“the world will soon wake up to the reality that everyone ... · rently playing out a real-life...

TRANSCRIPT

THINGS THAT MAKE YOU GOHmmm…A walk around the fringes of finance

12 May 2011 1

“The world will soon wake up to the reality that everyone is broke and can collect nothing from the bankrupt, who are owed unlimited amounts by the insolvent, who are attempting to make late payments on a bank holiday in the wrong country, with an unacceptable currency, against defaulted collateral, of which nobody is sure who holds title.””– ANONYMOUS (VIA GOLDEN TRUTH)

“...there are three kinds of politicians: those who do not lie full stop, those who lie if they absolutely have to, and those who do not give a bugger about lying”– John Humphrys

“Falsus in uno, falsus in omnibu”– He who lies once is not to be believed twice

2.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 2

BLACK KNIGHT: ‘Tis but a scratch.

ARTHUR: A scratch? Your arm’s off!

BLACK KNIGHT: No, it isn’t.

ARTHUR: Well, what’s that, then?

BLACK KNIGHT: I’ve had worse.

ARTHUR: You liar!

On May 10th, 1974, one of my favourite movies of all time was released. I was 7 years old when Monty Python and The Holy Grail was released, but had to wait until the ad-vent of the video recorder (for those of you under the age of about 30 – Google it) a few years later to see it for the first time. I then spent an entire summer watching it virtually every day with my mates – laughing harder each time and repeating the lines amongst ourselves until they were burned into our pre-pubescent brains.

To this day, I can still recite (almost) verbatim large swathes of dialogue from the movie and, having introduced my own daughters to the mov-ie a couple of years back, I discovered it still makes me laugh.

Sadly, it seems to have lost something in translation as my girls seemed far more amused (or rather bemused) at my laughter than any Pythonesque tomfoolery happening on screen. Must be a generational thing.

Anyway, as I replay the movie in my head for the umpteenth time, it occurs to me that we are cur-rently playing out a real-life version of the movie’s most iconic scene – King Arthur’s duel with the Black Knight.

The Black Knight (played by John Cleese) is described thus by Wikipedia:

As his name suggests, he is a black knight who guards a “bridge” (in reality a short plank of wood) over a small stream, for unknown reasons. Although supremely skilled in swordplay, he suffers from unchecked overconfidence and a staunch refusal ever to give up.

Interestingly enough, in the audio commentary on the DVD, Cleese recounts how the origin of this particular scene was a story told to him in an English class. Wikipedia again:

Two Roman wrestlers were engaged in a particularly intense match and had been fighting for such a substantial length of time that the match had degraded to the two combatants doing little more than leaning into one another with their body weight. When one wrestler finally tapped-out and pulled away from his opponent, it was only then that he and the crowd realised the other man was, in fact, dead and had effectively won the match posthumously. The moral of the tale, accord-ing to Cleese’s teacher, was “if you never give up, you can’t possibly lose”

One can’t help but assume that the guardians of the Eurozone have been watching Monty Python and the Holy Grail with the same frequency as I did all those years ago and have now decided that the Black Knight defence is, in fact their best way forward.

3.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 3

As the weeks pass by and we enter the Summer doldrums, when both the ambient and collective public temperatures begin to soar across Southern Europe, it is becoming ever more apparent that the Eurozone’s problems, far from receeding, are becoming incrementally worse.

Currently Greece is back in the firing line this past week and, after the short-lived euphoria of the capture of OUsama Bin Laden had dissipated, focus returned to the woes of Europe’s periphery.

ARTHUR: Eh.Youareindeedbrave,SirKnight,butthefightismine.

BLACK KNIGHT: Oh, had enough, eh?

ARTHUR: Look, you stupid bastard. You’ve got no arms left.

BLACK KNIGHT: Yes, I have.

ARTHUR: Look!

BLACK KNIGHT: Justafleshwound

There were some truly staggering headlines this past week (even by the standards of recent years – which is saying something), as first Greece then Portugal decided to bring the crazy once the ratings agencies finally decided they ought to do their job:

• PORTUGAL OPENS CRIMINAL INQUIRY INTO RATING AGENCIES

• GREEK FINANCE MINISTRY SAYS S&P CREDIBILITY IN QUESTION

• GREECE SAYS S&P MOVE ISN’T JUSTIFIED

But today we’re not all about the crazy - we’re about the hazy.

After Last Friday’s Der Spiegel article suggested secret talks were going on behind the scenes that may culminate in Greece’s unceremonious departure from the EU, the pace of the game accelerated noticeably.

First, secret talks were denied. Next, they were acknowledged - but the public were told they were NOT secret. Then the content of those talks was disputed. It was impossible to get a straight answer from anybody about the secret talks – but should that really surprise us?

The Associated Press printed an article earlier this week that is destined to go down in the annals of history. Here is the first pertinent extract:

On March 29, when speculation swirled that Portugal needed a bailout, Prime Minister Jose Socrates denied — again — that that would happen despite clearly unsustainable market pres-sures.

“I’m sick of saying we won’t” be requesting help, he told journalists.

Just eight days later, in a chastened appearance on national television, Socrates did just that.

An unusual about-turn? Hardly. Let’s take a little trip back in time, shall we?

Greek PM George Papandreou, Feb 26, 2010:

4.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 4

“No other country will pay for our debts,” he said. “It is a matter of honour and pride for our coun-try to put our own house in order.”

BBC News, May 2, 2010 - nine weeks later

Eurozone members and the IMF have agreed a 110bn-euro (£95bn; $146.2bn) three-year bail-out package to rescue Greece’s embattled economy.

In return for the loans, Greece will make major austerity cuts which Prime Minister George Papan-dreou said involved “great sacrifices”.

The EU will provide 80bn euros in funding and the rest will come from the International Monetary Fund (IMF).

The deal is designed to prevent Greece from defaulting on its massive debt.

Ah those crazy Greeks. Of COURSE you can expect this sort of thing from THEM, right? That wouldn’t fly in Northern Europe though. Would it?:

Irish Times, October 11, 2010:

Minister for Finance Brian Lenihan said today he is “absolutely” sure the country will not need to seek a bailout from the IMF and European Union…

Twenty-nine days later, Lenihan made the ballsy decision to allow himself to be questioned by British Bulldog interviewer Jer-emy Paxman on November 9th, 2010 (click on the picture of Paxman, right to watch a REAL interview):

A month later, PM Brian Cowen joined the party:

Irish Central, November 16, 2010:

Ireland will not be requesting funding for the state from the European Union or the Inter-national Monetary Fund according to Brian Cowen. Speaking last night, the Irish Prime Minister insisted that a funding application will not be made at today’s meetings in Brussels, as the country is funded up until the middle of next year.

Five days later – FIVE. DAYS. LATER. – on November 21, 2010, the following story appeared on the BBC News website:

The Republic of Ireland will make a formal request for international aid to shore up its finances later on Sunday.

Finance minister Brian Lenihan put no figure on how much may be borrowed, but told RTE radio it would be “tens of billions” of euros.

One week later still, on November 28, 2010, the Washington Post had this to say:

Ireland on Sunday reached agreement with the International Monetary Fund and the European Union for an emergency bailout package worth $90 billion, a rescue meant to both shore up that nation’s buckling banks and confront investor fears that Dublin’s problems are spreading to other European nations.

5.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 5

That’s a mere TWELVE DAYS between “definitely not” and “how much have you got?”

Shall we do the same with Portugal? No? Well, you get the idea.

The entire Eurozone bailout fiasco has been one long attempt to reassure, jawbone and cajole mar-kets in the hope that those asking the questions will just go away while things somehow get better on their own. Really? Does anybody (elected representatives of the PIIGS and all European Central Bankers notwithstanding) HONESTLY think that will work? I guess the evidence would suggest that clearly some people do (elected representatives of the PIIGS and all European Central Bankers most definitely WITHstanding).

Remarkably though, throughout the oscillations in the Eurozone, the single currency has somehow managed to float ever higher versus its transatlantic cousin. I’m not sure EXACTLY what that says about the dollar, or about the general acceptance of the assertions of Timothy Geithner, Ben Ber-nanke and Barack Obama that they are pursuing a ‘Strong Dollar Policy’, but one thing is for certain: it is truly remarkable that the dollar can’t even catch a break against a monetary clown car that is bar-reling around the ring as pieces fly off in every direction.

This week, the lies continued as new Irish PM Endra Kenny spoke to the Council on Foreign Relations in New York:

Bloomberg: Irish Prime Minister Enda Kenny said the nation can handle its debts, signaling the government has no plan to restructure its borrowings.

Ireland’s debt will peak at 116 percent of gross domestic product in 2014, according to govern-ment forecasts published on April 29. The figure was 25 percent at the end of 2007.

“I think we can deal with it,” Kenny said at the Council on Foreign Relations in New York today. “The scale of the challenge is enormous but so is the opportunity.”

Four days later?:

Reuters: Ireland warned on Monday it would need more favorable terms to rid itself of its debt troubles and said it was confident of securing a cut in the interest it pays for its EU aid without conceding ground on tax rates…”We carry a heavy burden of debt. Without strong growth, ques-tions of sustainability will remain,” Prime Minister Enda Kenny told a special meeting of Ireland’s parliament in celebration of Europe Day.

“There is no doubt that a reduction in the interest rate on the moneys we are borrowing from Eu-rope would be a meaningful and appreciated measure.”

The only area in which progress appears to be being made is in the compression of the timeline between the initial lies reassurances of elected officials and complete and seemingly cathartic ca-pitulation. Don’t these buffoons KNOW about the internet? Have they no grasp of the concept that EVERYTHING they say can be found in seconds? And believe me, if a muppet like ME sitting in front of a Mac in Singapore can find it, ANYBODY can.

But for the piece de resistance, we circle back to the AP article referenced earlier to hear the words of a few well-respected public officials at the top of the EU food chain:

Debt restructuring “is not part of our strategy and will not be,” the EU’s Monetary and Economic Affairs Commissioner Olli Rehn said Monday, echoing many of his colleagues in recent weeks…

6.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 6

Few people have had to answer more questions about the seeming contradiction of official com-ments and market swings than Amadeu Altafaj Tardio, Rehn’s spokesman, who faces off with jour-nalists at the EU’s press briefings almost on a daily basis.

“I know that every single word that I pronounce can have an impact on markets,” said Altafaj Tar-dio, a former journalist himself.

But those pressures cannot serve as an excuse to lie. “There have been so many leaks and there are so many sources of a different sort involved that there is never room for any lies,” he said of the current crisis. “You don’t survive 24 hours if you lie in this environment.”

Instead, the art of being a spokesman is to know when and how to release your information. “When I’m standing there on the podium, I’m doing political communication, I’m not an informa-tion desk,” said Altafaj Tardio. “We don’t tell all the truth all the time, but we never lie.”

But the final word has to go to Jean-Claude Juncker, Prime Minister of Luxembourg for the past 16 years and the longest standing head of government with undisputed democratic credentials in the world. He also happens to be the President of the Eurogroup – a meeting of the finance ministers of the Eurozone – which has effective political control over the Euro and all related aspects of the EU monetary union.

Juncker has,sadly, proven himself to be the ultimate oxymoron – an honest politician:

“If you are pre-indicating possible decisions, you are fueling speculation on the financial markets, throwing into misery mainly ordinary people whom we are trying to safeguard from this,”

“When it becomes serious, you have to lie,”

BLACK KNIGHT: Right. I’ll do you for that!

ARTHUR: You’ll what?

BLACK KNIGHT: Come here!

ARTHUR: What are you going to do, bleed on me?

BLACK KNIGHT: I’m invincible!

ARTHUR: You’re a looney.

BLACK KNIGHT: The Black Knight always triumphs! Have at you! Come on, then.

[whop] [ARTHUR chops the BLACK KNIGHT’s last leg off]

BLACK KNIGHT: Oh? All right, we’ll call it a draw.

In completely unrelated news, last month, as the Portuguese bailout was an-nounced, the UK Guardian ran the following story:

(April 7, 2011): Spain has insisted it will not become the next victim of the eurozone debt crisis af-ter Portugal finally bowed to widespread pressure on Wednesday night and joined Greece and Ire-

7.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 7

land in requesting a European Union bailout…Elena Salgado, the Spanish economy minister, said on Thursday morning that the risk of contagion “is absolutely ruled out... it has been some time since the markets have known that our economy is much more competitive”…Germany’s deputy finance minister, Werner Hoyer, also attempted to calm the situation by telling Reuters that there was no risk of a chain reaction spreading across the Iberian peninsula from Lisbon to Madrid.

In other unrelated news, since that article was published, Spanish retail sales have cratered (down 8.6% YoY), the Spanish economy has lost more jobs in Q1 2011 than in the whole of 2010, the unem-ployment rate has hit its highest level since 1997 and Spanish CPI has continued to accelerate.

Right then, today we take a look at what a US default might look like, William K. Black explains how CEOs have been successful at playing dodgeball, Andy Xie warns of impending stagflation and Matt Taibbi is back with perhaps his biggest swing to date at Goldman Sachs.

In precious metals we look at silver’s chances of getting to 200, find out the reasons NOT to fondle your gold, look at inflationary pressures in that most gold-friendly of countries - Vietnam - and Dan Norcini looks at the technical picture.

A Reuters investigation into crude oil’s 10% fall last week is educational, the leader of the True Finns lays out the case for a bailout boycott, the dollar is under serious threat as the world’s reserve cur-rency and we go behind the scenes at Foxconn in Taiwan to see what the Apple food chain really looks like.

Charts on the CPI and the world’s ‘best’ banks plus interviews with Ben Davies, Jim Sinclair and the great Felix Zulauf round things out for the day.

That’s all from me until the weekend. You’ve been a wonderful audience - please don’t forget to tip your waitress

8.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 8

Contents 12 May 2011

What Triggered Oil’s Greatest Rout

What A U.S. Default Might Look Like

Silver’s Destiny With 200

Reasons Not To Fondle Your Gold

Why CEOs Avoided Getting Busted In Meltdown

Rival Currencies Take Aim at Dollar’s Dominance

Chimerica’s Slippery Slope To Stagflation

Gold Traders Are Only Winners Amid 18% Inflation

Why I Don’t Support Europe’s Bailouts

The People vs. Goldman Sachs

‘We Were Not a Very Open Company Before’

Charts That Make You Go Hmmm.....

Words That Make You Go Hmmm.....

And Finally.....

9.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 9

When oil prices fell below $120 a barrel in early New York trade last Thursday, a few big companies that are major oil consumers started buying around $117.

It looked like a bargain. Brent crude had been trading above $120 for a month. But the buying proved ill-timed. Crude kept on falling.

“They were down millions by the end of the day, trying to catch a falling piano,” an executive at a major New York investment bank said.

Never before had crude oil plummeted so deeply during the course of a day. At one point, prices were off by nearly $13 a barrel, dipping below $110 a barrel for the first time since March.

Oil’s descent followed the biggest one-day price drop in silver since 1980 on Wednesday, after hedge fund titan George Soros was reported to be selling. Exchange operators raised silver’s margin re-quirements, making it more costly to trade the metal and sending investors out of the market. Silver plunged by 20 percent, more by week’s end. The rout unnerved some commodity investors.

Oil just doesn’t fall by 10 percent in the course of a normal day, though. In commodities markets, oil is king, and its daily contract turnover, typically around $200 billion, is usually able to absorb even large inflows or outflows of investment.

The rare moves of $10 a barrel usually are set off by dramatic events -- the outbreak of the first Gulf War in 1991, or the collapse in 2008 of Lehman Bros bank, which both led to recessions.

Of course, there was major news last week. But the daring Pakistan raid that killed Osama bin Laden had done little to shift the balance of oil markets on Monday.

In interviews with more than two dozen fund managers, bankers and traders, no clear cause emerged for the plunge in price. Market players were unable to identify any single bank or fund orchestrating a massive sale to liquidate positions, not even an errant trade that triggered panic selling, as seen in the equities flash crash last May.

Rather, the picture pieced together from interviews on Thursday and Friday is one of a richly priced commodities market -- raw goods have been on a five-month winning tear over all other major invest-ment classes -- hit by a flurry of negative factors that individually could be absorbed but cumulatively triggered a maelstrom.

Computerized trading kicked in when key price levels were reached, accelerating the fall.

“It was a domino effect,” said Dominic Cagliotti, a New York-based oil options broker.

The negative factors -- prominent cheerleaders turning bearish, some weak economic data, cheap money from the U.S. Federal Reserve ending by July, a lessening of political risk -- merely provide a backdrop for the waves of selling. What stands out is the way computers turned readjustment of posi-tions in a huge and deep market into a rout.

O O O REUTERS / LINK

Much has been written about the prospect of a technical default in the U.S. Treasury market, despite how unlikely that outcome really is. Any delay in making a coupon or principal pay-ment by the Treasury would almost certainly have a major impact on the financial system, including adverse long-term consequences for Treasury financing and the U.S. economy.

...Oil just doesn’t fall by 10 per-cent in the course of a normal day, though

10.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 10

A technical default would involve a missed payment as a result of failing to raise the debt limit, but the delay would likely only be a day or two in length. This scenario also assumes the market does not view the event as a serious deterioration of U.S. solvency.

One major threat would be a flight to liquidity out of money market funds as was seen during the Lehman Brothers crisis, since daily liquidity and stability are of paramount importance to these inves-tors, according to a report from J.P. Morgan analyst Terry Belton.

In the two days following the Lehman failure in 2008, the Reserve Primary fund received US$40-billion in redemption requests, despite holding less than US$1-billion, or 1.5%, of its US$62-billion in assets in Lehman debt. The fund soon ran out of cash and moved to liquidate portfolio holdings, before an-nouncing on Sept. 16 that they had broken the buck – the net asset value of the fund fell below $1 to 97¢.

The next week, prime institutional money market funds saw more than US$300-billion in redemptions as institutional investors no longer felt safe there. That number nearly hit US$500-billion before re-covering after the Treasury and Federal Reserve announced a temporary guarantee of money market funds and a liquidity facility extending credit to banks.

The repo market, home to contracts for the sale and future repurchases of financial assets such as Treasury securities, could also see a sharp spike in haircuts, which could lead to significant margin calls. This would cause deleveraging in lending markets and lenders demand high collateral require-ments, Mr. Belton said.

JPMorgan estimates that more than US$4-trillion in treasuries – nearly half of the outstanding stock – is used as collateral for repo agreements, futures, clearing houses and over-the-counter derivatives.

O O O FINANCIAL POST / LINK

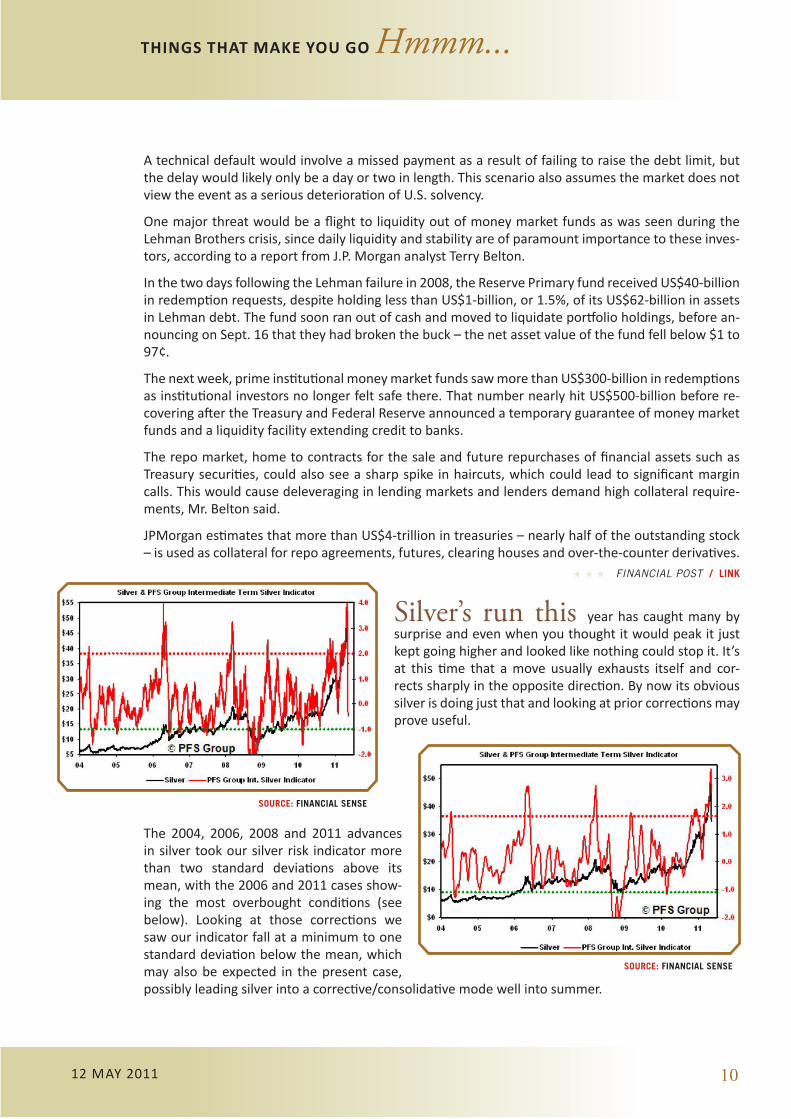

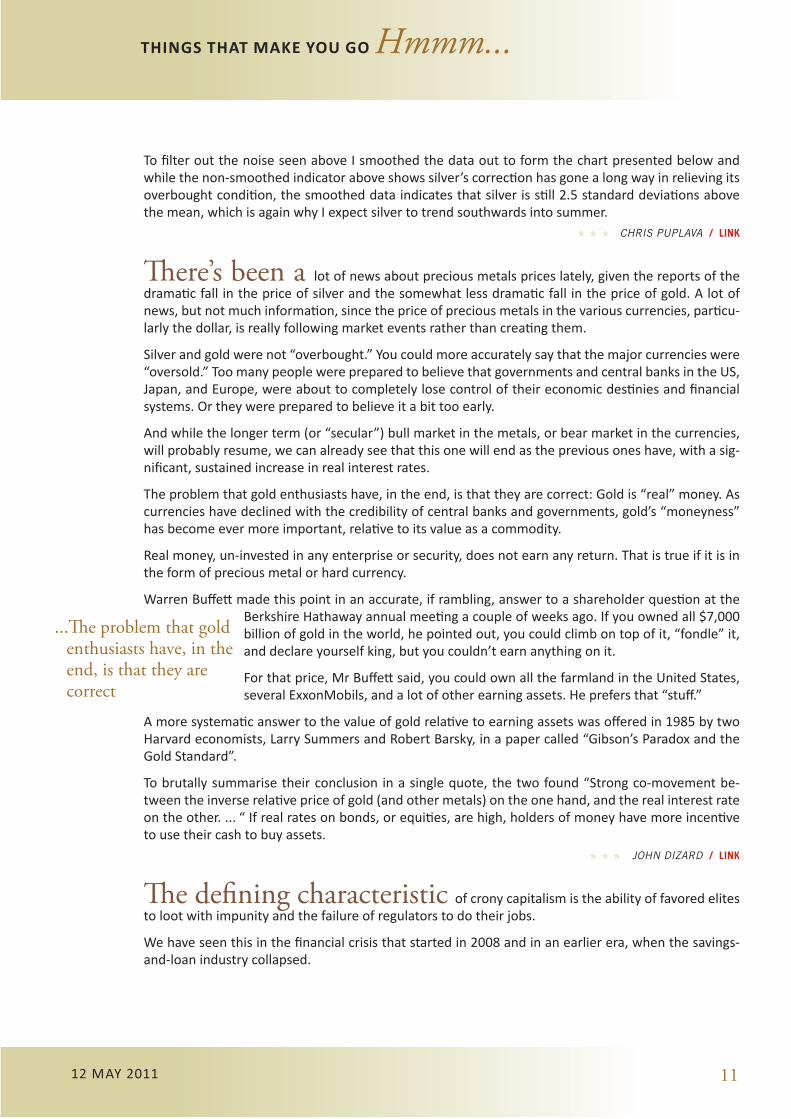

Silver’s run this year has caught many by surprise and even when you thought it would peak it just kept going higher and looked like nothing could stop it. It’s at this time that a move usually exhausts itself and cor-rects sharply in the opposite direction. By now its obvious silver is doing just that and looking at prior corrections may prove useful.

The 2004, 2006, 2008 and 2011 advances in silver took our silver risk indicator more than two standard deviations above its mean, with the 2006 and 2011 cases show-ing the most overbought conditions (see below). Looking at those corrections we saw our indicator fall at a minimum to one standard deviation below the mean, which may also be expected in the present case, possibly leading silver into a corrective/consolidative mode well into summer.

SOURCE: FINANCIAL SENSE

SOURCE: FINANCIAL SENSE

11.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 11

To filter out the noise seen above I smoothed the data out to form the chart presented below and while the non-smoothed indicator above shows silver’s correction has gone a long way in relieving its overbought condition, the smoothed data indicates that silver is still 2.5 standard deviations above the mean, which is again why I expect silver to trend southwards into summer.

O O O CHRIS PUPLAVA / LINK

There’s been a lot of news about precious metals prices lately, given the reports of the dramatic fall in the price of silver and the somewhat less dramatic fall in the price of gold. A lot of news, but not much information, since the price of precious metals in the various currencies, particu-larly the dollar, is really following market events rather than creating them.

Silver and gold were not “overbought.” You could more accurately say that the major currencies were “oversold.” Too many people were prepared to believe that governments and central banks in the US, Japan, and Europe, were about to completely lose control of their economic destinies and financial systems. Or they were prepared to believe it a bit too early.

And while the longer term (or “secular”) bull market in the metals, or bear market in the currencies, will probably resume, we can already see that this one will end as the previous ones have, with a sig-nificant, sustained increase in real interest rates.

The problem that gold enthusiasts have, in the end, is that they are correct: Gold is “real” money. As currencies have declined with the credibility of central banks and governments, gold’s “moneyness” has become ever more important, relative to its value as a commodity.

Real money, un-invested in any enterprise or security, does not earn any return. That is true if it is in the form of precious metal or hard currency.

Warren Buffett made this point in an accurate, if rambling, answer to a shareholder question at the Berkshire Hathaway annual meeting a couple of weeks ago. If you owned all $7,000 billion of gold in the world, he pointed out, you could climb on top of it, “fondle” it, and declare yourself king, but you couldn’t earn anything on it.

For that price, Mr Buffett said, you could own all the farmland in the United States, several ExxonMobils, and a lot of other earning assets. He prefers that “stuff.”

A more systematic answer to the value of gold relative to earning assets was offered in 1985 by two Harvard economists, Larry Summers and Robert Barsky, in a paper called “Gibson’s Paradox and the Gold Standard”.

To brutally summarise their conclusion in a single quote, the two found “Strong co-movement be-tween the inverse relative price of gold (and other metals) on the one hand, and the real interest rate on the other. ... “ If real rates on bonds, or equities, are high, holders of money have more incentive to use their cash to buy assets.

O O O JOHN DIZARD / LINK

The defining characteristic of crony capitalism is the ability of favored elites to loot with impunity and the failure of regulators to do their jobs.

We have seen this in the financial crisis that started in 2008 and in an earlier era, when the savings-and-loan industry collapsed.

CLICK TO ENLARGE

...The problem that gold enthusiasts have, in the end, is that they are correct

12.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 12

In the Texas “Rent-a-Bank” scandal of the 1970s, for example, two ringleaders created a fraud network of 50 lenders that caused billions of dollars in losses. The watchdogs removed and sanctioned one of the main culprits, but because the crimes weren’t prosecuted, the same crooks reappeared in the 1980s to do it all over again, only on a bigger scale. Unless you imprison the fraudsters, sophisticated financial scams grow ever more destructive.

It seems as if we have forgotten this lesson.

Take the seven senior officials convicted in the failure of one of the lenders that drove the 2008 credit crunch. All of the cases arose from an investigation of Taylor Bean & Whitaker Mortgage Corp. The first trial occurred last month -- 6 1/2 years after the Federal Bureau of Investigation warned publicly that there was an “epidemic” of mortgage fraud and predicted that it would cause a financial crisis if it weren’t contained. The trial and conviction of Taylor Bean’s former chairman, Lee Farkas, occurred nine years after his crimes were suspected.

Taylor Bean was a small Florida mortgage broker before the fraud began as the housing boom took off. Fannie Mae had cited Farkas for multiple violations, but never filed a criminal referral, which would have triggered an investigation. Had it done so, Farkas might have been prosecuted and Taylor Bean shut long before it caused so much damage. Instead, it expanded, then failed, pulling down a bank with it at a cost of $2.8 billion to the Federal Deposit Insurance Corp. Farkas plans to appeal the verdict.

O O O WILLIAM K BLACK / LINK

The historical first simply couldn’t end without the usual mantra. At the first-ever press conference in the 98-year history of the US Federal Reserve, Fed Chairman Ben Bernanke an-nounced last Wednesday what everyone was expecting, and wanting, to hear. Flanked by the Stars and Stripes as well as the flag of the US central bank, he said: “The Fed believes that a strong dollar is both in American interests and in the interest of the global economy.”

Bernanke has often made similar pronouncements -- as has US Treasury Secretary Timothy Geithner. Invoking the dollar’s strength was also part of their predecessors’ stan-dard repertoire.

This familiar litany is actually a worrying sign, however. The statement is always made when things are not look-ing good for the dollar. In one sense, currencies are just like people: Anyone who is genuinely strong doesn’t feel the need to emphasize that fact over and over.

In reality, the US currency is currently plagued by an acute bout of weakness. Its exchange rate has stabilized at around $1.50 to the euro, which is not far from the low point that it reached before the outbreak of the financial crisis. Since the beginning of the year, the dollar has lost 13 percent against the euro.

The decline in the value of the dollar on the currency markets, however, is merely an indication of a profound global development. The dollar is in danger of losing its

CLICK TO ENLARGE SOURCE: DER SPIEGEL

13.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 13

role as the global reserve currency and the world’s benchmark unit for exports.

Not only is the euro gaining in importance -- despite the debt crises in Greece, Portugal and Ireland -- but the currencies of emerging nations like China, India and Brazil will likely play a larger role in the near future, both in global trade and in the investment practices of central banks. The dollar no longer has a monopoly, according to US economist Barry Eichengreen, a professor at the University of California, Berkeley.

There are many reasons, both short-term and long-term, for the decline of the greenback, a currency once coveted around the world. The fiscal policies of US President Barack Obama and his predeces-sors cast doubt over whether the US will ever be able to repay its debts. The rating agency Standard & Poor’s has already threatened to downgrade the credit rating of the only remaining superpower.

To make matters worse, the low interest rate policy pursued by Bernanke’s Fed will further erode the value of the dollar. The central bank is printing money virtually without limit to finance the US federal budget. That’s a guarantee for higher inflation.

O O O DER SPIEGEL / LINK

The global economy is heading toward another double-dip scare, possibly in the third quarter, in what could be a repeat of summer 2010.

Financial markets may stumble in a few months, and that could prompt the U.S. Federal Reserve to introduce a third round of quantitative easing or an equivalent, which would be another step down the path toward stagflation. In this scenario, China’s current monetary tightening policy would be dif-ficult to sustain.

A decline for the U.S. property market is accelerating. It could fall another 20 percent over the next 12 months.

China’s economy could slow substantially in the second half due to liquidity constraints for the prop-erty industry and local government financing.

These factors contributing to a double-dip scare may push the U.S. Federal Reserve to launch another round of stimulus, although it may not be called QE 3. At the same time, the scare may cause oil prices to dip, easing infla-tion concerns.

The main aim of a QE 3 would be the same as QE 2 – to support U.S. stock and property markets. While it may succeed in reviving these asset markets, it would also yield surg-ing oil prices and inflation.

A real double dip would occur if either the U.S. Treasury bond market crashes or appreciation expecta-tions for China’s currency reverse on expectations of depreciation. The timing for this scenario could be fourth quarter 2012, possibly after the U.S. presidential election and Chinese Communist Party’s 18th Congress.

This year’s first quarter economic data points to a continuation of last year’s trend toward stagflation. The most important data were the U.S. annualized GDP growth rate of 1.8 percent for the first three months of this year, compared to 3.1 percent in the fourth quarter 2010, and 3.8 percent inflation for personal consumption expenditures (PCE), up from 1.7 percent for the previous three months.

The Fed pays closest attention to PCE in gauging inflation. Now, while economic growth seems to be stalling, inflation is spreading unambiguously.

...A decline for the U.S. property market is accelerating. It could fall another 20 percent over the next 12 months.

14.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 14

Even Fed Chairman Ben Bernanke says the tradeoffs for monetary policy aren’t appealing, i.e., the cost of inflation from additional monetary stimulus is probably higher than job creation benefits.

Euro zone inflation continued its march upward to 2.8 percent in April, the highest since October 2008, when oil prices rose above US$ 140 a barrel. The European Union has upgraded the euro zone’s GDP growth rate to 1.6 percent for 2011. The first quarter was probably better, possibly showing a 2 percent annual rate.

O O O ANDY XIE / LINK

Nguyen Van Giau sighs audibly and shifts in his chair when I ask him the dreaded question: Is Vietnam losing its inflation battle?

It’s one the country’s central bank governor can barely go an hour without fielding these days. Such is life in a nation where consumer prices climbed almost 18 percent in April from a year earlier.

Giau’s assurances that he’s committed to taming inflation aren’t resonating with Vietnam’s 87 million people. The steady erosion of the currency has driven locals to hoard gold as the dollar grows shaky. Capital controls don’t stop households from swapping growing piles of dong for hard assets.

Vietnam’s $102 billion economy is just one example of an epic inflation fight that Asia might lose if central banks don’t act more aggressively. Rather than yanking away the proverbial punchbowl, they are keeping the monetary taps open for too long and imperiling Asia’s outlook. Asia needs less talking about these risks, and more doing.

The story last week was of Asia going on the defensive. Interest rates went up in India, Malaysia, the Philippines and Vietnam and policy makers pledged additional moves should events warrant them. Well, they do and timidity is setting Asia up for an inevitable bust after the im-pressive boom of recent years.

Part of the problem is that Asia has internalized the Federal Reserve’s core inflation philosophy. From Hanoi to Beijing, policy makers have been reluctant to tighten credit on the assumption that inflation is being unduly driven by a short- term rise in food and energy costs, while other prices are stable.

There are now indications that inflation isn’t just being imported, but increasingly generated domesti-cally. Strong domestic demand is placing increased pressure on prices that won’t go away even if food and energy inflation moderates.

That puts the onus on central banks to assume the role of party pooper. Granted, it’s an incredibly dif-ficult balancing act. Clamp down too much on credit, and officials might derail Asia’s rapid growth and rising living standards. Also, each rate increase risks courting even more hot money. It’s a supreme paradox of modern central banking: the more you act to pull liquidity out of the domestic banking system, the greater the influx of cash from overseas.

O O O WILLIAM PESEK / LINK

When I had the honor of leading the True Finn Party to electoral victory in April, we made a solemn promise to oppose the bailouts of euro-zone member states. Europe is suffering from the economic gangrene of insolvency—both public and private. Unless we amputate that which cannot be saved, we risk poisoning the whole body.

To understand the real nature and purpose of the bailouts, we first have to understand who really

...There are now indications that inflation isn’t just being imported, but increasingly generated domestically

15.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 15

benefits from them.

At the risk of being accused of populism, we’ll begin with the obvious: It is not the little guy who ben-efits. He is being milked and lied to in order to keep the insolvent system running. He is paid less and taxed more to provide the money needed to keep this Ponzi scheme going. Meanwhile, a symbiosis has developed between politicians and banks: Our political leaders borrow ever more money to pay off the banks, which return the favor by lending ever more money back to our governments.

In a true market economy, bad choices get penalized. Instead of accepting losses on unsound invest-ments—which would have led to the probable collapse of some banks—it was decided to transfer the losses to taxpayers via loans, guarantees and opaque constructs such as the European Financial Stability Fund.

The money did not go to help indebted economies. It flowed through the European Central Bank and recipient states to the coffers of big banks and investment funds.

Further contrary to the official wisdom, the recipient states did not want such “help,” not this way. The natural option for them was to admit insolvency and let failed private lenders, wherever they were based, eat their losses.

That was not to be. Ireland was forced to take the money. The same happened to Portugal.

Why did the Brussels-Frankfurt extortion racket force these countries to accept the money along with “recovery” plans that would inevitably fail? Because they needed to please the tax-guzzling banks, which might otherwise refuse to turn up at the next Spanish, Belgian, Italian or even French bond auction.

Unfortunately for this financial and political cartel, their plan isn’t working. Already under this scheme, Greece, Ireland and Portugal are ruined. They will never be able to save and grow fast enough to pay back the debts with which Brussels has saddled them in the name of saving them.

O O O TIMO SOINI / LINK

They weren’t murderers or anything; they had merely stolen more money than most people can rationally conceive of, from their own customers, in a few blinks of an eye. But then they went one step further. They came to Washington, took an oath before Congress, and lied about it.

Thanks to an extraordinary investigative effort by a Senate subcommittee that unilaterally decided to take up the burden the criminal justice system has repeatedly refused to shoulder, we now know exactly what Goldman Sachs executives like Lloyd Blankfein and Daniel Sparks lied about. We know exactly how they and other top Goldman executives, including David Viniar and Thomas Montag, defrauded their clients. America has been waiting for a case to bring against Wall Street. Here it is, and the evidence has been gift-wrapped and left at the doorstep of federal prosecutors, evidence that doesn’t leave much doubt: Goldman Sachs should stand trial.

The great and powerful Oz of Wall Street was not the only target of Wall Street and the Financial Crisis: Anatomy of a Financial Collapse, the 650-page report just released by the Senate Subcommit-tee on Investigations, chaired by Democrat Carl Levin of Michigan, alongside Republican Tom Coburn of Oklahoma. Their unusually scathing bipartisan report also includes case studies of Washington Mutual and Deutsche Bank, providing a panoramic portrait of a bubble era that produced the most

... Why did the Brussels-Frankfurt extortion racket force these countries to accept the money along with “recovery” plans that would inevitably fail?

16.THINGS THAT MAKE YOU GO Hmmm...

12 May 2011 16

destructive crime spree in our history — “a million fraud cases a year” is how one former regulator puts it. But the mountain of evidence collected against Goldman by Levin’s small, 15-desk office of investigators — details of gross, baldfaced fraud delivered up in such quantities as to almost serve as a kind of sarcastic challenge to the curiously impassive Justice Department — stands as the most important symbol of Wall Street’s aristocratic impunity and prosecutorial immunity produced since the crash of 2008.

To date, there has been only one successful prosecution of a financial big fish from the mortgage bubble, and that was Lee Farkas, a Florida lender who was just convicted on a smorgasbord of fraud charges and now faces life in prison. But Farkas, sadly, is just an exception proving the rule: Like Bernie Madoff, his comically excessive crime spree (which involved such lunacies as kiting checks to his own bank and selling loans that didn’t exist) was almost completely unconnected to the systematic corrup-tion that led to the crisis. What’s more, many of the earlier criminals in the chain of corruption — from

subprime lenders like Countrywide, who herded old ladies and ghetto families into bad loans, to rapacious banks like Washington Mutual, who pawned off fraudulent mortgages on investors — wound up go-ing belly up, sunk by their own greed.

O O O MAT TAIBBI / LINK

They jog in orderly rows of twos through the industrial area. The young people, who look about 19 or 20, hope to be future builders of the iPad. Each of them holds a brown envelope in his or her left hand that contains their job application. At the foreman’s command, they turn a corner onto the steps of the recruitment office.

They are here because of electronic component manufacturer Foxconn, which is hiring tens of thou-sands of employees. The company has built new factories in the Chinese city of Chengdu to produce millions of iPads for Apple. The supplier is known for the strict rules it imposes on its employees. Last year, that strict discipline may have helped lead to the suicide of 13 workers at a Foxconn facility in Shenzhen. At the time, observers spoke of terrible working conditions there.

SPIEGEL ONLINE paid a visit to the Chengdu plant to examine the question of whether the company is now treating its employees better.

“We are not allowed to talk while we are working,” says 19-year-old Wang Cui, whose name was changed for this story. She has prominent eyes and dark skin, and wears a blue vest with the Foxconn logo over her white plastic jacket. Her long fingernails are well cared-for. She does not work on the production line, but instead performs quality control on iPad housings.

Is she bothered by the strict rules? “Work is work, the rest is the rest,” says Wang, shrugging her shoulders.

Then she does talk, despite the ban. She says she fears the foremen. “The supervisors do not respect the workers,” she says, adding that her colleagues have been punished even for small mistakes. The supervisors forced them to stand between the production lines for all to see -- almost as if they were in the pillory.

“Order and obedience rule here,” says Wang. Her colleagues nod.

Foxconn concedes the possibly that there might have been misconduct. “We do not support it, but cannot rule out that it can happen,” the company said in a statement. “But we want to change that.”

O O O DER SPIEGEL / LINK

... To date, there has been only one successful prosecution of a financial big fish from the mortgage bubble

17.CHARTS THAT MAKE YOU GO Hmmm...

12 May 2011 17

Based on the re-ported open interest and volume numbers by the exchange, silver’s rally yesterday was sparked by fresh shorts who sold the bottom last Thursday and Friday and are now having those sky high mar-gins hit them for a change. Per-haps they have now learned that what is good for the goose is also good for the gander.

The market has had a nice pop off the low down near $33 but has yet to regain its footing above the

40 and 50 day moving averages. Until it does, its technical posture, while greatly improved, still re-mains bearish on the daily chart. You will note on the chart that unlike gold, which has retraced half of its recent losses, silver has not yet been able to recapture the 38.2% retracement level of its recent leg lower.

These steep sell offs followed by steep recoveries are always unsettling. What silver needs is a period of consolidation which will allow this excess volatility to get wrung out and let things calm down a bit. There has been way too much emotion in this market and that is being reflected by these wide price swings.

I like the fact that it continues to move away from the $33 level but I would feel a bit more comfortable from a bullish standpoint if it could at the very least clear last Thursday’s high which is near $39.40.

That would also put it above that 38.2% retracement level referenced above.

We will have to watch and see what level the stronger-handed shorts begin to dig in. There does look to be some resistance entering in here above $38 as I write this.

Once again, as usual, the shares continue to weigh on the entire sector.

O O O DAN NORCINI / LINK

CLICK TO ENLARGE

CLICK TO ENLARGE SOURCE: DAN NORCINI

SOURCE: DAN NORCINI

18.CHARTS THAT MAKE YOU GO Hmmm...

12 May 2011 18

My monthly update Inside the Consumer Price Index identifies the components of the Consumer Price Index, documents their relative weights, and uses line charts to show the cu-mulative percentage change of each since 2000.

In this post I’m using a bar chart to illustrate the relative change over the same time frame. The table [right] documents the cur-rent weights assigned by the Bu-reau of Labor Statistics (BLS) to the eight components of CPI. I’ve also included the weights of the two aggregate categories — Food (ex alcoholic beverages) and En-ergy — that are excluded from CPI to determine the Core CPI. (Note: CPI is sometimes referred to as “Headline CPI” to distinguish it from the Core variety.)

The bar chart below shows the relative change for each component and the two special aggregates. I’ve also added College Tuition & Fees, a subcomponent of Education and Communication, because of its significant impact on house-holds with college expenses. Incidentally, the BLS assigns a mere 1.5% weight to this subcomponent of CPI. But for households planning for college expenses, the impact of inflation is dramatic.

The table and chart above help to explain why inflation is such a controversial topic. If your house-hold mirrors the expense ratios of the CPI weightings, then the monthly CPI re-ports may seem reasonably accurate. However, house-holds on tight budgets will be highly sensitive to the more volatile components of CPI — food and especially energy expenses. Also, for households with greater exposures to energy costs (especially gasoline), medi-cal expenses, or college bills than the BLS weightings, the CPI data will definitely un-derstate your experience.

O O O DSHORT / LINK

SOURCE: DSHORTCLICK TO ENLARGE

19.CHARTS THAT MAKE YOU GO Hmmm...

12 May 2011 19

Ask David Conner, chief executive officer of Singapore’s Oversea-Chinese Bank-ing Corp., what makes a world-class bank and he smiles and tells the story of how he was hired. It was April 2002, and Singapore’s banks faced a struggling economy, poor demand for credit and rising competition from foreign lenders that had just won greater access to the Singaporean market.

Conner, then 53, had taken charge of OCBC after 25 years as an executive at Citigroup Inc. (C) divisions in Singapore, India and Japan. When Conner -- who grew up in St. Louis -- sat down with OCBC’s top directors, they told him they wanted him to make the lender a world-class bank, Bloomberg Markets magazine reports in its June issue.

“What is a world-class bank to you?” Conner asked.

One board member responded, “You tell us.”O O O BLOOMBERG (VIA BARRY RITHOLTZ) / LINK

20.

12 May 2011 20

WORDS THAT MAKE YOU GO Hmmm...

Felix Zulauf is one of the smartest and most widely-respected asset managers in the world and when he talks people listen.

Here he talks - about inflation, the EU, China and the possibility of se-vere trouble in the bond market.

Listen.

Jim Sinclair knows more about mining than most. He tells Eric King that we are nowhere near the top in metal prices, but kicks things off with his views on the bond market

This video, from Monday, looks rather dated now in terms of the prices shown on the board at the outset (silver has been up and down about 10% since it was made), but Ben Davies is not only always worth listening to, but puts some excellent long-term perspective around the frenzied trading in the metals.

Quick.... get him off....

CLICK TO WATCH

CLICK TO LISTEN

CLICK TO LISTEN

SUBSCRIBE UNSUBSCRIBE COMMENTS

and finally…

12 May 2011 21

What else did you expect to find on this page?

Just in case there is anyone who hasn’t seen it...... and for the enjoyment of those who haven’t seen it for a while.

Hmmm…

CLICK TO WATCH

© THINGS THAT MAKE YOU GO HMMM..... 2011