cfc u.s. bank one cardeoplugin.commpartners.com/nreca/110712/nreca_110712... · 2011-07-12 ·...

TRANSCRIPT

CFC U.S. Bank One CardTuesday, July 12, 2011

2

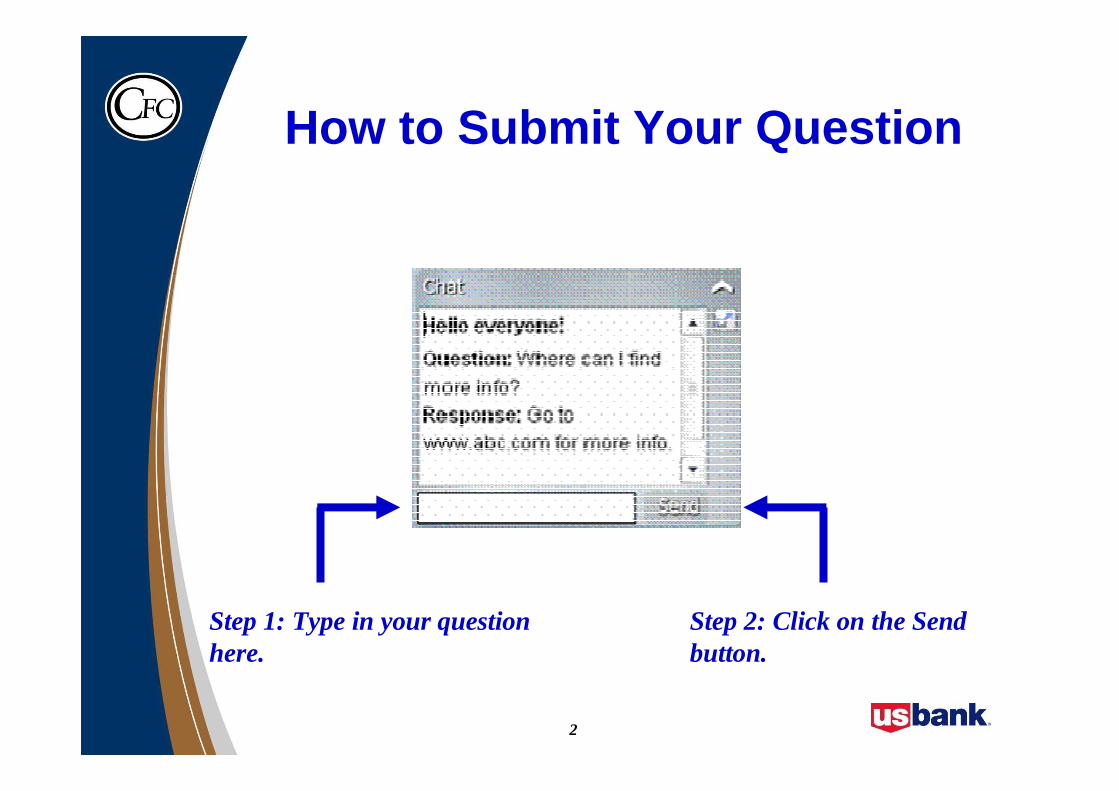

How to Submit Your Question

Step 2: Click on the Send button.

Step 1: Type in your question here.

4

Background• Original card programs began in 2001

• Consolidated products into One Card program in August 2006

• Program currently has 168 participants and generated $19.5 million in aggregated spending last year

5

U.S. Bank – A Strategic Resource• $311 billion in assets

• 5th-largest commercial bank in the United States

• Unparalleled industry experience

• Solutions for the entire payment continuum

• Program design/implementation expertise

• Unsurpassed resource commitments

• World-class, U.S.-based customer service

6

• A strong commitment to the payments business

• Ubiquitous merchant acceptance

• Competitive commercial card advantages for CFC members

• Long-term relationship with a strong and stable commercial bank

U.S. Bank Strategic Benefits

Does My Co -op Need a Commercial Card?

8

Purchasing Landscape• Annual purchasing card spending in

North America grew from $161 billion in 2009 to $176 billion in 2010

• Purchasing card spending in North America is expected to increase to $213 billion by 2012 and $255 billion by 2014

9

Purchasing Landscape

Purchasing Card Spend in North AmericaSource: 2010 Purchasing Card Benchmark Survey, RPMG Palmer & Gupta

1010

Cards Are Expanding Into Larger, Core Purchases

CARDS

• Rebate potential

• Extended DPO via credit function

• Control in the form of restricting spend categories and amounts

• Ability to automate G/L interface

• Pre-purchase process efficiencies

• Detailed transaction data

• No cost to buying organization

� T&E

� Office Supplies/MRO

� POS ad hoc purchases

� Petty cash alternative

� Increasingly used for larger purchases including COGS

Common Uses

CARDSCHECKS

Cap Ex

MROAd Hoc

COGS

11

Checks

ACH

Wire

Cards

25%

10%7%

13%

2%4%

81%

58%

B2B Payment Matrix(% of total number of transactions)

Source: AFP Electronic Payments Survey Data for 2004 - 2010

12

Bottom -Line Results• Average net savings of $69+ per transaction

• Average procurement cycle time reduction of 6.3 days

• Average reduction in supplier base of 31%

• 38% increase in ability to negotiate preferred pricing

• Happier and more productive employees

13

Real-World Successes*Procure-to-pay and commercial card programs build the bottom line.

– One electric utility expanded its card program from emergency purchases only to all its routine purchasing, reducing manual AP check payments by more than 65%.

– A leading provider of technology and business solutions plans to move more than $8 million of company spend from paper checks to its commercial card program.

– A construction company saved more than $100,000 and grew its commercial card program from $1 million to $6 million by eliminating local “house” charge accounts.

*2008 Visa Global Procure-to-Pay and Commercial Best Practices Study, Deloitte Consulting

The Program

15

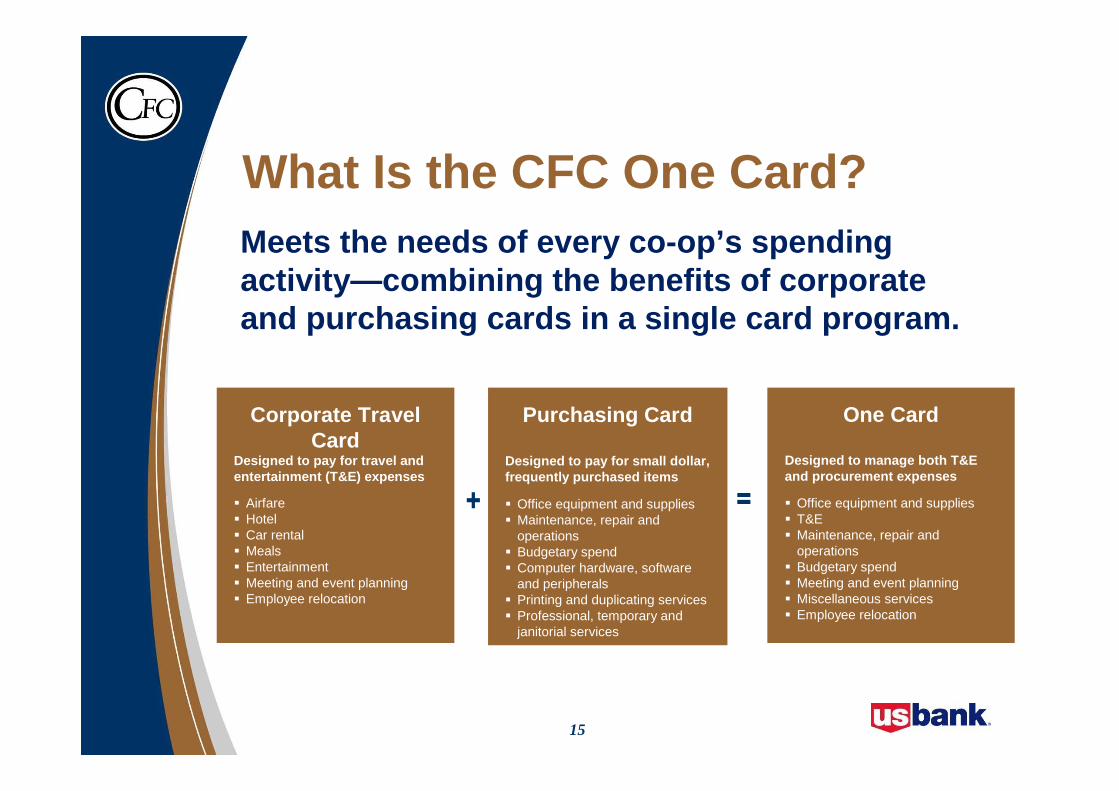

What Is the CFC One Card?Meets the needs of every co-op’s spending activity—combining the benefits of corporate and purchasing cards in a single card program.

+ =

Purchasing Card

Designed to pay for small dollar, frequently purchased items

� Office equipment and supplies� Maintenance, repair and

operations� Budgetary spend� Computer hardware, software

and peripherals� Printing and duplicating services� Professional, temporary and

janitorial services

Designed to pay for travel and entertainment (T&E) expenses

Corporate Travel Card

� Airfare� Hotel� Car rental� Meals� Entertainment� Meeting and event planning� Employee relocation

Designed to manage both T&E and procurement expenses

One Card

� Office equipment and supplies� T&E� Maintenance, repair and

operations� Budgetary spend� Meeting and event planning� Miscellaneous services� Employee relocation

16

Program Benefits• No annual fees or interest

• No credit check on cardholders

• No individual liability

• Flexible online reporting and administration capabilities

• Exciting rebate opportunity

17

Program Benefits• Simplify and streamline operations

• Save time, money and resources

• Stay in control and in compliance

• Tailor the card program to your specific needs

• Provide a convenient payment tool to employees

• Make better-informed business decisions

18

Types of One Card Accounts• Individual Cardholder Accounts

– A card assigned to an individual employee that has the employee’s name on the card

• Department Cardholder Accounts– A card that is commonly used by a department

or for a specific type of purchase

• Ghost Accounts– A virtual, card-free purchasing account tied to a

single department, supplier or spend category

19

One Card for Purchasing• Reduces volume of purchase orders, invoices

and check payments

• Improves purchasing management and provides reporting for IRS and state regulators

• Enables monitoring of corporate policy compliance

• Improves employee spending controls

• Facilitates vendor negotiations

20

One Card for T&E• Customized authorization controls

• Online account access

• Cash advance option

• Ability to interface with your accounting software

• Comprehensive travel benefits– Worldwide automatic travel accident insurance:

$250,000

– Excess lost/damaged luggage coverage: $1,250

21

Typical Co -op Cardholders• Human resources

• Plant and maintenance employees

• Technical and office staff

• General administration

• Purchasing department

• Advertising/marketing staff

• Sales force

22

Typical Co -op Expenditures• Oil and fuel

• Computer and software purchases

• Utilities payments

• Office supplies

• Continuing education expenses

• Online purchases

• Airfare and hotel expenses

23

VolumeWholesale Trade

Hotels

Business Expense

Vehicle Expense

Other

Eating/Drinking

Office Services

Airline

Office Supplies

MRO Supplies

Mail/Telphone

Auto/RV Dealers

Annual Volume Type of Spend ATS # of Transactions$5,043,787.93 WHOLESALE TRADE $164.23 30,712$3,610,702.51 HOTELS $295.52 12,218$2,578,426.81 BUSINESS EXPENSE $393.11 6,559$2,418,725.45 VEHICLE EXPENSE $59.73 40,495$1,763,016.10 OTHER $198.47 8,883$1,734,222.01 EATING/DRINKING $50.48 34,354$1,466,929.51 OFFICE SERVICES $364.36 4,026$1,302,718.90 AIRLINE $227.87 5,717$972,141.91 OFFICE SUPPLIES $166.86 5,826$499,338.89 MRO SUPPLIES $365.28 1,367$435,439.17 MAIL/TELEPHONE $312.59 1,393$225,941.45 AUTO/RV DEALERS $273.21 827

One CardTop Co -opSpendCategories

One Card Rebate Opportunity

25

Rebate Overview• Participating cooperatives have the

opportunity to qualify for an annual cash rebate

• The rebate period runs annually from September through August

26

How the Rebate Works• Participating cooperatives must collectively

generate at least $5 million in annual charge volume and have an average transaction size of at least $120.

• The higher the collective charge volume, the higher the percentage of rebate.

• Once the collective program rebate is attained, cooperatives can earn a portion of that rebate if they meet the individual eligibility requirement.

27

Individual Rebate Eligibility• The cooperative’s annual spend must be at

least $175,000.

• If the cooperative has an average transaction size of least $120, the rebate is even higher.

28

Effective September 1, 2011Two separate ways of earning a cash rebate through the One Card program:

– A portion of the collective rebate will be paid to each cooperative that spends a minimum amount of $5,000 in one rebate year.

– A separate rebate will be paid to each cooperative that averages at least $120 per transaction during the rebate year.

29

Rebate Success• 2008–2009 Rebate Year

– Total spend: $15.9 million

– Average transaction size: $125

– Performance Rebate: $67,687

– Individual co-op payouts ranged from $780 to $11,800

• 2009–2010 Rebate Year– Total spend: $19.5 million

– Average transaction size: $144

– Performance Rebate: $71,963

– Individual co-op payouts ranged from $640 to $8,170

Making One Card Work for You

31

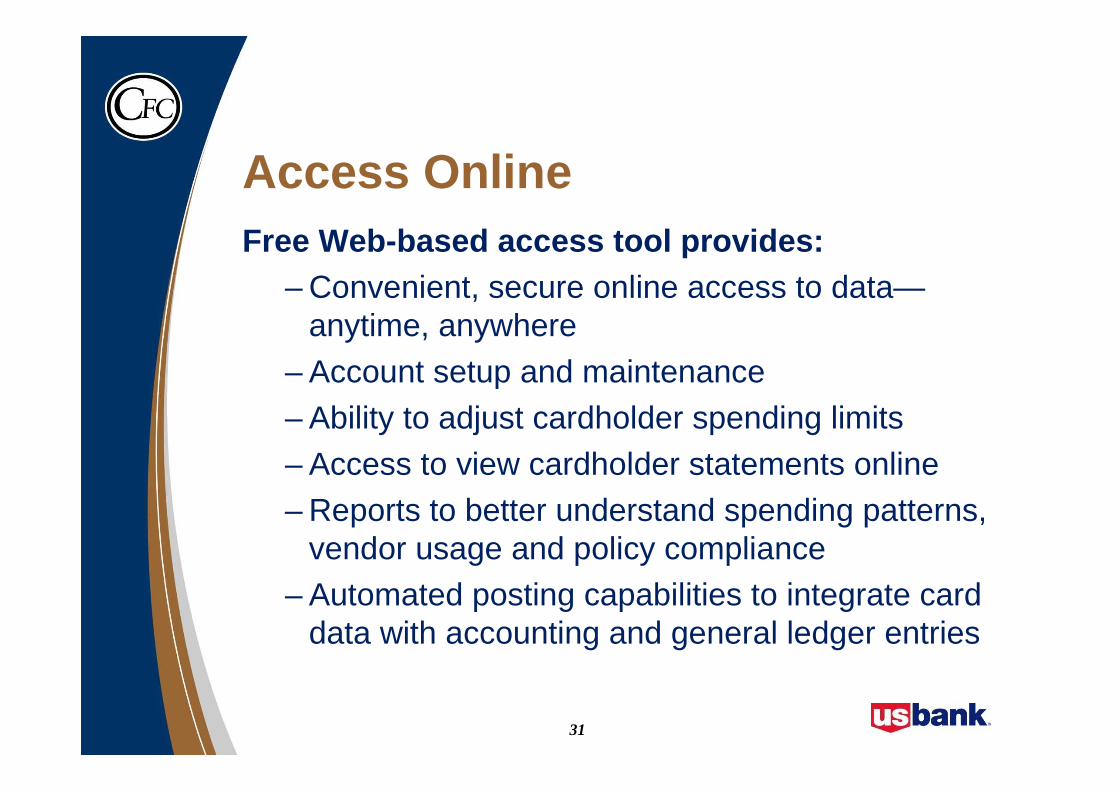

Access OnlineFree Web-based access tool provides:

– Convenient, secure online access to data—anytime, anywhere

– Account setup and maintenance– Ability to adjust cardholder spending limits

– Access to view cardholder statements online– Reports to better understand spending patterns,

vendor usage and policy compliance– Automated posting capabilities to integrate card

data with accounting and general ledger entries

32

AutoPay• Amount due is automatically drawn from

specified account

• Cycling date is the 16th of every month unless on a weekend or holiday

• Cooperative chooses a draft date that is within 14 days of the 16th

33

Fleet Capabilities• Cards issued at a driver or vehicle level

• Enhanced spending controls– Ability to limit spending to fuel and/or

maintenance only– Prompts for driver ID and odometer reading

– Velocity controls and hard limits

• Accepted by Visa and MasterCard merchants worldwide

• Enhanced fleet data capture ─provided by most major oil companies

34

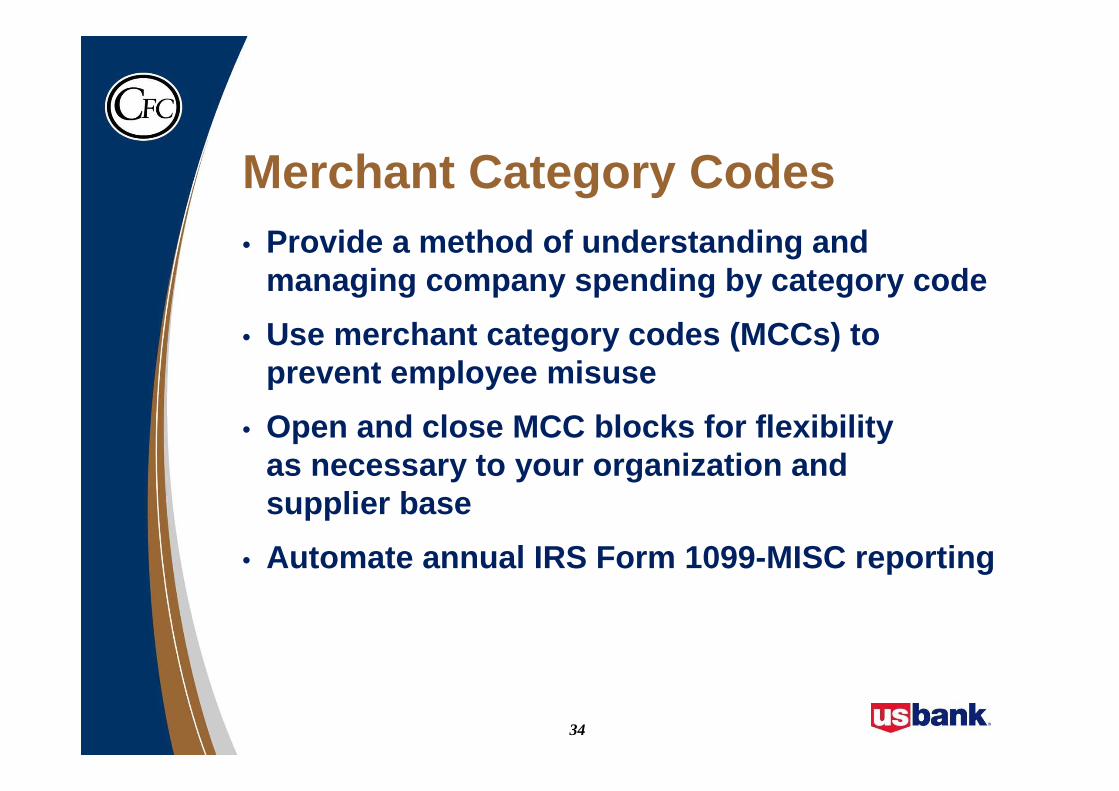

Merchant Category Codes • Provide a method of understanding and

managing company spending by category code

• Use merchant category codes (MCCs) to prevent employee misuse

• Open and close MCC blocks for flexibility as necessary to your organization and supplier base

• Automate annual IRS Form 1099-MISC reporting

35

Flexible Spending Management• Authorization parameters

– Monthly spending limit– Daily spending limit

– Single-purchase limit (SPL)

• Supplier category restrictions– Travel, casinos, jewelry, liquor, etc.

36

Automated Accounting Methods• Default account code assigned to each card

– Cost center, budget code, company code, etc.

• General Ledger object codes assigned by type of purchase

– Office supplies, computer equipment, hotels, hardware stores, etc.

• Accounting codes can be changed/edited as needed

• Transaction data can be exported for integration with accounting software

Addressing Cooperative Concerns

38

Cooperative Concern 1Spend Out of Policy

– (also known as “Maverick Spend”)– A commercial card is used in a way that does

not conform to the spending policies of the organization

39

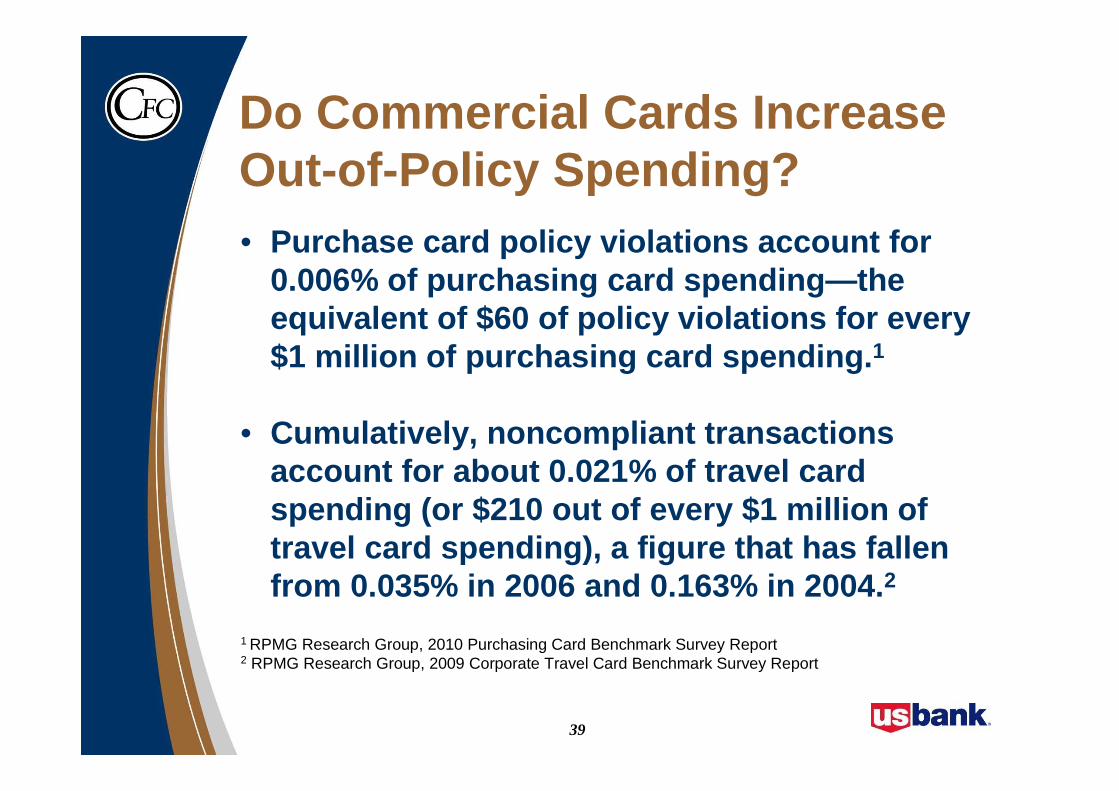

• Purchase card policy violations account for 0.006% of purchasing card spending—the equivalent of $60 of policy violations for every $1 million of purchasing card spending. 1

• Cumulatively, noncompliant transactions account for about 0.021% of travel card spending (or $210 out of every $1 million of travel card spending), a figure that has fallen from 0.035% in 2006 and 0.163% in 2004. 2

Do Commercial Cards Increase Out-of-Policy Spending?

1 RPMG Research Group, 2010 Purchasing Card Benchmark Survey Report 2 RPMG Research Group, 2009 Corporate Travel Card Benchmark Survey Report

40

Cooperative Concern 2Card Misuse

– An employee charges a personal expense through a commercial card and misrepresents it as a business expense.

41

Will Employees Misuse Commercial Cards?• Purchasing card misuse accounts for .014% of

purchasing card spending, which is the equivalent of $1.40 of misuse for every $10,000 of purchasing card spend.

– .008% for fraud and misrepresentation– .006% for policy violations

• Losses are a fraction of the administrative cost savings and other benefits attributable to card use .

• Visa Liability Waiver Program covers your cooperative up to $100,000 per cardholder in the event of employee card misuse.

Dedicated Program Support

43

U.S. Bank SupportGreg Wenisch, Relationship Manager

Jennifer Kartes, Program Coordinator– Custom implementation

– Ongoing strategic consultation– Training on Web-based access tools

– Problem resolution

– A complete partnership approach to your business success

44

CFC Program Support• Manages relationship with U.S. Bank• Provides day-to-day member contact• Establishes new cooperative accounts• Answers general member questions and

concerns

45

Get Started Today!Contact Tara Cromp for more details:

– Phone: 800-424-2954– E-mail: [email protected]

How to Submit Your Question

Step 2: Click on the Send button.

Step 1: Type in your question here.