cohnreznick private equity industry outlook

DESCRIPTION

CohnReznick Private Equity Industry OutlookTRANSCRIPT

A CohnReznick LLP Report FEBRUARY 2014

Momentum 2014Middle-Market

Private Equity Outlook

A CohnReznick Report 3

Today’s Private Equity Business Environment.................1

Critical Issues Facing Private Equity in 2014...................6

Private Equity Due Diligence Focus................................24

The Road Ahead..................................................................29

Table of Contents

Preface

The private equity (PE) industry is well-positioned for an optimistic 2014. After five challenging years, there were a number of positive developments for the industry in 2013, including a rebound in fundraising and a record $120 billion returned to investors in private equity.

mo • men • tum noun: the impetus gained by a moving object

Overall, 2013 will be remembered as a solid year for private equity. Although the year started off slowly, activity picked up considerably in the second half, particularly in the world of exits.The fourth quarter of 2013 was one of the strongest quarters on record for PE exits, attributable largely to a robust IPO market. The key topic that must be considered in projecting the industry’s outlook for 2014 is whether it can build upon this momentum, or whether the industry’s capital overhang and competition for quality deals will prove too great a resistive force.

While we’ll analyze the industry in its broadest sense, our focus is decidedly on the outlook for middle-market private equity firms―those firms with assets under management between $100 million and $5 billion. Lacking the resources and capital reserves of the private equity industry titans, middle market private equity better reflect whether industry momentum is building or waning.

We start by examining last year’s industry activity and transactions. While overall investment dollars soared, deal making was increasingly difficult as the total number of transactions fell 14 percent. CohnReznick also notes the change in the composition of deals, with a decrease in platform transactions and an increase in add-on deals and growth capital. Indeed, for the first time ever, add-on acquisitions surpassed platform deals, suggesting that PE firms were largely focused on helping grow their portfolio companies rather than chasing new deals. We continue by considering how broader economic and legislative forces will either assist or impede industry progress.

Next, we analyze how the key issues facing the industry in 2014―including competition for deals, crowdfunding, the changing balance of power between LPs and GPs, and the potential for carried interest tax reform―will shape the industry. We evaluate the impact on middle- market private equity and highlight how it will cause firms to re-evaluate what makes a good investment, lead to an era of increased industry specialization, and create a focus on providing “value” rather than simply access to capital. In light of these issues, we provide guidance on the key due diligence matters that private equity firms should consider in order to better ensure they make the most lucrative investments at the most conservative prices.

Throughout this outlook we’ve highlighted strategies for middle-market PE firms to best compete for deals and optimize the value of their portfolio. Although it is impossible to predict precisely what opportunities and challenges 2014 will present, we conclude with a cautiously optimistic outlook for increased momentum in the private equity sector.

Dom Esposito Jeremy Swan Partner, Principal, National Practice Private Equity and and Growth Director Venture Capital Industry Practice

A CohnReznick Report 1

Industry Climate: 2014―A Comeback Year for Private EquityIt has been five years since the beginning of the global financial crisis, but a bruised PE industry appears primed for a comeback in 2014. What are the positive indicators from 2013 that point to a brighter PE sector in 2014? Last year, the industry had its most successful fundraising year since the onset of the economic downturn. In addition, transaction activity has been gaining momentum and PE firms are placing an even greater emphasis on exits. In fact, the PE industry returned more money to its limited partners last year than ever before, selling a record $120 billion of investments, according to Cambridge Associates.

A strong indicator for 2014 is a rebound in the amount of capital invested. The $426 billion represents a 4.6% year-over-year increase and $64 billion more than the capital invested in 2008 (17.6% increase). The third quarter was particularly strong, registering as the fifth strongest quarter since 2008. The final 2013 statistics will only improve as fourth quarter data continues to be reported.

The uptick in capital needed is good news for a PE industry that has had difficulty putting money to work post-recession. Resurgent investment is also a positive development for business owners that have built successful companies and are now contemplating a liquidity event. There is already a strong pipeline of deals for the first quarter of 2014, therefore, CohnReznick does not anticipate another dramatic decline in deal making from the fourth quarter, as observed in the previous three years.

Today’s Private Equity Business Environment

Middle-Market Private Equity Outlook2

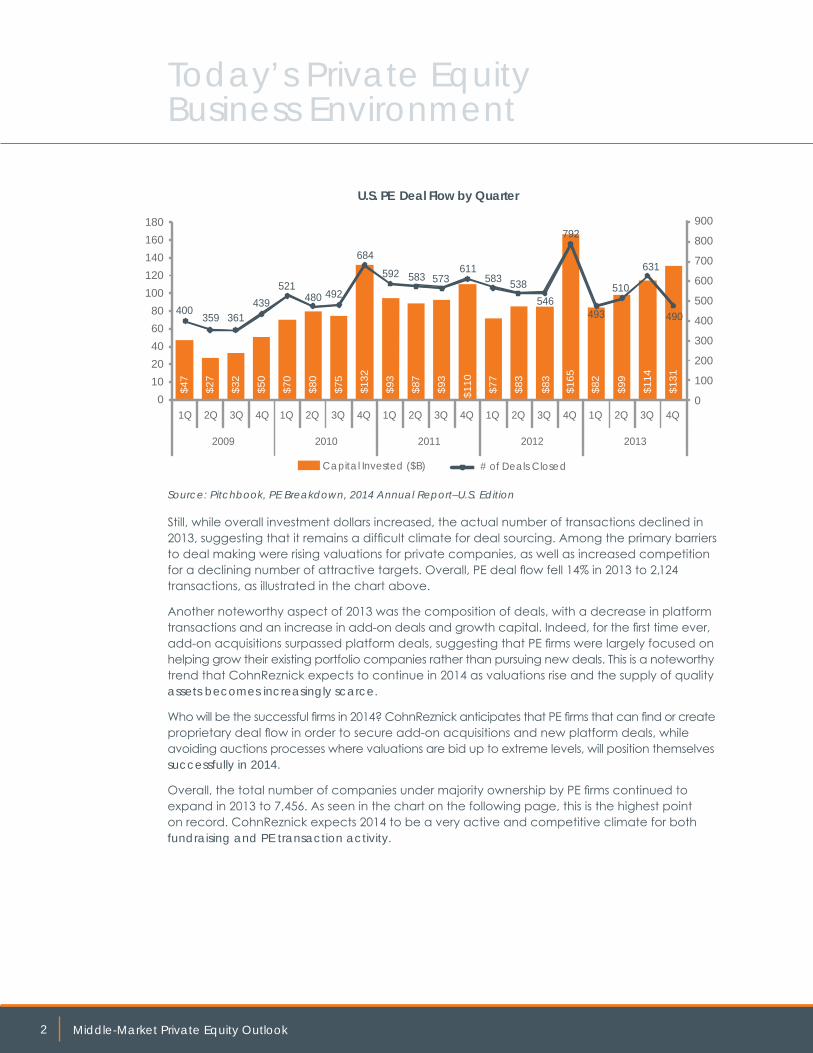

Still, while overall investment dollars increased, the actual number of transactions declined in 2013, suggesting that it remains a difficult climate for deal sourcing. Among the primary barriers to deal making were rising valuations for private companies, as well as increased competition for a declining number of attractive targets. Overall, PE deal flow fell 14% in 2013 to 2,124 transactions, as illustrated in the chart above.

Another noteworthy aspect of 2013 was the composition of deals, with a decrease in platform transactions and an increase in add-on deals and growth capital. Indeed, for the first time ever, add-on acquisitions surpassed platform deals, suggesting that PE firms were largely focused on helping grow their existing portfolio companies rather than pursuing new deals. This is a noteworthy trend that CohnReznick expects to continue in 2014 as valuations rise and the supply of quality assets becomes increasingly scarce.

Who will be the successful firms in 2014? CohnReznick anticipates that PE firms that can find or create proprietary deal flow in order to secure add-on acquisitions and new platform deals, while avoiding auctions processes where valuations are bid up to extreme levels, will position themselves successfully in 2014.

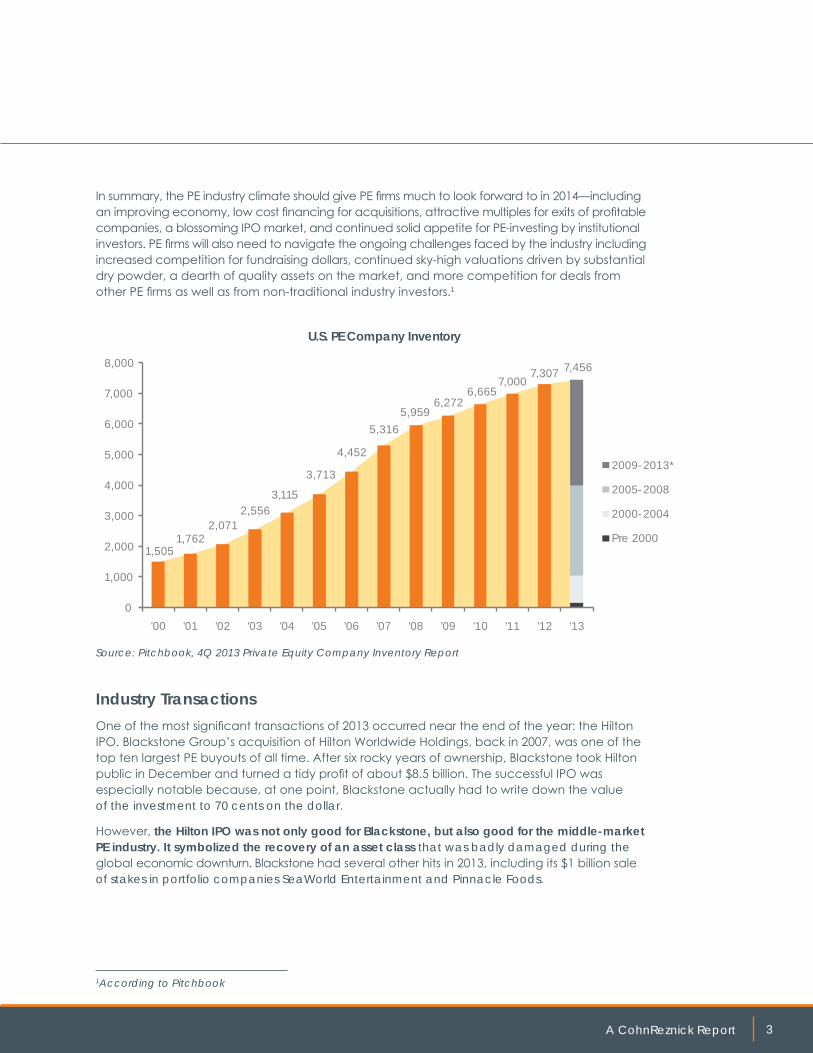

Overall, the total number of companies under majority ownership by PE firms continued to expand in 2013 to 7,456. As seen in the chart on the following page, this is the highest point on record. CohnReznick expects 2014 to be a very active and competitive climate for both fundraising and PE transaction activity.

Today’s Private Equity Business Environment

U.S. PE Deal Flow by Quarter$4

7

$27

$321

$50

$70

$80

$75

$132

$83

$93

$87

$93

$110

$77

$83

$165

$82

$99

$114

$131

$36

$75

$31

$37

400359 361

439521

480 492

684

592 583 573611

583 538546

792

493

510

631

490

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2009 2010 2011 2012 2013

Capital Invested ($B) # of Deals Closed

900

800

700

600

500

400

300

200

100

0

18016014012010080604020100

Source: Pitchbook, PE Breakdown, 2014 Annual Report–U.S. Edition

A CohnReznick Report 3

In summary, the PE industry climate should give PE firms much to look forward to in 2014—including an improving economy, low cost financing for acquisitions, attractive multiples for exits of profitable companies, a blossoming IPO market, and continued solid appetite for PE-investing by institutional investors. PE firms will also need to navigate the ongoing challenges faced by the industry including increased competition for fundraising dollars, continued sky-high valuations driven by substantial dry powder, a dearth of quality assets on the market, and more competition for deals from other PE firms as well as from non-traditional industry investors.1

Industry Transactions

One of the most significant transactions of 2013 occurred near the end of the year: the Hilton IPO. Blackstone Group’s acquisition of Hilton Worldwide Holdings, back in 2007, was one of the top ten largest PE buyouts of all time. After six rocky years of ownership, Blackstone took Hilton public in December and turned a tidy profit of about $8.5 billion. The successful IPO was especially notable because, at one point, Blackstone actually had to write down the value of the investment to 70 cents on the dollar.

However, the Hilton IPO was not only good for Blackstone, but also good for the middle-market PE industry. It symbolized the recovery of an asset class that was badly damaged during the global economic downturn. Blackstone had several other hits in 2013, including its $1 billion sale of stakes in portfolio companies SeaWorld Entertainment and Pinnacle Foods.

1According to Pitchbook

U.S. PE Company Inventory

1,505 1,762

2,071 2,556

3,115

3,713

4,452

5,316 5,959

6,272 6,665

7,000 7,307 7,456

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

2009 -2013*

2005 -2008

2000 -2004

Pre 2000

YEAR OFINVESTMENT

Source: Pitchbook, 4Q 2013 Private Equity Company Inventory Report

Middle-Market Private Equity Outlook4

Today’s Private Equity Business Environment

Another notable deal was Dell, which went from public company status to private. After a bruising seven-month battle with activist shareholders, Dell founder Michael Dell and Silver Lake Partners prevailed, winning approval in late 2013 for their $24.8 billion PE buyout of the company.

While these deals captured the news, middle-market PE drove hundreds of deals during 2013. Among the most active were Audax (33 deals), Parthenon Capital Partners (23 deals), Aisling Capital (22 deals), and The Riverside Company (20 deals). Capital from middle market firms flowed into nearly all industry sectors and included such diverse investments as H.I.G. Capital’s investment in LaRedoute, an online retail platform to sell apparel and beauty products; Catterton Partners’ $22 million stake in Protein Bar, a fast food health food chain; and Ironwood Capital’s leveraged buy-out of Advanced Recycling Systems, a designer and manufacturer of patented equipment to collect, remove, and recycle dust and debris generated in industrial environments.

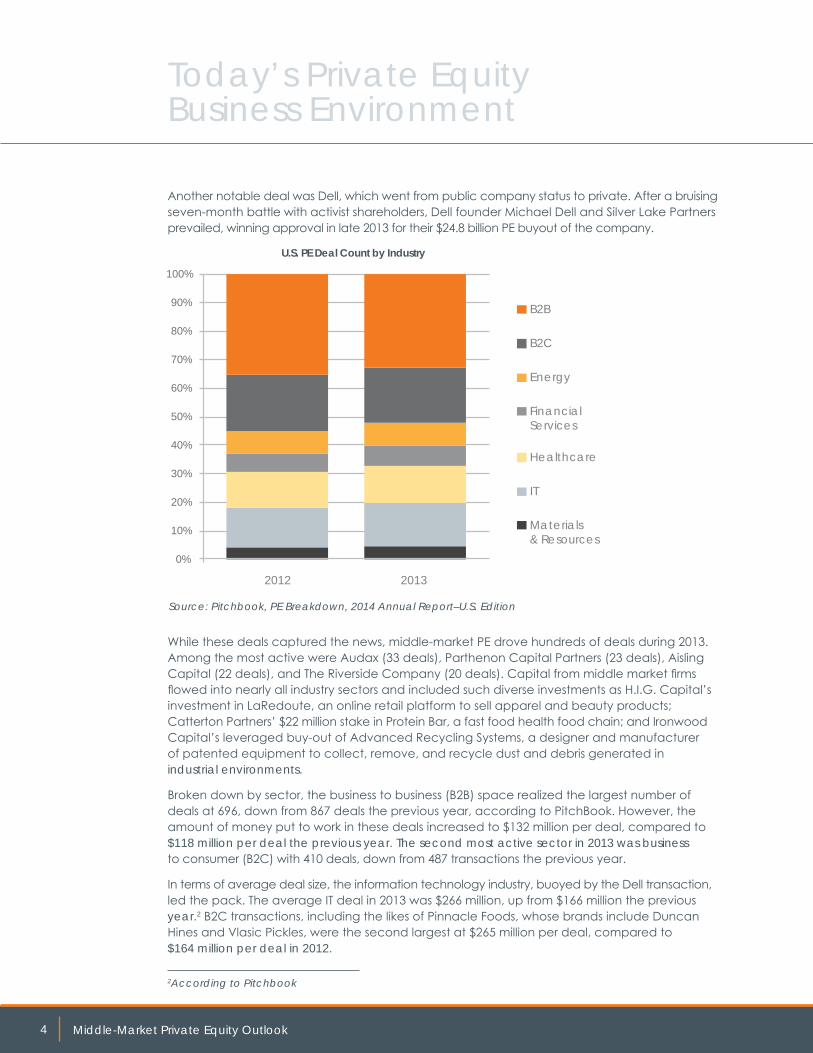

Broken down by sector, the business to business (B2B) space realized the largest number of deals at 696, down from 867 deals the previous year, according to PitchBook. However, the amount of money put to work in these deals increased to $132 million per deal, compared to $118 million per deal the previous year. The second most active sector in 2013 was business to consumer (B2C) with 410 deals, down from 487 transactions the previous year.

In terms of average deal size, the information technology industry, buoyed by the Dell transaction, led the pack. The average IT deal in 2013 was $266 million, up from $166 million the previous year.2 B2C transactions, including the likes of Pinnacle Foods, whose brands include Duncan Hines and Vlasic Pickles, were the second largest at $265 million per deal, compared to $164 million per deal in 2012.

U.S. PE Deal Count by Industry

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials& Resources

Source: Pitchbook, PE Breakdown, 2014 Annual Report–U.S. Edition

2According to Pitchbook

A CohnReznick Report 5

Legislative Update2013 was a very active year for legislative and regulatory changes. From Obamacare and immigration reform to the JOBS Act and tax reform, CohnReznick advises that regulatory and legislative changes will continue to be issues to contend with as they impact how PE firms conduct their business in 2014.

Obamacare was scheduled to take effect in January 2014 but the so-called employer mandate has been deferred for one year to January 1, 2015. This means that PE firms and their portfolio companies have an extra year to determine the best strategies for navigating healthcare reform. In light of the delay, PE firms should use the additional time to work with their portfolio companies to implement the mandate and the reporting procedures that come with it.

Meanwhile, the JOBS Act appears to be one of the most significant developments in the history of the PE industry. In 2013, Federal regulators lifted an 80 year-old ban on the advertising of private securities to the general public by hedge funds, venture capital funds, and start-up companies seeking capital. “The latest rollback of provisions of the 2010 Dodd-Frank law passed the House this past December. It will ease regulatory burdens on middle-market PE firms should it clear the Senate,” said Bob Moss, CohnReznick Principal and National Director of Governmental Affairs.

The rules around how PE firms can communicate and market themselves to investors have changed dramatically going into 2014. PE funds can now advertise their track record and solicit accredited investors for fund formation via new internet and social media channels, which could lead to a record amount of capital flowing into the industry.

Like the uncertainty and delays related to Obamacare, immigration reform faces its own ambiguity. It is still anyone’s guess as to whether a bill will be passed to increase the number of legal U.S. immigrant workers in 2014, but it is an issue that will continue to stir national debate. For private equity,

immigration reform represents an opportunity for portfolio companies, particularly those in the hospitality, manufacturing, and technology industries, to tap into a new and important source of legal labor. The Congressional Budget Office estimated that enacting the Senate immigration reform bill will increase real GDP by 3.3% in 2023 and 5.4% in 2033—an increase of about $700 billion in 2023 and $1.4 trillion in 2033 in today’s dollars.

Finally, the PE industry is anxious over the taxation of carried interest at ordinary income rates as opposed to the lower capital gains rates. Carried interest could play a major role in tax reform legislation over the next several years. “It has been a top “pay for” target since 2008 when it was brought to the

attention of then-Speaker Pelosi,” said Moss. Congress is aggressively searching for new revenue sources and carried interest continues to be in the crosshairs. Recent proposals from the House and Senate in 2013 indicate an increased willingness to treat carried interest compensation as ordinary income instead of taxing it at the lower capital gains rate. In fact, “During tax reform discussions carried interest is always number one on the list for elimination― and it usually has bipartisan support to remove it from the code,” said Moss. While the PE industry does not anticipate an immediate introduction of taxation on carried interest, it remains a simmering issue that will surface at almost any congressional mention of tax reform.

The latest rollback of provisions of the 2010 Dodd-Frank law passed the House this past December. It will ease regulatory burdens on middle- market PE firms should it clear the Senate.Bob Moss, Principal, National Director of Governmental Affairstal

“

”

Middle-Market Private Equity Outlook6

The Hunt for New DealsWhat is the key to success for PE firms in 2014? Jeremy Swan, Principal for CohnReznick’s Private Equity and Venture Capital Industry Practice says, “The key will be their ability to discover and craft new deals. Sourcing new deals has become increasingly challenging due to a larger amount of capital chasing a smaller number of quality opportunities. The most successful firms in 2014 will be those who can find or create high quality proprietary deal flow.”

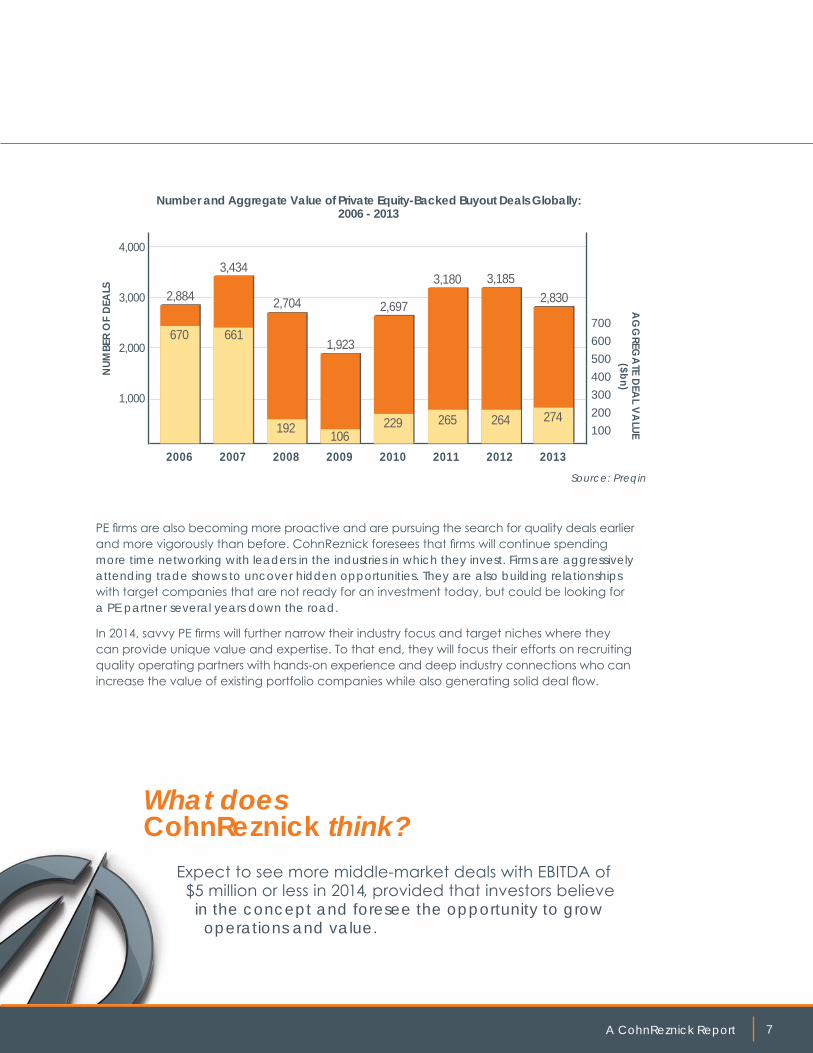

The total dollar value of PE deals increased in 2013, although the overall number of deals declined. According to Pitchbook, PE firms closed 2,124 transactions in 2013, down from 2,459 deals in 2012. Will this trend continue in 2014? “It may—however, rather than focus on the trend, we recommend that PE firms look for new and innovative approaches to deal sourcing,” said Swan.

CohnReznick foresees that the competition for quality deals will compel many firms to redefine the parameters of what constitutes a good investment. Previously, before PE would even consider an acquisition target in the hospitality space, for instance, the target would need at least $10 million in EBITDA, along with a very convincing growth profile. In 2014, CohnReznick believes that $5 million will be the new $10 million, and even that number may not be the minimum. An EBITDA bogey will no longer set the boundary for investment decisions in 2014. Plain and simple―investors are seeking innovative concepts that demonstrate potential for growth.

Critical Issues Facing Private Equity in 2014

A CohnReznick Report 7

PE firms are also becoming more proactive and are pursuing the search for quality deals earlier and more vigorously than before. CohnReznick foresees that firms will continue spending more time networking with leaders in the industries in which they invest. Firms are aggressively attending trade shows to uncover hidden opportunities. They are also building relationships with target companies that are not ready for an investment today, but could be looking for a PE partner several years down the road.

In 2014, savvy PE firms will further narrow their industry focus and target niches where they can provide unique value and expertise. To that end, they will focus their efforts on recruiting quality operating partners with hands-on experience and deep industry connections who can increase the value of existing portfolio companies while also generating solid deal flow.

NUM

BER

OF

DEA

LS

AG

GREG

ATE DEA

L VALUE

($bn)

2006 2007 2011201020092008 2012 2013

4,000

3,000

2,000

1,000

Number and Aggregate Value of Private Equity-Backed Buyout Deals Globally:2006 - 2013

2,884

670

3,434

2,704

1,923

2,697

3,180 3,1852,830

700600500400300200100

661

192 106229 265 264 274

Source: Preqin

Expect to see more middle-market deals with EBITDA of $5 million or less in 2014, provided that investors believe in the concept and foresee the opportunity to grow operations and value.

What does CohnReznick think?

Middle-Market Private Equity Outlook8

Critical Issues Facing Private Equity in 2014

A Favorite for 2014: Differentiated Strategies“Limited partners (LPs) will be searching for PE firms with a clearly differentiated strategy in 2014,” says Sharon Bromberg, Partner in CohnReznick’s Transactional Advisory Services Practice. LPs are no longer interested in investing in funds whose main point of distinction is purchasing companies with potential or growth and improving them. Similarly, with increasing competition for deals in 2014, target companies will want more than a check from PE firms—they will be in pursuit of partners who know their industry and can add real business value to the organization.

“As a result, specialist firms that have a track record of results are increasingly in vogue with both limited partners and mid-market companies,” said Bromberg. Research shows that competitive advantage confers to PE firms that have industry niche expertise. Specialized firms have a deeper understanding of their particular markets and can potentially uncover superior opportunities, generate proprietary deal flow, and provide more effective advice and connections, especially compared to their non-specialized competitors.

A differentiated strategy will continue to be a critical factor for PE firms that are determined to rise above the crowd in 2014 and beyond. CohnReznick believes more money will continue to chase fewer deals this year, putting industry expertise at a premium.

Specialization is particularly important to sellers that plan to retain an ownership stake in the business and want to partner with PE firms that can add the most value post-transaction. Entrepreneurs and business owners are increasingly eager, particularly in 2014, to team with PE firms that can quickly leverage their industry knowledge and make an immediate impact on the company. Likewise, LPs are attracted to firms that have the inside track on a particular industry and can invest in the most promising companies at the most competitive prices.

An increasing amount of capital will continue to chase fewer deals, placing industry expertise and differentiated strategies at a premium for middle-market PE firms.

What does CohnReznick think?

Specialist firms that have a track record of results are increasingly in vogue with both limited partners and mid-market companies.Sharon Bromberg, Partner, Transactional Advisory Services Practice

“

”

A CohnReznick Report 9

Economic Outlook: From a Walk to a Trot by Patrick J. O’Keefe, CohnReznick Director of Economic Research

The pace of the U.S. economic expansion should accelerate in 2014. While those gains will be solid and self-sustaining, reduced monetary stimulus and rising regulatory restrictions on the financial sector will constrain the degree of escalation.

Real gross domestic product (GDP)―that is, the total output of goods and services adjusted for inflation―is already at its highest level in history. Over the course of 2014, the rate of growth should approach that of 2010, the best year since the recession ended, when real GDP rose 2.8% on a fourth-quarter-over-fourth-quarter basis.

Total employment should exceed its pre-recession peak by mid-year as jobs gains average more than 220,000 per month in the year’s first half and then accelerate through the end of the year.

Household incomes―key, since consumers account for more than two-thirds of all spending― will grow moderately this year. Purchasing power will rise faster, however, as gains in after-tax income outstrip still-subdued inflation.

Consumers’ disbursable incomes will be augmented by further reductions in their financial obligations (viz., interest payments on mortgages and consumer credit).

Households’ annualized mortgage interest payments alone are down by more than one-third (about $210 billion) from 2007. Coincidentally, a revitalized housing sector and rising real estate values―together with buoyant equity markets―have increased net worth to a record $77 trillion and, thereby, bolstered consumer confidence.

Private investment should also provide impetus during 2014. Despite increases in 12 of the past 16 quarters, inflation-adjusted private investment is five percent below its 2006 peak. The ullage is attributable to spending on structures (primarily residential).

After languishing for much of the recovery, spending on structures―both residential and nonresidential―is gaining traction. But their contribution to total output is still one-fourth less than the average during the 25 years prior to the downturn.

A revitalized housing sector and continued jobs growth (i.e., increased demand for nonresidential space) will narrow that gap in the coming year.

As construction spending accelerates so will jobs growth. At the end of 2013, construction provided 1.6 million fewer jobs than pre-recession; lost construction jobs alone more than fully account for the nation’s total employment shortfall.

America’s industrial sector (manufacturers, utilities, and mines) entered 2014 on a sound footing, with fourth-quarter output recording its largest increase since mid-2010.

While manufacturers’ orders were wobbly as 2013 ended, shipments were up and inventories well behaved.

Manufacturing demand appears solid due to two factors. The first reflects increased demand for passenger vehicles in the aftermath of the recession- elongated replacement cycle. Auto assemblies in 2013 (10.8 million vehicles) were the highest since 2005 and almost double 2009’s output.

The second source of manufacturing strength is exports, which account for about one-quarter of total shipments. Although conditions globally are mixed, growth among the advanced economies should bolster demand for American goods.

Manufacturing jobs languished during the recovery. At 2013’s end, manufacturers employed 1.7 million fewer workers than pre-recession. As with construction, manufacturing alone more than accounts for the national jobs deficit.

Middle-Market Private Equity Outlook10

Coincidentally, private service employment is 2.6 million higher than pre-recession.

Inflation-adjusted spending on services by all sectors is at an all time high, almost five percent greater than before the recession began. Real services spending declined in one quarter during the downturn, twice afterwards. The declines were nugatory.

Services spending and employment are expected to accelerate steadily during 2014.

Fiscal policy, particularly Federal spending, has exerted drag on the economy for the past couple of years. In fiscal year 2013, the Federal deficit fell by more than one-third and it is still shrinking.

But even the reduced deficit is unsustainable. Despite narrowing its deficit, the Federal government is still borrowing one of every five dollars that it spends. Consequently, its debt burden grows and, eventually, debt service will impinge on other priorities.

Realigning the national budget should not be disruptive in 2014. Instead, on current policy, it should be marginally stimulative.

Since the start of the financial crisis in September 2008, the Federal Reserve has injected some $3.1 trillion into the economy by using newly created money to purchase U.S. Treasury instruments and federally-guaranteed mortgage-backed securities. Its intervention, commonly known as “quantitative easing” (QE), averted an implosion of the global financial system.

Since late 2010, QE has been used to stimulate job growth. But most of QE’s $3 trillion remains in the banking system (i.e., has not found its way into the general economy).

The Fed has now begun reducing (presumably to zero) its QE purchases.

QE “tapering” is a wild card for 2014’s economic outlook. In large part because QE of this magnitude is without precedent. It is probable that financial markets will be more volatile as tapering proceeds; but its impacts on the general economy will depend on the degree to which interest rates move upward.

A second wild card for 2014, one that directly affects the financial sector but has implications for the general economy, is the implementation of “Dodd-Frank” legislation that fundamentally restructures the nation’s entire financial apparatus.

Dodd-Frank’s goal is to prevent future financial catastrophes, but its inevitable consequence is that fewer prospective borrowers (businesses

and households) will qualify for a reduced pool of credit, with terms that are more restrictive and costs (interest and fees) that are higher.

Only about one-half of Dodd-Frank’s rules have been finalized and full implementation isn’t expected until the end of this decade. Nonetheless, it is already altering the financial landscape in unanticipated ways and, therefore, looms as a 2014 wild card.

QE ‘tapering’ is a wild card for 2014’s economic outlook...It is probable that financial markets will be more volatile as tapering proceeds...

“

”

Critical Issues Facing Private Equity in 2014

A CohnReznick Report 11

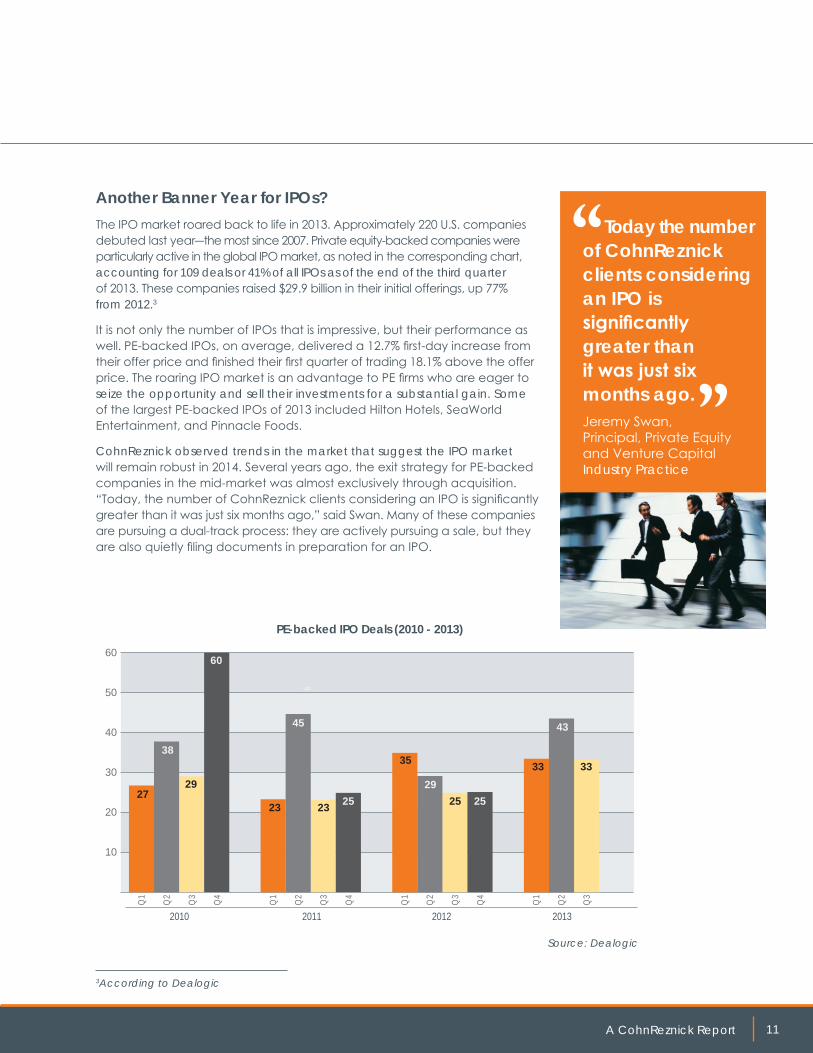

Another Banner Year for IPOs?The IPO market roared back to life in 2013. Approximately 220 U.S. companies debuted last year―the most since 2007. Private equity-backed companies were particularly active in the global IPO market, as noted in the corresponding chart, accounting for 109 deals or 41% of all IPOs as of the end of the third quarter of 2013. These companies raised $29.9 billion in their initial offerings, up 77% from 2012.3

It is not only the number of IPOs that is impressive, but their performance as well. PE-backed IPOs, on average, delivered a 12.7% fi rst-day increase from their offer price and fi nished their fi rst quarter of trading 18.1% above the offer price. The roaring IPO market is an advantage to PE fi rms who are eager to seize the opportunity and sell their investments for a substantial gain. Some of the largest PE-backed IPOs of 2013 included Hilton Hotels, SeaWorld Entertainment, and Pinnacle Foods.

CohnReznick observed trends in the market that suggest the IPO market will remain robust in 2014. Several years ago, the exit strategy for PE-backed companies in the mid-market was almost exclusively through acquisition. “Today, the number of CohnReznick clients considering an IPO is signifi cantly greater than it was just six months ago,” said Swan. Many of these companies are pursuing a dual-track process: they are actively pursuing a sale, but they are also quietly fi ling documents in preparation for an IPO.

Today the number of CohnReznick clients considering an IPO is signifi cantly greater than it was just six months ago.Jeremy Swan,Principal, Private Equity and Venture Capital Industry Practice

“

”

3According to Dealogic

PE-backed IPO Deals (2010 - 2013)

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

6

2010 2011 2012 2013

60

50

40

30

20

10

27

38

29

60

23

45

23 25

35

2925 25

33

43

33

Source: Dealogic

Middle-Market Private Equity Outlook12

Strategic Acquisitions Fuel Brisk M&A ActivityMerger and acquisition (M&A) activity also rebounded in 2013 with even brighter prospects for 2014. The total value of PE-backed M&A deals globally through July 2013 was $196.4 billion, according to Thomson Reuters—the strongest period since 2007.

CohnReznick believes M&A activity will continue to climb in 2014 as corporate buyers, emboldened by record-high cash positions and readily available debt, consider making strategic acquisitions to fuel future growth. As of November 2013, PE M&A transactions accounted for 17% of total deal value, representing $163 billion worth of disclosed transactions, according to Thomson Reuters. If the M&A market continues to gain momentum throughout 2014, PE investors will have an increasing number of options on the table and will be in an excellent position to create liquidity for their investors. Another burgeoning exit option for PE firms in 2014 is foreign buyers. Foreign companies with strong balance sheets are becoming increasingly active as they search for distribution in the U.S. market.

Overall, if the market conditions continue on course, CohnReznick anticipates brisk exit activity in 2014, especially as PE firms look to exit from companies that they have held in their portfolios for at least seven years or longer. To put into perspective the percentage of deals ripening toward exit in 2014, 62% of PE-backed deals completed in 2006 and 73% of deals in 2007 have yet to exit, according to research firm Preqin.

Critical Issues Facing Private Equity in 2014

The exit markets will continue to improve in 2014 as the IPO window remains open and corporate buyers, emboldened by record-high cash positions and readily available debt, consider making strategic acquisitions to fuel future growth.

What does CohnReznick think?

A CohnReznick Report 13

Rising Competition for PE DealsCompetition for PE transactions from non-traditional players like hedge funds, pension funds, and mezzanine lenders is on the rise.

Given improved market conditions in 2013 and into 2014, as hedge funds, pension funds, and mezzanine lenders grow in size and power, they are searching for new strategies that can earn ever-higher returns. “Today, we are seeing other alternative investment funds getting more involved in the direct investment market, this includes hedge funds building PE practices within the fund, LPs considering direct co-investments and mezzanine lenders being more active across the capital structure,” said Jeremy Swan. Hedge funds and pension funds, in particular, are starting to build out dedicated PE funds. They are recruiting external PE professionals and using pools of capital from their main operations to fund new deals.

A recent report by research firm Preqin found that 43% of institutional investors in PE funds are actively seeking opportunities to invest directly into companies―and that 11% are exploring the idea. In addition, new research conducted by Harvard Business School and Insead, a premier business school in France, concluded that direct investments into companies made by these institutions outperform the investments they make in the actual PE funds. However, hedge funds and pension funds are not the only new player. “Mezzanine lenders are starting to compete directly for deals with middle-market PE firms looking at an increased number of direct non-sponsor led transactions,” said Dom Esposito, CohnReznick Partner, National Practice and Growth Director. Rather than working with PE sponsors, some mezzanine lenders are going directly to companies and offering to finance transactions on their own, providing all or most of the needed capital.

Given the currently strong performance of PE activity, CohnReznick finds it plausible that increased competition for PE deals from non-traditional players will continue in 2014. PE firms will have to increase their flexibility as they compete for new deals. However, the impact on the industry could be higher valuations as well as more money chasing fewer quality deals.

Mezzanine lenders are starting to compete directly for deals with middle-market PE firms looking at an increased number of direct non-sponsor led transactions.Dom Esposito, Partner, National Practice and Growth Director

“

”

Increased competition from non-traditional players could result in higher valuations in 2014 as well as more money chasing fewer quality deals.

What does CohnReznick think?

Middle-Market Private Equity Outlook14

The Knowledge Bank: A Differentiator for PE Firms in 2014The U.S. middle market has changed significantly in the past decade and this has resulted in a host of new challenges for PE firms. Specifically, CohnReznick believes that one of the most challenging struggles for the middle-market in 2014 will be growth, not access to capital in 2014.

Previously, middle-market PE firms could endear themselves to target companies by offering large amounts of cash. “Today, however, target companies are more impressed with the skills and industry knowledge that a PE firm can bring to the table, rather than just the capital alone,” said Jeremy Swan. The evolution of the middle market means companies need new resources and guidance to compete. In the past, the ability to offer capital or financing was often enough, but PE firms now need to show they possess other assets. CohnReznick’s view is that adding value does not come from the capital itself. In 2014, it will be in the form of assisting a company to find third-party service providers who can identify solutions to specific problems or advise companies on pricing strategies and realizing profitable growth.”

“Another way PE firms can maximize value is by providing access to important contacts to enhance their supply chain effectiveness and open channels that they previously could not access.” Jeremy continues. Many companies can benefit from not only the capital, but the advice and access that a PE firm can give them.

Operating partners are also crucial to the equation, both in landing the deal and helping that portfolio company ultimately succeed. CohnReznick believes that PE firms that can recruit top-tier operational talent in the GP ranks stand the greatest chance of maximizing the value of their portfolio companies and thriving in the future.

“Successful PE firms will be those that can add the most value, post-acquisition, to their portfolio companies,” said Swan. This means that PE firms must continue to adapt and transform in 2014, whether that means hiring more operating talent, knowing when to replace a management team, or shift the firm culture to create more value.

Critical Issues Facing Private Equity in 2014

The challenge is not access to capital―the challenge to middle- market PE firms in 2014 will be propelling growth of portfolio companies. PE firms that can recruit top-tier operational talent in the GP ranks stand the greatest chance of growing their portfolio companies and thriving this year.

What does CohnReznick think?

A CohnReznick Report 15

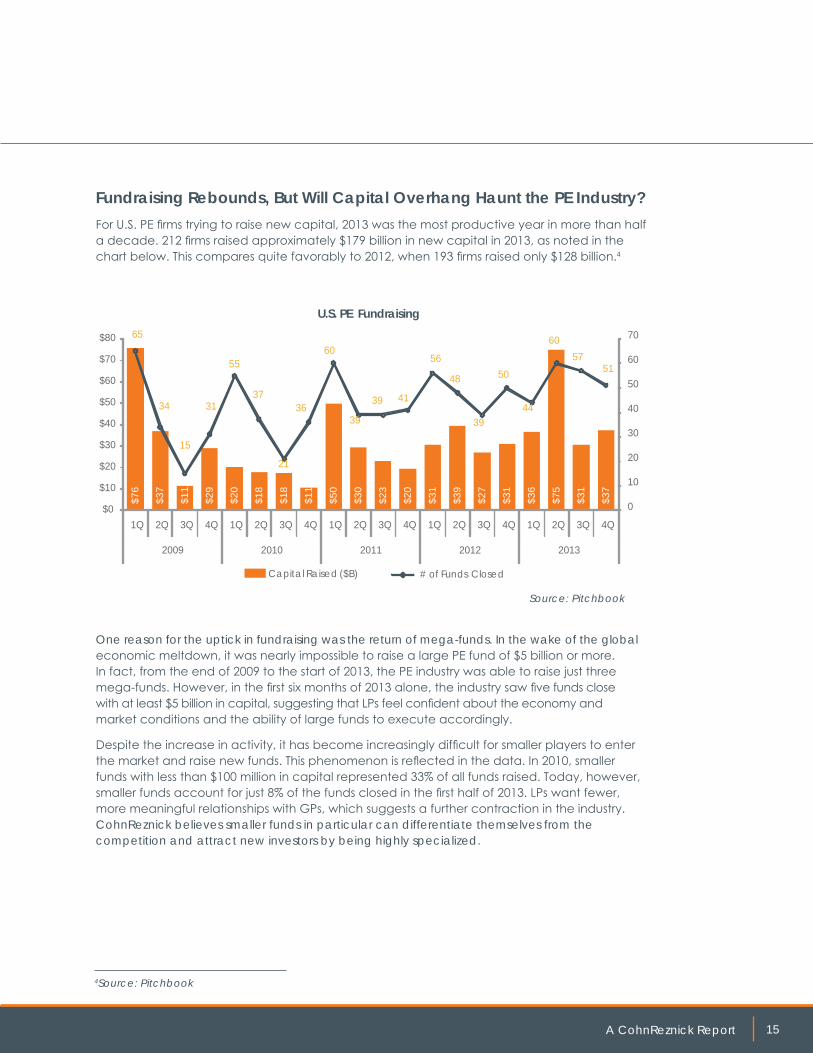

Fundraising Rebounds, But Will Capital Overhang Haunt the PE Industry?For U.S. PE firms trying to raise new capital, 2013 was the most productive year in more than half a decade. 212 firms raised approximately $179 billion in new capital in 2013, as noted in the chart below. This compares quite favorably to 2012, when 193 firms raised only $128 billion.4

One reason for the uptick in fundraising was the return of mega-funds. In the wake of the global economic meltdown, it was nearly impossible to raise a large PE fund of $5 billion or more. In fact, from the end of 2009 to the start of 2013, the PE industry was able to raise just three mega-funds. However, in the first six months of 2013 alone, the industry saw five funds close with at least $5 billion in capital, suggesting that LPs feel confident about the economy and market conditions and the ability of large funds to execute accordingly.

Despite the increase in activity, it has become increasingly difficult for smaller players to enter the market and raise new funds. This phenomenon is reflected in the data. In 2010, smaller funds with less than $100 million in capital represented 33% of all funds raised. Today, however, smaller funds account for just 8% of the funds closed in the first half of 2013. LPs want fewer, more meaningful relationships with GPs, which suggests a further contraction in the industry. CohnReznick believes smaller funds in particular can differentiate themselves from the competition and attract new investors by being highly specialized.

4Source: Pitchbook

U.S. PE Fundraising

$76

$37

$11

$29

$20

$18

$18

$11

$50

$30

$23

$20

$31

$39

$27

$31

$36

$75

$31

$37

65

34

15

31

55

37

21

36

60

39

39 41

56

48

39

50

44

6057

51

0

10

20

30

40

50

60

70

$0

$10

$20

$30

$40

$50

$60

$70

$80

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2009 2010 2011 2012 2013

Capital Raised ($B) # of Funds Closed

Source: Pitchbook

Middle-Market Private Equity Outlook16

Although smaller firms are finding it difficult to raise new funds, funding still presents challenges for larger PE firms. Fundraising can be a double-edged sword for larger funds when it results in PE firms having more capital on hand than they are able to spend due to a shortage of quality deals. Termed “capital overhang,” this so-called “dry powder” surged to $1.074 trillion as of December 2013―a record high, according to research firm Preqin.

CohnReznick anticipates that capital overhang challenges will continue into 2014 and that valuations could increase across the board as funds face pressure to put money to work before their investment period ends. Another consideration is that the overhang may also result in more sponsor-to-sponsor transactions, with PE firms selling their portfolio companies to other PE firms. With piles of dry powder still waiting to be put to work, it is reasonable to expect an overall increase in deal activity in 2014.

Critical Issues Facing Private Equity in 2014

Capital overhang challenges will continue into 2014 and valuations could increase across the board as funds feel the obligation to put money to work before their investment period ends.

What does CohnReznick think?

A CohnReznick Report 17

Crowdfunding: A Source of Wisdom for Private Equity?The JOBS Act and the introduction of equity-based crowdfunding may quite possibly be one of the most significant developments in the history of the capital markets. In 2013, Federal regulators lifted an 80 year ban on the advertising of private securities to the general public by hedge funds, venture capital funds, and start-up companies seeking capital. In essence, the market has democratized the flow of capital. It is no longer select investment professionals who can invest in the most promising private companies—any qualified buyer anywhere in the world can now hold an equity interest in a private organization.

Crowdfunding rules passed in 2013 permit an issuer to complete a Private Issuers Publicly Raising (PIPR) financing under the 506c exemption where there are no offering limits, no advertising restrictions, no audit requirements, and no ongoing filing obligations. In addition, recently approved intrastate crowdfunding rules enable emerging growth companies to raise up to $1 million from any investors, whether they are accredited or unaccredited, as long as that investor resides in the same state as the issuer. To date, only Georgia, Kansas, and Wisconsin have passed intrastate crowdfunding legislation.

Though the addition of new investors could result in increased competition for deals, CohnReznick believes there are certain aspects to crowdfunding that will benefit the PE industry in 2014 and beyond. One of the principal advantages to PE firms is the free flow of data and information covering private companies. For instance, sites like SecondMarket and AngelList are revolutionizing the financial markets by connecting issuers, investors, and sellers through technology-enabled solutions. These sites provide analytics about what the market likes or dislikes about a particular product or company.

How does this benefit PE firms? They can more effectively gauge the types of companies that are resonating in the market and where they should be allocating their funds. The more data that is made available by the crowd, the better private equity can identify the best deals and make the most profitable investments.

Another exciting development for the PE industry as a result of the JOBS Act is the opportunity for the PE funds themselves to raise money from non-accredited investors, possibly through options in their 401(k) plans. Currently, only accredited investors with more than $1 million in net worth are allowed to invest in PE funds.

Crowdfunding is democratizing the flow of capital and aspects of the JOBS Act could considerably benefit investment activity in the PE industry in 2014 and beyond.

What does CohnReznick think?

The market has democratized the flow of capital... any qualified buyer anywhere in the world can hold an equity interest in a private organization.

Middle-Market Private Equity Outlook18

How much of an impact can non-accredited investors potentially have on the equity market as a result of the JOBS Act? They could have a $3 trillion impact—that is the amount of capital available in self-directed IRAs and 401(k)s. That is a game-changing amount of money that, currently, is generally being invested into a narrow type of asset class: namely, mutual funds. CohnReznick believes that the industry will find that savvy PE firms will venture to create fund vehicles that can be sold directly to individuals via their defined contribution plans such as IRAs and 401(k)s. Pantheon Ventures, for instance, says it is the first PE firm to offer exposure to the asset class via so-called target date funds, which are the default investment in 401(k) plans. CohnReznick believes that defined contribution plans could eventually become a significant new source of capital for the PE industry, particularly as traditional capital sources like public employee pensions and corporate defined benefit plans continue to decline.

The GP/LP Power Pendulum—Which Way Will It Swing in 2014?The balance of power between LPs and GPs is always a hot-button issue in the PE world. During the financial crisis, momentum clearly shifted in favor of LPs, and they were able to have more control on a number of significant issues—including all-important fee structures.

But will momentum remain with LPs in 2014, or will the pendulum swing back? “When it comes to fee structures, LPs are asking for more concessions—and for the most part they appear to be getting them,” said Jay Levy, CohnReznick Partner and Financial Services Industry Practice Leader. Case in point: the deal fees that PE firms charge their portfolio companies for consulting services.

Prior to 2013, PE firms generally retained most of the deal fee income for themselves. Approaching and into 2014, CohnReznick observes that GPs are handing back anywhere from 80% to 100% of those deal fees to their LPs.

Critical Issues Facing Private Equity in 2014

LPs have become more savvy and sophisticated. They are not afraid to voice their concerns and tell their GPs exactly what they think. They are demanding more concessions from LPs and in many cases, they are getting them.

What does CohnReznick think?

A CohnReznick Report 19

A similar trend is developing with carried interest and the way in which proceeds from the sale of a portfolio company are distributed. LPs are displaying a preference for the European-style waterfall model where PE funds do not pay carried interest to their fund managers until all capital that has been drawn-down has first been returned to the investors. This is a change from the more GP-friendly distribution models in the U.S. that allow PE firms to receive their funds sooner.

“It is fair to say that PE has always been Darwinian in nature—and 2014 will be no different,” said Levy. Only the strong survive. CohnReznick believes that in the coming year, GPs will be rigorously tested. Those that do not heed the wishes of their LPs may find it difficult to raise new capital, even from their tried-and-true investors.

Tax Reform: Carried Interest in the Crosshairs?A perennial fear in the PE industry is that carried interest will be taxed not as capital gains, but as ordinary income, generally bearing higher tax rates. New developments in 2013 intensified the PE industry’s concern.

“In recent years, many have argued that income earned by investment managers through carried interest should be taxed as ordinary income rather than as an allocation of capital gains,” said Joseph Mudd, Partner and CohnReznick National Director of Tax Specialty Services. From 2007 to 2009, several proposals were introduced to eliminate the capital gains treatment of carried interest. The Obama administration included the elimination of favorable tax treatment for carried interests in its budgets for fiscal years 2012, 2013, and 2014—regardless of the character of the income at the partner level.

Recent proposals from the House and Senate in 2013 indicate an increased willingness to treat carried interest compensation as ordinary income instead of taxing it at the lower capital gains rate. Before the October 2013 sequestration, Congressman David Camp, Chair of the House Ways and Means Committee, stated that such a bill may come as part of a wider package of tax reforms.

Proposals to treat carried interest as ordinary income were introduced in the Senate in February of 2013 and again in the House in July of 2013. As of the publication of this report, the bills have moved forward out of the committee stage. Most recently, in November 2013, Senate Democrats proposed eliminating the carried interest benefit in their bipartisan budget conferences with Republicans to prevent another sequestration.

In addition, a decision by the First Circuit Court of Appeals in August of 2013 does not bode well for the carried interest benefit. The court ruled that Sun Capital Partners was liable for $4.5 million in pension payments to the employees of its bankrupt portfolio company Scott Brass.

Sun Capital argued that it was a passive investor in Scott Brass and thus was not subject to the tax laws that would require it to assume the pension liabilities. The court, however, didn’t buy the “passive investor” argument. Instead it ruled that Sun Capital was engaged in a “trade or business” through its management and operational control of Scott Brass and, therefore, was responsible for the pension obligations.

It is fair to say that PE has always been Darwinian in nature―and 2014 will be no different.Jay Levy, Partner, Financial Services Industry Practice Leader

“”

Middle-Market Private Equity Outlook20

“The ruling rang alarm bells throughout the PE sector and alerted investors to the additional risk attached to companies that have employee pension obligations” said Mudd. The ruling also raised a thornier and potentially more serious question: Will a new “trade or business” classification have implications for the treatment of carried interest?

Is this ruling the ammunition that PE opponents can lean on to support their claim that carried interest should be taxed not as capital gains but as ordinary income?

With budget deficits at all-time highs, Congress is looking aggressively for new revenue sources. Carried interest is an increasingly attractive target. The Sun Capital ruling could be the final impetus that pushes carried interest into the ordinary income chasm.

What should PE firms do now in 2014? “As no carried interest legislation has been enacted yet, PE firms should consider the benefit from the favorable treatment carried interest provides to the extent possible in filing their 2013 tax returns—and prepare for future potential negative reforms to the taxation of carried interest,” said Mudd. Selling positions, or creating constructive sales, will yield gains from the carried interest that will still be taxed at current capital gains rates. CohnReznick also recommends that private equity managers consider distributing securities to preserve potential capital gain income in 2014.

Critical Issues Facing Private Equity in 2014

To prepare for future potential reforms, it may be prudent for PE firms to sell positions in 2014 that yield gains from the carried interest that can still be taxed as capital gains.

What does CohnReznick think?

A CohnReznick Report 21

Will Big Data Boost PE Performance?Private equity is all about outsized returns. But the industry is more competitive than ever with pricing trending upwards and blockbuster exits becoming less frequent. That is why, in 2014, to bolster returns and jumpstart performance, CohnReznick anticipates that savvy PE firms will place greater reliance on IT and Big Data analytics within their portfolio companies.

Already, PE managers are relying less on financial engineering and focusing more on operational improvements to drive growth and create value. “They are increasingly investing in Big Data solutions to help their portfolio companies better understand customer behavior, control costs, and make smarter business decisions” said Dave Rubin, Principal, CohnReznick Advisory Group and Management Consulting National Director.

How can Big Data help private equity? “A PE firm that owns a large retail chain can use Big Data to dramatically improve the business,” said Rubin. Big Data enables a retail brand with thousands of locations to learn what similarities are shared by consumers at its top 10 stores. What attributes do the best-performing stores possess that others do not and how can those attributes be applied at other store locations? Analytics can show patterns and behaviors that best performers possess.

“Many companies still have trouble capturing and analyzing all the operational data within their organization,” said Rubin. But CohnReznick predicts the onus will increasingly be on PE investors to make technology a priority and help portfolio companies turn their mountains of information into meaningful insights. By doing so, Big Data can lead to even bigger returns for private equity.

Add-On Investments Add UpPE activity surrounding add-on financings continues to grow, accounting for 53% of all PE buyout deals in 2013, a record high. After more than a decade of steady growth, the number of add-on deals surpassed platform buyouts for the first time ever in 2013.

CohnReznick observes a continual shift away from platform buyouts to more add-on acquisitions and minority deals. With PE firms finding it more difficult to identify new platform deals, they appear to be spending more time and money on growing their existing portfolio companies primarily through acquisition. CohnReznick believes that the high demand and low supply for quality deals has fueled add-on acquisitions, which typically involve smaller companies that fly under the radar of many PE firms, resulting in less competition and lower prices.

“

”

How can Big Data help private equity? A PE firm that owns a large retail chain can use Big Data to dramatically improve the business.David Rubin, Principal, CohnReznick Advisory Group and Management Consulting National Director

Middle-Market Private Equity Outlook22

As the above chart shows, add-on activity has been steadily growing as a share of overall buyout activity over the last decade, jumping from 36% of buyouts in 2004 to 53% in 2013. Indeed, the remarkable growth of add-on deals over the past decade is one of the most significant trends in the PE industry, especially as firms focus their efforts on improving operations and boosting growth at portfolio companies.

CohnReznick expects that the trend toward add-ons may continue in 2014 as PE firms spend less time trying to generate returns though financial engineering and more time working hands-on with their portfolio companies to enhance operations through smaller add-on acquisitions and increasing value.

Critical Issues Facing Private Equity in 2014

The high demand and low supply for deals may continue to fuel add-on acquisitions.

What does CohnReznick think?

U.S. PE Buyout Add-On %

36%39% 41% 43% 44%

47% 45%49% 48%

53%

0%

10%

20%

30%

40%

50%

60%

0

500

1,000

1,500

2,000

2,500

3,000

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

on Add-On % of BuyoutNon Add-On Add-On

Source: Pitchbook, PE Breakdown, 2014 Annual Report–U.S. Edition

A CohnReznick Report 23

Public-to-Private Transactions on the Rise?2013 saw a noticeable resurgence in public-to-private transactions. “In addition to buyouts, other forms of PE activity are on the rise—PE-backed public-to-private transactions are once again showing signs of life,” said Dom Esposito, CohnReznick Partner and National Practice and Growth Director. These transactions have been relatively stagnant since the beginning of the financial crisis in 2008. However, last year saw the return of public-to-private mega-deals—including Dell, H.J. Heinz, and BMC software—which were not conspicuous before the global downturn. In fact, the Dell and Heinz deals were each larger in size than all of the 2012 sponsor-backed public-to-private transactions combined.

“Though it is still early to declare the return of the public-to-private market, the trend appears to be gaining traction,” said Esposito. In 2013, 71 companies as of November 2013 went from public to private, up from 66 companies in 2012, according to PitchBook. Why? One reason for the upward trend could be due to rising compliance and audit costs. CohnReznick expects to see an increase in 2014 public-to-private transactions as more middle- market companies conclude that the cost of maintaining public entity status outweighs the benefits being realized.

In fact, public companies paid average audit fees of $4.5 million in 20125, representing a 4% increase from the prior year’s audit fees. By contrast, private companies—on average—paid just $147,800 in audit fees in 2012. What is the outlook for audit fees in 2014? “We believe the costs of maintaining public company status are likely to increase in 2014 due to new standards imposed on audit firms by the Public Company Accounting Oversight Board (PCAOB),” said Kurtis Wolff, CohnReznick Managing Partner of Assurance. For instance, there will be a major change in how company audits are reported to the public. The new guidelines retain the pass/fail model in the existing auditor’s report, but would provide additional information to investors and other financial statement users about certain aspects of the audit and the auditor.

For public companies, the new PCAOB rules appear likely to increase the scope of audit services required as well as escalate compliance costs. But what does this mean for the PE industry? CohnReznick believes that more stringent audit rules will result in increased public entity compliance and regulatory costs, which could lead to greater acquisition opportunities for PE firms who are well-positioned to take public companies private.

Though it is still early to declare the return of the public-to-private market, the trend appears to be gaining traction.Dom Esposito, Partner, National Practice and Growth Director

“

”

5According to the Audit Fee Survey conducted by Financial Executives International

Middle-Market Private Equity Outlook24

”The capital markets improved considerably last year and continue to look promising for 2014. PE buyers, loaded with capital that largely sat idle over the past five years, are now vigorously pursuing growth opportunities. But it is more essential than ever for PE firms to catch the right wave in 2014. By conducting thorough due diligence, PE buyers can ensure they make the most lucrative investments at the most conservative price. What is key in 2014? Due diligence measures aimed at identifying opportunities to improve a company’s operating effectiveness and efficiency.

Financial Due DiligenceOne of the biggest trends in the PE industry is the growing appetite for smaller companies, especially as PE firms adopt a “buy and build” strategy. “As competition for good deals increases, PE firms that once only looked at companies with $100 million or more in EBITDA are now investing in companies at significantly smaller levels,” said Margaret Shanley, a CohnReznick Principal in the Transactional Advisory Services Practice. As more PE firms are likely to discover in 2014, conducting financial due diligence on small and mid-sized companies can prove to be challenging.

“It is our experience that many smaller companies, by nature of their size and lack of sophistication, do not have the proper accounting controls and systems in place,” said Claudine Cohen, a CohnReznick Principal in the Transactional Advisory Services Practice. The onus is on PE buyers to carefully scrutinize various aspects of a target―including the company’s revenue recognition policies and how it is reporting expenses.

Private Equity Due Diligence Focus

A CohnReznick Report 25

With smaller companies, due diligence may need to be performed in areas that may not be an issue for larger targets. For instance, if the owner pays for a trip with family members, are personal expenses mingled with business expenses? Or, in an effort to keep growing revenue, has the company instituted a series of price increases in an effort to conceal falling volume? Does the company have multiple product lines and revenue streams, but is the bulk of sales coming from one particular product or customer? These are serious issues that can materially impact the valuation of the company. “The challenge facing acquirers is that more often than not the operating metrics and data are not readily available due to lack of reporting systems. Due diligence techniques can find alternative methods to measure and analyze trends in the data,” says Cohen.

“As competition for good deals increases and PE firms potentially invest in smaller companies this year, these are the financial due diligence issues that PE buyers must increasingly delve into in 2014. They speak directly to the reliability and availability of the financial data as well as the quality of the finance team,” said Sharon Bromberg.

IT Due DiligenceIt was only a few years ago that information technology (IT) due diligence played second fiddle to other areas of due diligence. In 2014, based on what we are seeing that is no longer the case,” said Swan. It was previously common for PE buyers to examine a target company’s IT infrastructure only after the deal closed. This often led to unforeseen expenses as PE firms realized too late they would have to invest in new hardware, software, and services to scale the acquired business and make it more competitive in the marketplace.

Many PE professionals see IT as a black box. They do not know much about it, so they avoid it, but as they later find out, that can be a very costly mistake. Indeed, a 2011 study by McKinsey & Company found that most IT issues are not fully addressed during the due diligence period.

IT infrastructure should be one of the first assets PE firms examine when evaluating an acquisition target. After all, a solid information technology foundation is often the mark of a well-run business— and a signal that an investment has the propensity to be successful.

When conducting IT due diligence, PE buyers need to ensure that all business systems, including customer support, manufacturing, and HR applications, are modernized, well-implemented and integrated. Listed below are some questions to consider:

• Is the company using the current version of software packages and is the software still supported by the manufacturers?

• Are the systems integrated and does data flow seamlessly from one application to another? Is the technology scalable and can it grow with the business?

The challenge facing acquirers is that more often than not the operating metrics and data are not readily available due to lack of reporting systems.Claudine Cohen, Principal, Transactional Advisory Services Practice

“

”

Middle-Market Private Equity Outlook26

• Are the systems operating effectively and producing the timely, accurate information the company needs to stay ahead of the competition?

• Is there a disaster recovery program in place?

“The bottom line is that, well before making an investment decision, PE firms should determine the amount of money and resources required to upgrade or scale IT systems,” said Swan. In the modern business world, few companies can operate successfully or remain competitive without a robust IT infrastructure. A small investment in IT due diligence upfront can eliminate risks and result in significant benefits down the road.

Operational Due DiligenceIn 2014, PE professionals will rely less on financial engineering and more on operational improvements to grow portfolio companies and create value for their investments. Last year, PE firms concentrated on making add-on acquisitions and operational improvements at existing portfolio companies. We expect PE firms to increase their focus on operational due diligence throughout 2014 in order to expedite portfolio company growth and realize synergies that produce financial benefits.

Increasingly and particularly for 2014, a target company’s potential for operational improvement is a critical element of a successful acquisition. As such, PE buyers should be carefully scrutinizing the operational systems of target companies, including everything from supply chain and manufacturing applications to inventory management and logistics.

Questions that PE firms should be asking themselves ought to be directed at determining how efficiently operational processes are being conducted and where they can improve them and add value. Questions such as: Can the target company project customer demand and can it accurately stock inventory shelves for next week or next month? Are there opportunities to create a more efficient supply chain and reduce costs and resource requirements?

Private Equity Due Diligence Focus

A CohnReznick Report 27

The impetus is on PE buyers―failing to inspect the company’s operations can damage even the most promising acquisitions. Deals that initially appear attractive often fall short as a result of operational inefficiencies that go unnoticed during the due diligence process. These operational risks can vary from traditional back office operations to compliance-related risks to safety and environmental issues. For instance, PE firms should investigate whether safety and environmental processes are being conducted according to best practices, or are there better ways the target can approach the processes? Understanding and addressing such issues will arm PE buyers with a greater chance of capturing value quickly and ultimately making a more successful investment.

Tax Due DiligenceCohnReznick expects that federal, state, and local tax authorities will be even more aggressive in their application of tax regulations in 2014. With budget deficits reaching record highs in 2013, tax authorities are increasingly targeting small and mid-sized businesses to close the tax gap in 2014.

According to its own studies, the IRS approximates that 40 percent of the tax gap stems from small businesses. This contribution totals $180 billion of the $450 billion in taxes owed to the IRS with much of the balance stemming from underreported income.

While taxing authorities are taking extensive measures in an effort to raise more money for their coffers―the IRS has been inquiring with businesses that receive income via credit and debit cards about whether they are declaring all of their business income. The agency sent approximately 20,000 Notification of Possible Income Underreporting notices to businesses in 2013.

What does this mean for PE firms? CohnReznick suggests that PE firms become more sophisticated than ever in 2014 as they conduct their due diligence and identify tax issues that could potentially impact valuation. “By conducting the proper tax due diligence, PE firms can gain tremendous tax benefits by uncovering structuring opportunities and planning against tax challenges,” said Henry Paula, CohnReznick Tax Partner. After all, the last thing any PE firm wants is to buy a company for $100 million, only to find out that the target is later assessed $10 million in taxes. Although this is more likely to occur in the acquisition of C-corporation stock, buyers may still be responsible for non-income tax successor liabilities in the form of asset purchases and acquisitions of S corporations and partnerships. In either case, the PE firm’s internal rate of return, focus on the business, and potentially its credibility with investors and management could be impacted. The execution of a well thought-out tax due diligence plan could significantly reduce overall tax risk.

By conducting the proper tax due diligence, PE firms can gain tremendous tax benefits by uncovering structuring opportunities and planning against tax challenges.Henry Paula, Tax Partner

“

”

Middle-Market Private Equity Outlook28

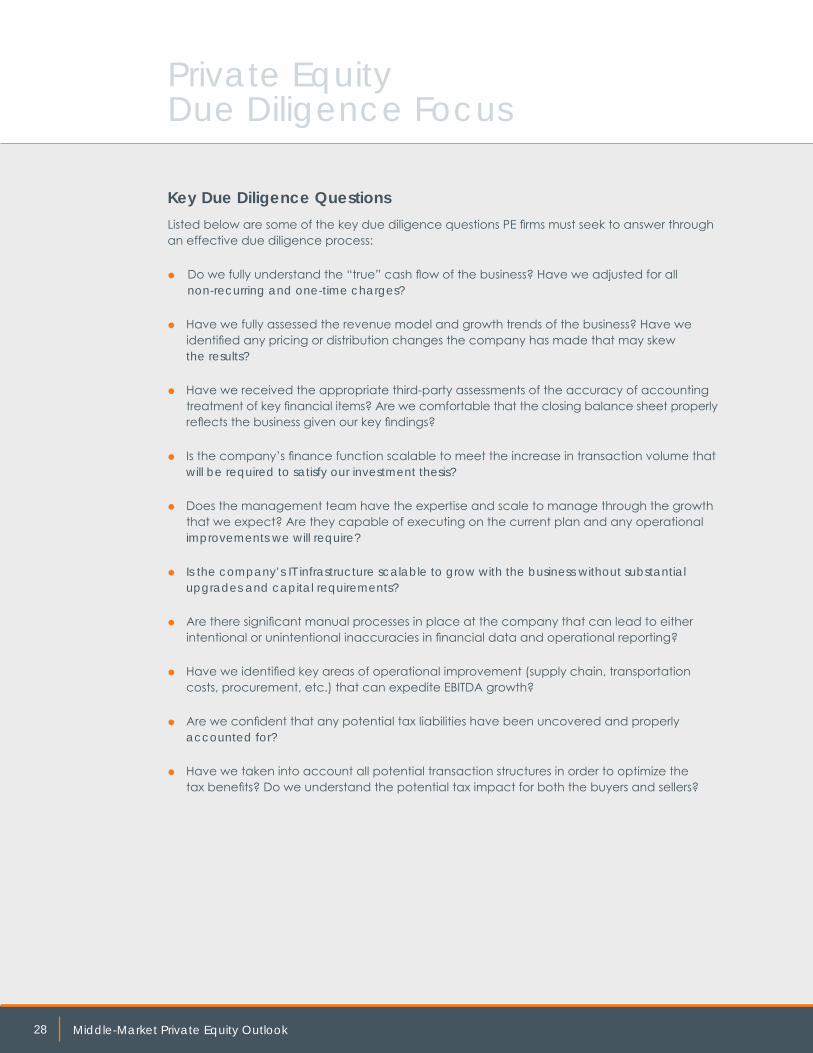

Key Due Diligence QuestionsListed below are some of the key due diligence questions PE firms must seek to answer through an effective due diligence process:

• Do we fully understand the “true” cash flow of the business? Have we adjusted for all non-recurring and one-time charges?

• Have we fully assessed the revenue model and growth trends of the business? Have we identified any pricing or distribution changes the company has made that may skew the results?

• Have we received the appropriate third-party assessments of the accuracy of accounting treatment of key financial items? Are we comfortable that the closing balance sheet properly reflects the business given our key findings?

• Is the company’s finance function scalable to meet the increase in transaction volume that will be required to satisfy our investment thesis?

• Does the management team have the expertise and scale to manage through the growth that we expect? Are they capable of executing on the current plan and any operational improvements we will require?

• Is the company’s IT infrastructure scalable to grow with the business without substantial upgrades and capital requirements?

• Are there significant manual processes in place at the company that can lead to either intentional or unintentional inaccuracies in financial data and operational reporting?

• Have we identified key areas of operational improvement (supply chain, transportation costs, procurement, etc.) that can expedite EBITDA growth?

• Are we confident that any potential tax liabilities have been uncovered and properly accounted for?

• Have we taken into account all potential transaction structures in order to optimize the tax benefits? Do we understand the potential tax impact for both the buyers and sellers?

Private Equity Due Diligence Focus

A CohnReznick Report 29

After several challenging years, private equity roared back to life in 2013. The industry returned record amounts of capital to investors, benefited from a blossoming exit market, and raised a respectable number of new funds.

However, the question now is: Can private equity carry that momentum into 2014? Dom Esposito says, “The signs are certainly favorable for the industry.” Institutional investors like pension funds and university endowments that were lured away from the asset class in favor of other markets, such as public stocks, may return to private equity in 2014 given its strong performance in 2013. In fact, the tenuous balance of power between PE firms and their investors could swing back in favor of general partners as more capital is committed to the asset class.

Indeed, PE performance could surpass last year given the red-hot IPO market and the success of PE-backed companies that have recently exited. Shares in PE-backed companies that listed last year rose 18.6 percent, a notable performance that is likely to spark interest from more institutional investors as the IPO pipeline grows.

The exit market could heat up further as PE firms are sitting on a record number of aging portfolio companies from the pre-recession period that are ripe for a liquidity event. “Exiting these unrealized investments and returning capital to investors will be a primary concern for PE firms in 2014,” said Esposito. Cambridge Associates reports that PE firms collectively have more than 3,000 investments on their books that need to be sold in the coming years.

Despite a positive outlook, 2014 undoubtedly brings forth challenges. With a sizable capital overhang and PE firms chasing a dwindling number of quality deals, valuations could increase dramatically, leading to bubble-like pricing. This scenario could be exacerbated if PE firms become reluctant to make new investments due to high prices and soaring valuations.

At a time when deal-making has become more challenging, CohnReznick advises that the ability to deploy capital will be a key to success. Firms that can wisely put their capital to work in 2014 will reap the rewards into 2014 and beyond.

The Road Ahead

Middle-Market Private Equity Outlook30

Members of CohnReznick’s Private Equity and Venture Capital Industry Practice contributing to Momentum 2014: Middle-Market Private Equity Outlook include:

Mark Alimena 203-399-1902 [email protected]

Chris Aroh 860-368-5284 [email protected]

Sharon Bromberg 732-635-3128 [email protected]

Claudine M. Cohen 646-625-5717 [email protected]

Dom Esposito 646-254-7414 [email protected]

Brian Gibney 301-280-3075 [email protected]

Ron Kaplan 646-834-4179 [email protected]

Gary Levy 646-254-7403 [email protected]

Jay Levy 646-254-7412 [email protected]

Maier Rosenberg 818-205-2681 [email protected]

David Rubin 973-871-4021 [email protected]

Richard Schurig 973-364-6670 [email protected]

Margaret Shanley 310-598-1669 [email protected]

Jeremy Swan 646-625-5716 [email protected]

Ira Weinstein 410-783-8328 [email protected]

About CohnReznick’s Private Equity and Venture Capital Industry PracticeAs one of the leading accounting, tax, and advisory firms in the United States, CohnReznick provides private equity and venture capital firms, family offices, small business investment companies (SBICs), and other investment groups with technical skills grounded in deep industry expertise. With partner-level involvement at all stages, CohnReznick’s PE and venture capital professionals offer fully coordinated delivery of services for every transaction—from acquisition to exit.

Our PE and venture capital clients rely on our professionals to help them maximize the value of their investments. Services to PE and venture capital clients include:

• Transaction Services due diligence and purchase price dispute services grounded in industry insight;

• Value Enhancement Services to improve EBITDA and increase cash flow. Our Business Discovery Boot Camps lead management through a collaborative process that looks beyond functional boundaries to root out opportunities to eliminate waste and add value;

• Portfolio Company Compliance including audit, tax, and consulting services that culminate with a summary of observations to improve EBITDA;

• Fund Compliance solutions; and

• Proprietary, Pre-Auction Deal Flow.

About CohnReznick’s Private Equity Practice

A CohnReznick Report 31

CohnReznick Advantage for Private Equity/Venture Capital Industry

Industry Insights, Optimized Solutions

• Our understanding of private equity and venture capital industry drivers, combined with consistent client service teams, translates to thoughtful, well-prepared transaction advisory, compliance, and value enhancement services.

• We leverage industry expertise to expose risks and identify opportunities inherent to each transaction.

Transformative Advice

• Timely, relevant views on topics such as carried interest, capital formation, exit strategies, tax issues, and the impact of sovereign governments on limited partner investors.

• Thought leadership on the JOBS Act, potential immigration reform, SEC oversight, and trends in liquidity events and capital formation.

Responsive Culture

• In competitive situations where successful deals often hinge on our ability to deliver insightful results quickly, our clients benefit from an accessible team, empowered to meet their needs.

• Whether providing due diligence, transaction advisory, tax, or compliance service at the fund or portfolio company level, we recognize the time sensitivity of helping clients achieve investment goals and meet regulatory requirements.

Capital Markets Dexterity

• Our Firm culture collaboratively connects clients with proprietary opportunities for acquisitions, dispositions, and strategic partnerships.

• We have the institutional credibility necessary to connect private investors and their portfolio companies with acquisition opportunities, liquidity events, and other capital-raising needs.

Proactive, Resourceful Services

• Partner-led service teams introduce opportunities, initiate critical discussions, and ensure that client expectations are documented and met through customized Client Service Plans.

• As advisers to the private equity and venture capital community, we connect clients to our vast resources, including educational events, regulatory updates, and business opportunities.

National with Global Reach

• With offices in the leading financial centers, we are geographically situated to perform local fund-level and portfolio company services.

• As an independent member of Nexia International, we assist clients with acquisitions, dispositions, compliance, tax, and advisory services in 590 offices in more than 100 countries.

About CohnReznick LLP

With origins dating back to 1919, CohnReznick LLP is the 11th largest accounting, tax, and advisory firm in the United States, combining the resources and technical expertise of a national firm with the hands-on, entrepreneurial approach that today’s dynamic business environment demands. CohnReznick serves a large number of diverse industries and offers specialized services for Fortune 1000 companies, owner-managed firms, international enterprises, government agencies, not-for-profit organizations, and other key market sectors.

Headquartered in New York, NY, CohnReznick serves its clients with more than 280 partners, 2,200 employees, and 26 offices. The Firm is a member of Nexia International, a global network of independent accountancy, tax, and business advisors. For more information, visit www.cohnreznick.com.

1212 Avenue of the Americas New York, NY 10036 212-297-0400

www.cohnreznick.comCohnReznick is an independent member of Nexia International