990’s do matter!

DESCRIPTION

990’s DO Matter!. All materials here have been developed (and are presented) by: Eve Borenstein Borenstein & McVeigh (BAM!) Law Office LLC Eve Rose Borenstein, LLC [prior permission is required for reprint/use] Funding for this presentation has been generously provided by - PowerPoint PPT PresentationTRANSCRIPT

© 2008, ERB LLC

990’s DO Matter!

All materials here have been developed (and are presented) by:

Eve BorensteinBorenstein & McVeigh (BAM!) Law Office

LLCEve Rose Borenstein, LLC

[prior permission is required for reprint/use]

Funding for this presentation has been generously provided by

The Otto Bremer Foundation

2

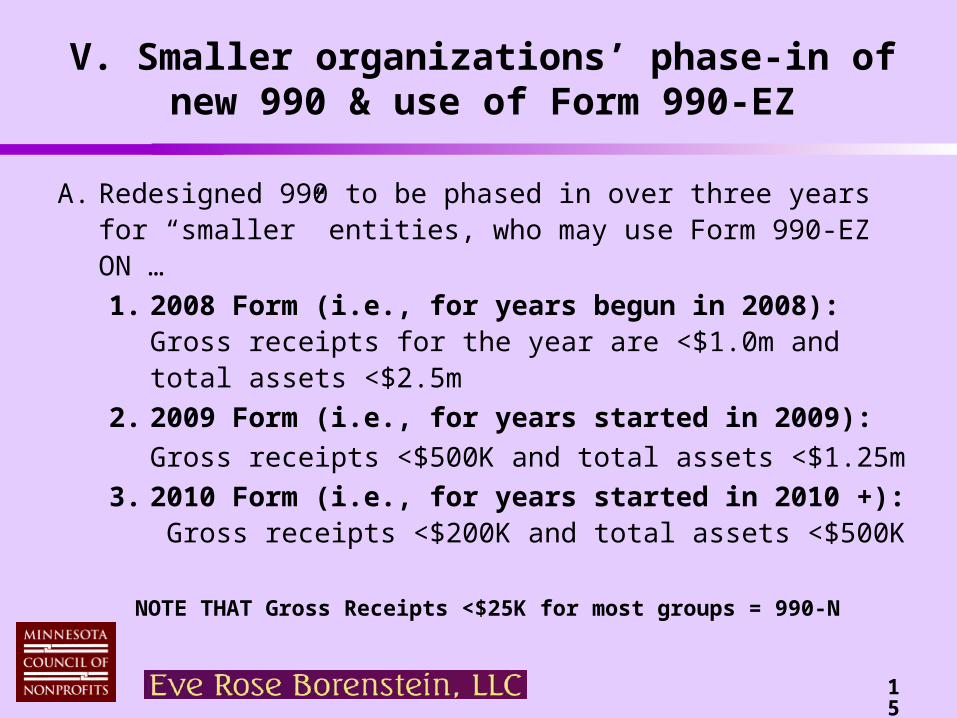

I-a. What’s “the deal” with the current and Redesigned Form 990?

A. 990 series of Forms are the “annual return” for all* tax-exempt organizations . . . . In its ‘current’ incarnation (2007 and prior years’), the Form 990 is/was:

1. “a disaster” [that’s a direct quote from IRS officials];

2. of unmanageable structure/design (a result of a decade of Congress’ mandated “add-on’s” and IRS’ attempts to adapt Form to new exam approaches);

3. truly a public accountability vehicle, not “just” a financial statement;*there is a major exception: 501(c)(3)’s with private foundation status file the Form 990-PF

3

I-a. What’s “the deal” with the current and Redesigned Form 990?

4. a lengthy read with no table of contents: “one-size-fits-all” approach drives 9 page Form (on top of which c3-filers add the 7 page Schedule A) and tons of lines demand “attach a statement”; and

5. full of suffocating minutiae, statements are hard to find, and result meets no one’s needs.

B. Although an abbreviated alternative was (and is) available to filers with smaller “gross receipts” (the 3-page Form 990-EZ), the “-EZ” does not save as much preparation time as one could infer from its shorter

number of pages (especially for c3 filers).

4

I-a. What’s “the deal” with the current and Redesigned Form 990?

C. Form 990 has become THE compliance and accountability tool accessible to both regulators and public.

1. 990’s (as-filed) ARE read:

a. Know of the “Guidestar” factor (enormous public use of that website – www.guidestar.org – to peruse Forms – ~14,000 a day!)

b. As of 1999, Guidestar posts the as-filed-with-the-IRS 990’s (and 990-EZ’s and 990-PF’s), tying each organization to the IRS’ Exempt Organizations “master file”

5

I-a. What’s “the deal” with the current and Redesigned Form 990?

2. Why are 990’s read? Of interest is:

a. gossip (chiefly, salaries)

b. fodder for whistleblowers

c. info for competitors

3. Note expectations are now high on part of regulators (big 3 = IRS/Congress, State offices with jurisdiction over those who are “charitably soliciting” and, finally, “court of public opinion”) that self-reporting accomplished on Form will not only be complete, but accurate!

6

I-a. What’s “the deal” with the current and Redesigned Form 990?

D. Form 990’s data does, for those who know how to read the current Form, provide a “thru the looking glass” view of organization. Upon the Form, filers roadmap:

1. what they got done during the year (was/remains Part III – Program Service Accomplishments; note acronym is same as ‘public service announcement’)

2. at what cost (was Part II, now on Redesigned 990’s front page summary & 2nd-to-last-page’s Part IX)

3. with what monies (was Part I, now on Redesigned 990’s front page summary & 3rd-to-last page’s Part VIII)

7

I-a. What’s “the deal” with the current and Redesigned Form 990?

4. all of above occurring on whose watch (filer’s list the year’s legal/quasi-legal managers), who got paid what (filer’s show their compensation); this Part is referred to as the listing of “TDOKE’s” / TDOKE = Trustee/Director, Officer, Key Employee (was Part V, now on Redesigned 990’s Part VII)

5. and, for c3-filers, disclosing also “High 5” employees (reaching folks NOT on TDOKE list), as well as contractors, and their pay (was at Schedule A’s Part I, now on Redesigned 990’s Part VII)

8

I-a. What’s “the deal” with the current and Redesigned Form 990?

a. IMPORTANT!: The Redesigned 990 requires “High 5” employees and contractors be disclosed by ALL filers (no longer just by 501(c)(3)’s!)

6. year-end financial posture (was Part IV, now on Redesigned 990’s front page summary and last page’s Part X)

7. Entire rest of Form is “turn yourself in” versus “applaud yourself for compliance” relating to “tax” attributes or compliance mandates (best case, this info is checklist for management; worst case, is fodder for whistle-blowers or red-flag for regulators)

9

I-a. What’s “the deal” with the current and Redesigned Form 990?

E. Achilles’ heel for IRS has been current Form’s illogical lay-out which defies and/or contradicts primacy of regulators’ key priorities: what gone done, with what monies accessed and disbursed, who’s in charge and how well are they running the show.

F. Achilles’ heel for exempt organizations in preparing Form has been failure to “own” key arenas, leaving all-too-often to professional preparers the work of:

1. Fleshing out program service accomplishments

2. Correctly inputting TDOKE’s and High 5’s, and (for c3’s:) tracking insider-transactions & (for all:) loans

10

I-a. What’s “the deal” with the current and Redesigned Form 990?

3. Properly disclosing fundraising-related in-flows & out-flows (especially on events and sales, where filers must show gross receipts – including bifurcating between “purchase” versus “true gift” revenues – and direct event/sales expenses which are different than overall fundraising expenses)

4. Understanding IRS’ conventions for financial statement reporting (e.g., donated services or discounted access to services/equipment/facilities are NOT included, distinction between what is a “true” grant versus what is sale of expertise)

11

I-a. What’s “the deal” with the current and Redesigned Form 990?

5. Documenting basis for compliance with various tax-exemption mandates, such as:

a. required solicitation disclosures

b. application (or not) of “unrelated business income tax” (a/k/a “UBIT”) to organization’s non-gift/grant revenues

c. for c3’s/c4’s, reach of “intermediate sanctions” tax to so-called “excess benefit transactions”

d. for c3’s, operating within “permissible lobbying limits”

12

I-a. What’s “the deal” with the current and Redesigned Form 990?

G. And finally, present Form 990 is rather opaque in disclosing arenas of operations Congress and/or IRS has expressed interest in reviewing:

1. Non-cash (i.e., property) contributions – e.g., artwork or other items held in collections, conservation easements, taxidermied animals!

2. Fundraising practices and payments (particularly in using agents and professional fundraisers)

3. Setting executives’ compensation and managing insider transactions

13

I-b. What’s the deal with YOUR Prior-filed 990’s?

A. Let’s be honest in reviewing the following questions:

1. who joins exempt organization Boards with the goal of having the group file the best 990 ever?

2. by whom and when does the information the 990 requires get culled?

3. what systems are in place during each tax year to document the necessary information that will be reported upon after the year closes?

B. Whether it’s internal staff OR an external professional who is preparing the Form, the dilemma is the same:

14

I-b. What’s the deal with YOUR Prior-filed 990’s?

1. different players hold YOUR information . . .

a. program service accomplishments and overall activities undertaken will be data that program office typically holds

b. finance department has data on quantified in-flows and out-flows (including compensation)

c. fundraising staff/committee has info on who gave what and, for special events or activities, what was expended along the way

d. those staffing the Board have info on Board/ Officers’ service & “conflict of interest” practice

15

I-b. What’s the deal with YOUR Prior-filed 990’s?

2. and accessing that information is time-consuming and challenging

a. program activities are often recorded by grant or program, and not necessarily tied to 990 year

b. finance department and fundraising staff/committee operate in different spheres, both may not be familiar with tax rules or each other’s definitions

c. key staff face tension in mandating info from Board members (and Officers), may not be privy to all compensation info or transaction details

16

I-b. What’s the deal with YOUR Prior-filed 990’s?

3. PLUS, pure “tax rules” and 990-reporting needs may not be known/tracked throughout the year, witness that 501(c)(3)’s:

a. need to capture data on their lobbying to pass laws (same is permitted but not “too much”)

b. report “insider transactions”, including “excess benefit transactions”

c. track their transactions with other exempts who are NOT (c)(3), and

d. explain how they fit nonprivate foundation standards

17

I-b. What’s the deal with YOUR Prior-filed 990’s?

4. ALL filers (not just c3’s) face at least 3 major (and tons of minor) “tax rules” and 990-reporting needs that need be known/tracked; the major ones are:

a. solicitation disclosure requirements (these are different for c3’s vs. non-c3’s)

b. reporting on TDOKE’s being paid by “related organizations”

c. reporting revenue-generating activities as either “substantially related” (to organization’s accomplishments) OR as taxed under, or excepted from, “unrelated business income tax”

18

I-b. What’s the deal with YOUR Prior-filed 990’s?

C. Mea culpa should be the key phrase ALL filers employ in looking back at already-filed Forms 990.

1. Were you to find areas of the 990 that are not properly fleshed out or documented, doing better the next time is the 21st Century NEED.

19

I-c. IRS’ Goals in Modernizing the Form 990

A. Change having the “big picture” from the Form be opaque or difficult to grasp by filers/readers:

1. Layout emphasizes “key” priorities; makes self-evident that Form is more than financial statement

2. Reporting on activities-operations “of interest” to regulators now occurs via structured statements (via Schedules that only apply to those conducting same), undoing “one-size-fits-all” prior approach

B. Take advantage of the Form as vehicle for public accountability and transparency . . .

20

I-c. IRS’ Goals in Modernizing the Form 990

1. have the Form promote education of and behavior modification within the filing sector, particularly through the new reporting questions on governance practices and management policies

2. provide key “snapshot” info on front page

3. use stand-alone Schedules specific to activities (such as insider transactions), rather than numbers

C. Place the responsibility for appropriate preparation on the filer, rather than outside paid preparers

D. Serve IRS’ needs as data-mining source overall and to identify potential single-issue audit examinees

21

I-d. IRS’ Reality in Modernizing the Form 990

Redesign process of IRS initiated 2006; draft-for-public-comment released June 2007. ‘Final’ (meaning-post

comment period) released late December 2007.

This ‘final’ Form is one in use on tax years begun in 2008.

The Redesigned 990 takes existing Form’s 9 pages [&Sched. A (for 501(c)(3)’s only) & Sched. B (info on donors)]

Replaces same with –

11 page “Core Form” and 16 Schedules

22

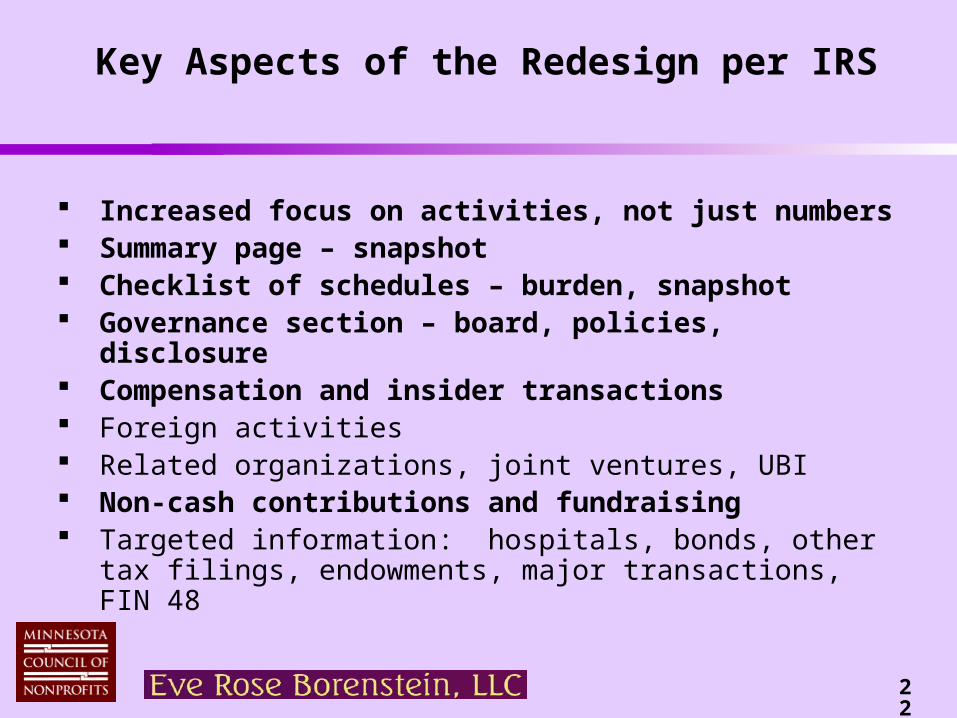

Key Aspects of the Redesign per IRS

Increased focus on activities, not just numbers Summary page – snapshot Checklist of schedules – burden, snapshot Governance section – board, policies, disclosure Compensation and insider transactions Foreign activities Related organizations, joint ventures, UBI Non-cash contributions and fundraising Targeted information: hospitals, bonds, other tax filings,

endowments, major transactions, FIN 48

23

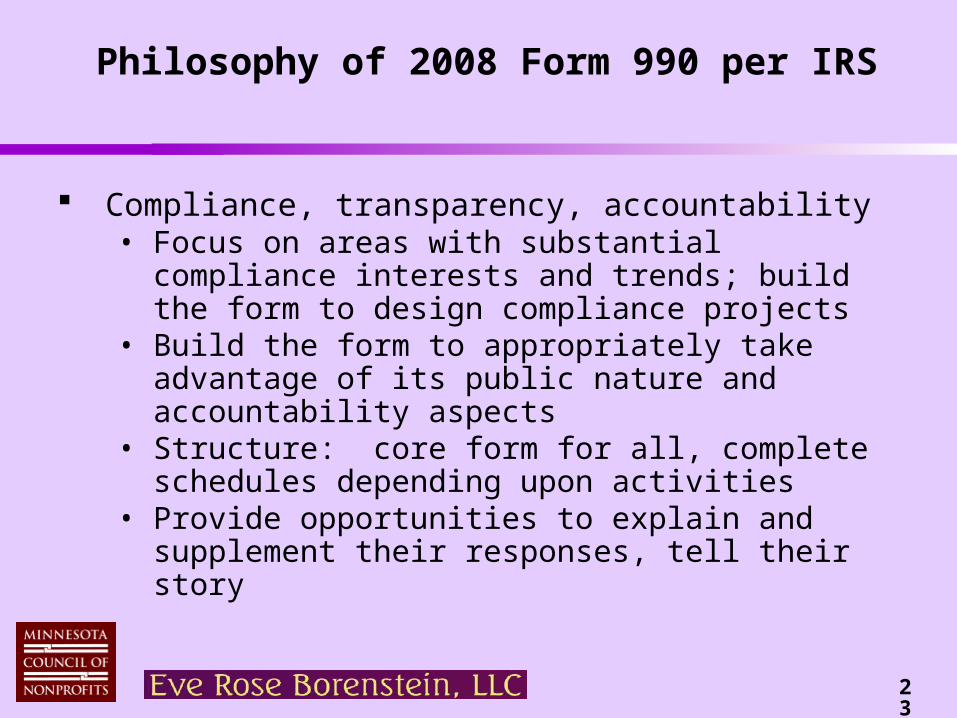

Philosophy of 2008 Form 990 per IRS

Compliance, transparency, accountability• Focus on areas with substantial compliance interests

and trends; build the form to design compliance projects

• Build the form to appropriately take advantage of its public nature and accountability aspects

• Structure: core form for all, complete schedules depending upon activities

• Provide opportunities to explain and supplement their responses, tell their story

24

A. Order of “core form” tracks relative priority of reporting concerns:

1. Program Service Accomplishments (Part III, entirety of page 2). Here is Form’s first “substantive” page as Parts I & II on 1st page provide “snap shot” info (pulled up from Form’s following substantive parts) and signature blank, respectively.

2. Parts IV & V are “checklists” of everything to include on Form and file otherwise. Pages 3-5 thus = paperwork “reminders” (had to go somewhere!)

3. Part VI (page 6) = new Governance Part

II-a. Brief Intro to the Redesigned Form 990

25

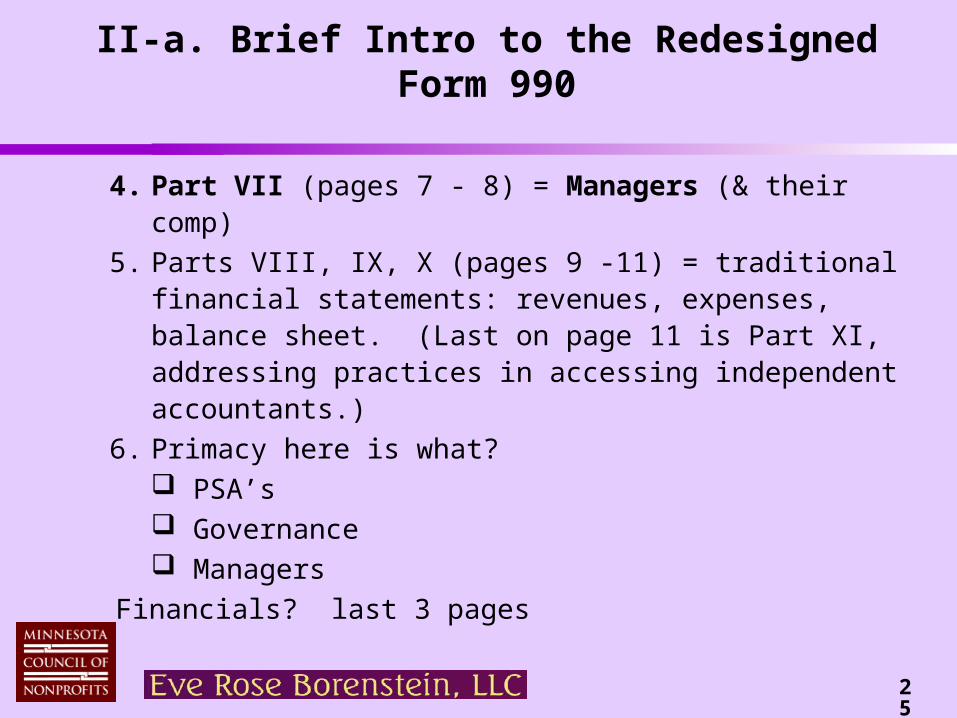

4. Part VII (pages 7 - 8) = Managers (& their comp)

5. Parts VIII, IX, X (pages 9 -11) = traditional financial statements: revenues, expenses, balance sheet. (Last on page 11 is Part XI, addressing practices in accessing independent accountants.)

6. Primacy here is what? PSA’s Governance Managers

Financials? last 3 pages

II-a. Brief Intro to the Redesigned Form 990

26

II-a. Brief Intro to the Redesigned Form 990

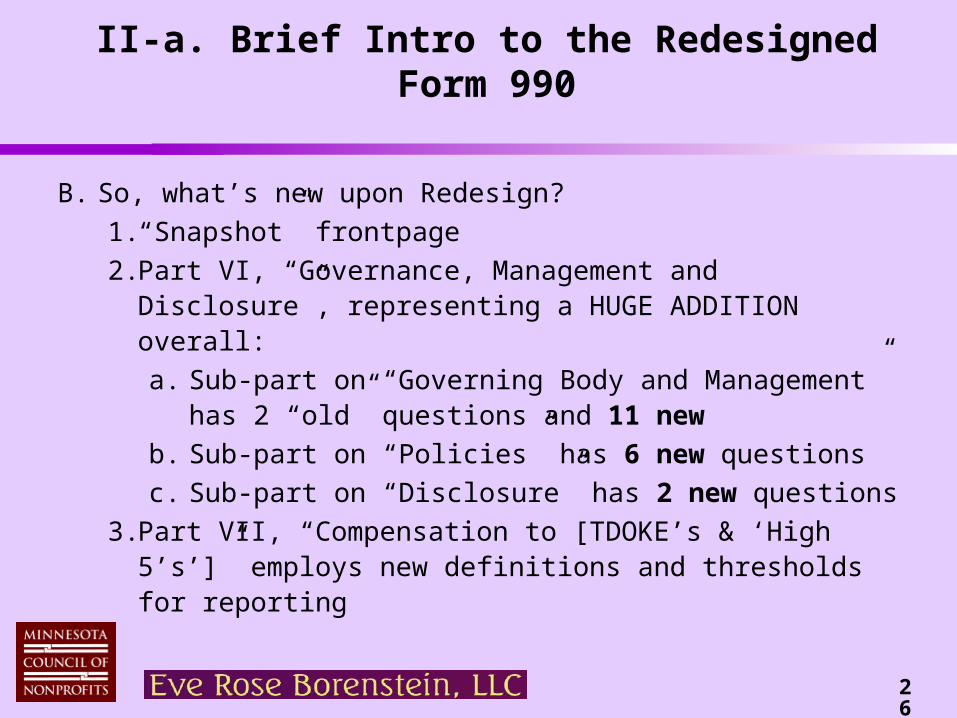

B. So, what’s new upon Redesign?

1. “Snapshot” frontpage

2. Part VI, “Governance, Management and Disclosure”, representing a HUGE ADDITION overall:

a. Sub-part on “Governing Body and Management” has 2 “old” questions and 11 new

b. Sub-part on “Policies” has 6 new questions

c. Sub-part on “Disclosure” has 2 new questions

3. Part VII, “Compensation to [TDOKE’s & ‘High 5’s’]” employs new definitions and thresholds for reporting

27

II-a. Brief Intro to the Redesigned Form 990

4. Employ of “overflow” schedule – Schedule O – the site at which filers provide narration (sometimes as mandated, other times by their own choice as an “opportunity”) of their individualized circumstances.

a. In essence, Schedule O exists as the 12th page of the Core Form.

b. It is an “outpost” where one supplements and/or “owns” (a verb akin to “confess”) its practices and circumstances related to:

new/changed/ended program activities; ‘did not comply’ or public relations explanations; myriad of governance “our circumstances”; explanation of late filing; details if return is amended

28

II-a. Brief Intro to the Redesigned Form 990

5. New schedule, L: site for disclosing fact of loans (but only those outstanding at yearend) or business transactions with or providing grants/assistance to “interested persons”.

6. New schedule, R: names filer’s related organizations and reports flow of funds between them and filer

7. Reporting on fundraising events/activities is now part of new schedule, G. This is also site for new disclosures on use of professional fundraisers.

8. New schedule, M: reports on receipts of noncash (i.e., property, securities) contributions and practices

29

II-a. Brief Intro to the Redesigned Form 990

C. Two things are key “needs to know” in planning for 2008 990:

1. Need know “related organizations” per Schedule R’s definitions. Schedule completion is only part of the equation, as “need” here relates to reporting comp provided by them to (and in certain cases, transactions with) your TDOKE’s and High 5’s.

a. Relatively simple definitions are used – control by one group over another (measured at >50%); supporting-supported orgs (under 509(a)(3); or operating as 1 of 3 (or less) general partners

30

2. Since behavior modification is very much a part of the new Part VI, all filers should begin (ideally IN tax year 2008) planning for three key questions: a. How and via what process do they review their top

management official’s compensation? (i.e., the CEO or Executive Director; those paying other officers/key employees have that same question apply there too)

b. Two-part question: will they have made a pre-filing disclosure of the 990 to their Board of Directors? AND: how DO they review the Form 990 before it is filed?

c. What practices, if any, do they employ to monitor and enforce the organization’s conflict of interest policy?

II-a. Brief Intro to the Redesigned Form 990

31

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

A. Appropriate reporting of one’s “program service accomplishments” (Part III of the Form; now also referred to as “program service achievements”)

1. This Part of Form has always called for quantitative measures to be reported (except with research or arenas where same are not susceptible of measure).

2. 2007 and prior years’ Form lists 4 largest programs; Redesign lists 3 largest programs. Size measure “to make the list” uses dollars/materials expended (in other words, program expenditures per Form 990, thus not included are donated services/access).

32

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

B. Part III now requires filers to note programs/operations that were not discussed on filer’s exemption application or reported (with respect to new activities) on a PRIOR Form 990; and also to disclose abandoned programs.

1. “New” methods of conducting programs was subtly asked for on 2007 Form for first time. New inquiries at questions 2 and 3 serve as an ‘update’ of exemption application, on an ongoing basis.

2. Having 990 ask for this info now abrogates determination letter’s mandate to “inform Cincinnati” of such changes in operations.

33

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

C. Part III’s “program service accomplishments” (Redesign inputs the “largest 3” programs at Lines 4a-4c) are the most important narrative disclosure all filers must make!

1. 1st visible self-disclosure AFTER the new summary page, quantifies WHAT the organization did in line with its exempt status programs 1, 2, and 3 (assuming it conducts multiple programs). a. Filers are directed to Schedule O to summarize the

programs not making the “largest 3” (i.e., 4 + on).

b. Filers may use Schedule O to note program(s) missing from “largest 3” due to 990’s measure of hard-dollars/materials, missing volunteered time, etc.

34

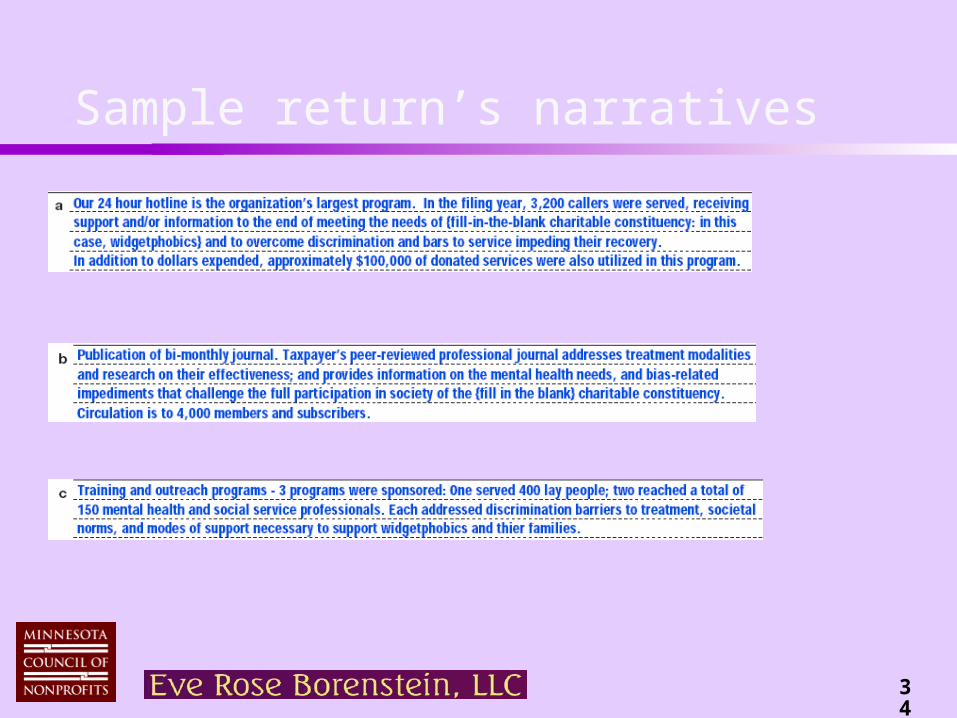

Sample return’s narratives

35

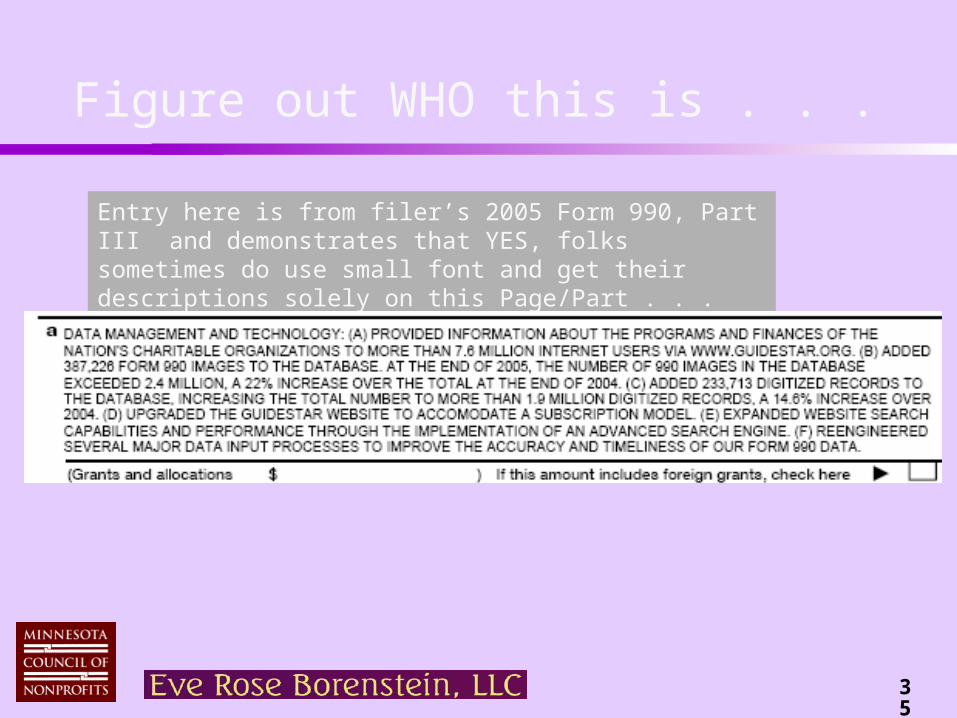

Figure out WHO this is . . .

Entry here is from filer’s 2005 Form 990, Part III and demonstrates that YES, folks sometimes do use small font and get their descriptions solely on this Page/Part . . .

36

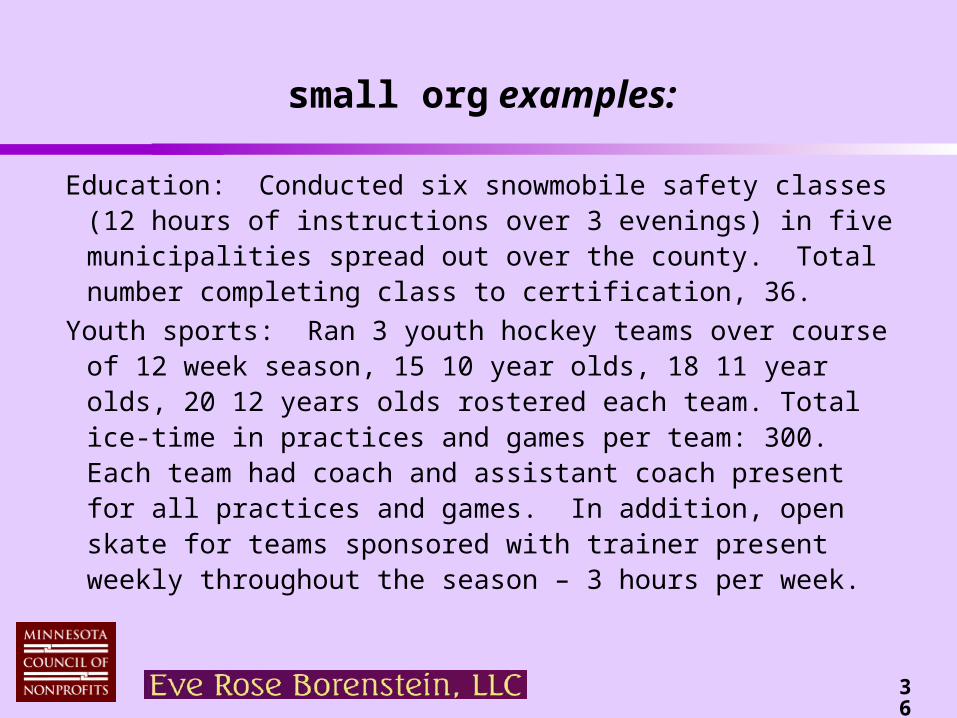

small org examples:

Education: Conducted six snowmobile safety classes (12 hours of instructions over 3 evenings) in five municipalities spread out over the county. Total number completing class to certification, 36.

Youth sports: Ran 3 youth hockey teams over course of 12 week season, 15 10 year olds, 18 11 year olds, 20 12 years olds rostered each team. Total ice-time in practices and games per team: 300. Each team had coach and assistant coach present for all practices and games. In addition, open skate for teams sponsored with trainer present weekly throughout the season – 3 hours per week.

37

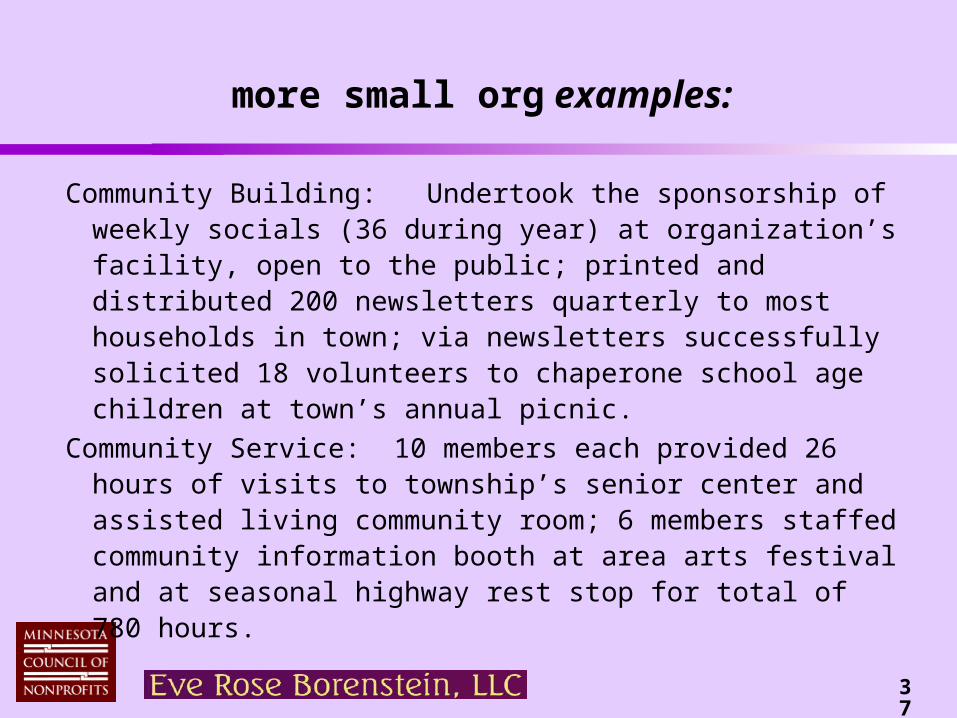

more small org examples:

Community Building: Undertook the sponsorship of weekly socials (36 during year) at organization’s facility, open to the public; printed and distributed 200 newsletters quarterly to most households in town; via newsletters successfully solicited 18 volunteers to chaperone school age children at town’s annual picnic.

Community Service: 10 members each provided 26 hours of visits to township’s senior center and assisted living community room; 6 members staffed community information booth at area arts festival and at seasonal highway rest stop for total of 780 hours.

38

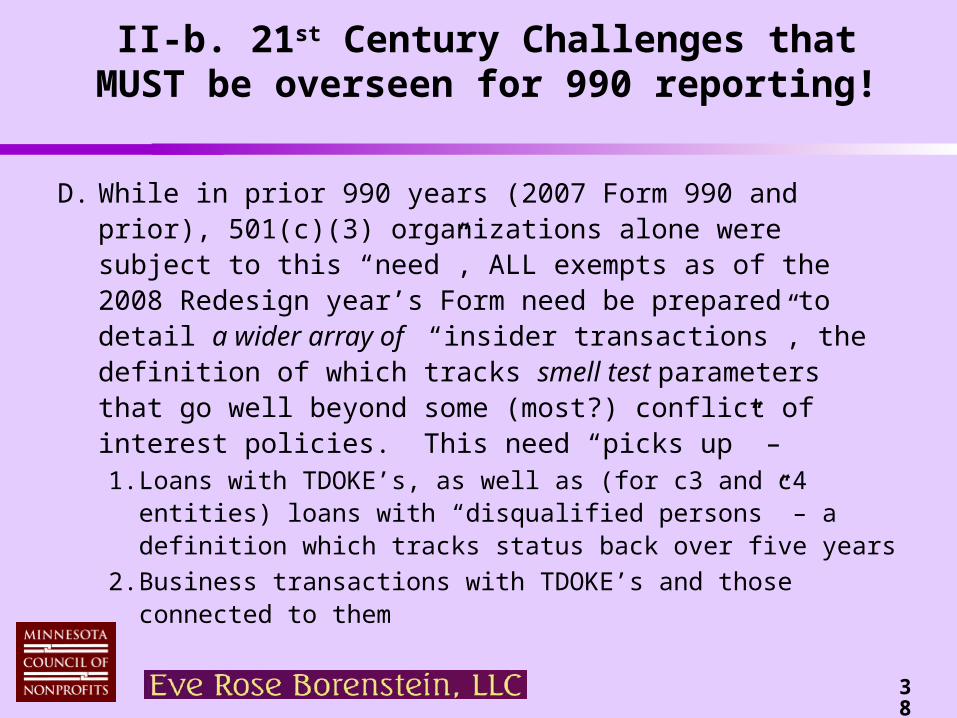

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

D. While in prior 990 years (2007 Form 990 and prior), 501(c)(3) organizations alone were subject to this “need”, ALL exempts as of the 2008 Redesign year’s Form need be prepared to detail a wider array of “insider transactions”, the definition of which tracks smell test parameters that go well beyond some (most?) conflict of interest policies. This need “picks up” – 1. Loans with TDOKE’s, as well as (for c3 and c4 entities)

loans with “disqualified persons” – a definition which tracks status back over five years

2. Business transactions with TDOKE’s and those connected to them

39

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

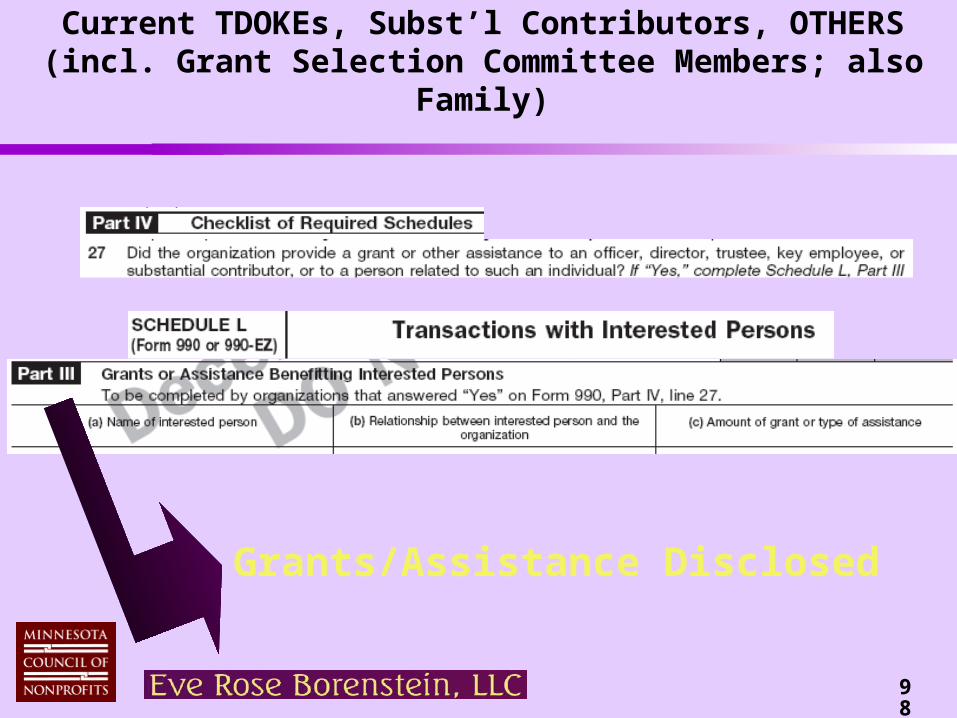

3. Grants or assistance being provided to TDOKE’s, substantial contributors AND grant selection committee members, as well as parties connected to them

4. And finally, (c)(3) and (c)(4) entities must be prepared to “turn in” – by name – disqualified parties [i.e., those who have been in a position of “substantial influence” over the organization in the prior 60 months (or whom are related to such parties)] were they to have received an excess benefit in transacting with the organization in the filing year, or have been discovered to have received an excess benefit in the course of a prior year.

40

E. Re fundraising, “smart” systems need be in place to:

1. Accept and record non-cash contributions (non-cash = property; for example, publicly-traded stock or items such as presenter’s “ugly candlesticks” to be ‘sold’ at silent auction)

2. Maintain complete information on donors’ identity (note this is the one arena of 990 input NOT open for public inspection)

3. Properly set and note “exchange” portion on special events/sales

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

41

F. 2008 Form 990 requires ALL filers know their “related organizations” and disclose their name/t.i.n./activities (and some further info). “Related organizations” are measured via Schedule R’s definition which pick up “parents”, “subsidiaries”, “brother”/“sister”, or those who are “supported” to “supporting” (or vice versa) under 509(a)(3). Also counted are partnerships where the filer is a general amongst 3 or fewer general partners.1. Definition of control used for finding parent-subsidiary-

brother/sister is >50% stock/Board.

2. Redesign also focuses on UNRELATED joint ventures – organizations taxable as partnerships

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

42

II-b. 21st Century Challenges that MUST be overseen for 990 reporting!

G. Grantmaking organizations need be prepared for the following questions on their 2008 990:

1. what systems are in place for recordkeeping on all grantees?

2. what systems are used to test grantees eligibility?

3. How are grantees monitored with respect to their compliance with terms of their grants?

43

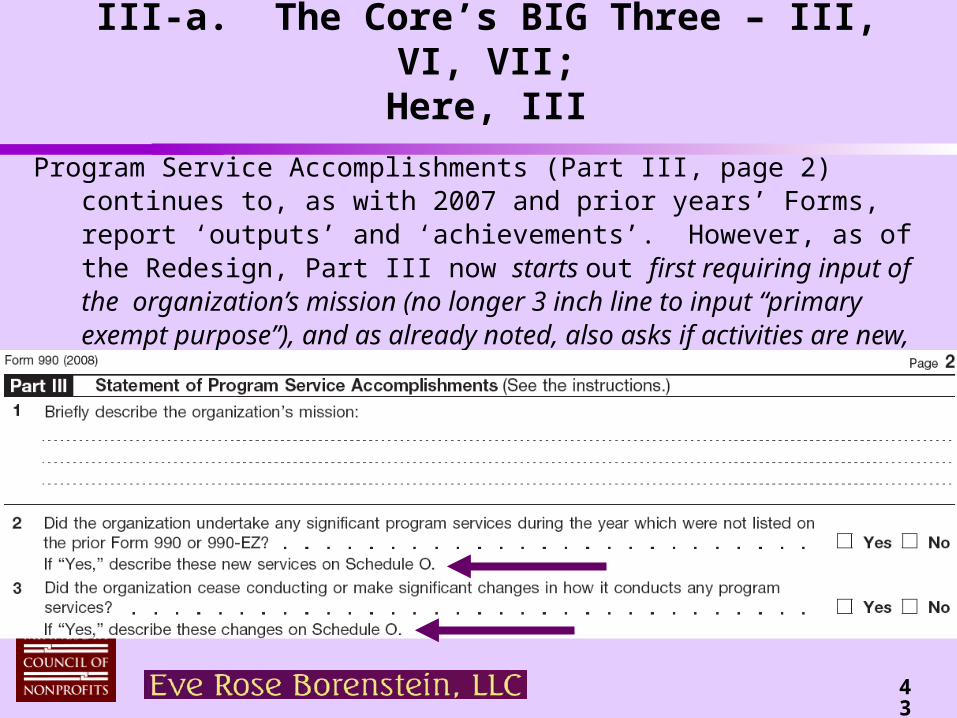

III-a. The Core’s BIG Three – III, VI, VII;Here, III

Program Service Accomplishments (Part III, page 2) continues to, as with 2007 and prior years’ Forms, report ‘outputs’ and ‘achievements’. However, as of the Redesign, Part III now starts out first requiring input of the organization’s mission (no longer 3 inch line to input “primary exempt purpose”), and as already noted, also asks if activities are new, changed, or have been terminated:

44

III-a. The Core’s BIG Three – III, VI, VII:Here, III

A. Requirement to disclose filer’s mission at Line 1:1. Instructions say that if Board has not adopted a mission

statement, state “none”!

2. Incorporated c3’s likely have Articles of Incorporation setting out purposes in which it is said the entity is “organized and operated exclusively for one or more of the following purposes -- charitable, educational, scientific, religious, literary, preventing cruelty to animals, promoting national or international amateur sports competition”, and perhaps an even more limiting statement (e.g., “to this end, the corporation shall undertake efforts to combat domestic violence”). That purpose clause equates to “mission” and should be inputted (rather than “none”).

45

III-a. The Core’s BIG Three – III, VI, VII;Here, III

Not in 2008 Same as in prior years NEW in 2008

(likely 2009)

46

III-a. The Core’s BIG Three – III, VI, VII;Here, III

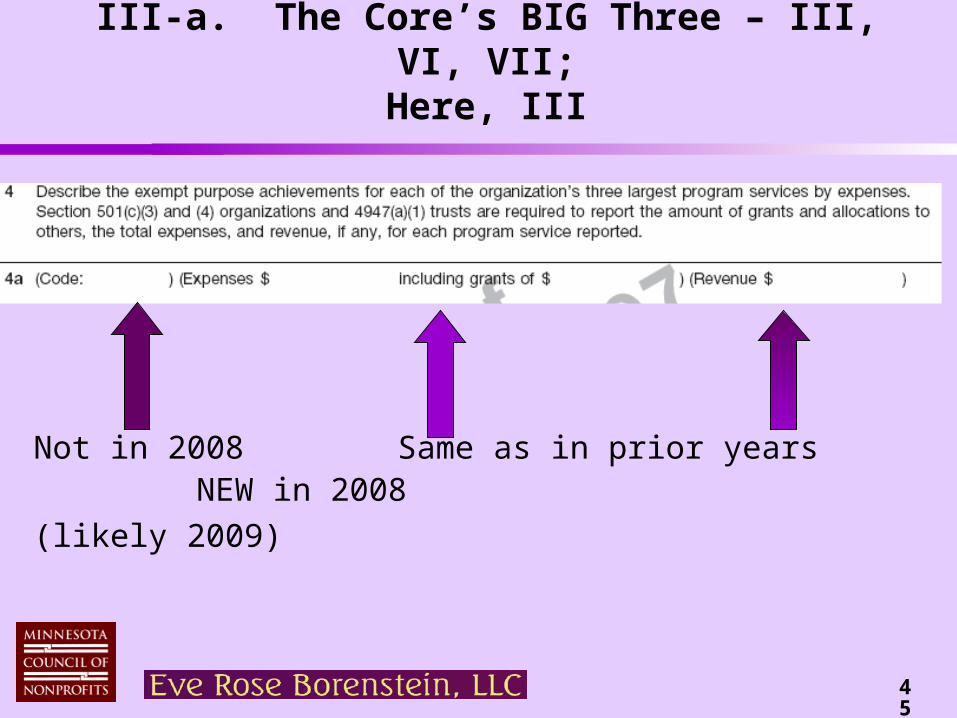

B. As noted earlier, this Part narrates the filing year’s achievements (via Line 4) and “updates” filer’s exemption application (via Lines 2 and 3). 1. As in prior years, c3’s and c4’s must also reflect, for each

program inputted on Lines 4a-4c, the total amount of expenditures incurred (per 990’s measures, which again do not include volunteered services or discounts in accessing use of equipment or facilities).

2. In addition, as of the Redesign, c3’s and c4’s must input program service dollars brought in by each program and as of the 2nd year of the Redesign (i.e., on the 2009 Form) will have to identify each program by program “codes”.

47

III-a. The Core’s BIG Three – III, VI, VII

C. Having dispensed with the FIRST of the BIG THREE, let’s take a look at the other TWO:

1. Governance, Management, and Disclosure (Part VI, page 6)

2. Compensation of TDOKE’s and Highest Compensated Employees, Independent Contractors (Part VII, pages 7 & 8)

48

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

D. Part VI is a completely NEW Part that asks for multiple comprehensive disclosures of governance policies and practices

E. This Part has been widely touted by the Commissioner of the Tax-exempt/Governmental Entities Operating Division of the IRS, Steve Miller, as the “crown jewel” in their efforts to promote “good governance”. WHY is “good governance” in the IRS’ vocabulary? The IRS (and most sector-observers!) believe appropriate policies and procedures are instrumental for healthy organizations AND to improve tax compliance!

49

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

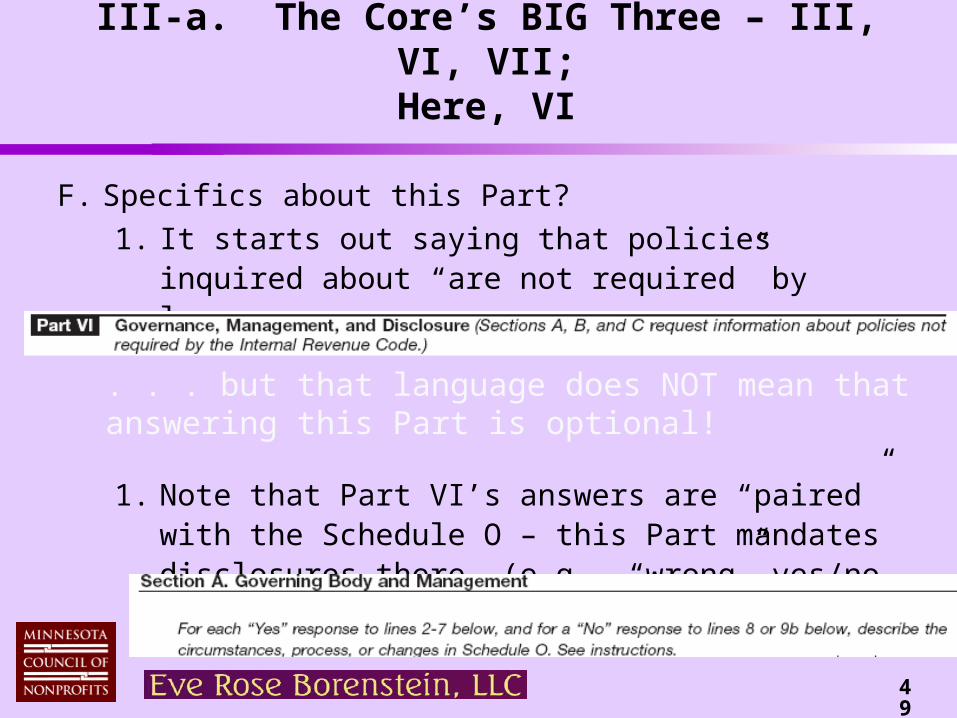

F. Specifics about this Part?

1. It starts out saying that policies inquired about “are not required” by law . . .

1. Note that Part VI’s answers are “paired” with the Schedule O – this Part mandates disclosures there (e.g., “wrong” yes/no responses & for all at Line 10)

. . . but that language does NOT mean that answering this Part is optional!

50

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

3. Section A is all about the Board. a. Its first question requires input of the NUMBER

OF VOTING MEMBERS OF THE BOARD (AT LAST DAY OF TAX YEAR) – this on Line 1a.

b. Next entry (1b) requires input of NUMBER OF THOSE VOTING MEMBERS WHO ARE “INDEPENDENT” (AGAIN, AT LAST DAY OF TAX YEAR). Note that this info is rebroadcast on the Redesigned 990’s Summary Page (Part I, Lines 5/6)!

c. So, what makes a Director “independent”?

51

Side Journey: Understanding the Count of “Independent” Board Members

A voting member of the governing body IS independent IF at all times during the tax year they were NOT: compensated as an officer or employee of the filer or a related

organization (hereafter, “FARO”); compensated (or otherwise receiving) payments >$10k from

FARO as an independent contractor (not included here are paying accountable plan expenses OR reasonable comp for serving as a member of the governing body); or

themselves (or a family member) involved directly with the organization OR indirectly (through affiliation with another organization) in what is (or would be) a Schedule L-reportable transaction.

52

Lack of “Independence” Due to Schedule L-Reportable Business Transaction, 1 of 4

That last factor requires one to journey to Schedule L’s complex reporting upon the fact of interested persons having been connected to the filer (or a related organization in certain cases) via: 1) “excess benefit transactions” 2) being provided grants/assistance 3) business transactions 4) loans

We’ll assume that knowing when 1, 2, or 4 apply is self-evident. But “business transaction” reporting thresholds/definitions ARE complex, and when the issue is the independence of voting members of the Board, the pertinent inquiry need be whether they OR their family members OR “certain organizations” (i.e., those connected to the director in specific ways) would be required to be reported on Schedule L for having engaged in a “business transaction”.

53

Lack of “Independence” due to Schedule L-Reportable Business Transaction, 2 of 4

“Certain organizations” are comprised by those:

1. under >35% aggregate control of a trustee/director and their family members and any other Part VII-listed current/former TDOKEs (more on that acronym shortly) and their family members; or

2. non-501(c) (thus, taxable) organizations who at the time of the transaction had a trustee/director OR a family member of a trustee/director serving as a TDOKE or holding/having a >5% stock or partnership interest (warning! the measure of stock or partnership interests is tied to “constructive ownership” rules that pick up a family members’ ownership interests as one’s own!)

54

Lack of “Independence” due to Schedule L-Reportable Business Transaction, 3 of 4

1st issue is whether there WAS a “business transaction” undertaken; these are: ● a contract or performance of services (or payment) regardless of when the underlying obligation was initiated; or

● joint ventures when the profits or capital interest of the organization and of the interested person each exceed 10%* (note that it is NOT a “business transaction” when one charges membership dues!) * a third category of “business transaction” is irrelevant when testing Directors’ independence – that category picks up transactions with a management company in which a former TDOKE (regardless of whether they are required to be listed in Part VII!) is a direct or indirect 35% owner or serves as a TDOKE

2nd issue is, when a “business transaction” is found, did it exceed the Schedule L reporting thresholds …

55

Lack of “Independence” due to Schedule L-Reportable Business Transaction, 4 of 4

The Schedule L “business transaction” reporting thresholds are as follows: paying compensation >$10,000 to a family member of a

current or former TDOKE who is listed in Part VII (since here we are concerned with current director “independence”, what matters is whether a director has a family member compensated >$10,000 in filing year)

the “interested person’s” dollar amounts of transactions were in excess of the greater of $10,000 or 1% of the organization’s total tax year revenue

total payments for all transactions undertaken with the “interested person” during the year exceeded $100,000

56

Lingo & Acronym Time

Presenter is fond of saying “t-doh-key’s” / IRS spits same out in the Forms as “odd-t-key’s” – either way they are the same:

T = Trustees O = Officers

D = Directors D = Directors

O = Officers T = Trustees

K = Key K = Key

E = Employees E = EmployeesYou’ll continue to hear presenter use the egyptian-sounding “FARO”

instead of the IRS’ mouthful, “filer or a related organization” or “filer and related organizations”

57

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

4. Line 2 asks if there were any family or business relationships among the filer’s current year officers, directors, trustees and key employees at any time during the tax year (who makes that list of individuals is shown upon Part VII). This question is analogous to current Form’s 75b, but for the Redesign the definitions are much more precise.a. “yes” answer here directs one “go-2-Sched.O”

where one lists the individuals by name who have the “relationship” and notes their link as a “family relationship” or “business relationship”

58

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

b. “Family” relationships pick up one’s ancestors, spouse, siblings, and children and their offspring (thru great-grandchildren), as well as spouses of siblings and children and their offspring

c. “Business” relationships are defined as: One is employed by another in a sole proprietorship or by

an organization in which the other is a TDOKE or >35%-owner

One is transacting biz with another (ASIDE from ordinary course of either party’s biz on same terms generally offered to the public) directly or indirectly with transactions valued in the aggregate to be >$10,000 [“indirectly” picks up transactions with organizations in which one person is a TDOKE or >35%-owner]

Both are a trustee/director, officer or >10% owner in the same biz or investment entity.

59

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

5. Line 3: Has there been delegation of management control to a management company or other person? [yes-go-2-Sched.O]

6. Line 4: Have there been any “significant changes” to governing documents? [yes-go-2-Sched.O]a. No longer are any such changes to be noticed to

IRS’ EO Rostering Office in Cincinnati Office; they are solely to be discussed in Sched.O.

b. Only Articles of Incorporation submissions required are for name change or upon dissolution

7. Line 5: Has there been any “material diversion” of entity’s assets? [yes-go-2-Sched.O]

60

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

8. Line 6/7: Organization have members? Those members elect Directors? Directors’ decisions subject in part or whole to approval of members? [any yes, go-2-Sched. O]

9. Line 8: Has there been contemporaneous documentation of all board and committee meetings? [no-go-2-Sched. O]

10. Line 9: Are there local chapters or affiliates? Written policies and procedures governing those chapters/affiliates so their operations are consistent with filer’s operations? [no-go-2-Sched.O]

11. Line 10: Was a copy of the 990 provided to the organization’s governing body before filing? [Regardless of answer, go-2-Sched.O is mandatory because ALL organizations must describe the process (or lack) used by organization to review the Form 990!]

61

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

12. Section B is all about the policies that the organization utilizes (of course, these would be purview of Board as well). The key ones address “conflict of interest” management and setting of executives’ compensation: a. Line 12a/b: does the organization have written conflict

of interest policy? If so, does that policy require disclosure of interests annually?

b. Line 12c: does organization regularly and consistently monitor and enforce compliance with the policy? [no means no (but what are the implications?) . . . , yes requires one go-2-Sched. O to narrate how one accomplishes that monitoring/enforcement!]

c. Line15: Does the organization have a process for…

62

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

determining compensation for the CEO, ED, or top management officials that includes review and approval by independent persons, use of comparability data and written contemporaneous substantiation ? (same Q is asked re setting comp for all other officers & key employees).i. these three inputs are the baseline by which due

diligence is inferred to have occurred (correlating to the so-called “rebuttable presumption” safeharbor that exists under intermediate sanctions excise tax law.

d. Note the apparent mandate at end of Line 15 for all filers to DESCRIBE these processes (whatever they are!) in Schedule O was clarified by IRS on 12/24: only req’d if “yes” answer to 15a or 15b

63

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

13. There are three other “policies” inquired of in Section B (but for these no narrative in Sched.O is sought, regardless of whether filer has the policy or not):

a. Line 13…Whistleblowerb. Line 14…Document retention and destructionc. Line 16…Asking (if the filer has answered that it DOES

participate or invest in a joint venture with taxable entity) if there are written policies & procedures in place to safeguard organization’s exempt status with respect to such arrangements

14. Part VI’s Sections A and B are augmented by Part XI’s Line 2 ask of whether filer has a committee to oversee audit/review of financial statements (assuming same is procured) AND select independent accountant

64

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

Obvious, isn’t it, that running a checklist of “suggested good practices” and/or pushing “behavior modification” is the IRS’ goal in asking each of these questions?

A wonderful enunciation of the IRS’ posture about what governance practices are expected of exempt entities is found in Board guidelines the IRS’ Exempt Orgs Office released in February 2008. These may be accessed at: www.irs.gov/pub/irs-tege/governance_practices.pdf

On November 20, 2008, IRS TE/GE Commissioner Steve Miller gave a speech explaining the IRS’ interest/goals with respect to encouraging good governance; same was posted to the IRS’ charities web-page immediately (in the speech the preceding document is cited), at: www.irs.gov/pub/irs-tege/stm_loyolagovernance_112008.pdf

65

Action Steps Given “New” Governance Focus

Question first. . . . Will ability to employ narrative in Schedule O to explain one’s practices make any of the policies/procedures inquired of less a presumptive or de facto standard? Only time will tell.

Suggested planning steps or goals: 1. Ensure key nucleus on governing body of

independent Directors/Trustees (e.g., State law for nonprofit corporations typically require 3 member Board of Directors)

66

Action Steps Given “New” Governance Focus

2. Get rid of loans by YEAREND with TDOKE’s and High 5s, and any/all of their family members. (This implication actually comes from the Part IV, Line 26 “trigger”)

3. Adopt/refine organization’s policies and practices: a. when organization’s transactions ARE – or appear to

be – in conflict with interests of any TDOKE or High 5 employee

b. to have errors reported without retaliationc. on document retention & destructiond. addressing consistency of affiliates’ activitiese. safeguarding exempt status whenever joint venturing

with taxable entities

67

Action Steps Given “New” Governance Focus

4. Publish/approve timely minutes of Board/committee meetings

5. Determine failures to monitor/enforce compliance with conflicts policy in past periods of 2008 990 year

6. Evaluate comp review and approval process to have same employ “rebuttable presumption” provisions from (c)(3)/(c)(4) tax scheme

7. Plan to provide 990 to Board before filing date if practicable and meaningful; consider 990 review process and how it will be explained

8. Consider what information is made public and be ready to explain decision

68

G. Moving on to the final Section of Part VI, Section C’s “disclosure” inquiries cover:1. Line19 mandates that the filer describe in Schedule

O how governing documents, conflicts policy, and financial statements are (IF indeed these are) made available to the public

2. Line18 uses checkboxes to signify the methods by which the filer provides the public with access to its 990 series filings and exemption application (one’s website, another’s website, or “upon request”)

3. Line17 requires a listing of the States with which this Form 990 is required to be filed

III-a. The Core’s BIG Three – III, VI, VII;Here, VI

69

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

A. Part VII reports “Compensation of Officers, Directors, Trustees, Key Employees, Highest Compensated Employees, and Independent Contractors” – i.e., covering TDOKE’s and High 5’s.

B. This Part correlates to 2007 and prior years’ Forms Parts V-A (and V-B) for input OF individuals who served in filing year as Trustees/Directors, Officers, and Key Employees (thus, “TDOKE’s”). On those years, 501(c)(3)’s alone (not non-c3’s) used a similar grid for reporting employees who made the “High 5” list.

70

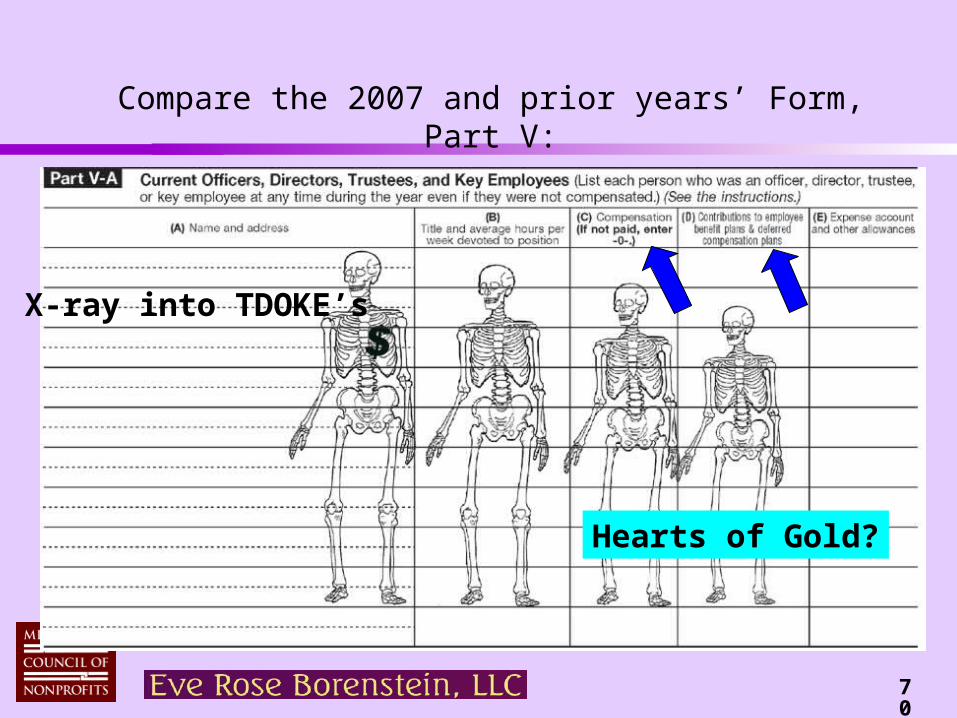

Compare the 2007 and prior years’ Form, Part V:

X-ray into TDOKE’s

Hearts of Gold?

71

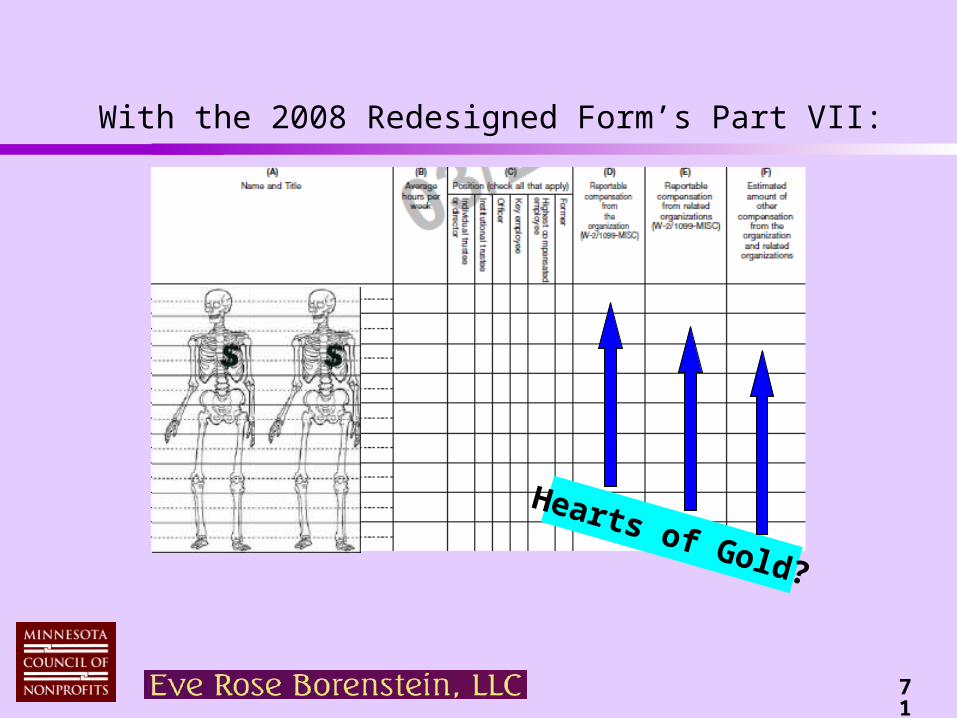

With the 2008 Redesigned Form’s Part VII:

Hearts of Gold?

72

2007 & prior (“current”) versus Redesigned Form – reporting Compensation

The “current” Form 990, at Part V, has long asked for info on TDOKEs serving in the filing year. As of the 2005 Form, the reach of asks expanded to include FORMER TDOKEs as well, with no limits in terms of how long ago they served or for remunerative amounts. The Redesigned 990 continues to ask for FORMERs, but with a five year look-back and with remunerative thresholds.

The “current” Form 990 required only of 501(c)(3) public charities reporting of “High 5” employees. The Redesigned 990 requires High 5’s BE DISCLOSED BY ALL, and the threshold for who is a “High 5” has been raised from >$50k total remuneration (by filer in the tax year) to >$100k reportable-on-Part-VII as having been paid by FARO (filer and related organizations).

73

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

C. Part VII of the Redesigned 990 situates inquiries and disclosures on all TDOKEs and High 5’s in the Core Form all filers complete. A key change in reporting methodology from the “current” Form is this Part ties dollar-inputs on compensation to an “easier” and hopefully-consistent-across-all-filers measure: filers report amounts that were (or should have been) “reportable” to the individuals upon a FORM W-2 (or 1099). As a result, Part VII discloses remuneration (both “reportable” per W-2/1099 and “other”) reflecting the CALENDAR YEAR ended in or with the filer’s year.

74

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

“Reportable compensation” is picked up in Part VII’s

Columns D and E (together those columns report pay by “FILER” AND * “RELATED ORGANIZATION(s)” (=FARO)).Use amounts reportable in Box 5, W-2 (medicare taxable wages) or Box 1, 1099.

* There is an exclusion which ignores each “related org’s” compensation for input to Column E if it is $10,000 or less(EXCEPT when reporting on a former T/D!)

75

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

Three types of benefits MUST be quantified for inclusion here (although estimates can be used):

1. Contributions to (or annual increase in value of defined-benefit) retirement plans

2. Payments for health benefits;3. Deferred compensation (regardless if plan is

funded, vested, or subject to substantial risk of forfeiture)

Value of benefits provided by FARO are in Column F.

Other types of benefits provided are ONLY to be have amounts included in Col. F if their value exceeds $10,000.

76

D. In spite of having noted that Part VII situates all compensation reporting in the Core Form, certain filers will find they are indeed required to provide additional comp detail on specific individuals (and answer inquiries re their compensation-setting practices overall). This occurs via Schedule J, “triggered” when Part VII includes:1. any “former” TDOKE or High 5

2. a listee whose total Part VII comp inputs – “reportable pay” and “other” (i.e., benefits) – thus D+E+F exceeds $150,000

3. a listee who the filer knows is also being paid by an unrelated organization for services they provide to the filer

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

77

E. With the 2008 Redesign, new definitions of “Officers” and “Key Employees” apply, ending issue as to whether CFO’s, CEO’s, and VP’s “make the list”. On Redesign:1. A filer’s top management official AND person with chief

responsibility over finances are “automatically” considered Officers (for 990-reporting purposes).

2. Key Employee status vests under 3-part test: one had responsibilities in the filing year like that of an Officer OR had significant responsibilities over one or more aspects of the organization’s in-flows/out-flows (see next slide); what would be disclosed on Part VII as the person’s “reportable compensation” (from FARO) exceeds $150,000; and that “reportable compensation” amount is amongst the top 20 of all individuals meeting the prior two tests.

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

78

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

3. ‘Key Employees’ “responsibilities test” asks if an employee at any time in the filing year:a. had or shared organization-wide responsibilities,

powers, or influence similar to that of an officer, director, or trustee (this is same standard as the 2007 and prior years’ Forms);

b. managed a discrete segment or activity of the organization that represents 10% or more of the activities, assets, income, or expenses of the organization; OR

c. had or shared authority to control or determine 10% or more of the organization’s capital expenditures, operating budget, or employees’ compensation

79

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

Who Gets Reported on Part VII? “Reportable Comp” Threshold Category (i.e., columns (D) & (E)) Filing year (i.e., “current”) officers, directors/trustees no threshold;

[now includes CEO, CFO] report ALL

Filing year (i.e., “current”) key employees – top 20 who >$150,000

meet “responsibilities test” & exceed this threshold

Current five highest compensated employees >$100,000

Also, and we will discuss this soon:

Former officers, key and five highest employees >$100,000

Former directors/trustees > $10,000*

*comp’d that amount in capacity as a former director or trustee

80

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

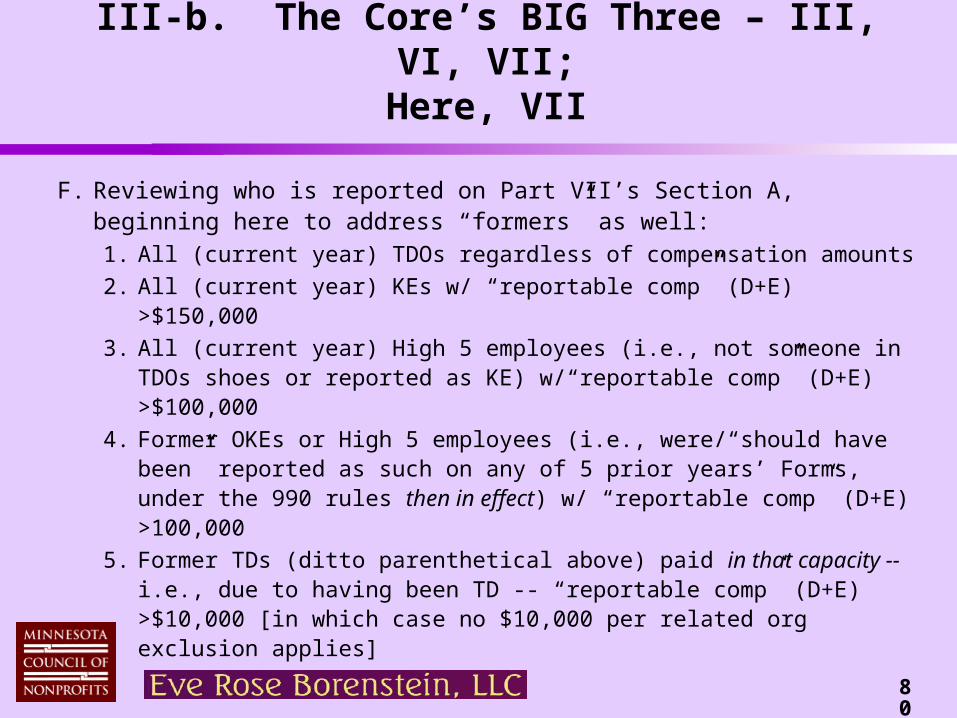

F. Reviewing who is reported on Part VII’s Section A, beginning here to address “formers” as well:1. All (current year) TDOs regardless of compensation amounts

2. All (current year) KEs w/ “reportable comp” (D+E) >$150,000

3. All (current year) High 5 employees (i.e., not someone in TDOs shoes or reported as KE) w/“reportable comp” (D+E) >$100,000

4. Former OKEs or High 5 employees (i.e., were/“should have been” reported as such on any of 5 prior years’ Forms, under the 990 rules then in effect) w/ “reportable comp” (D+E) >100,000

5. Former TDs (ditto parenthetical above) paid in that capacity -- i.e., due to having been TD -- “reportable comp” (D+E) >$10,000 [in which case no $10,000 per related org exclusion applies]

81

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

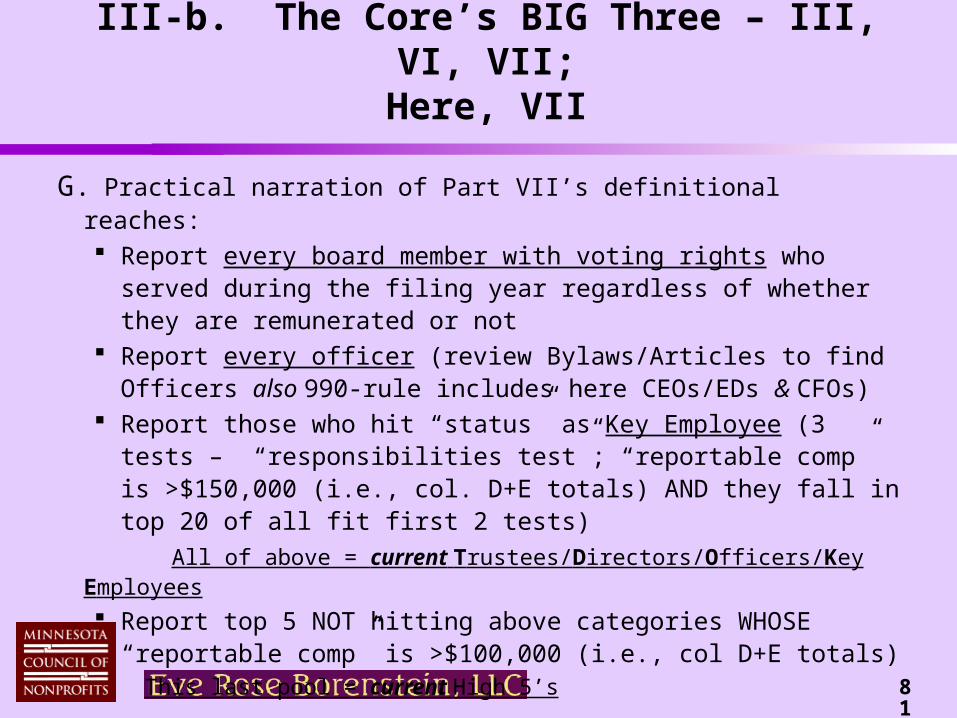

G. Practical narration of Part VII’s definitional reaches: Report every board member with voting rights who served

during the filing year regardless of whether they are remunerated or not

Report every officer (review Bylaws/Articles to find Officers also 990-rule includes here CEOs/EDs & CFOs)

Report those who hit “status” as Key Employee (3 tests – “responsibilities test”; “reportable comp” is >$150,000 (i.e., col. D+E totals) AND they fall in top 20 of all fit first 2 tests)

All of above = current Trustees/Directors/Officers/Key Employees

Report top 5 NOT hitting above categories WHOSE “reportable comp” is >$100,000 (i.e., col D+E totals)

This last pool = current High 5’s

82

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

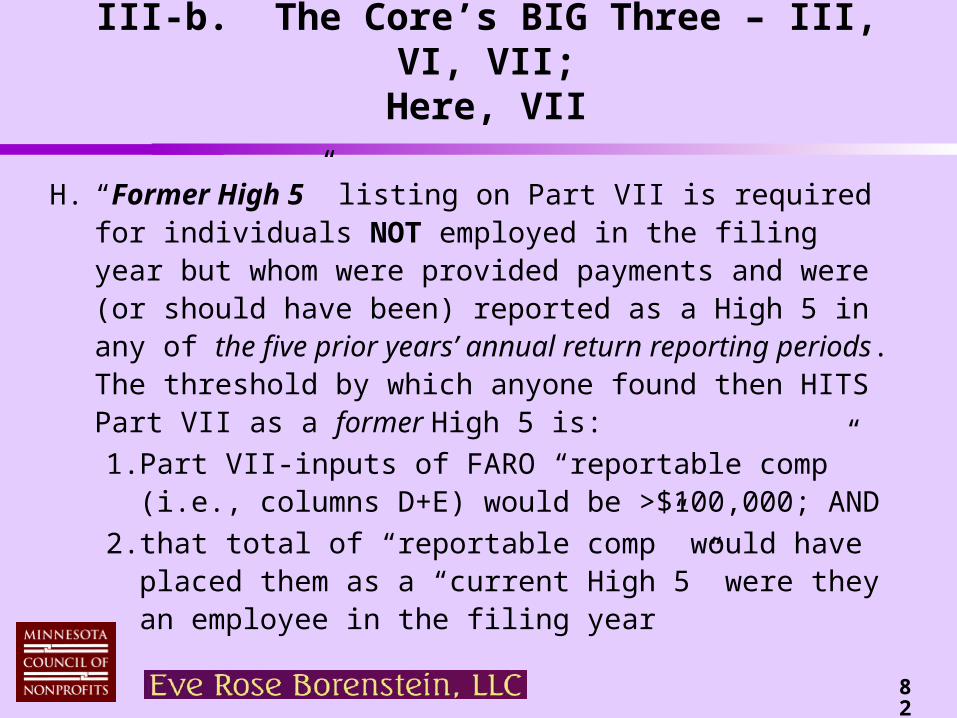

H. “Former High 5” listing on Part VII is required for individuals NOT employed in the filing year but whom were provided payments and were (or should have been) reported as a High 5 in any of the five prior years’ annual return reporting periods. The threshold by which anyone found then HITS Part VII as a former High 5 is:

1. Part VII-inputs of FARO “reportable comp” (i.e., columns D+E) would be >$100,000; AND

2. that total of “reportable comp” would have placed them as a “current High 5” were they an employee in the filing year

83

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

I. “Former T/D” listing is required for those individuals NOT on Part VII with any “current year” status, but who were a Trustee/Director in any of the five prior years’ reporting periods (i.e., tying to returns on Form 990, 990-EZ, or 990-PF) AND would have FARO “reportable comp” provided them because of having been a Trustee/Director in excess of $10,000 (and for these purposes, one must include ALL amounts paid by related organizations ignoring what would otherwise be Column E $10k exception-per-related organization).

84

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

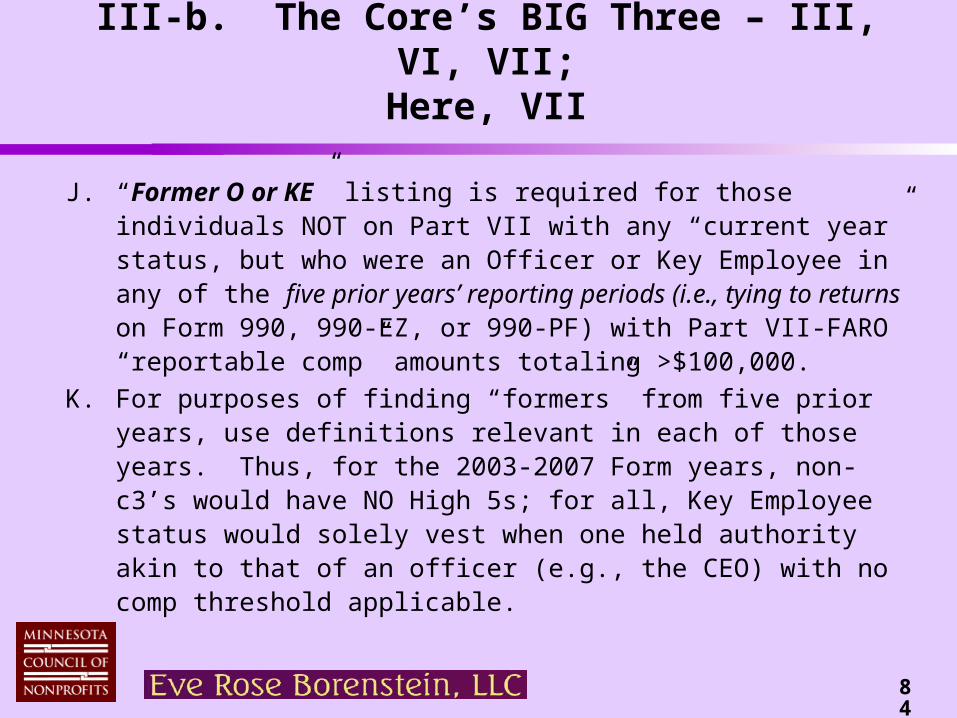

J. “Former O or KE” listing is required for those individuals NOT on Part VII with any “current year” status, but who were an Officer or Key Employee in any of the five prior years’ reporting periods (i.e., tying to returns on Form 990, 990-EZ, or 990-PF) with Part VII-FARO “reportable comp” amounts totaling >$100,000.

K. For purposes of finding “formers” from five prior years, use definitions relevant in each of those years. Thus, for the 2003-2007 Form years, non-c3’s would have NO High 5s; for all, Key Employee status would solely vest when one held authority akin to that of an officer (e.g., the CEO) with no comp threshold applicable.

85

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

L. “Related organization” comp reporting (Columns E & F)1. A “related organization” is a parent, subsidiary, group

under common control (called, “brother”/“sister”), or those who are “supported” to “supporting” (or vice versa) under 509(a)(3), as well as partnerships in which the filer is 1 of 3 (or fewer) general partners. Definition of control used for establishing parent-subsidiary or brother/sister is >50% control measured by stock ownership or intended or effective control of Directors. Imputed control rules apply in tiered-entity settings (A owns 80% of B, B has its officers, directors, or employees in 70% of C’s Director-seats; A is imputed to have 56% control of C).

86

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

L. “Related organization” comp reporting (continued ...)

2. Column E discloses amounts paid by a “related organization” that were (or should have been) reportable upon W-2 Box 5 (or 1099-MISC Box 1) for the calendar year ending at or within filer’s tax year. There is a $10,000-or-less exclusion per related organization.

3. Column F (“other” – i.e., not “reportable comp” that would be reported upon W-2 or 1099) reporting of benefits provided also is tied to calendar year measures. The rules for what goes into Column F are the same for the filer as for related organization (next slide reprises those rules).

87

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

• estimate if actual numbers not readily available• include all payments for ‘Big 3’: (1): for defined

contribution (or annual increase in value of defined-benefit) retirement plans; (2) for health benefits; for (or annual increase in value of) any/all tax-deferred non-qualified plans (i.e., deferred comp!) regardless if ‘plan’ is funded, vested, or subject to substantial risk of forfeiture

Value of benefits provided by FARO are in Column F. Rules for input are as follows:

• include payments toward/value of items not in ‘Big 3’ (such as value of housing provided, educational assistance, life insurance, disability benefits) EXCEPT if value of the item is $10,000 or less

88

III-b. The Core’s BIG Three – III, VI, VII;Here, VII

M. Final note on Part VII – Section B (page 8) requires the reporting of the filer’s “High 5” independent contractors for the year. Reported here are independent contractors who (by Form 1099 measures) were in the top 5 in receiving payments in excess of $100,000.1. Similar to TDOKE/High 5 employee reporting in Section A,

the method of reporting looks to remuneration provided in the calendar year ended within or with the filer’s tax year.

2. Dissimilar to TDOKE/High 5 employee reporting is there is NO reporting of amounts provided to the independent

contractor by “related organizations”.

89

IV. The BIG 10 SchedulesHere, Schedule J

A. As noted earlier, there may be more detailed disclosure regarding compensation provided to a Part VII-listed individual beyond Part VII’s disclosure of “reportable compensation” and “other compensation”. Same occurs when any one individual hits a Schedule J “trigger” (these are found in questions 3-5 on Part VII’s Section A):1. they are a “former” TDOKE or High 5

2. their total Part VII comp inputs – “reportable pay” and “other” (i.e., benefits) – thus D+E+F exceeds $150,000

3. they are also being paid by an unrelated organization for services they provide to the filer

90

IV. The BIG 10 SchedulesHere, Schedule J

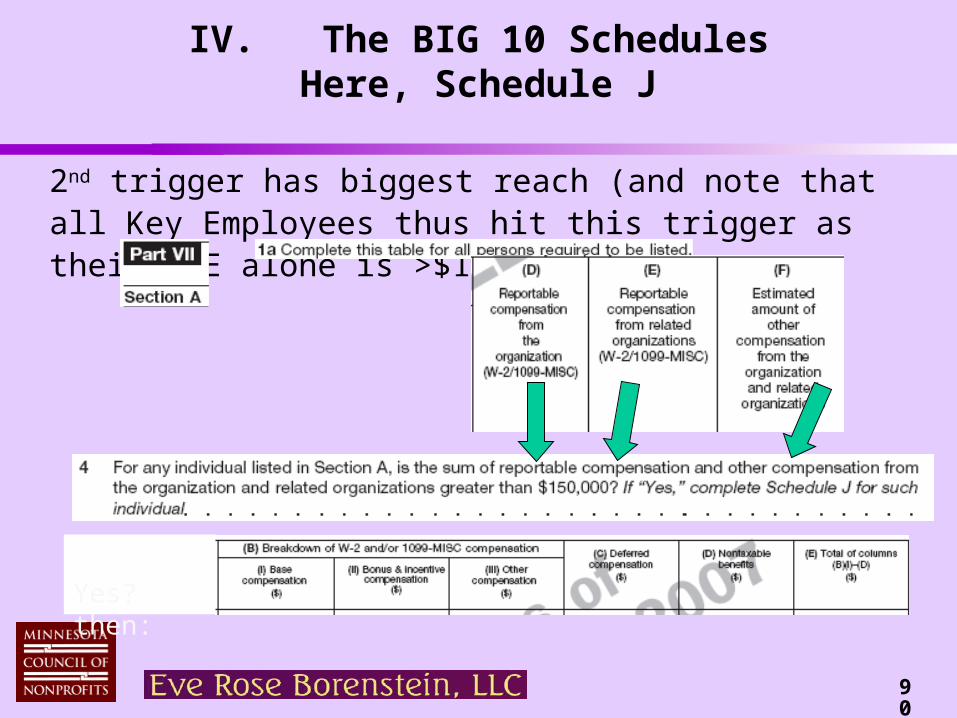

2nd trigger has biggest reach (and note that all Key Employees thus hit this trigger as their D+E alone is >$150k)

Yes? then:

91

IV. The BIG 10 SchedulesHere, Schedule J

B. Part VII listees who hit a Schedule J trigger have further information on their compensation disclosed in Schedule J’s Part II (as evidenced on preceding slide in pertinent part):

1. base compensation, bonus/incentive compensation, and other “pay” are separately itemized by filer versus related organizations with NO $10,000-per-related-organization exclusion; and

2. input of actual payments (i.e., ignoring Part VII Col. F $10,000-per-certain-item exclusion) toward non-”reportable compensation” is required (again same is to be shown by filer versus related organizations) and also requiring breakout of deferred comp from all “other benefits”.

92

IV. The BIG 10 SchedulesHere, Schedule J

C. Filers find in Schedule J’s Part I multiple questions pertaining to their executive compensation practices. These questions apply beyond the Part VII-listees who hit a Schedule J trigger.

1. Question 4 requires disclosure of whether ANY Part VII-listed individual participated in supplemental nonqualified retirement plans, received severance or change of control payments, or equity-based compensation

2. Questions 5 - 7 require c3 and c4 organizations to disclose if they or a related organization provided any Part VII-listed individual compensation contingent on revenues or net earnings, or other non-fixed payments

93

IV. The BIG 10 SchedulesHere, Schedule J

4. Q. 8 requires c3 and c4 organizations to disclose if the “initial contract exception” was accessed

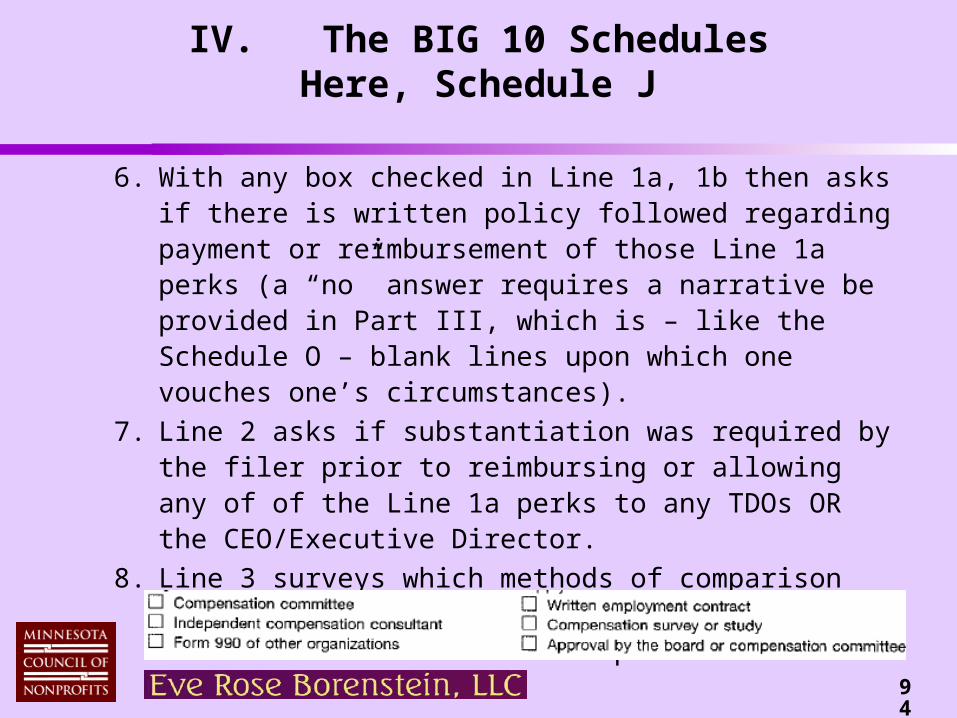

5. Q. 1a uses “check boxes” to see if organization provided to ANY Part VII-listed individual: First-class or charter travel (NOT intermediate classes) Travel for companions Tax indemnification and gross-up payments Discretionary spending accounts Housing allowance or personal residence Payment for business use of personal residence Health or social club dues or initiation fees Personal services (e.g., chef, chauffeur and/or maid)

94

IV. The BIG 10 SchedulesHere, Schedule J

6. With any box checked in Line 1a, 1b then asks if there is written policy followed regarding payment or reimbursement of those Line 1a perks (a “no” answer requires a narrative be provided in Part III, which is – like the Schedule O – blank lines upon which one vouches one’s circumstances).

7. Line 2 asks if substantiation was required by the filer prior to reimbursing or allowing any of of the Line 1a perks to any TDOs OR the CEO/Executive Director.

8. Line 3 surveys which methods of comparison data were accessed in setting the CEO/Executive Director’s comp:

95

IV. The BIG 10 SchedulesHere, Schedule L

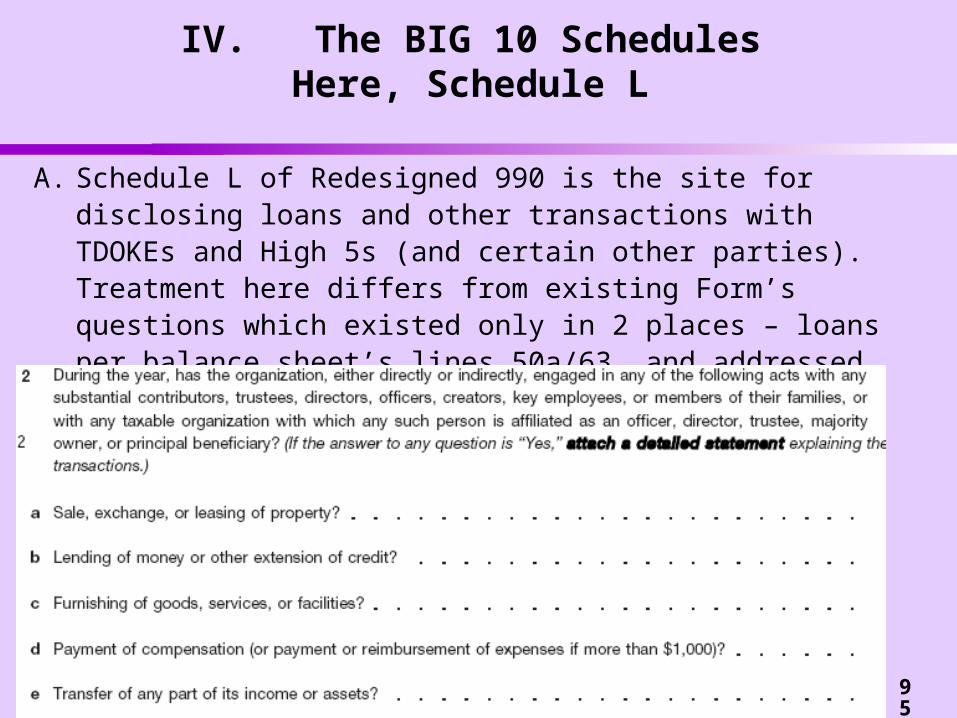

A. Schedule L of Redesigned 990 is the site for disclosing loans and other transactions with TDOKEs and High 5s (and certain other parties). Treatment here differs from existing Form’s questions which existed only in 2 places – loans per balance sheet’s lines 50a/63, and addressed (for c3’s only) overall at Sch. A, Part III:)

96

IV. The BIG 10 SchedulesHere, Schedule L

B. Schedule L – Transactions with Interested Persons -- is with certainty the most complicated Schedule/Part in the entire Redesign. While its Instructions are a slim nine pages, the objects addressed are confusing, as the definition of “Interested Persons” is different for each of the Schedule’s four Parts:

I. Excess Benefit Transactions

II. Loans

III. Grants/Assistance

IV. Business Transactions

as the accompanying slides’ “headers” detail:

97

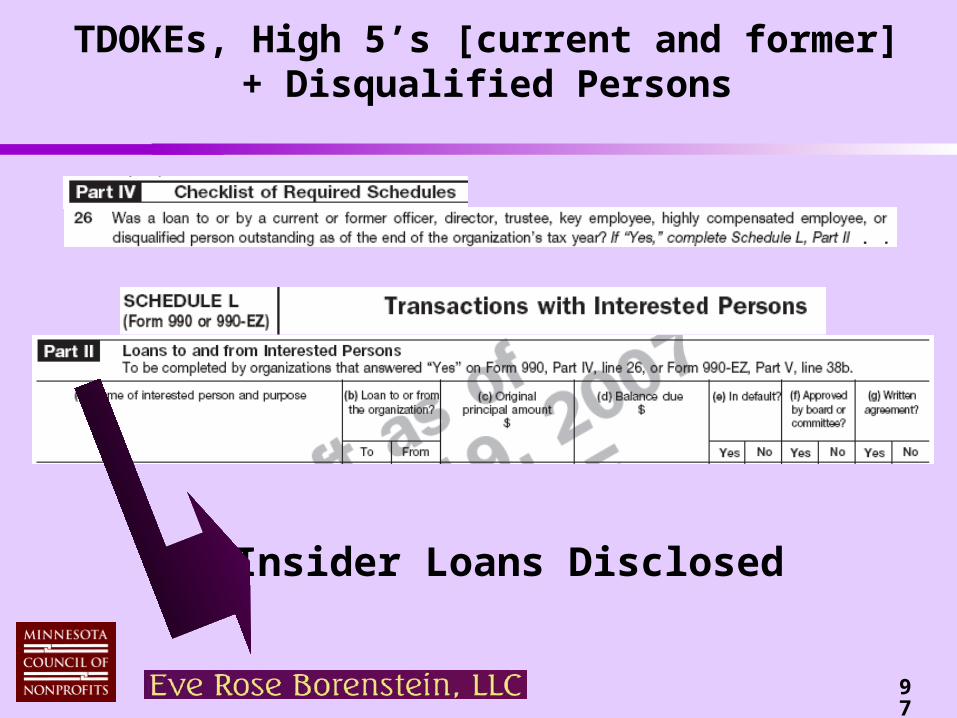

TDOKEs, High 5’s [current and former] + Disqualified Persons

Insider Loans Disclosed

98

Current TDOKEs, Subst’l Contributors, OTHERS(incl. Grant Selection Committee Members; also Family)

Grants/Assistance Disclosed

99

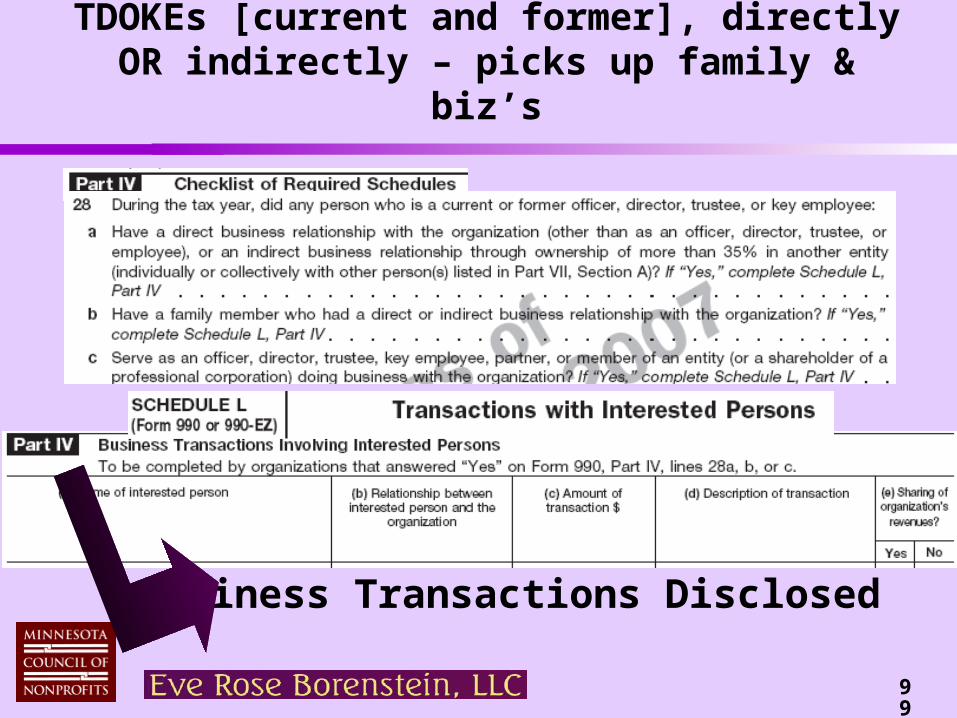

TDOKEs [current and former], directly OR indirectly – picks up family & biz’s

Business Transactions Disclosed

100

IV. The BIG 10 SchedulesHere, Schedule L

C. It is Part IV, “Business Transactions with Interested Persons”, that causes the largest headaches. This Part discloses if current/former TDOKE’s listed in Part VII, OR their family members, or certain other entities have conducted business transactions with the filer. “Other entities” encompass: >35%-owned/controlled-entities (ownership and control to be

measured by aggregating the interests and rights of Part VII-listed individuals and all their family members)

non-501(c) (i.e., TAXABLE) entities that have a Part VII-listed individual serving as one of their TDOKEs or as a 5% or greater partnership or membership interest at the time that the entity transacted with the filer

101

Warning re a Part VII-listed individual being imputed to be a 5% (or greater) partner/member/owner of 3rd party

Important note: the IRS has added to the Schedule L Part IV mix of rules the “constructive ownership” standards from Code section 267(c) to measure an individual’s partnership/professional corporation interests or entity-ownership. Section 267(c)(2) picks up the ownership interests of one’s “family members” as one’s own!

As a result, if a Board member’s child is a 5.25% profits-partner at the law firm providing services to the filer, the law firm IS an “interested person” per the prior slide’s 2nd point as one of the filer’s trustees/directors is, under 267(c)(2), imputed to be a 5% or greater partner at the law firm (this result is indeed the fact pattern behind Examples 2, 3 in Part IV’s Instructions).

102

IV. The BIG 10 SchedulesHere, Schedule L

D. A floor exists whereby not ALL business transactions between the filer and “interested persons” are reportable; those “excepted” are the following: compensation is paid to one whose “Interested person” status is

derived from being a family member in amounts of $10,000 or less total payments for all transactions between the filer and the

“Interested person” over the course of the tax year do not exceed $100,000

total payments from one transaction with an “Interested person” (without regard to when transaction was entered into) do not exceed the greater of $10,000 or 1% of the organization’s total revenues for the tax year

103

IV. The BIG 10 SchedulesHere, Schedule L

E. “Business transactions” include: Contracts and performance of services initiated during the

tax year or ongoing from a prior year. Joint ventures (whether new or ongoing) when the profits or

capital interest of the organization and of the interested person each exceed 10%.

Transaction with an organization and a management company in which a former TDOKE (regardless of whether they are required to be listed in Part VII!) is a direct or indirect 35% owner or a TDOKE

However, “business transactions” do NOT include the charging of membership dues!

104

IV. The BIG 10 SchedulesHere, Schedule L

F. A “yes” answer to any of Part IV, Q. 28’s subparts (a current or former TDOKE per Part VII-listing had a direct or indirect business relationship; one of their family members did; or an entity in which one of them served as a TDOKE or as partner/member did) . . . leads to completion of the Schedule L’s Part IV where one details: 1. name of interested person

2. relationship between interested person and the filer (e.g., spouse of Director)

3. description of transaction and amount

4. “yes”/”no” as to whether transaction involved sharing of entity’s revenue

105

IV. The BIG 10 SchedulesHere, Schedule L

G. The two remaining Parts of Schedule L that are “new” to Form 990 reporting are Parts IIII (triggered by a “yes” answer to the inquiry, “did organization provide a grant or other assistance to a TDOKE, substantial contributor, or to a person related to such an individual?”) and Part II (triggered by there being a loan outstanding at the end of the organization’s tax year to a current or former TDOKE, High 5s, or for 501(c)(3)/(c)(4)’s, to a disqualified person within the definitions of Code Section 4958).

106

IV. The BIG 10 SchedulesHere, Schedule L

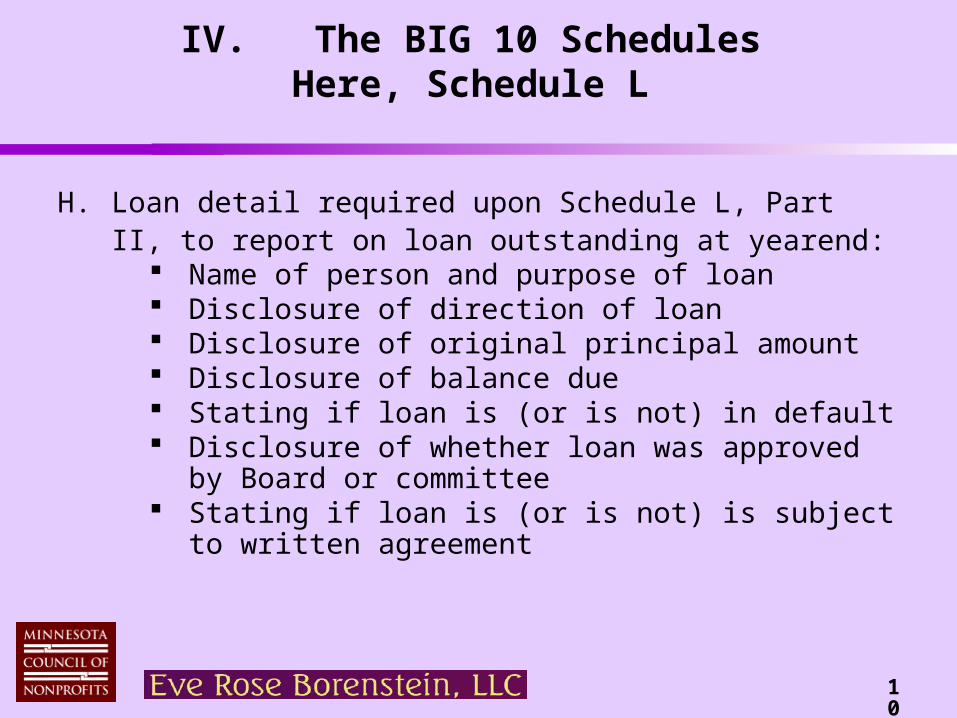

H. Loan detail required upon Schedule L, Part II, to report on loan outstanding at yearend:

Name of person and purpose of loan Disclosure of direction of loan Disclosure of original principal amount Disclosure of balance due Stating if loan is (or is not) in default Disclosure of whether loan was approved by

Board or committee Stating if loan is (or is not) is subject to written

agreement

107

IV. The BIG 10 SchedulesHere, Schedule L

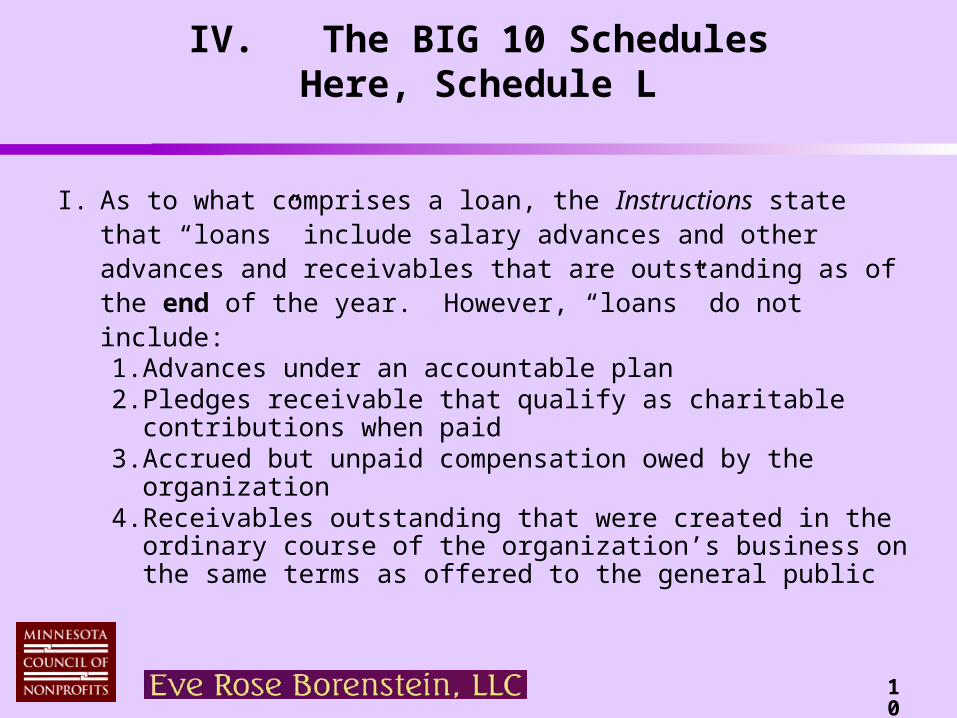

I. As to what comprises a loan, the Instructions state that “loans” include salary advances and other advances and receivables that are outstanding as of the end of the year. However, “loans” do not include: 1. Advances under an accountable plan 2. Pledges receivable that qualify as charitable contributions

when paid3. Accrued but unpaid compensation owed by the

organization4. Receivables outstanding that were created in the ordinary

course of the organization’s business on the same terms as offered to the general public

108

IV. The BIG 10 SchedulesHere, Schedule L

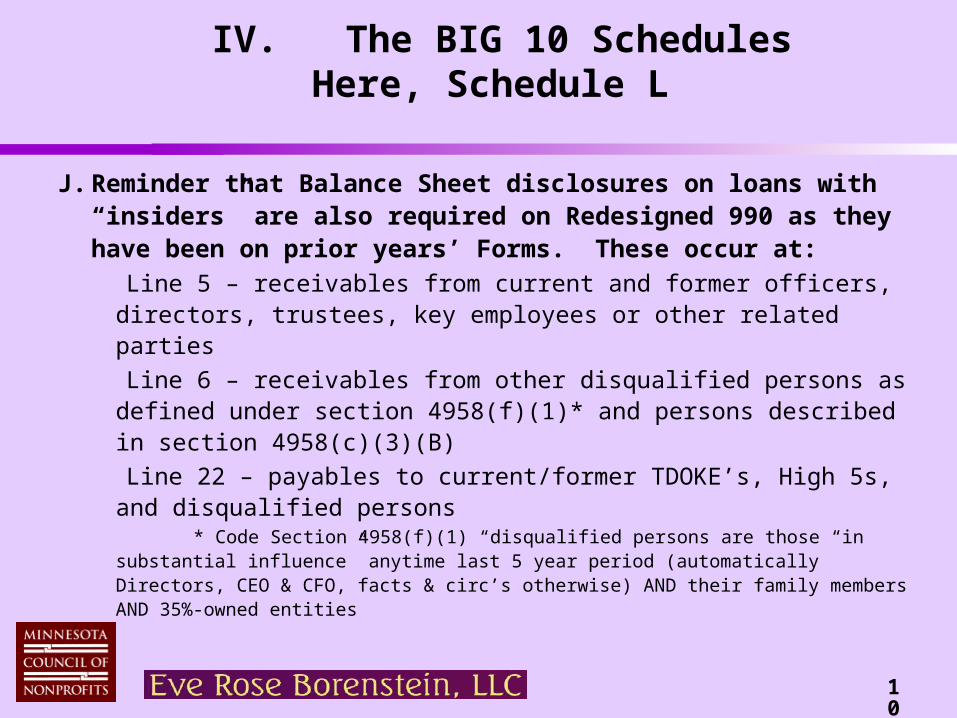

J. Reminder that Balance Sheet disclosures on loans with “insiders” are also required on Redesigned 990 as they have been on prior years’ Forms. These occur at:

Line 5 – receivables from current and former officers, directors, trustees, key employees or other related parties

Line 6 – receivables from other disqualified persons as defined under section 4958(f)(1)* and persons described in section 4958(c)(3)(B)

Line 22 – payables to current/former TDOKE’s, High 5s, and disqualified persons

* Code Section 4958(f)(1) “disqualified persons are those “in substantial influence” anytime last 5 year period (automatically Directors, CEO & CFO, facts & circ’s otherwise) AND their family members AND 35%-owned entities

109

IV. The BIG 10 SchedulesHere, Schedule L

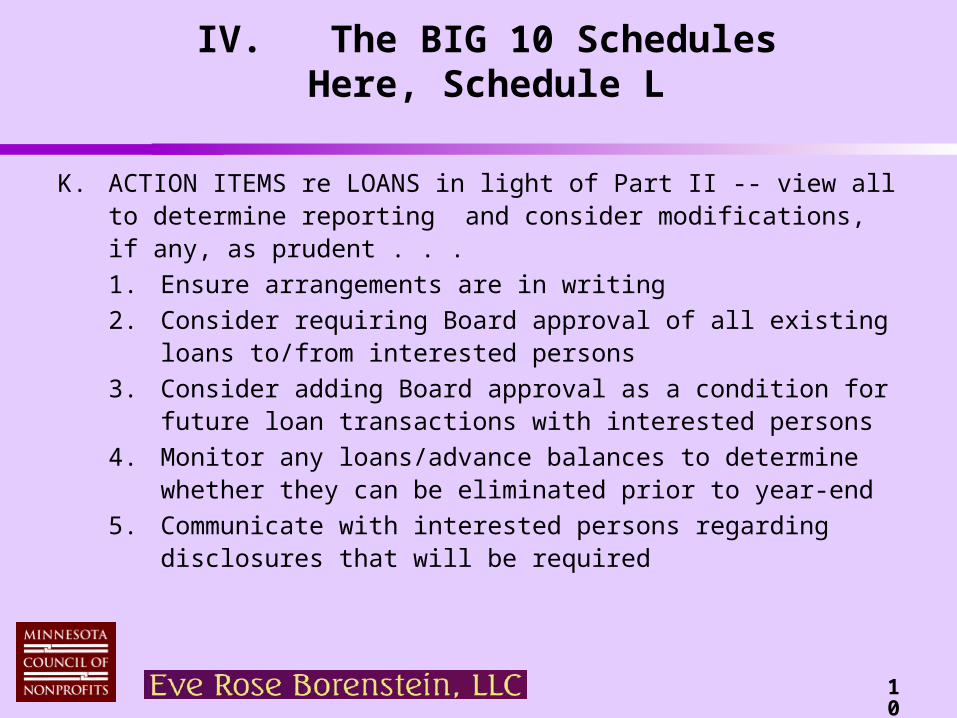

K. ACTION ITEMS re LOANS in light of Part II -- view all to determine reporting and consider modifications, if any, as prudent . . .

1. Ensure arrangements are in writing

2. Consider requiring Board approval of all existing loans to/from interested persons

3. Consider adding Board approval as a condition for future loan transactions with interested persons

4. Monitor any loans/advance balances to determine whether they can be eliminated prior to year-end

5. Communicate with interested persons regarding disclosures that will be required

110

IV. The BIG 10 SchedulesHere, Schedule L

L. Part III applies when filer has provided a grant or other assistance to a current or former TDOKE (listed in Part VII), a substantial contributor, or to a person related to such an individual?” 1. Definitions of “substantial contributor” and the

inclusion in the term “related person” of members of one’s grant selection committees are addressed in the next slide . . .

2. Unlike Part IV, no reporting thresholds exist, so all grants and assistance that are not in excepted category must be reported. The excepted categories are noted two slides forward . . . .

111

IV. The BIG 10 SchedulesHere, Schedule L

Instructions do not adopt “substantial contributor” definition from the private foundation rules, but instead create one for Part III purposes:

“Related persons” reached by this Part of Schedule L are: All members of grant selection committees Family members of preceding, or of current/former TDOKEs &

substantial contributors) 35%-controlled entities Employees (or child of employee) of a substantial contributor OR

of a 35%-controlled entity of a substantial contributor but only if the grant/assistance was under the direction/advice directly or indirectly of the contributor or controlled entity

112

IV. The BIG 10 SchedulesHere, Schedule L

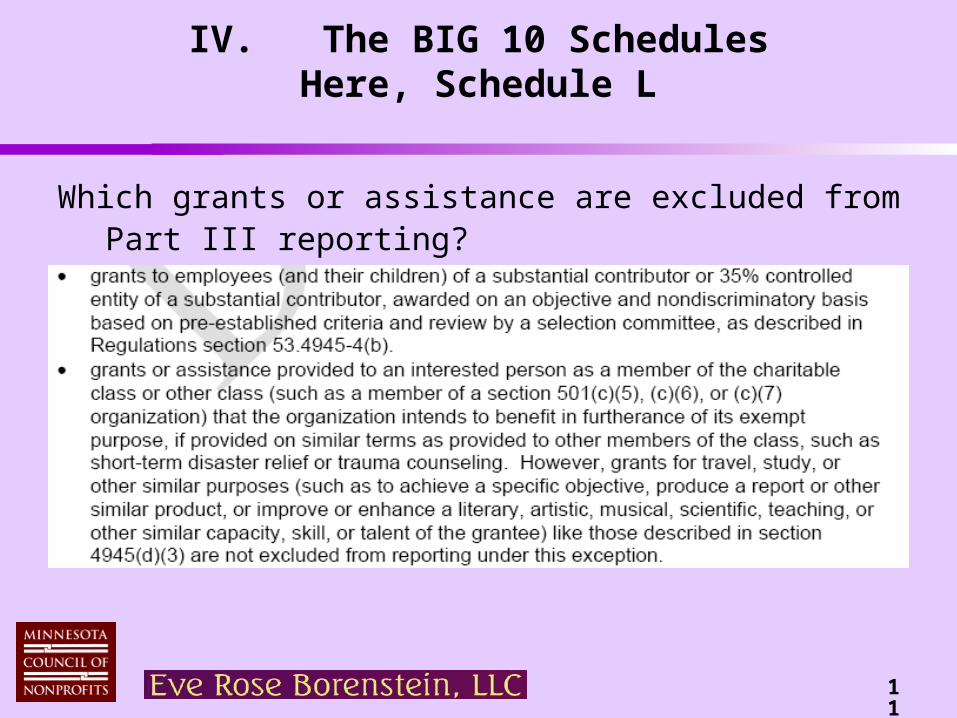

Which grants or assistance are excluded from Part III reporting?

113

IV. The BIG 10 SchedulesHere, Schedule L

M. Finally, we address the one Part of Schedule L that is exclusively for 501(c)(3)/(c)(4)’s, Part I. This Part is is the site for disclosing the fact of “excess benefit transactions” (a term of art that means there has been an “intermediate sanctions” violation under Internal Revenue Code Section 4958). The relevant trigger questions are at Part IV’s Lines 25a and 25b; these are identical to the 2007 Form 990’s question 89b.

1. Disclosure is different from existing Form 990 – MUST detail individual’s name and MUST detail if correction has occurred.

114

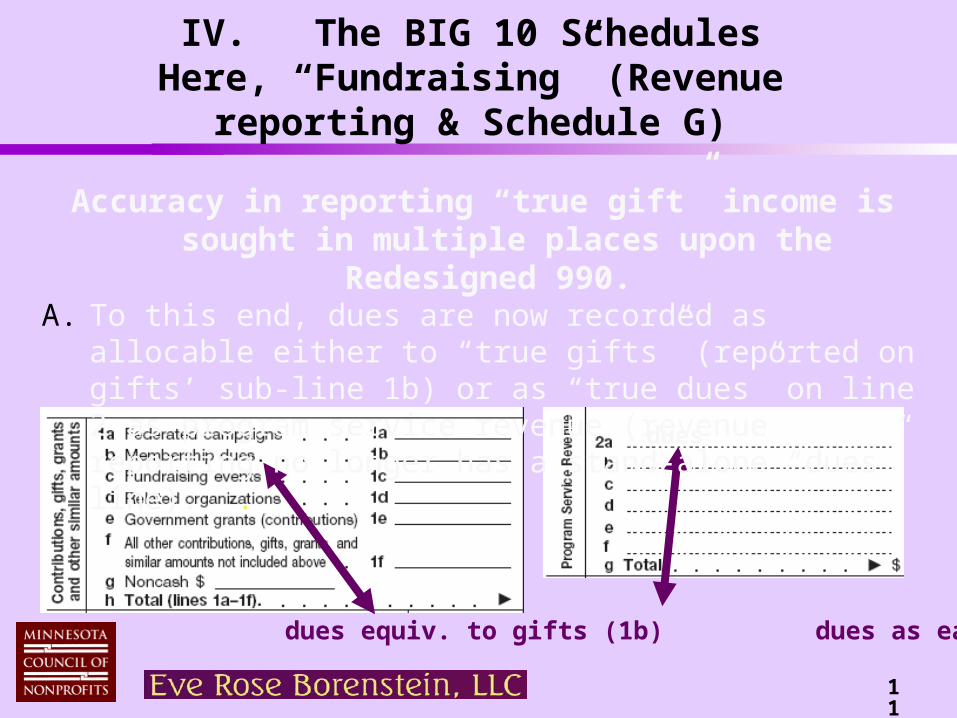

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

dues equiv. to gifts (1b) dues as earned revenue (2_)

dues

Accuracy in reporting “true gift” income is sought in multiple places upon the Redesigned 990.

A. To this end, dues are now recorded as allocable either to “true gifts” (reported on gifts’ sub-line 1b) or as “true dues” on line 2 as program service revenue (revenue reporting no longer has a stand-alone “dues” line). .

115

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

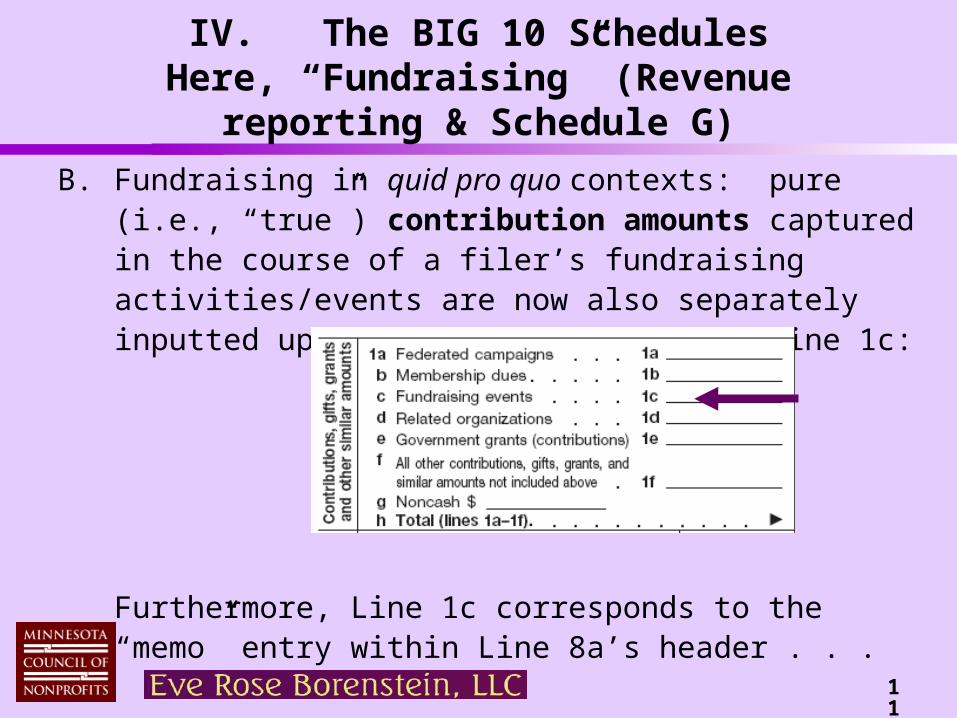

B. Fundraising in quid pro quo contexts: pure (i.e., “true”) contribution amounts captured in the course of a filer’s fundraising activities/events are now also separately inputted upon a dedicated sub-line, Line 1c:

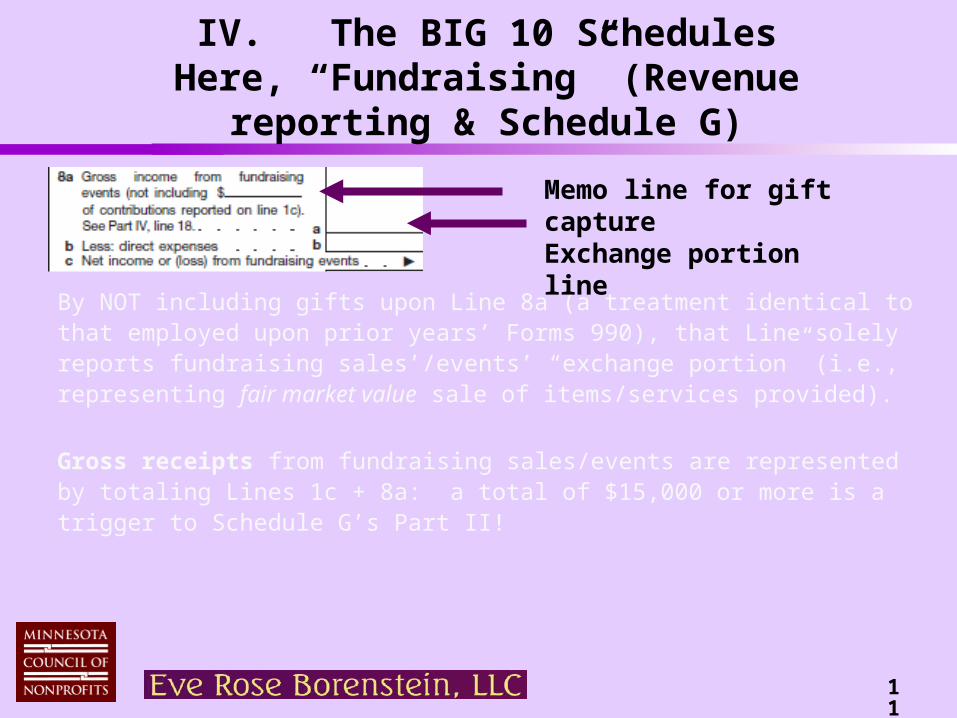

Furthermore, Line 1c corresponds to the “memo” entry within Line 8a’s header . . .

116

By NOT including gifts upon Line 8a (a treatment identical to that employed upon prior years’ Forms 990), that Line solely reports fundraising sales’/events’ “exchange portion” (i.e., representing fair market value sale of items/services provided).

Gross receipts from fundraising sales/events are represented by totaling Lines 1c + 8a: a total of $15,000 or more is a trigger to Schedule G’s Part II!

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

Memo line for gift captureExchange portion line

117

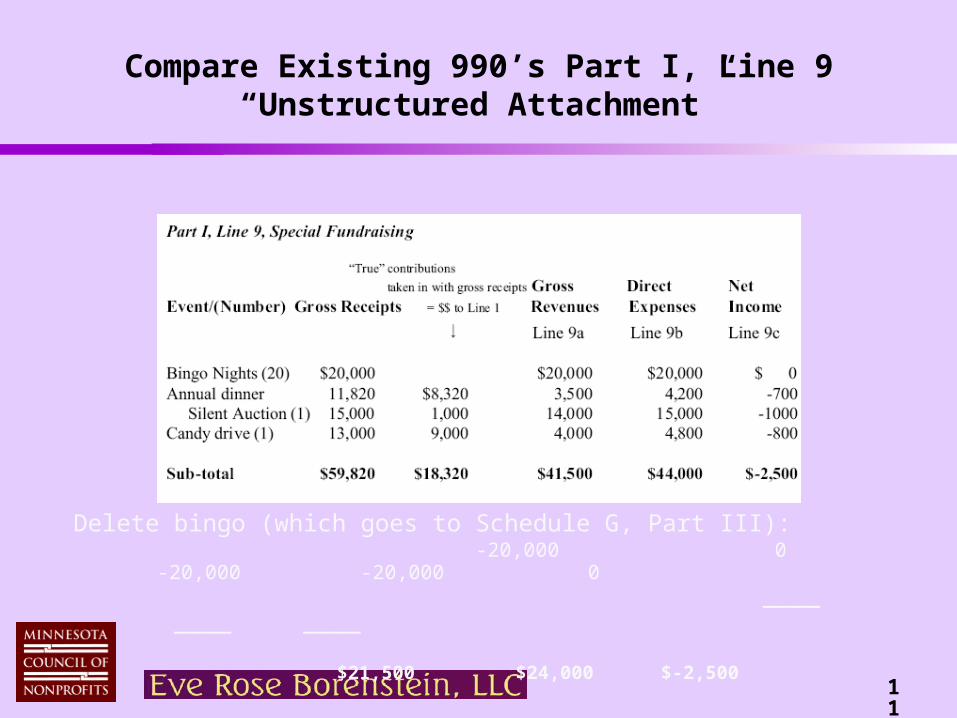

Compare Existing 990’s Part I, Line 9“Unstructured Attachment”

Delete bingo (which goes to Schedule G, Part III): -20,000 0 -20,000 -20,000 0

____ ____ ____ $21,500 $24,000 $-2,500

118

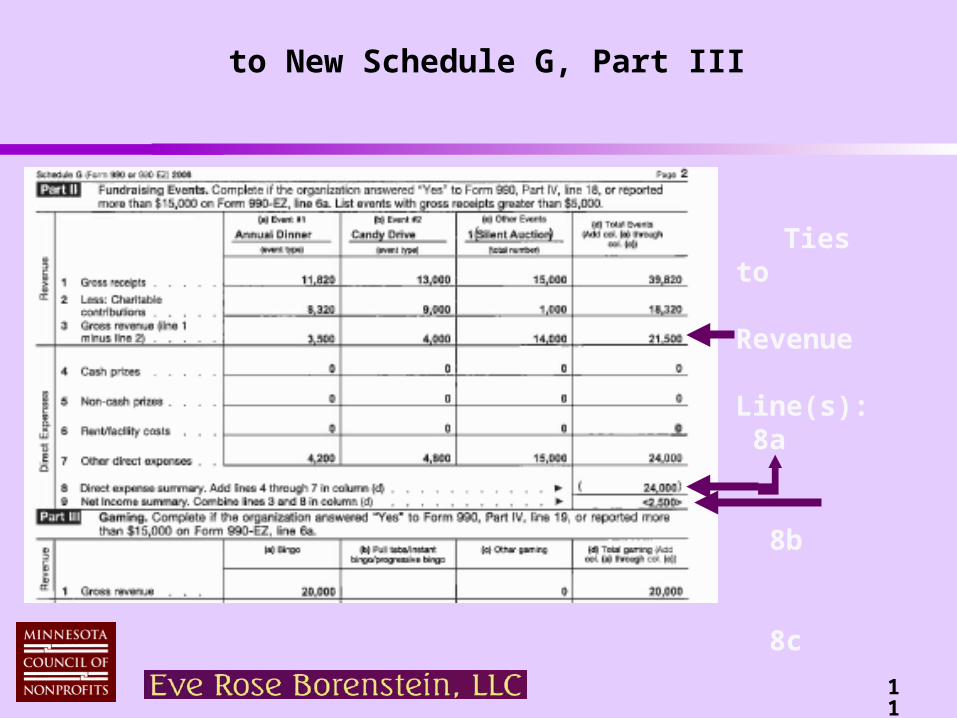

to New Schedule G, Part III

Ties to Revenue Line(s): 8a

8b

8c

119

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

C. As illustrated on the prior slides, capture of dollars from fundraising sales/events (the subject of Revenue Line 8) as well as from gaming activities (the subject of Revenue Line 9) generates the need to complete a “structured” attachment upon Schedule G’s Parts II (for non-gaming events/sales) and III (for gaming). What is sought on those Parts is almost identical to that required via the call for a ‘schedule-to-be-attached’ in the predecessor years’ of the Form 990.

Parts II and III (Gaming) both have “forced lines” for expenses, separately listing prizes (both cash and noncash), rent/facility costs, and bundled all other costs (i.e., direct expenses).

120

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

Part II requires input for two largest events AND then all others aggregated in third column

Part III requires separate input (by columns) for bingo (513(f)-definition) versus pull-tabs operation (and a third column for all other gaming). Specific questions for gaming operators:

%-volunteer labor used in bingo/pull-tabs/other States in which filer is licensed to conduct gaming,

disciplinary actions, explanation if not licensed Queries about gaming with nonmembers, %-age of

activity undertaken “in-house” versus outside ID of 3rd party operators, gaming manager, collaborative

121

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

D. In addition, expenditures (paid or accrued) to professional fundraisers in amounts for the year in excess of $15,000 (reported on the Core Form’s Part IX, expense reporting) triggers completion of Schedule G, Part I.Part I makes the following inquiries:

1. Asks about types of fundraising activities undertaken 2. Asks if filer had agreements with fundraisers3. If had agreements with any, list the 10 highest paid

parties (charted info, see next slide)4. Requires listing of all states in which organization is

registered or licensed to solicit funds (or has been determined to be exempted)

122

IV. The BIG 10 SchedulesHere, “Fundraising” (Revenue reporting &

Schedule G)

5. Disclosures on use of professional fundraisers (PFR) required of 990 filers (not -EZ), including listing highest 10 paid >$5,000. On each filer shows:a. Name of individual or entity

b. Fundraising activity that was conducted

c. Y/N did the PFR have control or custody of assets

d. Gross receipts (avoid disparities with Part VIII, Line 1c)

e. Amount paid to (or retained by) PFR (tie to Part IX, Line 11e)

f. Amount paid or retained by reporting organization

123

A Note Re Proper Recording of Event In- & Out-Flows

Fundraising events typically involve two undertakings:

1a. “Getting” non-cash contributions (e.g., property such as food for dinner, items to be raffled) or cash contributions such as sponsorships prior to holding the event. Solicitation costs/expenses for these are NOT direct event expenses (recordable on Revenues Line 8b), but stand-alone expenses reportable in Part IX in the “fundraising” column. Contributions get recorded on Revenues’ Line 1(f) [property contributions also listed again in memo Line 1(g)]

1b. Fundraising related to having people attend or getting donors/sponsors (e.g., sending out invitations, solicitations). These costs also are NOT direct event expenses, but stand-alone “fundraising” expenses.

124

A Note Re Proper Recording of Event In- & Out-Flows

2. The event’s conduct brings in its own in-flows and out-flows, reportable all on line 8, as follows:

“Sales” = quid pro quo’s (i.e., “exchange portion” for fair market value buyers’ procure) goes on 8a. Overpays above fair market value = contributions that are reported on Line 1c and on Line 8’s header memo line (8____).

Direct expenses of the event (inventory disposal, catering, rental, greens fees, etc.) go on 8b.

Disposition of property that has been contributed is an expense of the event as well . . .

125

Dispositions of Donated Properties (e.g., silent auction)

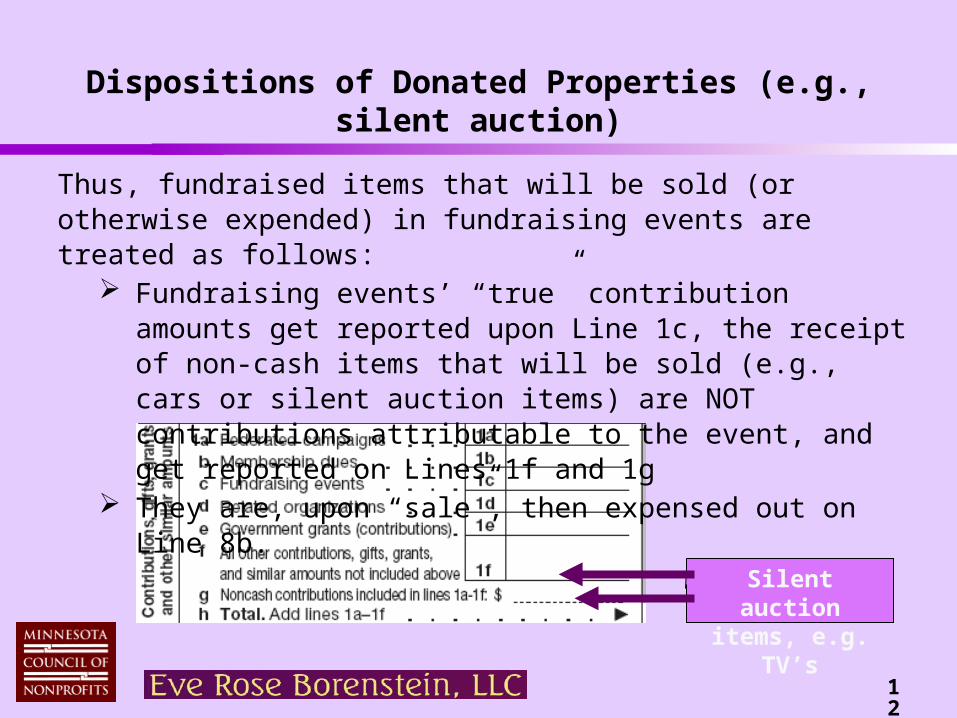

Thus, fundraised items that will be sold (or otherwise expended) in fundraising events are treated as follows:

Fundraising events’ “true” contribution amounts get reported upon Line 1c, the receipt of non-cash items that will be sold (e.g., cars or silent auction items) are NOT contributions attributable to the event, and get reported on Lines 1f and 1g

They are, upon “sale”, then expensed out on Line 8b.

Silent auction items, e.g. TV’s

126

Dispositions of Donated Properties (e.g., silent auction)

Upon the SALE of those items at the event, “sale” proceeds realized then need be itemized as attributable to the property’s fmv (thus leading to Line 8a entry) versus an overpay (leading to Line 1c entry). The value of the disposed-of items is an expense of the fundraising event that need be entered upon Line 8b.

Example: Bring in 10 TV’s selling typically between $1400-$1600. Book them in at average price, so 10 = $15,000 reportable upon Line 1f/1g. At disposition via silent auction, will have that same amount on Line 8b.

Silent Auction result, 1 of 2: 5 “sell” at $1700 apiece (receipts for those 5 are $8500: $7500 on Line 8a, $1000 on Line 1c)

Silent Auction result, 2 of 2: 5 “sell” at $1300 apiece (receipts for those 5 are $6500: $6500 on Line 8a).

Results: $16000 Line 1 [15000 Line 1f/1g (TVs), 1000 on Line 1c (overpays)] ($1000) Line 8c result ($14000 Line 8a, $15000 Line 8b xp-ing TVs)

Net Lines 1 & 8c = $15000 (ties to cash realized from TVs at auction!)

127

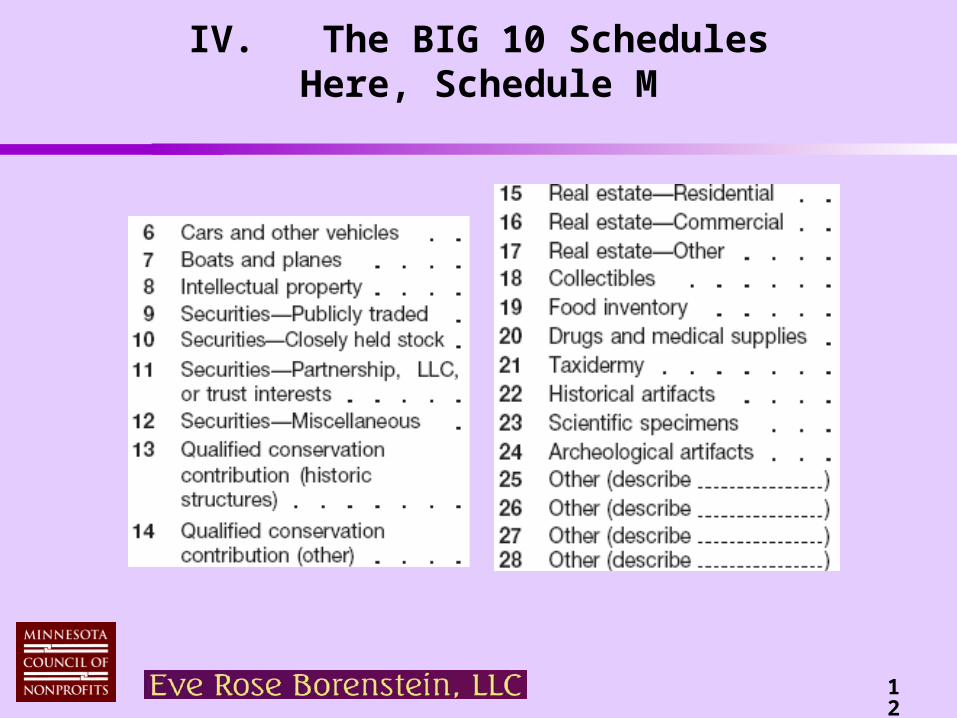

IV. The BIG 10 SchedulesHere, Schedule M

A. Schedule M (M for “moolah”) imposes new scheduling on non-cash contributions triggered EITHER by receipt of contributions (in filing year) of art, historical treasures or conservation easements with no dollar threshold OR having received/accrued non-cash contributions (e.g., stock) from deductible contributions totaling > $25,000.

1. While not a perfect tie, note new Line 1g (itself a memo line)

128

IV. The BIG 10 SchedulesHere, Schedule M

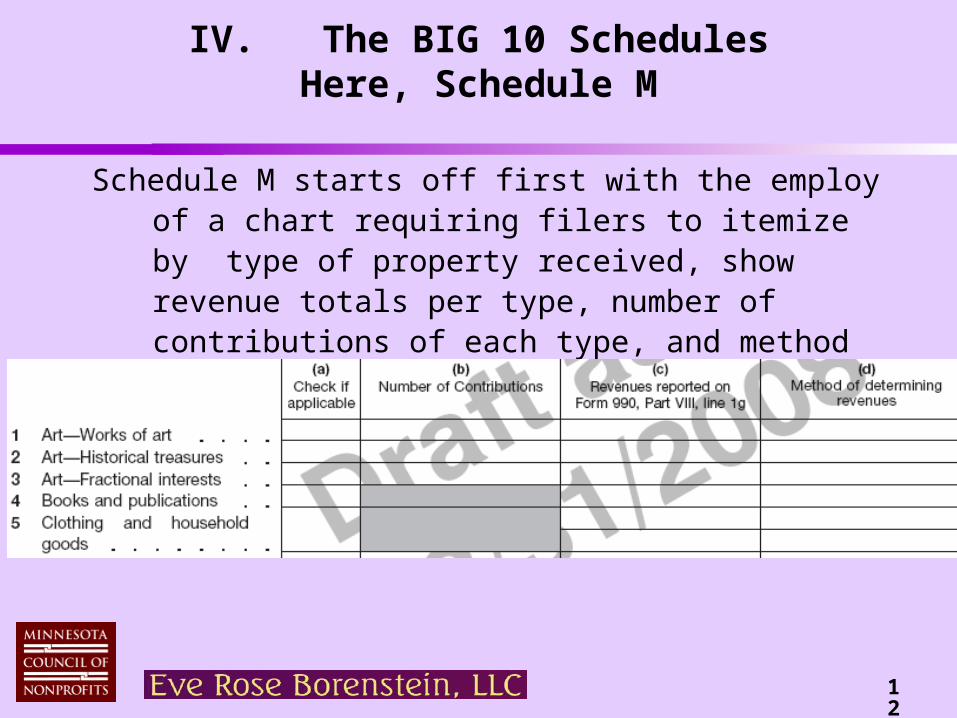

Schedule M starts off first with the employ of a chart requiring filers to itemize by type of property received, show revenue totals per type, number of contributions of each type, and method of determining value for each type

129

IV. The BIG 10 SchedulesHere, Schedule M

130

IV. The BIG 10 SchedulesHere, Schedule M

B. After the chart, the filer is asked to disclose:

1. Number of Forms 8283 organization completed for donors

2. Whether organization took property not to be used for exempt purposes but promising to hold for three year period

3. Whether some types of property were received but no revenues were ascribed to same

4. Whether the organization hires or uses others to “solicit, process, or sell non-cash contributions”

5. Whether the organization has a gift acceptance policy

131

IV. The BIG 10 SchedulesHere, Schedule M

C. The question on gift acceptance policies is there for “behavior modification” and/or “promoting good governance” reasons and is basically a helpful suggestion. These policies typically should take into consideration:

1. Organization’s mission statement

2. Purpose of policy guidelines

3. Donor conflict of interest – Independent counsel

4. Restrictions on gifts imposed by donor allowed

5. Types of assets accepted and any restrictions

132

IV. The BIG 10 SchedulesHere, Schedule I

A. Schedule I (“Eye”) – Domestic Grants Out

1. “Grants out” reporting has long been accomplished on the predecessor Form 990’s first expense Line (22). That Line has long required more information “be attached”. The sufficiency of filers’ following the Instructions as to what is to then be attached has been inconsistent at best. Schedule I replaces that “unstructured” attachment mandate with amplified scheduling when grants/assistance is provided to individuals and organizations in the U.S.

a. Note that it is Schedule F that is used for detailing grants/assistance provided to organizations or entities outside the U.S.

133

IV. The BIG 10 SchedulesHere, Schedule I

2. Schedule I is “triggered” when the filer has total grants to individuals OR total grants to organizations (again, both in the U.S.) in amounts exceeding $5,000.

B. Grants to organizational grantees are required to be reported via Part II. There a chart is employed asking:

Name and address of organization/gov’t recipient along with E.I.N. (T.I.N.)

501(c)-exemption code, if applicable, of grantee Amount of cash grant provided Amount of non-cash assistance, method of valuation,

description of non-cash grant/assistance Purpose of grant or assistance

134

IV. The BIG 10 SchedulesHere, Schedule I

C. Schedule I’s Part III is where one reports grants to individual grantees. The disclosures here are actually much less than on the predecessor Forms, only: Type of grant or assistance (no name!) Number of recipients (for each type) Amount of cash grant (for each type) Amount of non-cash assistance, method of valuation,

description of non-cash grant/assistance (for each type)

D. Part I (required whenever Parts II or III are) asks about: a. records substantiating eligibility and selection

b. monitoring procedures for use of grant funds

135

IV. The Remaining Big 10 Schedules

In addition to Schedule O, of the Big 10 Schedules (the most-likely to apply) we have addressed five so far:

1. J . . . Judging (this re how managers are compensated)

2. L . . . Lessons from Liaisons? (Loans, transactions, etc. with INSIDERS)

3. G. . . Fundraising/Gaming4. M . . . Moolah (in form of NONcash contributions)5. I . . . Instilling dollars/assistance out to others (grant-

making, but only in the United States)

136

IV. The Remaining Big 10 Schedules

Which leaves us 5 more:

1. A . . . A is for “(a)(1), (a)(2), (a)(3)”, that is,

how 501(c)(3)’s are in public charity (rather than private foundation) status

2. R . . . Related organizations

3. D . . . Details, balance sheet

(supplemental financial statements)

4. C . . . Political campaign and Lobbying Activities

5. F . . . Statement of Activities Outside the U.S. (i.e., foreign activities)

137

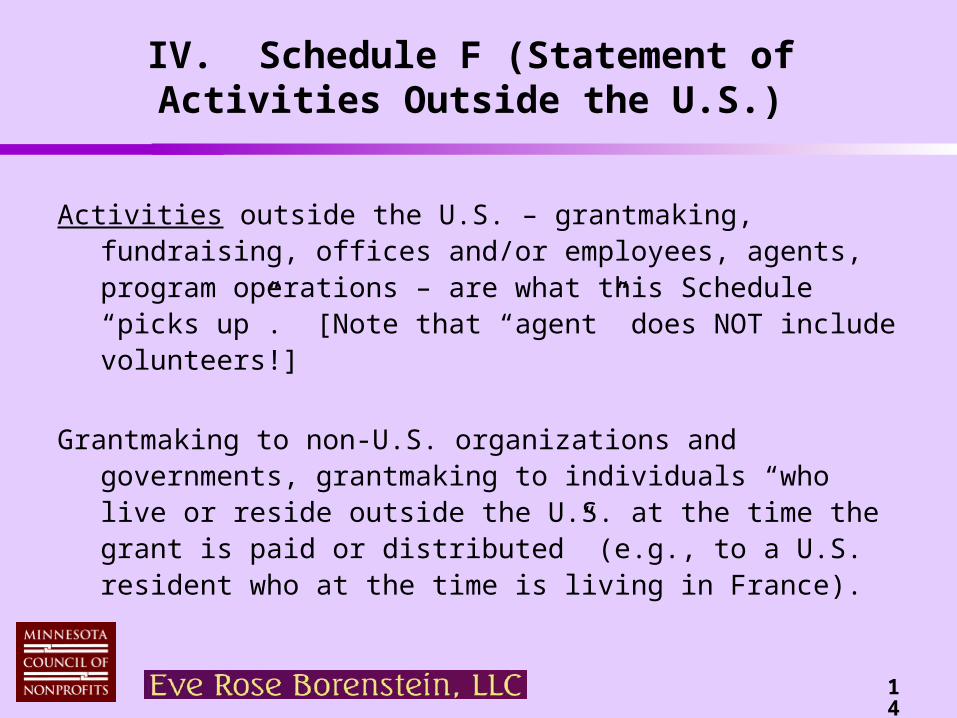

IV. Schedule A (501(c)(3) Public Charities)

Schedule A Part II: grid inputting data for first of two “public support tests” – this for 509(a)(1)/170(b)(1)(A)(vi) ‘test’

a. New: stand-alone grid inputs data, calculates test’s resultb. Accrual basis of accounting inputs allowed (follow method that

books are kept – all this from 9/9/08-released Regulations!)c. 5 years not 4 now basis of testing (= current year plus four back