1 optimal risky portfolio, capm, and apt diversification portfolio of two risky assets asset...

TRANSCRIPT

1

Optimal Risky Portfolio, CAPM, and APT Diversification Portfolio of Two Risky Assets Asset Allocation with Risky and Risk-free Assets Markowitz Portfolio Selection Model CAPM APT (arbitrage pricing theory)

2

Top-down process

Capital allocation between the risky portfolio and risk-free assets

Asset allocation across broad asset classes Security selection of individual assets within each

asset class

Chapter 1: Overview

3

Diversification Effect

4

Systematic risk v. Nonsystematic Risk Systematic risk, (nondiversifiable risk or market

risk), is the risk that remains after extensive diversifications

Nonsystematic risk (diversifiable risk, unique risk, firm-specific risk) – risks can be eliminated through diversifications

5

rp = w1r1 + w2r2

w1 = Proportion of funds in Security 1w2 = Proportion of funds in Security 2r1 = Expected return on Security 1r2 = Expected return on Security 2

1

n

1iiw

Two-Security Portfolio: Return

6

p2

= w121

2 + w222

2 + 2w1w2 Cov(r1r2)

12 = Variance of Security 1

22 = Variance of Security 2

Cov(r1r2) = Covariance of returns for security 1 and security 2

Two-Security Portfolio: Risk

7

1,2 = Correlation coefficient of returns

Cov(r1r2) = 1,212

1 = Standard deviation of returns for Security 12 = Standard deviation of returns for Security 2

Covariance

8

Range of values for 1,2

+ 1.0 > > -1.0

If = 1.0, the securities would be perfectly positively correlated

If = - 1.0, the securities would be perfectly negatively correlated

Correlation Coefficients: Possible Values

97-9

Three-Asset Portfolio

1 1 2 2 3 3( ) ( ) ( ) ( )pE r w E r w E r w E r

23

23

22

22

21

21

2 wwwp

3,2323,1312,121 222 wwwwww

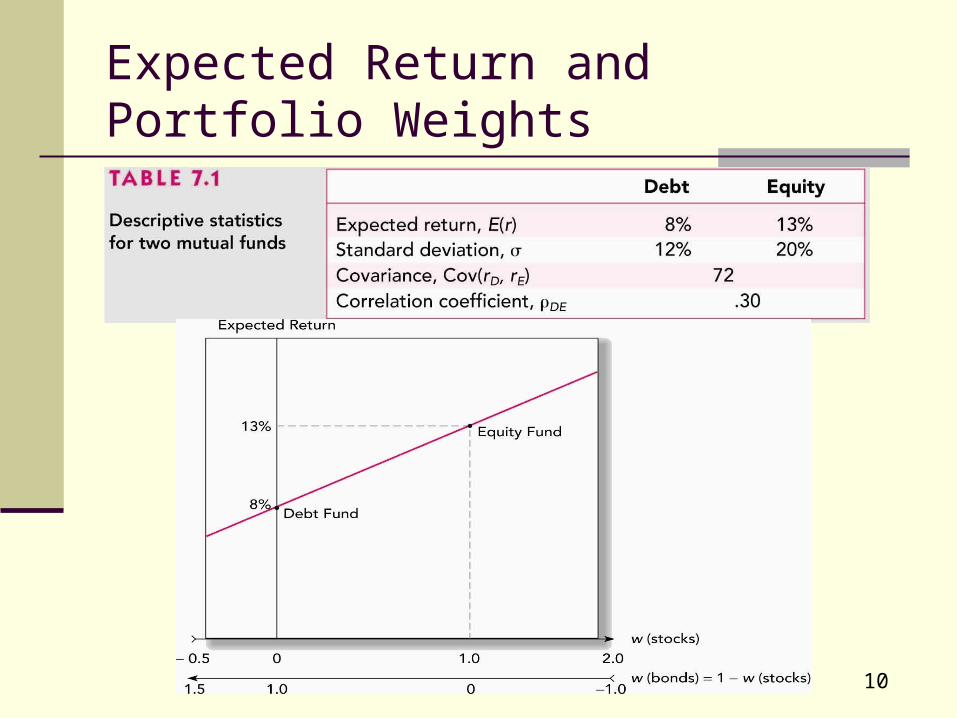

10

Expected Return and Portfolio Weights

11

Expected Return and Standard Deviation

Look at ρ=-1, 0 or 1.

Minimum Variance Portfolio

12

The relationship depends on correlation coefficient.

-1.0 < < +1.0 The smaller the correlation, the greater the risk

reduction potential. If = +1.0, no risk reduction is possible.

The Effect of Correlation

137-13

The Minimum Variance Portfolio

The minimum variance portfolio is the portfolio composed of the risky assets that has the smallest standard deviation, the portfolio with least risk.

See footnote 4 on page 204.

When correlation is less than +1, the portfolio standard deviation may be smaller than that of either of the individual component assets.

When correlation is -1, the standard deviation of the minimum variance portfolio is zero.

14

Optimal Portfolio

Given a level of risk aversion, on can determine the portfolio that provides the highest level of utility.

See formula on page 205. Note: no risk free asset is involved.

Chapter 1: Overview

15

Capital Asset Line

A graph showing all feasible risk-return combinations of a risky and risk-free asset.

See page 206 for possible CAL Optimal CAL – what is the objective function in

the optimization?

16

Sharpe ratio

Reward-to-volatility (Sharpe ratio) Page 206

Chapter 1: Overview

17

Optimal CAL and the Optimal Risky Portfolio

Equation 7.13, page 207

18

Exercises

A pension fund manager is considering 3 mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8%. The probability distribution of the risky funds is as following:

Exp(ret) Std DevStock fund 20% 30%

bond Fund 12% 15%The correlation between the fund returns is 0.10

Answer Problem 4 through 6, page 225.Also see Example 7.2 (optimal risky portfolio) on page 208

19

Determination of the Optimal Overall Portfolio

20

Markowitz Portfolio Selection

Generalize the portfolio construction problem to the case of many risky securities and a risk-free asset

Steps Get minimum variance frontier Efficient frontier – the part above global MVP An optimal allocation between risky and risk-free asset

21

Minimum-Variance Frontier

22

Capital Allocation Lines and Efficient Frontier

23

Harry Markowitz laid down the foundation of modern portfolio theory in 1952. The CAPM was developed by William Sharpe, John Lintner, Jan Mossin in mid 1960s.

It is the equilibrium model that underlies all modern financial theory.

Derived using principles of diversification with simplified assumptions.

Capital Asset Pricing Model (CAPM)

24

Individual investors are price takers. Single-period investment horizon. Investments are limited to traded financial assets. No taxes and transaction costs. Information is costless and available to all

investors. Investors are rational mean-variance optimizers. There are homogeneous expectations.

Assumptions

25

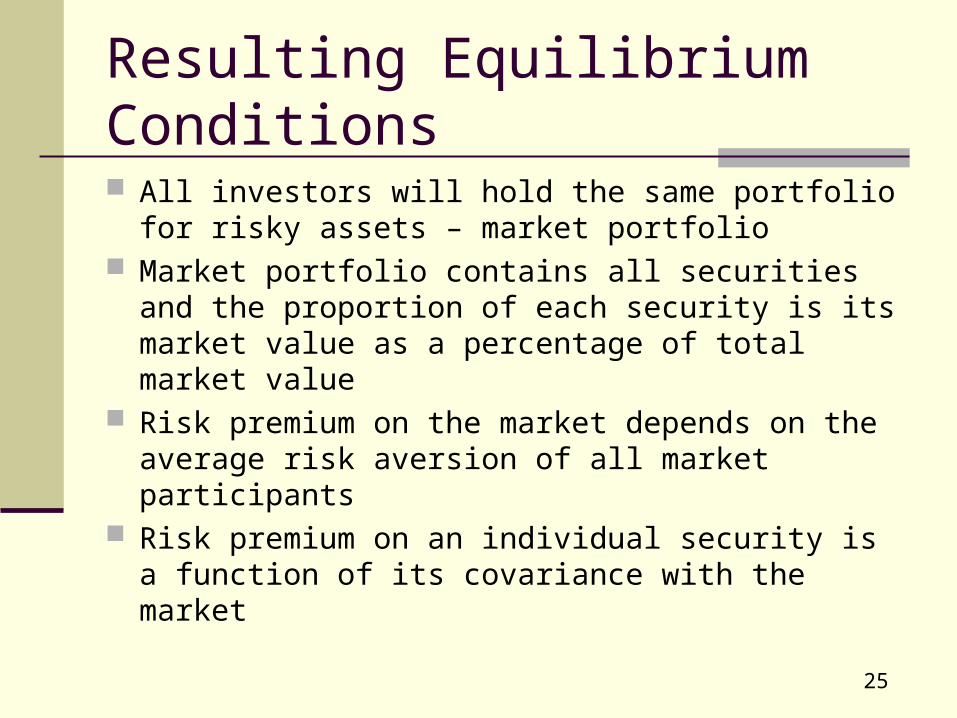

Resulting Equilibrium Conditions

All investors will hold the same portfolio for risky assets – market portfolio

Market portfolio contains all securities and the proportion of each security is its market value as a percentage of total market value

Risk premium on the market depends on the average risk aversion of all market participants

Risk premium on an individual security is a function of its covariance with the market

26

Figure 9.1 The Efficient Frontier and the Capital Market Line

27

CAPM

2

),(

M

Mii

rrCov

E(R)=Rf+β*(Rm-Rf)

)(RER

28

Security Market line and a Positive-Alpha Stock

29

CAPM Applications: Index Model

To move from expected to realized returns—use the index model in excess return form:

Ri=αi+βiRM+ei

The index model beta coefficient turns out to be the same beta as that of the CAPM expected return-beta relationship

What would be the testable implication?

30

Estimates of Individual Mutual Fund Alphas

31

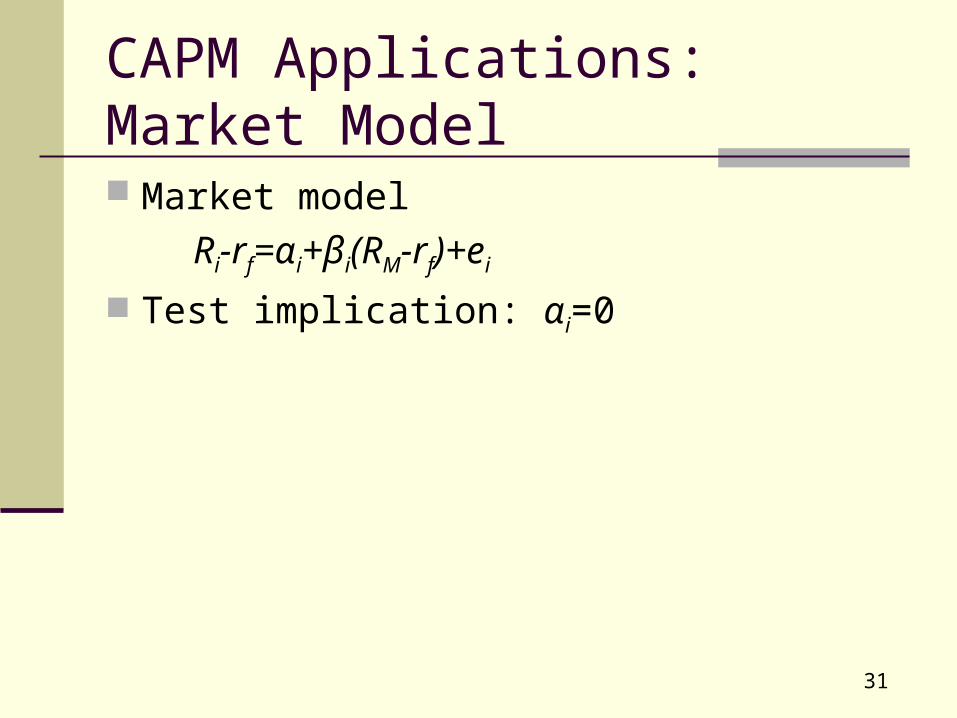

CAPM Applications: Market Model Market model

Ri-rf=αi+βi(RM-rf)+ei

Test implication: αi=0

32

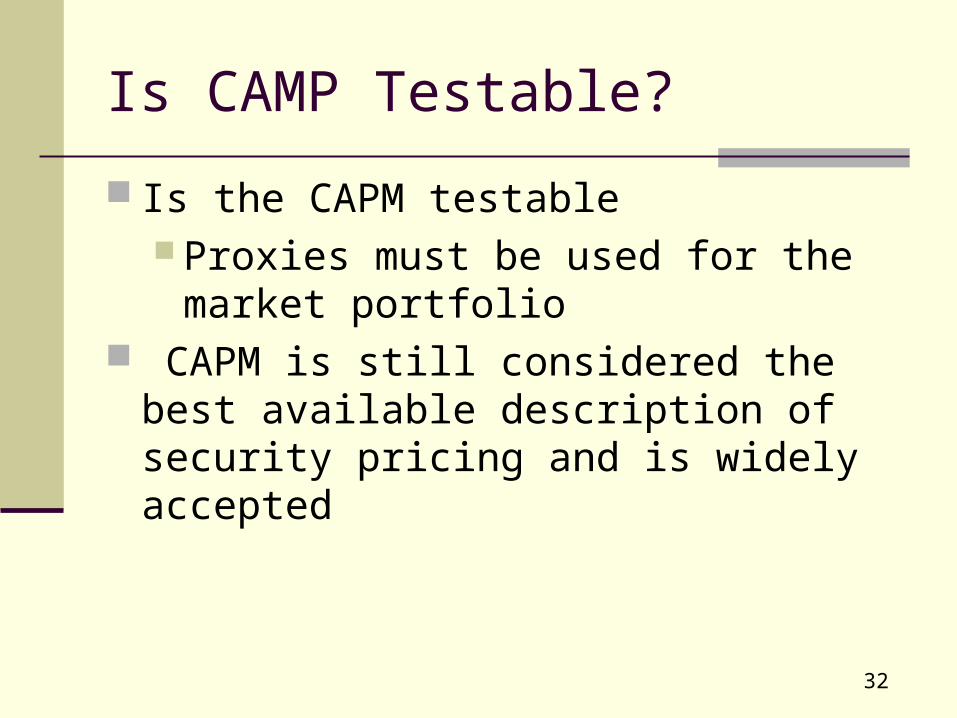

Is CAMP Testable?

Is the CAPM testable Proxies must be used for the market

portfolio CAPM is still considered the best available

description of security pricing and is widely accepted

33

Other CAPM Models: Multiperiod Model Page 303 Considering CAPM in the multi-period setting Other than comovement with the market portfolio,

uncertainty in investment opportunity and changes in prices of consumption goods may affect stock returns

Equation (9.14)

34

Other CAPM Models: Consumption Based Model

No longer consider the comovements in returns of individual securities with returns of market portfolios

Key intuition: investors balance between today’s consumption and the saving and investments that will support future consumption

Page 305; Equation (9.15)

35

Liquidity and CAPM

Liquidity – the ease and speed with which an asset can be sold at fair market value.

Illiquidity Premium The discount in security price that results from

illiquidity is large Compensation for liquidity risk – inanticipated

change in liquidity

Research supports a premium for illiquidity. Amihud and Mendelson and Acharya and Pedersen

36

Illiquidity and Average Returns

37

APT

Arbitrage Pricing Theory This is a multi-factor approach in pricing stock

returns. See chapter 10

38

Fama-French Three-Factor Model

The factors chosen are variables that on past evidence seem to predict average returns well and may capture the risk premiums (page 335)

rit=αi+βiMRMt+βiSMBSMBt+βiHMLHMLt+eit

Where:

SMB = Small Minus Big, i.e., the return of a portfolio of small stocks in excess of the return on a portfolio of large stocks

HML = High Minus Low, i.e., the return of a portfolio of stocks with a high book to-market ratio in excess of the return on a portfolio of stocks with a low book-to-market ratio

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/