auto dashboard april 2013

TRANSCRIPT

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 1/36

May 2013

DashboardThe Monthly Auto Update

Speedometer

12-month relative performance

April 2013 relative performance

Chirag Jain ([email protected]); + 91 22 3982 5418

Aggregate Volumes For April 2013*

Segment Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY13 FY12 Chg (%)

2-Wheelers 973,230 1,074,439 -9.4 909,966 7.0 1,007,966 1,098,338 -8.2

Motorcycl e 880,577 970,854 ‐9.3 809,267 8.8 915,313 994,753 ‐8.0

3‐Whe ele rs 52,100 46,829 11.3 39,018 33.5 52,100 46,829 11.3

Cars 102,252 115,405 ‐11.4 124,106 ‐17.6 102,252 115,405 ‐11.4

UVs 43,812 43,265 1.3 54,609 ‐19.8 43,812 43,265 1.3

Commercial Vehicles 51,198 50,787 0.8 79,989 -36.0 63,586 64,982 -2.1

LCV 31,628 29,768 6.2 49,916 ‐36.6 31,628 29,768 6.2

M&HCV 19,570 21,019‐6.9 30,073

‐34.9 31,958 35,214

‐9.2

Tractors 23,202 16,797 38.1 17,330 33.9 23,202 16,797 38.1

Total Volumes 1,245,794 1,347,522 -7.5 1,225,018 1.7 1,292,918 1,385,616 -6.7

* Aggrega te of Baja j, Hero, TVS Motor, Maruti, M&M, Tata Motors, Ash ok Leyland & Eicher Motors Source: Compa ny, MOSL

Investors are advised to refer through disclosures made at the end of the Research Report.

Jinesh Gandhi ([email protected]); +91 22 3982 5416

1

Data Track: April 2013 volume update of auto majors

Sector overview and outlook ........................................................... 2

Hero MotoCorp .................................................................................3

Bajaj Auto .......................................................................................... 4

Maruti Suzuki .................................................................................... 6

Mahindra & Mahindra ....................................................................... 8

Tata Motors ...................................................................................... 10

Ashok Leyland ................................................................................. 12

Eicher Motors .................................................................................. 13

TVS Motor ........................................................................................ 14

Special Report MARUTI SUZUKI: Internal target to grow volumes by 10-12% ....... 16

HMSI launches its cheapest motorcycle Dream Neo ..................... 19

Sector Gauge: March update

Two-wheelers ................................................................................. 21

Three-wheelers .............................................................................. 23

Cars and UVs .................................................................................... 25

Commercial vehicles ....................................................................... 27

News and Events ............................................................................... 30

Honda launches Amaze, to roll out UVs over two-three years

Royal Enfield starts new plant, targets to sell 175,000 units in CY13

Comparative Valuation

CMP * Rating

(INR) FY13E FY14E FY15E FY13E FY14E FY15E FY13E FY14E FY15E FY13E FY14E FY15E

Ba jaj Auto 1,860 Buy 18.0 15.1 13.0 12.5 9.9 8.2 44.7 44.0 41.8 61.8 61.5 57.0

Hero MotoCorp 1,613 Buy 15.2 14.3 10.5 9.3 8.2 6.8 45.6 41.9 48.0 43.6 50.8 60.6

M&M 955 Buy 15.3 12.2 9.8 9.5 7.7 6.1 22.0 20.5 20.1 24.2 24.5 24.1

Maruti Suzuki 1,680 Buy 21.0 14.6 12.1 10.5 7.2 5.6 12.9 15.9 16.5 15.5 19.5 20.3

Tata Motors 296 Buy 10.8 8.6 7.4 4.7 4.2 3.7 21.8 22.3 21.2 22.1 23.1 23.5

Ashok Leyland 23 Buy 22.0 13.4 9.3 10.2 7.7 6.6 6.6 10.5 14.6 8.0 10.3 12.6

Ei che r Mo tors # 3,046 B uy 25.3 26.6 18.7 20.7 18.5 11.3 20.3 17.1 21.4 22.9 17.5 23.7

* Price a s on 2nd Ma y 2013. # Nos. are on CY bas is Source: Compa ny, MOSL

P/E (x) EV/EBITDA (x) RoE (%) RoCE (%)

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 2/36

Dashboard

May 2013 2

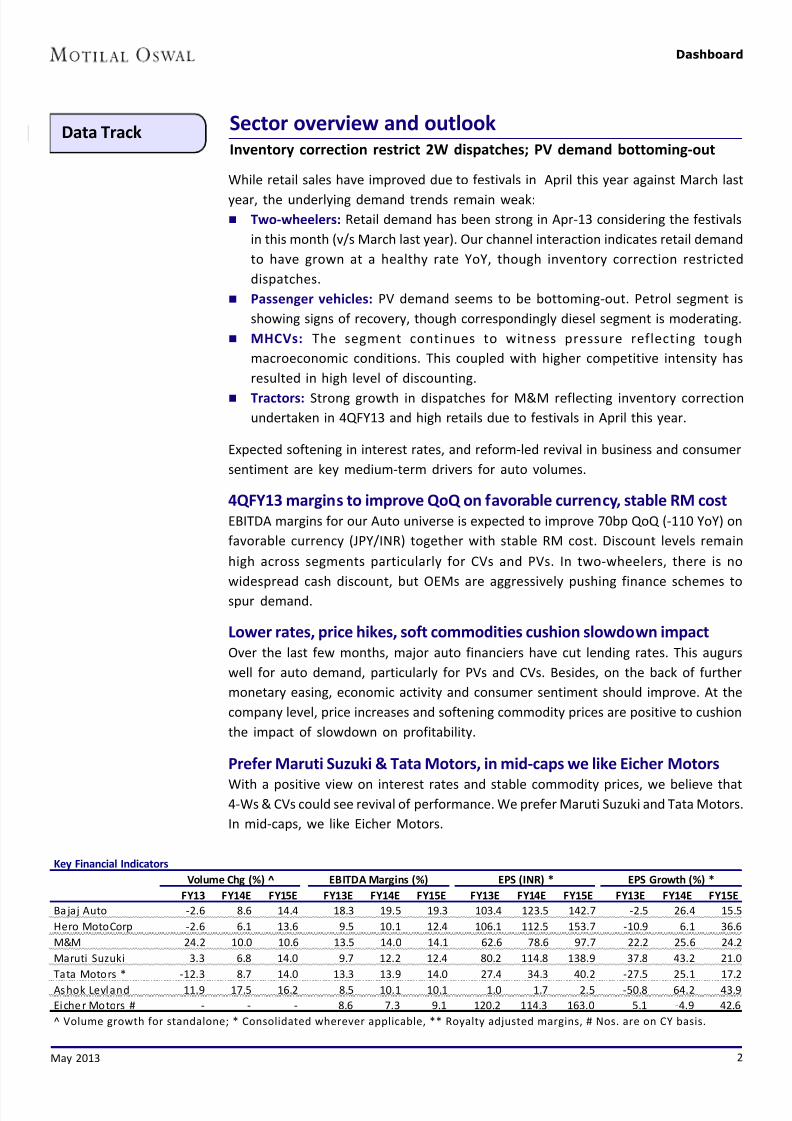

Sector overview and outlookInventory correction restrict 2W dispatches; PV demand bottoming-out

Data Track

While retail sales have improved due to festivals in April this year against March last

year, the underlying demand trends remain weak:

Two-wheelers: Retail demand has been strong in Apr-13 considering the festivals

in this month (v/s March last year). Our channel interaction indicates retail demand

to have grown at a healthy rate YoY, though inventory correction restricted

dispatches.

Passenger vehicles: PV demand seems to be bottoming-out. Petrol segment is

showing signs of recovery, though correspondingly diesel segment is moderating.

MHCVs: The segment continues to witness pressure reflecting tough

macroeconomic conditions. This coupled with higher competitive intensity has

resulted in high level of discounting.

Tractors: Strong growth in dispatches for M&M reflecting inventory correction

undertaken in 4QFY13 and high retails due to festivals in April this year.

Expected softening in interest rates, and reform-led revival in business and consumer

sentiment are key medium-term drivers for auto volumes.

4QFY13 margins to improve QoQ on favorable currency, stable RM cost

EBITDA margins for our Auto universe is expected to improve 70bp QoQ (-110 YoY) on

favorable currency (JPY/INR) together with stable RM cost. Discount levels remain

high across segments particularly for CVs and PVs. In two-wheelers, there is no

widespread cash discount, but OEMs are aggressively pushing finance schemes to

spur demand.

Lower rates, price hikes, soft commodities cushion slowdown impact

Over the last few months, major auto financiers have cut lending rates. This augurs

well for auto demand, particularly for PVs and CVs. Besides, on the back of further

monetary easing, economic activity and consumer sentiment should improve. At the

company level, price increases and softening commodity prices are positive to cushion

the impact of slowdown on profitability.

Prefer Maruti Suzuki & Tata Motors, in mid-caps we like Eicher Motors

With a positive view on interest rates and stable commodity prices, we believe that4-Ws & CVs could see revival of performance. We prefer Maruti Suzuki and Tata Motors.

In mid-caps, we like Eicher Motors.

Key Financial Indicators

FY13 FY14E FY15E FY13E FY14E FY15E FY13E FY14E FY15E FY13E FY14E FY15E

Ba jaj Auto -2.6 8.6 14.4 18.3 19.5 19.3 103.4 123.5 142.7 -2.5 26.4 15.5

Hero MotoCorp -2.6 6.1 13.6 9.5 10.1 12.4 106.1 112.5 153.7 -10.9 6.1 36.6

M&M 24.2 10.0 10.6 13.5 14.0 14.1 62.6 78.6 97.7 22.2 25.6 24.2

Maruti Suzuki 3.3 6.8 14.0 9.7 12.2 12.4 80.2 114.8 138.9 37.8 43.2 21.0

Tata Motors * -12.3 8.7 14.0 13.3 13.9 14.0 27.4 34.3 40.2 -27.5 25.1 17.2

Ashok Leyland 11.9 17.5 16.2 8.5 10.1 10.1 1.0 1.7 2.5 -50.8 64.2 43.9

Eiche r Motors # - - - 8.6 7.3 9.1 120.2 114.3 163.0 5.1 -4.9 42.6

^ Volume growth for standalone; * Consolidated wherever applicable, ** Royalty adjusted margins, # Nos. are on CY basis.

EPS (INR) * EPS Growth (%) *Volume Chg (%) ̂ EBITDA Margins (%)

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 3/36

Dashboard

May 2013 3

Data Track

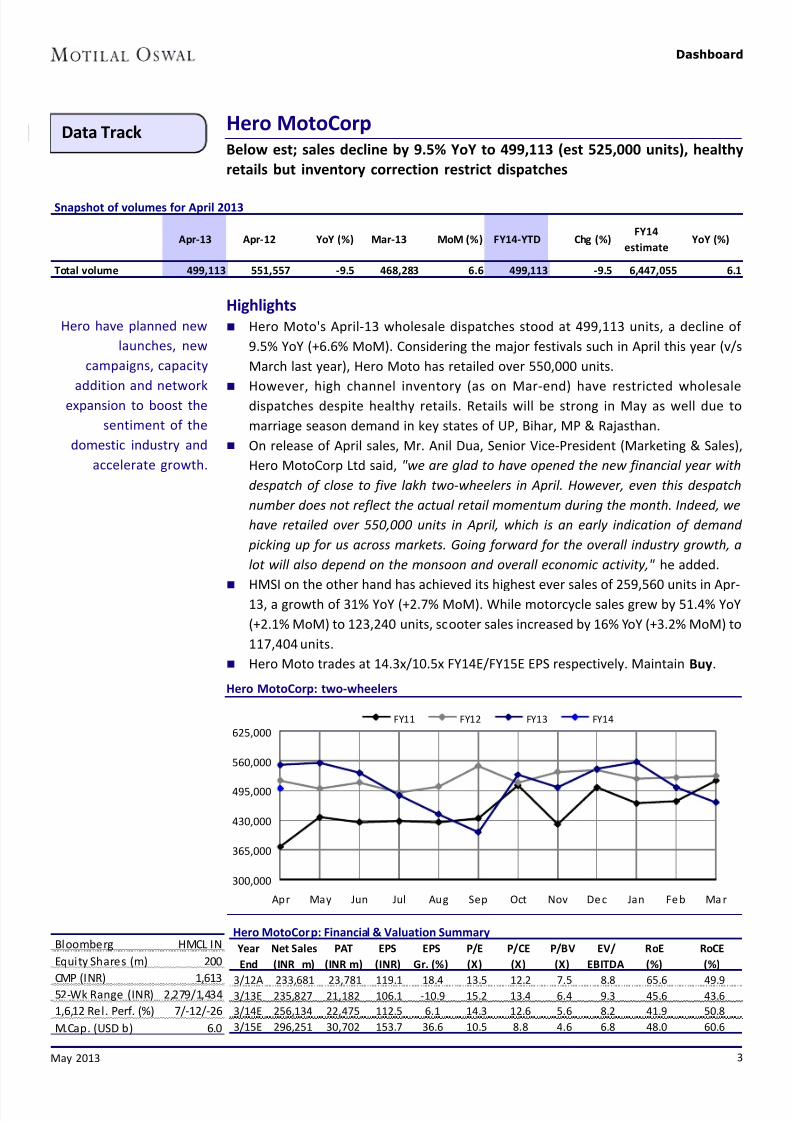

Hero MotoCorp: two-wheelers

Hero have planned new

launches, new

campaigns, capacity

addition and network

expansion to boost the

sentiment of the

domestic industry and

accelerate growth.

Hero MotoCorpBelow est; sales decline by 9.5% YoY to 499,113 (est 525,000 units), healthy

retails but inventory correction restrict dispatches

Highlights

Hero Moto's April-13 wholesale dispatches stood at 499,113 units, a decline of

9.5% YoY (+6.6% MoM). Considering the major festivals such in April this year (v/s

March last year), Hero Moto has retailed over 550,000 units.

However, high channel inventory (as on Mar-end) have restricted wholesaledispatches despite healthy retails. Retails will be strong in May as well due to

marriage season demand in key states of UP, Bihar, MP & Rajasthan.

On release of April sales, Mr. Anil Dua, Senior Vice-President (Marketing & Sales),

Hero MotoCorp Ltd said, "we are glad to have opened the new financial year with

despatch of close to five lakh two-wheelers in April. However, even this despatch

number does not reflect the actual retail momentum during the month. Indeed, we

have retailed over 550,000 units in April, which is an early indication of demand

picking up for us across markets. Going forward for the overall industry growth, a

lot will also depend on the monsoon and overall economic activity," he added.

HMSI on the other hand has achieved its highest ever sales of 259,560 units in Apr-13, a growth of 31% YoY (+2.7% MoM). While motorcycle sales grew by 51.4% YoY

(+2.1% MoM) to 123,240 units, scooter sales increased by 16% YoY (+3.2% MoM) to

117,404 units.

Hero Moto trades at 14.3x/10.5x FY14E/FY15E EPS respectively. Maintain Buy.

Hero MotoCorp: Financial & Valuation Summary

Year Net Sales PAT EPS EPS P/E P/CE P/BV EV/ RoE RoCE

End (INR m) (INR m) (INR) Gr. (%) (X) (X) (X) EBITDA (%) (%)

3/12A 233,681 23,781 119.1 18.4 13.5 12.2 7.5 8.8 65.6 49.93/13E 235,827 21,182 106.1 -10.9 15.2 13.4 6.4 9.3 45.6 43.6

3/14E 256,134 22,475 112.5 6.1 14.3 12.6 5.6 8.2 41.9 50.8

3/15E 296,251 30,702 153.7 36.6 10.5 8.8 4.6 6.8 48.0 60.6

Bloomberg HMCL IN

Equity Shares (m) 200

CMP (INR) 1,61352-Wk Range (INR) 2,279/1,434

1,6,12 Rel. Perf. (%) 7/-12/-26

M.Cap. (USD b) 6.0

300,000

365,000

430,000

495,000

560,000

625,000

Apr May Jun Jul Aug Sep Oct Nov De c Jan Fe b Ma r

FY11 FY12 FY13 FY14

Snapshot of volumes for April 2013

Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY14-YTD Chg (%)FY14

estimateYoY (%)

Total volume 499,113 551,557 -9.5 468,283 6.6 499,113 -9.5 6,447,055 6.1

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 4/36

Dashboard

May 2013 4

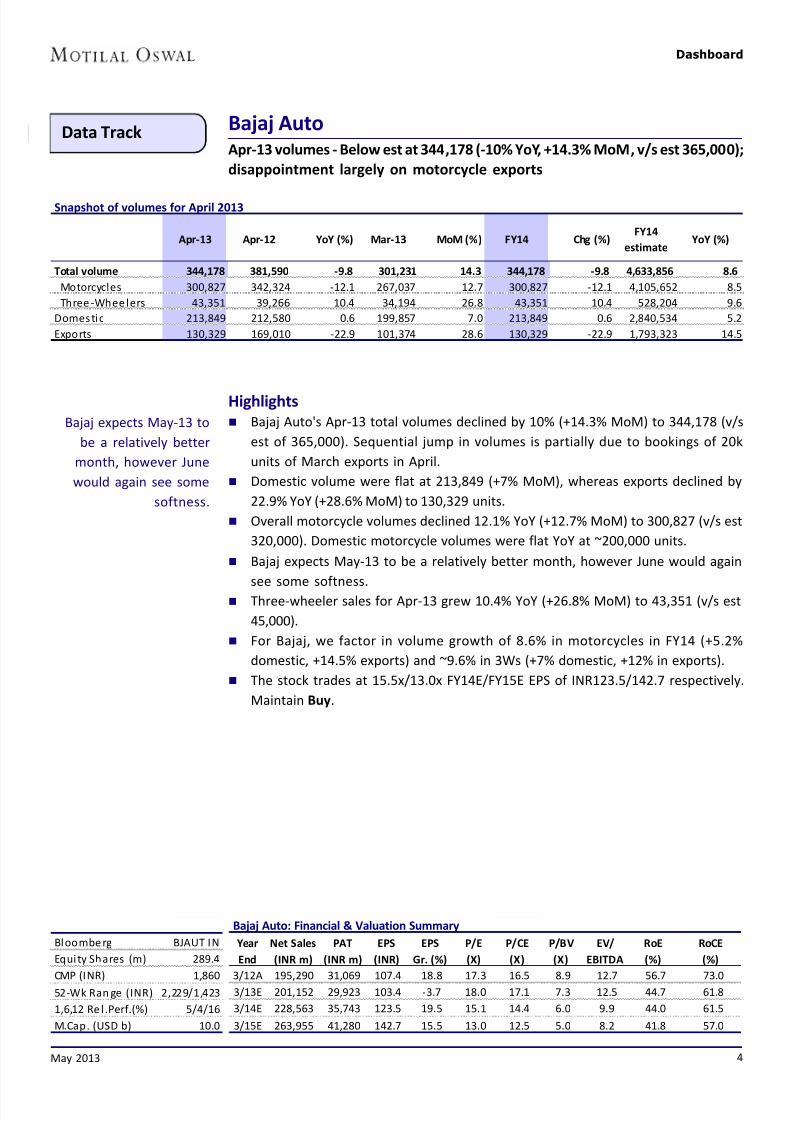

Bajaj AutoApr-13 volumes - Below est at 344,178 (-10% YoY, +14.3% MoM, v/s est 365,000);

disappointment largely on motorcycle exports

Data Track

Bloombe rg BJAUT IN

Equi ty Shares (m) 289.4

CMP (INR) 1,860

52-Wk Ran ge (INR) 2,229/1,423

1,6,12 Re l .Perf.(%) 5/4/16

M.Cap. (USD b) 10.0

Bajaj expects May-13 to

be a relatively better

month, however June

would again see some

softness.

Highlights

Bajaj Auto's Apr-13 total volumes declined by 10% (+14.3% MoM) to 344,178 (v/s

est of 365,000). Sequential jump in volumes is partially due to bookings of 20k

units of March exports in April.

Domestic volume were flat at 213,849 (+7% MoM), whereas exports declined by

22.9% YoY (+28.6% MoM) to 130,329 units.

Overall motorcycle volumes declined 12.1% YoY (+12.7% MoM) to 300,827 (v/s est

320,000). Domestic motorcycle volumes were flat YoY at ~200,000 units.

Bajaj expects May-13 to be a relatively better month, however June would again

see some softness.

Three-wheeler sales for Apr-13 grew 10.4% YoY (+26.8% MoM) to 43,351 (v/s est

45,000).

For Bajaj, we factor in volume growth of 8.6% in motorcycles in FY14 (+5.2%

domestic, +14.5% exports) and ~9.6% in 3Ws (+7% domestic, +12% in exports).

The stock trades at 15.5x/13.0x FY14E/FY15E EPS of INR123.5/142.7 respectively.

Maintain Buy.

Bajaj Auto: Financial & Valuation Summary

Year Net Sales PAT EPS EPS P/E P/CE P/BV EV/ RoE RoCE

End (INR m) (INR m) (INR) Gr. (%) (X) (X) (X) EBITDA (%) (%)

3/12A 195,290 31,069 107.4 18.8 17.3 16.5 8.9 12.7 56.7 73.0

3/13E 201,152 29,923 103.4 -3.7 18.0 17.1 7.3 12.5 44.7 61.8

3/14E 228,563 35,743 123.5 19.5 15.1 14.4 6.0 9.9 44.0 61.5

3/15E 263,955 41,280 142.7 15.5 13.0 12.5 5.0 8.2 41.8 57.0

Snapshot of volumes for April 2013

Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY14 Chg (%)FY14

estimateYoY (%)

Total volume 344,178 381,590 -9.8 301,231 14.3 344,178 -9.8 4,633,856 8.6

Motorcycles 300,827 342,324 -12.1 267,037 12.7 300,827 -12.1 4,105,652 8.5

Three -Whee lers 43,351 39,266 10.4 34,194 26.8 43,351 10.4 528,204 9.6

Domestic 213,849 212,580 0.6 199,857 7.0 213,849 0.6 2,840,534 5.2

Exports 130,329 169,010 -22.9 101,374 28.6 130,329 -22.9 1,793,323 14.5

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 5/36

Dashboard

May 2013 5

Exports under pressure

during the month

180,000

245,000

310,000

375,000

440,000

Apr Ma y Jun Ju l Aug Sep Oct Nov Dec Jan Feb Mar

FY11 FY12 FY13 FY14

24,000

31,000

38,000

45,000

52,000

Apr Ma y Jun Jul Aug Sep Oct Nov Dec Ja n Fe b Mar

FY11 FY12 FY13 FY14

40,000

80,000

120,000

160,000

200,000

Ap r May Jun Jul Aug Sep Oct No v De c Ja n Fe b Ma r

FY11 FY12 FY13 FY14

0%

25%

50%

75%

100%

A p r

‐ 1 0

M a y

‐ 1 0

J u n

‐

1 0

J u l

‐

1 0

A u g

‐ 1 0

S e p

‐

1 0

O c t

‐ 1 0

N o v

‐ 1 0

D e c

‐

1 0

J a n

‐

1 1

F e b

‐

1 1

M a r

‐ 1 1

A p r

‐ 1 1

M a y

‐ 1 1

J u n

‐

1 1

J u l

‐

1 1

A u g

‐ 1 1

S e p

‐

1 1

O c t

‐ 1 1

N o v

‐ 1 1

D e c

‐

1 1

J a n

‐

1 2

F e b

‐

1 2

M a r

‐ 1 2

A p r

‐ 1 2

M a y

‐ 1 2

J u n

‐

1 2

J u l

‐

1 2

A u g

‐ 1 2

S e p

‐

1 2

O c t

‐ 1 2

N o v

‐ 1 2

D e c

‐

1 2

J a n

‐

1 3

F e b

‐

1 3

M a r

‐ 1 3

A p r

‐ 1 3

Domestic Exports

Source: Company, MOSL

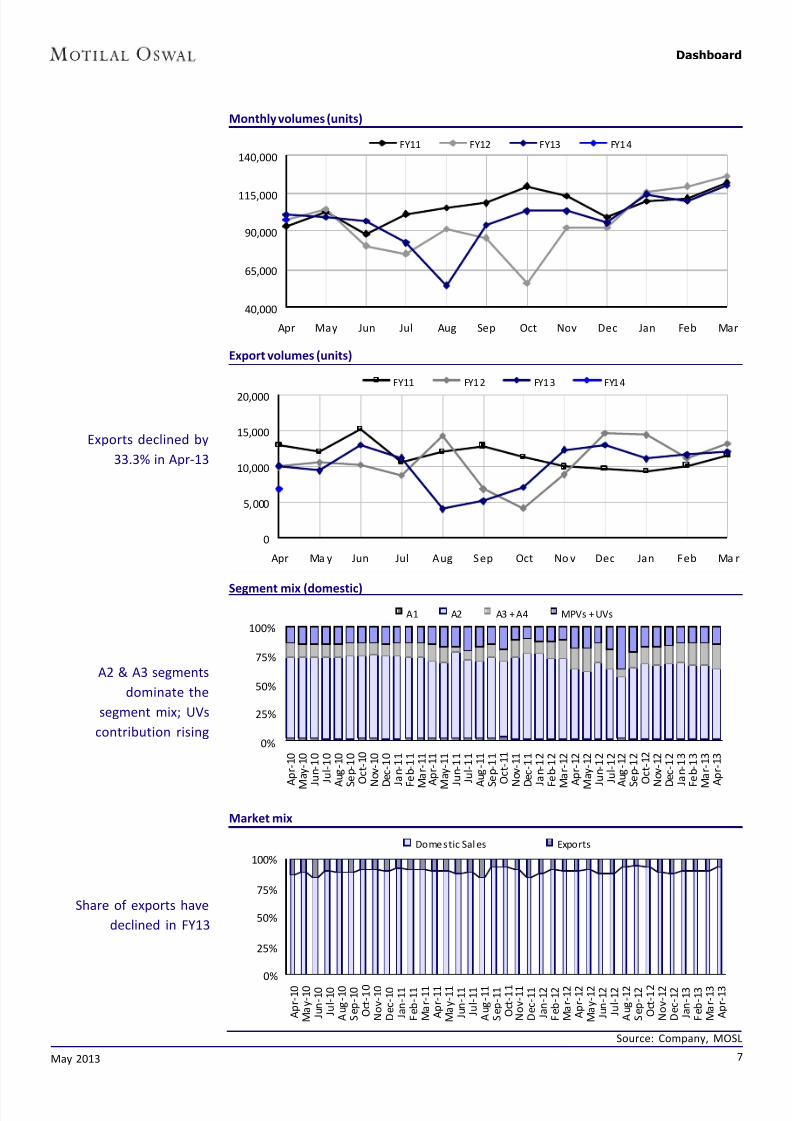

Three-wheeler volumes (units)

Two-wheeler volumes (units)

Discover and Pulsar

contribute ~70% to

two-wheeler volumes

Share of domestic sales

have increased in Apr-13

Market mix

Three-wheeler sales

sales bounces back

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 6/36

Dashboard

May 2013 6

Data Track Maruti SuzukiApr-13 volumes marginally below est at 97,302 units; Domestic sales in-line,

blip in exports temporary phenomena

Maruti Suzuki has been

gaining market share

over the last few months

led by steady deliveries

of diesel models (due to

bookings) and recovery in

petrol segment.

Bloomberg MSIL IN

Equity Shares (m) 302.1

CMP (INR) 1,68052-Wk Range (INR 1,690/1,052

1,6,12 Rel .Perf.(%) 30/16/22

M.Cap. (USD b) 9.4

Maruti Suzuki: Financial & Valuation Summary

Year Total Inc. PAT Con. EPS EPS Con. P/E P/CE P/BV EV/ RoE RoCE

End (INR m) (INR m) (INR) Gr. (%) (x) (x) (X) EBITDA (%) (%)

3/12A 355,871 16,351 58.2 -29.4 - - - - 10.8 13.23/13E 435,879 23,921 80.2 37.8 21.0 11.8 2.7 10.5 12.9 15.5

3/14E 481,250 34,284 114.8 43.2 14.6 8.9 2.3 7.2 15.9 19.5

3/15E 556,685 41,971 138.9 21.0 12.1 7.6 2.0 5.6 16.5 20.3

Highlights

Maruti's Apr-13 volumes de-grew by 3.1% YoY (-18.9% MoM) to 97,302 (v/s est

99,000 units).

While domestic volumes were flat YoY at 90,523 (v/s est 88,000), exports declined

by 33% YoY (-44% MoM) to 6,779 units. Management highlighted drop in export

volumes as a temporary phenomena and expects to recover next month onwards.

Dzire continues to perform strongly with 25% YoY growth to 19,446 units.

MSIL has guided for 5-6% industry growth for FY14. Our industry interaction

indicates that the company is internally targeting 10-12% growth in FY14 volumes.

Hyundai's domestic sales have declined by 7.6% YoY (-4.3% MoM). However,

exports have grown by 26% YoY (+8.7% MoM) to 24,551 units.

On release of April sales, Hyundai's Rakesh Srivastava (SVP - Sales & Marketing)

said "The exports have shown good growth on account of strong demand from

non-European markets, while the domestic market continues to witness

pressure...There are signs of recovery with the increase in demand for petrol cars".

Maruti Suzuki trades at 14.6x/12.1x FY14E/15E consolidated EPS and 8.9x/7.6x CEPS.

Maintain Buy.

Snapshot of volumes for April 2013

Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY14-YTD Chg (%)FY14

estimateYoY (%)

Total volume 97,302 100,415 -3.1 119,937 -18.9 97,302 -3.1 1,251,077 6.8

Domestic 90,523 90,255 0.3 107,890 -16.1 90,523 0.3 1,116,534 6.2

A1 1,500 1,705 -12.0 2,050 -26.8 1,500 -12.0

C 8,696 11,723 -25.8 9,506 -8.5 8,696 -25.8

A2 54,962 55,087 -0.2 68,865 -20.2 54,962 -0.2

A3 20,047 16,144 24.2 20,981 -4.5 20,047 24.2

A4 0 3 NA 0 NA 0 NA

UV 5,318 5,593 -4.9 6,488 -18.0 5,318 NA

Export 6,779 10,160 -33.3 12,047 -43.7 6,779 -33.3 134,542 11.8

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 7/36

Dashboard

7

Export volumes (units)

Segment mix (domestic)

Source: Company, MOSL

Monthly volumes (units)

Exports declined by

33.3% in Apr-13

A2 & A3 segments

dominate the

segment mix; UVs

contribution rising

Share of exports have

declined in FY13

Market mix

40,000

65,000

90,000

115,000

140,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

FY11 FY12 FY13 FY14

0%

25%

50%

75%

100%

A p r - 1 0

M

a y - 1 0

J u n - 1 0

J u l - 1 0

A

u g - 1 0

S

e p - 1 0

O c t - 1 0

N

o v - 1 0

D

e c - 1 0

J a n - 1 1

F

e b - 1 1

M

a r - 1 1

A p r - 1 1

M

a y - 1 1

J u n - 1 1

J u l - 1 1

A

u g - 1 1

S

e p - 1 1

O c t - 1 1

N

o v - 1 1

D

e c - 1 1

J a n - 1 2

F

e b - 1 2

M

a r - 1 2

A p r - 1 2

M

a y - 1 2

J u n - 1 2

J u l - 1 2

A

u g - 1 2

S

e p - 1 2

O c t - 1 2

N

o v - 1 2

D

e c - 1 2

J a n - 1 3

F

e b - 1 3

M

a r - 1 3

A p r - 1 3

A1 A2 A3 + A4 MPVs + UVs

0%

25%

50%

75%

100%

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

D e c - 1 0

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

J a n - 1 2

F e b - 1 2

M a r - 1 2

A p r - 1 2

M a y - 1 2

J u n - 1 2

J u l - 1 2

A u g - 1 2

S e p - 1 2

O c t - 1 2

N o v - 1 2

D e c - 1 2

J a n - 1 3

F e b - 1 3

M a r - 1 3

A p r - 1 3

Domestic Sal es Exports

0

5,000

10,000

15,000

20,000

Apr Ma y Jun Jul Aug Sep Oct No v Dec Jan Feb Ma r

FY11 FY12 FY13 FY14

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 8/36

Dashboard

May 2013 8

Mahindra and Mahindra: Financial & Valuation Summary

Year Net Sales S/A PAT * S/A EPS * Cons. Con. EPS P/E Cons. RoE RoCE EV/ EV/

End (INR m) (INR m) (INR) EPS (INR) Gr (%) (x) P/E (x) (%) (%) Sales (x) EBITDA

3/12A 318,535 28,888 48.3 51.2 6.6 19.8 18.6 23.0 23.1 0.0 0.0

3/13E 404,238 34,797 58.1 62.6 22.2 16.4 15.3 22.0 24.2 1.1 9.5

3/14E 457,392 38,596 64.5 78.6 25.6 14.8 12.2 20.5 24.5 0.9 7.7

3/15E 518,648 44,592 74.5 97.7 24.2 12.8 9.8 20.1 24.1 0.7 6.1

* S/A includi ng MVML

Data Track Mahindra & MahindraApr-13 volumes: Above est; Tractor volume surprises with 38% YoY growth,

growth in Auto disappoints with marginal growth of 2% YoY

"We are happy with the

38% growth which we

have achieved during

April 2013. We feel that

this is on the back of

improved market

sentiments. In addition

the expectation of a

normal monsoon is clearly

being seen as a positiveindicator" said Rajesh

Jejurikar, Chief Executive,

Farm Equipment Sector,

on release of tractor

sales.

Bloomberg MM IN

Equi ty Sha res (m) 587.2

CMP (INR) 955

52-Wk Range ( INR) 975/622

1,6,12 Rel .Perf.(%) -3/-1/14

M.Cap. (USD b) 10.6

Highlights M&M's Apr-13 Tractor volumes grew by 38% YoY (+33.9% MoM) to 23,202 units

(v/s 17,250 units). The company mentioned such high growth is due to improved

market sentiments (led by festivals in this month). Our channel interaction

indicates inventory build-up as well, apart from healthy retails, post the inventory

correction undertaken in 4QFY13. For FY14, we forecast a growth of 7% for M&M's

tractor volumes.

Auto volumes grew marginally by 2% YoY (-20% MoM) to 41,432 units (v/s est

~45,338 units). UVs & Pick-ups segment grew by 6.6% YoY (-19.7% MoM) to 35,742

units, against our expectation of 38,225 units. Growth in passenger UVs stood only

at 1% YoY, while SCVs (pick-ups) grew by 10% YoY to 14,414 units. Our industryinteraction indicates pressure across product segments except Bolero. Sales for

XUV5OO is estimated at 2,500 units (v/s FY13 avg of 3,800 units), while Xylo/Quanto

at 1,500 units. 3-wheeler volumes declined by 13.4% YoY (-16.5% MoM) to 4,036

(v/s est 5,032) units.

Pravin Shah, Chief Executive, Automotive Division, Mahindra & Mahindra Ltd.

said on release of monthly Auto division sales, "We are extremely disappointed

that the additional 3% excise duty on SUVs has not been reversed in the Finance Bill.

We remain cautiously optimistic of the current situation and do hope that with the

much awaited and needed reduction in interest rates announcement by the RBI

next week, the auto industry will look up. At Mahindra, we hope to create excitement

with the launch of the Verito Vibe and other product variants".

The stock trades at 12.2x/9.8x consol. FY14E/FY15E EPS of INR 78.6/97.7 respectively.

Maintain Buy.

Snapshot of volumes for April 2013

Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY14-YTD Chg (%)FY14

estimateYoY (%)

Total volume 64,634 57,516 12.4 69,234 -6.6 64,634 12.4 868,346 10.6

UV (incl . pick-ups) 35,742 33,531 6.6 44,527 -19.7 35,742 6.6 527,426 12.5

LCV (MNAL) 704 1,028 -31.5 1,335 -47.3 704 -31.5 13,001 10.0

Ve ri to 950 1,501 -36.7 1,211 -21.6 950 -36.7 18,011 15.0

Thre e-Wheele rs 4,036 4,659 -13.4 4,831 -16.5 4,036 -13.4 70,650 8.0

Tractors 23,202 16,797 38.1 17,330 33.9 23,202 38.1 239,259 7.0

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 9/36

Dashboard

May 2013 9

Tractor volume (units)

Tractor volumes grew by

38% YoY

Utility vehicle volumes (units)

Product mix

Source: Company, MOSL

Tractors and UVs

dominate the segment

mix, but we expect the

share of three wheelers

and LCVs to increase

Growth in UV volumes

have moderated in Apr-

13

12,000

21,000

30,000

39,000

48,000

Apr Ma y Jun Jul Aug Sep Oct Nov Dec Jan Feb Ma r

FY11 FY12 FY13 FY14

4,000

12,000

20,000

28,000

36,000

Apr Ma y Jun Jul Aug Sep Oct Nov De c Jan Fe b Mar

FY11 FY12 FY13 FY14

0%

25%

50%

75%

100%

A p r - 1 0

J u n - 1 0

A u g - 1 0

O c t - 1 0

D e c - 1 0

F e b - 1 1

A p r - 1 1

J u n - 1 1

A u g - 1 1

O c t - 1 1

D e c - 1 1

F e b - 1 2

A p r - 1 2

J u n - 1 2

A u g - 1 2

O c t - 1 2

D e c - 1 2

F e b - 1 3

A p r - 1 3

UVs Tractors LCVs , 3-wheelers Cars

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 10/36

Dashboard

May 2013 10

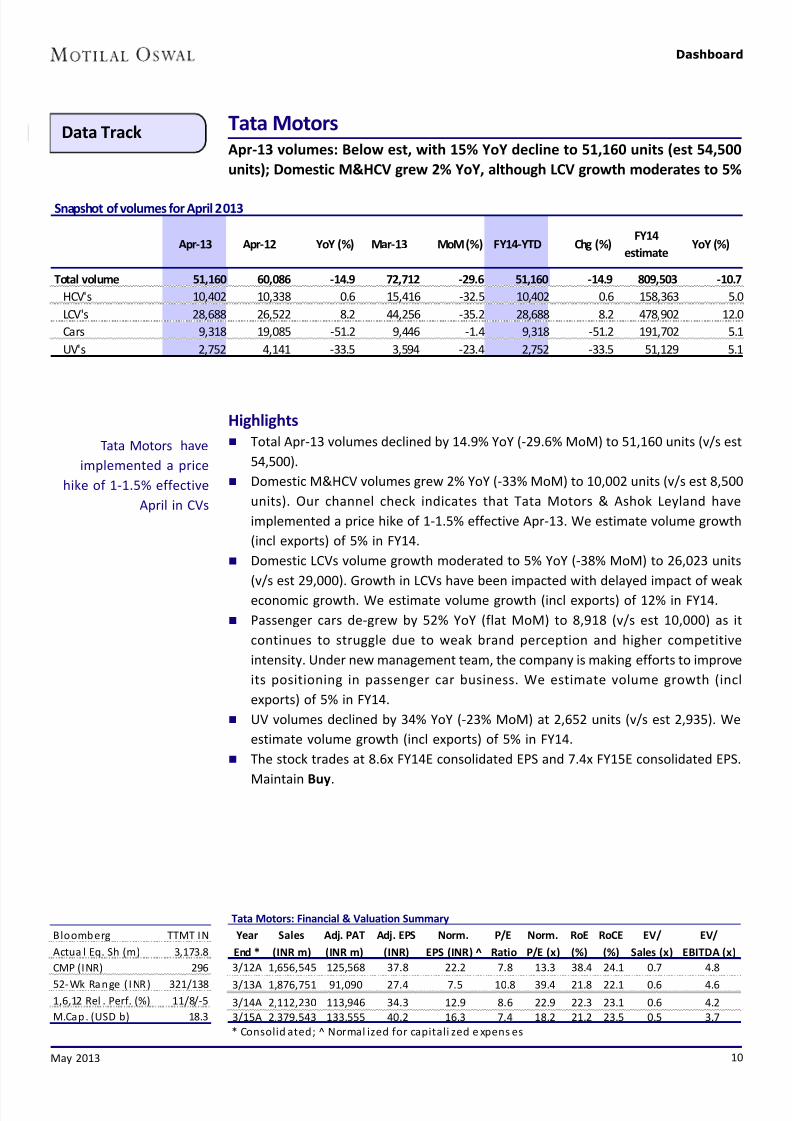

Data Track Tata MotorsApr-13 volumes: Below est, with 15% YoY decline to 51,160 units (est 54,500

units); Domestic M&HCV grew 2% YoY, although LCV growth moderates to 5%

Tata Motors have

implemented a price

hike of 1-1.5% effective

April in CVs

Highlights

Total Apr-13 volumes declined by 14.9% YoY (-29.6% MoM) to 51,160 units (v/s est

54,500).

Domestic M&HCV volumes grew 2% YoY (-33% MoM) to 10,002 units (v/s est 8,500

units). Our channel check indicates that Tata Motors & Ashok Leyland have

implemented a price hike of 1-1.5% effective Apr-13. We estimate volume growth

(incl exports) of 5% in FY14.

Domestic LCVs volume growth moderated to 5% YoY (-38% MoM) to 26,023 units

(v/s est 29,000). Growth in LCVs have been impacted with delayed impact of weak

economic growth. We estimate volume growth (incl exports) of 12% in FY14.

Passenger cars de-grew by 52% YoY (flat MoM) to 8,918 (v/s est 10,000) as it

continues to struggle due to weak brand perception and higher competitive

intensity. Under new management team, the company is making efforts to improve

its positioning in passenger car business. We estimate volume growth (incl

exports) of 5% in FY14.

UV volumes declined by 34% YoY (-23% MoM) at 2,652 units (v/s est 2,935). We

estimate volume growth (incl exports) of 5% in FY14.

The stock trades at 8.6x FY14E consolidated EPS and 7.4x FY15E consolidated EPS.

Maintain Buy.

Bloomberg TTMT IN

Actua l Eq. Sh (m) 3,173.8

CMP (INR) 296

52-Wk Range ( INR) 321/138

1,6,12 Rel . Perf. (%) 11/8/-5

M.Cap. (USD b) 18.3

Tata Motors: Financial & Valuation Summary

Year Sales Adj. PAT Adj. EPS Norm. P/E Norm. RoE RoCE EV/ EV/

End * (INR m) (INR m) (INR) EPS (INR) ̂ Ratio P/E (x) (%) (%) Sales (x) EBITDA (x)

3/12A 1,656,545 125,568 37.8 22.2 7.8 13.3 38.4 24.1 0.7 4.8

3/13A 1,876,751 91,090 27.4 7.5 10.8 39.4 21.8 22.1 0.6 4.6

3/14A 2,112,230 113,946 34.3 12.9 8.6 22.9 22.3 23.1 0.6 4.2

3/15A 2,379,543 133,555 40.2 16.3 7.4 18.2 21.2 23.5 0.5 3.7

* Consolid ated; ^ Normal ized for capitali zed e xpens es

Snapshot of volumes for April 2013

Apr-13 Apr-12 YoY (%) Mar-13 MoM (%) FY14-YTD Chg (%)FY14

estimateYoY (%)

Total volume 51,160 60,086 -14.9 72,712 -29.6 51,160 -14.9 809,503 -10.7

HCV's 10,402 10,338 0.6 15,416 -32.5 10,402 0.6 158,363 5.0

LCV's 28,688 26,522 8.2 44,256 -35.2 28,688 8.2 478,902 12.0

Cars 9,318 19,085 -51.2 9,446 -1.4 9,318 -51.2 191,702 5.1

UV's 2,752 4,141 -33.5 3,594 -23.4 2,752 -33.5 51,129 5.1

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 11/36

Dashboard

11

5,000

11,000

17,000

23,000

29,000

35,000

Ap r May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

FY11 FY12 FY13 FY14

LCV volumes (units)

Car volumes (units)

Source: Company, MOSL

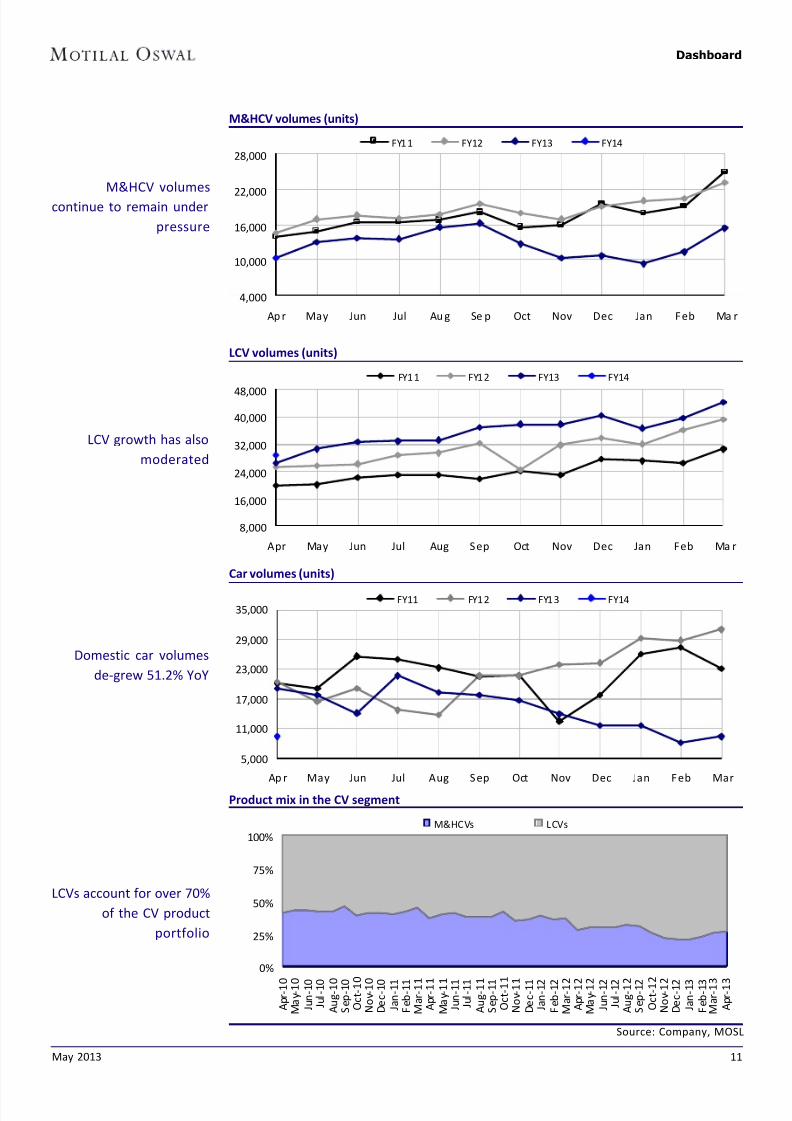

Product mix in the CV segment

LCV growth has also

moderated

Domestic car volumes

de-grew 51.2% YoY

M&HCV volumes (units)

M&HCV volumes

continue to remain under

pressure

LCVs account for over 70%

of the CV product

portfolio

4,000

10,000

16,000

22,000

28,000

Ap r May Jun Jul Au g Se p Oct Nov Dec Jan Feb Ma r

FY11 FY12 FY13 FY14

8,000

16,000

24,000

32,000

40,000

48,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Ma r

FY11 FY12 FY13 FY14

0%

25%

50%

75%

100%

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

D e c - 1 0

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

J a n - 1 2

F e b - 1 2

M a r - 1 2

A p r - 1 2

M a y - 1 2

J u n - 1 2

J u l - 1 2

A u g - 1 2

S e p - 1 2

O c t - 1 2

N o v - 1 2

D e c - 1 2

J a n - 1 3

F e b - 1 3

M a r - 1 3

A p r - 1 3

M&HCVs LCVs

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 12/36

Dashboard

May 2013 12

Data Track Ashok LeylandBelow est; MHCVs decline by 18.8% YoY to 5,251 (v/s 5,821), Dost volume grows

only by 1%

Ashok Leyland haveimplemented a price

hike of 1-1.5% and

discount reduction of 20-

25% MoM effective Apr-

13, as per our industry

interactions

Highlights

Ashok Leyland Apr-13 volumes declined by 13.8% YoY (-46.6% MoM) to 7,487 (v/s

est 8,686 units).

MHCVs registered a decline of 18.8% YoY (-45.8% MoM) to 5,251 units (v/s est

5,821 units) as weak economic growth impact freight availability and transporters

profitability. We estimate 6% growth in FY14 MHCV volumes.

Dost (LCV) sales at 2,236 units (v/s est 3,250 units), a growth of 1% YoY. We estimate

DOST volumes of 50,000 units in FY14.

With expected improvement in macro-economic environment, we expect MHCV

industry to recover in 2HFY14/FY15. AL, being pure play and second largest CV

player in India, is the best bet to play expected improvement in CV cycle.

The stock trades at 13.4x/9.3x FY14E/FY15E earnings of INR1.7/2.5 respectively.Maintain Buy.

Ashok Leyland: Financial & Valuation Summary

Year Net Sales PAT EPS EPS P/E P/BV RoE RoCE EV/ EV/

End (INR m) (INR m) (INR) Gr. (%) (x) (x) (%) (%) Sales (x) EBITDA (x)

3/11A 111,771 6,313 4.7 48.1 4.8 1.5 16.5 14.8 0.4 4.1

3/12A 128,420 5,660 2.1 -55.3 10.8 1.5 13.8 12.5 0.7 6.9

3/13E 123,590 4,155 1.0 -50.8 22.0 1.4 6.6 8.0 0.9 10.2

3/14E 141,214 4,564 1.7 64.2 13.4 1.4 10.5 10.3 0.8 7.7

3/15E 166,587 6,567 2.5 43.9 9.3 1.3 14.6 12.6 0.7 6.6

Bloomberg AL IN

Eq ui ty Sh are s (m) 2660.68

52-Wee k Range 33/20

1,6,12 Re l . Pe rf. (%) 4/-3/-29

M.Cap. (INR b) 61

M.Cap. (USD b) 1.1

Snapshot of volumes for April 2013

Apr‐13 Apr‐12 YoY (%) Mar‐13 MoM (%) FY14‐YTD Chg (%)FY14

estimateYoY (%)

Total volume 7,487 8,686 ‐13.8 14,020 ‐46.6 7,487 ‐13.8 134,547 17.5

CV (e x DOST SCV) 5,251 6,468 -18.8 9,695 -45.8 5,251 -18.8 84,547 6.0

DOST 2,236 2,218 0.8 4,325 -48.3 2,236 0.8 50,000 44.1

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 13/36

Dashboard

May 2013 13

Eicher MotorsAbove est, Buses continues to grow strongly with 41% YoY growth, decline in

LMD restricted to 11% (v/s 15.6% CY13-YTD)

Data Track

Royal Enfield continues

to enjoy average waiting

period of over 8-10

months across products.

Highlights

Eicher Motor's Apr-13 CV volumes declined 7% YoY (-11% MoM) to 3,917 units

(v/s est 3,638 units). Sales volumes were higher across segments v/s our estimates.

LMD segment declined by 10.6% YoY (-24.6% MoM) to 2,126 units. For CY13, we

estimate Eicher's LMD segment to decline by 12.8%.

HD volumes declined by 35.3% YoY (-42.2% MoM) to 506 units. For domestic HD

segment, we estimate 5.6% decline in CY13 for Eicher Motors due to challenging

macro-economic environment.

Bus volumes have increased by 41.4% YoY (+6.6% MoM) to 1,134 units. For CY13,

Eicher buses are expected to grow by 11.8%.

CY13 would witness the benefit in volumes from the start of bus body plant (in

1QFY13), commencement of medium duty engine project (3QCY13) and launch of

the new HD range in 4QCY13 (jointly developed by Eicher-Volvo).

Royal Enfield sales have grown by 42% YoY to 12,788 units. The company is targeting

sales of 175,000 units (v/s 113k units in CY12).

Eicher Motors trades at 26.6x/18.7x/13.7x CY13E/CY14E/CY15E EPS of INR 114.3/

163.0/222.5. Maintain Buy.

Snapshot of volumes for April 2013

Apr-13 Apr-12YoY (%)

chg

March1

3

MoM

(%) chgCY13

YTD (%)

chg

CY13

estimate

YoY (%)

chg

Residual

Growth

(%)

Residual

Monthly

Run rate

CY13

YTD

Monthly

Run rate

Royal Enfie ld 12,788 9,007 42.0 12,139 5.3 47,524 44.4 180,432 59.1 65.0 16,613 11,881

VECV 3,917 4,213 -7.0 4,962 -21.1 16,305 -11.4 44,497 -7.8 -5.6 3,524 4,076

Domes tic LMD 2,126 2,379 -10.6 2,820 -24.6 9,765 -15.6 25,762 -12.8 -11.0 2,000 2,441

Domestic HD 506 782 -35.3 876 -42.2 2,615 -14.9 7,268 -5.6 0.6 582 654

Domestic Buses 1,134 802 41.4 1,064 6.6 3,322 16.8 9,524 11.8 9.3 775 831

Total Domestic 3,766 3,963 -5.0 4,760 -20.9 15,702 -10.2 42,554 -7.0 -5.0 3,356 3,926

Exports 151 250 -39.6 202.0 -25.248 603 -34.6 1,944 -22.3 -15.1 168 151

Source: Compa ny, MOSL

Bloomberg EIM IN

Equity Sha res (m) 27.0

52-Wk Ra nge (INR) 3,240/1,620

1,6,12 Rel . Perf. (%) 3/26/56

M.Cap. (INR b) 72.7M.Cap. (USD b) 1.3

Eicher Motors: Financial & Valuation Summary

Year Net Sales PAT EPS EPS P/E P/BV RoE RoCE EV/EBITDA Div. Yld

End (INR b) (INR b) (INR) Gr (%) (x) (x) (%) (%) (x) (%)

12/12A 63.9 3.2 120.2 5.1 25.3 4.8 20.3 22.9 20.7 0.6

12/13E 71.7 3.1 114.3 -4.9 26.6 4.3 17.1 17.5 18.5 0.6

12/14E 95.3 4.4 163.0 42.6 18.7 3.7 21.4 23.7 11.3 0.912/15E 119.1 6.0 222.5 36.5 13.7 3.1 25.0 28.6 7.8 1.2

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 14/36

Dashboard

May 2013 14

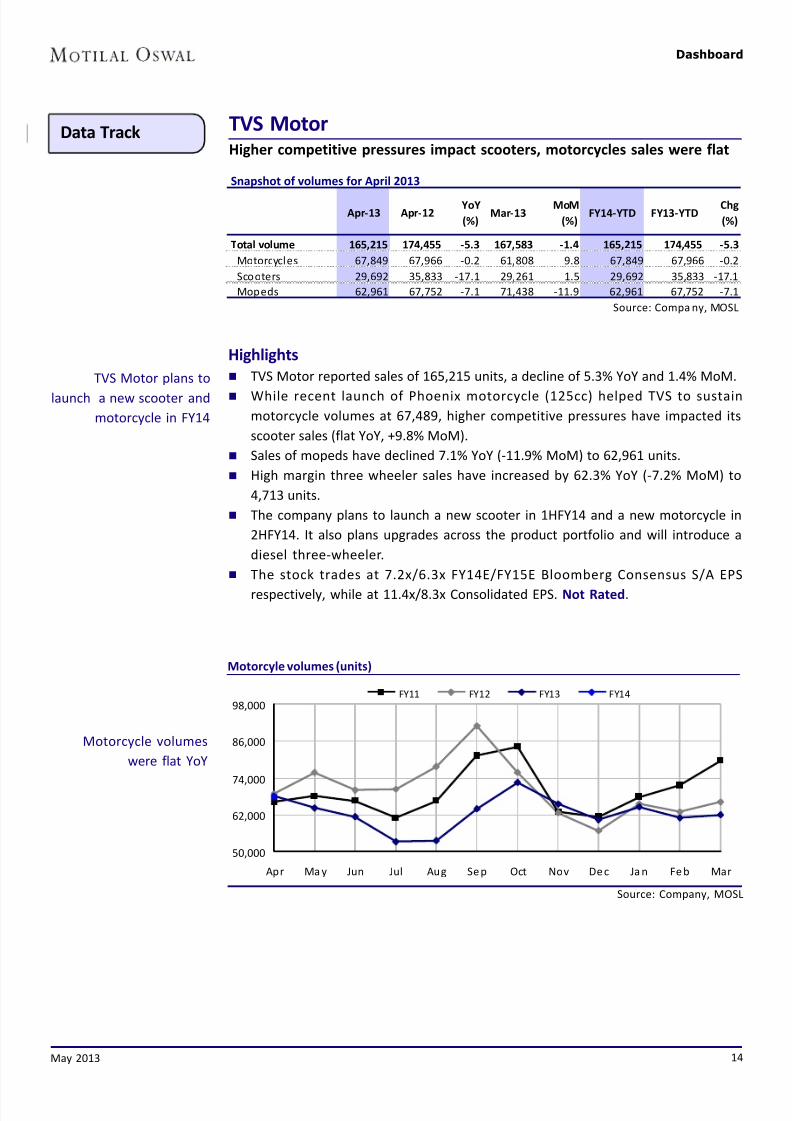

TVS MotorHigher competitive pressures impact scooters, motorcycles sales were flat

Data Track

Motorcyle volumes (units)

Motorcycle volumes

were flat YoY

Snapshot of volumes for April 2013

Apr‐13 Apr‐12YoY

(%)Mar‐13

MoM

(%)FY14‐YTD FY13‐YTD

Chg

(%)

Total volume 165,215 174,455 ‐5.3 167,583 ‐1.4 165,215 174,455 ‐5.3

Motorcycles 67,849 67,966 ‐0.2 61,808 9.8 67,849 67,966 ‐0.2

Scooters 29,692 35,833 ‐17.1 29,261 1.5 29,692 35,833 ‐17.1

Mopeds 62,961 67,752 ‐7.1 71,438 ‐11.9 62,961 67,752 ‐7.1

Source: Compa ny, MOSL

TVS Motor plans to

launch a new scooter and

motorcycle in FY14

Highlights

TVS Motor reported sales of 165,215 units, a decline of 5.3% YoY and 1.4% MoM.

While recent launch of Phoenix motorcycle (125cc) helped TVS to sustain

motorcycle volumes at 67,489, higher competitive pressures have impacted its

scooter sales (flat YoY, +9.8% MoM).

Sales of mopeds have declined 7.1% YoY (-11.9% MoM) to 62,961 units.

High margin three wheeler sales have increased by 62.3% YoY (-7.2% MoM) to

4,713 units.

The company plans to launch a new scooter in 1HFY14 and a new motorcycle in

2HFY14. It also plans upgrades across the product portfolio and will introduce a

diesel three-wheeler.

The stock trades at 7.2x/6.3x FY14E/FY15E Bloomberg Consensus S/A EPS

respectively, while at 11.4x/8.3x Consolidated EPS. Not Rated.

Source: Company, MOSL

50,000

62,000

74,000

86,000

98,000

Apr Ma y Jun Jul Aug Se p Oct Nov De c Ja n Fe b Mar

FY11 FY12 FY13 FY14

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 15/36

Dashboard

15

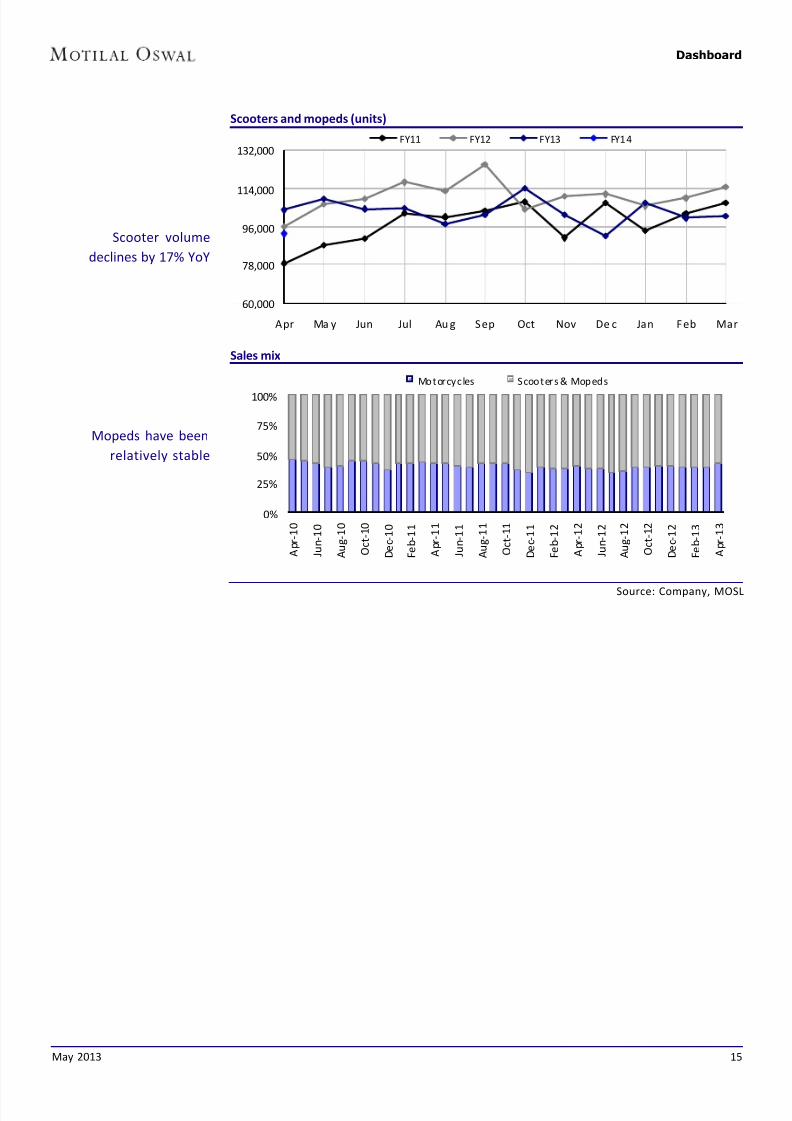

Scooters and mopeds (units)

Sales mix

Source: Company, MOSL

Mopeds have been

relatively stable

Scooter volume

declines by 17% YoY

0%

25%

50%

75%

100%

A p r - 1 0

J u n - 1 0

A u g - 1 0

O c t - 1 0

D e c - 1 0

F e b - 1 1

A p r - 1 1

J u n - 1 1

A u g - 1 1

O c t - 1 1

D e c - 1 1

F e b - 1 2

A p r - 1 2

J u n - 1 2

A u g - 1 2

O c t - 1 2

D e c - 1 2

F e b - 1 3

A p r - 1 3

Motorcycles Scooters & Mopeds

60,000

78,000

96,000

114,000

132,000

Apr Ma y Jun Jul Au g Sep Oct Nov De c Jan Feb Mar

FY11 FY12 FY13 FY14

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 16/36

Dashboard

16

Special Report MARUTI SUZUKI: Internal target to grow volumes by 10-

12% in FY14, against 5-6% industry growthRecovery in petrol segment to drive market share gains

We interacted with industry participants in the passenger vehicle space to get an update on

Maruti Suzuki's (MSIL) retail demand trends, discounts, inventory levels etc. Key takeaways:

MSIL has been gaining market share as: 1) Customers shift towards established brands

during uncertain times, 2) Strength of its experienced network and wide product portfolio,

3) Higher market share in the petrol segment (now recovering), 4) CNG offerings in key

markets (gaining traction over last few months), and 5) Higher exposure to relatively strong

rural market (15% growth in FY13, 28% of sales volumes).

Our industry interaction indicates that while MSIL is internally expecting industry growth of

5-6%, it is targeting 10-12% growth for itself in FY14 volumes.

While waiting period for popular models of Swift & Dzire have reduced on higher supplies,

our channel checks indicate there are no cash discounts on Swift/Dzire. Contrary to streetexpectations, Dzire still commands an average waiting of 1 month, though in metros/urban

markets it is available off the shelf due to higher competitive pressures.

While Honda has garnered healthy bookings for its recent launch of compact sedan Amaze,

our channel checks (even with Honda dealers) indicate that there are concerns on its interiors,

NVH (on diesel variant), lower pick-up compared to Dzire. While Amaze could perform

reasonably well due to its pricing, looks and Honda badge, it may not significantly impact

Dzire volumes.

While MSIL has not implemented a price hike in Apr-13, there has been seasonal reduction

in discounts in Apr-13 by 20-25% compared to Mar-13 levels.

While industry volumes continue to remain under pressure, MSIL is

estimated to report flat retail and wholesale dispatches for Apr-13.

The overall economic scenario and consequent consumer sentiments continues

to remain challenging.

However, our channel checks indicate that MSIL has been performing relatively

better than the PV Industry. Over the last few months, MSIL has been consistently

gaining market share.

Our channel interaction indicates that petrol car segment is witnessing higher

consumer interest with recent diesel de-regulation and continuous news flow ondiesel price hike.

Sustained increase in diesel prices could lead to meaningful shift towards petrol

segment, as per dealers. This would be beneficial to MSIL given its high exposure

towards petrol segment (entry level cars) and high discounts on petrol.

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 17/36

Dashboard

17

MSIL's market share have been on a rising trend MSIL has higher market share in petrol segment

MSIL internally targeting 10-12% growth in FY14 volumes, higher thanindustry volume growth expectation of 5-6%

While MSIL expects domestic industry volume growth of 5-6% in FY14, it is internally

targeting higher than industry growth at 10-12% in FY14 volumes.

MSIL has been gaining market share as 1) Customers shift towards established

brands during uncertain times, 2) Strength of its experienced/extensive network

and wide product portfolio, 3) Higher market share in the petrol segment (now

recovering), 4) CNG offerings in key markets of Delhi/Mumbai (gaining traction

over last few months), and 5) Higher exposure to relatively strong rural market

(15% growth in FY13, 28% of sales volumes).

Waiting period for popular diesel models have reduced on higher supplies;

Contrary to street expectations, Dzire still commands an average waiting

of 1 month

Strong response to new model launches (Swift, Dzire, Ertiga), shift of preference

towards diesel variants (due to differential fuel pricing) and lock-out at Manesar

led to huge order backlog for diesel variants of popular models for MSIL.

Post the normalization of Manesar operations, MSIL has been focusing on

increasing the supply of diesel variants of such popular models.

This has led to reduction in waiting period for diesel variants of Swift/Dzire and

almost NIL for Ertiga, while petrol variants of Swift/Dzire had come under waiting

list for few months.

Our channel interaction indicates that waiting period for Swift/Dzire have reduced

over the last few months on higher supplies.

However, Dzire continues to command a waiting period of average 1 month, though

in metros/urban markets it is available off the shelf on higher supplies (due to

relatively higher competitive pressures).

Despite declining waiting period, our channel checks indicate there are no cash

discounts on Swift/Dzire.

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 18/36

Dashboard

18

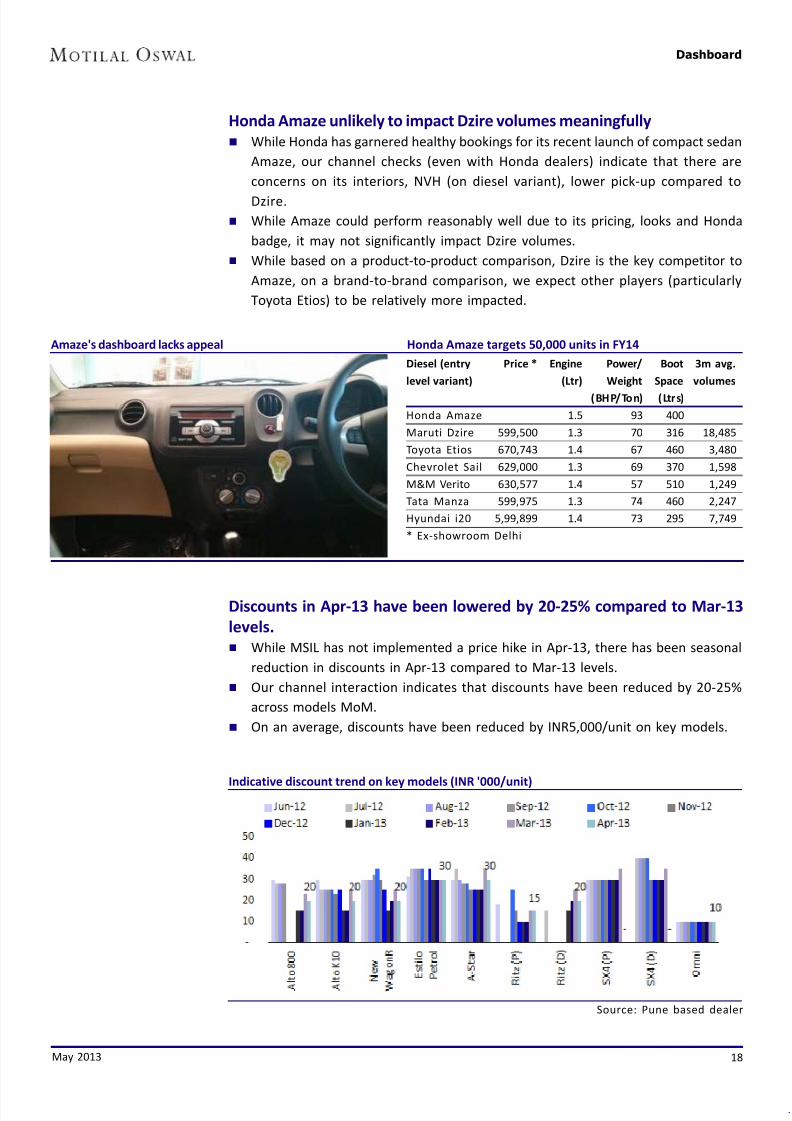

Honda Amaze unlikely to impact Dzire volumes meaningfully

While Honda has garnered healthy bookings for its recent launch of compact sedan

Amaze, our channel checks (even with Honda dealers) indicate that there are

concerns on its interiors, NVH (on diesel variant), lower pick-up compared to

Dzire.

While Amaze could perform reasonably well due to its pricing, looks and Honda

badge, it may not significantly impact Dzire volumes.

While based on a product-to-product comparison, Dzire is the key competitor to

Amaze, on a brand-to-brand comparison, we expect other players (particularly

Toyota Etios) to be relatively more impacted.

Amaze's dashboard lacks appeal Honda Amaze targets 50,000 units in FY14

Discounts in Apr-13 have been lowered by 20-25% compared to Mar-13

levels.

While MSIL has not implemented a price hike in Apr-13, there has been seasonal

reduction in discounts in Apr-13 compared to Mar-13 levels.

Our channel interaction indicates that discounts have been reduced by 20-25%

across models MoM.

On an average, discounts have been reduced by INR5,000/unit on key models.

Indicative discount trend on key models (INR '000/unit)

Source: Pune based dealer

Diesel (entry Price * Engine Power/ Boot 3m avg.

level variant) (Ltr) Weight Space volumes

(BHP/Ton) (Ltrs)

Honda Amaze 1.5 93 400

Maruti Dzire 599,500 1.3 70 316 18,485

Toyota Etios 670,743 1.4 67 460 3,480

Chevrolet Sail 629,000 1.3 69 370 1,598

M&M Verito 630,577 1.4 57 510 1,249

Tata Manza 599,975 1.3 74 460 2,247

Hyundai i20 5,99,899 1.4 73 295 7,749

* Ex-showroom Delhi

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 19/36

Dashboard

19

Special Report INDIA AUTO (2W): HMSI launches its cheapest new 110cc

motorcycle Dream Neo priced against Hero's SplendorHMSI aims to grow by 43% in FY14 to 3.93m units

HMSI has further expanded its product portfolio with the launch of 110cc motorcycle under

Dream series (Dream Neo) - its cheapest and most fuel efficient offering in India.

Dream Neo is priced at INR 43,150 (ex-showroom Delhi), INR2k cheaper than Dream Yuga

and similarly priced as Hero's Splendor (INR42,950, ex-showroom Delhi).

Dream Neo has the same engine (and looks) as Dream Yuga with marginally higher mileage

and lower power/torque than Dream Yuga. Dream Neo outputs a peak power of 8.36 PS at

7,500 rpm and a peak torque of 8.633 Nm at 5,500 rpm. These figures are slightly lower

than the 8.5 Bhp-8.91 Nm of Dream Yuga.

HMSI targets to grow by 150% in 100-110cc mass market segment in FY14. It is confident of

achieving 43% growth in FY14 to 3.93m units.

Talking about Honda's strategic direction, Mr. Keita Muramatsu - President & CEO, HMSI, said

"DREAM NEO is Honda's next big leap towards creating deep inroads into the Indian commuter

segment. Our newly opened Technical centre comprising of R&D, Engineering, Purchase &

Quality team, overcame the challenge of improving Mileage and meeting the competitive

price point. Backed by our new product launches & network expansion, Honda aims to grow

over 150% in 100-110cc motorcycle segment YoY. Overall, we are confident of customer

demand for Honda 2Wheelers and eye 43% growth with 39.3 lac unit sales in FY'14."

Elaborating on Dream Neo, Mr. Y. S. Guleria, Vice President - Sales & Marketing, HMSI, said

"Creating a new paradigm in mass mobility, DREAM NEO is Honda's Most Affordable and

Most Fuel Efficient 2Wheeler ever in India. While DREAM NEO is loaded with attractive & best

in class features like Top Mileage of 74 kmpl*, it is being delivered at a truly aggressive pricingto delight Indian customers. Finally DREAM NEO is a package which is hard to resist by 100-

110cc mass segment motorcycle customers".

Valuation & view: We expect two-wheeler volume recovery to be back-ended in

FY14, with near term volumes expected to remain weak. This coupled with HMSI's

continued expansion on capacity, dealer network and product portfolio would result

in sustained pressure on the domestic players. While valuations for both Hero

MotoCorp and Bajaj Auto are reasonable, demand recovery along with stability in

competitive intensity would be key driver for stock performance.

Honda Dream Neo

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 20/36

Dashboard

20

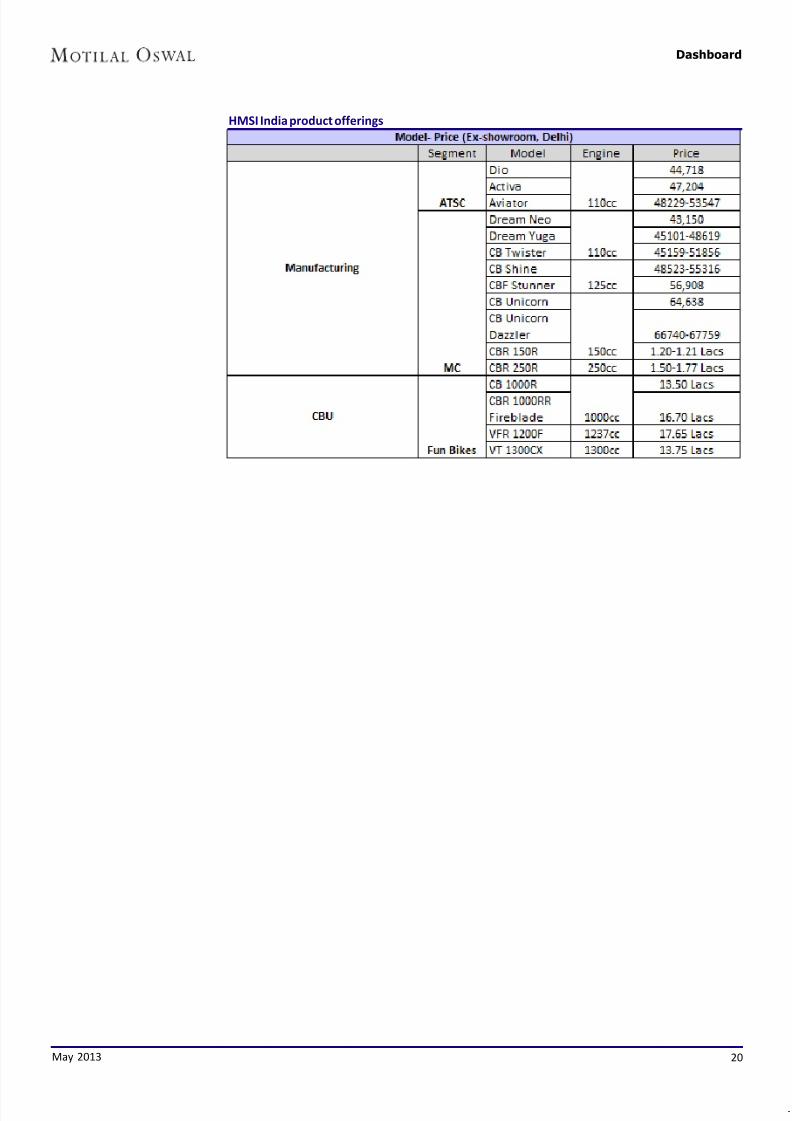

HMSI India product offerings

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 21/36

Dashboard

May 2013 21

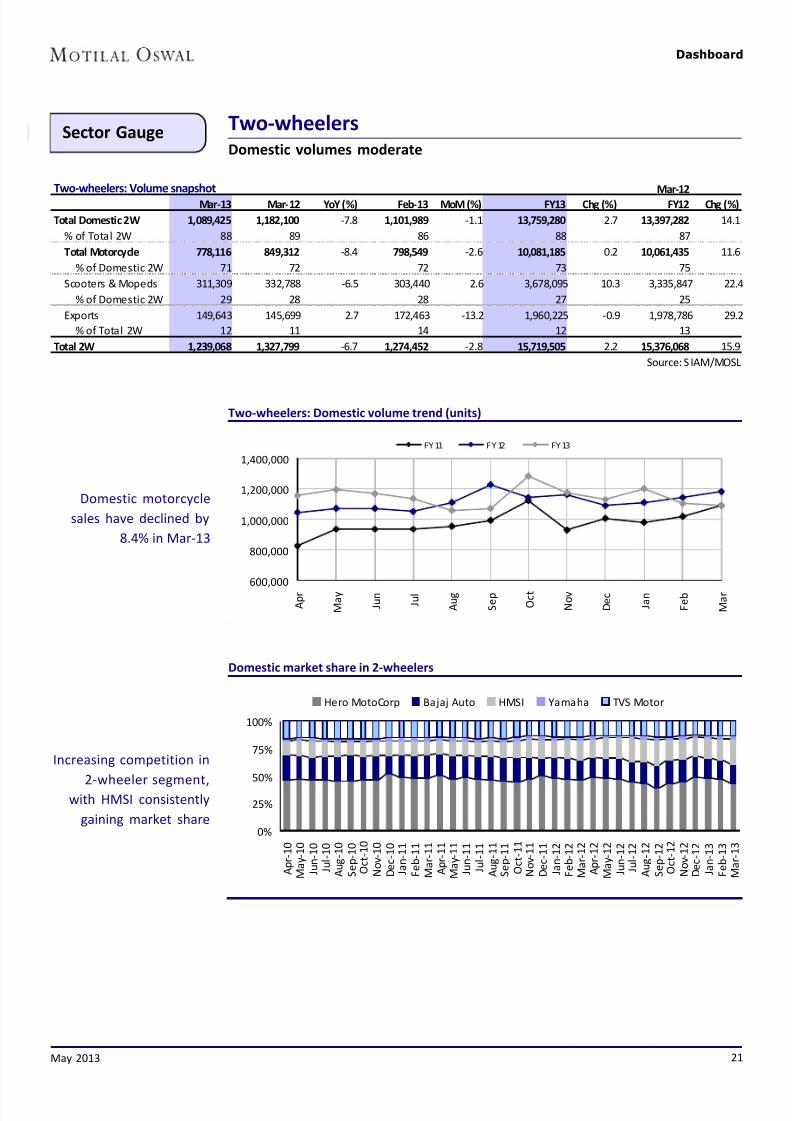

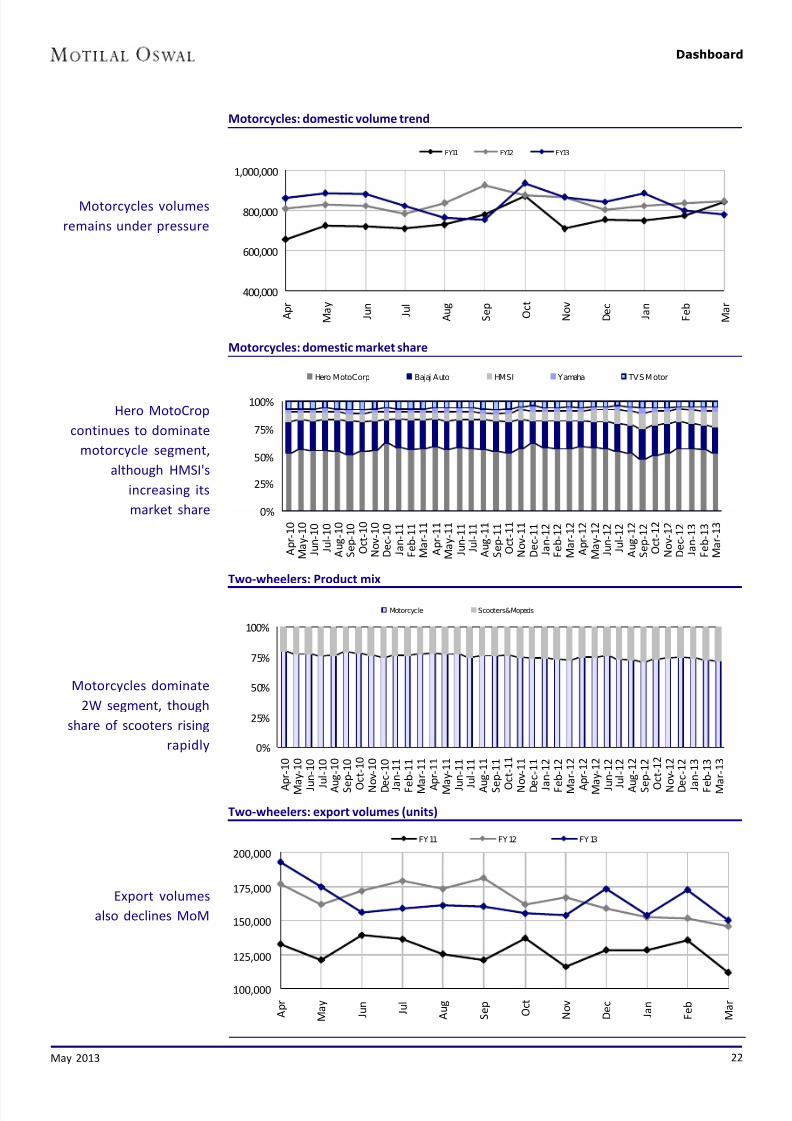

Sector Gauge Two-wheelersDomestic volumes moderate

Two-wheelers: Domestic volume trend (units)

Domestic market share in 2-wheelers

Domestic motorcycle

sales have declined by

8.4% in Mar-13

Increasing competition in

2-wheeler segment,with HMSI consistently

gaining market share

Two-wheelers: Volume snapshot Mar-12

Mar-13 Mar-12 YoY (%) Feb-13 MoM (%) FY13 Chg (%) FY12 Chg (%)

Total Domestic 2W 1,089,425 1,182,100 -7.8 1,101,989 -1.1 13,759,280 2.7 13,397,282 14.1

% of Total 2W 88 89 86 88 87

Total Motorcycle 778,116 849,312 -8.4 798,549 -2.6 10,081,185 0.2 10,061,435 11.6

% of Domestic 2W 71 72 72 73 75

Scooters & Mopeds 311,309 332,788 -6.5 303,440 2.6 3,678,095 10.3 3,335,847 22.4

% of Domestic 2W 29 28 28 27 25

Exports 149,643 145,699 2.7 172,463 -13.2 1,960,225 -0.9 1,978,786 29.2

% of Total 2W 12 11 14 12 13

Total 2W 1,239,068 1,327,799 -6.7 1,274,452 -2.8 15,719,505 2.2 15,376,068 15.9

Source: S IAM/MOSL

0%

25%

50%

75%

100%

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

D e c - 1 0

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

J a n - 1 2

F e b - 1 2

M a r - 1 2

A p r - 1 2

M a y - 1 2

J u n - 1 2

J u l - 1 2

A u g - 1 2

S e p - 1 2

O c t - 1 2

N o v - 1 2

D e c - 1 2

J a n - 1 3

F e b - 1 3

M a r - 1 3

Hero MotoCorp Bajaj Auto HMSI Yamaha TVS Motor

600,000

800,000

1,000,000

1,200,000

1,400,000

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

J a n

F e b

M a r

FY 11 F Y 12 FY 13

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 22/36

Dashboard

May 2013 22

Motorcycles: domestic volume trend

Motorcycles: domestic market share

Two-wheelers: Product mix

Two-wheelers: export volumes (units)

Motorcycles volumes

remains under pressure

Motorcycles dominate

2W segment, though

share of scooters rising

rapidly

Export volumes

also declines MoM

Hero MotoCrop

continues to dominate

motorcycle segment,

although HMSI's

increasing its

market share

400,000

600,000

800,000

1,000,000

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

J a n

F e b

M a r

FY11 FY12 FY13

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t

‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c ‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Hero MotoCorp Bajaj Auto HMSI Yamaha TVS Motor

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u

n ‐

1 0

J u l ‐ 1 0

A u

g ‐

1 0

S e

p ‐

1 0

O

c t ‐ 1 0

N o v

‐ 1 0

D e

c ‐

1 0

J a

n ‐

1 1

F e

b ‐

1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u

n ‐

1 1

J u l ‐ 1 1

A u

g ‐

1 1

S e

p ‐

1 1

O

c t ‐ 1 1

N o v

‐ 1 1

D e

c ‐

1 1

J a

n ‐

1 2

F e

b ‐

1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u

n ‐

1 2

J u l ‐ 1 2

A u

g ‐

1 2

S e

p ‐

1 2

O

c t ‐ 1 2

N o v ‐ 1 2

D e

c ‐

1 2

J a

n ‐

1 3

F e

b ‐

1 3

M a r ‐ 1 3

Motorcycle Scooters & Mopeds

100,000

125,000

150,000

175,000

200,000

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

J a n

F e b

M a r

FY11 FY12 FY13

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 23/36

Dashboard

23

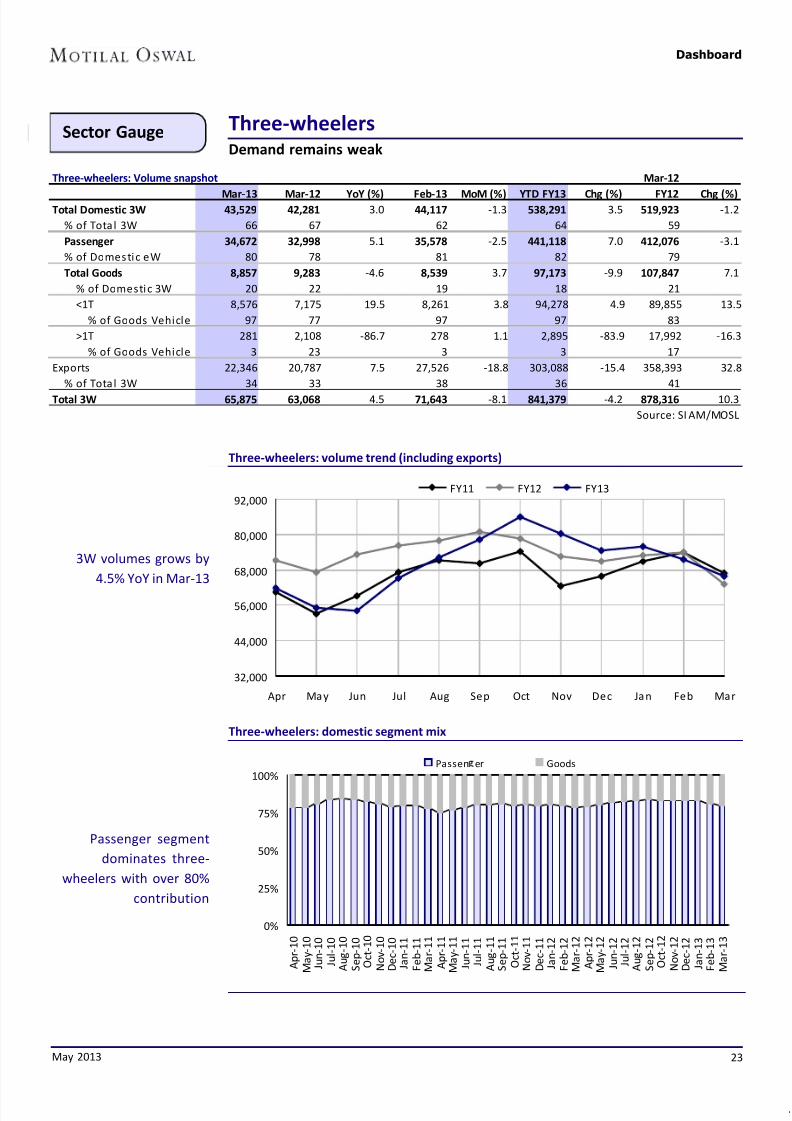

Sector Gauge Three-wheelersDemand remains weak

Three-wheelers: volume trend (including exports)

Three-wheelers: domestic segment mix

3W volumes grows by

4.5% YoY in Mar-13

Passenger segment

dominates three-

wheelers with over 80%

contribution

Three-wheelers: Volume snapshot Mar-12

Mar-13 Mar-12 YoY (%) Feb-13 MoM (%) YTD FY13 Chg (%) FY12 Chg (%)Total Domestic 3W 43,529 42,281 3.0 44,117 -1.3 538,291 3.5 519,923 -1.2

% of Tota l 3W 66 67 62 64 59

Passenger 34,672 32,998 5.1 35,578 -2.5 441,118 7.0 412,076 -3.1

% of Domestic eW 80 78 81 82 79

Total Goods 8,857 9,283 -4.6 8,539 3.7 97,173 -9.9 107,847 7.1

% of Domestic 3W 20 22 19 18 21

<1T 8,576 7,175 19.5 8,261 3.8 94,278 4.9 89,855 13.5

% of Goods Vehicle 97 77 97 97 83

>1T 281 2,108 -86.7 278 1.1 2,895 -83.9 17,992 -16.3

% of Goods Vehicle 3 23 3 3 17

Exports 22,346 20,787 7.5 27,526 -18.8 303,088 -15.4 358,393 32.8

% of Tota l 3W 34 33 38 36 41

Total 3W 65,875 63,068 4.5 71,643 -8.1 841,379 -4.2 878,316 10.3

Source: SI AM/MOSL

32,000

44,000

56,000

68,000

80,000

92,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

FY11 FY12 FY13

0%

25%

50%

75%

100%

A p r - 1 0

M a y - 1 0

J u n - 1 0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

D e c - 1 0

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

J a n - 1 2

F e b - 1 2

M a r - 1 2

A p r - 1 2

M a y - 1 2

J u n - 1 2

J u l - 1 2

A u g - 1 2

S e p - 1 2

O c t - 1 2

N o v - 1 2

D e c - 1 2

J a n - 1 3

F e b - 1 3

M a r - 1 3

Passen er Goods

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 24/36

Dashboard

24

Three wheelers: passenger segment market share

Three wheelers: goods segment market share

Bajaj Auto continues to

dominate passenger

segment…

... Piaggio continues to

lead in the goods

segment

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Baja j Auto Piaggio M&M TVS Others

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Baja j Auto Piaggio M&M Others

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 25/36

Dashboard

25

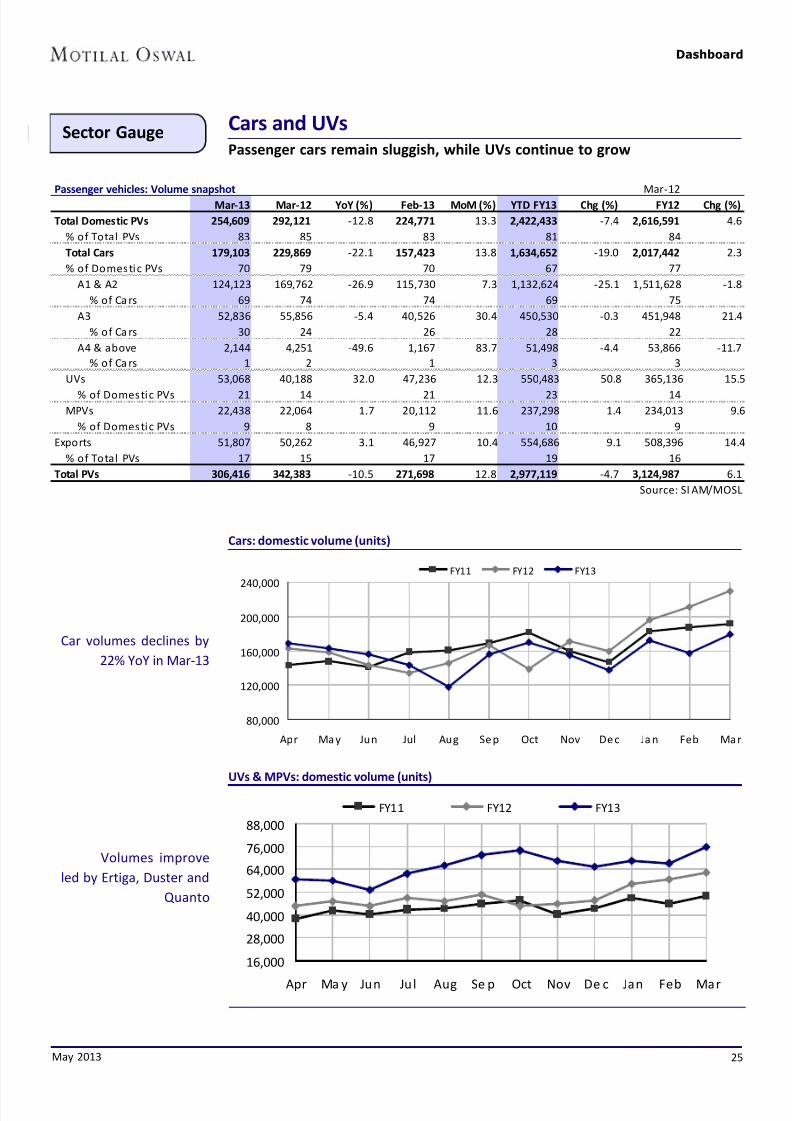

Sector Gauge Cars and UVsPassenger cars remain sluggish, while UVs continue to grow

Passenger vehicles: Volume snapshot Mar‐12

Mar‐13 Mar‐12 YoY (%) Feb‐13 MoM (%) YTD FY13 Chg (%) FY12 Chg (%)

Total Domestic PVs 254,609 292,121 ‐12.8 224,771 13.3 2,422,433 ‐7.4 2,616,591 4.6

% of Total PVs 83 85 83 81 84

Total Cars 179,103 229,869 ‐22.1 157,423 13.8 1,634,652 ‐19.0 2,017,442 2.3

% of Domestic PVs 70 79 70 67 77

A1 & A2 124,123 169,762 ‐26.9 115,730 7.3 1,132,624 ‐25.1 1,511,628 ‐1.8

% of Ca rs 69 74 74 69 75

A3 52,836 55,856 ‐5.4 40,526 30.4 450,530 ‐0.3 451,948 21.4

% of Ca rs 30 24 26 28 22

A4 & above 2,144 4,251 ‐49.6 1,167 83.7 51,498 ‐4.4 53,866 ‐11.7

% of Ca rs 1 2 1 3 3

UVs 53,068 40,188 32.0 47,236 12.3 550,483 50.8 365,136 15.5

% of Domestic PVs 21 14 21 23 14MPVs 22,438 22,064 1.7 20,112 11.6 237,298 1.4 234,013 9.6

% of Domestic PVs 9 8 9 10 9

Exports 51,807 50,262 3.1 46,927 10.4 554,686 9.1 508,396 14.4

% of Total PVs 17 15 17 19 16

Total PVs 306,416 342,383 ‐10.5 271,698 12.8 2,977,119 ‐4.7 3,124,987 6.1

Source: SI AM/MOSL

Cars: domestic volume (units)

UVs & MPVs: domestic volume (units)

Car volumes declines by

22% YoY in Mar-13

Volumes improve

led by Ertiga, Duster and

Quanto

80,000

120,000

160,000

200,000

240,000

Apr Ma y Jun Jul Aug Se p Oct Nov De c Ja n Feb Ma r

FY11 FY12 FY13

16,000

28,000

40,000

52,000

64,000

76,000

88,000

Apr Ma y Jun Jul Aug Se p Oct Nov De c Jan Feb Mar

FY11 FY12 FY13

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 26/36

Dashboard

26

Passenger vehicles: export volume (units)

Cars: domestic market share

UVs: domestic market share

Passenger vehicles: segment mix

Export volumes

pick-up MoM

Maruti's market share

improves, driven

by Ertiga

A2 dominates the

passenger vehicles

segment

MSIL market share

improves over the last

few months

20,000

29,000

38,000

47,000

56,000

65,000

Apr Ma y Jun Jul Aug Sep Oct Nov Dec Jan Feb Ma r

FY11 FY12 FY13

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Maruti TataMotor Hyundai GM Honda

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

M&M TataMotor Toyota Maruti GM

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

A1 A2 A3 A4 & above MPV UV

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 27/36

Dashboard

27

Sector Gauge Commercial vehiclesM&HCV declines, growth in LCV also moderates

M&HCVs: domestic volume - buses (units)

M&HCVs: Domestic volume - goods (units)

M&HCV volumes

remains under pressure

Commercial vehicles: Volume snapshot Mar‐

12Mar-13 Mar-12 YoY (%) F eb-13 MoM (%) YTD FY13 Chg (%) FY12 Chg (%)

Total Domestic CVs 84,956 90,343 ‐6.0 68,353 24.3 793,082 ‐0.5 797,257 16.6

% of Total CVs 94 92 91 91 90

Total M&HCV 29,591 40,004 ‐26.0 21,463 37.9 268,196 ‐22.8 347,364 7.5

% of Domestic CVs 35 44 31 34 44

Goods 23,724 33,664 ‐29.5 17,421 36.2 221,705 ‐25.9 299,085 8.7

% of M&HCVs 80 84 81 83 86

Pass enger 5,867 6,340 ‐7.5 4,042 45.2 46,491 ‐3.7 48,279 0.6

% of M&HCVs 20 16 19 17 14

Total LCVs 55,365 50,339 10.0 46,890 18.1 524,886 16.7 449,893 24.7

% of Domestic CVs 65 56 69 66 56

Goods 50,121 44,573 12.4 43,093 16.3 476,733 18.7 401,793 27.2

% of LCVs 59 49 63 60 50

Pass enger 5,244 5,766 ‐9.1 3,797 38.1 48,153 0.1 48,100 7.4

% of LCVs 6 6 6 6 6

Exports 5,848 8,160 ‐28.3 6,372 ‐8.2 80,002 ‐11.2 90,080 21.8

% of Total CVs 6 8 9 9 10

Total CVs 90,804 98,503 ‐7.8 74,725 21.5 873,084 ‐1.6 887,337 17.1

Source: SI AM/MOSL

0

8,000

16,000

24,000

32,000

40,000

Apr Ma y Jun Jul Aug Sep Oct Nov Dec Ja n Feb Ma r

FY11 FY12 FY13

0

1,500

3,000

4,500

6,000

7,500

Apr Ma y Jun Jul Aug Sep Oct Nov Dec Ja n Feb Ma r

FY11 FY12 FY13

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 28/36

Dashboard

28

M&HCVs: domestic market share, goods (%)

M&HCVs: domestic market share, buses (%)

LCVs: domestic volumes (units)

LCVs continue

robust growth

Tata Motors continue

to dominate M&HCV

goods segment

0%

25 %

50 %

75 %

100%

A p r ‐ 1 0

M a y ‐ 1 0

J u n ‐ 1 0

J u l ‐ 1 0

A u g ‐ 1 0

S e p ‐ 1 0

O c t ‐ 1 0

N o v ‐ 1 0

D e c ‐ 1 0

J a n ‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y ‐ 1 1

J u n ‐ 1 1

J u l ‐ 1 1

A u g ‐ 1 1

S e p ‐ 1 1

O c t ‐ 1 1

N o v ‐ 1 1

D e c ‐ 1 1

J a n ‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y ‐ 1 2

J u n ‐ 1 2

J u l ‐ 1 2

A u g ‐ 1 2

S e p ‐ 1 2

O c t ‐ 1 2

N o v ‐ 1 2

D e c ‐ 1 2

J a n ‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Ta ta Motor As hokLe yl and Eic he r

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y ‐ 1 0

J u n ‐ 1 0

J u l ‐ 1 0

A u g ‐ 1 0

S e p ‐ 1 0

O c t ‐ 1 0

N o v ‐ 1 0

D e c ‐ 1 0

J a n ‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y ‐ 1 1

J u n ‐ 1 1

J u l ‐ 1 1

A u g ‐ 1 1

S e p ‐ 1 1

O c t ‐ 1 1

N o v ‐ 1 1

D e c ‐ 1 1

J a n ‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y ‐ 1 2

J u n ‐ 1 2

J u l ‐ 1 2

A u g ‐ 1 2

S e p ‐ 1 2

O c t ‐ 1 2

N o v ‐ 1 2

D e c ‐ 1 2

J a n ‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

Ta taMoto r As ho kLe ylan d Eiche r Swara j

20,000

30,000

40,000

50,000

60,000

Ap r May Jun Ju l Aug Sep Oct Nov Dec Jan Fe b Mar

FY11 FY12 FY13

May 2013

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 29/36

Dashboard

May 2013 29

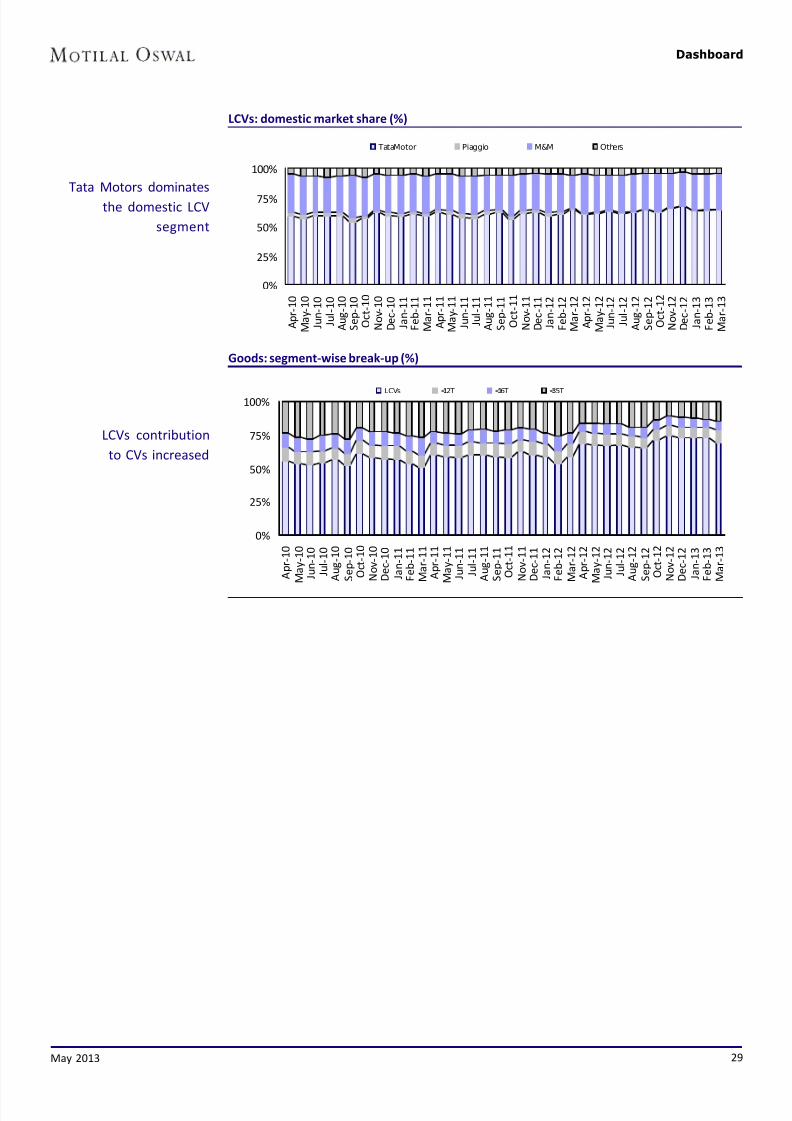

LCVs: domestic market share (%)

Goods: segment-wise break-up (%)

Tata Motors dominates

the domestic LCV

segment

LCVs contribution

to CVs increased

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t ‐ 1 0

N o v ‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y ‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v ‐ 1 1

D e c

‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

TataMotor Piaggio M&M Others

0%

25%

50%

75%

100%

A p r ‐ 1 0

M a y

‐ 1 0

J u n

‐ 1 0

J u l ‐ 1 0

A u g

‐ 1 0

S e p

‐ 1 0

O c t

‐ 1 0

N o v

‐ 1 0

D e c

‐ 1 0

J a n

‐ 1 1

F e b

‐ 1 1

M a r ‐ 1 1

A p r ‐ 1 1

M a y

‐ 1 1

J u n

‐ 1 1

J u l ‐ 1 1

A u g

‐ 1 1

S e p

‐ 1 1

O c t ‐ 1 1

N o v

‐ 1 1

D e c ‐ 1 1

J a n

‐ 1 2

F e b

‐ 1 2

M a r ‐ 1 2

A p r ‐ 1 2

M a y

‐ 1 2

J u n

‐ 1 2

J u l ‐ 1 2

A u g

‐ 1 2

S e p

‐ 1 2

O c t ‐ 1 2

N o v

‐ 1 2

D e c

‐ 1 2

J a n

‐ 1 3

F e b

‐ 1 3

M a r ‐ 1 3

LCVs <12T <16T <35T

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 30/36

Dashboard

May 2013 30

News and Events

Honda launches Amaze, to roll out UVs over two-three years

Japanese carmaker, Honda Motor launched its much-awaited compact sedan Amaze

at an aggressive price range of INR0.49m to INR0.76m (ex-showroom, Delhi). Honda's

game changer model and its first diesel product, Amaze would be country's most

fuel-efficient car with a mileage of 25.6 kmpl, as per the company.

The four diesel options come in priced band of INR0.59-0.76m, while the six petrol

trims would be available at INR0.49-0.75m. The petrol option has a 1.2 litre i-VTEC

engine. Its manual transmission delivers a fuel economy of 18 kmpl, while the

automatic offers 15.5 km in every litre.

Honda Motor is readying to roll out in two to three years a slew of diesel variants and

two new utility vehicles that will enable the Japanese car maker to participate in the

fastest-growing segment in the Indian passenger vehicle market. An MPV (multi

purpose vehicle), based on the Brio platform codenamed 2NH, is likely to hit the

market at the end of 2014, which will be followed by a compact SUV (sports utility

vehicle) based on Jazz platform in 2015.

Hironori Kanayama, MD, Honda Cars India, who underscored India being a "strategically

important market" for Honda's global operation, said: "Our counter attack in India has

just begun with the Amaze. We have a lot to do. Small cars, UVs are all under study.The SUV market is the fastest growing segment and we are studying every segment

surrounding the UV space, small or premium. You can anticipate some interesting

moves from Honda."

With the launch of new models, including full model changes (Jazz and City), Kanayama

says Honda will cater to 50% of the overall Indian passenger vehicle market from the

current 10%.

Honda Motor Corporation has set itself a target of selling 6m cars, up from 4m at the

end of 2012, and the company believes a large part of this growth will come fromemerging market like India.

The company is investing INR25b for setting up an additional assembly line in

Rajasthan, Tapakura, which will take up the company's total capacity to 0.24m units

per annum by the 2014-end. This can be further scaled up to 0.36m units.

The company is increasing the number of dealers from 150 to 162 across India this

year to promote the sale of Amaze whose target buyers seem to be middle-income

and middle-aged businessmen.

The company is now focusing on tier-2 and tier-3 towns and cities for its new,

prospective buyers.

Major developments in the auto sector

April 2013

Honda Amaze

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 31/36

Dashboard

May 2013 31

Royal Enfield Royal Enfield starts new plant, targets to sell 175,000 units in CY13

Royal Enfield has commenced operations at its new plant at Oragadam, Chennai.

Siddhartha Lal, (MD & CEO of Eicher Motors) believes Royal Enfield's new plant coming

up in Oragadam near Chennai next year will "once and forever" change the company.

"We are taking this new plant as an opportunity to upgrade ourselves to absolute

global standards in terms of manufacturing excellence".

The Oragadam facility will operate in tandem with the existing plant in Tiruvottiyur

for motorcycle assembly next year. This activity will, thereafter, be confined to the

new unit while engines will still be machined and assembled in the old plant. "Initially

in 2013, we will do a combined 150,000 units, while Oragadam can do twice as much

on its own subsequently," Lal says.

Lal's next step is to target markets beyond India. He shrugs off the ongoing crisis in

Europe saying the company's exposure to this part of the world is "extremely small".

Over the next decade, Royal Enfield sees developing markets as the bigger play, a list

that includes Latin America, Southeast Asia, Africa and West Asia.

South Africa first to get new Mahindra vehicle 'Genio'

South Africa has become the first country outside India to get the latest product

'Genio' from the Mahindra range of pick-up vehicles.

Mahindra South Africa has added another variant to its range of one-tonne Genio

pick-ups that are proving very popular in the country.

"This new addition is in response to customer requests and in line with Mahindra's

policy of listening to feedback and adapting our product range to meet these needs,

when volumes make it viable," said Mahindra South Africa CEO Ashok Thakur.

"In the case of the Genio with drop sides and a flat load bed we see this is well suited

to small business operators in need of a versatile, reliable and tough 1.2 tonne light

commercial vehicle to facilitate their daily working operations and delivery needs,"

Thakur said.

In the past, Mahindra has adapted Indian domestic models, such as the Bolero, Scorpio,

Thar and Xylo, for sale in the South African market, but the Genio is the result of a new

global approach to research and development.

"The Genio is the result of extensive worldwide research in terms of what the pick-up

buyer requires in the various markets where this type of vehicle is popular," Thakur

said, adding that South Africa was the first country outside India to receive the Genio.

Mahindra sees the Genio as a versatile pick-up that sits between the requirementsfor a workhorse bakkie and a recreational vehicle.

Mahindra Genio

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 32/36

Dashboard

May 2013 32

The Genio is made at Mahindra's state-of-the-art manufacturing facility in Chakan,

which was completed in November 2009, with an initial manufacturing capacity of

300,000 units a year and the potential to double this output in the future.

Mahindra South Africa is a fully-owned subsidiary of the USD 15.9-billionMahindra

Group, Mahindra & Mahindra of India, which was established in 1945.

The company operates in South Africa with over 50 dealerships, and is also exporting

vehicles to Zimbabwe, Zambia, Botswana, Swaziland and Namibia.

Mahindra South Africa has achieved significant growth in the country since its

establishment in October 2004, and since then, the company has sold a total of

approximately 18,000 vehicles.

Volkswagen launches Polo petrol variant at INR0.79mVolkswagen launched a petrol variant of its popular hatchback Polo. The 1.2-litre new

Polo is priced at INR0.79m (ex-showroom Delhi), said Arvind Saxena, Managing Director

for passenger cars, Volkswagen Group Sales India after the launch here.

"Fuel efficiency has become vital for every customer looking at purchasing a new car

and the Polo GT TSI is an answer to this demand offering maximum power and

minimum consumption," Saxena said, adding that the TSI is a pioneering technology

of petrol engines by Volkswagen.

Volkswagen, the largest European car maker, sells the Polo, Vento, Jetta, Passat and

the Touareg in the domestic market.

Mercedes-Benz to roll out 3 new models in 3 months

The German luxury carmaker Mercedes-Benz has set a hectic pace for itself and expects

to launch three new models in India within three months. The company will introduce

its all-new luxury sports utility vehicle GL in the presence of German tennis star Boris

Becker on May 16 in New Delhi.

This will be followed by the launch of the diesel variant of its B Class and the globally

popular A Class hatch in both the petrol and diesel variants.

Eberhard H. Kern, Managing Director and CEO of Mercedes-Benz India, said, "The

company will significantly expand its product portfolio during the year and thereby

be able to address a much larger luxury car market."

He told Business Line that the luxury auto market in India is set to grow significantly

from barely 1.2% of the 2.6-million passenger car market to about 4% of the expanded

market by 2020.

"We are currently functioning in India within fewer segments with the C, E and S Class

and the petrol variant of the B Class. But wherever we are present we have a

leadership role," he said.

7/30/2019 AUTO Dashboard April 2013

http://slidepdf.com/reader/full/auto-dashboard-april-2013 33/36

Dashboard

May 2013 33

BMW Mini Cooper

"Having closed 2012 with overall sales volumes of about 7,000 cars, and registering a

growth of about 5.3% during the first quarter ended March 31, 2013 with 2,009 cars,

we expect to register double-digit growth during the current year with the expanded

portfolio," he said.

The company last year commissioned a new paint shop at Chakan in Maharashtra,

which can handle up to 20,000 cars. It expects to complete the expansion project,

which will take the capacity to 20,000 vehicles per annum, by the year-end.

BMW starts production of 'MINI Countryman' at Chennai plant

A year after introducing its popular 'MINI' range of cars in India, luxury car maker BMW

has begun the local production of 'MINI Countryman' at the facility here.