audit highlights dec 2021 exams

TRANSCRIPT

CA Final – Audit Highlights for Dec 2021 Exams 1

Audit Highlights Dec 2021

Exams

CA Final – Audit Highlights for Dec 2021 Exams 2

COMPANY AUDIT Resignation of Auditor Sec 140(2)

➔ The auditor who has resigned from the company shall file within a period of 30 days from the date of resignation, a statement in the prescribed form with the company & the Registrar, & in case of companies referred to in sec 139(5), the auditor shall also file such statement with the Comptroller & Auditor General of India, indicating the reasons & other facts as may be relevant with regard to his resignation. ➔ If the auditor does not comply with the provisions of sub-section (2), he or it shall be liable to a penalty of Rs. 50,000 or an amount equal to the remuneration of the auditor, whichever is less, & in case of continuing failure, with further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 2 lakhs.

Sec 143 (3) The auditor’s report shall also state—

(j) such other matters as may be prescribed. The auditor’s report shall also include their views & comments on the following matters, namely:- (a) whether the company has disclosed the impact, if any, of pending litigations on its financial position in its financial statement; (b) whether the company has made provision, as required under any law or accounting standards, for material foreseeable losses, if any, on long term contracts including derivative contracts; (c) whether there has been any delay in transferring amounts, required to be transferred, to the Investor Education & Protection Fund by the company. (d) [Omitted] (e) (i) Whether the management has represented that, to the best of it’s knowledge & belief, other than as disclosed in the notes to the accounts, no funds have been advanced or loaned or invested (either from borrowed funds or share premium or any other sources or kind of funds) by the company to or in any other person(s) or entity(ies), including foreign entities (“Intermediaries”), with the understanding, whether recorded in writing or otherwise, that the Intermediary shall, whether, directly or indirectly lend or invest in other persons or entities

CA Final – Audit Highlights for Dec 2021 Exams 3

identified in any manner whatsoever by or on behalf of the company (“Ultimate Beneficiaries”) or provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries; (ii) Whether the management has represented, that, to the best of it’s knowledge & belief, other than as disclosed in the notes to the accounts, no funds have been received by the company from any person(s) or entity(ies), including foreign entities (“Funding Parties”), with the understanding, whether recorded in writing or otherwise, that the company shall, whether, directly or indirectly, lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the Funding Party (“Ultimate Beneficiaries”) or provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries; & (iii) Based on such audit procedures that the auditor has considered reasonable & appropriate in the circumstances, nothing has come to their notice that has caused them to believe that the representations under sub-clause (i) & (ii) contain any material misstatement. (f) Whether the dividend declared or paid during the year by the company is in compliance with sec 123 of the Companies Act, 2013. (g) [Whether the company, in respect of financial years commencing on or after the 1st April, 2022,] has used such accounting software for maintaining its books of account which has a feature of recording audit trail (edit log) facility & the same has been operated throughout the year for all transactions recorded in the software & the audit trail feature has not been tampered with & the audit trail has been preserved by the company as per the statutory requirements for record retention.]

Duty to Report Fraud to Central Government Sec 143(12)

Sec 143(15) If any auditor, cost accountant, or company secretary in practice does not comply with the provisions of Sec 143(12), he shall,— (a) in case of a listed company, be liable to a penalty of Rs. 5 lakhs; & (b) in case of any other company, be liable to a penalty of Rs. 1 lakh.

Punishment for Contravention Sec 147

(1) If any of the provisions of sec 139 to 146 (both inclusive) is contravened, the company shall be

CA Final – Audit Highlights for Dec 2021 Exams 4

punishable with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 lakhs & every officer of the company who is in default shall be punishable with fine which shall not be less than Rs. 10,000 but which may extend to Rs. 1 lakh. (2) If an auditor of a company contravenes any of the provisions of sec 139, sec 144 or sec 145, the auditor shall be punishable with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 lakhs or 4 times the remuneration of the auditor, whichever is less. ➔ Provided that if an auditor has contravened such provisions knowingly or wilfully with the intention to deceive the company or its shareholders or creditors or tax authorities, he shall be punishable with imprisonment for a term which may extend to 1 year & with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 25 lakhs or 8 times the remuneration of the auditor, whichever is less. (3) Where an auditor has been convicted under sub-section (2), he shall be liable to— (i) refund the remuneration received by him to the company; & (ii) pay for damages to the company, statutory bodies or authorities [or to members or creditors of the company] for loss arising out of incorrect or misleading statements of particulars made in his audit report. (4) The Central Government shall, by notification, specify any statutory body or authority or an officer for ensuring prompt payment of damages to the company or the persons under clause (ii) of sub-section (3) & such body, authority or officer shall after payment of damages to such company or persons file a report with the Central Government in respect of making such damages in such manner as may be specified in the said notification. (5) Where, in case of audit of a company being conducted by an audit firm, it is proved that the partner or partners of the audit firm has or have acted in a fraudulent manner or abetted or colluded in any fraud by, or in relation to or by, the company or its directors or officers, the liability, whether civil or criminal as provided in this Act or in any other law for the time being in force, for such act shall be of the partner or partners concerned of the audit firm & of the firm jointly & severally. Provided that in case of criminal liability of an audit firm, in respect of liability other than fine, the concerned partner or partners, who acted in a fraudulent manner or abetted or, as the case may be, colluded in any fraud shall only be liable.

Declaration of Dividend Sec 123

CA Final – Audit Highlights for Dec 2021 Exams 5

(1) No dividend shall be declared or paid by a company for any financial year except— (a) ➔ out of the profits of the company for that year arrived at after providing for depreciation in accordance with the provisions of sub-section (2), or ➔ out of the profits of the company for any previous financial year or years arrived at after providing for depreciation in accordance with the provisions of that sub-section & remaining undistributed, or ➔ out of both. Provided that in computing profits any amount representing unrealised gains, notional gains or revaluation of assets & any change in carrying amount of an asset or of a liability on measurement of the asset or the liability at fair value shall be excluded; or (b) out of money provided by the Central Government or a State Government for the payment of dividend by the company in pursuance of a guarantee given by that Government: ➔ Provided that a company may, before the declaration of any dividend in any financial year, transfer such percentage of its profits for that financial year as it may consider appropriate to the reserves of the company: ➔ Provided further that where, owing to inadequacy or absence of profits in any financial year, any company proposes to declare dividend out of the accumulated profits earned by it in previous years & transferred by the company to the free reserves, such declaration of dividend shall not be made except in accordance with such rules as may be prescribed in this behalf. ➔ Provided also that no dividend shall be declared or paid by a company from its reserves other than free reserves. ➔ Provided also that no company shall declare dividend unless carried over previous losses & depreciation not provided in previous year or years are set off against profit of the company for the current year. (2) For the purposes of clause (a) of sub-section (1), depreciation shall be provided in accordance with the provisions of Schedule II. (3) The Board of Directors of a company may declare interim dividend during any financial year or at any time during the period from closure of financial year till holding of the annual general meeting out of the surplus in the profit & loss account or out of profits of the financial year for which such interim dividend is sought to be declared or out of profits generated in the financial year till the quarter preceding the date of declaration of the interim dividend. ➔ Provided that in case the company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim

CA Final – Audit Highlights for Dec 2021 Exams 6

dividend shall not be declared at a rate higher than the average dividends declared by the company during the immediately preceding three financial years. (4) The amount of the dividend, including interim dividend, shall be deposited in a scheduled bank in a separate account within 5 days from the date of declaration of such dividend. (5) No dividend shall be paid by a company in respect of any share therein except to the registered shareholder of such share or to his order or to his banker & shall not be payable except in cash: ➔ Provided that nothing in this sub-section shall be deemed to prohibit the capitalisation of profits or reserves of a company for the purpose of issuing fully paid-up bonus shares or paying up any amount for the time being unpaid on any shares held by the members of the company: ➔ Provided further that any dividend payable in cash may be paid by cheque or warrant or in any electronic mode to the shareholder entitled to the payment of the dividend. (6) A company which fails to comply with the provisions of sec 73 & 74 shall not, so long as such failure continues, declare any dividend on its equity shares.

Unpaid Dividend Account Sec 124

(1) Where a dividend has been declared by a company but has not been paid or claimed within 30 days from the date of the declaration to any shareholder entitled to the payment of the dividend, the company shall, within 7 days from the date of expiry of the said period of 30 days, transfer the total amount of dividend which remains unpaid or unclaimed to a special account to be opened by the company in that behalf in any scheduled bank to be called the Unpaid Dividend Account. (2) The company shall, within a period of 90 days of making any transfer of an amount to the Unpaid Dividend Account, prepare a statement containing the names, their last known addresses & the unpaid dividend to be paid to each person & place it on the website of the company, if any, & also on any other website approved by the Central Government for this purpose, in such form, manner & other particulars as may be prescribed. (3) If any default is made in transferring the total amount to the Unpaid Dividend Account of the company, it shall pay, from the date of such default, interest on so much of the amount as has not been transferred to the said account, at the rate of 12% per annum & the interest accruing on such amount shall ensure to the benefit of the members of the company in proportion to the amount remaining unpaid to them. (4) Any person claiming to be entitled to any money transferred to the Unpaid Dividend Account of the company may apply to the company for payment of the money claimed.

CA Final – Audit Highlights for Dec 2021 Exams 7

(5) Any money transferred to the Unpaid Dividend Account of a company in pursuance of this section which remains unpaid or unclaimed for a period of 7 years from the date of such transfer shall be transferred by the company along with interest accrued, if any, thereon to the Fund established u/s 125(1) & the company shall send a statement in the prescribed form of the details of such transfer to the authority which administers the said Fund & that authority shall issue a receipt to the company as evidence of such transfer. (6) All shares in respect of which dividend has not been paid or claimed for 7 consecutive years or more shall be transferred by the company in the name of Investor Education & Protection Fund along with a statement containing such details as may be prescribed. ➔ Provided that any claimant of shares transferred above shall be entitled to claim the transfer of shares from Investor Education & Protection Fund in accordance with such procedure & on submission of such documents as may be prescribed. ➔ For the removal of doubts, it is hereby clarified that in case any dividend is paid or claimed for any year during the said period of 7 consecutive years, the share shall not be transferred to Investor Education & Protection Fund. (7) If a company fails to comply with any of the requirements of this section, such company shall be liable to a penalty of Rs. 1 lakh & in case of continuing failure, with a further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 10 lakhs & every officer of the company who is in default shall be liable to a penalty of Rs. 25,000 & in case of continuing failure, with a further penalty of Rs. 100 for each day after the first during which such failure continues, subject to a maximum of Rs. 2 lakhs.

Punishment for Failure to Distribute Dividends Sec 127

➔ Where a dividend has been declared by a company but has not been paid or the warrant in respect thereof has not been posted within 30 days from the date of declaration to any shareholder entitled to the payment of the dividend, every director of the company shall, if he is knowingly a party to the default, be punishable with imprisonment which may extend to two years & with fine which shall not be less than Rs. 1000 for every day during which such default continues & the company shall be liable to pay simple interest at the rate of 18% per annum during the period for which such default continues:

CA Final – Audit Highlights for Dec 2021 Exams 8

➔ Provided that no offence under this sec shall be deemed to have been committed:— (a) where the dividend could not be paid by reason of the operation of any law;

(b) where a shareholder has given directions to the company regarding the payment of the dividend & those directions cannot be complied with & the same has been communicated to him; (c) where there is a dispute regarding the right to receive the dividend; (d) where the dividend has been lawfully adjusted by the company against any sum due to it from the shareholder; or (e) where, for any other reason, the failure to pay the dividend or to post the warrant within the period under this section was not due to any default on the part of the company.

CA Final – Audit Highlights for Dec 2021 Exams 9

AUDIT OF BANKS

The Ministry of Corporate Affairs has further to amended the Companies (Audit & Auditors) Rules, 2014, through the Companies (Audit & Auditors) Amendment Rules, 2021 vide notification S.O. 206(E) dated 24th March, 2021. As per reporting requirements cast through Rule 11 of the Companies (Audit & Auditors) Rules, 2014 the auditor’s report shall also include their views & comments on the following matters, namely: (1) whether the bank has disclosed the impact, if any, of pending litigations on its financial position in its financial statement; (2) whether the bank has made provision, as required under any law or accounting standards, for material foreseeable losses, if any, on long term contracts including derivative contracts; (3) whether there has been any delay in transferring amounts, required to be transferred, to the Investor Education & Protection Fund by the bank. (4) (i) Whether the management has represented that, to the best of it’s knowledge & belief, other than as disclosed in the notes to the accounts, no funds have been advanced or loaned or invested (either from borrowed funds or share premium or any other sources or kind of funds) by the banks to or in any other person(s) or entity(ies), including foreign entities (“Intermediaries”), with the understanding, whether recorded in writing or otherwise, that the Intermediary shall, whether, directly or indirectly lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the bank (“Ultimate Beneficiaries”) or provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries; (ii) Whether the management has represented, that, to the best of it’s knowledge & belief, other than as disclosed in the notes to the accounts, no funds have been received by the bank from any person(s) or entity(ies), including foreign entities (“Funding Parties”), with the understanding, whether recorded in writing or otherwise, that the bank shall, whether, directly or indirectly, lend or invest in other persons or entities identified in any manner whatsoever by or on behalf of the Funding Party (“Ultimate Beneficiaries”) or provide any guarantee, security or the like on behalf of the Ultimate Beneficiaries; & (iii) Based on such audit procedures that the auditor has considered reasonable & appropriate in the circumstances, nothing has come to their notice that has caused them to believe that the

CA Final – Audit Highlights for Dec 2021 Exams 10

representations under sub-clause (i) & (ii) contain any material misstatement. (5) Whether the dividend declared or paid during the year by the bank is in compliance with sec 123 of the Companies Act, 2013. (6) Whether the bank, in respect of financial years commencing on or after the 1st April, 2022, has used such accounting software for maintaining its books of account which has a feature of recording audit trail (edit log) facility & the same has been operated throughout the year for all transactions recorded in the software & the audit trail feature has not been tampered with & the audit trail has been preserved by the company as per the statutory requirements for record retention.]

CA Final – Audit Highlights for Dec 2021 Exams 11

AUDIT UNDER FISCAL LAWS Tax Audit

44AB Applicability of Tax Audit

Threshold limit AY-2020-21: For a person carrying on business, has been increased from ` 1 crore to ` 5 crores. Threshold limit AY-2021-22: - For a person carrying on business, has been increased from ` 1 crore to ` 10 crores. ➔ The threshold limit, for a person carrying on business, is increased from Rs. 1 Crore to Rs. 5 crores (A.Y. 2020-21)/ Rs. 10 crores (A.Y. 2021-22) in case when cash receipt & payment made during the year does not exceed 5% of total receipt or payment, as the case may be. In other words, more than 95% of the business transactions should be done through banking channels.

➔ In other words, the above limits would be applicable only when cash receipts & payments made during the year does not exceed 5% of total receipt or payment, as the case may be. In other words, 95% or more of the business transactions should be done through banking channels. ➔ Provided further that for the purposes of this clause, the payment or receipt, as the case may be, by a cheque drawn on a bank or by a bank draft, which is not account payee, shall be deemed to be the payment or receipt, as the case may be, in cash.

Revision of Tax Audit Report

Revision of Tax Audit Report [Notification No.28/2021 dated 1.4.2021]

➔ Sec 44AB lays obligation on certain persons mentioned thereunder carrying on business or profession, to get their accounts audited before the “specified date” by a Chartered Accountant, if their turnover exceeds the stipulated threshold or in cases where they are eligible to declare income on presumptive basis, if they claim that their income is lower than the income so computed. These persons have to furnish by the specified date, a report of the audit in the prescribed form. For this purpose, the CBDT has prescribed under Rule 6G, Forms 3CA/ 3CB & Form 3CD. ➔ The CBDT has, vide this notification, amended Rule 6G to provide that the audit report furnished may be revised by the person by getting revised report of audit from a Chartered Accountant, duly

CA Final – Audit Highlights for Dec 2021 Exams 12

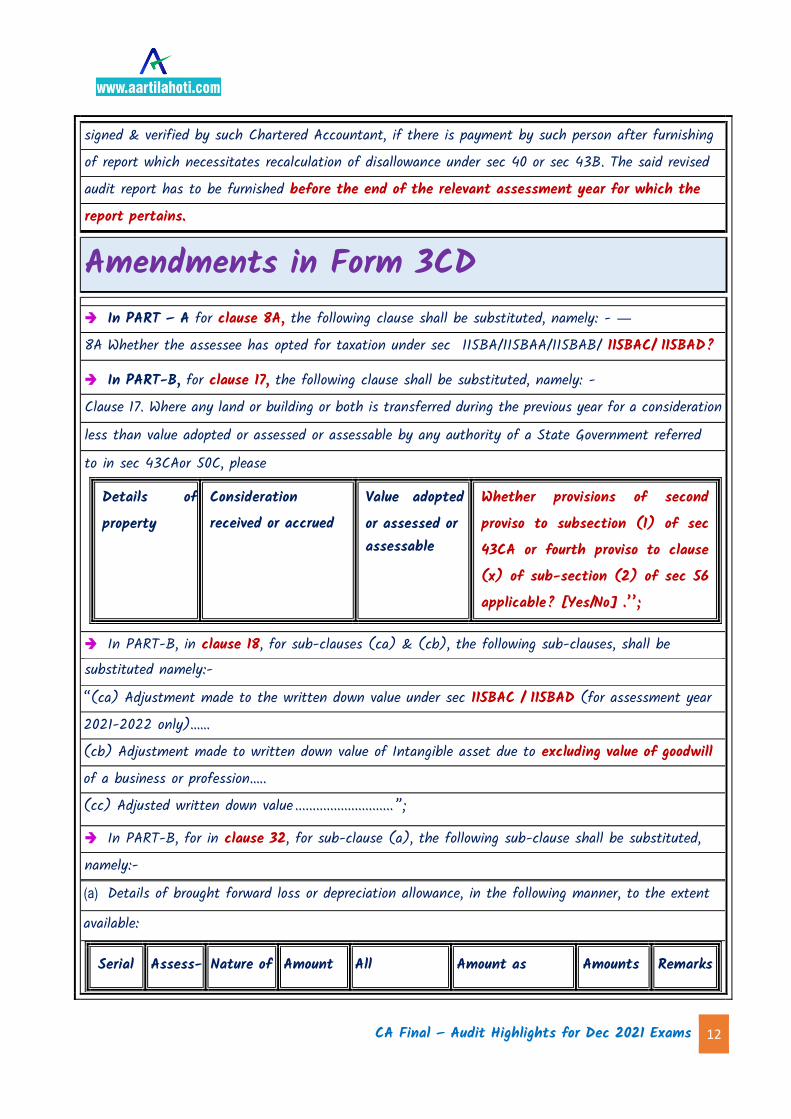

signed & verified by such Chartered Accountant, if there is payment by such person after furnishing of report which necessitates recalculation of disallowance under sec 40 or sec 43B. The said revised audit report has to be furnished before the end of the relevant assessment year for which the report pertains.

Amendments in Form 3CD

➔ In PART – A for clause 8A, the following clause shall be substituted, namely: - ― 8A Whether the assessee has opted for taxation under sec 115BA/115BAA/115BAB/ 115BAC/ 115BAD?

➔ In PART-B, for clause 17, the following clause shall be substituted, namely: - Clause 17. Where any land or building or both is transferred during the previous year for a consideration less than value adopted or assessed or assessable by any authority of a State Government referred to in sec 43CAor 50C, please

Details of property

Consideration received or accrued

Value adopted or assessed or assessable

Whether provisions of second proviso to subsection (1) of sec 43CA or fourth proviso to clause (x) of sub-section (2) of sec 56 applicable? [Yes/No] .’’;

➔ In PART-B, in clause 18, for sub-clauses (ca) & (cb), the following sub-clauses, shall be substituted namely:- “(ca) Adjustment made to the written down value under sec 115BAC / 115BAD (for assessment year 2021-2022 only)…… (cb) Adjustment made to written down value of Intangible asset due to excluding value of goodwill of a business or profession….. (cc) Adjusted written down value ............................ ”;

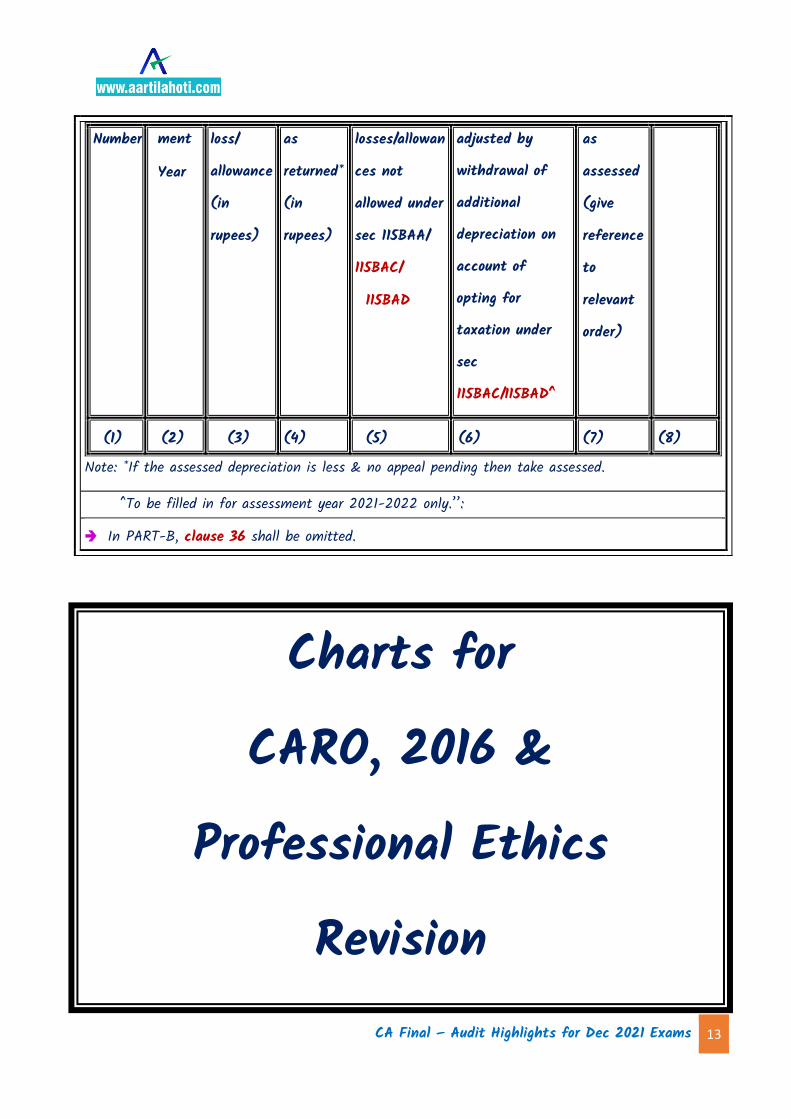

➔ In PART-B, for in clause 32, for sub-clause (a), the following sub-clause shall be substituted, namely:- (a) Details of brought forward loss or depreciation allowance, in the following manner, to the extent

available:

Serial Assess- Nature of Amount All Amount as Amounts Remarks

CA Final – Audit Highlights for Dec 2021 Exams 13

Number ment

Year

loss/

allowance

(in

rupees)

as

returned*

(in

rupees)

losses/allowan

ces not

allowed under

sec 115BAA/

115BAC/

115BAD

adjusted by

withdrawal of

additional

depreciation on

account of

opting for

taxation under

sec

115BAC/115BAD^

as

assessed

(give

reference

to

relevant

order)

(1) (2) (3) (4) (5) (6) (7) (8) Note: *If the assessed depreciation is less & no appeal pending then take assessed.

^To be filled in for assessment year 2021-2022 only.’’:

➔ In PART-B, clause 36 shall be omitted.

Charts for CARO, 2016 &

Professional Ethics Revision

CA Final – Audit Highlights for Dec 2021 Exams 14

CA Final – Audit Highlights for Dec 2021 Exams 15

CA Final – Audit Highlights for Dec 2021 Exams 16