abakkus smart build india portfolio

TRANSCRIPT

Abakkus SmartBuild India Portfolio

• Abakkus is alpha focused asset management firm set-up in 2018 by Sunil Singhania.

• Sunil, a CA Rank Holder and CFA charter holder, has a distinguished track record of over 2 decades in Equity Investments.Earlier as CIO-Equities for Reliance Mutual Fund (now Nippon India Mutual Fund), he played an instrumental role in buildingRMF (now Nippon India Mutual Fund) into one of India’s largest AMCs overseeing ~USD 11bn of equity assets.

• Reliance Growth Mutual Fund (now Nippon India Growth Mutual Fund), independently managed by him, has the uniquedistinction of having grown over 100 times in 21 years. Reliance Small Cap Mutual Fund (now Nippon India Small Cap MutualFund) was rated amongst the top Mutual funds in its category.

• He is currently appointed on the IFRS Capital Markets Advisory Committee (CMAC) and the only member from India to beappointed for the same. (2020-2023).

• He served on the Global board of CFA Institute, USA (2013-2019) and as Chairman of the Investment Committee (2017-2019)of the CFA Institute, USA.

• Abakkus is managing ~ Rs 6,000** crs across AIF, PMS and Advisory platform.

INTRODUCING ABAKKUS INVESTMENT ADVISORS*

2

CA Chetan Vora has over a decade of equity market experience.

• Prior to Abakkus Asset Manager LLP, he has been associated as an equity research analyst for organizations like ValueQuestInvestment Advisor, Edelweiss and Brics, whereby he has tracked multiple sectors like Capital Goods, Auto, Auto Ancillary,Consumer Durables, Infrastructure Sectors, etc.

• His expertise lies in stock selection across the market cap with strong focus on bottom-up research.

• Chetan is Chartered Accountant by Profession and has cleared CFA level 2.

ADVISOR PROFILE***

*Investment Advisory Division of Abakkus Asset Managers LLP, ** as on dated 31st AUGUST 2021, ***Person Associated with Investment Advice

• Believe in investing with an endevour to generate alpha over the markets than just allocation within benchmark index• Growth companies where profitability is expected to grow higher than market average• Fundamentally underpriced stocks with reasonable growth expectations to triggers• Mid Cap companies with a scalable business model and growth potential to become large cap

ALPHA GENERATORS

• Bottom-up research with focus on Balance sheet

• Numbers speak more than presentations and hype

• Returns ultimately are all about earnings, earnings & earnings

FUNDAMENTAL DRIVEN

• Prefer to be first, early and/or only investors

• Don’t chase momentum

• Open to look at companies across sectors and market caps and business cycle

HAPPY TO BE CONTRARIAN

• Each investment opportunity is looked upon individual merit

• Not constrained to a particular theme or styleAGILE & FLEXIBLE

• Buy and hold

• Invest in a stock as if investing in a business

• Think like a partner

PATIENT INVESTORS

• Estimated expected returns in line with risk taken

• A good company might not necessarily be a good stock

• Focus on the price we pay, and value derived

• What is in the price?

RISK REWARD EQUATION

INVESTMENT PHILOSOPHY

3

OUR UNIQUE MEETS FRAMEWORK

Management

Earnings

Events/Trends

Timing

Structural

Quality - Capability a n d track record

Capital Allocation – c a p e x is fine if ROE is maintained or e n h a n c e d

Capital Distribution – fair to minority shareholders

Error in decision – Business errors vs intentional mishaps

Quality of earnings vs reported numbers

Actual earnings vs exp ected

Cycl ical vs Structural earnings

Companies that c a n double profits in 4 years or less or where EV/EBITDA c a n halvein four years

Stock movement b ecau se of events. C a n b e Buy or Sell opportunity

Events on the horizon

Disruptive trends/New themes

G o o d co m p a ny is not necessarily a g o o d investment if price is not right What

is the price discounting

Time frame of investment

M e a n Reversion

Size of the opportunity

Competitive positioning / MOAT

Consistent growth in profits

www.abakkusinvest.com 4

Chase Momentum We would let fundamentals drive our investment decision rather than price movements

Avoid the four “C”s

Churn Unnecessarily

Copy & Mimic

Analyze, research, be convinced and then BUY. Once done, STAY PUT. No needlesschurning of the portfolio

We will not be influenced by ‘herd mentality’. All investments have to be necessarilyworked internally

Credit Risk - Fractured Balance Sheet

We believe it is very difficult to rebuild a broken balance sheet and these stockseventually turn value traps and hence, are best avoided

5

WHAT WE WON’T DO

• OPPORTUNISTIC

• Greater flexibility in investing compared to mutual funds

• PERFORMANCE

• Abakkus has a well-established performance track record since inception

• EXPERIENCE

• Backed by a well qualified and performing team of professionals that have experience across market cycles

• COMMITMENT

• Follow a start-up culture with a high degree of commitment, ethics and passion

• POSITIONING

• Differentiated Alpha focused strategy

6

WHY US: OUR ADVANTAGE

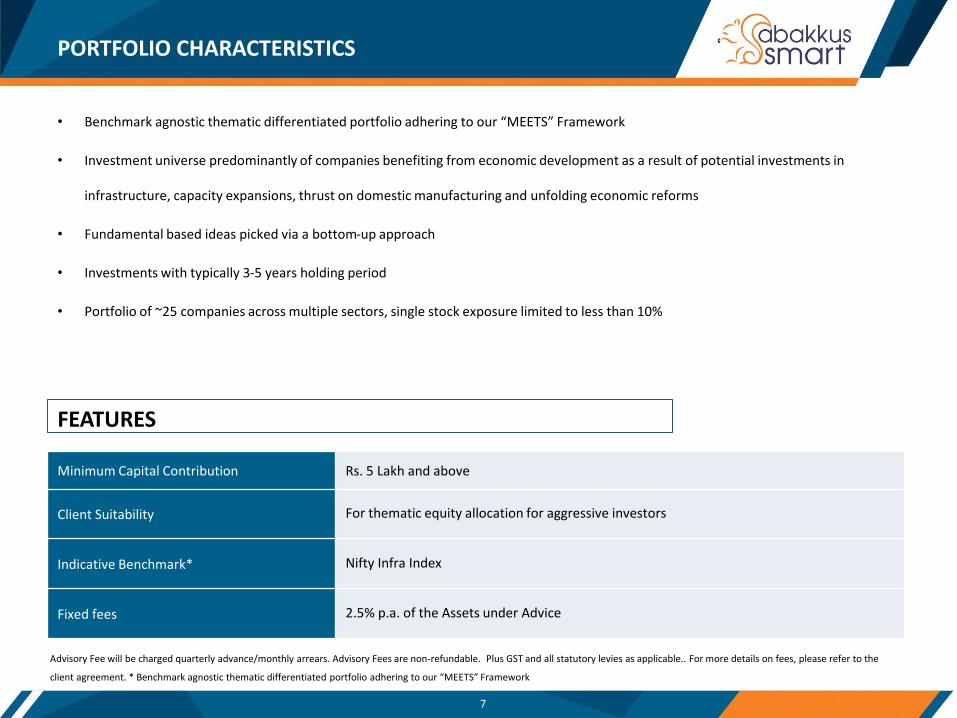

• Benchmark agnostic thematic differentiated portfolio adhering to our “MEETS” Framework

• Investment universe predominantly of companies benefiting from economic development as a result of potential investments in

infrastructure, capacity expansions, thrust on domestic manufacturing and unfolding economic reforms

• Fundamental based ideas picked via a bottom-up approach

• Investments with typically 3-5 years holding period

• Portfolio of ~25 companies across multiple sectors, single stock exposure limited to less than 10%

PORTFOLIO CHARACTERISTICS

Minimum Capital Contribution Rs. 5 Lakh and above

Client Suitability For thematic equity allocation for aggressive investors

Indicative Benchmark* Nifty Infra Index

Fixed fees 2.5% p.a. of the Assets under Advice

FEATURES

7

Advisory Fee will be charged quarterly advance/monthly arrears. Advisory Fees are non-refundable. Plus GST and all statutory levies as applicable.. For more details on fees, please refer to the

client agreement. * Benchmark agnostic thematic differentiated portfolio adhering to our “MEETS” Framework

PORTFOLIO CONSTRUCT

8

Predominantly investing in sectors

benefitting from Build India theme.

• Investment Universe

200 companies

• Filtered for Management Quality , Corporate Governance, Sector headwinds, etc

120 companies• In-depth research,

Financials & bottom up approach

20-25 companies

•Valuation , favourable Risk-reward equation, diversification , liquidity

WHY BUILD INDIA PORTFOLIO

9

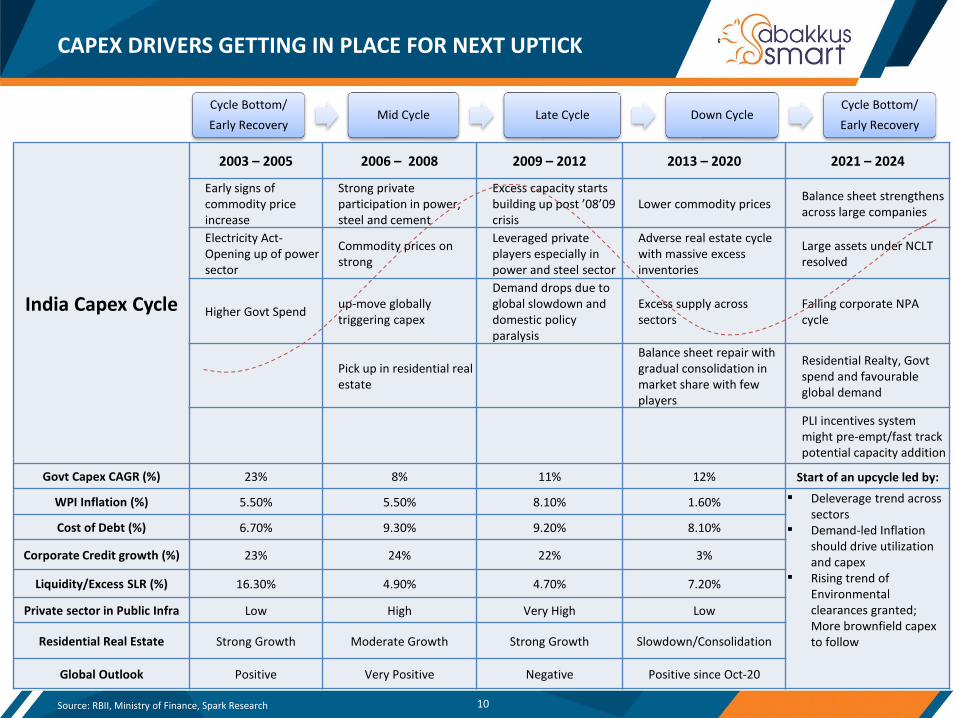

CAPEX DRIVERS GETTING IN PLACE FOR NEXT UPTICK

India Capex Cycle

2003 – 2005 2006 – 2008 2009 – 2012 2013 – 2020 2021 – 2024

Early signs of commodity price increase

Strong private participation in power, steel and cement

Excess capacity starts building up post ’08’09 crisis

Lower commodity pricesBalance sheet strengthens across large companies

Electricity Act-Opening up of power sector

Commodity prices on strong

Leveraged private players especially in power and steel sector

Adverse real estate cycle with massive excess inventories

Large assets under NCLT resolved

Higher Govt Spendup-move globally triggering capex

Demand drops due to global slowdown and domestic policy paralysis

Excess supply across sectors

Falling corporate NPA cycle

Pick up in residential real estate

Balance sheet repair with gradual consolidation in market share with few players

Residential Realty, Govt spend and favourable global demand

PLI incentives system might pre-empt/fast track potential capacity addition

Govt Capex CAGR (%) 23% 8% 11% 12% Start of an upcycle led by:

WPI Inflation (%) 5.50% 5.50% 8.10% 1.60% ▪ Deleverage trend across sectors

▪ Demand-led Inflation should drive utilization and capex

▪ Rising trend of Environmental clearances granted; More brownfield capex to follow

Cost of Debt (%) 6.70% 9.30% 9.20% 8.10%

Corporate Credit growth (%) 23% 24% 22% 3%

Liquidity/Excess SLR (%) 16.30% 4.90% 4.70% 7.20%

Private sector in Public Infra Low High Very High Low

Residential Real Estate Strong Growth Moderate Growth Strong Growth Slowdown/Consolidation

Global Outlook Positive Very Positive Negative Positive since Oct-20

Cycle Bottom/

Early RecoveryMid Cycle Late Cycle Down Cycle

Cycle Bottom/

Early Recovery

Source: RBII, Ministry of Finance, Spark Research 10

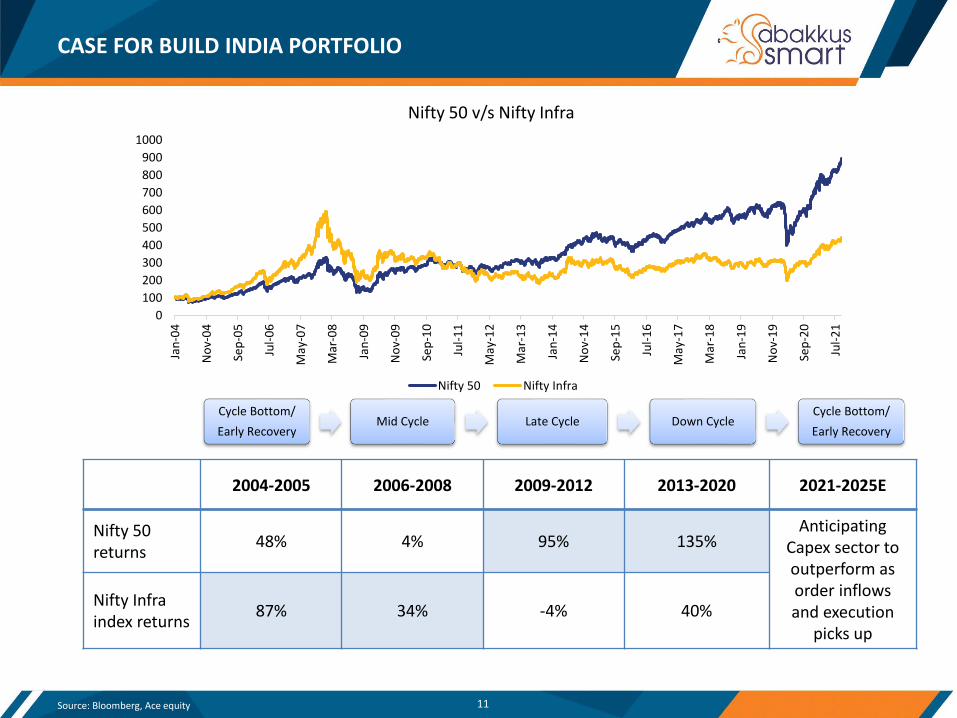

CASE FOR BUILD INDIA PORTFOLIO

Source: Bloomberg, Ace equity 11

0

100

200

300

400

500

600

700

800

900

1000

Jan

-04

No

v-0

4

Sep

-05

Jul-

06

May

-07

Mar

-08

Jan

-09

No

v-0

9

Sep

-10

Jul-

11

May

-12

Mar

-13

Jan

-14

No

v-1

4

Sep

-15

Jul-

16

May

-17

Mar

-18

Jan

-19

No

v-1

9

Sep

-20

Jul-

21

Nifty 50 v/s Nifty Infra

Nifty 50 Nifty Infra

2004-2005 2006-2008 2009-2012 2013-2020 2021-2025E

Nifty 50 returns

48% 4% 95% 135%Anticipating

Capex sector to outperform as order inflows and execution

picks up

Nifty Infra index returns

87% 34% -4% 40%

Cycle Bottom/

Early RecoveryMid Cycle Late Cycle Down Cycle

Cycle Bottom/

Early Recovery

WHY LOOK AT INFRA NOW

• Last 10 years Infra index has given 35% return v/s Nifty 50 has given 178% returns

• During the previous capex cycle between 2004-07 Nifty Infra index was a significant outperformer, gaining 475%

Source: Bloomberg, Ace equity 12

• Post disruption of GST and Demonetization, over the last couple of years there is renewed focus on infrastructure growth

• NDA government was always pro growth, what is different this time is government has cleared the bottlenecks and has a

clear funding plan in place which should ensure execution pickup

• Thanks to various govt initiatives like PLI, protection duties & taxation, Private capex too is looking up

• Sector prospects are looking up and there is valuation comfort given the underperformance of the sector over the last 4

years, hence the Build India theme opportunity

1500

2500

3500

4500

5500

Jan

11

Ap

r 1

1

Jul 1

1

Oct

11

Jan

12

Ap

r 1

2

Jul 1

2

Oct

12

Jan

13

Ap

r 1

3

Jul 1

3

Oct

13

Jan

14

Ap

r 1

4

Jul 1

4

Oct

14

Jan

15

Ap

r 1

5

Jul 1

5

Oct

15

Jan

16

Ap

r 1

6

Jul 1

6

Oct

16

Jan

17

Ap

r 1

7

Jul 1

7

Oct

17

Jan

18

Ap

r 1

8

Jul 1

8

Oct

18

Jan

19

Ap

r 1

9

Jul 1

9

Oct

19

Jan

20

Ap

r 2

0

Jul 2

0

Oct

20

Jan

21

Ap

r 2

1

Jul 2

1

Nifty Infra Index Performance

Key Contributors

➢ Domestic demand driven economy, less dependent on global growth

➢ Large and growing middle class, increased consumption demand.

➢ Favorable demographics – more than 65% population below 35 years of age, under penetration growth opportunity.

➢ Strong credit mechanism through a well-regulated banking and financial sector

➢ High savings rate

➢ Healthy capital inflows helping investments in industry and infrastructure

➢ A pragmatic government with focus on policy reforms and growth impetus

Source: Motilal Oswal Securities Limited, Data as on 30/04/2021, Wikipedia

India has grown at an average of 6.2% for last 33 years with no negative annual growth. Low impact of Covid -19 on economy, consumption helpedto gain V shape recovery in FY21. If the crisis doesn’t materially escalate, FY22 could see double digit growth.

37 62 18

4

31

7

47

7

49

4

52

4

61

8

72

2

83

4

94

9 12

39

12

24

13

65

17

08

18

23

18

28

18

57

20

39

21

04

22

90 26

52

27

17

29

72

32

58

35

77

39

24 43

06 47

29

19

60

19

70

19

80

19

90

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

E

20

23

E

20

24

E

India GDP (USD bn)

Ist USD Trn 58

2nd USD Trn 7 yrs

3rd USD Trn 6 yrs

4th USD Trn 3 yrs

13

INDIA MACRO: INDIA GROWTH OPPORTUNITY

GOVT SPENDING ON INFRA INVESTMENT TO BE 2X (FY20-25)

~INR 57 lakhs Crores ~INR 111 lakhs Crores

Source: Source: Report of the Task Force Department of Economic Affairs Ministry of Finance Government of India-Volume I.

14

• The National Infrastructure Pipeline (NIP) is government’s effort to augment India's infrastructure through an identifiedinvestment of INR 111 Lakh crores between FY 2020-2025 doubled from FY 2013-2019

• Sectors such as energy, roads, urban and railways amount to ~71% of the projected infrastructure investments in India.

WHAT WILL HELP CAPITAL SPENDING

15Source: Spark Research, NMP Report

Ample Liquidity in the banking system to fund growth and keep the interest rates low

6.6

3.2

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Ap

r 1

6

Jul 1

6

Oct

16

Jan

17

Ap

r 1

7

Jul 1

7

Oct

17

Jan

18

Ap

r 1

8

Jul 1

8

Oct

18

Jan

19

Ap

r 1

9

Jul 1

9

Oct

19

Jan

20

Ap

r 2

0

Jul 2

0

Oct

20

Jan

21

Ap

r 2

1

Jul 2

1

Net liquidity (Rs. Tn) Call Money rate (%)-RHS

Interest rates are low (3 year G-sec %)

882

1624

17951673

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY 22 FY 23 FY 24 FY 25

(IN

R B

llio

n)

National Monetization Pipeline Plan

4

5

6

7

8

9

10

11

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

While total credit growth is moderate, there is a pick up in credit growthin pockets like Housing, Road & SME

Absolute (Rs. tn) Incremental credit Growth

Mar-20 Apr-21 Rs. bn YoY

Personal Loan 25.5 28.1 2,568 12.60%

Housing 13.4 14.6 1,225 9.50%

Credit Card 1.1 1.1 55 17.10%

Vehicle Loan 2.2 2.4 218 11.70%

Other Personal 7.3 7.9 592 17.80%

Roads infra 1.9 2.4 485 35.50%

SME 1.1 1.4 375 43.80%

Total 103.7 108.6 4,896 5.70%

Make in India initiatives from GOI and global sourcing moving to "China+1" model has resulted in better demand. India has a strong chance to usher a meaningful private sector capex in manufacturing and infrastructure to capture the economy.

PLI Scheme: GOI approved the production-linked incentive (PLI) scheme for 10 key sectors to boost local manufacturing that could add USD 520 billion to the GDP in the next five years.

Corporate Tax Rate: To encourage ‘Make in India’ policy, corporate tax rate was reduced from 25% to 15% for new manufacturing firms to make it competitive across Asian Countries.

Reforms: Indian government has brought various reforms in Farm bill, Land and Labour for ease of doing business.

Disinvestment: The govt of India has announced divestments and privatization of select public sector companies and financial institutions to bring efficiency, raise resources and contain fiscal deficit.

Focus on Growth: Government of India has in the Union Budget has announced fiscal stimulus measures to help economy survive the Covid impact.

GOVT’S PROACTIVE STEPS : BUILDING BLOCKS IN LAST 2-3 YEARS

16Source: https://in.pinterest.com/

PLI TO BE A CATALYST FOR PRIVATE SECTOR INVESTMENTS

CategoryOverall PLI Incentive committed (Rs. Bn)

Committed/Likely Investment/Capex (Rs. Bn)

Mobiles 410 110

Pharma 150 100

Pharma – API/KSM 63 54

Pharma - Medical Devices 28 9

White Goods & LED 62 79

Solar PV 45 175

Telecom 122 30

Food 109 61

Automobile & Auto Components

570 400

IT Hardware 50 24

Speciality Steel 63 150

Textile 107 100

EV Battery 181 80

Total 1,960 1,371

• PLI likely to lead to capex of ~Rs.1.4tn over

the next 2-3 years

• It will reduce the dependence on imports

which is to the tune of ~Rs. 5tn (USD 70bn)

currently across 13 sectors.

• We believe PLI could fast track the capex

plans from the private sector at-least by two

years.

17Source: Sector PLI Gazette Notification, Spark Research

WHY CAPITAL SPENDING LOOKS POSITIVE

18Source: NHAI, NIP Report, Spark Research

1435

3067

4344 4335

7396

2222

3211

4788 ~5000

0

1000

2000

3000

4000

5000

6000

7000

8000

FY 14 FY 15 FY 16 FY 17 FY 18 FY 19 FY 20 FY 21 FY 22

Road Projects Awarded by NHAI (in kms)

Overall 68000 kms road to be constructed with total outlay of INR~19.6 lakh crore over FY20-25

The total amount to be spent through NIP in Railway Sector from FY20– FY25 will be INR ~14 lakh crore

Airports – (Project Summary)

ParticularsNo. of

projectsCapex over FY20-

FY25 (INR Bn)

Completely Greenfield Projects 8 361

Expansion and modernization existing airports

50 530

Total 58 892

3

8

FY21 FY26

Data Center Industry ($, bn)

Data Center spend is expected to reach $8bn in FY26E from $3bn inFY21, 22% CAGR

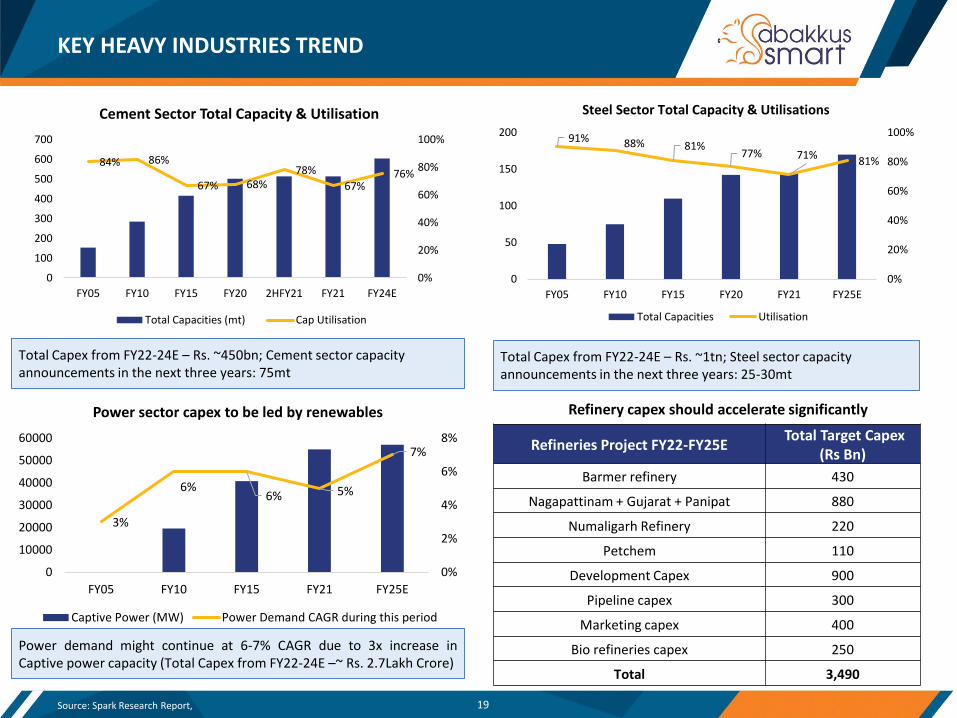

KEY HEAVY INDUSTRIES TREND

Power demand might continue at 6-7% CAGR due to 3x increase inCaptive power capacity (Total Capex from FY22-24E –~ Rs. 2.7Lakh Crore)

3%

6%6% 5%

7%

0%

2%

4%

6%

8%

0

10000

20000

30000

40000

50000

60000

FY05 FY10 FY15 FY21 FY25E

Power sector capex to be led by renewables

Captive Power (MW) Power Demand CAGR during this period

84% 86%

67% 68%78%

67%76%

0%

20%

40%

60%

80%

100%

0

100

200

300

400

500

600

700

FY05 FY10 FY15 FY20 2HFY21 FY21 FY24E

Cement Sector Total Capacity & Utilisation

Total Capacities (mt) Cap Utilisation

91% 88% 81%77% 71%

81%

0%

20%

40%

60%

80%

100%

0

50

100

150

200

FY05 FY10 FY15 FY20 FY21 FY25E

Steel Sector Total Capacity & Utilisations

Total Capacities Utilisation

Total Capex from FY22-24E – Rs. ~450bn; Cement sector capacity announcements in the next three years: 75mt

Total Capex from FY22-24E – Rs. ~1tn; Steel sector capacity announcements in the next three years: 25-30mt

Refineries Project FY22-FY25ETotal Target Capex

(Rs Bn)

Barmer refinery 430

Nagapattinam + Gujarat + Panipat 880

Numaligarh Refinery 220

Petchem 110

Development Capex 900

Pipeline capex 300

Marketing capex 400

Bio refineries capex 250

Total 3,490

Refinery capex should accelerate significantly

19Source: Spark Research Report,

20Source: Spark Research, Investec Securities research

32%

39%

42%

46%49%

51%54% 53%

50%

45%

42%

37% 38%35% 36% 37%

30%

35%

40%

45%

50%

55%

60%

Dec

-04

Sep

-05

Jun

-06

Mar

-07

Dec

-07

Sep

-08

Jun

-09

Mar

-10

Dec

-10

Sep

-11

Jun

-12

Mar

-13

Dec

-13

Sep

-14

Jun

-15

Mar

-16

Dec

-16

Sep

-17

Jun

-18

Mar

-19

Dec

-19

Sep

-20

Jun

-21

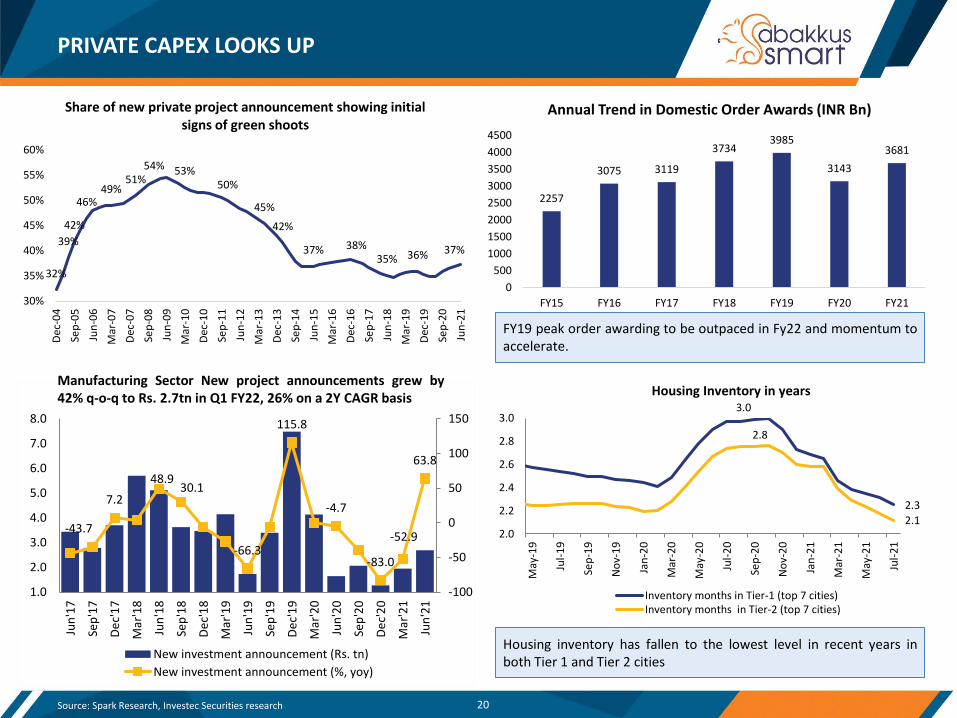

Share of new private project announcement showing initial signs of green shoots

PRIVATE CAPEX LOOKS UP

2257

3075 3119

37343985

3143

3681

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY15 FY16 FY17 FY18 FY19 FY20 FY21

Annual Trend in Domestic Order Awards (INR Bn)

FY19 peak order awarding to be outpaced in Fy22 and momentum toaccelerate.

-43.7

7.2

48.930.1

-66.3

115.8

-4.7

-83.0

-52.9

63.8

-100

-50

0

50

100

150

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Jun

'17

Sep

'17

De

c'1

7

Mar

'18

Jun

'18

Sep

'18

De

c'1

8

Mar

'19

Jun

'19

Sep

'19

De

c'1

9

Mar

'20

Jun

'20

Sep

'20

De

c'2

0

Mar

'21

Jun

'21

New investment announcement (Rs. tn)

New investment announcement (%, yoy)

3.0

2.3

2.8

2.12.0

2.2

2.4

2.6

2.8

3.0

May

-19

Jul-

19

Sep

-19

No

v-1

9

Jan

-20

Mar

-20

May

-20

Jul-

20

Sep

-20

No

v-2

0

Jan

-21

Mar

-21

May

-21

Jul-

21

Housing Inventory in years

Inventory months in Tier-1 (top 7 cities)Inventory months in Tier-2 (top 7 cities)

Housing inventory has fallen to the lowest level in recent years inboth Tier 1 and Tier 2 cities

Manufacturing Sector New project announcements grew by42% q-o-q to Rs. 2.7tn in Q1 FY22, 26% on a 2Y CAGR basis

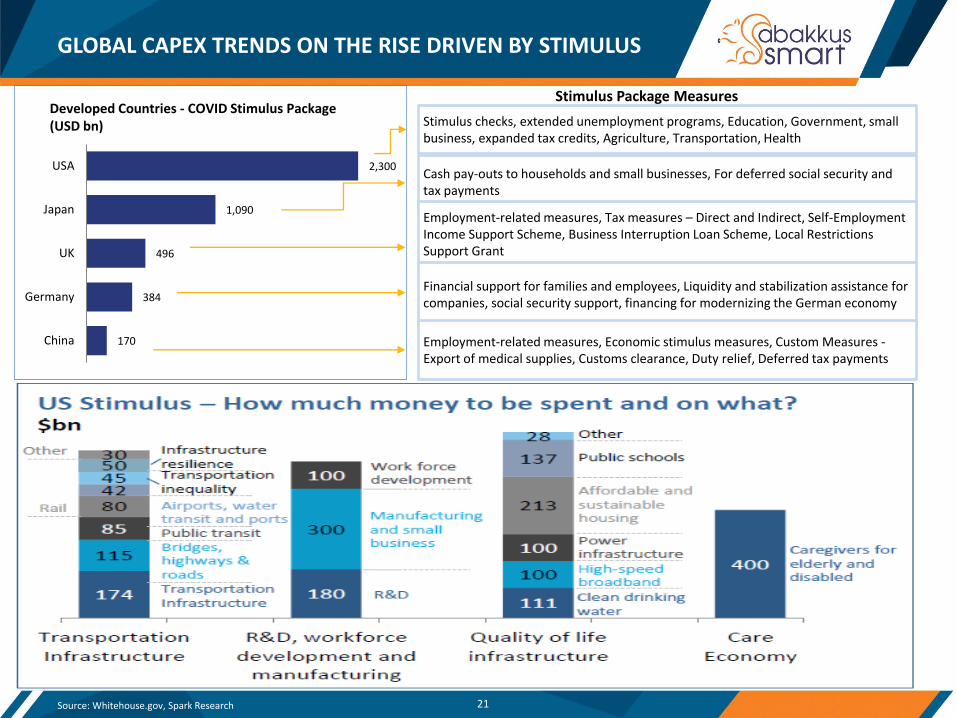

GLOBAL CAPEX TRENDS ON THE RISE DRIVEN BY STIMULUS

2,300

1,090

496

384

170

USA

Japan

UK

Germany

China

Developed Countries - COVID Stimulus Package(USD bn) Stimulus checks, extended unemployment programs, Education, Government, small

business, expanded tax credits, Agriculture, Transportation, Health

Cash pay-outs to households and small businesses, For deferred social security and tax payments

Employment-related measures, Tax measures – Direct and Indirect, Self-Employment Income Support Scheme, Business Interruption Loan Scheme, Local Restrictions Support Grant

Financial support for families and employees, Liquidity and stabilization assistance for companies, social security support, financing for modernizing the German economy

Employment-related measures, Economic stimulus measures, Custom Measures -Export of medical supplies, Customs clearance, Duty relief, Deferred tax payments

Stimulus Package Measures

21Source: Whitehouse.gov, Spark Research

22

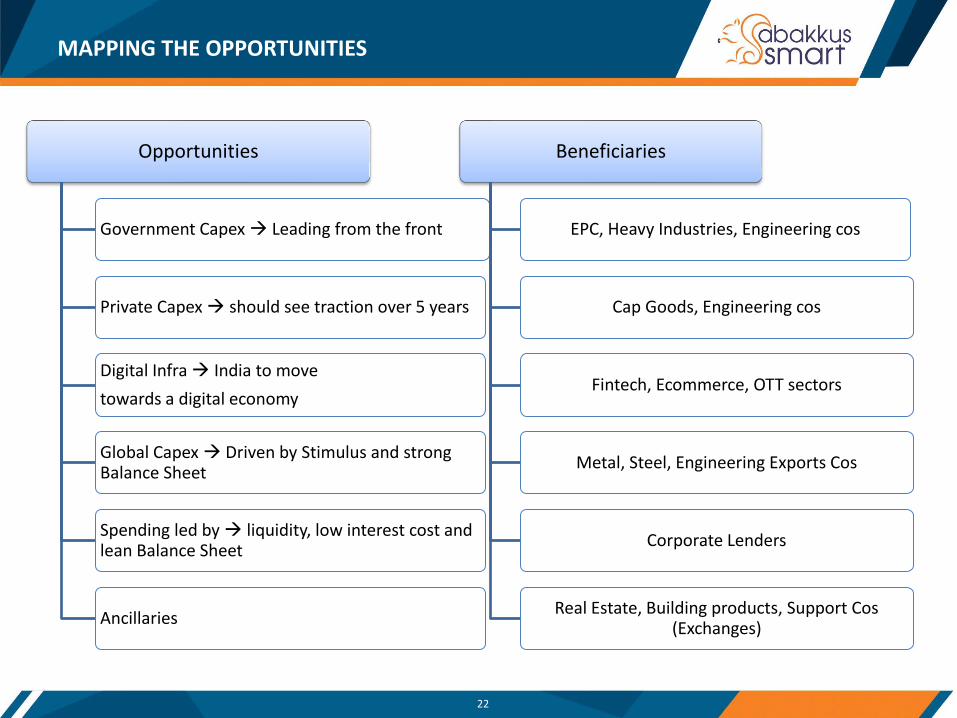

MAPPING THE OPPORTUNITIES

Opportunities

Government Capex → Leading from the front

Private Capex → should see traction over 5 years

Digital Infra → India to move

towards a digital economy

Global Capex → Driven by Stimulus and strong Balance Sheet

Spending led by → liquidity, low interest cost and lean Balance Sheet

Ancillaries

Beneficiaries

EPC, Heavy Industries, Engineering cos

Cap Goods, Engineering cos

Fintech, Ecommerce, OTT sectors

Metal, Steel, Engineering Exports Cos

Corporate Lenders

Real Estate, Building products, Support Cos (Exchanges)

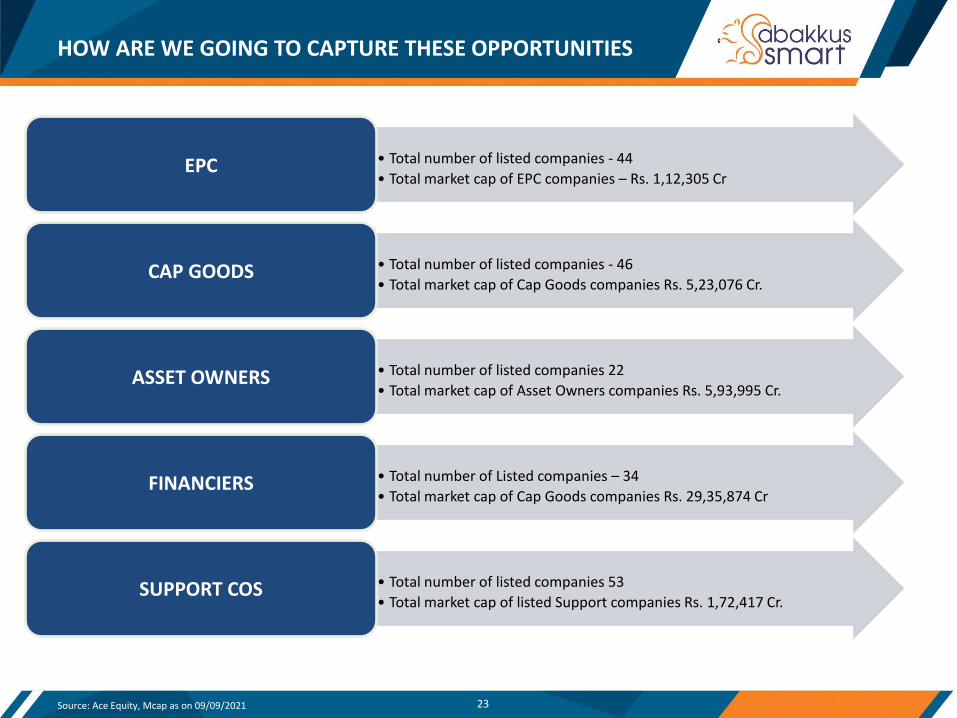

HOW ARE WE GOING TO CAPTURE THESE OPPORTUNITIES

23

• Total number of listed companies - 44

• Total market cap of EPC companies – Rs. 1,12,305 CrEPC

• Total number of listed companies - 46

• Total market cap of Cap Goods companies Rs. 5,23,076 Cr.CAP GOODS

• Total number of listed companies 22

• Total market cap of Asset Owners companies Rs. 5,93,995 Cr.ASSET OWNERS

• Total number of Listed companies – 34

• Total market cap of Cap Goods companies Rs. 29,35,874 CrFINANCIERS

• Total number of listed companies 53

• Total market cap of listed Support companies Rs. 1,72,417 Cr.SUPPORT COS

Source: Ace Equity, Mcap as on 09/09/2021

• Globally high and cheap liquidity will stay for long is a consensus view

• Inflation risks can creep in forcing central banks to revisit their monetary stance

• Rising commodity and other costs are a risk to corporate profitability and can impact earnings growth

• 3rd wave of medical emergency

• Re-emergence of global trade or currency war

• High Beta Sector, ONLY FOR HIGH RISK/AGGRESIVE INVESTORS

KEY MARKET RISKS

24

RISK FACTORS

• Company risk: The performance of the model portfolio will depend upon the business performance of the Portfolio Entity and its

future prospects. Investment Advisors focus on studying the business sustainability and studying the balance sheet will help in

mitigating these sector or company risks.

• Valuation risk: Investment Advisor will assess the Portfolio entities from varied valuation parameters in order to establish whether

the valuations are reasonable while creating the model portfolio and reassess the same from time to time.

• Market risk: Investment Advisor endeavours to create a portfolio of companies using bottom-up fundamental research rather than

trying to time the markets. However, the Investment Advisor will monitor the market and economic circumstances from time to

time that may affect the performance of the Portfolio entities.

• Sector concentrated Risk: Portfolio is concentration to few sectors and hence carries higher risk and not suitable for risk averse

investors

• Liquidity risk: While investing in equities and Portfolio Entities, liquidity constraints are potential near-term risk while investing and

disinvesting the Portfolio entities. The Investment Advisor endeavours to mitigate the risks by creating a diversified portfolio with a

medium to long term time horizon.

• Other risks: The advisory portfolio offered by the Investment Advisor is suitable for clients with “Aggressive”/ “High Risk” risk

profile. The Investment Advisory does not offer any assured / guaranteed returns. Investments in securities is subject to market risk.

25

DISCLOSURES AND DISCLAIMERS

26

This Key Information and Disclosure Document has been prepared inter-alia in pursuant to regulation 18 of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, as amended from

time to time (the Regulations) and the Circulars, Guidelines and instructions issued by SEBI thereunder from time to time. This document is intended only for the personal use of the prospective investors to whom

it is addressed or delivered and must not be reproduced or redistributed in any form to any other person without prior written consent of Abakkus Asset Manager LLP (the “Investment Advisor”). This document

does not purport to be all-inclusive / comprehensive, nor does it contain all the information which a prospective investor may desire for making decisions for engaging the Investment Advisor.

History, Present Business and Background

Abakkus Asset Manager LLP (‘Abakkus’) is a SEBI registered Portfolio Manager and Investment Advisor and offers portfolio management and advisory services to clients vide SEBI registration No. INP0006457 and

INA000015729 respectively and is also the Investment Manager of Abakkus Growth Fund, a SEBI registered Category III Alternative Investment Fund (AIF) vide SEBI registration No.IN/AIF3/18-19/0550.

Partners Name: (i) Mr. Sunil Singhania

Sunil Singhania, CFA, is the Founder of Abakkus Asset Management, LLP, an India-focused Asset Management Company established in 2018. Prior to this, in his role as Global Head – Equities at Reliance Capital

Ltd., he oversaw equity assets and provided strategic inputs across Reliance Capital Group of companies including asset management, insurance, AIF and offshore assets. And as CIO – Equities, Singhania led

Reliance Mutual Fund (now Nippon India Mutual Fund) equity schemes. Reliance Growth Fund (now Nippon India Growth Fund) grew over 100 times in less than 22 years under Singhania’s leadership.

Furthermore, he led Reliance Nippon Life Asset Management Ltd.’s (now Nippon Life India Asset Management) international efforts and was instrumental in launching India funds in Japan, South Korea, and the

UK, besides managing mandates from institutional investors based in the US, Singapore, and other countries. He is currently appointed on the IFRS Capital Market Advisory Committee. (2020-2023). He was the

Promoter of The Association of NSE Members of India; a body of stockbrokers. He served on the Global board of CFA Institute, USA (2013-2019) and as Chairman of the Investment Committee (2017-2019) of the

CFA Institute, USA. He also sat on CFA Institute’s Standards of Practice Council for six years and was the Founder of the Indian Association of Investment Professionals (now CFA Society India) and served as its

President for eight years. He is a CA rankholder and a CFA charterholder and graduated in commerce from the Mumbai University.

(ii) Abakkus Expert Professionals Private Limited: Abakkus Expert Professionals Private Limited is a Private Company, incorporated on 20 February 2018 in Mumbai under the Companies Act,2013. Its main objects

are to act as financial consultants, management consultants, and provide advice, services, consultancy in various fields viz. general, administrative, secretarial, commercial, financial, and legal. Abakkus Expert is

registered with PFRDA as Retirement Advisor.

Affiliation with other intermediaries

There are no affiliations with other intermediaries except that Abakkus has empanelled various financial intermediaries and / or financial institutions and / or individuals for promoting / distributing its various

financial product offerings including availing theirs advisory / distribution / on-boarding platform(s).

Disciplinary History / Complaint Status

(i) No penalties / directions have been issued by SEBI under the SEBI Act or Regulations made there under against Abakkus or its Partners, or employees relating to Investment Advisory services.

(ii) There are no pending material litigations or legal proceedings, findings of inspections or investigations for which action has been taken or initiated by any regulatory authority against the Abakkus or its

Partners, or employees

(iii) For latest update on complaints kindly visit website: www.abakkusinvest.com

DISCLOSURES AND DISCLAIMERS

27

Services offered and terms of offerings

(a) The Investment Adviser shall provide investment advice to the Clients relating to investing, purchasing, selling, or dealing in securities or investment products/asset classes such as shares, debentures, bonds,derivatives, securities instruments, structured products, units of MF/AIF/REIT/InvIT/ETF/PMS, private equity, alternative asset class such as real estate, commodities, angel investment, offshore investment etc.

(b) The Investment Adviser provides advice on investment portfolio containing or any other investment product suitable to the Client’s needs and on-going monitoring, periodic review, asset allocation and financialplanning including analysis of Clients’ financial position, identification of its financial goals and developing and recommending financial strategies to realise such goals.

(c) Investment Adviser undertakes that all such Investment Advisor services shall be offered to the client with no binding whatsoever and client shall be free to implement or execute the services with anydistributor/broker/intermediary of his/her/its choice.

(d) The performance related information stated by the Investment Adviser will be on a consolidated basis which would neither be verified nor approved by SEBI. The performance / returns of the stock acrossadvised individual portfolios may vary significantly from the data depicted by the Investment Adviser. No claims may be made or entertained for any variances between the performance depictions and that of thestock within individual client portfolios. Neither the Investment Adviser, nor its Partners, employees, affiliates shall in any way be liable for any variation noticed in the returns of individual portfolios. Performanceof Abakkus shall have no bearing on the expected performance of an Individual Client Portfolio. Abakkus also does not guarantee or assure any minimum or risk free returns. Past performance of the financialproducts, instruments and the portfolio may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Risk Factors

The value of the investments and the expected returns may be affected generally by factors affecting financial and securities markets, such as price and volume, volatility in interest rates, currency exchange rates,

changes in regulatory and administrative policies of the Government or any other appropriate authority (including tax laws) or other political, economic, and other developments as detailed below:

Portfolio Entities/ Companies Risk: The performance of the model portfolio will depend upon the business performance of the Portfolio Entities and Companies and its prospects. Investment Advisor focuses on

studying the business and the sustainability with focus on studying the balance sheet will help the Investment Advisor in mitigating these sector or company risks.

Valuation Risk: Investment Advisor will assess the Portfolio Entities from varied valuation parameters in order to establish whether the valuations are reasonable while creating the model portfolio and reassess the

same from time to time.

Market Risk: Investment Advisor endeavours to create a portfolio of Entities /Companies using bottom-up fundamental research rather than trying to time the markets. However, in order to mitigate Market Risk,

the Investment Advisor will monitor and analyse the market and economic circumstances from time to time that may affect the performance of the Portfolio Entities.

Liquidity Risk: While investing in equities and Portfolio Entities, liquidity constraints are potential near-term risk while investing and disinvesting the Portfolio Entities. The Investment Advisor endeavours to

mitigate the risks by investing creating a portfolio with a medium to long term time horizon.

Other Risks: The advisory portfolio offered by the Investment Advisor is suitable for clients with “Aggressive”/ “High Risk” risk profile. The Investment Advisory does not offer any assured / guaranteed returns.

Investments in securities is subject to market risk. Please read the Key Information and Disclosure Document carefully before investing.

The Investment Adviser shall not be liable or responsible for any loss or shortfall resulting on account of Non-Discretionary Investment Advice. The views represented by Investment Adviser should not be taken as

the basis for an investment decision.

DISCLOSURES AND DISCLAIMERS

28

Holdings and Disclosure of Interest

Abakkus or its affiliates or employees/partners or funds advised/managed by Abakkus may have same or contra positions in personal or fiduciary capacity the above securities/stocks. Investors should take caution

while executing the advice based on their risk/return profile and suitability.

Conflict of Interest

(i) Client understands that subject to the applicable laws, Abakkus may give advice or take action in performing its duties to other clients, or for its own accounts, that may or may not differ from advice given to or

acts taken for the Client. Abakkus is not obligated to recommend to the Client, any security or other investment that Abakkus may buy, sell, or recommend for any other client or for its own accounts.

(ii) Abakkus or its affiliates may be involved in other financial, investment or other professional activities which may on occasion cause conflicts of interest with the investment advisory services being provided to

the Client. These include serving as directors, officers, advisers, or agents of other companies.

(iii) In addition to the investment advisory services, the Client may also choose to avail any other services inter-alia related to Portfolio Management Services/Alternative Investment Fund Services as may be

provided by its affiliates or through its separate division(s)/entities. The Parties may have to accordingly govern themselves by the terms and conditions as may be laid down or applicable in case of the

aforementioned activities subject to the following:

• As an entity: Abakkus, for its own proprietary purposes may invest / divest in various securities / investments, from time to time at its own discretion which will be undertaken by a separate and dedicated

team. The said segregation will ensure avoidance of conflict of interest with regard to the investment advisory and related business of the Company. Such proprietary investment transactions may at times

be contrary to the investment advice or other related business or actions inter-alia due to reasons such as different risk profile, returns expectation, investment objective or risk perception of the entity

being advised

• As its business activities: Apart from providing investment advisory services through its separately identifiable division/entity called Abakkus Investment Advisor under Abakkus Smart Brand, Abakkus is also

engaged in providing various financial services and in connection with any advice on securities or investment products so serviced, Abakkus may earn fees or remuneration in form of management fees or

any other fees by whatever name called.

• As its Partners or employees: Abakkus, its partners or employees may also advice or be connected with any fund house, portfolio manager, mutual fund/asset management company, alternative investment

funds, broking company or any other entity or its partners or employees offering any financial product (which may be part of investment advice) or undertake any execution services and accordingly they

may earn management fees, for the same.

• Future business activity: During the course of business, as part of normal business activity, Abakkus, its partners or its affiliates may undertake any other business or register with SEBI or any other regulator

or body for conducting business activities that may be directly or indirectly connected with its long-term business objectives in line with its Object Clause inter alia including corporate advisory etc.

However, the Client shall not be under any obligation to avail the execution, or any other such services offered by Abakkus Smart or Abakkus Investment Advisors, the division of Abakkus or affiliate of Abakkus. All

fees and charges, wherever applicable, for such services shall be paid directly to execution service providers and not through the Investment Advisor.

DISCLOSURES AND DISCLAIMERS

29

Other Disclosures

The information shared by the Investment Adviser from time to time should not be construed as any form of advice, recommendation, or suggestion, to buy or sell any securities or financial instruments or avail any

services to any individual or entity. Investment Adviser shall not be responsible for the loss or damage (financial or otherwise) caused due to incorrect, inaccurate, or erroneous information, details or data stated in the

document(s).

Abakkus retains all the rights in relation to all information contained in the document(s) shared from time to time.

Abakkus operates from within India and is subject to Indian laws and any dispute shall be resolved in the courts of Mumbai, Maharashtra only.

Abakkus declare that the data and analysis provided shall be for informational purposes. The information contained in the analysis shall been obtained from various sources and reasonable care would be taken to

ensure sources of data to be accurate and reliable. Abakkus will not be responsible for any error or omission in the data or for any losses suffered on account of information contained in the analysis. While Abakkus will

take due care to ensure that all information provided is accurate however Abakkus neither guarantees/warrants the sequence, accuracy, completeness, or timeliness of the report. Neither Abakkus nor its affiliates or

their partners, directors, employees, agents, or representatives, shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this analysis or the contents or any systemic errors

or discrepancies or for any decisions or actions taken in reliance on the analysis. Abakkus does not take any responsibility for any clerical, computational, systemic, or other errors in comparison analysis.

The Investment Advisor warrants that the contents of this Key Information and Disclosure Ddocument are true to the best of the knowledge, belief, and information of the Partners of Abakkus , however, assume no

liability for the relevance, accuracy, or completeness of the contents herein.

The Investment Advisors (including its affiliates) and any of its Partners , officers, employees, and other personnel will not accept any liability, loss, damage of any nature, including but not limited to direct, indirect,

punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this document in any manner whatsoever.

This document may include certain forward-looking statements which contain words or phrases such as “believe”, “expect”, “anticipate”, “estimate”, “intend”, “plan”, “objective”, “goal”, “project”, "endeavor" and

similar expressions or variations of such expressions that are forward-looking statements. Actual results may differ materially from those suggested by the forward-looking statements due to risks, uncertainties, or

assumptions. Abakkus takes no responsibility of updating any data/information.

This document cannot be copied, reproduced, in whole or in part or otherwise distributed without prior written approval of the Investment Advisor.

Abakkus Investment Advisors or Portfolio Manager (including its affiliates) may offer services in nature of advisory, consultancy, sponsorship of funds, investment management of funds including category III AIF under

SEBI registration number IN/AIF3/18-19/0550 for Abakkus Growth Fund and all its schemes, etc., which may be in conflict with the activities of portfolio management services.

Prospective clients are advised to review this document, Advisory Agreement, presentation(s), and other related documents carefully and in its entirety. Prospective clients should make an independent assessment,

and consult their own counsel, business/investment advisor and tax advisor as to legal, business and tax related matters concerning this document, the Advisory Agreement, and the other related documents before

becoming interested in the Advisory Portfolio.

Tenure or investment horizon of typically investments advisory portfolio will have a medium to long term time horizon of 3-5 years. The Investment Advisor may, at its discretion if it deems fit, advise any Portfolio

Investment beyond 5 years. The risks disclosed may affect portfolio performance.

The information contained in this document has been prepared for general guidance and does not constitute a professional advice /assurance and no person should act upon any information contained herein without obtaining specific professional advice/Assurance. Neither the Investment Advisor nor its Affiliates or advisors would be held responsible for any reliance placed on the content of this document or for any decision based on it. Each existing / prospective client , by accepting delivery of this document agrees to the foregoing. The Investment portfolio are subject to several risk factors including but not limited to political, legal, social, economic, and overall market risks. The recipient alone shall be fully responsible/are liable for any decision taken on the basis of this document. The Investment Advisor is also registered with SEBI as a Portfolio Manager and Investment Manager to SEBI registered Category III Alternative Investment Fund. Abakkus, its partners employees, PMS clients and AIF scheme may have existing exposure to the stocks that form part of the investment advisory portfolio. Further, in view of the investment objective and strategy of the PMS clients and AIF scheme there may be situations where Abakkus may be selling a stock which is part of the advisory portfolio.

DISCLOSURES AND DISCLAIMERS

30

The advisory portfolio offered by the Investment Advisor is suitable for clients with “Aggressive”/ “High Risk” risk profile. The Investment Advisory does not offer any assured / guaranteed returns. Investments in

securities is subject to market risk.

The information can be no assurance that future results or events will be consistent with this information. Any decision or action taken by the recipient based on this information shall be solely and entirely at the risk of

the recipient. The distribution of this information in some jurisdictions may be restricted and/or prohibited by law, and persons into whose possession this information comes should inform themselves about such

restriction and/or prohibition and observe any such restrictions and/or prohibition. Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. Abakkus will not

treat recipient/user as customer by virtue of their receiving/using this report. Neither Abakkus nor its affiliates, directors, partners, employees, agents, or representatives, shall be responsible or liable in any manner,

directly or indirectly, for the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the information. The person accessing this information specifically agrees to exempt

Abakkus or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Abakkus or any of its affiliates or employees responsible for any such misuse and

further agrees to hold Abakkus or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and

delays.

Contact Us:

Website: www.abakkusinvest.com |Email: [email protected] | Tel: 022-68846600

Corporate and Registered Address:

Abakkus Corporate Center, 6th Floor, Param House, Shanti Nagar, Near Grand Hyatt, Off Santacruz Chembur Link Road, Santacruz East, Mumbai – 400055 LLPIN: AAM-2364; RIA Registration SEBI Number:

INA000015729

Principal Officer/Compliance Officer Details

Biharilal Deora , Phone no. +91 22 6884 6604,

For Queries / Grievances

Email – [email protected]; [email protected]

THANK YOU

31