employee stock ownership plans: an overview how esops work

TRANSCRIPT

ESOP FactsEmployee Stock Ownership Plans: An Overview

How ESOPs Work

Are ESOPs Really More Complex than Other Ways to Sell a Business?

America’s Largest Majority Employee-Owned Companies

ESOP Limitations: How Small is Too Small?

Operating an ESOP Successfully

ESOPs in S Corporations

n SPECIAL OFFERS FOR ATTENDEES n NCEO MEMBERSHIP AND ORDER FORM

www.nceo.org

Since their origin in 1956, the number of employee stock ownership plan (ESOP) companies has grown to almost 11,000. ESOPs are used for many reasons, including providing for a tax-favored, flexible transition of ownership in closely held companies and as a means of providing an additional benefit that ties employee and company interests together. ESOP companies outperform conventional companies, are less likely to lay people off, and generate substantial retirement assets for employees. Despite their growth and success relatively few people know about them, and people who do often have profound misconceptions about how they work.

How Many ESOPs are There?As of 2012, the National Center for Employee Ownership (NCEO) estimates there are approximately 10,900 companies with ESOPs or substantially equivalent plans. Counting other forms of employee ownership of company stock, the NCEO calculates that approximately 25 million employees participate in an employee ownership plan. These numbers are estimates, but are probably conservative. Overall, employees now control about 8% of corporate equity. Although other plans now have substantial assets, most of the estimated 4,000 majority employee-owned companies have ESOPs.

Employee Ownership and Corporate PerformanceA 2000 Rutgers study found that ESOP companies grow 2.3% to 2.4% faster after setting up their ESOP than would have been expected without it. Companies that combine employee ownership with employee workplace participation programs

show even more substantial gains in performance. A 1986 NCEO study, confirmed by several subsequent academic studies, found that employee ownership firms that practice participative management grow 8% to 11% per year faster with their ownership plans than they would have without them. Note, however, that participation plans alone have little impact on company performance.

How ESOPs WorkIn an ESOP, companies set up a trust fund for employees and either contribute cash to buy company stock, contribute shares directly to the plan, or have the plan borrow money to buy shares. If the plan borrows money, the company makes contributions to the plan to enable it to repay the loan. Employee contributions are almost never involved. After participants leave the company, they either sell the shares in their account on the market or sell them back to the company or the plan. The Employee Retirement Income Security Act (ERISA) provides a regulatory framework for plan participation, vesting, benefit distribution, diversification, and more. The ESOP trust must act for the exclusive benefit of plan participants.

Tax IssuesIn S corporations, earnings attribu-table to the ESOP’s ownership share in S corporations are not taxable. In other words, if an ESOP owns 100% of a company’s stock, the company is not subject to federal, and often state, income tax. In C corporations, provided that an ESOP owns 30% of company stock and the seller meets certain requirements, owners of a private firm selling to an ESOP can defer taxation on their gains by reinvesting in securities of other companies. In either type of company contributions to the plan are tax-deductible. Employees pay no tax on

the contributions until they receive the stock when they leave or retire.

How Employees FareParticipants in ESOPs do well. A 1997 Washington State study found that ESOP participants earned 5% to 12% more in wages and had almost three times the retirement assets as did workers in comparable non-ESOP companies.

According to a 2010 NCEO analysis of ESOP company government filings in 2008, the average ESOP participant receives about $4,443 per year in company contributions to the ESOP and has an account balance of $55,836, both of which are substantially higher than people in comparable non-ESOP companies. People in the plan for many years would have much larger balances. In addition, 56% of the ESOP companies have at least one additional defined contribution retirement plan. By contrast, only about 44% of all companies otherwise comparable to ESOPs have any retirement plan, and many of these are funded entirely by employees.

Examples of Major ESOP CompaniesESOPs can be found in all kinds of sizes of companies. Some of the more notable majority employee-owned companies are Publix Supermarkets (over 152,000 employees), Nypro (17,000 employees), Lifetouch (26,000 employees), W.L. Gore and Associates (maker of Gore-Tex, 9,000 employees), and Davey Tree Company (7,000 employees).

Companies with ESOPs and other broad-based employee ownership plans account for well over half of all the 100 Best Companies to Work for in America year after year.

Employee Stock Ownership Plans: An Overview

www.nceo.org National Center for Employee Ownership

ESOP Facts

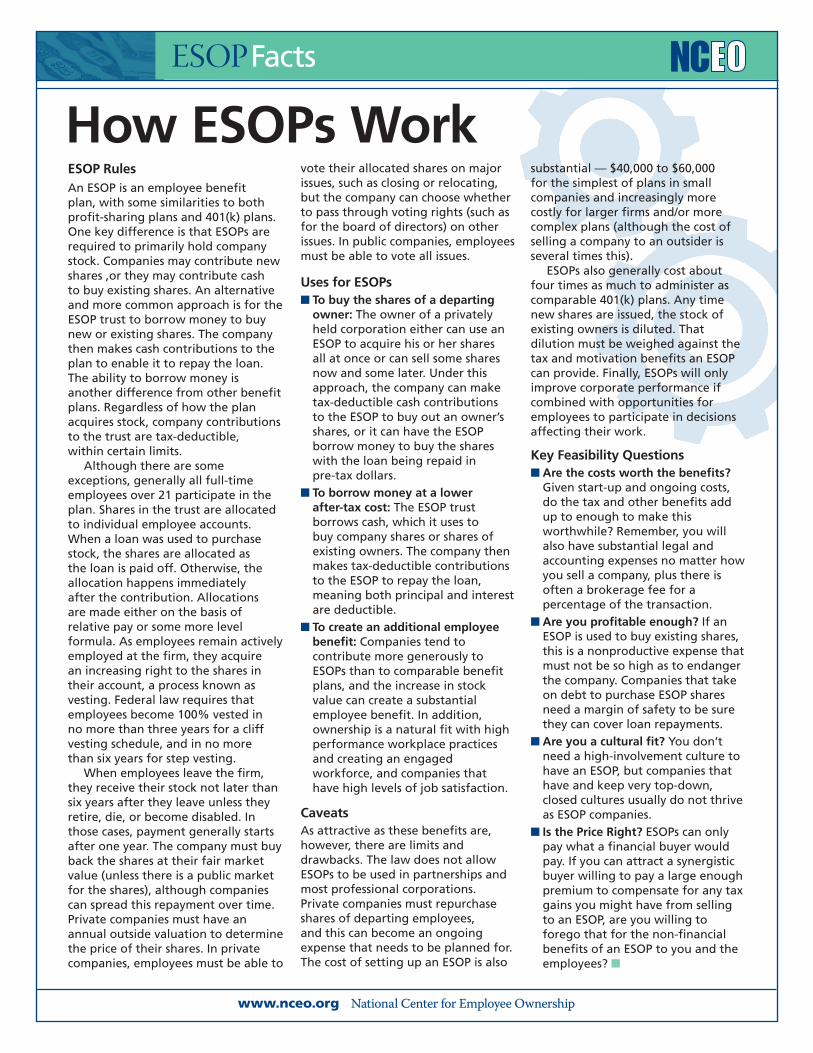

How ESOPs Workvote their allocated shares on major issues, such as closing or relocating, but the company can choose whether to pass through voting rights (such as for the board of directors) on other issues. In public companies, employees must be able to vote all issues.

Uses for ESOPs■n To buy the shares of a departing owner: The owner of a privately held corporation either can use an ESOP to acquire his or her shares all at once or can sell some shares now and some later. Under this approach, the company can make tax-deductible cash contributions to the ESOP to buy out an owner’s shares, or it can have the ESOP borrow money to buy the shares with the loan being repaid in pre-tax dollars. ■n To borrow money at a lower after-tax cost: The ESOP trust borrows cash, which it uses to buy company shares or shares of existing owners. The company then makes tax-deductible contributions to the ESOP to repay the loan, meaning both principal and interest are deductible.■n To create an additional employee benefit: Companies tend to contribute more generously to ESOPs than to comparable benefit plans, and the increase in stock value can create a substantial employee benefit. In addition, ownership is a natural fit with high performance workplace practices and creating an engaged workforce, and companies that have high levels of job satisfaction.

CaveatsAs attractive as these benefits are, however, there are limits and drawbacks. The law does not allow ESOPs to be used in partnerships and most professional corporations. Private companies must repurchase shares of departing employees, and this can become an ongoing expense that needs to be planned for. The cost of setting up an ESOP is also

ESOP RulesAn ESOP is an employee benefit plan, with some similarities to both profit-sharing plans and 401(k) plans. One key difference is that ESOPs are required to primarily hold company stock. Companies may contribute new shares ,or they may contribute cash to buy existing shares. An alternative and more common approach is for the ESOP trust to borrow money to buy new or existing shares. The company then makes cash contributions to the plan to enable it to repay the loan. The ability to borrow money is another difference from other benefit plans. Regardless of how the plan acquires stock, company contributions to the trust are tax-deductible, within certain limits.

Although there are some exceptions, generally all full-time employees over 21 participate in the plan. Shares in the trust are allocated to individual employee accounts. When a loan was used to purchase stock, the shares are allocated as the loan is paid off. Otherwise, the allocation happens immediately after the contribution. Allocations are made either on the basis of relative pay or some more level formula. As employees remain actively employed at the firm, they acquire an increasing right to the shares in their account, a process known as vesting. Federal law requires that employees become 100% vested in no more than three years for a cliff vesting schedule, and in no more than six years for step vesting.

When employees leave the firm, they receive their stock not later than six years after they leave unless they retire, die, or become disabled. In those cases, payment generally starts after one year. The company must buy back the shares at their fair market value (unless there is a public market for the shares), although companies can spread this repayment over time. Private companies must have an annual outside valuation to determine the price of their shares. In private companies, employees must be able to

substantial — $40,000 to $60,000 for the simplest of plans in small companies and increasingly more costly for larger firms and/or more complex plans (although the cost of selling a company to an outsider is several times this).

ESOPs also generally cost about four times as much to administer as comparable 401(k) plans. Any time new shares are issued, the stock of existing owners is diluted. That dilution must be weighed against the tax and motivation benefits an ESOP can provide. Finally, ESOPs will only improve corporate performance if combined with opportunities for employees to participate in decisions affecting their work.

Key Feasibility Questions■n Are the costs worth the benefits? Given start-up and ongoing costs, do the tax and other benefits add up to enough to make this worthwhile? Remember, you will also have substantial legal and accounting expenses no matter how you sell a company, plus there is often a brokerage fee for a percentage of the transaction.■n Are you profitable enough? If an ESOP is used to buy existing shares, this is a nonproductive expense that must not be so high as to endanger the company. Companies that take on debt to purchase ESOP shares need a margin of safety to be sure they can cover loan repayments.■n Are you a cultural fit? You don’t need a high-involvement culture to have an ESOP, but companies that have and keep very top-down, closed cultures usually do not thrive as ESOP companies.■n Is the Price Right? ESOPs can only pay what a financial buyer would pay. If you can attract a synergistic buyer willing to pay a large enough premium to compensate for any tax gains you might have from selling to an ESOP, are you willing to forego that for the non-financial benefits of an ESOP to you and the employees? n

www.nceo.org National Center for Employee Ownership

ESOP Facts

Are ESOPs Really More Complex than Other Ways to Sell a Business?ESOP Sale to Another Company

Key legal documents

■n ESOP plan document■n Trust agreement■n Lender agreements■n Corporate resolutions■n Stock purchase agreements■n Corporate governance agreements■n Employee contracts/management incentives

■n Detailed selling memorandum■n Sale agreement (similar to stock purchase)■n Non-compete agreements (often)■n Liens, escrow, security agreement, and personal guarantees■n Corporate resolutions■n Employee contracts/management incentives

Feasibility studies and preparation

Feasibility studies assess if the company has sufficient payroll and cash flow to buy the desired amount of stock. Can be performed internally or with expert advice. Forensic due diligence rarely needed.

Companies must prepare a detailed and accurate description of the firm and its finances, prospects, and risks. Buyers will want to do a forensic due diligence investigation and sellers should do the same to assess the financial soundness of the buyer and the terms of the offer.

Valuation Outside appraisal required Outside appraisal not required but highly recommended to help determine an appropriate selling price

Terms and risks Plans can be structured in a variety of ways in terms of financing. Rules for the operation of the plan must comply with ERISA, but leave room for considerable flexibility in design, requiring advice and consultation with experts. Escrow may be, but usually is not, required.

Buyers will typically have multiple contingencies:■n Earn-outs often required, often in the 10% to 20% range.■n Escrow held back■n Purchase price adjustments may be required based on working capital or earnings requirements■n Buyers prefer to purchase assets, with potential tax and liability implications for sellers.■n Financing may fall through

Time to sell Once the seller has decided on doing an ESOP and its basic structure, four to six months.

Median formal offer to sale time is 10 months for companies in the small to mid-market range

Role of seller post-transaction

Flexible depending on seller interests Buyer will determine role

Sale of minority interest

ESOPs can buy any percentage of stock Buyers almost invariably want to buy the entire company

Success rates If an ESOP is determined to be feasible, only rarely do transactions fall through once a decision to proceed has been made

Overall, only about 25% of privately held businesses put up for sale are sold and only about 50% of businesses with 100 or more employees are sold.

Transaction costs ■n For most closely held companies, between $60,000 and $100,000, with a minority in the $100,000 to $200,000 range.■n A small number of ESOPs will require investment banking assistance to raise financing, adding to costs.■n No broker fees should ever be paid in an ESOP ■n The ESOP pays the buyer’s diligence, financing, and legal fees.

■n Legal costs may be somewhat lower. Appraisal costs would be similar; feasibility and due diligence comparable or higher to ESOPs. ■n Broker success fees generally between 5% and 12% of the sale price. Seller typically formally pays this cost, but buyer and seller factor these costs into the ultimate price. ■n The buyer pays the diligence, financing, and legal fees.

www.nceo.org National Center for Employee Ownership

ESOP Facts

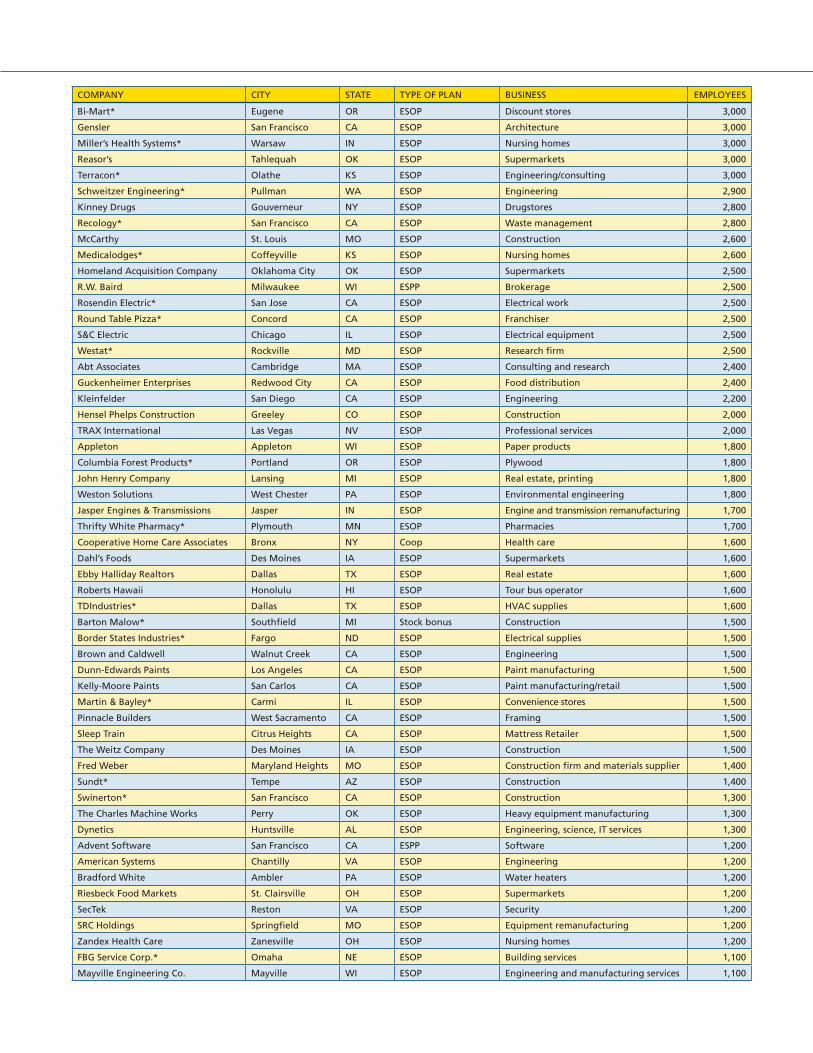

America’s Largest Majority Employee-Owned Companies

To be on the list, the NCEO must have been able to verify that a company is at least 50% owned by an ESOP, by another qualified plan, or by one or more other kinds of plans in which at least 50% of full-time employees are eligible to participate. Companies marked by an asterisk in their names are 100% employee-owned. Employment includes all full- and part-time employees in the U.S. and worldwide.

COMPANY CITY STATE TYPE OF PLAN BUSINESS EMPLOYEES

Publix Super Markets Lakeland FL ESOP, stock purchase Supermarkets 152,000

Hy-Vee West Des Moines IA Profit sharing Supermarkets 60,200

CH2M Hill Englewood CO Stock incentive and purchase plan Engineering/construction 28,400

Lifetouch Eden Prairie MN ESOP Photography studios 26,000

Price Chopper Schenectady NY Profit sharing Supermarkets 23,000

Daymon Worldwide Stamford CT ESOP/others Food distribution 18,000

Nypro Clinton MA ESOP Plastics manufacturing 17,000

Penmac Springfield MO ESOP Staffing 17,000

Houchens Industries Bowling Green KY ESOP Supermarkets and other services 16,600

WinCo Foods* Boise ID ESOP Supermarkets 14,000

Alliance Holdings* Abington PA ESOP Holding company 13,300

Parsons* Pasadena CA ESOP Engineering/construction 11,500

Amsted Industries Chicago IL ESOP Industrial components 9,600

Black & Veatch Overland Park KS ESOP Engineering 9,000

W.L. Gore & Associates Newark DE ESOP Manufacturing 9,000

Graybar Electric St. Louis MO Stock purchase Electrical equipment wholesale 8,400

HDR Omaha NE ESOP Architecture/engineering 7,800

Davey Tree Expert* Kent OH ESOP Tree services 7,400

Austin Industries* Dallas TX ESOP Construction 7,100

Burnett Staffing Houston TX ESOP Staffing services 7,000

Jacobson Companies Salt Lake City UT ESOP Construction 7,000

MWH Americas Broomfield CO ESOP Engineering/consulting 7,000

Schreiber Foods Green Bay WI ESOP Cheese manufacturing 6,800

Brookshire Brothers* Lufkin TX ESOP Supermarkets 6,000

CDM Smith Cambridge MA Profit sharing Engineering and construction 6,000

Hanson Pipe & Precast Irving TX ESOP Pipe manufacturing 6,000

Piggly Wiggly Carolina Company* Charleston SC ESOP Supermarkets 5,700

EHC Management* Vancouver WA ESOP Health-care staffing 5,400

Scheels All Sports Fargo ND ESOP Retail sporting goods 5,000

Herff Jones* Indianapolis IN ESOP Awards and gifts 4,500

Tharaldson Motels* Fargo ND ESOP Motel management 4,500

Cianbro Pittsfield ME ESOP Construction 4,000

Food Giant* Sikeston MO ESOP Supermarkets 4,000

KeHE Distributors Romeoville IL ESOP Food distribution 4,000

Ramey, Price Cutter, Smitty’s (RPCS)* Springfield MO ESOP Supermarkets 4,000

HNTB Kansas City MO ESOP Architecture/engineering 3,800

Lewis Tree Service* West Henrietta NY ESOP Tree services 3,700

Chemonics* Washington DC ESOP International development 3,500

CentiMark Canonsburg PA ESOP Roof repair 3,400

Sammons Enterprises* Dallas TX ESOP Diversified holding company 3,400

Acadian Ambulance Lafayette LA ESOP Ambulance services 3,300

EOD Technology Lenoir City TN ESOP Security and munitions services 3,300

Harps Food Stores* Springdale AR ESOP Supermarkets 3,200

Burns & McDonnell Engineering* Kansas City MO ESOP Architecture/engineering 3,200

Alion Science and Technology McLean VA ESOP Technology services 3,100

American Cast Iron Pipe Birmingham AL Stock trust Manufacturing 3,000

The 2012 Employee Ownership 100

COMPANY CITY STATE TYPE OF PLAN BUSINESS EMPLOYEES

Bi-Mart* Eugene OR ESOP Discount stores 3,000

Gensler San Francisco CA ESOP Architecture 3,000

Miller’s Health Systems* Warsaw IN ESOP Nursing homes 3,000

Reasor’s Tahlequah OK ESOP Supermarkets 3,000

Terracon* Olathe KS ESOP Engineering/consulting 3,000

Schweitzer Engineering* Pullman WA ESOP Engineering 2,900

Kinney Drugs Gouverneur NY ESOP Drugstores 2,800

Recology* San Francisco CA ESOP Waste management 2,800

McCarthy St. Louis MO ESOP Construction 2,600

Medicalodges* Coffeyville KS ESOP Nursing homes 2,600

Homeland Acquisition Company Oklahoma City OK ESOP Supermarkets 2,500

R.W. Baird Milwaukee WI ESPP Brokerage 2,500

Rosendin Electric* San Jose CA ESOP Electrical work 2,500

Round Table Pizza* Concord CA ESOP Franchiser 2,500

S&C Electric Chicago IL ESOP Electrical equipment 2,500

Westat* Rockville MD ESOP Research firm 2,500

Abt Associates Cambridge MA ESOP Consulting and research 2,400

Guckenheimer Enterprises Redwood City CA ESOP Food distribution 2,400

Kleinfelder San Diego CA ESOP Engineering 2,200

Hensel Phelps Construction Greeley CO ESOP Construction 2,000

TRAX International Las Vegas NV ESOP Professional services 2,000

Appleton Appleton WI ESOP Paper products 1,800

Columbia Forest Products* Portland OR ESOP Plywood 1,800

John Henry Company Lansing MI ESOP Real estate, printing 1,800

Weston Solutions West Chester PA ESOP Environmental engineering 1,800

Jasper Engines & Transmissions Jasper IN ESOP Engine and transmission remanufacturing 1,700

Thrifty White Pharmacy* Plymouth MN ESOP Pharmacies 1,700

Cooperative Home Care Associates Bronx NY Coop Health care 1,600

Dahl’s Foods Des Moines IA ESOP Supermarkets 1,600

Ebby Halliday Realtors Dallas TX ESOP Real estate 1,600

Roberts Hawaii Honolulu HI ESOP Tour bus operator 1,600

TDIndustries* Dallas TX ESOP HVAC supplies 1,600

Barton Malow* Southfield MI Stock bonus Construction 1,500

Border States Industries* Fargo ND ESOP Electrical supplies 1,500

Brown and Caldwell Walnut Creek CA ESOP Engineering 1,500

Dunn-Edwards Paints Los Angeles CA ESOP Paint manufacturing 1,500

Kelly-Moore Paints San Carlos CA ESOP Paint manufacturing/retail 1,500

Martin & Bayley* Carmi IL ESOP Convenience stores 1,500

Pinnacle Builders West Sacramento CA ESOP Framing 1,500

Sleep Train Citrus Heights CA ESOP Mattress Retailer 1,500

The Weitz Company Des Moines IA ESOP Construction 1,500

Fred Weber Maryland Heights MO ESOP Construction firm and materials supplier 1,400

Sundt* Tempe AZ ESOP Construction 1,400

Swinerton* San Francisco CA ESOP Construction 1,300

The Charles Machine Works Perry OK ESOP Heavy equipment manufacturing 1,300

Dynetics Huntsville AL ESOP Engineering, science, IT services 1,300

Advent Software San Francisco CA ESPP Software 1,200

American Systems Chantilly VA ESOP Engineering 1,200

Bradford White Ambler PA ESOP Water heaters 1,200

Riesbeck Food Markets St. Clairsville OH ESOP Supermarkets 1,200

SecTek Reston VA ESOP Security 1,200

SRC Holdings Springfield MO ESOP Equipment remanufacturing 1,200

Zandex Health Care Zanesville OH ESOP Nursing homes 1,200

FBG Service Corp.* Omaha NE ESOP Building services 1,100

Mayville Engineering Co. Mayville WI ESOP Engineering and manufacturing services 1,100

■n Both C and S corporations can deduct contributions of up to 25% of the eligible payroll in an ESOP to repay an ESOP loan, but C corporations base this calculation only on the amount of principal paid, while S corporations must count interest as well.

■n In C corporations, dividends paid on ESOP-held company stock are tax-deductible if they are used to repay an ESOP loan or passed directly to employees. In S corpora-tions, however, distributions (the equivalent of C corporation dividends) paid on ESOP-held stock are not deductible.

Use of DistributionsIf S corporations make distributions, usually to enable shareholders to pay taxes, a pro-rata distribution must be

ESOPs in S Corporations Legislation in the late 1990s made it

possible for S corporations to have ESOPs. If they do, the percentage

of profits attributable to the ESOP’s ownership is not subject to federal, and usually state, income tax. So a 30% ESOP S corporation pays no tax on 30% of its profits; a 100% ESOP pays none. Because some companies tried to use this law to set up plans that only benefitted a few people, not employees broadly, Congress enacted special rules to prevent these kinds of abuses.

Main Differences in Tax TreatmentS and C corporation ESOPs have somewhat different tax treatment:■n Sellers to an S ESOP cannot defer taxes on gains made from the sale of stock to an ESOP. Instead, they pay capital gains on their adjusted basis.

made to the ESOP as well. Distri-butions on allocated shares must be made relative to account balances; distributions on unallocated shares (shares held in the ESOP but not yet paid for when the ESOP borrows money to purchase stock) can be based either on allocated shares or the company’s normal contribution formula (typically relative compen-sation). These distributions can, in turn, be used to buy additional shares from owners if the plan fiduciary determines that it is fiduciarially sound to do so.

Distributions paid on ESOP-held company stock can be used to repay an ESOP loan and operate in much the same way as do dividends on stock in a C corporation ESOP, releasing additional shares from the suspense account (the unpaid-for shares) to existing employee accounts.

ESOP Limitations: How Small is Too Small?

Companies of any size can sponsor ESOPs, but in practice ESOPs do not usually make sense for

very small companies. There are few ESOP companies with fewer than 20 employees. To find whether an ESOP is financially practical for your company, you need to estimate how much an ESOP would cost. To get an accurate picture, your estimate should include fees associated with plan document preparation, required government filings, professional valuation, and plan administration. You also need to assess if you have adequate cash flow to buy shares.

If you are considering a leveraged ESOP, your estimate should also include loan commitment and document fees, lender’s legal counsel

fees, and possibly services of a financial consultant to structure the transaction. Some of these fees are transaction based, such as documentation or filing fees; and others will be ongoing, such as yearly valuation (usually about half the cost of the transaction valuation) and administration.

Due to the cost associated with the setup and maintenance of an ESOP it is a good idea to consider additional things to see if the cost of the ESOP is justifiable for your business. Some of these include: the cost associated with alternative sale options, the value of the ESOP tax incentives based on your current tax bracket, a comparison of annual ESOP costs to annual contributions, and the size of your eligible payroll.

Generally, businesses with the following characteristics are good ESOP candidates:

■n Minimum of $500,000 in eligible payroll

■n Reasonable levels of debt

■n Company is currently profitable or has the potential for profitability in the near-term

■n Successor management is in place

If this initial analysis indicates you might be a good candidate for an ESOP, the next step is conducting a more detailed pre-feasibility study. It is important to work with knowledge-able professionals and get multiple cost estimates to ensure your company is getting the best deal. n

For a further discussion on calculating and assessing the cost of setting up and maintaining an ESOP, please see the NCEO publication: “How Small is Too Small for an ESOP?” which can be found at: www.nceo.org/articles/too-small-for-esop.

www.nceo.org National Center for Employee Ownership

ESOP Facts

Converting from C to SWhen converting from C to S, several issues are important to note:■n The election requires the consent of all shareholders.■n An S corporation can only have 100 shareholders, but the ESOP counts as only as one. ■n S corporations can only have one class of stock, with the one exception that it can have voting and nonvoting common shares.■n After conversion to S status, corporations using last-in, first-out (LIFO) accounting are subject to a LIFO recapture tax. This could be substantial in some cases, especially in capital-intensive businesses. The tax is based on the corporation’s last C tax year.■n For a 10-year period after conversion, if the company sells any asset it held on the day of its S corporation

election, it will have to pay “built-in gains” tax on that sale. This tax is in addition to taxes paid by shareholders.

■n In S corporations, some fringe benefits paid to 2% or more owners are taxable.

■n Net operating losses incurred as a C corporation are suspended while an S corporation. These losses may be applied against LIFO or built-in gains taxes, however.

■n State laws vary, and some states may not track federal laws. In California, for instance, ESOPs are subject to state unrelated business income tax.

■n S corporations must operate on a calendar year.

Anti-Abuse RulesThe 2001 tax bill included provisions to discourage the use of ESOPs in S cor- porations for the primary benefit of just a few employees. The law includes

a two-step process to determine whether the S corporation ESOP will not be subject to punitive tax treat-ment. The rules are somewhat compli-cated and generally only affect very small ESOP companies (under 15 or 20 employees) or companies where there are a very few people with unusually large (intentionally or not) amounts of ownership inside the ESOP and/or synthetic equity outside the plan.

The first step in the testing process is to define “disqualified persons.” Under the law, a “disqualified person” is an individual who owns 10% or more of the “deemed-owned shares” or who, together with family members, owns 20% or more. “Deemed-owned shares” include stock allocated to that person’s ESOP account; a proportionate amount of shares bought by the ESOP but not yet released to participant accounts; and synthetic equity, broadly defined to include stock options, stock appreciation rights, and other forms of equity compensation. Stock directly owned outside the ESOP is not considered to be deemed-owned.

The second step is to determine whether disqualified individuals as a group own at least 50% of all shares in the company. In making this determination, ownership is defined to include:1. shares held directly2. shares owned through synthetic

equity3. allocated or unallocated shares

owned through the ESOPIf disqualified individuals own at

least 50% of the stock of the company, then the rules specify that they may not receive allocations of company stock in the ESOP or any other tax-qualified plan that year without causing a prohibited transaction. The IRS interpretation of these rules, however, are even stricter. They specify that an impermissible accrual will have occurred if stock is held for the benefit of a disqualified individual. In other words, when disqualified persons own at least 50% of the stock, the company will have to pay a draconian tax penalty so large it will put the company out of business. n

www.nceo.org National Center for Employee Ownership

ESOP Facts

Operating an ESOP Successfully CommunicationsIn order for ESOPs to work, employees need to understand how they work. There are several key steps to creating an effective communications program:

■n Set up an ESOP communications committee: The best committees are those that are made up of peers. They are better able to know what their colleagues know, don’t know, and want to know. Give the committee a budget and make it clear that they are not only allowed but expected to take the time they need to communicate effectively.

■n Start with an orientation: This applies at the rollout but also for new employees and ongoing ones wanting a refresher. This class might last an hour or two a day for a few days.

■n Communicate often in small pieces: On an ongoing basis, send out regular communications on different issues, such as vesting, allocation, and distributions. These small pieces are easier to understand and the regularity of the communications reinforces the message.

■n Have fun: Associating communi-cations events with food, games, and other enjoyable events creates a kind of positive halo effect.

■n Use multiple ways to communicate: Internet FAQs, account value projection tools, emails, newsletters, small group meetings, and other approaches are important because different people learn differently.

■n Provide source material: Make sure people acknowledge receiving their summary plan descriptions and provide an ESOP handbook that is easier to read than the often very formal SPD.

■n Use account statements to make a statement: Hand them out personally, send them to home addresses, illustrate them, and take other steps to make these annual statements more memorable.

Corporate CultureResearch on employee ownership and corporate performance very clearly shows that only companies that combine ESOPs with a high degree of employee involvement in day-to-day decisions show improved performance – and these companies perform dramatically better. An ESOP that just motivates people to work harder at the same tasks improves performance marginally, but one that engages employees to regularly generate new ideas on how to do things better is a game changer. To get there, companies need to go well beyond “open door management.” They need to share key performance data and create structured opportunities for employees to share ideas and information to make better decisions.

The structure of participation varies from company to company, but basically boils down to employees forming groups to share informa- tion, generate ideas, and make recommendations. At Springfield Remanufacturing in Springfield, Missouri, employee-owners are taught to read detailed financial and production data. Meeting in work groups, they go over the numbers, then figure out ways to improve them. The company has grown from 119 employees in 1983 to over 1,200 in 2012. One share was worth 10 cents in 1983, but someone who held onto that share would now have stock worth $237. Phelps County Bank set up an employee “problem buster committee” to hear ideas (suggestions or unresolved problems), then, where appropriate, assigns ad hoc committees to address them. Scot Forge has work teams throughout the plant who meet regularly to decide how to run their operations more effectively. Web Industries has all employees meet periodically to remap production and brainstorm new ideas. There is no right or wrong way to do participation other than not to do it at all. Start somewhere, evaluate how it is working, and change as needed.

GovernanceThe ESOP trust is governed by a trustee usually appointed by the board. The trustee is legally charged with operating the plan in the best interests of plan participants. The key issues are making sure the valuation is done properly, voting shares in the plan (in some plans, employees direct the trustee on these issues), overseeing plan administration to make sure it complies with all requirements, and acting as a shareholder to object when corporate assets are used improperly. About one-fifth of closely held companies appoint an independent outside trustee to do this work. That provides additional protection in case of a lawsuit or government challenge, plus considerable expertise. Other companies have one or more insiders as trustees, usually officers. Sellers should not act as trustees for any actions that can affect the value of their ownership.

Boards in ESOP companies operate much as they normally do, but with a special eye to the interests of this now major shareholder. That includes making sure the trustees are doing their job. Increasingly, ESOP companies are bringing in outside directors to add expertise and perspective.

Plan OperationsIt is essential to have someone in the company who knows ESOPs well who is charged with working with a qualified ESOP plan administrator. The administrator will take care of the details and reports, so find one who truly is an ESOP expert.

ESOP companies should regularly perform repurchase studies, either in-house or by asking the plan administrator to do this. Experience shows that addressing the repurchase obligation is very manageable, but only if the obligation is taken seriously and planned for carefully. n

www.nceo.org National Center for Employee Ownership

ESOP Facts

Operating an ESOP Successfully

Attendees can join the NCEO for an introductory rate of $90 with this form (see form on

other side). The National Center for Employee

Ownership is the leading source of informa tion about employee ownership in the U.S. and abroad. As you will learn from today’s meeting, employee stock ownership plans provide substantial tax benefits for business conti nuity, corporate growth, and employee benefit planning. Employee ownership also can be a powerful way to energize your company. But employee ownership is not for every one. Making the decision to set up a plan, and making the plan work well for your company, require good information and considered judgment. The NCEO was created to provide the kind of objective, reliable information you need to make these important choices.

As a member of the NCEO, you will receive a detailed bimonthly newsletter, access to the members area of our Web site, free access to live ESOP Webinars, discounts on publications and events, and the right to call us any time for information. To join, simply fill out the order form on the other side.

Key Publications Understanding ESOPSThis book will teach you what ESOPs really are, how they work in both C and S corporations, what their uses are, what the valuation and financing issues are, what the steps to set them up are, and much more.Members: $25 Nonmembers: $35

Selling Your Business to an ESOPHow to use an ESOP for business continuity in a privately held company.Members: $25 Nonmembers: $35

Leveraged ESOPs and Employee BuyoutsHow ESOPs borrow money to buy out entire companies, purchase shares from a retiring owner, or finance new capital. Discusses rules, transaction structures, and financing.Members: $25 Nonmembers: $35

ESOP ValuationA detailed look at various aspects of ESOP valuation, including the repurchase obligation, S corporations, and selecting an appraiser.Members: $25 Nonmembers: $35

How ESOP Companies Handle the Repurchase ObligationThis book combines practical discussions with research in exploring the repurchase obligation and how it can be planned for and dealt with.Members: $25 Nonmembers: $35

ESOPs and Corporate GovernanceThis book was written to help ESOP companies think through their governance issues. Includes a new survey on governance practices in ESOP companies. Details on board compensation and composition, trustee selection and responsibilities, and employee roles on boards. Members: $25 Nonmembers: $35

S Corporation ESOPsEverything from the history of S corporation ESOPs to tax issues, compliance, administration, and more. Updated to take account of important recent developments.Members: $25 Nonmembers: $35

Executive Compensation in ESOP CompaniesProvides an overview of how to share equity with key employees and then discusses general executive compensation issues; special ESOP considerations such as fiduciary issues; using competitive compensation studies; and how to determine appropriate compensation.Members: $25 Nonmembers: $35

ESOP Communications Sourcebook Ideas, forms, and examples on how to share financial information, explain plan features, create events, market employee ownership to customers, and other issues. Includes a CD with resource materials.Members: $35 Nonmembers: $50

Special Offers for Attendees

NCEO: “The single best source of information on employee ownership anywhere in the world.” — Inc. magazine

Become a member today!

Questions?Call the NCEO: 510-208-1300 or send an email to: [email protected]

2 Fax credit card orders to: 510-272-9510

(Place credit card orders by phone: 510-208-1300

+ Or mail check or credit card orders to:

NCEO 1736 Franklin Street, 8th Floor Oakland, CA 94612

: Order online at: www.nceo.org

MEMBER INFORMATION:

NAME

ORGANIZATION

ADDRESS

CITY STATE ZIP

PHONE FAX

CREDIT CARD NUMBER EXPIRATION CVV CODE

ORDER INFORMATION:

ITEM NAME QUANTITY x MEMBER RATE = TOTAL PRICE

PUBLICATIONS TOTAL $

(California residents add 8.75% on publications) SALES TAX $

INTRODUCTORY MEMBERSHIP $ 90.00

TOTAL $

PAYMENT METHOD:n VISA n MC n AMEX

n CHECK (payable to NCEO)

SIGNATURE

www.nceo.org