beyond the horizon: what’s next?

TRANSCRIPT

1

Beyond the Horizon: What’s Next?Session PH6, March 5, 2018

Don Calcagno, President, Advocate Physician Partners

2

Don Calcagno

Has no real or apparent conflicts of interest to report.

Conflict of Interest

3

Agenda

Advocate Overview

Healthcare Value Chain

Understand and Optimize Care

Disruption

4

Learning Objectives

• Describe the sustainability of a changing business model to accelerate the population health movement

• Explore advanced and disruptive technologies and their role in enabling innovative care delivery models

• Illustrate that population health will require understanding and optimization of a personalized longitudinal plan inclusive of clinical, behavioral, socioeconomic, and other factors

55

Advocate and APP Overview

6

Advocate Health Care$6.4 billion of revenue1.6 million unique patients1,007,000 value based lives35,000 associates

Physicians/Ambulatory1,400 employed + 400 APCsOver 6,000 physicians in 450+ sites of care

Hospitals (11)4 teaching |5 level 1 trauma centers1 children's |1 critical access | 2 LTACH

Post-acuteHome health, hospice, SNF and palliative care

7

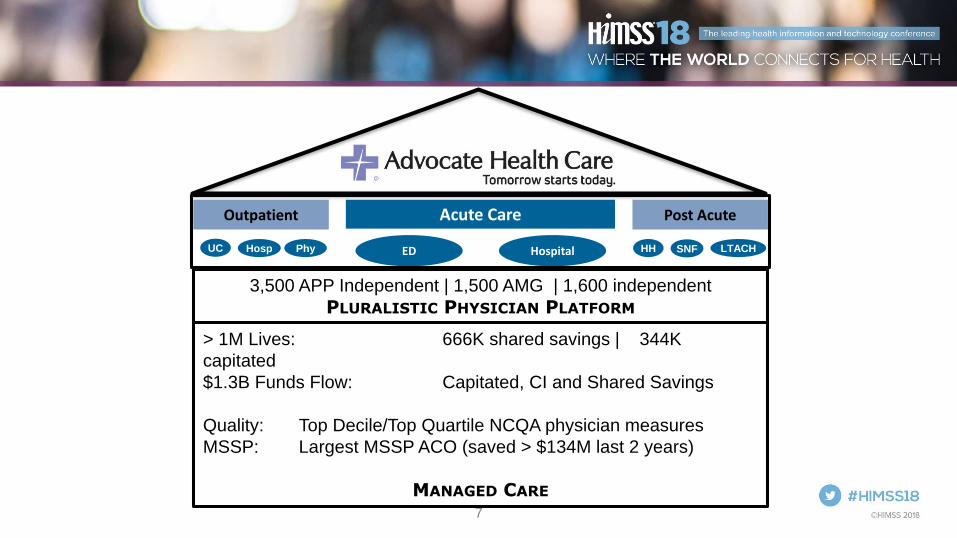

Post AcuteAcute CareOutpatient

ED Hospital HH SNF LTACHUC Hosp Phy

3,500 APP Independent | 1,500 AMG | 1,600 independent

PLURALISTIC PHYSICIAN PLATFORM

> 1M Lives: 666K shared savings | 344K

capitated

$1.3B Funds Flow: Capitated, CI and Shared Savings

Quality: Top Decile/Top Quartile NCQA physician measures

MSSP: Largest MSSP ACO (saved > $134M last 2 years)

MANAGED CARE

88

Performance Highlights

• TOP DECILE level based on available NCQA benchmarks on 28 CI MEASURES

• TOP QUARTILE on 7 CI MEASURES

http://www.advocatehealth.com/ValueReport

99

Decreasing Variation across Populations%Patients who had a HbA1c Performed Diabetes: HbA1c >=9

1010

-0.6%

1.5%

1.1%

3.1%

2.4% 2.4%

3.5%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2013 2014 2015 2016

AdvocateCare® PerformanceNational Medical

Services Inflation*

%Change RBC

Medical Expense

1111

MSSP SavingsTop 3 2015Top 2 2016

2015 2016

Beneficiaries 145,365 139,617

Expenditure $11,229 $10,995

Quality Score 94.2% 97.28%

Total Savings $73 M $61 M

Earned Savings $34 M $29 M

1212

Value

13

14

Health Care Value Chain

Provider

Payer &

Product

Distributor

Employer

Consumer

15

Payor-Provider Relationships

Operational

Excellence

Partnership

Transactional

Provider

Payer &

ProductDistributor

Employer

Consumer

16

Who bears

financial risk?

Who’s capable of

bearing risk?

Provider

Payer &

ProductDistributor

Employer

Consumer

17

IDN Financial ForecastProvider

Payer &

ProductDistributor

Employer

Consumer

18

Changing Paradigms

FROM... TO...

Silo care management Enterprise care management

Episodes of care Coordination of care

Discharges Transitions

Utilization managementRight care at the right place at the

right time

Caring for the sick Keeping people well

Production (volume) Performance (value)

Provider

Payer &

ProductDistributor

Employer

Consumer

19

Provider

Payer &

Product

Distributor

Employer

Consumer

20

Employers

Provider

Payer &

ProductDistributor

Employer

Consumer

21

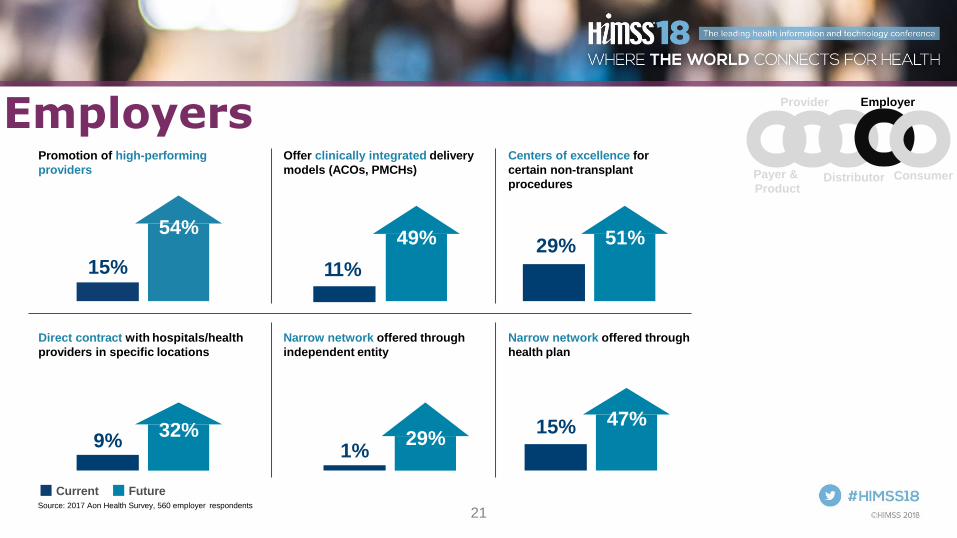

EmployersPromotion of high-performing

providers

Offer clinically integrated delivery

models (ACOs, PMCHs)

Centers of excellence for

certain non-transplant

procedures

Direct contract with hospitals/health

providers in specific locations

Narrow network offered through

independent entity

Narrow network offered through

health plan

9%32%

1%29%

15% 47%

15%

54%

11%

51%29%49%

Current FutureSource: 2017 Aon Health Survey, 560 employer respondents

Provider

Payer &

ProductDistributor

Employer

Consumer

22

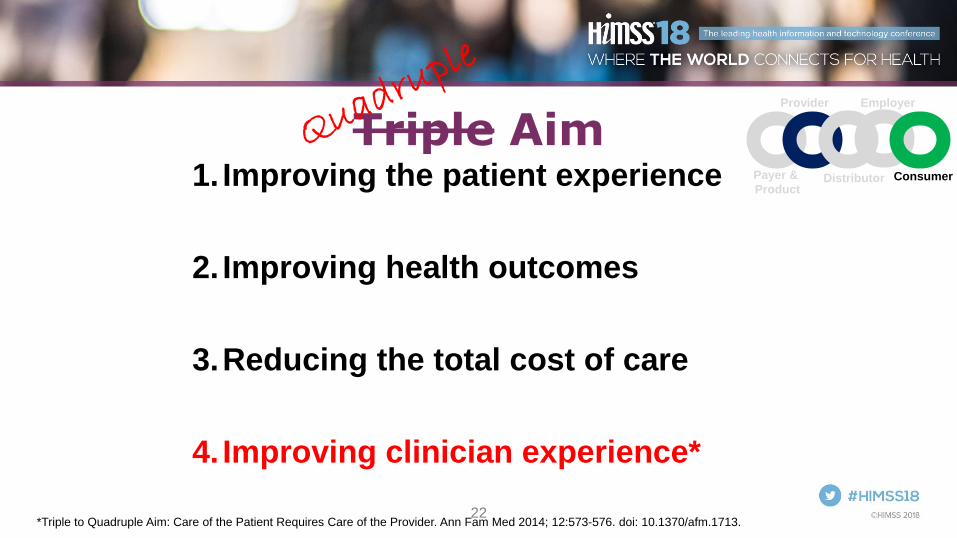

Triple Aim1. Improving the patient experience

2. Improving health outcomes

3.Reducing the total cost of care

4. Improving clinician experience*

*Triple to Quadruple Aim: Care of the Patient Requires Care of the Provider. Ann Fam Med 2014; 12:573-576. doi: 10.1370/afm.1713.

Provider

Payer &

ProductDistributor

Employer

Consumer

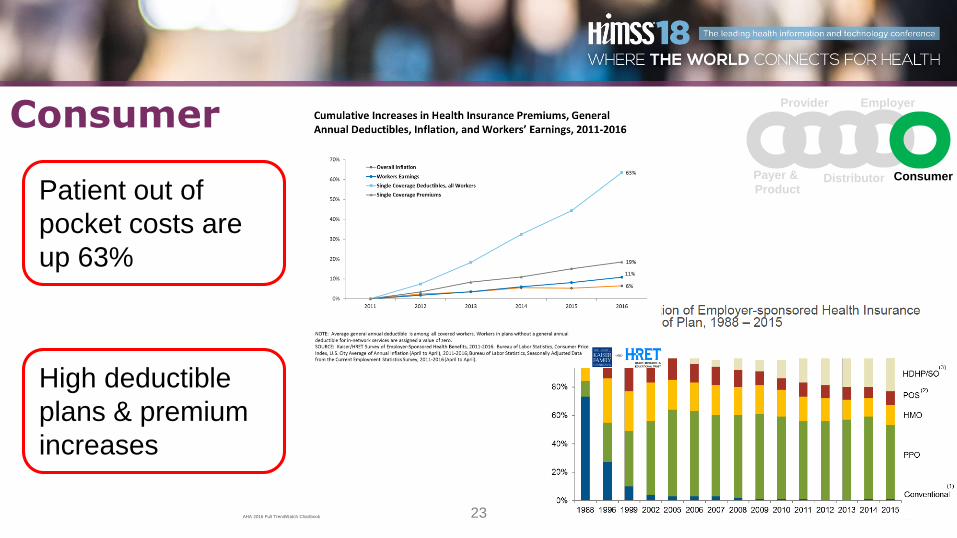

23AHA 2016 Full TrendWatch Chartbook

Patient out of

pocket costs are

up 63%

High deductible

plans & premium

increases

ConsumerProvider

Payer &

ProductDistributor

Employer

Consumer

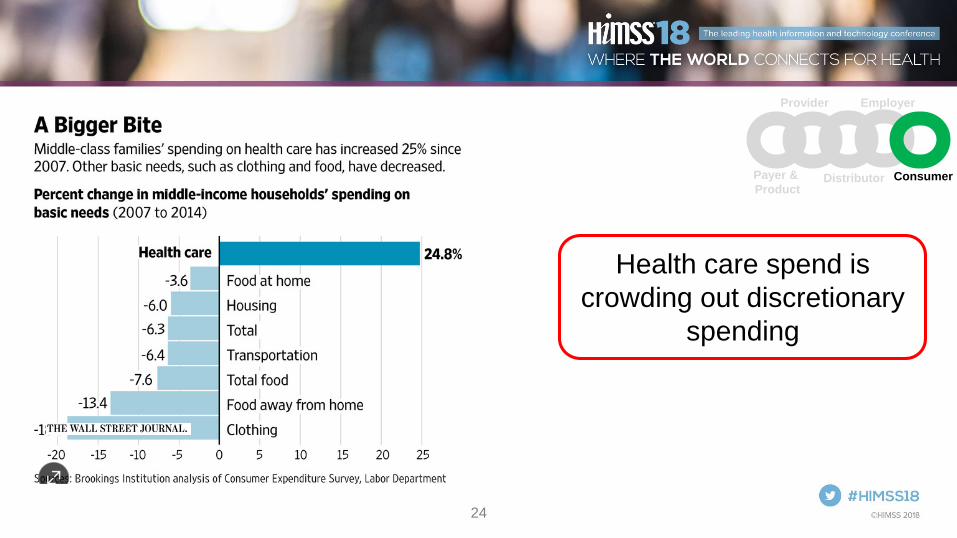

24

Health care spend is

crowding out discretionary

spending

Provider

Payer &

ProductDistributor

Employer

Consumer

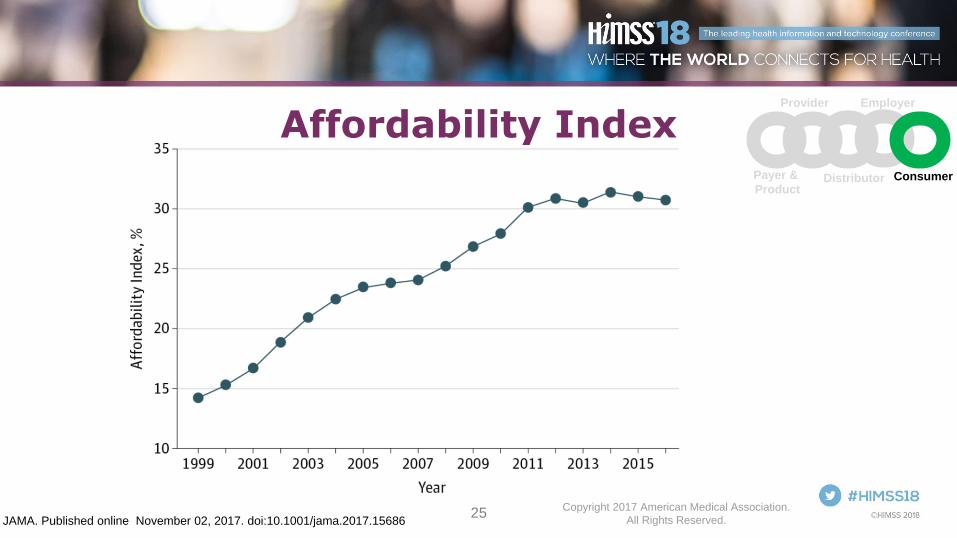

25Copyright 2017 American Medical Association.

All Rights Reserved.JAMA. Published online November 02, 2017. doi:10.1001/jama.2017.15686

Affordability IndexProvider

Payer &

ProductDistributor

Employer

Consumer

26

Prisoner’s Dilemma

The prisoner's dilemma is a standard example

of two completely "rational" individuals might not

cooperate, even if it appears that it is in their

best interests to do so.

2727

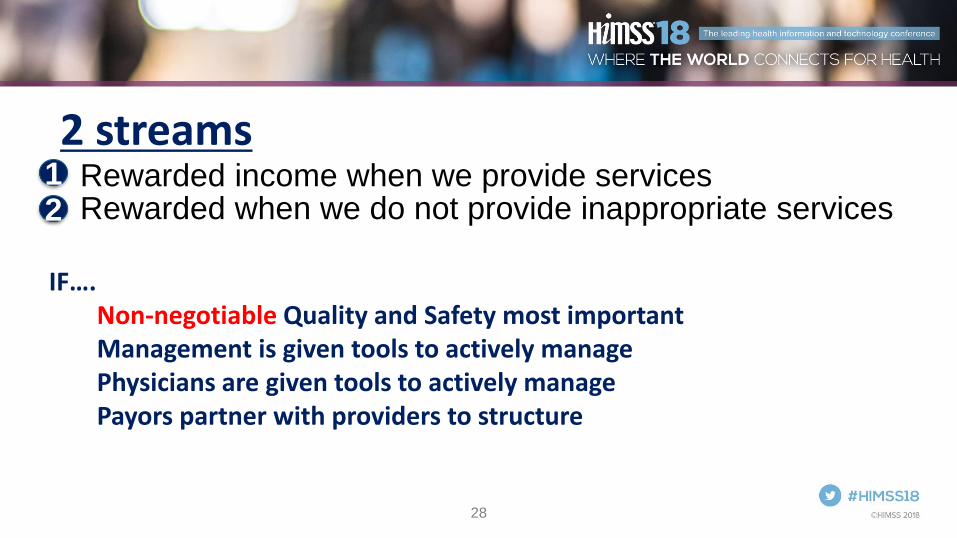

What is a providers business model?

28

2 streams1 Rewarded income when we provide services 2 Rewarded when we do not provide inappropriate services

IF….Non-negotiable Quality and Safety most importantManagement is given tools to actively managePhysicians are given tools to actively managePayors partner with providers to structure

29

30

2 DRG/Case Rate

1

3 Shared Savings

4 Fee for Service

Global

Capitation

Lot’s of forms of Financial Risk

31

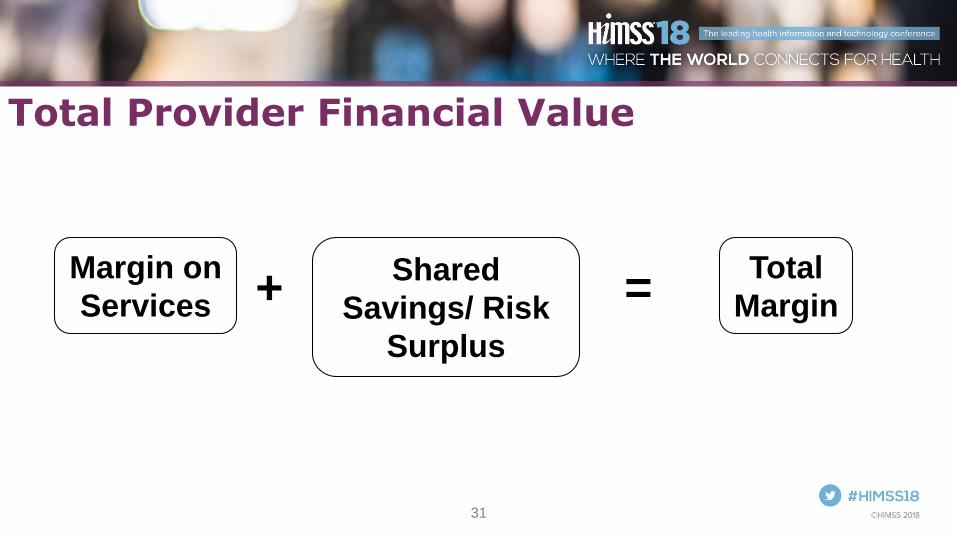

Total Provider Financial Value

Margin on

ServicesShared

Savings/ Risk

Surplus

Total

Margin+ =

3232

Understand and Optimize Care

33

True North

Leading Indicators Drivers

ACI Total Expense PMPM

$x

$x PMPM

ED Expense

$x

$x PMPM

ED Visits/ 1,000

$x

$x PMPM

Low Acuity ED Visits

$x

$x PMPM

Hospitalizations Expense

$x

$x PMPM

Hospitalizations/ 1,000

$x

$x PMPM

Chronic Disease Hospitalizations

$x

$x PMPM

SNF Expense

$x

$x PMPM

Discharge to SNF/ 1,000

Discharge to PAN SNF

Program %

Access

Acute Care

Post Acute

Analysis Framework

34

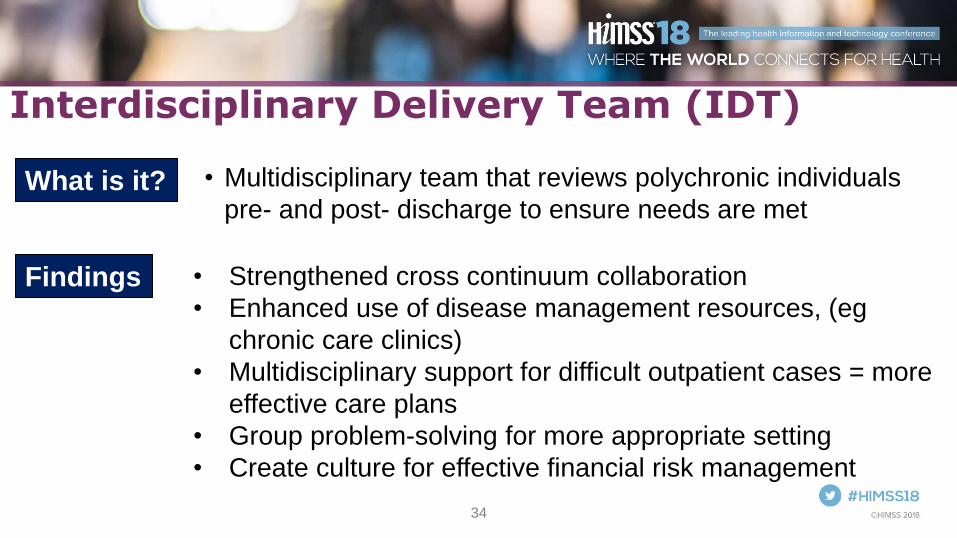

Interdisciplinary Delivery Team (IDT)

• Multidisciplinary team that reviews polychronic individuals

pre- and post- discharge to ensure needs are metWhat is it?

Findings • Strengthened cross continuum collaboration

• Enhanced use of disease management resources, (eg

chronic care clinics)

• Multidisciplinary support for difficult outpatient cases = more

effective care plans

• Group problem-solving for more appropriate setting

• Create culture for effective financial risk management

35

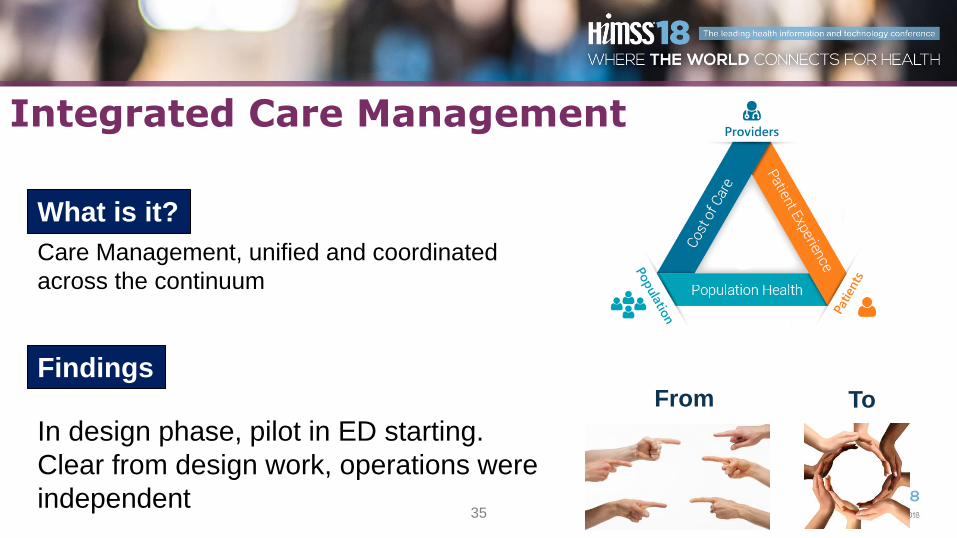

Integrated Care Management

Care Management, unified and coordinated

across the continuum

What is it?

Findings

In design phase, pilot in ED starting.

Clear from design work, operations were

independent

From To

3636

Disruption

37

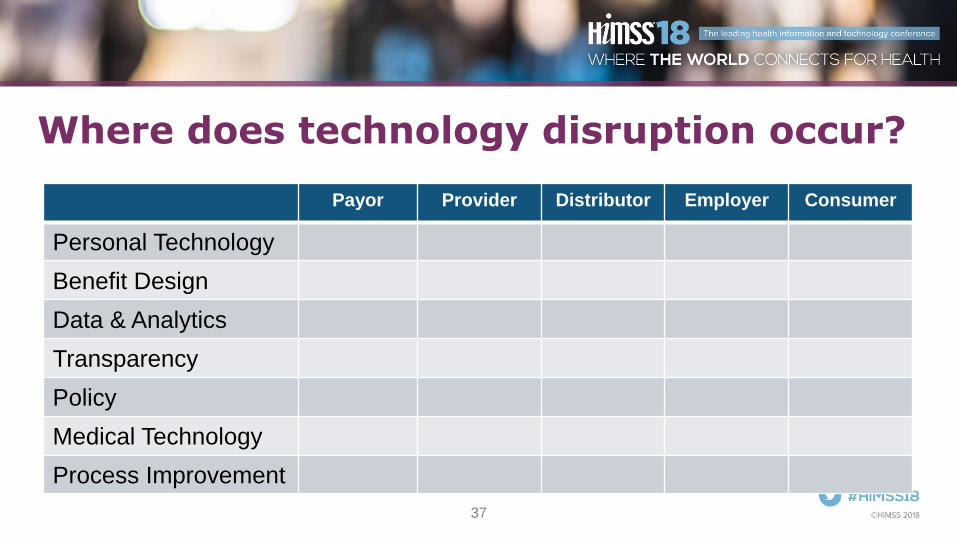

Where does technology disruption occur?

Payor Provider Distributor Employer Consumer

Personal Technology

Benefit Design

Data & Analytics

Transparency

Policy

Medical Technology

Process Improvement

38

Connected Data Sources

Immunizations MasterPerson Indexes

Pharmacy Benefit

Management

ElectronicHealth Records

Registrationand Billing

Labs

Claimsand Payers

39

850,000+

5,000+

11

14,670

+

39

Social Determinants of Health

40

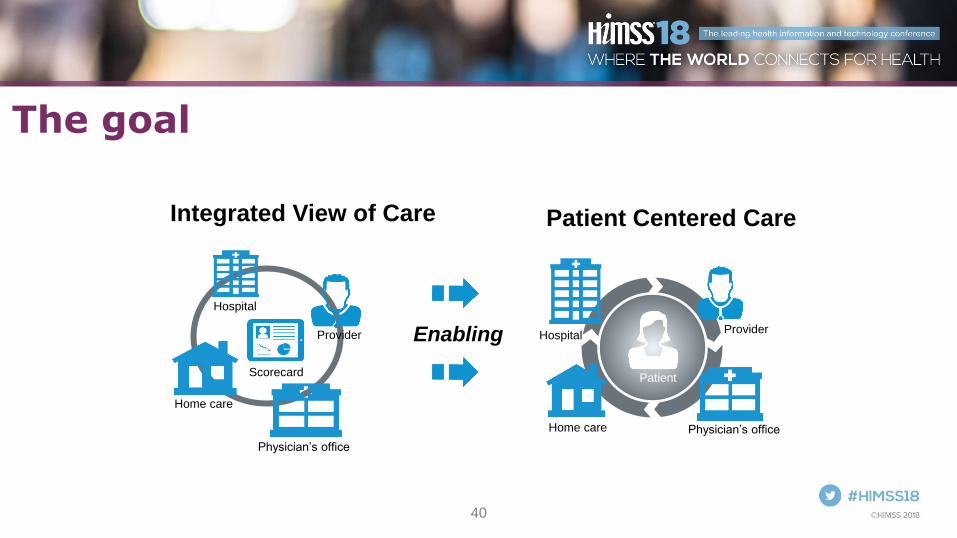

Physician’s office

Provider

Home care

Patient

Patient Centered Care

HospitalEnabling

Hospital

Physician’s office

Provider

Scorecard

Home care

Integrated View of Care

The goal

41

Works in progress• Patient Engagement phone app

• Payor analytics systems

• Asthma phone app

• Network utilization

• Tele-medicine

• Population Health platform

• Mobile eye exams

Lessons• Members/Patients

– Engage how they want to

– Bandwidth for apps/videos

– Follow-through

• Some technology disrupts care continuum

• Administrative burden

• Systematic vs individual solutions

What’s Next for APP?

42

Questions?

• Please complete online session evaluation