(based on unaudited figures) - bank audi group – home presentation...other entities include: baf,...

TRANSCRIPT

1

INVESTORS’ PRESENTATIONSeptember 2016(based on unaudited figures)

2www.bankaudigroup.com

CONTENTS

GROUP OVERVIEW 4

MAIN DEVELOPMENT PILLARS 8

CONSOLIDATED FINANCIAL STANDING 14

MAIN STRATEGIC ORIENTATIONS 20

SHARE INFORMATION 21

APPENDIX 23

3www.bankaudigroup.com

DISCLAIMER

This presentation has been prepared by Bank Audi s.a.l. (“Bank Audi”); is for informationpurposes only and is intended only for the initial direct recipient hereof. It may not bereproduced or redistributed to any other person. It shall not and does not constitute either anoffer to purchase or buy or a solicitation to purchase or buy or an offer to sell or exchange or asolicitation to sell or exchange any securities of Bank Audi and neither this presentation noranything contained herein shall form the basis of any contract or commitment whatsoever.

Certain statements in this presentation may constitute “forward-looking statements”. Thesestatements appear in a number of places in this presentation and include statements regardingBank Audi’s intent, belief or current expectations.

These forward-looking statements can be identified by the use of forward-looking terminologysuch as “believes”, “expects”, “may”, “is expected to”, “will”, “will continue”, “should”,“approximately”, “would be”, “seeks” or “anticipates”; or similar expressions or comparableterminology, or the negatives thereof. Such forward-looking statements are not guarantees offuture performance and involve risks and uncertainties and actual results, performance orachievements of Bank Audi may differ materially from those expressed or implied in theforward-looking statements as a result of various factors. There are many factors which couldaffect Bank Audi’s actual financial results or results of operations and could cause actual resultsto differ materially from those in the forward-looking statements. In addition, even if BankAudi’s results of operations and financial condition and the development of the industry inwhich it operates are consistent with forward-looking statements contained herein, thoseresults, condition or developments may not be indicative of results or developments insubsequent periods. Bank Audi does not undertake to update any forward-looking statementsmade herein. Past results are not indicative of future performance.

While the information contained in this presentation and documenthas been prepared in good faith, no representation or warranty, express or implied, is or willbe made and no responsibility or liability is or will be accepted by Bank Audi or any of itssubsidiaries or affiliates or by any of their respective directors, officers, employees or agents asto or in relation to the accuracy or completeness thereof or for any loss arising from any usethereof and any and all such liability is expressly disclaimed. This document is not to be reliedupon as such in any manner as legal, tax or investment advice and shall not be used insubstitution for the exercise of independent judgment and each recipient hereof shall beresponsible for conducting its own investigation and analysis of the information containedherein. Except where otherwise indicated, the information provided in this document is basedon matters as they exist as of the date stated or, if no date is stated, as of the date ofpreparation and not as of any future date, and the information and opinions contained hereinare subject to change without notice.

None of Bank Audi or any of its subsidiaries or affiliates accepts any obligation to update orotherwise revise any such information to reflect information that subsequently becomesavailable or circumstances existing or changes occurring after the date hereof.

This presentation may not and will not be made directly or indirectly and may not be and willnot be distributed in any jurisdiction in which it is unlawful to make such presentation ordistribution under applicable laws and regulations. Persons whoattend any meeting at which this presentation is used or distributed or who otherwise receivethis presentation are required to make themselves aware of and adhere to any and allrestrictions applicable to them. In particular, this presentation may not be made in, and maynot be and will not be distributed, directly or indirectly, in or into the United States or to anyU.S. Person (as defined in Regulation S under the U.S. Securities Act of 1933, as amended “S”),other than as permitted by Regulation S, or to qualified institutional buyers as defined in and inaccordance with Rule 144A under the U.S.

Securities Act of 1933, as amended, and this document is not to be distributed, directly orindirectly, in Canada, Australia or Japan or to any citizen or resident of Canada, Australia orJapan.

This presentation may only be attended by, and this document may only be distributed to,persons in member states of the European Economic Area who are qualified investors withinthe meaning of Article 2(1)(E) of the Prospectus Directive (2003/7/EC) (including anyamendments thereto, including Directive 2010/73/EU, and including any relevant implementingmeasure in each relevant member state of the EEA) (“Qualified Investors”) and persons who (i)are outside the United Kingdom, (ii) who have professional experience in matters relating toinvestments, i.e. investment professionals within the meaning of Article 19(5) of the FinancialServices an Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”), and(c) are high net worth companies, unincorporated associations and other bodies to whom itmay otherwise lawfully be communicated in accordance with Article 49 (2)(a) to (d) of theOrder (all such persons, together with Qualified Investors, being referred to as “relevantpersons” ).

This presentation must not be acted on or relied on by persons who are not relevant personsand any investment or investment activity to which this presentation relates is available only torelevant persons and will be engaged in only with relevant persons.

The information contained herein must be kept strictly confidential and may not be reproducedor redistributed in any format to any person other than the initial direct recipient hereofwithout the express written approval of Bank Audi.

4www.bankaudigroup.com

Connecting customers to opportunitiesUS$ 125 billion of yearly inter –Arab trade turnover in 2015US$ 39 billion of yearly Turkish Arab trade turnover in 2015

COUNTRY COMPANY

Lebanon Bank Audi

Lebanon Audi Private Bank

Lebanon Audi Investment Bank

Switzerland Bank Audi (Suisse)

France Bank Audi France

Jordan Bank Audi - Jordan Network

Saudi Arabia Audi Capital

Egypt Bank Audi

UAE Bank Audi (Representative office)

Qatar Bank Audi

Monaco Audi Capital Gestion

Turkey Odea Bank

Iraq Bank Audi - Iraq Network

CORPORATE VALUESo INNOVATIONo TRANSPARENCYo HERITAGEo CIVIC ROLEo HUMAN CAPITALo QUALITY

Ranking by AssetsNo. 1 in Lebanon

No. 18 in MENA

GROUP OVERVIEW: COVERING THE EUROPE – MENAT CORRIDOR

1962

1967

1974

1975

1979

2004

2006

2006

2007

2007

2010

2012

2016

www.bankaudigroup.com

Main Development Pillars

5www.bankaudigroup.com

CORPORATE HIGHLIGHTS

o

o

o

o

o

o

o

o

o

Competitive National and Regional Positioning

GROUP OVERVIEW: CORPORATE & FINANCIAL HIGHLIGHTS

FINANCIAL HIGHLIGHTS IN U$ MILLION

6www.bankaudigroup.com

CORPORATE GOVERNANCEEthical conduct, Compliance, Anti-corruption,Risk management, Non-discriminationEnvironmental & Social Management System (ESMS)

ECONOMIC DEVELOPMENTProduct portfolio, Economic performance, Indirect economic impacts, Procurement practices, Market presence

COMMUNITY DEVELOPMENTLocal community developmentLocal community support

HUMAN DEVELOPMENTEmployment practices, Diversity & equal opportunityTraining, education, talent development, External human development

ENVIRONMENTAL PROTECTIONEmissions, Effluents & waste, Energy consumption, ESMS

GROUP OVERVIEW:CORPORATE AND SOCIAL RESPONSIBILITY (CSR) PILLARS

E & S MANAGEMENT

SYSTEM

IDENTIFICATION

SCREENING

CATEGORIZATION

ASSESSMENTAPPROVAL

MONITORING

REPORTING

7www.bankaudigroup.com

Notes to shareholders structure:1 Percentage ownership figures represent Common Shares owned by the named Shareholders and are expressed as a percentage

of the total number of Common Shares issued and outstanding. As at the date hereof, the Bank (and its affiliates) is thecustodian of Shares &/Or GDRs representing 68.21% of the Bank’s common shares;

2 Excluding members of the Audi Family accounted for in a separate row appearing above;3 Deutsche Bank Trust Company Americas holds Common Shares in its capacity as depositary under the Bank’s GDR Program. In

addition to the ownership of Common shares mentioned above, 10.6% of the Bank’s Common Shares are held through GDRs byeach of FRH Investment Holding Company s.a.l., The Audi Family, Sheikha Suad H. Al Homaizi, Sheikh Dhiab Bin Zayed Al-Nehayan, and the Al-Hobayeb Family (respectively, 2.30%, 0.92%, 1.81%, 3.13% and 2.44%). Information on GDR ownership isbased on self declarations (pursuant to applicable Lebanese regulations) as GDR ownership is otherwise anonymous to BankAudi.

CORPORATE GOVERNANCE

BOD Structure

10 Members 5 Executive directors 1 Shareholders representative 4 Independent directors

BOD Committees

Group Audit Committee Group Risk Committee Remuneration Committee Corporate Governance & Nomination Committee Group Executive Committee

ManagementCommittees

Asset-Liability Committee Anti-Money Laundering Committee Credit Committee Information Technology Strategic Committee Disclosure Committee

Set of Charters

Corporate Governance Guidelines Chart of Authorities Committees Charters

GROUP OVERVIEW: GOVERNANCE OF HOLDING BANK

8www.bankaudigroup.com

Main Development Pillars

GROUP OVERVIEW: MENAT OPERATING ENVIRONMENT

Nominal GDP 2016F (US$ billion)

Population 2016F (million)

Bank assets* (US$ billion)

*August2016 or latest available

Lebanon

Turkey

Egypt

MENA

9www.bankaudigroup.com

1 Including consolidation adjustments Lebanese entities include: Bank Audi Lebanon, AIB, Solifac, Gamma, other Lebanese entities and consolidation adjustmentsPrivate Banking entities include: APB, BAS, Audi Capital Gestion , BAQ and AC-KSA,Other entities include: BAF, other European entities, BAJO and BAIQ

LebaneseUniversal Bank

Lebanese UniversalBank with MENA

Footprints

Regional Universal Bank

-2004-

GROUP OVERVIEW: BUSINESS SEGMENTATION – THE DIVERSIFICATION TREND

ASSETS LOANS NET PROFITSIn US$ million

-2010- -2016-

10www.bankaudigroup.com

MAIN DEVELOPMENT PILLARS - LEBANONSTRONG

LEADERSHIP IN LEBANON

CURRENT STATUS

OPPORTUNITY

OUTLOOK

o Signals of domestic political settlement paving the way for Presidential elections and putting an end to a two and a half year constitutional vacuum

o Bolstered financial resilience on the back of the recent financial engineering operations of the Central Bank

o Large cyclical output gap between actual and potential output, suggesting pent up aggregate demand for goods and services

o Potential of gas and oil extraction reinforcing growth, investment and income per capita while apt to gradually contain public finance imbalances

o Universal banking profile with dominant positioning

o Largest retail accounts portfolio with an 18% market share supported by innovative technologies, products and services

o Banking with the top 100 corporates with dominant corporate and commercial loan market shares

o Market maker in trading operations with a turnover on Lebanese fixed income securities of US$ 8.5 billion in the first nine months of 2016 and an important market share in equity trading on the Beirut Stock Exchange

o Leverage on existing corporate relationship, expertise and regional presence to grow the regional business with a focus on trade

o Upgrade the SME financing proposition on track to become a high value driver for the Bank, capturing growth opportunities

o Focus on customer centric retail model supported by innovative delivery channels, state of the art technologies and tailored made products and services

1 Return on required regulatory capital

11www.bankaudigroup.com

MAIN DEVELOPMENT PILLARS - TURKEYROBUST

GROWTH WITH ENTICING

PROSPECTS

o A diversified and growing economy with favorable sovereign debt dynamics and improving trade linkage beyond the country’s traditional European markets

o Real GDP growth in 2015 equivalent to more than twice the average real GDP growth in emerging markets (excluding China and India), with a forecast of a robust growth to be sustained in 2016, despite challenges, and beyond

o Resilient domestic demand and strong fiscal buffers are easing the downside risks to economic activity despite recent political challenges

o A challenger bank profile with a universal product range

o 1.3% market share in assets, (1.7% in deposits and 1.4% in loans) in 4 years of average activity, ranking 9th in terms of assets and loans and 8th in terms of deposits among non-state owned conventional banks

o Optimized operating model supported by a good mix of people / products / technology, leading to best cost to assets to deposits ratios among peers

o Quick franchise building without incurring any goodwill expense, profitable after 19 months since launch

o Self-funded balance sheet structure leading to one of the lowest loan to deposit ratios in the sector

o Grow middle corporate and develop value-added SMEs and consumer segments

o Leverage on the Group’s wide footprint in the MENA region to capture cross-border opportunities, permitting to become the top MENA bank in Turkey and at the forefront of Turkish banks covering the region

o Sustain growing positive jaws, to quickly improve efficiency and profitability

CURRENT STATUS

OPPORTUNITY

OUTLOOK

12www.bankaudigroup.com

MAIN DEVELOPMENT PILLARS - EGYPT EXPANSIONOF NETWORK& PRODUCT

RANGE

CURRENT STATUS

OPPORTUNITY

OUTLOOK

o Gradual return of confidence since the start of the second transition, generating a noticeable turnaround in economic activity and investment

o State showing firm commitment to address macro challenges through the implementation of a series of reforms within the context of strong foreign support

o A stream of recent financing agreements (IMF, World Bank, bilateral, etc.) relatively easing Egypt’s external financing needs

o Macro outlook remain favorable on the overall in spite of monetary and price pressures (inflation and exchange rates)

o Real GDP growth to average close to 5% over the next 5 years, exceeding population growth, reinforcing per capital income and translating into double digit growth in banking aggregates

o Resilient to successive political transitions since 2011, sustaining solid growth trajectory outpacing peers with 20% CAGR in assets and 32% in net profits over the 2010-Sep16 period

o Sound credit policies focusing on defensive businesses translating into a NPL ratio of 1.4% well below the sector

o Efficient and profitable growing bank with an average ROAA and ROACE of 1.6% and 18% over the 2010-9M16 period

o New development plan encompassing the expansion of the network and extension of the scope of products and services to cover new business segments such as Islamic, mass affluent, mortgages and others

o Building on a visible and highly regarded brand, to achieve ambitious growth targets by 2019

13www.bankaudigroup.com

STRATEGY

OPPORTUNITY

MAIN DEVELOPMENT PILLARS – PRIVATE BANKINGSTRONG

EXPERTISE & KNOW-HOW

CURRENT STATUS

o The Middle East region continues to be second-fasted growing private banking market, trailing only to Asia

o Robust growing wealth pools fostering need for wealth and asset management services

o Wealth management industry currently in transition to accommodate increasing regulatory transparency requirements and related cost investment, allowing smaller and more agile institution to gain market shares

o Operates thru Banque Audi Suisse, the second largest Arab Private Bank based in Switzerland since the mid-70s and thru 2 main entities in Lebanon (Audi Private Bank) and Saudi Arabia (Audi Capital-KSA) with additional offices in Monaco, Qatar, Jordan and Abu Dhabi

o Full diversified offering with full access to major markets worldwide and global investment products including discretionary portfolio management, investment advisory, trade execution in all asset classes, structuring and management of Saudi and regional funds and other private banking services

o Deep-rooted in the MENA region, Bank Audi Private Bank also covers Sub-Saharan Africa (AuMs of US$ 1,075 million) and Latin America (US$ 1,162 million) through dedicated desks and RMs

o Recent restructuring of the business line to improve intergroup synergies and efficiencies

o Plan to establish a footprint in the United Kingdom and Singapore via partnership with Crossbridge Capital based in London, to create a centralized and specialized wealth management platform to support the private banking development strategy and future expansion to the greater Middle-East, Sub-Saharan Africa and Latin America

14www.bankaudigroup.com

1 o.w. US$ 642.9 million of exceptional net fees and commissions resulting from the Central Bank of Lebanon exchange transactions

2 o.w. US$ 217.9 million of exceptional expenses related to goodwill expenses and one-offs3 o.w. US$ 112.2 million of free provisions4 o.w. US$ 86.8 million of exceptional tax expense resulting from the Central Bank of Lebanon

exchange transactions 5 o.w. US$ 219.9 million of write off of investments in Syria and Sudan

CONSOLIDATED FINANCIAL STANDING: PERFORMANCE HIGHLIGHTS

INCOME STATEMENT IN US$ MILLIONASSETS & FOOTINGS IN US$ MILLION

1 Includes collective provisions of US$ 302 million in preparation for the application of IFRS 9

15www.bankaudigroup.com

CONSOLIDATED FINANCIAL STANDING: STEADY AND RESILIENT GROWTH

ASSETS IN US$ MILLION LOANS TO CUSTOMERS IN US$ MILLION CUSTOMERS’ DEPOSITS IN US$ MILLION

REVENUES & NET EARNINGS IN US$ MILLION EARNINGS PER COMMON SHARE IN US$ KEY PERFORMANCE METRICS

16www.bankaudigroup.com

LOANS BREAKDOWN BY ECONOMIC SECTOR

CONSOLIDATED FINANCIAL STANDING: LOAN PORTFOLIO BREAKDOWN (42% OF TOTAL ASSETS) – END SEPTEMBER 2016

LOANS BREAKDOWNBY COLLATERAL

Cash and bank

guarantee, 12.3%

Real estate mortgage,

25.9%

Securities, 5.5%

Personal guarantee,

28.4%

Unsecured, 27.9%

NET EXPOSURES BY DEVELOPMENT PILLARS

USD, 46.7%

TRY, 16.2%

EUR, 15.1%

EGP, 11.0%

LBP, 7.8%

JOD, 1.9%

OTHER, 1.3%

LOANS BREAKDOWNBY CURRENCY

LOANS BREAKDOWNBY CUSTOMERS’ TYPE

Corporate & commercial

clients, 62.2%

SMEs & small business

owners, 13.8%

Private & personal

clients, 6.3%

Retail & consumer

clients, 17.7%

LOANS BREAKDOWNBY MATURITY

Short-term facilities, (<1 year), 40.3%

Medium-term facilities, (1-3 years), 16.0%

Long-term facilities, (>3 years), 43.8%

17www.bankaudigroup.com

CONSOLIDATED FINANCIAL STANDING: LOAN QUALITY - END SEPTEMBER 2016

GROSS DOUBTFUL LOANS MOVEMENT IN US$ MILLION

SPLIT OF LLP CHARGES IN 9M-16 IN US$ MILLION

www.bankaudigroup.com

1.2%

1 As compared to an average of 3.7% in the MENA region, 7.0% in emerging markets and 6.2% in the world.

13.0%

18www.bankaudigroup.com

G10 Countries, 35.9%

MENA, 13.2%

Other Europe, 50.7%

Other, 0.1%

By Region

CONSOLIDATED FINANCIAL STANDING: LIQUIDITY & PORTFOLIO SECURITIES (55% of TOTAL ASSETS) - END SEPTEMBER 2016

LIQUIDITY PORTFOLIO SECURITIES

BREAKDOWN OF PLACEMENTS WITH BANKS BREAKDOWN OF PORTFOLIO SECURITIES BY CURRENCY & TYPE

Aaa to Aa3, 16.8%

A1 to A3, 22.1%

Baa1 to Baa3, 2.1%

Ba1 to B3, 51.7%

Below B3, 0.7%

Not Rated, 6.5%

By Rating 1

CB CDs51.2%

TBs in LL11.7%

Eurobonds in US$1.9%

TBs in TRY1.6%

TBs in EGP11.0%

Bonds in other FCY5.6%

Risk ceded leb eurobonds

10.5%

Equity instruments1.9%

Other fixed income instruments

4.7%

1 As per Basel requirement

19www.bankaudigroup.com

CONSOLIDATED FINANCIAL STANDING: CAPITALIZATION

CONSOLIDATED CAR AS PER BASEL III IN US$ MILLION CONSOLIDATED CAPITAL ADEQUACY RATIO EVOLUTION

ODEA BANK & BANK AUDI EGYPT CAR (AS PER LOCAL REGULATIONS)

1 Adjusted to account the collective provisions taken in anticipation of IFRS 9 application in 2018 in CET1 capital instead of Tier two capital,

2 When including the US$ 237 million of collective provisions on loans, the CET1 ratio would then reach 12.9% and the total CAR ratio 16.2%.

20www.bankaudigroup.com

o Preparing Turkey for its next stage of growtho Growth mode in Egypto Efficiency enhancement in Lebanono Re-organizing and expanding the Private Banking business line

o 3 main pillars: Lebanon, Turkey, Egypt.

o Growth strategy for the Private Banking business line through improved synergies across entities and enhanced operating model

o Medium term expansion plans under consideration, the United Kingdom (thru a light structure), Sub-Saharan Africa and Latin America

CURRENT STRATEGY

MAIN STRATEGIC ORIENTATIONS: POSITION THE GROUP AS A LEADING MENAT BANK

www.bankaudigroup.comMain Development Pillars

21www.bankaudigroup.com

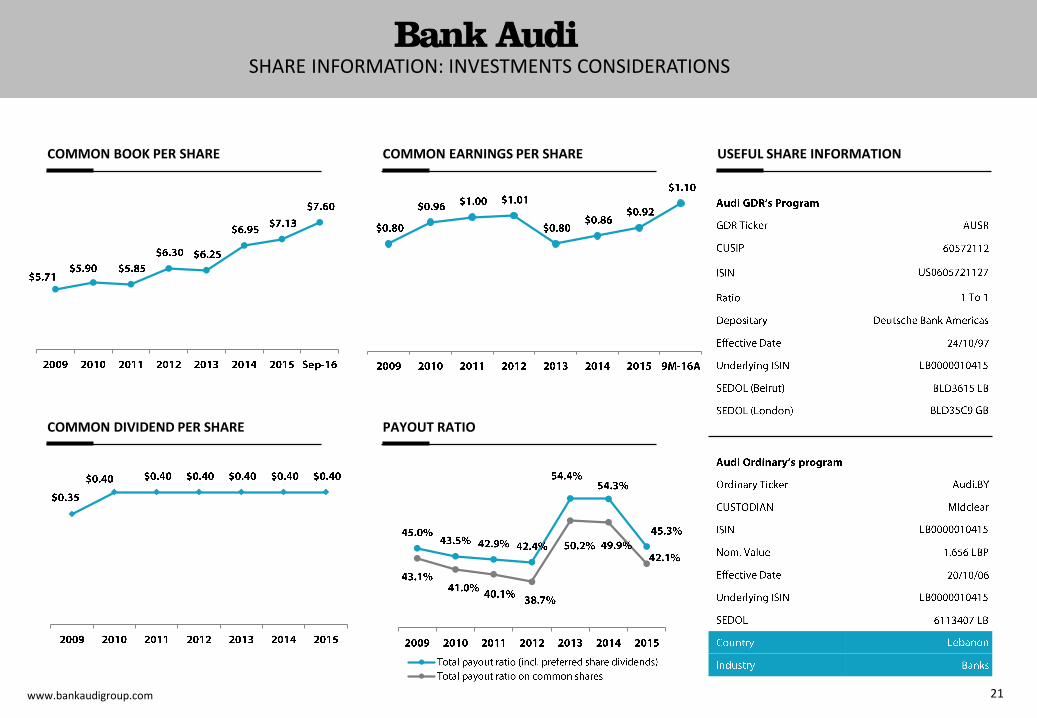

COMMON EARNINGS PER SHARE

SHARE INFORMATION: INVESTMENTS CONSIDERATIONS

COMMON BOOK PER SHARE

COMMON DIVIDEND PER SHARE PAYOUT RATIO

USEFUL SHARE INFORMATION

22www.bankaudigroup.com

SHARE INFORMATION: STOCK MARKET PERFORMANCE & RATIOS

GLOBAL AVERAGE

1.48

EMERGING MARKETS AVERAGE

2.20

MENA AVERAGE

1.45AUDI 1

0.9

PRICE TO BOOK AS AT OCTOBER 18th, 2016

GLOBAL AVERAGE

12.6

EMERGING MARKETS AVERAGE

13.3

MENA AVERAGE

9.6AUDI 1

6.3

PRICE TO EARNINGS AS AT OCTOBER 18th, 2016

GLOBAL AVERAGE

15.7%

EMERGING MARKETS AVERAGE

25.5%

MENA AVERAGE

16.3%AUDI 1

6.1%

PRICE TO ASSETS AS AT OCTOBER 18th, 2016

GLOBAL AVERAGE

3.4

EMERGING MARKETS AVERAGE

2.9

MENA AVERAGE

1.4AUDI 1

1.0

PEG RATIO AS AT OCTOBER 18th, 2016

Stock Market RatiosBank Audi v/s MENA Peers

1 Prices as at Oct 18, 2016 Sources: Bloomberg, Beirut Stock Exchange, Bank Audi’s Group Research Department 1 On the basis of a Bank Audi GDR price of US$ 6.40 on the Beirut

Stock Exchange as at 18/10/2016Sources: Bloomberg, Citigroup, IMF, Beirut Stock Exchange, Bank Audi’s Group Research Department

COMPARATIVE P/E RATIOS FOR BANKS1

Audi GDR 6.3x MENA 9.6x KSA 7.7x Qatar 11.6x

Audi Listed 6.1x Jordan 14.2x UAE 7.6x Bahrain 8.6x

Lebanon 6.8x Egypt 11.4x Kuwait 13.1x Oman 5.7x

23

APPENDIXwww.bankaudigroup.com

24www.bankaudigroup.com

FINANCIAL STATEMENTS: CONSOLIDATED STATEMENT OF FINANCIAL POSITION

1

2

3

4

1 After deduction of provisions amounting to US$ 629 million from loans and advances to customers as per IAS 39, of which US$ 237 million representing provisions on collective assessment;2 Loans granted to related parties against cash collateral amounted to US$ 118 million;3 Includes an amount of US$ 998 million with risk ceded to customers.4 Includes IFRS 9 collective provisions of USD 302 million taken in preparation for the application of IFRS 9

25www.bankaudigroup.com

FINANCIAL STATEMENTS: CONSOLIDATED PROFIT & LOSS STATEMENT

2014 9M-15 2015 9M-16

Interest & similar income

Interest & similar expenses

Net Interest Income

Non interest income

Total Operating Income

Net provisions for credit losses

Provision on impairment of financial instruments

Net Operating income

Personnel expenses

Other operating expenses

Depreciation of property & equipment

Amortization of intangible assets

Impairment of goodwill & investments

Total Operating Expenses

Profit Before Tax

Income tax

Profit After Tax

Net results from discontinued operations

= Profit After Tax and Discontinued Operations

Minority Interest

Net Profit - Minority Share

26

www.bankaudigroup.com