amendment no. 3 to form s-4 registration ... amend 3.pdf2003, by and among airborne, dhl worldwide...

TRANSCRIPT

As Filed With the Securities and Exchange Commission on July 11, 2003Registration No. 333-105137

SECURITIES AND EXCHANGE COMMISSIONWASHINGTON, D.C. 20549

Amendment No. 3to

FORM S-4REGISTRATION STATEMENT

UNDERTHE SECURITIES ACT OF 1933

ABX AIR, INC.(Exact Name of Registrant as Specified in its Governing Instrument)

Delaware(State or Other Jurisdiction ofIncorporation or Organization)

4512(Primary Standard IndustrialClassification Code Number)

91-1091619(I.R.S. EmployerIdentification No.)

145 Hunter DriveWilmington, Ohio 45177

(937) 382-5591(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Joseph C. HetePresident and Chief Operating Officer

ABX Air, Inc.145 Hunter Drive,

Wilmington, Ohio 45177937-382-5591

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies To:

C. James Levin, Esq.Mark C. Easton, Esq.

O’Melveny & Myers LLP400 S. Hope Street

Los Angeles, California 90071(213) 430-6000

D. Rhett Brandon, Esq.Peter S. Malloy, Esq.

Simpson Thacher & Bartlett425 Lexington AvenueNew York, NY 10017

(212) 455-2000

APPROXIMATE DATE OF COMMENCEMENT OF PROPOSED SALE OF THE SECURITIES TO THE PUBLIC: As soon as practicable after theeffective date of this Registration Statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with GeneralInstruction G, check the following box. ‘

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list theSecurities Act registration statement number of the earlier effective registration statement for the same offering. ‘

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registrationstatement number of the earlier effective registration statement for the same offering. ‘

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAYITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THISREGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(A) OF THE SECURITIES ACT OF1933 OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TOSAID SECTION 8(A), MAY DETERMINE.

AIRBORNE, INC.3101 Western Avenue

P.O. Box 662Seattle, Washington 98111

July 11, 2003

Dear Stockholder:You are cordially invited to attend the annual meeting of stockholders of Airborne, Inc. (“Airborne”) to be

held on August 14, at 10:00 a.m., local time, at The Westin Hotel, 1900 Fifth Avenue, Seattle, Washington forthe following purposes:

1. To consider and vote upon a proposal to adopt the agreement and plan of merger, dated as of March 25,2003, by and among Airborne, DHL Worldwide Express B.V. (“DHL”) and Atlantis AcquisitionCorporation, an indirect, wholly-owned subsidiary of DHL (“Atlantis Acquisition”).

2. To approve the alternative merger consideration of $21.65 as described in the proxy statement/prospectus.3. To approve the supermajority voting provision to be contained in the amended and restated certificate of

incorporation of ABX Air, Inc. (“ABX Air”).4. To approve the ABX Air rights agreement.5. To elect two directors for terms of three years.6. To hear and consider reports from officers of Airborne.7. To transact such other business, including consideration of stockholder proposals, as may properly

come before the meeting and any adjournments thereof.

If our merger agreement with DHL, the alternative merger consideration, the ABX Air supermajority votingprovision and the ABX Air rights agreement are adopted and the transaction is completed, DHL will acquire ourground operations in the following steps:

• Airborne’s air operations will be separated from its ground operations, with the air operations beingretained by ABX Air;

• DHL will acquire Airborne’s ground operations (including all operations conducted by Airborne Express,Inc., including its customer relationships, pick up and delivery network and all related sales, marketingand administrative services) through a merger of Atlantis Acquisition with and into Airborne; and

• Airborne stockholders will receive $21.25 in cash and one share of common stock of ABX Air per shareof Airborne common stock.

There is no established public trading market for ABX Air common stock. Immediately following thecompletion of the merger and the separation, the ABX Air common stock will not be traded on a nationalexchange or NASDAQ. We expect that the ABX Air common stock may be traded on the OTC Bulletin Board orits successor.

Immediately following the closing of the transaction, Airborne will be an indirect, wholly-owned subsidiaryof DHL (but may subsequently be merged with another wholly-owned indirect subsidiary of DHL) and ABX Airwill become an independent public company wholly-owned by Airborne’s former stockholders. ABX Air willalso enter into a number of commercial agreements with Airborne, which after the merger will be owned byDHL, including an ACMI service agreement and a hub and line-haul services agreement. Under certain limitedcircumstances, you will instead receive a cash payment of $21.65 for each share of common stock that you ownat the time of the merger and you will not receive a share of common stock of ABX Air (referred to as the“alternative merger consideration”).

Our Board of Directors has carefully considered the merger agreement and the proposed transaction and hasdetermined that the terms of the merger are fair to and in the best interests of our stockholders. Our Board ofDirectors unanimously recommends that our stockholders vote FOR the adoption of the merger agreement, FORthe alternative merger consideration, FOR the ABX Air supermajority voting provision and FOR the ABX Airrights agreement. Although proposals 1, 2, 3 and 4 above are separate matters to be voted upon by you, each ofthese proposals is expressly conditioned upon the approval of the others. This means that you must approveproposals 1, 2, 3 and 4 if you wish to approve the merger.

This booklet provides you with detailed information about the proposed transaction and related matters.This booklet is also a prospectus that describes ABX Air, the ABX Air common stock and the separation. Youshould carefully consider the risk factors beginning on page 30 of the proxy statement/prospectus. Weurge you to read these documents carefully, including the appendices. If you have any questions about themerger or the separation please call Georgeson Shareholder Communications, Inc., our proxy solicitors,toll-free (888) 897-5991.

Your vote is very important. We cannot complete the merger unless the merger agreement, the alternativemerger consideration, the ABX Air supermajority voting provision and the ABX Air rights agreement areapproved by holders of a majority of all of the outstanding shares of our common stock. Accordingly, failing tovote your shares will have the same effect as a vote against the merger. Whether or not you plan to be present atthe annual meeting, we urge you to complete, sign, date and return the enclosed proxy card to ensure that yourshares are represented at the annual meeting. If you hold your shares as a holder of record, you may also vote bytelephone, or electronically over the Internet, by following the instructions on your proxy card.

In addition to voting on the merger agreement, the alternative merger consideration, the ABX Airsupermajority voting provision and the ABX Air rights agreement, you are being asked to elect two directors andto consider a number of stockholder proposals. We urge you to cast your votes on these important matters aswell. For the reasons described in the proxy statement/prospectus, our Board of Directors unanimouslyrecommends that our stockholders vote FOR the two nominees for directors and AGAINST the variousstockholder proposals.

On behalf of our Board of Directors, I thank you for your support and appreciate your consideration of thesematters.

Very truly yours,

Carl D. DonawayChairman and Chief Executive Officer

Neither the Securities and Exchange Commission nor any state securities commission has approved ordisapproved of the merger and separation described in this proxy statement/prospectus or the ABX Aircommon stock to be issued in connection with the merger or determined if this proxy statement/prospectusis accurate or adequate. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus is dated July 11, 2003 and is first being mailed to stockholders on or aboutJuly 16, 2003.

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information about Airbornefrom documents that are not included in or delivered with this proxy statement/prospectus. This information isavailable to you without charge upon your written or oral request. You can obtain the documents incorporated byreference in this proxy statement/prospectus by requesting them in writing or by telephone from GeorgesonShareholder Communications Inc. at the following address and telephone number:

Georgeson Shareholder Communications Inc.17 State Street10th Floor

New York, New York 10004Telephone: (888) 897-5991

If you would like to request documents, please request them by August 8, 2003 in order to receivethem before the annual meeting.

See “Where You Can Find More Information” on page 174 of the proxy statement/prospectus.

This proxy statement/prospectus serves as a prospectus of ABX Air relating to the shares of ABX Aircommon stock to be issued to Airborne’s former stockholders in the merger.

AIRBORNE, INC.NOTICE OF ANNUALMEETING OF STOCKHOLDERS

TO BE HELD ON AUGUST 14, 2003

To Our Stockholders:

NOTICE IS HEREBY GIVEN that the annual meeting of stockholders of Airborne, Inc. (“Airborne”) willbe held on August 14, 2003, at 10:00 a.m., local time, at The Westin Hotel, 1900 Fifth Avenue, Seattle,Washington 98111 for the following purposes:

1. To consider and vote upon a proposal to adopt the agreement and plan of merger, dated as of March 25,2003, by and among Airborne, DHL Worldwide Express B.V. (“DHL”) and Atlantis AcquisitionCorporation, an indirect, wholly-owned subsidiary of DHL.

2. To approve the alternative merger consideration of $21.65 as described in the proxy statement/prospectus.

3. To approve the supermajority voting provision to be contained in ABX Air’s amended and restatedcertificate of incorporation.

4. To approve the ABX Air rights agreement.

5. To elect two directors for terms of three years.

6. To hear and consider reports from officers of Airborne.

7. To transact such other business, including consideration of stockholder proposals, as may properlycome before the meeting and any adjournments thereof.

Only stockholders of record on July 8, 2003, the record date for the annual meeting, are entitled to notice of,and to vote at, the annual meeting or any adjournments or postponements of the meeting. The number ofoutstanding shares of Airborne common stock on the record date was 48,852,991. Each stockholder is entitled toone vote for each share of common stock held on the record date. A list of stockholders will be open forexamination by any stockholder at the annual meeting.

Our Board of Directors has carefully considered the merger agreement and the proposed transaction and hasdetermined that the terms of the merger are fair to and in the best interests of our stockholders. The Board ofDirectors unanimously recommends that our stockholders vote FOR the adoption of the merger agreement, FORthe alternative merger consideration, FOR the ABX Air supermajority voting provision and FOR the ABX Airrights agreement. Although proposals 1, 2, 3 and 4 above are separate matters to be voted upon by you, theseproposals are expressly conditioned upon the approval of the others. This means that you must approve proposals1, 2, 3 and 4 if you wish to approve the merger. We cannot complete the merger unless the merger agreement, thealternative merger consideration, the ABX Air supermajority voting provision and the ABX Air rights agreementare approved by holders of a majority of all of the outstanding shares of our common stock. Accordingly, failingto vote your shares will have the same effect as a vote against the merger.

The Board of Directors has also carefully considered the two nominees for directors and the Board ofDirectors unanimously recommends that our stockholders vote FOR each of the nominees.

The Board of Directors has also carefully considered the various stockholder proposals that have beensubmitted for consideration at the annual meeting. Each of these proposals is contained in the proxy statement/prospectus. For the reasons described in the proxy statement/prospectus, the Board of Directors unanimouslyrecommends that our stockholders vote AGAINST the adoption of the various stockholder proposals.

Please do not send any stock certificates at this time. If the merger and the separation are completed, youwill be sent instructions regarding the surrender of your stock certificates.

By Order of the Board of Directors,

David C. AndersonSecretary

Seattle, WashingtonJuly 11, 2003

Your vote is very important to us. A proxy card is contained in the envelope in which this proxy statement/prospectus was mailed. Whether or not you plan to attend the annual meeting, you are encouraged to vote on thematters to be considered at the annual meeting and complete, sign and date the proxy card and return it promptlyin the enclosed postage-prepaid envelope. If you hold your shares as a holder of record, you may also vote bytelephone, or electronically over the Internet, by following the instructions on your proxy card.

TABLE OF CONTENTS

Page

QUESTIONS AND ANSWERS ABOUT THE MERGER AND THE SEPARATION . . . . . . . . . . . . . . . . 1

QUESTIONS AND ANSWERS ABOUT THE STOCKHOLDERS MEETING . . . . . . . . . . . . . . . . . . . . . 5

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

The Annual Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Procedure for Voting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

The Parties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Background of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Form of Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Merger Consideration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Effects of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

The Separation of ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Structure of Transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Post-Closing Arrangements Between Airborne and ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Reasons for the Merger and Separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Recommendation of Airborne’s Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Opinion of Airborne’s Financial Advisor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Interests of Certain Persons in the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Federal Income Tax Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Appraisal Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Regulatory Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Conditions to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Termination of the Merger Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Termination Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Other Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

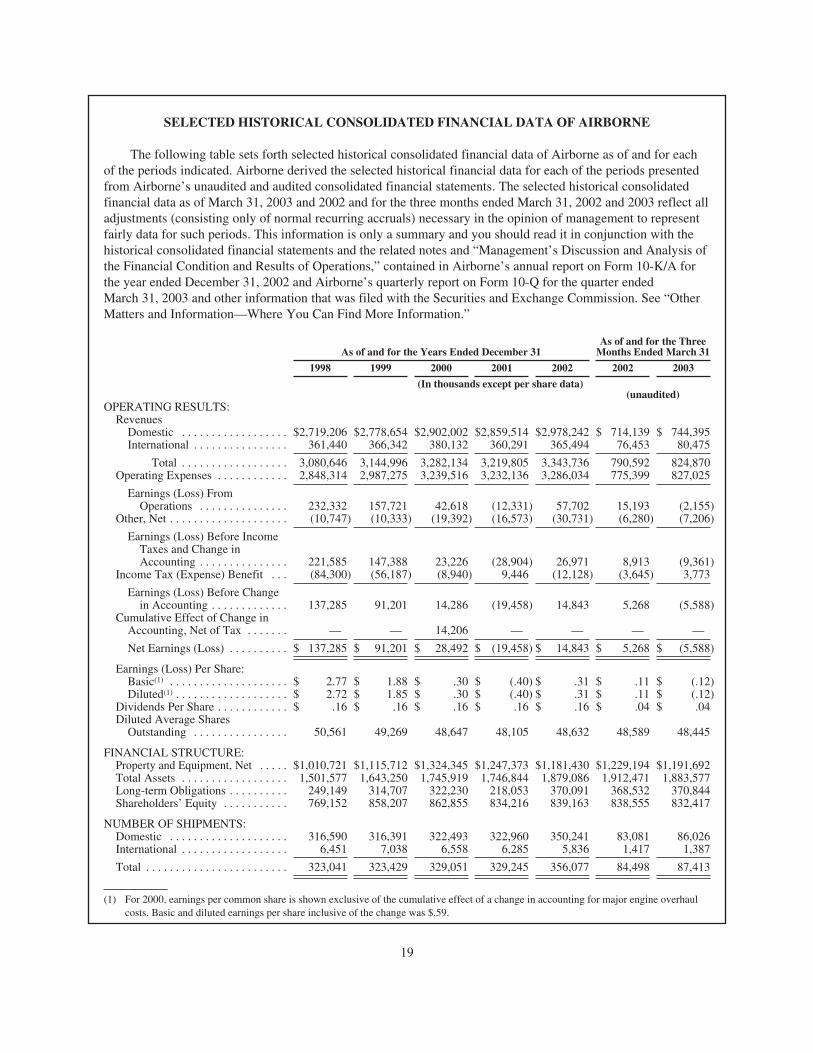

Selected Historical Consolidated Financial Data of Airborne . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Selected Historical Consolidated Financial Data of ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Pro Forma Consolidated Financial Data of ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Comparative Per Share Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Market Price Data and Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

INFORMATION CONCERNING THE ANNUAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Matters to be Considered . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Record Date; Shares Entitled to Vote; Quorum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Vote Required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

i

TABLE OF CONTENTS(continued)

Page

Shares Owned by Airborne Directors, Executive Officers and Affiliates . . . . . . . . . . . . . . . . . . . . . . . . 40

Proxies and Proxy Solicitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Effects of Abstentions and Broker Non-Votes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Stock Certificates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

PROPOSAL 1 AND PROPOSAL 2—THE MERGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Background of the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Purpose and Effects of the Merger and Separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Separation of ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Reasons for the Separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Results of the Merger and Separation on ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Post-Closing Agreements Between Airborne and ABX Air . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Airborne’s Reasons for the Merger; Recommendation of the Airborne Board of Directors . . . . . . . . . 48

Opinion of Airborne’s Financial Advisor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Financial Advisor Fee Arrangements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Financial Projections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Interests of Certain Persons in the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Material Federal Income Tax Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Appraisal Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Regulatory Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Accounting Treatment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

THE MERGER AGREEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Certificate of Incorporation; Bylaws; Directors and Officers of the Surviving Corporation . . . . . . . . . 65

Merger Consideration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

Stock Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Payment Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Representations and Warranties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Interim Operating Covenants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

Recommendation by the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

No Solicitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

Directors & Officers Indemnification and Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

U.S. Department of Transportation Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Access to Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Best Efforts; Consents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

ii

TABLE OF CONTENTS(continued)

Page

Employee Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Fees and Expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Public Announcements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Collective Bargaining Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

No Solicitation of Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Closing ABX Air Balance Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Conditions to the Merger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Termination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

Effect of Termination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Termination Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Amendment/Waivers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Assignment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Performance Guaranty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

THE SEPARATION AGREEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

Structure of the Transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

ABX Air Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

Transferred Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Balance Sheet Adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Trademark License . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Software License . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Indemnification and Mutual Release . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

Dispute Resolution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

OTHER ANCILLARY AGREEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Employee Matters Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Global Transportation Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

Tax Sharing Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

COMMERCIAL AGREEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

ACMI Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

Hub Services Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

Promissory Note . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Transition Services Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

Sublease . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

DIVIDEND POLICY OF ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

iii

TABLE OF CONTENTS(continued)

Page

CAPITALIZATION OF ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA OF ABX AIR . . . . . . . . . . . . . . . . . . 96

PRO FORMA CONSOLIDATED FINANCIAL DATA OF ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

ABX AIR’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION ANDRESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

ABX AIR’S QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK . . . . . . 115

ABX AIR’S BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

Markets, Products and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

Aircraft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

Strategy and Competitive Strengths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

Customers and Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

Competition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

Intellectual Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

Information Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

Environmental . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

Security and Safety . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

ABX AIR MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Compensation of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Committees of the ABX Air Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

Option Grants in 2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Aggregate Option Exercises in 2002 and Year-End Option Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Change in Control Severance Benefits and Retention Arrangements . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Limitation of Liability of Directors and Indemnification of Directors and Officers . . . . . . . . . . . . . . . 134

Compensation Committee Interlocks and Insider Participation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

OWNERSHIP OF ABX AIR’S COMMON STOCK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

DESCRIPTION OF CAPITAL STOCK OF ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

Authorized Capital Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

Common Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

iv

TABLE OF CONTENTS(continued)

Page

Preferred Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

Series A Junior Participating Preferred Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

Limitation on Voting by Foreign Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

Anti-Takeover Effects of Provisions of ABX Air’s Certificate of Incorporation and Bylaws . . . . . . . . 140

Anti-Takeover Effects of Section 203 of the Delaware General Corporation Law . . . . . . . . . . . . . . . . 141

Authorized but Unissued Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

Transfer Agent and Registrar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

Shares in Book-Entry Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

Listing and Trading of ABX Air Common Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

MATERIAL DIFFERENCES IN THE RIGHTS OF AIRBORNE STOCKHOLDERS AND ABX AIRSTOCKHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

ISSUANCE OF SHARES UPON CONVERSION OF AIRBORNE CONVERTIBLE SENIOR NOTES . . 146

PROPOSAL 3—SUPERMAJORITY VOTING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

PROPOSAL 4—APPROVAL OF ABX AIR RIGHTS AGREEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

PROPOSAL 5—ELECTION OF DIRECTORS OF AIRBORNE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

AIRBORNE’S BOARD OF DIRECTORS AND COMMITTEES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Board of Directors Committees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Director Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

AIRBORNE’S BENEFICIAL STOCK OWNERSHIP TABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

AIRBORNE EXECUTIVE COMPENSATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 156

Summary Compensation Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 156

Option Grants in 2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

Aggregate Option Exercises in 2002 and Year-End Option Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

Comparative Performance Graph . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158

Compensation Committee Report on Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158

Audit Committee Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

Retirement Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

Change in Control Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161

AIRBORNE’S INDEPENDENT AUDITORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Principal Accountant Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

AIRBORNE STOCKHOLDER PROPOSALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

PROPOSAL 6—STOCKHOLDER PROPOSAL—POISON PILLS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

PROPOSAL 7—STOCKHOLDER PROPOSAL—NON-EXECUTIVE CHAIRMAN OF THE BOARD . . . 166

PROPOSAL 8—STOCKHOLDER PROPOSAL—REGARDING INDEXED STOCK OPTIONS . . . . . . . 168

PROPOSAL 9—STOCKHOLDER PROPOSAL—REGARDING EXPENSING OF STOCK OPTIONS . . . 170

v

TABLE OF CONTENTS(continued)

Page

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE OF AIRBORNE . . . . . . . . . 173

STOCKHOLDER PROPOSALS FOR AIRBORNE’S 2004 ANNUAL MEETING . . . . . . . . . . . . . . . . . . . 173

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173

EXPERTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173

OTHER MATTERS AND INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

Non-GAAP Financial Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

Where You Can Find More Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174

CONSOLIDATED FINANCIAL STATEMENTS OF ABX AIR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

APPENDICES

APPENDIX A—AGREEMENT AND PLAN OF MERGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

APPENDIX B—MASTER SEPARATION AGREEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B-1

APPENDIX C—OPINION OF GOLDMAN, SACHS & CO. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C-1

APPENDIX D—DELAWARE CODE SECTION 262 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . D-1

vi

QUESTIONS AND ANSWERS ABOUT THE MERGERAND THE SEPARATION

Q: What is happening in the proposed transaction?

A: This transaction is comprised of the following steps which will take place virtually simultaneously:(1) Airborne, Inc.’s (“Airborne”) air operations will be separated from its ground operations, with the airoperations being retained by ABX Air, Inc. (“ABX Air”); (2) DHL Worldwide Express B.V. (“DHL”) willacquire Airborne’s ground operations (including all operations conducted by Airborne Express, Inc.(“AEI”), including its customer relationships, pick up and delivery network and all related sales, marketingand administrative services) through a merger of Atlantis Acquisition Corporation, an indirect, wholly-owned subsidiary of DHL (“Atlantis Acquisition”), with and into Airborne; and (3) Airborne stockholderswill receive $21.25 in cash and one share of common stock of ABX Air per share of Airborne commonstock. Immediately following the closing of the transaction, Airborne will be an indirect, wholly-ownedsubsidiary of DHL (but may subsequently be merged with another wholly-owned subsidiary of DHL) andABX Air will become an independent public company wholly-owned by Airborne’s former stockholders.ABX Air will also enter into a number of commercial agreements with Airborne, which will be a wholly-owned indirect subsidiary of DHL immediately after the merger, including an ACMI service agreement(the “ACMI agreement”) and a hub and line-haul services agreement (the “hub services agreement”).

Q: What will I receive for my shares if the merger and the separation are completed?

A: If the merger is completed, and you have not exercised your right to an appraisal of the value of your shares,you will receive a cash payment of $21.25 and one share of common stock of ABX Air for each share ofAirborne’s common stock that you own at the time of the merger. Under certain limited circumstancesdescribed below, you will receive a cash payment of $21.65 for each share of common stock that you own atthe time of the merger and you will not receive a share of common stock of ABX Air (referred to as the“alternative merger consideration”). The alternative merger consideration will be paid if (1) a court orderblocking the transaction or other legal prohibition has been obtained by the U.S. Department ofTransportation (the “DOT”) or otherwise arises under Title 49 of the United States Code, and the paymentof the alternative merger consideration, among other things, would be sufficient to remove the legalprohibition, or (2) after the mailing of this proxy statement/prospectus, the parties to the merger agreementmutually so agree.

Q: What will happen to my stock options if the merger and the separation are completed?

A: The holders of stock options (whether or not vested or exercisable) will be entitled to receive (1) from DHL,an amount in cash (net of any applicable withholding taxes) equal to the product of (a) the number of sharesof Airborne common stock previously subject to the Airborne stock option and (b) the excess of the pershare amount of cash to be paid in the merger over the exercise price per share of Airborne common stockpreviously subject to the Airborne stock option, and (2) if any shares of ABX Air common stock are beingissued as part of the merger consideration, one share of ABX Air common stock for each share of Airbornecommon stock previously subject to such holder’s Airborne stock options. Any stock option with anexercise price per share of Airborne common stock that is equal to or greater than the per share amount ofcash to be paid in the merger will be cancelled in full without any cash payment or ABX Air stockconsideration. After the merger, all Airborne stock options will be cancelled in full and no Airborne stockoptions will be exercisable, whether for shares of Airborne common stock, shares of ABX Air commonstock or shares of DHL common stock.

Q: Will the separation occur even if the merger agreement is not adopted?

A: No.

1

Q: When will the proposed merger and the separation occur?

A: The parties are working toward completing the merger and separation as quickly as possible. The mergerand separation are expected to be completed in the third quarter of 2003. If Airborne’s stockholders vote toadopt the merger agreement, the alternative merger consideration, the ABX Air supermajority votingprovision and the ABX Air rights agreement, and the other conditions to the merger are satisfied or waived,the separation will occur immediately prior to the completion of the merger. The separation will occur onlyif the merger occurs. If any of the conditions to consummation of the merger are not satisfied or waived, theseparation will be delayed or may not occur. If the alternative merger consideration is paid by DHL, themerger will occur but the separation contemplated by the merger agreement will not.

Q: What are the United States federal income tax consequences of the merger and the separation tostockholders?

A: It is expected that each stockholder will recognize capital gain or loss, equal, in each case, to the differencebetween (1) the sum of (a) the fair market value of the shares of ABX Air received in the merger and (b) thecash proceeds received pursuant to the merger and (2) the stockholder’s adjusted tax basis in Airborne’scommon stock surrendered in exchange therefor. Because the tax consequences of the separation and themerger are complex and may vary depending on your particular circumstances, you are advised to consultyour tax advisor concerning the federal (and any state, local or foreign) tax consequences to you of theseparation and the merger. If you acquired ABX Air stock in connection with any stock option, you aresubject to special rules.

Q: In determining whether I recognize a capital gain or loss, how do I determine the fair market value of ABXAir?

A: The fair market value of the ABX Air common stock will be determined by the best available evidence as toits value at the effective time of the merger. You should consult with your own tax advisor with respect toyour particular circumstances concerning taking a tax return position consistent with such reporting.

Q: Do I have appraisal rights?

A: Yes. If you make a written demand for appraisal of your shares prior to the vote at the annual meeting, donot vote in favor of adoption of the merger agreement, the alternative merger consideration, the ABX Airsupermajority voting provision and the ABX Air rights agreement, continue to hold your shares of recordthrough the date of the merger and otherwise follow the procedural requirements of the Delaware GeneralCorporation Law, you will be entitled to have your shares appraised by the Delaware Court of Chancery andreceive the fair value of your shares, as determined by the Court, in cash. See “The Merger—AppraisalRights.”

Q: Other than stockholder adoption, what are the material conditions to completing the merger?

A: Among other matters, completion of the merger requires receipt of necessary regulatory approvals. See “TheMerger—Regulatory Requirements.”

Q: What if the merger and the separation are not completed?

A: It is possible the merger and the separation will not be completed. That might happen if, for example,Airborne’s stockholders do not adopt the merger agreement, the alternative merger consideration, the ABXAir supermajority voting provision and the ABX Air rights agreement. Should that occur, neither DHL norany third party is under any obligation to make or consider any alternative proposals regarding the purchaseof the shares of Airborne’s common stock.

2

Q: How can I find more information about ABX Air?

A: A description of ABX Air and the common stock of ABX Air is being provided to you in this proxystatement/prospectus. You are urged to read the proxy statement/prospectus carefully, including the riskfactors beginning on page 30.

Q: Why is ABX Air separating from Airborne?

A: The merger agreement with DHL requires that Airborne separate its air operations from its groundoperations, with its air operations being retained by ABX Air. Under United States law, a U.S. air carriercannot be owned or controlled by a non-U.S. citizen or non-U.S. citizens. Airborne and ABX Air believethat the separation will result in compliance with this law because ABX Air will be owned by the formerstockholders of Airborne.

Q: Will Airborne have any ownership interest in ABX Air after the separation?

A: No. After the merger, Airborne will not own any ABX Air common stock, nor will Airborne have the powerto appoint directors to the Board of Directors of ABX Air.

Q: Will ABX Air and Airborne have any continuing commercial or other agreements after the separation?

A: Yes. The following agreements between Airborne and ABX Air will be effective from and after theseparation date:

• a separation agreement, which provides for the separation and governs various relationships andcircumstances that may arise between Airborne and ABX Air after the separation;

• a tax sharing agreement, which allocates responsibilities and liabilities for pre-separation tax mattersbetween Airborne and ABX Air;

• an employee matters agreement, which allocates responsibilities and liabilities for pre-separationemployee matters between Airborne and ABX Air;

• a transition services agreement, which provides for Airborne to temporarily provide ABX Air with certainadministrative and support services;

• an ACMI agreement under which ABX Air will provide air cargo transportation services to Airborne on acost plus basis;

• a hub services agreement under which ABX Air will provide staff to Airborne to conduct hub, line-hauland equipment and facilities maintenance services on a cost plus basis;

• a sublease, under which ABX Air will sublease a portion of the Wilmington Air Park airport fromAirborne and will have the right to use certain common use facilities.

Q: What is ABX Air’s dividend policy?

A: The payment of dividends by ABX Air after the separation will be subject to the discretion of the ABX AirBoard of Directors. Under the terms of the one or more promissory notes to be issued to DHL Holdings,ABX Air will be restricted from making annual cash dividends in excess of $1 million.

Q: How will ABX Air common stock trade?

A: There is no established public trading market for ABX Air common stock. Immediately following theconsummation of the merger, ABX Air common stock will not trade on a national exchange or NASDAQ.

3

ABX Air expects that the ABX Air common stock may be traded on the OTC Bulletin Board or itssuccessor. ABX Air expects trading in ABX Air common stock to commence on the effective date of themerger.

Q: If my stock is not listed on a National Exchange, how can I trade shares of ABX Air?

A: In order to trade shares of ABX Air, you will need to contact a stock broker and inform the broker that youdesire to buy or sell the stock. The stock broker is required by securities law to search out the best price atwhich your shares may be sold by contacting the registered market maker(s) for ABX Air shares, if any.

Q: How will I receive my ABX Air common stock?

A: Promptly after the effective time of the merger, the exchange agent will send the Airborne stockholders aletter of transmittal and instructions explaining how to send their Airborne stock certificates to the exchangeagent. Promptly following the exchange agent’s receipt and processing of the Airborne common stockcertificates and properly completed transmittal documents, the exchange agent will (1) mail checks for theappropriate cash merger consideration, minus any withholding taxes required by law, and (2) register yourownership interest in the shares of ABX Air common stock in uncertificated shares in book-entry formthrough the direct registration system with the registrar. Your book-entry shares will be held with ABXAir’s transfer agent and registrar, National City Bank, which will serve as the official record keeper for theABX Air common stock. Under the direct registration system, instead of receiving stock certificates, youwill receive an account statement reflecting your ownership interest in shares of ABX Air common stock. Ifat any time you want to receive a physical certificate evidencing your shares of ABX Air common stock,you may do so by contacting ABX Air’s transfer agent and registrar.

Q: Should I send in my stock certificates now?

A: No. If Airborne completes the merger, you will receive written instructions for exchanging your Airbornestock certificates for your cash payment and shares of ABX Air common stock.

Q: Who will be the exchange agent, transfer agent and registrar for the ABX Air common stock?

A: Bank of New York, which is the registrar and transfer agent for Airborne common stock, will be theexchange agent for the ABX Air common stock. You may contact Bank of New York by telephone at1-800-507-9357 or by mail at 101 Barclay Street, New York, NY 10286. National City Bank will be thetransfer agent and registrar for the ABX Air common stock. You may contact National City Bank bytelephone at 1-800-622-6757 or by mail at Corporate Trust Operations, Dept. 5252, P.O. Box 92301,Cleveland, Ohio 44193-0900.

Q: Where are the principal executive offices of ABX Air?

A: 145 Hunter Drive, Wilmington, Ohio 45177Telephone (937) 382-5591

4

QUESTIONS AND ANSWERS ABOUT THESTOCKHOLDERS MEETING

Q: When and where is the annual meeting?

A: The annual meeting will take place on August 14, 2003, at 10:00 a.m., local time, at The Westin Hotel,1900 Fifth Avenue, Seattle, Washington.

Q: What specifically am I being asked to vote on?

A: You are being asked to vote on whether to adopt the merger agreement, to approve the alternative mergerconsideration, to approve the ABX Air supermajority voting provision and to approve the ABX Air rightsagreement, to elect two directors for terms of three years and on various stockholder proposals that aredescribed herein.

Q: How does the Board of Directors recommend that I vote?

A: Merger Proposal (No. 1). After considering a number of factors, including the opinion of Airborne’sfinancial advisor, Goldman, Sachs & Co. (“Goldman Sachs”), Airborne’s Board of Directors unanimouslybelieves that the terms of the merger agreement are fair to and in the best interests of Airborne’sstockholders. The Board of Directors recommends a vote FOR the merger proposal.

Alternative Merger Consideration (No. 2). The Board of Directors recommends a vote FOR the alternativemerger consideration of $21.65.

ABX Air Supermajority Voting Provision (No. 3). The Board of Directors recommends a vote FOR theABX Air supermajority voting provision.

ABX Air Rights Agreement (No. 4). The Board of Directors recommends a vote FOR the ABX Air rightsagreement.

Although proposals 1, 2, 3, and 4 above are separate matters to be voted upon by you, these proposalsare expressly conditioned upon the approval of the others. This means that you must approveproposals 1, 2, 3, and 4 if you wish to approve the merger.

Election of Directors (No. 5). The Board of Directors recommends a vote FOR each of the nominees.

Stockholder Proposals (Nos. 6 through 9). The Board of Directors recommends a vote AGAINST each ofthe various stockholder proposals.

Q: What is the vote required to adopt the merger agreement and other proposals?

A: In accordance with Delaware law and Airborne’s amended and restated certificate of incorporation, therequired vote to adopt the merger agreement, the alternative merger consideration, the ABX Airsupermajority voting provision and the ABX Air rights agreement is the affirmative vote of a majority of theoutstanding shares of Airborne’s common stock entitled to vote on these proposals. This means that theaffirmative vote of at least 24,426,496 shares of common stock is required for adoption of the mergeragreement, the alternative merger consideration, the ABX Air supermajority voting provision and the ABXAir rights agreement. To elect directors, the two candidates for director who receive the most votes willbecome directors of Airborne. To approve a stockholder proposal, a majority of the shares represented at themeeting, either in person or by proxy, must be voted in favor of the stockholder proposal. Each share ofcommon stock is entitled to one vote.

Q: What do I need to do now?

A: You are urged to read this proxy statement/prospectus carefully (including its appendices), consider how themerger would affect you as a stockholder, and vote. After you read this proxy statement/prospectus, you

5

should complete, sign and date your proxy card and mail it in the enclosed return envelope as soon aspossible, even if you plan to attend the annual meeting in person, so that your shares may be represented atthe annual meeting. If you hold your shares in your own name as a holder of record, you may vote bytelephone by calling the toll free number listed on the accompanying proxy card. Telephone voting isavailable 24 hours a day until 5:00 P.M. Seattle time on August 13, 2003. You also have the option to votevia the Internet. The website for Internet voting is printed on your proxy card. Internet voting is available24 hours a day until 5:00 P.M. Seattle time on August 13, 2003. If you vote by telephone or via the Internet,you do not need to return your proxy card.

Q: If my shares are held in “street name” by my broker, will my broker vote my shares for me?

A: Your broker will only be permitted to vote your shares on the proposal for the adoption of the mergeragreement, approval of the alternative merger consideration, approval of the ABX Air supermajority votingprovision and approval of the ABX Air rights agreement if you provide instructions to your broker on how tovote. You should follow the procedures provided by your broker regarding the voting of your shares and besure to provide your broker with instructions on how to vote your shares. If you do not give voting instructionsto your broker, you will, in effect, be voting against the adoption of the merger agreement, the alternativemerger consideration, the ABX Air supermajority voting provision and the ABX Air rights agreement.Notwithstanding the foregoing, under the rules of the New York Stock Exchange in effect at the time of thisproxy statement/prospectus, your broker is permitted to vote your shares on the election of directors, even ifthe broker does not receive instructions from you. Your broker, however, is not permitted to vote your shareswith respect to the stockholder proposals. Your broker will provide you with directions on voting your shares,and you should instruct your broker to vote your shares according to those instructions.

Q: What if I want to change my vote after I have mailed my signed proxy card or voted by telephone or theInternet?

A: You can change your vote by sending in a later-dated, signed proxy card or a written revocation toAirborne’s Secretary at 3101 Western Avenue, P.O. Box 662, Seattle, Washington 98111, who must receiveit before your proxy has been voted at the annual meeting, or by attending the annual meeting in person andvoting. If you voted by telephone or the Internet, you may revoke your vote in the same manner prior to5:00 P.M. Seattle time on August 13, 2003. Your attendance at the annual meeting will not, by itself, revokeyour proxy. If you have instructed a broker to vote your shares, you must follow the directions receivedfrom your broker to change those voting instructions.

Q: What happens if I do not vote my proxy, if I do not instruct my broker to vote my shares or if I abstain fromvoting with respect to any proposal?

A: If you do not vote your proxy, do not instruct your broker to vote your shares, or abstain from voting withrespect to the merger proposal, the alternative merger consideration, the ABX Air supermajority votingprovision or the ABX Air rights agreement, it will have the same effect as a vote against the adoption of themerger. Shares of common stock represented by properly executed proxies for which no instruction is givenon the proxy card will be voted “FOR” the adoption of the merger agreement, “FOR” the alternative mergerconsideration, “FOR” the ABX Air supermajority voting provision, “FOR” the ABX Air rights agreement,“FOR” the election of the two directors and “AGAINST” each of the stockholder proposals.

Q: Who can help answer my questions?

A: If you have more questions about the merger or the separation, or if you would like additional copies of thisproxy statement/prospectus or the proxy card, you should call Airborne’s proxy solicitors, GeorgesonShareholder Communications, Inc., toll-free at (888) 897-5991.

6

FORWARD-LOOKING STATEMENTS

Certain information contained in, or incorporated by reference in, this proxy statement/prospectus should beconsidered “forward-looking statements” and are identified by the use of forward-looking words and phrases,such as “estimates,” “plans,” “expects,” “to continue,” “subject to,” “target” and such other similar phrases.These forward-looking statements are based on Airborne’s current expectations.

Because forward-looking statements involve risks and uncertainties, Airborne’s plans, actions and actualresults could differ materially. Among the factors that could cause Airborne’s plans, actions and results to differmaterially from current expectations are:

• gaining regulatory and stockholder approval to complete the merger and separation,

• the possibility that the merger and separation may not be completed,

• legislative or regulatory developments that could have the effect of delaying or preventing the merger,

• the possibility that the companies may be required to modify aspects of the merger or separation toachieve regulatory approval,

• domestic and international economic conditions,

• the impact of war and terrorism on the package delivery business,

• the ability to mitigate volatile fuel costs,

• competitive pressure,

• maintaining customer relationships,

• cost cutting initiatives,

• improving operating margins and productivity,

• realignment and overhead reduction efforts,

• changes in customers’ shipping patterns,

• the ability to make planned capital expenditures,

• the ability to react to changes in economic conditions, and

• risks and uncertainties that are described in the reports that Airborne has filed with the Securities andExchange Commission (“SEC”), including Airborne’s Annual Report on Form 10-K for the fiscal yearended December 31, 2002, as amended by the Form 10-K/A filed on April 29, 2003, and the Form 8-Kfiled by Airborne on April 4, 2003.

This proxy statement/prospectus also contains forward-looking statements that are based on currentexpectations, estimates, forecasts, and projections about ABX Air’s business and the industry in which ABX Airoperates, and management’s beliefs and assumptions. Such statements include, in particular, statements about itsplans, strategies, and prospects under the headings “Summary,” “Risk Factors,” “Capitalization,” “Pro FormaConsolidated Financial Data,” “Selected Historical Financial Data,” “Management’s Discussion and Analysis ofFinancial Condition and Results of Operations,” “Management,” “Ownership of ABX Air Common Stock,”“Dividend Policy” and “Business.” Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,”“seeks,” “estimates,” variations of such words, and similar expressions are intended to identify such forward-looking statements.

These forward-looking statements are not guarantees of future performance and are based on a number ofassumptions and estimates that are inherently subject to significant risks and uncertainties, many of which arebeyond ABX Air’s control, cannot be foreseen, and reflect future business decisions that are subject to change.

7

Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in suchforward-looking statements. There are a number of important factors that could cause actual results to differmaterially from those anticipated by any forward-looking information, including, but are not limited to:

• the ability of ABX Air to operate successfully as an independent company;

• early termination of the ACMI agreement or the hub services agreement;

• changes in customer demand and prices resulting in a negative impact on revenues and margins;

• increases in the costs of labor and unreimbursed costs under the ACMI agreement and hub servicesagreement;

• increased competition in ABX Air’s product lines and its ability to develop new products;

• changes in capital availability or costs and ABX Air’s ability to execute capital programs;

• workforce factors such as strikes or labor interruptions;

• the cost of compliance with applicable governmental regulations and laws, and changes in suchregulations, including aviation and environmental regulations, and laws;

• the general political, economic and competitive conditions in markets where ABX Air operates;

• the timing and occurrence (or non-occurrence) of transactions and events which may be subject tocircumstances beyond ABX Air’s control;

• the impact of war and terrorism on the air cargo business;

• maintaining customer relationships;

• ABX Air’s ability to gain additional business;

• risks associated with maintaining a fleet of aircraft; and

• the trading liquidity of ABX Air common stock, as well as other matters discussed under the heading“Risk Factors.”

ABX Air cautions that the factors described above are not all inclusive. All of the forward-lookingstatements made in this proxy statement/prospectus are qualified by this cautionary statement, and readers arecautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of thisproxy statement/prospectus. Except as required under the federal securities laws and the rules and regulations ofthe Securities and Exchange Commission, ABX Air does not have any intention or obligation to update publiclyany forward-looking statements after ABX Air distributes this proxy statement/prospectus, whether as a result ofnew information, future events or otherwise.

8

SUMMARY

This summary, together with the question and answer section, highlights important information discussed ingreater detail elsewhere in this proxy statement/prospectus. This summary may not contain all of the informationyou should consider before voting on the merger agreement, the alternative merger consideration, the ABX Airsupermajority voting provision and the ABX Air rights agreement. To more fully understand the merger and theseparation, you should read carefully this entire proxy statement/prospectus and all of its appendices, includingthe merger agreement and the separation agreement, before voting on whether to adopt the merger agreement, thealternative merger consideration, the ABX Air supermajority voting provision and the ABX Air rightsagreement. You may also refer to “Other Matters and Information—Where You Can Find More Information” onpage 174 for additional information about Airborne.

THE ANNUALMEETING (PAGE 39)

Date, Time and Place (page 39).

The annual meeting will take place on August 14, 2003, at 10:00 a.m., local time, at The Westin Hotel, 1900Fifth Avenue, Seattle, Washington.

Vote Required (page 40).

In order for the merger agreement to be adopted, the holders of a majority of Airborne’s outstanding commonstock entitled to vote at the annual meeting must vote “FOR” its adoption, “FOR” the alternative mergerconsideration, “FOR” the ABX Air supermajority voting provision and “FOR” the ABX Air rights agreement.Although the proposal to adopt the merger agreement, the proposal to approve the alternative mergerconsideration, the proposal to approve the ABX Air supermajority voting provision and the proposal to approvethe ABX Air rights agreement are separate matters to be voted upon by you, each proposal is expresslyconditioned upon the approval of the others. This means that you must approve all four proposals if you wish toapprove the merger. To elect directors, the two candidates for director who receive the most votes will becomedirectors of Airborne. To approve a stockholder proposal, a majority of the shares represented at the meeting,either in person or by proxy, must be voted in favor of the stockholder proposal. Each share of common stock isentitled to one vote.

Record Date (page 39).

The record date for determining the holders of shares of Airborne’s outstanding common stock entitled to vote atthe annual meeting is July 8, 2003. On the record date, 48,852,991 shares of Airborne’s common stock wereoutstanding and entitled to vote.

Proxies (page 40).

Shares of common stock represented by properly executed proxies received at or prior to the annual meeting thathave not been revoked will be voted at the annual meeting in accordance with the instructions indicated on theproxies. Shares of common stock represented by properly executed proxies for which no instruction is given onthe proxy card will be voted “FOR” the adoption of the merger agreement, “FOR” the alternative mergerconsideration, “FOR” the ABX Air supermajority voting provision, “FOR” the ABX Air rights agreement,“FOR” the election of the two directors and “AGAINST” each of the stockholder proposals. Your proxy may berevoked at any time before it is voted.

9

PROCEDURE FOR VOTING (PAGE 40).

You may vote in any of the following ways:

• by completing and returning the enclosed proxy card,

• by telephoning the toll free number listed on the enclosed proxy card,

• by Internet voting by visiting the website printed on the enclosed proxy card, or

• at the annual meeting.

If you complete and return the enclosed proxy card, but wish to revoke it, you must either file withAirborne’s Secretary a written, later-dated notice of revocation, send a later-dated proxy card relating to the sameshares to the Secretary at or before the annual meeting, attend the annual meeting and vote in person, or if youvoted by telephone or the Internet, you may revoke your vote in the same manner prior to 5:00 P.M. Seattle timeon August 13, 2003. Please note that your attendance at the meeting will not, by itself, revoke your proxy.

THE PARTIES

Airborne, Inc.3101 Western AvenueP.O. Box 662Seattle, Washington 98111(206) 285-4600

Airborne, a Delaware corporation formed in 1999, is a holding company operating through its subsidiariesas an air express company and air freight forwarder. Airborne expedites shipments of all sizes to destinationsthroughout the United States and most foreign countries. Airborne’s wholly-owned operating subsidiaries includeAEI, Sky Courier, Inc. (“Sky Courier”) and ABX Air. AEI provides domestic and international delivery servicesin addition to customer service, sales and marketing activities. Sky Courier provides delivery service on anexpedited basis. ABX Air provides air cargo transportation and other support services for AEI and otherbusinesses in the air cargo transportation industry. AEI and Sky Courier will remain subsidiaries of Airbornefollowing the merger. As a result of the merger and separation, ABX Air will become an independent publiccompany wholly-owned by Airborne’s former stockholders. ABX Air will continue to provide services toAirborne following the merger and separation pursuant to the ACMI agreement and the hub services agreement.You can refer to “Commercial Agreements” on page 85 of this proxy statement/prospectus for additionalinformation about these agreements.

DHL Worldwide Express B.V.c/o DHL InternationalGlobal Coordination Centre, De Kleetaan11831 Diegem, Belgium

10

DHL, a company organized and existing under the laws of the Netherlands, is a leading express and logisticscompany which, together with its subsidiaries and affiliates, offers customers innovative and customizedsolutions from a single source. With global expertise in solutions, express, air and ocean freight and overlandtransport, DHL combines worldwide coverage with an in-depth understanding of local markets. DHL’sinternational network links over 120,000 destinations in more than 220 countries and territories. DHL is wholly-owned by Deutsche Post World Net.

Atlantis Acquisition Corporationc/o DHL InternationalGlobal Coordination Centre, De Kleetaan11831 Diegem, Belgium

Atlantis Acquisition, a Delaware corporation and an indirect, wholly-owned subsidiary of DHL, was formedsolely for the purpose of facilitating the merger. If and when the merger takes place, Atlantis Acquisition will bemerged with and into Airborne and Airborne will become an indirect, wholly-owned subsidiary of DHL.

BACKGROUND OF THE MERGER (PAGE 42)

For a description of events leading to the approval of the merger agreement by Airborne’s Board ofDirectors, and the reasons for such approval, you should refer to “The Merger—Background of the Merger.”

FORM OF MERGER

Subject to the terms and conditions of the merger agreement and in accordance with Delaware law, at theeffective time of the merger, Atlantis Acquisition, an indirect, wholly-owned subsidiary of DHL, will merge withand into Airborne and Airborne will survive the merger as an indirect, wholly-owned subsidiary of DHL.

The merger will occur subject to the terms and conditions of the merger agreement, which is attached asAppendix A to this proxy statement/prospectus. You should read carefully the merger agreement and thedescription of the merger agreement contained in this proxy statement/prospectus under “The MergerAgreement.” The merger and the separation are expected to be completed during the third quarter of 2003.

MERGER CONSIDERATION (PAGE 65)

In the merger, you will receive $21.25 in cash and one share of common stock of ABX Air for each share ofAirborne common stock you own at the time of the merger. Under certain limited circumstances describedbelow, you will instead receive a cash payment of $21.65 for each share of Airborne common stock and you willnot receive stock of ABX Air (referred to as the “alternative merger consideration”). The alternative mergerconsideration will be paid if (1) a court order blocking the merger or other legal prohibition has been obtained bythe DOT or otherwise arises under Title 49 of the United States Code, and the payment of the alternative mergerconsideration, among other things, would be sufficient to remove the legal prohibition, or (2) after the mailing ofthis proxy statement/prospectus the parties to the merger agreement mutually so agree.

The holders of stock options (whether or not vested or exercisable) will be entitled to receive (1) from DHL,an amount in cash (net of any applicable withholding taxes) equal to the product of (a) the number of shares ofAirborne common stock previously subject to the Airborne stock option and (b) the excess of the per shareamount of cash to be paid in the merger over the exercise price per share of Airborne common stock previouslysubject to the Airborne stock option, and (2) if any shares of ABX Air common stock are being issued as part ofthe merger consideration, one share of ABX Air common stock for each share of Airborne common stockpreviously subject to such holder’s Airborne stock options. Any stock option with an exercise price per share of

11

Airborne common stock that is equal to or greater than the per share amount of cash to be paid in the merger willbe cancelled in full without any cash payment or ABX Air stock consideration. After the merger, all Airbornestock options will be cancelled in full and no Airborne stock options will be exercisable, whether for shares ofAirborne common stock, shares of ABX Air common stock or shares of DHL common stock.

EFFECTS OF THE MERGER (PAGE 46)

If the merger agreement, the alternative merger consideration, the ABX Air supermajority voting provisionand the ABX Air rights agreement are approved by Airborne’s stockholders and if the other conditions to themerger are either satisfied or waived:

• you will receive the merger consideration described above under “Merger Consideration”;

• ABX Air will be separated from Airborne and will become an independent company wholly-owned byAirborne’s former stockholders;

• ABX Air will enter into a number of commercial agreements with Airborne, including the ACMIagreement and hub services agreement;

• Airborne will become an indirect, wholly-owned subsidiary of DHL;