accounting (professional) diploma - oilsia · the accounting professional diploma (apd) ... 4-...

TRANSCRIPT

Accounting (professional)

Diploma Study Plan

About the Diploma:The Accounting Professional Diploma (APD) is a one-year course leading to the Diploma in Accounting and Finance. The APD is designed for students with little or no previous knowledge of accounting and finance who wish to study these subjects further, or who wish to undertake postgraduate studies in accounting and finance but lack the depth of knowledge necessary to commence masters level study.

Learning Outcomes:In the APD program the student will:• Learn manual bookkeeping and accounting processes and how to prepare financial statements, budgets, and financial records• Learn to use computerized accounting software and gain keyboarding and basic computer skills• Gain essential administrative and support skills to ensure the smooth operation of any office• Develop written and oral business communications skillsAccounting Assistant Program PracticumAt the end of the program, students will participate in a 4-week practicum to gain valuable work experience before graduation.

Training methods:The lecture and explanation, working in groups, individual tasks, brainstorming, practical applications in classrooms, role-playing, enter the Accounting Assistant Program Practicum.

Diploma's period:270 training hours distributed on 30 weeks training, three days a week, three hours a day.Target Group:Anyone who wishes to become Business professional or non-graduates already employed in business and wishes to have a formal qualification in the discipline.

Expected Number of Participants: No more than 20 students.

Conditions of Participation:1. The participant should be at least 18 years’ old2. Participants interested in applying should already have a degree of general qualification for university entrance.3. Participants must be permanently residing in that same country where the program takes place and must have an official and a fixed address and must give his contact details correctly.4. Foreign nationals interested in applying must prove that they possess a valid residence in the country where the program takes place.5. Participants must be financially able to pay the feesof the program.Participants finished the APD program and theprofessional criteria mentioned above could participatein the professional master and doctorate degrees(provided that the participants fulfill the admission requirements)

The main lecturers Dr. Maher M. Attieh/ Accounting – The World Islamic Sciences & Education University – Supervisor, coordinator, and lecturer.Dr. Sulaiman Weshah/ Accounting - The World Islamic Sciences & Education University - lecturer.*Other lecturers will be identified later. The list of lecturers is canceled and updated according to the available data by the Institute and in accordance with the trainers' programs. Also, the Institute or its branches in other countries have the right to change and modify the list of coaches in proportion to the session, place, serving students, participants and according to criteria that operates internationally Institute.

Examinations:Two exams per session will be held for trainees:First exam: will be at the end of the program, as a written and oral exam and oral as part of a Committee composed of the faculty and administration.Final graduation exam: will be an online exam, which will be held at the end of the program. This exam is an international program in the Kingdom of Norway, under the general supervision of the institute and the lecturers. (The exam is entering over the Internet by the name and number of the student, under a time limit and specific questions which are answered online).The success rate is 75%, and it is decided by the committee which supervises the exams that is composedof the institute and the lecturers.The result of the exam is given after the completion of the exam, in a period not more than 48 working hour according to the Norwegian labor system.

Advantages of Participating:1- The participant will receive an international certificate of Oslo Institute, restricted assets in an international verification Code.2- The participant will receive an international student card in his study period.3- The student receive an international card after the completion of the study for a year (renewable after the payment of fees)4- The student gets his testimony authenticated by (The Norwegian Ministry of Justice, The Norwegian Ministry of Foreign Affairs, Embassy of The Hashemite Kingdom of Jordan in Brussels, and The Jordanian Ministry of Foreign Affairs)5- A student can request to ratify the testimony by the European Apostille but after paying an additional fee.6- The student receives an international verification code for him as a restricted student within the Institute records in the Kingdom of Norway, and he can check the data on the official website of the Institute on the Internet on the following link:7- A student can submit researches and studies for the Institute to be able to continue his scientific research grant from the Institute for high achievers and distinctive researches.8- The high achievers' students can register after graduation in order to be among the teaching staff of the Institute, and start an exclusive jurisdiction of courses for international coaches.

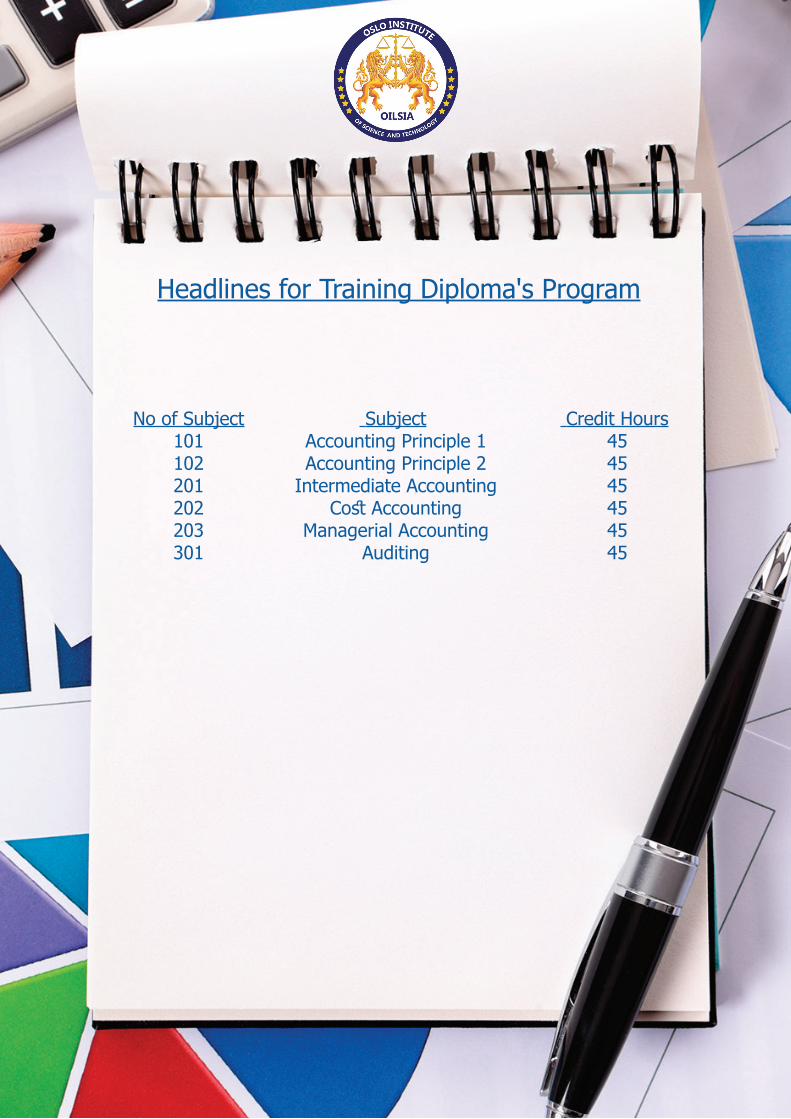

Headlines for Training Diploma's Program

No of Subject101102201202203301

Credit Hours454545454545

SubjectAccounting Principle 1

Accounting Principle 2 Intermediate Accounting Cost Accounting Managerial Accounting Auditing

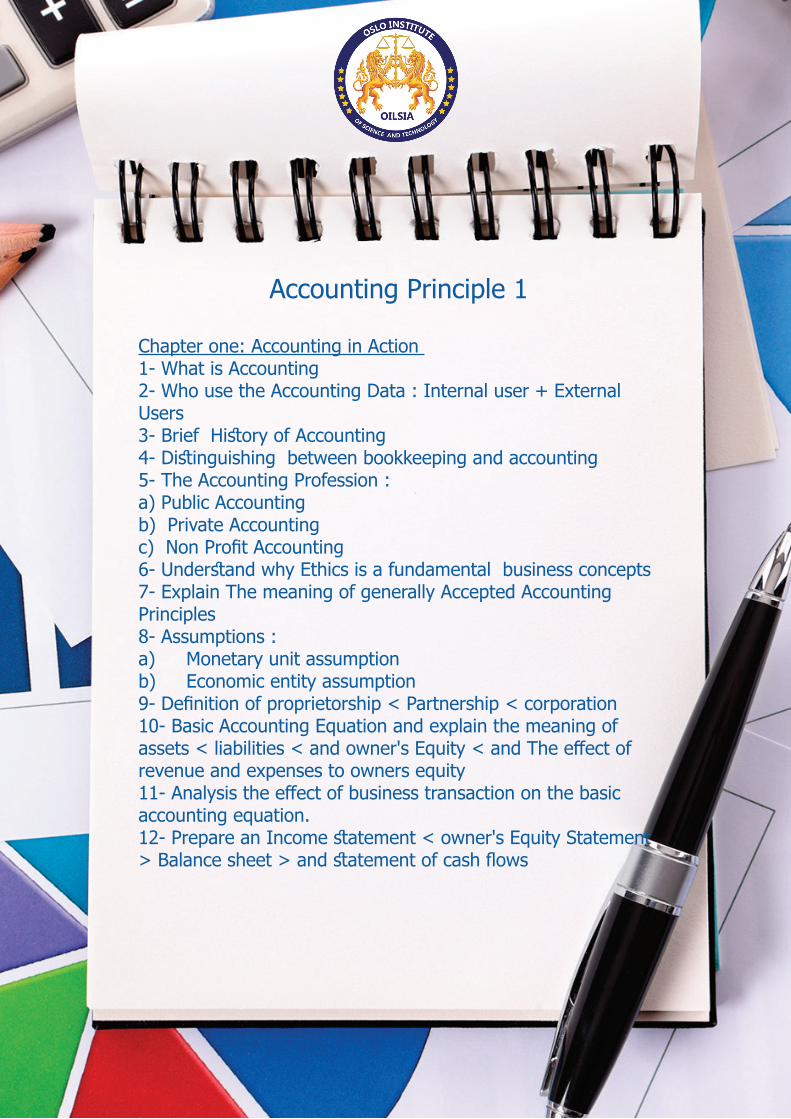

Accounting Principle 1

Chapter one: Accounting in Action 1- What is Accounting 2- Who use the Accounting Data : Internal user + External Users 3- Brief History of Accounting 4- Distinguishing between bookkeeping and accounting 5- The Accounting Profession : a) Public Accounting b) Private Accounting c) Non Profit Accounting 6- Understand why Ethics is a fundamental business concepts 7- Explain The meaning of generally Accepted Accounting Principles 8- Assumptions :a) Monetary unit assumptionb) Economic entity assumption 9- Definition of proprietorship < Partnership < corporation 10- Basic Accounting Equation and explain the meaning of assets < liabilities < and owner's Equity < and The effect of revenue and expenses to owners equity 11- Analysis the effect of business transaction on the basic accounting equation.12- Prepare an Income statement < owner's Equity Statement > Balance sheet > and statement of cash flows

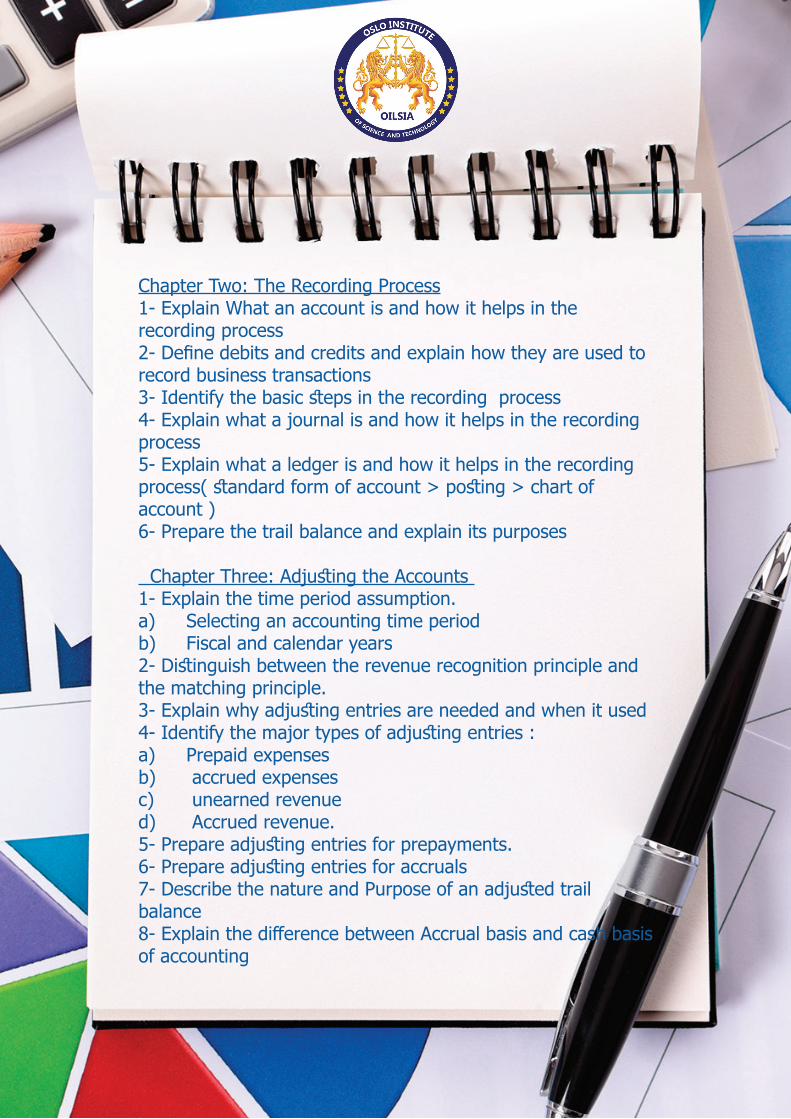

Chapter Two: The Recording Process1- Explain What an account is and how it helps in the recording process 2- Define debits and credits and explain how they are used to record business transactions3- Identify the basic steps in the recording process 4- Explain what a journal is and how it helps in the recording process5- Explain what a ledger is and how it helps in the recording process( standard form of account > posting > chart of account )6- Prepare the trail balance and explain its purposes Chapter Three: Adjusting the Accounts 1- Explain the time period assumption.a) Selecting an accounting time period b) Fiscal and calendar years2- Distinguish between the revenue recognition principle and the matching principle.3- Explain why adjusting entries are needed and when it used 4- Identify the major types of adjusting entries :a) Prepaid expensesb) accrued expenses c) unearned revenue d) Accrued revenue.5- Prepare adjusting entries for prepayments.6- Prepare adjusting entries for accruals 7- Describe the nature and Purpose of an adjusted trail balance 8- Explain the difference between Accrual basis and cash basis of accounting

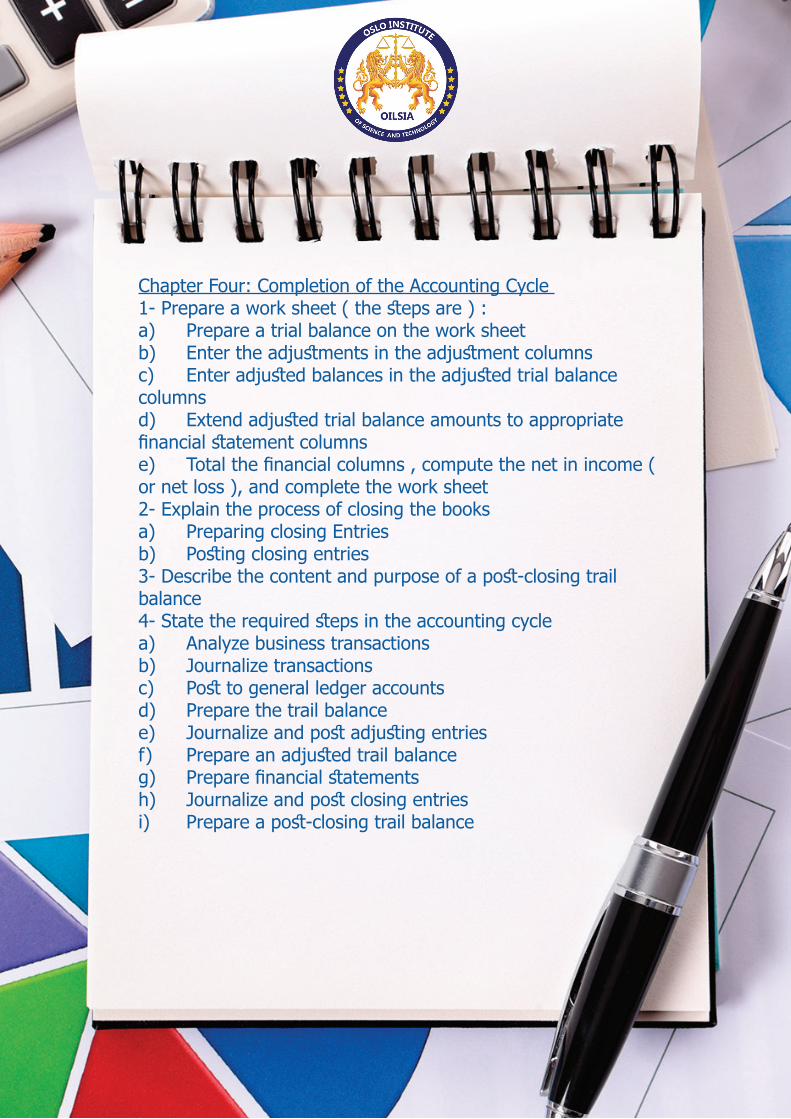

Chapter Four: Completion of the Accounting Cycle 1- Prepare a work sheet ( the steps are ) : a) Prepare a trial balance on the work sheet b) Enter the adjustments in the adjustment columns c) Enter adjusted balances in the adjusted trial balance columns d) Extend adjusted trial balance amounts to appropriate financial statement columns e) Total the financial columns , compute the net in income ( or net loss ), and complete the work sheet 2- Explain the process of closing the books a) Preparing closing Entries b) Posting closing entries 3- Describe the content and purpose of a post-closing trail balance 4- State the required steps in the accounting cycle a) Analyze business transactions b) Journalize transactions c) Post to general ledger accounts d) Prepare the trail balance e) Journalize and post adjusting entries f) Prepare an adjusted trail balance g) Prepare financial statements h) Journalize and post closing entries i) Prepare a post-closing trail balance

5- Explain the approaches to preparing correcting entriesa) Reversing entries – an optional step b) Correcting entries – an avoidable step6- Identify the sections of a classified balance sheeta) Assets :- Current assets - Long-term investments- Property , Plants , and Equipments- Intangible assets b) Liabilities : - Current liabilities - Long – term liabilities c) Owner's Equity

Chapter five: Accounting for merchandizing operations 1- Identifies the differences between a service enterprise and a merchandizing company 2- Explain the deference between the entries under perpetual inventory system and periodic inventory system for ( revenues and purchases)3- Explain the computation and importance of gross profit 4- Identify the features of the of income statement for merchandizing company.5- Distinguish between a multiple – step and a single step income statement

Chapter six: Accounting for Receivable:1- Identify the different types of receivablea) Accounts receivable b) Notes receivable c) Other receivable 2- Explain how account receivable are recognized in the accounts 3- Distinguish between the methods and bases used to value account receivable 4- Describe the entries to record the disposition of accounts receivable.5- Compute the maturity date of < and interest on < notes receivable.6- Describe how notes receivable are valued.7- Describe the entries to record the disposition of notes receivable 8- Explain the statement presentation and analysis of receivable

Chapter seven: Inventories:1- Describe the steps in determining inventory quantitiesa) Taking a physical inventory b) Determining ownership of goods 2- Prepare the entries for purchases and sales of inventory under :a) Periodic inventory system b) Perpetual inventory system3- Determine cost of goods sold under :a) Periodic inventory systemb) Perpetual inventory system

4- Identify the unique features of the income statement for Merchandizing Company using a periodic inventory system. 5- Explain the basis of accounting for inventories and describe the inventory cost flow methods.a) Using actual physical flow ( Costing – specific identification )b) Using assumed cost flow methods - FIFO - LIFO - Weighted average 6- Explain the financial statement and tax effects of each of the inventory cost flow methods.7- Explain the lower of cost or market bases of accounting for inventories 8- Indicate the effects of inventory errors on the financial statements.9- Compute and interpret the inventory turnover ratio.

Accounting Principle 2

Chapter one: Internal control and cash 1- Define internal control.2- Identify Principles of internal control :a) Establishment of responsibility b) Segregation of duties c) Documentation proceduresd) Physical , mechanical , and electronic control e) Independent internal verification 3- Explain the applications of internal control principles to cash receipt4- Explain the applications of internal control principles to cash disbursements 5- Explain the operation of a petty cash fund.6- Indicate the control feature of a bank account 7- Prepare a bank reconciliation statement. The content of statement are : a) Deposits in transit b) Outstanding checks c) Errors d) Bank memoranda like ( check charges , interest )8- Explain the reporting of cash.

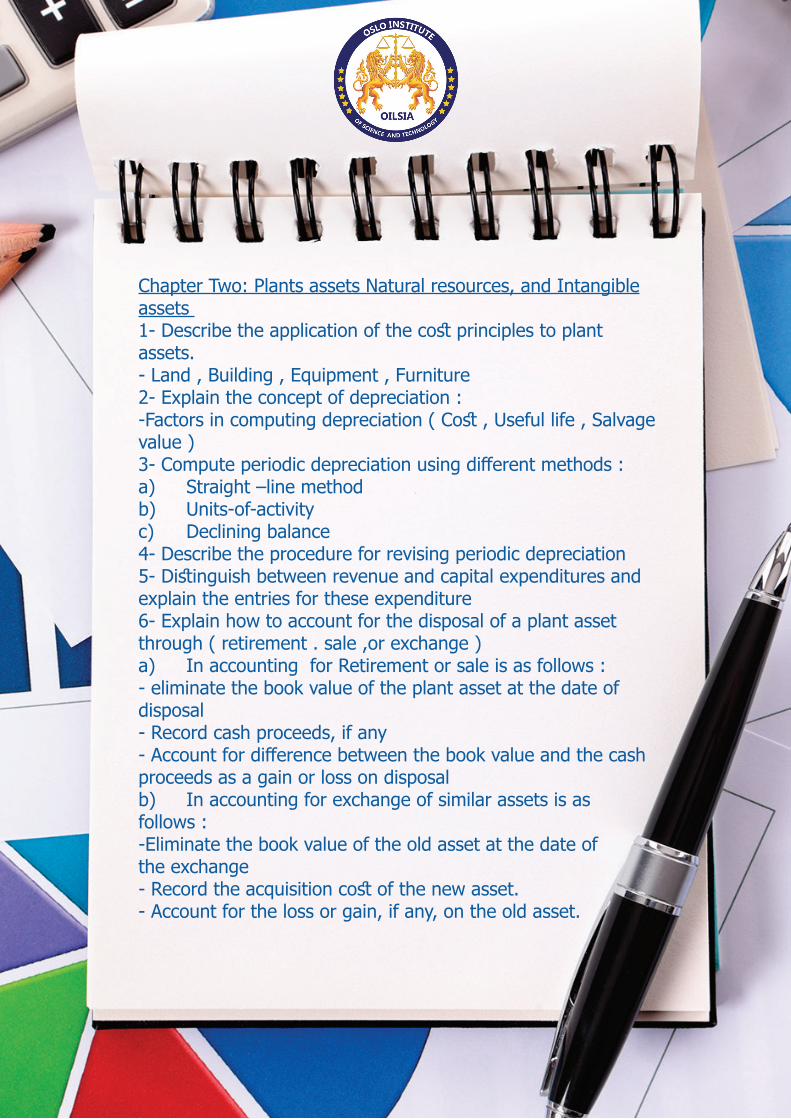

Chapter Two: Plants assets Natural resources, and Intangible assets 1- Describe the application of the cost principles to plant assets.- Land , Building , Equipment , Furniture 2- Explain the concept of depreciation : -Factors in computing depreciation ( Cost , Useful life , Salvage value )3- Compute periodic depreciation using different methods :a) Straight –line method b) Units-of-activityc) Declining balance4- Describe the procedure for revising periodic depreciation 5- Distinguish between revenue and capital expenditures and explain the entries for these expenditure 6- Explain how to account for the disposal of a plant asset through ( retirement . sale ,or exchange )a) In accounting for Retirement or sale is as follows :- eliminate the book value of the plant asset at the date of disposal - Record cash proceeds, if any - Account for difference between the book value and the cash proceeds as a gain or loss on disposal b) In accounting for exchange of similar assets is as follows :-Eliminate the book value of the old asset at the date of the exchange - Record the acquisition cost of the new asset. - Account for the loss or gain, if any, on the old asset.

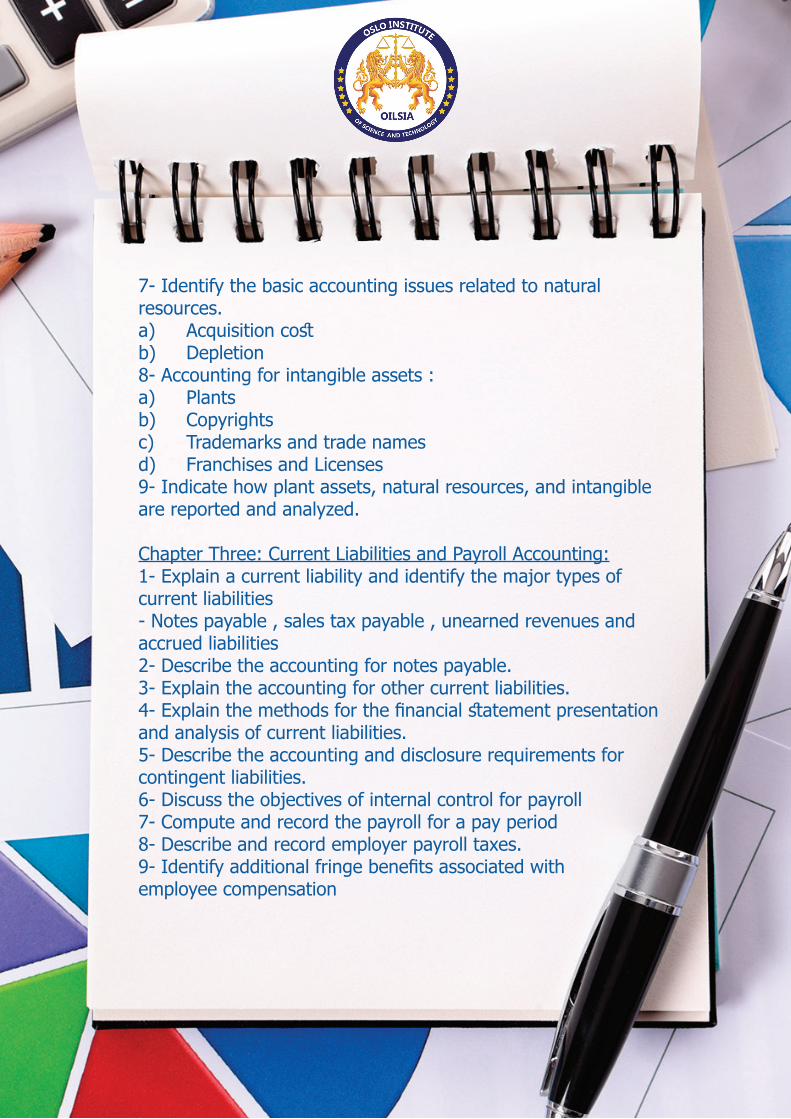

7- Identify the basic accounting issues related to natural resources.a) Acquisition cost b) Depletion 8- Accounting for intangible assets : a) Plantsb) Copyrights c) Trademarks and trade names d) Franchises and Licenses 9- Indicate how plant assets, natural resources, and intangible are reported and analyzed.

Chapter Three: Current Liabilities and Payroll Accounting:1- Explain a current liability and identify the major types of current liabilities - Notes payable , sales tax payable , unearned revenues and accrued liabilities 2- Describe the accounting for notes payable.3- Explain the accounting for other current liabilities. 4- Explain the methods for the financial statement presentation and analysis of current liabilities.5- Describe the accounting and disclosure requirements for contingent liabilities.6- Discuss the objectives of internal control for payroll 7- Compute and record the payroll for a pay period 8- Describe and record employer payroll taxes.9- Identify additional fringe benefits associated with employee compensation

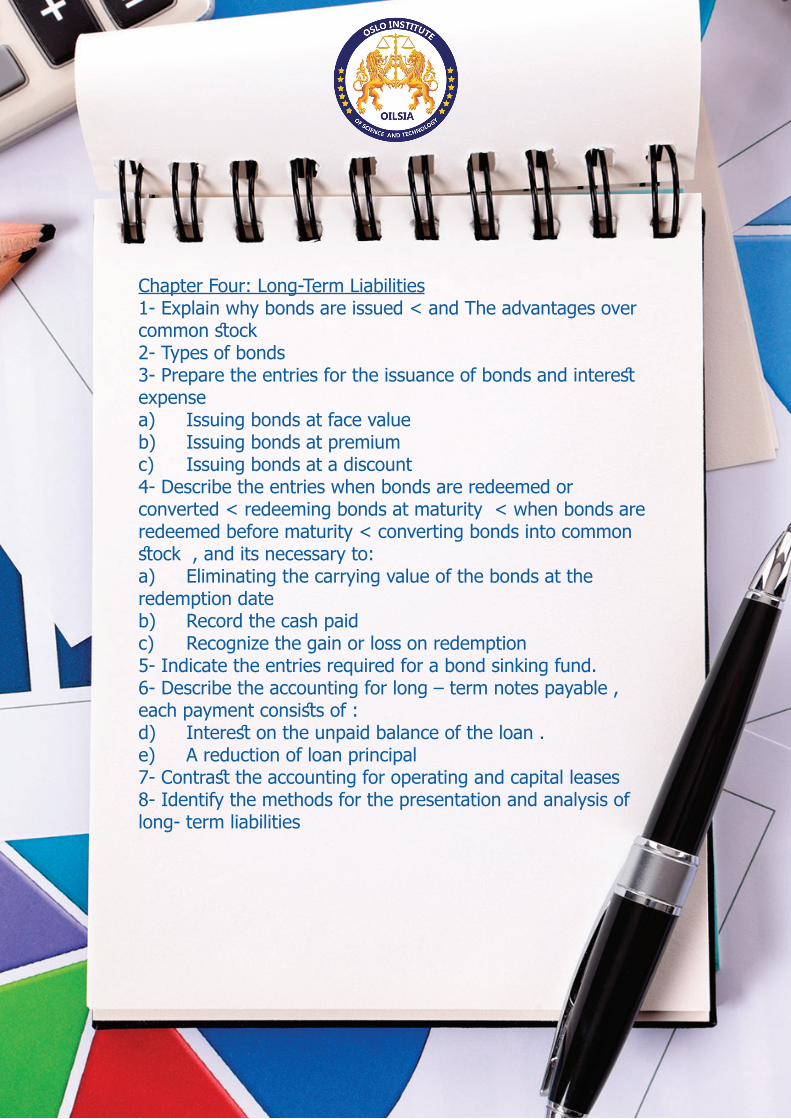

Chapter Four: Long-Term Liabilities1- Explain why bonds are issued < and The advantages over common stock 2- Types of bonds 3- Prepare the entries for the issuance of bonds and interest expensea) Issuing bonds at face value b) Issuing bonds at premium c) Issuing bonds at a discount 4- Describe the entries when bonds are redeemed or converted < redeeming bonds at maturity < when bonds are redeemed before maturity < converting bonds into common stock , and its necessary to: a) Eliminating the carrying value of the bonds at the redemption date b) Record the cash paid c) Recognize the gain or loss on redemption 5- Indicate the entries required for a bond sinking fund.6- Describe the accounting for long – term notes payable , each payment consists of :d) Interest on the unpaid balance of the loan . e) A reduction of loan principal 7- Contrast the accounting for operating and capital leases 8- Identify the methods for the presentation and analysis of long- term liabilities

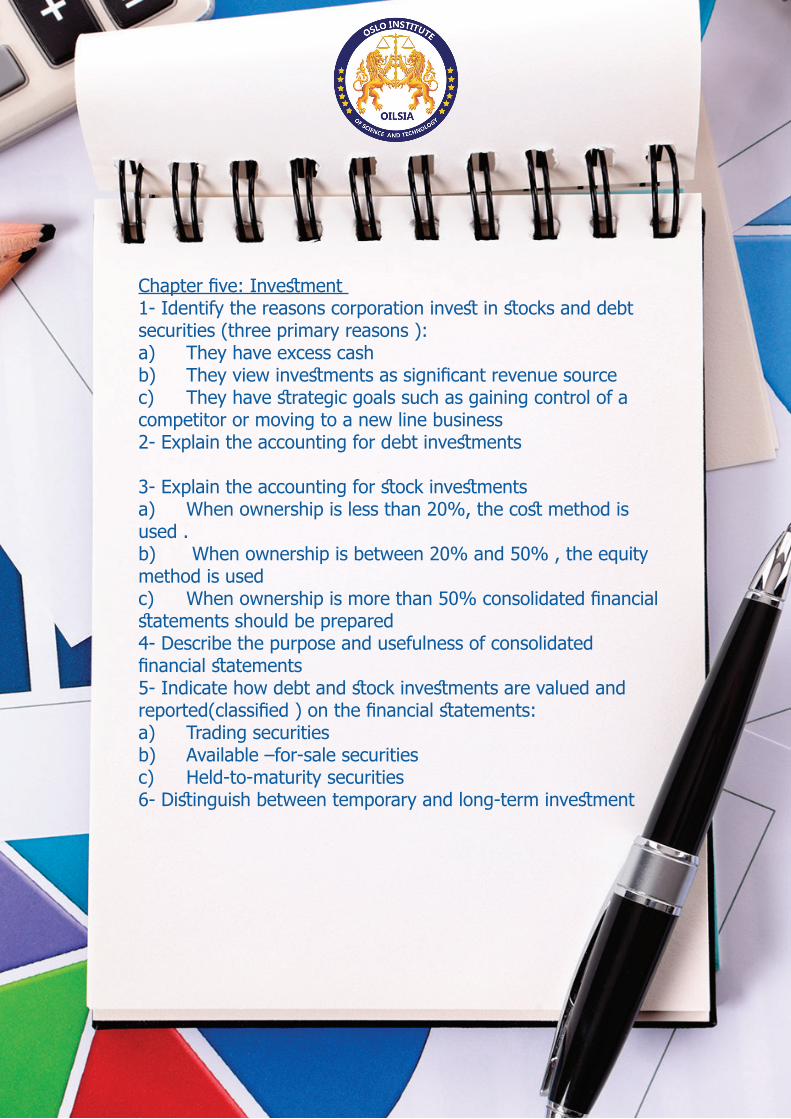

Chapter five: Investment 1- Identify the reasons corporation invest in stocks and debt securities (three primary reasons ):a) They have excess cash b) They view investments as significant revenue source c) They have strategic goals such as gaining control of a competitor or moving to a new line business 2- Explain the accounting for debt investments

3- Explain the accounting for stock investmentsa) When ownership is less than 20%, the cost method is used .b) When ownership is between 20% and 50% , the equity method is used c) When ownership is more than 50% consolidated financial statements should be prepared4- Describe the purpose and usefulness of consolidated financial statements 5- Indicate how debt and stock investments are valued and reported(classified ) on the financial statements: a) Trading securitiesb) Available –for-sale securities c) Held-to-maturity securities6- Distinguish between temporary and long-term investment

Chapter six: The statement of cash flows 1- Indicate the primary purpose of the statement of cash flows 2- Distinguish among : a) Operating activities b) Investing activities c) Financing activities 3- Prepare a statement of cash flows using the indirect method (4 steps)a) Determine the net increase or decrease in cash b) Determine net cash provided by operating activities c) Determine net cash provided by investing activities d) Determine net cash provided by financing activities 4- Prepare a statement of cash flows using the direct method: ( the same steps as indirect methods )5- Analyze the statement of cash flows : Ratio analysis of the statement of cash flows can evaluated Liquidity, Profitability, Solvency by computing:

a) The current cash debt coverage ratio b) The cash return on sales ratio c) The cash debt coverage ratio

Intermediate Accounting Part one: Accounting For Partnerships 1- Identify the characteristics of the partnership form of business organization a) Association of Individuals b) Mutual Agency c) Limited Life d) Unlimited Liability 2- Advantages and disadvantages of partnerships3- The partnership agreement4- Explain the accounting entries for the formation of partnership 5- Identify the bases for dividing net income or net loss ( 5 basis ):a) A fixed ratio b) A ratio based on beginning or average capital balances c) Salaries to partners and the remainder on a fixed ratio d) Interest on partners' capitals and the remainder on a fixed ratioe) Salaries to partners , interest on partners , capital , and the remainder on a fixed ratio 6- Describe the form and content of partnership financial statements. The principle difference between partnership financial statements and proprietorship financial statements : a) The division of net income is shown on the income statement b) The owners equity statement is called a partners' capital statement c) Each partner's capital is reported on the balance sheet.

7- Explain the effects of the entries when a new partner is admitted : a) Increase both net assets and total capital b) May result in recognition of a bonus ti either the old partners or the new partner.8- Describe the effects of the entries when a partner withdraws from the firm :a) Decrease net assets and total capital b) May result in recognizing a bonus either to the retiring partner or the remaining partner9- Prepare the entries to record the liquidation of a partnership , the steps are :a) Sale of noncash assets b) Allocation of the gain or loss on realization c) Payment of partnership liabilities d) Distribution of cash to the partners.

Part Two: Corporations Organization and Capital Stock Transactions 1- Identify and discuss the major characteristics of a corporation:a) Separate legal existence b) Limited liability of stockholdersc) Transferable ownership rights d) Ability to acquire capital e) Continuous life f) Corporation management g) Government regulations h) Additional taxes

2- Forming a Corporation 3- Ownership rights of stockholders 4- Stock issue consideration :a) Authorized stock b) Issuance stockc) Market value of stock 5- Differentiate between paid-in capital and retained earning 6- Record the issuance of common stock a) Issuing Par value common stock for cash b) Issuing no-par common stock for cash c) Issuing common stock for services or noncash assets 7- Explain the accounting for treasury stock a) Purchase of treasury stock b) Disposal of treasury stock - Sale of treasury stock above cost - Sale of treasury stock below cost 8- Differentiate preferred stock from common stock < The preferred stock : a) Preferred to Dividends b) Assets in the event of Liquidationc) Do not have voting rights d) Preferred stock may be convertible or callable 9- Prepare a stockholders' equity section a) Paid-in-capital - Capital stock - Additional paid-in capital b) Returned earning c) Treasury stock ( deducted ) 10- Compute book value per share : Total stockholders' equity ÷ Number of common shares outstanding = Book value per share11- Book value versus market value

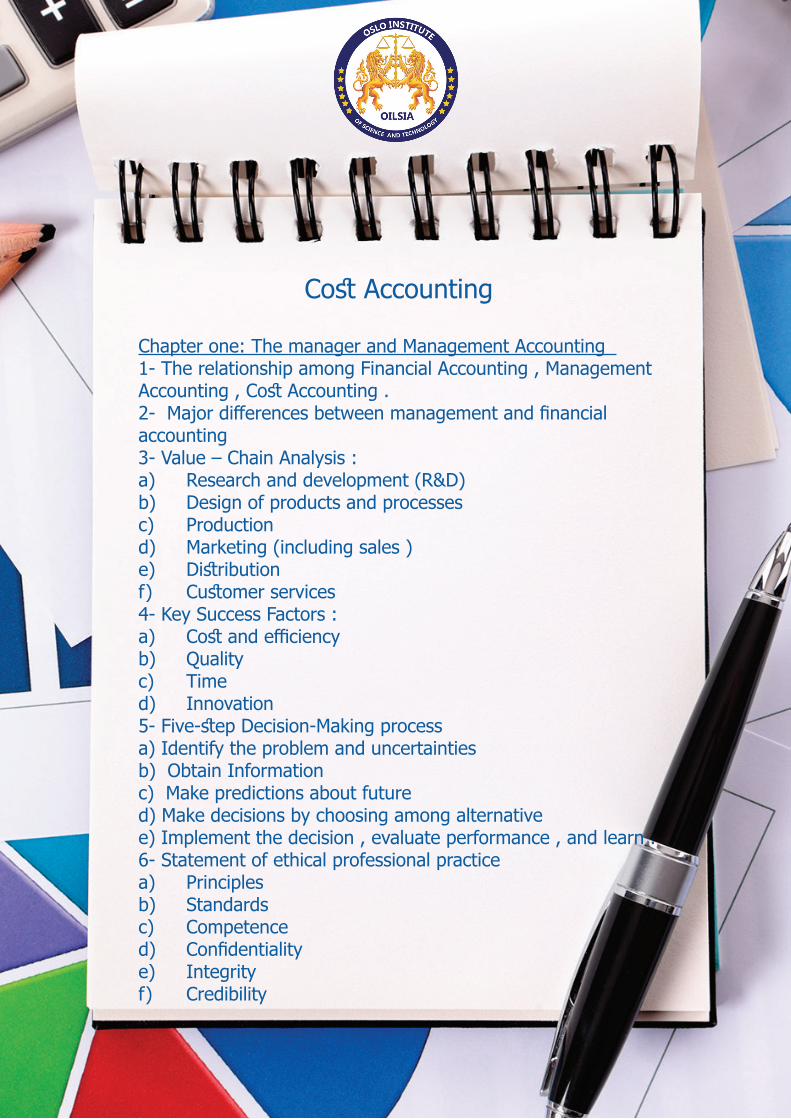

Cost Accounting

Chapter one: The manager and Management Accounting 1- The relationship among Financial Accounting , Management Accounting , Cost Accounting .2- Major differences between management and financial accounting 3- Value – Chain Analysis :a) Research and development (R&D)b) Design of products and processes c) Production d) Marketing (including sales )e) Distribution f) Customer services 4- Key Success Factors :a) Cost and efficiency b) Quality c) Time d) Innovation 5- Five-step Decision-Making process a) Identify the problem and uncertainties b) Obtain Information c) Make predictions about future d) Make decisions by choosing among alternative e) Implement the decision , evaluate performance , and learn .6- Statement of ethical professional practice a) Principlesb) Standardsc) Competence d) Confidentiality e) Integrity f) Credibility

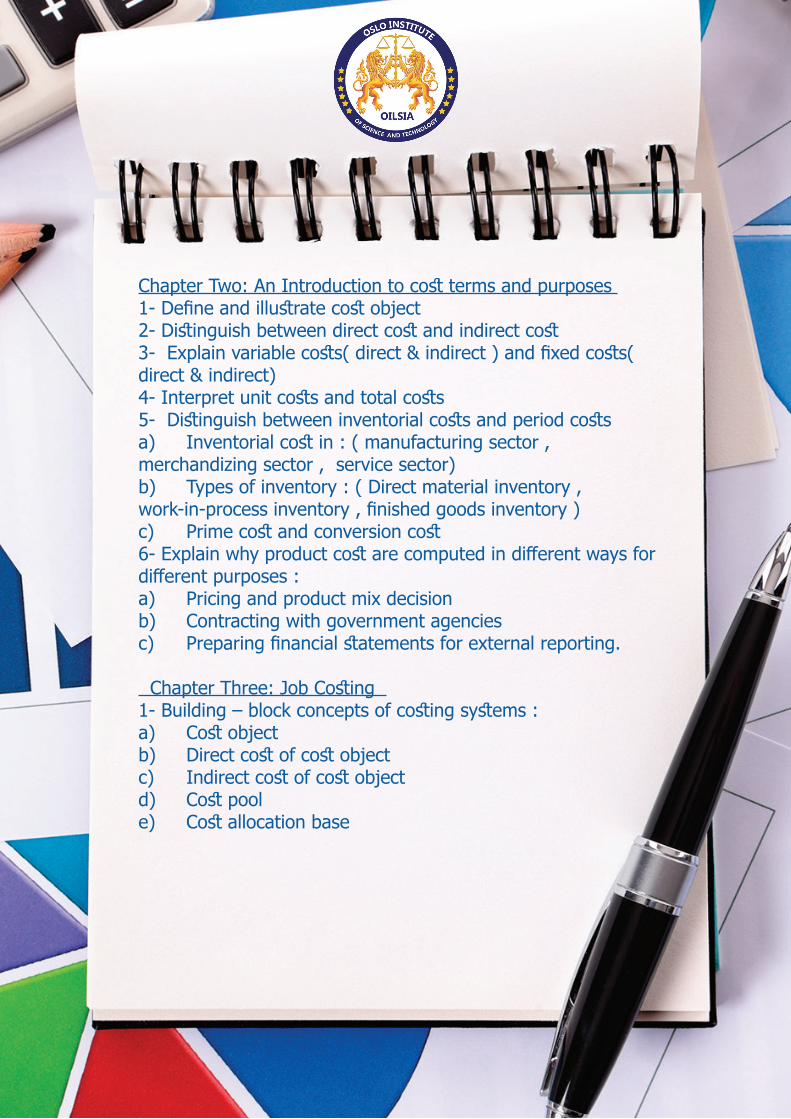

Chapter Two: An Introduction to cost terms and purposes 1- Define and illustrate cost object 2- Distinguish between direct cost and indirect cost 3- Explain variable costs( direct & indirect ) and fixed costs( direct & indirect) 4- Interpret unit costs and total costs5- Distinguish between inventorial costs and period costs a) Inventorial cost in : ( manufacturing sector , merchandizing sector , service sector) b) Types of inventory : ( Direct material inventory , work-in-process inventory , finished goods inventory ) c) Prime cost and conversion cost6- Explain why product cost are computed in different ways for different purposes : a) Pricing and product mix decision b) Contracting with government agencies c) Preparing financial statements for external reporting.

Chapter Three: Job Costing 1- Building – block concepts of costing systems :a) Cost objectb) Direct cost of cost objectc) Indirect cost of cost objectd) Cost pool e) Cost allocation base

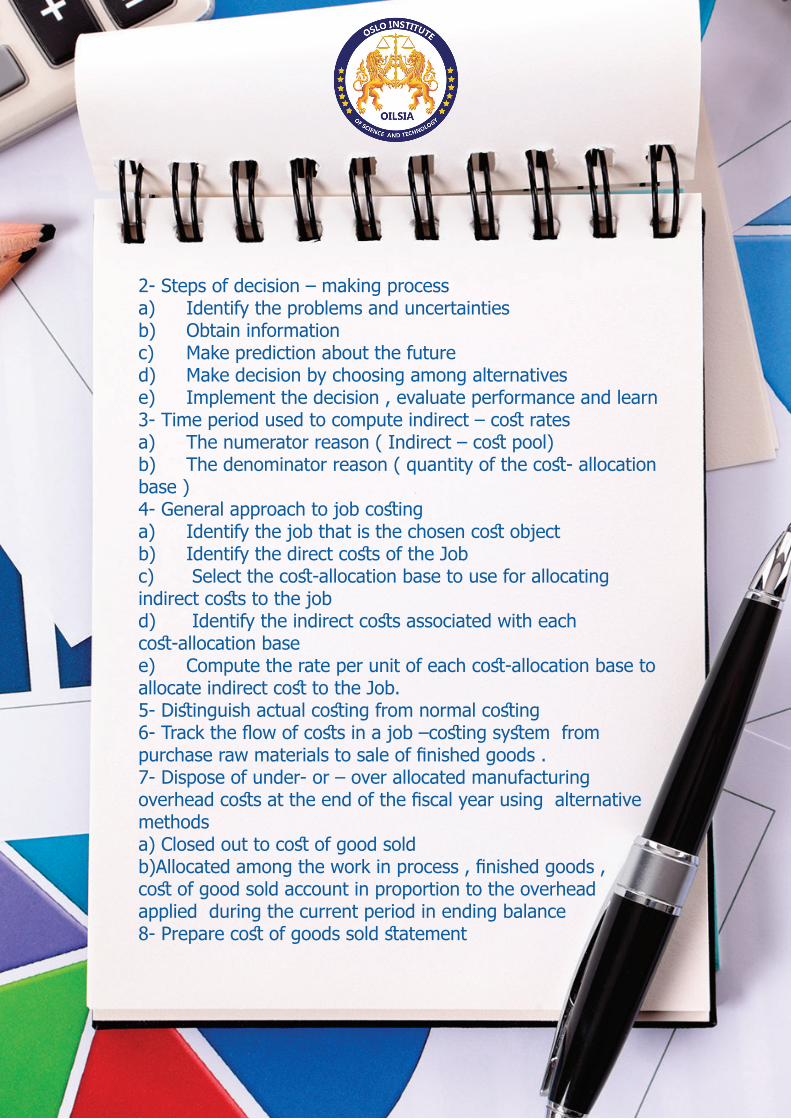

2- Steps of decision – making process a) Identify the problems and uncertaintiesb) Obtain information c) Make prediction about the future d) Make decision by choosing among alternatives e) Implement the decision , evaluate performance and learn 3- Time period used to compute indirect – cost rates a) The numerator reason ( Indirect – cost pool) b) The denominator reason ( quantity of the cost- allocation base )4- General approach to job costing a) Identify the job that is the chosen cost object b) Identify the direct costs of the Job c) Select the cost-allocation base to use for allocating indirect costs to the jobd) Identify the indirect costs associated with each cost-allocation basee) Compute the rate per unit of each cost-allocation base to allocate indirect cost to the Job.5- Distinguish actual costing from normal costing6- Track the flow of costs in a job –costing system from purchase raw materials to sale of finished goods .7- Dispose of under- or – over allocated manufacturing overhead costs at the end of the fiscal year using alternative methods a) Closed out to cost of good soldb)Allocated among the work in process , finished goods , cost of good sold account in proportion to the overhead applied during the current period in ending balance 8- Prepare cost of goods sold statement

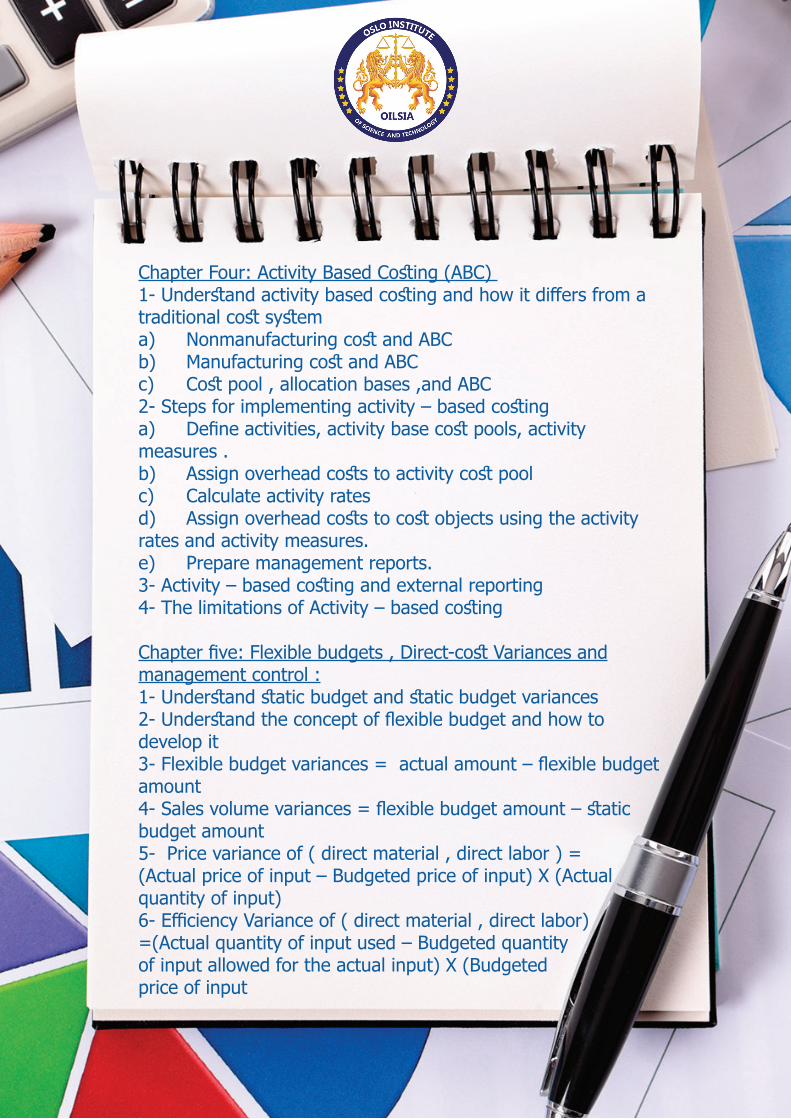

Chapter Four: Activity Based Costing (ABC) 1- Understand activity based costing and how it differs from a traditional cost system a) Nonmanufacturing cost and ABC b) Manufacturing cost and ABCc) Cost pool , allocation bases ,and ABC 2- Steps for implementing activity – based costing a) Define activities, activity base cost pools, activity measures .b) Assign overhead costs to activity cost pool c) Calculate activity rates d) Assign overhead costs to cost objects using the activity rates and activity measures.e) Prepare management reports.3- Activity – based costing and external reporting 4- The limitations of Activity – based costing

Chapter five: Flexible budgets , Direct-cost Variances and management control :1- Understand static budget and static budget variances 2- Understand the concept of flexible budget and how to develop it3- Flexible budget variances = actual amount – flexible budget amount4- Sales volume variances = flexible budget amount – static budget amount 5- Price variance of ( direct material , direct labor ) =(Actual price of input – Budgeted price of input) X (Actual quantity of input)6- Efficiency Variance of ( direct material , direct labor)=(Actual quantity of input used – Budgeted quantityof input allowed for the actual input) X (Budgeted price of input

7- Flexible budget variance = price variance + efficiency variance 8- Journal Entries using standard costs 9- Multiple causes of variances :a) Poor design of products or processesb) Poor work on the production line because of under skilled workers or faulty machines c) Inappropriate assignment of labor or machines to specific jobs.d) Congestion due to scheduling a large number of rush orders from Webb's sales representatives e) Webb's suppliers not manufacturing cloth materials of uniformly high quality.10- Performance measurement using variances : a) Effectiveness b) Efficiency

Chapter six: Process Costing 1- Comparison of Job-Order and Process costing a) Similarities between Job-order and process costingb) Differences between Job-order and process costing2- Cost flows in process costing a) Processing department b) The flow of materials , labor , and overhead costs c) Materials , labor , and overhead cost entries 3- Equivalent units of production : 4- Process costing with no beginning or ending inventory.5- Process costing with zero beginning and some ending work-in-process inventory a) Physical units and equivalent units b) Calculation of product cost c) Journal entries 6- Process costing with some beginning and some ending work-in-process inventory a) Weighted average method b) FIFO method c) Comparison of weighted – average and FIFO methods 7- Transferred –in costs in process costing using : a) Weighted average method b) FIFO method

Chapter seven: Spoilage, Rework, and Scrap 1- Defining Spoilage , Rework , and Scrap2- Defining type of Spoilage :a) Normal Spoilage b) Abnormal Spoilage. 3- The procedures for Process Costing with Spoilage :a) Summarize the flow of physical units of output. Indentify the number of units of both normal and abnormal spoilage b) Compute output in terms of equivalent units. c) Summarize total costs to account for d) Compute cost per equivalent unit .4- How to calculate and( journal entries ) spoilage using : a) Weighted average method b) FIFO method5- Inspection points and allocating costs of normal spoilage 6- The procedures for Job-Costing with Spoilagea) Normal Spoilage attributable to a specific Job b) Normal Spoilage Common to All Jobs c) Abnormal Spoilage 7- Rework and Job costing :a) Normal Rework attributable to a specific Job b) Normal Rework common to all Jobsc) Abnormal Rework 8- Accounting for Scrap a) Recognizing Scrap at the time of its sale-Scrap attributable to a specific job - Scrap common to all Jobs b) Recognizing Scrap at the time of its production -Scrap attributable to a specific job-Scrap common to all Jobs

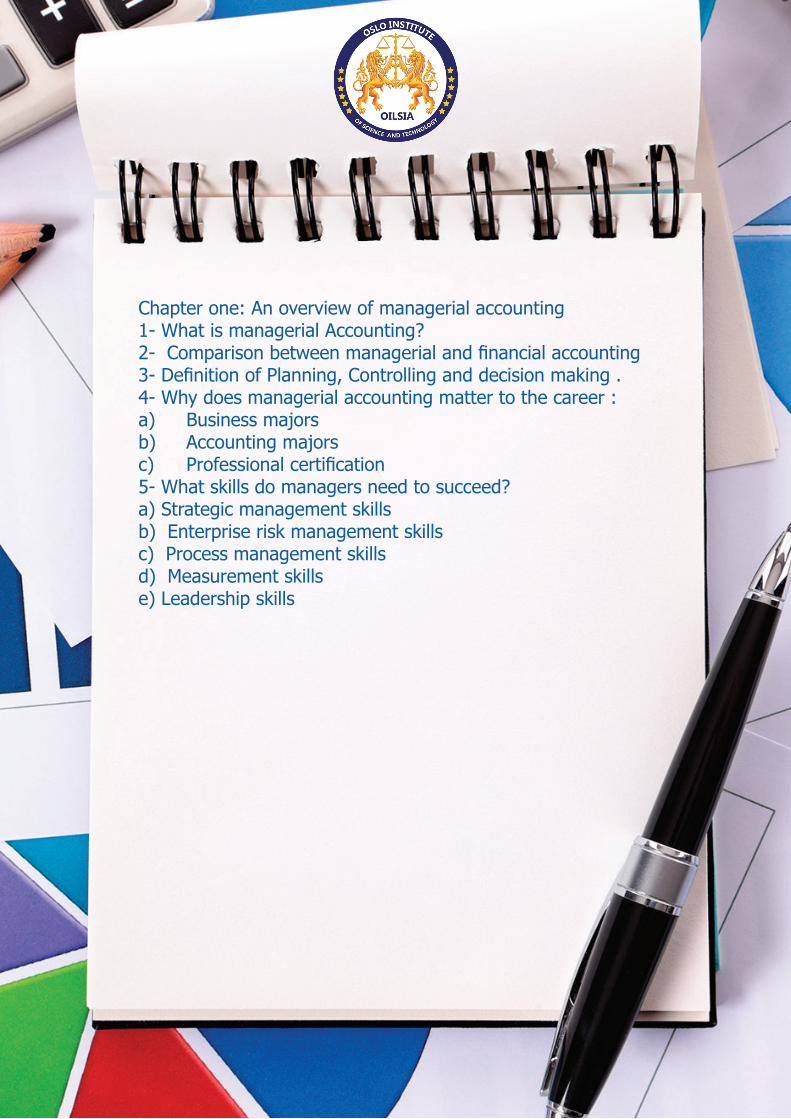

Managerial Accounting Chapter one: An overview of managerial accounting1- What is managerial Accounting?2- Comparison between managerial and financial accounting 3- Definition of Planning, Controlling and decision making .4- Why does managerial accounting matter to the career :a) Business majors b) Accounting majors c) Professional certification 5- What skills do managers need to succeed? a) Strategic management skillsb) Enterprise risk management skills c) Process management skillsd) Measurement skills e) Leadership skills Chapter one: An overview of managerial accounting 1- What is managerial Accounting?2- Comparison between managerial and financial accounting 3- Definition of Planning, Controlling and decision making .4- Why does managerial accounting matter to the career :a) Business majors b) Accounting majors c) Professional certification 5- What skills do managers need to succeed? a) Strategic management skillsb) Enterprise risk management skills c) Process management skillsd) Measurement skills e) Leadership skills

Chapter one: An overview of managerial accounting 1- What is managerial Accounting?2- Comparison between managerial and financial accounting 3- Definition of Planning, Controlling and decision making .4- Why does managerial accounting matter to the career :a) Business majors b) Accounting majors c) Professional certification 5- What skills do managers need to succeed? a) Strategic management skillsb) Enterprise risk management skills c) Process management skillsd) Measurement skills e) Leadership skills

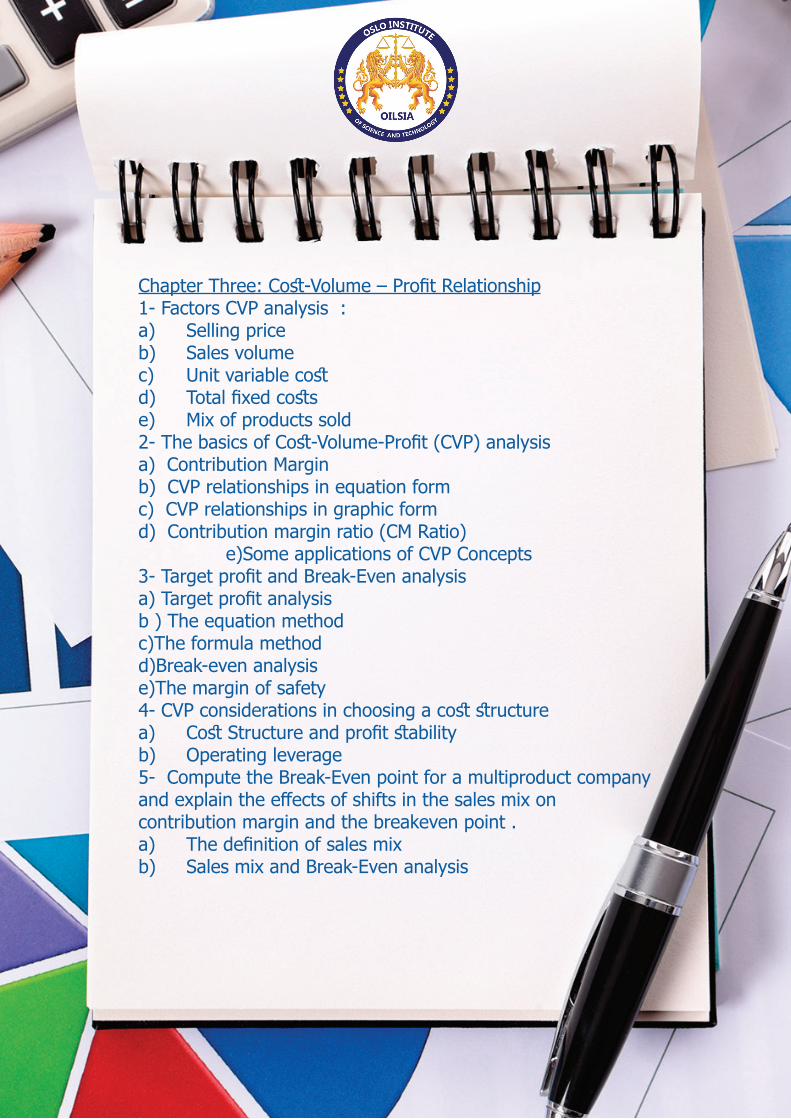

Chapter Three: Cost-Volume – Profit Relationship1- Factors CVP analysis :a) Selling price b) Sales volume c) Unit variable cost d) Total fixed costs e) Mix of products sold 2- The basics of Cost-Volume-Profit (CVP) analysis a) Contribution Margin b) CVP relationships in equation form c) CVP relationships in graphic form d) Contribution margin ratio (CM Ratio) e)Some applications of CVP Concepts 3- Target profit and Break-Even analysis a) Target profit analysis b ) The equation methodc)The formula method d)Break-even analysis e)The margin of safety 4- CVP considerations in choosing a cost structure a) Cost Structure and profit stability b) Operating leverage 5- Compute the Break-Even point for a multiproduct company and explain the effects of shifts in the sales mix on contribution margin and the breakeven point . a) The definition of sales mix b) Sales mix and Break-Even analysis

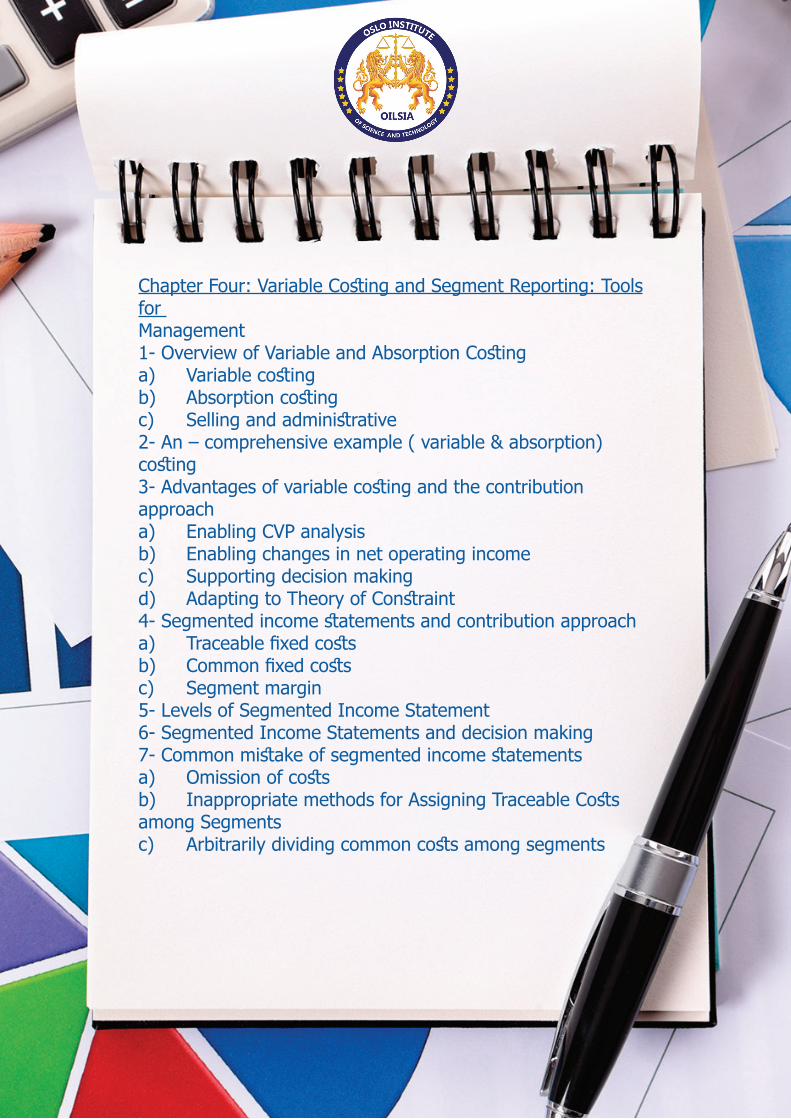

Chapter Four: Variable Costing and Segment Reporting: Tools for Management 1- Overview of Variable and Absorption Costing a) Variable costing b) Absorption costing c) Selling and administrative 2- An – comprehensive example ( variable & absorption) costing 3- Advantages of variable costing and the contribution approach a) Enabling CVP analysis b) Enabling changes in net operating income c) Supporting decision making d) Adapting to Theory of Constraint 4- Segmented income statements and contribution approach a) Traceable fixed costs b) Common fixed costsc) Segment margin 5- Levels of Segmented Income Statement 6- Segmented Income Statements and decision making 7- Common mistake of segmented income statementsa) Omission of costs b) Inappropriate methods for Assigning Traceable Costs among Segmentsc) Arbitrarily dividing common costs among segments

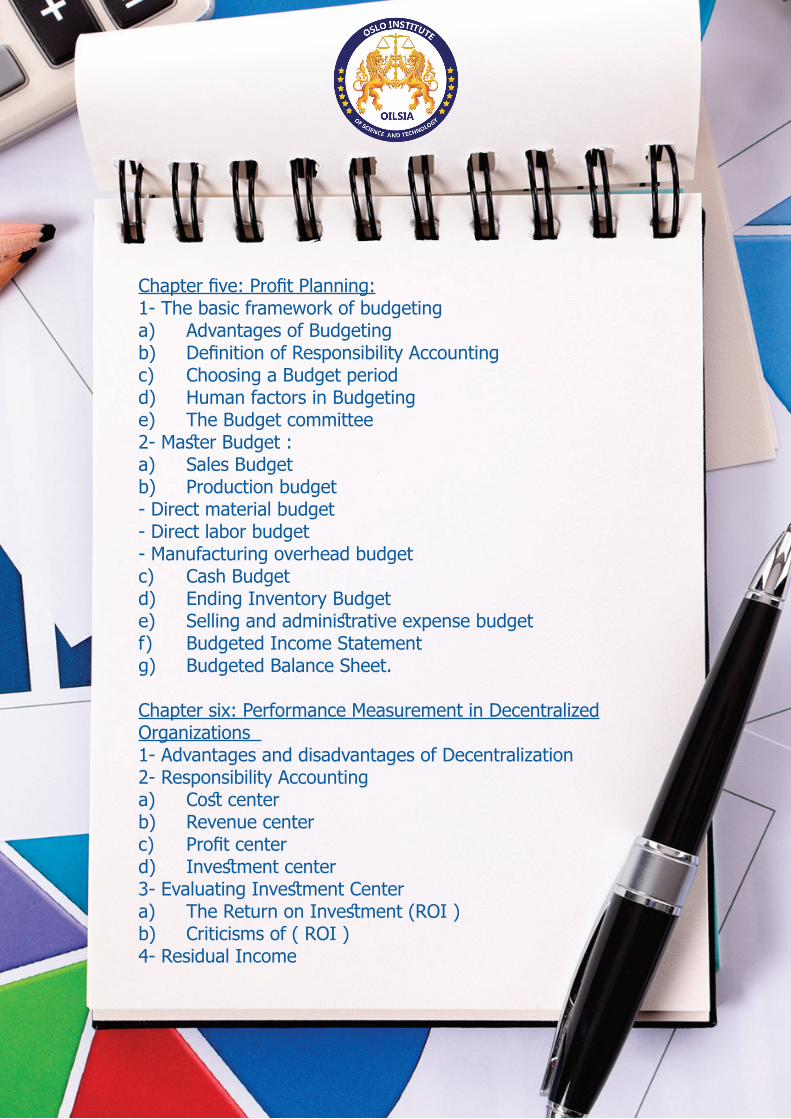

Chapter five: Profit Planning:1- The basic framework of budgeting a) Advantages of Budgeting b) Definition of Responsibility Accounting c) Choosing a Budget period d) Human factors in Budgeting e) The Budget committee 2- Master Budget :a) Sales Budgetb) Production budget - Direct material budget - Direct labor budget - Manufacturing overhead budgetc) Cash Budget d) Ending Inventory Budget e) Selling and administrative expense budget f) Budgeted Income Statement g) Budgeted Balance Sheet.

Chapter six: Performance Measurement in Decentralized Organizations 1- Advantages and disadvantages of Decentralization 2- Responsibility Accounting a) Cost center b) Revenue centerc) Profit center d) Investment center 3- Evaluating Investment Center a) The Return on Investment (ROI )b) Criticisms of ( ROI )4- Residual Income

5- Balanced Scorecard ( Performance Measures ) :a) Financial : has financial performance improved b) Customer : Do customers recognize that we are delivering more valuec) Internal Business Processes : d) Learning and Growth

Chapter seven: Capital Budgeting Decisions 1- Defining Capital Budgeting 2- The time value of money 3- Discounted cash Flows :a) The Net Present Value method b) The internal rate of return method. 4- Other approaches to capital budgeting decisions :a) The Payback period method b) Payback and uneven cash flows c) The simple rate of return

Chapter eight: Financial statements Analysis: 1- Liquidity Ratio a) Current Ratiob) Acid Test Ratio2- Asset Management Ratios a) Inventory Turnover Ratiob) Days sales outstanding Ratio ( DSO )c) Fixed Assets Turnover Ratio d) Total assets turnover Ratio e) Operating capital requirement Ratio 3- Debt Management Ratiosa) Debt Ratio b) Time- Interest – Earned (TIE) Ratio 4- Profitability Ratio

a) Profit Margin on sales Ratiob) Basic Earning Power Ratio ( BEP )c) Operating Profit Margin after Tax d) Return on Total Assets ( ROA ) e) Return on Common Equity 5- Market Value Ratios :a) Price / earnings ( P/E ) Ratiob) Book value per share c) Market / Book ( M/B ) Ratio

Auditing

Chapter one: The Audit Services & Profession1. Describe assurance services and distinguish audit services from other assurance and non assurance services provided by CPAs.2. Explain the importance of auditing in reducing information risk.3. List the causes of information risk, and explain how this risk may be reduced.4. Define auditing, and what is the nature of auditing.5. What are the differences between auditing and accounting, and what is the relation between them.6. Types of Audits:a) Financial Statement Auditb) Operational Auditc) Compliance Audit

7. Requirements for becoming a CPA:a) Educational Requirementb) Examination Requirementc) Experience Requirement

8. What is an Audit Standards, and what is the role of international standards on auditing (ISA), Some main and important standards will be selected, such as:a) ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing.b) ISA 240, The Auditor's Responsibilities Relating to Fraud in an Audit of Financial Statements c) ISA 610, Using the Work of Internal Auditors (Other important standards will discussed in further chapters)9. Describe the nature of CPA firms:a) what they do, and b) what their structure.

Chapter Two: Audit Reports: (ISA 700, Forming an Opinion and Reporting on Financial Statements )

1. Describe the parts of the standard unqualified audit report.a) Audit Report titleb) Audit report addressc) Introductory paragraphd) Scope paragraphe) Opinion paragraphf) Name of CPA firmg) Audit report date

2. Required Conditions to issue the standard unqualified audit report.3. Describe the five circumstances when an unqualified report with an explanatory paragraph or modified wording is appropriate:1) Lack of consistent application of generally accepted accounting principles.2) Substantial doubt about going concern.3) Auditor agrees with a departure from promulgated accounting principles.4) Emphasis of a matter.5) Reports involving other auditors.

4. Types of audit reports that can be issued when an unqualified opinion is not justified:a) Qualified Opinion.b) Adverse Opinion.c) Disclaimer of Opinion.

5. What is materiality, and what are levels of materiality.6. Explain how materiality affects audit reporting decisions.7. Determine the appropriate audit report for a given audit situation.8. Auditors independence and Professional Ethics.9. Implementation and reviewing of published audit’s reports.

Chapter Three: Audit Evidence: (ISA 500, Audit Evidence)

1. Contrast audit evidence with evidence used by other professions.2. What is the nature of evidence.3. Identify the four audit evidence decisions that are needed to create an audit program:a) Which audit procedures to useb) What sample size to select for a given procedurec) Which items to select from the populationd) When to perform the procedures

4. What is an audit program5. Specify the characteristics that determine the persuasiveness of evidence:a) Competenceb) Sufficiencyc) Combined effectd) Persuasiveness and cost

6. Types of evidence used in auditing:a) Physical examination.b) Confirmation (Positive, negative and blind confirmation).c) Documentation.d) Analytical procedures. e) Inquiries.f) Reperformance.g) Observation.

7. Audit documentation:a) What is audit documentationb) What is the purpose of audit documentation

8. Prepare organized audit documentation.

Chapter Four: Audit Planning and Analytical Procedures (ISA 520, Analytical Procedures) and (ISA 320, Materiality in Planning and Performing an Audit) 1. What is audit planning, and why adequate audit planning is essential.2. What is audit risk and inherent risk.3. Accept and reject client.4. Make client acceptance decisions and perform initial audit planning.5. Understanding of the client’s business and industry.6. Audit and information technology.7. Assess client business risk.8. Perform preliminary analytical procedures.9. State the purposes of analytical procedures and the timing of each purpose.10. Select the most appropriate analytical procedure from among the five major types:a) Compare client and industry data.b) Compare client data with similar prior-period data.c) Compare client data with client-determined expected results.d) Compare client data with auditor-determined expected results.e) Compare client data with expected results, using nonfinancial data.

11. Calculation of common financial ratios:a) Short-term debt-paying abilityb) Liquidity activity ratiosc) Ability to meet long-term debt obligationsd) Profitability ratios

12. Calculation and using of vertical and horizontal analysis.13. The concept of Materiality and Risk.

Chapter Five: Internal Control and Control Risk (ISA 330, The Auditor's Responses to Assessed Risks )

1. Contrast management’s need for internal control with the auditor’s need to consider internal control when designing an audit:a) Client’s Concerns.b) Auditor Concerns.

2. Describe how information technology affects internal control:- Risks Associated With the Use of Information Technology:a) Programmed errorsb) Processing incorrect datac) Unauthorized access

3. Five components of internal control:1) Control Environment2) Risk Assessment3) Control Activities4) Information and Communication5) Monitoring

4. Methods used to obtain an understanding of internal control.5. Documentation methods:A) Narrative.B) Flow Chart.C) Internal Control Questionnaire.

6. Assess control risk by linking strengths and weaknesses of internal control to transaction-related audit objectives.7. Describe the process of designing and performing tests of controls.

References 1- Jerry J. Weygandt, Paul D. Kimmel , Donald E. Kieso "

Accounting Principle " Edition 12Th

2- Eugene F. Brigham , Michael C. Ehrhardt " Financial Management " Theory and Practice . Edition 14th

3- Ray H. Garrison , D,B,A . ERC W. Noreen . Peter C. Brewer " Managerial Accounting " Edition 14TH

4- Charles T. Horngren ; Srikant M. Datar ; Madhav V. Rajan ; " Cost Accounting " Edition 15Th

5- Alvin A. Arens ; Randal J. Elder ; Mark S. Beasley ; "

Auditing and Assurance Services" Edition 14th

6 Guide to using International Standards of Auditing in the audits of Small – and – Medium sized entities

7- International Accounting Standard (IASs) issued by

International Accounting standard Council ( IASC )

i

Important Information:All certi�cates issued by the Institute bearing check code

Student must verify the institute validation of the certi�cate by typing the check code in the following link: http://www.oilsia.com/index.php/veri�cation/

In case the certi�cate has been veri�ed that means it has a data and that the certi�cate is considered valid. If no data occurs, student should immediately contact and check on the certi�cate validation with the Institute General department through the following e-mail address: [email protected]

All cards issued by the Institute bearing a code and a speci�c number as well

Student must check the card validity issued by the Institute through the follow-ing link: http://www.oilsia.com/index.php/veri�cation/

In case the certi�cate has been veri�ed, that means the card has a data and so it is a valid card. if no data occurs, student should immediately contact and check on the certi�cate validation with the Institute General department through the following e-mail address: [email protected]

i

i

i

i

i

i

Certi�cate Model:

ID card Model: