an historical perspective on the current crisis michael d. bordo rutgers university and nber...

TRANSCRIPT

An Historical Perspective An Historical Perspective on the Current Crisison the Current Crisis

Michael D. BordoMichael D. Bordo

Rutgers University and Rutgers University and NBERNBER

Prepared for: The conference “The Global Financial Crisis: Historical Perspective and Implications for New Zealand”

Reserve Bank of New ZealandWellington

Wednesday June 17, 2009

22

An Historical Perspective on the Current An Historical Perspective on the Current CrisisCrisis

IntroductionIntroduction The current global financial crisis displays many similarities to The current global financial crisis displays many similarities to

crises observed across the world in the past two centuries.crises observed across the world in the past two centuries.

There are also some novel features.There are also some novel features.

This talk considers how the present crisis fits into the historical This talk considers how the present crisis fits into the historical pattern. I discuss what is familiar and what is novel about recent pattern. I discuss what is familiar and what is novel about recent events with emphasis on financial innovation, policy errors and events with emphasis on financial innovation, policy errors and private sector behavior.private sector behavior.

As background I also briefly survey the historical evidence for As background I also briefly survey the historical evidence for many countries on crisis incidence, duration and depth.many countries on crisis incidence, duration and depth.

Finally I assess how economic policy has addressed the current Finally I assess how economic policy has addressed the current crisis and conclude with some lessons for policy from an historical crisis and conclude with some lessons for policy from an historical perspective. perspective.

33

2. Historical Evidence on Crisis 2. Historical Evidence on Crisis IncidenceIncidence

2.1 – Bordo, Eichengreen, Kliengebiel and 2.1 – Bordo, Eichengreen, Kliengebiel and Martinez-Peria(2001)Martinez-Peria(2001)

Bordo, Eichengreen, Kliengebiel, and Bordo, Eichengreen, Kliengebiel, and Martinez-Peria(2001), provide Martinez-Peria(2001), provide evidence for a panel of 21 countries evidence for a panel of 21 countries for 120 years and 56 countries for the for 120 years and 56 countries for the 4 recent decades on: the frequency, 4 recent decades on: the frequency, duration and severity of currency, duration and severity of currency, banking and twin crises across 4 banking and twin crises across 4 policy regimes.policy regimes.

44

2.2 - Counting Crises We define financial crises as episodes of financial turbulence

leading to distress – significant problems of illiquidity and insolvency—among major financial market participants and/or to official intervention to contain those consequences.

We identified currency crisis dates using “exchange market pressure” measure and, alternatively, survey of expert opinion. We use the union of these indicators and an EMP cutoff of 1.5 standard deviations from the mean.

For banking crises, we adopted World Bank dates for post-1971 period, and used similar criteria (bank runs, bank failures, and suspensions of convertibility, fiscal resolution) for earlier periods.

Twin crises: banking and currency crises in same or consecutive years. Crises in consecutive years counted as one event.

55

We distinguish four periods:

1880-1914: prior period of financial liberalization and globalization

1919-1939: period of exceptional currency, banking and macro instability

1945-1971: Bretton Woods period of tight regulation of domestic financial systems and of capital controls

1973-1998: second period of financial liberalization and globalization

66

2.3 – Frequency of Crises

We divide the number of crises by the number of country year observations in each sub-period. (See figure l)

Alarmingly, all crises appear to be growing more frequent

Crisis frequency of 12.2% since 1973 exceeds even the unstable interwar period and is three times as great as the pre 1914 earlier era of globalization

Results driven by currency crises, which have become much more frequent in recent period

This challenges the notion that financial globalization creates instability in foreign exchange markets since pre 1914 was the earlier era of globalization

May be due to a combination of capital mobility and democratization

77

88

In contrast, incidence of banking crises only slightly larger than prior to 1914, while twin crises more frequent in the late twentieth century

Note that interwar period had highest incidence of banking crises

Bretton Woods period was notable for the absence of banking crises due to financial repression

A comparison of crisis frequency between emerging and industrial countries (See figure 2), suggests that with the exception of the interwar period, the majority of crises occurred in the emerging countries

99

1010

2.4 – Duration of Crises We define the duration of crises as the average recovery

time. The number of years before the rate of GDP growth returns to its 5-year trend preceding the crisis. (See Figure 3 and Table 1)

Recovery time today for currency crises is longer than preceding 2 regimes but shorter than pre 1914

Banking crises last not much longer now than in earlier periods

Recent period twin crises produce the longest slump for emerging markets

The dominant impression from comparison of pre 1914 and today for all crises is how little has changed

To the extent that crises have been growing longer, we have simply been going back to the future

1111

1212

2.5 – Depth of Crises We calculate the depth of crises by calculating, over the

years prior to full recovery, the difference between pre-crisis trend growth and actual growth. (See Figure 4 and Table 1 – which shows cumulative output loss as a percentage of GDP)

We find that output losses from currency crises were even greater before 1914 than today. The difference is most pronounced for emerging countries.

Output losses from banking crises also greater in pre 1914 regime than today

Twin crises show comparable output losses for today and pre-1914 for emerging markets

Key unsurprising fact is the large output losses in the interwar from both currency and twin crises

1313

1414

1515

2.6 – Reinhart and Rogoff Carmen Reinhart and Kenneth Rogoff (2008) have

extended the data base of financial crises in Bordo et al (2001) to include many more countries, to include episodes back to 1800 and forward to 2008

The incidence of banking crises they show in Figure 5 (the proportion of countries with crises weighted by their shares of income) presents a pattern for banking crises which echoes that in Bordo et al(2001), with the highest incidence in the interwar and a recurrence of crises since the early 1970’s.

The recent episode promises to be as severe as the crises of the 90s

1616

1717

3. Credit Crunches, Asset 3. Credit Crunches, Asset Busts, Banking Crises and Busts, Banking Crises and

RecessionsRecessions The current recession was preceded by a massive housing boom in the

U.S., U.K., and a number of other countries. The boom turned into a bust in 2007 and this led to serious financial stress, then a credit crunch and now a serious recession which has become global

There is considerable evidence both recent and historical linking the severity of recessions to asset price busts and credit crunches

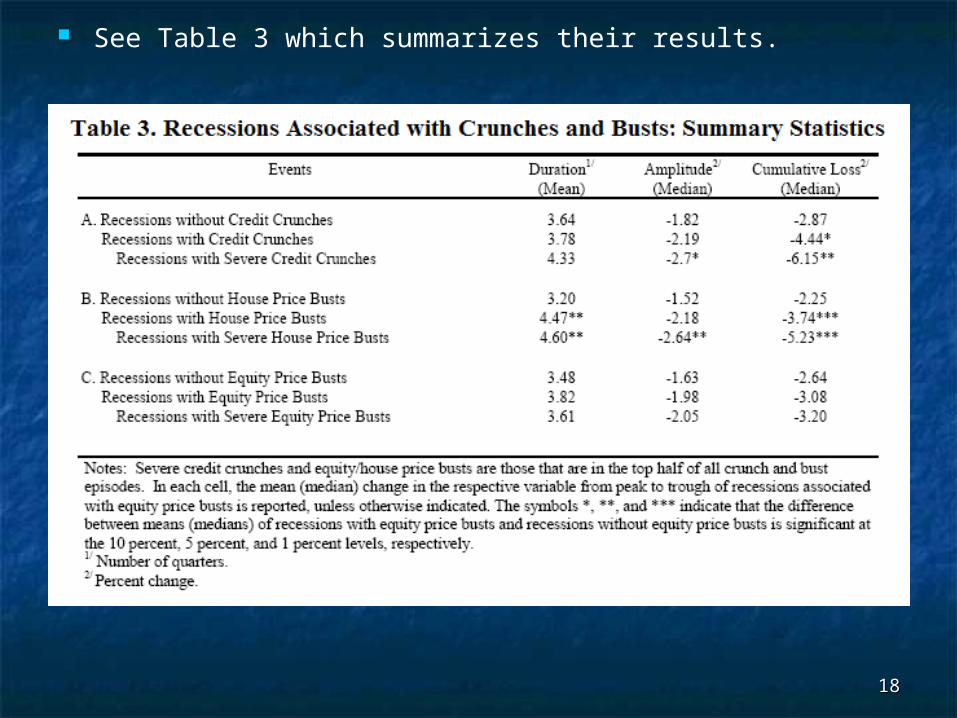

Claessens, Kose, and Terrones (2008) study the behavior of financial variables around recessions, credit crunches, and asset price busts for a panel of 21 OECD countries, 1960-2007

They find that house price busts (declines in real prices from cyclical peaks to troughs of at least 30%) significantly deepen and prolong recessions

They also find that credit crunches (declines of at least 20% from cyclical peaks to troughs) also worsen and prolong recessions

Real equity price busts (declines of at least 50% from cyclical peak to trough) do not have as serious effects on recessions.

1818

See Table 3 which summarizes their results.

1919

Reinhart and Rogoff (2009) present historical evidence on systemic financial crises.

They include the recent “big five” advanced economy crises (Spain 1977, Norway 1987, Finland 1991, Sweden 1991, and Japan 1992), the Asian crisis of 1992, Colombia 1998, Argentina 2001 and two historical episodes Norway 1899 and the U.S. 1929.

They calculate peak to trough changes in real housing prices, real equity prices and real per capita GDP for each banking crisis episode.

Figure 6 shows that real housing price busts associated with banking crises last an average 6 years. Housing prices fell on average by 35.5%

Figure 7 shows that real equity price busts, associated with banking crises, although deeper than housing price busts, last much shorter, for 3.4 years. Stock prices fell on average by 55.9%

Finally, they show in Figure 8 that real per capita GDP in these events declines on average by 9.3 percent and lasts 2 years.

The current U.S. recession which began in December 2007 may very well fit this pattern.

2020

Figure 6Figure 6

2121

Figure 6Figure 7

2222

Figure 6Figure 8

2323

An Historical Perspective on the Crisis of 2007-An Historical Perspective on the Crisis of 2007-20082008

IntroductionIntroduction TodayToday’’s events have echoes in earlier big international s events have echoes in earlier big international

financial crises which were triggered by events in the US financial crises which were triggered by events in the US financial system. e.g. 1857,1893,1907 and 1929-33.financial system. e.g. 1857,1893,1907 and 1929-33.

This crisis has many similarities to those of the recent past This crisis has many similarities to those of the recent past but also some important modern twists.but also some important modern twists.

Crisis started with collapse of US subprime mortgage Crisis started with collapse of US subprime mortgage market spring 2007.market spring 2007.

Causes include : government initiatives to extend home Causes include : government initiatives to extend home ownership, changesownership, changes in regulation , lax oversight, relaxing in regulation , lax oversight, relaxing of lending standards, a prolonged period of abnormally low of lending standards, a prolonged period of abnormally low interest rates, and a savings glut in Asia.interest rates, and a savings glut in Asia.

2424

IntroductionIntroduction Default on mortgages following housing bust spread via Default on mortgages following housing bust spread via

elaborate network of derivatives. elaborate network of derivatives.

The crisis has spread over the real economy through a The crisis has spread over the real economy through a virulent credit crunch. virulent credit crunch.

The crisis and recession has spread from the U.S. to the The crisis and recession has spread from the U.S. to the rest of the world.rest of the world.

Fed and other CBs responded in a classical way by flooding Fed and other CBs responded in a classical way by flooding the financial markets with liquidity. the financial markets with liquidity.

Fiscal authorities still to deal fully with the decline in Fiscal authorities still to deal fully with the decline in solvency in banking system following template of earlier solvency in banking system following template of earlier bailouts like RFC in the 1930s, Sweden 1992 and Japan late bailouts like RFC in the 1930s, Sweden 1992 and Japan late 19901990’’s.s.

2525

IntroductionIntroduction

I provide an historical perspective on I provide an historical perspective on the current crisis, contrasting the old the current crisis, contrasting the old with the modern and offer some with the modern and offer some lessons for policy. lessons for policy.

2626

Some Descriptive Historical Some Descriptive Historical EvidenceEvidence

Figure 1 upper panel shows monthly Baa-Ten year Treasury Figure 1 upper panel shows monthly Baa-Ten year Treasury constant maturity bond spread and NBER recessions : 1953 constant maturity bond spread and NBER recessions : 1953 to January 2009.to January 2009.

The quality spread can reflect asymmetric information and The quality spread can reflect asymmetric information and signal a credit crunch.signal a credit crunch.

Figure 1 also shows important events like banking crises, Figure 1 also shows important events like banking crises, stock market crashes and political events. Lower panel stock market crashes and political events. Lower panel shows the Federal Funds rateshows the Federal Funds rate

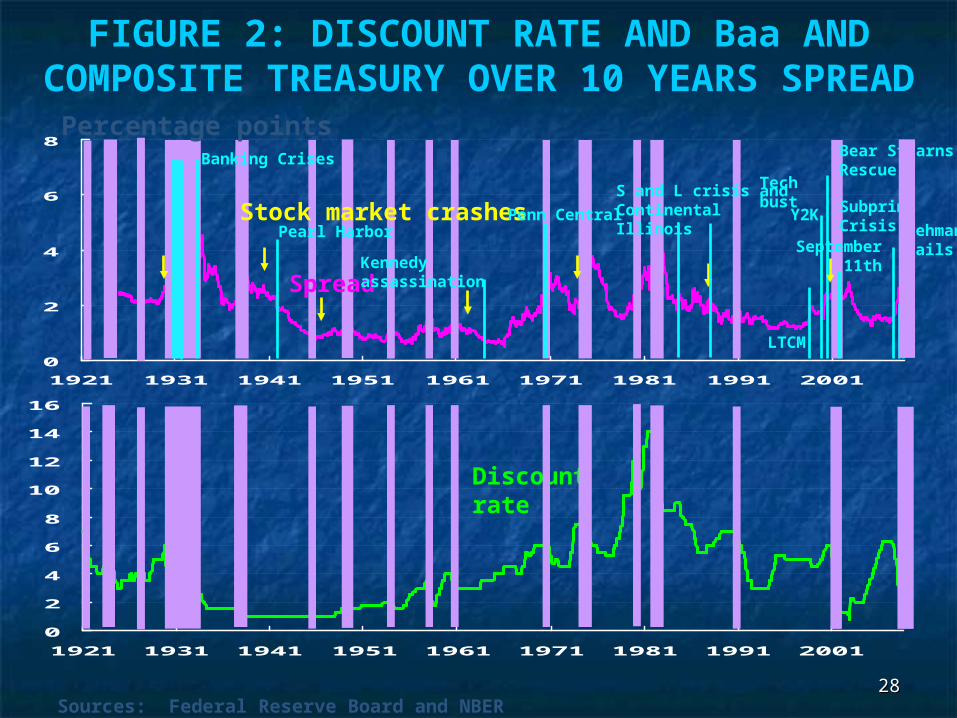

Figure 2 shows Baa, ten year Treasury composite bond Figure 2 shows Baa, ten year Treasury composite bond spread from 1921 to January 2009. The discount rate is spread from 1921 to January 2009. The discount rate is substituted for the FFR. substituted for the FFR.

2727

0

4

8

12

16

20

1953 1963 1973 1983 1993 2003

Percentage points

FIGURE 1: FEDERAL FUNDS RATE AND Baa AND 10-YEAR TCM SPREAD

Sources: Federal Reserve Board and NBER

Stock market crashes

Spread

Federal Funds Rate

Kennedy assassinationPenn Central

S and L crisis and Continental Illinois

LTCM

Y2KTech bust

September 11

Sub-primecrisis

Bear Stearns Rescue

Lehman fails

2828

0

2

4

6

8

10

12

14

16

1921 1931 1941 1951 1961 1971 1981 1991 2001

0

2

4

6

8

1921 1931 1941 1951 1961 1971 1981 1991 2001

Percentage points

FIGURE 2: DISCOUNT RATE AND Baa AND COMPOSITE TREASURY OVER 10 YEARS SPREAD

Sources: Federal Reserve Board and NBER

Stock market crashes

Spread

Discount rate

Banking Crises

September 11th

Tech bust

Y2K

LTCM

S and L crisis and Continental IllinoisPenn Central

Kennedy assassination

Pearl Harbor

Subprime Crisis

Bear Stearns Rescue

Lehman fails

2929

Some Descriptive Historical Some Descriptive Historical EvidenceEvidence

The peaks in the credit cycle proxied by the spread The peaks in the credit cycle proxied by the spread line up with upper turning points of the business line up with upper turning points of the business cycle. cycle.

Many events like banking crises and stock market Many events like banking crises and stock market crashes occur close to the peaks. crashes occur close to the peaks.

Policy rates peak very close to or before the peaks of Policy rates peak very close to or before the peaks of the credit cycle. the credit cycle.

In the recent crisis the spreads are higher than the In the recent crisis the spreads are higher than the recession of 2001 and the recession of the early recession of 2001 and the recession of the early 19801980’’s. They are close to those of the early 1930s. They are close to those of the early 1930’’s.s.

3030

Historical Parallels and Modern Historical Parallels and Modern TwistsTwists

Many of the financial institutions and instruments caught Many of the financial institutions and instruments caught up in the crisis are part of the centuries old phenomenon of up in the crisis are part of the centuries old phenomenon of financial innovation. financial innovation.

The rise and fall of financial institutions and instruments The rise and fall of financial institutions and instruments occurs as part of the lending booms and busts cycle occurs as part of the lending booms and busts cycle financed by credit. Credit cycle connected to the business financed by credit. Credit cycle connected to the business cycle. cycle.

Irving Fisher ( 1933) and others tell the story of a business Irving Fisher ( 1933) and others tell the story of a business cycle upswing driven by a displacement leading to an cycle upswing driven by a displacement leading to an investment boom financed by bank credit and new credit investment boom financed by bank credit and new credit instruments. instruments.

The boom leads to a state of euphoria and possibly bubble.The boom leads to a state of euphoria and possibly bubble.

3131

Historical Parallels and Modern Historical Parallels and Modern TwistsTwists

A state of overindebtedness leads to a crisis. A state of overindebtedness leads to a crisis.

A key dynamic in the crisis stressed is information A key dynamic in the crisis stressed is information asymmetry manifest in the spread between risky and asymmetry manifest in the spread between risky and safe securities. (Mishkin, 1997) safe securities. (Mishkin, 1997)

The bust would lead to bank failures and possibly panics. The bust would lead to bank failures and possibly panics. This led to the case for a LLR following BagehotThis led to the case for a LLR following Bagehot ’’s rule.s rule.

Countercyclical monetary policy is also an integral part Countercyclical monetary policy is also an integral part of the boom-bust credit cycle. of the boom-bust credit cycle.

Stock market booms occur in environments of low Stock market booms occur in environments of low inflation, rising real GDP growth and low policy interest inflation, rising real GDP growth and low policy interest rates. As the boom progresses and inflationary pressure rates. As the boom progresses and inflationary pressure builds up, central banks inevitably tighten policy helping builds up, central banks inevitably tighten policy helping to trigger the ensuing crash. (Bordo and Wheelock, to trigger the ensuing crash. (Bordo and Wheelock, 2005)2005)

3232

Historical Parallels and Modern Historical Parallels and Modern TwistsTwists

Similar story in housing (Leamer 2007)Similar story in housing (Leamer 2007)

Stock market crashes can have serious real Stock market crashes can have serious real consequences via wealth effects and liquidity consequences via wealth effects and liquidity crises. crises.

Housing busts can destabilize the banking system Housing busts can destabilize the banking system and depress the real economy.and depress the real economy.

The recent housing boom was likely triggered by The recent housing boom was likely triggered by a long period of abnormally low interest rates a long period of abnormally low interest rates reflecting loose monetary policy from 2001 to reflecting loose monetary policy from 2001 to 2004 and a global savings glut. 2004 and a global savings glut.

The bust was likely induced by a rise in rates in The bust was likely induced by a rise in rates in reaction to inflationary pressure. reaction to inflationary pressure.

3333

The Non Bank Financial Sector, Financial The Non Bank Financial Sector, Financial Innovation and Financial Crises Innovation and Financial Crises

The traditional view sees a financial crisis as coming from the The traditional view sees a financial crisis as coming from the liability side as depositors rush to convert deposits into liability side as depositors rush to convert deposits into currency. In recent decades, currency. In recent decades, since advent of deposit since advent of deposit insurance, pressure has come from the insurance, pressure has come from the asset sideasset side. .

Examples include the commercial paper market Penn Central Examples include the commercial paper market Penn Central 1970 ; Emerging market debt in 1982 ; hedge funds LTCM in 1970 ; Emerging market debt in 1982 ; hedge funds LTCM in 1998.1998.

Historical example of 1763 crisis in market for bills of Historical example of 1763 crisis in market for bills of exchange.(exchange.(Schnabel and Shinn 2001)Schnabel and Shinn 2001)

Financial innovationFinancial innovation which increased leverage is part of the which increased leverage is part of the story with Penn Central (commercial paper) ; savings and loan story with Penn Central (commercial paper) ; savings and loan crisis (junk bonds) ; LTCM (derivatives and hedge funds) ; crisis (junk bonds) ; LTCM (derivatives and hedge funds) ; today securitization of subprime mortgages today securitization of subprime mortgages

3434

Modern TwistsModern Twists Recently risk has been shifted from the originating bank Recently risk has been shifted from the originating bank

into mortgage backed securities which bundles shaky into mortgage backed securities which bundles shaky risk with the more creditworthyrisk with the more creditworthy

Asset backed securities absorbed by hedge funds, Asset backed securities absorbed by hedge funds, offshore banks and commercial paper. offshore banks and commercial paper.

Shifting of risk didn’t reduce systematic risk and may Shifting of risk didn’t reduce systematic risk and may have increased risk of a more widespread meltdown. have increased risk of a more widespread meltdown.

Another key modern twist is growth of the unregulated Another key modern twist is growth of the unregulated shadow banking system shadow banking system

Repeal of Glass Steagall in 1999 encouraged investment Repeal of Glass Steagall in 1999 encouraged investment banks to increase leverage. So did the investment banks to increase leverage. So did the investment banks going public.banks going public.

3535

Modern TwistsModern Twists

When the crisis hit they were forced to When the crisis hit they were forced to delever, leading to a fire sale of assets in a delever, leading to a fire sale of assets in a declining market which lowered the value of declining market which lowered the value of their assets and those of other financial their assets and those of other financial firms. firms.

A similar feedback loop in Great Depression A similar feedback loop in Great Depression (Friedman and Schwartz, 1963)(Friedman and Schwartz, 1963)

3636

Prospects for the Emerging Prospects for the Emerging MarketsMarkets

Financial crises have always had an international Financial crises have always had an international dimension. dimension.

Contagion spreads through asset markets ,international Contagion spreads through asset markets ,international banking and international standard. banking and international standard.

Baring crisis of 1890 classic historical example of Baring crisis of 1890 classic historical example of contagion, central bank tightening led to sudden stops, contagion, central bank tightening led to sudden stops, currency crises and debt defaults in the emergers currency crises and debt defaults in the emergers similar to 1997-98.similar to 1997-98.

Current crisis has spread from the US to the advanced Current crisis has spread from the US to the advanced countries via holding of opaque subprime mortgage countries via holding of opaque subprime mortgage derivatives in diverse banks in Europe and elsewhere. derivatives in diverse banks in Europe and elsewhere.

3737

Prospects for the Emerging Prospects for the Emerging MarketsMarkets

Current crisis initially was contained to the advanced Current crisis initially was contained to the advanced countries, which were exposed to subprime mortgages. countries, which were exposed to subprime mortgages.

Pressure has subsequently spread to emerging markets, Pressure has subsequently spread to emerging markets, especially those indebted in hard currency to advanced especially those indebted in hard currency to advanced countries, e.g. Iceland, Hungary, Latvia and Ukraine. countries, e.g. Iceland, Hungary, Latvia and Ukraine.

Many Asian and Latin countries initially avoided the Many Asian and Latin countries initially avoided the crisis because of defensive measures taken in reaction crisis because of defensive measures taken in reaction to the 1990s meltdown. to the 1990s meltdown.

As the credit crunch continued and recession spread in As the credit crunch continued and recession spread in US and Europe, emergers also were affected. US and Europe, emergers also were affected.

They are facing sudden stops and some may end up They are facing sudden stops and some may end up defaulting on sovereign debt.defaulting on sovereign debt.

3838

Policy LessonsPolicy Lessons

Crisis has implications for monetary policy on Crisis has implications for monetary policy on key issues of : liquidity, solvency, stability of key issues of : liquidity, solvency, stability of real economy. real economy.

3939

LiquidityLiquidity Central banks reacted quickly in the Bagehot manner to Central banks reacted quickly in the Bagehot manner to

unfreeze interbank market in August 2007.unfreeze interbank market in August 2007.

Run on Northern RockRun on Northern Rock September 14, 2007 reflected September 14, 2007 reflected inadequacies in UK deposit insurance and separation of inadequacies in UK deposit insurance and separation of financial supervison and regulation from the central bank. financial supervison and regulation from the central bank.

Bear Stearns crisis in March 2008 led Fed to develop new Bear Stearns crisis in March 2008 led Fed to develop new programs for access to discount window lending. programs for access to discount window lending.

The Fed changed its tactics away from general liquidity The Fed changed its tactics away from general liquidity provision via OMO and leaving distribution of liquidity to provision via OMO and leaving distribution of liquidity to individual firms to the market.individual firms to the market.

It has developed a large number of credit allocation It has developed a large number of credit allocation facilities. Much of the credit extended was sterilized. facilities. Much of the credit extended was sterilized. However since September 2008, the monetary base has However since September 2008, the monetary base has expanded.expanded.

4040

LiquidityLiquidity

Targeted lending exposes the Fed to politicize Targeted lending exposes the Fed to politicize its selection of recipients of credit. This is a its selection of recipients of credit. This is a throwback to policies followed earlier in the throwback to policies followed earlier in the twentieth century.twentieth century.

Also the Fed has greatly reduced its holdings Also the Fed has greatly reduced its holdings of Treasury securities. How will it be able to of Treasury securities. How will it be able to eventually tighten with its large holdings of eventually tighten with its large holdings of unmarketable mortgage backed securities?unmarketable mortgage backed securities?

4141

SolvencySolvency The Fed and US monetary authorities bailed out firms too The Fed and US monetary authorities bailed out firms too

systematically connected to fail : Bear Stearns March systematically connected to fail : Bear Stearns March 2008, GSEs July 2008, AIG September 2008 and three 2008, GSEs July 2008, AIG September 2008 and three times since, Citigroup (three times) and Bank of America.times since, Citigroup (three times) and Bank of America.

Lehman Brothers was allowed to fail in September on the Lehman Brothers was allowed to fail in September on the grounds it was basically insolvent and not as grounds it was basically insolvent and not as systematically important as the others. systematically important as the others.

Had Bear Stearns been allowed to fail, could the more Had Bear Stearns been allowed to fail, could the more severe crisis in September/October 2008 have been severe crisis in September/October 2008 have been avoided?avoided?

Had Bear Stearns been closed and liquidated it is likely Had Bear Stearns been closed and liquidated it is likely that more demand for Fed credit would have come forward that more demand for Fed credit would have come forward than actually occurred. than actually occurred.

4242

SolvencySolvency When Drexel Burnham Lambert was shut When Drexel Burnham Lambert was shut

down in 1990, there were no spillover effects.down in 1990, there were no spillover effects.

Assume a crisis in March 2008 like the one Assume a crisis in March 2008 like the one that followed Lehman’ failure in September that followed Lehman’ failure in September had occurred as the Fed feared at the time.had occurred as the Fed feared at the time.

It would have not been as bad as what It would have not been as bad as what actually occurred in September because the actually occurred in September because the Bear Stearns rescue led investment banks Bear Stearns rescue led investment banks and other market players to follow riskier and other market players to follow riskier strategies than otherwise on the assumption strategies than otherwise on the assumption that they also would be bailed out. that they also would be bailed out.

4343

SolvencySolvency This surely made the financial system more fragile than This surely made the financial system more fragile than

otherwise so that when the MA let Lehman fail the shock otherwise so that when the MA let Lehman fail the shock that occurred and the damage to confidence was much that occurred and the damage to confidence was much worse.worse.

The deepest problem facing the banking system is The deepest problem facing the banking system is solvency. The problem stems from the difficulty of pricing solvency. The problem stems from the difficulty of pricing securities backed by a pool of assets because the quality securities backed by a pool of assets because the quality of individual components of the pool variesof individual components of the pool varies

The credit market is plagued by the inability to determine The credit market is plagued by the inability to determine which firms are solvent and which firms are not.which firms are solvent and which firms are not.

Lenders are unwilling to extend loans when they cannot Lenders are unwilling to extend loans when they cannot be sure that a borrower is credit worthybe sure that a borrower is credit worthy

4444

SolvencySolvency This is a serious shortcoming of the securitization This is a serious shortcoming of the securitization

process that is responsible for the paralysis of the process that is responsible for the paralysis of the credit marketscredit markets

The Fed was slow to recognize the solvency problem.The Fed was slow to recognize the solvency problem.

The US Treasury's TARP plan of October 13 2008 The US Treasury's TARP plan of October 13 2008 based on the UK plan to inject capital into the banking based on the UK plan to inject capital into the banking system only went part way to help solve this problem. system only went part way to help solve this problem. However the credit crunch continues and bad assets However the credit crunch continues and bad assets keep piling up as house prices have continued to keep piling up as house prices have continued to decline.decline.

There is precedence to the Treasury's plan with the There is precedence to the Treasury's plan with the RFC in the 1930s, Sweden in 1992 and Japan in the RFC in the 1930s, Sweden in 1992 and Japan in the late 1990s. late 1990s.

4545

SolvencySolvency The recent Financial Stability Plan to set up a Public The recent Financial Stability Plan to set up a Public

Private Investment Fund whereby private institutions Private Investment Fund whereby private institutions will be subsidized to acquire troubled assets may work will be subsidized to acquire troubled assets may work but the banks may be reluctant to sell them. They fear but the banks may be reluctant to sell them. They fear that this would further erode their capital base.that this would further erode their capital base.

The Treasury’s plan to provide capital to the leading The Treasury’s plan to provide capital to the leading U.S. banks as warranted by a stress test combined with U.S. banks as warranted by a stress test combined with the (PPIP) may only help to overcome the banking crisis the (PPIP) may only help to overcome the banking crisis when insolvent banks have been taken over, their when insolvent banks have been taken over, their management replaced and they are recapitalized.management replaced and they are recapitalized.

Adopting the Good Bank Bad Bank solution of the Adopting the Good Bank Bad Bank solution of the Swedes may still be required.Swedes may still be required.

4646

Real EconomyReal Economy Given the Fed’s dual mandate, attenuating the Given the Fed’s dual mandate, attenuating the

recession consequent upon the credit crunch is recession consequent upon the credit crunch is now the primary goal of monetary policy.now the primary goal of monetary policy.

The recent shift to Quantitative Easing will most The recent shift to Quantitative Easing will most likely attenuate the recession.likely attenuate the recession.

The fiscal stimulus will not likely be as potent The fiscal stimulus will not likely be as potent as monetary ease. The record of the 1930s in as monetary ease. The record of the 1930s in the U.S. and Japan in the 1990s makes the the U.S. and Japan in the 1990s makes the case.case.

Once recovery is in sight and inflationary Once recovery is in sight and inflationary expectations pick up it will behoove the Fed to expectations pick up it will behoove the Fed to return to its (implicit) inflation target. return to its (implicit) inflation target.

4747

The monetary authorities in the US and Europe The monetary authorities in the US and Europe acted quickly to resolve the liquidity aspects of acted quickly to resolve the liquidity aspects of the crisis. the crisis.

This is in stark contrast to the Great Depression This is in stark contrast to the Great Depression when the Fed did virtually nothing. when the Fed did virtually nothing.

Expansionary monetary policy and less likely Expansionary monetary policy and less likely fiscal stimulus packages may attenuate the fiscal stimulus packages may attenuate the downturn.downturn.

The solvency aspect still remains.The solvency aspect still remains.

Without a resolution to the banking crisis as Without a resolution to the banking crisis as occurred in the U.S. in the 1930’s, 1990’s, occurred in the U.S. in the 1930’s, 1990’s, Sweden in 1992 and elsewhere, and until the Sweden in 1992 and elsewhere, and until the solvency problem is solved, recovery will be solvency problem is solved, recovery will be limited.limited.

ConclusionConclusion