beyond markowitz - regionsbankbeyond markowitz: a comprehensive wealth allocation framework for...

TRANSCRIPT

VOLUME 8 NUMBER 1 SPRING 2005

Beyond Markowitz: A Comprehensive WealthAllocation Framework for Individual InvestorsASHVIN B. CHHABRA

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

1. DISCREPANCIES BETWEENTHEORY AND REALITY

The principles of Modern PortfolioTheory, as outlined in Markowitz’sfamous 1952 paper (Markowitz[1952a]) speak clearly and unam-

biguously to the benefits of portfolio diversi-fication. There is an optimum way to create aportfolio by combining different asset classes.This construction depends crucially on themarket risk and return of each asset class andon the correlations between different assetclasses. These optimal portfolios, when mappedon the risk-return plane, form a curve knownas the efficient frontier. Each investor, basedon his personal utility function, finds the appro-priate point on this line, which then prescribesan optimum allocation between different assetclasses such as stocks, bonds, and cash.

It should be intuitively obvious that, inorder to achieve a truly diversified portfolio,one must also diversify within each asset class.For example, equity portfolios should be com-posed of a large number of minimally corre-lated stocks, bonds should be diversified acrossboth maturities and credit ratings. Accordingto Modern Portfolio Theory, diversificationminimizes non-systematic risk and diversifi-cation combined with the use of a utility func-tion provides the investor with the rightbalance between risk and reward. The inter-ested reader may refer to Appendix A fordetails on how the Markowitz framework is

implemented in practice. More ambitiousapproaches such as Merton’s [1992] pioneeringwork on dynamic asset allocation, which in-corporates multi-period investor consump-tion, unfortunately have not found widespreadacceptance in the personal finance world.

However, in sharp contrast to these rec-ommendations, a vast majority of investors in theU.S. and in countries around the world are notwell diversified. This neglect of diversificationis also seen across all client segments, includingaffluent clients who have access to financial advi-sors, financially sophisticated investors, and par-ticipants of employer-sponsored retirement plans(Goetzmann and Kumar [2003]; Kennickell[2003]; Polkovinchenko [2003]).

What does lack of diversification resultin? The dangers of undiversified portfolioshave been indelibly etched in the minds ofmany thousands of investors who participatedin the Internet bubble with “irrational exu-berance” (Greenspan [1996]; Shiller [2001]).Many of their investments became worthless,as their technology-heavy portfolios sustainedheavy losses and never recovered.

Yet there is a remarkable group of people,a minority of the general population but a sig-nificant majority of the affluent, who havebecome wealthy over the years by defyingmarket diversification. Ironically, many of themwould not have become so wealthy had theyfollowed a conventional diversified approach.

Some examples of such successful “undi-versified” strategies have been:

Beyond Markowitz: A Comprehensive WealthAllocation Framework for Individual InvestorsASHVIN B. CHHABRA

ASHVIN B. CHHABRA

is first vice president andhead of Wealth Manage-ment Strategies and Ana-lytics, Global PrivateClient, Merrill [email protected]

• Investors who assumed a mortgage to invest insingle-property real estate and saw the value of theirproperty double in a few years. This has often meanta severalfold return on their down payment, whichof course corresponds to a highly leveraged invest-ment. In contrast, investors whose property valuedecreased saw their down payment vanish.

• Corporate executives who accumulated low-basisstock and stock options and did not diversify, whilethe value of their company stock and options dou-bled and redoubled. In contrast, others who usedthe same strategy saw their company stock fallsharply and their options expire worthless.

• Individuals who invested most of their human andfinancial capital and started a small business thatbecame successful over time. During this periodthey continued to reinvest in their business intensi-fying their risk, until they finally cashed out in asingle buyout transaction. In contrast, nearly 33%of small businesses fail within four years of startingup (Headd [2003]).

It is important to emphasize that, when we look atthe wealthy, we clearly suffer from what we call “survivorbias,” i.e., we are only looking at the winners. On theother hand, one cannot dismiss most of the wealthy (num-bering 10 million or more in the U.S. alone) as mere win-ners of “lotteries” or of “excessively risky strategies.”

Three Important Questions

Probing deeper, we seek to understand three issues:

1. Did these “now affluent” individuals take unneces-sary, foolhardy, or excessive risks to achieve wealth?

2. When people ignore Modern Portfolio Theory’sadvice on diversification, are they behaving irra-tionally (as MPT would suppose) or is there a fun-damental flaw in the theory itself?

3. Is there a framework that provides an optimum wayof assuming risk, while still protecting oneself, inorder to achieve or significantly increase affluence?If so, is this framework consistent with Modern Port-folio Theory or is it at odds with it?

The aim of this article is to provide answers to thequestions posed above. We develop a comprehensive riskallocation framework by expanding the traditionalMarkowitz (market risk) framework to include safety (per-

sonal risk) and aspirational components. In section 6, thisapproach is illustrated through an idealized example usinga stock index, a call, and a put. In section 7, we discussbenchmarks and asset classification in the context of riskallocation. Subsequently, in section 8, we analyze a morecomplex real world example. Finally, several differentaspects of the framework are discussed in section 9, notablyhow real estate, stock options, human capital, and annu-ities naturally fit into this expanded framework. AppendixC provides an approach to evaluate investor risk prefer-ence based on combining both objective and subjectivemeasures.

2. A CHANGING REALITY

The three questions stated earlier are not merelyacademic questions. Changes in the structure of pensionplans, life expectancy, and the globalization of financialmarkets have increasingly thrust upon individuals greaterresponsibility for their financial future. The ability to investappropriately to meet their individual requirements willbe the single most important determinant of their abilityto maintain their current standard of living during theirretirement years and of financial success.

Let us discuss some of the major changes.

1. The movement of corporations from defined ben-efit plans to defined contribution plans has effectivelytransferred the risk of (the future underperformance of) cap-ital markets to the individual. Individuals now are leftwith lump sums of liquid assets as opposed to stablepensions. The well-being of people in their retire-ment is critically dependent on the correct invest-ment of their assets. Should investors follow theprinciples of Modern Portfolio Theory?

2. Increases in average life expectancy require a greateramount of savings in order to maintain a standardof living through retirement. Furthermore, lifeexpectancy is likely to continue to increase duringour lifetimes. Defined benefit pension streams wereguaranteed to continue throughout the beneficia-ry’s lifetime. Defined contribution lump sums, incontrast, will have to be stretched further throughappropriate investment choices made by the bene-ficiary. What does Modern Portfolio Theory tell usabout how best to allocate an individual’s assets toprovide for the extended lifespan?

3. Different financial markets and fund managers nowdisplay a greater degree of correlation than what

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

historical data would suggest. This means that port-folios thought to be diversified in the past may notbe so today. Does that minimize the benefits of diver-sification? What effect does that have on risk-returnexpectations for diversified portfolios?

4. Constant innovation in financial products, as well asenhanced access to more sophisticated financial instru-ments such as options, hedge funds, and structuredproducts, present compelling, yet more complex risk-reward opportunities to investors. What does ModernPortfolio Theory tell us about their choice and allo-cation to an individual’s personal portfolio?

3. THE JOURNEY MATTERS: INDIVIDUAL INVESTORS AND MARKETSON THE AVERAGE

The needs of individual investors impose differentconsiderations than simply the averages of the market(Brunel [2003]). The emphasis of the efficient frontierapproach using market risks, without consideration forits effect on the portfolio holder, is fundamentally unsat-isfactory. Personal utility functions are hard to determineand have well-documented flaws (Allais [1953]; Kah-neman and Tversky [1979]).

In addition, the efficient frontier approach optimizesfor a portfolio’s outcome at the end of a single predeter-mined time period. There are at least two problems withthis.

• Investors need to maintain their lifestyle and meettheir financial obligations during this time periodregardless of market conditions.

• We do not always know at the outset what the spec-ified time period should be. For example, we needto provide for retirement without knowing exactlyhow long we will live.

In the standard framework, risk is defined by thevolatility of the underlying portfolio. Volatility is a one-dimensional measure of market risk which tracks howmuch the price of the portfolio fluctuates, on the average,over a specified period of time. For example, a diversifiedindex consisting of large-cap stocks, such as the S&P 500,has a daily volatility (standard deviation) of about 1%.Within the confines of the mean-variance framework, thisnumber indicates that we should expect a daily movegreater than 2% only about once a month. A 3% movewould happen once every three years, while the market

crash of October 19, 1987, where the index fell by 20.47%should happen only once in a billion years. However, suchcrashes (of varying magnitude) have happened many timesin the past century. Clearly, the mean-variance frameworkand the associated volatility number do not capture thetrue frequency of short-term market crashes.

The same measure viewed over a longer time frame,such as a year, does much better. The historical (1926-2003) annual volatility of the S&P 500 is about 21.9%and the average annual return is about 12.5%. This pro-vides a much better estimate of the movements of theindex that an investor can expect over a year. For example,the investor should expect a two standard deviation eventor a 31.3% loss on a single portfolio only once every 20years. This has occurred only twice in the last 75 years andon both occasions in the 1930s, once in 1931 and then,unexpectedly, six years later in 1937. This last observa-tion highlights another important point: the assumptionthat the market returns have no memory breaks downoften, due in part to the impact of economic cycles. Thesecycles create bull and bear markets that consist of closelyspaced or successive years of economic feast or famine.

The consequences on the individual investor of suchlarge deviations or several consecutive years of negativereturns may range from mere annoyance to catastrophe.In other words, the market understands risks only at anaggregate level, not at an individual level.

Personal risk is thus an additional dimension thatmust be factored in to construct appropriate portfoliosfor individuals. This consideration also makes the problempath-dependent. Clearly the journey matters. All pathsin Exhibit 1 lead to success, but the one that dips belowthe client’s minimum acceptable wealth level is fraughtwith danger. A stream may have an average depth of fivefeet, but a traveler wading through it will not make it tothe other side if its mid-point is 10 feet deep. Similarly,an overly volatile investing strategy may sink an investorbefore she gets to reap its anticipated rewards.

It is worthwhile to point out that most extensions ofModern Portfolio Theory have been directed at improvingthe description of market risks (Fabozzi et al. [2002]). Thesame emphasis has not been placed on understanding theissue of personal risks, although Roy [1952] placed par-ticular emphasis on “safety first” within the context ofportfolio diversification. Innovations in the marketplaceover the past few decades, leading to instruments likeoptions, convertible bonds, and principal protected funds,should allow for the creation of portfolios that are moresuitable to different individual risk tolerances.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

What Are Some of the Components of Personal Risk?

• Cash flow: The investor’s current and foreseeable cashflow is at least as important as his asset allocation. Ishe a net-saver or net-spender on an annual basis?Will he need to withdraw money at any juncture oron a regular basis? If so, will it be a fixed or variablesum? For example, withdrawing a fixed amount ofmoney every year can have adverse consequences inthe context of a declining market.

• Lifecycle stage: Someone at the peak of her earningcapacity may be able to take on more risk thansomeone approaching retirement. On the other hand,a wealthy person in an advanced stage of retirementseeking to achieve an ambitious legacy goal may wantto take on more risk with a portion of the portfolio.

• Ability to weather shortfalls: How does one protectagainst outliving one’s assets, e.g., living 10-15 yearslonger than life expectancy? What is an effectivesolution to an eventual decreasing gap between theminimum acceptable wealth level and the individ-ual’s current wealth?

• Event risk: The investor needs to understand andprotect, if possible, against a variety of singular eventssuch as loss of job, major health problems, disability,the need to support an additional family member,lawsuits, etc. Macro events, such as market crashesor country defaults due to political or economicreasons, also present real threats to maintaining per-sonal wealth (Zaharoff [2004]).

In order to understand how to suc-cessfully incorporate these diverse riskfactors into an individual’s financialstrategy, it is instructive to consider howwealth is measured on both absolute andrelative scales.

4. THE WEALTH OF AMERICA: WHO IS WEALTHY?

Individual investors consider theirsuccess and wealth not just in absoluteterms, but also relative to their peers.Therefore, it is instructive to consider thewealth of America and how it is distrib-uted among its population.

This distribution of wealth in Amer-ica (Exhibit 2) is fascinating in manyrespects. As is well known, wealth isunevenly distributed. If we divide the total

wealth of American households into three equal parts,we find that each third is approximately shared among90%, 9%, and 1% of the households respectively. Theshape of the wealth distribution is far from the usual sym-metrical bell curve. Starting from the far left of the curve,approximately 7 million households are in debt. Thereare another 33 million households with almost no networth. A startling fact: one in three American householdsis a single event away from bankruptcy. An importantquestion is: What should be the financial strategy for thesehouseholds? For the other two-thirds of households, thepurpose of a good wealth management strategy is to pro-tect them from ever coming close to this region at anystage. On the other side of the wealth spectrum, the farright region of the curve is where everyone aspires tomove to. However, the long tail (similar to a lognormaldistribution) indicates that it is not so easy to move right-wards. It is useful to introduce the concept of a wealth percentile.

Every American household can find its place on thistable (Exhibit 3) and thus determine its wealth percentile.There are a total of about 106 million households; there-fore each percentile represents about 1.1 million Americanfamilies. The median wealth of an American householdis about $86,100 (Kennickell [2003]); Sahadi [2003]), whichcorresponds to the 50th wealth percentile. Households inthe lowest seven percentiles (0-7th) have a negative networth, while those in the top percentile (99-100th) haveat least $5 million each.

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

Minimum Wealth

Time

Target Wealth

Failure

Success

Deterministic Approach

Wealth

Starting Wealth

Success

Minimum Wealth

Time

Target Wealth

Failure

Success

Deterministic Approach

Wealth

Starting Wealth

Success

E X H I B I T 1The Journey Matters

At the very outset, it should be clear that everyhousehold, regardless of its current wealth, should makesure that it:

• does not move leftwards (decrease its wealthpercentile);

• at least keeps up with its wealth group; • aspires to move rightwards (increase its relative

wealth standing).

However, the details of this wealth distribution chartindicate that this is a non-trivial task.

In general, you need a lot of money (relative to whatyou have) in order to increase your wealth percentile. Forexample, for a household to move from the 40th (slightlybelow the median) to the 60th percentile (slightly abovethe median), its net worth would need to triple! This meansthat, in order to move up in the wealth structure, one mustacquire substantially, not incrementally, more wealth. Onecannot meet such an aspiration without taking on substan-tial risk, what we will call “aspirational risk.” On the sur-face, this risk taking is at odds with the imperative to protectfrom falling to a lower wealth percentile. It would seemreasonable to assume that most investors in this situationwould pass up the opportunity for improvement in favor ofthe certainty of the status quo. However, it is not so.

Among all wealth levels, aspirational risk taking isquite common. Examples range from the frequent buyingof lottery tickets to more mainstream financial investmentssuch as the substantial purchase of a single stock, invest-

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

<$0 $0 - $50K

$50K - $100K

$100K - $250K

$250K - $500K

$500K - $750K

$750K - $1MM

$1MM - $2MM

$2MM - $6MM

$6MM - $10MM

$10MM - $20MM

>$20MM

Net Worth (in 2001 U.S dollars)

Nu

mb

ero

fFa

mili

es

~ 33% of Total Net Worth is held by

90% (95.8 Million) U.S.Families $0 - $750K

~ 33% of Total Net Worth is held by

9% (9.6 Million) U.S.Families

$750K - $6MM

~ 33% of Total Net Worth is held by

1% (1.1 Million) U.S.Families

$6MM+

E X H I B I T 2The Wealth of America Including Home Equity

Source: Calculation by R. Babu Koneru based on 2001 Survey of Consumer Finances Data (Federal Reserve Board [2003]).

Wealth Percentile Net Worth

6.8 <0

10 $100

20 $6,760

30 $22,840

40 $49,560

50 $86,100

60 $138,100

70 $226,210

80 $375,100

90 $734,100

95 $1,308,520

99 >$5,865,000

E X H I B I T 3Cumulative Distribution of Net Worth of U.S. Families in 2001

Source: Calculation by R. Babu Koneru based on 2001 Survey of ConsumerFinances Data (Federal Reserve Board [2003]).

ment in real estate, or starting a small business. Every timea member of the peer group succeeds in his aspirationalrisk taking, the difficulty of staying in the peer group israised for those who passed on the opportunity. It is easyto see how the desire to keep up with the Joneses raisesthe general level of risk taking, especially among theaffluent. This becomes more and more prevalent in higherwealth percentiles. An extreme example is that of main-taining or improving one’s position in the Forbes 400 list.The net worth required to be the 400th richest Americanincreased sixfold (from $100 million to $600 million) overthe last 20 years (Zaharoff [2004]). In comparison the Con-sumer Price Index increased by 90% over the same period.

Even at the lower wealth spectrum, it is impossibleto maintain one’s standard of living by keeping assets onlyin the bank. Inflation requires some degree of investmentin bond or equity markets and therefore the assumptionof additional risk.

The conventional framework does not have the flex-ibility to accommodate the dual demands of safety andaspiration (Lopes and Oden [1999]). This issue, whichpoints to the need for non-concave utility functions, wasfirst addressed by Friedman and Savage [1948] and was thesubject of a paper by Markowitz [1952b]. However, thisarea received limited attention, in comparison to the workon portfolio diversification (Markowitz [1952a]), till Kah-neman and Tversky’s [1979] work on prospect theory.

In conclusion, we need a new framework that incor-porates these aspects of safety and aspiration, while buildingupon the foundations of Modern Portfolio Theory.

5. A WEALTH ALLOCATION FRAMEWORKFOR THE INDIVIDUAL INVESTOR

To develop a comprehensive wealth strategy we willexpand the definition of portfolio to cover all assets andliabilities such as investments, home, mortgage, and humancapital. Human capital can be loosely defined as earningpotential.

Let us re-emphasize that a person’s portfolio shouldallow him to achieve the following three purposes:

• Protection from anxiety/poverty: We will refer tothis as protection from personal risk.

• Ability to maintain his standard of living and statusin society, i.e., keep up with family and friends. Asdiscussed earlier, in order to do this, investors mustearn a rate higher than inflation and thus take onmarket risk.

• Provide an opportunity to increase his wealth sub-stantially or meet his aspirational goals. This involvestaking on some aspirational risk.

In their famous 1979 paper, Kahneman and Tverskylaid the groundwork for prospect theory, which attemptsto understand and incorporate actual investor behavior.They found several important factors that dominate deci-sion making in the face of risk and return trade-offs, notjust in finance, but across a wide variety of human deci-sion making. By using a series of cleverly formulated ques-tions, they found that certainty, probability, and possibility(among others) were important mindsets that dominatedecision making in the face of risk and return trade-offs.For example, they found that people will most oftenchoose lower but certain payoffs, rather than higher pay-offs with less than certain probability. This experimentallyverified behavior runs counter to standard utility theory.We embrace and incorporate these psychological prefer-ences as a fundamental part of the expanded framework.

We will strive to construct an ideal portfolio thatprovides:

1. The certainty of protection from anxiety.2. The high probability of maintaining one’s standing.3. The possibility of substantially moving upwards

in the wealth spectrum.

Three Dimensions of Risk

The three objectives of an “ideal portfolio” leadnaturally to a framework with three very different dimen-sions of risk: personal, market, and aspirational.

• Personal Risk: You must protect yourself from per-sonal risk. This means protecting yourself from anx-iety regarding a dramatic decrease in your lifestyle(Chhabra and Zaharoff [2001]).

• Market Risk: You need to take on market risk(Markowitz [1952a]; Sharpe et al. [1998]), in orderto grow with your wealth segment and maintainyour lifestyle.

• Aspirational Risk: You could take on aspirational riskif you desire to break away from your wealth seg-ment and enhance your lifestyle.

Modern Portfolio Theory only recognizes marketrisk and seeks to minimize it through optimal asset allo-cation. In contrast, the wealth allocation framework iden-

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

tifies three very different risk dimensions and seeks to opti-mize all three of them simultaneously. We call this risk allo-cation. In the new framework risk allocation needs toprecede asset allocation. Exhibit 4 illustrates each riskdimension with its corresponding objective and trade-offs.

In summary:

• Allocations to the personal risk bucket will limit lossof wealth, but will yield below-market returns.

• Allocations to the market risk bucket will providerisk-adjusted market returns (this is the Markowitzframework).

• Allocations to the aspirational risk bucket shouldyield higher-than-market returns, but with the riskof substantial loss of capital.

In the very simplest case this wealth allocation frame-work can be reduced to a standard diversified portfoliowith downside protection and enhanced upside poten-tial. To illustrate the added capabilities of this frameworkit is instructive to consider one such example in detail.

6. AN IDEALIZED EXAMPLE

We will use a simple albeit idealized example toillustrate many of the issues we have discussed so far. Con-

sider an investor with a portfolio of $100 represented bya “diversified asset” such as a stock index. For the pur-pose of this discussion, we will simply use the historicalrecord of the S&P 500. We will compare and contrast therisk-return characteristics of such portfolio with those ofone constructed using the expanded approach by addinga put option (to protect from loss of capital) and a calloption (to deliver additional upside).

For illustration we will assume a two-year timehorizon. Historically, a long-term investment in the S&P500 has been richly rewarded. In the past 79 years (1926-2004) the average two-year total returns on a monthlyrolling basis for the S&P 500 has been 26.5% with avolatility of 32.8% (an annualized volatility of 23.2%). Inother words, on the average, the investor should expectto have about $126 at the end of two years.

However, examining the history of the index, wefind several two-year periods almost every decade thatprovided either handsome gains or heavy losses. Thesetime periods of larger than expected market movementsare evidence of the deviation from the mean-varianceframework. They also underscore the importance of pro-tecting an investor from such large deviations on thedownside and the opportunity of capitalizing on largeupside movements.

Our investor, of course, does not know a priori how

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

• Minimize downside risk

• Safety

• Accept below market returns for minimal risk

“Personal ” Risk

“Do Not Jeopardize Basic

Standard of Living”

• Balance Risk and Return to

attain market level performance from a broadly diversified

portfolio

“Maintain Lifestyle”

• Maximize Upside

• Take measured risk to achieve significant return enhancement

“Enhance Lifestyle”

“Market ” Risk “Aspirational ” Risk

Cash

Flo

w

Preserve Lifestyle

Principal Protection

• Minimize downside risk

• Safety

• Accept below-market returns for minimal risk

“Personal ” Risk

“Do Not Jeopardize Basic

Standard of Living”

• Balance risk and return to

attain market-level performance from a broadly diversified

portfolio

“Maintain Lifestyle”

• Maximize upside

• Take measured risk to achieve significant return enhancement

“Enhance Lifestyle”

“Market ” Risk “Aspirational” Risk

Ou

tperfo

rm

Saf

ety

Ou

tperfo

rm

Ou

tperfo

rm

CashEquities

AIFixed

Income

E X H I B I T 4Three Dimensions of Risk

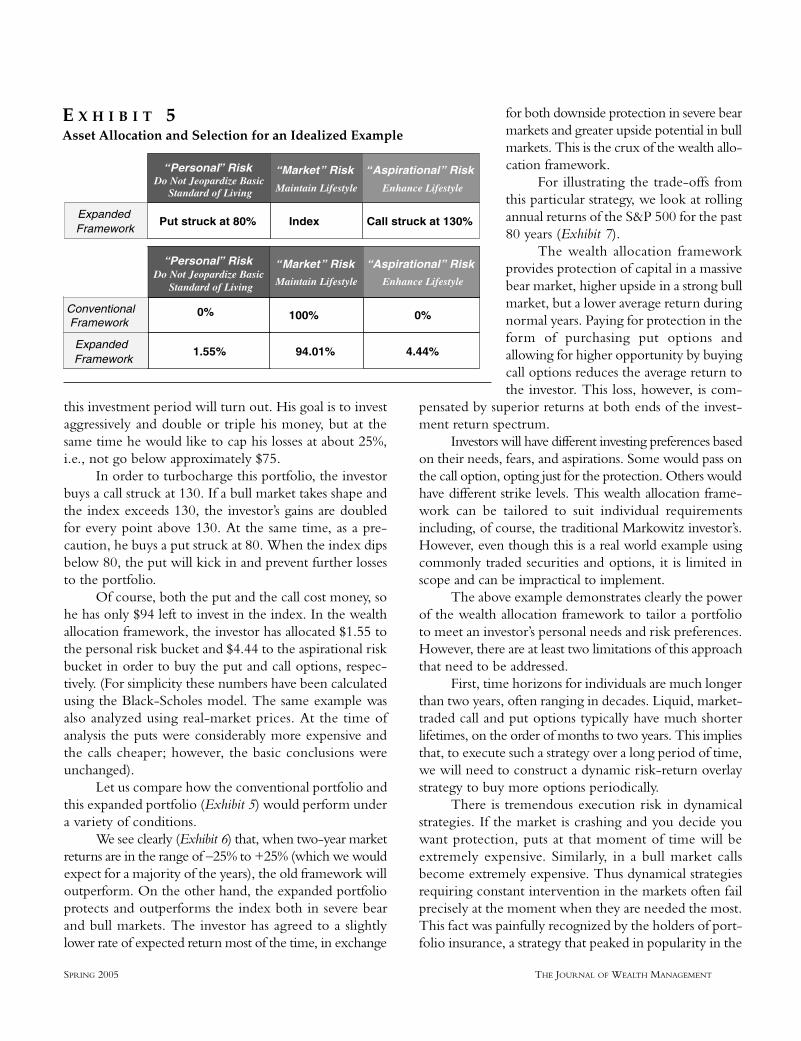

this investment period will turn out. His goal is to investaggressively and double or triple his money, but at thesame time he would like to cap his losses at about 25%,i.e., not go below approximately $75.

In order to turbocharge this portfolio, the investorbuys a call struck at 130. If a bull market takes shape andthe index exceeds 130, the investor’s gains are doubledfor every point above 130. At the same time, as a pre-caution, he buys a put struck at 80. When the index dipsbelow 80, the put will kick in and prevent further lossesto the portfolio.

Of course, both the put and the call cost money, sohe has only $94 left to invest in the index. In the wealthallocation framework, the investor has allocated $1.55 tothe personal risk bucket and $4.44 to the aspirational riskbucket in order to buy the put and call options, respec-tively. (For simplicity these numbers have been calculatedusing the Black-Scholes model. The same example wasalso analyzed using real-market prices. At the time ofanalysis the puts were considerably more expensive andthe calls cheaper; however, the basic conclusions wereunchanged).

Let us compare how the conventional portfolio andthis expanded portfolio (Exhibit 5) would perform undera variety of conditions.

We see clearly (Exhibit 6) that, when two-year marketreturns are in the range of –25% to +25% (which we wouldexpect for a majority of the years), the old framework willoutperform. On the other hand, the expanded portfolioprotects and outperforms the index both in severe bearand bull markets. The investor has agreed to a slightlylower rate of expected return most of the time, in exchange

for both downside protection in severe bearmarkets and greater upside potential in bullmarkets. This is the crux of the wealth allo-cation framework.

For illustrating the trade-offs fromthis particular strategy, we look at rollingannual returns of the S&P 500 for the past80 years (Exhibit 7).

The wealth allocation frameworkprovides protection of capital in a massivebear market, higher upside in a strong bullmarket, but a lower average return duringnormal years. Paying for protection in theform of purchasing put options andallowing for higher opportunity by buyingcall options reduces the average return tothe investor. This loss, however, is com-

pensated by superior returns at both ends of the invest-ment return spectrum.

Investors will have different investing preferences basedon their needs, fears, and aspirations. Some would pass onthe call option, opting just for the protection. Others wouldhave different strike levels. This wealth allocation frame-work can be tailored to suit individual requirementsincluding, of course, the traditional Markowitz investor’s.However, even though this is a real world example usingcommonly traded securities and options, it is limited inscope and can be impractical to implement.

The above example demonstrates clearly the powerof the wealth allocation framework to tailor a portfolioto meet an investor’s personal needs and risk preferences.However, there are at least two limitations of this approachthat need to be addressed.

First, time horizons for individuals are much longerthan two years, often ranging in decades. Liquid, market-traded call and put options typically have much shorterlifetimes, on the order of months to two years. This impliesthat, to execute such a strategy over a long period of time,we will need to construct a dynamic risk-return overlaystrategy to buy more options periodically.

There is tremendous execution risk in dynamicalstrategies. If the market is crashing and you decide youwant protection, puts at that moment of time will beextremely expensive. Similarly, in a bull market callsbecome extremely expensive. Thus dynamical strategiesrequiring constant intervention in the markets often failprecisely at the moment when they are needed the most.This fact was painfully recognized by the holders of port-folio insurance, a strategy that peaked in popularity in the

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

Index Call struck at 130%ExpandedFramework

Put struck at 80%

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

ExpandedFramework

94.01%

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

100% 0%Conventional Framework

1.55% 4.44%Expanded Framework

0%

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

Conventional Framework

Expanded Framework

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

Conventional Framework

Expanded Framework

E X H I B I T 5Asset Allocation and Selection for an Idealized Example

’80s and never recovered after the market crash of 1987. Second, investors desire (and need) such protection

and upside potential to cover all of their financial assets,not just their liquid investment portfolio. Put and calloptions often exist only on liquid market securities.

Therefore this strategy needs both to be generalizedto cover all of the individual’s assets and to be executed in

a systematic manner that does not require constant marketintervention. In other words, we need to choose asset typesand the right risk allocation, so that parts of the portfolio“partially” self-hedge during bear markets (Merton [1995]),while other parts automatically outperform during bullmarkets, without constant market intervention.

This strategy will be judiciously combined with

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

0%

1%

2%

3%

4%

5%

6%

7%

8%

-90% -70% -50% -30% -10% 10% 30% 50% 70% 90% 110% 130% 150%

Index Return

Fre

qu

ency

of

Occ

urr

ence

$0

$50

$100

$150

$200

$250

$300

$350

$400

Po

rtfo

lioV

alu

e

Standard

ExpandedFramework

Outperformance Underperformance Outperformance

E X H I B I T 7Comparison of Portfolio Values

$0

$100

$200

$300

$400

-90.0% -50.0% -24.5% 0.0% 25.0% 38.3% 50.0% 100.0% 125.0% 150.0%Index Return

Po

rtfo

lioV

alu

e Conventional

Expanded Framework

Outperformance Underperformance Outperformance (Relative to Index)

Initial Investment

E X H I B I T 6Comparison of Portfolio Values

some amount of market intervention, including periodicrebalancing, which is and usually will be necessary.

7. RISK ALLOCATION

Individuals have more complex wealth profiles. Theyhave multiple (often conflicting) goals and constraints andtheir portfolios include several different kinds of assets,all of which need to be considered simultaneously. Beforewe delved into the simplified example, we introduced theconcept of risk allocation. Accordingly, portfolio assets,as well as appropriate risk-adjusted benchmarks, need tobe assigned to each of the personal risk, market risk, andaspirational risk buckets.

7.1 Benchmarks

Investors should have very different performanceexpectations for the assets allocated to each of the threerisk buckets, and these expectations must be benchmarkedagainst appropriate indices (Exhibit 8). The idea of havinga different benchmark for each of the three parts of theportfolio is an important one. In the first bucket one paysfor and receives safety. In the third bucket one gets out-

sized returns, unfortunately accompanied by a significantprobability of loss of capital. These two parts of the port-folio, in general, will behave differently than the middleportion, which can be benchmarked against risk-adjustedmarket indices.

In fact, often the entire portfolio will be mean-vari-ance inefficient, when viewed in the narrower mean-vari-ance framework, but will provide more robust protectionand upside, when viewed over a wider range of outcomes.

• Assets in the personal risk bucket should be expectedto appreciate at below-market rates. Suitable bench-marks are the Consumer Price Index or three-monthLIBOR. Suitable risk measures could use downsiderisk rather than volatility.

• Assets in the market risk bucket follow the standardMarkowitz framework. Their performance can becompared to a standard benchmark constructed fromappropriate weighting of the S&P 500 and an aggre-gate bond index. Similarly, the Sharpe ratio can beused to provide a suitable risk-adjusted measurement.

• Assets in the aspirational risk bucket should signif-icantly outperform standard market indices whenthey succeed. Examples of such benchmarks could

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

Expected Performance

Below Market returns for below market risks.

Sample Benchmarks

Consumer Price Inflation

3 Month LIBOR

Risk Measures

Downside Risk

Scenario Analysis

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

Expected Performance

Market returns and Market risks.

Sample Benchmarks

S&P 500

Lehman Agg. Bond

MSCI World index

Risk Measures

Standard Deviation

Sharpe Ratio

Beta

Scenario Analysis

Expected Performance

Above Market returns with high targeted risks.

Sample Benchmarks

¥ CLEW Index

¥ Absolute Return Value

Risk Measures

¥ Upside return measures

¥ Manager alpha

¥ Scenario Analysis

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

Risk / Return SpectrumLow High

Expected Performance

Below-market returns for below-market risks.

Sample Benchmarks

Consumer Price Index

3-Month LIBOR

Risk Measures

Downside Risk

Scenario Analysis

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

Expected Performance

Market returns and market risks.

Sample Benchmarks

S&P 500

Lehman Agg. Bond

MSCI World index

Risk Measures

Standard Deviation

Sharpe Ratio

Beta

Scenario Analysis

Expected Performance

Above-market returns with high targeted risks.

Sample Benchmarks

•

•

CLEW Index

•

•

•

•

•

•

•

•

•

Absolute Return Value

Risk Measures

• Upside Return Measures

• Manager Alpha

•

•

•

•

• Scenario Analysis

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

Risk / Return SpectrumLow High

Protective Assets Market Assets Aspirational Assets

E X H I B I T 8Performance and Risk Measurement Basis for Each Risk Bucket

be Forbes magazine’s Cost of Living Extremely WellIndex (CLEWI) (Yen [2001]), a hedge fund index,or a large alpha over a standard market index. Otherrisk measures could incorporate default probabili-ties or use upside risk rather than volatility.

For an excellent discussion of several new bench-marks for managing risk relating both to individual andnational risk factors, see Shiller [2003].

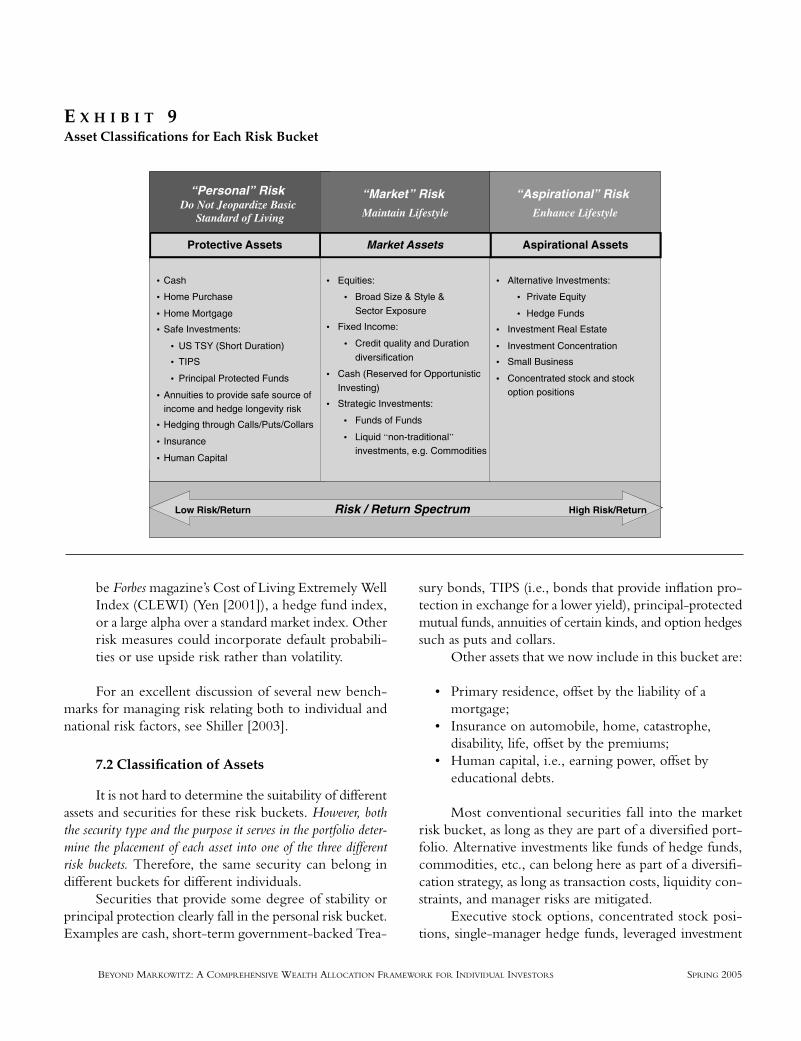

7.2 Classification of Assets

It is not hard to determine the suitability of differentassets and securities for these risk buckets. However, boththe security type and the purpose it serves in the portfolio deter-mine the placement of each asset into one of the three differentrisk buckets. Therefore, the same security can belong indifferent buckets for different individuals.

Securities that provide some degree of stability orprincipal protection clearly fall in the personal risk bucket.Examples are cash, short-term government-backed Trea-

sury bonds, TIPS (i.e., bonds that provide inflation pro-tection in exchange for a lower yield), principal-protectedmutual funds, annuities of certain kinds, and option hedgessuch as puts and collars.

Other assets that we now include in this bucket are:

• Primary residence, offset by the liability of amortgage;

• Insurance on automobile, home, catastrophe,disability, life, offset by the premiums;

• Human capital, i.e., earning power, offset byeducational debts.

Most conventional securities fall into the marketrisk bucket, as long as they are part of a diversified port-folio. Alternative investments like funds of hedge funds,commodities, etc., can belong here as part of a diversifi-cation strategy, as long as transaction costs, liquidity con-straints, and manager risks are mitigated.

Executive stock options, concentrated stock posi-tions, single-manager hedge funds, leveraged investment

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

¥ Alternative Investments:

¥ Private Equity

¥ Hedge Funds

¥ Investment Real Estate

¥ Investment Concentration

¥ Small Business

¥ Concentrated stock and stock option positions.

¥ Cash

¥ Home Purchase

¥ Home Mortgage

¥ Safe Investments:

¥ US TSY (Short Duration)

¥ TIPS

¥ Principal Protected Funds

¥ Annuities to provide safe source of income and hedge longevity risk

¥ Hedging through Calls/Puts/Collars

¥ Insurance

¥

Human Capital

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

¥ Equities:

¥ Broad Size & Style &

Sector Exposure

¥ Fixed Income:

¥ Credit quality and Duration

diversification.

¥ Cash (Reserved for Opportunistic

Investing)

¥ Strategic Investments:

¥ Funds of Funds

¥ Liquid Ònon-traditionalÓ investments e.g. Commodities

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

Risk / Return SpectrumLow Risk/Return High Risk/Return

Aspirational AssetsMarket AssetsProtective Assets

• Alternative Investments:

• Private Equity

• Hedge Funds

• Investment Real Estate

• Investment Concentration

• Small Business

• Concentrated stock and stock option positions

¥ Cash

¥ Home Purchase

¥ Home Mortgage

¥ Safe Investments:

¥ US TSY (Short Duration)

¥ TIPS

¥ Principal Protected Funds

¥ Annuities to provide safe source of income and hedge longevity risk

¥ Hedging through Calls/Puts/Collars

¥ Insurance

¥

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

¥ Equities:

¥ Broad Size & Style &

Sector Exposure

¥ Fixed Income:

¥ Credit quality and Duration

diversification.

¥ Cash (Reserved for Opportunistic

Investing)

¥ Strategic Investments:

¥ Funds of Funds

¥ Liquid Ònon-traditionalÓ investments e.g. Commodities

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

Risk / Return SpectrumLow Risk/Return High Risk/Return

Aspirational AssetsMarket AssetsProtective Assets

• Cash

• Home Purchase

• Home Mortgage

• Safe Investments:

• US TSY (Short Duration)

• TIPS

• Principal Protected Funds

• Annuities to provide safe source of income and hedge longevity risk

• Hedging through Calls/Puts/Collars

• Insurance

• Human Capital

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

• Equities:

• Broad Size & Style &

Sector Exposure

• Fixed Income:

• Credit quality and Duration

diversification

• Cash (Reserved for Opportunistic

Investing)

• Strategic Investments:

• Funds of Funds

• Liquid “non-traditional”investments, e.g. Commodities

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

Risk / Return SpectrumLow Risk/Return High Risk/Return

Aspirational AssetsMarket AssetsProtective Assets

E X H I B I T 9Asset Classifications for Each Risk Bucket

real estate, and call options are examples of investmentsthat fall in the aspirational risk bucket. A family-ownedbusiness that forms a significant part of an individual’s wealthwould also belong here. For more examples see Exhibit 9.

8. AN AFFLUENT INVESTOR EXAMPLE: A HIGH-LEVEL OVERVIEW

It is important to emphasize that the wealth alloca-tion framework can be implemented rather simply. Ahigh-level overview can identify key issues quickly. Fur-ther analysis, for example inclusion of cash flows andMonte Carlo simulations, naturally leads to more accu-rate and detailed solutions.

Let us demonstrate this with an example. Consideran executive whose net worth is summarized in Exhibit 10.

8.1 Identification of Market Risk Factors inTraditional Approach

In the traditional approach (Exhibit 11), we consideronly market portfolio (investment assets) and ignore theother assets and liabilities from the asset allocation analysis.The investor is often advised to get a comprehensive finan-cial plan to address cash flow, estate planning, and otherissues. The asset allocation process in the traditional approachinvolves the following steps to minimize market risk.

1. Identification of concentrated stock positions andtheir diversification.

2. Readjustment of the asset allocation based on theinvestor’s risk tolerance.

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

Personal Assets Liabilities

Primary Residence $1,500,000Mortgage on Primary Residence (5.5% adjustable rate) $700,000

Investment Real Estate $400,000Mortgage on Investment Real Estate (7.5% adjustable rate) $300,000

Total Personal Assets $1,900,000 Total Liabilities $1,000,000

Investment AssetsPortfolio Assets

Equity Portfolio $1,500,000Concentrated Stock $1,250,000Fixed Income Portfolio $350,000Cash Equivalents $150,000

Total Portfolio Assets $3,250,000

Retirement AssetsEquities $0Fixed Income $250,000Cash Equivalents $0

Total Retirement Assets $250,000

Total Investment Assets $3,500,000

Other AssetsEmployee Stock Options $100,000

Total Other Assets $100,000

Total Assets $5,500,000

$4,500,000Total Net Worth

NET WORTH

E X H I B I T 1 0Net Worth Statement for the Executive

3. Diversification of equity allocation across differentmarket sectors and size (based on market capital-ization) and style (value or growth) factors.

4. Diversification of fixed income allocation acrossmaturities and credit quality.

5. Possible inclusion of alternative investments, e.g.,hedge funds, commodities, private equity, toachieve further diversification and superior risk-adjusted returns.

Assuming that the executive is a moderate investor,one possible asset allocation mix is shown in Exhibit 12.

Two major challenges in the traditional approach are:

• Convincing clients to liquidate all of their concen-trated stock position and invest in a diversified port-folio. This is a traditional stumbling block for clients,as it is often the above-average return of that par-ticular stock that has led to their wealth, and thuscorrespondingly, that stock constitutes a dispropor-tionate part of their total investment assets.

• Constructing and maintaining an investment port-folio that takes into account the advice provided bythe comprehensive financial plan. In particular, com-prehensive financial planning is done only once everyfew years while investment portfolios are readjustedto market conditions much more frequently.

8.2 Asset Allocation Construction in Wealth Allocation Framework

The new framework (Exhibit 13) allows the investorto classify all of his assets and liabilities.

Three important high-level questions that need tobe covered are:

1. What are my (personal, market, and aspirational)risk factors?

2. Do I have the correct risk allocation?3. Do I have the right asset allocation within each risk

bucket?

The answers to these questions must be first esti-mated and determined qualitatively, and then determinedquantitatively, if possible.

Our simple risk analysis shows that the executive inour example has a 20%:48%:32% allocation across thepersonal, market, and aspirational risk buckets. Intuitively,it seems that 32% is perhaps too large a portion of theportfolio to allocate for aspirational reasons. At the sametime, one may wonder whether the assets allocated to thepersonal risk bucket (20%) protect him adequately fromhis personal risk factors.

A simple overview of the client risk factors is pro-vided below:

Personal Risk: • An exposure to floating-rate mortgages exposes the

investor to the risk of rising interest rates.• We need to understand if the client’s goal of main-

taining a minimum net worth of $3 million is real-istic.

• Cash reserves are too low and may lead to a liquid-ity crunch.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

Equities43%

Fixed

Income17%

Cash4%

Concentrated Stock

36%

+

Investment Assets Non-Investment Assets

Personal Assets Liabilities

Primary Residence $1,500,000Mortgage on Primary Residence (5.5% adjustable rate) $700,000

Investment Real Estate $400,000Mortgage on Investment Real Estate (7.5% adjustable rate) $300,000

Total Personal Assets $1,900,000 Total Liabilities $1,000,000

Other AssetsEmployee Stock Options $100,000

Total Other Assets $100,000

Total Assets $2,000,000

NON-INVESTMENT ASSETS

Equities43%

Fixed

Income17%

Cash4%

Concentrated Stock

36%

+

Equities43%

Fixed

Income17%

Cash4%

Concentrated Stock

36%

+

Personal Assets Liabilities

Primary Residence $1,500,000Mortgage on Primary Residence (5.5% adjustable rate) $700,000

Investment Real Estate $400,000Mortgage on Investment Real Estate (7.5% adjustable rate) $300,000

Total Personal Assets $1,900,000 Total Liabilities $1,000,000

Other AssetsEmployee Stock Options $100,000

Total Other Assets $100,000

Total Assets $2,000,000

NON-INVESTMENT ASSETS

E X H I B I T 1 1Executive’s Asset Allocation and Net Worth Statement in the Conventional Framework

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

Equities

43%

Fixed Income

17%

Cash4%

Concentrated Stock

36%

Cash10%

Fixed

Income25%

65%Equities

Current Recommended

E X H I B I T 1 2Executive’s Current and Recommended Asset Allocations for the Investment Assets in the Conventional Framework

Primary Residence

89%

Cash11%

Real Estate

7%Stock

Options7%

Concentrated Stock86%

Equities70%

Fixed Income

28%

Cash2%

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

(20%)

“Market” Risk

Maintain Lifestyle

(48%)

“Aspirational” Risk

Enhance Lifestyle

Risk / Return SpectrumLow High

$2,150,000Total

$50,000Cash

$600,000Int. and Long-Term Fixed Income

$1,500,000Equities

$2,150,000Total

$50,000Cash

$600,000Income

$1,500,000Equities

$100,000Cash/Short Term Treasury Bonds & Notes

($700,000)

Mortgage on Primary Residence @ 5.5% adjustable rate.

$900,000Total

$1,500,000Home

$100,000Cash/Short Term Treasury Bonds & Notes

($700,000)

Mortgage on Primary

adjustable rate.

$900,000Total

$1,500,000Home

($300,000)

Mortgage on Investment Real Estate @ 7.5% adjustable rate.

$400,000Investment Real Estate

$100,000Employee Stock Options

$1,450,000Total

$1,250,000Concentrated Stock

($300,000)

Mortgage on Investment

adjustable rate.

$400,000Investment Real Estate

$100,000Employee Stock Options

$1,450,000Total

$1,250,000Concentrated Stock

Protective Assets Market Assets Aspirational Assets

(32%)

E X H I B I T 1 3Executive’s Current Risk and Asset Allocation in the Wealth Allocation Framework

Market Risk:These factors dealing with diversification were cov-

ered earlier in reviewing the traditional approach to assetallocation.

Aspirational Risk:• The exposure to a single company stock and stock

options is too large.• There is exposure to rising short-term interest rates

through a large floating rate mortgage on his invest-ment real estate.

The recommended asset allocation summarized inExhibit 14 was arrived at by taking into account the above

risk factors and the client’s financial objectives.A summary of the recommended changes and ratio-

nale behind them is given below.

Personal Risk:• The overall amount of assets in this bucket was

increased in order to lower the client’s personal risk.• Inflation risk and the desire to maintain a minimum

wealth level of $3 million dollars led to the purchaseof TIPS as well as to an increase in the cash reserves.

• The floating-rate mortgage was switched to a (slightlyhigher rate) fixed-rate mortgage to decrease theinvestor’s exposure to rising interest rates.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

Alternative Investments

10%

Equities60%

Fixed Income

25%

Cash5%

Single Stock11%

Real Estate45%

Stock Options

22%

Hedge Funds22%

Residence44%

Inflation Indexed Bonds39%

Cash17%

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

(40%)

“Market” Risk

Maintain Lifestyle

(50%)

“Aspirational” RiskEnhance Lifestyle

(10%)

$700,000

Inflation Indexed Treasury Bonds

$300,000Cash/Short Term Treasury Bonds & Notes

($700,000)

Mortgage on Primary Residence @ 6.0% fixed rate.

$1,800,000Total

$1,500,000Home

$225,000

Alternative Investments—Fund of

Hedge Funds—Commodities—Foreign Exchange

$2,250,000 $450,000Total

$112,500Cash

$562,500Int. and Long Term Fixed Income

$1,350,000Equities

—

——

Income

Equities

($200,000)

Mortgage on Investment Real Estate @7.5% adjustable rate.

$400,000Investment Real Estate

$100,000Employee Stock Options

Total

$100,000Single Manager Hedge Fund

$50,000Single Stock Position

Protective Assets Market Assets Aspirational Assets

E X H I B I T 1 4Executive’s Recommended Risk and Asset Allocation in the Wealth Allocation Framework

Market Risk:The portfolio was fully diversified in accordance to

the tenets of Modern Portfolio Theory. Note that, inaddition to rebalancing the basic asset classes, we addedalternative investments in the form of a fund of hedgefunds, as well as limited exposure to commodities andforeign exchange due to their diversification benefits.

Aspirational Risk:• The overall assets in this bucket were decreased,

because the client was taking on too much aspira-tional risk.

• The concentrated stock position was decreased, someof which went to the personal risk bucket for thepurchase of TIPS. The rest of the proceeds wereused to reduce the amount of the floating-rate mort-gage for the investment property, and to buy a single-manager absolute return hedge fund.

• There is now some diversification, i.e., a better bal-ancing of different risk exposures in this bucket.

In the next section we will show that the new port-folio also does better under a variety of different scenariosand market shocks.

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

Expected Return Current RecommendedScenario Description

PersonalPortfolio(%)

MarketPortfolio(%)

AspirationalPortfolio (%)

Net Worth($)

NetReturn(%)

NetWorth ($)

NetReturn(%)

1Short-TermUnderperformance 4 -20 -100 2,656,000 -41 3,672,000 -18

2Long-TermUnderperformance 4 0 -50 3,811,000 -15 4,347,000 -3

3 Likely-I 4 7 -20 4,396,500 -2 4,639,500 3

4 Likely-II 4 7 20 4,976,500 11 4,819,500 7

5 Optimistic 4 10 50 5,476,000 22 5,022,000 12

6 Long Shot 4 20 100 6,416,000 43 5,472,000 22

E X H I B I T 1 5Comparison of Performance Under Different Scenarios

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

Scenario - 1 Scenario - 2 Scenario - 3 Scenario - 4 Scenario - 5 Scenario - 6

Current

Recommended

E X H I B I T 1 6Comparison of Performance Under Different Scenarios

8.3 Scenario Analysis

A quick and simple scenario analysis of the client’scurrent and recommended asset allocations is shown inExhibits 15 and 16. The first scenario also incorporates,for example, the possibility of the bankruptcy of the com-pany associated with the client’s single stock position.

Note that the expanded strategy concentrates onincorporating the goals and risk preferences of the investor(such as minimizing the chances of having a net worthbelow $3 million), in addition to attempting to immunizethe client from the identified client risk factors, includingmarket crashes.

Once the correct allocations have been made in thethree buckets, the middle bucket should be diversified asprescribed by MPT. In the wealth allocation frameworkthere is no reason not to diversify the holdings in the middle(market risk) bucket—as MPT explains you do not get paidfor holding non-systematic risk. The aspirational bucket,however, retains some portion of the concentrated stock.

8.4 Impact of Market Shocks

The scenarios analyzed above capture effectively theimpact of market shocks. One such shock the marketrecently experienced was the bursting of the technologybubble, “Tech-Wreck,” in the year 2000. We analyze theimpact of this event on the investor’s current and recom-mended portfolios.

• We assume a nominal 5% decline in the investor’sinvestment real estate during this period and no appre-ciable change in the value of his primary residence.

• We study the impact of an investor holding concen-trated stock positions in one of two randomly selectedtechnology or telecommunication companies.

The impact of this market shock event on differentU.S. markets and the current and recommended asset allo-cations is summarized in Exhibit 17. It can be observedthat the impact of market shocks on the investor’s networth is relatively small for the recommended asset allo-cation in the wealth allocation framework, when com-pared with the current asset allocation. This is due to thefact that assets are more appropriately distributed betweenthe three risk buckets, which take into view the investor’sentire financial situation.

To keep this example simple, we decided to notethe human capital but not compute or use its value in therisk allocation. We could have instead explicitly present-valued the cashflows (current salary and future social secu-rity income) and adjusted the personal risk bucketaccordingly (Chen [2004]). However, even when theearning capacity is included simply as a risk factor, theclient is led to a judgement of how stable that is and maydecide to lighten up on the aspirational bucket, if needed.Alternatively, the client may decide to continue to earnon a limited basis even after retiring and feel confidentabout his large aspirational risk allocation.

A more detailed analysis (schematically outlined inAppendix B) uses cashflows and measures such as max-imum loss and allows the investor to optimize on the useof annuities to mitigate the prospect of outliving his assets.The objective is to immunize the client against all of hisrisk factors.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

Market Benchmark Index Tech-Wreck Event Impact*

Equity S&P 500 -23.04%

Fixed Income Merrill Lynch Domestic Master Bond Index 8.11%

Cash US 30-Day T-Bill 3.45%

Inflation Indexed Treasury Bonds Merrill Lynch U.S. Treasury Inflation-linked Securities Index 9.22%

Technology Stock - -26.97%

Telecommunication Stock - -74.63%

Alternative Investments CSFB Tremont Hedge Fund Index -0.44%

Current Allocation With Tech Stock - -15.02%

Current Allocation With Telcom Stock - -29.32%

Recommended Allocation With Tech Stock - -6.11%

Recommended Allocation With Telcom Stock - -8.76%

*Based on Ibbotson Encorr data for the broad market indices during the period September 2000 to March 2001.

E X H I B I T 1 7Impact of Tech-Wreck Event on U.S. Markets

9. APPLYING THE WEALTH ALLOCATIONFRAMEWORK IN DIFFERENT SITUATIONS

9.1 Goal-Based Asset Allocation Strategies

The concept of personal risk was introduced inChhabra and Zaharoff [2001] in the context of setting anasset allocation strategy to meet the client’s goals.

The definition of both personal risk and market riskused in that article have been refined and expanded toform essential building blocks of the wealth allocationframework.

The wealth allocation framework allows clients tosegment their assets and create appropriate financial strate-gies towards particular goals, while assuming a consistentoverall approach to resource allocation.

9.2 The Role of Alternative Investments(Including Commodities and ForeignExchange) in Investment Portfolios

Alternative investments such as hedge funds, pri-vate equity, real estate, futures, commodities, and FX havein recent years become an integral part of the investmentportfolios of the wealthy. If these investments have ben-eficial roles in the portfolios of the affluent, do they alsohave a similar role in the portfolios of all investors?

The wealth allocation framework looks at all of theseinvestments in terms of both their particular risk-returncharacteristics and the role they play in investors’ portfo-lios, i.e., hedging, diversification, or a pure absolute returnstrategy. For these classes of securities it is crucial to weighthe benefits of their inclusion against counteracting fac-tors, such as higher transaction costs, fees, minimuminvestment thresholds, liquidity constraints, higher defaultrisks, as well as suitability and transparency issues, in orderto arrive at a decision.

Fixed income securities with lower credit qualityhave many of the same issues described above; however,individuals increasingly hold fixed income mutual fundsthat are diversified in credit quality. The underlyingthinking is that every portfolio needs exposure to thefixed income markets and there is a risk-return trade-offbetween accepting the risk from lower-credit-quality fixedincome securities and receiving higher yields.

The same logic applies to markets other than fixedincome. Securities that hedge against various risk factorsalso provide similar risk-return trade-offs.

The price of a gallon of gas is related to the price of

a barrel of oil. Other commodities such as precious metals,natural gas, and agricultural products have a natural con-nection with the cost of living and inflation. However,traditionally, the presence of commodities in investors’portfolios has been limited to gold, often in its physicalform. Investors would benefit from liquid, low-cost waysto hedge exposures to broad-based commodity indexes.

Similarly, investors are strongly exposed to countrydefault and currency devaluation risks. These risks areoften neglected, but they do occur frequently, e.g., inrecent years in Argentina, Russia, and Korea. A pure FXhedge (which may be not just on the investment portfoliobut also on other investments such as real estate holdingsor business contracts) would have an underlying cost asso-ciated with it and would belong in the personal riskbucket. However, FX can also serve as a diversifier, inwhich case it can be a small percentage of a diversifiedportfolio in the market risk bucket. On the other hand,a speculative FX position naturally carries the associatedrisk of losing one’s investment and would clearly be cat-egorized in the aspirational risk bucket.

Similar arguments can be made regarding hedgefunds. While single-manager absolute return hedge fundsare clearly “aspirational investments,” a broad-based port-folio that diversifies across different managers and invest-ment strategies could form an alternative and attractivediversifier, when compared, for example, with the addi-tion of a portfolio of emerging market high-yield bonds.Some of the challenges that need to be addressed in orderto facilitate a wider use of these investments are: greatertransparency of the active strategy and current holdingswithin hedge funds in order to mitigate operational risk;removal of liquidity constraints; lowering of cost structuresin terms of both fees and minimum investments; avail-ability and sharing of good historical data; establishmentof widely accepted representative indexes or benchmarks;and good estimates of the after-tax risk-return character-istics of these investments.

9.3 Use of Real Estate as a Diversifier

In recent years, the outperformance of the real estatemarket has caused investors to look favorably at real estateas a diversifier to investing in the capital markets. Thequestion of what risk bucket the real estate holdings belongin is answered by reiterating our criterion for asset clas-sification: both the security type and the purpose it serves in theportfolio determine the placement of each asset into one of thethree different risk buckets.

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

A sensible primary home, together with its mort-gage, fits in the personal risk bucket. An investment prop-erty like a condominium for rental purposes could belongin either the market risk bucket or the aspirational riskbucket depending on the leverage used. If the asset to lia-bility ratio is large, and the location is relatively stable,then the condominium belongs in the market risk bucket,where it serves to diversify the risk-return characteristicsof the investment portfolio. If the asset-liability ratio issmall, i.e., the position is highly leveraged, or if the loca-tion is “filled with potential,” then clearly the investor ishoping for outsized gains (in comparison to the downpayment) but could also end up losing most of the downpayment. This investment then would clearly belong inthe aspirational bucket. In the client example discussed ear-lier, the investor split his aspirational risk between a con-dominium and a concentrated stock position. The clientrisk factors here would clearly be the ability to hold onto the property through a down market, as well as the lia-bility aspects of holding real estate.

9.4 Incorporating Executive Stock Options and Company Stock

Stock options are an important and efficient way ofcompensating executives. This piece obviously belongsin the aspirational risk bucket for it is both highly lever-aged and strongly correlated to human capital and sourceof income of the individual. If any of the stock or stockoptions can be hedged, then depending on the structureof the hedge, the hedged portion would move to the per-sonal or market risk bucket. It is not uncommon to neglectthe value of the unhedged piece while considering retire-ment savings.

An interesting and important contrast betweenModern Portfolio Theory and the wealth allocation frame-work was brought out in the client example with respectto concentrated stock. It is worth repeating that MPTwould suggest complete diversification from the concen-trated position. The wealth allocation framework attemptsto work out an appropriate percentage of the position theclient may still retain in order to balance the allocationsto the three different risk buckets.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

Minimum $ Level

Risk -Return Measures

Time

Wea

lth

Client is willing to pay for enhanced returns e.g. Hedge Funds

Client pays for asset protection

Client essentially pays for market like returns - standard risk/return trade-off achieved with active and passive funds, stocks, etc.

Minimum $ Level

Risk -Return Measures

Minimum $ Level

Risk -Return Measures

Time

Wea

lth

Client is willing to pay for enhanced returns -

Client pays for asset protection

E X H I B I T 1 8Dynamic Risk Allocation

9.5 Dynamic Characteristics of Optimal Risk Allocation

The investor’s optimal risk allocation depends notjust on the relative risk-return characteristics of markets, butalso on how much wealth an investor has relative to whatshe needs and how far way from the danger zone she is.This is a dynamic situation that is illustrated in Exhibit 18.

If the individual is in the danger zone, she shouldbe more conservative. She will value more highly invest-ments that do not go down. This means that the relevantrisk measure will weigh more heavily the possibility ordanger of negative returns, rather than the possibility ofupside returns; for example, she will look more favorablyat a principal-protected mutual fund (with correspond-ingly limited upside) than at a conventional unhedgedsecurity. This risk allocation will be dominated by per-sonal risk (Exhibit 19).

If the investor has a decent cushion from the dangerzone, then her allocation is similar to that of the aggregatemarket and the appropriate risk measure is similar or iden-tical to the one used by the financial markets, i.e., volatility.This risk allocation will be overweighted by assets in themarket risk bucket. The benefits of being in this zone arethat, since one has similar risk-return considerations as theaggregate market, one invests in liquid and (comparatively)low-transaction-cost securities such as stocks and bonds. Asinvestors get wealthier, they begin to look for investments

that allow for further upside potential, e.g., some types ofhedge funds or venture capital. In this region, they arewilling to take greater risks, i.e., possible loss of principal(Exhibit 20).

Their risk measure is therefore weighted more towardsthe potential of upside gains than the possibility of neg-ative returns. This risk allocation will be over-weightedby assets in the aspirational risk bucket.

It is worth noting that the minimum level of wealthshown in Exhibit 18 will often vary based on the currentwealth of the investor as opposed to a hard number basedon the actual amount needed to maintain a lifestyle. Thisis consistent with Kahneman and Tversky’s [1979] obser-vations that gains and losses by investors are viewed in rela-tion to a reference level. Finally, these ratios may be affectedby other factors, such as the lifecycle stage of the investor.

9.6 Annuitization Strategy

With ever-decreasing mortality rates among theU.S. population, longevity risk, i.e., the risk of outlivingone’s assets, can be very high, especially for retirees witha family history of longevity. Traditional asset allocationmethods based on MPT cannot guarantee protectionagainst longevity risk. By guaranteeing a fixed or vari-able stream of cash flow for the entire lifetime of theinvestor in exchange for a fixed up-front premium,immediate annuities act as an effective hedging strategy

for longevity risk. When theanalysis of client risk factorsindicates exposure to longevityrisk, the expanded allocationframework includes immediateannuities in the asset mix forthe personal risk bucket.Depending upon the client’snet worth, lifestyle needs,bequest motive, and risk tol-erance, the amount allocatedto annuities is then deter-mined. Exhibit 21 shows a typ-ical asset allocation in thewealth allocation frameworkfor an investor with highlongevity risk. The wealthallocation framework includesannuities in the asset allocationdecision by including them inthe personal risk bucket. The

SPRING 2005 THE JOURNAL OF WEALTH MANAGEMENT

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

60% 30% -40% 0% -10%Conservative

Investor

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

60%Conservative

Investor

E X H I B I T 1 9Sample Risk Allocation for a Conservative Investor

40% -60%

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

40% 0% -20%Affluent Investor

Small / Medium Medium / Large Medium / LargeWealthy Investor

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

40% 0% Affluent Investor

Small / Medium Medium / Large Medium / LargeWealthy Investor

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

40%Affluent Investor

Small / Medium Medium / Large Medium / LargeWealthy Investor

E X H I B I T 2 0Sample Risk Allocation for Affluent and Wealthy Investors

bulk of the assets is invested in the personal risk bucket(~75%), which includes significant exposure to annu-ities and inflation-protected securities. The market riskbucket (~20%) provides the necessary cushion to main-tain lifestyle in the event of significant inflation and othermarket risks.

Recently Chen and Milevsky [2003] proposedoptimal asset allocation strategies by including annuities inthe asset allocation, and Dus and Mitchell [2004] showedthat a delayed annuitization, in addition to a phased with-drawal scheme, can reduce shortfall probabilities. Thewealth allocation framework can incorporate both theseapproaches in a flexible manner.

9.7 Barbell Strategies: Insurance and Lottery Tickets

We emphasized earlier that the idea of combiningdownside protection and upside potential is not new. Infact Markowitz himself addressed this issue. In 1952 hepublished two papers: The first (Markowitz [1952a]) out-lined the foundations of Modern Portfolio Theory; thesecond (Markowitz [1952b]), entitled “The Utility ofWealth,” built upon Friedman and Savage’s [1948] work andtalked about non-concave utility functions based on thesimultaneous desire of individuals to pay for insurance andinvest in lottery tickets. This idea has been subsequentlyexplored by a number of people including Lopes [1987] andLopes and Oden [1999], who constructed the notion ofSP/A portfolios, in which investors decompose their port-folios in terms of a safe portion known as security protec-

tion and a risky portion termed as the aspi-ration part. Such a strategy may also betermed as a barbell strategy, where investorsmakes sure they have a safe cushion andthen invest the rest of the portfolio in anaggressive allocation.

The barbell approach reflects the rel-ative importance of the extremes to themore diversified Markowitz approach.This group is really a risk-seeking groupthat first protects the basics and then feelsfree to take on substantial risk (Exhibit22). Investing strategies have been put for-ward to try and replicate these character-istics. We will discuss some of these furtherin the next section.

9.8 Option-Based and Dynamical Replication Strategies

Bodie [2001] explores the use of a call-option-basedasset allocation strategy for retirement planning. In the stan-dard of living adjustment (SOLA) strategy, the investor buysTIPS to protect herself from credit risk and inflation risk,as well as call options on the equity market. If the optionsend up in the money, the investor uses the gain to buymore TIPS and more call options and the process goes on.

Other work in option-based investing strategiesincludes: Haugh and Lo [2001], who show that certaindynamic asset allocation strategies can be approximatedusing simple buy-and-hold strategies that include options,and Van Capelleveen et al. [2003], who study the impactof including options for managing pension funds and findthat incorporating options may help the sustainability ofpension funds.

Note that our framework does not exclude thesestrategies. Rather, it provides an organizational frameworkwithin which these strategies can be evaluated. However,the main thrust of the framework is to set up a portfoliothat provides a majority of protection and upside basedon the correct risk allocation and selection of financialinstruments, rather than by dynamical replication.

BEYOND MARKOWITZ: A COMPREHENSIVE WEALTH ALLOCATION FRAMEWORK FOR INDIVIDUAL INVESTORS SPRING 2005

“Personal” RiskDo Not Jeopardize Basic

Standard of Living

“Market” Risk

Maintain Lifestyle

“Aspirational” Risk

Enhance Lifestyle

75% 20% 5%Annuitization

Strategy

E X H I B I T 2 1Sample Risk Allocation for an Annuitization Strategy

60% 10% 30%Barbell Strategy

“Personal ” RiskDo Not Jeopardize Basic

Standard of Living

“Market ” Risk

Maintain Lifestyle

“Aspirational ” Risk

Enhance Lifestyle

60% 10% 30%Barbell Strategy

“Personal” RiskDo Not Jeopardize Basic