ch.6 internal control and accounting for cash · ch.6 internal control and accounting for cash 1...

TRANSCRIPT

Ch.6 Internal Control and Accounting for Cash

1

Internal control and its objectives

Understand cash and internal control procedures

related to cash

Accounting for petty cash

Combined Journal

Prepare a bank reconciliation

The Sarbanes-Oxley Act of 2002

• Congress responded by passing the

Sarbanes-Oxley Act of 2002

• Among other provisions, companies are

required to maintain strong and effective

internal controls over recording business

transactions and preparing financial

statements

2

Internal Control

• The methods and procedures a business uses

to internally protect its assets

• A good system of internal control is designed

to

Safeguard assets

Ensure the accuracy and reliability of

accounting records

Promote operational efficiency

Ensure compliance with laws and

regulations

3

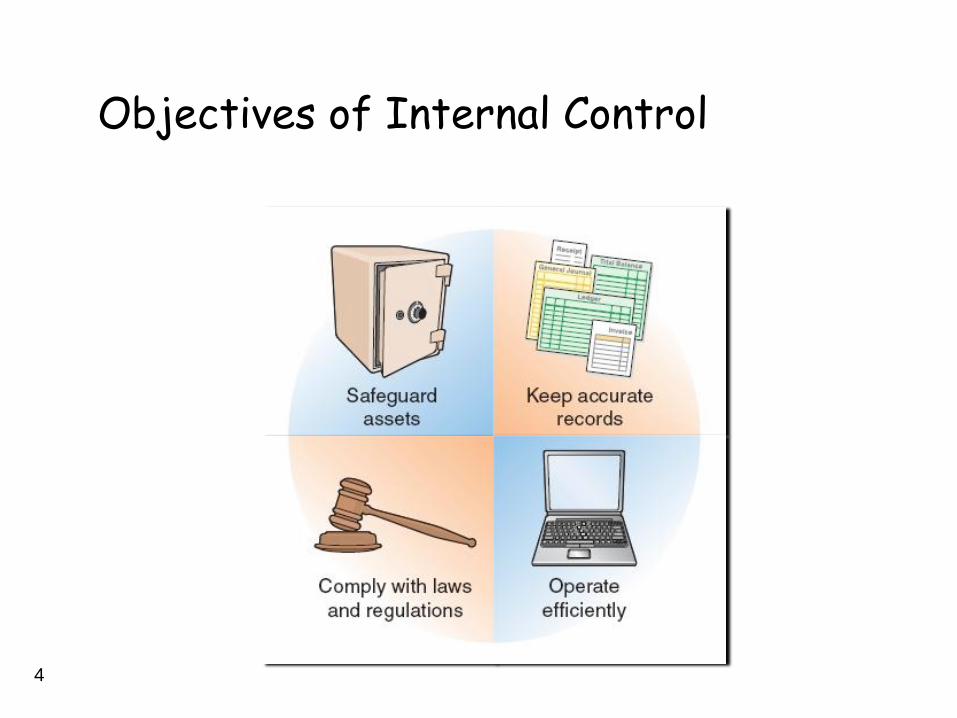

Objectives of Internal Control

4

Cash

• Includes currency, coins, checks made

payable to the business, money orders,

and amounts on deposit in banks and

other financial institutions

• Generally considered the most precious

of all assets

• Almost everyone wants it

• Easily taken if not protected

5

Steps in Controlling and Protecting Cash

• Establish ResponsibilityOnly properly designated

personnel are authorized to

handle cash receipts.

• Separation of DutiesThe individual who accounts for

cash is different from the persons

who receive and deposit cash.6

Steps in Controlling and Protecting Cash

• Physical ProtectionCash on hand should be in a

secure location and cash should

be deposited daily.

• DocumentationCash register tapes, summaries

of checks received, etc. should

be kept to show the amount of

cash received.7

Steps in Controlling and Protecting Cash

• Independent VerificationCashiers check cash registers,

supervisors count cash receipts

daily, and company treasurer

compares cash receipts with

bank deposits.

• Keep Only a Small Amount of Cash on Hand

Only a small amount of cash

should be maintained on hand

to make small expenditures.8

The Petty Cash Account

• To control cash, most businesses use bank

checking accounts when making cash

expenditures

• It is not practical to write checks for very

small amounts

• Most businesses maintain a petty cash

fund which is a small amount of money

kept in the office for making small

expenditures9

Establishing a Petty Cash Fund

1. Estimate the amount of cash needed in the

fund.

2. A check for this amount is written payable to

Petty Cash.

3. The check is then cashed, and the money is

placed in a box, a drawer, or a safe to be used

for the fund.

10

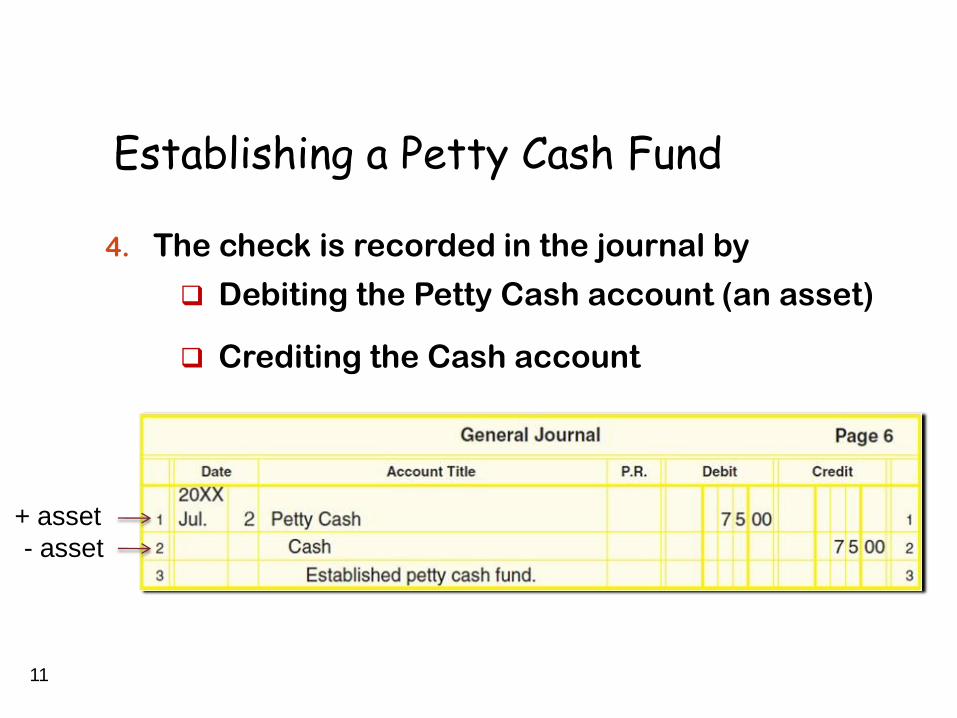

Establishing a Petty Cash Fund

4. The check is recorded in the journal by

Debiting the Petty Cash account (an asset)

Crediting the Cash account

11

+ asset

- asset

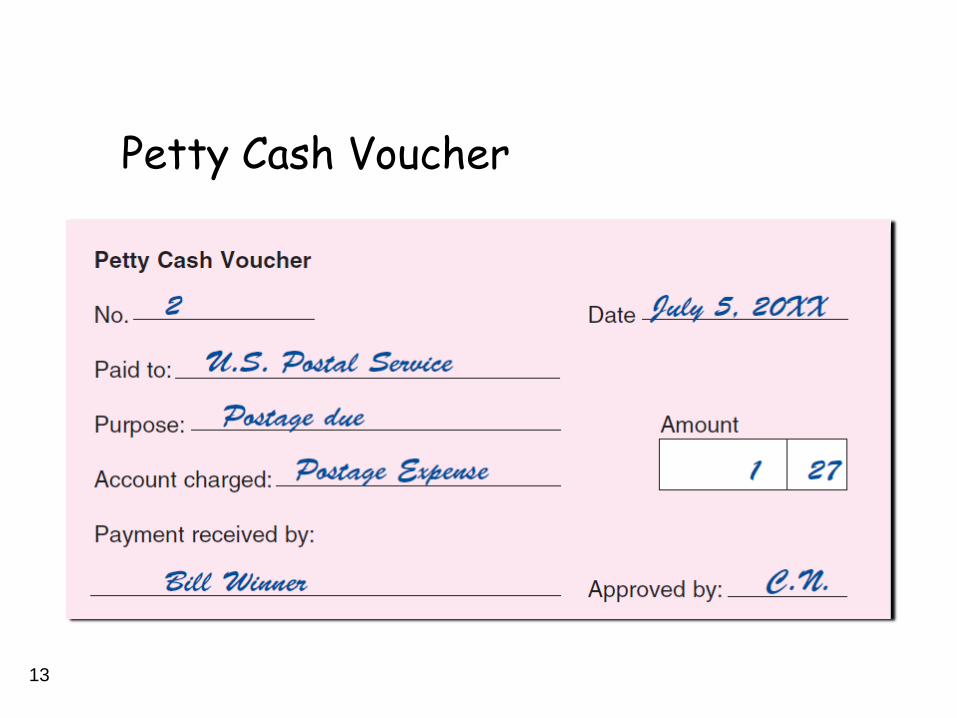

Making Payments from the Petty Cash Fund

• Petty cashier (usually) is the only person who

makes payments from the fund.

• Petty cash voucher

Prepared for each payment

Shows the details of the payment

Serves as proof of payment

12

Petty Cash Voucher

13

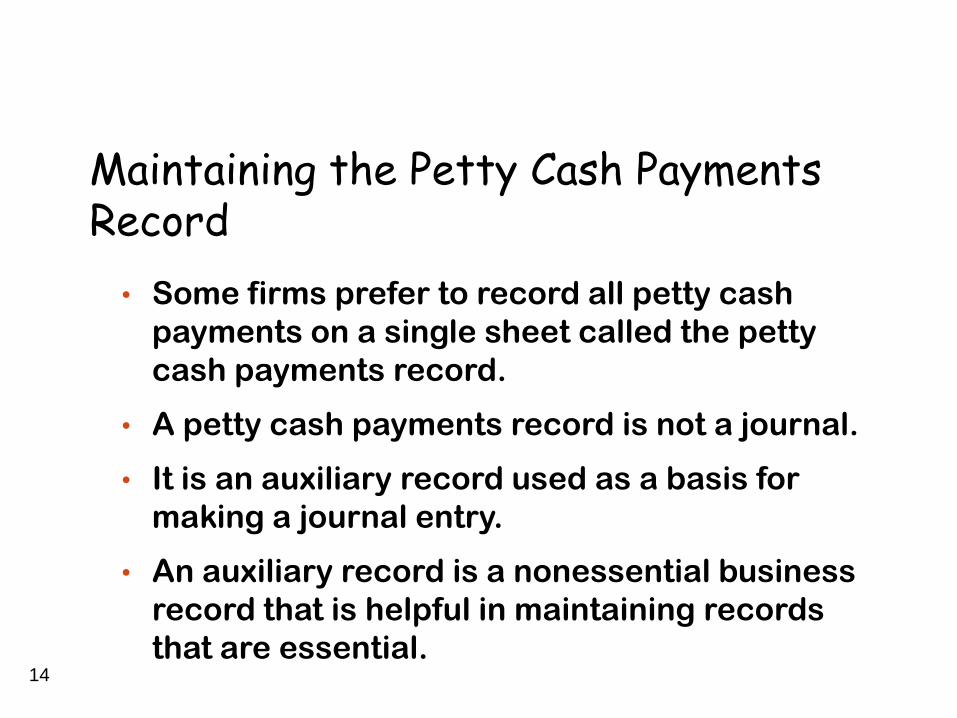

Maintaining the Petty Cash Payments Record

• Some firms prefer to record all petty cash

payments on a single sheet called the petty

cash payments record.

• A petty cash payments record is not a journal.

• It is an auxiliary record used as a basis for

making a journal entry.

• An auxiliary record is a nonessential business

record that is helpful in maintaining records

that are essential.14

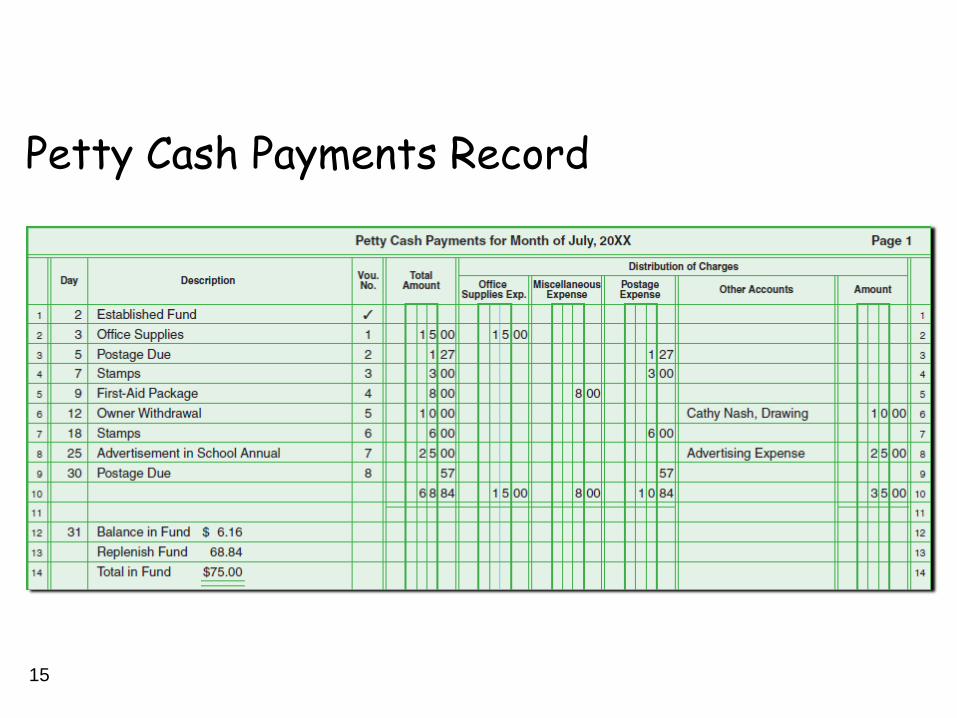

Petty Cash Payments Record

15

Replenishing the Petty Cash Fund

• Normally replenished at month-end or when it

nears depletion or reaches a minimum amount

• When replenished, the Petty Cash account is

NOT debited

• The accounts debited are determined by

analyzing the petty cash vouchers

• The Cash account is credited

16

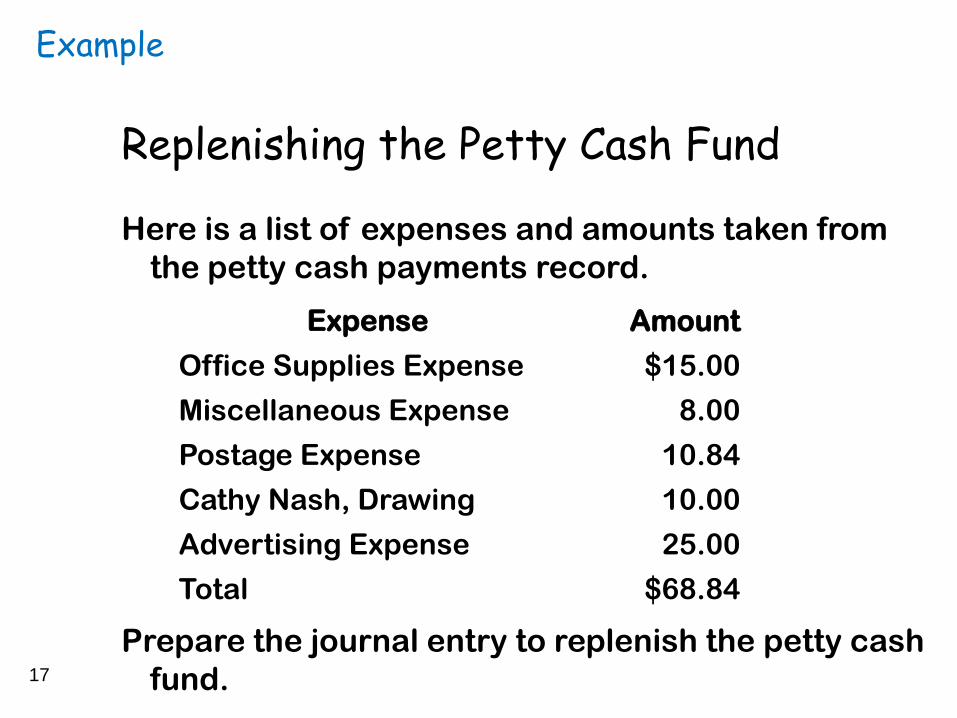

Example

Replenishing the Petty Cash Fund

Here is a list of expenses and amounts taken from

the petty cash payments record.

Prepare the journal entry to replenish the petty cash

fund.17

Expense Amount

Office Supplies Expense $15.00

Miscellaneous Expense 8.00

Postage Expense 10.84

Cathy Nash, Drawing 10.00

Advertising Expense 25.00

Total $68.84

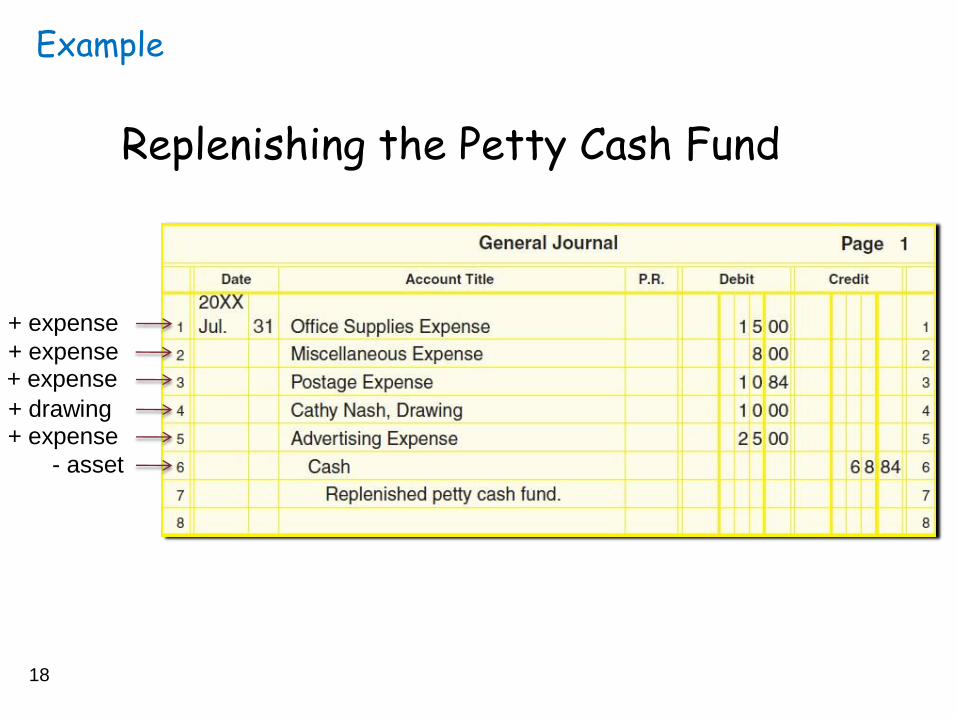

Example

Replenishing the Petty Cash Fund

18

+ expense

+ expense+ expense

+ drawing+ expense

- asset

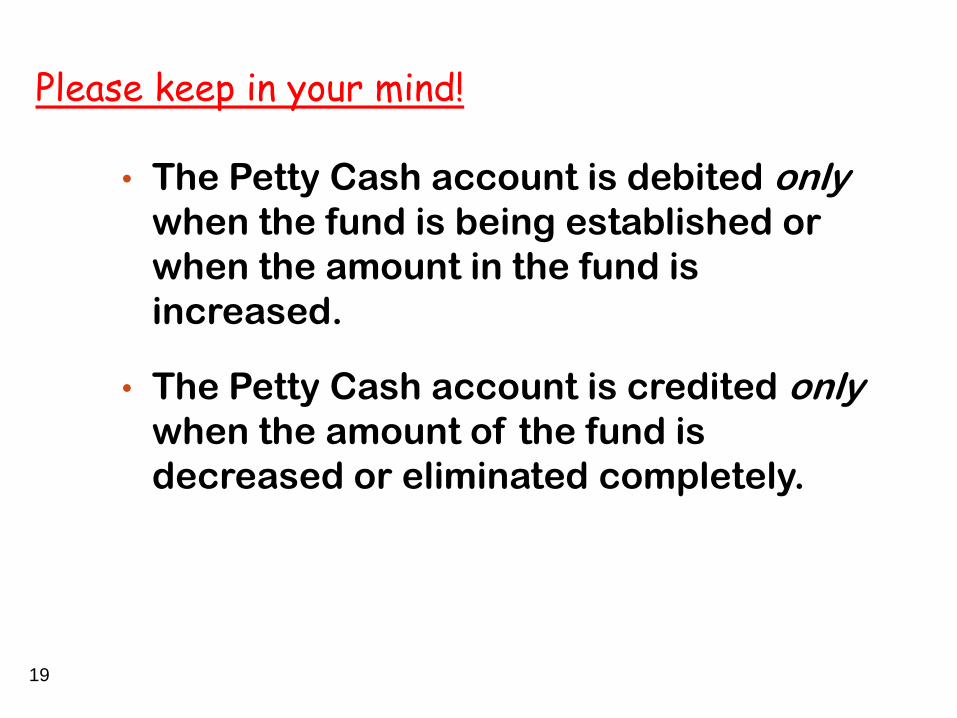

Please keep in your mind!

• The Petty Cash account is debited onlywhen the fund is being established or

when the amount in the fund is

increased.

• The Petty Cash account is credited onlywhen the amount of the fund is

decreased or eliminated completely.

19

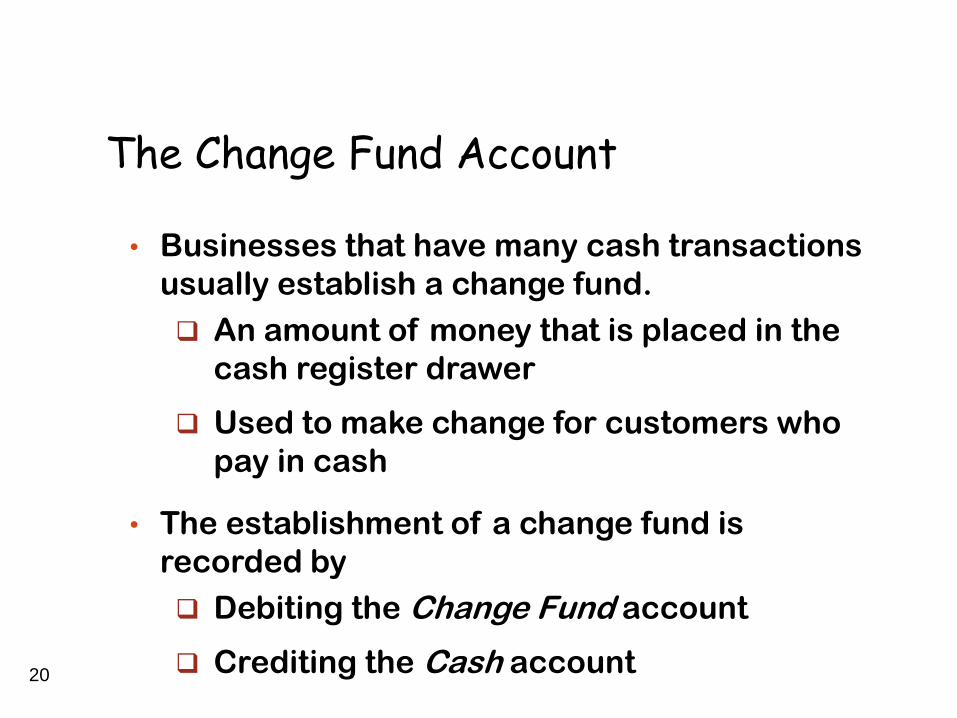

The Change Fund Account

• Businesses that have many cash transactions

usually establish a change fund.

An amount of money that is placed in the

cash register drawer

Used to make change for customers who

pay in cash

• The establishment of a change fund is

recorded by

Debiting the Change Fund account

Crediting the Cash account20

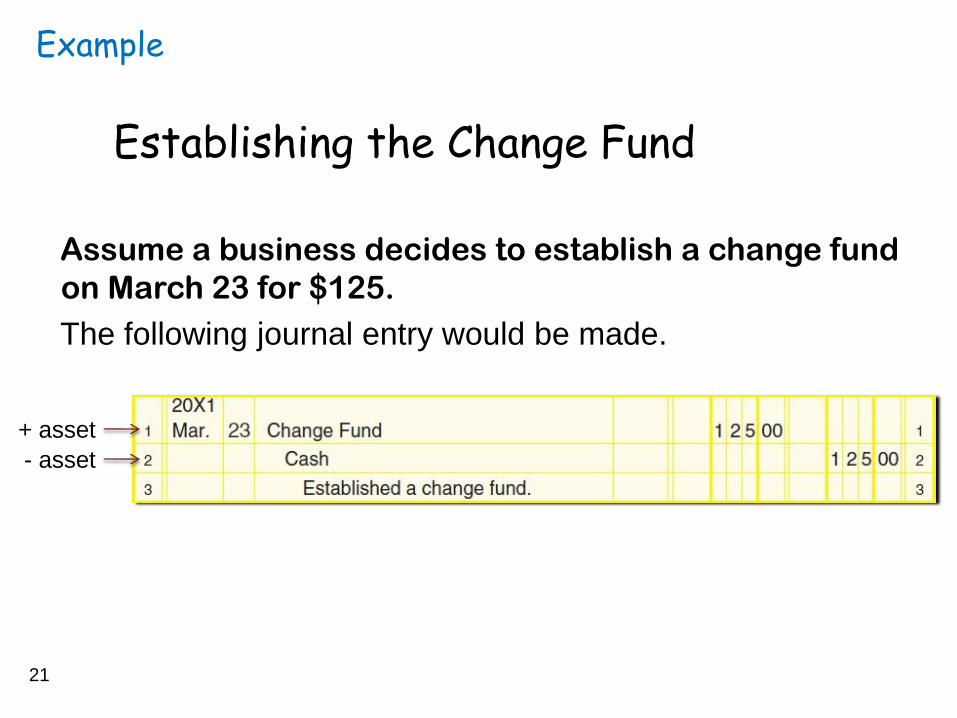

Example

Establishing the Change Fund

Assume a business decides to establish a change fund

on March 23 for $125.

The following journal entry would be made.

21

+ asset

- asset

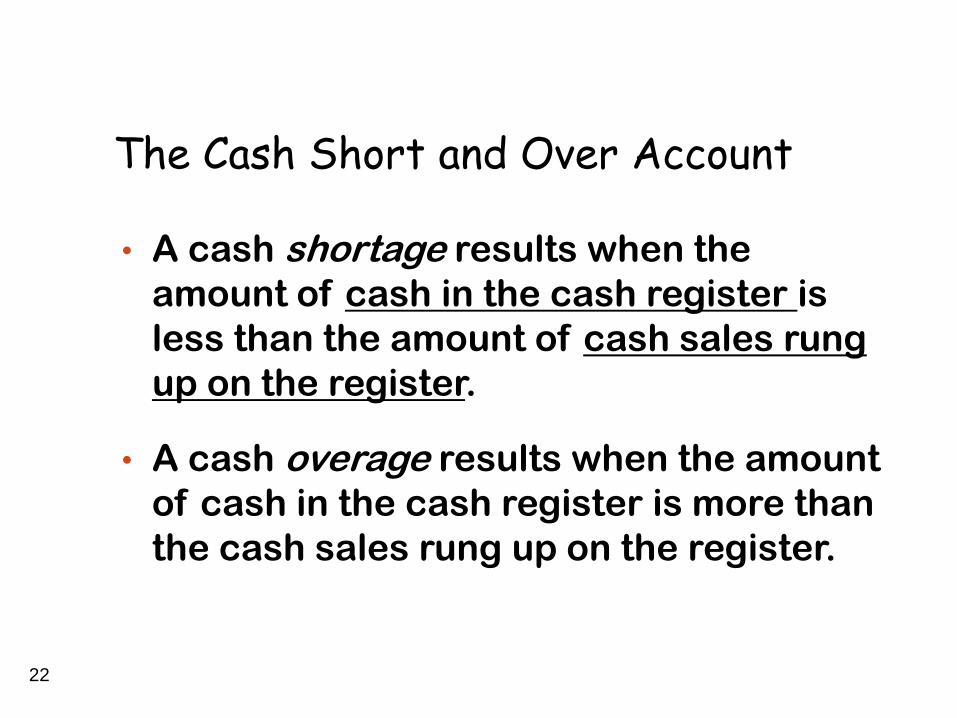

The Cash Short and Over Account

• A cash shortage results when the

amount of cash in the cash register is

less than the amount of cash sales rung

up on the register.

• A cash overage results when the amount

of cash in the cash register is more than

the cash sales rung up on the register.

22

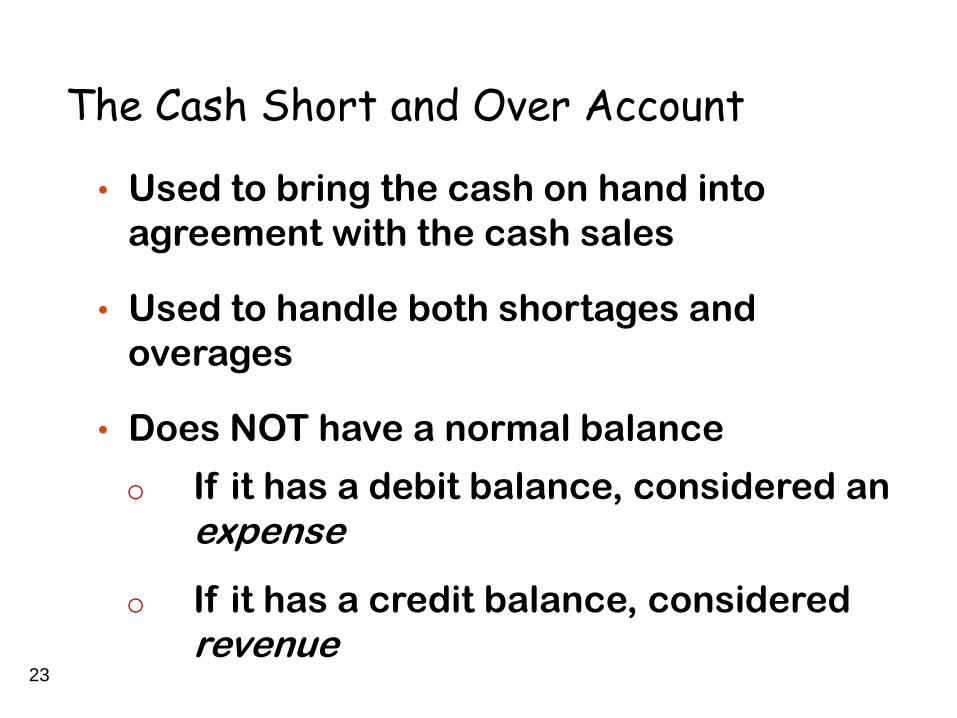

The Cash Short and Over Account

• Used to bring the cash on hand into

agreement with the cash sales

• Used to handle both shortages and

overages

• Does NOT have a normal balance

o If it has a debit balance, considered an

expense

o If it has a credit balance, considered

revenue23

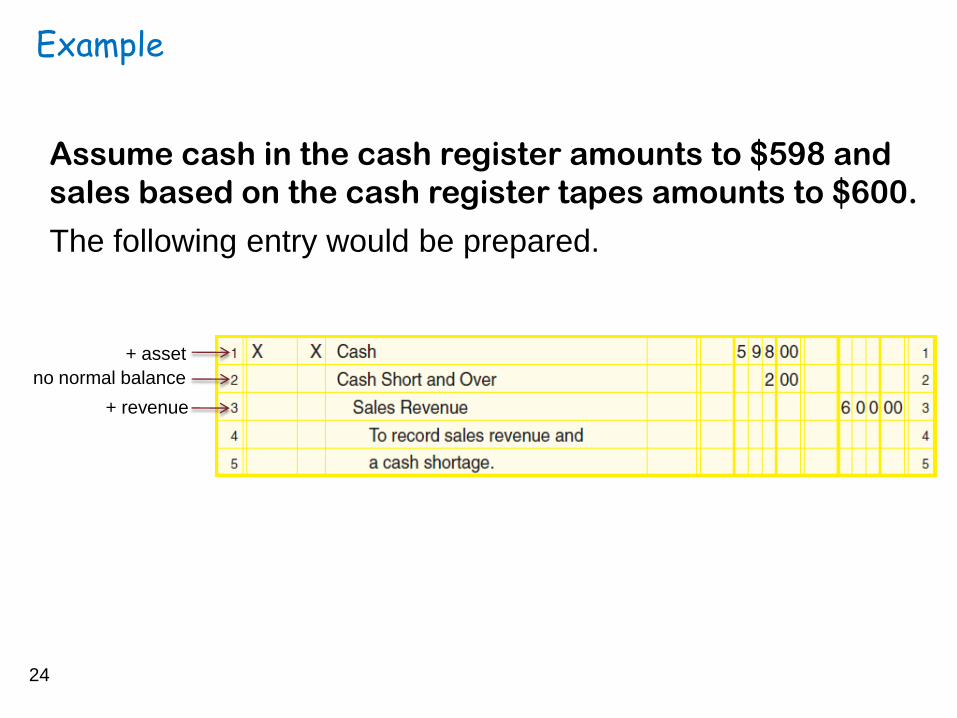

Example

Assume cash in the cash register amounts to $598 and

sales based on the cash register tapes amounts to $600.

The following entry would be prepared.

24

no normal balance

+ asset

+ revenue

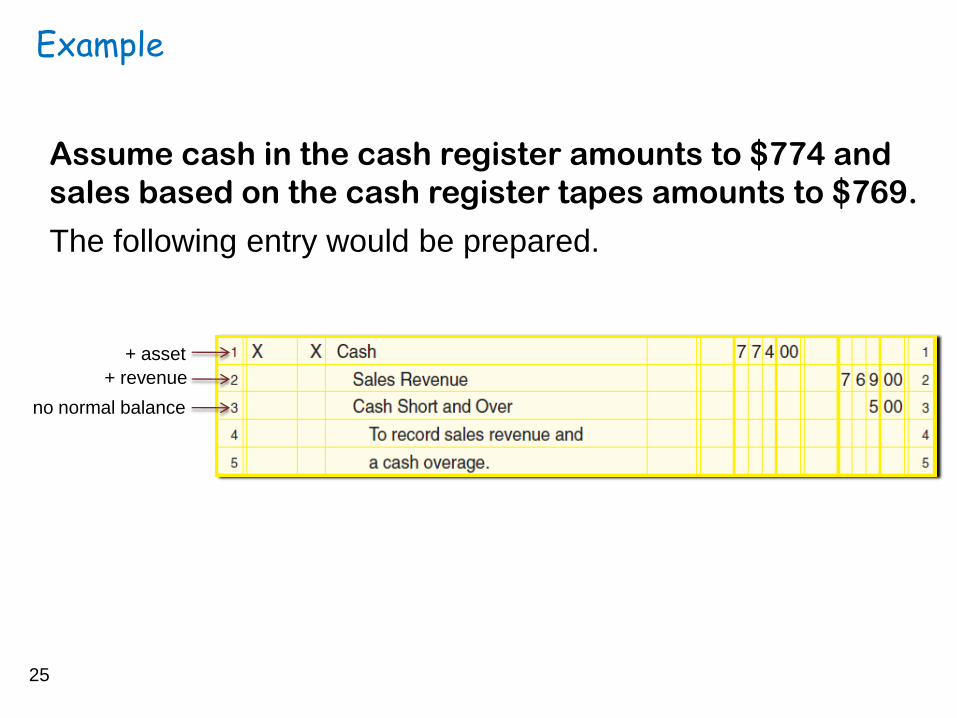

Example

Assume cash in the cash register amounts to $774 and

sales based on the cash register tapes amounts to $769.

The following entry would be prepared.

25

no normal balance

+ asset

+ revenue

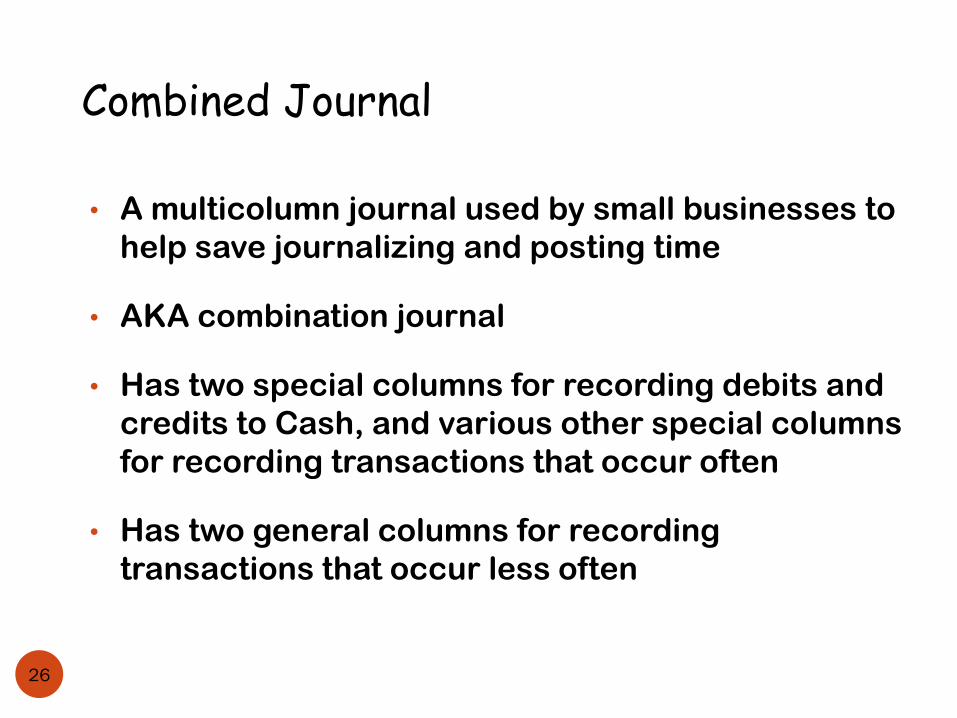

Combined Journal

• A multicolumn journal used by small businesses to

help save journalizing and posting time

• AKA combination journal

• Has two special columns for recording debits and

credits to Cash, and various other special columns

for recording transactions that occur often

• Has two general columns for recording

transactions that occur less often

26

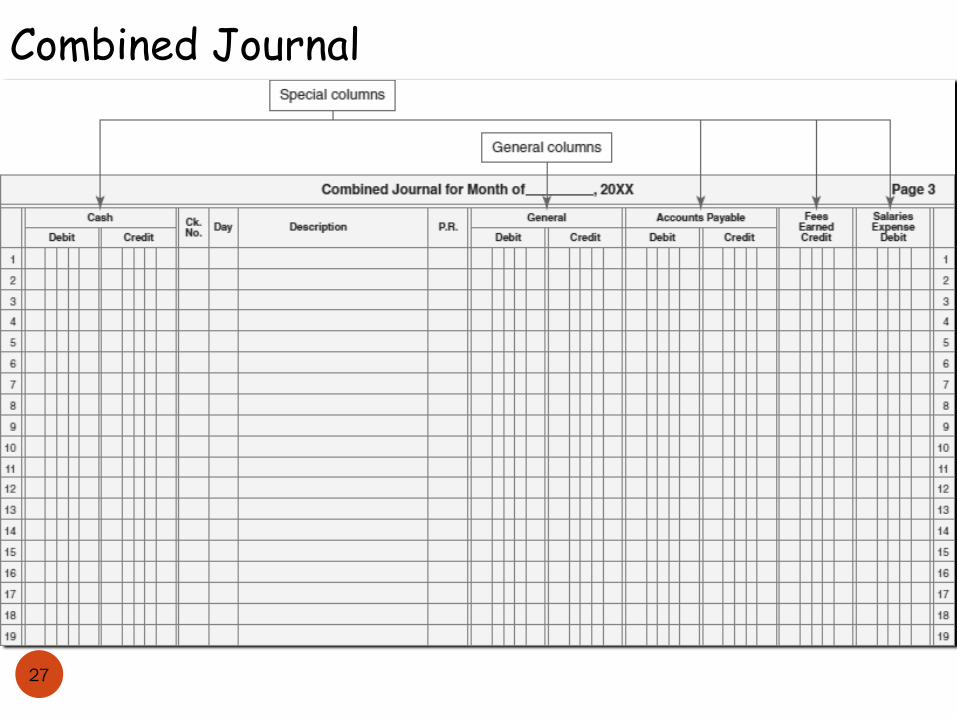

Combined Journal

27

Designing a Combined Journal

• Designed to fit the individual needs of the business

using it

• Special columns should be set up for those accounts

that are most often affected by business transactions

Cash Debit Column

Cash Credit Column

Accounts Payable Debit Column

Accounts Payable Credit Column

Fees Earned Credit Column

Salaries Expense Debit Column

General Debit and Credit Columns

• When the month’s transactions have been

journalized, each column of the combined journal

should be totaled28

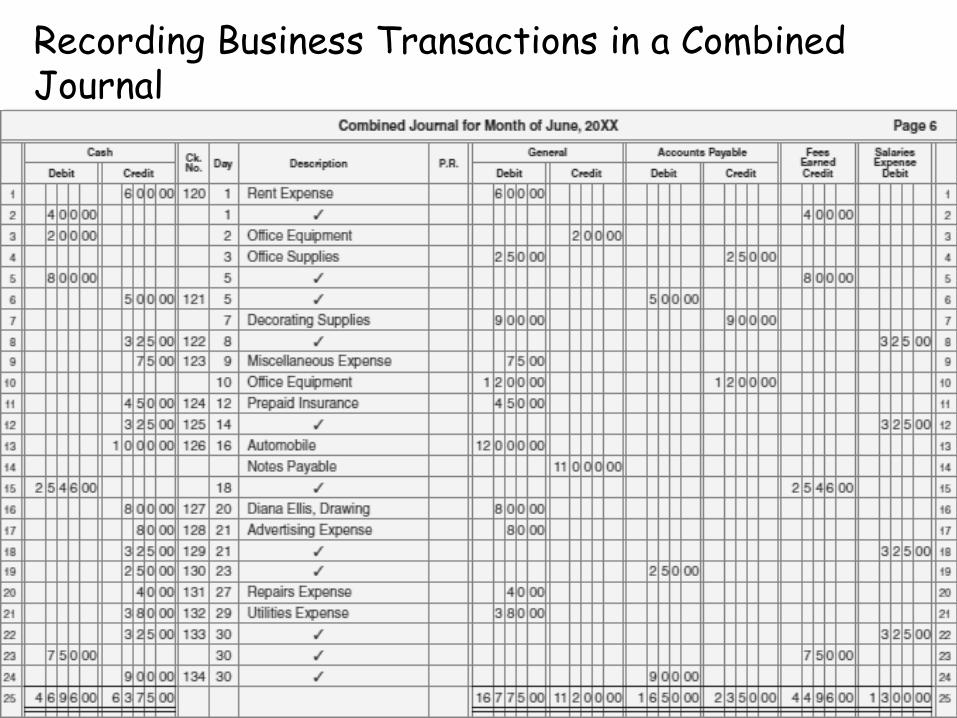

Recording Business Transactions in a Combined Journal

Two transactions to record on Jun. 1:

29

1. Issued Check No. 120 for June rent, $600

2. Received cash for services performed, $400

On the next slide, we’ll see these transactions along with all

of Diana’s transactions for the month of June recorded in a

combined journal:

30

Recording Business Transactions in a Combined Journal

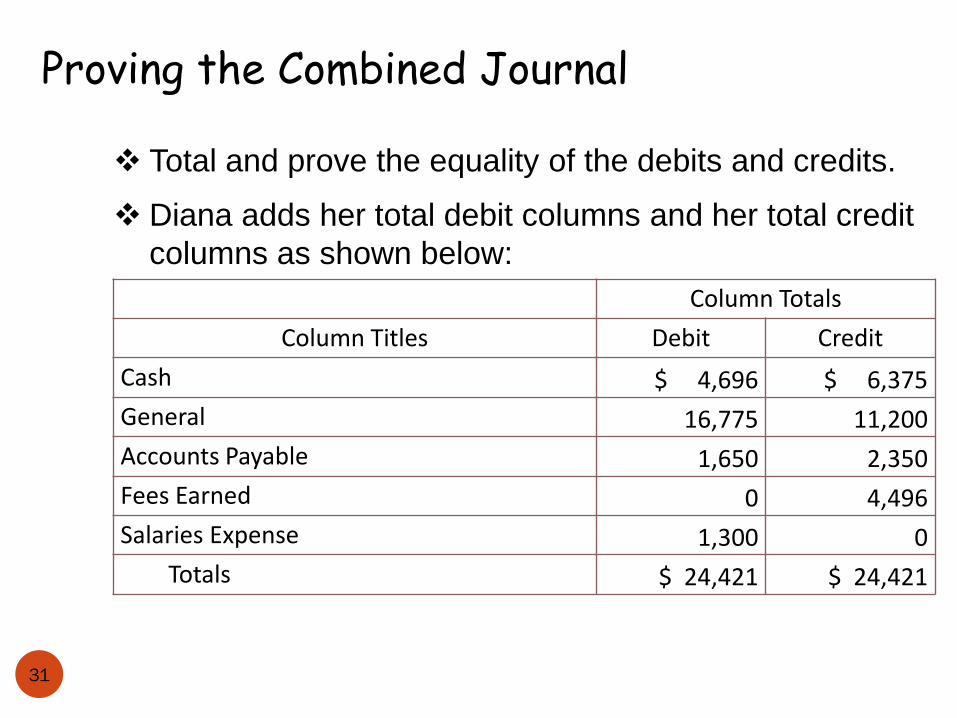

Proving the Combined Journal

31

Total and prove the equality of the debits and credits.

Diana adds her total debit columns and her total credit

columns as shown below:

Column Totals

Column Titles Debit Credit

Cash $ 4,696 $ 6,375

General 16,775 11,200

Accounts Payable 1,650 2,350

Fees Earned 0 4,496

Salaries Expense 1,300 0

Totals $ 24,421 $ 24,421

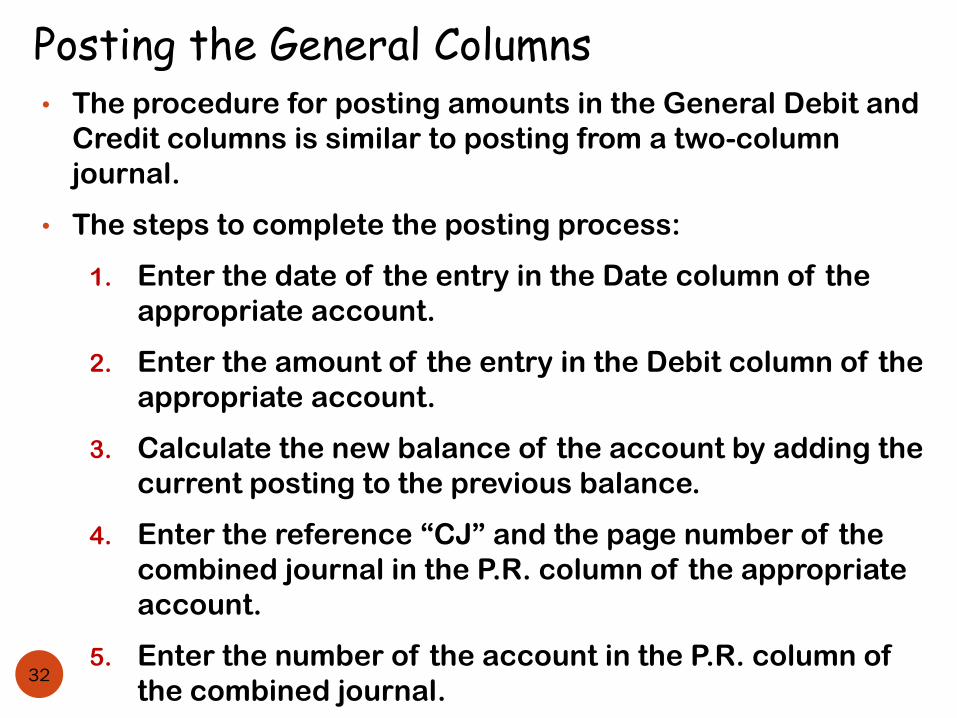

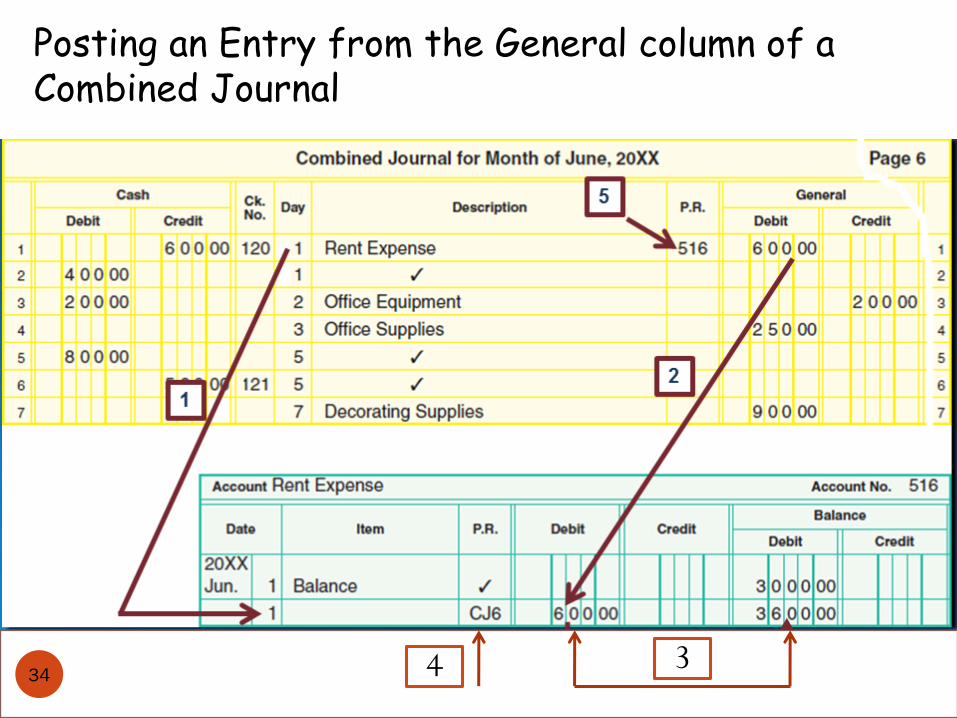

Posting the General Columns• The procedure for posting amounts in the General Debit and

Credit columns is similar to posting from a two-column

journal.

• The steps to complete the posting process:

1. Enter the date of the entry in the Date column of the

appropriate account.

2. Enter the amount of the entry in the Debit column of the

appropriate account.

3. Calculate the new balance of the account by adding the

current posting to the previous balance.

4. Enter the reference “CJ” and the page number of the

combined journal in the P.R. column of the appropriate

account.

5. Enter the number of the account in the P.R. column of

the combined journal.32

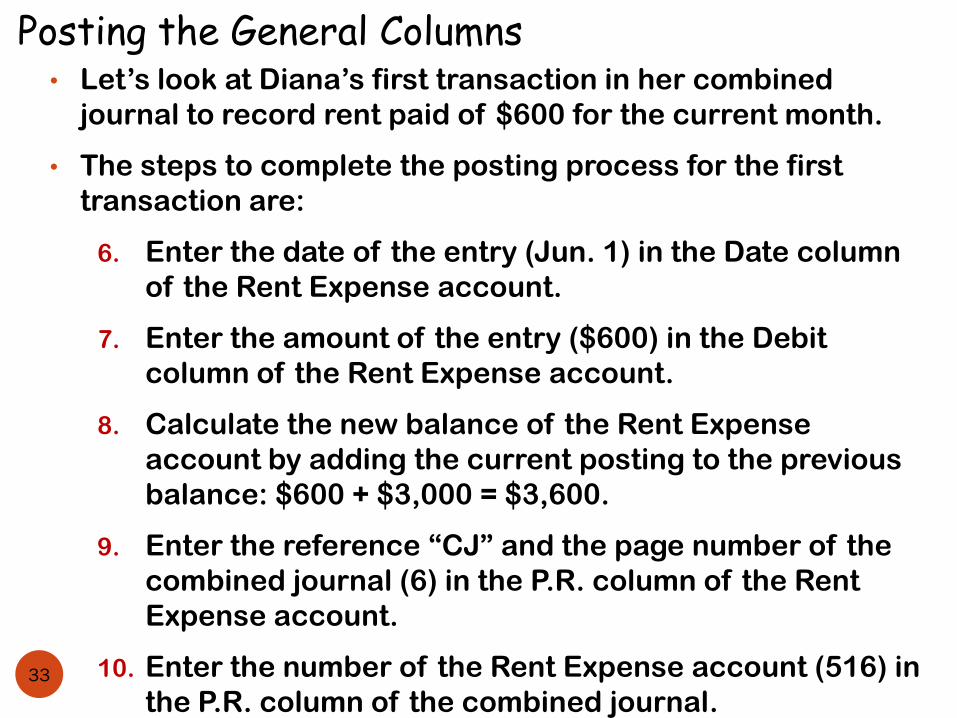

Posting the General Columns• Let’s look at Diana’s first transaction in her combined

journal to record rent paid of $600 for the current month.

• The steps to complete the posting process for the first

transaction are:

6. Enter the date of the entry (Jun. 1) in the Date column

of the Rent Expense account.

7. Enter the amount of the entry ($600) in the Debit

column of the Rent Expense account.

8. Calculate the new balance of the Rent Expense

account by adding the current posting to the previous

balance: $600 + $3,000 = $3,600.

9. Enter the reference “CJ” and the page number of the

combined journal (6) in the P.R. column of the Rent

Expense account.

10. Enter the number of the Rent Expense account (516) in

the P.R. column of the combined journal.33

34

Posting an Entry from the General column of a Combined Journal

4 3

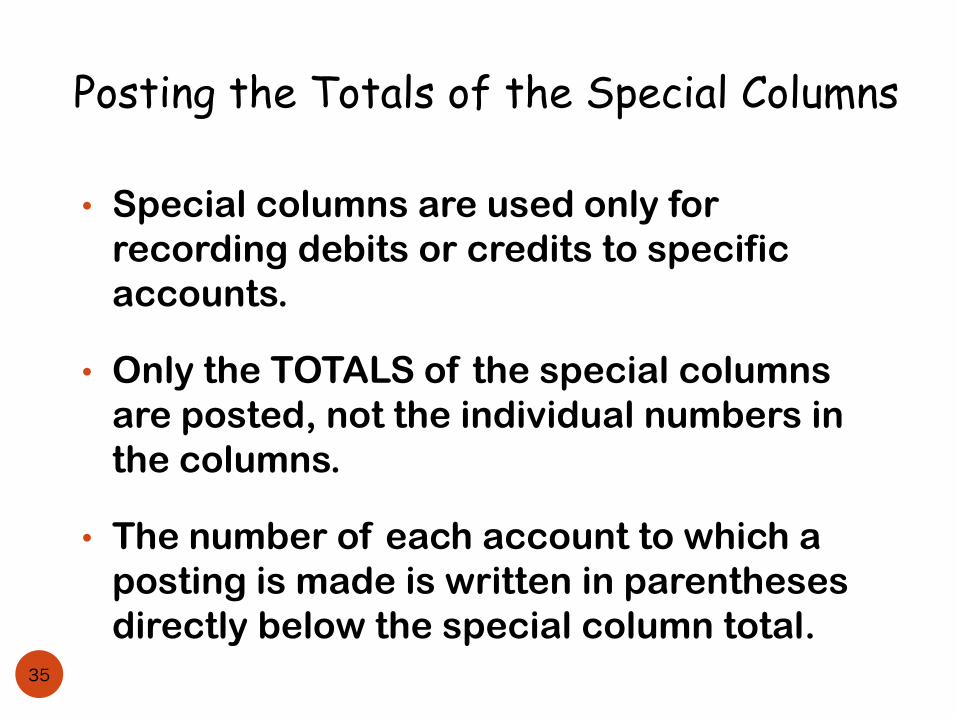

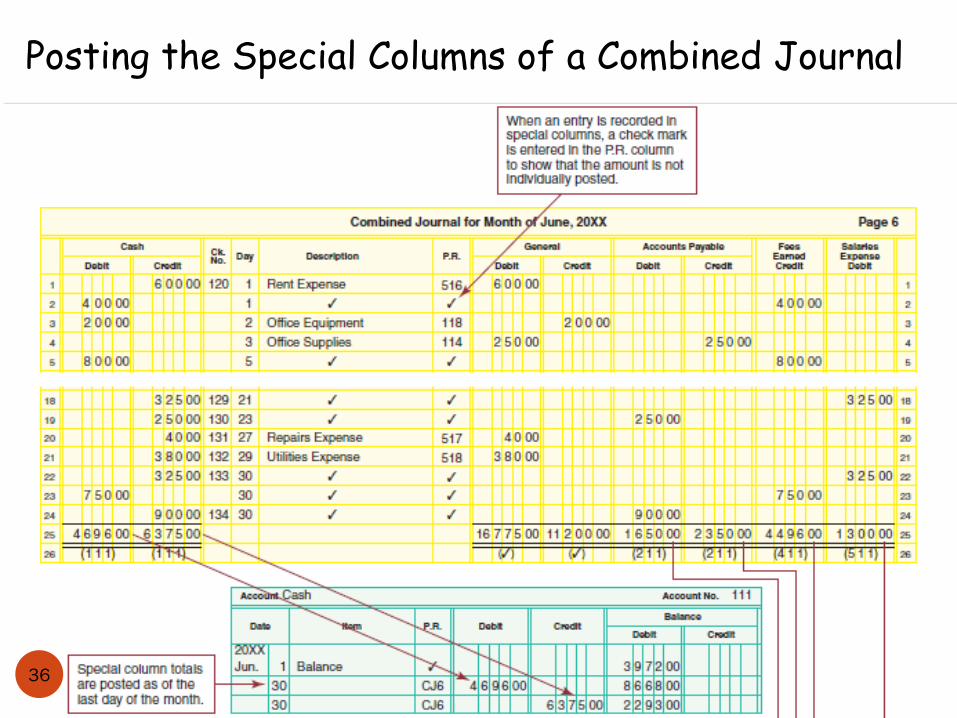

Posting the Totals of the Special Columns

• Special columns are used only for

recording debits or credits to specific

accounts.

• Only the TOTALS of the special columns

are posted, not the individual numbers in

the columns.

• The number of each account to which a

posting is made is written in parentheses

directly below the special column total.35

Posting the Special Columns of a Combined Journal

36

Bank Checking Accounts

• Bank Checking Accountan amount of cash on deposit with a bank that

the bank must pay at the written order of the

depositor

• American Bankers Association (ABA) Transit Number

a number printed on checks and deposit slips

that identifies the bank and the area in which

the bank is located as well as other

information

37

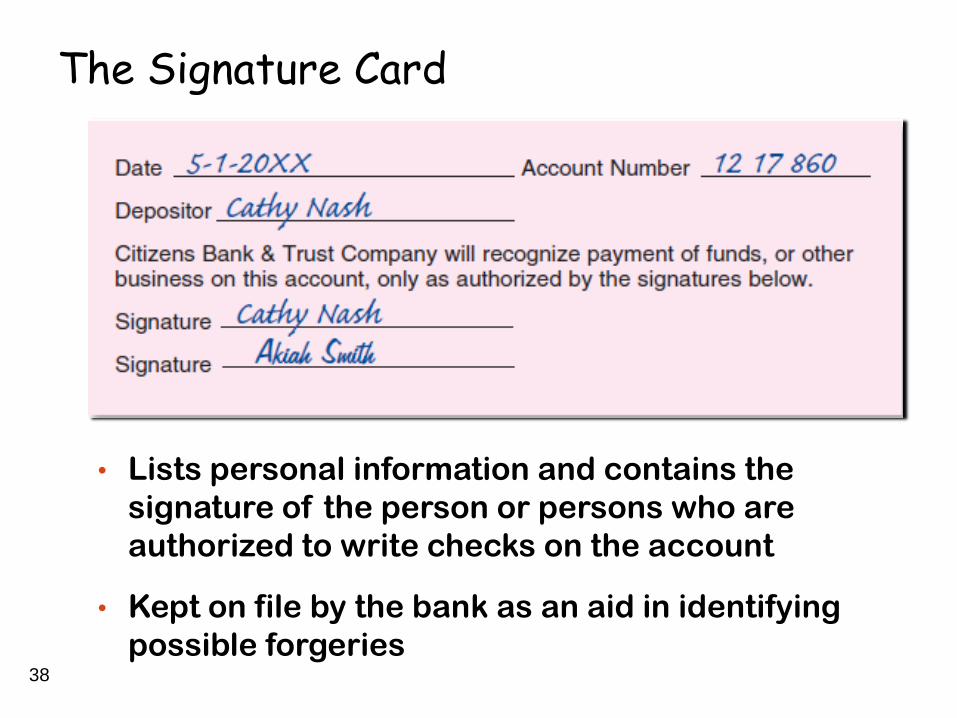

The Signature Card

• Lists personal information and contains the

signature of the person or persons who are

authorized to write checks on the account

• Kept on file by the bank as an aid in identifying

possible forgeries38

Deposit Slip

• Prepared when coin, currency, or checks

are deposited in a bank account

• Indicates

Name of the depositor

Account number

Summarizes the amount deposited

39

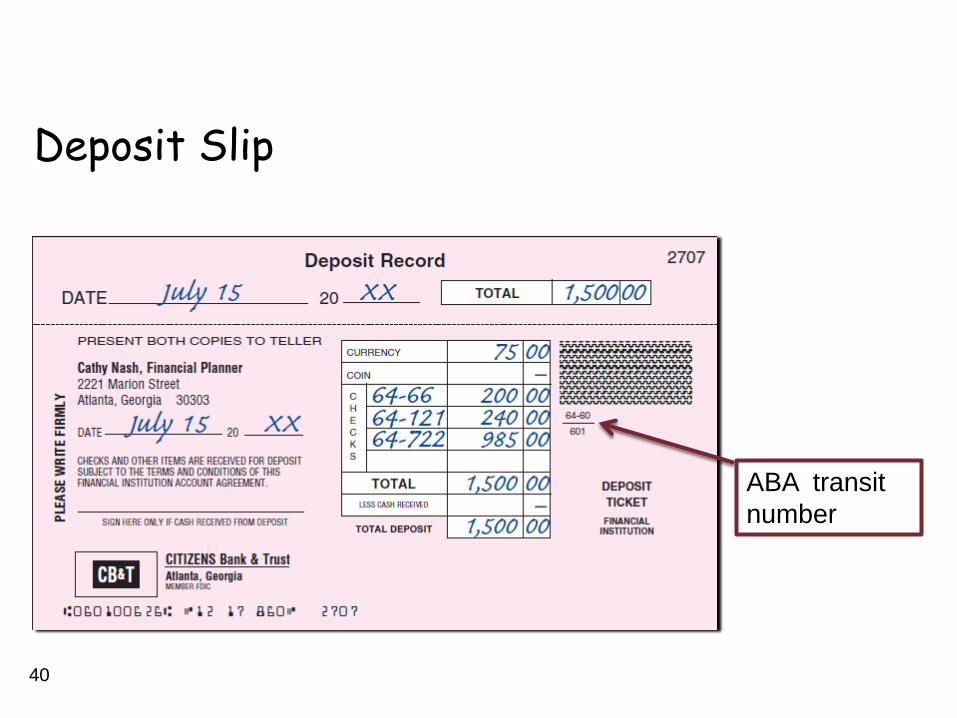

Deposit Slip

40

ABA transit

number

Endorsement

• A signature or stamp on the back of the

check

• Transfers ownership of the check to the

bank (or to another person or to an

individual)

• Authorizes payment of the check

41

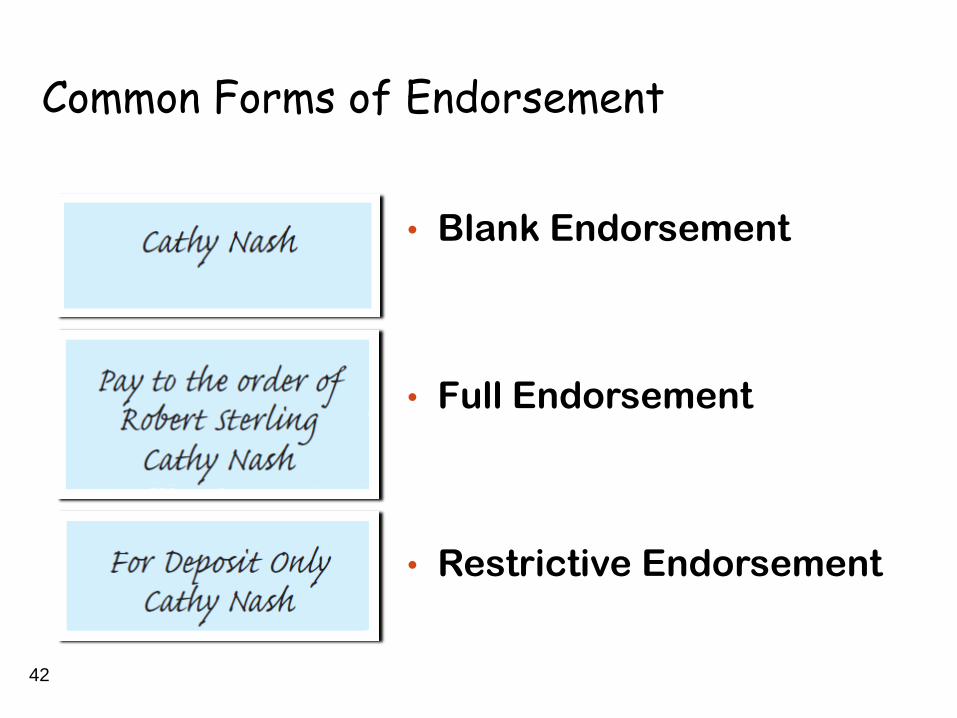

Common Forms of Endorsement

• Blank Endorsement

• Full Endorsement

• Restrictive Endorsement

42

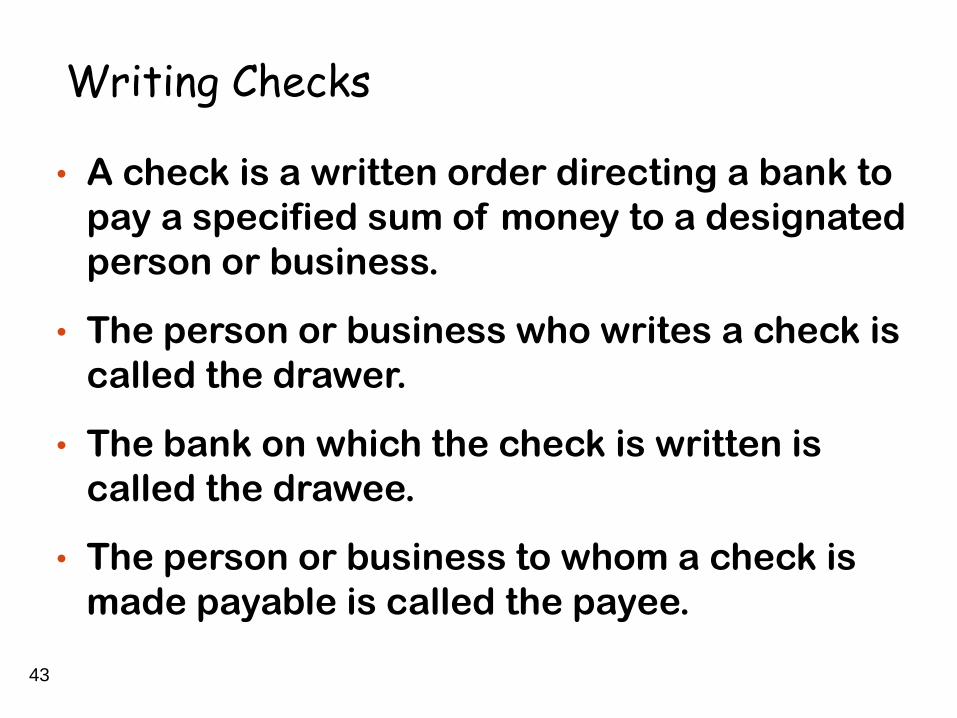

Writing Checks

• A check is a written order directing a bank to

pay a specified sum of money to a designated

person or business.

• The person or business who writes a check is

called the drawer.

• The bank on which the check is written is

called the drawee.

• The person or business to whom a check is

made payable is called the payee.

43

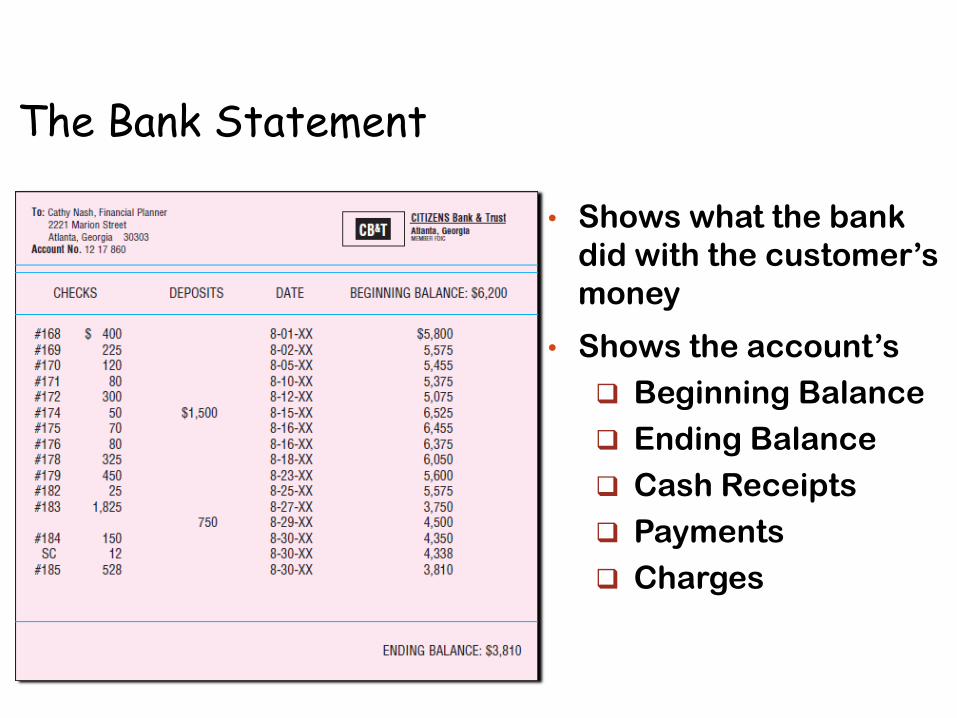

The Bank Statement

• Shows what the bank

did with the customer’s

money

• Shows the account’s

Beginning Balance

Ending Balance

Cash Receipts

Payments

Charges

44

Reconciling the Bank Statement

• The balance shown on the bank statement

and the balance in the checkbook

normally do not agree at the end of the

month

• Bank reconciliation — the process of

making the bank statement agree with the

checkbook balance

45

Reconciling the Bank Statement

Common reasons why the bank statement

balance may not agree with the checkbook

balance include:

• Outstanding checks

• Deposits in transit

• Service charges and other bank fees

• Errors, either the depositor’s or the bank’s

• Bank collections

• NSF checks

46

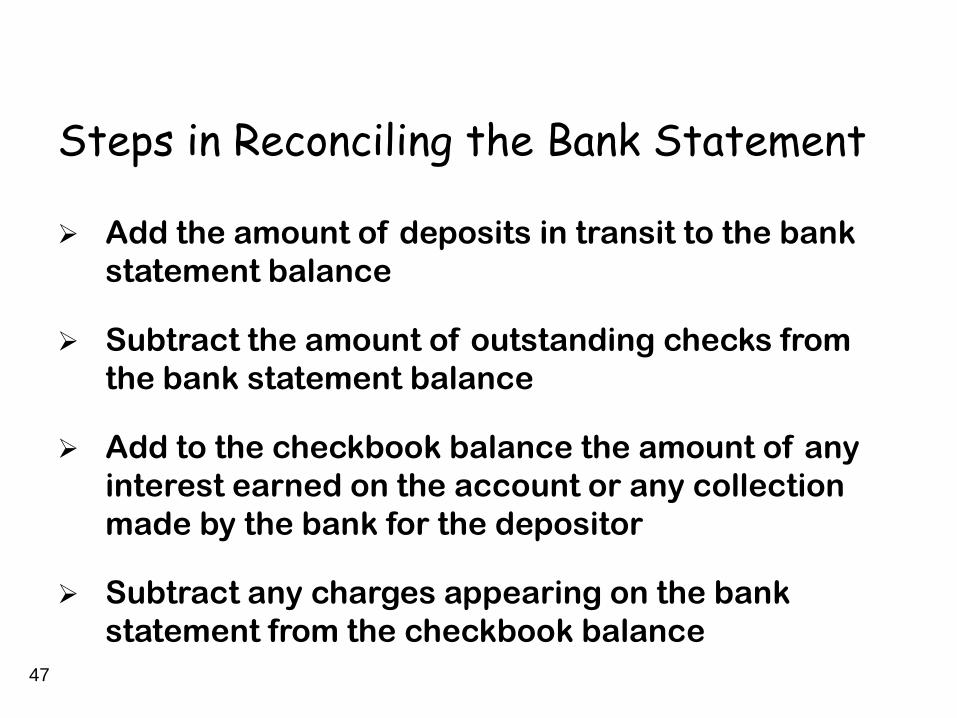

Steps in Reconciling the Bank Statement

Add the amount of deposits in transit to the bank

statement balance

Subtract the amount of outstanding checks from

the bank statement balance

Add to the checkbook balance the amount of any

interest earned on the account or any collection

made by the bank for the depositor

Subtract any charges appearing on the bank

statement from the checkbook balance

47

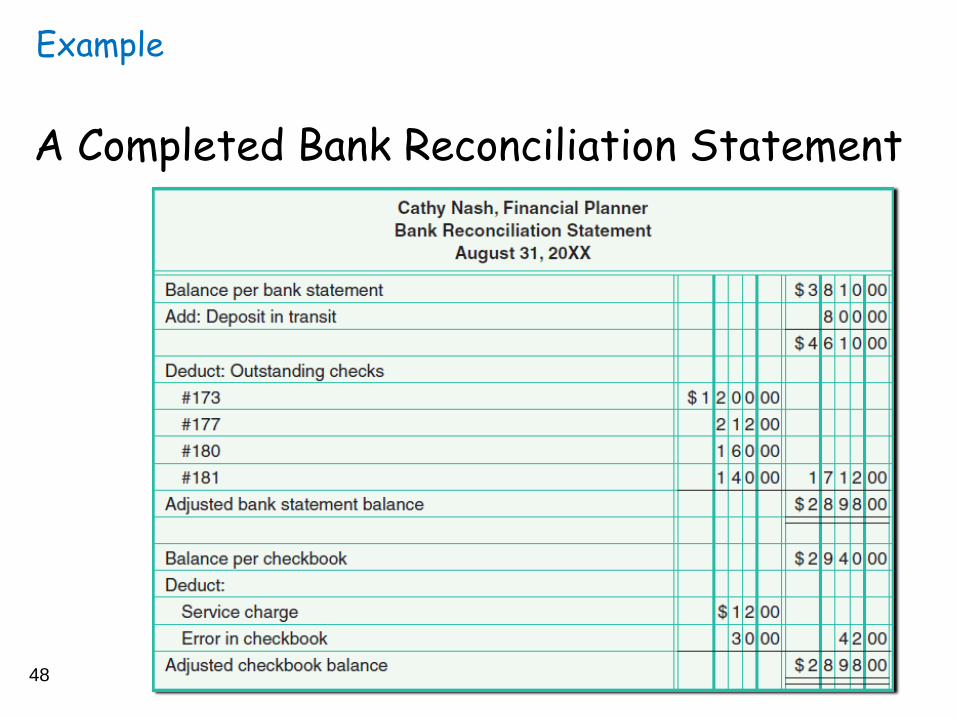

Example

A Completed Bank Reconciliation Statement

48

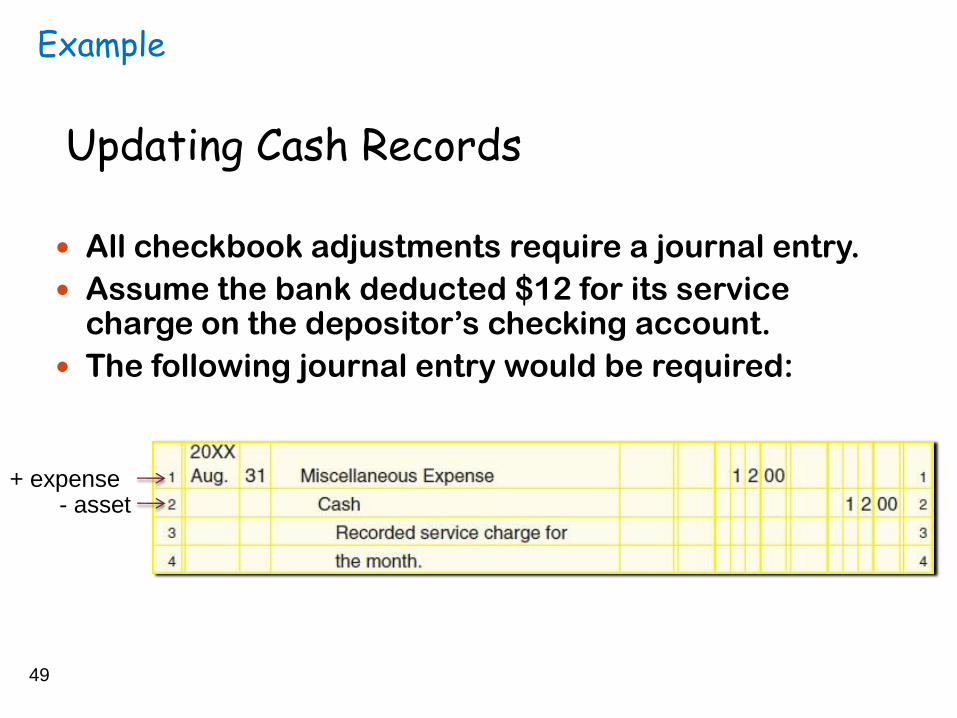

Example

Updating Cash Records

All checkbook adjustments require a journal entry.

Assume the bank deducted $12 for its service charge on the depositor’s checking account.

The following journal entry would be required:

49

+ expense- asset