care equity research rswm limited · rswm (earlier rajasthan spinning and weaving mills), was...

TRANSCRIPT

RSWM LIMITED

1 www.careratings.com

CARE

EQUITY

RESEARCH

Independent Equity Research

RSWM LIMITED TEXTILES

BSE Scrip Code: 500350

Integrated textile player having significant brand awareness

RSWM Limited (RSWM) is a leading and integrated

manufacturer of synthetic and blended spun yarn, PV fabric and

denim fabric. The company sells its product under the “Mayur”

brand in the domestic markets and enjoys significant brand

awareness. RSWML exports a complete range of yarn and fabric

to over 70 countries worldwide with presence across Europe,

South Africa, North America, Australia, South Korea, Belgium,

Singapore, Italy, Egypt and the Gulf countries. The company has

six manufacturing facilities — Kharigram, Mandpam, Banswara,

Rishabhdev, Ringas and Mordi. The company also has a

presence in Tamil Nadu and Pondicherry through its subsidiary

Cheslind Textiles Ltd.

Stable growth outlook for the Indian Textile sector

A growing economy, rising disposable incomes, increase in

exports and the growing aspirations of Indian consumers are

expected to continue driving growth in the Indian Textile and

Apparel (T&A) industry. CARE Research expects the domestic

consumption of Man Made Fibre (MMF) to grow at a CAGR of

5.8 per cent from 2,802 thousand tonnes in FY12 to 3,717

thousand tonnes in FY17. The cotton yarn segment is also

expected to grow at about 10 per cent CAGR between FY12 to

FY17. However, issues such as weakness in yarn prices, volatile

raw material prices and exchange rate fluctuations remain the key

challenges for the sector.

Key concerns

• Risk of rising material prices and margin pressures evident in

the textile industry

• Low entry barriers in the industry because of which the

industry faces a lot of competition

• Revenue concentration risk

• Exchange rate volatility

Valuations

RSWM is currently trading at trailing P/E and EV/EBITDA

multiples of 1.5x and 3.6x, respectively.

CMP Rs.87.51

March 16, 2012

RSWM LIMITED

www.careratings.com 2

CARE

EQUITY

RESEARCH

Background

RSWM (earlier Rajasthan Spinning and Weaving Mills), was incorporated in 1960 and is the flagship company of

the Bhilwara group. The company is one of the leading and integrated manufacturers of synthetic and blended spun

yarn, PV fabric and denim fabrics. The product-mix of the company includes blends such as polyester, viscose,

polyester sewing threads, acrylic, silk blends, viscose/ flax, and cotton melange yarn. The product range for the

company includes specialty, functional, technical and eco-friendly yarn and fabric along-with basic and commodity

products. The company is focusing to produce more natural textiles in order to meet the emerging needs of the

market. RSWML exports a complete range of yarn and fabric to over 70 countries worldwide, giving it presence

across Europe, South Africa, North America, Australia, South Korea, Belgium, Singapore, Italy, Egypt and the Gulf

countries. It also holds the prestigious ‘Three Star Export House’ status.

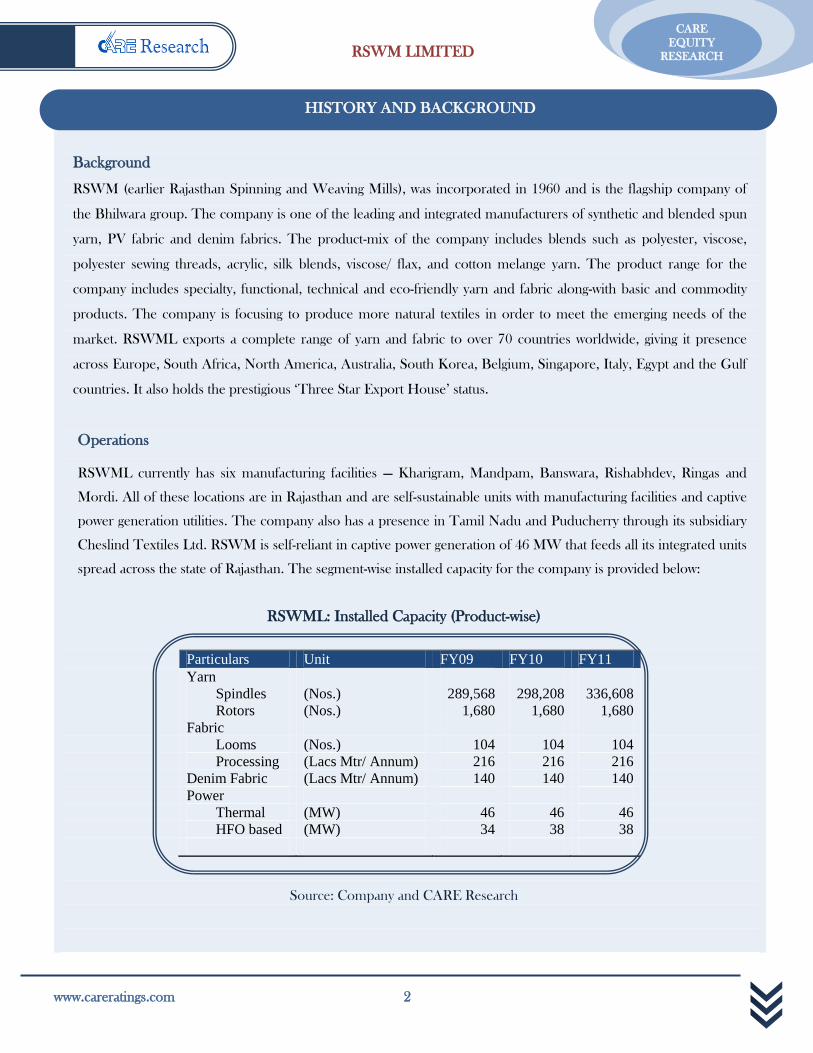

Operations

RSWML currently has six manufacturing facilities — Kharigram, Mandpam, Banswara, Rishabhdev, Ringas and

Mordi. All of these locations are in Rajasthan and are self-sustainable units with manufacturing facilities and captive

power generation utilities. The company also has a presence in Tamil Nadu and Puducherry through its subsidiary

Cheslind Textiles Ltd. RSWM is self-reliant in captive power generation of 46 MW that feeds all its integrated units

spread across the state of Rajasthan. The segment-wise installed capacity for the company is provided below:

RSWML: Installed Capacity (Product-wise)

Particulars Unit FY09 FY10 FY11

Yarn

Spindles (Nos.) 289,568 298,208 336,608

Rotors (Nos.) 1,680 1,680 1,680

Fabric

Looms (Nos.) 104 104 104

Processing (Lacs Mtr/ Annum) 216 216 216

Denim Fabric (Lacs Mtr/ Annum) 140 140 140

Power

Thermal (MW) 46 46 46

HFO based (MW) 34 38 38

Source: Company and CARE Research

HISTORY AND BACKGROUND

RSWM LIMITED

3 www.careratings.com

CARE

EQUITY

RESEARCH

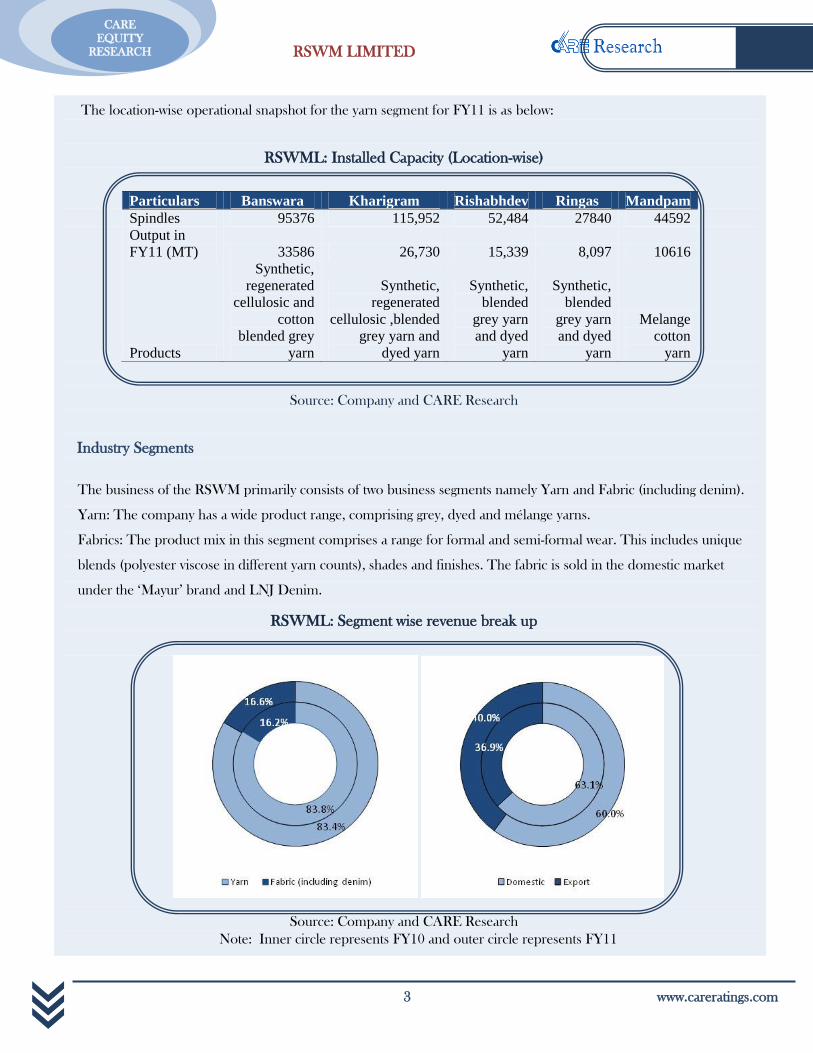

The location-wise operational snapshot for the yarn segment for FY11 is as below:

RSWML: Installed Capacity (Location-wise)

Particulars Banswara Kharigram Rishabhdev Ringas Mandpam

Spindles 95376 115,952 52,484 27840 44592

Output in

FY11 (MT) 33586 26,730 15,339 8,097 10616

Products

Synthetic,

regenerated

cellulosic and

cotton

blended grey

yarn

Synthetic,

regenerated

cellulosic ,blended

grey yarn and

dyed yarn

Synthetic,

blended

grey yarn

and dyed

yarn

Synthetic,

blended

grey yarn

and dyed

yarn

Melange

cotton

yarn

Source: Company and CARE Research

Industry Segments

The business of the RSWM primarily consists of two business segments namely Yarn and Fabric (including denim).

Yarn: The company has a wide product range, comprising grey, dyed and mélange yarns.

Fabrics: The product mix in this segment comprises a range for formal and semi-formal wear. This includes unique

blends (polyester viscose in different yarn counts), shades and finishes. The fabric is sold in the domestic market

under the ‘Mayur’ brand and LNJ Denim.

RSWML: Segment wise revenue break up

Source: Company and CARE Research

Note: Inner circle represents FY10 and outer circle represents FY11

RSWM LIMITED

www.careratings.com 4

CARE

EQUITY

RESEARCH

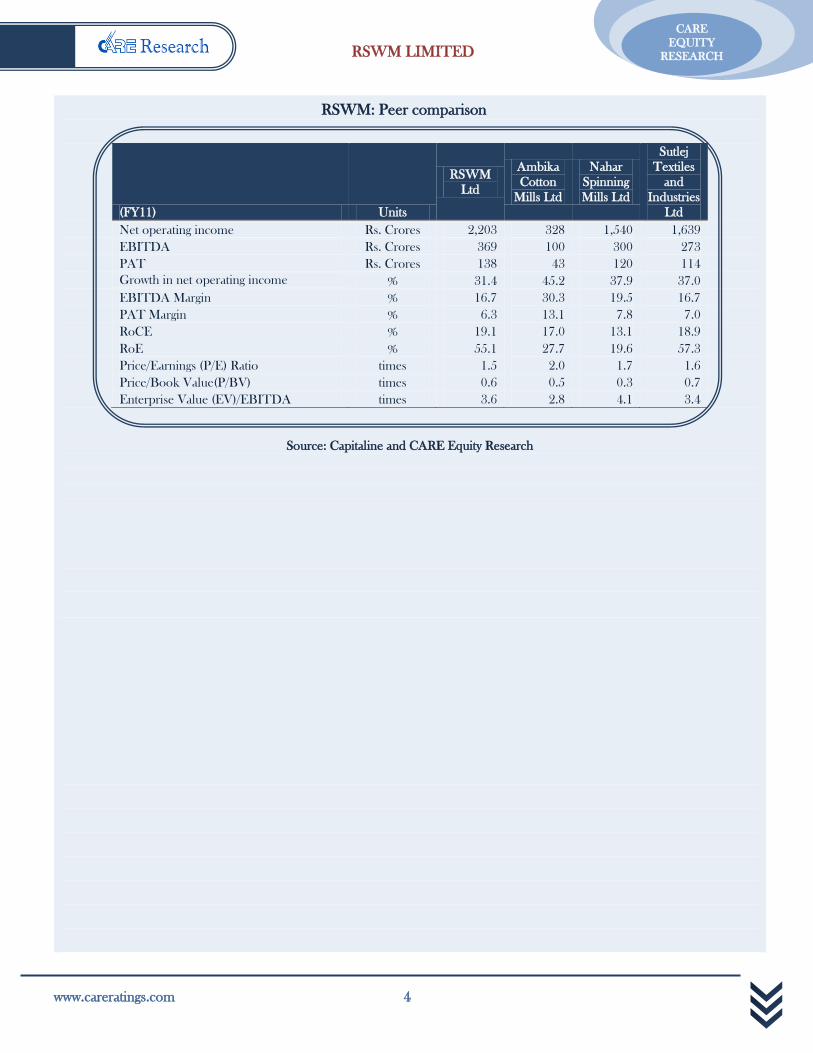

RSWM: Peer comparison

(FY11) Units

RSWM

Ltd

Ambika

Cotton

Mills Ltd

Nahar

Spinning

Mills Ltd

Sutlej

Textiles

and

Industries

Ltd

Net operating income Rs. Crores 2,203 328 1,540 1,639

EBITDA Rs. Crores 369 100 300 273

PAT Rs. Crores 138 43 120 114

Growth in net operating income % 31.4 45.2 37.9 37.0

EBITDA Margin % 16.7 30.3 19.5 16.7

PAT Margin % 6.3 13.1 7.8 7.0

RoCE % 19.1 17.0 13.1 18.9

RoE % 55.1 27.7 19.6 57.3

Price/Earnings (P/E) Ratio times 1.5 2.0 1.7 1.6

Price/Book Value(P/BV) times 0.6 0.5 0.3 0.7

Enterprise Value (EV)/EBITDA times 3.6 2.8 4.1 3.4

Source: Capitaline and CARE Equity Research

RSWM LIMITED

5 www.careratings.com

CARE

EQUITY

RESEARCH

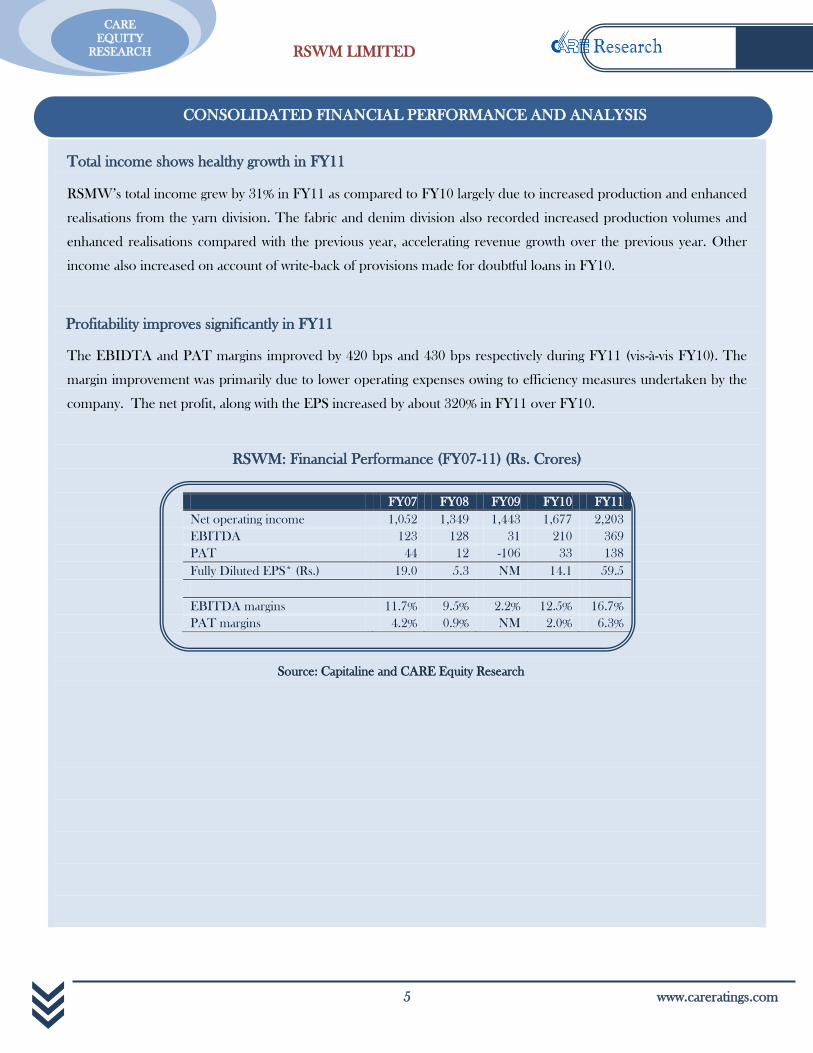

Total income shows healthy growth in FY11

RSMW’s total income grew by 31% in FY11 as compared to FY10 largely due to increased production and enhanced

realisations from the yarn division. The fabric and denim division also recorded increased production volumes and

enhanced realisations compared with the previous year, accelerating revenue growth over the previous year. Other

income also increased on account of write-back of provisions made for doubtful loans in FY10.

Profitability improves significantly in FY11

The EBIDTA and PAT margins improved by 420 bps and 430 bps respectively during FY11 (vis-à-vis FY10). The

margin improvement was primarily due to lower operating expenses owing to efficiency measures undertaken by the

company. The net profit, along with the EPS increased by about 320% in FY11 over FY10.

RSWM: Financial Performance (FY07-11) (Rs. Crores)

FY07 FY08 FY09 FY10 FY11

Net operating income 1,052 1,349 1,443 1,677 2,203

EBITDA 123 128 31 210 369

PAT 44 12 -106 33 138

Fully Diluted EPS* (Rs.) 19.0 5.3 NM 14.1 59.5

EBITDA margins 11.7% 9.5% 2.2% 12.5% 16.7%

PAT margins 4.2% 0.9% NM 2.0% 6.3%

Source: Capitaline and CARE Equity Research

CONSOLIDATED FINANCIAL PERFORMANCE AND ANALYSIS

RSWM LIMITED

www.careratings.com 6

CARE

EQUITY

RESEARCH

Expansion plans and initiatives

RSWM increased production capacity in the yarn segment through the addition of 36,128 spindles for an

investment of Rs.72 crore in FY11.

The company has also planned a Rs.150 crore brown-field expansion to be commissioned by the end of FY12 to

increase the annual manufacturing capacity of yarn by 900 tonnes and denim fabric by 40 lac metres.

The company expects to increase its yarn making capacity to 7,00,000 spindles by the year 2016, thereby

generating economies of scale.

The company plans to strengthen presence in established export destinations and capitalise on opportunities in

Turkey and Columbia.

Key concerns

Risk of rising material prices and margin pressures evident in the textile industry.

Low entry barriers in the industry because of which the industry faces a lot of competition.

With exports forming around 40% of the total revenue in FY11 coupled with the volatility seen in the currency

movements, RSWM is exposed to the foreign currency fluctuation risk. However, the company currently has

policy to hedge majority of its foreign exchange exposure through forward contracts; therefore this risk to that

extent is mitigated.

EXPANSIONS, NEW INITIATIVES AND CONCERNS

RSWM LIMITED

7 www.careratings.com

CARE

EQUITY

RESEARCH

The Indian Textile and Apparel (T&A) industry was estimated to be worth USD 55 billion in 2009-10 as per the

Office of the Textiles Commissioner. It has witnessed robust growth over the last two decades, especially in the period

after the abolition of the Quota regime on January 1, 2005, which led to free cross-border textile trade. India is

positioned as a key manufacturing destination with inexpensive labor, abundant cotton supplies and good designing

skills. Approximately 60% of the total T&A production is consumed domestically. India’s T&A exports grew from

USD 17.7 billion in FY06 to USD 22.4 billion in FY10, registering a CAGR of 6 per cent. T&A is one of the largest

and the most important sectors for the Indian economy in terms of output, foreign exchange earnings and

employment. It contributes approximately 14% to India’s industrial production, 4% to the country's GDP and 17% to

the country’s export earnings. It provides direct employment to over 35 million people and is the second-largest

employment provider after agriculture. The development of this sector has had a significant overall impact on the

economy. Indian T&A makes up approximately 4% of the global T&A market.

As an industry with economic importance, the textile industry has always been an important sector for the

government. The government has therefore introduced policies such as Technology Upgradation Fund Scheme,

Scheme for Integrated Textile Parks, National Textile Policy, with low excise duty and high import duty (to

discourage imports) to benefit the development of the textile sector. The largest sector within the textile industry is the

decentralized power-loom and knitting sector. The major sub-sectors that comprise the textile sector include the

cotton/Man-Made Fiber (MMF) textile mill industry, the MMF/filament yarn industry, the wool & woollen textile

industry, the sericulture and silk textile industry, handlooms, the jute & jute textiles industry and textiles exports. A

growing economy, rising disposable incomes and the growing aspirations of Indian consumers are expected to

continue driving growth in the Indian T&A industry.

Classification of the Indian Textile Industry based on fibres

Cotton: Cotton is a natural fibre that is harvested from a cotton plant and is one of the oldest forms of fibres under

cultivation as its history dates back over 7,000 years. It is a soft, fluffy staple fibre that grows in a protective capsule of a

cotton plant. Cotton is used to make a number of textile products like terrycloth for bath towels & robes that require

high absorbent qualities, denim jeans, corduroy and t-shirts. Cotton is also used in manufacturing bed linen. Cotton

may also be used by blending it with other fibres like rayon & synthetic products like polyester. World cotton

production in the cotton season 2010-11 has increased by 13% to 24.8 million tonnes on yoy basis. This rise in

production was driven by USA & India whereas China & Pakistan witnessed a decline in production. BT Cotton that

constitutes almost 88% of the total acreage under cotton saw harvests touching to 5.30 million tonnes in 2010-11 v/s

5.02 million tonnes in 2009-10, witnessing a growth of 6%.

SECTOR OUTLOOK

RSWM LIMITED

www.careratings.com 8

CARE

EQUITY

RESEARCH

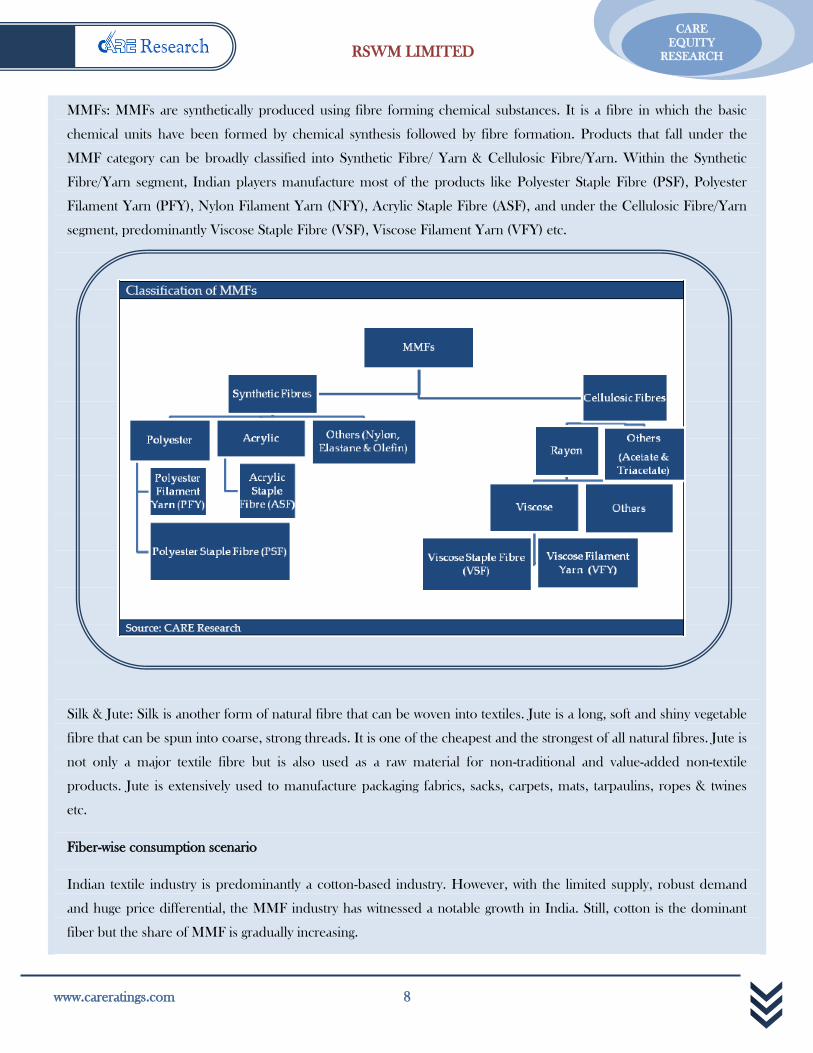

MMFs: MMFs are synthetically produced using fibre forming chemical substances. It is a fibre in which the basic

chemical units have been formed by chemical synthesis followed by fibre formation. Products that fall under the

MMF category can be broadly classified into Synthetic Fibre/ Yarn & Cellulosic Fibre/Yarn. Within the Synthetic

Fibre/Yarn segment, Indian players manufacture most of the products like Polyester Staple Fibre (PSF), Polyester

Filament Yarn (PFY), Nylon Filament Yarn (NFY), Acrylic Staple Fibre (ASF), and under the Cellulosic Fibre/Yarn

segment, predominantly Viscose Staple Fibre (VSF), Viscose Filament Yarn (VFY) etc.

Silk & Jute: Silk is another form of natural fibre that can be woven into textiles. Jute is a long, soft and shiny vegetable

fibre that can be spun into coarse, strong threads. It is one of the cheapest and the strongest of all natural fibres. Jute is

not only a major textile fibre but is also used as a raw material for non-traditional and value-added non-textile

products. Jute is extensively used to manufacture packaging fabrics, sacks, carpets, mats, tarpaulins, ropes & twines

etc.

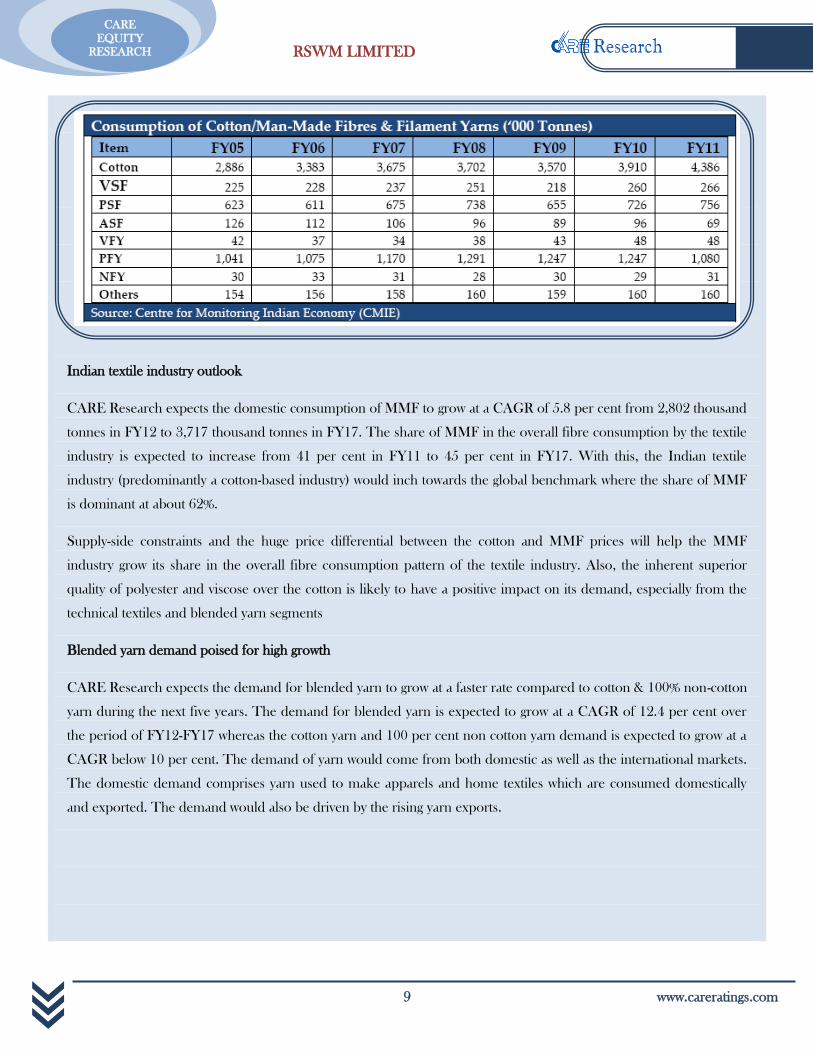

Fiber-wise consumption scenario

Indian textile industry is predominantly a cotton-based industry. However, with the limited supply, robust demand

and huge price differential, the MMF industry has witnessed a notable growth in India. Still, cotton is the dominant

fiber but the share of MMF is gradually increasing.

RSWM LIMITED

9 www.careratings.com

CARE

EQUITY

RESEARCH

Indian textile industry outlook

CARE Research expects the domestic consumption of MMF to grow at a CAGR of 5.8 per cent from 2,802 thousand

tonnes in FY12 to 3,717 thousand tonnes in FY17. The share of MMF in the overall fibre consumption by the textile

industry is expected to increase from 41 per cent in FY11 to 45 per cent in FY17. With this, the Indian textile

industry (predominantly a cotton-based industry) would inch towards the global benchmark where the share of MMF

is dominant at about 62%.

Supply-side constraints and the huge price differential between the cotton and MMF prices will help the MMF

industry grow its share in the overall fibre consumption pattern of the textile industry. Also, the inherent superior

quality of polyester and viscose over the cotton is likely to have a positive impact on its demand, especially from the

technical textiles and blended yarn segments

Blended yarn demand poised for high growth

CARE Research expects the demand for blended yarn to grow at a faster rate compared to cotton & 100% non-cotton

yarn during the next five years. The demand for blended yarn is expected to grow at a CAGR of 12.4 per cent over

the period of FY12-FY17 whereas the cotton yarn and 100 per cent non cotton yarn demand is expected to grow at a

CAGR below 10 per cent. The demand of yarn would come from both domestic as well as the international markets.

The domestic demand comprises yarn used to make apparels and home textiles which are consumed domestically

and exported. The demand would also be driven by the rising yarn exports.

RSWM LIMITED

www.careratings.com 10

CARE

EQUITY

RESEARCH

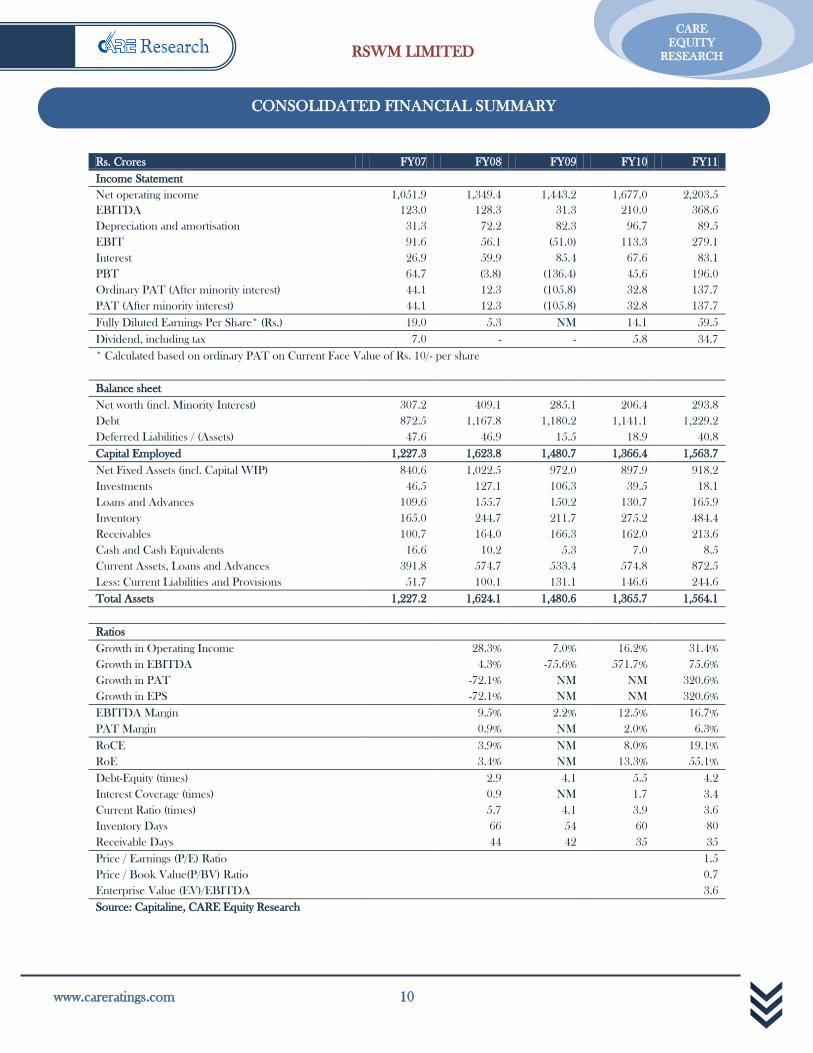

Rs. Crores FY07 FY08 FY09 FY10 FY11

Income Statement

Net operating income 1,051.9 1,349.4 1,443.2 1,677.0 2,203.5

EBITDA 123.0 128.3 31.3 210.0 368.6

Depreciation and amortisation 31.3 72.2 82.3 96.7 89.5

EBIT 91.6 56.1 (51.0) 113.3 279.1

Interest 26.9 59.9 85.4 67.6 83.1

PBT 64.7 (3.8) (136.4) 45.6 196.0

Ordinary PAT (After minority interest) 44.1 12.3 (105.8) 32.8 137.7

PAT (After minority interest) 44.1 12.3 (105.8) 32.8 137.7

Fully Diluted Earnings Per Share* (Rs.) 19.0 5.3 NM 14.1 59.5

Dividend, including tax 7.0 - - 5.8 34.7

* Calculated based on ordinary PAT on Current Face Value of Rs. 10/- per share

Balance sheet

Net worth (incl. Minority Interest) 307.2 409.1 285.1 206.4 293.8

Debt 872.5 1,167.8 1,180.2 1,141.1 1,229.2

Deferred Liabilities / (Assets) 47.6 46.9 15.5 18.9 40.8

Capital Employed 1,227.3 1,623.8 1,480.7 1,366.4 1,563.7

Net Fixed Assets (incl. Capital WIP) 840.6 1,022.5 972.0 897.9 918.2

Investments 46.5 127.1 106.3 39.5 18.1

Loans and Advances 109.6 155.7 150.2 130.7 165.9

Inventory 165.0 244.7 211.7 275.2 484.4

Receivables 100.7 164.0 166.3 162.0 213.6

Cash and Cash Equivalents 16.6 10.2 5.3 7.0 8.5

Current Assets, Loans and Advances 391.8 574.7 533.4 574.8 872.5

Less: Current Liabilities and Provisions 51.7 100.1 131.1 146.6 244.6

Total Assets 1,227.2 1,624.1 1,480.6 1,365.7 1,564.1

Ratios

Growth in Operating Income 28.3% 7.0% 16.2% 31.4%

Growth in EBITDA

4.3% -75.6% 571.7% 75.6%

Growth in PAT

-72.1% NM NM 320.6%

Growth in EPS -72.1% NM NM 320.6%

EBITDA Margin

9.5% 2.2% 12.5% 16.7%

PAT Margin 0.9% NM 2.0% 6.3%

RoCE 3.9% NM 8.0% 19.1%

RoE 3.4% NM 13.3% 55.1%

Debt-Equity (times) 2.9 4.1 5.5 4.2

Interest Coverage (times)

0.9 NM 1.7 3.4

Current Ratio (times)

5.7 4.1 3.9 3.6

Inventory Days

66 54 60 80

Receivable Days

44 42 35 35

Price / Earnings (P/E) Ratio 1.5

Price / Book Value(P/BV) Ratio

0.7

Enterprise Value (EV)/EBITDA 3.6

Source: Capitaline, CARE Equity Research

CONSOLIDATED FINANCIAL SUMMARY

RSWM LIMITED

11 www.careratings.com

CARE

EQUITY

RESEARCH

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there

exists no conflict of interest that can bias the grading recommendation of the company.

This report has been sponsored by the Bombay Stock Exchange (BSE).

DISCLAIMER

This BSE sponsored report is prepared by CARE Research, a division of Credit Analysis & REsearch

Limited [CARE]. CARE Research has taken utmost care to ensure accuracy and objectivity while developing

this report based on information available in public domain or from sources considered reliable. However,

neither the accuracy nor completeness of information contained in this report is guaranteed. Opinions

expressed herein are our current opinions as on the date of this report. Nothing in this report can be

construed as either investment or any other advice or any solicitation, whatsoever. The subscriber / user

assumes the entire risk of any use made of this report or data herein. CARE specifically states that it or any

of its divisions or employees do not have any financial liabilities whatsoever to the subscribers / users of this

report. This report is for personal information only of the authorised recipient in India only. This report or

part of it should not be reproduced or redistributed or communicated directly or indirectly in any form to

any other person or published or copied for any purpose.

“Credit Analysis and Research Limited proposes, subject to receipt of requisite approvals, market conditions

and other considerations, to make an initial public offer of its equity shares and has filed a draft red herring

prospectus (“DRHP”) with the Securities and Exchange Board of India (the “SEBI”). The DRHP is

available on the website of SEBI at www.sebi.gov.in as well as on the websites of the Book Running Lead

Managers at www.investmentbank.kotak.com, www.dspml.com, www.edelcap.com, www.icicisecurities.com,

www.idbicapital.com, and www.sbicaps.com. Investors should note that investment in equity shares involves a

high degree of risk and for details relating to the same, see the section titled “Risk Factors” of the DRHP.”

[“This press release is not for publication or distribution to persons in the United States, and is not an offer

for sale within the United States of any equity shares or any other security of Credit Analysis and Research

Limited. Securities of Credit Analysis and Research Limited, including its equity shares, may not be offered

or sold in the United States absent registration under U.S. securities laws or unless exempt from registration

under such laws.”]

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway,

Somaiya Hospital Road, Sion East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results

obtained from the use of information contained in this report and especially states that CARE (including all

divisions) has no financial liability whatsoever to the user of this product. This report is for the information of

the intended recipients only and no part of this report may be published or reproduced in any form or

manner without prior written permission of CARE Research.

DISCLAIMER

RSWM LIMITED

www.careratings.com 12

CARE

EQUITY

RESEARCH

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full-service rating company. CARE Research is involved

in preparing detailed industry research reports with 5-year demand and 2-year profitability outlook on the industry besides

providing comprehensive trend analysis and the current state of the industry. CARE Research currently offers reports on more

than 26 industries which are updated on a monthly/quarterly basis. Subscribers can access CARE Research reports online. CARE

Research also offers research that is customized to client requirements. Customized Research involves business analysis and

position in the market, financial analysis and market sizing etc.

HEAD OFFICE

Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai – 400 022

Tel: +91-22-67543456, Fax: +91-22-67543457.

NEW DELHI

3rd Floor, B -47, Inner Circle, Near Plaza Cinema, Connaught

Place, New Delhi - 110 001.

Tel: +91-11-23318701 / 23716199 / 23328524.

KOLKATA

3rd Floor, Prasad Chambers (Shagun Mall Building), 10A,

Shakespeare Sarani, Kolkata - 700 0717

Tel: +91-33-22831800 / 22831803 / 22808472.

CHENNAI

Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769,

Anna Salai, Chennai 600 002

Tel: +91-44-28497812/28490811

AHMEDABAD

32, Titanium, Prahaladnagar Corporate Road, Satellite,

Ahmedabad - 380 015

Tel: +91-79-40265656.

HYDERABAD

401, Ashoka Scintilla, 3-6-520, Himayat Nagar,

Hyderabad - 500 029

Tel: +91-040 40102030

BENGALURU

Unit No. 8, I floor, Commander's Place,

No. 6, Raja Ram Mohan Roy Road, (Opp. P F Office),

Richmond Circle, Bangalore - 560 025

Tel: +91-80-22117140

ABOUT US

Published on behalf of The Stock Exchange Investors' Protection Fund

Bombay Stock Exchange Ltd.

P J Towers, Dalal Street, Mumbai. Tel: 22721233/34 www.bseindia.com