australian housing markets report - ffx.adcentre.com.au.s3...

TRANSCRIPT

Australian housing markets reportCairns – rise and rise

Dr Andrew Wilson – Domain Group senior economistNovember 2014

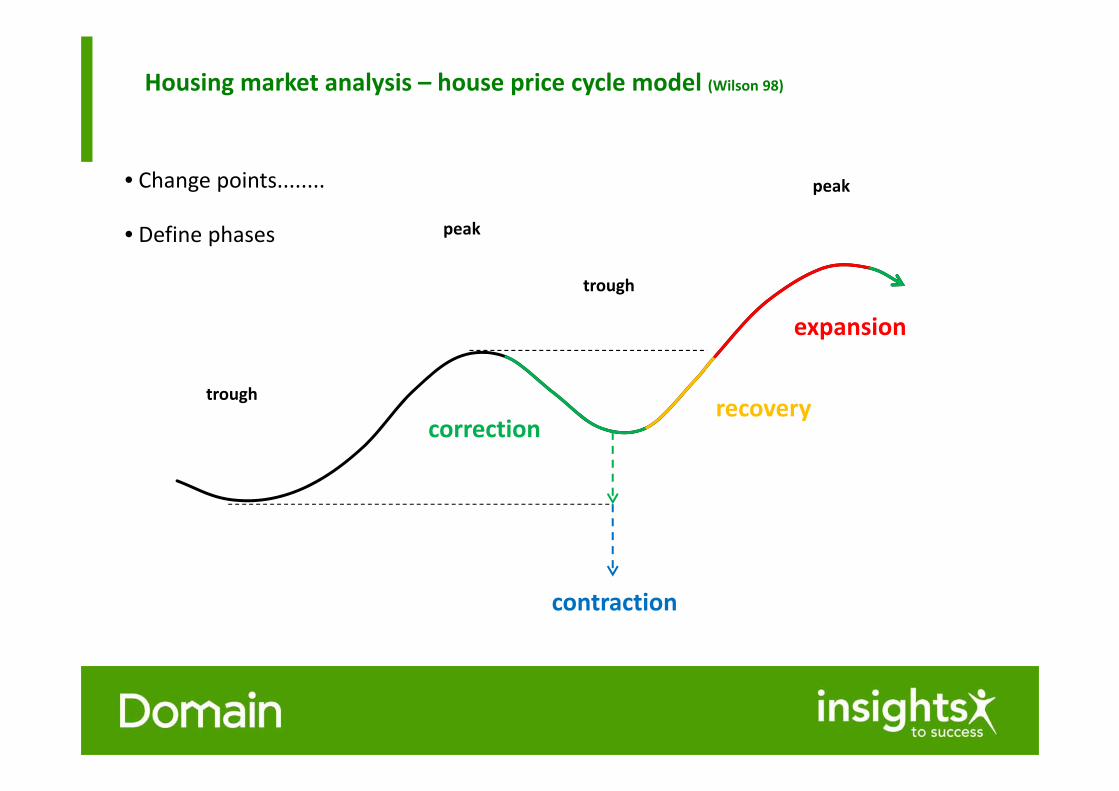

Housing market model – Wilson Curve

trough

peak

trough

peak

correctionrecovery

expansion

contraction

• Change points........

• Define phases

Housing market analysis – house price cycle model (Wilson 98)

Recent capital city performance

Capital city house price cycle ‐ recent history

Correction 2011 Prices fall

Affordability falls from higher rates, higher prices PLUS economy down

Recovery 2012 Prices rise

Affordability improves as rates fall, lower prices AND economy revives

Expansion 2013 Price records emerge and consolidate as affordability peaks

Historically low rates, still solid economy, CONFIDENCE RESTORED

Current state of the national market

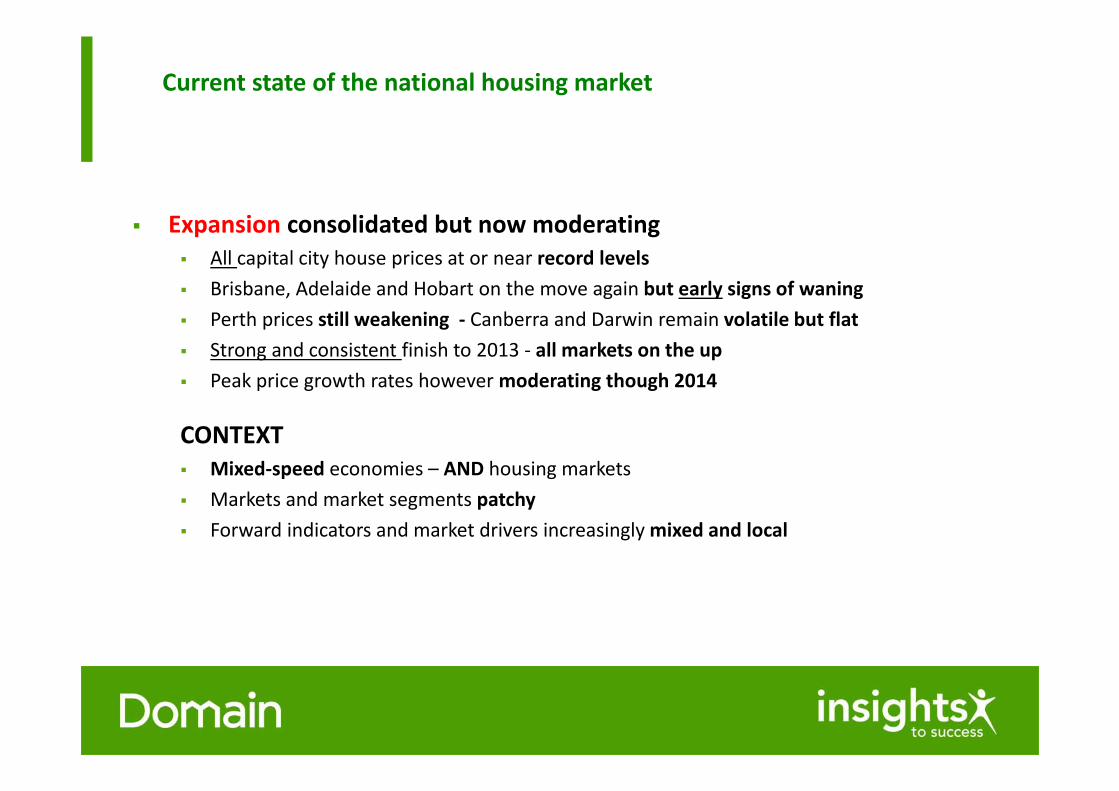

Current state of the national housing market

Expansion consolidated but now moderating All capital city house prices at or near record levels Brisbane, Adelaide and Hobart on the move again but early signs of waning Perth prices still weakening ‐ Canberra and Darwin remain volatile but flat Strong and consistent finish to 2013 ‐ all markets on the up Peak price growth rates however moderating though 2014

CONTEXT Mixed‐speed economies – AND housing markets Markets and market segments patchy Forward indicators and market drivers increasingly mixed and local

Key price drivers

The future for house price growth?

....as usual depends on the economy

Key Drivers Low unemployment and more jobs Rising wages, incomes and profits Lower interest rates Rising stockmarket Confidence

Recent prices growth

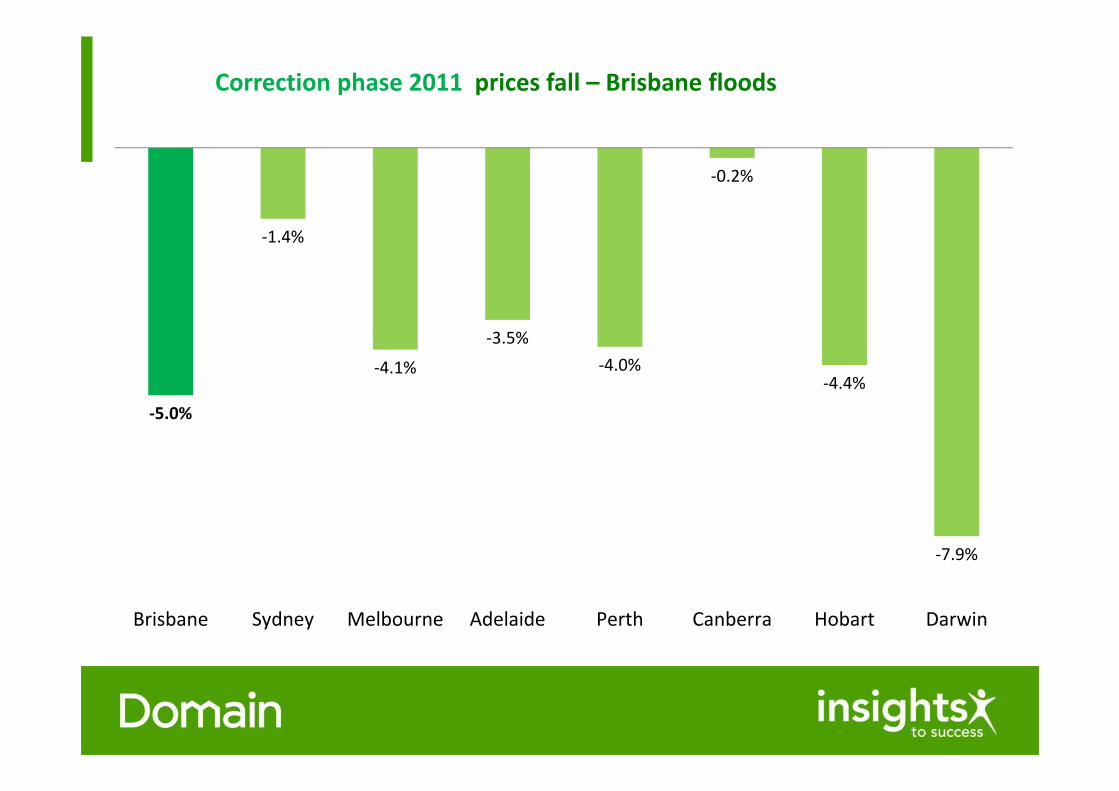

Correction phase 2011 prices fall – Brisbane floods

‐5.0%

‐1.4%

‐4.1%

‐3.5%‐4.0%

‐0.2%

‐4.4%

‐7.9%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

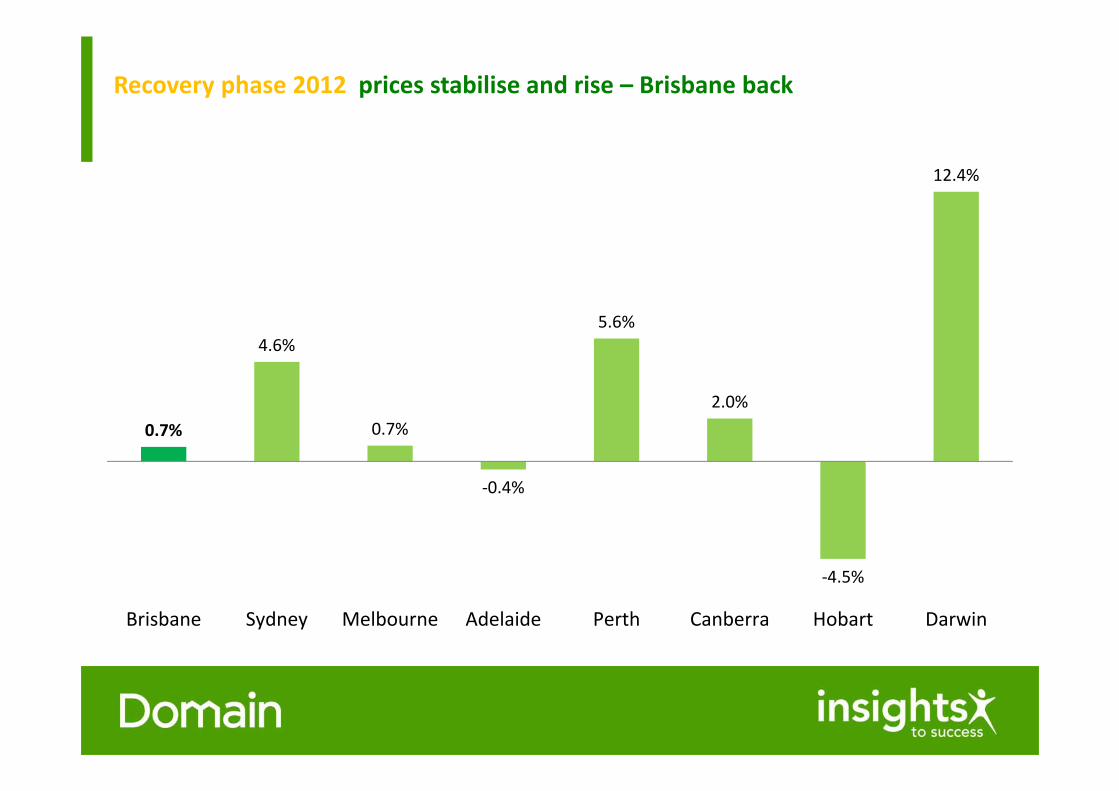

Recovery phase 2012 prices stabilise and rise – Brisbane back

0.7%

4.6%

0.7%

‐0.4%

5.6%

2.0%

‐4.5%

12.4%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

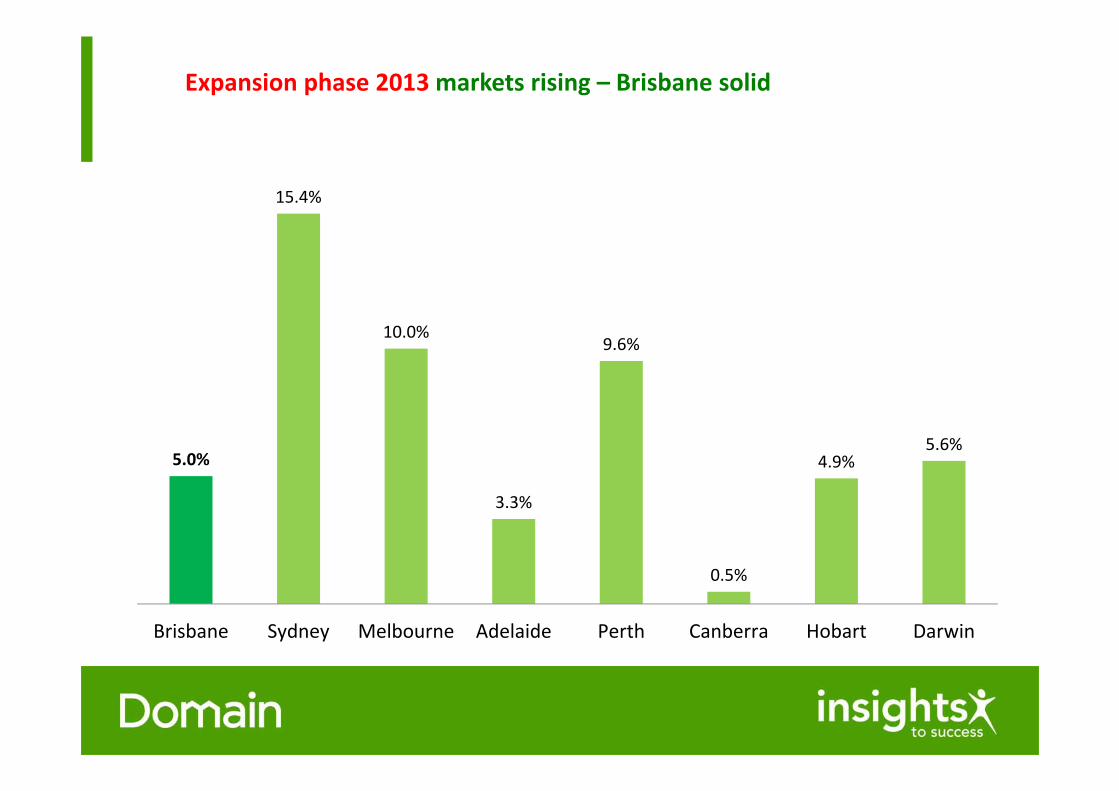

Expansion phase 2013 markets rising – Brisbane solid

5.0%

15.4%

10.0%

3.3%

9.6%

0.5%

4.9%5.6%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

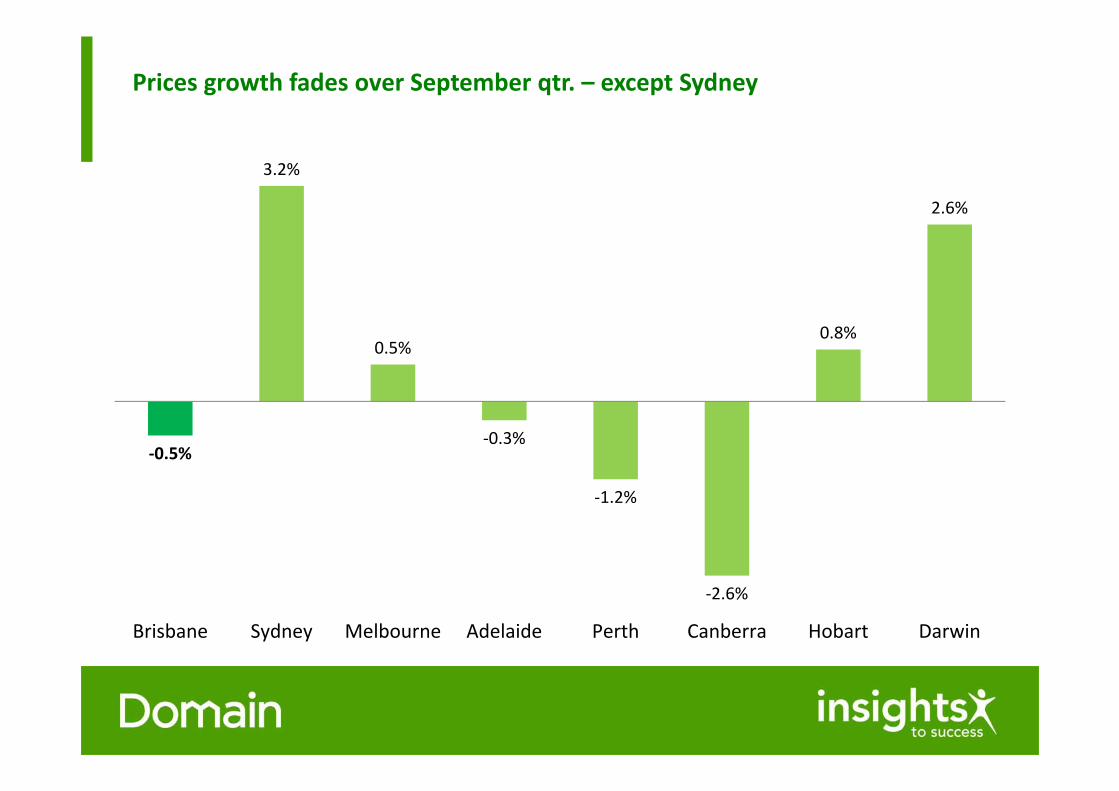

Prices growth fades over September qtr. – except Sydney

‐0.5%

3.2%

0.5%

‐0.3%

‐1.2%

‐2.6%

0.8%

2.6%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

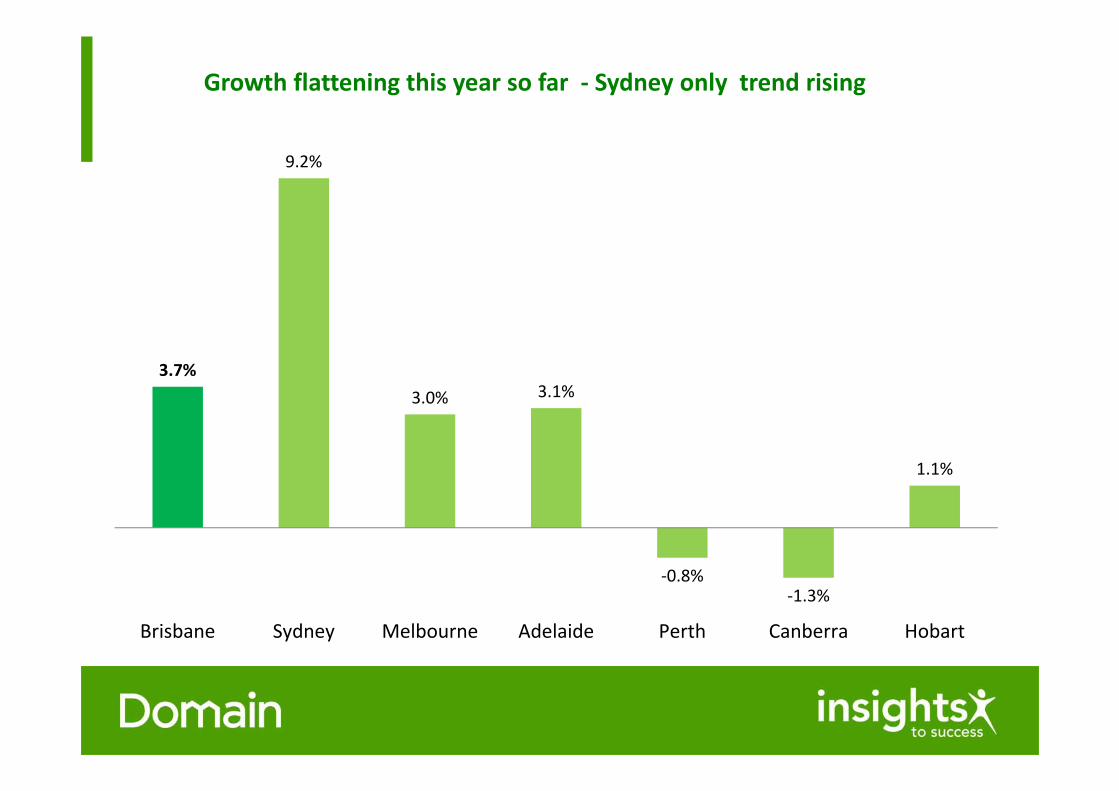

Growth flattening this year so far ‐ Sydney only trend rising

3.7%

9.2%

3.0% 3.1%

‐0.8%‐1.3%

1.1%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart

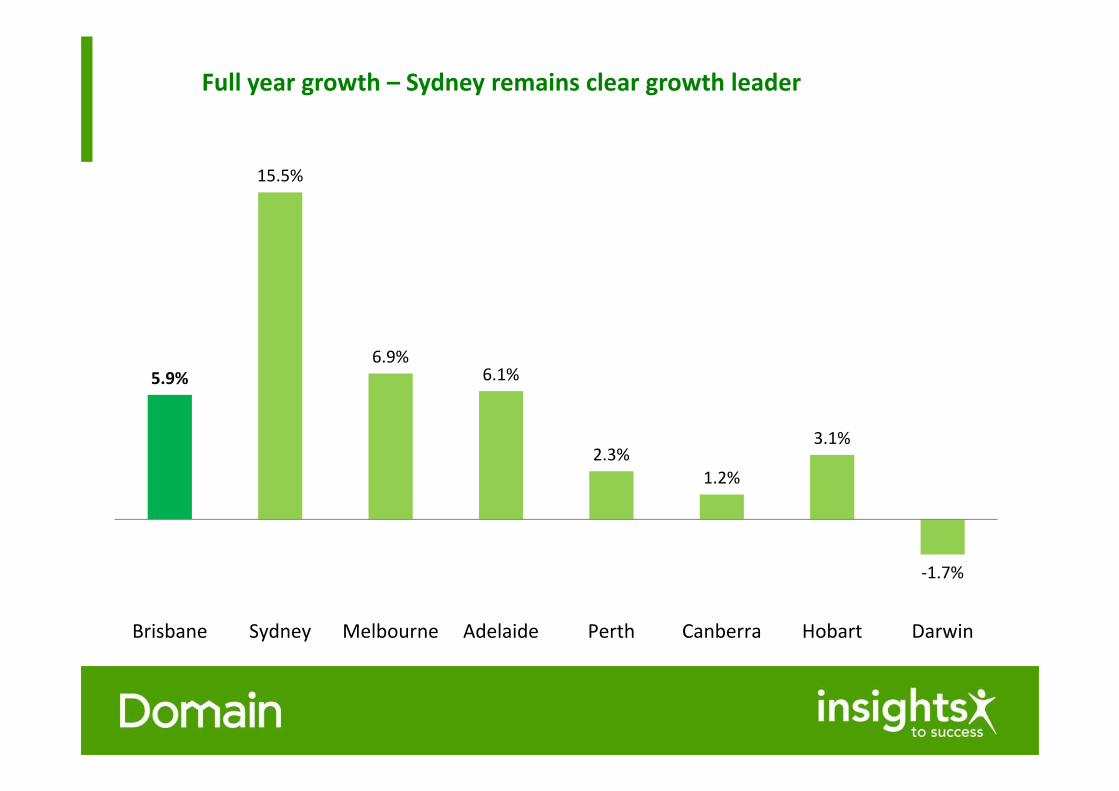

Full year growth – Sydney remains clear growth leader

5.9%

15.5%

6.9%6.1%

2.3%1.2%

3.1%

‐1.7%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

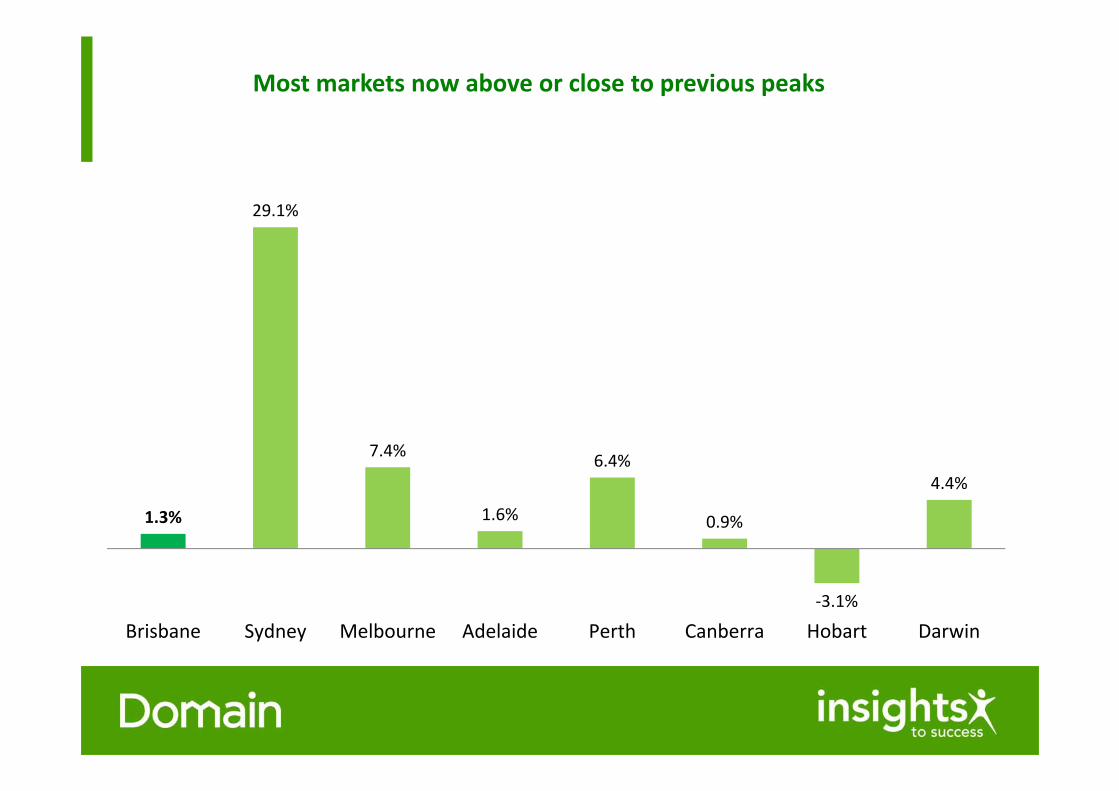

Most markets now above or close to previous peaks

1.3%

29.1%

7.4%

1.6%

6.4%

0.9%

‐3.1%

4.4%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

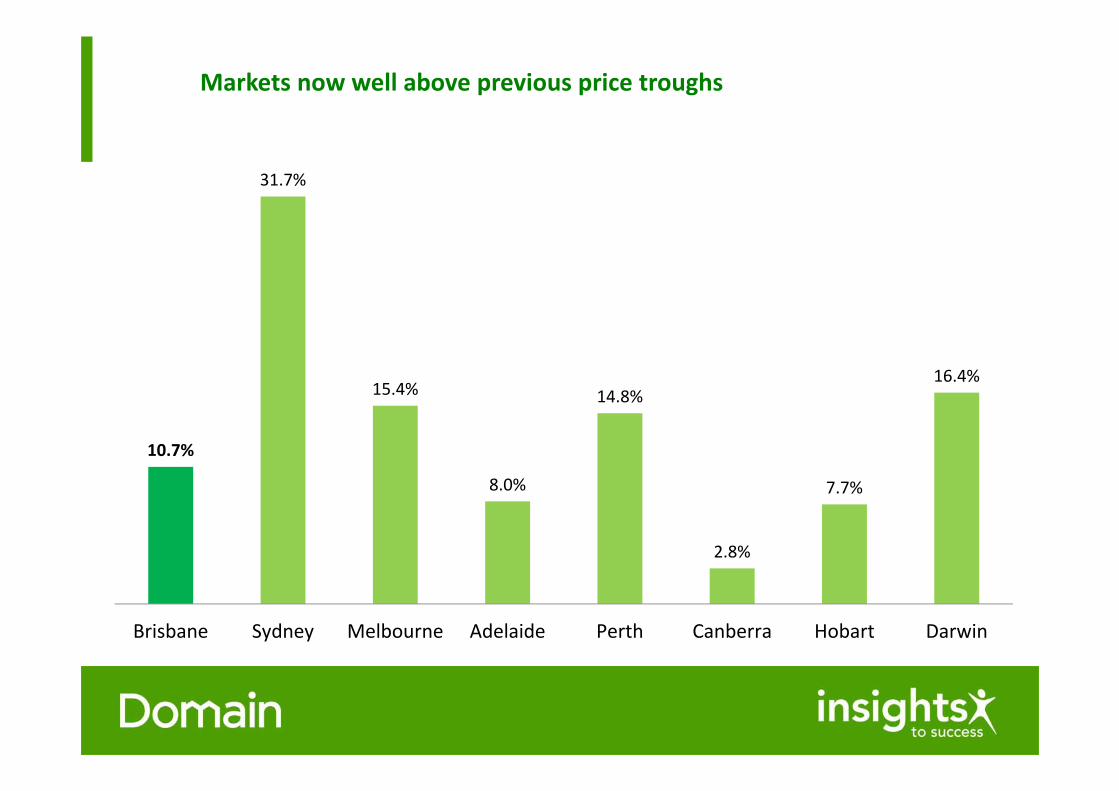

Markets now well above previous price troughs

10.7%

31.7%

15.4%

8.0%

14.8%

2.8%

7.7%

16.4%

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

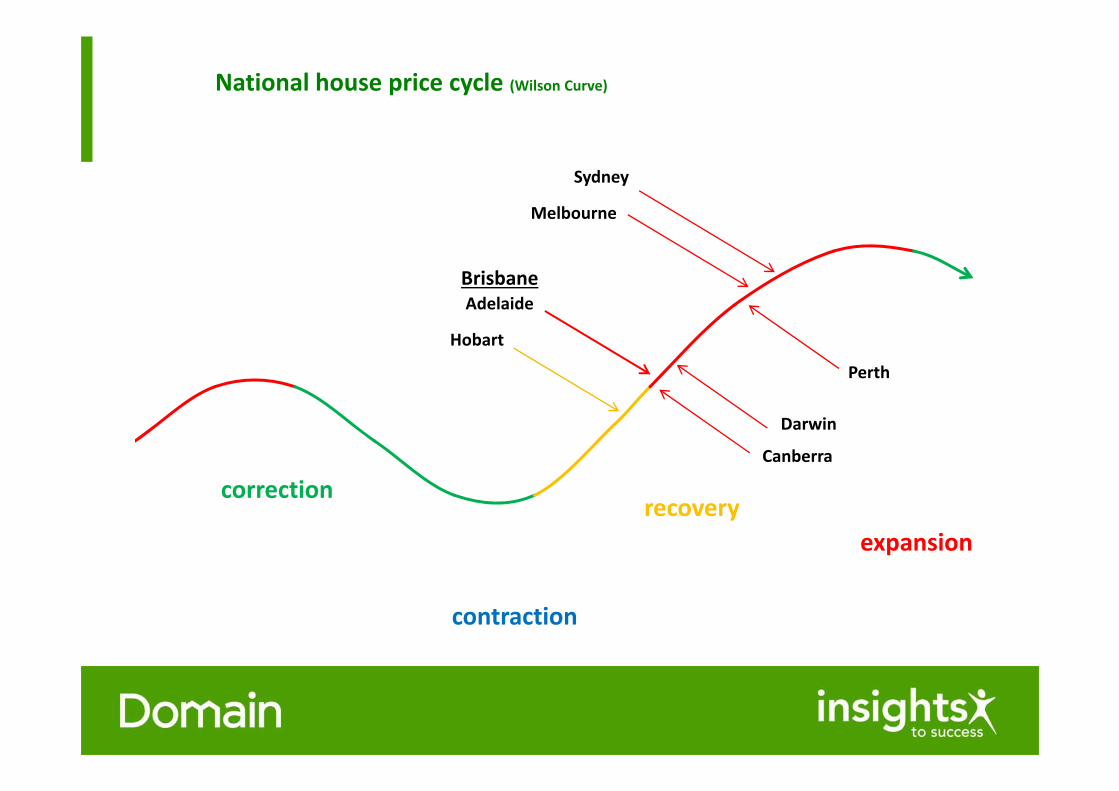

Current capital city price cycle

National house price cycle (Wilson Curve)

correctionrecovery

expansion

contraction

Sydney

Perth

Melbourne

BrisbaneAdelaide

Darwin

Hobart

Canberra

Current capital city growth

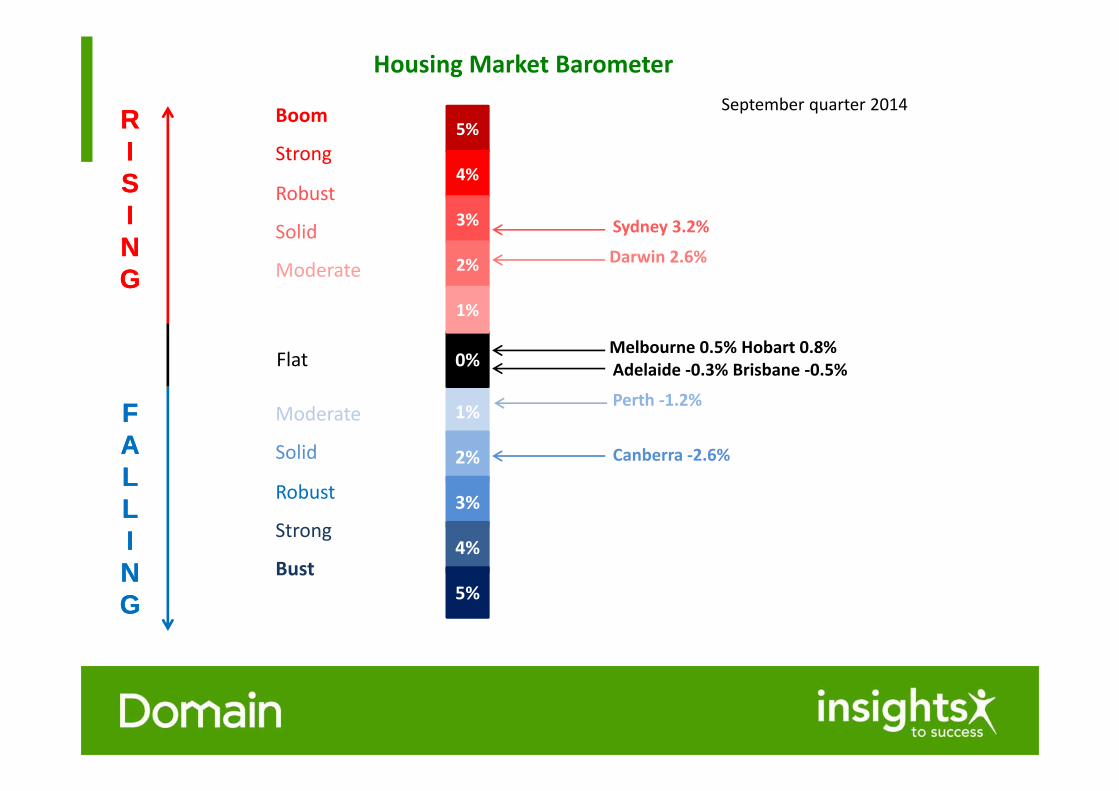

Housing Market Barometer

5%

2%

1%

0%

0%

Sydney 3.2%

Canberra ‐2.6%

Melbourne 0.5% Hobart 0.8%

RISING

FALLING

September quarter 2014

5%

4%4%

3%

2%

1%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

Darwin 2.6%

RISING

FALLING

Perth ‐1.2%

Adelaide ‐0.3% Brisbane ‐0.5%

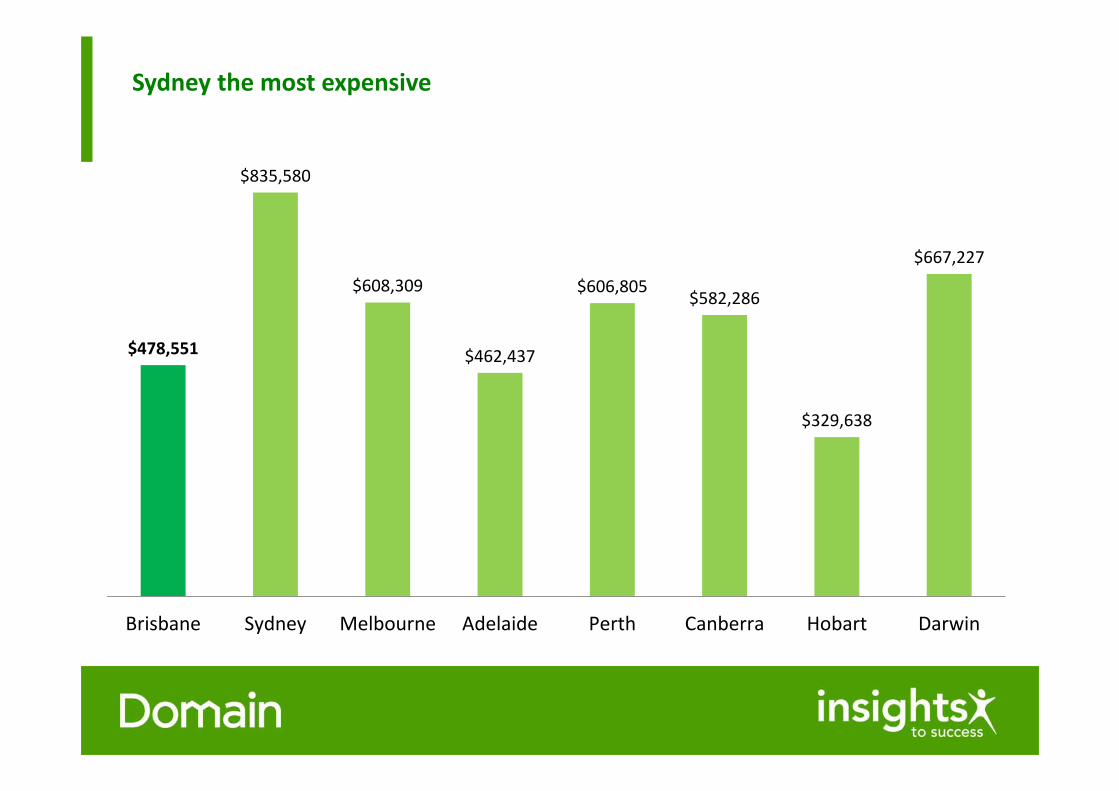

Sydney the most expensive

$478,551

$835,580

$608,309

$462,437

$606,805$582,286

$329,638

$667,227

Brisbane Sydney Melbourne Adelaide Perth Canberra Hobart Darwin

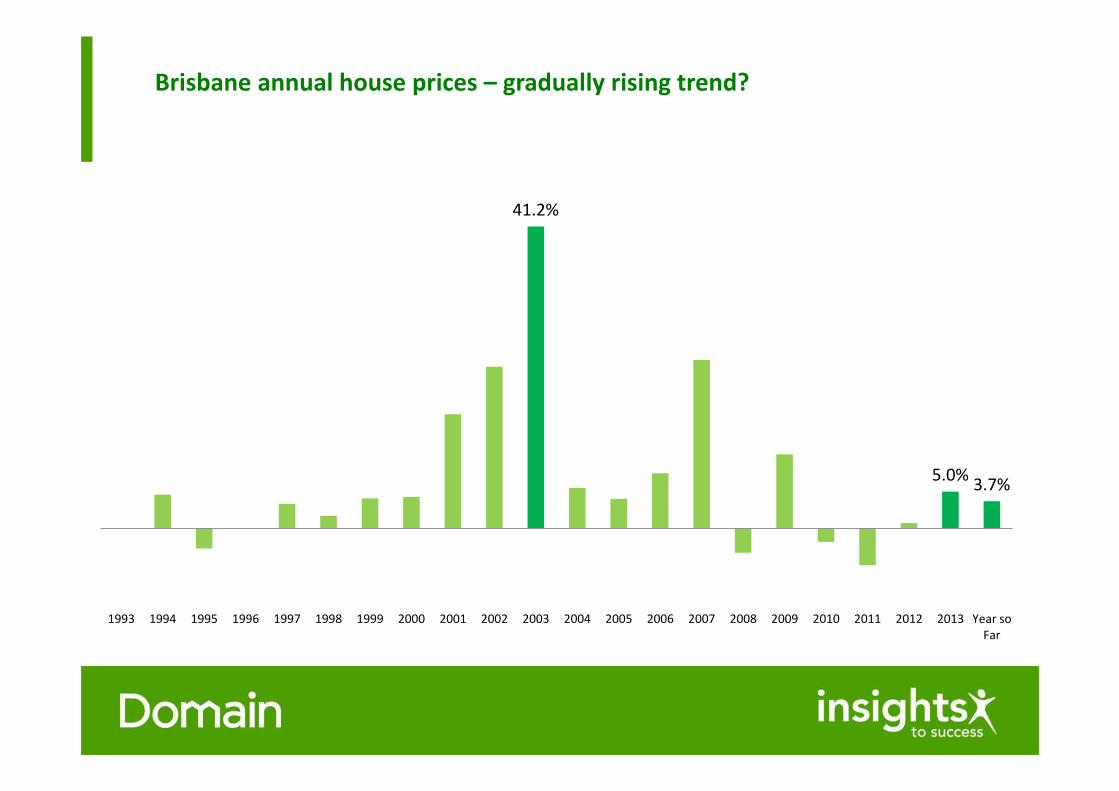

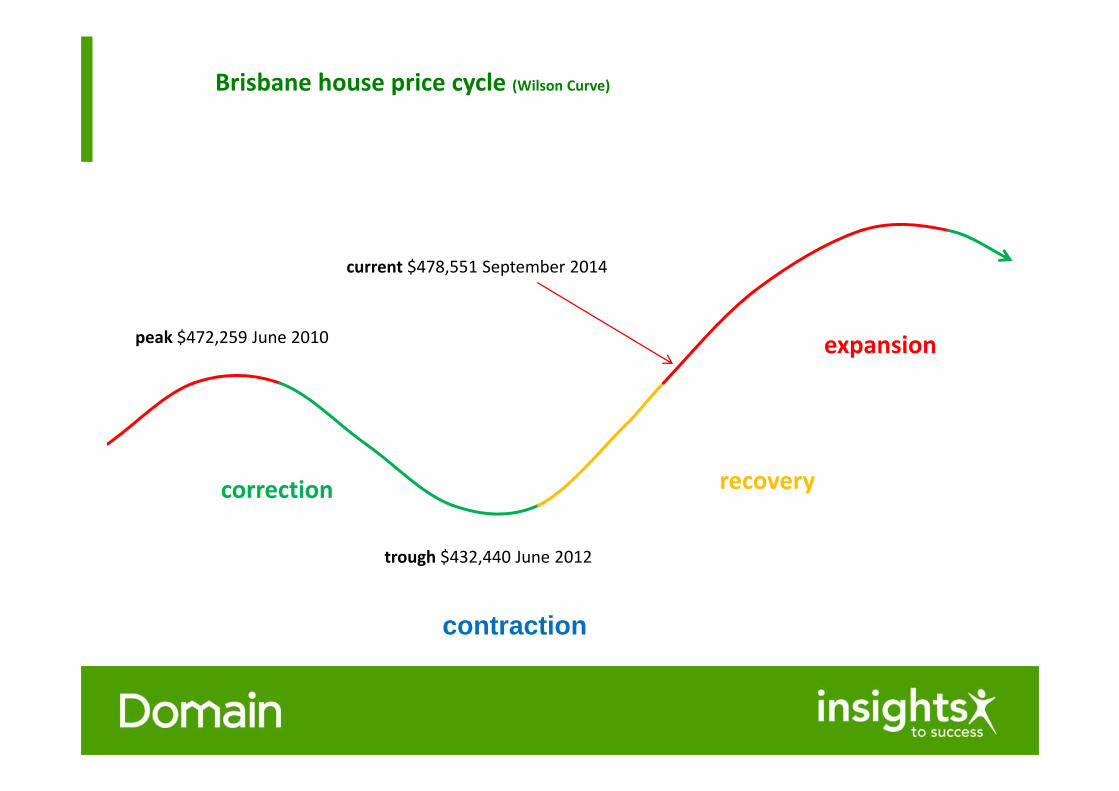

Brisbane price cycle

Brisbane annual house prices – gradually rising trend?

41.2%

5.0% 3.7%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Year soFar

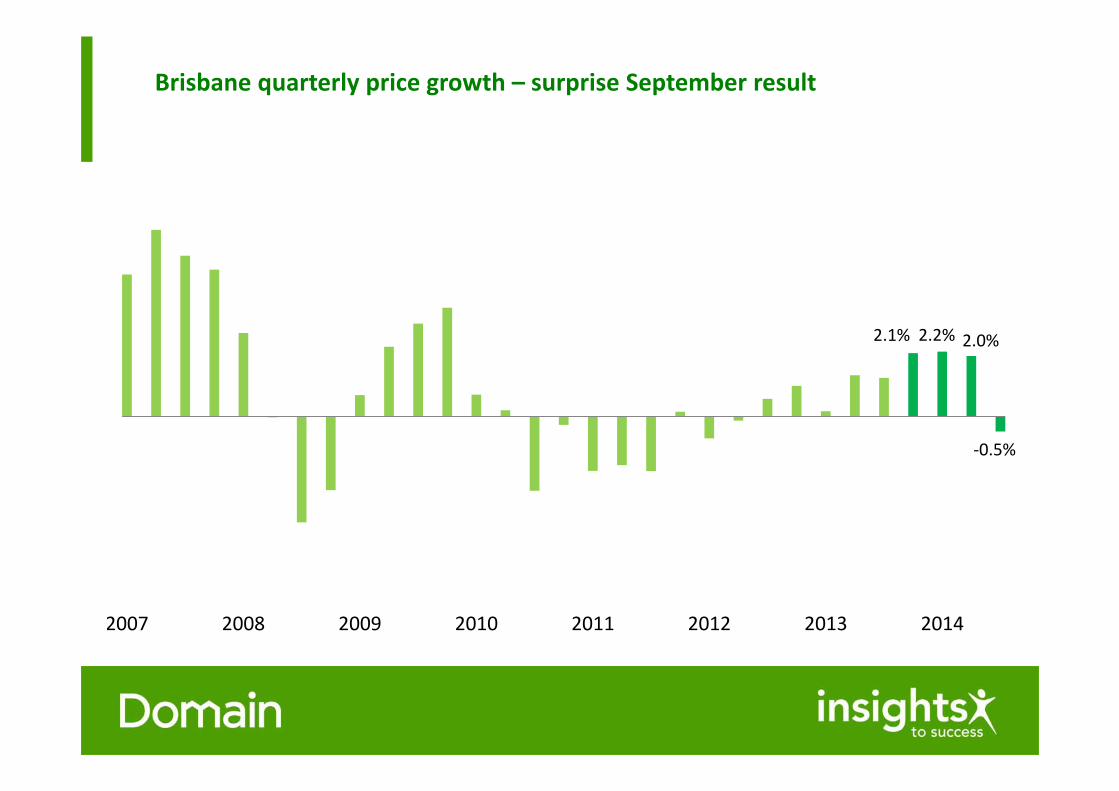

Brisbane quarterly price growth – surprise September result

2.1% 2.2% 2.0%

‐0.5%

2007 2008 2009 2010 2011 2012 2013 2014

Brisbane house price cycle (Wilson Curve)

correction recovery

expansion

contraction

peak $472,259 June 2010

current $478,551 September 2014

trough $432,440 June 2012

Interest rates and housing markets

1%

2%

3%

4%

5%

6%

7%

8%

$250,000

$350,000

$450,000

$550,000

$650,000

$750,000

$850,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Sydney Melbourne Brisbane Adelaide Perth Interest rate

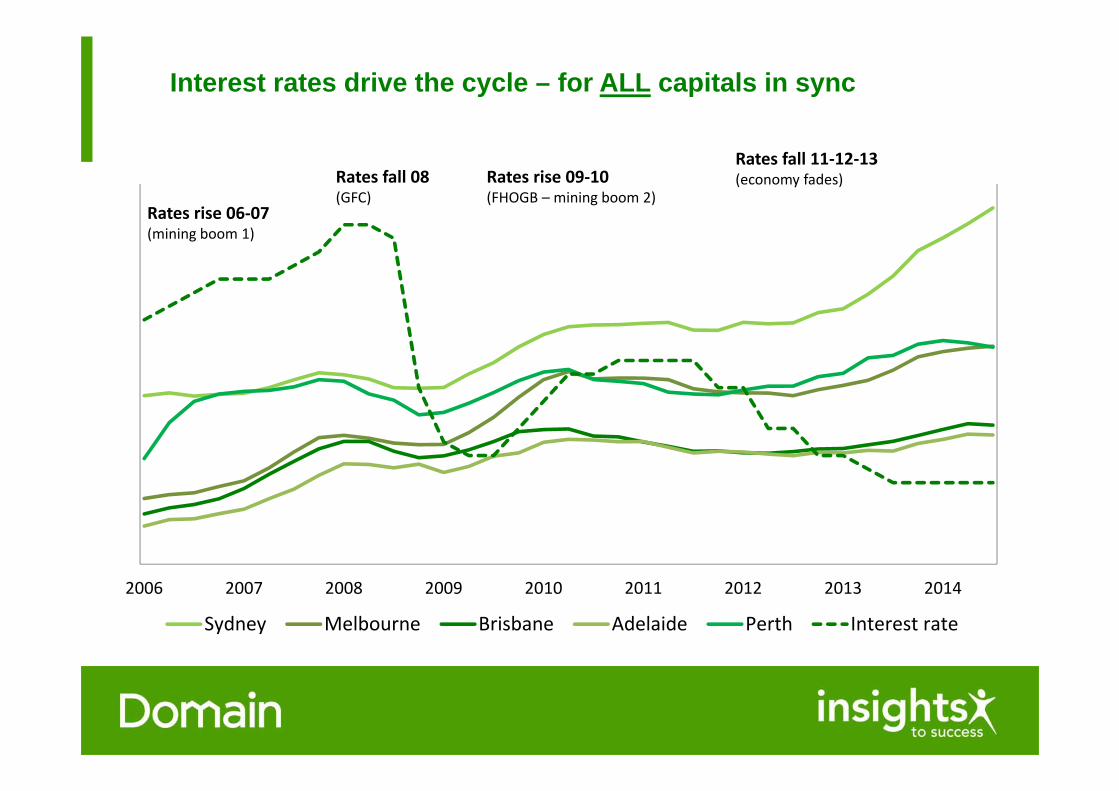

Interest rates drive the cycle – for ALL capitals in sync

Rates rise 09‐10(FHOGB – mining boom 2)

Rates fall 11‐12‐13(economy fades)Rates fall 08

(GFC)Rates rise 06‐07(mining boom 1)

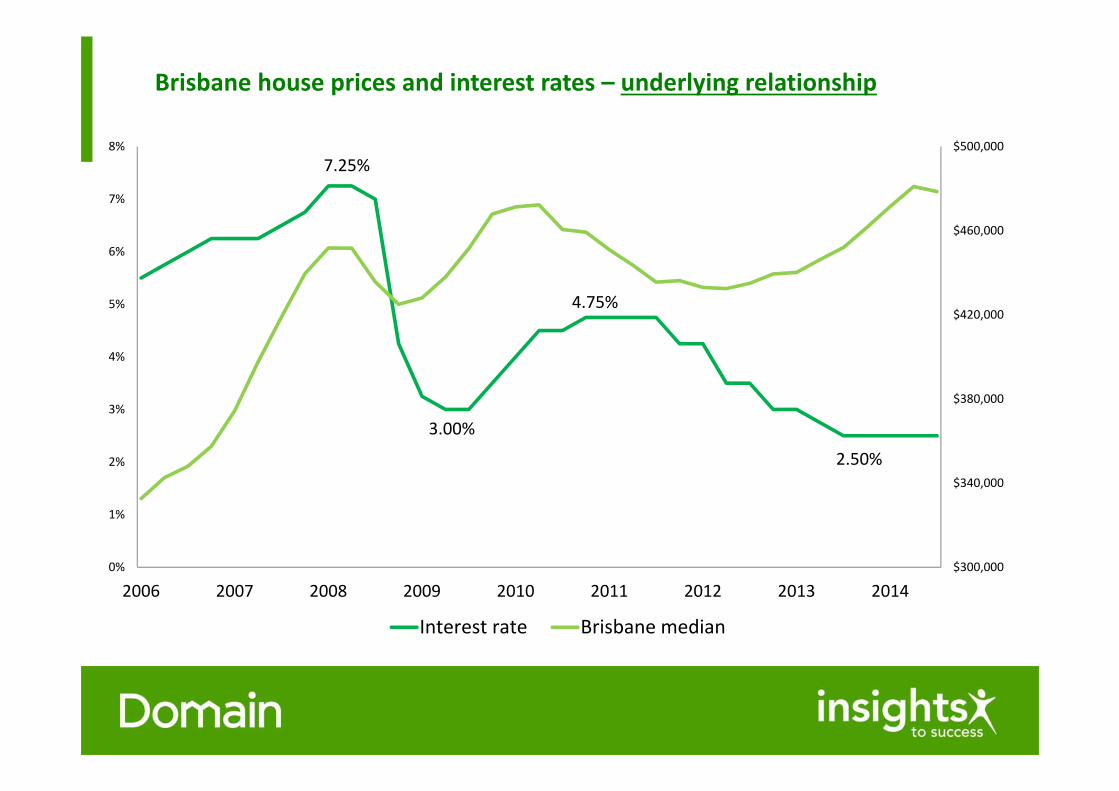

Brisbane house prices and interest rates – underlying relationship

7.25%

3.00%

4.75%

2.50%

$300,000

$340,000

$380,000

$420,000

$460,000

$500,000

0%

1%

2%

3%

4%

5%

6%

7%

8%

2006 2007 2008 2009 2010 2011 2012 2013 2014

Interest rate Brisbane median

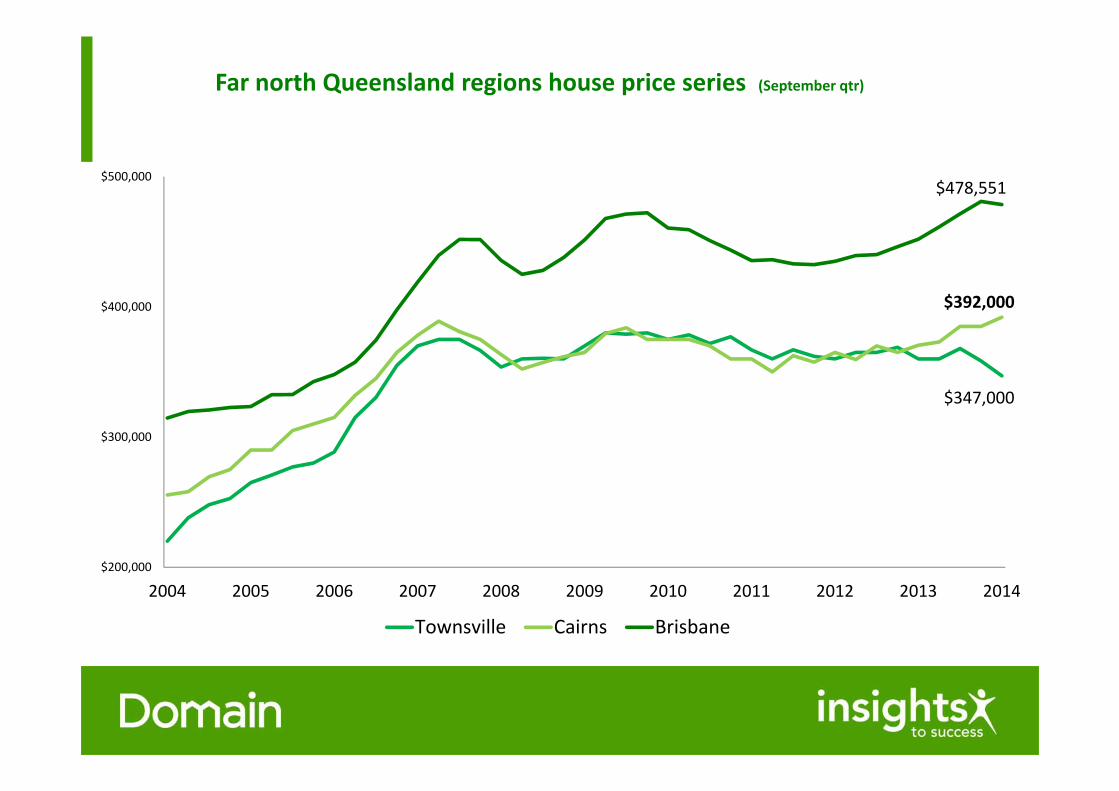

Far north Queensland

Far north Queensland regions house price series (September qtr)

$347,000

$392,000

$478,551

$200,000

$300,000

$400,000

$500,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Townsville Cairns Brisbane

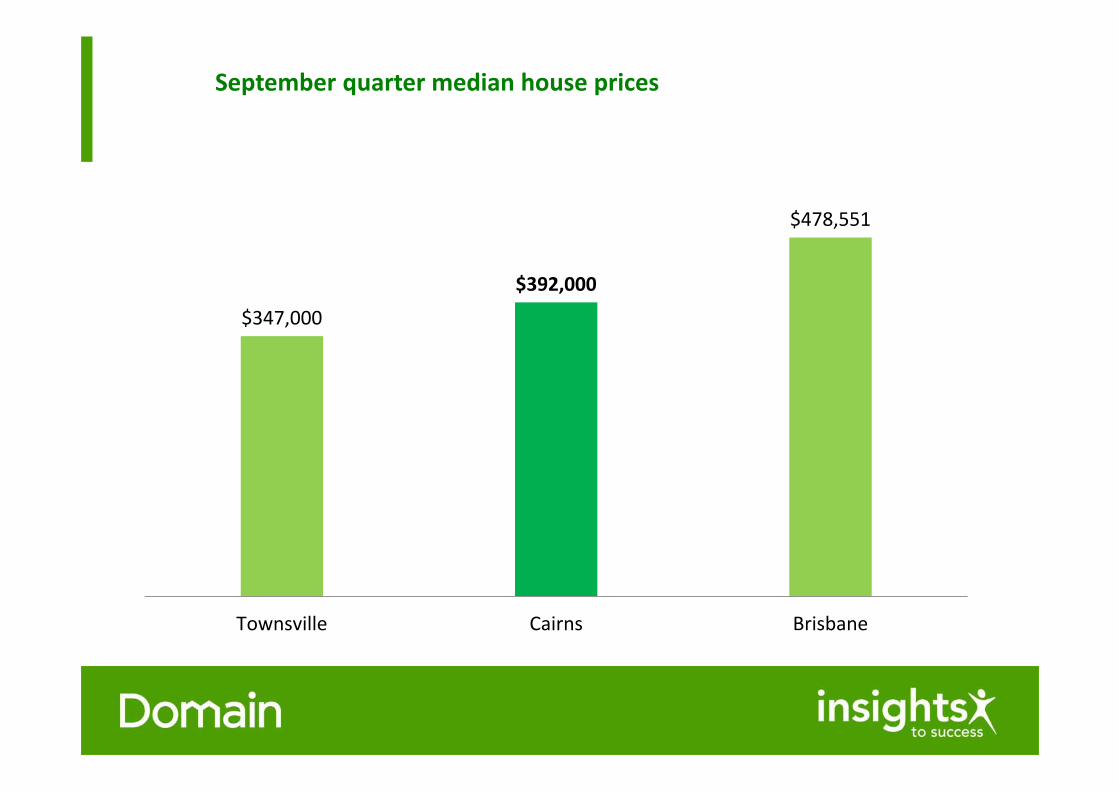

September quarter median house prices

$347,000

$392,000

$478,551

Townsville Cairns Brisbane

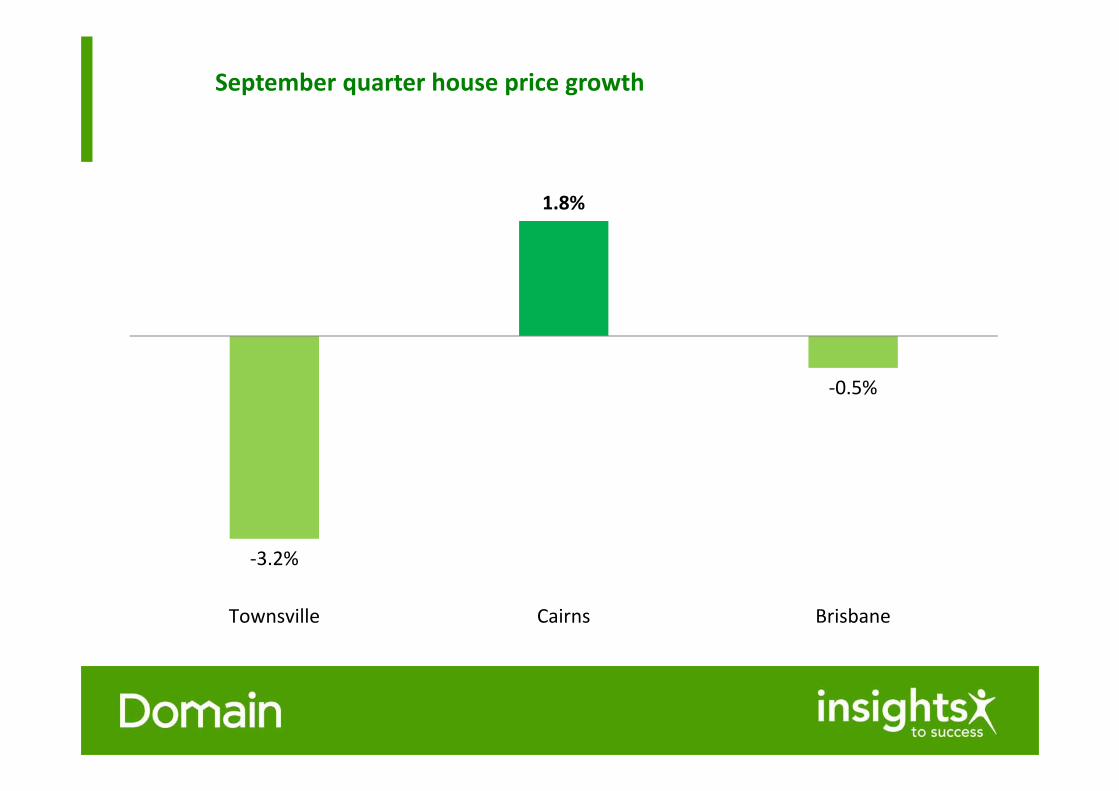

September quarter house price growth

‐3.2%

1.8%

‐0.5%

Townsville Cairns Brisbane

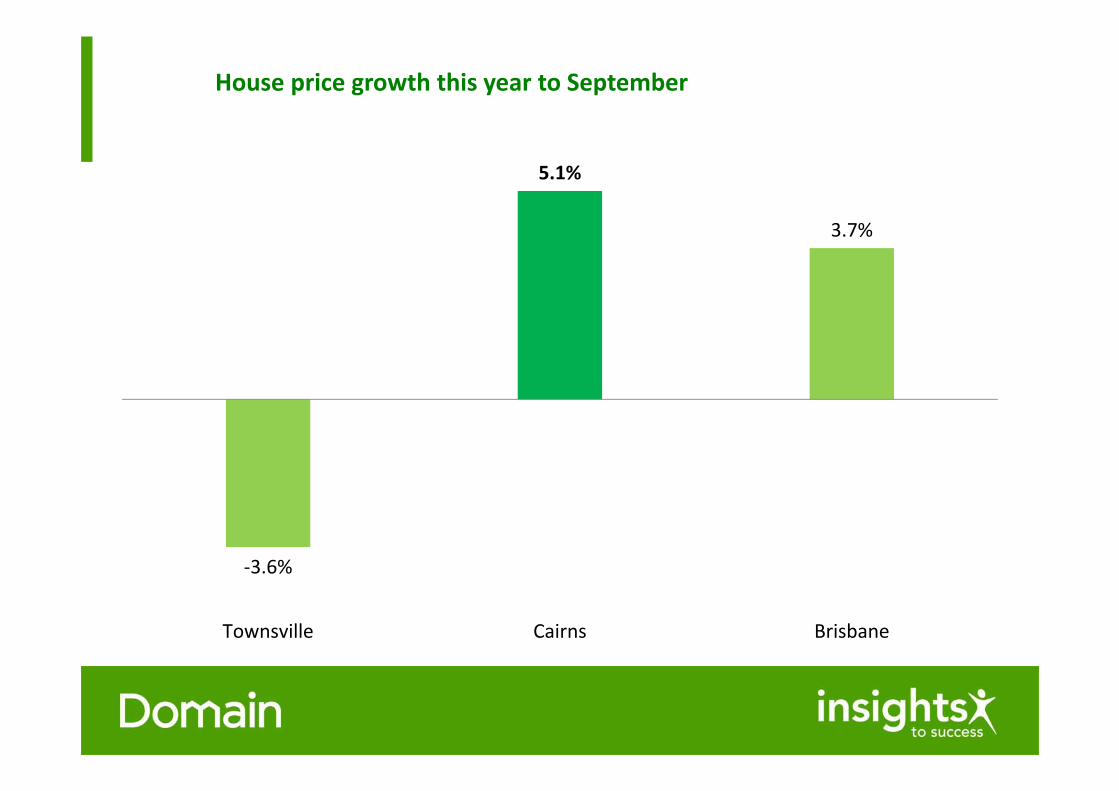

House price growth this year to September

‐3.6%

5.1%

3.7%

Townsville Cairns Brisbane

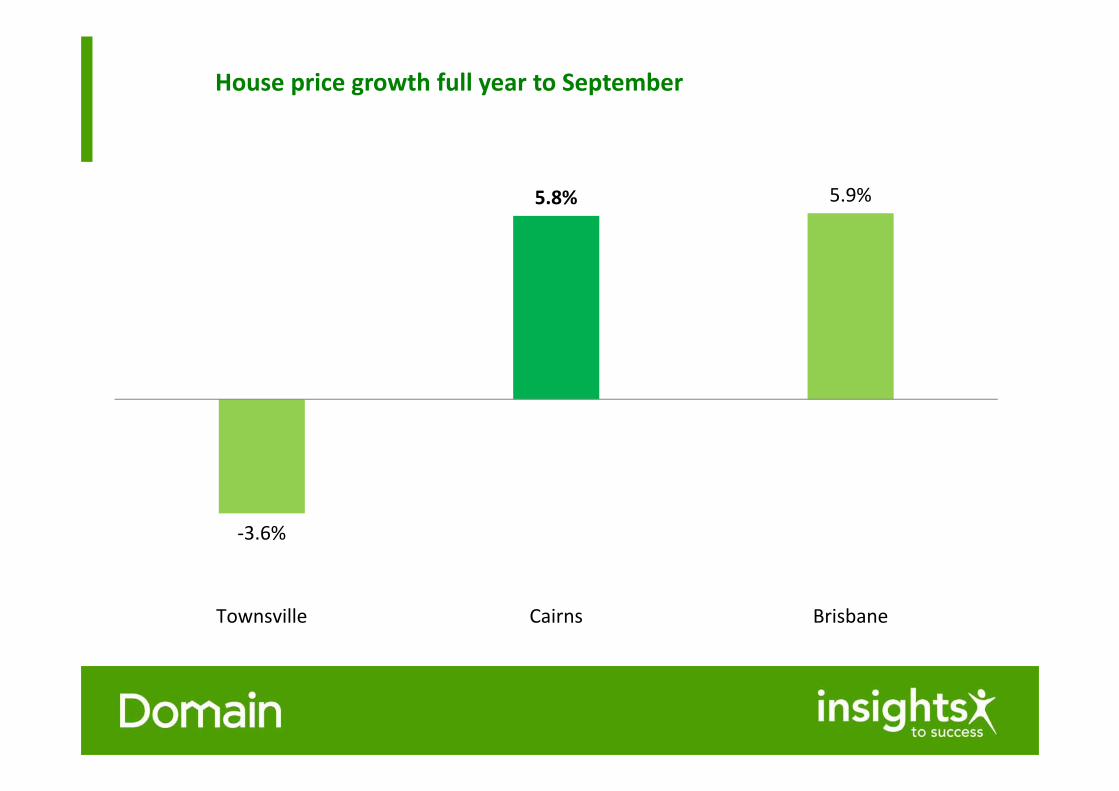

House price growth full year to September

‐3.6%

5.8% 5.9%

Townsville Cairns Brisbane

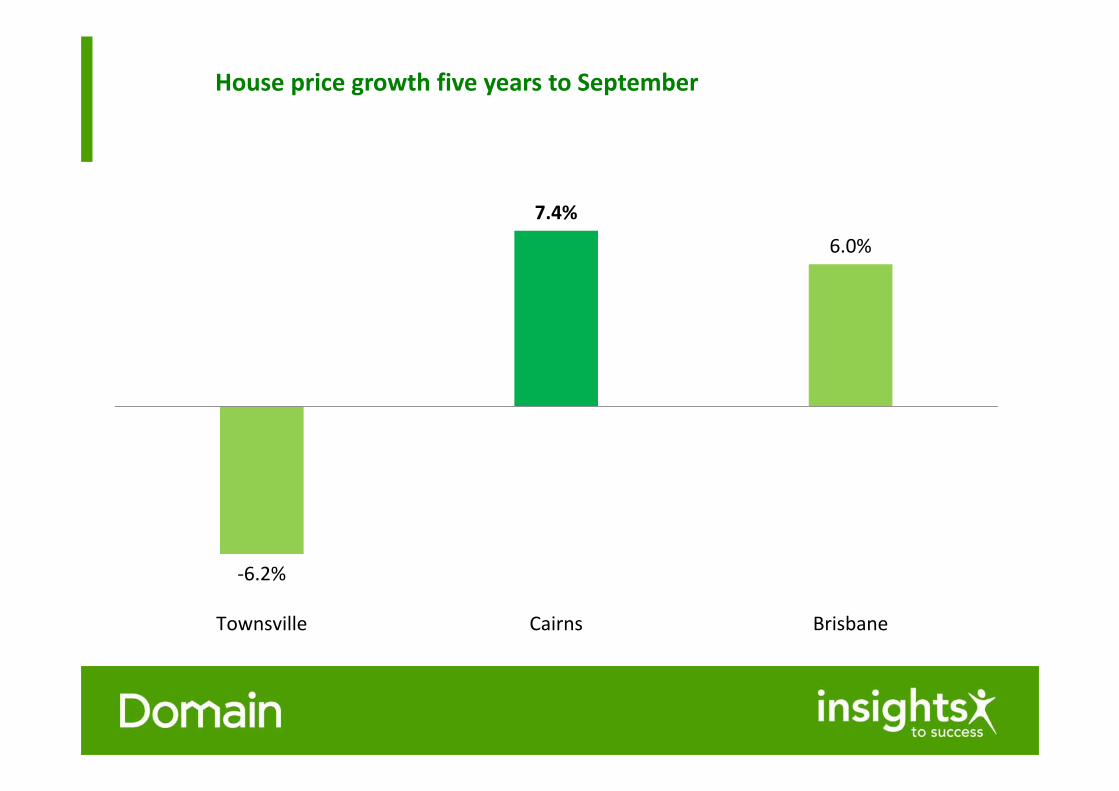

House price growth five years to September

‐6.2%

7.4%

6.0%

Townsville Cairns Brisbane

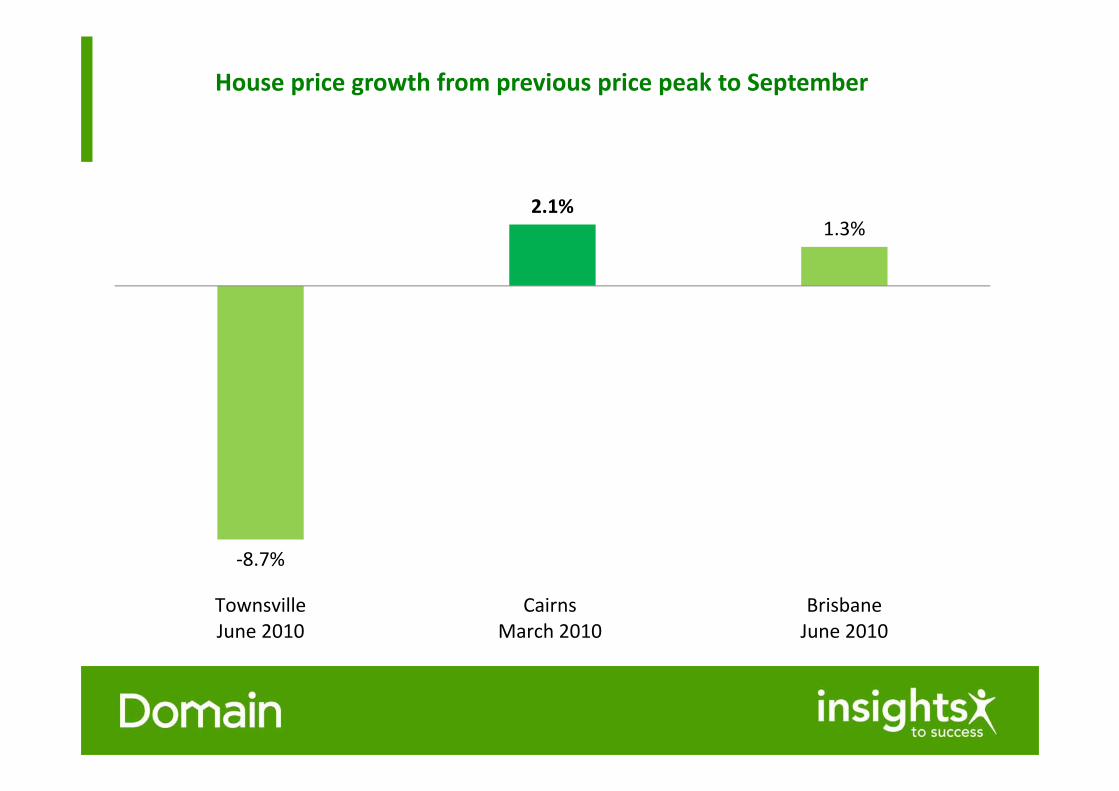

House price growth from previous price peak to September

‐8.7%

2.1%1.3%

TownsvilleJune 2010

CairnsMarch 2010

BrisbaneJune 2010

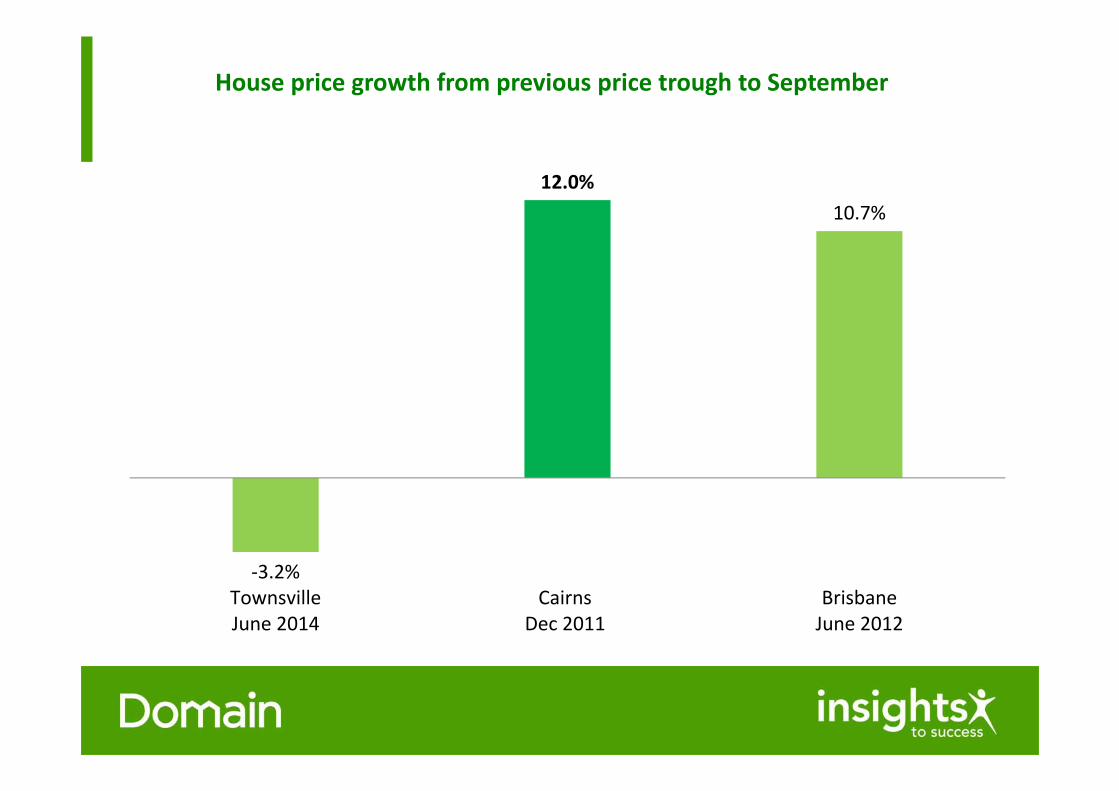

House price growth from previous price trough to September

‐3.2%

12.0%10.7%

TownsvilleJune 2014

CairnsDec 2011

BrisbaneJune 2012

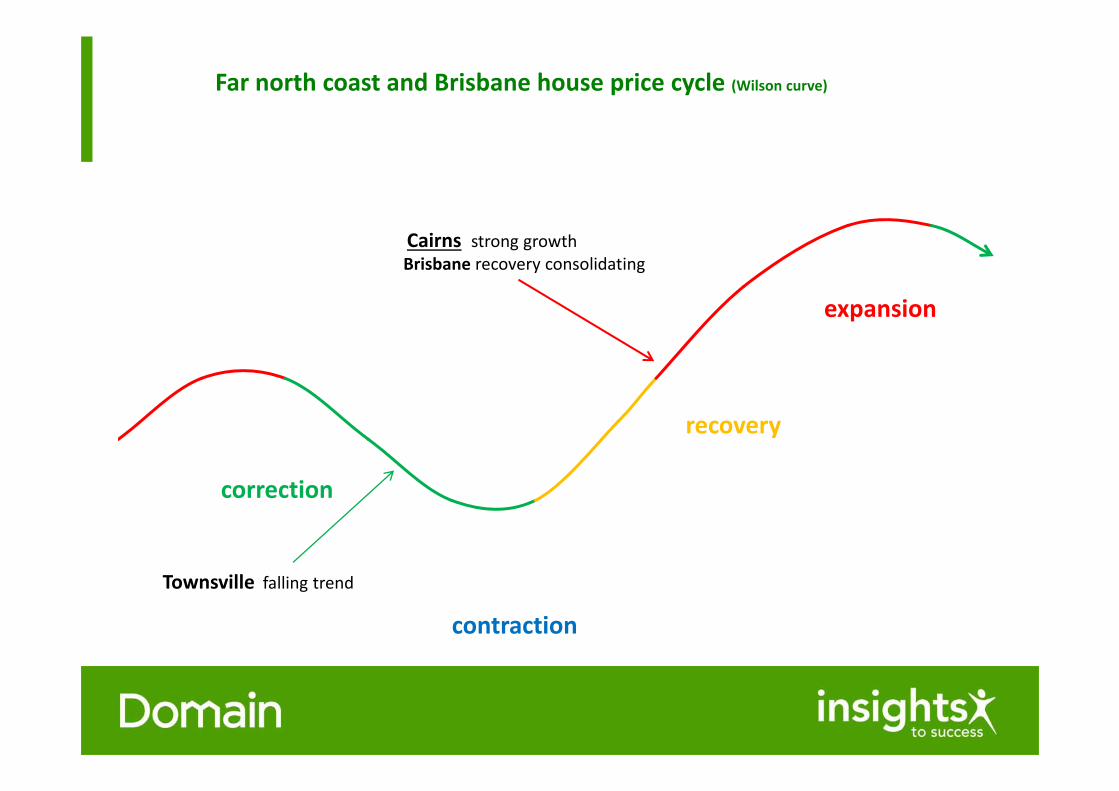

Far north coast and Brisbane house price cycle (Wilson curve)

correction

recovery

expansion

contraction

Cairns strong growthBrisbane recovery consolidating

Townsville falling trend

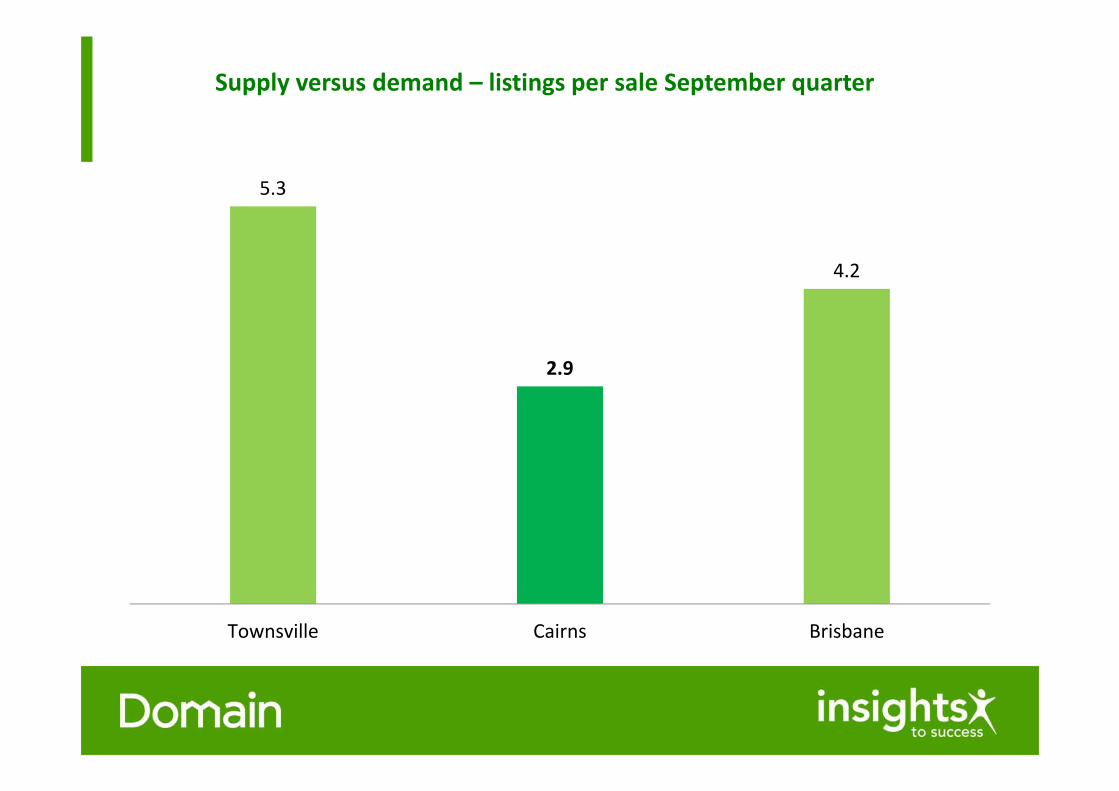

Supply versus demand – listings per sale September quarter

5.3

2.9

4.2

Townsville Cairns Brisbane

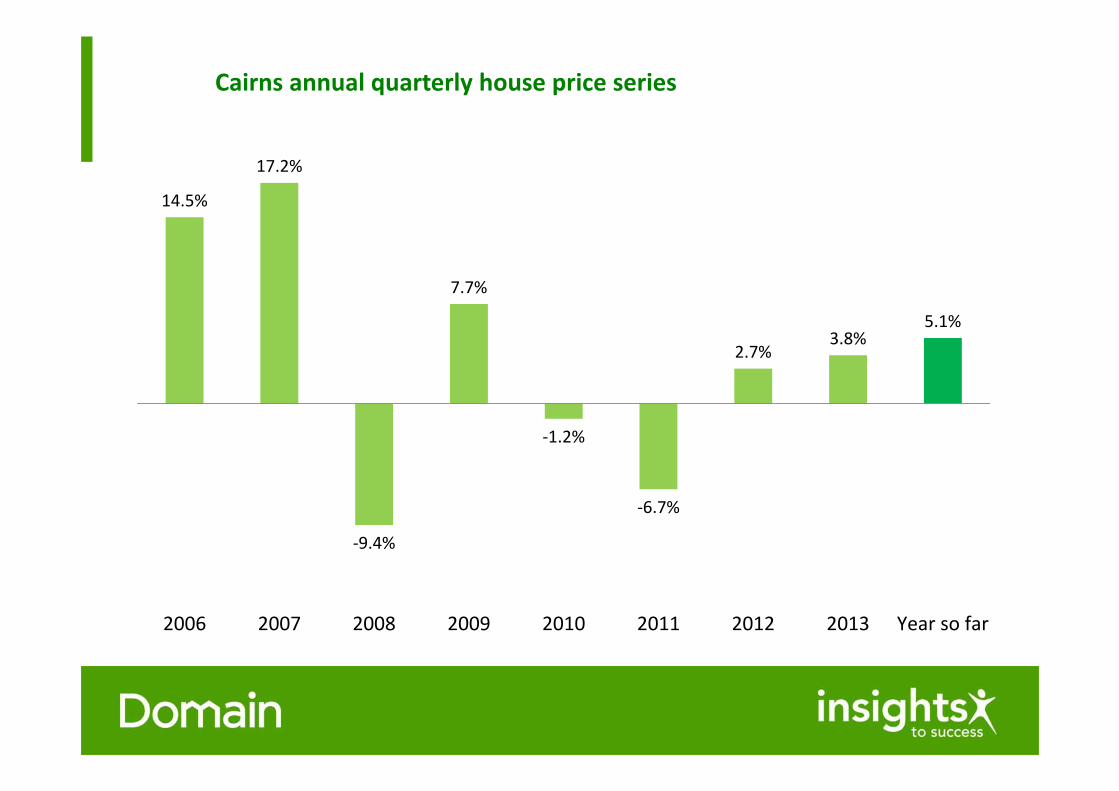

Cairns annual quarterly house price series

14.5%

17.2%

‐9.4%

7.7%

‐1.2%

‐6.7%

2.7%3.8%

5.1%

2006 2007 2008 2009 2010 2011 2012 2013 Year so far

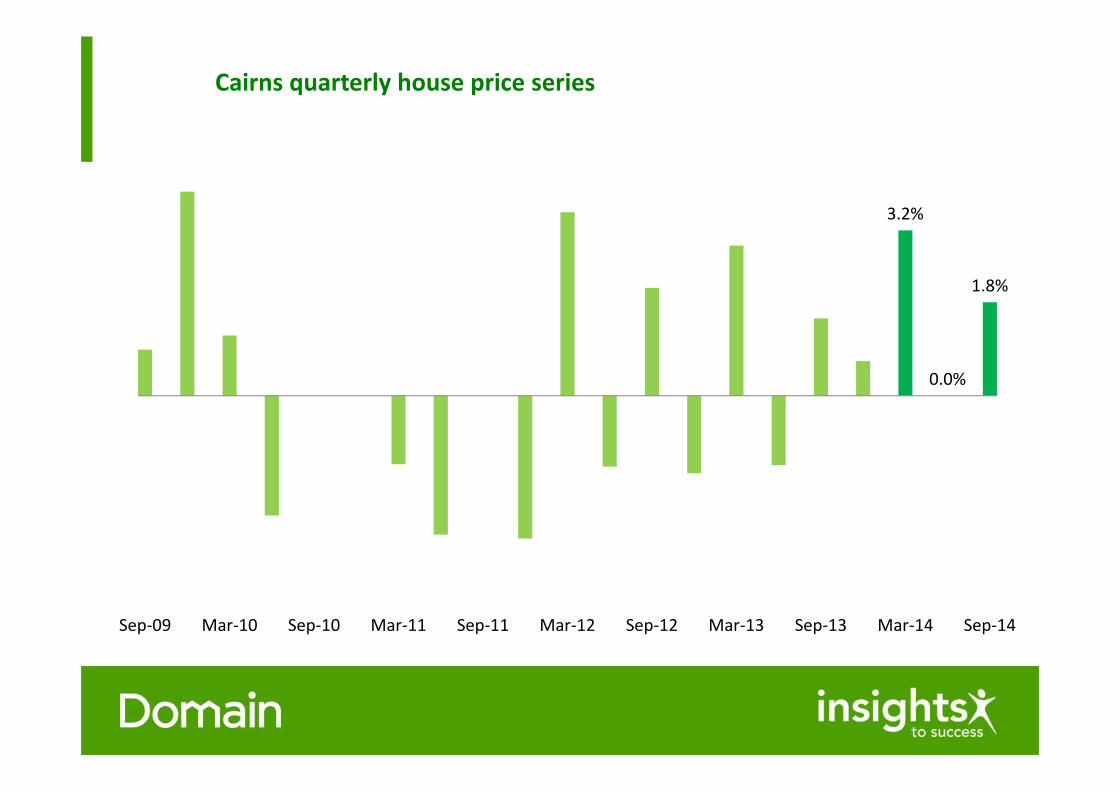

Cairns quarterly house price series

3.2%

0.0%

1.8%

Sep‐09 Mar‐10 Sep‐10 Mar‐11 Sep‐11 Mar‐12 Sep‐12 Mar‐13 Sep‐13 Mar‐14 Sep‐14

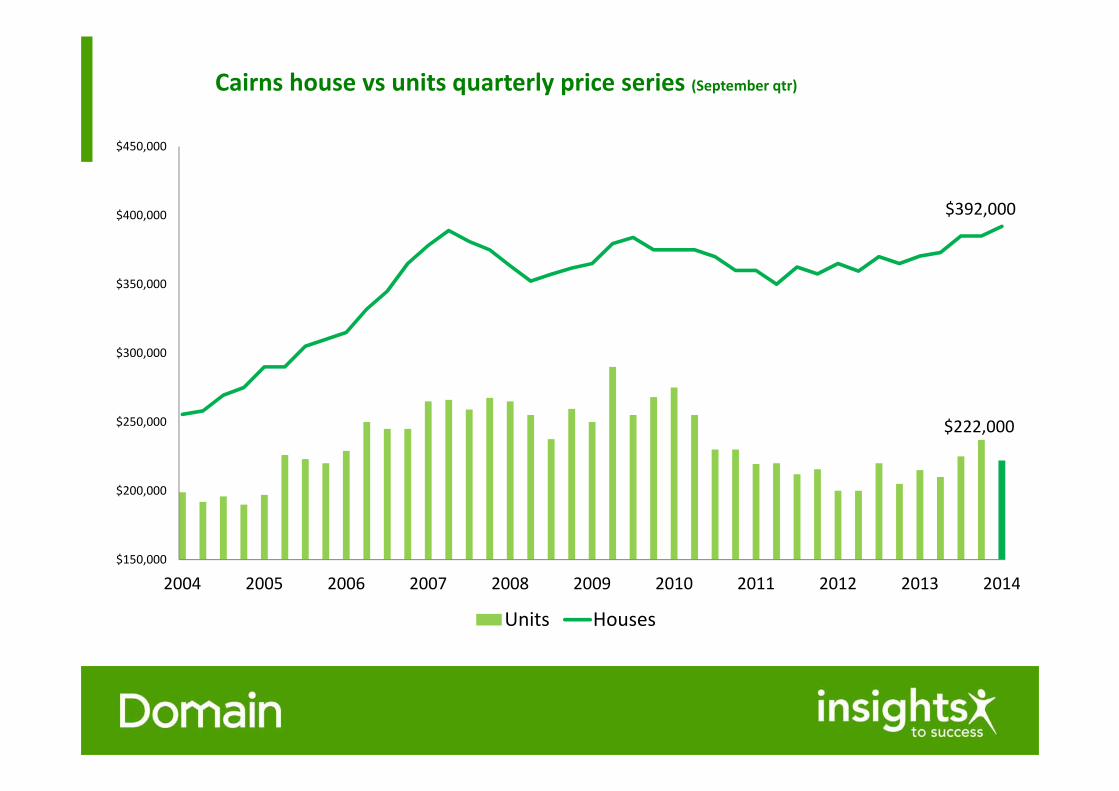

Cairns house vs units quarterly price series (September qtr)

$222,000

$392,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Units Houses

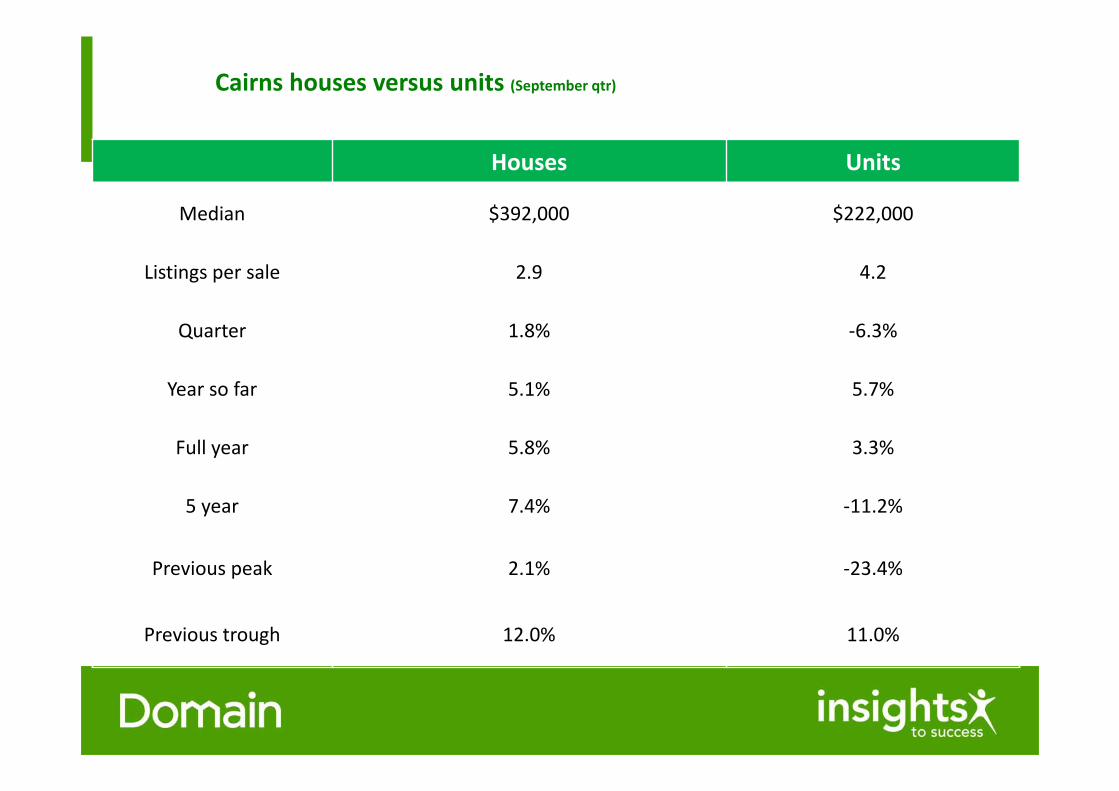

Cairns houses versus units (September qtr)

Houses Units

Median $392,000 $222,000

Listings per sale 2.9 4.2

Quarter 1.8% ‐6.3%

Year so far 5.1% 5.7%

Full year 5.8% 3.3%

5 year 7.4% ‐11.2%

Previous peak 2.1% ‐23.4%

Previous trough 12.0% 11.0%

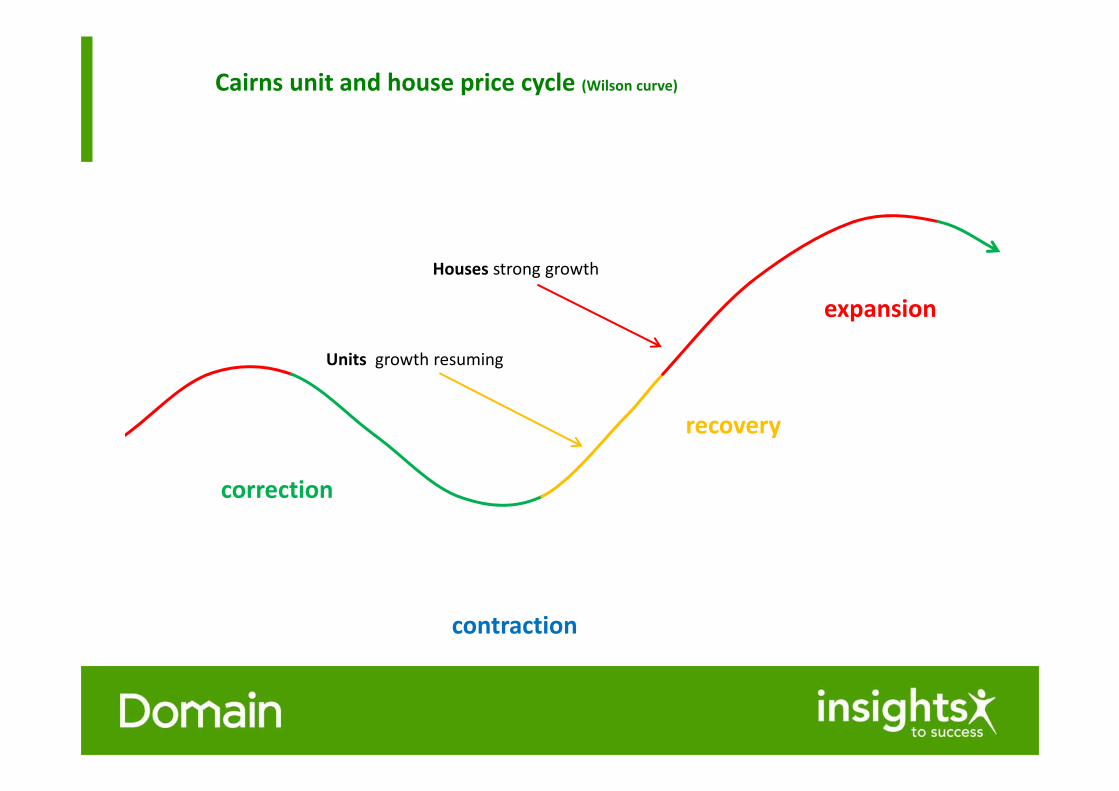

Cairns unit and house price cycle (Wilson curve)

correction

recovery

expansion

contraction

Houses strong growth

Units growth resuming

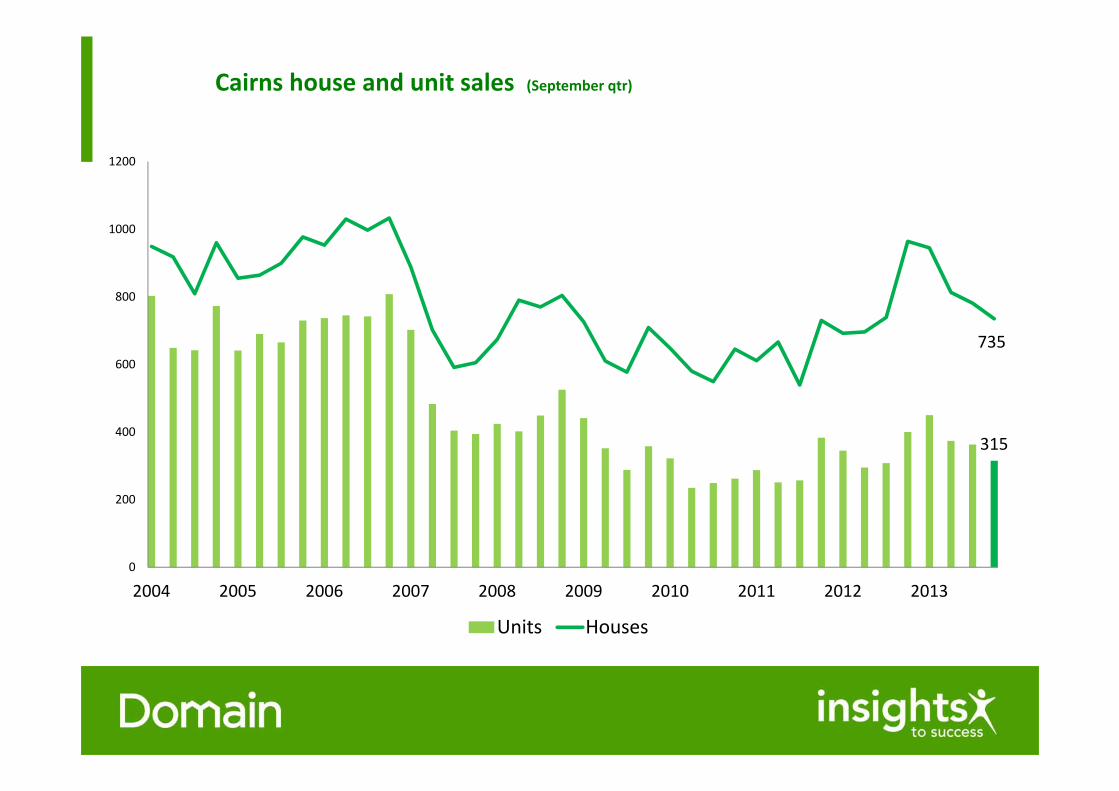

Cairns house and unit sales (September qtr)

315

735

0

200

400

600

800

1000

1200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Units Houses

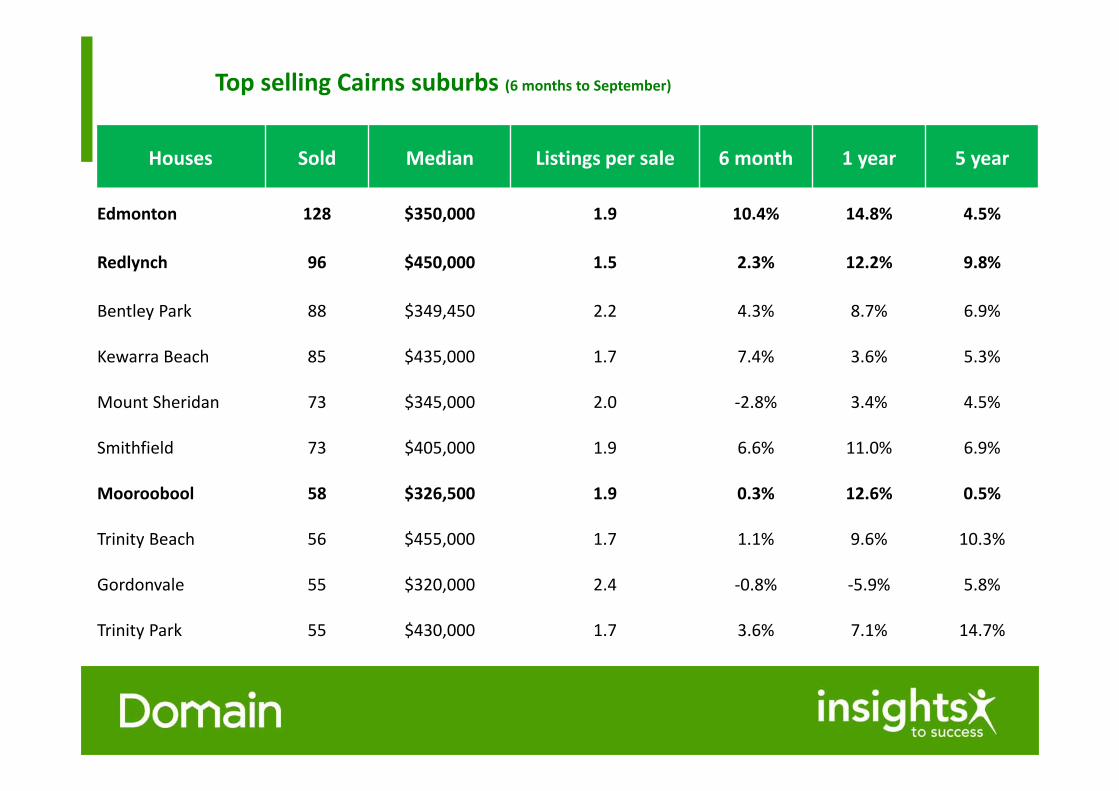

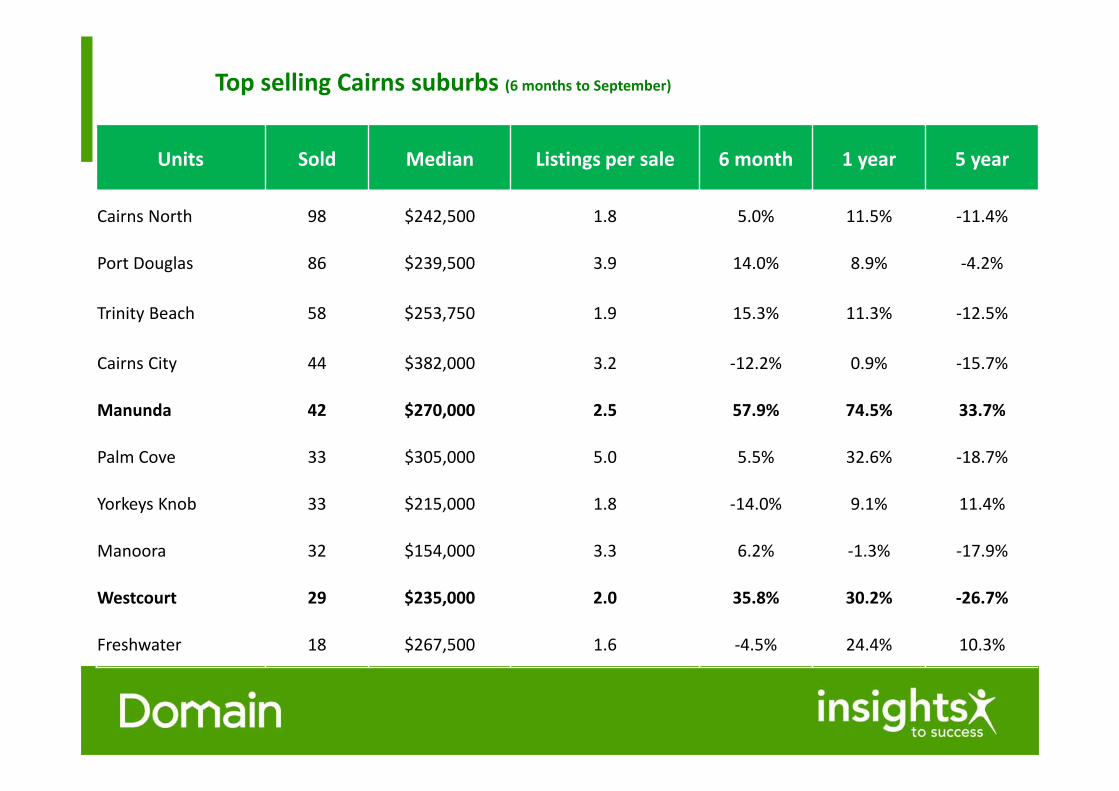

Top selling Cairns suburbs (6 months to September)

Houses Sold Median Listings per sale 6 month 1 year 5 year

Edmonton 128 $350,000 1.9 10.4% 14.8% 4.5%

Redlynch 96 $450,000 1.5 2.3% 12.2% 9.8%

Bentley Park 88 $349,450 2.2 4.3% 8.7% 6.9%

Kewarra Beach 85 $435,000 1.7 7.4% 3.6% 5.3%

Mount Sheridan 73 $345,000 2.0 ‐2.8% 3.4% 4.5%

Smithfield 73 $405,000 1.9 6.6% 11.0% 6.9%

Mooroobool 58 $326,500 1.9 0.3% 12.6% 0.5%

Trinity Beach 56 $455,000 1.7 1.1% 9.6% 10.3%

Gordonvale 55 $320,000 2.4 ‐0.8% ‐5.9% 5.8%

Trinity Park 55 $430,000 1.7 3.6% 7.1% 14.7%

Top selling Cairns suburbs (6 months to September)

Units Sold Median Listings per sale 6 month 1 year 5 year

Cairns North 98 $242,500 1.8 5.0% 11.5% ‐11.4%

Port Douglas 86 $239,500 3.9 14.0% 8.9% ‐4.2%

Trinity Beach 58 $253,750 1.9 15.3% 11.3% ‐12.5%

Cairns City 44 $382,000 3.2 ‐12.2% 0.9% ‐15.7%

Manunda 42 $270,000 2.5 57.9% 74.5% 33.7%

Palm Cove 33 $305,000 5.0 5.5% 32.6% ‐18.7%

Yorkeys Knob 33 $215,000 1.8 ‐14.0% 9.1% 11.4%

Manoora 32 $154,000 3.3 6.2% ‐1.3% ‐17.9%

Westcourt 29 $235,000 2.0 35.8% 30.2% ‐26.7%

Freshwater 18 $267,500 1.6 ‐4.5% 24.4% 10.3%

Cairns rental market

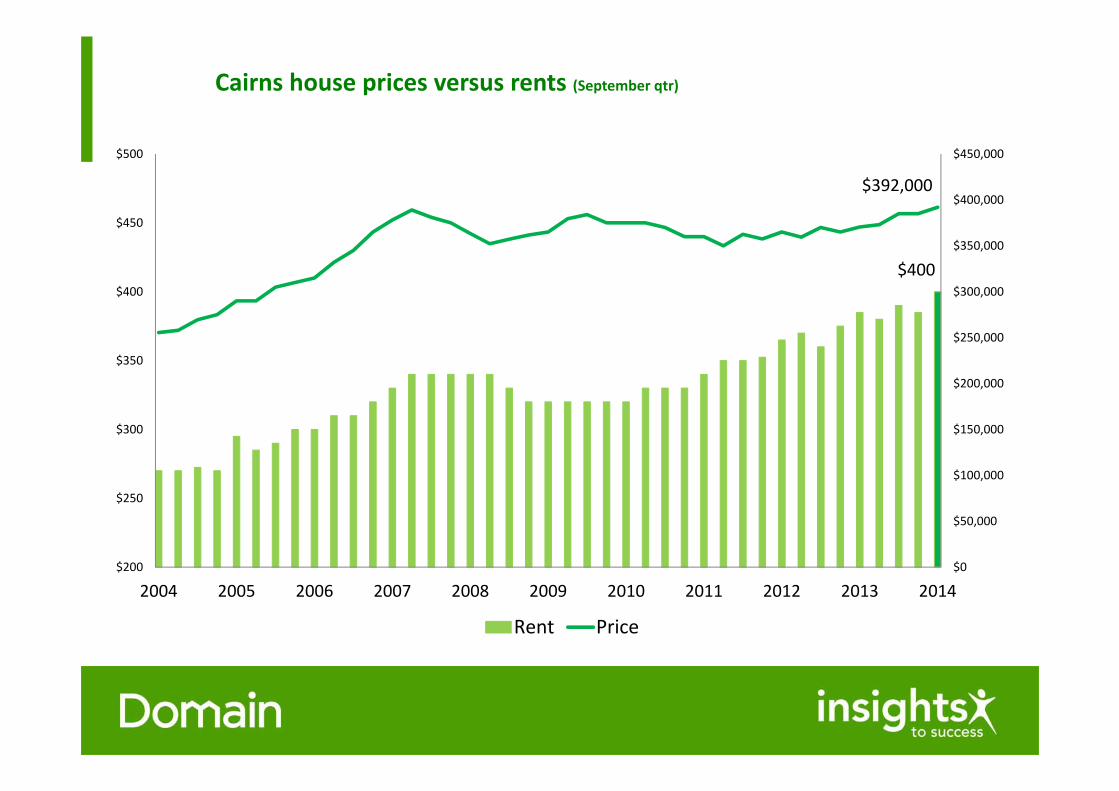

Cairns house prices versus rents (September qtr)

$400

$392,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$200

$250

$300

$350

$400

$450

$500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Rent Price

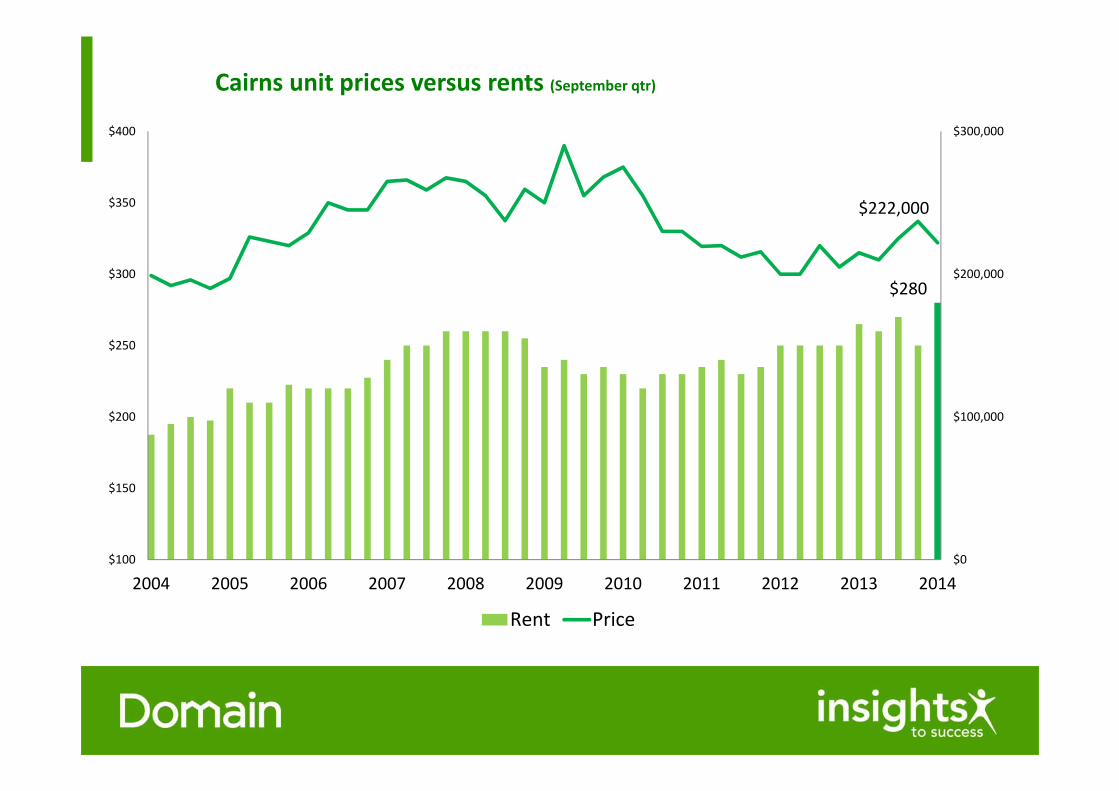

Cairns unit prices versus rents (September qtr)

$280

$222,000

$0

$100,000

$200,000

$300,000

$100

$150

$200

$250

$300

$350

$400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Rent Price

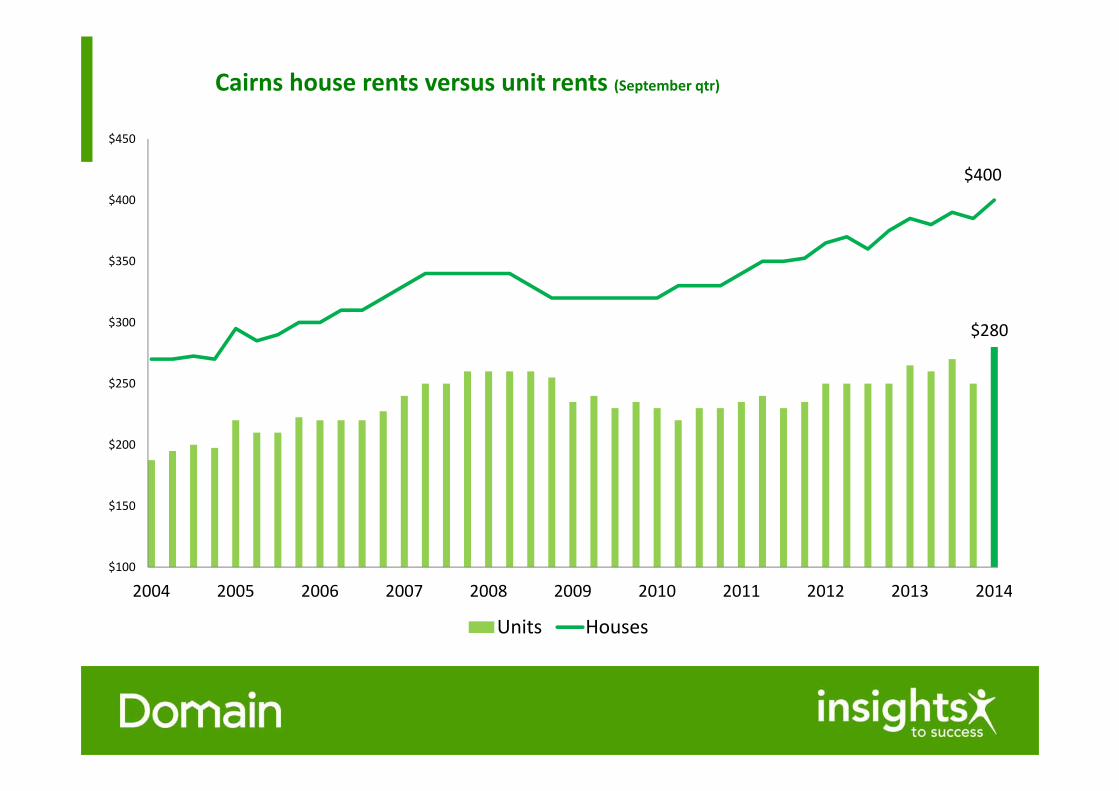

Cairns house rents versus unit rents (September qtr)

$280

$400

$100

$150

$200

$250

$300

$350

$400

$450

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Units Houses

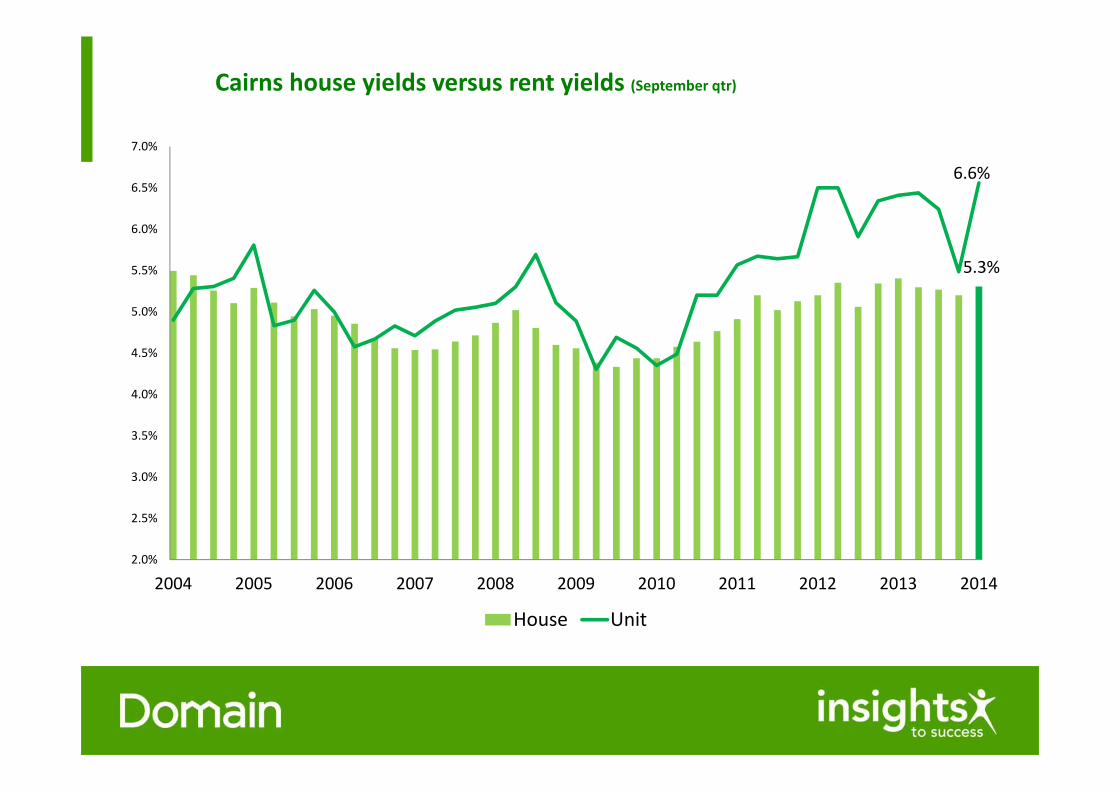

Cairns house yields versus rent yields (September qtr)

5.3%

6.6%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

House Unit

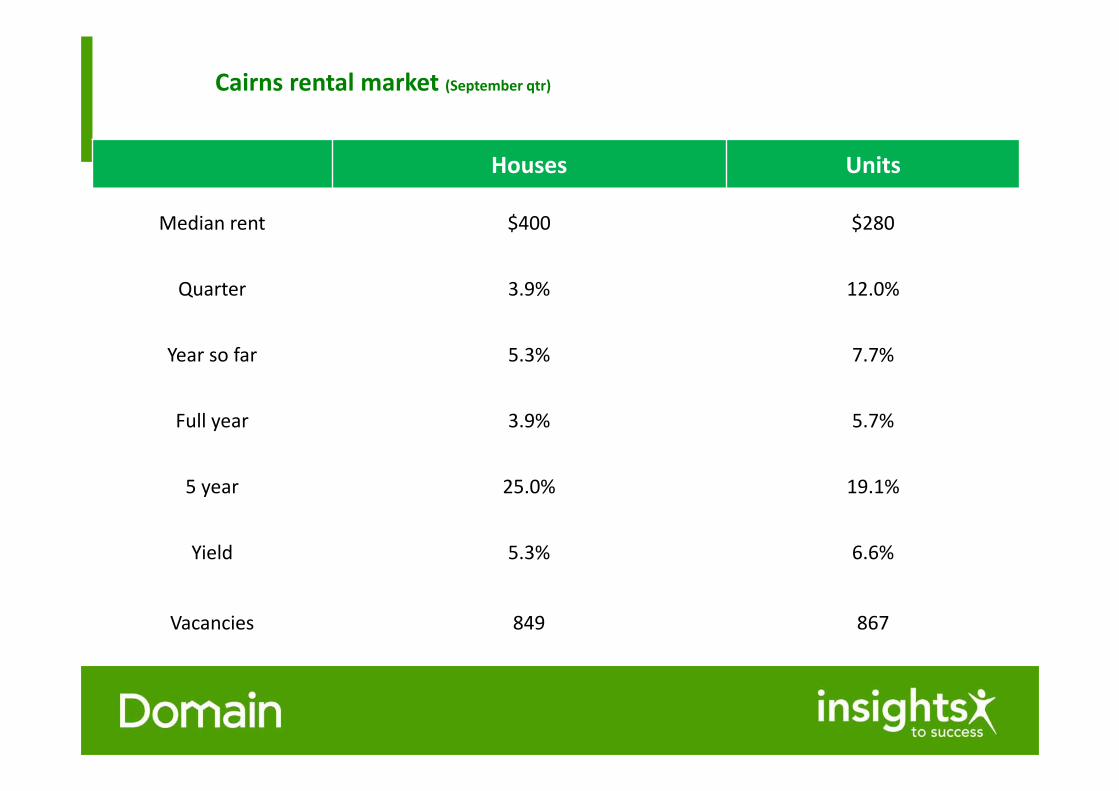

Cairns rental market (September qtr)

Houses Units

Median rent $400 $280

Quarter 3.9% 12.0%

Year so far 5.3% 7.7%

Full year 3.9% 5.7%

5 year 25.0% 19.1%

Yield 5.3% 6.6%

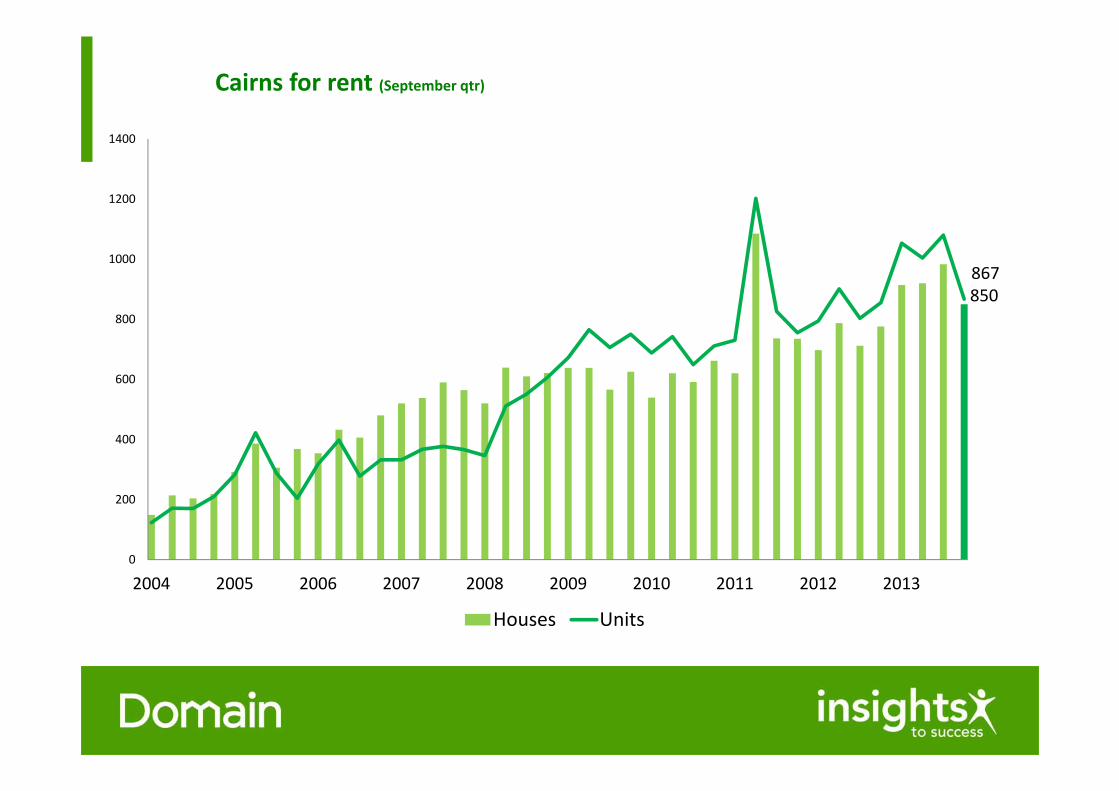

Vacancies 849 867

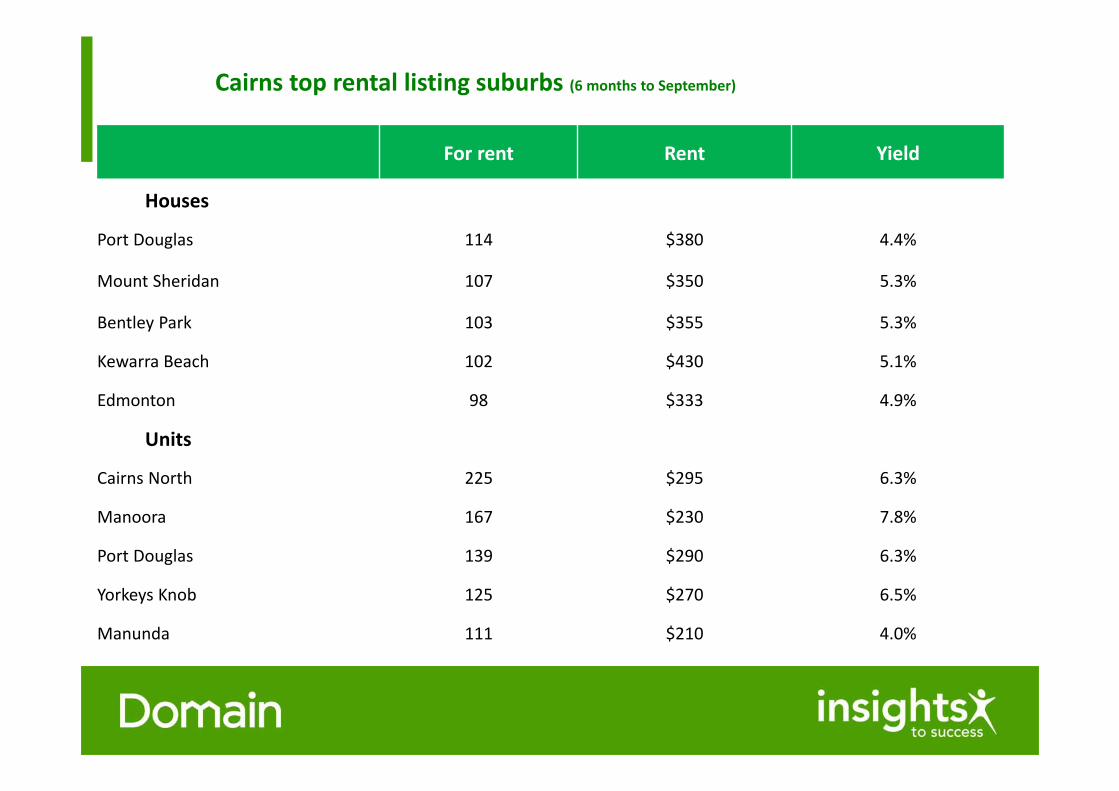

Cairns top rental listing suburbs (6 months to September)

For rent Rent Yield

Houses

Port Douglas 114 $380 4.4%

Mount Sheridan 107 $350 5.3%

Bentley Park 103 $355 5.3%

Kewarra Beach 102 $430 5.1%

Edmonton 98 $333 4.9%

Units

Cairns North 225 $295 6.3%

Manoora 167 $230 7.8%

Port Douglas 139 $290 6.3%

Yorkeys Knob 125 $270 6.5%

Manunda 111 $210 4.0%

Cairns for rent (September qtr)

850867

0

200

400

600

800

1000

1200

1400

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Houses Units

Cairns key market drivers

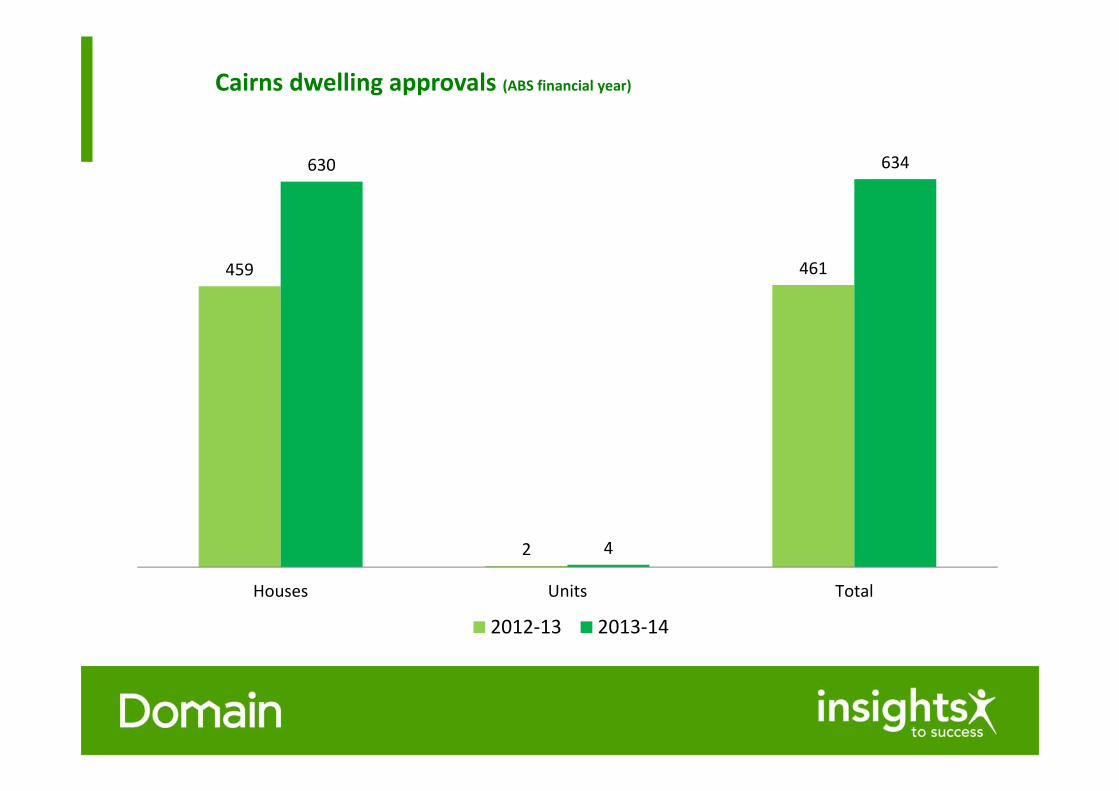

Cairns dwelling approvals (ABS financial year)

459

2

461

630

4

634

Houses Units Total

2012‐13 2013‐14

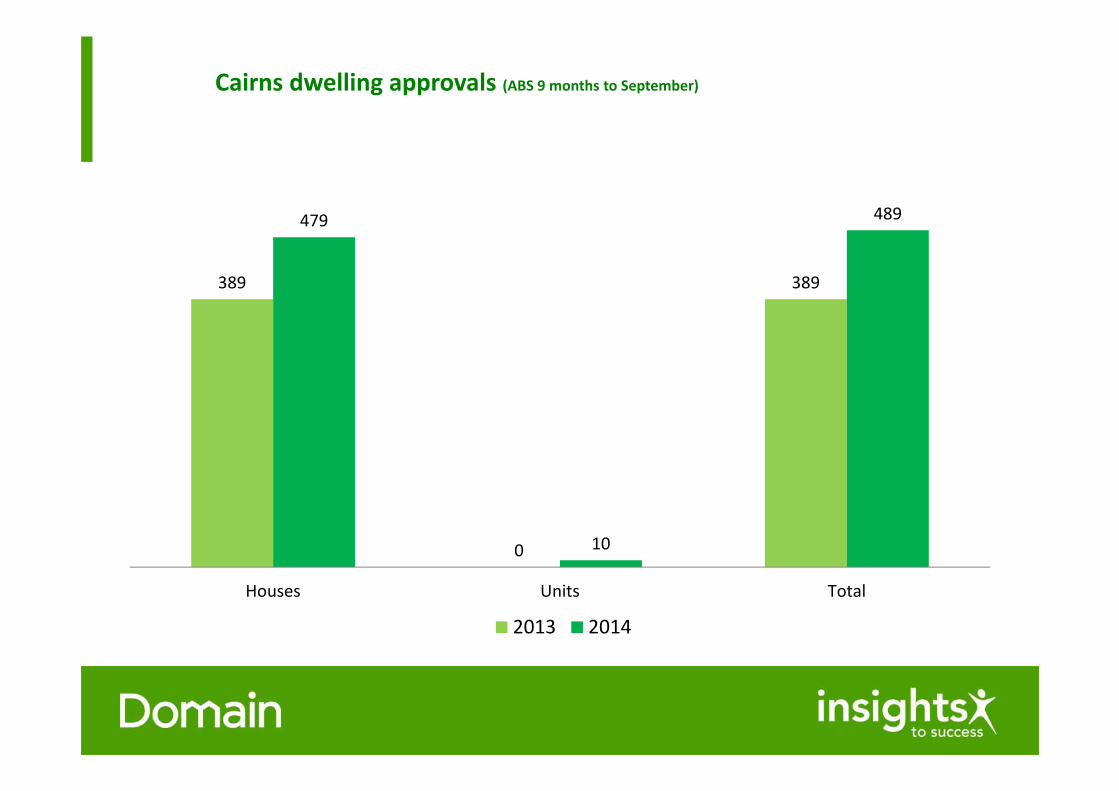

Cairns dwelling approvals (ABS 9 months to September)

389

0

389

479

10

489

Houses Units Total

2013 2014

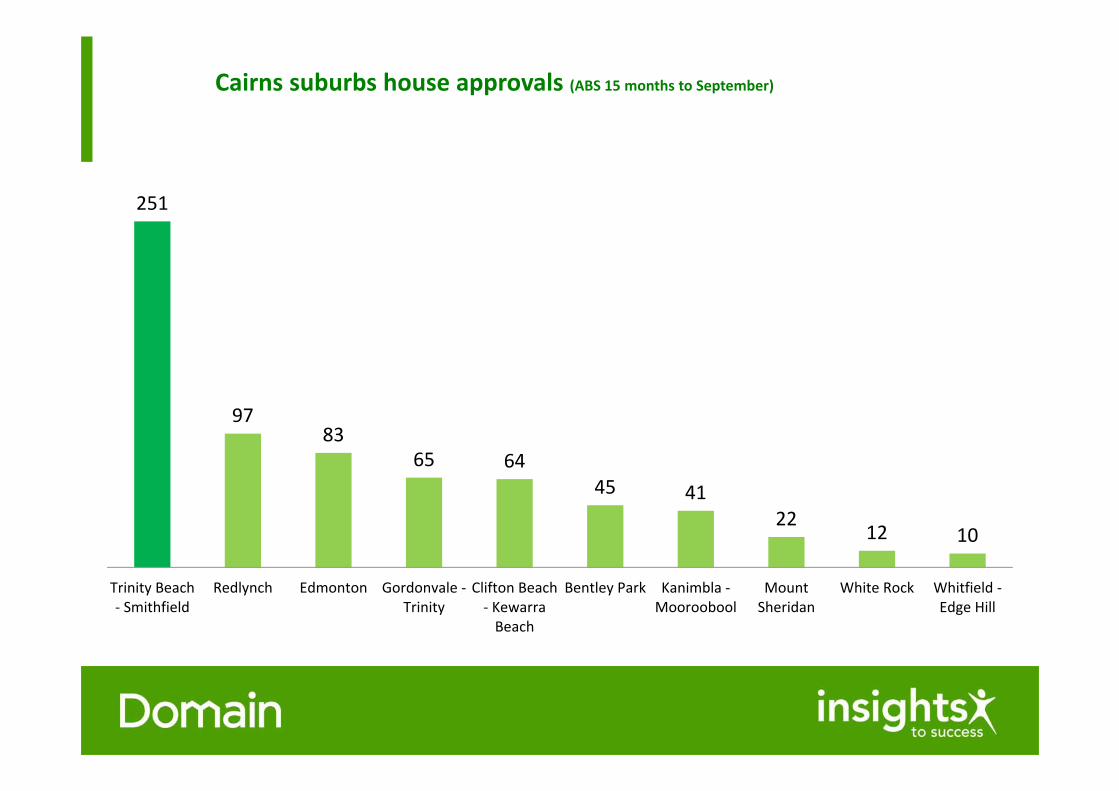

Cairns suburbs house approvals (ABS 15 months to September)

251

9783

65 6445 41

2212 10

Trinity Beach‐ Smithfield

Redlynch Edmonton Gordonvale ‐Trinity

Clifton Beach‐ KewarraBeach

Bentley Park Kanimbla ‐Mooroobool

MountSheridan

White Rock Whitfield ‐Edge Hill

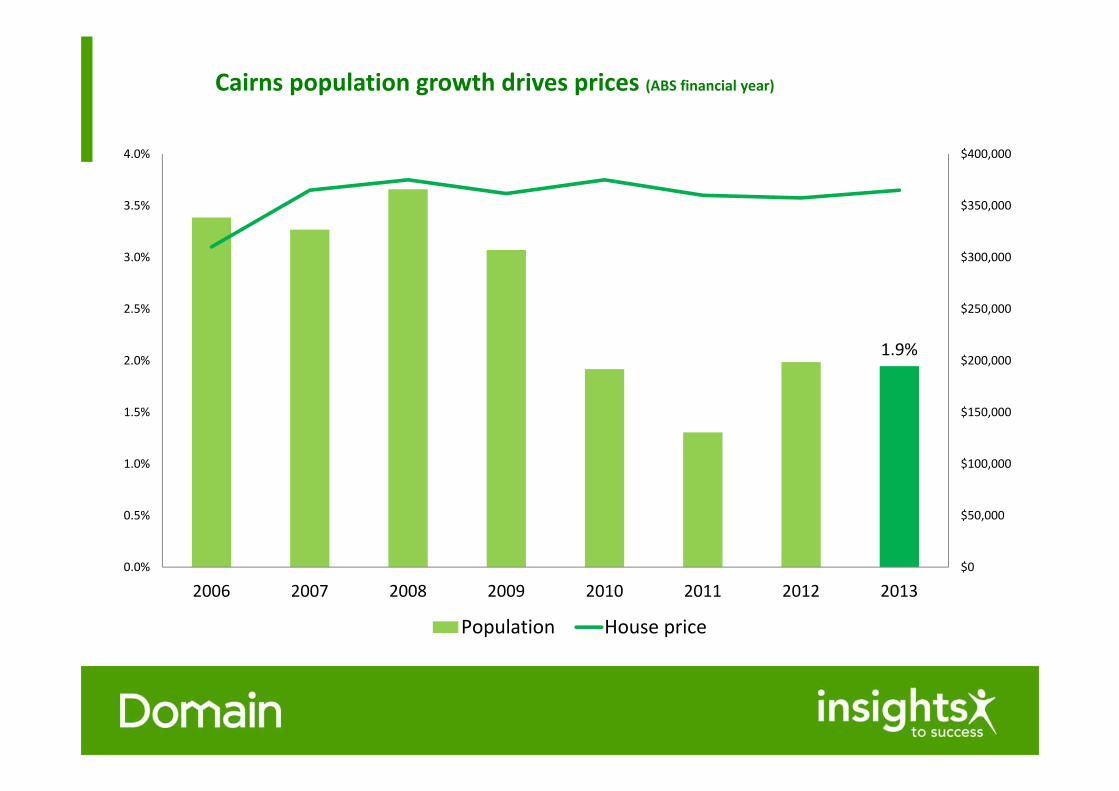

Cairns population growth drives prices (ABS financial year)

1.9%

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2006 2007 2008 2009 2010 2011 2012 2013

Population House price

Cairns economic performance

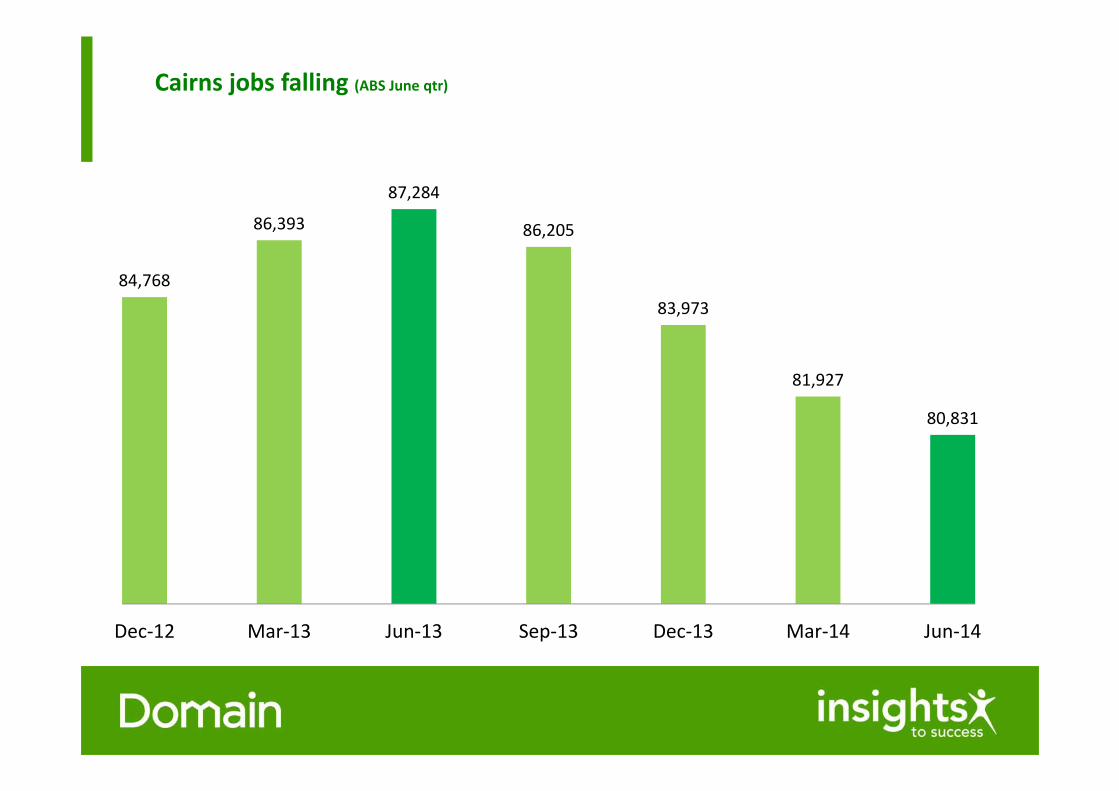

Cairns jobs falling (ABS June qtr)

84,768

86,393

87,284

86,205

83,973

81,927

80,831

Dec‐12 Mar‐13 Jun‐13 Sep‐13 Dec‐13 Mar‐14 Jun‐14

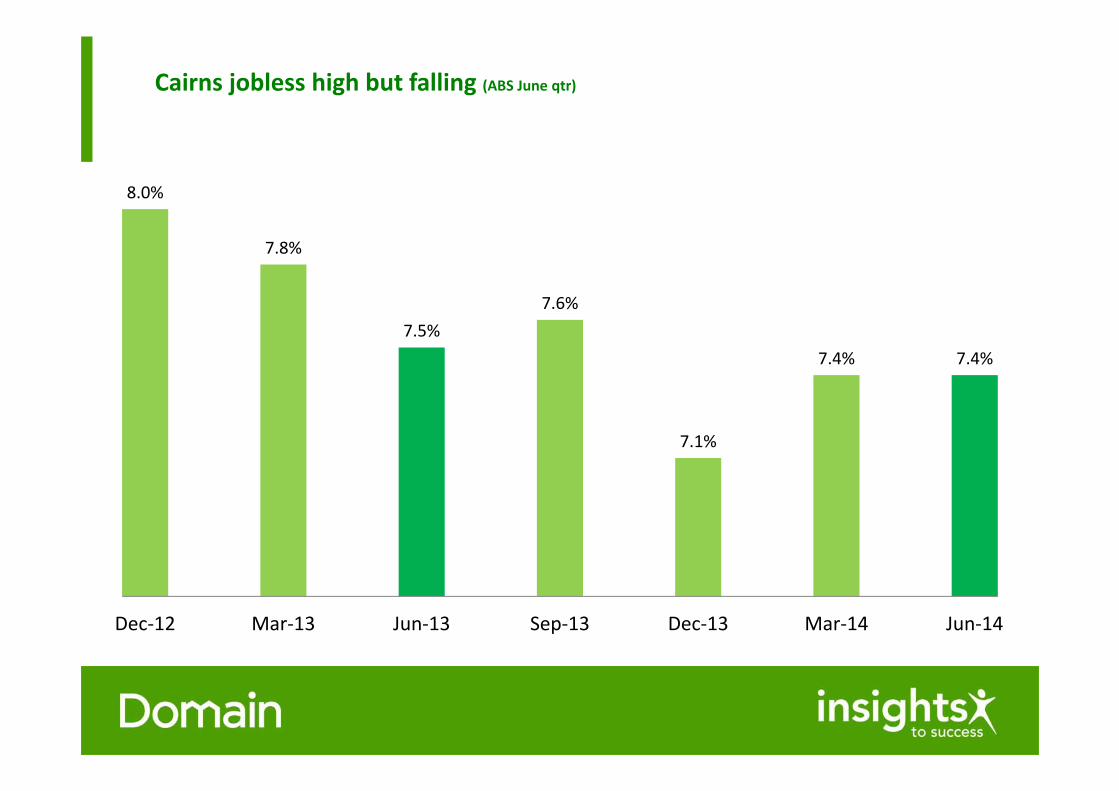

Cairns jobless high but falling (ABS June qtr)

8.0%

7.8%

7.5%7.6%

7.1%

7.4% 7.4%

Dec‐12 Mar‐13 Jun‐13 Sep‐13 Dec‐13 Mar‐14 Jun‐14

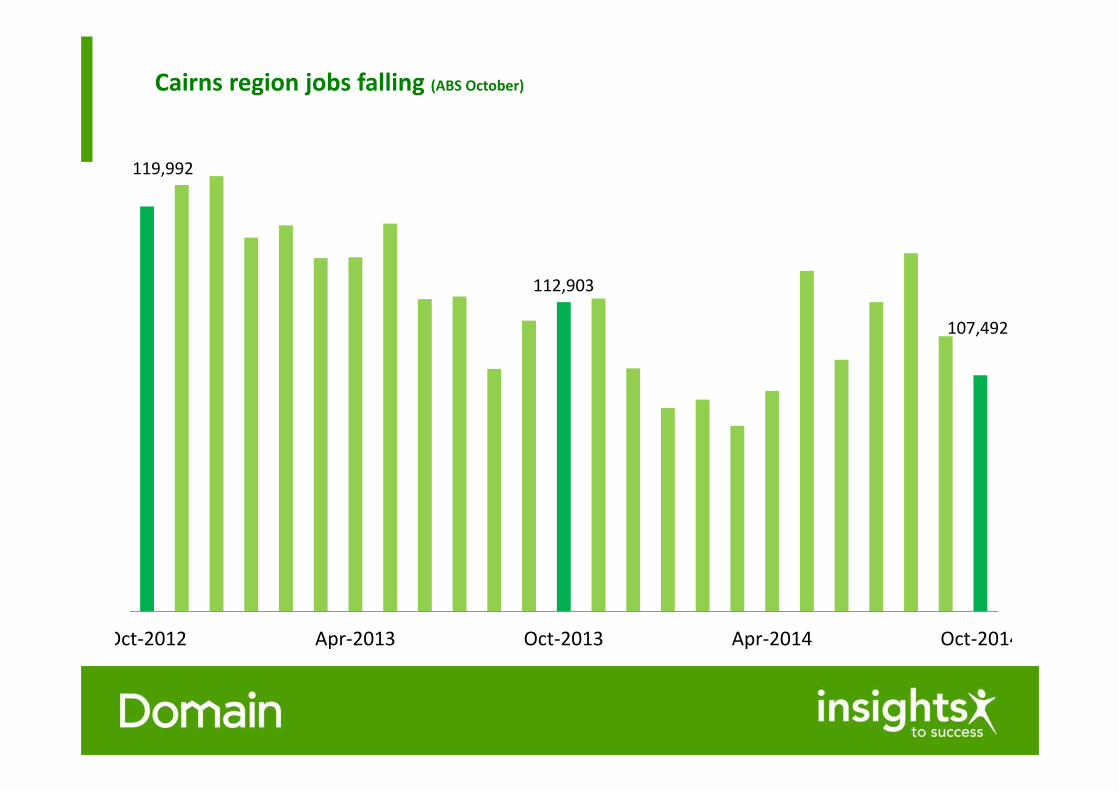

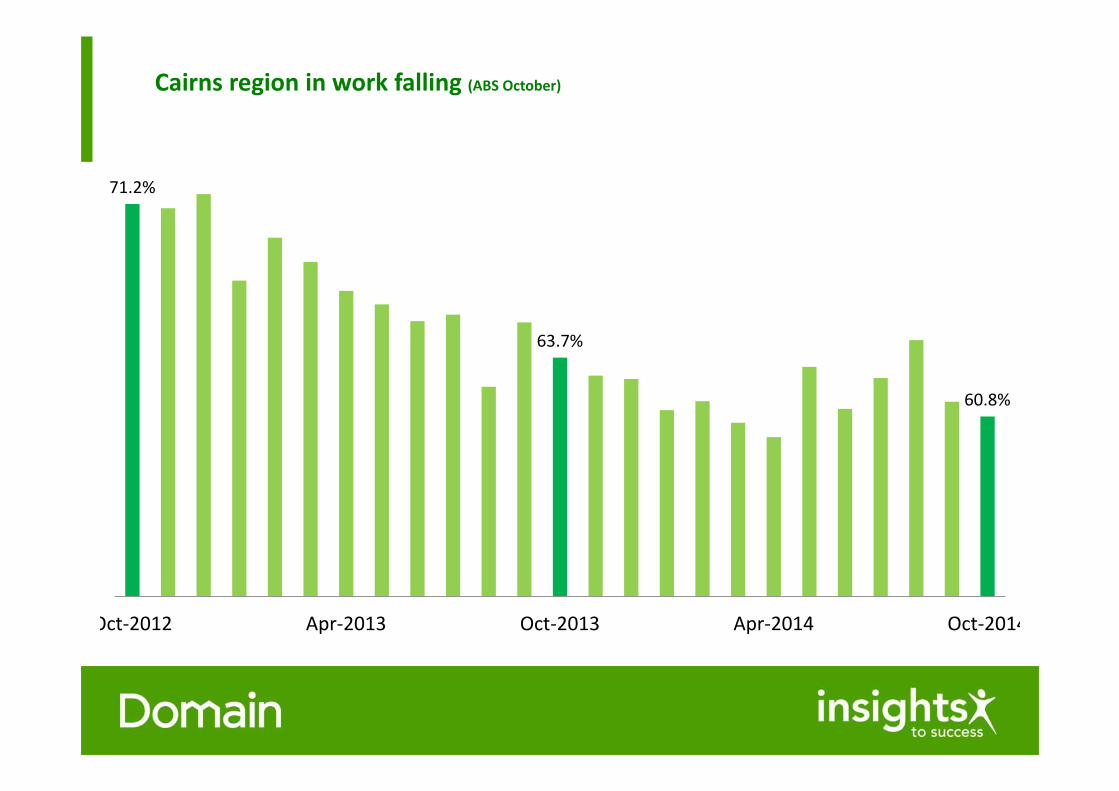

Cairns region jobs falling (ABS October)

119,992

112,903

107,492

Oct‐2012 Apr‐2013 Oct‐2013 Apr‐2014 Oct‐2014

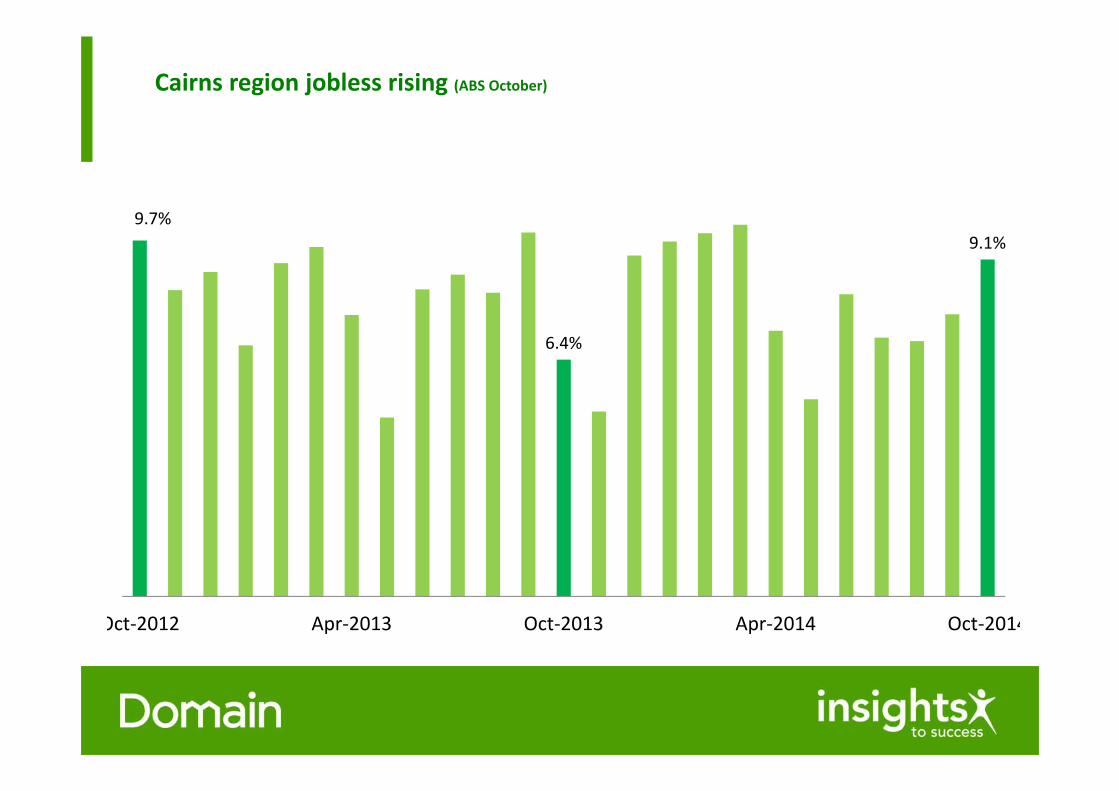

Cairns region jobless rising (ABS October)

9.7%

6.4%

9.1%

Oct‐2012 Apr‐2013 Oct‐2013 Apr‐2014 Oct‐2014

Cairns region in work falling (ABS October)

71.2%

63.7%

60.8%

Oct‐2012 Apr‐2013 Oct‐2013 Apr‐2014 Oct‐2014

National economic performance

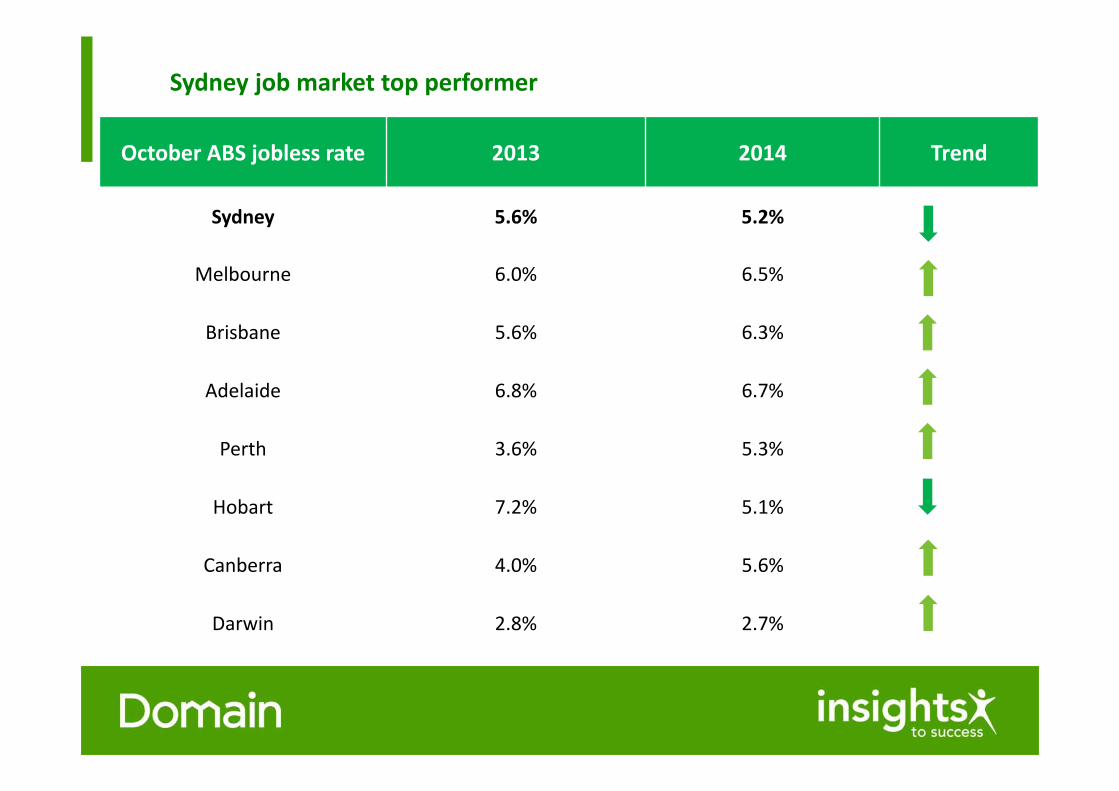

Sydney job market top performer

October ABS jobless rate 2013 2014 Trend

Sydney 5.6% 5.2%

Melbourne 6.0% 6.5%

Brisbane 5.6% 6.3%

Adelaide 6.8% 6.7%

Perth 3.6% 5.3%

Hobart 7.2% 5.1%

Canberra 4.0% 5.6%

Darwin 2.8% 2.7%

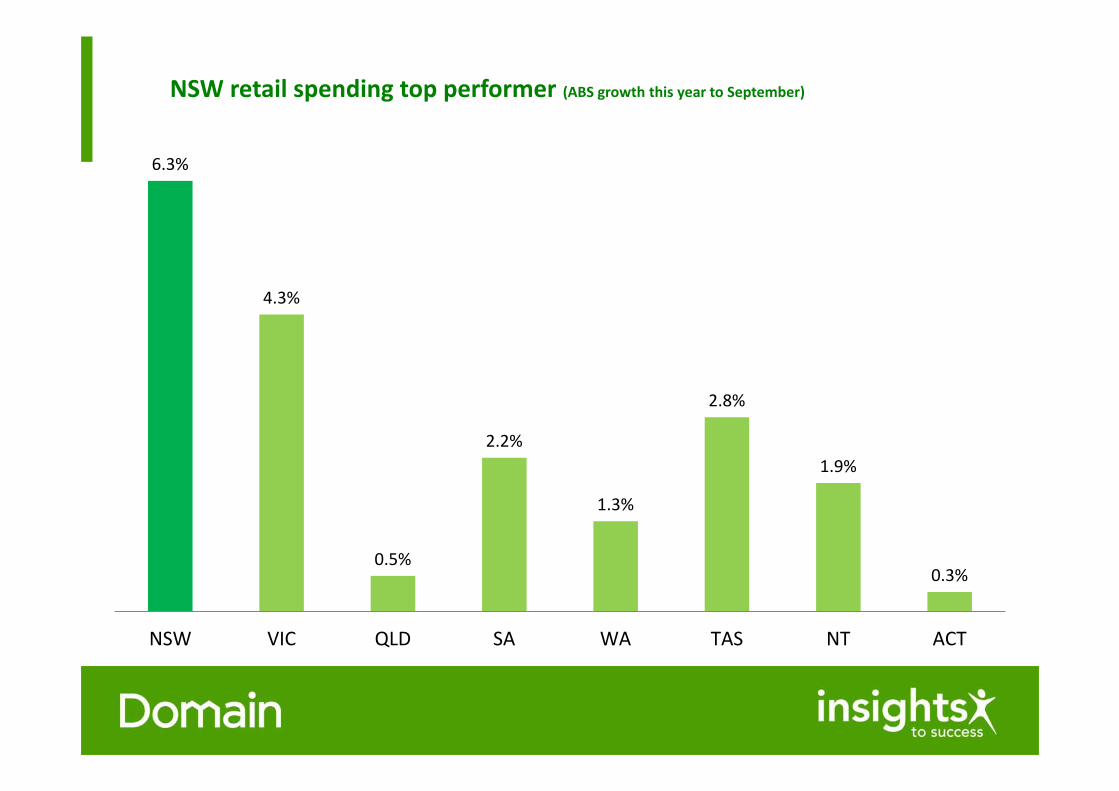

6.3%

4.3%

0.5%

2.2%

1.3%

2.8%

1.9%

0.3%

NSW VIC QLD SA WA TAS NT ACT

NSW retail spending top performer (ABS growth this year to September)

Economic outlook

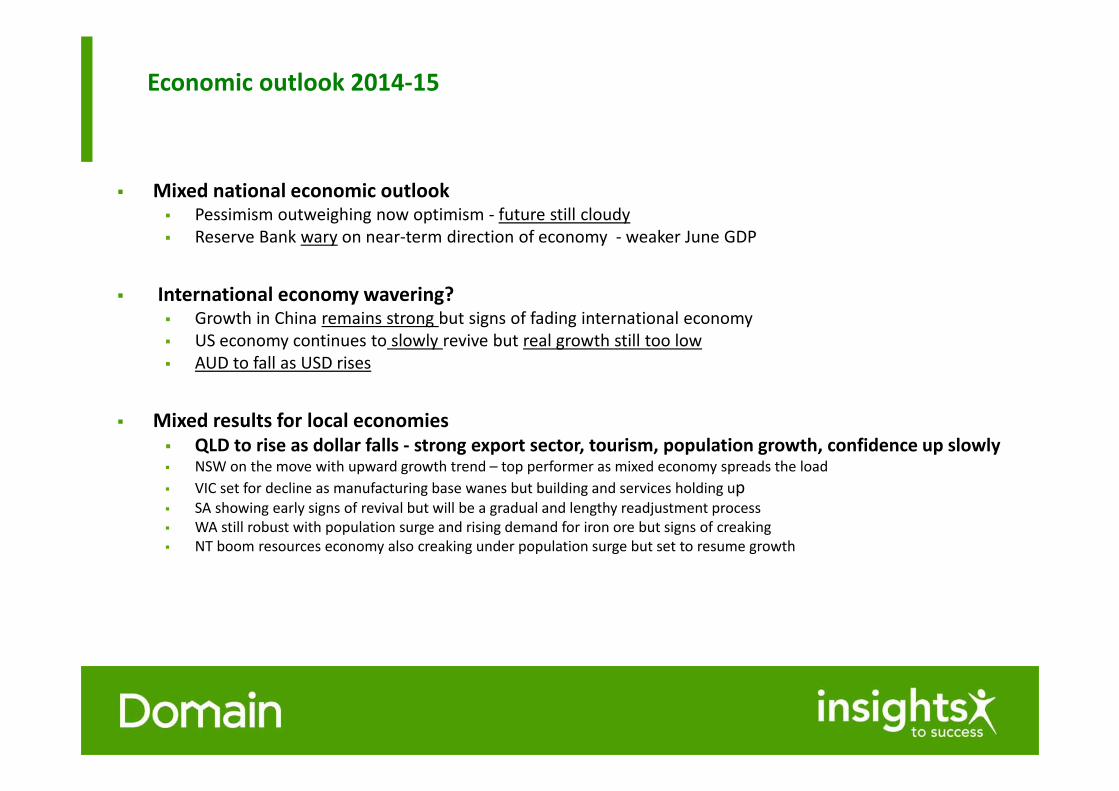

Economic outlook 2014‐15

Mixed national economic outlook Pessimism outweighing now optimism ‐ future still cloudy Reserve Bank wary on near‐term direction of economy ‐ weaker June GDP

International economy wavering? Growth in China remains strong but signs of fading international economy US economy continues to slowly revive but real growth still too low AUD to fall as USD rises

Mixed results for local economies QLD to rise as dollar falls ‐ strong export sector, tourism, population growth, confidence up slowly NSW on the move with upward growth trend – top performer as mixed economy spreads the load VIC set for decline as manufacturing base wanes but building and services holding up SA showing early signs of revival but will be a gradual and lengthy readjustment process WA still robust with population surge and rising demand for iron ore but signs of creaking NT boom resources economy also creaking under population surge but set to resume growth

Local economic drivers ‐ rates low, shares up, dollar too high, wages flat

Interest rates to remain at 60 year low Downward bias if jobless above 6% ‐ upward bias if below 5% Mortgage costs falling as banks compete for market share – but still above 2009 rates Rates to remain on hold over short‐term – at least into 2015 – but watch the currency

Stockmarket rising gradually with lower dollar but hostage to global forces Investors shift to shares and increased international investment with lower dollar Solid growth upside as still 15% below 2007 peak, unlike other exchanges at or near highs

Inflation to rise gradually with medium‐term lower dollar Then imports more expensive – higher fuel cost impacts economy. Living standards fall But wages and profits subdued in a low inflation economy – places lid on house price growth

Government spending constrained by high deficit ‐ horror budget? Retail sales, building , profits, sentiment and exports improving but still mixed

Cairns housing market outlook

• Continued solid prices growth from strong regional housing market – despite economic concerns• High levels of confidence re‐established in local market• Best performer of all major Queensland housing markets• Solid competition for available property from buyers • Market continues to track Brisbane long‐term price relationship• Unit market rising with houses – but from low base • Rents rising with prices for houses and units – high gross yields

• Still reasonable economic performance for a lifestyle market – but challenges remain • Unemployment still high but down• But job numbers down as mining activity diminishes and agriculture flat• Lower dollar will however reactivate Queensland economy – over medium term• Lower dollar also a big positive for Cairns ‐ significant tourism and international investment • House construction on the rise as demand intensifies – positive for the local economy

• Cairns house prices set to increase by 5‐7 percent in 2015 ‐ one of the best national outcomes

Cairns housing market outlook 2015 ‐ solid prices growth to continue

National housing market outlook

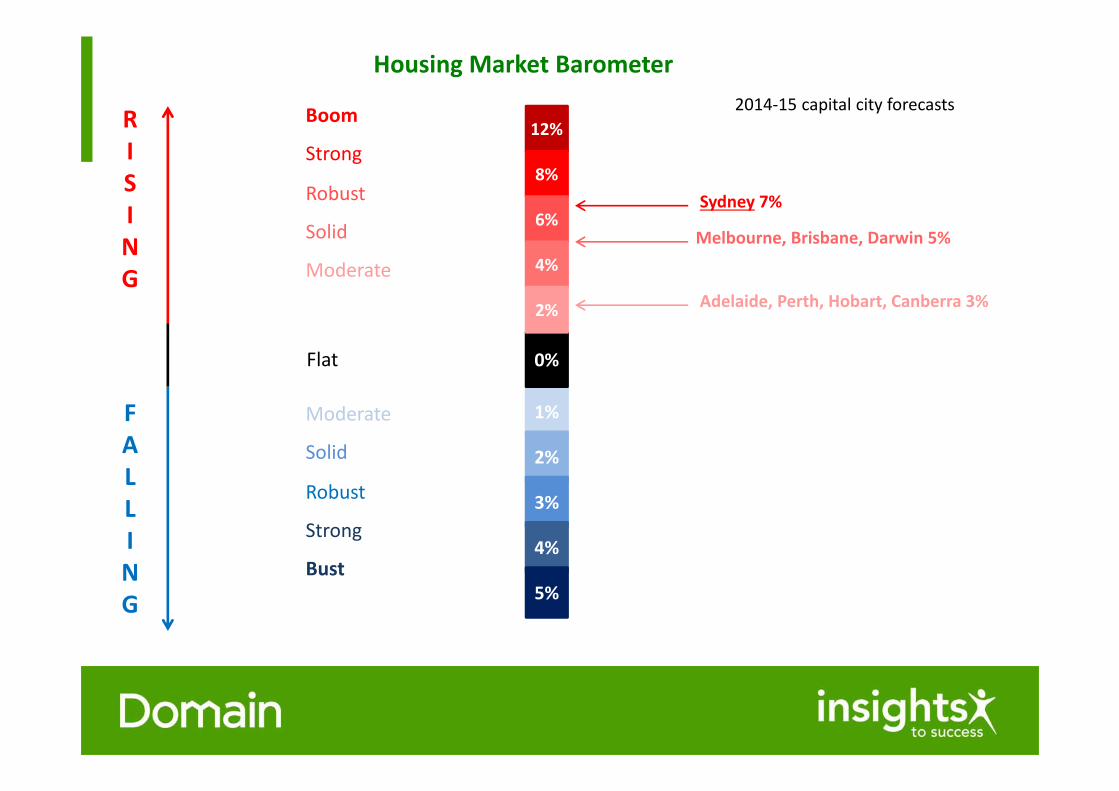

Housing Market Barometer

12%

2%

1%

0%

0%

Sydney 7%

Adelaide, Perth, Hobart, Canberra 3%

Melbourne, Brisbane, Darwin 5%

RISING

FALLING

2014‐15 capital city forecasts

5%

4% 8%

6%

4%

2%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

The rising tide

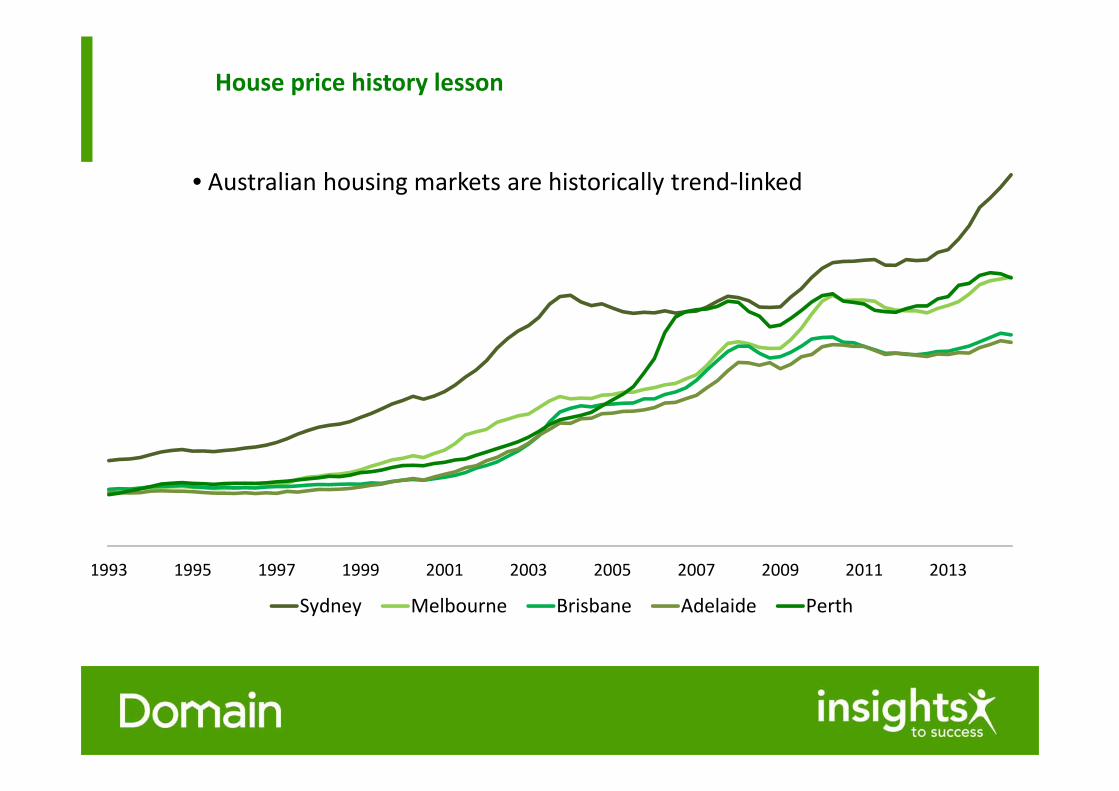

House price history lesson

• Australian housing markets are historically trend‐linked

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Sydney Melbourne Brisbane Adelaide Perth

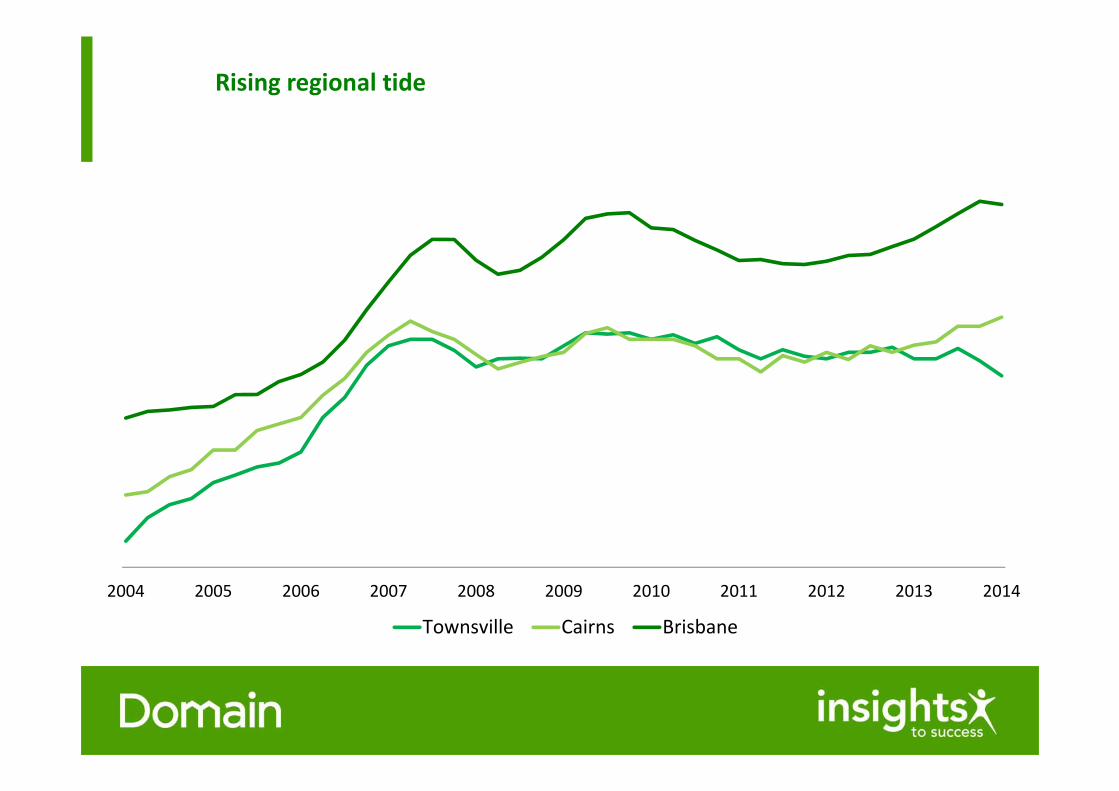

Rising regional tide

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Townsville Cairns Brisbane

A rising tide lifts all boats ‐ in time (JF Kennedy, AJ Wilson)

Economies Employment Incomes Population growth Prosperity Confidence House prices

Monolithic Australian economy and housing market

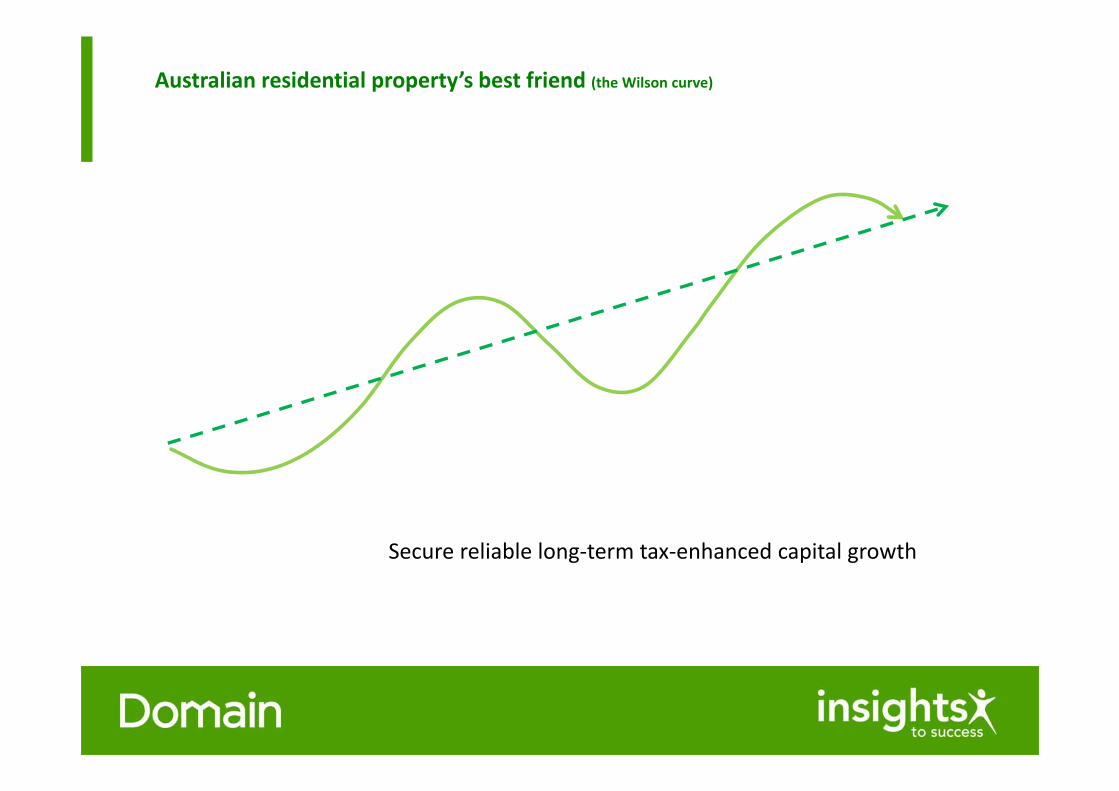

Australian residential property’s best friend (the Wilson curve)

Secure reliable long‐term tax‐enhanced capital growth

If you require any further information regarding Australian property market analysis I may be contacted by email at [email protected] or phone 0427 410 240

For all the real-time housing market insights follow me on twitter at @DocAndrewWilson

Listen to me on Radio 2UE Saturdays 12.30 to 1pm

Australian property market analysis

Thank you