the new 990 presenter: kris mcmackin cpa. the new 990 what is the 990 what is all the hoopla about...

TRANSCRIPT

The New 990The New 990

Presenter:Presenter:

Kris McMackin CPAKris McMackin CPA

The New 990The New 990

What is the 990 What is all the hoopla about changes

to the 990? What do you need to know about it? What do you need to do about it? Disclosure requirements & Conflict

of Interest Policy Financial Statements for the Board

What is the 990?What is the 990?

Is it just that document that the IRS demands we file every year?

What is the 990?What is the 990?

The answer is NO, it’s important to:-Federal government-State government-Other tax-exempt organizations -Public Each year, approximately 550,000

organizations file a Form 990 or Form 990-EZ with the IRS.

What is the 990?What is the 990?

IRS’ primary tax compliance tool for tax-exempt organizations.

Most states rely on the form for charitable and other regulatory oversight, and to satisfy state income tax filing requirements for organizations claiming exemption from state income tax.

Public document that is made available by filing organizations, the IRS, and others. The public, state regulators, media, researchers, and policymakers rely on the 990 to obtain information about the tax-exempt sector and individual organizations, helping to ensure transparency.

What is the 990What is the 990

Most of all, it is your story. The design Most of all, it is your story. The design of the new 990 allows tax exempt of the new 990 allows tax exempt organizations to tell their story organizations to tell their story throughout the form.throughout the form.

Use of a new summary page, Use of a new summary page, supplemental information, the core supplemental information, the core return and schedules allow for return and schedules allow for narrativenarrative

You can use the 990 to your You can use the 990 to your advantageadvantage

Create a good impressionCreate a good impression

Tell the world about your workTell the world about your work

Show you’re tax compliantShow you’re tax compliant

Show accountability and transparencyShow accountability and transparency

Explain how your activities support your Explain how your activities support your mission or goalmission or goal

Provide explanations to clarify information Provide explanations to clarify information of interest to the IRS and publicof interest to the IRS and public

* It’s not just about the numbers anymore** It’s not just about the numbers anymore*

Why Change the 990?Why Change the 990?

The 990 was last changed in 1979. The The 990 was last changed in 1979. The form no longerform no longer reflected the changes in tax law and the increasing size, diversity and complexity of the exempt sector.

The three guiding principles of the changes are:

enhancing transparency promoting tax compliance and minimizing burden on the filing

organization.

Summary of Key ChangesSummary of Key Changes

Opportunities throughout the forms and schedules for narrative information

New 3 part section on governance Revised reporting of compensation Revised reporting of compensation

and insider transactionsand insider transactions Revamping form layout- more Revamping form layout- more

schedules and fewer attachmentsschedules and fewer attachments Minimized reporting burden through Minimized reporting burden through

use of thresholds and exceptions use of thresholds and exceptions

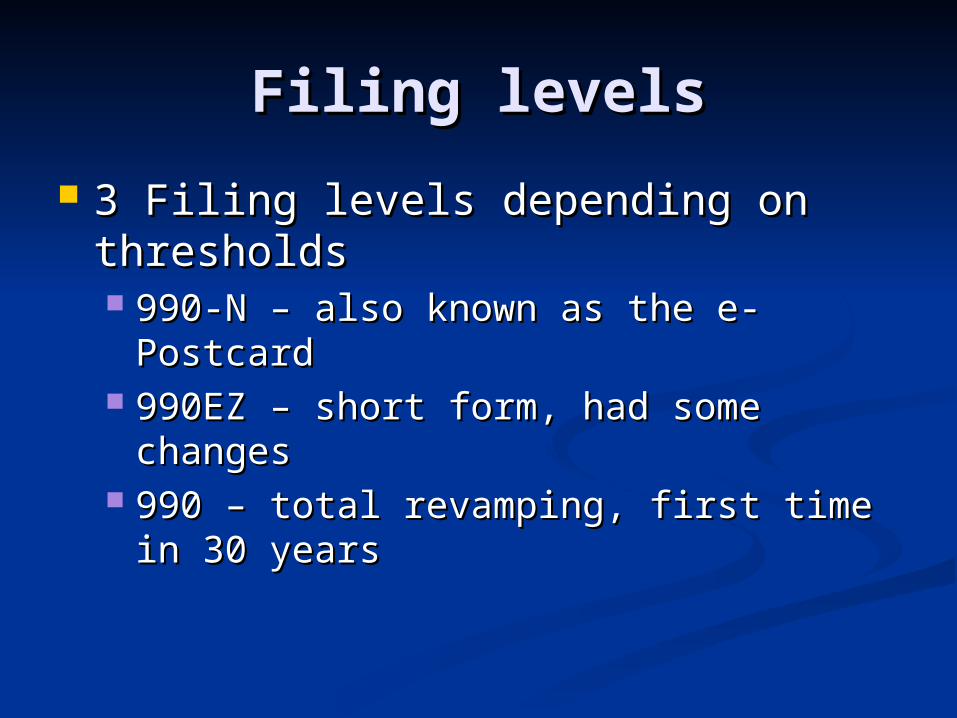

Filing levelsFiling levels

3 Filing levels depending on 3 Filing levels depending on thresholdsthresholds 990-N – also known as the e-Postcard990-N – also known as the e-Postcard 990EZ – short form, had some changes990EZ – short form, had some changes 990 – total revamping, first time in 30 990 – total revamping, first time in 30

yearsyears

Phase inPhase inChanges were made in 2008 but the IRS has Changes were made in 2008 but the IRS has

allowed a 3 year phase in. (see handout)allowed a 3 year phase in. (see handout)Starting with the 2010 tax year:Starting with the 2010 tax year:

Form to FileForm to FilePrivate FoundationPrivate Foundation 990-PF990-PFGross receipts normally <= $50kGross receipts normally <= $50k 990-N990-NGross receipts <$200k &Gross receipts <$200k & 990-EZ990-EZ

Total assets< $500kTotal assets< $500kGross receipts =>$200k orGross receipts =>$200k or 990990

Total assets =>$500kTotal assets =>$500k

New layout of 990:New layout of 990:

consists of a 12 page core form to be consists of a 12 page core form to be completed by all organizationscompleted by all organizations

16 schedules that may be filled out 16 schedules that may be filled out depending on the organizations activitiesdepending on the organizations activities

Many of the schedules replace Many of the schedules replace “unstructured attachments” previously “unstructured attachments” previously requiredrequired

Some schedules replace the previous Some schedules replace the previous Schedule A which has been split into 4 Schedule A which has been split into 4 separate schedulesseparate schedules

990 Layout990 Layout Part I, Summary Part I, Summary Part II, Signature Block Part II, Signature Block Part III, Statement of Program Service Accomplishments Part III, Statement of Program Service Accomplishments Part IV, Checklist of Required Schedules Part IV, Checklist of Required Schedules Part V, Statements Regarding Other IRS Filings and Tax Part V, Statements Regarding Other IRS Filings and Tax

Compliance Compliance Part VI, Governance, Management, and Disclosure Part VI, Governance, Management, and Disclosure Part VII, Compensation of Officers, Directors, Trustees, Part VII, Compensation of Officers, Directors, Trustees,

Key Employees, Highest Compensated Employees, and Key Employees, Highest Compensated Employees, and Independent Contractors Independent Contractors

Part VIII, Statement of Revenue Part VIII, Statement of Revenue Part IX, Statement of Functional Expenses Part IX, Statement of Functional Expenses Part X, Balance Sheet Part X, Balance Sheet Part XI, Financial Statements and Reporting Part XI, Financial Statements and Reporting

SchedulesSchedules A – public charity status and public supportA – public charity status and public support B- schedule of contributorsB- schedule of contributors C- political campaign and lobbying activitiesC- political campaign and lobbying activities D- supplemental financial statementsD- supplemental financial statements E- schools E- schools F- activities outside of the U.S.F- activities outside of the U.S. G- fundraising and gaming activitiesG- fundraising and gaming activities H- hospitalsH- hospitals I- grants and other assistance orgs, govts & individuals in the U.S.I- grants and other assistance orgs, govts & individuals in the U.S. J- compensation informationJ- compensation information K- supplemental information on tax exempt bondsK- supplemental information on tax exempt bonds L- transactions with interested personsL- transactions with interested persons M- non-cash contributionsM- non-cash contributions N- liquidation, terminations, dissolution, or significant disposition of N- liquidation, terminations, dissolution, or significant disposition of

assetsassets O- supplemental information O- supplemental information R- related organizations and unrelated partnershipsR- related organizations and unrelated partnerships

New layout of 990-EZ:New layout of 990-EZ:

consists of a 4 page core form to be consists of a 4 page core form to be completed by all organizationscompleted by all organizations

7 potential schedules that may be filled 7 potential schedules that may be filled out depending on the organizations out depending on the organizations activitiesactivities

In the past two formal schedules- A & BIn the past two formal schedules- A & B Schedule A was converted to 3 separate Schedule A was converted to 3 separate

schedulesschedules Other “unstructured attachments” Other “unstructured attachments”

converted to schedulesconverted to schedules

990-EZ Layout990-EZ Layout Part I, Statement of Revenue Part I, Statement of Revenue Part II, Balance SheetsPart II, Balance Sheets Part III, Statement of Program Service Part III, Statement of Program Service

Accomplishments Accomplishments Part IV, Compensation of Officers, Part IV, Compensation of Officers,

Directors, Trustees, Key Employees Directors, Trustees, Key Employees Part V, Other Information Part V, Other Information Part VI, To be completed by 501(c)(3) Part VI, To be completed by 501(c)(3)

organizations – covers lobbying, schools, organizations – covers lobbying, schools, highest compensated employees and highest compensated employees and independent contractorsindependent contractors

SchedulesSchedules A – public charity status and public A – public charity status and public

supportsupport B- schedule of contributorsB- schedule of contributors C- political campaign and lobbying C- political campaign and lobbying

activitiesactivities E- schools E- schools G- fundraising and gaming activitiesG- fundraising and gaming activities L- transactions with interested personsL- transactions with interested persons N- liquidation, terminations, dissolution, N- liquidation, terminations, dissolution,

or significant disposition of assetsor significant disposition of assets

A Closer Look at Key A Closer Look at Key ChangesChanges

The Summary (page 1) designed to The Summary (page 1) designed to enhance transparency by providing key enhance transparency by providing key information on the first page for the information on the first page for the benefit of the publicbenefit of the public Summarizes info found elsewhere on form, Summarizes info found elsewhere on form,

snapshot of key financial governance & snapshot of key financial governance & operational infooperational info

Includes mission, unrelated business income, Includes mission, unrelated business income, professional fundraising expenses, number professional fundraising expenses, number of directors & number of independent of directors & number of independent directorsdirectors

A Closer Look at Key A Closer Look at Key ChangesChanges

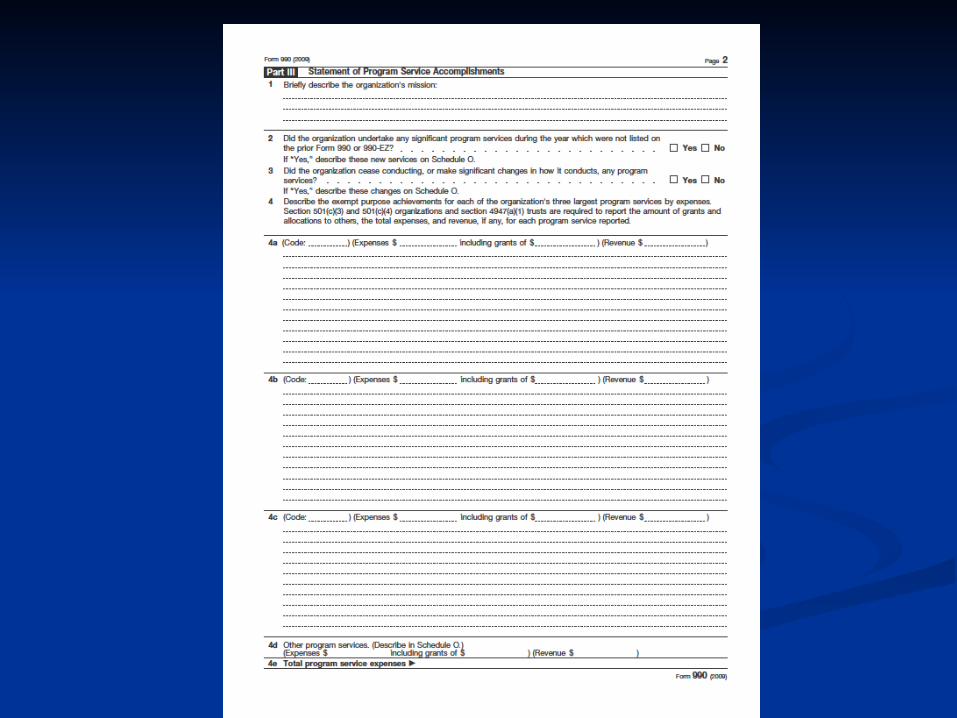

Part III – Statement of Program Part III – Statement of Program Service Accomplishments (page 2)Service Accomplishments (page 2) Briefly describes mission (again), new Briefly describes mission (again), new

activities and any activities ceased, 3 activities and any activities ceased, 3 largest program svceslargest program svces Additional descriptions can be given on Additional descriptions can be given on

Sched OSched O Great opportunity for organization to Great opportunity for organization to

promote its accomplishments to the publicpromote its accomplishments to the public

A Closer Look at Key A Closer Look at Key ChangesChanges

Part IV Checklist of Required Schedules

Designed to assist org in Designed to assist org in determining which of the 16 determining which of the 16 schedules they are required to fileschedules they are required to file

Eases the filing burden by assisting Eases the filing burden by assisting in determining which schedules to in determining which schedules to filefile

A Closer Look at Key A Closer Look at Key ChangesChanges

Part VI Governance, Management, Disclosure (p6)

Good governance promotes Good governance promotes compliancecompliance

Not requirements for tax exemption Not requirements for tax exemption under federal law but IRS has under federal law but IRS has indicated that orgs without these indicated that orgs without these policies run a greater risk of auditpolicies run a greater risk of audit

Governance, Mgmt, Governance, Mgmt, DisclosureDisclosure

3 parts: Part I asks questions about the governing

body & management Number of voting members of BoardNumber of voting members of Board Number of independent voting directors or Number of independent voting directors or

trusteestrustees Family or business relationships among Family or business relationships among

officers, directors, trustees, or key employeesofficers, directors, trustees, or key employees Material diversion of assets during the yearMaterial diversion of assets during the year Are meetings documented at the time of the Are meetings documented at the time of the

meetingmeeting

Governance, Mgmt, Governance, Mgmt, DisclosureDisclosure

Part II asks questions about policies If the org has local chapters are there written If the org has local chapters are there written

policies & procedures to ensure consistency in policies & procedures to ensure consistency in operationsoperations

Was the 990 reviewed by the board before it was Was the 990 reviewed by the board before it was filed and a description of the review processfiled and a description of the review process

Written conflict of interest policy with annual Written conflict of interest policy with annual disclosure requirement and enforcement policydisclosure requirement and enforcement policy

Written whistleblower policyWritten whistleblower policy Written document retention & destruction policyWritten document retention & destruction policy Determination of compensationDetermination of compensation

Governance, Mgmt, Governance, Mgmt, DisclosureDisclosure

Part III asks questions about public disclosure and if any additional forms are made available such as articles of incorporation, bylaws, etc

Conflict of InterestConflict of Interest

Q12 Section B asks whether the organization has a conflict of interest policy in place

Conflict of Interest Policy: Defines conflicts of interest Identifies the classes of individuals within the

org covered by the policy Facilitates disclosure of information that can

help identify conflicts Specifies procedures to be followed in

managing conflicts

Conflict of InterestConflict of Interest

What is a conflict of interest? When a person in a position of authority

such as an officer, director, or manager, can benefit financially from a decision he/she can make in such capacity. (includes indirect benefits such as family members or businesses)

Conflict of InterestConflict of Interest So, again, the Conflict of Interest Policy:

Defines circumstances under which a conflict of interest may arise- ie. a voting member of governing board who receives compensation- vote on matters of compensation?

Identifies the classes of individuals within the org covered by the policy- such as directors, officers, managers

Facilitates disclosure of information that can help identify conflicts- such as annual statement, named individual to discuss

Specifies procedures to be followed in managing conflicts- such as excluded from vote, minimum number of bids

Conflict of InterestConflict of Interest

Example policy is included in your handout

Public Disclosure Public Disclosure RequirementsRequirements

Section C is concerned with the disclosure requirements and how those are met

Public Disclosure Public Disclosure RequirementsRequirements

Certain annual returns Certain annual returns Applications for exemption Applications for exemption Copies must be provided immediately in Copies must be provided immediately in

the case of in-person requests the case of in-person requests Within 30 days in the case of written Within 30 days in the case of written

requests. requests. May charge a reasonable copying fee May charge a reasonable copying fee

plus actual postage, if any.plus actual postage, if any.

(handout)(handout)

Public Disclosure Public Disclosure RequirementsRequirements

Which tax documents must be Which tax documents must be available?available? Exemption applicationExemption application

Form 1023 (for 501(c)(3) orgs)Form 1023 (for 501(c)(3) orgs) Form 1024 for most other 501(c) Form 1024 for most other 501(c) Submission letter where no form is prescribedSubmission letter where no form is prescribed All supporting documents & any IRS letter or All supporting documents & any IRS letter or

document concerning the applicationdocument concerning the application Political orgs exempt under 527(a) must make Political orgs exempt under 527(a) must make

Form 8871 Notice of Status availableForm 8871 Notice of Status available

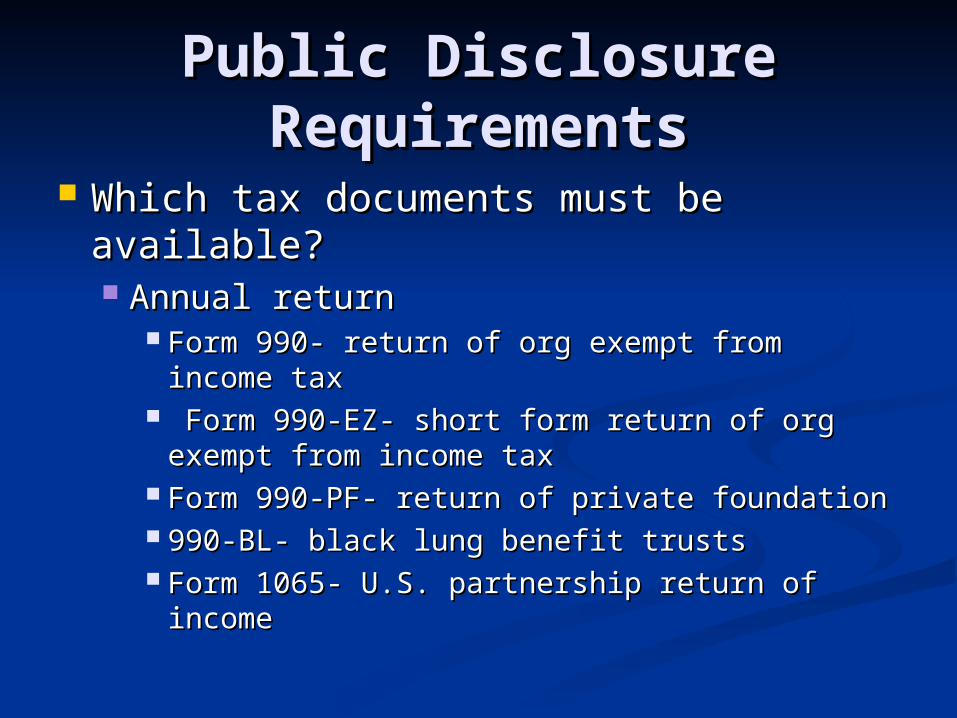

Public Disclosure Public Disclosure RequirementsRequirements

Which tax documents must be Which tax documents must be available?available? Annual returnAnnual return

Form 990- return of org exempt from income Form 990- return of org exempt from income taxtax

Form 990-EZ- short form return of org Form 990-EZ- short form return of org exempt from income tax exempt from income tax

Form 990-PF- return of private foundationForm 990-PF- return of private foundation 990-BL- black lung benefit trusts990-BL- black lung benefit trusts Form 1065- U.S. partnership return of incomeForm 1065- U.S. partnership return of income

Public Disclosure Public Disclosure RequirementsRequirements

Which tax documents must be available?Which tax documents must be available? Additionally, a 501(c)(3)Additionally, a 501(c)(3)

Form 990T- exempt organization business income Form 990T- exempt organization business income tax return- this includes all schedules, attachments, tax return- this includes all schedules, attachments, or supporting documents related to tax on unrelated or supporting documents related to tax on unrelated business incomebusiness income

Not required to discloseNot required to disclose Schedule K-1 of Form 1065Schedule K-1 of Form 1065 Schedule A of Form 990-BLSchedule A of Form 990-BL Name and address of any contributor (except private Name and address of any contributor (except private

foundations)foundations)

Public Disclosure Public Disclosure RequirementsRequirements

Which tax documents must be Which tax documents must be available?available? Returns must be available for a three-year Returns must be available for a three-year

period beginning with the due date of the period beginning with the due date of the return (including any extension of time for return (including any extension of time for filing). filing).

Where must they be available?Where must they be available? at the principal office of the organization, at the principal office of the organization,

and any regional or district offices having and any regional or district offices having three or more employeesthree or more employees

Public Disclosure Public Disclosure RequirementsRequirements

In person request- honored same In person request- honored same dayday

Written request (also fax or email)- Written request (also fax or email)- 30 days30 days

May charge reasonable copying fees May charge reasonable copying fees and actual postageand actual postage

Public Disclosure Public Disclosure RequirementsRequirements

Exception to requirement to provide Exception to requirement to provide copiescopies If the documents are made If the documents are made widely widely

availableavailable Ie. via the internet Ie. via the internet Must be in pdf format or other form as Must be in pdf format or other form as

described in the regulationsdescribed in the regulations Must be able to download documents for freeMust be able to download documents for free The organization must advise requesters of The organization must advise requesters of

how to access documentshow to access documents

Public Disclosure Public Disclosure RequirementsRequirements

Other documents you may make Other documents you may make availableavailable These are not requiredThese are not required

Governing documentsGoverning documents Conflict of interest policyConflict of interest policy Financial statementsFinancial statements

A Closer Look at Key A Closer Look at Key Changes:Changes:

Part VI Compensation of Officers, Directors, Part VI Compensation of Officers, Directors, Trustees, Key Employees, Highest Compensated Trustees, Key Employees, Highest Compensated Employees, and Independent Contractors:Employees, and Independent Contractors:

List of persons whose compensation must be List of persons whose compensation must be disclosed is expanded:disclosed is expanded: Current officers, directors, trusteesCurrent officers, directors, trustees Up to 20 key employees who have reportable Up to 20 key employees who have reportable

compensation greater than $150k from org & relatedcompensation greater than $150k from org & related Five highest paid current employees w/ compensation Five highest paid current employees w/ compensation

exceeding $100kexceeding $100k Former officers, key emps, highest compensated Former officers, key emps, highest compensated

employees w/ compensation exceeding $100kemployees w/ compensation exceeding $100k Former directors or trustees whose compensation Former directors or trustees whose compensation

exceeds $10kexceeds $10k

A Closer Look at Key A Closer Look at Key Changes:Changes:

Must disclose name, title, average Must disclose name, title, average weekly hours, compensation, and weekly hours, compensation, and estimated “other” compensation such estimated “other” compensation such as housing, education, insuranceas housing, education, insurance

Must identify independent contractors Must identify independent contractors such as law firms, accounting firms, such as law firms, accounting firms, consultants receiving more than $100kconsultants receiving more than $100k

Series of trigger questions to Series of trigger questions to determine if schedule J must be fileddetermine if schedule J must be filed

What you need to do:What you need to do: Determine which form the organization will Determine which form the organization will

need to fileneed to file Identify related organizations required to Identify related organizations required to

be listed on Schedule Rbe listed on Schedule R Identify officers, directors, trustees and Identify officers, directors, trustees and

potential key employees and top 5 highest potential key employees and top 5 highest compensated employees and subcontractorscompensated employees and subcontractors

Review new governance questions which Review new governance questions which will be answered based on policies in place will be answered based on policies in place on the last day of the yearon the last day of the year

Identify schedules the organization will Identify schedules the organization will likely be required to filelikely be required to file

What you need to do:What you need to do:

Obviously your organization will have Obviously your organization will have to provide the accounting firm to provide the accounting firm preparing the tax return with much preparing the tax return with much of this new informationof this new information

Your accountant should be asking Your accountant should be asking questions!questions!

Financial StatementsFinancial Statements

What information should the Board What information should the Board be reviewing on a monthly basis?be reviewing on a monthly basis?

Financial StatementsFinancial Statements

What information should the Board What information should the Board be reviewing on a monthly basis?be reviewing on a monthly basis? Balance SheetBalance Sheet Income Statement (Profit & Loss)Income Statement (Profit & Loss) Compared to BudgetCompared to Budget

Balance Sheet

Income Statement (Profit & Loss)Income Statement (Profit & Loss)

Budget vs ActualBudget vs Actual

For Start-upsFor Start-ups

Consider partnering with an Consider partnering with an established organization such as the established organization such as the United Way, Goodwill, etc and United Way, Goodwill, etc and operate under their 501(c)(3) operate under their 501(c)(3) designationdesignation

ResourcesResources

http://www.irs.gov/charities/index.html?navmenu=menu1

http://www.irs.gov/charities/article/0,,id=166625,00.html

http://stayexempt.org/