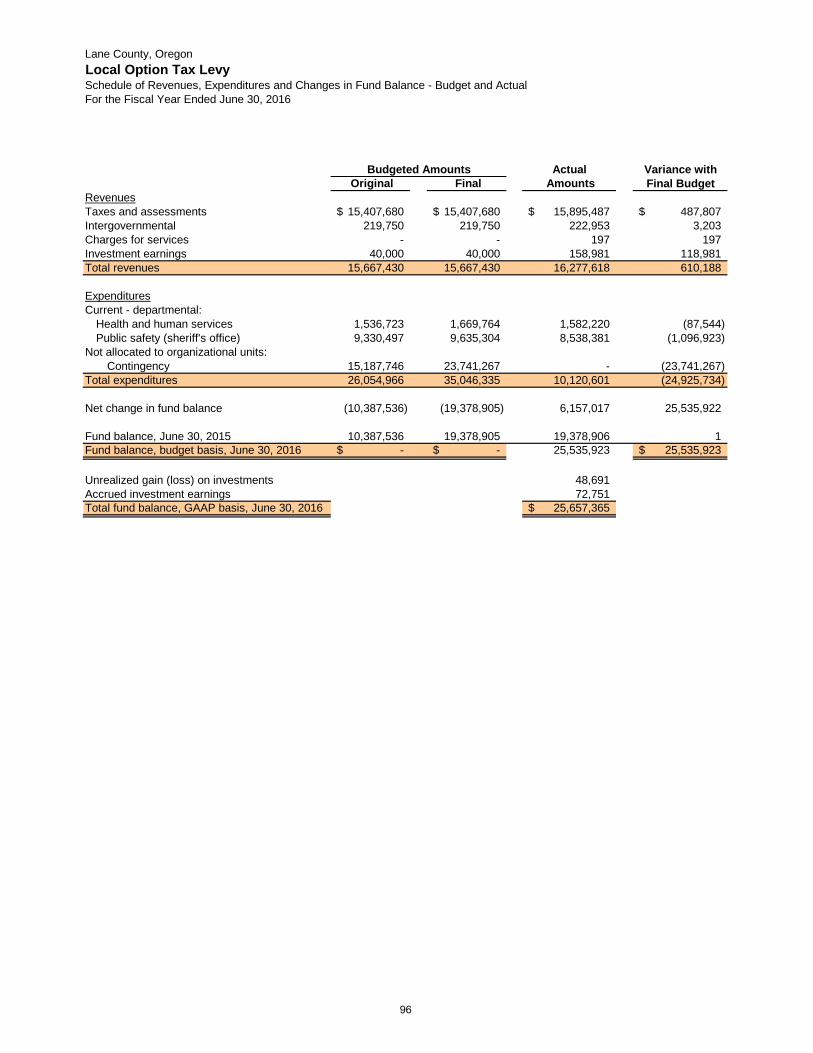

The Special Revenue/Services Fund accounts for dedicated revenue sources and programs. During fiscal year 2016 the fund balance experienced an increase of $2 million which was largely attributable to reduced expenditures in public safety. In fiscal year 2016, the fund balance of the Health and Human Services (H&HS) Fund experienced an increase of $1.1 million. This was due to an increase in mental health division revenues for developmental disabilities, medical subcontracts, behavioral health services, and A&D subcontracts. The Trillium Behavioral Health Fund accounts for mental health services for county residents. During fiscal year 2016, the ending fund balance increased by $8.4 million. The majority of the increase is due to the health and human services reserve refund of $5 million when Trillium Community Health Plan was purchased by Centene. The Local Option Tax Levy Fund was established in fiscal year 2014 to account for property tax revenues along with public safety and public health and welfare expenses from the five-year local option tax levy. Proceeds from the local option tax levy are designated for the restoration of jail beds and critical youth services. Revenues continued to increase in fiscal year 2016. Due to the lengthy recruitment process including physical agility and other testing, background history and medical evaluation the number of deputies hired with levy funds was less than anticipated during the first two years of the levy. During fiscal year 2016, the fund balance increased by $6.2 million to $25.7 million. The levy is set to expire in fiscal year 2018. In May, 2016, the Lane County Budget Committee approved a 31% decrease to the Local Option Levy tax currently authorized by voters at a rate 55 cents per $1,000 maximum assessed value. The lower tax amount for this Levy in FY 16-17 will be 38 cents per $1,000 maximum assessed value.

21

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

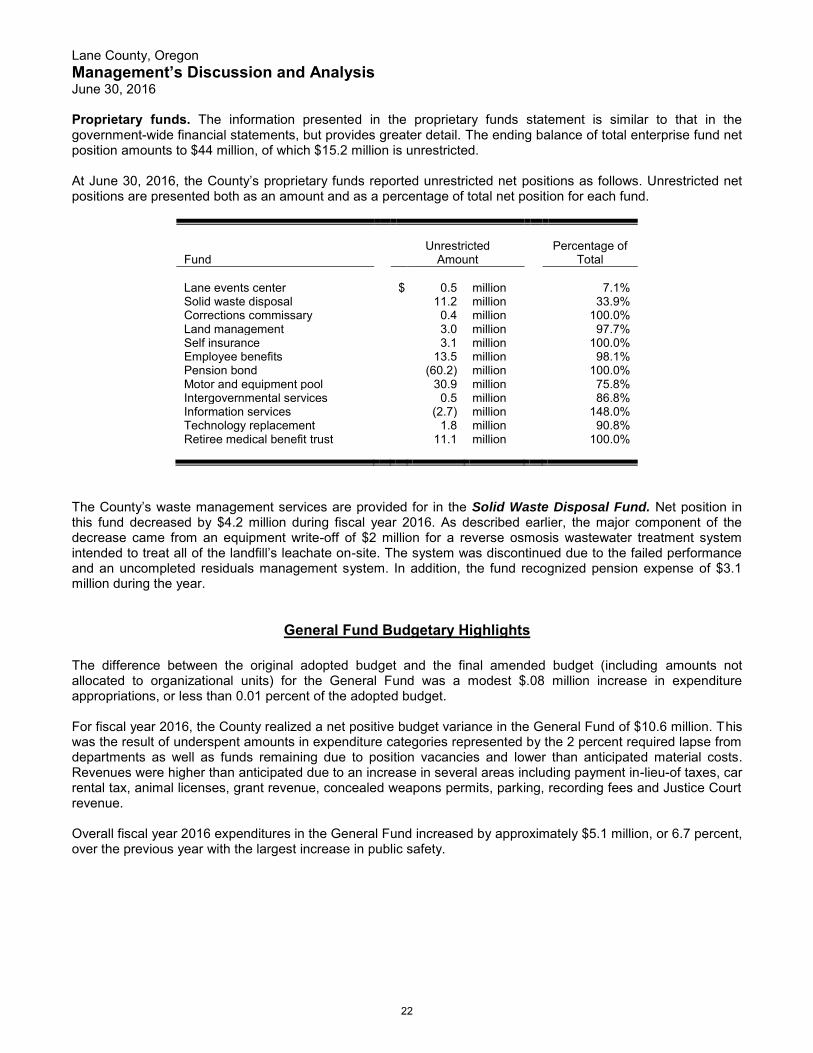

Proprietary funds. The information presented in the proprietary funds statement is similar to that in the government-wide financial statements, but provides greater detail. The ending balance of total enterprise fund net position amounts to $44 million, of which $15.2 million is unrestricted. At June 30, 2016, the County’s proprietary funds reported unrestricted net positions as follows. Unrestricted net positions are presented both as an amount and as a percentage of total net position for each fund.

Fund

Unrestricted

Amount

Percentage of

Total Lane events center

$

0.5

million

7.1%

Solid waste disposal 11.2 million 33.9% Corrections commissary 0.4 million 100.0% Land management 3.0 million 97.7% Self insurance 3.1 million 100.0% Employee benefits 13.5 million 98.1% Pension bond (60.2) million 100.0% Motor and equipment pool 30.9 million 75.8% Intergovernmental services 0.5 million 86.8% Information services (2.7) million 148.0% Technology replacement 1.8 million 90.8% Retiree medical benefit trust 11.1 million 100.0%

The County’s waste management services are provided for in the Solid Waste Disposal Fund. Net position in this fund decreased by $4.2 million during fiscal year 2016. As described earlier, the major component of the decrease came from an equipment write-off of $2 million for a reverse osmosis wastewater treatment system intended to treat all of the landfill’s leachate on-site. The system was discontinued due to the failed performance and an uncompleted residuals management system. In addition, the fund recognized pension expense of $3.1 million during the year.

General Fund Budgetary Highlights

The difference between the original adopted budget and the final amended budget (including amounts not allocated to organizational units) for the General Fund was a modest $.08 million increase in expenditure appropriations, or less than 0.01 percent of the adopted budget. For fiscal year 2016, the County realized a net positive budget variance in the General Fund of $10.6 million. This was the result of underspent amounts in expenditure categories represented by the 2 percent required lapse from departments as well as funds remaining due to position vacancies and lower than anticipated material costs. Revenues were higher than anticipated due to an increase in several areas including payment in-lieu-of taxes, car rental tax, animal licenses, grant revenue, concealed weapons permits, parking, recording fees and Justice Court revenue. Overall fiscal year 2016 expenditures in the General Fund increased by approximately $5.1 million, or 6.7 percent, over the previous year with the largest increase in public safety.

22

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

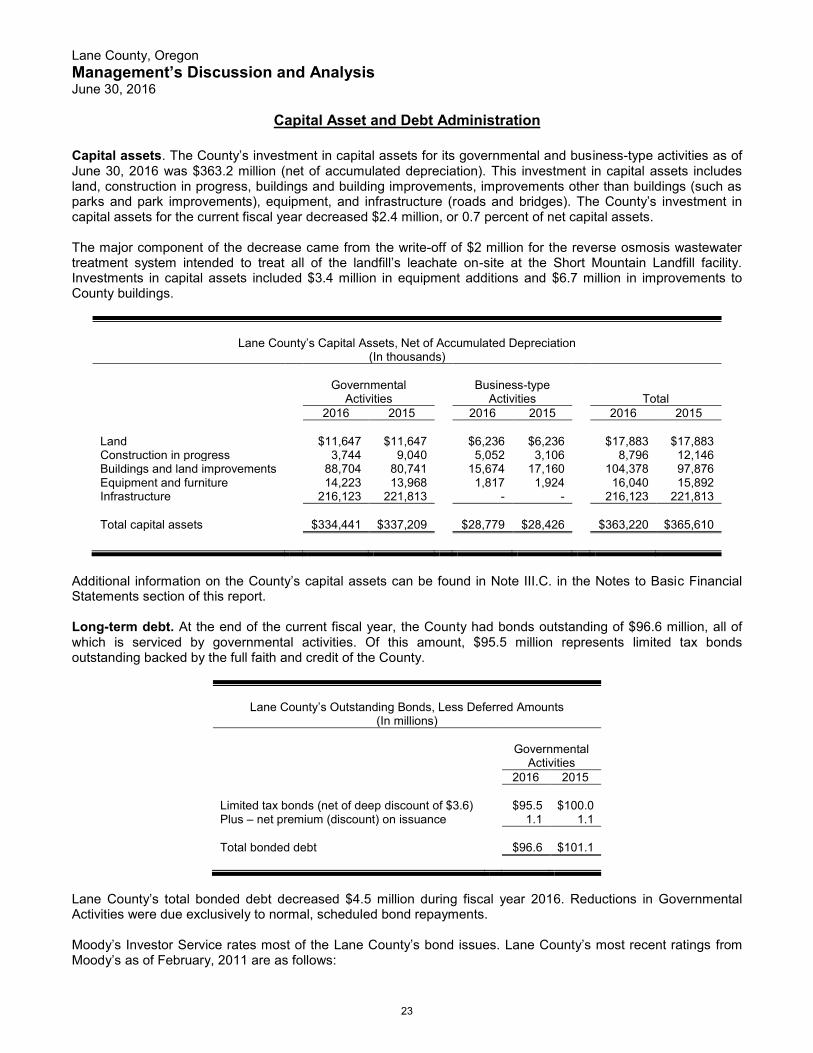

Capital Asset and Debt Administration

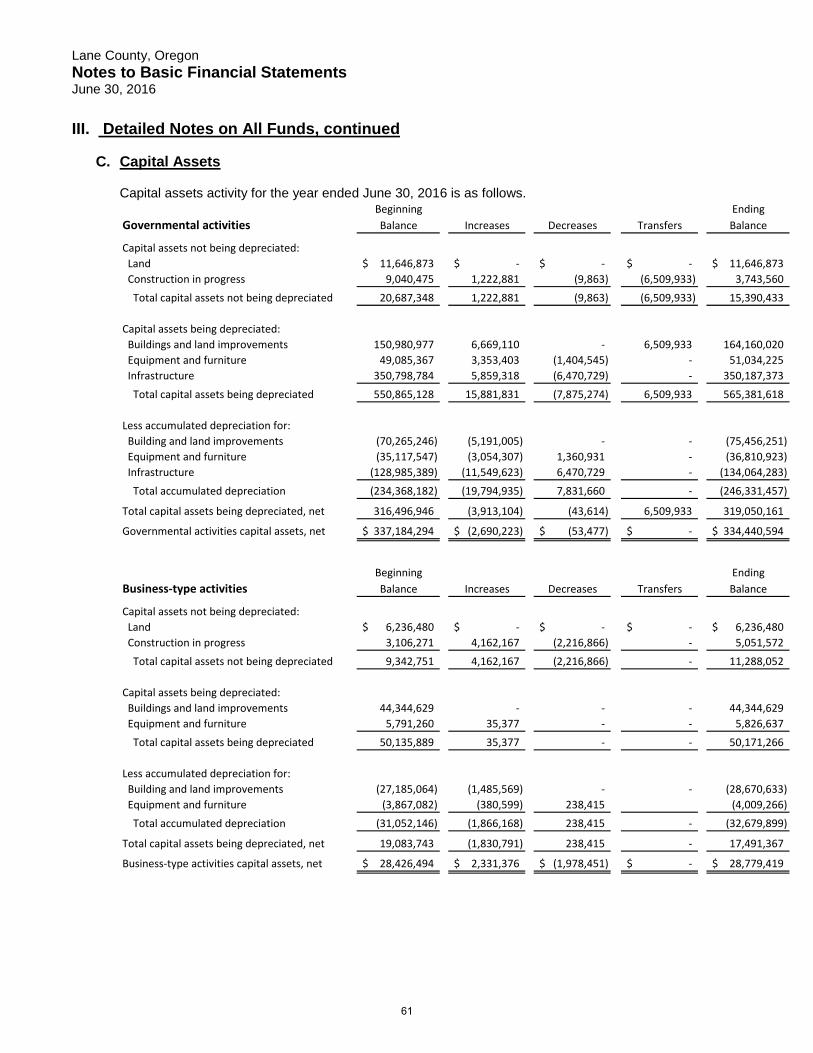

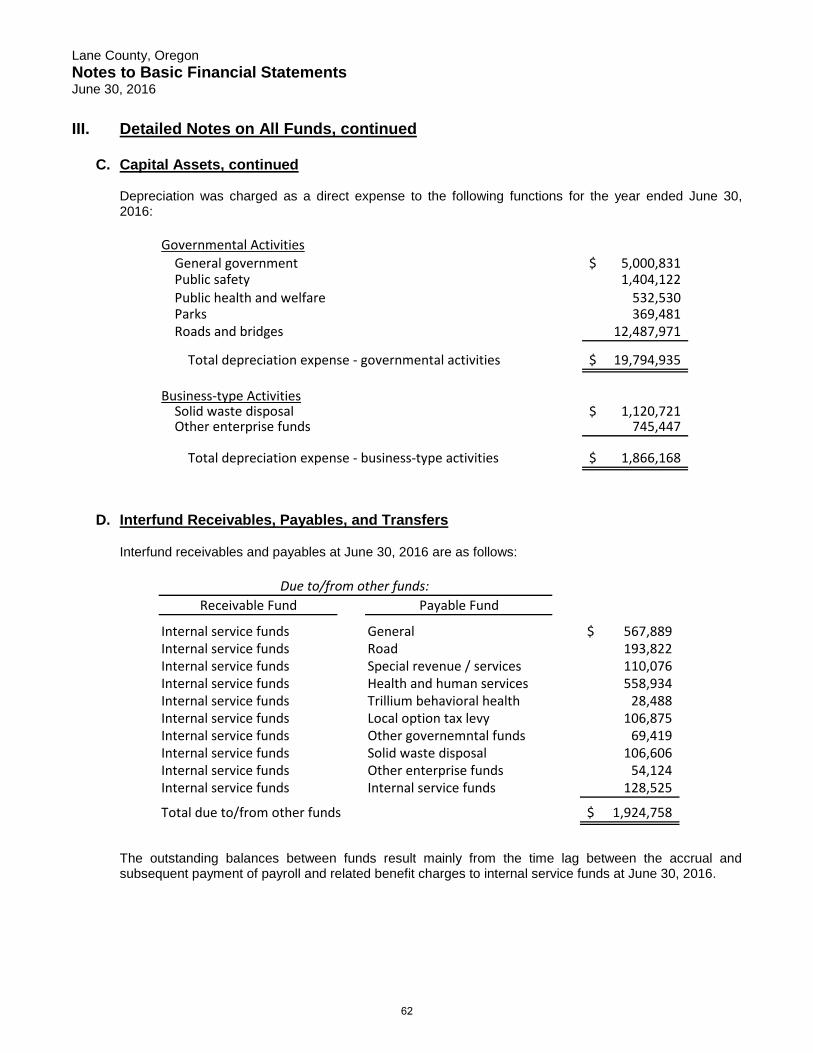

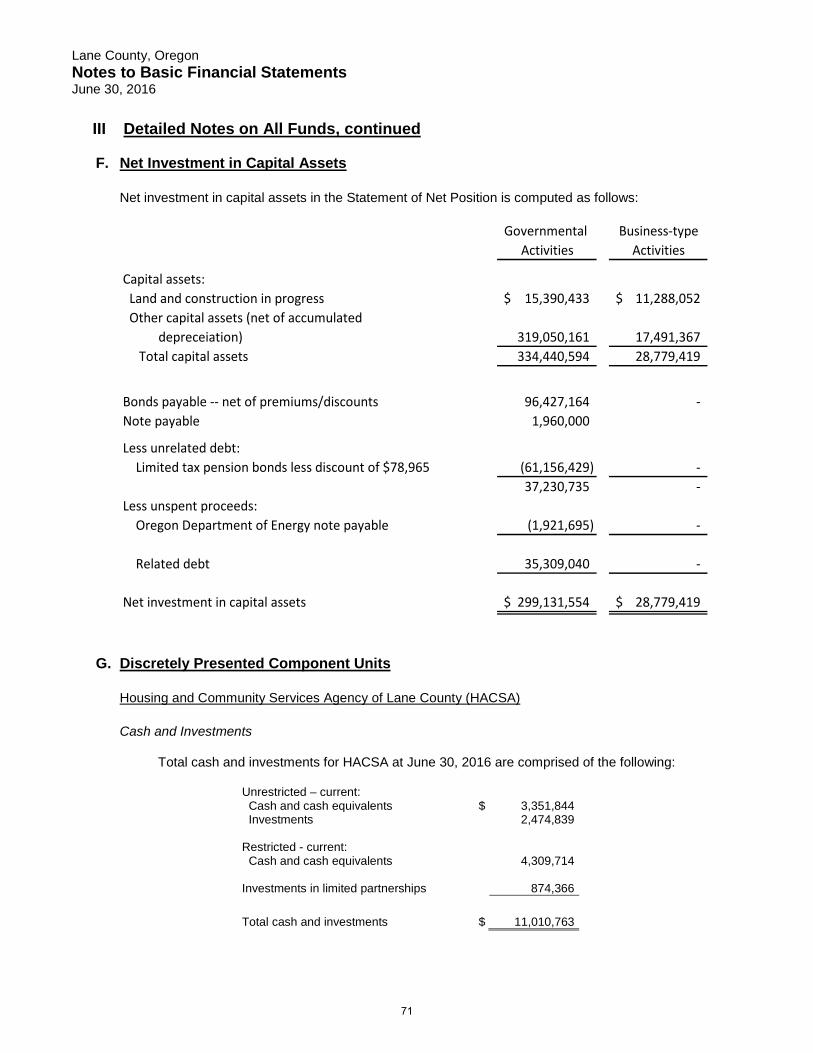

Capital assets. The County’s investment in capital assets for its governmental and business-type activities as of June 30, 2016 was $363.2 million (net of accumulated depreciation). This investment in capital assets includes land, construction in progress, buildings and building improvements, improvements other than buildings (such as parks and park improvements), equipment, and infrastructure (roads and bridges). The County’s investment in capital assets for the current fiscal year decreased $2.4 million, or 0.7 percent of net capital assets.

The major component of the decrease came from the write-off of $2 million for the reverse osmosis wastewater treatment system intended to treat all of the landfill’s leachate on-site at the Short Mountain Landfill facility. Investments in capital assets included $3.4 million in equipment additions and $6.7 million in improvements to County buildings.

Lane County’s Capital Assets, Net of Accumulated Depreciation

(In thousands)

Governmental

Activities

Business-type

Activities

Total 2016 2015 2016 2015 2016 2015

Land $11,647 $11,647 $6,236 $6,236 $17,883 $17,883 Construction in progress 3,744 9,040 5,052 3,106 8,796 12,146 Buildings and land improvements 88,704 80,741 15,674 17,160 104,378 97,876 Equipment and furniture 14,223 13,968 1,817 1,924 16,040 15,892 Infrastructure 216,123 221,813 - - 216,123 221,813 Total capital assets

$334,441

$337,209

$28,779

$28,426

$363,220

$365,610

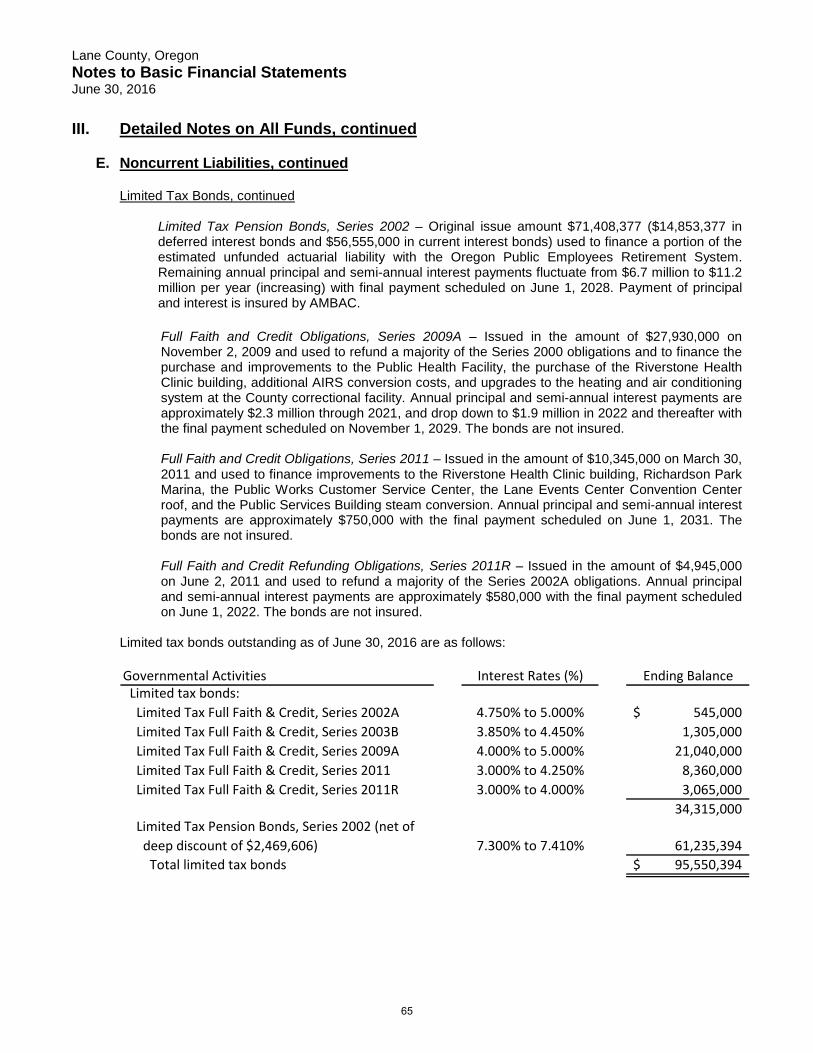

Additional information on the County’s capital assets can be found in Note III.C. in the Notes to Basic Financial Statements section of this report. Long-term debt. At the end of the current fiscal year, the County had bonds outstanding of $96.6 million, all of which is serviced by governmental activities. Of this amount, $95.5 million represents limited tax bonds outstanding backed by the full faith and credit of the County.

Lane County’s Outstanding Bonds, Less Deferred Amounts

(In millions)

Governmental Activities

2016 2015 Limited tax bonds (net of deep discount of $3.6) $95.5 $100.0 Plus – net premium (discount) on issuance 1.1 1.1 Total bonded debt

$96.6

$101.1

Lane County’s total bonded debt decreased $4.5 million during fiscal year 2016. Reductions in Governmental Activities were due exclusively to normal, scheduled bond repayments. Moody’s Investor Service rates most of the Lane County’s bond issues. Lane County’s most recent ratings from Moody’s as of February, 2011 are as follows:

23

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

Aa2 for general obligation bonds Aa3 for limited tax bonds

Moody’s performed a follow-up surveillance review in August of 2013 and did not recommend any changes.

Lane County’s rating of “Aa” is defined by Moody’s as demonstrating “very strong creditworthiness relative to other US municipal or tax-exempt issuers or issues.” The numerical modifier of “2” and “3” reflect the “mid-range” and “lower end” rankings, respectively, within the “Aa” rating.

Oregon Revised Statutes set the following debt limits:

General obligation debt issues are limited to 2 percent of the real market value of all taxable property within the County’s boundaries. Lane County had no general obligation debt at June 30, 2016. The statutory ceiling for general obligation debt, 2 percent of real market value of all taxable property, is $820.2 million.

Limited tax obligation debt issues are limited to 1 percent of the real market value of all taxable property within the County’s boundaries. The $34.3 million in limited tax obligation debt is $375.8 million below the statutory ceiling.

Limited tax pension debt issues are limited to 5 percent of the real market value of all taxable property within the County’s boundaries. The $61.2 million in limited tax obligation debt is $1.99 billion below the statutory ceiling.

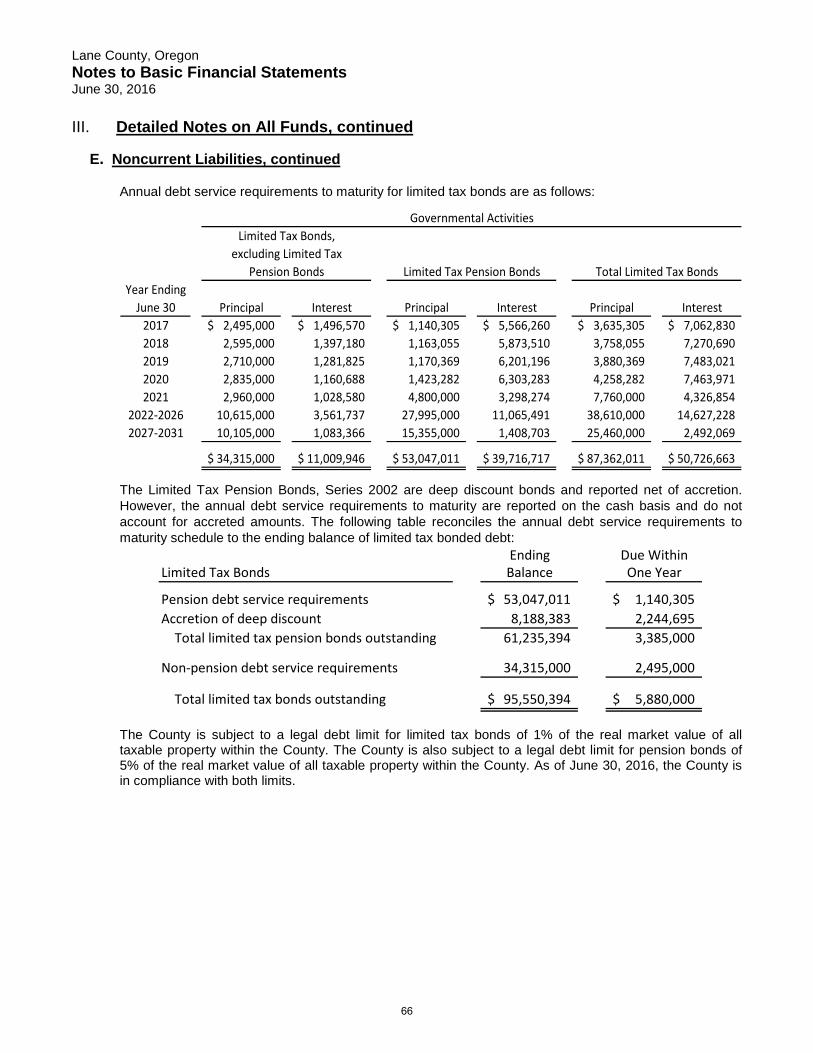

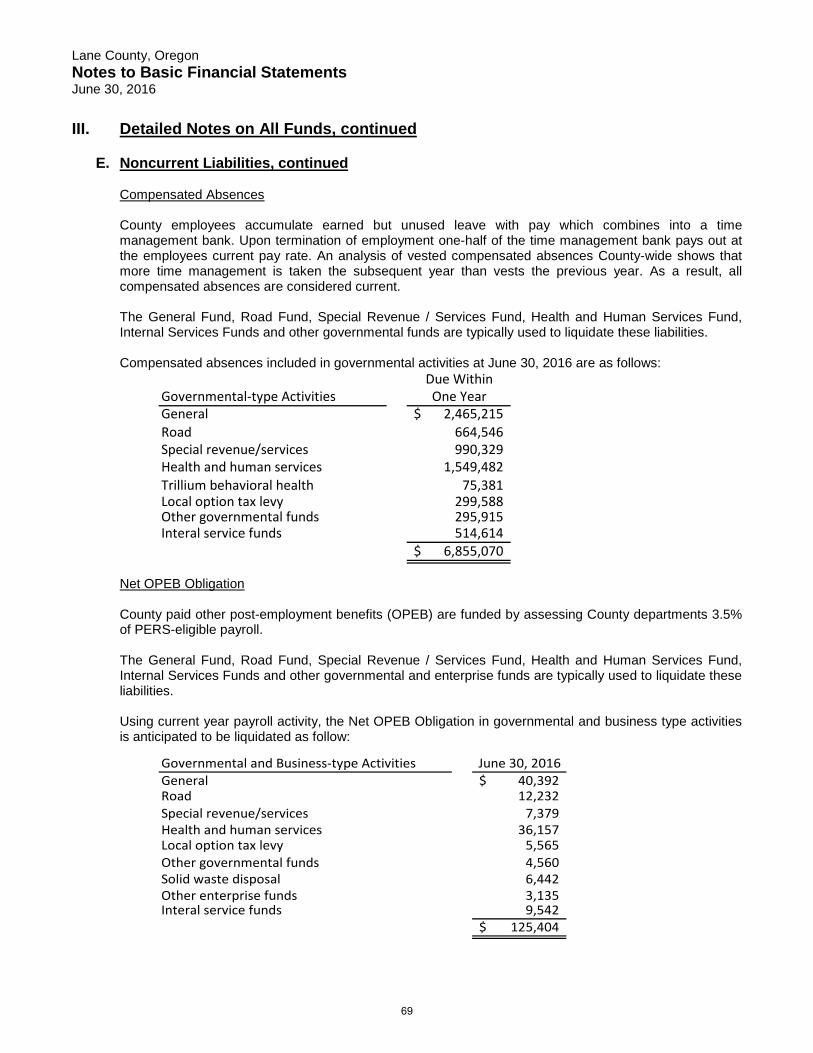

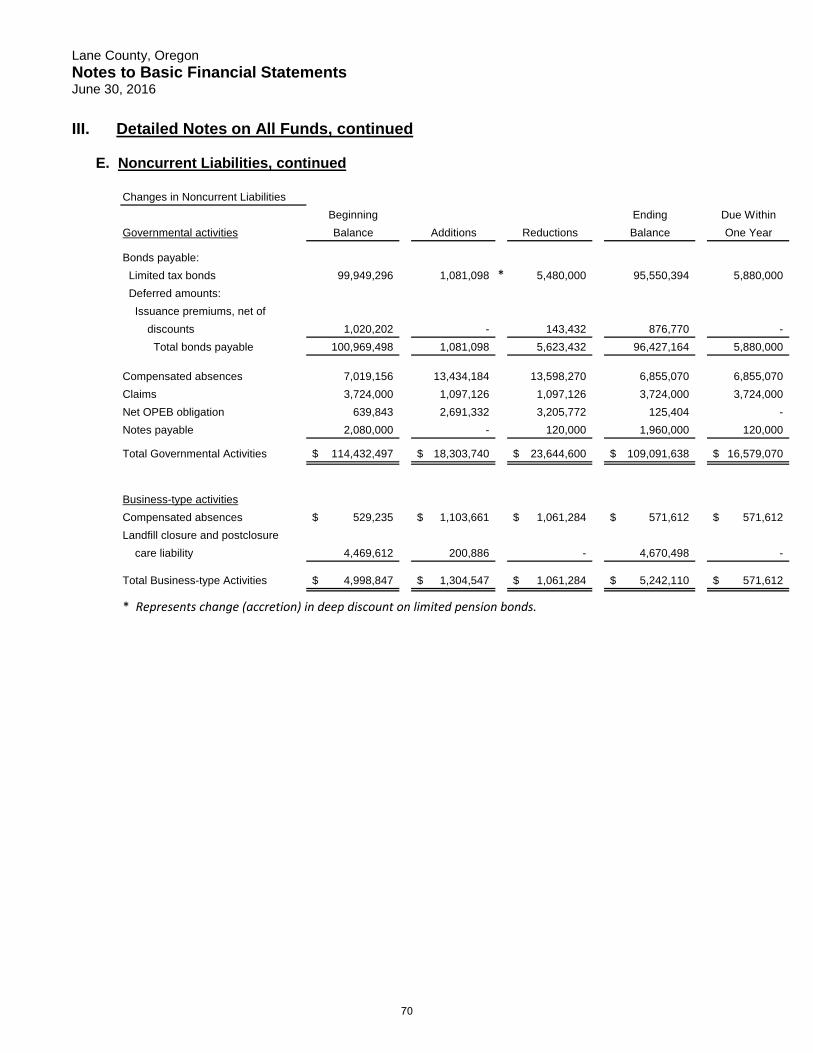

In June 2014, the County signed a note payable for $2,080,000 with the Oregon Department of Energy’s Small Scale Local Energy Loan Program to finance machinery, equipment, and improvements to the regional computer data center. As of June 30, 2016, the balance of the note payable was $1,960,000. The note is backed by the full faith and credit of the County. Additional information on the County’s long-term debt can be found in Note III.E. in the Notes to Basic Financial Statements section of this report.

Economic Factors and Next Year’s Budgets and Rates

The title of the fiscal year 2017 Budget Message was Finding Opportunity In Scarcity. The County has used the recognition of ongoing and increasing scarcity as an opportunity to focus, align and excel. Through the strategic vision and commitment, the fiscal year 2017 budget recognizes the County’s substantial constraints while advancing and improving the range of essential services the residents of Lane County require and deserve. The fiscal year 2017 budget focused on two goals: 1) Enhance critical services to make our community safer, healthier and more vibrant 2) Create long-term financial stability through a structurally balanced budget As a result of this focus, the General Fund budget includes over $4 million in structural adjustments through a combination of expense reductions and revenue enhancements, which exceeds the targeted goal. Additionally, there are strategic investments in priority services that will improve the community, while demonstrating an obligation to taxpayers to responsibly manage scarce resources and create long-term financial stability. Following are the major factors and assumptions used in developing the fiscal year 2017 budget:

The Adopted Budget is $569 million, including expenditures and reserves for all funds. Resources overall are down by $32 million, or 5.33 percent, compared to the fiscal year 2016 final budget. This decrease in resources is a combination of reducing fund balances due to the elimination of the Secure Rural Schools federal payments, and a decreased property tax rate for the local option levy. For fiscal year 2017, the budget committee decreased the approved local option levy tax amount to $0.38 per $1,000 assessed value due to higher than anticipated revenue and lower than projected expenditures. This change represents almost a 30% decrease in the local option levy tax rate to Lane County taxpayers while still providing a higher service level than originally promised during passage of the levy.

24

Lane County, Oregon Management’s Discussion and Analysis June 30, 2016

Property tax collections are based on the County’s permanent tax rate under voter approved Measure 50 is $1.2793 per $1,000 of Assessed Value (AV). The County also has two local option levies appearing within its budget. The first one was passed by voters in 2013 for restoration of jail beds and critical youth services. In May 2016, voters also passed 4H Extension Service levy of $0.015 cents per $1,000 AV. While the 4H funds appear within the Lane County budget they are paid directly to the OSU Extension Service which is a separate entity for Lane County government to provide the services. Overall, Lane County is seeing the growth of property tax revenue from its permanent rate exceed the statutory 3 percent growth due to a strong housing market.

State revenue consists of 24.17% of total County revenue and comes primarily in in the form of specific use grants. Total state revenue is decreasing by $1.6 million, or 1.83 percent, as compared to fiscal year 2016 due to one-time projected related funds received from the Department of Transportation and the Coordinated Care Organization. State shared revenues (cigarette, liquor, and amusement device tax, video lottery proceeds and a recreational vehicle fee) total $4.47 million, or 5.2 percent, of total state revenues. Video lottery, which must be spent on economic development, is projected to grow by over 5 percent from original state projections. Cigarette tax revenue continues to decline in recent years, while liquor tax shows modest increases. The State legislature changed the distribution of the recreation vehicle fee which will result in an additional $64,000 in revenue for County Parks.

Federal revenue, $45 million or 12.69 percent of overall County revenue, is projected to decrease by $6.2 million due to elimination of the Secure Rural Schools payments, which have not been renewed by the U.S. Congress. The County continues to see declining Federal revenue. The resulting decrease over the past 6 years is 37.8 percent, not adjusted for inflation. This reduction in revenue has the largest impact within the General Fund.

Fees and charges for services rendered to residents, a few examples being Short Mountain Landfill fees, Land Management permit fees and recording fees within Deeds and Records, will total $36.4 million in fiscal year 2017. The decrease from 2016 is due to several one-time reimbursements. Recording fees, which saw a substantial decrease three years ago, has rebounded and has returned to prior revenue amounts due in part to continued low mortgage interest rates and a strong local real estate market. The trend for that revenue source is dependent on decisions made by the Federal Reserve and long-term interest rates.

Personnel services which consists of employee wages and benefits, totals $165.2 million, or 43 percent of the County’s total expenditure budget. This represents growth of 2.49 percent when compared to the fiscal year 2016 budget. The County's services, like most governmental agencies, are labor intensive. Of this amount, $65.5 million is for taxes and benefit costs such as social security, Medicare, medical insurance, retirement, and other provided benefits. Health insurance costs are projected to stay relatively flat due to the change to a self-funded model and lower than projected medical claims in fiscal year 2016.

Materials and services total $188.1 million and represents 50 percent of the overall expenditure budget, a decrease of $25 million, or 12 percent from fiscal year 2016. This decrease is attributed to one-time expenses in fiscal year 2016, as well as a continued focus on reduction of internal expenses and other material and services to maintain the personnel needed to provide direct services to citizens. The continued decrease within the Road Fund of available funding for road improvements and maintenance due to the loss of Secure Rural Schools also impacts this expense category.