california commercial real estate investor panel: office, retail and industrial executives discuss...

TRANSCRIPT

Timing Matters

DISTRESSED REAL ESTATE SUMMIT: CALIFORNIA

Fred CordovaFebruary 4, 2010

CRE Value & the 4th Dimension

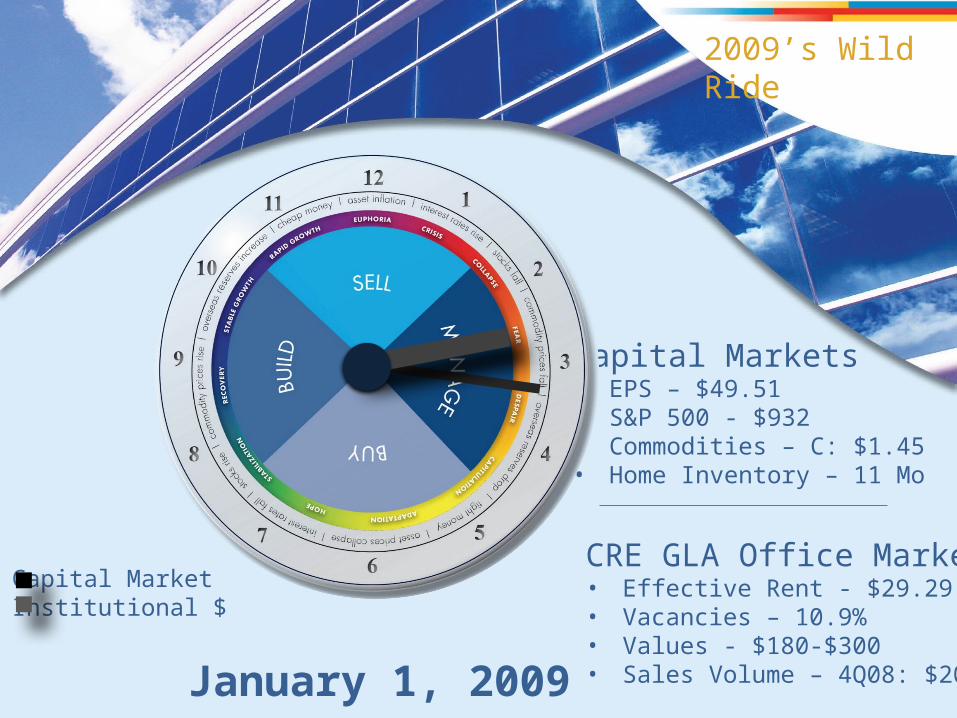

January 1, 2009

Capital Markets• EPS – $49.51• S&P 500 - $932• Commodities – C: $1.45• Home Inventory – 11 Mo

CRE GLA Office Market• Effective Rent - $29.29• Vacancies – 10.9%• Values - $180-$300• Sales Volume – 4Q08: $200m

2009’s Wild Ride

Capital MarketInstitutional $

January 1, 2010

Capital Markets• EPS - $56.21/ F: $74.98• S&P 500 - $1126 (15.25 X F)• Commodities – C: $3.40• Home Inventory - TBD

CRE GLA Office Market• Effective rents - $26.41• Vacancies – 13.5%• Values - $180-$300 psf• Sales Volume – Q4 $200m

2009’s Wild Ride

Capital MarketInstitutional $Lender / ServicerForeign / Private $

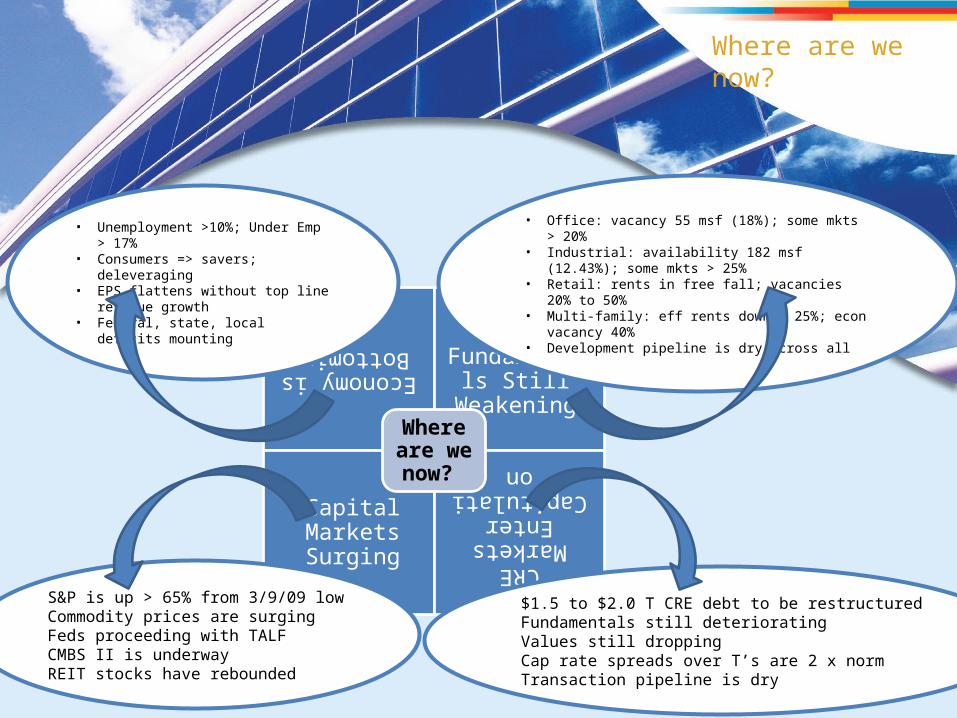

Where are we now?

Economy is

Bottoming GLA Fundamentals

Still Weakening

Capital Markets Surging

CRE Markets

Enter Capitulati

on

Where are we now?

S&P is up > 65% from 3/9/09 lowCommodity prices are surgingFeds proceeding with TALFCMBS II is underwayREIT stocks have rebounded

$1.5 to $2.0 T CRE debt to be restructuredFundamentals still deterioratingValues still dropping Cap rate spreads over T’s are 2 x normTransaction pipeline is dry

• Unemployment >10%; Under Emp > 17%

• Consumers => savers; deleveraging• EPS flattens without top line revenue

growth• Federal, state, local deficits mounting

• Office: vacancy 55 msf (18%); some mkts > 20%• Industrial: availability 182 msf (12.43%); some mkts >

25%• Retail: rents in free fall; vacancies 20% to 50%• Multi-family: eff rents down > 25%; econ vacancy 40%• Development pipeline is dry across all

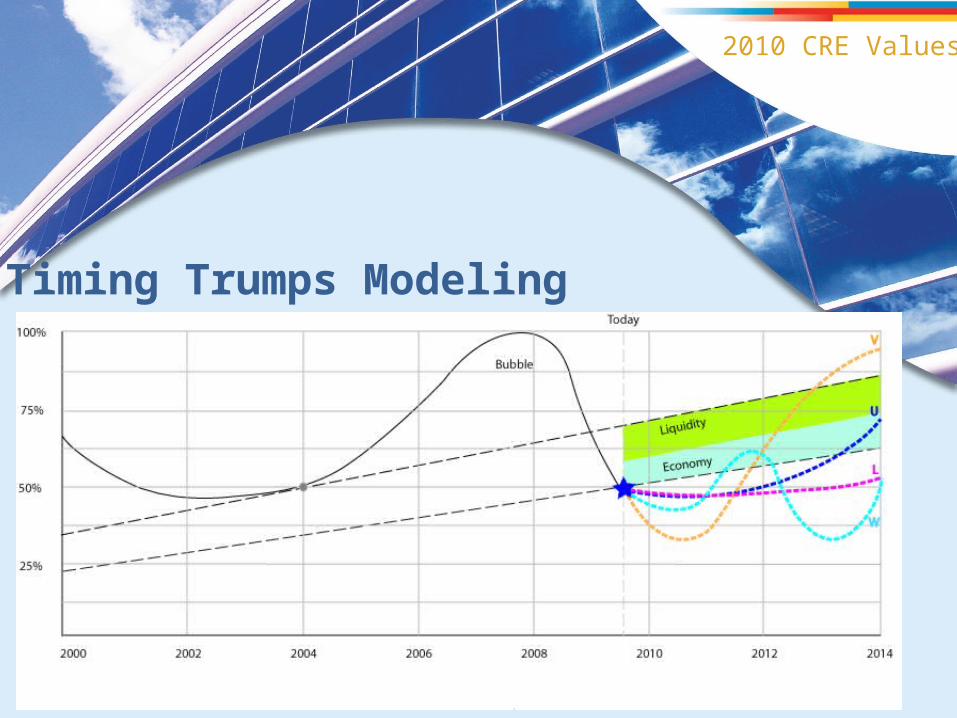

2010 CRE Values

Timing Trumps Modeling

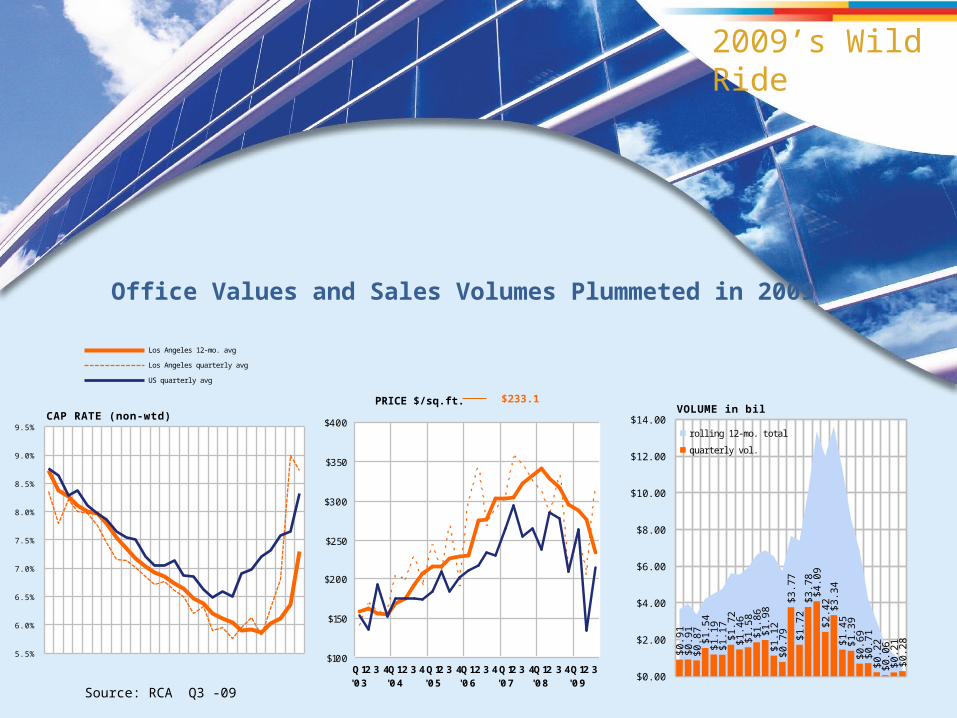

Office Values and Sales Volumes Plummeted in 2009

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

Los Angeles 12-mo. avg

Los Angeles quarterly avg

US quarterly avg

CAP RATE (non-wtd)

$100

$150

$200

$250

$300

$350

$400

Q1'03

2 3 4Q1'04

2 3 4Q1'05

2 3 4Q1'06

2 3 4Q1'07

2 3 4Q1'08

2 3 4Q1'09

2 3

PRICE $/sq.ft. $233.1

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$0.9

1$0

.91

$0.8

7$1

.54

$1.1

9$1

.17

$1.7

2$1

.46

$1.5

8$1

.86

$1.9

8$1

.12

$0.7

9$3

.77

$1.7

2$3

.78

$4.0

9$2

.42 $3

.34

$1.4

5$1

.39

$0.6

9$0

.71

$0.2

2$0

.06

$0.2

1$0

.28

rolling 12-mo. total

quarterly vol.

VOLUME in bil

Source: RCA Q3 -09

2009’s Wild Ride

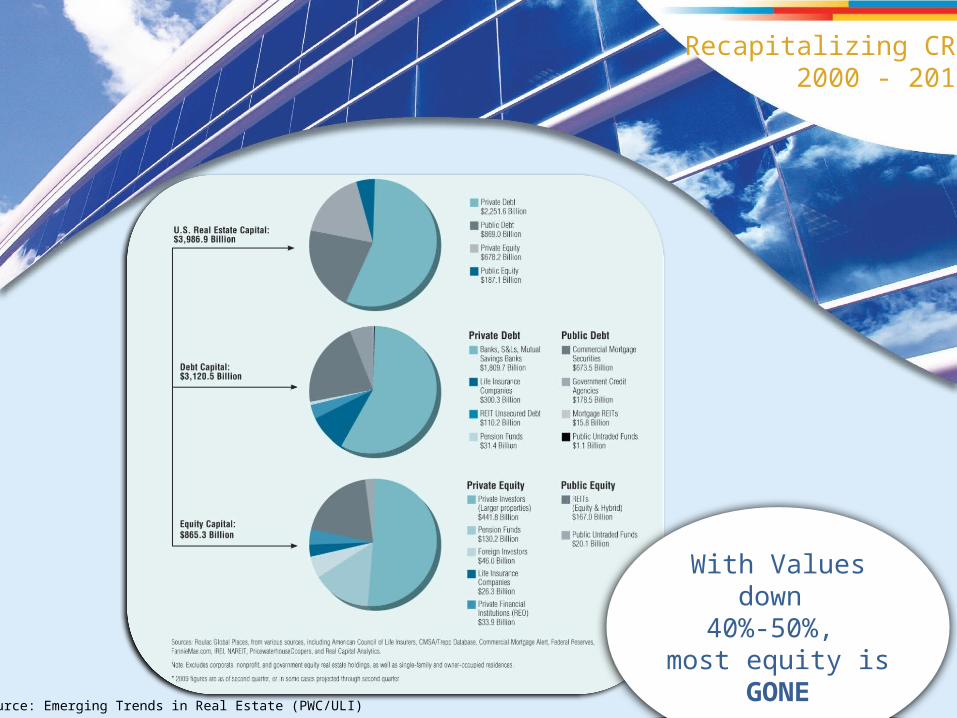

Recapitalizing CRE2000 - 2010

With Values down 40%-50%,

most equity is GONE

Source: Emerging Trends in Real Estate (PWC/ULI)

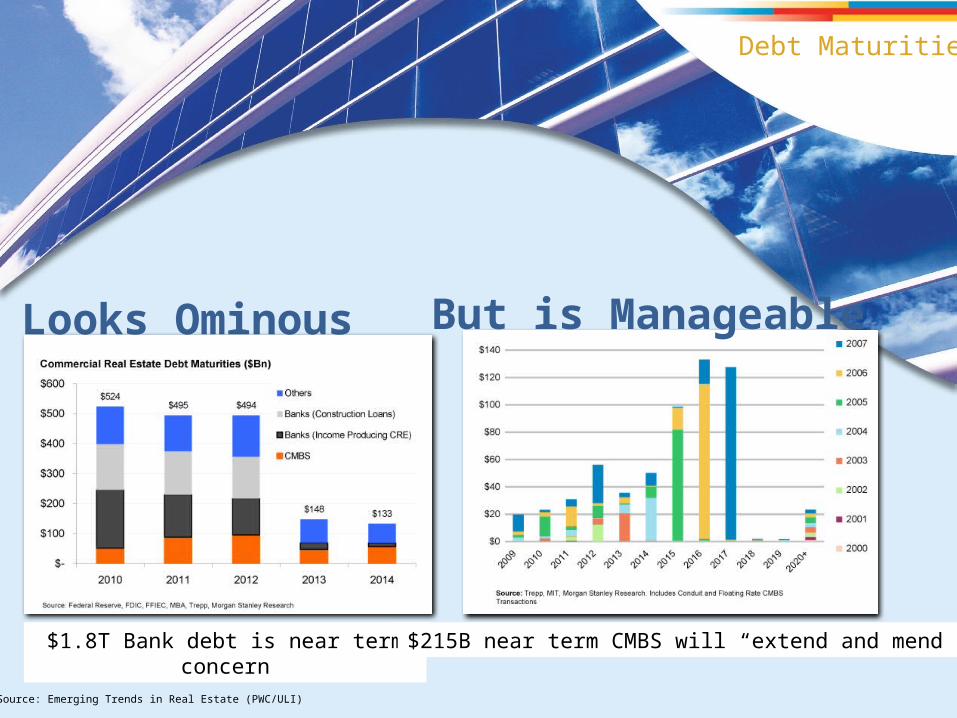

Looks Ominous

$1.8T Bank debt is near term concern $215B near term CMBS will “extend and mend”

Source: Emerging Trends in Real Estate (PWC/ULI)

Debt Maturities

But is Manageable

Is a Myth

The Tsunami

Timing Matters

CRE Value & the 4th Dimension