automotive monitor - great american group · honda chrysler toyota ford general motors ... the...

TRANSCRIPT

1 August 2014 — Automotive Monitor

1

Automotive Monitor

1 August 2014 — Automotive Monitor

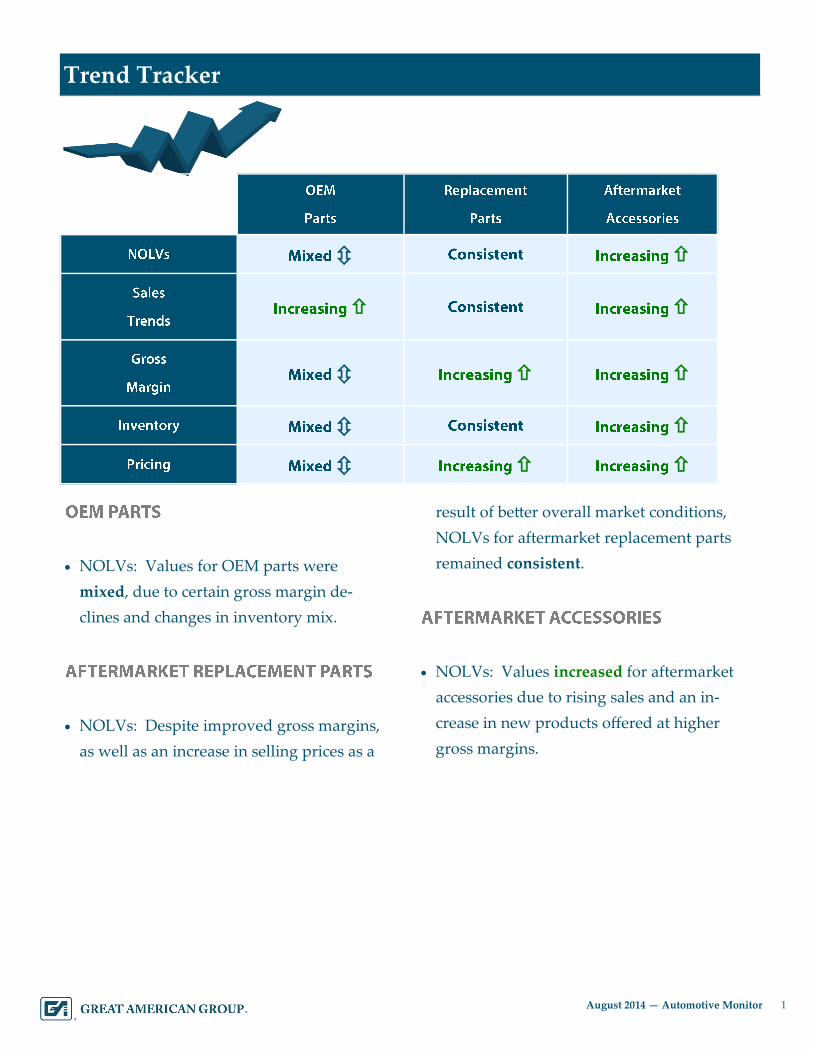

1 Trend Tracker

NOLVs: Values for OEM parts were

mixed, due to certain gross margin de-

clines and changes in inventory mix.

NOLVs: Despite improved gross margins,

as well as an increase in selling prices as a

result of better overall market conditions,

NOLVs for aftermarket replacement parts

remained consistent.

NOLVs: Values increased for aftermarket

accessories due to rising sales and an in-

crease in new products offered at higher

gross margins.

2 August 2014 — Automotive Monitor

2 Overview

Consistent sales increases set the tone for the

overall automotive industry, as a higher

number of new vehicles on the road translates

into higher demand for various OEM parts

and tires.

Additionally, as research continues to show

that the average age of cars on the road

hovers near peak levels, demand for

aftermarket parts is strong as well. As

consumers continue to hold onto cars longer,

the need for replacement and repair parts

increases.

Due to the discretionary nature of many

aftermarket accessories, demand for these

items are traditionally linked to disposable

incomes.

Recent reports indicate that consumer

spending in June 2014 witnessed modest

growth, following a similar increase in May.

Personal income exhibited a slight increase as

well, which bodes well for the U.S. economy

as a whole.

After getting off to a slow start in 2014 amid freezing winter

weather, the domestic automotive industry has proved to be a

consistently strong sector of the U.S. economy, with sales

continuing to rebound. In the first half of 2014, unit sales totaled

8.2 million vehicles, an increase of approximately 4.3% from the

same period of 2013. Experts originally projected sales to reach

16 million by year-end, yet are now projecting even higher totals.

3 August 2014 — Automotive Monitor

3 Overview

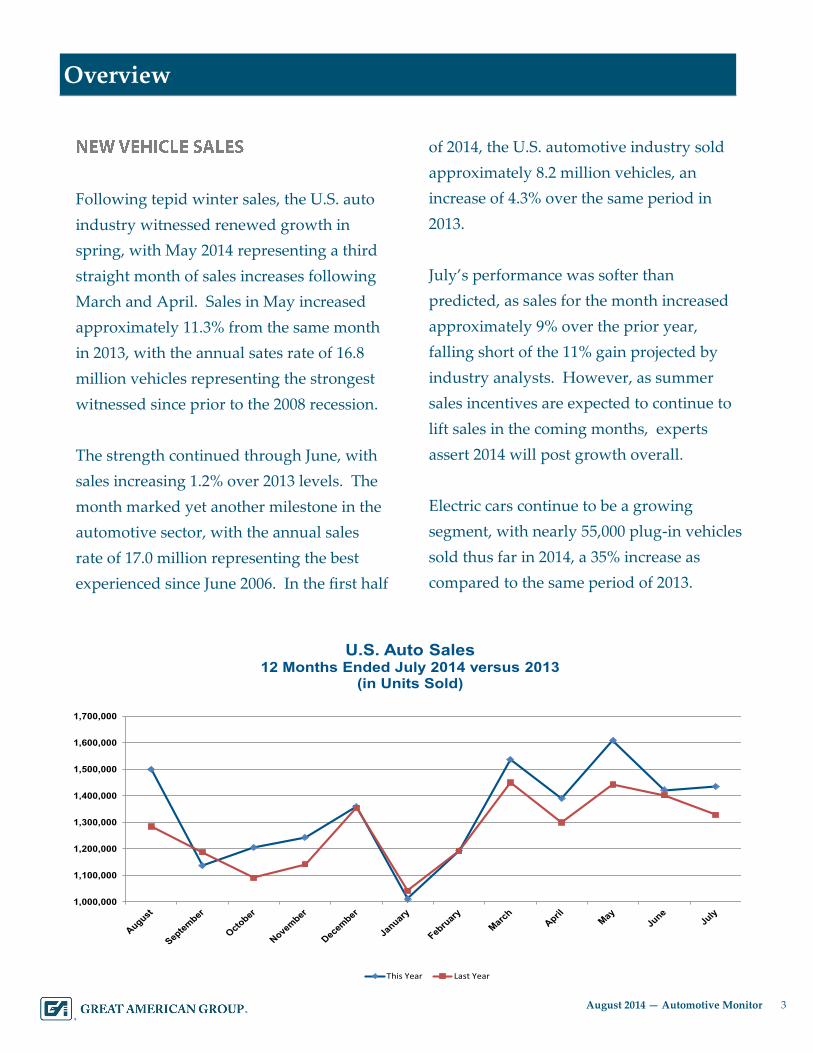

Following tepid winter sales, the U.S. auto

industry witnessed renewed growth in

spring, with May 2014 representing a third

straight month of sales increases following

March and April. Sales in May increased

approximately 11.3% from the same month

in 2013, with the annual sates rate of 16.8

million vehicles representing the strongest

witnessed since prior to the 2008 recession.

The strength continued through June, with

sales increasing 1.2% over 2013 levels. The

month marked yet another milestone in the

automotive sector, with the annual sales

rate of 17.0 million representing the best

experienced since June 2006. In the first half

of 2014, the U.S. automotive industry sold

approximately 8.2 million vehicles, an

increase of 4.3% over the same period in

2013.

July’s performance was softer than

predicted, as sales for the month increased

approximately 9% over the prior year,

falling short of the 11% gain projected by

industry analysts. However, as summer

sales incentives are expected to continue to

lift sales in the coming months, experts

assert 2014 will post growth overall.

Electric cars continue to be a growing

segment, with nearly 55,000 plug-in vehicles

sold thus far in 2014, a 35% increase as

compared to the same period of 2013.

1,000,000

1,100,000

1,200,000

1,300,000

1,400,000

1,500,000

1,600,000

1,700,000

U.S. Auto Sales12 Months Ended July 2014 versus 2013

(in Units Sold)

This Year Last Year

4 August 2014 — Automotive Monitor

4 Overview

According to a recent press release, Ford

sold over 212 thousand vehicles in July 2014,

which is a 10% increase from the previous

year and the company’s best performance in

eight years. The increase was attributed to

strong sales for its Ford Explorer and Ford

Fusion models, which posted gains of 32%

and 17% respectively. Its F-Series line of

pickup trucks continued to be popular

items, with sales increasing 5% at 63

thousand trucks sold for the month.

General Motors reported that unit sales

totaled 256,160 vehicles in July, which

represents a 9% increase from 2013 and its

best performance since 2007. Retail sales

increased 4%. Performance was strong

across the company’s brands, with every

GMC nameplate posting sales growth for

the month. Chevrolet-branded vehicles

witnessed an increase in deliveries of 8% in

July.

Chrysler Group reported its best July since

2005 with sales of 167,667 vehicles for the

month, representing a 20% increase from

2013. Jeep was the group’s strongest brand,

with sales increasing 41% from the same

month in 2013, representing the brand’s best

July sales in the company’s history. Ram

also performed well for the month, with

sales increasing 14%.

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 1,800,000

Suzuki

Ferrari

Maserati

Tesla

Porsche

Volvo

Jaguar-Land Rover

Mitsubishi

Mazda

Daimler

BMW

Subaru

Volkswagen

Kia

Hyundai

Nissan

Honda

Chrysler

Toyota

Ford

General Motors

U.S. Light Vehicle Retail SalesYear-to-Date July 2014 versus 2013

Year-to-Date - July 2013Year-to-Date - July 2014

Source: Autodata Corporation

5 August 2014 — Automotive Monitor

5 Recent Appraisal Trends

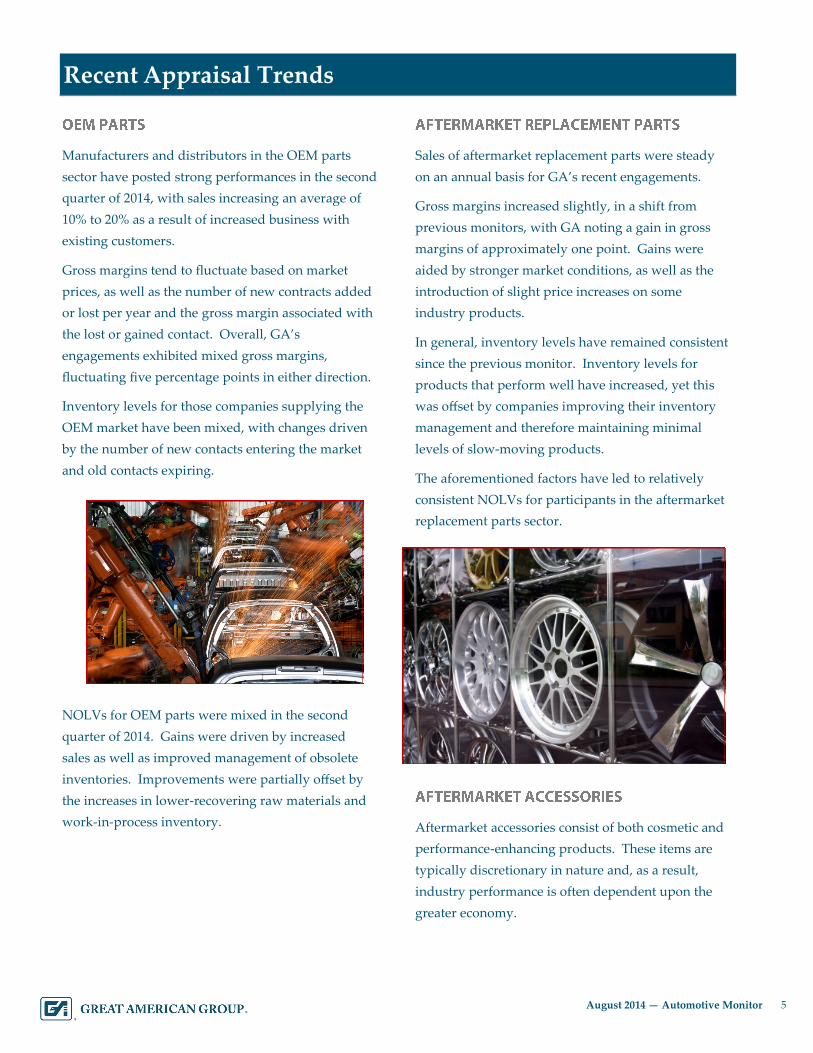

Manufacturers and distributors in the OEM parts

sector have posted strong performances in the second

quarter of 2014, with sales increasing an average of

10% to 20% as a result of increased business with

existing customers.

Gross margins tend to fluctuate based on market

prices, as well as the number of new contracts added

or lost per year and the gross margin associated with

the lost or gained contact. Overall, GA’s

engagements exhibited mixed gross margins,

fluctuating five percentage points in either direction.

Inventory levels for those companies supplying the

OEM market have been mixed, with changes driven

by the number of new contacts entering the market

and old contacts expiring.

NOLVs for OEM parts were mixed in the second

quarter of 2014. Gains were driven by increased

sales as well as improved management of obsolete

inventories. Improvements were partially offset by

the increases in lower-recovering raw materials and

work-in-process inventory.

Sales of aftermarket replacement parts were steady

on an annual basis for GA’s recent engagements.

Gross margins increased slightly, in a shift from

previous monitors, with GA noting a gain in gross

margins of approximately one point. Gains were

aided by stronger market conditions, as well as the

introduction of slight price increases on some

industry products.

In general, inventory levels have remained consistent

since the previous monitor. Inventory levels for

products that perform well have increased, yet this

was offset by companies improving their inventory

management and therefore maintaining minimal

levels of slow-moving products.

The aforementioned factors have led to relatively

consistent NOLVs for participants in the aftermarket

replacement parts sector.

Aftermarket accessories consist of both cosmetic and

performance-enhancing products. These items are

typically discretionary in nature and, as a result,

industry performance is often dependent upon the

greater economy.

6 August 2014 — Automotive Monitor

6 Recent Appraisal Trends

In general, sales increased on an annual basis,

approximately 5% to 10% year-over-year. The

increased sales can be attributed to an overall

improvement in market conditions, as well as a

rise in the number of new products offered.

Along with increased sales, gross margins

increased zero to two percentage points.

Margins were positively impacted by the

aforementioned improvement in market

conditions. Additionally, some industry

participants have introduced new products at

higher price points, which has positively

impacted margins.

Inventory levels for thus far in 2014 have

increased, with companies maintaining higher

inventory levels for those products which

perform well.

As a result of improvements in sales, gross

margins, and inventory mix, NOLVs for

aftermarket accessory parts increased for the

second quarter of 2014. However, the amount of

increased varied by participant, anywhere from

zero to five percentage points.

7 August 2014 — Automotive Monitor

7 Experience

GA has worked with and appraised numerous companies within the automotive industry.

While our clients remain confidential, they include companies throughout the automotive

supply chain, including manufacturers, importers, distributors, and retailers of aftermarket,

performance, replacement, and OEM parts and accessories.

GA’s extensive list of appraisal experience includes:

A remanufacturer and distributor of alternators

and starters for imported and domestic vehicles

with over $170 million in sales and over $60 mil-

lion in inventory, including $20 million of core

inventory.

A U.S.-based producer and recycler of automo-

tive and industrial lead acid batteries, with loca-

tions throughout North American and the world,

an inventory of approximately $200 million, and

sales of $1.2 billion.

An Internet retailer of aftermarket replacement

automotive parts, including auto body and en-

gine parts, as well as accessories, to customers

worldwide. The company’s $50 million of inven-

tory includes approximately 1.8 million types of

aftermarket auto parts for nearly all makes and

models of domestic and foreign cars and

trucks. The company’s nearly $300 million in

sales are primarily generated via hundreds of

websites.

OEM parts suppliers to the “big three” U.S. au-

tomakers, which includes manufacturers of

transmission, interior, wheel, and accessory

products.

A distributor of replacement passenger, light

truck, and commercial truck tires, including win-

ter, four-season, and high-performance tires.

A wholesale distributor and retailer of aftermar-

ket automotive parts and accessories, including

engine and exhaust components such as fuel in-

jectors, steering and suspension parts, oil and air

filters, performance parts, shock absorbers, chas-

sis parts, gaskets, water/fuel pumps, brake

drums and rotors, and other related aftermarket

automotive replacement parts.

A designer, manufacturer, and distributor of spe-

cialty products for the performance automotive

aftermarket, specializing in motorcycles and

boats, with products including fuel, air, and in-

ternal engine management systems, which are

designed to enhance vehicle performance

through generating increased horsepower and

torque.

GA has also liquidated a number of manufacturers and distributors of OEM

and aftermarket parts, including Midas Corporation, Trak Auto, Smittybilt

Outland Automotive Group, Inc., and American Products Company, Inc. In

addition to our vast liquidation and appraisal experience, GA maintains con-

tacts within the automotive industry that we utilize for insight and perspective

on recovery values.

8 August 2014 — Automotive Monitor

8 Monitor Information

The Automotive Monitor relates information covering most automotive products, including

industry trends, market pricing, and their relation to the valuation process. GA provides our

customer base with a concise document highlighting the automotive industry. GA strives to

contextualize important indicators in order to provide a more in-depth perspective of the

market as a whole. This publication will provide you with market value and industry trends

for a variety of products within the automotive sector.

GA internally tracks recovery ranges for parts, but we are mindful to adhere to your request

for a simple reference document. Should you need any further information or wish to discuss

recovery ranges for a particular segment, please feel free to contact your GA Business

Development Officer.

GA’s Automotive Monitor provides market value and industry trend information for a

variety of automotive products. The information contained herein is based on a composite

of GA’s industry expertise, contact with industry personnel, liquidation and appraisal

experience, and data compiled from a variety of well-respected sources believed to be

reliable. We do not guarantee the completeness of such information or make any

representation as to its accuracy.

9 August 2014 — Automotive Monitor

9 Appraisal & Valuation Team

Mark Weitz

President

(818) 884-3737

Ken Bloore

Chief Operating Officer

(818) 884-3737

Thomas Mitchell

Project Manager, Automotive Parts/Petroleum Specialist

(818) 746-9356

About Great American Group

Great American Group is a leading provider of asset disposition solutions and valuation and appraisal services to

a wide range of retail, wholesale, and industrial clients, as well as lenders, capital providers, private equity

investors, and professional services firms. In addition to the Automotive Monitor , GA also provides clients with

industry expertise in the form of monitors for the chemicals and plastics, metals, food, and building products

sectors, among many others. GA offers the European Automotive Monitor via its subsidiary, GA Europe

Valuations Limited.

Headquarters

21860 Burbank Blvd. Suite 300 South

Woodland Hills, CA 91367 800-45-GREAT www.greatamerican.com

Mike Marchlik

National Sales & Marketing Director

(818) 746-9306

David Seiden

Executive Vice President, Southeast Region

(770) 551-8114

Ryan Mulcunry

Executive Vice President - Northeast Region, Canada & Europe

(617) 692-8310

Bill Soncini

Senior Vice President, Midwest Region

(312) 777-7945

Drew Jakubek

Managing Director, Southwest Region

(972) 265-7981

Jennie Kim

Vice President, Western Region

(818) 746-9370

Dan Williams

Managing Director, New York Region

(646) 381-9221