chapter 6 esops as a financial strategy &mlps. agenda employee stock ownership plans (esops)...

TRANSCRIPT

Chapter 6ESOPs As a financial strategy &MLPs

Agenda

Employee Stock Ownership Plans (ESOPs) Establish of ESOPs Implementation of ESOPs Advantages of ESOP Disadvantages of ESOP Types of ESOPs ESOPs as a financial strategy Uses of ESOPs Master Limited Partnerships (MLPs) Tax treatment of MLPs Types of MLPs

ESOP

An employee stock ownership plan is a type of stock bonus plan which invest primarily in the securities of the sponsoring employer firm.

Employee Stock Ownership Plan is an employee benefit plan which makes the employees of company owners of stock in that company

Definition: Defined contribution employee benefit

pension plans designed to invest at least 50% of its assets in qualifying employer securities

ESOPs may be Stock bonus plans Combined stock bonus plans and money purchase

plans May also provide for employee contributions May represent portion of profit-sharing plan

Employee Stock Ownership Plans (ESOPs)

ESOPs different from: Employee stock purchase plans

Enable employees to buy company stock at discount

Participation of all or most employees Shares sold at 85% or more of prevailing market

price of shares Executive incentive programs

Provided mainly to top management and other key employees

Part of executive compensation packages Two types

Incentive stock options Stock appreciation rights

Establish of ESOPs

A company interested in establishing an Employee

Stock Ownership Plan (ESOP) has a wide range of

options in tailoring a plan that is best suited to its

particular needs and goals.

The first step in the process of establishing an ESOP is

to develop an idea of the type of plan that will best

serve the company's interests

Implementation of ESOPs

For implementation of ESOPs the company creates a

trust to which it makes annual contributions. These

contributions are then allocated to the individual

employee accounts within the trust.

employees might join the plan and begin receiving

allocations after completing a year of service with the

company, where any year in which an employee works

at least 1000 hours is counted as a year of service.

Advantages of ESOP

Employee loyalty enhanced

Liquidity and diversification for firm owner

Minimizes dilution of control

Establishes market value for privately held stock which

could be used to value estate

Tax-free rollover is actually only a tax deferral

until securities are sold

Motivates employees because they feel they are

getting

"a piece of the rock“

A ESOP-owned corporation are 100% tax-exempt

entity

Disadvantages of ESOP

Dilution - The equity of the company is being diluted

because of the issue of further equity shares of the

company which ultimately leads to a negative effect on

the Earning per Share.

Fiduciary Liability -The plan committee members who

administer the plan are deemed to be fiduciaries, and can be

held liable if they knowingly participate in improper transactions.

substantially, the ESOP and/or the company may not have

sufficient funds to repurchase stock, upon employees’

retirement.

Stock Performance - If the value of the company does not

increase, the employees may feel that the ESOP is less

attractive than a profit sharing plan. In an extreme case, if the

company fails, the employees willLiquidity. If the value of the

stock appreciates lose their benefits to the extent that the

ESOP is not diversified in other investments

Types of ESOPs

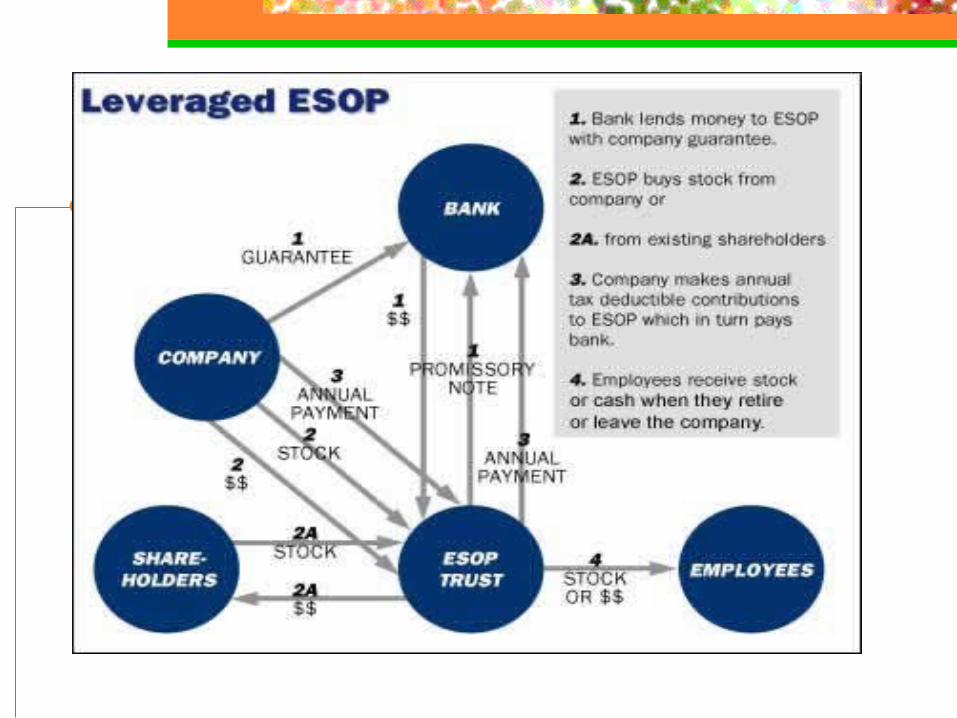

Leveraged Recognized under ERISA in 1974 Leveraged ESOP operation

ESOP fund or trust borrows funds from financial institutions

Lender transfers cash to ESOP trust in return for written obligation

Sponsoring (employer) firm generally guarantees loan

ESOP trust uses borrowed funds to purchase securities from sponsoring firm

Sponsoring firm transfers stock to name of ESOP trust as portions of principal are repaid

Types of ESOPs

Leveragable Recognized under ERISA Plan authorized but not required to borrow funds

Nonleveraged The sponsoring employer contributes newly issued or

treasury stock and/or cash to buy stock form existing owners. Contributions generally may equal up to 15% of covered payroll

Recognized under ERISA Plan does not provide for borrowing of funds Essentially stock bonus plan

ESOPs as a financial strategy

ESOPs may provide shareholders with increased value When the company's performance lags, employee

shareholders are exposed to market losses in an investment that they cannot divest while employed by the firm. Tax credits ESOPs

Provided by Tax Reduction Act of 1975; known as Tax Reduction Act ESOPs or TRASOPs

In addition to regular investment credit in existence at that time, additional investment credit of 1% of qualified investment in plant and equipment could be earned by contribution of that amount to ESOP

ESOPs as a financial strategy

In 1976, additional 0.5% credit added for companies that

matched contributions of employees of same amount to TRASOP

In 1983, basis for credit was changed from plant and equipment

investments to 0.5% of covered payroll — plans called payroll-

based ESOPs or PAYSOPs

Recently, the Reconciliation Act of 2001, exempted employees' elective

deferrals to their retirement plans from the calculation of total employer

contribution to defined-contribution plans such as ESOPs and 401(k)s.

In addition, the maximum contribution percentage was raised to 25%

from 15% of total eligible pay

Uses of ESOPs

Corporate restructuring activities Buy private companies (59% of leveraged

ESOPs) Divestitures (37% of leveraged ESOPs) Rescue operations of failing companies Raising new capital Takeover defense to hostile tender offers

Master Limited Partnerships (MLPs)

Business organizational forms in general Proprietorships and partnerships

Most numerous Mostly small businesses

Corporations Dominant in terms of total assets

MLPs

Four advantages in raising large sums of money

Limited liability for shareholders Unlimited life Ownership divided into many shares — limits

risk exposure Shares freely tradable for liquidity,

diversification, transferability of ownership

MLPs — relatively new form of business organization

MLPs

Master Limited Partnerships Type of limited partnerships whose interests

are divided into units that are traded on organized exchanges

First developed in oil and gas industry Some advantages

Unit tradability similar to stock Limited liability (for limited partners) Continuity of life No double taxation of business earnings

Tax treatment of MLPs

IRS focused on four characteristics to

distinguish between corporations and MLPs

Unlimited life

Limited liability

Centralized management

Transferability

MLPs may have only two of four corporate

characteristics to avoid being taxed as corporation —

usually centralized management and transferability

MLPs typically specify limited life of 100 years

MLPs have limited liability for limited partners but

unlimited liability for general partner or manager

General partner of MLPs

General manager (partner) of MLPs has unlimited liability

Virtually autocratic power Difficult to change general partner in

absence of provable fraud Alignment of interests between general

partner and public unit holders Management incentive fees Ownership of significant number of limited

partnership units

Types of MLPs

Roll-up MLPs Combine existing limited partnerships into

one publicly traded partnership First type of MLPs organized; began in oil

industry by Apache Petroleum Company in 1981

Provide liquidity for nontraded limited partnerships

Nature of roll-up

Before roll-up, there are a number of limited

partnerships in existence

General partners enter into agreement to combine a

number of previously sponsored limited partnerships; in

return for their old shares, units in new MLP are issued

After MLP has been formed, there is a general partner

and units which are owned by limited partners; units

may trade on stock exchange or over the counter

Roll-out (spin-off) MLPs

Formed by a corporation's contribution of

operating assets in exchange for general and

limited partnership interests in MLP

Sold on a yield comparison basis

First roll-out MLP created by Transco Corp in

1983

Nature of roll-out

Corporation holds a number of business segments

Corporation places assets of one or more of its business

segments into MLP

Avoid double taxation of corporate dividends

Establish a new value on undervalued assets

MLP transfers MLP units to corporation which in turn

distributes them to its shareholders

Stockholder hold stock in corporation and own units in MLP

Corporation could sell portion or all of units to outside public

Start-up MLPs

Start-up (new issue, or acquisition) MLPs

Formed by a partnership that is initially privately held but offers its interests to the public in order to finance internal growth

Nature of start-up Existing entity transfers assets to MLP Management company may be involved that provides

services to MLP and probably will be its general partner

In return, management company receives certain percentage of cash flows of MLP

General partner does not have to hold units in order to receive income